(1)AT&T Inc. does not disclose postpaid net account additions. Comcast and Charter do not disclose postpaid phone net customer additions. Industry-leading claims are based on consensus expectations if results are not yet reported.

(2)Core Adjusted EBITDA, Adjusted Free Cash Flow and Adjusted Free Cash Flow margin are non-GAAP financial measures. These non-GAAP financial measures should be considered in addition to, but not as a substitute for, the information provided in accordance with GAAP. Reconciliations for these non-GAAP financial measures to the most directly comparable GAAP financial measures are provided in the Reconciliation of Non-GAAP Financial Measures to GAAP Financial Measures tables. We are not able to forecast Net income on a forward-looking basis without unreasonable efforts due to the high variability and difficulty in predicting certain items that affect Net income, including, but not limited to, Special Items, Income tax expense and Interest expense. Core Adjusted EBITDA should not be used to predict Net income as the difference between this measure and Net income is variable.

4

Postpaid Accounts

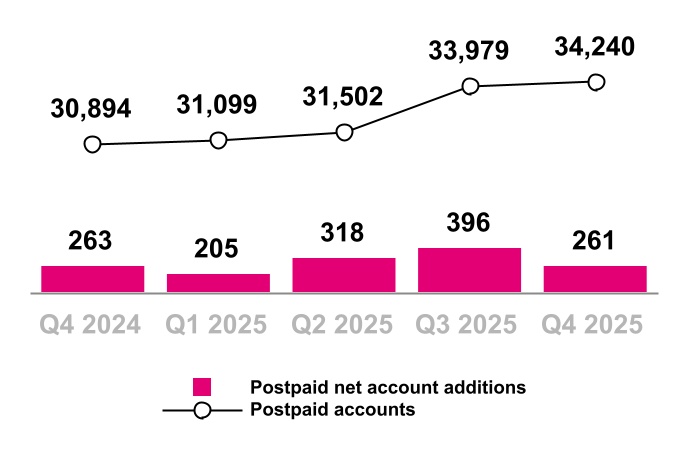

(in thousands)

During Q2 2025, we acquired 85,000 postpaid accounts from Lumos.

During Q3 2025, we acquired 1,448,000 postpaid accounts, net of certain base adjustments, through the UScellular acquisition.

During Q3 2025, we acquired 633,000 postpaid accounts from Metronet and other acquisitions.

Year-Over-Year

Continued growth in Postpaid accounts with net additions relatively flat primarily due to:

■Higher account deactivations driven by the impact from a growing account base, including following the UScellular acquisition, and higher industry switching

■Mostly offset by higher gross account additions, including fiber account additions following the acquisitions of Metronet and Lumos

Sequential

Continued growth in Postpaid accounts with a decrease in net additions primarily due to:

■Higher account deactivations, including seasonal trends, higher industry switching and the impact from a growing account base

Year-Over-Year

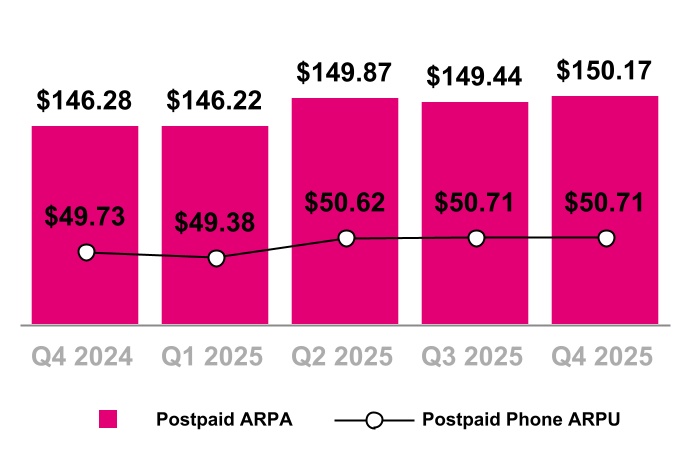

Postpaid ARPA increased 3% primarily due to:

■The positive impact from rate plan optimizations and higher fee revenue, including from the adoption of new tax and fee exclusive plans

■An increase in customers per account, including from the continued adoption of 5G broadband and continued growth of T-Mobile for Business customers, partially offset by fiber and UScellular accounts with fewer customers per account

■Partially offset by increased promotional activity, including the success of bundled offerings

Postpaid phone ARPU increased 2% primarily due to:

■The positive impact from rate plan optimizations and higher fee revenue, including from the adoption of new tax and fee exclusive plans

■The acquisition of higher-ARPU UScellular customers

■Partially offset by increased promotional activity, including the success of bundled offerings

Sequential

Postpaid ARPA increased slightly primarily due to:

■An increase in customers per account, including from the continued adoption of 5G broadband and continued growth of T-Mobile for Business customers, partially offset by fiber and UScellular accounts with fewer customers per account

■Higher fee revenue, including from the adoption of new tax and fee exclusive plans

■Mostly offset by increased promotional activity, including the success of bundled offerings

Sequential

Postpaid phone ARPU was flat primarily due to:

■Higher fee revenue, including from the adoption of new tax and fee exclusive plans

■The acquisition of higher-ARPU UScellular customers

■Offset by increased promotional activity, including the success of bundled offerings

Postpaid ARPA & Postpaid Phone ARPU

5

Postpaid Customers

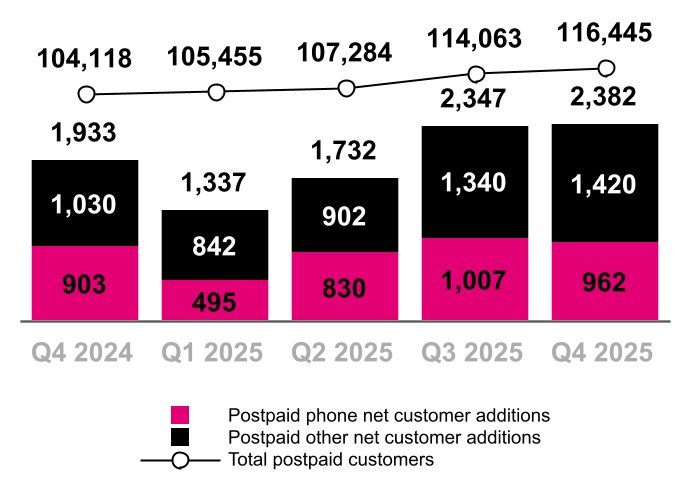

(in thousands)

During Q2 2025, we acquired 97,000 postpaid fiber customers from Lumos.

During Q3 2025, we acquired 3,677,000 postpaid customers, net of certain base adjustments, through the UScellular acquisition.

During Q3 2025, we acquired 755,000 postpaid fiber customers from Metronet and other acquisitions.

Year-Over-Year

Postpaid phone net customer additions increased primarily due to:

■Higher gross additions

■Partially offset by increased deactivations from higher churn and a growing customer base

Postpaid other net customer additions increased primarily due to:

■Higher net additions from mobile internet devices, including from success in business customers

■Higher broadband net additions

■Higher net additions from other connected devices

Sequential

Postpaid phone net customer additions decreased primarily due to:

■Increased deactivations from higher churn and a growing customer base

■Partially offset by higher gross additions, including seasonal trends

Postpaid other net customer additions increased primarily due to:

■Higher net additions from mobile internet devices

■Higher net additions from other connected devices

Year-Over-Year

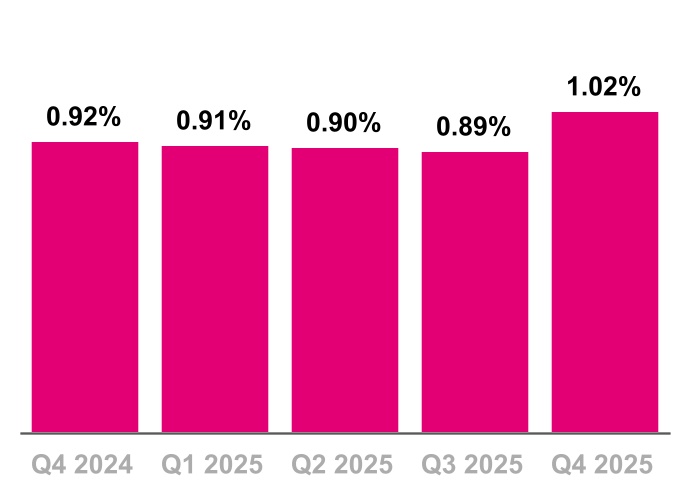

Postpaid phone churn increased 10 basis points primarily due to:

■Higher industry switching

Sequential

Postpaid phone churn increased 13 basis points primarily due to:

■Seasonal trends

■Higher industry switching

Postpaid Phone Churn

6

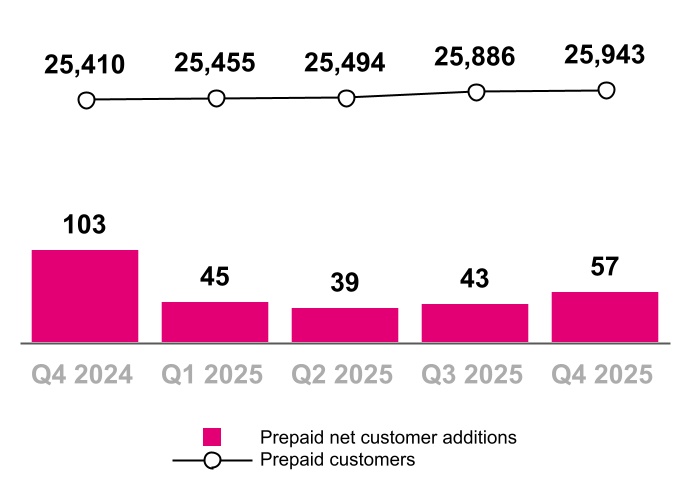

Prepaid Customers

(in thousands)

During Q3 2025, we acquired 349,000 prepaid customers, net of certain base adjustments, through the UScellular acquisition.

Year-Over-Year

Prepaid net customer additions decreased primarily due to:

■Increased deactivations from a growing customer base

■Lower gross additions

■Partially offset by lower churn

Sequential

Prepaid net customer additions increased primarily due to:

■Fewer prepaid to postpaid migrations

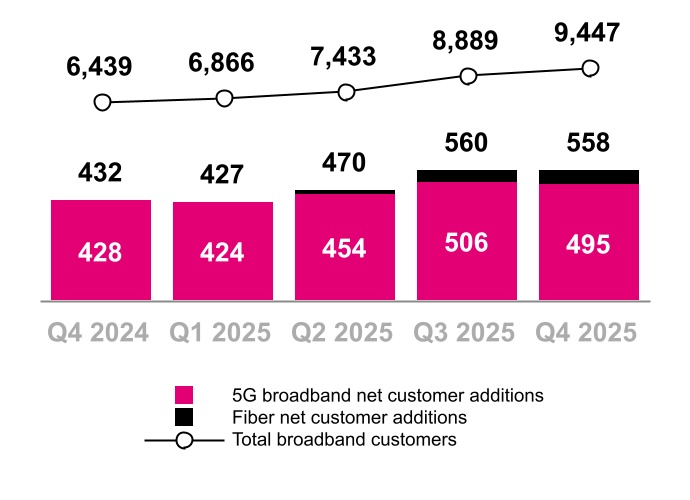

Year-Over-Year

Total broadband net customer additions increased primarily due to:

■Higher gross additions, including fiber gross additions following the acquisitions of Metronet and Lumos

■Lower 5G broadband churn

■Partially offset by increased deactivations from a growing customer base

Sequential

Total broadband net customer additions were relatively flat primarily due to:

■Increased deactivations from a growing customer base

■Mostly offset by lower 5G broadband churn

Broadband Customers

(in thousands)

During Q2 2025, we acquired 97,000 fiber customers from Lumos.

During Q3 2025, we acquired 141,000 postpaid 5G broadband customers, net of certain base adjustments, through the UScellular acquisition.

During Q3 2025, we acquired 755,000 fiber customers from Metronet and other acquisitions.

7

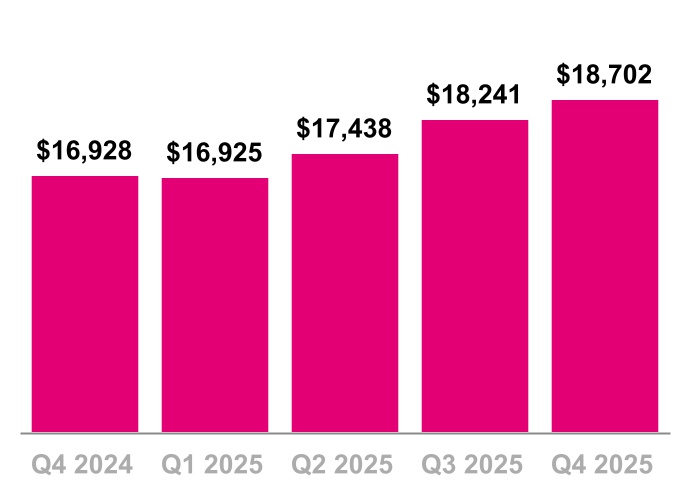

Service Revenues

($ in millions)

Year-Over-Year

Service revenues increased 10% primarily due to:

■An increase in Postpaid service revenues, including following the acquisitions of UScellular, Metronet and Lumos

■Partially offset by lower Prepaid service revenues

Sequential

Service revenues increased 3% primarily due to:

■An increase in Postpaid service revenues, including following the acquisitions of Metronet and UScellular which closed during Q3

Year-Over-Year

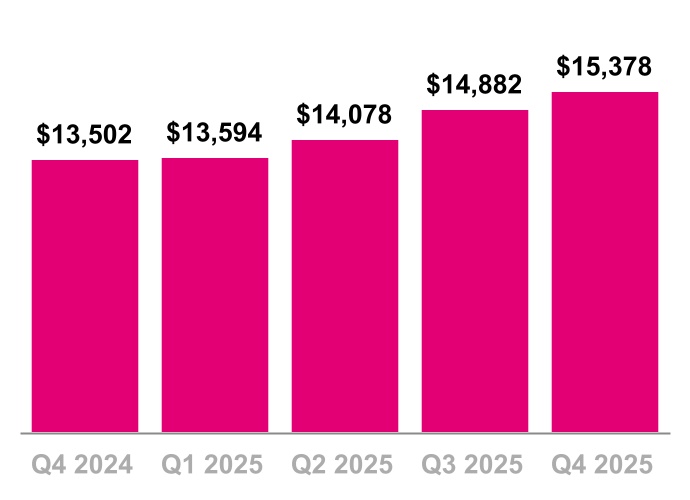

Postpaid service revenues increased 14% primarily due to:

■Higher average postpaid accounts, including following the acquisitions of UScellular, Metronet and Lumos

■Higher postpaid ARPA

Sequential

Postpaid service revenues increased 3% primarily due to:

■Higher average postpaid accounts, including following the acquisitions of UScellular and Metronet which closed during Q3

Postpaid Service Revenues

($ in millions)

8

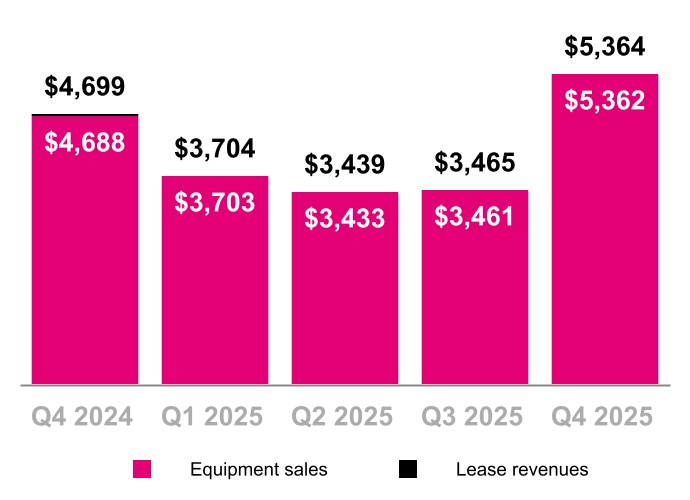

Equipment Revenues

($ in millions)

Year-Over-Year

Equipment revenues increased 14% primarily due to:

■A higher average revenue per device sold, net of promotions, primarily driven by an increase in the high-end phone mix

■Higher liquidation revenue primarily due to a higher number of liquidated devices

■A higher number of devices sold, including following the UScellular acquisition

Sequential

Equipment revenues increased 55% primarily due to:

■A higher average revenue per device sold, net of promotions, primarily due to an increase in the high-end phone mix, including seasonal trends

■A higher number of devices sold, including seasonal trends and following the UScellular acquisition which closed during Q3

■Higher liquidation revenue primarily due to a higher number of liquidated devices and an increase in the high-end phone mix

Year-Over-Year

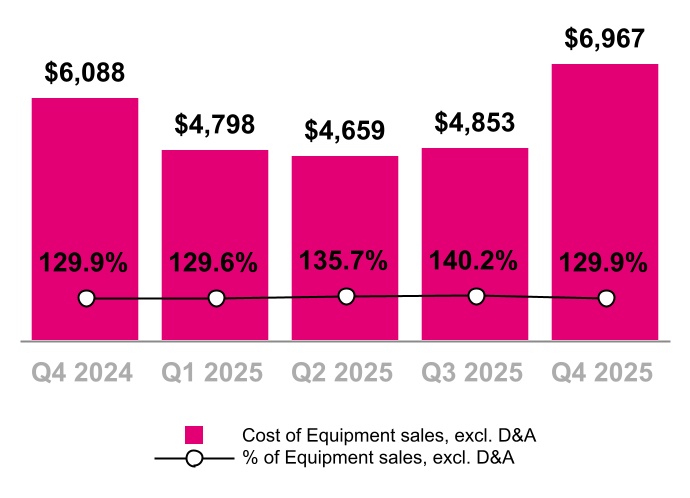

Cost of equipment sales, exclusive of Depreciation and Amortization (D&A), increased 14% primarily due to:

■A higher average cost per device sold primarily driven by an increase in the high-end phone mix

■A higher number of devices sold, including following the UScellular acquisition

■Higher liquidation costs primarily due to a higher number of liquidated devices

Sequential

Cost of equipment sales, exclusive of D&A, increased 44% primarily due to:

■A higher average cost per device sold primarily due to an increase in the high-end phone mix, including seasonal trends

■A higher number of devices sold, including seasonal trends and following the UScellular acquisition which closed during Q3

■Higher liquidation costs primarily due to a higher number of liquidated devices and an increase in the high-end phone mix

Cost of Equipment Sales, exclusive of D&A

($ in millions, % of Equipment sales)

9

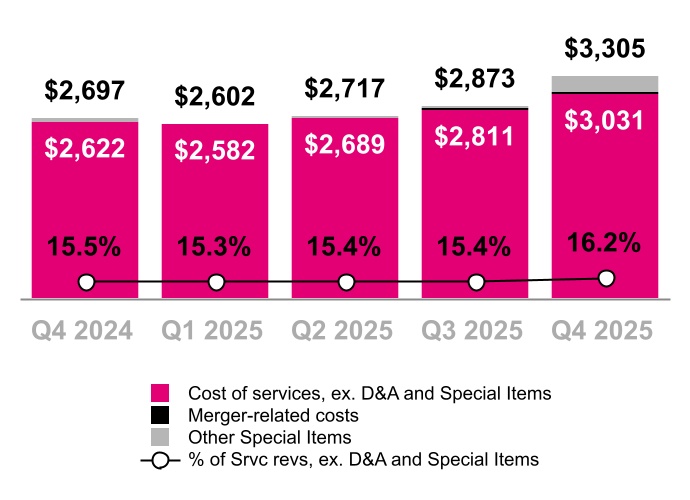

Cost of Services, exclusive of D&A

($ in millions, % of Service revenues)

Year-Over-Year

Cost of services, exclusive of D&A, increased 23% primarily due to:

■Higher costs following the UScellular acquisition, including merger-related costs

■Wholesale network access costs and customer installation fees paid to Metronet and Lumos

■$111 million of severance and related costs associated with the 2025 workforce transformation and reinvestment initiative

■Higher restructuring costs associated with network optimization

Sequential

Cost of services, exclusive of D&A, increased 15% primarily due to:

■$111 million of severance and related costs associated with the 2025 workforce transformation and reinvestment initiative

■Higher repair and maintenance expenses

■Higher restructuring costs associated with network optimization

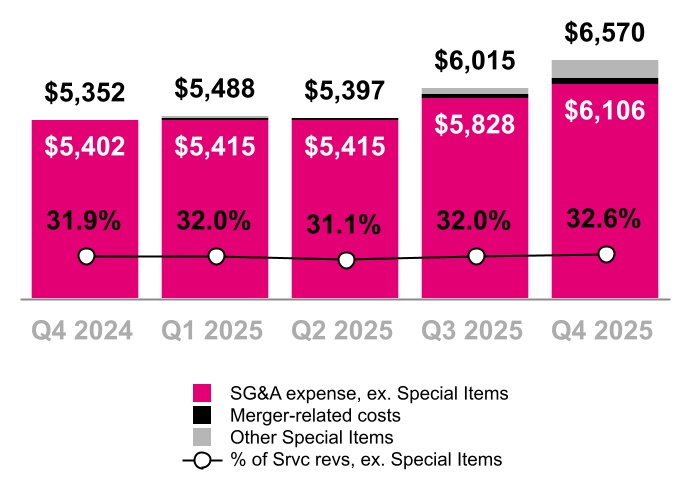

Year-Over-Year

SG&A expense increased 23% primarily due to:

■Higher costs following the UScellular acquisition, including merger-related costs

■$279 million of severance and related costs associated with the 2025 workforce transformation and reinvestment initiative

■Prior year gains related to the closing of certain spectrum exchange transactions and legal-related insurance recoveries

■Higher personnel-related costs, including payroll and benefits

■Higher advertising expenses

Sequential

SG&A expense increased 9% primarily due to:

■$279 million of severance and related costs associated with the 2025 workforce transformation and reinvestment initiative

■Higher advertising expenses

Selling, General and Administrative (SG&A) Expense

($ in millions, % of Service revenues)

10

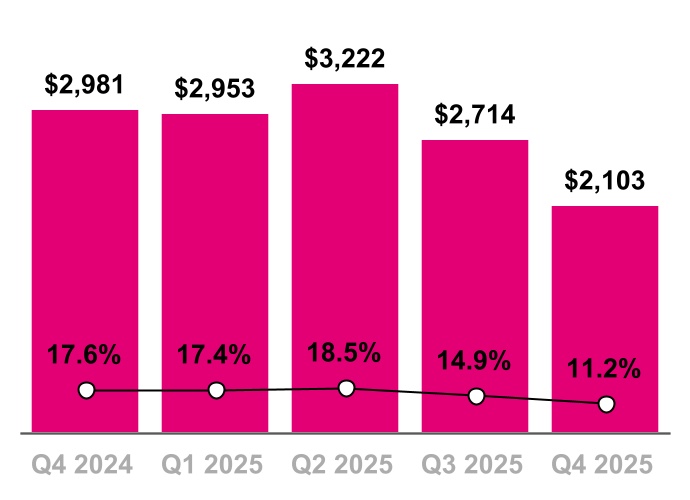

Net Income

($ in millions, % of Service revenues)

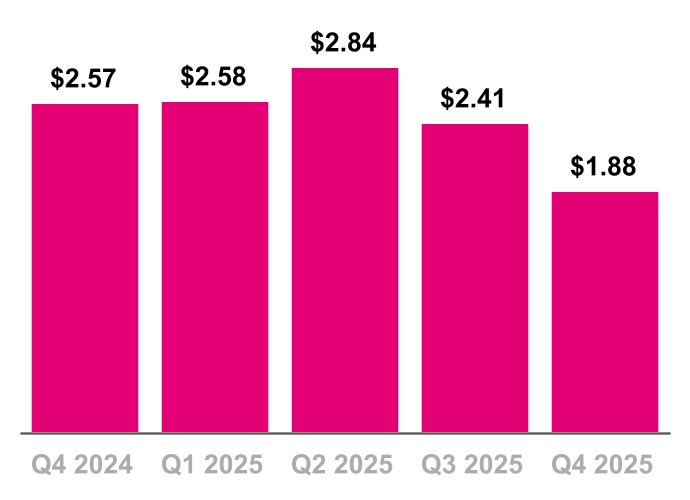

Diluted Earnings Per Share

(Diluted EPS)

Year-Over-Year

Net income was $2.1 billion and Diluted earnings per share was $1.88 in Q4 2025, compared to $3.0 billion and $2.57 in Q4 2024, primarily due to the factors described above and included the following:

■Severance and related costs associated with the 2025 workforce transformation and reinvestment initiative, net of tax, of $293 million, or $0.26 per share, in Q4 2025

Sequential

Net income was $2.1 billion and Diluted earnings per share was $1.88 in Q4 2025, compared to $2.7 billion and $2.41 in Q3 2025, primarily due to the factors described above and included the following:

■Severance and related costs associated with the 2025 workforce transformation and reinvestment initiative, net of tax, of $293 million, or $0.26 per share, in Q4 2025

■Impairment expense related to certain capitalized software development costs, net of tax, of $208 million, or $0.18 per share, in Q3 2025

11

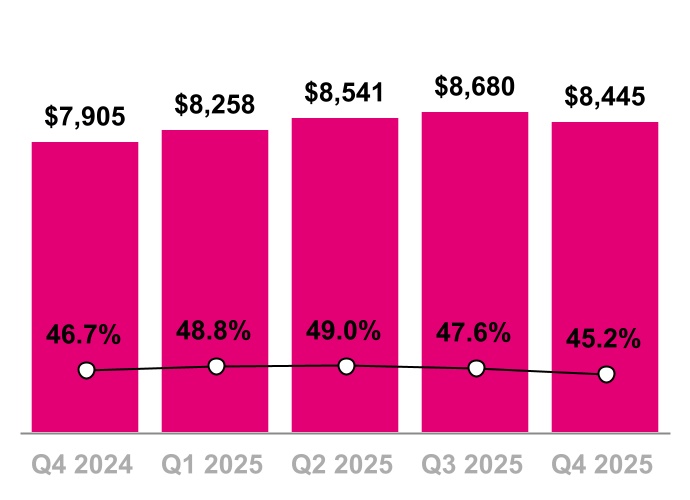

Core Adjusted EBITDA*

($ in millions, % of Service revenues)

*Excludes Special Items (see detail on page 25)

Year-Over-Year

Core Adjusted EBITDA increased 7% primarily due to:

■Partially offset by higher Cost of equipment sales, excluding Special Items, higher SG&A expenses, excluding Special Items, and higher Cost of services, excluding Special Items

Sequential

Core Adjusted EBITDA decreased 3% primarily due to:

■Higher Cost of equipment sales, excluding Special Items

■Higher SG&A expenses, excluding Special Items

■Higher Cost of services, excluding Special Items

■Partially offset by higher Equipment revenues, excluding Lease revenues, and higher Total service revenues

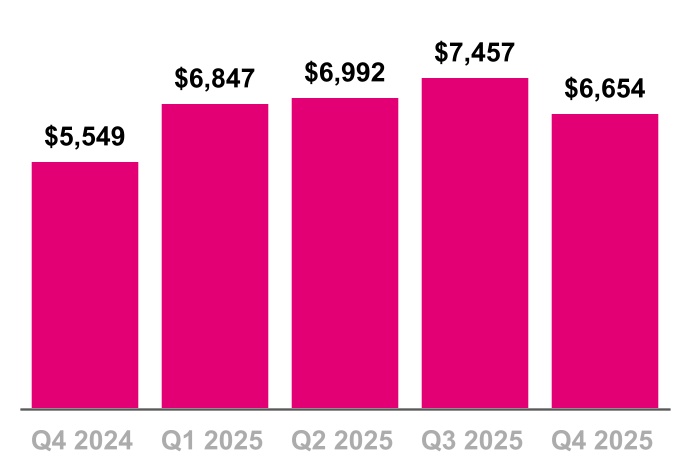

Year-Over-Year

Net cash provided by operating activities increased 20% primarily due to:

■Lower net cash outflows from changes in working capital, including the impact of certain cash proceeds associated with the sale of receivables, which were recognized within investing cash flows before November 1, 2024

■Partially offset by lower Net income, adjusted for non-cash income and expenses

Sequential

Net cash provided by operating activities decreased 11% primarily due to:

■Lower Net income, adjusted for non-cash income and expenses

■Partially offset by lower net cash outflows from changes in working capital

The impact of net payments for Merger-related costs on Net cash provided by operating activities was $100 million in Q4 2025 compared to $96 million in Q3 2025 and $123 million in Q4 2024.

Net Cash Provided by Operating Activities

($ in millions)

Effective November 1, 2024, following amendments to the company’s Equipment Installment Plan Sale and Service Receivable Sale arrangements, all cash proceeds associated with the sale of such receivables, a portion of which was previously recognized as Proceeds related to beneficial interests in securitization transactions within investing cash flows, were recognized as operating cash flows. These amendments did not have a net impact on Adjusted Free Cash Flow.

12

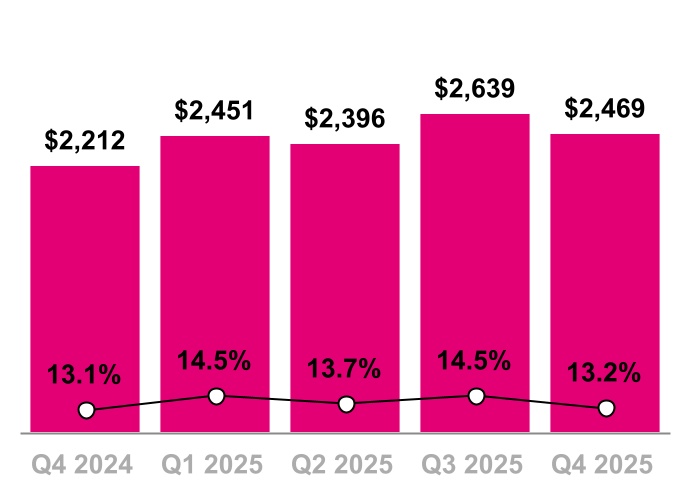

Cash Purchases of Property and Equipment, incl. Capitalized Interest

($ in millions, % of Service revenues)

Year-Over-Year

Cash purchases of property and equipment, including capitalized interest, increased 12% primarily due to:

■Planned timing of capital purchases, including for increased greenfield site builds and incremental capital expenditures following the UScellular acquisition

Sequential

Cash purchases of property and equipment, including capitalized interest, decreased 6% primarily due to:

■Planned timing of capital purchases

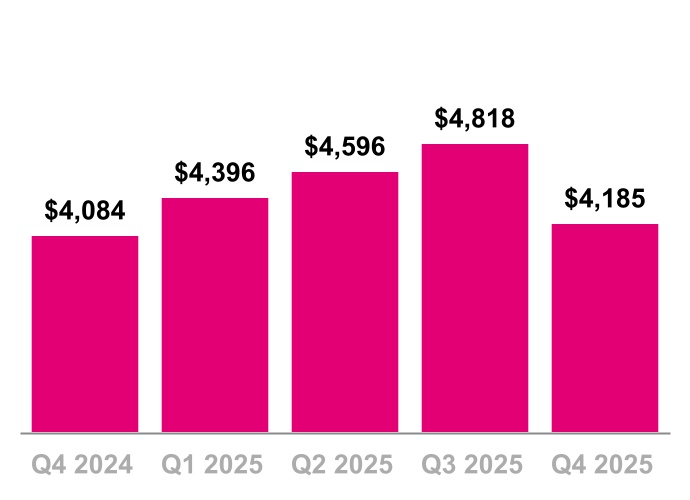

Year-Over-Year

Adjusted Free Cash Flow increased 2% primarily due to:

■Higher Net cash provided by operating activities

■Partially offset by the impact of certain cash proceeds associated with the sale of receivables, which were recognized within investing cash flows before November 1, 2024, and are now recognized as operating cash flows, and higher Cash purchases of property and equipment. The change to the recognition of cash proceeds from the sale of receivables had no net impact to Adjusted Free Cash Flow.

All cash proceeds from the sale of receivables are now recognized within Net cash provided by operating activities. There were no significant net cash impacts during the quarter from securitization.

Sequential

Adjusted Free Cash Flow decreased 13% primarily due to:

■Lower Net cash provided by operating activities

■Partially offset by lower Cash purchases of property and equipment

The impact of net payments for Merger-related costs on Adjusted Free Cash Flow was $100 million in Q4 2025 compared to $96 million in Q3 2025 and $123 million in Q4 2024

Adjusted Free Cash Flow

($ in millions)

13

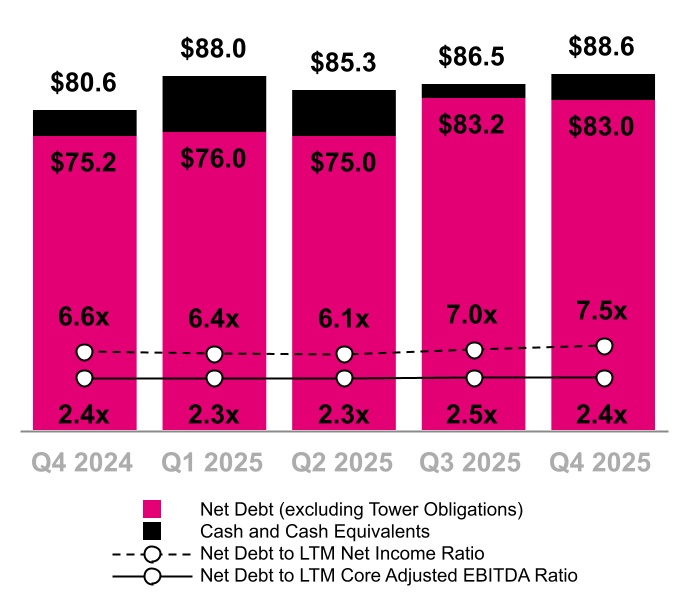

Total Debt (Excluding Tower Obligations),

Net Debt (Excluding Tower Obligations), and

Net Debt to LTM Net Income and Core Adj. EBITDA Ratios

($ in billions)

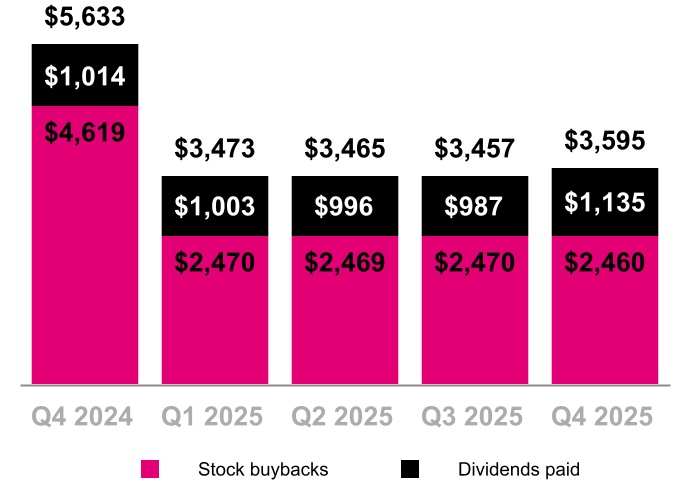

Stockholder Returns

($ in millions)

Total debt, excluding tower obligations, at the end of Q4 2025 was $88.6 billion.

Net debt, excluding tower obligations, at the end of Q4 2025 was $83.0 billion.

■On a cumulative basis, since the company initiated its stockholder return program in Q3 2022, a total of $45.4 billion has been returned to stockholders as of December 31, 2025, with 216.0 million shares repurchased for $37.2 billion, and cumulative cash dividends of $8.2 billion.

■During Q4 2025, 11.9 million shares were repurchased for $2.5 billion.

■During Q4 2025, the company paid a cash dividend of $1.02 per share of common stock, or $1.1 billion, on December 11, 2025.

■On December 11, 2025 the Board of Directors announced a stockholder return program for up to $14.6 billion that will run through December 31, 2026, consisting of additional repurchases of shares and payment of cash dividends, with the next dividend payable on March 12, 2026.

14

2026 Outlook

Postpaid net account additions

900 thousand to

1.0 million

Net income (1)

N/A

Effective tax rate

25% to 26%

Core Adjusted EBITDA (2)

$37.0 to $37.5 billion

Net cash provided by operating activities

$28.0 to $28.7 billion

Capital expenditures (3)

~$10.0 billion

Adjusted Free Cash Flow

$18.0 to $18.7 billion

(1)We are not able to forecast Net income on a forward-looking basis without unreasonable efforts due to the high variability and difficulty in predicting certain items that affect GAAP Net income, including, but not limited to, Special Items, Income tax expense and Interest expense. Core Adjusted EBITDA should not be used to predict Net income as the difference between this measure and Net income is variable.

(2)Management uses Core Adjusted EBITDA as a measure to monitor the financial performance of our operations, excluding the impact of lease revenues from our related device financing programs.

(3)Capital expenditures means cash purchases of property and equipment, including capitalized interest.

15

Investor Relations

Cathy Yao

Matthew Hale

Jon Lanterman

Senior Vice President

Senior Director

Senior Director

Investor Relations

Investor Relations

Investor Relations

Chris Lo

Rose Kopecky

Charles Buffum

Danna Tao

Investor Relations

Investor Relations

Investor Relations

Investor Relations

Manager

Manager

Manager

Manager

investor.relations@t-mobile.com

https://investor.t-mobile.com

16

T-Mobile US, Inc.

Consolidated Balance Sheets

(Unaudited)

(in millions, except share and per share amounts)

December 31, 2025

December 31, 2024

Assets

Current assets

Cash and cash equivalents

$

5,598

$

5,409

Accounts receivable, net of allowance for credit losses of $226 and $176

4,874

4,276

Equipment installment plan receivables, net of allowance for credit losses and imputed discount of $733 and $656

4,997

4,379

Inventory

2,405

1,607

Prepaid expenses

1,215

880

Other current assets

5,372

1,853

Total current assets

24,461

18,404

Property and equipment, net

38,333

38,533

Operating lease right-of-use assets

25,692

25,398

Financing lease right-of-use assets

2,760

3,091

Goodwill

13,678

13,005

Spectrum licenses

98,032

100,558

Other intangible assets, net

3,843

2,512

Equipment installment plan receivables due after one year, net of allowance for credit losses and imputed discount of $213 and $158

2,683

2,209

Other assets

9,755

4,325

Total assets

$

219,237

$

208,035

Liabilities and Stockholders' Equity

Current liabilities

Accounts payable and accrued liabilities

$

10,280

$

8,463

Short-term debt

5,135

4,068

Deferred revenue

1,533

1,222

Short-term operating lease liabilities

3,814

3,281

Short-term financing lease liabilities

1,163

1,175

Other current liabilities

2,575

1,965

Total current liabilities

24,500

20,174

Long-term debt

79,649

72,700

Long-term debt to affiliates

1,498

1,497

Tower obligations

3,532

3,664

Deferred tax liabilities

19,583

16,700

Operating lease liabilities

26,371

26,408

Financing lease liabilities

1,107

1,151

Other long-term liabilities

3,794

4,000

Total long-term liabilities

135,534

126,120

Commitments and contingencies

Stockholders' equity

Common stock, par value $0.00001 per share, 2,000,000,000 shares authorized; 1,275,774,235 and 1,271,074,364 shares issued, 1,106,930,661 and 1,144,579,681 shares outstanding

—

—

Additional paid-in capital

69,460

68,798

Treasury stock, at cost, 168,843,574 and 126,494,683 shares issued

(30,545)

(20,584)

Accumulated other comprehensive loss

(848)

(857)

Retained earnings

21,136

14,384

Total stockholders' equity

59,203

61,741

Total liabilities and stockholders' equity

$

219,237

$

208,035

17

T-Mobile US, Inc.

Consolidated Statements of Comprehensive Income

(Unaudited)

Three Months Ended

Year Ended December 31,

(in millions, except share and per share amounts)

December 31, 2025

September 30, 2025

December 31, 2024

2025

2024

Revenues

Postpaid revenues

$

15,378

$

14,882

$

13,502

$

57,932

$

52,340

Prepaid revenues

2,586

2,625

2,688

10,497

10,399

Wholesale and other service revenues

738

734

738

2,877

3,439

Total service revenues

18,702

18,241

16,928

71,306

66,178

Equipment revenues

5,364

3,465

4,699

15,972

14,263

Other revenues

268

251

245

1,031

959

Total revenues

24,334

21,957

21,872

88,309

81,400

Operating expenses

Cost of services, exclusive of depreciation and amortization shown separately below

3,305

2,873

2,697

11,497

10,771

Cost of equipment sales, exclusive of depreciation and amortization shown separately below

6,967

4,853

6,088

21,277

18,882

Selling, general and administrative

6,570

6,015

5,352

23,470

20,818

Impairment expense

—

278

—

278

—

Depreciation and amortization

3,756

3,408

3,149

13,508

12,919

Total operating expenses

20,598

17,427

17,286

70,030

63,390

Operating income

3,736

4,530

4,586

18,279

18,010

Other expense, net

Interest expense, net

(1,012)

(924)

(841)

(3,774)

(3,411)

Other (expense) income, net

(89)

(78)

94

(224)

113

Total other expense, net

(1,101)

(1,002)

(747)

(3,998)

(3,298)

Income before income taxes

2,635

3,528

3,839

14,281

14,712

Income tax expense

(532)

(814)

(858)

(3,289)

(3,373)

Net income

$

2,103

$

2,714

$

2,981

$

10,992

$

11,339

Net income

$

2,103

$

2,714

$

2,981

$

10,992

$

11,339

Other comprehensive income, net of tax

Reclassification of loss from cash flow hedges, net of tax effect of $17, $16, $15, $65 and $60

49

48

46

190

176

(Losses) gains on fair value hedges, net of tax effect of $(9), $(7), $20, $(64) and $5

(27)

(20)

58

(187)

16

Unrealized loss on foreign currency translation adjustment, net of tax effect of $0, $0, $0, $0 and $0

—

—

—

(1)

—

Actuarial gain (loss), net of amortization and reclassification, on pension and other postretirement benefits, net of tax effect of $3, $0, $(24), $2 and $(29)

11

(1)

(72)

7

(85)

Other comprehensive income

33

27

32

9

107

Total comprehensive income

$

2,136

$

2,741

$

3,013

$

11,001

$

11,446

Earnings per share

Basic

$

1.89

$

2.42

$

2.58

$

9.75

$

9.70

Diluted

$

1.88

$

2.41

$

2.57

$

9.72

$

9.66

Weighted-average shares outstanding

Basic

1,115,209,714

1,123,754,096

1,154,679,440

1,127,984,348

1,169,195,373

Diluted

1,117,388,934

1,126,627,708

1,159,095,696

1,131,076,251

1,173,213,898

18

T-Mobile US, Inc.

Consolidated Statements of Cash Flows

(Unaudited)

Three Months Ended

Year Ended December 31,

(in millions)

December 31, 2025

September 30, 2025

December 31, 2024

2025

2024

Operating activities

Net income

$

2,103

$

2,714

$

2,981

$

10,992

$

11,339

Adjustments to reconcile net income to net cash provided by operating activities

Depreciation and amortization

3,756

3,408

3,149

13,508

12,919

Stock-based compensation expense

216

227

175

829

649

Deferred income tax expense

359

797

841

2,864

3,120

Bad debt expense

445

337

356

1,370

1,192

Losses (gains) from sales of receivables

—

17

(7)

58

62

Impairment expense

—

278

—

278

—

Changes in operating assets and liabilities

Accounts receivable

42

(366)

(652)

(755)

(3,088)

Equipment installment plan receivables

(1,010)

44

(883)

(877)

(523)

Inventory

(24)

(537)

188

(615)

131

Operating lease right-of-use assets

968

929

875

3,635

3,480

Other current and long-term assets

(505)

(322)

(136)

(1,488)

(411)

Accounts payable and accrued liabilities

813

890

(180)

1,542

(2,041)

Short- and long-term operating lease liabilities

(737)

(936)

(909)

(3,457)

(3,879)

Other current and long-term liabilities

30

(239)

(21)

(379)

(678)

Other, net

198

216

(228)

445

21

Net cash provided by operating activities

6,654

7,457

5,549

27,950

22,293

Investing activities

Purchases of property and equipment, including capitalized interest of $(10), $(13), $(8), $(43) and $(34)

(2,469)

(2,639)

(2,212)

(9,955)

(8,840)

Purchases of spectrum licenses and other intangible assets, including deposits

(63)

(1,590)

(835)

(2,568)

(3,471)

Proceeds from the sale of property, equipment and intangible assets

77

18

61

2,168

99

Proceeds related to beneficial interests in securitization transactions

—

—

747

—

3,579

Acquisition of companies, net of cash acquired

—

(2,797)

17

(3,523)

(373)

Investments in unconsolidated affiliates, net

(1)

(3,072)

(18)

(4,056)

(18)

Other, net

(44)

(59)

(60)

327

(48)

Net cash used in investing activities

(2,500)

(10,139)

(2,300)

(17,607)

(9,072)

Financing activities

Proceeds from issuance of long-term debt, net

3,744

498

498

12,010

8,587

Repayments of financing lease obligations

(288)

(318)

(342)

(1,252)

(1,367)

Repayments of long-term debt

(1,635)

(828)

(1,904)

(6,199)

(5,073)

Repurchases of common stock

(2,446)

(2,479)

(4,687)

(9,974)

(11,228)

Dividends on common stock

(1,135)

(987)

(1,014)

(4,121)

(3,300)

Tax withholdings on share-based awards

(40)

(92)

(25)

(434)

(269)

Other, net

(31)

(32)

(48)

(111)

(165)

Net cash used in financing activities

(1,831)

(4,238)

(7,522)

(10,081)

(12,815)

Effect of exchange rate changes on cash and cash equivalents, including restricted cash

(12)

—

—

1

—

Change in cash and cash equivalents, including restricted cash

2,311

(6,920)

(4,273)

263

406

Cash and cash equivalents, including restricted cash

Beginning of period

3,665

10,585

9,986

5,713

5,307

End of period

$

5,976

$

3,665

$

5,713

$

5,976

$

5,713

19

T-Mobile US, Inc.

Consolidated Statements of Cash Flows (Continued)

(Unaudited)

Three Months Ended

Year Ended December 31,

(in millions)

December 31, 2025

September 30, 2025

December 31, 2024

2025

2024

Supplemental disclosure of cash flow information

Interest payments, net of amounts capitalized

$

959

$

997

$

905

$

3,882

$

3,683

Operating lease payments

1,079

1,269

1,234

4,764

5,162

Income tax payments, net of refunds received

36

63

44

451

179

Non-cash investing and financing activities

Non-cash beneficial interest obtained in exchange for securitized receivables

$

—

$

—

$

138

$

—

$

2,421

Change in accounts payable and accrued liabilities for purchases of property and equipment

231

136

1,190

(227)

105

Operating lease right-of-use assets obtained in exchange for lease obligations

590

1,064

441

2,728

1,741

Financing lease right-of-use assets obtained in exchange for lease obligations

230

324

239

1,232

1,222

Deferred consideration related to the Ka’ena Acquisition

—

—

8

—

218

Debt assumed in the UScellular Acquisition

—

1,653

—

1,653

—

20

T-Mobile US, Inc.

Supplementary Operating and Financial Data

(Unaudited)

Quarter

Year Ended December 31,

(in thousands)

Q1 2024

Q2 2024

Q3 2024

Q4 2024

Q1 2025

Q2 2025

Q3 2025

Q4 2025

2024

2025

Customers, end of period

Postpaid phone customers (1)

76,468

77,245

78,110

79,013

79,508

80,338

84,632

85,594

79,013

85,594

Postpaid other customers (1) (2) (3)

22,804

23,365

24,075

25,105

25,947

26,946

29,431

30,851

25,105

30,851

Total postpaid customers

99,272

100,610

102,185

104,118

105,455

107,284

114,063

116,445

104,118

116,445

Prepaid customers (1) (4)

21,600

25,283

25,307

25,410

25,455

25,494

25,886

25,943

25,410

25,943

Total customers

120,872

125,893

127,492

129,528

130,910

132,778

139,949

142,388

129,528

142,388

Adjustments to customers (1) (2) (3) (4)

—

3,504

—

—

—

97

4,781

—

3,504

4,878

(1)In the third quarter of 2025, we acquired 3,287,000 postpaid phone customers, 390,000 postpaid other customers and 349,000 prepaid customers through the UScellular acquisition, which includes the impact of certain base adjustments to align the policies of UScellular and T-Mobile.

(2)In the third quarter of 2025, we acquired 755,000 fiber customers from Metronet and other acquisitions.

(3)In the second quarter of 2025, we acquired 97,000 fiber customers from Lumos.

(4)In the second quarter of 2024, we acquired 3,504,000 prepaid customers through the Ka’ena acquisition, which includes the impact of certain base adjustments to align the policies of Ka’ena and T-Mobile.

Quarter

Year Ended December 31,

(in thousands)

Q1 2024

Q2 2024

Q3 2024

Q4 2024

Q1 2025

Q2 2025

Q3 2025

Q4 2025

2024

2025

Net customer additions (losses)

Postpaid phone customers

532

777

865

903

495

830

1,007

962

3,077

3,294

Postpaid other customers

688

561

710

1,030

842

902

1,340

1,420

2,989

4,504

Total postpaid customers

1,220

1,338

1,575

1,933

1,337

1,732

2,347

2,382

6,066

7,798

Prepaid customers

(48)

179

24

103

45

39

43

57

258

184

Total net customer additions

1,172

1,517

1,599

2,036

1,382

1,771

2,390

2,439

6,324

7,982

Migrations from prepaid to postpaid plans

145

140

175

160

115

205

215

185

620

720

Quarter

Year Ended December 31,

Q1 2024

Q2 2024

Q3 2024

Q4 2024

Q1 2025

Q2 2025

Q3 2025

Q4 2025

2024

2025

Churn

Postpaid phone churn

0.86

%

0.80

%

0.86

%

0.92

%

0.91

%

0.90

%

0.89

%

1.02

%

0.86

%

0.93

%

Prepaid churn

2.75

%

2.54

%

2.78

%

2.85

%

2.68

%

2.65

%

2.77

%

2.76

%

2.73

%

2.72

%

Quarter

Year Ended December 31,

Q1 2024

Q2 2024

Q3 2024

Q4 2024

Q1 2025

Q2 2025

Q3 2025

Q4 2025

2024

2025

Postpaid upgrade rate

Postpaid device upgrade rate

2.4

%

2.3

%

2.6

%

3.6

%

2.8

%

2.5

%

2.7

%

3.8

%

11.1

%

11.8

%

21

T-Mobile US, Inc.

Supplementary Operating and Financial Data (Continued)

(Unaudited)

Quarter

Year Ended December 31,

(in thousands)

Q1 2024

Q2 2024

Q3 2024

Q4 2024

Q1 2025

Q2 2025

Q3 2025

Q4 2025

2024

2025

Accounts, end of period

Total postpaid accounts (1) (2) (3)

30,015

30,316

30,631

30,894

31,099

31,502

33,979

34,240

30,894

34,240

(1)In the second quarter of 2025, we acquired 85,000 postpaid accounts from Lumos.

(2)In the third quarter of 2025, we acquired 633,000 postpaid accounts from Metronet and other acquisitions.

(3)In the third quarter of 2025, we acquired 1,448,000 postpaid accounts through the UScellular acquisition, which includes the impact of certain base adjustments to align the policies of UScellular and T-Mobile.

Quarter

Year Ended December 31,

(in thousands)

Q1 2024

Q2 2024

Q3 2024

Q4 2024

Q1 2025

Q2 2025

Q3 2025

Q4 2025

2024

2025

Net account additions

Postpaid net account additions

218

301

315

263

205

318

396

261

1,097

1,180

Quarter

Year Ended December 31,

(in thousands)

Q1 2024

Q2 2024

Q3 2024

Q4 2024

Q1 2025

Q2 2025

Q3 2025

Q4 2025

2024

2025

Broadband customers, end of period

Postpaid 5G broadband customers (1)

4,634

4,992

5,377

5,742

6,129

6,556

7,163

7,602

5,742

7,602

Prepaid 5G broadband customers

547

595

625

688

725

752

792

848

688

848

Total 5G broadband customers, end of period

5,181

5,587

6,002

6,430

6,854

7,308

7,955

8,450

6,430

8,450

Fiber customers (2) (3)

1

2

5

9

12

125

934

997

9

997

Total broadband customers, end of period

5,182

5,589

6,007

6,439

6,866

7,433

8,889

9,447

6,439

9,447

Adjustments to customers (1) (2) (3)

—

—

—

—

—

97

896

—

—

993

(1)In the third quarter of 2025, we acquired 141,000 postpaid 5G broadband customers through the UScellular acquisition, which includes the impact of certain base adjustments to align the policies of UScellular and T-Mobile.

(2)In the third quarter of 2025, we acquired 755,000 fiber customers from Metronet and other acquisitions.

(3)In the second quarter of 2025, we acquired 97,000 fiber customers from Lumos.

Quarter

Year Ended December 31,

(in thousands)

Q1 2024

Q2 2024

Q3 2024

Q4 2024

Q1 2025

Q2 2025

Q3 2025

Q4 2025

2024

2025

Broadband - net customer additions

Postpaid 5G broadband customers

346

358

385

365

387

427

466

439

1,454

1,719

Prepaid 5G broadband customers

59

48

30

63

37

27

40

56

200

160

Total 5G broadband net customer additions

405

406

415

428

424

454

506

495

1,654

1,879

Fiber customers

—

1

3

4

3

16

54

63

8

136

Total broadband net customer additions

405

407

418

432

427

470

560

558

1,662

2,015

22

T-Mobile US, Inc.

Supplementary Operating and Financial Data (Continued)

(Unaudited)

Quarter

Year Ended December 31,

(in millions)

Q1 2024

Q2 2024

Q3 2024

Q4 2024

Q1 2025

Q2 2025

Q3 2025

Q4 2025

2024

2025

Device financing - equipment installment plans

Gross EIP financed

$

3,218

$

3,037

$

3,304

$

4,689

$

3,565

$

3,503

$

3,871

$

5,774

$

14,248

$

16,713

EIP billings

3,880

3,604

3,423

3,509

3,551

3,553

3,766

4,066

14,416

14,936

EIP receivables, net

5,967

5,556

5,347

6,588

6,405

6,201

6,915

7,680

6,588

7,680

Device financing - leased devices

Lease revenues

$

35

$

26

$

21

$

11

$

1

$

6

$

4

$

2

$

93

$

13

Leased device depreciation

22

15

11

6

4

1

—

—

54

5

Quarter

Year Ended December 31,

(in dollars)

Q1 2024

Q2 2024

Q3 2024

Q4 2024

Q1 2025

Q2 2025

Q3 2025

Q4 2025

2024

2025

Operating measures

Postpaid ARPA

$

140.88

$

142.54

$

145.60

$

146.28

$

146.22

$

149.87

$

149.44

$

150.17

$

143.85

$

148.97

Postpaid phone ARPU

48.79

49.07

49.79

49.73

49.38

50.62

50.71

50.71

49.35

50.37

Prepaid ARPU

37.18

35.94

35.81

35.49

34.67

34.63

33.93

33.33

36.06

34.14

23

T-Mobile US, Inc.

Supplementary Operating and Financial Data (continued)

(Unaudited)

Quarter

Year Ended December 31,

(in millions, except percentages)

Q1 2024

Q2 2024

Q3 2024

Q4 2024

Q1 2025

Q2 2025

Q3 2025

Q4 2025

2024

2025

Financial measures

Service revenues

$

16,096

$

16,429

$

16,725

$

16,928

$

16,925

$

17,438

$

18,241

$

18,702

$

66,178

$

71,306

Equipment revenues

$

3,251

$

3,106

$

3,207

$

4,699

$

3,704

$

3,439

$

3,465

$

5,364

$

14,263

$

15,972

Lease revenues

35

26

21

11

1

6

4

2

93

13

Equipment sales

$

3,216

$

3,080

$

3,186

$

4,688

$

3,703

$

3,433

$

3,461

$

5,362

$

14,170

$

15,959

Total revenues

$

19,594

$

19,772

$

20,162

$

21,872

$

20,886

$

21,132

$

21,957

$

24,334

$

81,400

$

88,309

Net income

$

2,374

$

2,925

$

3,059

$

2,981

$

2,953

$

3,222

$

2,714

$

2,103

$

11,339

$

10,992

Net income margin

14.7

%

17.8

%

18.3

%

17.6

%

17.4

%

18.5

%

14.9

%

11.2

%

17.1

%

15.4

%

Adjusted EBITDA

$

7,652

$

8,053

$

8,243

$

7,916

$

8,259

$

8,547

$

8,684

$

8,447

$

31,864

$

33,937

Adjusted EBITDA margin

47.5

%

49.0

%

49.3

%

46.8

%

48.8

%

49.0

%

47.6

%

45.2

%

48.1

%

47.6

%

Core Adjusted EBITDA

$

7,617

$

8,027

$

8,222

$

7,905

$

8,258

$

8,541

$

8,680

$

8,445

$

31,771

$

33,924

Core Adjusted EBITDA margin

47.3

%

48.9

%

49.2

%

46.7

%

48.8

%

49.0

%

47.6

%

45.2

%

48.0

%

47.6

%

Cost of services, exclusive of depreciation and amortization

$

2,688

$

2,664

$

2,722

$

2,697

$

2,602

$

2,717

$

2,873

$

3,305

$

10,771

$

11,497

Merger-related costs

107

73

—

—

—

—

7

24

180

31

Other Special Items

1

—

67

75

20

28

55

250

143

353

Cost of services, excluding depreciation and amortization and Special Items

$

2,580

$

2,591

$

2,655

$

2,622

$

2,582

$

2,689

$

2,811

$

3,031

$

10,448

$

11,113

Cost of equipment sales, exclusive of depreciation and amortization

$

4,399

$

4,088

$

4,307

$

6,088

$

4,798

$

4,659

$

4,853

$

6,967

$

18,882

$

21,277

Merger-related costs

$

—

—

—

—

—

—

2

8

—

10

Cost of equipment sales, exclusive of depreciation and amortization and Special Items

$

4,399

$

4,088

$

4,307

$

6,088

$

4,798

$

4,659

$

4,851

$

6,959

$

18,882

$

21,267

Selling, general and administrative

$

5,138

$

5,142

$

5,186

$

5,352

$

5,488

$

5,397

$

6,015

$

6,570

$

20,818

$

23,470

Merger-related costs (gain), net

23

(82)

16

10

14

33

64

111

(33)

222

Other Special Items

12

37

70

(60)

59

(51)

123

353

59

484

Selling, general and administrative, excluding Special Items

$

5,103

$

5,187

$

5,100

$

5,402

$

5,415

$

5,415

$

5,828

$

6,106

$

20,792

$

22,764

Total bad debt expense and losses from sales of receivables

$

303

$

280

$

322

$

349

$

345

$

284

$

354

$

445

$

1,254

$

1,428

Bad debt and losses from sales of receivables as a percentage of Total revenues

1.5

%

1.4

%

1.6

%

1.6

%

1.7

%

1.3

%

1.6

%

1.8

%

1.5

%

1.6

%

Cash purchases of property and equipment including capitalized interest

$

2,627

$

2,040

$

1,961

$

2,212

$

2,451

$

2,396

$

2,639

$

2,469

$

8,840

$

9,955

Capitalized interest

9

8

9

8

10

10

13

10

34

43

Net cash proceeds from securitization

$

(29)

$

(30)

$

(29)

$

(27)

$

(26)

$

(23)

$

(25)

$

(22)

$

(115)

$

(96)

Net cash payments for Merger-related costs

$

293

$

241

$

132

$

123

$

70

$

92

$

96

$

100

$

789

$

358

24

T-Mobile US, Inc.

Supplementary Operating and Financial Data (Continued)

(Unaudited)

Quarter

Year Ended December 31,

(in millions, except share and per share amounts)

Q1 2024

Q2 2024

Q3 2024

Q4 2024

Q1 2025

Q2 2025

Q3 2025

Q4 2025

2024

2025

Stockholder returns

Total repurchases

$

3,568

$

2,277

$

644

$

4,619

$

2,470

$

2,469

$

2,470

$

2,460

$

11,108

$

9,869

Total shares repurchased

21,933,790

13,979,843

3,179,707

20,283,582

10,091,227

10,148,791

10,204,072

11,919,136

59,376,922

42,363,226

Average purchase price per share

$

162.69

$

162.85

$

202.45

$

227.72

$

244.77

$

243.32

$

242.01

$

206.38

$

187.07

$

232.96

Total dividends paid

$

769

$

759

$

758

$

1,014

$

1,003

$

996

$

987

$

1,135

$

3,300

$

4,121

Dividends per share

$

0.65

$

0.65

$

0.65

$

0.88

$

0.88

$

0.88

$

0.88

$

1.02

$

2.83

$

3.66

Total stockholder returns

$

4,337

$

3,036

$

1,402

$

5,633

$

3,473

$

3,465

$

3,457

$

3,595

$

14,408

$

13,990

Cumulative total repurchases

$

19,775

$

22,052

$

22,696

$

27,315

$

29,785

$

32,254

$

34,724

$

37,184

$

27,315

$

37,184

Cumulative shares repurchased

136,220,243

150,200,086

153,379,793

173,663,375

183,754,602

193,903,393

204,107,465

216,026,601

173,663,375

216,026,601

Cumulative stockholder returns

$

21,291

$

24,327

$

25,729

$

31,362

$

34,835

$

38,300

$

41,757

$

45,352

$

31,362

$

45,352

25

T-Mobile US, Inc.

Reconciliation of Non-GAAP Financial Measures to GAAP Financial Measures

(Unaudited)

This Investor Factbook includes non-GAAP financial measures, including Adjusted EBITDA, Core Adjusted EBITDA, Net Debt, Adjusted Free Cash Flow and Adjusted Free Cash Flow margin. The non-GAAP financial measures should be considered in addition to, but not as a substitute for, the information provided in accordance with GAAP. Reconciliations for the non-GAAP financial measures to the most directly comparable GAAP financial measures are provided below. T-Mobile is not able to forecast Net income on a forward-looking basis without unreasonable efforts due to the high variability and difficulty in predicting certain items that affect GAAP net income, including, but not limited to, Special Items, Income tax expense and Interest expense. Adjusted EBITDA and Core Adjusted EBITDA should not be used to predict Net income, as the difference between either of these measures and Net income is variable.

Adjusted EBITDA and Core Adjusted EBITDA are reconciled to Net income as follows:

Quarter

Year Ended December 31,

(in millions, except percentages)

Q1 2024

Q2 2024

Q3 2024

Q4 2024

Q1 2025

Q2 2025

Q3 2025

Q4 2025

2024

2025

Net income

$

2,374

$

2,925

$

3,059

$

2,981

$

2,953

$

3,222

$

2,714

$

2,103

$

11,339

$

10,992

Adjustments:

Interest expense, net

880

854

836

841

916

922

924

1,012

3,411

3,774

Other (income) expense, net

(20)

8

(7)

(94)

46

11

78

89

(113)

224

Income tax expense

764

843

908

858

885

1,058

814

532

3,373

3,289

Operating income

3,998

4,630

4,796

4,586

4,800

5,213

4,530

3,736

18,010

18,279

Depreciation and amortization

3,371

3,248

3,151

3,149

3,198

3,146

3,408

3,756

12,919

13,508

Stock-based compensation (1)

140

147

143

156

168

178

217

209

586

772

Merger-related costs (gain), net (2)

130

(9)

16

10

14

33

73

143

147

263

Network restructuring initiative

costs (3)

—

—

—

—

—

—

—

93

—

93

Legal-related expenses (recoveries), net (4)

—

15

1

(105)

6

(4)

8

6

(89)

16

Impairment expense

—

—

—

—

—

—

278

—

—

278

Other, net (5)

13

22

136

120

73

(19)

170

504

291

728

Adjusted EBITDA

7,652

8,053

8,243

7,916

8,259

8,547

8,684

8,447

31,864

33,937

Lease revenues

(35)

(26)

(21)

(11)

(1)

(6)

(4)

(2)

(93)

(13)

Core Adjusted EBITDA

$

7,617

$

8,027

$

8,222

$

7,905

$

8,258

$

8,541

$

8,680

$

8,445

$

31,771

$

33,924

Net income margin (Net income divided by Service revenues)

14.7

%

17.8

%

18.3

%

17.6

%

17.4

%

18.5

%

14.9

%

11.2

%

17.1

%

15.4

%

Adjusted EBITDA margin (Adjusted EBITDA divided by Service revenues)

47.5

%

49.0

%

49.3

%

46.8

%

48.8

%

49.0

%

47.6

%

45.2

%

48.1

%

47.6

%

Core Adjusted EBITDA margin (Core Adjusted EBITDA divided by Service revenues)

47.3

%

48.9

%

49.2

%

46.7

%

48.8

%

49.0

%

47.6

%

45.2

%

48.0

%

47.6

%

(1)Stock-based compensation includes payroll tax impacts and may not agree to stock-based compensation expense on the Consolidated Financial Statements. Additionally, certain stock-based compensation expenses associated with the Sprint merger have been included in Merger-related costs (gain), net.

(2)Merger-related costs (gain), net, for the three months ended June 30, 2024 and the year ended December 31, 2024, includes the $100 million gain recognized for the extension fee previously paid by DISH associated with the license purchase agreement for 800 MHz spectrum licenses, which was not purchased.

(3)In Q4 2025, we began implementing network restructuring initiatives as a result of recent technological advancements that enhanced our Customer-Driven Coverage insights. Network restructuring initiative costs consist of network decommissioning and contract termination costs related to the rationalization of our network and backhaul services and the elimination of duplicative costs.

(4)Legal-related expenses (recoveries), net, consists of the settlement of certain litigation and compliance costs associated with the August 2021 cyberattack and is presented net of insurance recoveries.

(5)Other, net, primarily consists of certain severance, restructuring and other expenses, gains and losses, not directly attributable to the Sprint merger or UScellular acquisition, which are not reflective of T-Mobile’s ongoing core business activities and are, therefore, excluded from Adjusted EBITDA and Core Adjusted EBITDA. Other, net, for the three months ended and year ended December 31, 2025, includes $390 million of severance and related costs associated with the 2025 workforce transformation.

26

T-Mobile US, Inc.

Reconciliation of Non-GAAP Financial Measures to GAAP Financial Measures (continued)

(Unaudited)

Net debt (excluding tower obligations) to the LTM Net income, LTM Adjusted EBITDA and LTM Core Adjusted EBITDA ratios are calculated as follows:

(in millions, except net debt ratios)

Mar 31, 2024

Jun 30, 2024

Sep 30, 2024

Dec 31, 2024

Mar 31, 2025

Jun 30, 2025

Sep 30, 2025

Dec 31, 2025

Short-term debt

$

5,356

$

5,867

$

5,851

$

4,068

$

8,214

$

6,408

$

6,333

$

5,135

Short-term financing lease liabilities

1,265

1,252

1,252

1,175

1,136

1,157

1,157

1,163

Long-term debt

71,361

70,203

72,522

72,700

76,033

75,018

76,365

79,649

Long-term debt to affiliates

1,496

1,496

1,497

1,497

1,497

1,497

1,498

1,498

Financing lease liabilities

1,163

1,133

1,185

1,151

1,117

1,188

1,186

1,107

Total debt (excluding tower obligations)

$

80,641

$

79,951

$

82,307

$

80,591

$

87,997

$

85,268

$

86,539

$

88,552

Less: Cash and cash equivalents

(6,708)

(6,417)

(9,754)

(5,409)

(12,003)

(10,259)

(3,310)

(5,598)

Net debt (excluding tower obligations)

$

73,933

$

73,534

$

72,553

$

75,182

$

75,994

$

75,009

$

83,229

$

82,954

Divided by: Last twelve months Net income

$

8,751

$

9,455

$

10,372

$

11,339

$

11,918

$

12,215

$

11,870

$

10,992

Net debt (excluding tower obligations) to LTM Net income Ratio

8.4

7.8

7.0

6.6

6.4

6.1

7.0

7.5

Divided by: Last twelve months Adjusted EBITDA

$

29,881

$

30,529

$

31,172

$

31,864

$

32,471

$

32,965

$

33,406

$

33,937

Net debt (excluding tower obligations) to LTM Adjusted EBITDA Ratio

2.5

2.4

2.3

2.4

2.3

2.3

2.5

2.4

Divided by: Last twelve months Core Adjusted EBITDA

$

29,681

$

30,372

$

31,047

$

31,771

$

32,412

$

32,926

$

33,384

$

33,924

Net debt (excluding tower obligations) to LTM Core Adjusted EBITDA Ratio

2.5

2.4

2.3

2.4

2.3

2.3

2.5

2.4

Adjusted Free Cash Flow and Adjusted Free Cash Flow margin are calculated as follows:

Quarter

Year Ended December 31,

(in millions, except percentages)

Q1 2024

Q2 2024

Q3 2024

Q4 2024

Q1 2025

Q2 2025

Q3 2025

Q4 2025

2024

2025

Net cash provided by operating activities (1)

$

5,084

$

5,521

$

6,139

$

5,549

$

6,847

$

6,992

$

7,457

$

6,654

$

22,293

$

27,950

Cash purchases of property and equipment, including capitalized interest

(2,627)

(2,040)

(1,961)

(2,212)

(2,451)

(2,396)

(2,639)

(2,469)

(8,840)

(9,955)

Proceeds related to beneficial interests in securitization transactions (1)

890

958

984

747

—

—

—

—

3,579

—

Adjusted Free Cash Flow

$

3,347

$

4,439

$

5,162

$

4,084

$

4,396

$

4,596

$

4,818

$

4,185

$

17,032

$

17,995

Net cash provided by operating activities margin

31.6

%

33.6

%

36.7

%

32.8

%

40.5

%

40.1

%

40.9

%

35.6

%

33.7

%

39.2

%

Adjusted Free Cash Flow margin

20.8

%

27.0

%

30.9

%

24.1

%

26.0

%

26.4

%

26.4

%

22.4

%

25.7

%

25.2

%

(1)Effective November 1, 2024, following amendments to the company’s Equipment Installment Plan Sale and Service Receivable Sale arrangements, all cash proceeds associated with the sale of such receivables, a portion of which was previously recognized as Proceeds related to beneficial interests in securitization transactions within investing cash flows, were recognized as operating cash flows. These amendments did not have a net impact on Adjusted Free Cash Flow.

27

T-Mobile US, Inc.

Reconciliation of Non-GAAP Financial Measures to GAAP Financial Measures (continued)

(Unaudited)

The guidance range for Adjusted Free Cash Flow is calculated as follows:

FY 2026

(in millions)

Guidance Range

Net cash provided by operating activities

$

28,000

$

28,700

Cash purchases of property and equipment, including capitalized interest

(10,000)

(10,000)

Adjusted Free Cash Flow

$

18,000

$

18,700

28

Definitions of Terms

Operating and financial measures are utilized by T-Mobile’s management to evaluate its operating performance and, in certain cases, its ability to meet liquidity requirements. Although companies in the telecommunications industry may not define measures in precisely the same way, T-Mobile believes the measures facilitate key operating performance comparisons with other companies in the telecommunications industry to provide management, investors and analysts with useful information to assess and evaluate past performance and assist in forecasting future performance.

1.Account - A billing account number that generates revenue. Postpaid accounts generally consist of customers that are qualified for postpaid service utilizing phones, 5G broadband gateways, fiber connections, mobile internet devices, including tablets and hotspots, wearables, DIGITS or other connected devices, including SyncUP and IoT, where they generally pay after receiving service.

2.Customer - A SIM number with a unique T-Mobile identifier which is associated with an account that generates revenue. Customers are qualified either for postpaid service utilizing phones, 5G broadband gateways, fiber connections, mobile internet devices, including tablets and hotspots, wearables, DIGITS or other connected devices, including SyncUP and IoT, where they generally pay after receiving service, or prepaid service, where they generally pay in advance of receiving service.

3.Churn - The number of customers whose service was deactivated as a percentage of the average number of customers during the specified period further divided by the number of months in the period. The number of customers whose service was deactivated is presented net of customers that subsequently have their service restored within a certain period of time and excludes customers who received service for less than a certain minimum period of time.

4.Postpaid Average Revenue Per Account (“ARPA”) - Average monthly postpaid service revenue earned per account. Postpaid service revenues for the specified period divided by the average number of postpaid accounts during the period, further divided by the number of months in the period.

Average Revenue Per User (“ARPU”) - Average monthly service revenue earned per customer. Service revenues for the specified period divided by the average number of customers during the period, further divided by the number of months in the period.

Postpaid phone ARPU excludes postpaid other customers and related revenues.

Service revenues - Postpaid, including handset insurance, prepaid, wholesale and other service revenues.

5.Cost of services - Costs directly attributable to providing wireless communications and broadband services, including direct switch and cell site costs, such as rent, network access and transport costs, utilities, maintenance, associated labor costs, long distance costs, regulatory program costs, roaming fees paid to other carriers and data content costs.

Cost of equipment sales - Costs of devices and accessories sold to customers and dealers, device costs to fulfill insurance and warranty claims, write-downs of inventory related to shrinkage and obsolescence, and shipping and handling costs.

Selling, general and administrative expenses - Costs not directly attributable to providing wireless communications and broadband services for the operation of sales, customer care and corporate activities. These include all commissions paid to dealers and retail employees for activations and upgrades, labor and facilities costs associated with retail sales force and administrative space, marketing and promotional costs, customer support and billing, bad debt expense and administrative support activities.

6.Net income margin - Net income divided by Service revenues.

7.Adjusted EBITDA and Core Adjusted EBITDA - Adjusted EBITDA represents earnings before Interest expense, net of Interest income, Income tax expense, Depreciation and amortization, stock-based compensation and Special Items. Core Adjusted EBITDA represents Adjusted EBITDA less device lease revenues. Core Adjusted EBITDA and Adjusted EBITDA are non-GAAP financial measures utilized by T-Mobile’s management, including our chief operating decision maker, to monitor the financial performance of our operations and allocate resources of the Company as a whole. T-Mobile historically used Adjusted EBITDA and T-Mobile currently uses Core Adjusted EBITDA internally as a measure to evaluate and compensate its personnel and management for their performance. T-Mobile uses Adjusted EBITDA and Core Adjusted EBITDA as benchmarks to evaluate its operating performance in comparison to competitors. Management believes analysts and investors use Core Adjusted EBITDA and Adjusted EBITDA as supplemental measures to evaluate overall operating performance and to facilitate comparisons with other wireless communications and broadband services companies because they are indicative of T-Mobile’s ongoing operating performance and trends by excluding the impact of Interest expense from financing, non-cash depreciation and amortization from capital investments, non-cash stock-based compensation and Special Items. Management believes analysts and investors use Core Adjusted EBITDA because it normalizes for the transition in the company’s device financing strategy, by excluding the impact of device lease revenues from Adjusted EBITDA, to align with the related depreciation expense on leased devices, which is excluded from the definition of Adjusted EBITDA. Core Adjusted EBITDA and Adjusted EBITDA have limitations as analytical tools and should not be considered in isolation or as a substitute for Income from operations, Net income or any other measure of financial performance reported in accordance with U.S. Generally Accepted Accounting Principles (“GAAP”).

8.Special Items - Certain expenses, gains, and losses which are not reflective of our ongoing performance. Special Items include Merger-related costs (gain), net, network restructuring initiative costs (as discussed above), certain legal-related recoveries and expenses, Impairment expense, restructuring costs not directly attributable to the Sprint merger or UScellular acquisition (including severance), and other non-core gains and losses.

9.Adjusted EBITDA margin and Core Adjusted EBITDA margin - Adjusted EBITDA margin is calculated as Adjusted EBITDA divided by Service revenues. Core Adjusted EBITDA margin is calculated as Core Adjusted EBITDA divided by Service revenues. Adjusted EBITDA margin and Core Adjusted EBITDA margin are non-GAAP financial measures utilized by T-Mobile’s management, including our chief operating decision maker, to monitor the financial performance of our operations and allocate resources of the Company as a whole.

10.Net cash provided by operating activities margin - Net cash provided by operating activities margin is calculated as Net cash provided by operating activities divided by Service revenues.

11.Adjusted Free Cash Flow - Net cash provided by operating activities less cash payments for purchases of property and equipment, plus proceeds related to beneficial interests in securitization transactions. Adjusted Free Cash Flow is utilized by T-Mobile’s management, investors, and analysts of our financial information to evaluate cash available to pay debt, repurchase shares, pay dividends and provide further investment in the business.

29

12.Adjusted Free Cash Flow margin - Adjusted Free Cash Flow margin is calculated as Adjusted Free Cash Flow divided by Service revenues. Adjusted Free Cash Flow margin is utilized by T-Mobile’s management, investors, and analysts to evaluate the company’s ability to convert service revenue efficiently into cash available to pay debt, repurchase shares, pay dividends and provide further investment in the business.

13.Net debt - Short-term debt, short-term debt to affiliates, long-term debt (excluding tower obligations), and long-term debt to affiliates, short-term financing lease liabilities and financing lease liabilities, less cash and cash equivalents.

14.Merger-related costs include Sprint merger-related costs and UScellular merger-related costs.

15.Sprint merger-related costs include:

•Integration costs to achieve efficiencies in network, retail, information technology and back office operations, migrate customers to the T-Mobile network and billing systems and the impact of legal matters assumed as part of the Sprint merger;

•Restructuring costs, including severance, store rationalization and network decommissioning; and

•Transaction costs, including legal and professional services related to the completion of the Sprint merger and the acquisitions of affiliates.

16.UScellular merger-related costs to date include:

•Integration costs to achieve efficiencies in network, retail, information technology and back office operations and migrate customers to the T-Mobile network and billing systems;

•Restructuring costs, including contract terminations, severance and network decommissioning; and

•Transaction costs, including legal and professional services related to the completion of the UScellular acquisition.

This communication includes forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995. All statements other than statements of historical fact, including information concerning T-Mobile US, Inc.’s future results of operations, are forward-looking statements. These forward-looking statements are generally identified by the words “anticipate,” “believe,” “estimate,” “expect,” “intend,” “may,” “could” or similar expressions. Forward-looking statements are based on current expectations and assumptions, which are subject to risks and uncertainties and may cause actual results to differ materially from the forward-looking statements. Important factors that could affect future results and cause those results to differ materially from those expressed in the forward-looking statements include, among others, the following: competition, industry consolidation and changes in the market for wireless communications services and other forms of connectivity; cyberattacks, disruptions, data loss or other security breaches; our inability to adopt and deploy network technologies in a timely and effective manner; our inability to effectively execute our digital transformation and drive customer and employee adoption of emerging technologies; our inability to retain or motivate key personnel, hire qualified personnel or maintain our corporate culture; system failures and business disruptions, allowing for unauthorized use of or interference with our network and other systems; the scarcity and cost of additional wireless spectrum, and regulations relating to spectrum use; the timing and effects of any pending and future acquisition, investment, joint venture, merger or divestiture involving us, including our inability to obtain any required regulatory approval necessary to consummate any such transactions or to achieve the expected benefits of such transactions; adverse economic, political or market conditions in the U.S. and international markets, including changes resulting from increases in inflation or interest rates, tariffs and trade restrictions, supply chain disruptions, fluctuations in global currencies, immigration policies, and impacts of geopolitical instability, such as the Ukraine-Russia and Israel-Hamas wars and further escalations thereof; potential operational delays, higher procurement and operational costs, and increased regulatory and compliance complexities as result of changes to trade policies, including higher tariffs, restrictions and other economic disincentives to trade; our inability to successfully deliver new products and services; any disruption or failure of our third parties (including key suppliers) to provide products or services for the operation of our business; sociopolitical volatility and polarization and risks related to environmental, social and governance matters; our substantial level of indebtedness and our inability to service our debt obligations in accordance with their terms; changes in the credit market conditions, credit rating downgrades or an inability to access debt markets; our inability to maintain effective internal control over financial reporting; compliance with the current regulatory framework, including our national security obligations, and any changes in regulations or in the regulatory framework under which we operate; laws and regulations relating to the handling of privacy, data protection and artificial intelligence; unfavorable outcomes of and increased costs from existing or future regulatory or legal proceedings; difficulties in protecting our intellectual property rights or if we infringe on the intellectual property rights of others; our offering of regulated financial services products and exposure to a wide variety of state and federal regulations; new or amended tax laws or regulations or administrative interpretations and judicial decisions affecting the scope or application of tax laws or regulations; our wireless licenses, including those controlled through leasing agreements, are subject to renewal and may be revoked; our exclusive forum provision as provided in our Certificate of Incorporation; interests of Deutsche Telekom AG (“DT”), our controlling stockholder, which may differ from the interests of other stockholders; our current and future stockholder return programs may not be fully utilized, and our share repurchases and dividend payments pursuant thereto may fail to have the desired impact on stockholder value; future sales of our common stock by DT and SoftBank Group Corp. and our inability to attract additional equity financing outside the United States due to foreign ownership limitations by the Federal Communications Commission; and other risks as disclosed in our most recent annual report on Form 10-K, and subsequent Forms 10-Q and other filings with the Securities and Exchange Commission. Given these risks and uncertainties, readers are cautioned not to place undue reliance on such forward-looking statements. We undertake no obligation to revise or publicly release the results of any revision to these forward-looking statements, except as required by law.

About T-Mobile US, Inc.

As the supercharged Un-carrier, T-Mobile US, Inc. (NASDAQ: TMUS) is powered by an award-winning 5G network that connects more people, in more places, than ever before. With T-Mobile’s unique value proposition of best network, best value and best experiences, the Un-carrier is redefining connectivity and fueling competition while continuing to drive the next wave of innovation in wireless and beyond. Headquartered in Bellevue, Wash., T-Mobile provides services through its subsidiaries and operates its flagship brands, T-Mobile, Metro by T-Mobile and Mint Mobile. For more information, visit https://www.t-mobile.com.