|

MANAGEMENT'S DISCUSSION AND ANALYSIS FOR THE YEAR ENDED DECEMBER 31, 2021 |

This Management Discussion and Analysis ("MD&A") should be read in conjunction with the consolidated financial statements of Endeavour Silver Corp. ("Endeavour" or "the Company") for the year ended December 31, 2021 and the related notes contained therein, which were prepared in accordance with International Financial Reporting Standards ("IFRS") as issued by the International Accounting Standards Board ("IASB"). The Company uses certain non-IFRS financial measures in this MD&A as described under "Non-IFRS Measures". Additional information relating to the Company, including the most recent Annual Information Form (the "Annual Information Form"), is available on SEDAR at www.sedar.com, and the Company's most recent annual report on Form 40-F has been filed with the U.S. Securities and Exchange Commission (the "SEC"). This MD&A contains "forward-looking statements" that are subject to risk factors set out in a cautionary note contained herein. All dollar ($) amounts are expressed in United States ("$.") dollars and tabular amounts are expressed in thousands of U.S. dollars unless Canadian dollars (CAN$) are otherwise indicated. This MD&A is dated as of March 8, 2022 and all information contained is current as of March 8, 2022 unless otherwise stated.

Cautionary Note to U.S. Investors Regarding Mineral Reserves and Resources

This MD&A has been prepared in accordance with the requirements of Canadian provincial securities laws, which differ from the requirements of U.S. securities laws. As a result, the Company reports the mineral reserves and resources of the projects it has an interest in according to Canadian standards. Canadian reporting requirements for disclosure of mineral properties are governed by National Instrument 43 101 - Standards of Disclosure for Mineral Projects ("NI 43 101"). NI 43 101 is a rule developed by the Canadian Securities Administrators that establishes standards for all public disclosure an issuer makes of scientific and technical information concerning mineral projects. These standards differ from the requirements of the SEC that are applicable to domestic United States reporting companies under subpart 1300 of Regulation S-K ("S K 1300") under the Exchange Act. As an issuer that prepares and files its reports with the SEC pursuant to the MJDS, the Company is not subject to the requirements of S K 1300. Any mineral reserves and mineral resources reported by the Company in accordance with NI 43 101 may not qualify as such under or differ from those prepared in accordance with S K 1300. Accordingly, information included or incorporated by reference in this MD&A concerning descriptions of mineralization and estimates of mineral reserves and resources under Canadian standards may not be comparable to similar information made public by United States companies subject to the reporting and disclosure requirements of S K 130

|

MANAGEMENT'S DISCUSSION AND ANALYSIS FOR THE YEAR ENDED DECEMBER 31, 2021 |

Forward-Looking Statements

This MD&A contains "forward-looking statements" within the meaning of the U.S. Securities Litigation Reform Act of 1995, as amended and "forward-looking information" within the meaning of applicable Canadian securities legislation. Such forward-looking statements and information include, but are not limited to, statements regarding Endeavour's anticipated performance in 2022, including silver and gold production, financial results, timing and expenditures to develop new silver mines and mineralized zones, silver and gold grades and recoveries, cash costs per ounce (oz), capital expenditures and sustaining capital and the impact of the COVID 19 pandemic on operations. Forward-looking statements are frequently characterized by words such as "plan", "expect", "forecast", "project", "intend", "believe", "anticipate", "outlook" and other similar words, or statements that certain events or conditions "may" or "will" occur. Forward- looking statements are based on the opinions and estimates of management at the dates the statements are made, and are subject to a variety of risks and uncertainties and other factors that could cause actual events or results to differ materially from those projected in the forward-looking statements.

The Company does not intend to, and does not assume any obligation to, update such forward-looking statements or information, other than as required by applicable law. Forward-looking statements or information involve known and unknown risks, uncertainties and other factors and are based on assumptions that may cause the actual results, level of activity, performance or achievements of the Company and its operations to be materially different from those expressed or implied by such statements. Such factors and assumptions include, among others: the ultimate impact of the COVID 19 pandemic on operations and results, fluctuations in the prices of silver and gold, fluctuations in the currency markets (particularly the Mexican peso, Chilean peso, Canadian dollar and U.S. dollar); changes in national and local governments, legislation, taxation, controls, regulations and political or economic developments in Canada and Mexico; operating or technical difficulties in mineral exploration, development and mining activities; risks and hazards of mineral exploration, development and mining (including, but not limited to environmental hazards, industrial accidents, unusual or unexpected geological conditions, pressures, cave-ins and flooding); inadequate insurance, or inability to obtain insurance; availability of and costs associated with mining inputs and labour; the speculative nature of mineral exploration and development, diminishing quantities or grades of mineral reserves as properties are mined; the ability to successfully integrate acquisitions; risks in obtaining necessary licenses and permits, and challenges to the Company's title to properties; as well as those factors described under "Risk Factors" in the Company's Annual Information Form. Although the Company has attempted to identify important factors that could cause actual results to differ materially from those contained in forward-looking statements or information, there may be other factors that cause results to be materially different from those anticipated, described, estimated, assessed or intended. There can be no assurance that any forward-looking statements or information will prove to be accurate as actual results and future events could differ materially from those anticipated in such statements or information. Accordingly, readers should not place undue reliance on forward-looking statements or information.

Qualified Person

The scientific and technical information contained in this MD&A relating to the Company's mines and mineral projects has been reviewed and approved by Dale Mah, B.Sc., P.Geo., Vice President Corporate Development of Endeavour, a Qualified Person within the meaning of NI 43-101.

Table of Contents

|

MANAGEMENT'S DISCUSSION AND ANALYSIS FOR THE YEAR ENDED DECEMBER 31, 2021 |

OPERATING HIGHLIGHTS

| Three Months Ended December 31 | 2021 Highlights | Year Ended December 31 | ||||

| 2021 | 2020 | % Change | 2021 | 2020 | % Change | |

| Production | ||||||

| 1,443,564 | 1,117,289 | 29% | Silver ounces produced | 4,870,787 | 3,513,767 | 39% |

| 9,446 | 12,586 | (25%) | Gold ounces produced | 42,262 | 37,139 | 14% |

| 1,432,578 | 1,108,848 | 29% | Payable silver ounces produced | 4,826,681 | 3,482,094 | 39% |

| 9,261 | 12,314 | (25%) | Payable gold ounces produced | 41,438 | 36,392 | 14% |

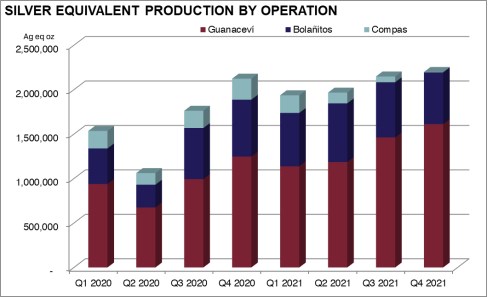

| 2,199,244 | 2,124,169 | 4% | Silver equivalent ounces produced(1) | 8,251,747 | 6,484,887 | 27% |

| 8.65 | 6.83 | 27% | Cash costs per silver ounce(2)(3) | 9.31 | 5.55 | 68% |

| 11.99 | 14.58 | (18%) | Total production costs per ounce(2)(4) | 14.70 | 14.01 | 5% |

| 19.48 | 18.52 | 5% | All-in sustaining costs per ounce(2)(5) | 20.34 | 17.59 | 16% |

| 213,492 | 237,389 | (10%) | Processed tonnes | 887,424 | 757,160 | 17% |

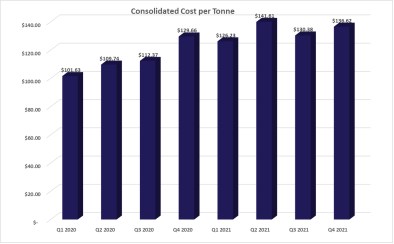

| 112.91 | 105.07 | 7% | Direct operating costs per tonne(2)(6) | 115.36 | 101.17 | 14% |

| 136.62 | 129.66 | 5% | Direct costs per tonne(2)(6) | 133.97 | 114.57 | 17% |

| 13.41 | 14.83 | (10%) | Silver co-product cash costs(7) | 15.11 | 12.97 | 16% |

| 1,038 | 1,129 | (8%) | Gold co-product cash costs(7) | 1,072 | 1,109 | (3%) |

| Financial | ||||||

| 48.5 | 60.7 | (20%) | Revenue ($ millions) | 165.3 | 138.4 | 19% |

| 1,413,699 | 1,419,037 | (0%) | Silver ounces sold | 3,856,883 | 3,460,638 | 11% |

| 8,715 | 13,850 | (37%) | Gold ounces sold | 39,113 | 35,519 | 10% |

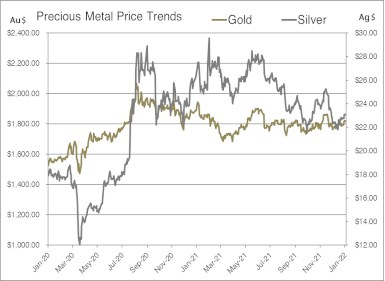

| 23.41 | 24.76 | (5%) | Realized silver price per ounce | 25.22 | 21.60 | 17% |

| 1,811 | 1,885 | (4%) | Realized gold price per ounce | 1,790 | 1,846 | (3%) |

| (0.5) | 19.9 | (102%) | Net earnings (loss) ($ millions) | 14.0 | 1.2 | 1104% |

| (0.5) | 20.3 | (102%) | Adjusted net earnings (loss) (11) ($ millions) | (8.6) | 1.6 | (646%) |

| 12.2 | 20.8 | 41% | Mine operating earnings (loss) ($ millions) | 36.4 | 27.3 | 33% |

| 18.2 | 30.2 | (40%) | Mine operating cash flow before taxes ($ millions)(8) | 61.9 | 56.2 | 10% |

| 10.7 | 21.6 | (51%) | Operating cash flow before working capital changes(9) | 32.2 | 28.8 | 12% |

| 10.7 | 24.3 | (56%) | Earnings before ITDA(10) ($ millions) | 54.9 | 29.4 | 87% |

| 121.2 | 70.4 | 72% | Working capital(12) ($ millions) | 121.2 | 70.4 | 72% |

| Shareholders | ||||||

| 0.00 | 0.13 | (100%) | Earnings (loss) per share - basic | 0.08 | 0.01 | 700% |

| 0.00 | 0.13 | (98%) | Adjusted earnings (loss) per share - basic(8) | (0.05) | 0.01 | (593%) |

| 0.06 | 0.14 | (54%) | Operating cash flow before working capital changes per share(9) | 0.19 | 0.19 | 1% |

| 170,518,894 | 157,536,658 | 8% | Weighted average shares outstanding | 167,289,732 | 150,901,598 | 11% |

(1) Silver equivalents are calculated using an 80:1 (Ag/Au) ratio.

(2) The Company reports non-IFRS measures and ratios which include cash costs net of by-product revenue on a payable silver basis, total production costs per oz, all-in sustaining costs ("AISC") per oz, direct operating cost per tonne, direct cost per tonne, silver co-product cash costs and gold co-product cash costs in order to manage and evaluate operating performance at each of the Company's mines. These measures, some established by the Silver Institute (Production Cost Standards, June 2011), are widely used in the silver mining industry as a benchmark for performance, but do not have a standardized meaning. These measures are reported on a production basis. See Reconciliations to IFRS beginning on page 20.

(3) Cash costs net of by-product revenue per payable silver oz include mining, processing (including smelting, refining, transportation and selling costs), and direct overhead, net of gold credits. See Reconciliation to IFRS on pages 23 and 24.

(4) Total production costs per oz include mining, processing (including smelting, refining, transportation and selling costs), direct overhead, amortization, depletion and amortization at the operation sites net of by-product revenues. See Reconciliation to IFRS on pages 23 and 24.

(5) AlSC per oz include mining, processing (including smelting, refining, transportation and selling costs), direct overhead, corporate general and administration expenses, on-site exploration, share-based compensation, reclamation and sustaining capital net of gold credits. See Reconciliation to IFRS on pages 24 to 26.

(6) Direct operating costs per tonne include mining, processing (including smelting, refining, transportation and selling costs) and direct overhead at the operation sites. Direct cost per tonne include all direct operating costs, royalties and special mining duty. See Reconciliation to IFRS on pages 23 and 24.

(7) Silver co-product cash cost and gold co-product cash cost include mining, processing (including smelting, refining, transportation and selling costs), and direct overhead allocated on pro-rated basis of realized metal value. See Reconciliation to IFRS on pages 26 and 27.

(8) Mine operating cash flow is calculated by adding back amortization, depletion, inventory write-downs and share-based compensation to mine operating earnings. Mine operating earnings and mine operating cash flow are before taxes. See Reconciliation to IFRS on page 22.

(9) See Reconciliation to IFRS on page 22 for the reconciliation of operating cash flow before working capital changes and for the operating cash flow before working capital changes per share.

(10) See Reconciliation of Earnings before interest, taxes, depreciation and amortization on pages 22 and 23.

(11) Adjusted net earnings is calculated by adding back reversals of impairment on non-current assets and the gain on asset disposal for the El Cubo mine, which had a significant effect on reported net earnings. See Reconciliation to IFRS on page 21.

(12) Working capital is calculated by deducting current liabilities from current assets. See Reconciliation to IFRS on page 21.

The above highlights are key measures used by management, however they should not be the sole measures used in determining the performance of the Company’s operations.

|

MANAGEMENT'S DISCUSSION AND ANALYSIS FOR THE YEAR ENDED DECEMBER 31, 2021 |

HISTORY AND STRATEGY

The Company is engaged in silver mining in Mexico and related activities including property acquisition, exploration, development, mineral extraction, processing, refining and reclamation. The Company is also engaged in exploration activities in Chile and Nevada, USA. Since 2002, the Company's business strategy has been to focus on acquiring advanced-stage silver mining properties in Mexico. Mexico, despite its long and prolific history of metal production, appears to be relatively under-explored using modern exploration techniques and offers promising geological potential for precious metals exploration and production.

The Company's Guanaceví and Bolañitos mines acquired in 2004 and 2007, respectively, demonstrate its initial business model of acquiring fully built and permitted silver mines that were about to close for lack of ore. Investing resources expertise needed to discover new silver ore-bodies, the Company successfully re-opened and expanded these mines to realize their full potential. The benefit of acquiring fully built and permitted mining and milling infrastructure is that, if new exploration efforts are successful, the mine development cycle from discovery to production only takes a matter of months instead of the several years normally required in the traditional mining business model.

In addition to operating the Guanaceví and Bolañitos mines in 2021, the Company also operated the El Compas mine. The Company acquired the El Compas mine in 2016, which was commissioned in March 2019, and operated until August 2021, when the Company suspended mining and milling operations. Management is currently evaluating it alternatives for the asset.

In 2012, the Company acquired the El Cubo silver-gold mine located in Guanajuato, Mexico, which was operated until November 2019. On March 17, 2021, the Company signed a definitive agreement to sell the El Cubo mine and related assets to Guanajuato Silver Company Ltd. ("GSilver") (formerly known as VanGold Mining Corp.) for a combination of cash and share payments plus additional contingency payments with completion of the sale on April, 9, 2021.

The Company is advancing the Terronera development project and on September 9, 2021 released a positive feasibility study for the project. The Company intends to make a formal construction decision, subject to completion of a financing package and receipt of amended permits.

On August 31, 2021 the Company acquired the Bruner Property, a gold exploration project, located in Nye County, Nevada. The Company paid $10 million in cash for 100% of the Bruner Gold Project which includes mineral claims, mining rights, property assets, water rights, and government authorizations and permits.

On January 12, 2022, the Company entered into a definitive agreement to purchase the Pitarrilla project in Durango State, Mexico from SSR Mining Inc. ("SSR") for total consideration of US$70 million, consisting of US$35 million in common shares and a further $35 million in cash or in common shares at the election of SSR and agreed to by the Company, and a grant of a 1.25% NSR royalty. Closing is expected to occur in the first half of 2022 and is subject to TSX and NYSE approvals and receipt of Mexican Federal Economics Competition Commission approval, as well as customary closing conditions for a transaction of this kind.

The Company is advancing several other exploration projects in order to achieve its goal to become a premier senior producer in the silver mining sector.

The Company has historically funded its acquisition, exploration and development activities through equity financings, debt facilities and convertible debentures. In recent years, the Company has financed most of its acquisition, exploration, development and operating activities from production cash flows, treasury and equity financings. The Company may choose to undertake equity, debt, convertible debt or other financings, on an as-needed basis, in order to facilitate its growth.

As of December 31, 2021, the Company held $103.3 million in cash and $121.2 million in working capital. Management believes there is sufficient working capital to meet the Company's current obligations, however the ultimate duration and severity of the COVID-19 pandemic remains uncertain and could impact the financial liquidity of the Company.

|

MANAGEMENT'S DISCUSSION AND ANALYSIS FOR THE YEAR ENDED DECEMBER 31, 2021 |

REVIEW OF OPERATING RESULTS

The Company operates the Guanaceví and Bolañitos mines. The Company suspended mining operations at the El Compas mine in August 2021 due to exhaustion of reserves and it currently remains on care and maintenance.

Consolidated Production Results for the Three Months and Years Ended December 31, 2021 and 2020

|

Three Months Ended December 31 |

CONSOLIDATED |

Years Ended December 31 |

||||

|

2021 |

2020 |

% Change |

|

2021 |

2020 |

% Change |

|

213,492 |

237,389 |

(10%) |

Ore tonnes processed |

887,424 |

757,160 |

17% |

|

235 |

169 |

39% |

Average silver grade (gpt) |

195 |

167 |

17% |

|

89.4 |

86.8 |

3% |

Silver recovery (%) |

87.6 |

86.5 |

1% |

|

1,443,564 |

1,117,289 |

29% |

Total silver ounces produced |

4,870,787 |

3,513,767 |

39% |

|

1,432,578 |

1,108,848 |

29% |

Payable silver ounces produced |

4,826,681 |

3,482,094 |

39% |

|

1.52 |

1.90 |

(20%) |

Average gold grade (gpt) |

1.65 |

1.78 |

(7%) |

|

90.8 |

87.0 |

4% |

Gold recovery (%) |

89.8 |

85.9 |

5% |

|

9,446 |

12,586 |

(25%) |

Total gold ounces produced |

42,262 |

37,139 |

14% |

|

9,261 |

12,314 |

(25%) |

Payable gold ounces produced |

41,438 |

36,392 |

14% |

|

2,199,244 |

2,124,169 |

4% |

Silver equivalent ounces produced(1) |

8,251,747 |

6,484,887 |

27% |

|

8.65 |

6.83 |

27% |

Cash costs per silver ounce(2)(3) |

9.31 |

5.55 |

68% |

|

11.98 |

14.58 |

(18%) |

Total production costs per ounce(2)(4) |

14.70 |

14.01 |

5% |

|

19.48 |

18.52 |

5% |

All in sustaining cost per ounce (2)(5) |

20.34 |

17.59 |

16% |

|

112.91 |

105.07 |

7% |

Direct operating costs per tonne(2)(6) |

115.36 |

101.17 |

14% |

|

136.62 |

129.66 |

5% |

Direct costs per tonne(2)(6) |

133.97 |

114.57 |

17% |

|

13.41 |

14.83 |

(10%) |

Silver co-product cash costs(7) |

15.11 |

12.97 |

16% |

|

1,038 |

1,129 |

(8%) |

Gold co-product cash costs(7) |

1,072 |

1,109 |

(3%) |

(1) Silver equivalents are calculated using an 80:1 (Ag/Au) ratio.

(2) The Company reports non-IFRS measures which include cash costs net of by-product revenue on a payable silver basis, total production costs per oz, AISC per oz, direct operating cost per tonne, direct cost per tonne, silver co-product cash costs and gold co-product cash costs in order to manage and evaluate operating performance at each of the Company's mines. These measures, some established by the Silver Institute (Production Cost Standards, June 2011), are widely used in the silver mining industry as a benchmark for performance, but do not have a standardized meaning. These measures are reported on a production basis. See Reconciliations to IFRS on page 21.

(3) Cash costs net of by-product revenue per payable silver oz include mining, processing (including smelting, refining, transportation and selling costs), and direct overhead, net of gold credits. See Reconciliation to IFRS on pages 23 and 24.

(4) Total production costs per oz include mining, processing (including smelting, refining, transportation and selling costs), direct overhead, amortization, depletion and amortization at the operation sites net of by product revenues. See Reconciliation to IFRS on pages 23 and 24.

(5) AISC per oz include mining, processing (including smelting, refining, transportation and selling costs), direct overhead, corporate general and administration expenses, on-site exploration, share-based compensation, reclamation and sustaining capital net of gold credits. See Reconciliation to IFRS on pages 24 to 26.

(6) Direct operating cost per tonne include mining, processing (including smelting, refining, transportation and selling costs) and direct overhead at the operation sites. Direct cost per tonne include all direct operating costs, royalties and special mining duty. See Reconciliation to IFRS on pages 23 and 24.

(7) Silver co-product cash cost and gold co-product cash cost include mining, processing (including smelting, refining, transportation and selling costs), and direct overhead allocated on pro-rated basis of realized metal value. See Reconciliation to IFRS on pages 26 and 27.

|

MANAGEMENT'S DISCUSSION AND ANALYSIS FOR THE YEAR ENDED DECEMBER 31, 2021 |

(1) Silver equivalents are calculated using an 80:1 (Ag/Au) ratio.

Consolidated Production

Three months ended December 31, 2021 (compared to the three months ended December 31, 2020)

Consolidated silver production during Q4, 2021 was 1,443,564 oz, an increase of 29% compared to 1,117,289 oz in Q4, 2020, and gold production was 9,446 oz, a decrease of 25% compared to 12,586 oz in Q4, 2020. Plant throughput was 213,492 tonnes at average grades of 235 grams per tonne (gpt) silver and 1.52 gpt gold, compared to 237,389 tonnes grading 169 gpt silver and 1.9 gpt gold in Q4, 2020. Consolidated silver production increased by 29% compared to Q4, 2020, driven by a 31% increase in silver production at the Guanaceví mine and a 42% increase in silver production at the Bolañitos mine, partially offset by the suspension of the El Compas operations. Consolidated gold production decreased by 25% compared to Q4, 2020, primarily due to the suspension of the El Compas operation and a 19% decrease at the Bolañitos mine, partially offset by a 21% increase in gold production at the Guanaceví mine. The increase in silver and gold production at the Guanaceví mine was driven by a 26% increase in silver grade and a 20% increase in gold grade, with slightly higher recoveries. At the Bolañitos mine the increase in silver production was attributable to a 41% increase in ore grade and slightly higher recoveries and the decrease in gold production was attributable to an 18% decrease in ore grade.

Year ended December 31, 2021 (compared to the year ended December 31, 2020)

Consolidated silver production during 2021 was 4,870,787 oz, an increase of 39% compared to 3,513,767 oz in 2020, and gold production was 42,262 oz, an increase of 14% compared to 37,139 oz in 2020. Plant throughput was 887,424 tonnes at average grades of 195 gpt silver and 1.65 gpt gold, a 17% increase compared to 757,160 tonnes grading 167 gpt silver and 1.78 gpt gold in 2020. Consolidated silver production increased by 39% compared to 2020, primarily driven by a 41% increase in silver production at the Guanaceví mine and a 39% increase in silver production at the Bolañitos mine, offset by a 49% reduction in silver production at the El Compas mine. Consolidated gold production increased by 14% compared to 2020, primarily driven by a 36% increase in gold production at the Guanaceví mine and a 30% increase at the Bolañitos mine, offset by a 49% decrease in gold production at the El Compas mine. The increases at the Guanaceví mine were driven by a 20% increase in throughput, an 18% increase in silver grade and a 14% increase in gold grade. The increases at the Bolañitos mine were driven by a 26% increase in throughput, a 5% increase in silver grade with a 6% increase in silver recovery and similar gold grades with a 3% increase in gold recovery. The comparative information for 2020 is also affected by the temporary suspension of the Guanaceví, Bolañitos and El Compas mines during Q2, 2020 due to the COVID-19 pandemic

The Company's 2021 full year production exceeded both original and revised guidance with annual silver production exceeding the high range of revised guidance by 3%, while gold production was in line with the upper range of revised guidance and silver equivalent production beating the high range of the revised 2021 production guidance.

Actual cost metrics were slightly higher than 2021 cost guidance primarily due to the increased labour, power, consumables, third-party ore, higher royalties and special mining duty offset by the higher ore grades mined at Guanaceví

|

MANAGEMENT'S DISCUSSION AND ANALYSIS FOR THE YEAR ENDED DECEMBER 31, 2021 |

Consolidated Operating Costs

Three months ended December 31, 2021 (compared to the three months ended December 31, 2020)

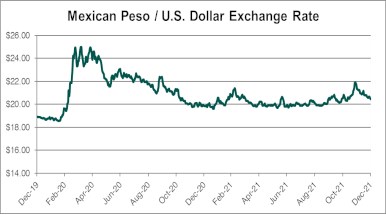

Direct operating costs per tonne in Q4, 2021 increased 7%, to $112.91 compared with Q4, 2020 due to higher operating costs at Guanaceví and Bolañitos. Guanaceví and Bolañitos have seen increased labour, power and consumable costs and at Guanaceví, increased third party ore purchased and operating development have increased compared to the prior year. There has also been a strengthening of the Mexican peso comparative to the U.S. dollar, which increased expenses denominated in that currency. Including royalties and special mining duty, direct costs per tonne increased 5% to $136.62. Royalties were relatively flat compared to Q4, 2020.

Consolidated cash costs per oz, net of by-product credits increased to $8.65 due to higher direct costs per tonne and the lower gold credit driven by lower gold grades and prices. AISC increased by 5% on a per oz basis compared to Q4, 2020 as a result of higher cash costs, increased mine-site exploration and increased capital expenditures at Guanaceví to accelerate mine development within the El Curso ore body, offset by increased production and decreased general and administrative costs. In Q4, 2021 corporate general and administrative expenses included a $0.2 million mark to market expense of cash-settled deferred share units, whereas the mark to market expense was $1.9 million in Q4, 2020, attributed to period end changes in the Company's share price.

On a co-product cash costs basis, silver cost per oz decreased 10% and gold cost per oz decreased 8% compared to the Q4, 2020. The silver co-product cost per oz decreased due to the suspension of operations during Q3, 2021 of the El Compas mine, which contributed higher costs on a per oz basis. Gold co-product cash costs decreased due to the reduced contribution of gold oz from the higher cost El Compas mine, which was partially offset by an increase in gold recovery.

Year ended December 31, 2021 (compared to the year ended December 31, 2020)

Direct operating costs per tonne in 2021 increased 14%, to $115.36 compared with 2020 due to higher operating costs at Guanaceví and Bolañitos. Guanaceví and Bolañitos have seen increased labour, power and consumables costs and at Guanaceví, increased third party ore purchased and operating development have increased compared to the prior year. The appreciation of the Mexican peso to the U.S. dollar increased expenses denominated in Mexican peso compared to the prior period. Including royalties and special mining duty, direct costs per tonne increased 17% to $133.97. Royalties increased 69% to $13.8 million with increased production from the El Curso and El Porvenir concessions at Guanaceví with higher prices. The higher prices and higher grades improved profitability considerably, increasing special mining duty expense 37% to $2.7 million for 2021 from $2.0 million in 2020.

Consolidated cash costs per oz net of by-product credits increased to $9.31 primarily due to the higher direct costs per tonne and lower realized gold prices compared to 2020. AISC increased 16% to $20.34 per oz in 2021 as a result of higher cash costs, increased mine site expensed exploration and increased capital expenditures at Guanaceví to accelerate mine development within the El Curso ore body.

On a co-product cash costs basis silver cost per oz increased 16% and gold cost per oz decreased 3% compared to 2020. The improved silver ore grade was offset by higher operating, royalty and special mining duty costs primarily at the Guanaceví mine. Gold co-product cash costs decreased due to higher gold ore grades and higher gold recoveries offset by the higher operating costs at Bolañitos.

|

MANAGEMENT'S DISCUSSION AND ANALYSIS FOR THE YEAR ENDED DECEMBER 31, 2021 |

GUANACEVÍ OPERATIONS

The Guanaceví operation is currently producing from three underground silver-gold mines along a five kilometre ("km") length of the prolific Santa Cruz vein. Guanaceví provides steady employment to over 500 people and engages over 300 contractors.

In July 2019, the Company acquired a 10 year right to explore and exploit the El Porvenir and El Curso concessions from Ocampo Mining SA de CV ("Ocampo"), a subsidiary of Grupo Frisco. The Company agreed to meet certain minimum production targets from the properties, subject to various terms and conditions and pay Ocampo a $12 fixed per tonne production payment plus a floating net smelter return royalty based on the spot silver price. The Company pays a 4% royalty on sales below $15.00 per silver oz, 9% above $15.00 per silver oz, 13% above $20.00 per silver oz, and a maximum of 16% above $25 per silver oz, based on then current realized prices. On December 12, 2021, the Company executed an amendment to the agreement whereby two additional concessions, adjacent to the existing and historic mine workings, were included in the existing agreement.

The development of two new orebodies, Milache and SCS, and the acquisition of the Ocampo concession rights have provided sufficient ore and flexibility to increase mine output and to reach designed plant capacity.

Production Results for the Three Months and Years Ended December 31, 2021 and 2020

| Three Months Ended December 31 | GUANACEVÍ | Years Ended December 31 | ||||

| 2021 | 2020 | % Change | 2021 | 2020 | % Change | |

| 108,334 | 106,425 | 2% | Ore tonnes processed | 414,355 | 346,679 | 20% |

| 417 | 331 | 26% | Average silver grade (g/t) | 370 | 314 | 18% |

| 89.6 | 87.6 | 2% | Silver recovery (%) | 87.9 | 87.7 | 0% |

| 1,301,941 | 991,697 | 31% | Total silver ounces produced | 4,333,567 | 3,071,075 | 41% |

| 1,298,036 | 988,722 | 31% | Payable silver ounces produced | 4,320,567 | 3,061,982 | 41% |

| 1.21 | 1.01 | 20% | Average gold grade (g/t) | 1.09 | 0.96 | 14% |

| 92.2 | 92.5 | (0%) | Gold recovery (%) | 91.7 | 91.7 | 0% |

| 3,885 | 3,198 | 21% | Total gold ounces produced | 13,317 | 9,814 | 36% |

| 3,873 | 3,188 | 21% | Payable gold ounces produced | 13,277 | 9,786 | 36% |

| 1,612,741 | 1,247,537 | 29% | Silver equivalent ounces produced(1) | 5,398,927 | 3,856,195 | 40% |

| 10.74 | 13.21 | (19%) | Cash costs per silver ounce(2)(3) | 12.12 | 10.44 | 16% |

| 12.49 | 15.52 | (20%) | Total production costs per ounce(2)(4) | 14.40 | 13.36 | 8% |

| 18.74 | 19.67 | (5%) | All in sustaining cost per ounce (2)(5) | 19.46 | 17.14 | 14% |

| 146.51 | 129.91 | 13% | Direct operating costs per tonne(2)(6) | 145.64 | 117.38 | 24% |

| 193.87 | 179.34 | 8% | Direct costs per tonne(2)(6) | 183.86 | 143.46 | 28% |

| 13.11 | 15.45 | (15%) | Silver co-product cash costs(7) | 14.43 | 12.72 | 13% |

| 1,014 | 1,176 | (14%) | Gold co-product cash costs(7) | 1,024 | 1,087 | (6%) |

(1) Silver equivalents are calculated using an 80:1 (silver/gold) ratio.

(2) The Company reports non-IFRS measures which include cash costs net of by-product revenue on a payable silver basis, total production costs per oz, AISC per oz, direct operating cost per tonne, direct cost per tonne, silver co-product cash costs and gold co-product cash costs in order to manage and evaluate operating performance at each of the Company's mines. These measures, some established by the Silver Institute (Production Cost Standards, June 2011), are widely used in the silver mining industry as a benchmark for performance, but do not have a standardized meaning. These measures are reported on a production basis. See Reconciliations to IFRS on page 21.

(3) Cash costs net of by-product revenue per payable silver oz include mining, processing (including smelting, refining, transportation and selling costs), and direct overhead, net of gold credits. See Reconciliation to IFRS on pages 23 and 24.

(4) Total production costs per oz include mining, processing (including smelting, refining, transportation and selling costs), direct overhead, amortization, depletion and amortization at the operation sites net of by product revenues. See Reconciliation to IFRS on pages 23 and 24.

(5) AISC per oz include mining, processing (including smelting, refining, transportation and selling costs), direct overhead, corporate general and administration expenses, on-site exploration, share-based compensation, reclamation and sustaining capital net of gold credits. See Reconciliation to IFRS on pages 24 to 26.

(6) Direct operating costs per tonne include mining, processing (including smelting, refining, transportation and selling costs) and direct overhead at the operation sites. Direct cost per tonne include all direct operating costs, royalties and special mining duty. See Reconciliation to IFRS on pages 23 and 24.

(7) Silver co-product cash cost and gold co-product cash cost include mining, processing (including smelting, refining, transportation and selling costs), and direct overhead allocated on pro-rated basis of realized metal value. See Reconciliation to IFRS on pages 26 and 27.

|

MANAGEMENT'S DISCUSSION AND ANALYSIS FOR THE YEAR ENDED DECEMBER 31, 2021 |

Guanaceví Production Results

Three months ended December 31, 2021 (compared to the three months ended December 31, 2020)

Silver production at the Guanaceví mine during Q4, 2021 was 1,301,941 oz, an increase of 31% compared to 991,697 oz in Q4, 2020, and gold production was 3,885 oz, an increase of 21% compared to 3,198 oz in Q4, 2020. Plant throughput was consistent with Q4, 2020 with 108,334 tonnes at average grades of 417 gpt silver and 1.21 gpt gold, compared to 106,425 tonnes grading 331 gpt silver and 1.01 gpt gold in Q4, 2020. The 31% increase in silver production is due to a 26% increase in silver grades with slightly higher throughput and slightly increased recoveries and the 21% increase in gold production is due to a 20% increase in gold grade. The purchase of third-party ores continued to supplement mine production, amounting to 14% of quarterly throughput, and contributed to the higher ore grades.

Year ended December 31, 2021 (compared to the year ended December 31, 2020)

Silver production at the Guanaceví mine for year ended December 31, 2021 was 4,333,567 oz, an increase of 41% compared to 3,071,075 oz in 2020, and gold production was 13,317 oz, an increase of 36% compared to 9,814 oz in 2020. Plant throughput was 414,355 tonnes at average grades of 370 gpt silver and 1.09 gpt gold, compared to 346,679 tonnes at average grades of 314 gpt silver and 0.96 gpt gold in 2020. The 41% increase in silver production and 36% increase in gold production compared to 2020 are due to the 20% increase in throughput, as the plant reached its 1,200 tonnes per day ("tpd") capacity in Q2, 2021 and maintained it for the remainder of 2021, and increased grades with similar recoveries. Silver and gold grades increased by 18% and 14% respectively. The comparative information for 2020 is also affected by the impact on throughput due to the temporary suspension of the Guanaceví mine during Q2, 2020 due to the COVID-19 pandemic. The purchase of local third-party ores continued to supplement mine production, amounting to 11% of year-to-date throughput, and contributed to the higher ore grades.

Guanaceví Operating Costs

Three months ended December 31, 2021 (compared to the three months ended December 31, 2020)

Direct operating costs per tonne for the three months ended December 31, 2021 increased 13% to $146.51 compared with the same period in 2020, resulting from increased purchase of local third-party ores, increased labour, power and consumables costs, and an increase in operating development. The Company increased in the purchase of local third-party ore contributed $29.04 per tonne during Q4, 2021 $18.58 per tonne in Q4 2020. Including royalty and special mining duty costs, direct cost per tonne increased 8% to $193.87 compared with the same period in 2020. There was a slight reduction in royalty and special mining duty costs during the three months ended December 31, 2021 compared to the prior period primarily due to the timing of sales. In Q4 2020 the Company sold the majority of Q4, 2020 production as well as finished goods inventory that was held as of September 30, 2020.

Cash costs per oz, net of by-product credits, was $10.74 compared to $13.21 for the same period in 2020, with the reduction due to the increased ore grades offset by higher direct costs. AISC per oz decreased 5% to $18.74 per oz for the three months ended December 31, 2021, as a result of the increased silver production offset by increased sustaining capital expenditures.

Year ended December 31, 2021 (compared to the year ended December 31, 2020)

Direct operating costs per tonne for the year ended December 31, 2021 increased 24% to $145.64 compared with 2020, as a result of increased purchase of local third-party ores, increased labour, power and consumables costs, the expensing of development costs at El Porvenir, as there were no reserves to allow for deferral of development costs, and in increase in operating development. Including royalty and special mining duty costs, direct cost per tonne increased 28% to $183.86 compared with 2020. Increased production from the El Curso and El Porvenir concession and higher prices significantly increased the royalties paid during the year. The increased metal prices and higher ore grades resulted in improved profitability and higher special mining duty payable to the Mexican government. The improved profitability of the operations resulted in $2.7 million Mexico special mining duty during 2021 compared to $1.6 million in 2020, and royalties increasing from $7.4 million to $13.2 million, which are included in cost per tonne and oz metrics.

Cash costs per oz, net of by-product credits was $12.12, 16% higher than 2020 due to the higher direct cost per tonne, offset by the higher ore grades and higher gold credit. Similarly, AISC per oz increased 14% to $19.46 per oz for 2021. The increase in cash costs per oz was the primary driver of the higher AISC, while higher capital and exploration expenditures partially offset by lower general and administration expenses contributed to the higher costs compared to 2020. In Q2, 2020 there was a sharp reduction in capital and exploration expenditures due to the suspension of activities due to COVID-19.

|

MANAGEMENT'S DISCUSSION AND ANALYSIS FOR THE YEAR ENDED DECEMBER 31, 2021 |

BOLAÑITOS OPERATIONS

The Bolañitos operation encompasses three underground silver-gold mines and a flotation plant. Bolañitos provides steady employment for over 475 people and engages over 150 contractors.

Production Results for the Three Months and Years Ended December 31, 2021 and 2020

|

Three Months Ended December 31 |

BOLAÑITOS |

Years Ended December 31 |

||||

|

2021 |

2020 |

% Change |

|

2021 |

2020 |

% Change |

|

105,158 |

107,332 |

(2%) |

Ore tonnes processed |

418,514 |

331,174 |

26% |

|

48 |

34 |

41% |

Average silver grade (g/t) |

42 |

40 |

5% |

|

87.0 |

84.7 |

3% |

Silver recovery (%) |

87.0 |

83.0 |

5% |

|

141,258 |

99,417 |

42% |

Total silver ounces produced |

491,412 |

353,318 |

39% |

|

134,178 |

94,526 |

42% |

Payable silver ounces produced |

462,700 |

333,293 |

39% |

|

1.83 |

2.22 |

(18%) |

Average gold grade (g/t) |

2.02 |

2.02 |

0% |

|

88.9 |

88.2 |

1% |

Gold recovery (%) |

90.7 |

88.2 |

3% |

|

5,502 |

6,754 |

(19%) |

Total gold ounces produced |

24,652 |

18,963 |

30% |

|

5,330 |

6,551 |

(19%) |

Payable gold ounces produced |

23,971 |

18,429 |

30% |

|

581,418 |

639,737 |

(9%) |

Silver equivalent ounces produced(1) |

2,463,572 |

1,870,358 |

32% |

|

(10.69) |

(44.56) |

76% |

Cash costs per silver ounce(2)(3) |

(19.77) |

(32.11) |

38% |

|

6.71 |

(15.50) |

143% |

Total production costs per ounce(2)(4) |

10.93 |

(4.76) |

330% |

|

27.46 |

16.98 |

62% |

All in sustaining cost per ounce (2)(5) |

25.14 |

23.53 |

7% |

|

78.38 |

71.88 |

9% |

Direct operating costs per tonne(2)(6) |

79.37 |

70.11 |

13% |

|

77.68 |

75.82 |

2% |

Direct costs per tonne(2)(6) |

80.13 |

71.78 |

12% |

|

14.41 |

13.26 |

9% |

Silver co-product cash costs(7) |

14.96 |

12.04 |

24% |

|

1,115 |

1,010 |

10% |

Gold co-product cash costs(7) |

1,062 |

1,029 |

3% |

(1) Silver equivalents are calculated using an 80:1 (silver/gold) ratio.

(2) The Company reports non-IFRS measures which include cash costs net of by-product revenue on a payable silver basis, total production costs per oz, AISC per oz, direct operating cost per tonne, direct cost per tonne, silver co-product cash costs and gold co-product cash costs in order to manage and evaluate operating performance at each of the Company's mines. These measures, some established by the Silver Institute (Production Cost Standards, June 2011), are widely used in the silver mining industry as a benchmark for performance, but do not have a standardized meaning. These measures are reported on a production basis. See Reconciliations to IFRS on page 21.

(3) Cash costs net of by-product revenue per payable silver oz include mining, processing (including smelting, refining, transportation and selling costs), and direct overhead, net of gold credits. See Reconciliation to IFRS on pages 23 and 24.

(4) Total production costs per oz include mining, processing (including smelting, refining, transportation and selling costs), direct overhead, amortization, depletion and amortization at the operation sites net of by product revenues. See Reconciliation to IFRS on pages 23 and 24.

(5) AISC per oz include mining, processing (including smelting, refining, transportation and selling costs), direct overhead, corporate general and administration expenses, on-site exploration, share-based compensation, reclamation and sustaining capital net of gold credits. See Reconciliation to IFRS on pages 24 to 26.

(6) Direct operating costs per tonne include mining, processing (including smelting, refining, transportation and selling costs) and direct overhead at the operation sites. Direct cost per tonne include all direct operating costs, royalties and special mining duty. See Reconciliation to IFRS on pages 23 and 24.

(7) Silver co-product cash cost and gold co-product cash cost include mining, processing (including smelting, refining, transportation and selling costs), and direct overhead allocated on pro-rated basis of realized metal value. See Reconciliation to IFRS on pages 26 and 27.

Bolañitos Production Results

Three months ended December 31, 2021 (compared to the three months ended December 31, 2020)

Silver production at the Bolañitos mine was 141,258 oz in Q4, 2021, an increase of 42% compared to 99,417 oz in Q4, 2020, and gold production was 5,502 oz in Q4, 2021, a decrease of 19% compared to 6,754 oz in Q4, 2020. Plant throughput in Q4, 2021 was 105,158 tonnes at average grades of 48 gpt silver and 1.83 gpt gold, compared to 107,332 tonnes at average grades of 34 gpt silver and 2.22 gpt gold in Q4, 2020. The 42% increase in silver production and 19% decrease in gold production compared to Q4, 2020 is primarily due to the fluctuations of ore grades from accessing different areas of the mine. Recoveries improved slightly as the operations improved ore blending to maximize recoveries compared to the prior period.

|

MANAGEMENT'S DISCUSSION AND ANALYSIS FOR THE YEAR ENDED DECEMBER 31, 2021 |

Year ended December 31, 2021 (compared to the year ended December 31, 2020)

Silver production at the Bolañitos mine was 491,412 oz for 2021, an increase of 39% compared to 353,318 oz in 2020, and gold production was 24,652 oz for 2021, an increase of 30% compared to 18,963 oz in 2020. Plant throughput in 2021 was 418,514 tonnes at average grades of 42 gpt silver and 2.02 gpt gold, compared to 331,174 tonnes at average grades of 40 gpt silver and 2.02 gpt gold in 2020. The 39% increase in silver production and 30% increase in gold production compared to 2020 are primarily due to the 26% increase in plant throughput, a 5% increase in silver grades and increased silver and gold recoveries of 5% and 3%, respectively. The comparative information for 2020 was also affected by the impact on throughput due to the temporary suspension of the Bolañitos mine during Q2, 2020 due to the COVID-19 pandemic. Recoveries improved as the operations improved ore blending to maximize recoveries compared to the prior period.

Bolañitos Operating Costs

Three months ended December 31, 2021 (compared to the three months ended December 31, 2020)

Direct costs per tonne in Q4, 2021 increased 2% to $77.68 per tonne primarily due to a slight increase in costs and decrease in throughput tonnes compared to the same period in 2020. Cash costs net of by-product credits, were negative $10.69 per oz of payable silver in Q4, 2021 compared to negative $44.56 per oz in Q4, 2020 due in large part to an 18% reduction in the gold grade and a reduction in realized gold price compared to the same period in the prior year. AISC increased in Q4, 2021 to $27.46 per oz as they were similarly affected by the reduction in by-product gold sales.

On a co-product cash costs basis, silver cost per oz increased compared to Q4, 2020. Silver co-product cash costs increased 9% and gold co-product costs increased 10% to $14.41 per silver oz and $1,115 per gold oz, respectively. The increase in the silver cost on a co-product basis was primarily driven by the higher direct costs per tonne and the variation in ore grades, while the higher gold costs on a co-product basis was driven by the lower ore gold grades and the higher direct costs per tonne.

Year ended December 31, 2021 (compared to the year ended December 31, 2020)

Direct costs per tonne in 2021 increased 12%, to $80.13 per tonne due to higher labour, power and consumables costs as well as higher waste tonnes handled during the year. Cash costs net of by-product credits were negative $19.77 per oz of payable silver in 2021 compared to negative $32.11 per oz in the comparative period of 2020 due to the higher direct costs and a 4% decrease in the realized gold price offset by a higher proportion of gold production. AISC increased by 7% in 2021, compared to 2020, to $25.14 per oz due to higher operating cost per oz and increased sustaining capital expenditures offset by lower corporate general and administrative charges. Compared to 2020, there was an increase in mine development of $3.1 million which will extend the mine life.

On a co-product cash costs basis, silver cost per oz increased compared to 2020. Silver co-product cash costs increased 24%, while gold co-product costs increased by 3% to $14.96 per silver oz and $1,062 per gold oz respectively. The increase in the silver cost on a co-product basis was primarily driven by the higher direct costs per tonne and the variation in ore, while the higher gold costs on a co-product basis was driven by the decreased proportional gold production.

EL COMPAS OPERATIONS

The El Compas operation is a small but high grade, permitted gold-silver mine with a small leased flotation plant in the historic silver mining district of Zacatecas, with exploration potential to expand resources. The leased floatation plant has a nominal plant capacity of 250 tpd.

El Compas employed close to 200 people and engaged over 55 contractors until the suspension of operations in mid-August 2021 as the mineral reserves were exhausted. The mine, plant and tailings facilities are on short term care and maintenance, while management conducts an evaluation of the alternatives including final closure.

|

MANAGEMENT'S DISCUSSION AND ANALYSIS FOR THE YEAR ENDED DECEMBER 31, 2021 |

There remain several brownfield exploration opportunities on concessions owned by the Company, however further resource definition and evaluation is required to recommence production. Temporary closure costs were $1.4 million for 2021, inclusive of $0.8 million in severance costs. Company management and contract personnel continue to maintain the security of the mine, plant, and tailings facilities. The mining equipment and selected other assets have been relocated to Endeavour's other operating mines, particularly to Bolañitos and Terronera, to reduce their future capital costs.

Production Results for the Three Months and Years Ended December 31, 2021 and 2020

|

Three Months Ended December 31 |

El Compas |

Years Ended December 31 |

||||

|

2021 |

2020 |

% Change |

|

2021 |

2020 |

% Change |

|

N/A |

23,632 |

N/A |

Ore tonnes processed |

54,555 |

79,307 |

(31%) |

|

N/A |

50 |

N/A |

Average silver grade (g/t) |

36 |

53 |

(32%) |

|

N/A |

68.9 |

N/A |

Silver recovery (%) |

72.5 |

66.1 |

10% |

|

365 |

26,175 |

(99%) |

Total silver ounces produced |

45,808 |

89,374 |

(49%) |

|

364 |

25,600 |

(99%) |

Payable silver ounces produced |

43,414 |

86,819 |

(50%) |

|

N/A |

4.41 |

N/A |

Average gold grade (g/t) |

3.05 |

4.32 |

(29%) |

|

N/A |

78.6 |

N/A |

Gold recovery (%) |

80.2 |

75.9 |

6% |

|

59 |

2,634 |

(98%) |

Total gold ounces produced |

4,293 |

8,362 |

(49%) |

|

58 |

2,575 |

(98%) |

Payable gold ounces produced |

4,190 |

8,177 |

(49%) |

|

5,085 |

236,895 |

(98%) |

Silver equivalent ounces produced(1) |

389,248 |

758,334 |

(49%) |

|

N/A |

(50.04) |

N/A |

Cash costs per silver ounce(2)(3) |

39.37 |

(22.51) |

275% |

|

N/A |

89.45 |

N/A |

Total production costs per ounce(2)(4) |

84.88 |

109.10 |

(22%) |

|

N/A |

(20.19) |

N/A |

All in sustaining cost per ounce (2)(5) |

56.71 |

10.98 |

417% |

|

N/A |

143.96 |

N/A |

Direct operating costs per tonne(2)(6) |

161.56 |

160.04 |

1% |

|

N/A |

150.52 |

N/A |

Direct costs per tonne(2)(6) |

167.98 |

166.97 |

1% |

|

N/A |

15.69 |

N/A |

Silver co-product cash costs(7) |

26.15 |

16.47 |

59% |

|

N/A |

1,194 |

N/A |

Gold co-product cash costs(7) |

1,856 |

1,408 |

32% |

(1) Silver equivalents are calculated using an 80:1 (silver/gold) ratio.

(2) The Company reports non-IFRS measures which include cash costs net of by-products on a payable silver basis, total production costs per oz, AISC per oz and direct production costs per tonne, in order to manage and evaluate operating performance at each of the Company's mines. These measures, some established by the Silver Institute (Production Cost Standards, June 2011), are widely used in the silver mining industry as a benchmark for performance, but do not have a standardized meaning. These measures are reported on a production basis. See Reconciliation to IFRS on page 21.

(3) Cash costs net of by-product revenue per payable silver oz include mining, processing (including smelting, refining, transportation and selling costs), and direct overhead, net of gold credits. See Reconciliation to IFRS on pages 23 and 24.

(4) Total production costs per oz include mining, processing (including smelting, refining, transportation and selling costs), direct overhead, amortization, depletion and amortization at the operation sites net of by product revenues. See Reconciliation to IFRS on pages 23 and 24.

(5) AISC per oz include mining, processing (including smelting, refining, transportation and selling costs), direct overhead, corporate general and administration expenses, on-site exploration, share-based compensation, reclamation and sustaining capital net of gold credits. See Reconciliation to IFRS on pages 24 to 26.

(6) Direct operating costs per tonne include mining, processing (including smelting, refining, transportation and selling costs) and direct overhead at the operation sites. Direct cost per tonne include all direct operating costs, royalties and special mining duty. See Reconciliation to IFRS on pages 23 and 24.

(7) Silver co-product cash cost and gold co-product cash cost include mining, processing (including smelting, refining, transportation and selling costs), and direct overhead allocated on pro-rated basis of realized metal value. See Reconciliation to IFRS on pages 26 and 27.

El Compas Production Results

Three months ended December 31, 2021 (compared to the three months ended December 31, 2020)

As mining and milling operations were suspended in August, 2021, there was no silver production, other than final settlements in Q4, 2021 of concentrates shipped prior to the suspension resulting in the recognition of 365 silver oz and 59 gold oz in the quarter. During Q4, 2020, silver production at the El Compas mine was 26,175 oz and gold production was 2,634 oz with plant throughput of 23,632 tonnes at average grades of 50 gpt silver and 4.41 gpt gold.

|

MANAGEMENT'S DISCUSSION AND ANALYSIS FOR THE YEAR ENDED DECEMBER 31, 2021 |

Year ended December 31, 2021 (compared to the year ended December 31, 2020)

Silver production at the El Compas mine was 45,808 oz and gold production was 4,293 oz for January to mid-August 2021 compared to 89,374 silver oz and 8,362 gold oz in 2020. Plant throughput was 54,555 tonnes at average grades of 36 gpt silver and 3.05 gpt gold compared to 79,307 tonnes at average grades of 53 gpt silver and 4.32 gpt gold in 2020. Although throughput remained steady from January to August 2021, both silver and gold grades decreased significantly resulting in lower proportional production. The comparative information for 2020 was also affected by the impact on throughput due to the temporary suspension of the El Compas mine during Q2, 2020 due to the COVID-19 pandemic.

El Compas Operating Costs

Three months ended December 31, 2021 (compared to the three months ended December 31, 2020)

As mining and milling operations were suspended in August, 2021, there is no comparative cost information for Q4, 2021.

Year ended December 31, 2021 (compared to the year ended December 31, 2020)

Direct costs were $167.98 per tonne for 2021, a 1% increase from 2020. Silver cash costs net of by-product credits were $39.37 per oz of payable silver compared to negative $22.51 per oz in 2020. The significantly lower gold grade was the primary driver in the increase in cash costs compared to the comparative period in 2020. The decrease in costs per tonne was a result of normal variations in costs incurred.

On a co-product cash costs basis, both silver co-product cost per ounce and gold co-product costs per ounce increased to $26.15 per ounce and $1,856 per ounce, respectively, compared to 2020. Both co-product cash cost metrics increased due to the lower ore grades and the slightly higher operating costs on a per tonne basis.

AISC increased to $56.71 per oz compared to $10.98 per oz in the same period ended in 2020. The higher AISC are a function of the lower silver and gold grades.

EL CUBO OPERATIONS

The El Cubo operation included two previously operating underground silver-gold mines and a flotation plant, which employed over 350 people and engaged over 200 contractors until the suspension of operations at the end of November 2019 as the mineral reserves had been exhausted. The mine, plant and tailings facilities were on care and maintenance until the sale of the El Cubo mine and related assets in April 2021.

Company management and contract personnel maintained the security of the mine, plant and tailings facilities until the sale. The Company incurred $0.6 million in legal, administrative and care and maintenance expenses in 2021. In 2020, $0.3 million severance costs and $1.5 million in legal, administrative and care and maintenance expenses were incurred and $0.2 million in building and office depreciation.

On March 17, 2021, the Company signed a definitive agreement to sell the El Cubo mine and related assets to GSilver for $15.0 million in cash and share payments plus additional contingency payments. On April 9, 2021, GSilver purchased the El Cubo assets for the following gross consideration:

GSilver is required to pay the Company up to an additional $3.0 million in contingent payments based on the following events:

|

MANAGEMENT'S DISCUSSION AND ANALYSIS FOR THE YEAR ENDED DECEMBER 31, 2021 |

On November 16, 2021, the Company arranged for early payment of the $2.5 million promissory note. In consideration for the early repayment, the Company agreed to reduce the principal amount of the note by $25,000 and settle the Mexican value added tax payable on the promissory note for 901,224 common shares of GSilver.

DEVELOPMENT ACTIVITIES

Terronera Project

The Terronera project, located 40 km northeast of Puerto Vallarta in the state of Jalisco, Mexico, features a high-grade silver-gold mineral resource in the Terronera vein, which is now over 1,400 metres long, 400 metres deep, 3 to 16 metres thick, and remains open along strike to the southeast and down dip.

In 2020, the Company engaged an external consultant to update a previous Preliminary Feasibility Study based on updated information gathered in 2019 and 2020. In Q3, 2020 the Company completed an updated summary of the project's economics and published the NI 43-101 Technical Report ("2020 PFS"). The 2020 PFS included significant changes to the operations plan, capital and operating costs assumed compared to the previous study and, as a result, project economics improved. The external consultant reviewed all aspects of the previous studies, while further cost-benefit initiatives have been evaluated.

In September 2020, the Company engaged Wood PLC to complete a Feasibility Study ("FS") at an estimated cost of $2.1 million, with the economic information released in a press release dated September 9, 2021 and the full report filed on SEDAR and EDGAR and posted to the Company's website on October 25, 2021.

The FS base case assumed a silver price of $20 per oz and a gold price of $1,575 per oz with an implied 79:1 silver to gold ratio, and a Mexico peso to U.S. dollar exchange rate of 20:1. At base case prices, the improved economics estimated an after-tax net present value of $174.1 million at a 5% discount rate, internal rate of return of 21.3%, and payback period of 3.6 years. Initial capital expenditures were estimated to be $175 million with capital expenditures during production estimated to be $108.5 million. The 12-year life of mine was estimated to produce an average of 3.3 million silver oz and 32,874 gold oz per year generating $476 million pre-tax, $311 million after-tax, free cash flow over the life of the project.

The Company is preparing to commence initial earthworks and intends to make a formal construction decision, subject to completion of a financing package and receipt of additional amended permits, in the coming months. A budget of $9.5 million has been approved for Q1, 2022 to continue to advance the site clearing, preparations for initial earthworks, temporary camp and procuring of long lead items.

The Company re-classified the Terronera Project from an exploration and evaluation project to a development project in September, 2021 and during the year invested $11.8 million on land acquisition, initial development and capital assets to advance development and $8.0 million on exploration and evaluation activities including the completion of the FS.

|

MANAGEMENT'S DISCUSSION AND ANALYSIS FOR THE YEAR ENDED DECEMBER 31, 2021 |

EXPLORATION RESULTS

In 2021, the Company planned to spend $10.2 million drilling 50,000 metres of core on brownfields projects, greenfields exploration and development engineering across its portfolio of mines and properties. At the Guanaceví and Bolañitos operating mines, 11,500 metres of core drilling were planned at a cost of $2.0 million and $1.9 million, respectively to replace reserves and expand resources.

On the exploration and development projects, expenditures of $6.3 million were planned to fund 27,000 metres of core drilling at the Terronera project to test multiple regional targets, the Parral project to continue drilling the San Patricio and Veta Colorada vein systems and the Paloma project in Chile. The Company is currently permitting the Aida project and will continue to map and sample to prioritize targets for drilling.

At Guanaceví, in 2021 the Company drilled 15,360 metres in 60 holes at a total expense of $1.6 million to delineate the extension of the Porvenir Cuatro, El Curso, and SCS ore bodies. Drilling confirmed expectations and intersected significant mineralization with similar ore grades and vein widths to historical results.

At Bolañitos, in 2021 the Company drilled 15,227 metres in 72 holes at total expense of $1.2 million to target the Melladito, Plateros and Belén veins. The Company intersected significant mineralization with ore grades over mineable widths.

At Terronera, the 2021 drill program targeted the southeast area near the Terronera vein and regional area acquired in 2020. A total of 15,448 metres were drilled in 54 holes at a total expense of $2.2 million intersecting high-grade silver-gold mineralization in a number of structures near the Terronera vein, highlighting the potential surrounding the current resource estimate. Four intercepted structures, the San Simon, Fresno, Pendencia and Lindero veins, are located immediately to the southeast of the Terronera vein, and the Los Cuates vein is located approximately 10 km to the northwest of the Terronera Project. The drill results confirm management's projection to grow resources in the district. As the FS is complete, all 2021 drill results are not included as part of FS or initial development plan.

At Parral, the Company commenced the 2021 drill program in March, drilling 80 holes totalling 18,245 metres, with a total cost of $2.6 million targeting various areas of the Colorada vein. Drilling confirmed expectations in a number of areas, intersecting significant mineralization with meaningful vein widths. Management will continue the exploration program in 2022 with the intention to expand the resource estimate published in December 2019 and initiate an economic study in 2022.

In Chile, the Company completed initial drilling on the Paloma properties targeting a bulk tonnage, high-sulfidation epithermal deposit related to intrusive domes or the tops of porphyry systems located in the Chilean Miocene deposit belt, 180 km southeast of the city of Calama, 5,000 metres above sea level. The Company has an option to acquire up to 70% ownership of 5,100 hectares from Compañía Minera del Pacifico. Drilling confirmed widespread alteration and low-grade gold mineralization, however it is interpreted that the drilling did not reach the core of the system. The exploration team has analyzed drill results and commenced a second drill program to test targets for higher-grade mineralization.

RESERVES AND RESOURCES

Proven and probable silver and gold mineral reserves increased year on year by 28% and 29% respectively. Mineral reserves are estimated to be 62.0 million oz silver and 608,000 oz gold. On a silver equivalent basis, mineral reserves total 110.6 million oz using a silver to gold ratio of 80:1. A significant portion of the mineral reserve increase is due to the updated estimate for the Terronera FS, resulting in a 10.7 million increase is silver ounce reserves and 124,000 increase gold ounce reserves. Additionally, the positive delineation drill results and the conversion of mineral resources at Guanacevi and Bolañitos through continued mine development more than offset 2021 production

Measured and indicated mineral resources for silver increased by 1% to 26.1 million oz and measured and indicated mineral resources for gold increased by 8% to 237,700 oz gold. Silver equivalent measured and indicated mineral resources increased 4% to 45.1 million oz due mainly to resource growth at Guanacevi and Bolañitos offset by conversion of resources to reserves through mine development.

|

MANAGEMENT'S DISCUSSION AND ANALYSIS FOR THE YEAR ENDED DECEMBER 31, 2021 |

2021 Mineral Reserve and Resource Estimate Highlights (Compared to December 31, 2020):

Mineral reserve and resource estimates are based on pricing assumptions of $23.00 per oz of silver and $1,725 per oz of gold at Guanaceví and Bolañitos, $20.00 per oz of silver and $1,575 per oz of gold at Terronera and $15.00 per oz of silver and $1,275 per oz of gold at Parral.

Note to U.S Investors: Mineral reserve and resources are as defined by Canadian securities laws. See "Cautionary Note to U.S. Investors Regarding Mineral Reserves and Resources".

CONSOLIDATED FINANCIAL RESULTS

Three months ended December 31, 2021 (compared to the three months ended December 31, 2020)

In Q4, 2021, the Company's mine operating earnings were $12.2 million (Q4, 2020: $20.8 million) on net revenue of $48.5 million (Q4, 2020: $60.7 million) with cost of sales of $36.2 million (Q4, 2020: $39.9 million).

In Q4, 2021, the Company had operating earnings of $4.1 million (Q4, 2020: $12.0 million) after exploration and evaluations costs of $4.1 million (Q4, 2020: $4.1million), general and administrative expense of $2.8 million (Q4, 2020: expense of $3.9 million), care and maintenance expense of $0.4 million (Q4, 2020: $0.4 million), severance costs of $0.2 million (Q4, 2020: $Nil) and a write-off of exploration properties of $0.7 million. In Q4, 2020, the operating earnings included impairments and impairments reversals of non-current assets of $0.4 million related to value in use estimates of the Guanaceví and El Compas operation.

The income before taxes for Q4, 2021 was $5.5 million (Q4, 2020: $14.8 million) after finance costs of $0.3 million (Q4, 2020: $0.3 million), a foreign exchange gain of $0.1 million (Q4, 2020: $1.8 million) and investment and other income of $1.6 million (Q4, 2020: $1.3 million). The Company realized a net loss for the period of $0.5 million (Q4, 2020: net earnings of $20.0 million) after an income tax expense of $6.0 million (Q4, 2020: income tax recovery of $5.2 million).

Net revenue of $48.5 million in Q4, 2021, net of $0.4 million of smelting and refining costs, decreased by 20% compared to $60.7 million, net of $0.5 million of smelting and refining costs, in Q4, 2020. Gross sales of $48.9 million in Q4, 2021 represented a 20% decrease over the $61.2 million for the same period in 2020. Silver oz sold were similar with a 5% decrease in the realized silver price, resulting in a 6% decrease to silver sales. Gold oz sold decreased by 37% with a 4% decrease in realized gold prices resulting in a 40% decrease in gold sales. The significant decrease in gold sales is primarily driven by the decreased gold grades at the Bolañitos mine and the suspension of production from the El Compas mine. During the period, the Company sold 1,413,699 oz silver and 8,715 oz gold, for realized prices of $23.41 and $1,811 per oz, respectively, compared to sales of 1,419,037 oz silver and 13,850 oz gold, for realized prices of $24.76 and $1,885 per oz, respectively, in the same period of 2020. For the three months ended December 31, 2021, the realized prices of silver and gold were within approximately 2% of the London spot prices. Silver and gold London spot prices averaged $23.76 and $1,795, respectively, during the three months ended December 31, 2021.

|

MANAGEMENT'S DISCUSSION AND ANALYSIS FOR THE YEAR ENDED DECEMBER 31, 2021 |

The Company slightly increased its finished goods silver and gold inventory to 1,082,610 oz and 3,674 oz, respectively, at December 31, 2021 compared to 1,067,404 oz silver and 3,239 oz gold at September 30, 2021. The Company significantly increased its finished goods silver and gold inventory compared to 116,484 oz silver and 1,459 oz gold at December 31, 2020. The cost allocated to these finished goods was $15.6 million at December 31, 2021, compared to $18.3 million at September 30, 2021 and $3.6 million at December 31, 2020. At December 31, 2021, the finished goods inventory fair market value was $31.7 million, compared to $28.2 million at September 30, 2021 and $5.8 million at December 31, 2020.

Cost of sales for Q4, 2021 was $36.2 million, a decrease of 9% over the cost of sales of $39.9 million for Q4, 2020. The decrease in cost of sales was primarily impacted by no production in Q4, 2021 from El Compas offset by higher costs at Guanaceví and Bolañitos. Overall costs for Q4, 2021 were impacted by higher labour, power and consumables costs, a strengthening of the Mexican peso partially offset by improved productivity at the Guanaceví and Bolañitos operations, compared to Q4, 2020. The current year cost of sales also includes write down of warehouse inventory of $0.9 million. During Q4, 2021 the Company's operations experienced higher costs than budgeted due to global supply constraints creating inflationary pressure, labour costs tracking higher than planned and increased purchased third-party ore at the Guanaceví operation.

Exploration and evaluation expenses were flat at $4.1 million compared to the same period of 2020. General and administrative expenses decreased to $2.8 million in Q4, 2021 compared to $3.9 million for the same period of 2020 primarily due to the mark-to-market impact of cash-settled director's deferred share units, which comparatively decreased costs by $1.8 million. This was offset by increased labour, legal and investor relations costs.

The Company incurred a foreign exchange gain of $0.1 million in Q4, 2021 compared to $1.8 million in Q4, 2020 due to a strengthening of the Mexican peso at the end of Q4, 2020 compared to Q3, 2020 which resulted in higher valuations of peso denominated tax receivables and cash balances. The Company incurred $0.3 million in finance charges primarily related to mobile equipment purchased compared to $0.3 million in the same period in 2020. The Company recognized $1.6 million in investment and other income compared to $1.3 million in Q4, 2020 with the gain during the quarter primarily resulting from an unrealized gain on marketable securities of $1.1 million, $0.2 million in interest income and $0.2 million in royalty income. In 2020, the majority of the other income derived from interest received on IVA collections.

Income tax expense was $6.0 million in Q4, 2021 compared to income tax recovery of $5.2 million in Q4, 2020. The $6.0 million tax expense is comprised of $1.0 million in current income tax expense (Q4, 2020: $1.9 million) and $5.0 million in deferred income tax expense (Q4, 2020: deferred income tax recovery of $7.1 million). The current income tax expense consists of $0.8 million of special mining duty taxes and $0.2 million of income taxes. The deferred income tax expense of $5.0 million is primarily due to the use of loss carry forwards to offset taxable income generated at the Guanaceví operations and a change in the estimated deferred income tax assets for the Bolañitos operation.

Year ended December 31, 2021 (compared to the year ended December 31, 2020)

For the year ended December 31, 2021, the Company's mine operating earnings were $36.4 million (2020: $27.3 million) on net revenue of $165.3 million (2020: $138.4 million) with cost of sales of $128.9 million (2020: $111.1 million).

The Company had operating earnings of $22.3 million (2020: operating loss $0.8 million) after exploration and evaluation costs of $17.9 million (2020: $9.8 million), general and administrative costs of $10.1 million (2020: $12.7 million), an impairment reversal of $16.8 million (2020: $0.4 million impairment expense), care and maintenance cost of $1.3 million (2020: $5.2 million), severance cost of $0.7 million in severance (2020: $Nil) and a write-off of exploration properties of $0.7 million (2020: $Nil). The impairment reversal of $16.8 million resulted from the valuation assessment done for the El Cubo mine and related assets upon classification as held for sale and the 2020 net impairment charge on non-current assets of $0.4 million related to the value in use estimates of the Guanaceví and El Compas operations. The $1.3 million in care and maintenance costs for 2021 are comprised of $0.7 million recognized for the El Cubo operation for costs to the sale of the mine and related assets in April 2021, and $0.6 million recognized for the El Compas operation, where operations were suspended in mid-August, 2021. During the comparative period of 2020, the Company recognized $3.0 million in care and maintenance costs for the suspended El Cubo operation and $2.2 million in care and maintenance costs related to the temporary suspension of the Guanaceví, Bolañitos and El Compas operations due to COVID-19.

|

MANAGEMENT'S DISCUSSION AND ANALYSIS FOR THE YEAR ENDED DECEMBER 31, 2021 |

The earnings before taxes were $29.7 million (2020: loss before taxes $1.0 million) after finance costs of $1.0 million (2020: $1.3 million), a foreign exchange loss of $1.1 million (2020: $1.5 million), a gain on disposal of the El Cubo mine and related assets of $5.8 million (2020: $Nil) and investment and interest income of $3.7 million (2020: $2.6 million). The Company realized net earnings for the period of $14.0 million (2020: $1.2 million) after an income tax expense of $15.7 million (2020: income tax recovery of $2.2 million).

Net revenue of $165.3 million in 2021, net of $2.0 million of smelting and refining costs, increased by 19% compared to $138.4 million, net of $1.8 million of smelting and refining costs, in 2020. Gross sales of $167.3 million in 2021 represented a 19% increase over the $140.2 million in 2020. Silver oz sold increased by 11% with a 17% increase in the realized silver price, resulting in a 30% increase to silver sales. Gold oz sold increased by 10% with a 3% reduction in realized gold prices resulting in a 7% increase in gold sales. During the period, the Company sold 3,856,883 oz silver and 39,113 oz gold, for realized prices of $25.22 and $1,790 per oz, respectively, compared to sales of 3,460,638 oz silver and 35,519 oz gold, for realized prices of $21.60 and $1,846 per oz, respectively, in 2020. For 2021, the realized prices of silver and gold were within 1% of London spot prices. Silver and gold London spot prices averaged $25.14 and $1,799, respectively, during 2021.

The Company significantly increased its finished goods silver and gold inventory to 1,082,610 oz and 3,674 oz, respectively at December 31, 2021 compared to 116,484 oz silver and 1,459 oz gold at December 31, 2020. The cost allocated to these finished goods was $15.6 million at December 31, 2021, compared to $3.6 million at December 31, 2020. At December 31, 2021, the finished goods inventory fair market value was $31.7 million, compared to $5.8 million at December 31, 2020.