.2

IRRAS HOLDINGS, INC. AND SUBSIDIARIES

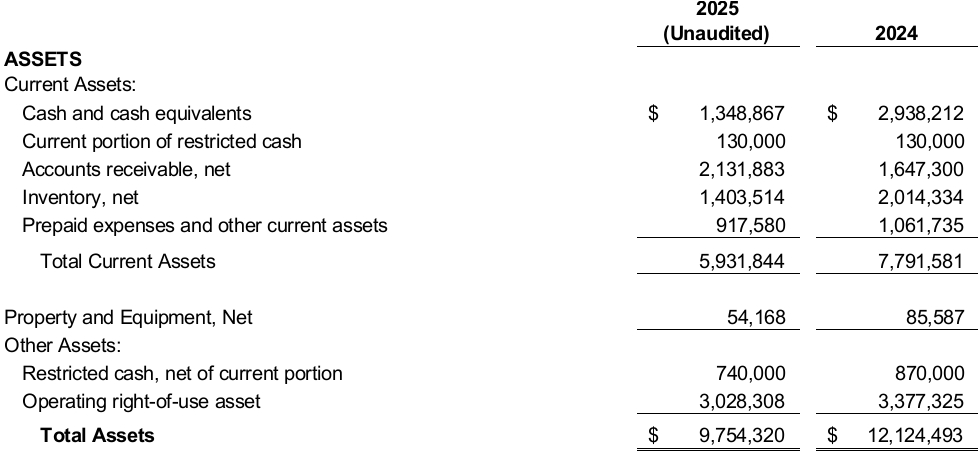

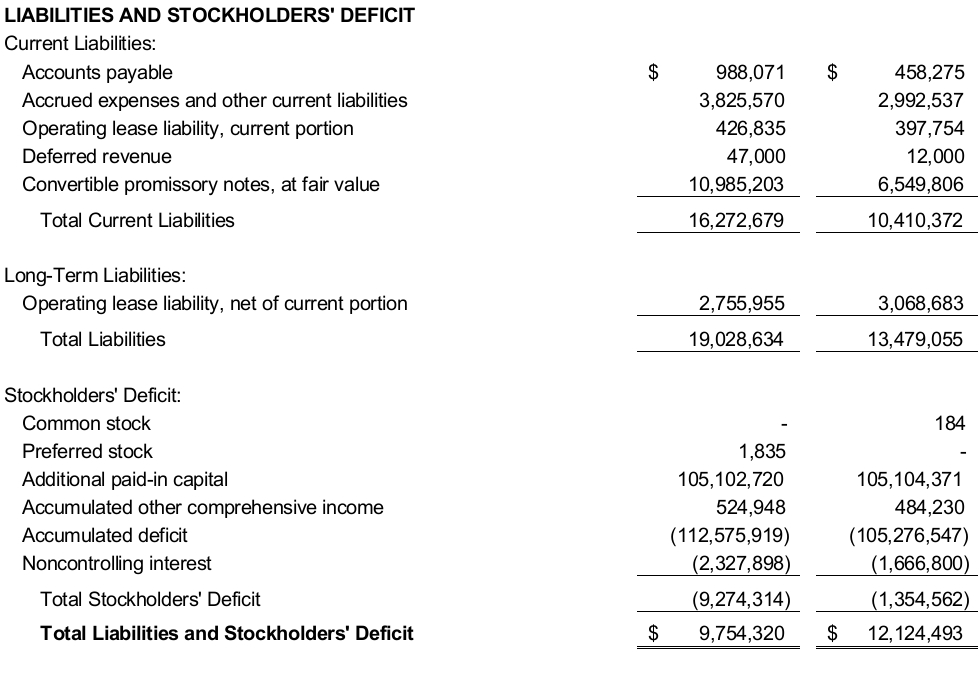

CONSOLIDATED BALANCE SHEETS

AS OF SEPTEMBER 30, 2025 (UNAUDITED) AND DECEMBER 31, 2024

The accompanying notes to the consolidated financial statements are an integral part of these statements.

1

IRRAS HOLDINGS, INC. AND SUBSIDIARIES

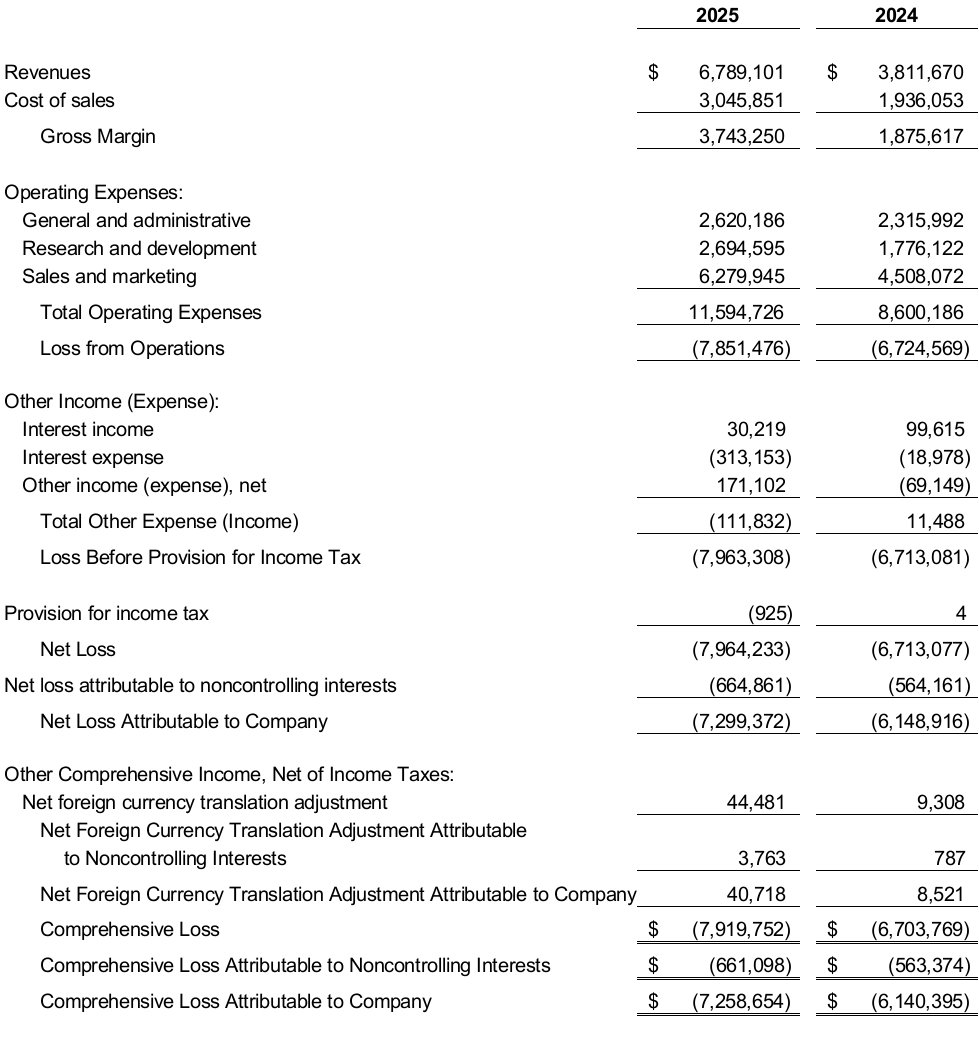

CONSOLIDATED STATEMENTS OF OPERATIONS AND COMPREHENSIVE INCOME

FOR THE NINE MONTHS ENDED SEPTEMBER 30, 2025 AND SEPTEMBER 30, 2024 (UNAUDITED)

The accompanying notes to the consolidated financial statements are an integral part of these statements.

2

IRRAS HOLDINGS, INC. AND SUBSIDIARIES

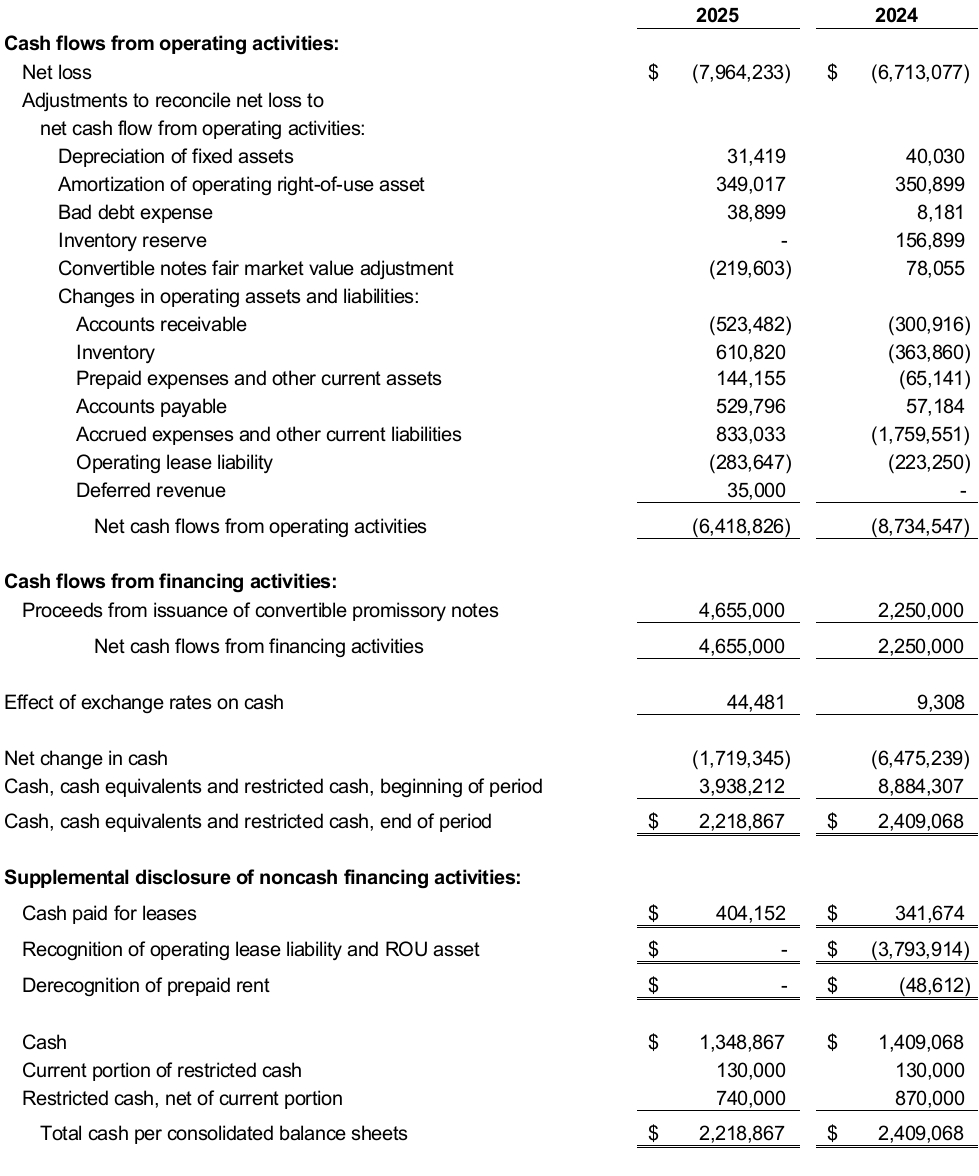

CONSOLIDATED STATEMENTS OF CASH FLOWS

FOR THE NINE MONTHS ENDED SEPTEMBER 30, 2025 AND SEPTEMBER 30, 2024 (UNAUDITED)

The accompanying notes to the consolidated financial statements are an integral part of these statements.

3

IRRAS HOLDINGS, INC. AND SUBSIDIARIES

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

SEPTEMBER 30, 2025 (UNAUDITED) AND DECEMBER 31, 2024

Note 1—Description of business

Nature of Business and Basis of Consolidation – The consolidated financial statements of IRRAS Holdings, Inc. and Subsidiaries (together the “Company”) include the accounts of IRRAS Holdings, Inc. (“IRRAS Holdings”), IRRAS AB (“IRRAS AB”), IRRAS USA, Inc. (“IRRAS USA”), and IRRAS GmbH (“IRRAS GmbH”).

IRRAS Holdings was originally incorporated as IR Holding Bidco Inc. as a Delaware corporation on June 26, 2023, for the purpose of acquiring control of IRRAS AB. In January 2024, IR Holding Bidco Inc. changed its name to IRRAS Holding, Inc. IRRAS Holdings owns 91.5% of the equity interests in IRRAS AB. IRRAS Holdings does not conduct business operations, outside of its ownership interests in IRRAS AB.

IRRAS AB was organized as a Sweden company on November 21, 2011. IRRAS AB owns 100% of the equity interests of IRRAS USA and IRRAS GmbH.

IRRAS USA was organized as a Delaware corporation on July 29, 2016, and is the entity that conducts business operations. The Company is located in San Diego, California. The Company is a commercial medical technology company focused on neurocritical care, with an emphasis on treatments for intracerebral hemorrhage, intraventricular hemorrhage, and other conditions requiring intracranial fluid management. The Company’s cornerstone product is the IRRAflow system, an FDA-cleared and CE-marked platform which integrates continuous irrigation, drainage, and real-time intracranial pressure monitoring.

IRRAS GmbH was organized as a Germany company on July 14, 2016. IRRAS GmbH does not conduct business operations and was dissolved during the period ended September 30, 2025.

Risks and Uncertainty – The Company is subject to a number of risks and uncertainties common to biotechnology companies including competition from larger and more established companies, marketing of its products, and the uncertainty of future profitability. The Company has negative cash flows from operations of $6,418,826 for the nine months ended September 30, 2025, and has an accumulated deficit of $112,575,919 as of September 30, 2025. Operating results in the future could vary from the amounts derived from management’s estimates and assumptions. Management has considered whether there is substantial doubt about its ability to continue as a going concern. Management believes the current cash balance, forecasted cash flows from operations, and funding from ClearPoint Neuro, Inc. (“ClearPoint”) which acquired the Company during November 2025, see Note 10, as necessary, are sufficient to finance the Company’s continued operations for at least one year from the date of issuance of these consolidated financial statements and these consolidated financial statements have been prepared assuming that the Company will continue as a going concern.

Note 2—Summary of significant accounting policies

Principles of Consolidation – The consolidated financial statements include the accounts of IRRAS Holdings and its subsidiaries. All significant intercompany transactions and balances have been eliminated in consolidation.

4

IRRAS HOLDINGS, INC. AND SUBSIDIARIES

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

SEPTEMBER 30, 2025 (UNAUDITED) AND DECEMBER 31, 2024

Note 2—Summary of significant accounting policies (continued)

Basis of Presentation – In the opinion of management, the accompanying unaudited condensed consolidated financial statements have been prepared on a basis consistent with the Company’s December 31, 2024 audited financial statements, and include all adjustments, consisting of only normal recurring adjustments, necessary to fairly state the information set forth therein. These condensed consolidated financial statements have been prepared in accordance with SEC rules for interim financial information, and, therefore, omit certain information and footnote disclosures necessary to present such statements in accordance with accordance with accounting principles generally accepted in the United States (“U.S. GAAP”). The preparation of these condensed consolidated financial statements in conformity with U.S. GAAP requires management to make estimates and assumptions that affect the reported amounts of assets, liabilities, revenue, expenses and the related disclosures at the date of the financial statements and during the reporting period. Actual results could materially differ from these estimates. These condensed consolidated financial statements should be read in conjunction with the audited financial statements and notes thereto. The accompanying condensed balance sheet as of December 31, 2024 has been derived from the audited financial statements at that date but does not include all information and footnotes required by U.S. GAAP for a complete set of financial statements. The results of operations for the nine months ended September 30, 2025, may not be indicative of the results to be expected for the entire year or any future periods.

The consolidated financial statements include accounts of the following companies:

|

|

Form of Entity |

|

Ownership |

|

Domiciled |

IRRAS Holdings: |

|

Corporation |

|

|

|

Delaware |

IRRAS AB: |

|

Limited liability company |

|

91.5% |

|

Sweden |

IRRAS USA: |

|

Corporation |

|

100% |

|

Delaware |

IRRAS GmbH: |

|

Limited liability company |

|

100% |

|

Germany |

Use of Estimates – The preparation of consolidated financial statements in conformity with U.S. GAAP requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the consolidated financial statements and the reported amounts of revenues and expenses during the reporting period. Actual results can differ from these estimates.

Cash, Cash Equivalents, and Restricted Cash – For purposes of the consolidated financial statement presentation, the Company considers all highly liquid instruments with original maturities of three months or less to be cash equivalents. The Company has cash pledged as collateral related to their operating lease which is classified as restricted cash. Amounts related to the cash pledged as collateral expected to be released within twelve months of the accompanying consolidated balance sheet is classified as a current asset.

Accounts Receivable – The Company accounts for trade receivables by adjusting the outstanding principal through charge offs and maintaining an allowance for credit losses which reserves for expected credit losses. In determining the amount of the allowance, the Company considers factors such as historical experience, creditworthiness, the age of the trade receivable balances, current economic conditions, customer-specific information and reasonable and supportable forecasts of future economic conditions. The Company makes judgments about the creditworthiness of significant customers based on ongoing credit evaluation. When the Company determines the amounts are fully uncollectible, they are written off against the allowance. Gross accounts receivable totaled $2,193,324, $1,669,842, $1,501,842, and $1,165,705 as of September 30, 2025, January 1, 2025, September 30, 2024, and January 1, 2024, respectively.

As of September 30, 2025, September 30, 2024, and December 31, 2024, the allowance for credit losses totaled $61,441, $63,310, and $22,542, respectively. There were no uncollectable trade accounts receivable written-off during the nine months ended September 30, 2025 or the year ended December 31, 2024.

5

IRRAS HOLDINGS, INC. AND SUBSIDIARIES

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

SEPTEMBER 30, 2025 (UNAUDITED) AND DECEMBER 31, 2024

Note 2—Summary of significant accounting policies (continued)

Inventory – Inventory, which consist of raw materials, work in process, and finished goods available for sale, is recorded at standard cost. The standard cost is re-evaluated on a quarterly basis and adjusted if underlying assumptions change, and is valued at the lower of cost or net realizable value. This valuation requires the Company to make judgments, based on currently available information, about the likely method of disposition, and expected recoverable value of each disposition category. The inventory valuation allowance was $46,607 and $46,595 as of September 30, 2025 and December 31, 2024, respectively.

Equipment, Furniture, and Depreciation – Property and equipment are stated at cost, less accumulated depreciation. Expenditures for betterments and major renewals are charged to the property and equipment accounts, while expenditures for maintenance, repairs and minor improvements are charged to expense. When assets are retired or otherwise disposed of, the assets and related accumulated depreciation are removed from the accounts, and any resulting gain or loss is reflected in operations. Depreciation is computed over the estimated useful lives of assets using the straight-line method. Estimated useful lives used for computing deprecation is three to five years.

Revenue Recognition – The Company derives their revenue from the sale of medical devices. In accordance with Accounting Standards Codification (“ASC”) 606, revenue is recognized upon the transfer of control of promised products to customers in amounts that reflect the consideration the Company expect to receive in exchange for those products.

The Company determines the amount of revenue to be recognized through the application of the following steps:

The Company generates revenue through the sale of products, with standard shipping terms and discounts. The Company’s revenue transactions consist of a single performance obligation to transfer promised goods. Quantities to be delivered to the customer are determined through orders received from the customer. The Company recognizes revenue when it has fulfilled the performance obligation, which is typically determined by the shipping terms. Revenue is measured as the amount of consideration the Company expects to receive in exchange for the transferred goods. Payment terms are consistent with terms standard to the market the Company serves. The Company does not offer warranties. All returns of non-disposable products must be approved by the Company.

Income Taxes – The Company accounts for income taxes under the asset and liability method, whereby deferred tax assets and liabilities are recorded for the future tax impact attributable to differences between the consolidated financial statements carrying amounts of existing assets and liabilities and their respective tax bases as well as expected benefits of utilizing net operating losses and credit carryforwards.

The Company measures deferred tax assets and liabilities using enacted tax rates that are expected to apply in the years in which the Company expects to recover or settle those temporary differences. The Company recognizes in income the effect of a change in tax rates on deferred tax assets and liabilities in the period that includes the enactment date.

6

IRRAS HOLDINGS, INC. AND SUBSIDIARIES

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

SEPTEMBER 30, 2025 (UNAUDITED) AND DECEMBER 31, 2024

Note 2—Summary of significant accounting policies (continued)

The Company recognizes the effect of income tax positions only if sustaining those positions is more likely than not. The Company reflects changes in recognition or measurement of uncertain tax positions in the period in which a change in judgment occurs. The Company recognizes interest and penalties, if any, related to uncertain tax positions within income tax expense. Accrued interest and penalties are included within the related tax liability line in the accompanying consolidated balance sheets.

The Company evaluates the need to establish a valuation allowance based upon expected levels of taxable income, future reversals of existing temporary differences, tax planning strategies and recent financial operations. The Company establishes a valuation allowance to reduce deferred tax assets to the extent it is more likely than not that some or all of the deferred tax assets will not be realized.

Advertising and Marketing – The Company expenses advertising and marketing costs as they are incurred. Total costs for the nine months ended September 30, 2025 and September 30, 2024 were $279,799 and $364,181, respectively, and are included in sales and marketing expense in the accompanying consolidated statements of operations and comprehensive loss.

Research and Development Costs – Expenditures for research and development activities include costs incurred for experimentation, design, and testing and are expensed as incurred. Research and development expense were $584,797 and $487,114 for the nine months ended September 30, 2025 and September 30, 2024, respectively, and are included in research and development expense in the accompanying consolidated statements of operations and comprehensive loss.

Lease Accounting Policy – The Company leases office space in San Diego, California. The Company determines whether a contract contains a lease at inception by determining if the contract conveys the right to control the use of identified property, plant, or equipment for a period of time in exchange for consideration. The Company has a lease agreement with lease and non-lease components, which are generally accounted for separately with amounts allocated to the lease and non-lease components based on relative stand-alone prices.

Operating right-of-use assets and operating lease liabilities are recognized at the commencement date based on the present value of the future minimum lease payments over the lease term. Renewal and termination clauses are factored into the determination of the lease term, if it is reasonably certain these options would be exercised by the Company. Lease assets are amortized over the lease term, unless there is a transfer of title or purchase option reasonably certain of exercise, in which case the asset life is used. In order to determine the present value of lease payments, the Company estimated their incremental borrowing rate to calculate lease assets and liabilities.

The Company’s lease agreements do not contain any material residual value guarantees or material restrictive covenants. The Company has no material obligation for leases signed but not yet commenced as of September 30, 2025. The Company does not have any sublease activities. The Company elected to apply the short-term lease measurement and recognition exemption to its leases where applicable.

Foreign Currency Translation Adjustments – IRRAS AB, located in Sweden, uses the local currency as its functional currency. The local currency was the Swedish Krona for the nine months ended September 30, 2025 and September 30, 2024. Assets and liabilities of IRRAS AB are translated to the reporting currency (U.S. dollars) based on the current exchange rate in effect at the consolidated balance sheet date. IRRAS AB income and expenses are translated at average rates for the year presented. IRRAS GmbH, located in Germany, uses the local currency as its functional currency. The local currency was the Euro during the periods for the nine months ended September 30, 2025 and September 30, 2024. Assets and liabilities of IRRAS GmbH are translated to the reporting currency (U.S. dollars) based on the current exchange rate in effect at the consolidated balance sheet date. IRRAS GmbH income and expenses are translated at average rates for the year presented.

7

IRRAS HOLDINGS, INC. AND SUBSIDIARIES

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

SEPTEMBER 30, 2025 (UNAUDITED) AND DECEMBER 31, 2024

Note 3—Equipment and furniture

Equipment and furniture consist of the following as of September 30, 2025 and December 31, 2024:

Note 4—Convertible promissory note

During 2024, the Company entered into convertible promissory notes (“Convertible Notes”) with certain investors in exchange for an aggregate principal amount of $6,330,203. The Convertible Notes accrue simple interest at a rate of 5% per annum and mature in October 2025, unless otherwise converted. The Convertible Notes are automatically convertible upon the completion of a qualified financing, as defined in the convertible promissory note agreements. The Convertible Notes convert into the same class and series of capital stock of the Company issued to other investors in qualified financing. The amount of shares received upon conversion is determined by dividing the unpaid principal amount plus related interest on the date of conversion by a conversion price equal to the lower of: (a) 65% of the price per share, or (b) the price per share that results when $34,000,000 is divided by the fully diluted capitalization as defined in the convertible promissory note agreements, as of immediately prior to the initial closing of such qualified financing. As of December 31, 2024, the principal balance of the Convertible Notes was $6,330,203.

During 2025, the Company obtained additional Convertible Notes with certain investors in exchange for an aggregate principal amount of $4,655,000. As of September 30, 2025, the principal balance of the Convertible Notes was $10,985,203.

Interest accrued on the Convertible Notes as of September 30, 2025 and December 31, 2024 were $378,028 and $68,727, respectively. Interest expense totaled $309,301 and $18,801 for the nine months ended September 30, 2025 and September 30, 2024, respectively.

In September 2025, the Company entered into an omnibus amendment to the Convertible Notes to extend the maturity date from October 1, 2025 to October 1, 2026.

The Company concluded that the Convertible Notes have an embedded derivative that did not require bifurcation and qualifies for the fair value option under current accounting guidance. The Company elected to account for the Convertible Notes using the fair value option, which requires the Company to record changes in fair value as a component of other income or expense. The fair value of the Convertible Notes as of September 30, 2025 and December 31, 2024 was $10,985,203 and $6,549,806, respectively, which resulted in the recognition of an other expense (income) of $(219,603) and $78,055 for the nine months ended September 30, 2025 and September 30, 2024, respectively, from the change in the fair value of the Convertible Notes on the Company’s accompanying consolidated statements of operations and comprehensive loss. The fair value of the Convertible Notes was estimated using the risky bond plus call coupled with a probability weighted expected return method.

8

IRRAS HOLDINGS, INC. AND SUBSIDIARIES

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

SEPTEMBER 30, 2025 (UNAUDITED) AND DECEMBER 31, 2024

Note 4—Convertible promissory note (continued)

The significant assumptions as of September 30, 2025 and December 31, 2024 are as follows:

Note 5—Capital structure

Conversion of Common Stock – In May 2025, all 1,835,095 outstanding shares of $0.0001 par value of the Company’s common stock were automatically converted into ten (10) validly issued, fully paid and non‑assessable shares of series seed preferred stock (the “Preferred Stock”) in accordance with the Company’s governing documents. As a result of this automatic conversion, all 1,835,095 outstanding shares of common stock were converted into 18,350,950 shares of Preferred Stock, each with a par value of $0.0001.

Common Stock – In accordance with the Company’s Amendment to Certificate of Incorporation (the “ARCI”) dated May 2, 2025, the Company is authorized to issue 22,000,000 shares of $0.0001 par value common stock. There were -0- and 184 shares of common stock issued and outstanding at September 30, 2025 and December 31, 2024, respectively.

Preferred Stock – In accordance with the ARCI, dated May 2, 2025, the Company is authorized to issue 18,350,950 shares of $0.0001 par value Preferred Stock.

The business and affairs of the Company shall be managed by or under the direction of the board of directors. The board of directors is expressly authorized to adopt, amend, alter, or repeal the by-laws of the Company.

The holders of Preferred Stock have various rights and preferences as follows.

Voting – The holders of Preferred Stock shall be entitled to cast the number of votes equal to the number of whole shares of common stock into which the shares of preferred could be converted as of the record date for determining stockholders entitled to vote.

Dividends – Except for distributions on common stock in the form of additional common stock or other securities and rights convertible into or entitling the holder thereof to receive additional shares of common stock, any dividend or distribution shall be distributed among all holders Preferred Stock in proportion to the number of shares of common stock that would be held by each such holder if all shares of Preferred Stock were converted to common stock at the then effective conversion rate, as defined in the ARCI.

Conversion – Each share of Preferred Stock shall be convertible, at the option of the holder thereof, at any time after the date of issuance of such shares, into such number of fully paid and non‑assessable shares of common stock as is determined by dividing (i) in the case of Preferred Stock, the series seed original issue price, as defined in the ARCI, by the series seed conversion price, as defined, both originally $1.194 per share.

9

IRRAS HOLDINGS, INC. AND SUBSIDIARIES

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

SEPTEMBER 30, 2025 (UNAUDITED) AND DECEMBER 31, 2024

Note 5—Capital structure (continued)

Liquidation – In the event of liquidation, the holders of each series of Preferred Stock shall be entitled to receive liquidation proceeds in preference to holders of the common stock. The holders of Preferred Stock shall be entitled to receive an amount equal to the sum of the applicable original issue price, as defined in the ARCI, for such series of Preferred Stock, plus declared but unpaid dividends on such shares. If upon any such liquidation, the proceeds available for distribution to the holders of Preferred Stock shall be insufficient to pay the stockholders the full amount to which they shall be entitled, the holders of Preferred Stock shall share ratably in any distributions of the proceeds available for distribution in proportion to the respective amounts which would otherwise be payable in respect of the shares held by them upon such distribution if all amounts payable on or with respect to such shares were paid in full.

Redemption – The Company’s Preferred Stock is not redeemable.

Note 6—Commitments and contingencies

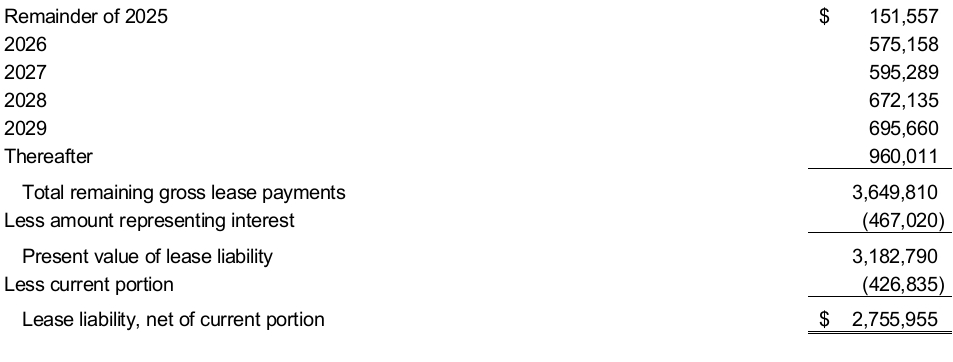

Operating Lease – In March 2023, the Company entered into an operating lease agreement for its U.S. office space in San Diego, California. The lease commencement date was January 1, 2024 (the “2023 Lease”). The 2023 Lease is set to expire in April 2031. The 2023 Lease contains provisions for free rent and future rent increases along with a $1,000,000 letter of credit subject to adjustments, as defined in the operating lease agreement.

Total fixed operating lease expense for the nine months ended September 30, 2025 and September 30, 2024 was $469,522 in both periods.

Future minimum payments under the operating lease as of September 30, 2025 are as follows:

As of September 30, 2025 and December 31, 2024, other information related to the leases was as follows:

10

IRRAS HOLDINGS, INC. AND SUBSIDIARIES

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

SEPTEMBER 30, 2025 (UNAUDITED) AND DECEMBER 31, 2024

Note 7—Income taxes

The components of income tax provision from continued operations for the nine months ended September 30, 2025 and September 30, 2024 are as follows:

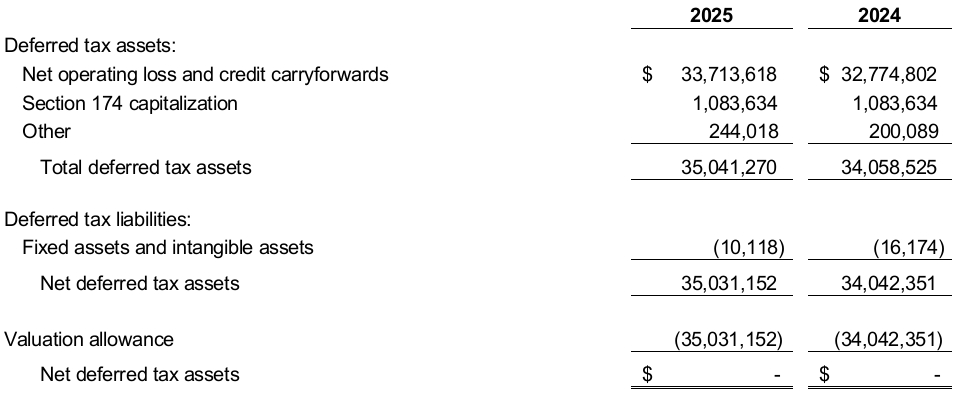

The significant components of deferred tax assets and liabilities as of September 30, 2025 and December 31, 2024 are as follows:

The Company has determined it is more likely than not that its deferred tax assets will not be realized. Accordingly, a valuation allowance has been recorded at September 30, 2025 and December 31, 2024 to fully offset the deferred tax asset of $35,031,152 and $34,042,351, respectively.

As of September 30, 2025, the Company had approximately $87,397,000 of net operating loss carryforwards available for federal tax purposes of which $86,682,000 were generated after 2017 and do not expire. As of September 30, 2025, the Company also had approximately $715,000 of net operating loss carryforwards that will begin to expire in 2036. As of September 30, 2025, the Company also had approximately $52,477,000 of net operating loss carryforwards in various states. The state net operating loss carryforwards begin to expire based on state specific rules. In addition, as of September 30, 2025, the Company had foreign net operating loss carryforwards which begin to expire in 2036.

11

IRRAS HOLDINGS, INC. AND SUBSIDIARIES

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

SEPTEMBER 30, 2025 (UNAUDITED) AND DECEMBER 31, 2024

Note 7—Income taxes (continued)

Utilization of the net operating loss carryforwards may be subject to a substantial annual limitation due to ownership change limitations that may have occurred or that could occur in the future, as required by Section 382 of the Internal Revenue Code of 1986, as amended, as well as similar state provisions. These ownership changes may limit the amount of the net operating loss carryover that can be utilized annually to offset future taxable income. In general, an "ownership change" as defined by Section 382 of the Code results from a transaction or series of transactions over a three-year period resulting in an ownership change of more than 50 percentage points of the outstanding stock of a company by certain stockholders.

The Company has not completed a study to assess whether an ownership change has occurred or whether there have been multiple ownership changes since the Company's formation due to the complexity and cost associated with such a study, and the fact that there may be additional such ownership changes in the future.

The Company has no unrecognized tax benefits. It is not anticipated that there will not be a significant change in unrecognized tax benefits over the next 12 months.

The Company and its subsidiaries are subject to U.S. federal and state income tax, and in the normal course of business, its income tax returns are subject to examination by the relevant taxing authorities. As of September 30, 2025, the 2020 – 2025 tax years remain subject to examination in the U.S. federal tax and various state tax jurisdictions. However, to the extent allowed by law, the taxing authorities may have the right to examine the period from inception through 2025 where net operating losses and income tax credits were generated and carried forward and make adjustments to the amount of the net operating loss and income tax credit carryforward amount. The Company is not currently under examination by federal or state jurisdictions.

The Company recorded deferred tax assets during the year related to net operating loss carryforwards and capitalized research costs under IRC 174. Because the Company does not have sufficient positive evidence to conclude that these deferred tax assets are realizable, the deferred tax assets were fully offset by a corresponding valuation allowance.

The Company has identified that Form 5471, Information Return of U.S. Persons With Respect to Certain Foreign Corporations, was not timely filed for certain foreign subsidiaries for prior tax years. Failure to file Form 5471 may subject the Company to penalties of up to $10,000 per form per year. The Company is currently evaluating its eligibility for relief under the reasonable cause provisions of the Internal Revenue Code. At this time, the Company cannot reasonably estimate the outcome or amount of any potential penalty assessment. Accordingly, no liability has been recorded related to this matter as of September 30, 2025 or December 31, 2024.

Note 8—401(k) plan

The Company maintains a 401(k) plan (the “Plan”) for all eligible employees. The Company has not made contributions to the Plan during the nine months ended September 30, 2025 and September 30, 2024.

Uninsured Cash – The Company maintains its cash in bank deposit accounts that, at times, may exceed federally insured limits. The Federal Deposit Insurance Corporation provides a $250,000 guarantee per depositor for accounts held at insured banks. At September 30, 2025, the Company had $1,060,231 uninsured bank deposits. Management believes the Company is not exposed to significant credit risk in these accounts.

12

IRRAS HOLDINGS, INC. AND SUBSIDIARIES

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

SEPTEMBER 30, 2025 (UNAUDITED) AND DECEMBER 31, 2024

Note 9—Concentrations

Major Customers – For the nine months ended September 30, 2025, two customers accounted for 25% of the Company’s sales. As of September 30, 2025, there were two customers who accounted for 25% of the Company’s accounts receivable.

Note 10—Subsequent events

The Company has evaluated all subsequent events through February 3, 2026, the date the consolidated financial statements were available to be issued and determined no additional subsequent events had occurred that would require disclosure in the consolidated financial statements, except as discussed below.

Issuance of Convertible Promissory Notes – During October and November 2025, the Company entered into convertible promissory notes for total proceeds of $3,030,000.

Squeeze-Out Payment – Immediately before the acquisition by ClearPoint Neuro, Inc. detailed below, the Company paid approximately $2,200,000 to complete the squeeze-out of the remaining minority shareholders of IRRAS AB.

Acquisition by ClearPoint Neuro, Inc. – On November 6, 2025, the Company entered into a Merger agreement with ClearPoint Neuro, Inc. (“ClearPoint”) whereby ClearPoint acquired the Company in an all-stock and cash transaction. Under the terms of the agreement, the Company’s stockholders will receive $5 million in cash and 1,325,000 shares of ClearPoint common stock at closing. As additional consideration for the Company’s stockholders, the merger agreement provides for ClearPoint to pay earnout consideration during three one-year earnout periods equal to 25% of net sales of certain the Company’s products above certain thresholds. All convertible notes and related interest noted above were automatically converted into common stock of IRRAS Holdings, Inc. immediately before the closing of the transaction.

13