Please wait

|

|

As filed with the Securities and Exchange Commission on [March 9, 2015] |

Registration No. 333-194396 |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

_____________________________

POST-EFFECTIVE AMENDMENT NO. 1

to

FORM S-1

REGISTRATION STATEMENT UNDER THE SECURITIES ACT OF 1933

_____________________________

|

|

Interline Brands, Inc. |

(Exact name of registrant as specified in its charter) |

_____________________________

|

|

Delaware |

(State or other jurisdiction of incorporation or organization) |

|

5070 |

(Primary Standard Industrial Classification Code Number) |

|

03-0542659 |

(I.R.S. Employer Identification No.) |

_____________________________

|

|

701 San Marco Boulevard |

Jacksonville, Florida 32207 |

(904) 421-1400 |

(Address, including zip code, and telephone number, including area code, of registrants' principal executive offices) |

|

Michael Agliata, Esq. |

Interline Brands, Inc. |

701 San Marco Boulevard |

Jacksonville, Florida 32207 |

(904) 421-1400 |

(Name, address, including zip code, and telephone number, including area code, of agent for service) |

_____________________________

|

|

Copies to: |

Stuart H. Gelfond, Esq. |

Fried, Frank, Harris, Shriver & Jacobson LLP |

One New York Plaza |

New York, New York 10004 |

(212) 859-8000 |

_____________________________

|

|

As soon as practicable after the effective date of this Registration Statement |

(Approximate date of commencement of proposed sale to the public) |

If any of the securities being registered on this form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box. ý

If this form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

If this form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act Registration Statement of the earlier effective registration statement for the same offering. o

If this form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

|

| | | | |

| Large accelerated filer o | | Accelerated filer o | |

| | | | |

| Non-accelerated filer ý (Do not check if smaller reporting company) | | Smaller reporting company o | |

_____________________________

CALCULATION OF REGISTRATION FEE

|

| | | | |

Title of each class of securities to be registered | Amount to be registered | Proposed maximum offering price per unit(1) | Proposed maximum aggregate offering price | Amount of registration fee |

10% / 10.75% Senior Notes Due 2018 | (1) | (1) | (1) | (1) |

| |

(1) | An indeterminate amount of securities are being registered hereby to be offered solely for market-making purposes by specified affiliates of the registrant. Pursuant to Rule 457(q) under the Securities Act of 1933, as amended, no filing fee is required. |

_____________________________

The registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the registrant shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until this Registration Statement shall become effective on such date as the Commission, acting pursuant to said Section 8(a), may determine.

The information in this prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This prospectus is not an offer to sell these securities and it is not soliciting an offer to acquire or exchange these securities in any state where the offer or sale is not permitted.

Subject to Completion, Dated March 9, 2015

Prospectus

Interline Brands, Inc.

$285,000,000

10% / 10.75% Senior Notes due 2018

_____________________________

The 10% / 10.75% senior notes due November 15, 2018 offered hereby, which we refer to as “the notes”, relate to an aggregate of $285,000,000 of 10% / 10.75% senior notes due November 15, 2018 that were originally issued on August 6, 2012.

We pay interest on the notes on January 15 and July 15 of each year. With respect to each interest payment other than the final interest payment made at stated maturity, which will be made in cash, we will be required to pay interest on the notes entirely in cash unless the conditions described in this prospectus are satisfied, in which case we will be entitled to pay, to the extent described herein, interest for such interest period by increasing the principal amount of the notes or issuing new notes (such increase or issuance being referred to herein as “PIK Interest”). Cash interest will accrue on the notes at the rate of 10% per annum, and PIK Interest will accrue on the notes at the rate of 10.75% per annum. The notes will mature on November 15, 2018. We have the option to redeem all or a portion of the notes at any time on or after November 15, 2014 at the redemption prices set forth in this prospectus plus accrued and unpaid interest.

The notes are our senior unsecured obligations and rank pari passu in right of payment with all of our existing and future senior debt, senior in right of payment to all of our existing and future subordinated debt and effectively subordinated to all of our existing and future secured indebtedness to the extent of the value of the collateral securing such obligations. The notes are not guaranteed by any of our subsidiaries and therefore are structurally subordinated to all existing and future indebtedness (including the Interline Brands, Inc., a New Jersey corporation (“Interline New Jersey”), asset-based senior secured revolving credit facility and existing notes) of, and other obligations and preferred stock of, our subsidiaries (other than indebtedness and other obligations owed to us).

We do not intend to list the notes on any securities exchange or seek approval for quotation through any automated trading system.

_____________________________

You should consider carefully the “Risk Factors” beginning on page 11 of this prospectus. Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

This prospectus has been prepared for and will be used by Goldman, Sachs & Co. in connection with offers and sales of the notes in market-making transactions. These transactions may occur in the open market or may be privately negotiated at prices related to prevailing market prices at the time of sales or at negotiated prices. Goldman, Sachs & Co. may act as principal or agent in these transactions. We will not receive any proceeds of such sales.

_____________________________

Goldman, Sachs & Co.

The date of this prospectus is , 2015.

TABLE OF CONTENTS

_____________________________

MARKET, RANKING AND OTHER DATA

The data included in this prospectus regarding markets and ranking are estimates based on our management’s knowledge and experience in the markets in which we operate, using various third party sources where available. We believe these estimates to be reliable as of their respective dates; however, no independent sources have verified such estimates. These estimates involve risks and uncertainties and are subject to change based on various factors, including those discussed under “Risk Factors” and “Special Note Regarding Forward-Looking Statements.” As a result, you should be aware that market, ranking and other similar data included in this prospectus, and estimates and beliefs based on that data, may not be reliable.

NON-GAAP FINANCIAL INFORMATION

In this prospectus, we present EBITDA, Adjusted EBITDA and Average Organic Daily Sales, which are “non-GAAP financial measures” that exclude amounts that are not excluded in the most directly comparable measure calculated and presented in accordance with accounting principles generally accepted in the United States (“U.S. GAAP”). We present EBITDA, Adjusted EBITDA and Average Organic Daily Sales herein because we believe these metrics to be relevant and useful information to our investors since they are consistently used by our management to evaluate the operating performance of our business and to compare our operating performance with that of our competitors. Management also uses EBITDA, Adjusted EBITDA and Average Organic Daily Sales for planning purposes, including the preparation of annual operating budgets, and to determine appropriate levels of operating and capital investments. We utilize EBITDA, Adjusted EBITDA and Average Organic Daily Sales as useful alternatives to net (loss) income and net sales as an indicator of our operating performance compared to our plan.

EBITDA, Adjusted EBITDA and Average Organic Daily Sales are not measures of financial performance under U.S. GAAP. Accordingly, EBITDA, Adjusted EBITDA and Average Organic Daily Sales should not be used in isolation or as substitutes for other measures of financial performance reported in accordance with U.S. GAAP, such as gross margin, operating income, net income, cash flows from operating, investing and financing activities or other income or cash flow statement data prepared in accordance with U.S. GAAP.

EBITDA is defined as net (loss) income adjusted to:

| |

• | exclude interest expense, net of interest income; |

| |

• | exclude (benefit) provision for income taxes; and |

| |

• | exclude depreciation and amortization. |

Adjusted EBITDA is defined as EBITDA adjusted to:

| |

• | exclude Merger related expenses associated with the acquisition of the Company by affiliates of GS Capital Partners and P2 Capital Partners; |

| |

• | exclude share-based compensation, which is comprised of non-cash compensation expense arising from the grant of equity incentive awards; |

| |

• | exclude impairment of other intangible assets, which is comprised of excess carrying value over fair value for certain trademark assets determined to have a definite life during 2014; |

| |

• | exclude loss on extinguishment of debt, net, which is comprised of net losses associated with specific significant financing transactions, such as writing off the deferred financing costs associated with refinancing previous credit facilities and indentures as well as tender premiums and transaction costs associated with refinancing previous indentures; |

| |

• | exclude distribution center consolidations and restructuring costs, which are comprised of facility closing costs, such as lease termination charges, property and equipment write-offs and headcount reductions, incurred as part of the rationalization of our distribution network, as well as employee separation costs, such as severance charges, incurred as part of a restructuring; |

| |

• | exclude acquisition-related costs, which includes our direct acquisition-related expenses, including legal, accounting and other professional fees and expenses arising from acquisitions, as well as severance charges and stay bonuses, offset by the fair market value adjustments to earn-outs; |

| |

• | exclude litigation related costs associated with the class action lawsuit filed by Craftwood Lumber Company in 2011 and other nonrecurring litigation related costs; and |

| |

• | exclude the non-cash impact on rent expense associated with the effect of straight-line rent expense on leases. |

We believe EBITDA and Adjusted EBITDA allow management and investors to evaluate our operating performance without regard to the adjustments described above which can vary from company to company depending upon the acquisition history, capital intensity, financing options and the method by which its assets were acquired. While adjusting for these items limits the usefulness of these non-GAAP measures as performance measures because they do not reflect all the related expenses we incurred, we believe adjusting for these items and monitoring our performance with and without them helps management and investors more meaningfully evaluate and compare the results of our operations from period to period and to those of other companies. Actual results could differ materially from those presented. We believe these items for which we are adjusting are not indicative of our core operating results. These items impacted net income over the periods presented, which makes direct comparisons between years less meaningful and more difficult without adjusting for them. While we believe that some of the items excluded in the calculation of EBITDA and Adjusted EBITDA are not indicative of our core operating results, these items did impact our income statement during the relevant periods, and management therefore utilizes EBITDA and Adjusted

EBITDA as operating performance measures in conjunction with other measures of financial performance under U.S. GAAP such as net income. For a reconciliation of EBITDA and Adjusted EBITDA to the most directly comparable U.S. GAAP financial measure, which is net (loss) income, see “Summary—Summary Historical Consolidated Financial Data” and “Selected Historical Consolidated Financial Data.”

Average Organic Daily Sales is defined as sales for a period of time divided by the number of shipping days in that period of time excluding any sales from acquisitions made subsequent to the beginning of the prior year period.

Average Organic Daily Sales is presented herein because we believe it to be relevant and useful information to our investors since it is used by our management to evaluate the operating performance of our business, as adjusted to exclude the impact of acquisitions, and to compare our organic operating performance with that of our competitors. However, Average Organic Daily Sales is not a measure of financial performance under U.S. GAAP and it should be considered in addition to, but not as a substitute for, other measures of financial performance reported in accordance with U.S. GAAP, such as net sales. Management utilizes Average Organic Daily Sales as an operating performance measure in conjunction with U.S. GAAP measures such as net sales. For a reconciliation of Average Organic Daily Sales to the most directly comparable U.S. GAAP financial measure, which is net sales, see “Management’s Discussion and Analysis of Financial Condition and Results of Operations.”

PART I

PROSPECTUS SUMMARY

This summary provides an overview of selected information and does not contain all the information you should consider. Before making a decision to invest in the notes, you should carefully read the entire prospectus, including the sections of this prospectus entitled “Risk Factors,”“Use of Proceeds,” “Capitalization,” “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and the historical financial statements of Interline Brands, Inc., and the related notes appearing elsewhere in this prospectus before deciding whether to invest in the notes.

Unless otherwise indicated or as the context otherwise requires, in this prospectus, (i) the “Issuer” refers to Interline Brands, Inc., a Delaware corporation, the issuer of the notes; (ii) “Interline New Jersey” refers to Interline Brands, Inc., a New Jersey corporation, a subsidiary of the Issuer; (iii) the “Company,” “Interline Brands,” “we,” “us” and “our” refer to the Issuer and its consolidated subsidiaries; and (iv) “Sponsors” refers to GS Capital Partners VI Fund, L.P. and its related entities and P2 Capital Partners, LLC and its related entities, collectively.

Business

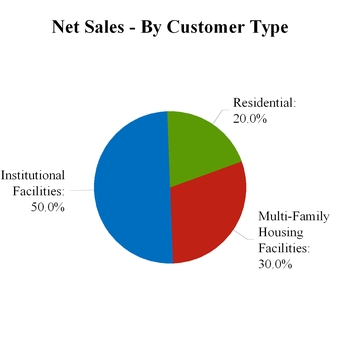

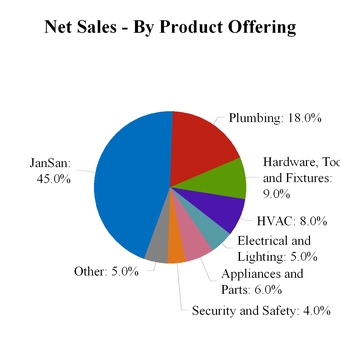

We are a leading national distributor and direct marketer of broad-line maintenance, repair and operations ("MRO") products. We have one operating segment, the distribution of MRO products into the facilities maintenance end-market. We stock approximately 100,000 MRO products in the following categories: janitorial and sanitation ("JanSan"); plumbing; heating, ventilation and air conditioning ("HVAC"); hardware, tools and fixtures; electrical and lighting; appliances and parts; security and safety; and other miscellaneous maintenance products. Our products are primarily used for the repair, maintenance, remodeling, and refurbishment of non-industrial, commercial, multi-family and residential facilities.

Our diverse facilities maintenance customer base includes institutions, such as educational, lodging, health care, and government facilities; multi-family housing, such as apartment complexes; and residential, such as professional contractors, and plumbing and hardware retailers. Our customers range in size from individual contractors and independent hardware stores to apartment management companies and national purchasing groups.

The following charts illustrate the approximate percentage of our net sales by customer type and product offerings for the year ended December 26, 2014:

We currently market and sell our products primarily through thirteen distinct and targeted brands, each of which is recognized in the facilities maintenance market they serve for providing quality products at competitive prices with reliable same-day or next-day delivery. The AmSan®, JanPak® , CleanSource®, Sexauer®, and Trayco® brands generally serve our institutional facilities customers; the Wilmar® and Maintenance USA® brands generally serve our multi-family housing facilities customers; and the Barnett®, Copperfield®, U.S. Lock®, Hardware Express®, LeranSM and AF Lighting® brands

generally serve our residential facilities customers. Our multi-brand operating model, which we believe is unique in the industry, allows us to use a single platform to deliver tailored products and services to meet the individual needs of each respective customer group served. During the second quarter of 2014, management made a strategic marketing decision to simplify our brand structure for our institutional customer base during 2015. This rebranding initiative is designed to consolidate our institutional brands under a single national brand name and increase brand awareness as a market leading institutional business.

We reach our markets using a variety of sales channels, including a field sales force of approximately 1,160 associates, which includes sales management and related associates, approximately 470 inside sales and customer service and support associates, a direct marketing program consisting of catalogs and promotional flyers, brand-specific websites, a national accounts sales program, and other supply chain programs, such as vendor managed inventory. We deliver our products through our network of 67 distribution centers and 21 professional contractor showrooms located throughout the United States ("U.S."), Canada, and Puerto Rico, 72 vendor-managed inventory locations at large customer locations and a dedicated fleet of trucks and third party carriers. Our broad distribution network enables us to provide reliable, next-day delivery service to approximately 98% of the U.S. population and same-day delivery service to most major metropolitan markets in the U.S.

The following map depicts the location of our primary distribution centers as of December 26, 2014(1).

_____________________________

(1) Distribution Centers not shown on map: Mississauga, Ontario and Bayamon, Puerto Rico.

Our information technology and logistics platforms support our major business functions, allowing us to market and sell our products with same-day or next-day delivery depending on the customer’s service requirements. While we market our products under a variety of brands, generally our brands draw from the same inventory within common distribution centers and share associated employee and transportation costs. In addition, we have centralized marketing, purchasing and catalog production operations to support our brands. We believe that our information technology and logistics platforms also benefit our customers by allowing us to offer a broad product selection at highly competitive prices while maintaining the unique customer appeal, market expertise and service capabilities of each of our targeted brands. Overall, we believe that our common operating platforms have enabled us to improve customer service, maintain lower operating costs, efficiently manage working capital and support our growth initiatives.

Strategy

Our objective is to become the leading supplier of MRO products to the facilities maintenance end-market, which is comprised of our institutional, multi-family housing and residential facilities customers. In pursuing this objective, we plan to increase our net sales, earnings and return on invested capital by capitalizing on our size and scale, sales force, supply chain programs, information technology and logistics platforms to successfully execute our organic growth, operating efficiency and strategic acquisition initiatives.

• Organic Growth Initiatives. We seek to satisfy and solve key customer supply chain needs, which enables us to further penetrate the markets we serve, and to expand into new product and geographic areas by adding sales professionals, and utilizing and increasing our already successful new product and marketing strategies, including: growing web-based sales capabilities; targeting new customer acquisitions; expanding our national accounts program; increasing customer use of our supply chain management services; continuing to develop proprietary products under our exclusive brands; and selectively adding new products and new categories to our various brand offerings.

• Increased Operating Efficiencies. We will continue to focus on enhancing our operating efficiency, which will increase profitability, improve our cash conversion cycle and increase our return on capital.

• Acquisitions. We will continue to maintain a disciplined acquisition strategy of adding new customers and/or product offerings in markets we currently serve and pursuing acquisitions of established brands in new or existing markets in an effort to further leverage our operating infrastructure.

Industry and Market Overview

The MRO distribution industry in the U.S. and Canada is approximately $525 billion in size according to MRO market analyses by Modern Distribution Management ("MDM"), a trade company specializing in wholesale distribution, and Industrial Marketing Information, Inc. ("IMI"), a market research company specializing in quantification of the industrial business-to-business markets. The MRO distribution industry encompasses the supply of a wide range of products, including plumbing and electrical supplies, hand-tools, janitorial supplies, safety equipment and many other categories. Customers served by the MRO distribution industry include heavy industrial manufacturers that use MRO supplies for the repair and overhaul of production equipment and machinery; owners and managers of facilities such as apartment complexes, office buildings, schools, hotels and hospitals that use MRO supplies largely for maintenance, repair and refurbishment; and professional contractors.

Within the MRO distribution industry, we focus on serving customers in the facilities maintenance end-market. Our customers are primarily engaged in the repair, maintenance, remodeling, refurbishment and, to a lesser extent, construction of non-industrial and residential facilities.

The Transactions

On May 29, 2012, Interline Brands entered into an Agreement and Plan of Merger (the “Merger Agreement”) with Isabelle Holding Company LLC (formerly known as Isabelle Holding Company Inc.) (“Parent”) and Isabelle Acquisition Sub Inc. (“Merger Sub”). On September 7, 2012, pursuant to the Merger Agreement, Merger Sub merged with and into Interline Brands, with Interline Brands continuing as the surviving corporation (the “Merger”). Immediately following the completion of the Merger, Parent was merged with and into Interline Brands, with Interline Brands as the surviving entity. In connection with the closing of the Merger, certain members of management purchased shares of common stock of Interline Brands.

The Merger was financed using the proceeds of (i) $365.0 million of debt financing from the issuance of the 10% / 10.75% senior notes due 2018 (the “HoldCo Notes”), (ii) $350.9 of equity capital from the Sponsors and certain members of management, (iii) $107.6 million of available cash from operations, and (iv) $80.0 of drawings under a new senior secured asset-based revolving credit facility (the “ABL Facility”). In addition, in connection with the Merger, Interline New Jersey engaged in a successful consent solicitation to make certain amendments to the terms of our OpCo Notes due 2018 (the "OpCo Notes"). We refer to the Merger, the financing thereof, the consent solicitation and the related transactions collectively as the “Transactions.”

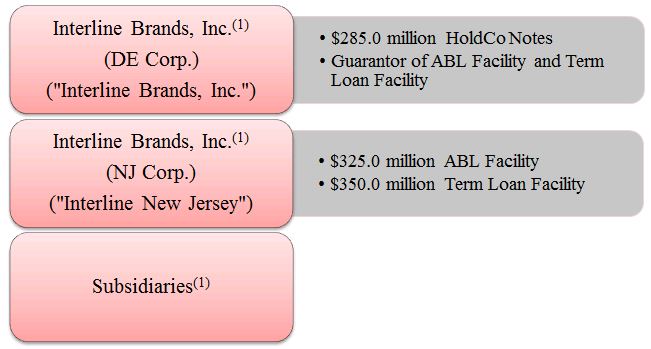

Corporate Structure

The following diagram illustrates our corporate structure and the aggregate principal amount of indebtedness outstanding as of December 26, 2014. The diagram does not display all of our subsidiaries.

_____________________________

| |

(1) | Interline Brands, along with certain domestic subsidiaries, guarantee Interline New Jersey’s Term Loan Facility and guarantees the ABL Facility. Neither Interline New Jersey nor any of our other subsidiaries guarantee the notes offered hereby, and as a result have no contractual obligations with respect thereto. |

Recent Developments

On December 30, 2014, the Company used a combination of cash on hand and borrowings under the recently amended ABL Facility to redeem $80.0 million of the $365.0 million outstanding aggregate principal amount of the HoldCo Notes at a redemption price of 105% of the outstanding aggregate principal amount to be redeemed, plus accrued and unpaid interest through the redemption date. In connection with the redemption of the HoldCo Notes, the Company recorded a loss on early extinguishment of debt in the amount of $6.6 million which will be included in the statement of operations for the three months ended March 27, 2015. The loss was comprised of $4.0 million in tender premium and related transactions costs and the write-off of the unamortized deferred debt issuance costs of $2.6 million. As a result of this transaction, $285.0 million of the HoldCo Notes are outstanding as of the date of this prospectus.

Our Sponsors

GS Capital Partners LP

Since 1986, the Goldman Sachs Merchant Banking Division ("MBD") has raised $94 billion of fund capital (including leverage) for Corporate Equity and Credit investing. A global leader in private corporate equity investing, MBD focuses on large, high quality companies with strong management in order to fund acquisition or expansion across a range of industries and geographies. Within Corporate investing, of which GS Capital Partners is a part, MBD has invested approximately $95 billion through a combination of external investment funds and firm capital. GS Capital Partners VI fund, the sixth in a series of global diversified private equity funds formed since 1992, was formed in 2007 with $20.3 billion in commitments. Founded in 1869, Goldman Sachs is a leading global investment banking, securities and investment management firm that provides a wide range of financial services to a substantial and diversified client base that includes corporations, financial institutions, governments and high-net-worth individuals.

P2 Capital Partners, LLC

P2 is a New York-based investment firm that applies a private equity approach to investing in the public market. P2 manages a concentrated portfolio of significant ownership stakes in high quality public companies in which it is an active shareholder focused on creating long-term value in partnership with management. The firm also leads private equity transactions within its public portfolio. P2’s limited partners include leading public pension funds, corporate pension funds, endowments, foundations, insurance companies, and high net worth investors.

Corporate Information

Interline Brands was incorporated in the state of Delaware in 2004. Our principal executive offices are located at 701 San Marco Boulevard, Jacksonville, Florida 32207 and our telephone number is (904) 421-1400. We also maintain a website at www.interlinebrands.com. The information on or accessible through our website is not part of this prospectus.

Summary of Terms of the Notes

The summary below describes the principal terms of the notes. Some of the terms and conditions described below are subject to important limitations and exceptions. The “Description of the Notes” section of this prospectus contains a more detailed description of the terms and conditions of the notes.

|

| | | |

Issuer | Interline Brands, Inc., a Delaware corporation. |

| | | |

Securities | $285,000,000 principal amount of 10% / 10.75% Senior Notes due 2018. |

| | | |

Maturity Date | November 15, 2018 |

| | | |

Interest | The initial interest payment on the notes was made in cash. For each interest payment thereafter (other than the final interest payment ending at stated maturity, which will be made in cash), the Issuer will be required to pay interest on the notes entirely in cash unless the conditions described in this prospectus are satisfied, in which case the Issuer will be entitled to pay, to the extent described herein, interest for such interest period by increasing the principal amount of the notes or issuing new notes (such increase or issuance being referred to herein as “PIK Interest”). For additional information on the requirement to pay cash interest or a combination of cash interest and PIK Interest, see “Description of the Notes—Principal, Maturity and Interest.” Cash interest on the notes will accrue at a rate of 10% per annum. PIK interest on the notes will accrue at the rate of 10.75% per annum. If the Issuer pays any PIK Interest, the Issuer will increase the principal amount of the notes or issue new notes in an amount equal to the interest payment for the applicable interest period (rounded up to the nearest $1.00) to holders of notes on the relevant record date. |

| | | |

Interest Payment Dates | January 15 and July 15 of each year, commencing January 15, 2013. |

| | | |

Guarantees | The notes are not guaranteed, and will only be guaranteed in the future under certain limited circumstances. See “Description of the Notes—Guarantees.” |

| | | |

Ranking | The notes constitute our senior unsecured debt and rank: |

| | Ÿ | pari passu in right of payment with all of the Issuer’s future senior debt; |

| | Ÿ | senior in right of payment to all of the Issuer’s existing and future subordinated debt; |

| | Ÿ | effectively subordinated to all of the Issuer’s existing and future secured indebtedness, to the extent of the value of the collateral securing such obligations; and |

| | Ÿ | structurally subordinated to all existing and future indebtedness of, and other obligations and preferred stock of, the Issuer’s subsidiaries (other than indebtedness and other obligations owed to the Issuer). |

| | | As of December 26, 2014, the Issuer had $786.4 million of indebtedness on a consolidated basis, including the notes offered hereby, the Term Loan Facility, borrowings under the ABL Facility, each of which we guarantee and capital leases of $0.01 million. The Issuer’s subsidiaries had $421.4 million of indebtedness and all of the indebtedness of such subsidiaries were structurally senior to the notes. |

| | | |

| | | On December 30, 2014, the Company used a combination of cash on hand and borrowings under the recently amended ABL Facility to redeem $80.0 million of the $365.0 million outstanding aggregate principal amount of the HoldCo Notes at a redemption price of 105% of the outstanding aggregate principal amount to be redeemed, plus accrued and unpaid interest through the redemption date. See "Summary—Recent Developments" for additional information. |

Optional Redemption | The Issuer may redeem some or all of the notes at the redemption prices listed under “Description of the Notes—Optional Redemption,” plus accrued and unpaid interest to the redemption date. |

| | | |

|

| | | |

Mandatory Principal Redemption | If the notes would otherwise constitute “applicable high yield discount obligations” within the meaning of Section 163(i)(1) of the Internal Revenue Code of 1986, as amended (the “Code”), at the end of each “accrual period” (as defined in Section 1272(a)(5) of the Code) ending after the fifth anniversary of the notes’ issuance (each, an “AHYDO redemption date”), the Issuer will be required to redeem for cash a portion of each note then outstanding equal to the “Mandatory Principal Redemption Amount” (each such redemption, a “Mandatory Principal Redemption”). The redemption price for the portion of each note redeemed pursuant to any Mandatory Principal Redemption will be 100% of the principal amount of such portion plus any accrued interest thereon on the date of redemption. “Mandatory Principal Redemption Amount” means, as of each AHYDO redemption date, the portion of a note required to be redeemed to prevent such note from being treated as an “applicable high yield discount obligation” within the meaning of Section 163(i)(1) of the Code. No partial redemption or repurchase of the notes prior to any AHYDO redemption date pursuant to any other provision of the indenture governing the notes will alter the Issuer’s obligation to make any Mandatory Principal Redemption with respect to any notes that remain outstanding on such AHYDO redemption date. |

| | | |

Change of Control | If a change of control occurs, the Issuer must give holders of the notes the opportunity to sell their notes to us at 101% of the principal amount thereof, plus accrued and unpaid interest. See “Description of the Notes—Change of Control.” We may not have sufficient liquidity or have the ability to raise the funds necessary to finance a change of control offer required by the indenture relating to the notes in the event of a change of control. See “Risk Factors—Risks Relating to the Notes—We may not have the ability to raise the funds necessary to finance a change of control offer required by the indenture relating to the notes or the terms of our other indebtedness. In addition, under certain circumstances, we may be permitted to use the proceeds from debt to effect merger payment in compliance with the indenture.” |

| | | |

Certain Covenants | The indenture governing the notes contains covenants that, among other things, limit the Issuer’s ability and the ability of the Issuer’s restricted subsidiaries to: |

| | Ÿ | pay dividends or distributions, repurchase equity, prepay junior debt and make certain investments; |

| | Ÿ | incur additional debt or issue certain disqualified stock and preferred stock; |

| | Ÿ | incur liens on assets; |

| | Ÿ | merge, consolidate or sell all or substantially all assets; |

| | Ÿ | enter into transactions with affiliates; and |

| | Ÿ | allow to exist certain restrictions on the ability of restricted subsidiaries to pay dividends or make other payments to us. |

| | These covenants are subject to important exceptions and qualifications. During any period in which the notes have an investment grade rating from both Rating Agencies (as defined herein) and no default has occurred and is continuing under the indenture governing the notes, the Issuer will not be subject to certain of these covenants. See “Description of the Notes—Material Covenants.” |

| | | |

No Prior Market | The Issuer does not intend to list the notes on any national securities exchange or automated quotation system. Accordingly, we cannot assure you that an active public or other market will develop for the notes or as to the liquidity of the trading market for the notes. If a trading market does not develop or is not maintained, holders of the notes may experience difficulty in reselling the notes or may be unable to sell them at all. If a market for the notes develops, any such market may be discontinued at any time. Accordingly, you may have to bear the financial risks of investing in the notes for an indefinite period of time. The Issuer does not intend to apply for a listing of the notes on any securities exchange or automated dealer quotation system. See “Plan of Distribution |

| | | |

Risk Factors | You should consider carefully the information set forth in the section entitled “Risk Factors” beginning on page 10 and all other information contained in this prospectus before deciding to invest in the notes. |

Summary Historical Consolidated Financial Data

The table below sets forth certain of Interline Brands’ historical consolidated financial data as of and for each of the periods indicated. The consolidated historical financial information as of and for the fiscal years ended December 28, 2012, December 27, 2013, and December 26, 2014 is derived from our audited consolidated financial statements appearing elsewhere in this prospectus. Our historical operating results are not necessarily indicative of future operating results.

The data below should be read in conjunction with “Non-GAAP Financial Information,” “Risk Factors,” “Capitalization,” “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and our consolidated financial statements and the notes thereto appearing elsewhere in this prospectus.

|

| | | | | | | | | | | | | | | | |

| Successor | | | Predecessor |

| Fiscal Year Ended | | For the period September 8, 2012 through December 28, 2012 (1)(3) | | | For the period December 31, 2011 through September 7, 2012 (3) |

| December 26, 2014 | | December 27, 2013 | | | |

Income Statement Data: | | | | | | | | |

Net sales | $ | 1,676,221 |

| | $ | 1,598,055 |

| | $ | 404,593 |

| | | $ | 917,752 |

|

Cost of sales | 1,094,578 |

| | 1,045,084 |

| | 256,349 |

| | | 584,033 |

|

Gross profit | 581,643 |

| | 552,971 |

| | 148,244 |

| | | 333,719 |

|

Operating expenses(5) | 529,729 |

| | 508,651 |

| | 168,011 |

| | | 292,165 |

|

Operating income (loss) | 51,914 |

| | 44,320 |

| | (19,767 | ) | | | 41,554 |

|

Impairment of other intangible assets | (67,500 | ) | | — |

| | — |

| | | — |

|

Loss on extinguishment of debt, net | (4,257 | ) | | — |

| | — |

| | | (2,214 | ) |

Interest and other expense, net | (58,195 | ) | | (61,507 | ) | | (19,180 | ) | | | (15,132 | ) |

(Loss) income before income taxes | (78,038 | ) | | (17,187 | ) | | (38,947 | ) | | | 24,208 |

|

Income tax (benefit) provision | (30,966 | ) | | (10,847 | ) | | (10,503 | ) | | | 11,384 |

|

Net (loss) income | $ | (47,072 | ) | | $ | (6,340 | ) | | $ | (28,444 | ) | | | $ | 12,824 |

|

| | | | | | | | |

Balance Sheet Data (as of end of period): | | | | | | | | |

Cash and cash equivalents | $ | 6,064 |

| | $ | 6,102 |

| | $ | 15,801 |

| | | N/A |

|

Total assets | 1,460,622 |

| | 1,517,733 |

| | 1,523,233 |

| | | N/A |

|

Total debt(6) | 786,385 |

| | 798,588 |

| | 814,741 |

| | | N/A |

|

Stockholders' equity | 316,517 |

| | 356,853 |

| | 357,470 |

| | | N/A |

|

| | | | | | | | |

Other Data: | | | | | | | | |

Depreciation and amortization | $ | 53,814 |

| | $ | 50,038 |

| | $ | 12,837 |

| | | $ | 17,707 |

|

Adjusted EBITDA(7) | 141,802 |

| | 134,144 |

| | 37,610 |

| | | 84,132 |

|

Capital expenditures | 17,437 |

| | 18,738 |

| | 5,748 |

| | | 11,966 |

|

Capital expenditures as a percentage of net sales | 1.0 | % | | 1.2 | % | | 1.4 | % | | | 1.3 | % |

_____________________________

| |

(1) | As a result of the Merger, we applied the acquisition method of accounting, which established a new accounting basis as of September 8, 2012. The financial results for the period September 8, 2012 through December 28, 2012 represent the 16-week Successor Period subsequent to the Merger. |

| |

(2) | As a result of the Merger, we applied the acquisition method of accounting, which established a new accounting basis as of September 8, 2012. The financial results for the period December 31, 2011 through September 7, 2012 represent the 36-week Predecessor Period prior to the Merger. |

| |

(3) | We acquired JanPak, Inc. in December 2012 and Northern Colorado Paper ("NCP") in January 2011. Their results have been included in the financial statements since each respective acquisition date. |

| |

(4) | All fiscal years presented were 52-week years, with the exception of 2012, which is presented as Successor and Predecessor Periods. |

| |

(5) | Included in operating expenses were Merger related costs of $0.1 million for the fiscal year ended December 26, 2014, $1.4 million for the fiscal year ended December 27, 2013, $39.6 million for the period September 8, 2012 through December 28, 2012 (Successor Period), and $19.0 million for the period December 31, 2011 through September 7, 2012 (Predecessor Period). |

| |

(6) | Total debt represents the amount of our short-term debt and long-term debt and short and long-term capital leases. |

| |

(7) | The reconciliation of EBITDA and Adjusted EBITDA to the most directly comparable US GAAP financial measure, which is net (loss) income, is as follows (in thousands): |

|

| | | | | | | | | | | | | | | | |

| Successor | | | Predecessor |

| Fiscal Year Ended | | For the period September 8, 2012 through December 28, 2012 | | | For the period December 31, 2011 through September 7, 2012 |

| December 26, 2014 | | December 27, 2013 | | | |

EBITDA | | | | | | | | |

Net (loss) income | $ | (47,072 | ) | | $ | (6,340 | ) | | $ | (28,444 | ) | | | $ | 12,824 |

|

Interest expense, net | 59,099 |

| | 63,042 |

| | 19,758 |

| | | 16,613 |

|

(Benefit) provision for income taxes | (30,966 | ) | | (10,847 | ) | | (10,503 | ) | | | 11,384 |

|

Depreciation and amortization | 53,814 |

| | 50,038 |

| | 12,837 |

| | | 17,707 |

|

EBITDA | 34,875 |

| | 95,893 |

| | (6,352 | ) | | | 58,528 |

|

| | | | | | | | |

EBITDA Adjustments | | | | | | | | |

Impairment of other intangible assets | 67,500 |

| | — |

| | — |

| | | — |

|

Loss on extinguishment of debt, net | 4,257 |

| | — |

| | — |

| | | 2,214 |

|

Merger related expenses | 102 |

| | 1,377 |

| | 39,641 |

| | | 19,049 |

|

Share-based compensation | 3,720 |

| | 5,330 |

| | 2,945 |

| | | 3,922 |

|

Distribution center consolidations and restructuring costs | 7,459 |

| | 8,307 |

| | 484 |

| | | 323 |

|

Acquisition-related costs, net | 1,496 |

| | 372 |

| | 610 |

| | | 96 |

|

Litigation-related costs | 21,604 |

| | 21,841 |

| | — |

| | | — |

|

Impact of straight-line rent expense | 789 |

| | 1,024 |

| | 282 |

| | | — |

|

Adjusted EBITDA | $ | 141,802 |

| | $ | 134,144 |

| | $ | 37,610 |

| | | $ | 84,132 |

|

Risk Factors

Before making a decision to invest in the notes, you should carefully consider the following risk factors described below. Additional risks and uncertainties not currently known to us or that we currently deem to be immaterial may also materially adversely affect our business, financial condition or results of operations. Any of the following risks could materially adversely affect our business, financial condition or results of operations. In addition, there may be other risks that a prospective investor should consider that are relevant to its particular circumstances or generally. In such case, you may lose all or part of your original investment.

Risks Relating to the Notes

Claims of noteholders will be structurally subordinated to claims of creditors of our subsidiaries.

The notes are not guaranteed by any of our subsidiaries. Accordingly, claims of holders of the notes will be structurally subordinated to the claims of creditors of our subsidiaries, including trade creditors. All obligations of our subsidiaries will have to be satisfied before any of the assets of such subsidiaries would be available for distribution, upon a liquidation or otherwise, to us or our creditors, including the holders of the notes.

As of December 26, 2014, our subsidiaries had total indebtedness of approximately $421.4 million, including $347.4 million outstanding under the Term Loan Facility, $74.0 million outstanding on the ABL Facility and $0.01 million of capital lease obligations, all of which are structurally senior to the notes. On December 30, 2014, the Company used a combination of cash on hand and borrowings under the recently amended ABL Facility to redeem $80.0 million of the $365.0 million outstanding aggregate principal amount of the HoldCo Notes at a redemption price of 105% of the outstanding aggregate principal amount to be redeemed, plus accrued and unpaid interest through the redemption date. See "Summary—Recent Developments" for additional information.

We are the sole obligor of the notes and our direct and indirect subsidiaries do not guarantee our obligations under the notes and do not have any obligation with respect to the notes.

We are a holding company with no business operations or assets other than the capital stock of Interline New Jersey. Operations are conducted through Interline New Jersey and its subsidiaries. Consequently, we will be dependent on loans, dividends and other payments from Interline New Jersey, and, indirectly, its subsidiaries, to make payments of principal and interest in cash on the notes. However, our subsidiaries are separate and distinct legal entities, and they will have no obligation, contingent or otherwise, to pay the amounts due under the notes or to make any funds available to pay those amounts, whether by dividend, distribution, loan or other payments. You will not have any direct claim on the cash flows or assets of our direct and indirect subsidiaries. Moreover, we are a guarantor of the Term Loan Facility and the ABL Facility, and as such, we are an obligor thereunder and have pledged all of our equity interests in Interline New Jersey to secure its obligations under the ABL Facility and Term Loan Facility.

The ability of our subsidiaries to pay dividends and make other payments to us will depend on their cash flows and earnings, which, in turn, will be affected by all of the factors discussed in “Risks Related to Our Business” below. The ability of our direct and indirect subsidiaries to pay dividends and make distributions to us may be restricted by, among other things, applicable laws and regulations and by the terms of the agreements into which they enter. If we are unable to obtain funds from our direct and indirect subsidiaries as a result of restrictions under their debt or other agreements, applicable laws and regulations or otherwise, we may not be able to pay cash interest or principal on the notes when due. The terms of the credit agreement, and any future credit agreements or indentures, governing the ABL Facility and the Term Loan Facility significantly restrict Interline New Jersey from paying dividends and otherwise transferring assets to us, except for administrative, legal and accounting services.

Our ability to make payments on our indebtedness and to fund our other obligations is dependent not only on the ability of our subsidiaries to generate cash, but also on the ability of our subsidiaries to distribute cash to us in the form of dividends, fees, interest, loans or otherwise, as well as our ability to obtain funds from other sources of financing, which may not be available if and when required.

The indenture governing the notes offered hereby requires us to determine the amount of cash interest we will pay in respect of each interest period no later than fifteen days prior to the beginning of such interest period, and there can be no assurance that Interline New Jersey will continue to have sufficient capacity under the restricted payments basket governing the its indebtedness to dividend cash to us at the end of the interest period (over six months after the determination date), when such cash interest would actually be paid to holders of the notes offered hereby. This could lead to a breach of the indenture governing the notes hereby (if we fail to make the required cash interest payment) and/or the indebtedness of Interline New

Jersey (if Interline New Jersey pays such dividend absent sufficient restricted payments availability under its indebtedness), which may result in a cross default under the ABL Facility or the Term Loan Facility.

Our substantial indebtedness could adversely affect our financial health and prevent us from fulfilling our obligations.

As of December 26, 2014, our total indebtedness was $786.4 million comprised of $365.0 million in outstanding HoldCo Notes, a $347.4 million Term Loan Facility, $74.0 million outstanding on the ABL Facility, and capital lease obligations of $0.01 million. As of the same date, cash and cash equivalents were $6.1 million, outstanding letters of credit totaled $11.3 million and there was $209.7 million available under the ABL Facility. Our substantial indebtedness could have important consequences to our financial health including, but not limited to:

| |

• | increased vulnerability to general adverse economic and industry conditions or a downturn in our business; |

| |

• | limited flexibility in planning for, or reacting to, changes in our business and the industry in which we operate; |

| |

• | a competitive disadvantage compared to our competitors that are not as highly leveraged; |

| |

• | difficulties related to satisfying our obligations with respect to the HoldCo Notes, Term Loan Facility, ABL Facility, and our other indebtedness; |

| |

• | reduced availability of cash flows to fund working capital, capital expenditures and general corporate purposes as a result of debt service requirements; |

| |

• | limited capacity to borrow additional funds, if needed; and |

| |

• | an event of default if we fail to satisfy our obligations under the HoldCo Notes, Term Loan Facility, the ABL Facility, or our other indebtedness or if we fail to comply with the financial other restrictive covenants contained in the indenture and agreements governing the ABL Facility, Term Loan Facility and other debt; such event of default could result in all of our debt becoming immediately due and payable and could permit certain of our lenders to foreclose on assets securing our indebtedness. |

If our cash flow and capital resources are insufficient to fund our debt service obligations, including timely payment of principal and interest on our outstanding indebtedness, we may be required to reduce or delay capital expenditures, sell assets, seek to obtain additional capital or refinance all or part of our existing debt. There can be no assurance that we will be able to successfully complete any of these transactions or do so on favorable terms. Any of the above listed factors could have a material adverse effect on our business, financial condition and results of operations.

If we do not have sufficient funds to pay cash interest on the notes offered hereby, all or part of the interest on the notes may be paid in PIK interest.

We will be required to pay interest on the notes entirely in cash unless the conditions described in this prospectus are satisfied, in which case we will be entitled to pay, to the extent described herein, PIK interest. See “Description of the Notes—Principal, Maturity and Interest.” Our ability to pay cash interest is dependent on distributions from our subsidiaries, including Interline New Jersey. The credit agreements governing the ABL Facility and the Term Loan Facility and the indenture governing the notes offered hereby allow our subsidiaries to utilize amounts that would otherwise be available to pay cash dividends to us for purposes such as making restricted investments, capital expenditures and prepaying subordinated indebtedness and, subject to certain limitations, making cash dividends to and other payments in respect of equity holders, and such uses would reduce the amounts available to pay dividends to us in order to pay cash interest on the notes offered hereby. The indenture governing the notes does not restrict the ability of our subsidiaries to use their dividend payment capacity for such alternative uses. See “Description of the Notes—Principal, Maturity and Interest.” As a result, we cannot assure you that we will be required (or able) to make cash interest payments on the notes. The payment of interest through PIK interest will increase the amount of our indebtedness and would exacerbate the risks associated with our high level indebtedness.

The agreements and indenture governing our debt include restrictive and financial covenants that may limit our operating and financial flexibility.

The indenture governing the HoldCo Notes and the agreements governing the ABL Facility and Term Loan Facility, each contain covenants that, among other things, restrict our ability to take specific actions, even if we believe them to be in our best interest. These include restrictive covenants that limit, among other things, our ability to:

| |

• | incur any additional indebtedness; |

| |

• | consolidate, merge, or sell assets or enter into other business combination transactions; |

| |

• | make certain restricted payments, such as paying dividends, making distributions on, redeeming or repurchasing stock; |

| |

• | make certain investments, including acquisitions and capital expenditures; |

| |

• | amend the terms of certain subordinated indebtedness; |

| |

• | enter into transactions with affiliates; |

| |

• | enter into sale leaseback transactions; |

| |

• | use proceeds from sale of assets; |

| |

• | limit the payment of dividends by our subsidiaries; |

| |

• | prepay, redeem or repurchase certain indebtedness; and |

In addition, the ABL Facility requires the Company and its restricted subsidiaries, on a consolidated basis, to maintain a fixed charge coverage ratio (defined as the ratio of EBITDA, as defined in the credit agreement, to the sum of cash interest, principal payments on indebtedness and accrued income taxes, dividends or distributions and repurchases, redemptions or retirement of the equity interest of the Company) of at least 1.00:1.00 when the excess availability is less than or equal to the greater of: (i) 10% of the total commitments under the ABL Facility; and (ii) $25.0 million.

The Term Loan Facility contains similar covenants, including coverage ratio requirements, as discussed in Management's Discussion and Analysis of Financial Condition and Results of Operations—Liquidity and Capital Resources, "—ABL Credit Facility” “—Term Loan Facility” and “—HoldCo Notes.”

To service our indebtedness, we will require a significant amount of cash, which depends on many factors beyond our control.

Based on our current level of operations, we believe our cash flow from operations, available cash and available borrowings under the ABL Facility will be adequate to meet our future liquidity needs for the foreseeable future. However, we cannot assure you that our business will generate sufficient cash flow from operations, or that future borrowings will be available to us under the ABL Facility in amounts sufficient to enable us to fund our liquidity needs, including with respect to the notes and our other indebtedness. In addition, if we consummate significant acquisitions in the future, our cash requirements may increase significantly. As our debt matures, we may also need to raise funds to refinance all or a portion of our debt. We cannot assure you that we will be able to refinance any of our debt, including the ABL Facility or the Term Loan Facility, on attractive terms, commercially reasonable terms or at all. Our future operating performance and our ability to service or refinance the notes and to service, extend or refinance our other debt, including the ABL Facility, the Term Loan Facility and the notes offered hereby, will be subject to future economic conditions and to financial, business and other factors, many of which are beyond our control.

The notes are our senior unsecured obligations. Therefore, our secured creditors (including the lenders under the ABL Facility and the Term Loan Facility) would have a prior claim, ahead of the notes, on our assets.

The notes are our senior unsecured obligations. As a result, upon any distribution to our creditors in a bankruptcy, liquidation or reorganization or similar proceeding relating to us or our property, the holders of our secured indebtedness, including the lenders under the ABL Facility, will be entitled to be paid in full from our assets securing that secured indebtedness before any payment may be made with respect to the notes. Although the indenture governing the notes restricts our ability to incur liens, that restriction is subject to important exceptions such that we may be able to incur more secured debt in the future, which amount could be material. In addition, if we fail to meet our payment or other obligations under our secured debt, the holders of that secured indebtedness would be entitled to foreclose on our assets securing that secured debt and liquidate those assets. Accordingly, we may not have sufficient funds to pay amounts due on the notes. As a result you may lose a portion of or the entire value of your investment in the notes.

Our debt agreements give us flexibility to undertake certain transactions which could be adverse to the interests of holders of the notes, including making restricted payments and incurring additional indebtedness, including secured indebtedness.

Notwithstanding the restrictive covenants described above in our debt agreements, the terms of the ABL Facility, the Term Loan Facility, and indentures (including the indenture governing the notes) give us flexibility to undertake certain transactions which could be adverse to the interests of holders of the notes. For example, the provisions contained in the agreements relating to our indebtedness, including the notes offered hereby, limit but do not prohibit our ability to incur additional indebtedness, including secured indebtedness, and the amount of indebtedness that we could incur could be substantial and could be used to finance acquisitions or to assume debt in connection with an acquisition. Accordingly, we could incur significant additional indebtedness in the future, including additional indebtedness under the ABL Facility. Similarly, if we incur any secured indebtedness, the holders of that secured indebtedness will be entitled to be paid in full from the assets securing that indebtedness before any payment may be made with respect to the notes. If we incur any additional indebtedness that ranks equally with the notes offered hereby, the holders of that indebtedness will be entitled to share ratably with the holders of these notes in any proceeds distributed in connection with any bankruptcy, liquidation, reorganization or similar

proceedings. This may have the effect of reducing the amount of proceeds paid to you. If new indebtedness is added to our current debt levels, the related risks that we now face, including those described above, could intensify.

We may not have the ability to raise the funds necessary to finance a change of control offer required by the indenture relating to the notes or the terms of our other indebtedness. In addition, under certain circumstances, we may be permitted to use the proceeds from debt to effect merger payments in compliance with the indenture.

Upon the occurrence of a change of control, a default could occur in respect of the ABL Facility and the Term Loan Facility, and we will be required to make an offer to purchase all outstanding notes. If such a change of control event were to occur, we cannot assure you that we would have sufficient funds to pay the purchase price for all the notes tendered by the holders or such other indebtedness. See “Description of the Notes—Change of Control.” The ABL Facility, the Term Loan Facility, and the indenture governing the notes offered hereby contain, and any future agreements relating to indebtedness to which we become a party may contain, provisions restricting our ability to purchase notes or providing that an occurrence of a change of control constitutes an event of default, or otherwise requiring payment of amounts borrowed under those agreements. If such a change of control event occurs at a time when we are prohibited from purchasing the notes, we may seek the consent of our then existing lenders and other creditors to the purchase of the notes or may attempt to refinance the indebtedness that contains the prohibition. If we do not obtain such a consent or repay such indebtedness, we would remain prohibited from purchasing the notes. In that case, our failure to purchase tendered notes would constitute a default under the terms of the indenture governing the notes and any other indebtedness that we may enter into from time to time with similar provisions.

It may be difficult for the holders of notes to ascertain that a change of control has occurred, leading to uncertainty as to whether a holder of notes may require us to repurchase the notes.

The definition of change of control includes a disposition of all or substantially all of our and our restricted subsidiaries’ assets. Although there is a limited body of case law interpreting the phrase “substantially all,” there is no precise established definition of the phrase under applicable law. Accordingly, in certain circumstances there may be a degree of uncertainty as to whether a particular transaction would involve a disposition of “all or substantially all” of our and our restricted subsidiaries’ assets. As a result, it may be unclear as to whether a change of control has occurred and whether a holder of notes may require us to make an offer to repurchase the notes. See “Description of the Notes—Change of Control.”

We may enter into certain transactions that would not constitute a change of control but that result in an increase of our indebtedness.

Subject to limitations under the indenture governing the notes offered hereby, and the credit agreement governing the ABL Facility and the Term Loan Facility, we could, in the future, enter into certain transactions, including acquisitions, refinancings or other recapitalizations, that would not constitute a change of control under the indenture governing the notes, the Term Loan Facility, and the ABL Facility, but that could increase the amount of indebtedness outstanding at such time or otherwise affect our capital structure or credit ratings in a way that adversely affects the holders of the notes. See “Description of the Notes—Change of Control.”

Changes in credit ratings issued by statistical rating organizations could adversely affect our cost of financing and the market price of the notes.

Credit rating agencies rate the notes and our other indebtedness on factors that include our operating results, actions that we take, their view of the general outlook for our industry and their view of the general outlook for the economy. Actions taken by the rating agencies can include maintaining, upgrading or downgrading the current rating or placing us on a watch list for possible future downgrading. Downgrading the credit rating of the notes or our other indebtedness or placing us on a watch list for possible future downgrading could limit our ability to refinance maturing liabilities, access the capital markets to meet liquidity needs, increase our cost of financing and lower the market price or liquidity of the notes.

Credit ratings are not recommendations to purchase, hold or sell the notes. Additionally, credit ratings may not reflect the potential effect of risks relating to the structure or marketing of the notes. Any future lowering of our ratings likely would make it more difficult or more expensive for us to obtain additional debt financing. If any credit rating initially assigned to the notes is subsequently lowered or withdrawn for any reason, you may not be able to resell your notes at a favorable price or at all.

Certain restrictive covenants in the indenture governing the notes will be suspended if the notes achieve investment grade ratings.

Most of the restrictive covenants in the indenture governing the notes will not apply so long as the notes achieve investment grade ratings from Moody’s Investor Service, Inc. and Standard & Poor’s Rating Services, and no default or event of default has occurred, subject to continued compliance with our other outstanding debt instruments. If these restrictive covenants cease to apply, we may take actions, such as incurring additional indebtedness or making certain dividends or distributions, which would otherwise be prohibited under the indenture governing the notes. Ratings are given by these rating agencies based on analyses that include many subjective factors. We cannot assure you that the notes will achieve investment grade ratings, nor can we assure you that investment grade ratings, if granted, will reflect all of the factors that would be important to holders of the notes.

Despite our current indebtedness levels, we may incur substantial additional indebtedness.

We may incur substantial additional indebtedness in the future to finance acquisitions, investments, or for other purposes, subject to the restrictions contained in the documents governing our current outstanding indebtedness. For example, based on year-end inventory and trade accounts receivable balances as of December 26, 2014 we were able to incur up to a maximum of $209.7 million in additional indebtedness under the ABL Facility. Although the ABL Facility, the indenture and our other debt agreements contain some limitations on our ability to incur indebtedness, we may still incur substantial indebtedness to refinance existing indebtedness or for other purposes. If new debt is added to our current indebtedness levels, the substantial leverage risks that we now face could intensify.

Major disruptions and volatility in the capital and credit markets may impact our ability to secure sufficient financing on favorable terms.

The availability of financing is dependent on numerous factors, some of which are beyond our control, including, but not limited to, general economic conditions and the volatility of the capital and credit markets. We may not able to obtain additional financing on favorable terms, or at all, which could have a material adverse effect on our business, including the ability to make acquisitions and execute our growth strategies. Furthermore, if our operating results, cash flow or capital resources prove inadequate, or if interest rates increase significantly, we could face substantial liquidity problems, which may impede our ability to seek additional capital in a timely manner or refinance our existing debt on favorable terms. If we are unable to service our debt, we could be forced to reduce or delay planned capital expenditures, sell assets, restructure or refinance our debt or seek additional equity capital. There can be no assurance that any of these actions will be sufficient to allow us to service our debt obligations or that such actions will not result in an adverse impact on our business. In addition, the terms of the ABL Facility, Term Loan Facility and the indenture governing the HoldCo Notes and any future indebtedness may limit our ability to take certain of these actions thereby adversely impacting our results of operations and financial condition.

Risks Relating to Our Business

General economic conditions may adversely impact our industry and customers resulting in adverse effects on the Company’s operating results.

Financial markets in the United States, Europe and Asia experienced substantial disruption from prior recessions, including, among other things, extreme volatility in security prices, severely diminished liquidity and credit availability, rating downgrades of certain investments and declining valuations of others. A slow and extended recovery or a downturn, worsening or broadening of adverse conditions in the worldwide and domestic economies could negatively affect purchases of our products, and create or exacerbate credit issues, cash flow issues and other financial issues for us and for our suppliers and customers. Depending upon their severity and duration, these conditions could have a material adverse impact on our business, liquidity, financial condition and results of operations.

Current and future economic conditions and other factors, including consumer confidence, interest rates, unemployment trends, government regulations, and liquidity in capital markets can impact consumer spending and demand for our products. Such economic developments may affect our business in a number of ways. Reduced demand may drive us and our competitors to offer products at promotional prices, which would have a negative impact on our profitability. Also, credit availability may adversely affect the ability of our customers and suppliers to obtain financing for significant purchases and operations which could result in a decrease in, or cancellation of, orders for our products. If demand for our products slows down or decreases, we will not be able to improve our revenues and we may run the risk of failing to satisfy the financial and other restrictive covenants to which we are subject under our existing indebtedness. Reduced revenues as a result of decreased demand may also hinder our ability to improve our performance in connection with our long-term strategy.

We operate in a highly competitive industry, which may have a material adverse effect on our business, financial condition, and results of operations.

The MRO product distribution industry is highly competitive. We face significant competition from national and regional distributors that market their products through the use of direct sales forces as well as direct marketing, websites and catalogs. In addition, we face competition from traditional channels of distribution such as retail outlets, small wholesalers and large warehouse stores and from buying groups formed by smaller distributors, internet-based procurement service companies, auction businesses and trade exchanges. We expect that new competitors may develop over time as internet-based enterprises become more established and reliable and refine their service capabilities.

Competition in our industry is primarily based upon product line breadth, product availability, technology, service capabilities and price. To the extent that existing or future competitors seek to gain or retain market share by reducing price or by increasing support service offerings, we may be required to lower our prices or to make additional expenditures for support services, thereby reducing our profitability.

In addition, the MRO product distribution industry is undergoing changes driven by ongoing industry consolidation and increased customer demands. Traditional MRO product distributors are consolidating operations and acquiring or merging with other MRO product distributors to achieve greater economies of scale capabilities and increase efficiency. This consolidation trend could cause the industry to become more competitive and may adversely affect our operating margins and growth prospects. Furthermore, an inability on our part to successfully compete within our target markets could result in lost customers and a corresponding decline in sales, which may have a material adverse effect on our business, financial condition, and results of operations.

Adverse changes in industry trends and economic factors specific to the principal markets in which we serve may negatively impact our net sales growth and operating margins.

We currently market and sell our products across certain facilities maintenance end-markets, including institutional facilities, multi-family housing facilities, and residential facilities. The demand for our products and services depends to some degree on the capital spending levels of end-users within these markets. The strength of these markets depends on many factors, generally outside of the Company’s control, including general economic conditions, government spending, credit availability and stability of the housing markets, including new residential construction and home improvement activity levels. The success of our business depends in part on our ability to identify and respond promptly to evolving trends in demographics, consumer preferences, expectations and needs, and unexpected weather conditions. Adverse changes in industry trends as well as weaknesses in the industries in which our customers operate may negatively impact the rate of growth of our net sales and operating margins.

We are exposed to additional risks as a result of our foreign operations and global product sourcing.

Our foreign operations expose us to certain risks associated with global economic conditions, political instability, regulatory changes, cultural and legal differences, and currency exchange rate fluctuations. Risks inherent in international operations also include, among others, potential adverse tax consequences, greater credit risk exposure and risks associated with enhanced logistics complexity. Adverse changes to any of these factors may negatively impact our profitability and results of operations.

Because the functional currency related to most of our foreign operations is the applicable local currency, we are exposed to foreign currency exchange rate risks arising from transactions in the normal course of business. Our primary currency exposure risks are with the Canadian dollar and the Chinese Yuan. Fluctuations in the relative strength of foreign economies and volatility in their related currencies could impact our foreign sales and the ability to procure products overseas.

In addition, China’s turnover tax system consists of value-added tax ("VAT"), consumption tax and business tax. Export sales are exempted under VAT rules and an exporter who incurs input VAT on the manufacture of goods can claim a tax rebate from Chinese tax authorities. Currently, our Chinese suppliers benefit from the tax rebates that China provides them to export their products. If these tax rebates are reduced or eliminated, some of our Chinese-sourced products could become more expensive for us, thereby reducing our profitability.

Fluctuations in the availability or price of raw materials, products, and fuel resources could significantly reduce our revenues and profitability.

As a distributor of manufactured products, our profitability is related to the prices we pay to the suppliers from which we purchase our products and to the cost of transporting the products to us and our customers. The price that our suppliers charge us for our products is dependent in part upon the availability and cost of the raw materials used to produce those products. Such raw materials are often subject to price fluctuations, frequently due to factors beyond our control, including changes in supply and demand, U.S. and global economic conditions, labor costs, competition and government regulations. Increases in the cost of raw materials, such as copper, oil, stainless steel, aluminum, zinc, plastic and polyvinyl chloride ("PVC") and other commodities and raw materials have occurred in the past and adversely impacted our operating results. In addition, transportation prices are significantly dependent on fuel prices, which generally change due to factors beyond our control, such as changes in worldwide demand, disruptions in supply, changes in the political climate in the Middle East and other regions and changes in government regulations, including existing and pending legislation and regulations relating to climate change. For example, efforts to combat climate change through reduction of greenhouse gases may result in higher fuel costs through taxation or other means.

Fluctuations in raw materials and fuel prices may increase our costs and significantly reduce our revenues and profitability. We deliver a significant volume of products to our customers by truck. Our operating margin may be adversely affected if we are unable to obtain the fuel we require or offset the anticipated impact of higher fuel prices through other means. The nature and extent of such an impact is difficult to predict, quantify and measure. To the extent the costs of products increase or decrease, the prices we charge for our products may correspondingly increase or decrease, potentially affecting our revenues and profitability.