OPTION EXCHANGE

PROGRAM OFFER TO EXCHANGE CERTAIN OUTSTANDING OPTIONS FOR NEW STOCK

OPTIONS

Exhibit 99.(a)(1)(E) |

| OPTION EXCHANGE

PROGRAM OFFER TO EXCHANGE CERTAIN OUTSTANDING OPTIONS FOR NEW STOCK

OPTIONS

Exhibit 99.(a)(1)(E) |

2

PURPOSE OF THE PRESENTATION

•

Remind Zymers of the key dates and terms of the Exchange Offer

•

Provide you with considerations for your decision making

•

Illustrate what terms mean

•

Review exchange mechanics

•

Ensure you know where to go for help

Reminder:

Solazyme is not authorized to give financial, legal or tax advice

|

3

AGENDA

•

Review of Offer Terms, Eligibility, and Key Dates

•

Considerations and Trade-offs

•

Illustrations

•

Tender Mechanics

•

Where to go for help |

4

OFFER TERMS, ELIGIBILITY AND KEY DATES

Eligibility

All options held by Solazyme, Inc.

employees that have exercise prices of

$6.79 or more

Exchange Ratio

2 for 1 (two old options for one new

option)

Exercise Price

Closing price on grant date (expected to

be February 19, 2015)

Vesting

Same rate as surrendered option except

vesting will cumulate and cliff vest on

January 1, 2016

Term

Same as surrendered option

Tax Treatment of New Options

Non-qualified stock options

Offering Begins

January 21, 2015

Offering Ends

February 18, 2015

New Option Grant Date

February 19, 2015 |

5

CONSIDERATIONS AND TRADE OFFS

Deciding whether to participate in the exchange offer is a personal

decision. This is a voluntary program, you are not required to

participate.

Among the many factors to keep in mind:

•

Would

you

rather

have

more

options

with

a

higher

exercise

price

or

fewer

options

with

a

lower

exercise

price?

•

If

your

existing

option

is

an

incentive

stock

option

(ISO),

would

you

rather

have

ISOs

or

non-qualified

stock

options

(NQ)?

•

Where

do

you

see

the

Solazyme

stock

price

moving?

When?

•

What

is

your

investment

time

horizon?

Please consider consulting with a professional financial, legal or

tax advisor for your specific situation. |

6

ILLUSTRATION

Employee has an incentive stock option covering 1,000 shares with an exercise price of

$8.00/share.

Should s/he exchange this option for a non-qualified stock option covering 500 shares

with an exercise price of $2.50/share*

Possible economic analysis:

Ignoring the tax differences between the two options, at stock prices below $13.50 the

employee is better off having 500 options @ $2.50 than 1,000 options @ $8.00; however

at prices above $13.50, the employee is better off having 1,000 options @ $8.00

than 500 options

@

$2.50

(thus

for

this

option,

the

“equalization

price”

would

be

$13.50).

In addition, exercise of the old ISO option may not trigger immediate taxation and would not

trigger

certain

other

taxes

(like

FICA).

Exercise

of

the

new

NQ

option

would

trigger

immediate

taxes (including FICA). This will also have an impact on the economic analysis.

*hypothetical new option exercise price |

7

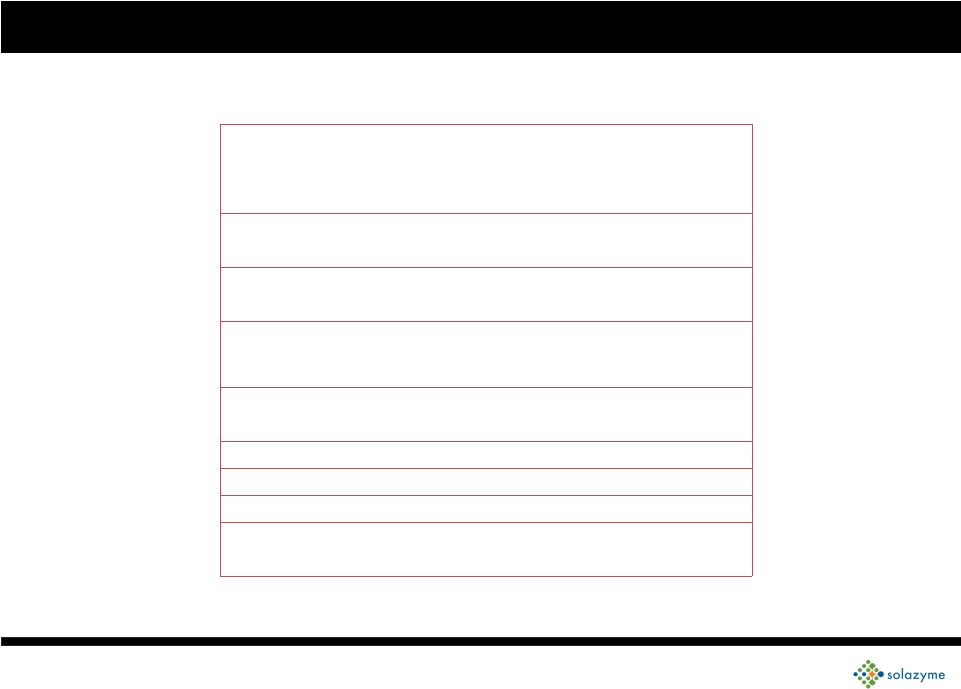

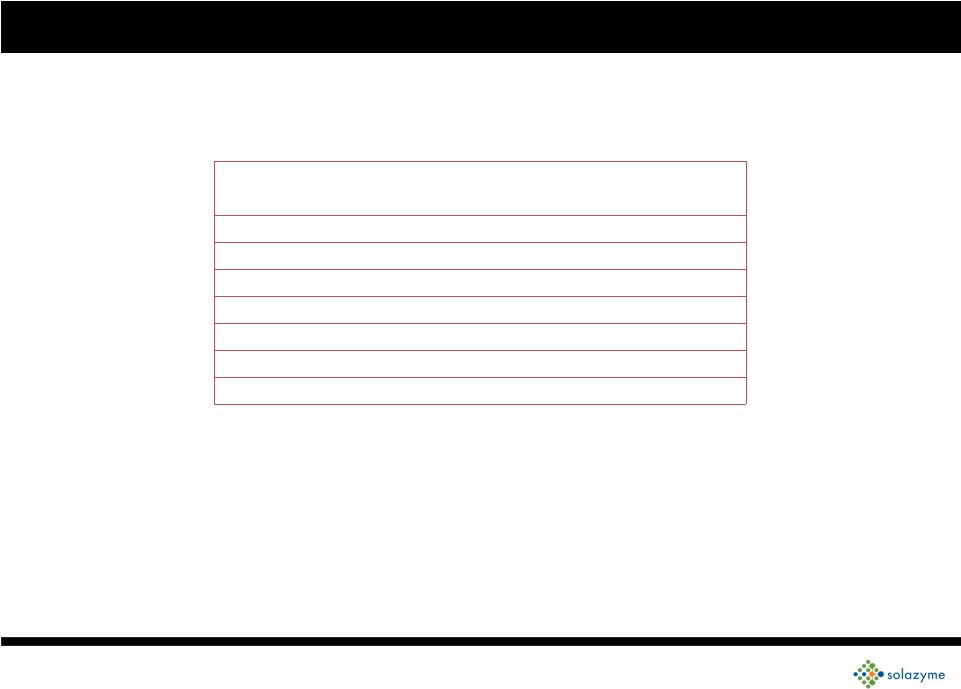

“EQUALIZATION PRICE”

†

FOR NEW OPTIONS WITH A $2.50 EXERCISE PRICE

Old Option Exercise Price ($)

Equalization Price

†

($)

6.79

11.08

7.80

13.10

8.77

15.04

10.89

19.28

11.24

19.98

11.49

20.48

14.38

26.26

If the existing option is an ISO, exercise of that ISO may not trigger immediate taxation

and

would

not

trigger

certain

other

taxes

(like

FICA).

Exercise

of

the

new

NQ

option

would trigger immediate taxes (including FICA).

†

Solazyme

can

make

no

assurance

as

to

what

its

stock

price

may

be

in

the

future. |

8

VESTING

New stock options will be subject to the same rate of vesting, from the same

vesting commencement date, as the exchanged options, provided that any vesting

that would have occurred prior to January 1, 2016 will cumulate and cliff vest on

January 1, 2016

Example:

If you tendered an option for exchange that covered 9,600 shares

that vested

monthly over four years from May 1, 2014 (200 shares per month),

your new

option will cover 4,800 shares (based on the two-for-one exchange rate) with the

same vesting rate (1/48, or 100 shares, per month) with a cliff vest of 2,000 shares

on January 1, 2016 and 100 shares vesting per month thereafter until fully vested

on May 1, 2018

Each new option will have the same final vest date as the corresponding eligible

option.

There

will

be

no

vesting

prior

to

January

1,

2016

even

if

the

tendered

option was partially or fully vested at the time of exchange. |

9

TENDER MECHANICS

Complete the Election Form provided to you

•

Election

Form

includes

a

listing

of

all

your

eligible

option

grants

Complete, execute and deliver the Election Form so it is received by Solazyme prior

to the offer termination (9:00 p.m. Pacific Time on February 18,

2015)

Delivery options:

•

Via

electronic

delivery

to

options-exchange@solazyme.com

•

Via

facsimile

to

650-989-6700

Attn:

Idalina

Chan

•

Via

mail

courier

or

hand

delivery

to:

Solazyme,

225

Gateway

Boulevard,

South

San

Francisco,

CA

94080

Attn:

Idalina

Chan

Election Form must be received by the offer termination.

If you do not wish to participate in the offering you need not do anything and your

existing options will remain outstanding with their current terms and exercise

price. |

10

WHERE TO GO FOR HELP

For a complete description of the exchange offer, terms and mechanics please review the

exchange offer documents (in particular the Offer to Exchange) found at:

•

https://intranet.internal.solazyme.com/index.php/Options-Exchange

For questions on the exchange offer please call:

•

Paul

Quinlan;

•

Lori

Urushima;

•

Megan

Comport;

or

•

Kathy

Stafford

or send an e-mail with your question(s) to options-exchange@solazyme.com

To review a list of your eligible options please consult your personalized Election

Form. For an additional copy of your Election Form please send an e-mail

request to options- exchange@solazyme.com. |