| Hilltop Holdings Inc. Q2 2025 Earnings Presentation July 25, 2025 |

| Preface 2 Corporate Headquarters Additional Information 6565 Hillcrest Ave Dallas, TX 75205 Phone: 214-855-2177 www.hilltop.com Please Contact: Matt Dunn Phone: 214-525-4636 Email: mdunn@hilltop.com FORWARD-LOOKING STATEMENTS This presentation and statements made by representatives of Hilltop Holdings Inc. (“Hilltop” or the “Company”) during the course of this presentation include “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995. These forward-looking statements involve known and unknown risks, uncertainties and other factors that may cause the Company’s actual results, performance or achievements to be materially different from any future results, performance or achievements anticipated in such statements. Forward-looking statements speak only as of the date they are made and, except as required by law, the Company does not assume any duty to update forward-looking statements. Such forward-looking statements include, but are not limited to, statements concerning such things as the Company’s outlook, business strategy, financial condition, efforts to make strategic acquisitions, liquidity and sources of funding, market trends, operations and business, the impact of natural disasters or public health emergencies, information technology expenses, capital levels, mortgage servicing rights (“MSR”) assets, stock repurchases, dividend payments, expectations concerning mortgage loan origination volume, servicer advances and interest rate compression, expected levels of refinancing as a percentage of total loan origination volume, projected losses on mortgage loans originated, total expenses, anticipated changes in our revenue, earnings, or taxes, the effects of government regulation applicable to our operations, the appropriateness of, and changes in, our allowance for credit losses and provision for (reversal of) credit losses, future benchmark rates and economic growth, anticipated investment yields, the collectability of loans, cybersecurity incidents, the outcome of litigation (both internal and external), and the Company’s other plans, objectives, strategies, expectations and intentions and other statements that are not statements of historical fact, and may be identified by words such as “anticipates,” “believes,” “building,” “continue,” “could,” “estimates,” “expects,” “forecasts,” “goal,” “guidance,” “intends,” “may,” “might,” “outlook,” “plan,” “probable,” “projects,” “seeks,” “should,” “target,” “view” or “would” or the negative of these words and phrases or similar words or phrases. The following factors, among others, could cause actual results to differ from those set forth in the forward-looking statements: (i) the credit risks of lending activities, including the Company’s ability to estimate credit losses and increases to the allowance for credit losses, as well as the effects of changes in the level of, and trends in, loan delinquencies and write-offs; (ii) effectiveness of the Company’s data security controls in the face of cyberattacks and any legal, reputational and financial risks following a cybersecurity incident; (iii) changes in general economic, market and business conditions in areas or markets where the Company competes, including changes in the price of crude oil; (iv) changes in the interest rate environment; (v) risks associated with concentration in real estate related loans; (vi) the effects of the Company’s indebtedness on its ability to manage its business successfully, including the restrictions imposed by the indenture governing such indebtedness; (vii) disruptions to the economy and financial services industry, risks associated with uninsured deposits and responsive measures by federal or state governments or banking regulators, including increases in the cost of the Company’s deposit insurance assessments; (viii) cost and availability of capital; (ix) changes in state and federal laws, regulations or policies affecting one or more of the Company’s business segments, including changes in regulatory fees, capital requirements and the Dodd-Frank Wall Street Reform and Consumer Protection Act; (x) changes in key management; (xi) competition in the Company’s banking, broker-dealer and mortgage origination segments from other banks and financial institutions, as well as investment banking and financial advisory firms, mortgage bankers, asset-based non-bank lenders and government agencies; (xii) legal and regulatory proceedings; (xiii) risks associated with merger and acquisition integration; and (xiv) the Company’s ability to use excess capital in an effective manner. For further discussion of such factors, see the risk factors described in our most recent Annual Report on Form 10-K, subsequent Quarterly Reports on Form 10-Q and other reports that we have filed with the Securities and Exchange Commission. All forward-looking statements are qualified in their entirety by this cautionary statement. The information contained herein is preliminary and based on Company data available at the time of the earnings presentation. It speaks only as of the particular date or dates included in the accompanying slides. Except as required by law, Hilltop does not undertake an obligation to, and disclaims any duty to, update any of the information herein. |

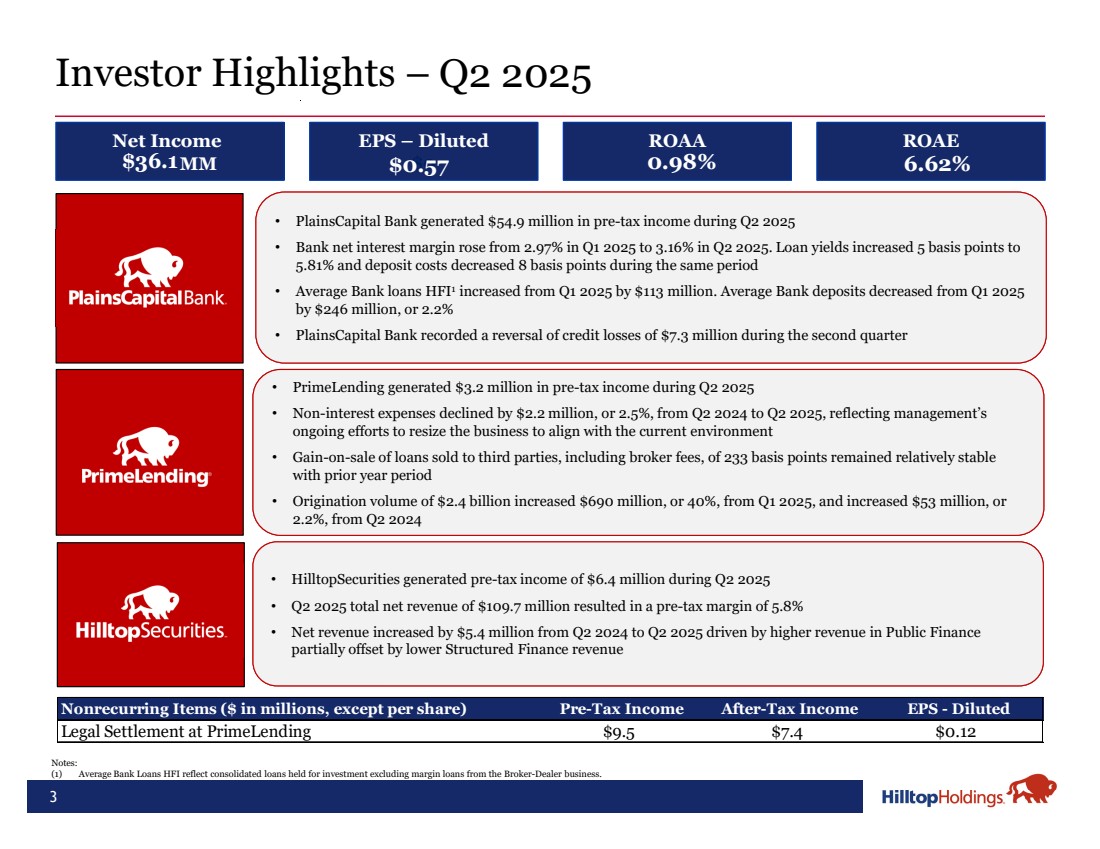

| Q2 2025 3 Investor Highlights – Notes: (1) Average Bank Loans HFI reflect consolidated loans held for investment excluding margin loans from the Broker-Dealer business. • PlainsCapital Bank generated $54.9 million in pre-tax income during Q2 2025 • Bank net interest margin rose from 2.97% in Q1 2025 to 3.16% in Q2 2025. Loan yields increased 5 basis points to 5.81% and deposit costs decreased 8 basis points during the same period • Average Bank loans HFI1 increased from Q1 2025 by $113 million. Average Bank deposits decreased from Q1 2025 by $246 million, or 2.2% • PlainsCapital Bank recorded a reversal of credit losses of $7.3 million during the second quarter • PrimeLending generated $3.2 million in pre-tax income during Q2 2025 • Non-interest expenses declined by $2.2 million, or 2.5%, from Q2 2024 to Q2 2025, reflecting management’s ongoing efforts to resize the business to align with the current environment • Gain-on-sale of loans sold to third parties, including broker fees, of 233 basis points remained relatively stable with prior year period • Origination volume of $2.4 billion increased $690 million, or 40%, from Q1 2025, and increased $53 million, or 2.2%, from Q2 2024 • HilltopSecurities generated pre-tax income of $6.4 million during Q2 2025 • Q2 2025 total net revenue of $109.7 million resulted in a pre-tax margin of 5.8% • Net revenue increased by $5.4 million from Q2 2024 to Q2 2025 driven by higher revenue in Public Finance partially offset by lower Structured Finance revenue ROAA .86% EPS – Diluted $0 ROAE $36.1 5.76% Net Income MM $0.57 0.98% 6.62% Nonrecurring Items ($ in millions, except per share) Pre-Tax Income After-Tax Income EPS - Diluted Legal Settlement at PrimeLending $9.5 $7.4 $0.12 |

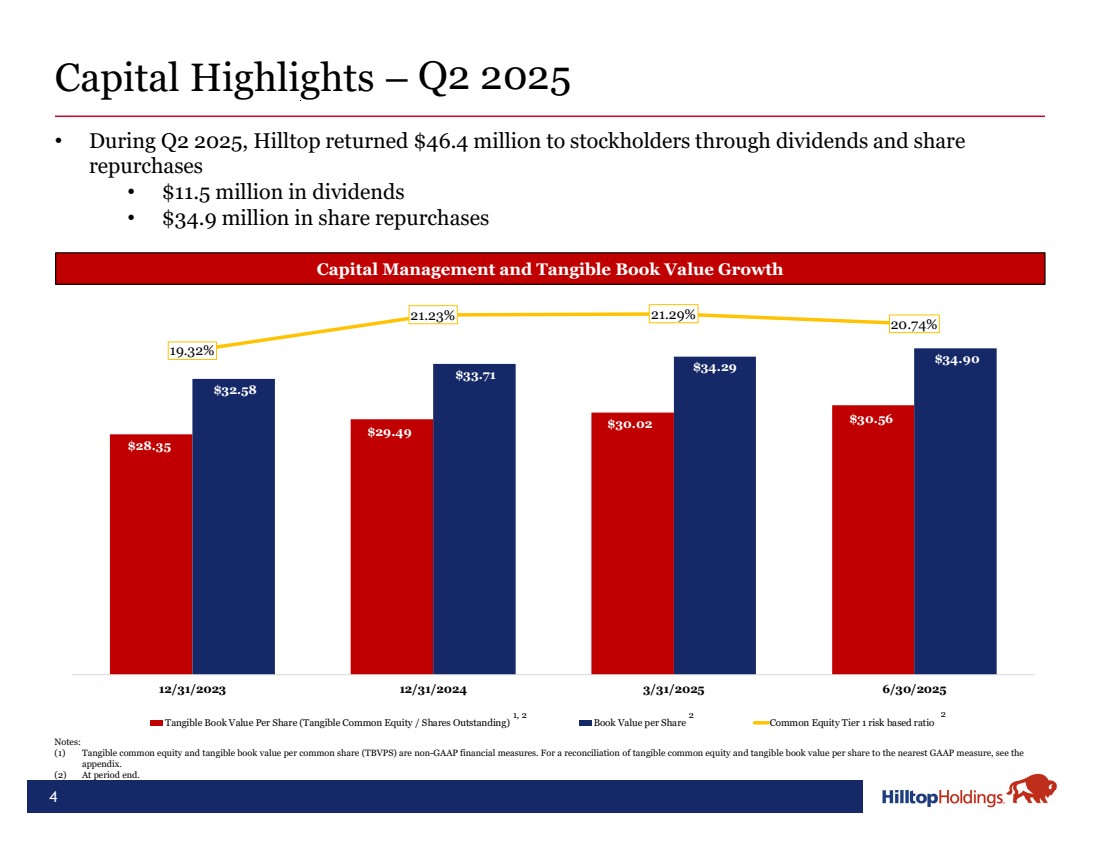

| $28.35 $29.49 $30.02 $30.56 $32.58 $33.71 $34.29 $34.90 19.32% 21.23% 21.29% 20.74% 2.00% 22.00% $10.00 $15.00 $20.00 $25.00 $30.00 $35.00 $40.00 12/31/2023 12/31/2024 3/31/2025 6/30/2025 Tangible Book Value Per Share (Tangible Common Equity / Shares Outstanding) Book Value per Share Common Equity Tier 1 risk based ratio Capital Highlights – 4 Capital Management and Tangible Book Value Growth Notes: (1) Tangible common equity and tangible book value per common share (TBVPS) are non-GAAP financial measures. For a reconciliation of tangible common equity and tangible book value per share to the nearest GAAP measure, see the appendix. (2) At period end. 1, 2 2 • During Q2 2025, Hilltop returned $46.4 million to stockholders through dividends and share repurchases • $11.5 million in dividends • $34.9 million in share repurchases 2 Q2 2025 |

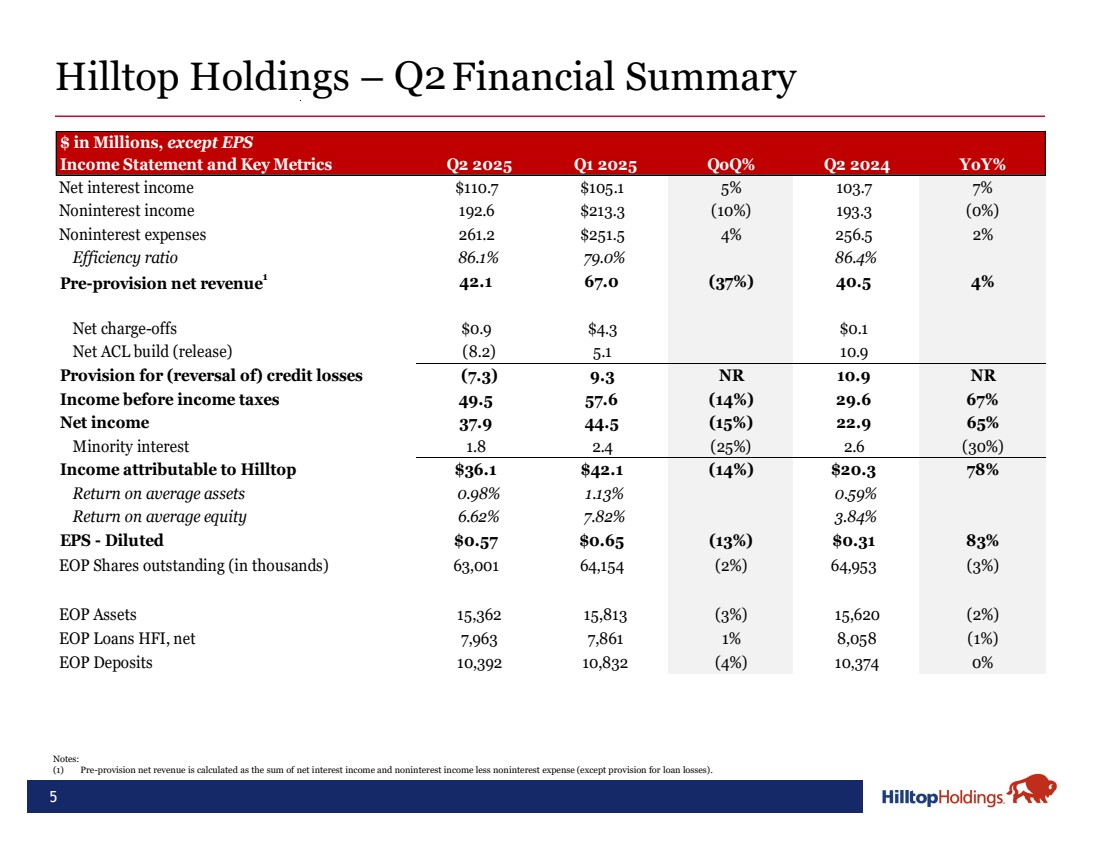

| 5 Hilltop Holdings – Financial Summary $ in Millions, except EPS Income Statement and Key Metrics Q2 2025 Q1 2025 QoQ% Q2 2024 YoY% Net interest income $110.7 $105.1 5% 103.7 7% Noninterest income 192.6 $213.3 (10%) 193.3 (0%) Noninterest expenses 261.2 $251.5 4% 256.5 2% Efficiency ratio 86.1% 79.0% 86.4% Pre-provision net revenue1 42.1 67.0 (37%) 40.5 4% Net charge-offs (recoveries) $0.9 $4.3 $0.1 Net ACL build (release) (8.2) 5.1 10.9 Provision for (reversal of) credit losses (7.3) 9.3 NR 10.9 NR Income before income taxes 49.5 57.6 (14%) 29.6 67% Net income 37.9 44.5 (15%) 22.9 65% Minority interest 1.8 2.4 (25%) 2.6 (30%) Income attributable to Hilltop $36.1 $42.1 (14%) $20.3 78% Return on average assets 0.98% 1.13% 0.59% Return on average equity 6.62% 7.82% 3.84% EPS - Diluted $0.57 $0.65 (13%) $0.31 83% EOP Shares outstanding (in thousands) 63,001 64,154 (2%) 64,953 (3%) EOP Assets 15,362 15,813 (3%) 15,620 (2%) EOP Loans HFI, net 7,963 7,861 1% 8,058 (1%) EOP Deposits 10,392 10,832 (4%) 10,374 0% Notes: (1) Pre-provision net revenue is calculated as the sum of net interest income and noninterest income less noninterest expense (except provision for loan losses). Q2 |

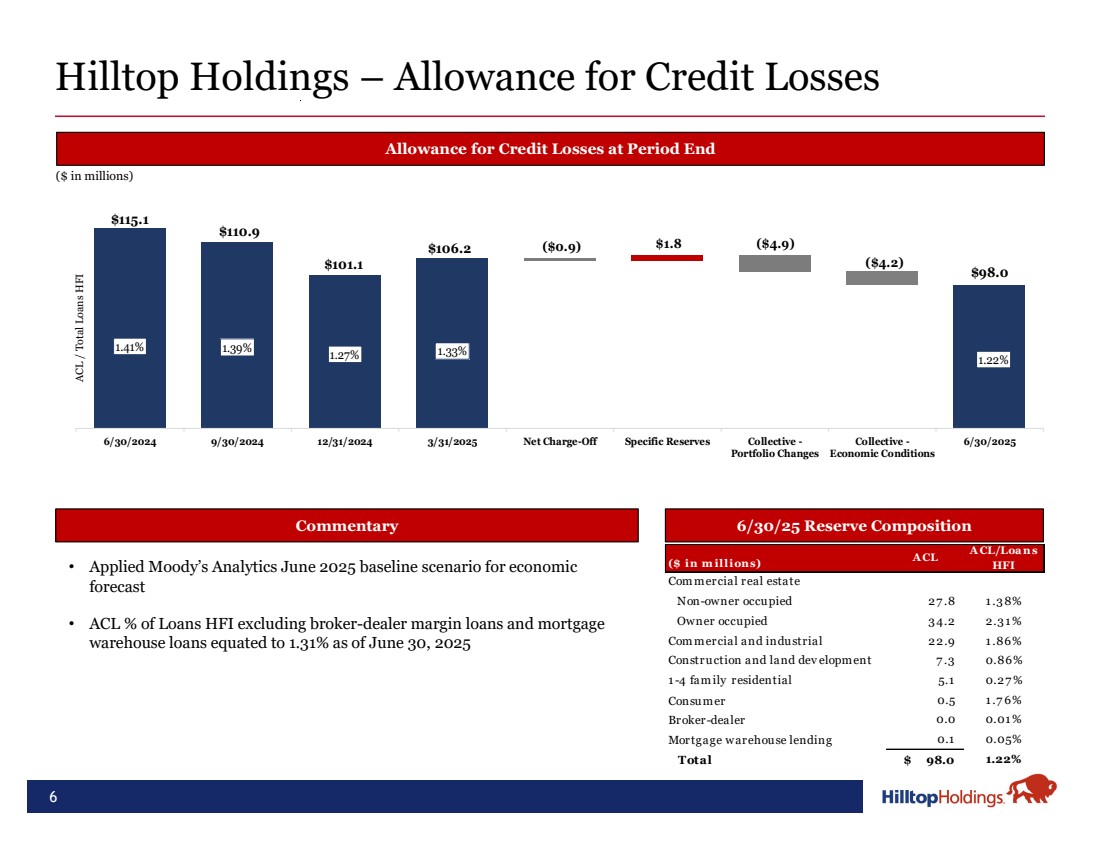

| $115.1 $110.9 $101.1 $106.2 $98.0 ($0.9) $1.8 ($4.9) ($4.2) 1.41% 1.39% 1.27% 1.33% 1.22% 0.00% 0.50% 1.00% 1.50% 2.00% 2.50% 3.00% 3.50% 4.00% $55.0 $65.0 $75.0 $85.0 $95.0 $105.0 $115.0 $125.0 6/30/2024 9/30/2024 12/31/2024 3/31/2025 Net Charge-Off Specific Reserves Collective - Portfolio Changes Collective - Economic Conditions 6/30/2025 6 Hilltop Holdings – Allowance for Credit Losses Allowance for Credit Losses at Period End 6/30/25 Reserve Composition ($ in millions) ACL / Total Loans HFI Commentary • Applied Moody’s Analytics June 2025 baseline scenario for economic forecast • ACL % of Loans HFI excluding broker-dealer margin loans and mortgage warehouse loans equated to 1.31% as of June 30, 2025 ($ in m illions) A CL A CL/Loa ns HFI Commercial real estate Non-owner occupied 27 .8 1 .38% Owner occupied 34.2 2.31 % Commercial and industrial 22.9 1 .86% Construction and land dev elopment 7 .3 0.86% 1 -4 family residential 5.1 0.27 % Consumer 1 .7 6% 0.5 Broker-dealer 0.01 % 0.0 Mortgage warehouse lending 0.05% 0.1 Total 98.0 $ 1.22% |

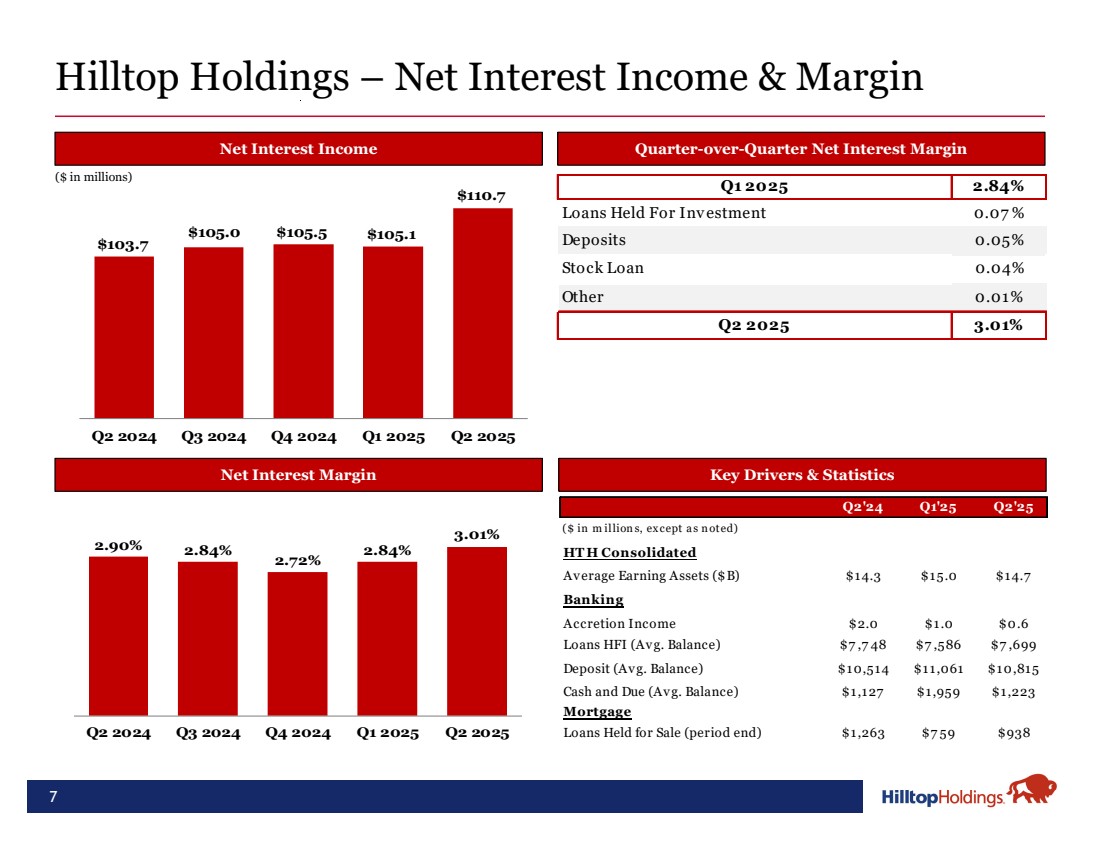

| 2.90% 2.84% 2.72% 2.84% 3.01% 1 .00% 1 .50% 2 .00% 2 .50% 3 .00% 3 .50% 4 .00% 4 .50% Q2 2024 Q3 2024 Q4 2024 Q1 2025 Q2 2025 7 Hilltop Holdings – Net Interest Income & Margin Net Interest Margin 2 Net Interest Income Quarter-over-Quarter Net Interest Margin Key Drivers & Statistics ($ in millions) Q2'24 Q1'25 Q2'25 ($ in m illion s, ex cept a s n oted) HT H Consolidated Average Earning Assets ($B) $14.3 $15.0 $14.7 Banking Accretion Income $2.0 $1.0 $0.6 Loans HFI (Avg. Balance) $7 ,7 48 $7 ,586 $7 ,699 Deposit (Avg. Balance) $10,514 $11,061 $10,815 Cash and Due (Avg. Balance) $1,127 $1,959 $1,223 Mortgage Loans Held for Sale (period end) $1,263 $7 59 $938 Q1 2025 2.84% Loans Held For Inv estment 0.07 % Deposits 0.05% Stock Loan 0.04% Other 0.01% Q2 2025 3.01% $103.7 $105.0 $105.5 $105.1 $110.7 $80.0 $85 .0 $90.0 $95 .0 $1 00.0 $105.0 $1 1 0. 0 $1 1 5. 0 Q2 2024 Q3 2024 Q4 2024 Q1 2025 Q2 2025 |

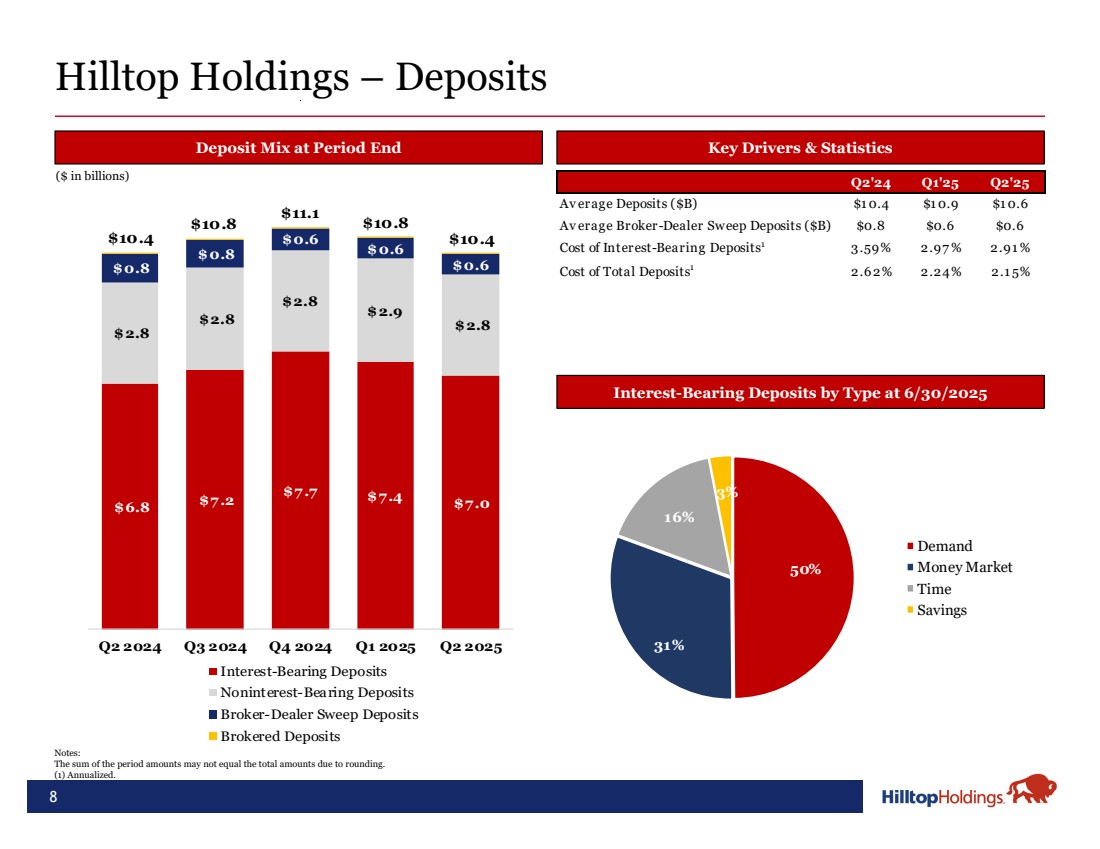

| $6.8 $7.2 $7.7 $7.4 $7.0 $2.8 $2.8 $2.8 $2.9 $2.8 $0.8 $0.8 $0.6 $0.6 $0.6 $10.4 $10.8 $11.1 $10.8 $10.4 Q2 2024 Q3 2024 Q4 2024 Q1 2025 Q2 2025 Interest-Bearing Deposits Noninterest-Bearing Deposits Broker-Dealer Sweep Deposits Brokered Deposits 8 Notes: The sum of the period amounts may not equal the total amounts due to rounding. (1) Annualized. Deposit Mix at Period End Hilltop Holdings – Deposits Key Drivers & Statistics Interest-Bearing Deposits by Type at 6/30/2025 ($ in billions) 50% 31% 16% 3% Demand Money Market Time Savings Q2'24 Q1'25 Q2'25 Av erage Deposits ($B) $1 0.4 $1 0.9 $1 0.6 Av erage Broker-Dealer Sweep Deposits ($B) $0.8 $0.6 $0.6 Cost of Interest-Bearing Deposits1 3.59% 2.97% 2.91% Cost of Total Deposits1 2.62% 2.24% 2.15% |

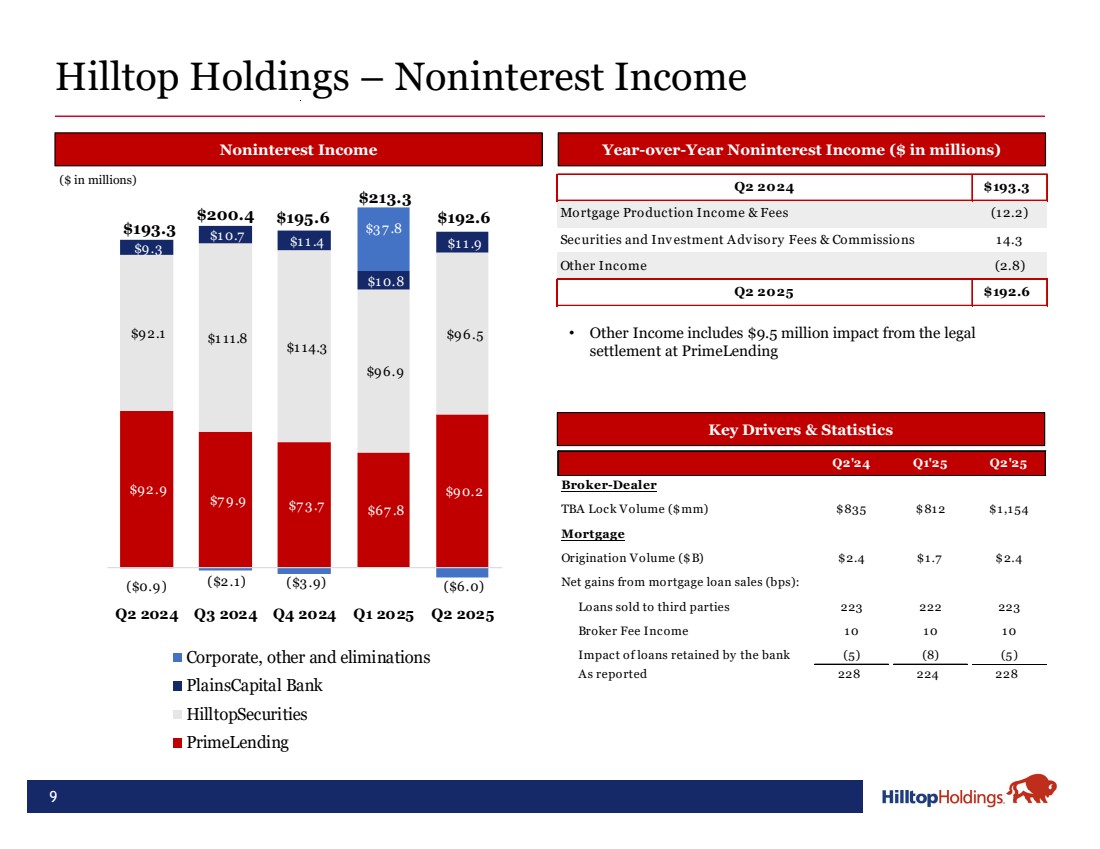

| $92.9 $7 9.9 $7 3.7 $67 .8 $90.2 $92.1 $1 11.8 $1 14.3 $96.9 $96.5 $9.3 $1 0.7 $1 1 .4 $1 0.8 $1 1 .9 ($0.9) ($2.1) ($3.9) $37 .8 ($6.0) $193.3 $200.4 $195.6 $213.3 $192.6 Q2 2024 Q3 2024 Q4 2024 Q1 2025 Q2 2025 Corporate, other and eliminations PlainsCapital Bank HilltopSecurities PrimeLending 9 Hilltop Holdings – Noninterest Income Noninterest Income Year-over-Year Noninterest Income ($ in millions) Key Drivers & Statistics ($ in millions) Q2 2024 $193.3 Mortgage Production Income & Fees (12.2) Securities and Investment Advisory Fees & Commissions 14.3 Other Income (2.8) Q2 2025 $192.6 Q2'24 Q1'25 Q2'25 Broker-Dealer TBA Lock Volume ($mm) $835 $812 $1,154 Mortgage Origination Volume ($B) $2.4 $1.7 $2.4 Net gains from mortgage loan sales (bps): Loans sold to third parties 223 222 223 Broker Fee Income 10 10 10 Impact of loans retained by the bank (5) (8) (5) As reported 228 224 228 • Other Income includes $9.5 million impact from the legal settlement at PrimeLending |

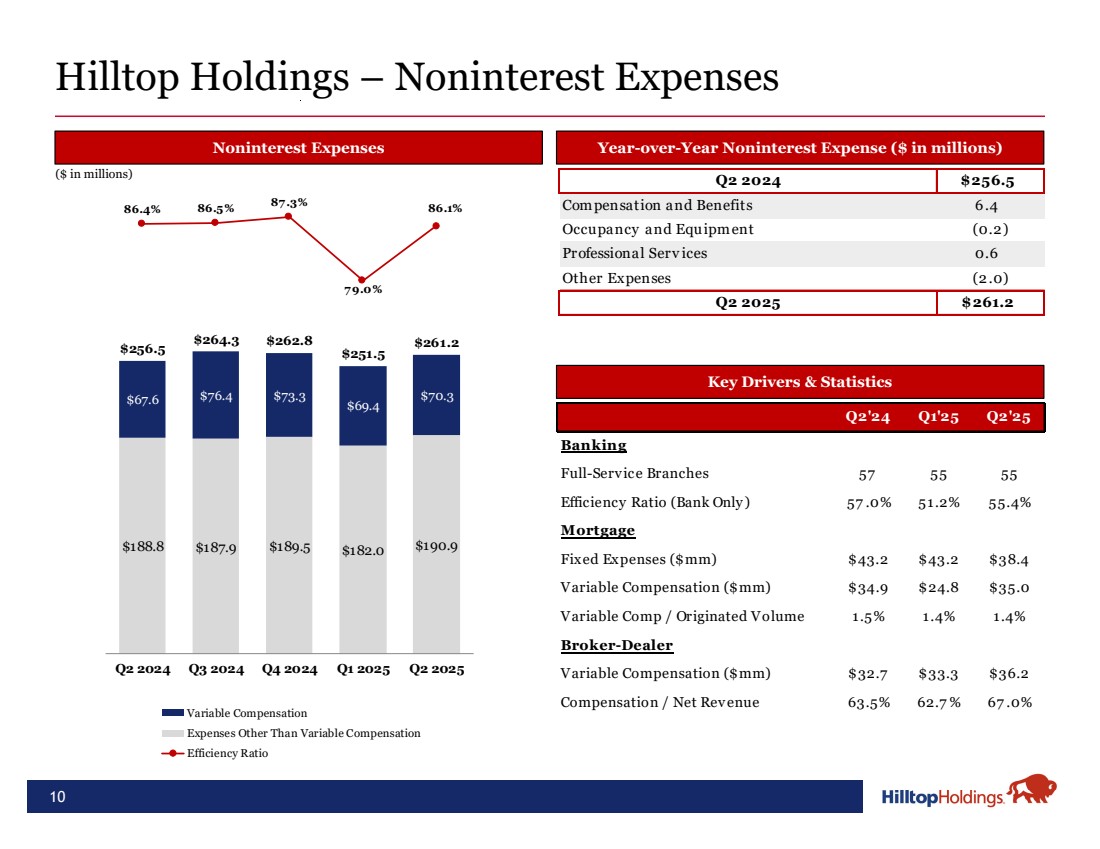

| $188.8 $187.9 $189.5 $182.0 $190.9 $67.6 $76.4 $73.3 $69.4 $70.3 $256.5 $264.3 $262.8 $251.5 $261.2 86.4% 86.5% 87 .3% 7 9.0% 86.1% Q2 2024 Q3 2024 Q4 2024 Q1 2025 Q2 2025 $0.0 $5 0. 0 $ 100.0 $ 15 0.0 $2 0. 0 $2 50 .0 $3 0. 0 $350 .0 $4 0. 0 Variable Compensation Expenses Other Than Variable Compensation Efficiency Ratio 10 Hilltop Holdings – Noninterest Expenses Noninterest Expenses Year-over-Year Noninterest Expense ($ in millions) Key Drivers & Statistics ($ in millions) Q2 2024 $256.5 Com pensation and Benefits 6.4 Occupancy and Equipment (0.2) Professional Serv ices 0.6 Other Expenses (2.0) Q2 2025 $261.2 Q2'24 Q1'25 Q2'25 Banking Full-Serv ice Branches 57 55 55 Efficiency Ratio (Bank Only) 57 .0% 51.2% 55.4% Mortgage Fixed Expenses ($mm) $43.2 $43.2 $38.4 Variable Compensation ($mm) $34.9 $24.8 $35.0 Variable Comp / Originated Volume 1.5% 1.4% 1.4% Broker-Dealer Variable Compensation ($mm) $32.7 $33.3 $36.2 Compensation / Net Rev enue 63.5% 62.7 % 67 .0% |

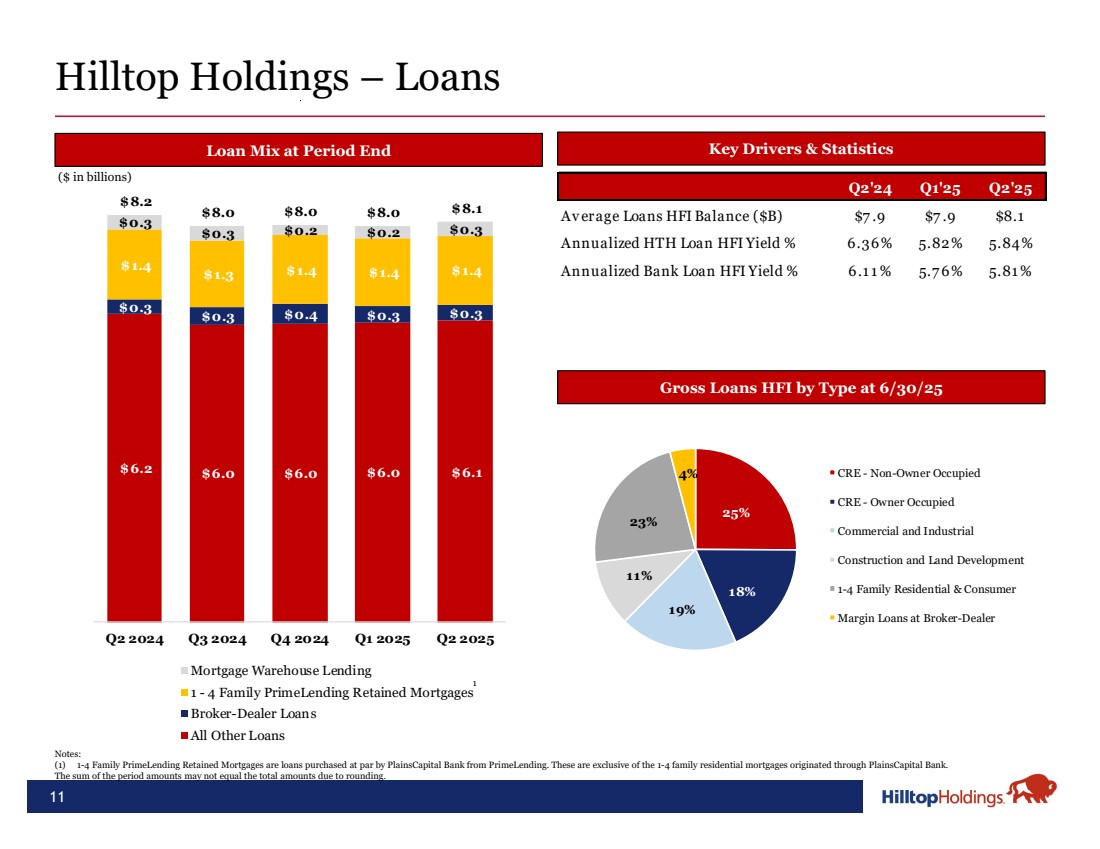

| $6.2 $6.0 $6.0 $6.0 $6.1 $0.3 $0.3 $0.4 $0.3 $0.3 $1.4 $1.3 $1.4 $1.4 $1.4 $0.3 $0.3 $0.2 $0.2 $0.3 $8.2 $8.0 $8.0 $8.0 $8.1 Q2 2024 Q3 2024 Q4 2024 Q1 2025 Q2 2025 Mortgage Warehouse Lending 1 - 4 Family PrimeLending Retained Mortgages Broker-Dealer Loans All Other Loans 11 Notes: (1) 1-4 Family PrimeLending Retained Mortgages are loans purchased at par by PlainsCapital Bank from PrimeLending. These are exclusive of the 1-4 family residential mortgages originated through PlainsCapital Bank. The sum of the period amounts may not equal the total amounts due to rounding. Loan Mix at Period End Hilltop Holdings – Loans Key Drivers & Statistics Q2'24 Q1'25 Q2'25 Av erage Loans HFI Balance ($B) $7 .9 $7 .9 $8.1 Annualized HTH Loan HFI Yield % 6.36% 5.82% 5.84% Annualized Bank Loan HFI Yield % 6.1 1 % 5.7 6% 5.81 % Gross Loans HFI by Type at 6/30/25 ($ in billions) 25% 18% 19% 11% 23% 4% CRE - Non-Owner Occupied CRE - Owner Occupied Commercial and Industrial Construction and Land Development 1-4 Family Residential & Consumer Margin Loans at Broker-Dealer 1 |

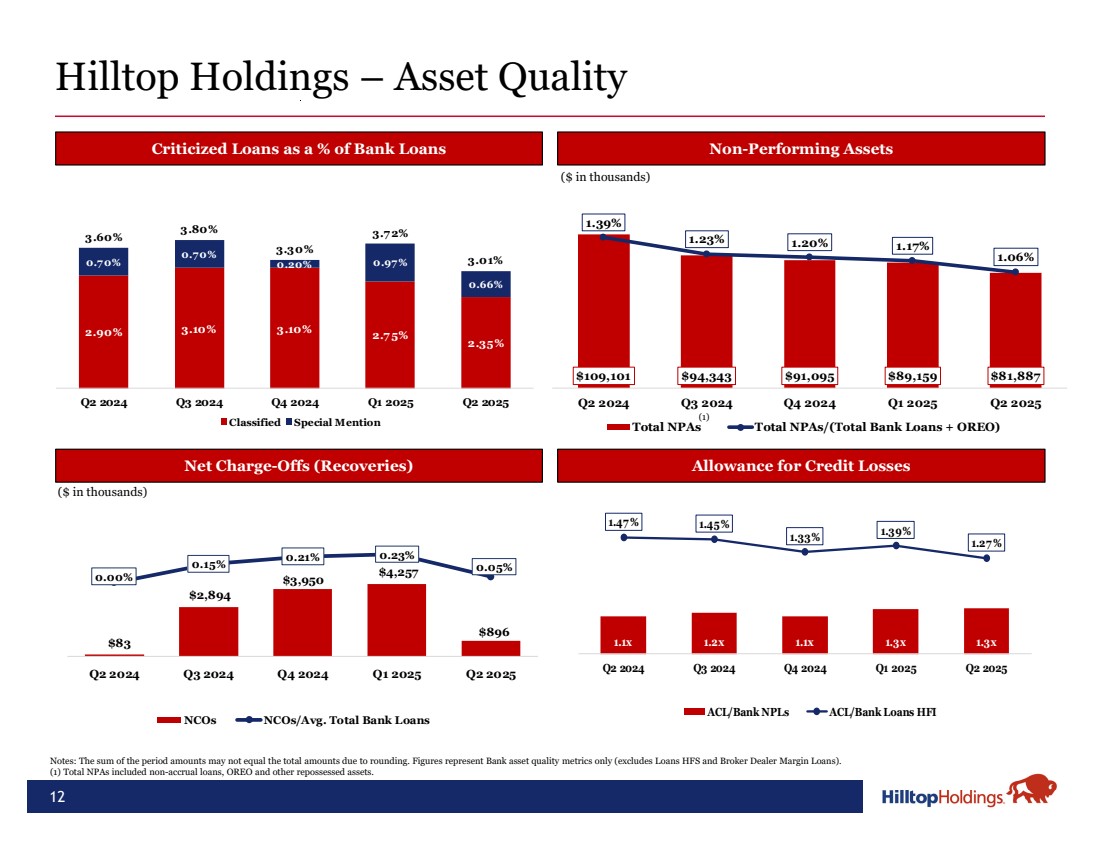

| $109,101 $94,343 $91,095 $89,159 $81,887 1.39% 1.23% 1.20% 1.17% 1.06% -0.0 0.20 0.45 0.70 0.95 1.20 1.45% 1.70% $0 $25,000 $50,000 $75,000 $100,000 $125,000 Q2 2024 Q3 2024 Q4 2024 Q1 2025 Q2 2025 Total NPAs Total NPAs/(Total Bank Loans + OREO) $83 $2,894 $3,950 $4,257 $896 0.00% 0.15% 0.21% 0.23% 0.05% -1.00% -0.80% -0.60% -0.40% -0.20% 0.00% 0.20% 0.40% $(3,000) $(1,000) $1,000 $3,000 $5,000 $7,000 Q2 2024 Q3 2024 Q4 2024 Q1 2025 Q2 2025 NCOs NCOs/Avg. Total Bank Loans 1.1x 1.2x 1.1x 1.3x 1.3x 1.47 % 1.45% 1.33% 1.39% 1.27 % 0.00% 0.50% 1.00% 1.50% 2.00% -1.0x 0.0x 1.0x 2.0x 3.0x 4.0x 5.0x Q2 2024 Q3 2024 Q4 2024 Q1 2025 Q2 2025 ACL/Bank NPLs ACL/Bank Loans HFI 12 Hilltop Holdings – Asset Quality Criticized Loans as a % of Bank Loans Non-Performing Assets Notes: The sum of the period amounts may not equal the total amounts due to rounding. Figures represent Bank asset quality metrics only (excludes Loans HFS and Broker Dealer Margin Loans). (1) Total NPAs included non-accrual loans, OREO and other repossessed assets. Net Charge-Offs (Recoveries) Allowance for Credit Losses ($ in thousands) ($ in thousands) 2.90% 3.10% 3.10% 2.7 5% 2.35% 0.70% 0.70% 0.20% 0.97% 0.66% 3.60% 3.80% 3.30% 3.7 2% 3.01% Q2 2024 Q3 2024 Q4 2024 Q1 2025 Q2 2025 Classified Special Mention (1) |

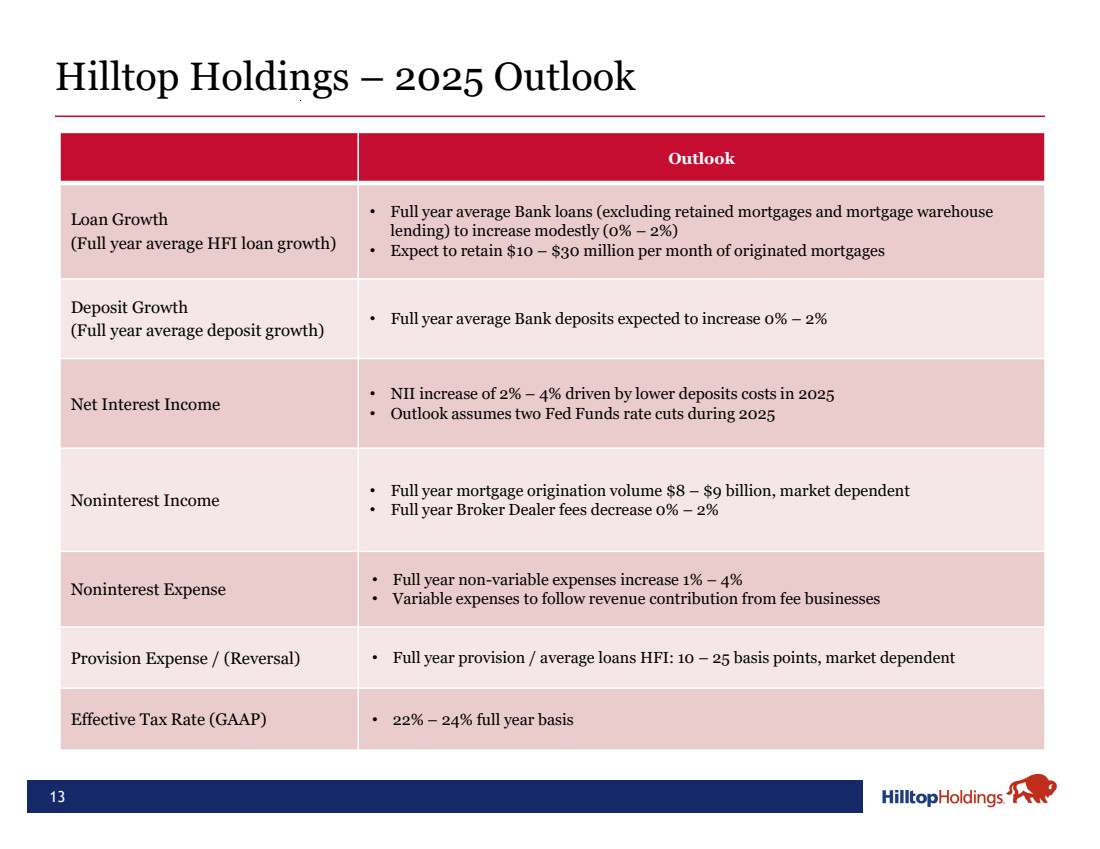

| 13 Hilltop Holdings – 2025 Outlook Outlook • Full year average Bank loans (excluding retained mortgages and mortgage warehouse lending) to increase modestly (0% – 2%) • Expect to retain $10 – $30 million per month of originated mortgages Loan Growth (Full year average HFI loan growth) • Full year average Bank deposits expected to increase 0% – 2% Deposit Growth (Full year average deposit growth) • NII increase of 2% – 4% driven by lower deposits costs in 2025 • Outlook assumes two Fed Funds rate cuts during 2025 Net Interest Income • Full year mortgage origination volume $8 – $9 billion, market dependent • Full year Broker Dealer fees decrease 0% – 2% Noninterest Income • Full year non-variable expenses increase 1% – 4% • Variable expenses to follow revenue contribution from fee businesses Noninterest Expense Provision Expense / (Reversal) • Full year provision / average loans HFI: 10 – 25 basis points, market dependent Effective Tax Rate (GAAP) • 22% – 24% full year basis |

| Appendix 14 |

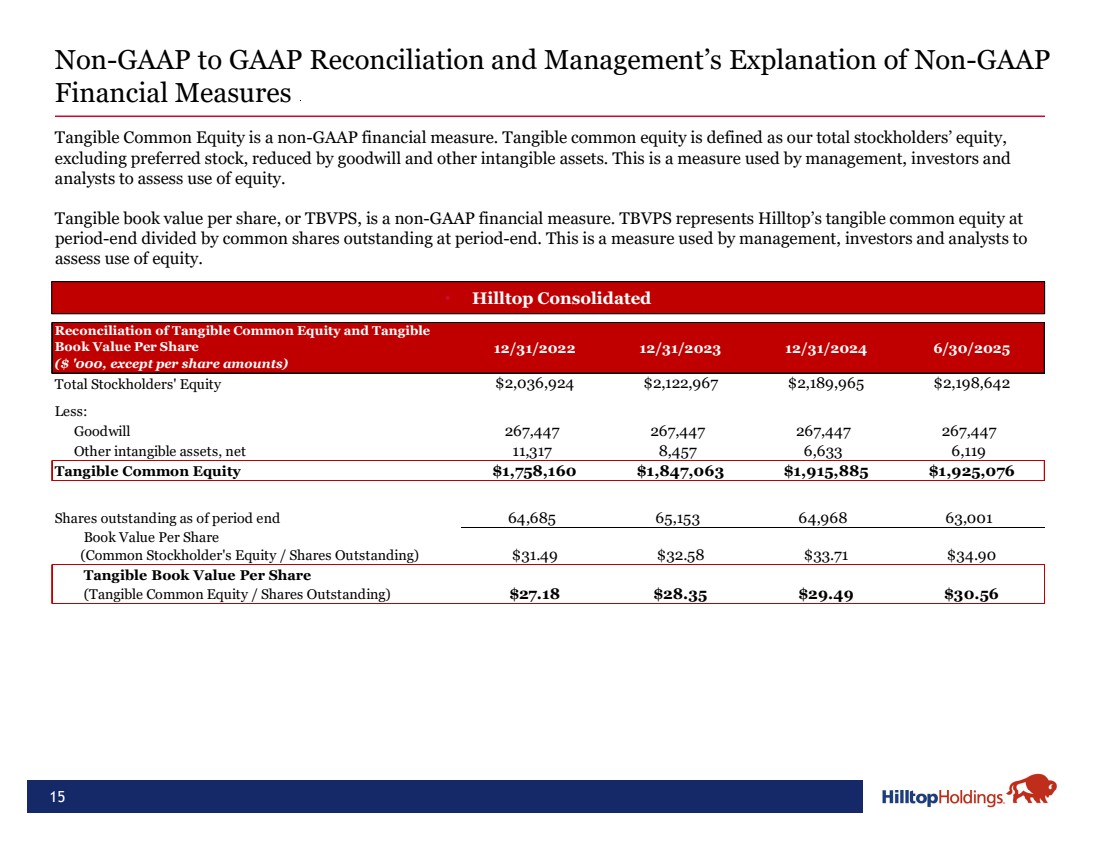

| 15 Non-GAAP to GAAP Reconciliation and Management’s Explanation of Non-GAAP Financial Measures • Hilltop Consolidated Tangible Common Equity is a non-GAAP financial measure. Tangible common equity is defined as our total stockholders’ equity, excluding preferred stock, reduced by goodwill and other intangible assets. This is a measure used by management, investors and analysts to assess use of equity. Tangible book value per share, or TBVPS, is a non-GAAP financial measure. TBVPS represents Hilltop’s tangible common equity at period-end divided by common shares outstanding at period-end. This is a measure used by management, investors and analysts to assess use of equity. Reconciliation of Tangible Common Equity and Tangible Book Value Per Share ($ '000, except per share amounts) 12/31/2022 12/31/2023 12/31/2024 6/30/2025 Total Stockholders' Equity $2,036,924 $2,122,967 $2,189,965 $2,198,642 Less: Goodwill 267,447 267,447 267,447 267,447 Other intangible assets, net 11,317 8,457 6,633 6,119 Tangible Common Equity $1,758,160 $1,847,063 $1,915,885 $1,925,076 Shares outstanding as of period end 64,685 65,153 64,968 63,001 Book Value Per Share (Common Stockholder's Equity / Shares Outstanding) $31.49 $32.58 $33.71 $34.90 Tangible Book Value Per Share (Tangible Common Equity / Shares Outstanding) $27.18 $28.35 $29.49 $30.56 |

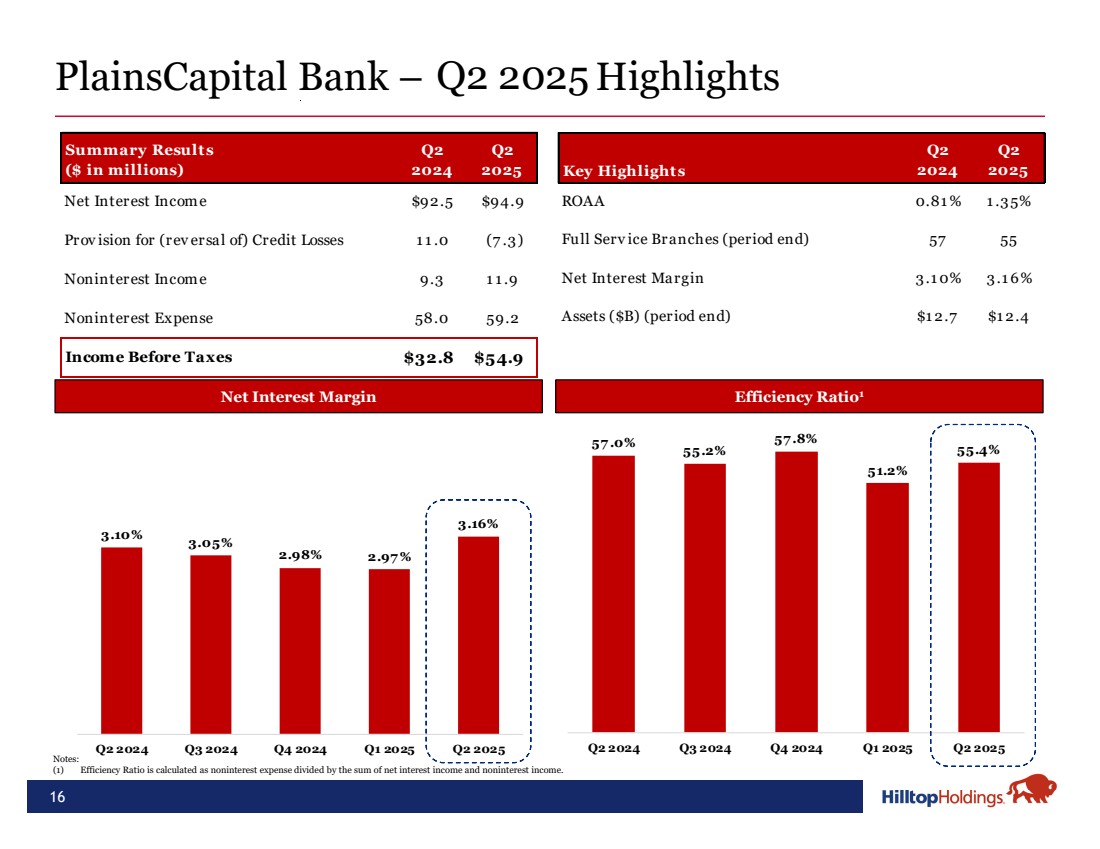

| 57 .0% 55.2% 57 .8% 51.2% 55.4% Q2 2024 Q3 2024 Q4 2024 Q1 2025 Q2 2025 3.10% 3.05% 2.98% 2.97 % 3.16% Q2 2024 Q3 2024 Q4 2024 Q1 2025 Q2 2025 PlainsCapital Bank – Highlights Q2 2025 16 Efficiency Ratio1 Notes: (1) Efficiency Ratio is calculated as noninterest expense divided by the sum of net interest income and noninterest income. Net Interest Margin Summary Results ($ in millions) Q2 2024 Q2 2025 Net Interest Income $92.5 $94.9 Prov ision for (rev ersal of) Credit Losses 1 1 .0 (7 .3) Noninterest Income 9.3 1 1 .9 Noninterest Expense 58.0 59.2 Income Before Taxes $32.8 $54.9 Key Highlights Q2 2024 Q2 2025 ROAA 0.81 % 1 .35% Full Serv ice Branches (period end) 57 55 Net Interest Margin 3.1 0% 3.1 6% Assets ($B) (period end) $1 2.7 $1 2.4 |

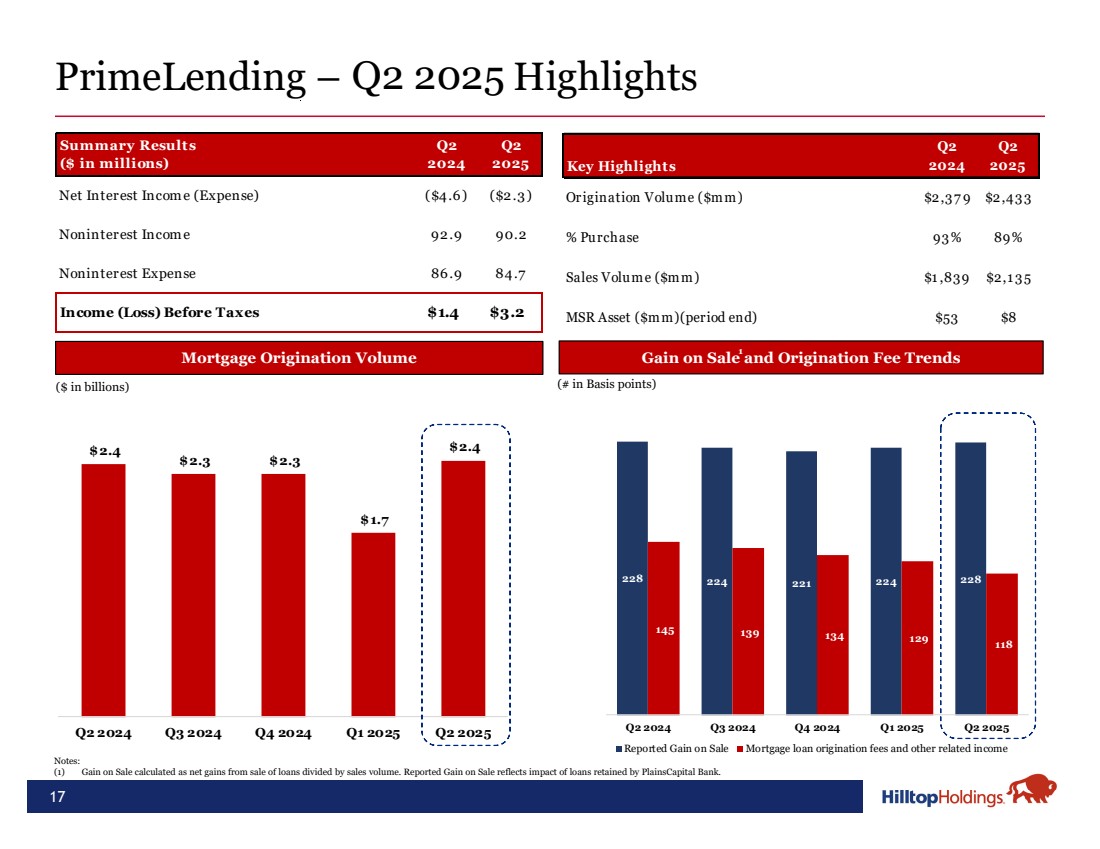

| 17 PrimeLending – Highlights Gain on Sale and Origination Fee Trends Notes: (1) Gain on Sale calculated as net gains from sale of loans divided by sales volume. Reported Gain on Sale reflects impact of loans retained by PlainsCapital Bank. 1 Mortgage Origination Volume $2.4 $2.3 $2.3 $1.7 $2.4 Q2 2024 Q3 2024 Q4 2024 Q1 2025 Q2 2025 ($ in billions) Q2 2025 (# in Basis points) Key Highlights Q2 2024 Q2 2025 Origination Volum e ($m m ) $2,37 9 $2,43 3 % Purchase 93% 89% Sales Volum e ($m m ) $1 ,839 $2,1 3 5 MSR Asset ($m m)(period end) $53 $8 228 224 221 224 228 145 139 134 129 118 Q2 2024 Q3 2024 Q4 2024 Q1 2025 Q2 2025 Reported Gain on Sale Mortgage loan origination fees and other related income Summary Results ($ in millions) Q2 2024 Q2 2025 Net Interest Income (Expense) ($4.6) ($2.3) Noninterest Income 92.9 90.2 Noninterest Expense 86.9 84.7 Income (Loss) Before Taxes $1.4 $3.2 |

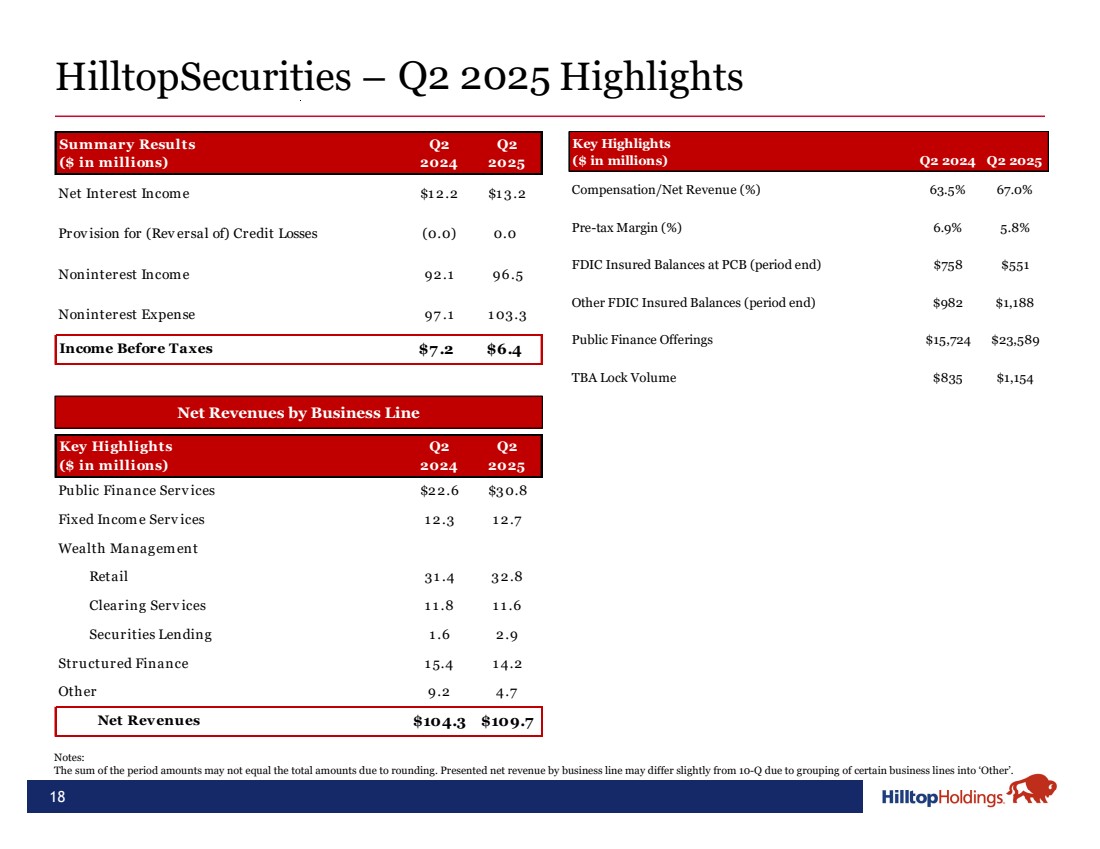

| HilltopSecurities – Highlights Q2 2025 18 Notes: The sum of the period amounts may not equal the total amounts due to rounding. Presented net revenue by business line may differ slightly from 10-Q due to grouping of certain business lines into ‘Other’. Net Revenues by Business Line Key Highlights ($ in millions) Q2 2024 Q2 2025 Public Finance Serv ices $22.6 $30.8 Fixed Income Serv ices 1 2.3 1 2.7 Wealth Management Retail 31 .4 32.8 Clearing Serv ices 1 1 .8 1 1 .6 Securities Lending 1 .6 2.9 Structured Finance 1 5.4 1 4.2 Other 9.2 4.7 Net Revenues $104.3 $109.7 Key Highlights ($ in millions) Q2 2024 Q2 2025 Compensation/Net Revenue (%) 63.5% 67.0% Pre-tax Margin (%) 6.9% 5.8% FDIC Insured Balances at PCB (period end) $758 $551 Other FDIC Insured Balances (period end) $982 $1,188 Public Finance Offerings $15,724 $23,589 TBA Lock Volume $835 $1,154 Summary Results ($ in millions) Q2 2024 Q2 2025 Net Interest Income $1 2.2 $1 3.2 Prov ision for (Rev ersal of) Credit Losses (0.0) 0.0 Noninterest Income 92.1 96.5 Noninterest Expense 97 .1 1 03.3 Income Before Taxes $7 .2 $6.4 |

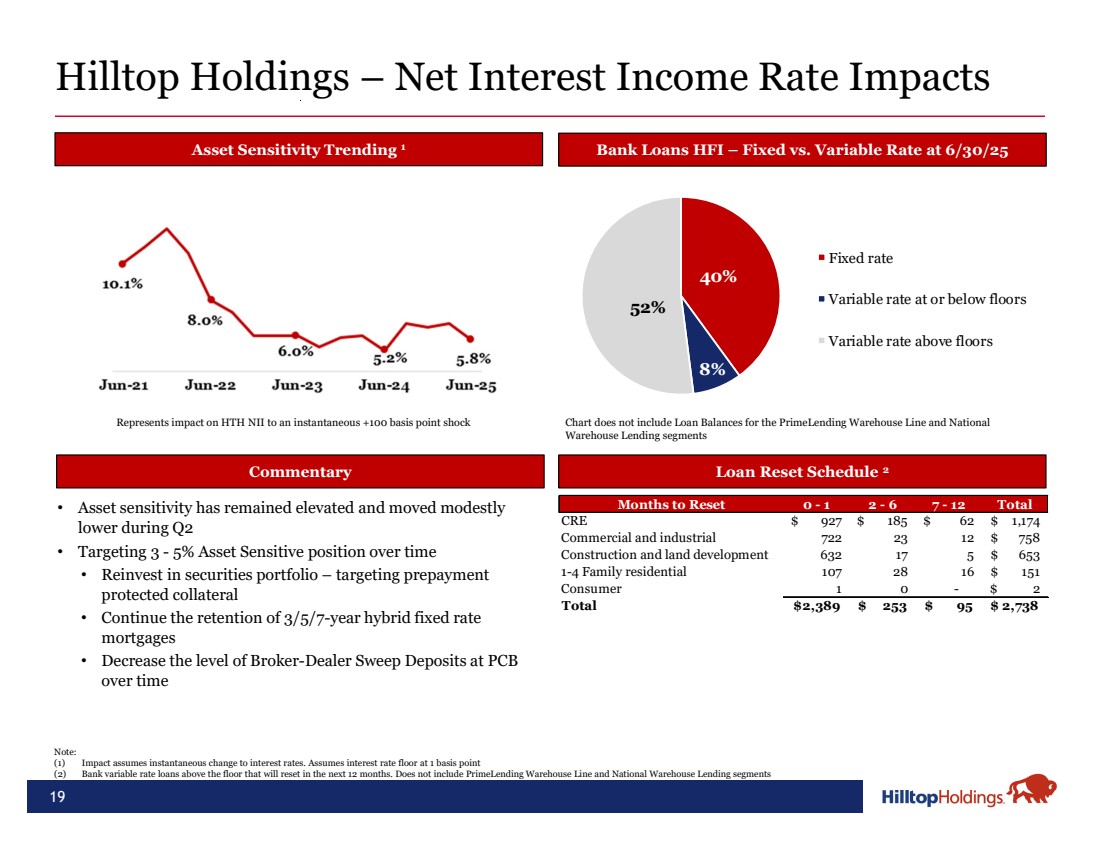

| 19 Hilltop Holdings – Net Interest Income Rate Impacts Asset Sensitivity Trending 1 Note: (1) Impact assumes instantaneous change to interest rates. Assumes interest rate floor at 1 basis point (2) Bank variable rate loans above the floor that will reset in the next 12 months. Does not include PrimeLending Warehouse Line and National Warehouse Lending segments Loan Reset Schedule 2 Bank Loans HFI – Fixed vs. Variable Rate at 6/30/25 40% 8% 52% Fixed rate Variable rate at or below floors Variable rate above floors Chart does not include Loan Balances for the PrimeLending Warehouse Line and National Warehouse Lending segments Represents impact on HTH NII to an instantaneous +100 basis point shock Commentary • Asset sensitivity has remained elevated and moved modestly lower during Q2 • Targeting 3 - 5% Asset Sensitive position over time • Reinvest in securities portfolio – targeting prepayment protected collateral • Continue the retention of 3/5/7-year hybrid fixed rate mortgages • Decrease the level of Broker-Dealer Sweep Deposits at PCB over time Months to Reset 0 - 1 2 - 6 7 - 12 Total CRE 927 $ 185 $ 62 $ 1,174 $ Commercial and industrial 722 23 12 758 $ Construction and land development 632 17 5 653 $ 1-4 Family residential 107 28 16 151 $ Consumer 1 0 - 2 $ Total 2,389 $ 253 $ 95 $ 2,738 $ |

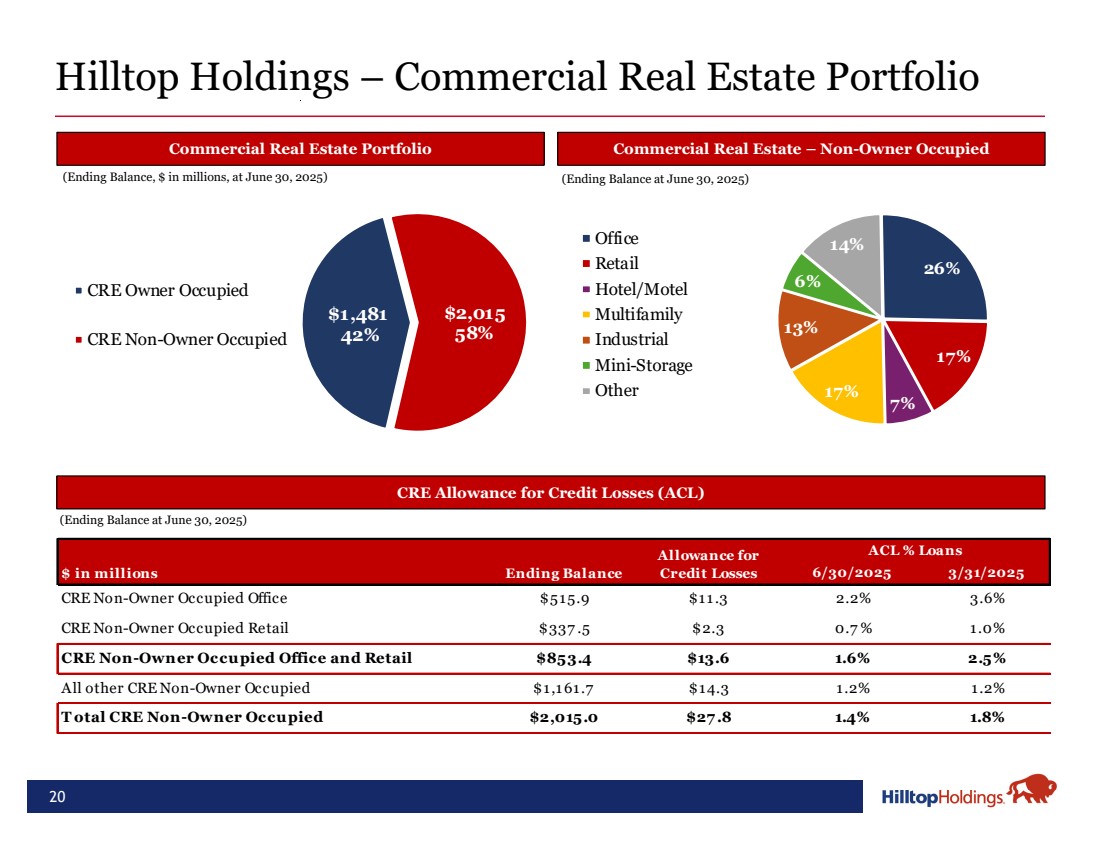

| 20 Hilltop Holdings – Commercial Real Estate Portfolio Commercial Real Estate Portfolio (Ending Balance, $ in millions, at June 30, 2025) CRE Allowance for Credit Losses (ACL) Commercial Real Estate – Non-Owner Occupied (Ending Balance at June 30, 2025) (Ending Balance at June 30, 2025) $1,481 42% $2,015 58% CRE Owner Occupied CRE Non-Owner Occupied 26% 17% 7% 17% 13% 6% Office 14% Retail Hotel/Motel Multifamily Industrial Mini-Storage Other 6/30/2025 3/31/2025 CRE Non-Owner Occupied Office $515.9 $11.3 2.2% 3.6% CRE Non-Owner Occupied Retail $337 .5 $2.3 0.7 % 1.0% CRE Non-Owner Occupied Office and Retail $853.4 $13.6 1.6% 2.5% All other CRE Non-Owner Occupied $1,161.7 $14.3 1.2% 1.2% T otal CRE Non-Owner Occupied $2,015.0 $27 .8 1.4% 1.8% $ in millions Ending Balance Allowance for Credit Losses ACL % Loans |

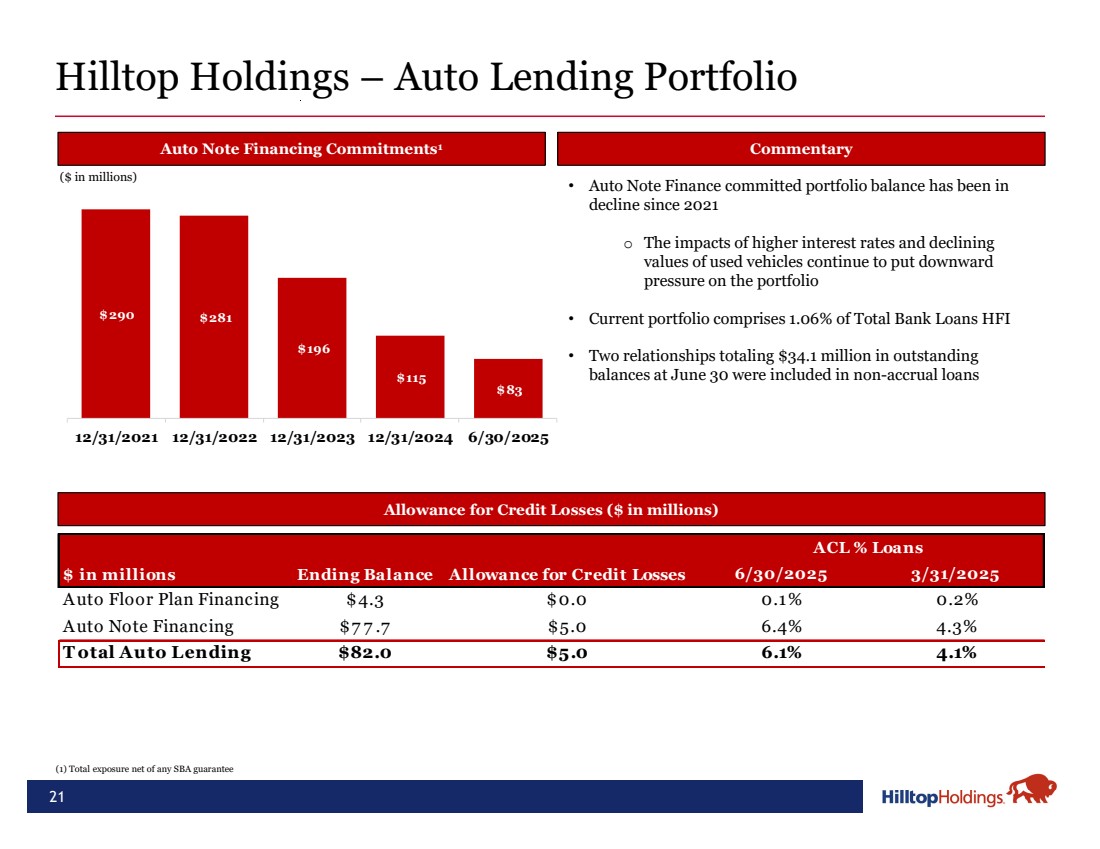

| 21 Hilltop Holdings – Auto Lending Portfolio Auto Note Financing Commitments1 Commentary Allowance for Credit Losses ($ in millions) • Auto Note Finance committed portfolio balance has been in decline since 2021 o The impacts of higher interest rates and declining values of used vehicles continue to put downward pressure on the portfolio • Current portfolio comprises 1.06% of Total Bank Loans HFI • Two relationships totaling $34.1 million in outstanding balances at June 30 were included in non-accrual loans (1) Total exposure net of any SBA guarantee ($ in millions) $290 $281 $196 $115 $83 12/31/2021 12/31/2022 12/31/2023 12/31/2024 6/30/2025 6/30/2025 3/31/2025 Auto Floor Plan Financing $4.3 $0.0 0.1% 0.2% Auto Note Financing $7 7 .7 $5.0 6.4% 4.3% T otal Auto Lending $82.0 $5.0 6.1% 4.1% $ in millions Ending Balance Allowance for Credit Losses ACL % Loans |