| Discussion Materials for Goldman Sachs & Co. LLC December 2025 Goldman Sachs does not provide accounting, tax, or legal advice. Notwithstanding anything in this document to the contrary, and except as required to enable compliance with applicable securities law, you (and each of your employees, representatives, and other agents) may disclose to any and all persons the US federal income and state tax treatment and tax structure of the transaction and all materials of any kind (including tax opinions and other tax analyses) that are provided to you relating to such tax treatment and tax structure, without Goldman Sachs imposing any limitation of any kind. |

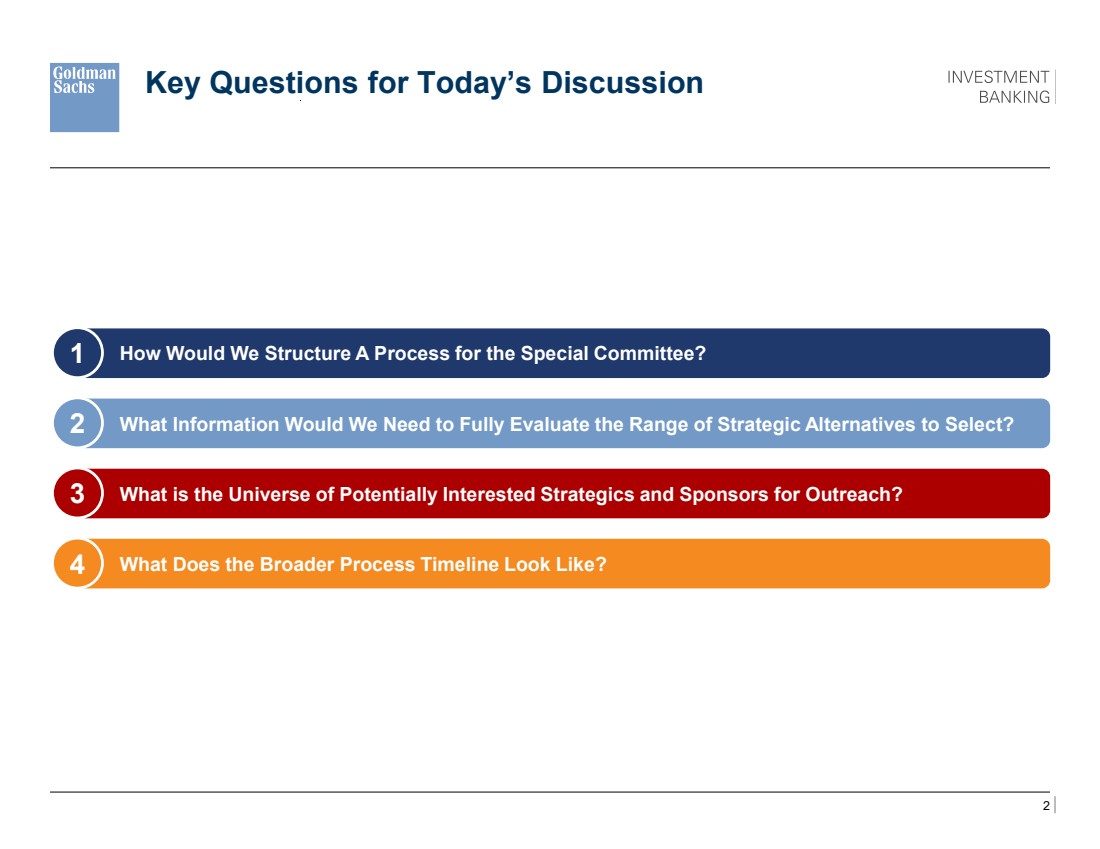

| 2 Key Questions for Today’s Discussion 1 How Would We Structure A Process for the Special Committee? 2 What Information Would We Need to Fully Evaluate the Range of Strategic Alternatives to Select? 3 What is the Universe of Potentially Interested Strategics and Sponsors for Outreach? 4 What Does the Broader Process Timeline Look Like? |

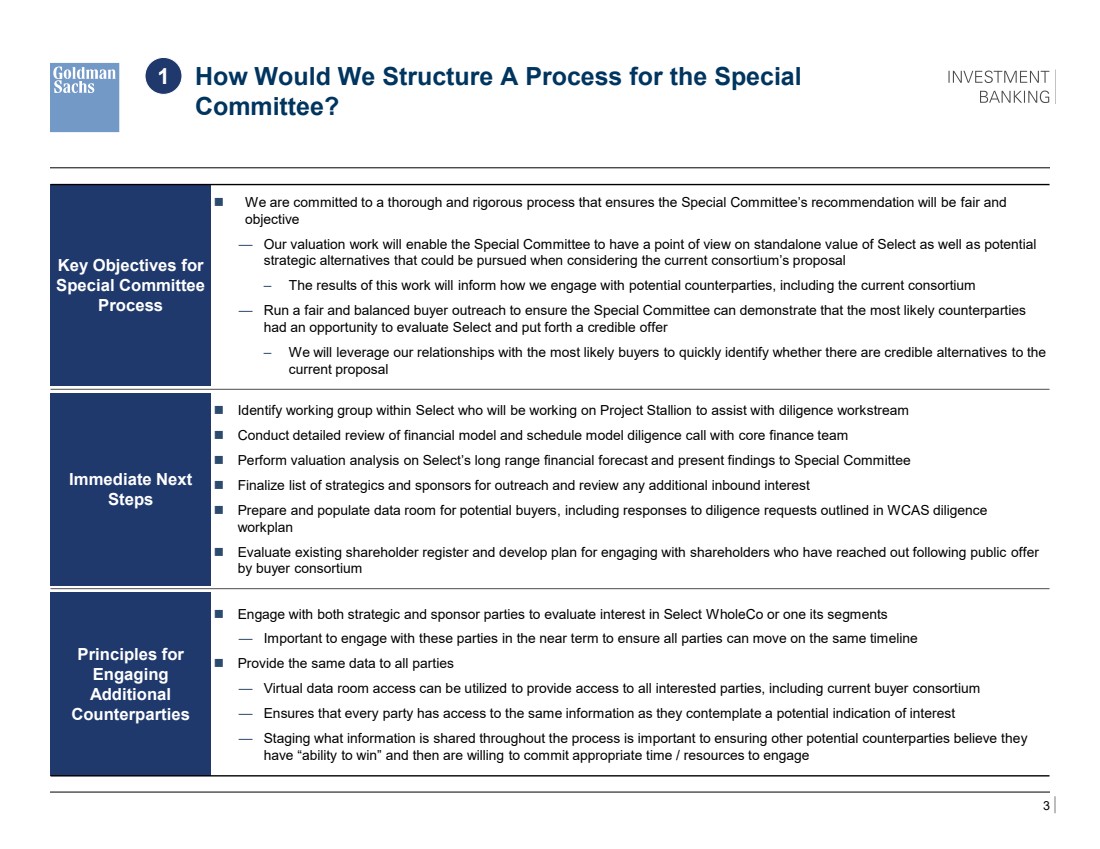

| 3 4 Outside in Perspectives on the Consortium’s Offer & Path Forward 6 Is GS an Independent Advisor and What is the Scope of the GS Engagement? 5 How Can GS Help the Select Special Committee Maximize Value? How Would We Structure A Process for the Special Committee? 1 Key Objectives for Special Committee Process ◼ We are committed to a thorough and rigorous process that ensures the Special Committee’s recommendation will be fair and objective — Our valuation work will enable the Special Committee to have a point of view on standalone value of Select as well as potential strategic alternatives that could be pursued when considering the current consortium’s proposal – The results of this work will inform how we engage with potential counterparties, including the current consortium — Run a fair and balanced buyer outreach to ensure the Special Committee can demonstrate that the most likely counterparties had an opportunity to evaluate Select and put forth a credible offer – We will leverage our relationships with the most likely buyers to quickly identify whether there are credible alternatives to the current proposal Immediate Next Steps ◼ Identify working group within Select who will be working on Project Stallion to assist with diligence workstream ◼ Conduct detailed review of financial model and schedule model diligence call with core finance team ◼ Perform valuation analysis on Select’s long range financial forecast and present findings to Special Committee ◼ Finalize list of strategics and sponsors for outreach and review any additional inbound interest ◼ Prepare and populate data room for potential buyers, including responses to diligence requests outlined in WCAS diligence workplan ◼ Evaluate existing shareholder register and develop plan for engaging with shareholders who have reached out following public offer by buyer consortium Principles for Engaging Additional Counterparties ◼ Engage with both strategic and sponsor parties to evaluate interest in Select WholeCo or one its segments — Important to engage with these parties in the near term to ensure all parties can move on the same timeline ◼ Provide the same data to all parties — Virtual data room access can be utilized to provide access to all interested parties, including current buyer consortium — Ensures that every party has access to the same information as they contemplate a potential indication of interest — Staging what information is shared throughout the process is important to ensuring other potential counterparties believe they have “ability to win” and then are willing to commit appropriate time / resources to engage |

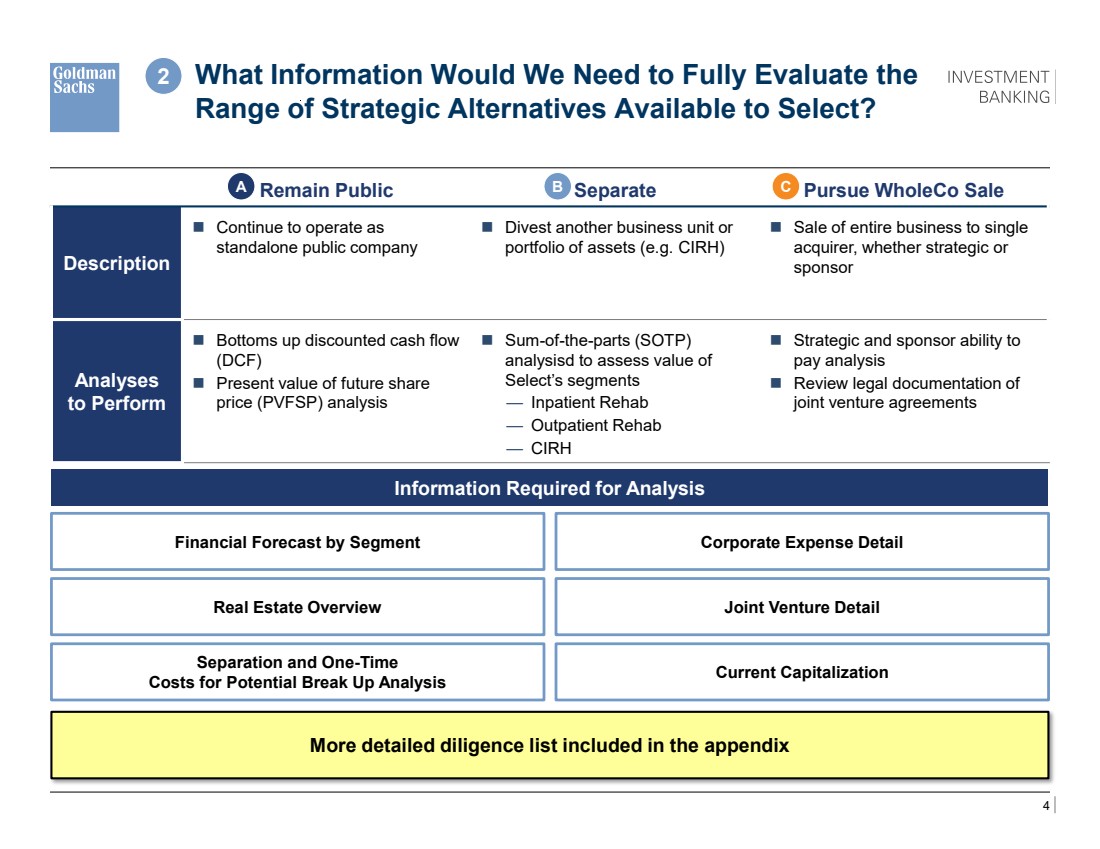

| 4 4 Outside in Perspectives on the Consortium’s Offer & Path Forward 6 Is GS an Independent Advisor and What is the Scope of the GS Engagement? 5 How Can GS Help the Select Special Committee Maximize Value? What Information Would We Need to Fully Evaluate the Range of Strategic Alternatives Available to Select? 2 Remain Public Separate Pursue WholeCo Sale Description ◼ Continue to operate as standalone public company ◼ Divest another business unit or portfolio of assets (e.g. CIRH) ◼ Sale of entire business to single acquirer, whether strategic or sponsor Analyses to Perform ◼ Bottoms up discounted cash flow (DCF) ◼ Present value of future share price (PVFSP) analysis ◼ Sum-of-the-parts (SOTP) analysisd to assess value of Select’s segments — Inpatient Rehab — Outpatient Rehab — CIRH ◼ Strategic and sponsor ability to pay analysis ◼ Review legal documentation of joint venture agreements A B C Information Required for Analysis More detailed diligence list included in the appendix Financial Forecast by Segment Corporate Expense Detail Real Estate Overview Joint Venture Detail Separation and One-Time Costs for Potential Break Up Analysis Current Capitalization |

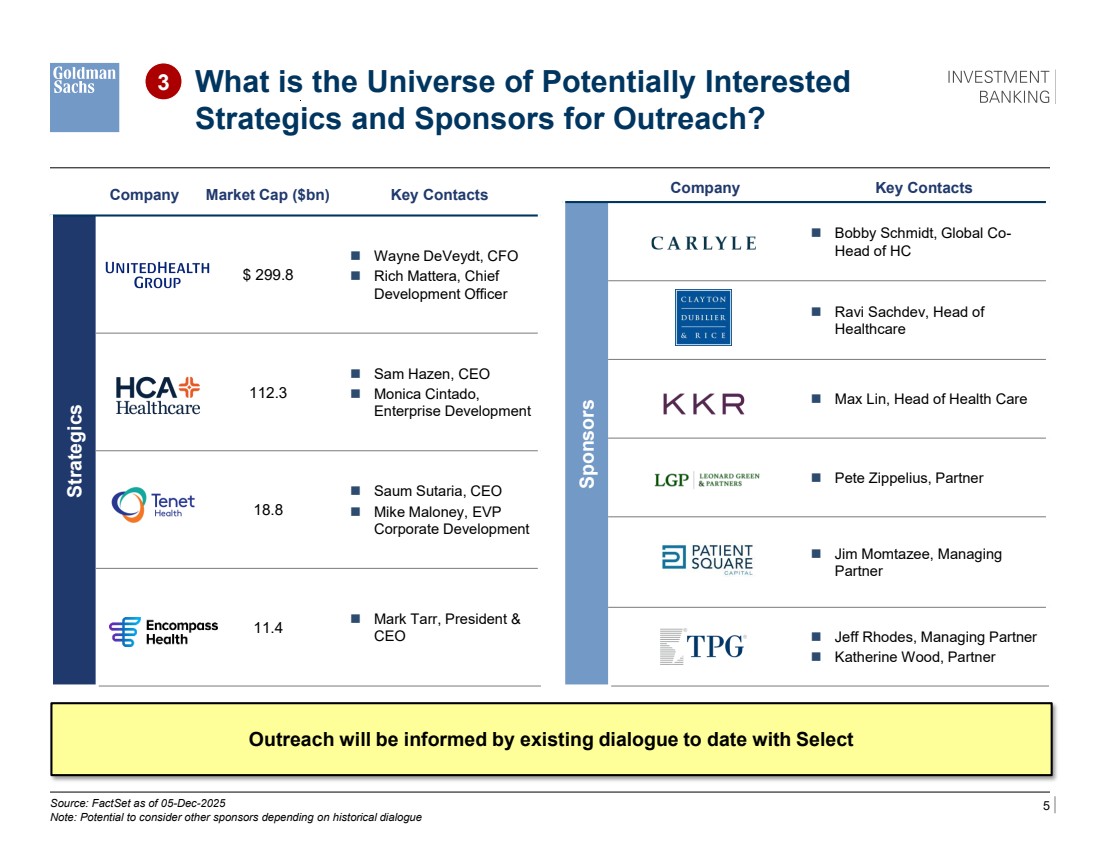

| 5 Company Key Contacts Sponsors Carlyle ◼ Bobby Schmidt, Global Co-Head of HC CD&R ◼ Ravi Sachdev, Head of Healthcare LGP ◼ Max Lin, Head of Health Care Patient Square ◼ Pete Zippelius, Partner Towerbookook ◼ Jim Momtazee, Managing Partner TPG ◼ Jeff Rhodes, Managing Partner ◼ Katherine Wood, Partner What is the Universe of Potentially Interested Strategics and Sponsors for Outreach? Company Market Cap ($bn) Key Contacts Strategics UNH $ 299.8 ◼ Wayne DeVeydt, CFO ◼ Rich Mattera, Chief Development Officer HCA 112.3 ◼ Sam Hazen, CEO ◼ Monica Cintado, Enterprise Development THC 18.8 ◼ Saum Sutaria, CEO ◼ Mike Maloney, EVP Corporate Development Encompass 11.4 ◼ Mark Tarr, President & CEO 3 Outreach will be informed by existing dialogue to date with Select Source: FactSet as of 05-Dec-2025 Note: Potential to consider other sponsors depending on historical dialogue |

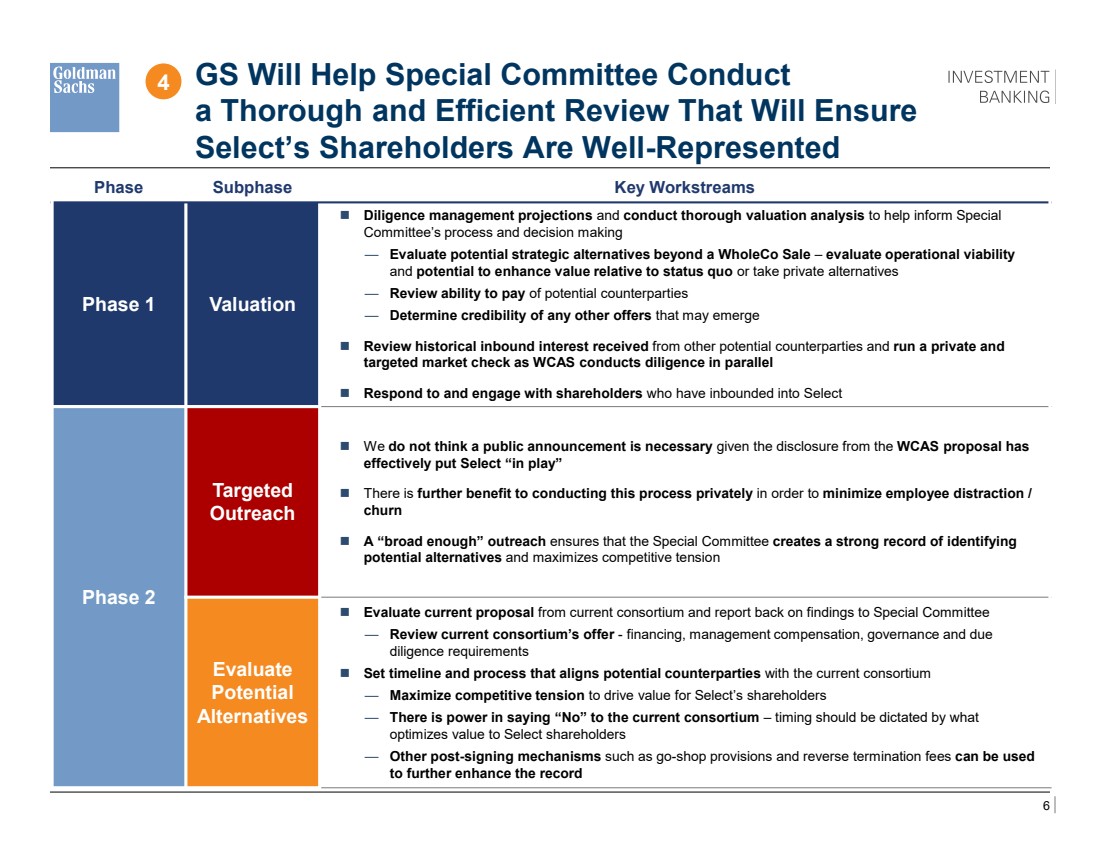

| 6 GS Will Help Special Committee Conduct a Thorough and Efficient Review That Will Ensure Select’s Shareholders Are Well-Represented 4 Guiding Principles ◼ Demonstrate independence and rigor in process in a way that will stand up to public scrutiny and potential litigation ◼ Explore all potential value maximizing alternatives beyond a WholeCo sale ◼ Demand transparency from current consortium on key deal terms ◼ Develop timeline and move forward efficiently, but do not let insider timing pressures drive process Potential ◼ Diligence management projections and conduct valuation analysis to help inform Special Committee’s process and decision making — Evaluate all potential strategic alternatives beyond a WholeCo Sale – evaluate operational viability and potential to enhance value relative to status quo or take private alternatives — Review ability to pay of potential counterparties — Determine credibility of any other offers that may emerge ◼ Review historical inbound interest received from other potential counterparties and run a private and targeted market check — We do not think a public announcement is necessary given the disclosure from the WCAS proposal has effectively put Select “in play” — There is further benefit to conducting this process privately in order to minimize employee distraction / churn — A “broad enough” outreach ensures that the Special Committee and maximize competitive tension ◼ Evaluate current proposal from current consortium — Review current consortium’s offer - financing, management compensation, governance and due diligence requirements ◼ Set timeline and process that aligns potential counterparties with the current consortium — Maximize competitive tension to drive value for Select’s shareholders — There is power in saying “No” to the current consortium – timing should be dictated by what optimizes value to Select shareholders — Other post-signing mechanisms such as go-shop provisions and reverse termination fees record Phase Subphase Key Workstreams Phase 1 Valuation ◼ Diligence management projections and conduct thorough valuation analysis to help inform Special Committee’s process and decision making — Evaluate potential strategic alternatives beyond a WholeCo Sale – evaluate operational viability and potential to enhance value relative to status quo or take private alternatives — Review ability to pay of potential counterparties — Determine credibility of any other offers that may emerge ◼ Review historical inbound interest received from other potential counterparties and run a private and targeted market check as WCAS conducts diligence in parallel ◼ Respond to and engage with shareholders who have inbounded into Select Phase 2 Targeted Outreach ◼ We do not think a public announcement is necessary given the disclosure from the WCAS proposal has effectively put Select “in play” ◼ There is further benefit to conducting this process privately in order to minimize employee distraction / churn ◼ A “broad enough” outreach ensures that the Special Committee creates a strong record of identifying potential alternatives and maximizes competitive tension Evaluate Potential Alternatives ◼ Evaluate current proposal from current consortium and report back on findings to Special Committee — Review current consortium’s offer - financing, management compensation, governance and due diligence requirements ◼ Set timeline and process that aligns potential counterparties with the current consortium — Maximize competitive tension to drive value for Select’s shareholders — There is power in saying “No” to the current consortium – timing should be dictated by what optimizes value to Select shareholders — Other post-signing mechanisms such as go-shop provisions and reverse termination fees can be used to further enhance the record 4 |

| 7 Perspectives on How Process May Unfold from Here ◼ The current consortium has engaged Bain and outlined the diligence they will need to complete in order to be ready to submit an updated proposal ◼ Focus is on understanding opportunity by segment and the potential to unlock value via a sum-of-the-parts analysis ◼ Our perspective is that the details requested are appropriate, but will require significant commitment from Select management in order to finalize due diligence ◼ We understand and recommend that Select is preparing information to be responsive to WCAS requests today, but not to immediately engage with them on their diligence roadmap for the following reasons — Important for the Special Committee to have a point of view on Select’s standalone valuation before committing additional time and resources to this proposal — Enables a process where all parties can be moving forward on the same timeline which can help create competitive tension ◼ The Special Committee retains flexibility to accelerate work with the current consortium once it has a point of view on valuation — Furthermore, potential to further negotiate on value as a gating item for additional access / information sharing 4 |

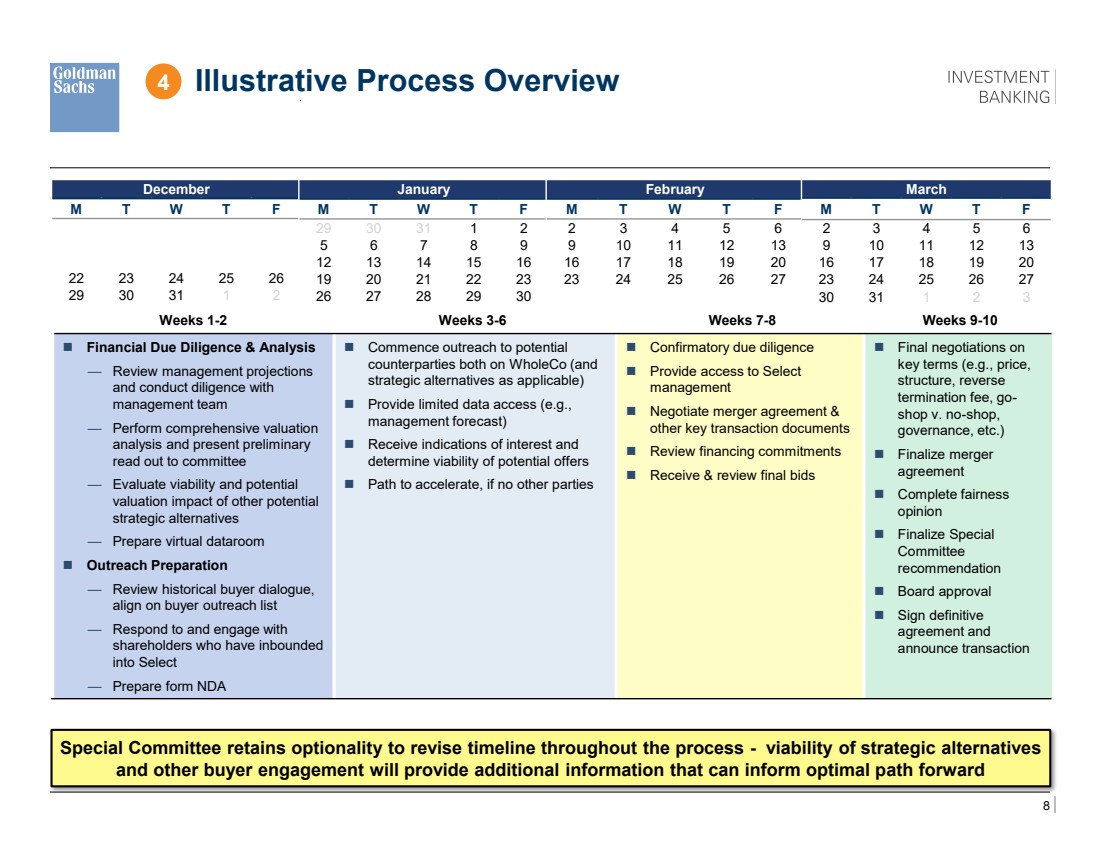

| 8 Illustrative Process Overview Weeks 1-2 Weeks 3-6 Weeks 7-8 Weeks 9-10 ◼ Financial Due Diligence & Analysis — Review management projections and conduct diligence with management team — Perform comprehensive valuation analysis and present preliminary read out to committee — Evaluate viability and potential valuation impact of other potential strategic alternatives — Prepare virtual dataroom ◼ Outreach Preparation — Review historical buyer dialogue, align on buyer outreach list — Respond to and engage with shareholders who have inbounded into Select — Prepare form NDA ◼ Commence outreach to potential counterparties both on WholeCo (and strategic alternatives as applicable) ◼ Provide limited data access (e.g., management forecast) ◼ Receive indications of interest and determine viability of potential offers ◼ Path to accelerate, if no other parties ◼ Confirmatory due diligence ◼ Provide access to Select management ◼ Negotiate merger agreement & other key transaction documents ◼ Review financing commitments ◼ Receive & review final bids ◼ Final negotiations on key terms (e.g., price, structure, reverse termination fee, go-shop v. no-shop, governance, etc.) ◼ Finalize merger agreement ◼ Complete fairness opinion ◼ Finalize Special Committee recommendation ◼ Board approval ◼ Sign definitive agreement and announce transaction Special Committee retains optionality to revise timeline throughout the process - viability of strategic alternatives and other buyer engagement will provide additional information that can inform optimal path forward 4 December M T W T F 22 23 24 25 26 29 30 31 1 2 January M T W T F 29 30 31 1 2 5 6 7 8 9 12 13 14 15 16 19 20 21 22 23 26 27 28 29 30 February M T W T F 2 3 4 5 6 9 10 11 12 13 16 17 18 19 20 23 24 25 26 27 March M T W T F 2 3 4 5 6 9 10 11 12 13 16 17 18 19 20 23 24 25 26 27 30 31 1 2 3 |

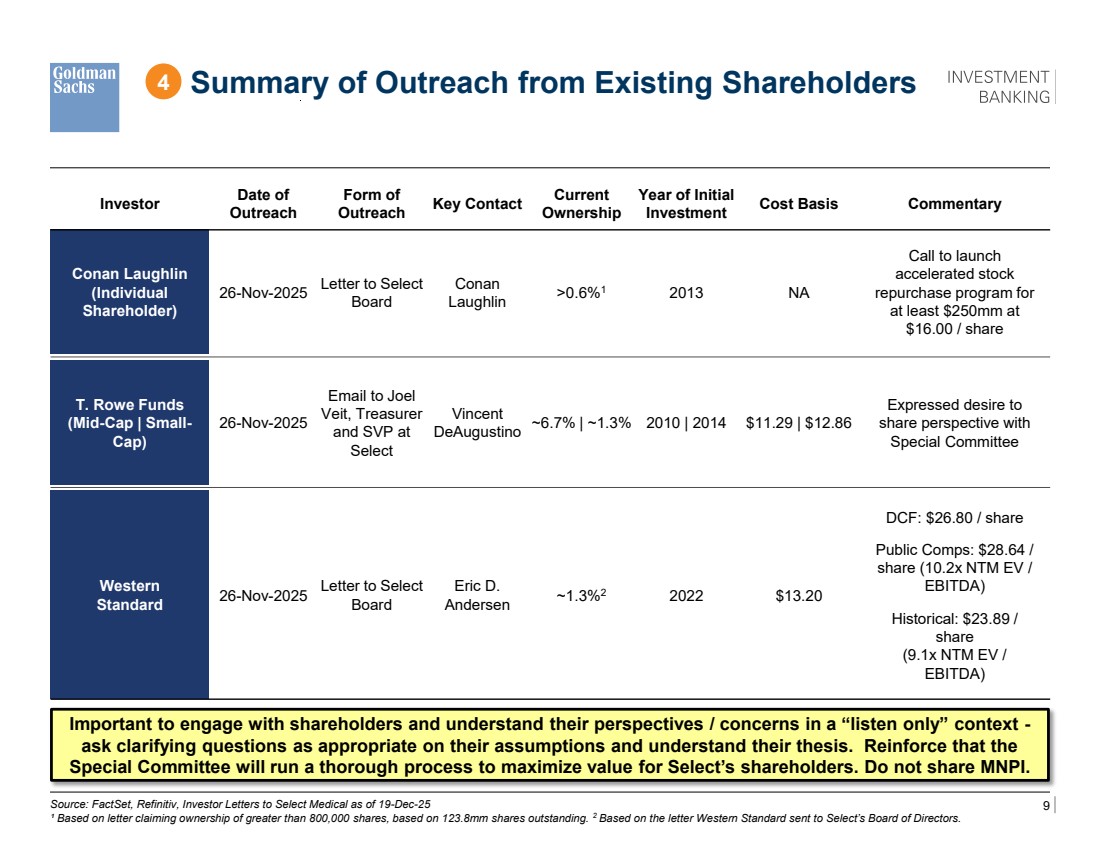

| 9 Summary of Outreach from Existing Shareholders Source: FactSet, Refinitiv, Investor Letters to Select Medical as of 19-Dec-25 ¹ Based on letter claiming ownership of greater than 800,000 shares, based on 123.8mm shares outstanding. 2 Based on the letter Western Standard sent to Select’s Board of Directors. Investor Date of Outreach Form of Outreach Key Contact Current Ownership Year of Initial Investment Cost Basis Commentary Conan Laughlin (Individual Shareholder) 26-Nov-2025 Letter to Select Board Conan Laughlin >0.6%1 2013 NA Call to launch accelerated stock repurchase program for at least $250mm at $16.00 / share T. Rowe Funds (Mid-Cap | Small-Cap) 26-Nov-2025 Email to Joel Veit, Treasurer and SVP at Select Vincent DeAugustino ~6.7% | ~1.3% 2010 | 2014 $11.29 | $12.86 Expressed desire to share perspective with Special Committee Western Standard 26-Nov-2025 Letter to Select Board Eric D. Andersen ~1.3%2 2022 $13.20 DCF: $26.80 / share Public Comps: $28.64 / share (10.2x NTM EV / EBITDA) Historical: $23.89 / share (9.1x NTM EV / EBITDA) 4 Important to engage with shareholders and understand their perspectives / concerns in a “listen only” context - ask clarifying questions as appropriate on their assumptions and understand their thesis. Reinforce that the Special Committee will run a thorough process to maximize value for Select’s shareholders. Do not share MNPI. |

| 10 I Shareholder Base Analysis A Appendix |

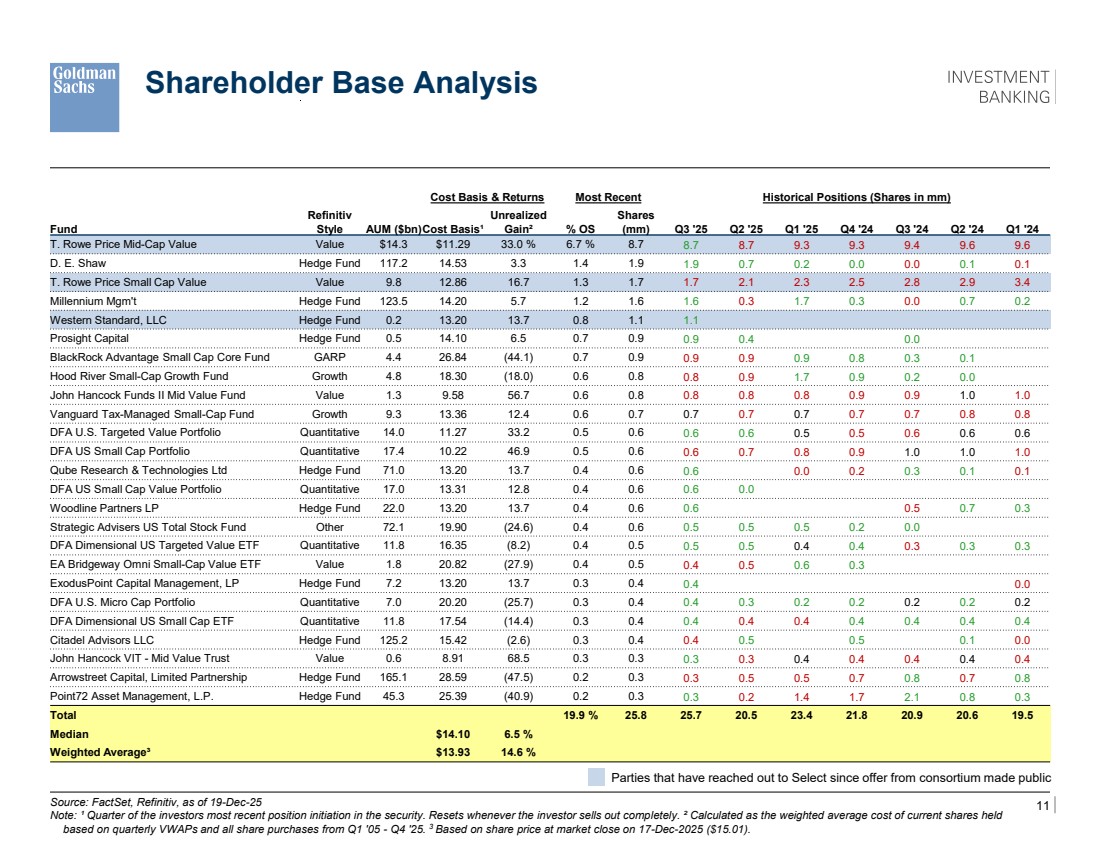

| 11 Shareholder Base Analysis Source: FactSet, Refinitiv, as of 19-Dec-25 Note: ¹ Quarter of the investors most recent position initiation in the security. Resets whenever the investor sells out completely. ² Calculated as the weighted average cost of current shares held based on quarterly VWAPs and all share purchases from Q1 '05 - Q4 '25. 3 Based on share price at market close on 17-Dec-2025 ($15.01). Cost Basis & Returns Most Recent Historical Positions (Shares in mm) Fund Refinitiv Style AUM ($bn)Cost Basis¹ Unrealized Gain² % OS Shares (mm) Q3 '25 Q2 '25 Q1 '25 Q4 '24 Q3 '24 Q2 '24 Q1 '24 T. Rowe Price Mid-Cap Value Value $14.3 $11.29 33.0 % 6.7 % 8.7 8.7 8.7 9.3 9.3 9.4 9.6 9.6 D. E. Shaw Hedge Fund 117.2 14.53 3.3 1.4 1.9 1.9 0.7 0.2 0.0 0.0 0.1 0.1 T. Rowe Price Small Cap Value Value 9.8 12.86 16.7 1.3 1.7 1.7 2.1 2.3 2.5 2.8 2.9 3.4 Millennium Mgm't Hedge Fund 123.5 14.20 5.7 1.2 1.6 1.6 0.3 1.7 0.3 0.0 0.7 0.2 Western Standard, LLC Hedge Fund 0.2 13.20 13.7 0.8 1.1 1.1 Prosight Capital Hedge Fund 0.5 14.10 6.5 0.7 0.9 0.9 0.4 0.0 BlackRock Advantage Small Cap Core Fund GARP 4.4 26.84 (44.1) 0.7 0.9 0.9 0.9 0.9 0.8 0.3 0.1 Hood River Small-Cap Growth Fund Growth 4.8 18.30 (18.0) 0.6 0.8 0.8 0.9 1.7 0.9 0.2 0.0 John Hancock Funds II Mid Value Fund Value 1.3 9.58 56.7 0.6 0.8 0.8 0.8 0.8 0.9 0.9 1.0 1.0 Vanguard Tax-Managed Small-Cap Fund Growth 9.3 13.36 12.4 0.6 0.7 0.7 0.7 0.7 0.7 0.7 0.8 0.8 DFA U.S. Targeted Value Portfolio Quantitative 14.0 11.27 33.2 0.5 0.6 0.6 0.6 0.5 0.5 0.6 0.6 0.6 DFA US Small Cap Portfolio Quantitative 17.4 10.22 46.9 0.5 0.6 0.6 0.7 0.8 0.9 1.0 1.0 1.0 Qube Research & Technologies Ltd Hedge Fund 71.0 13.20 13.7 0.4 0.6 0.6 0.0 0.2 0.3 0.1 0.1 DFA US Small Cap Value Portfolio Quantitative 17.0 13.31 12.8 0.4 0.6 0.6 0.0 Woodline Partners LP Hedge Fund 22.0 13.20 13.7 0.4 0.6 0.6 0.5 0.7 0.3 Strategic Advisers US Total Stock Fund Other 72.1 19.90 (24.6) 0.4 0.6 0.5 0.5 0.5 0.2 0.0 DFA Dimensional US Targeted Value ETF Quantitative 11.8 16.35 (8.2) 0.4 0.5 0.5 0.5 0.4 0.4 0.3 0.3 0.3 EA Bridgeway Omni Small-Cap Value ETF Value 1.8 20.82 (27.9) 0.4 0.5 0.4 0.5 0.6 0.3 ExodusPoint Capital Management, LP Hedge Fund 7.2 13.20 13.7 0.3 0.4 0.4 0.0 DFA U.S. Micro Cap Portfolio Quantitative 7.0 20.20 (25.7) 0.3 0.4 0.4 0.3 0.2 0.2 0.2 0.2 0.2 DFA Dimensional US Small Cap ETF Quantitative 11.8 17.54 (14.4) 0.3 0.4 0.4 0.4 0.4 0.4 0.4 0.4 0.4 Citadel Advisors LLC Hedge Fund 125.2 15.42 (2.6) 0.3 0.4 0.4 0.5 0.5 0.1 0.0 John Hancock VIT - Mid Value Trust Value 0.6 8.91 68.5 0.3 0.3 0.3 0.3 0.4 0.4 0.4 0.4 0.4 Arrowstreet Capital, Limited Partnership Hedge Fund 165.1 28.59 (47.5) 0.2 0.3 0.3 0.5 0.5 0.7 0.8 0.7 0.8 Point72 Asset Management, L.P. Hedge Fund 45.3 25.39 (40.9) 0.2 0.3 0.3 0.2 1.4 1.7 2.1 0.8 0.3 Total 19.9 % 25.8 25.7 20.5 23.4 21.8 20.9 20.6 19.5 Median $14.10 6.5 % Weighted Average³ $13.93 14.6 % Parties that have reached out to Select since offer from consortium made public |

| 12 II Preliminary Diligence Checklist A Appendix |

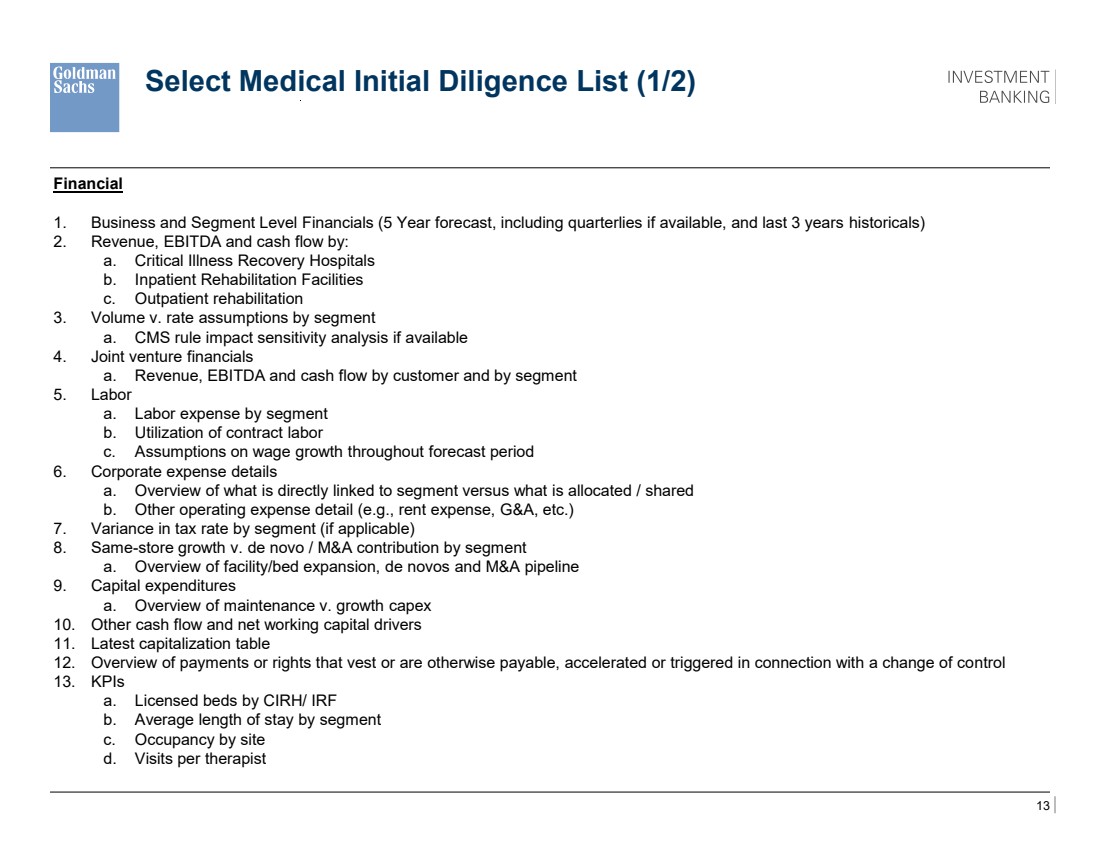

| 13 Select Medical Initial Diligence List (1/2) Financial 1. Business and Segment Level Financials (5 Year forecast, including quarterlies if available, and last 3 years historicals) 2. Revenue, EBITDA and cash flow by: a. Critical Illness Recovery Hospitals b. Inpatient Rehabilitation Facilities c. Outpatient rehabilitation 3. Volume v. rate assumptions by segment a. CMS rule impact sensitivity analysis if available 4. Joint venture financials a. Revenue, EBITDA and cash flow by customer and by segment 5. Labor a. Labor expense by segment b. Utilization of contract labor c. Assumptions on wage growth throughout forecast period 6. Corporate expense details a. Overview of what is directly linked to segment versus what is allocated / shared b. Other operating expense detail (e.g., rent expense, G&A, etc.) 7. Variance in tax rate by segment (if applicable) 8. Same-store growth v. de novo / M&A contribution by segment a. Overview of facility/bed expansion, de novos and M&A pipeline 9. Capital expenditures a. Overview of maintenance v. growth capex 10. Other cash flow and net working capital drivers 11. Latest capitalization table 12. Overview of payments or rights that vest or are otherwise payable, accelerated or triggered in connection with a change of control 13. KPIs a. Licensed beds by CIRH/ IRF b. Average length of stay by segment c. Occupancy by site d. Visits per therapist |

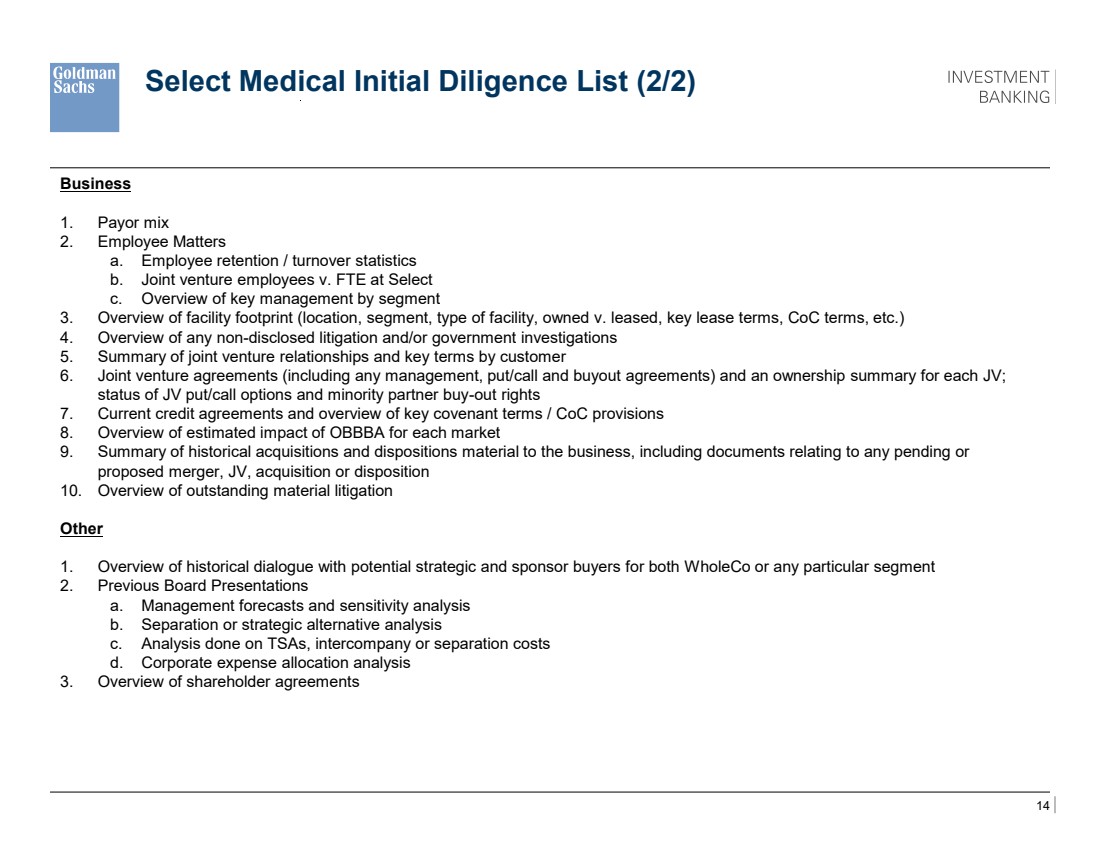

| 14 Select Medical Initial Diligence List (2/2) Business 1. Payor mix 2. Employee Matters a. Employee retention / turnover statistics b. Joint venture employees v. FTE at Select c. Overview of key management by segment 3. Overview of facility footprint (location, segment, type of facility, owned v. leased, key lease terms, CoC terms, etc.) 4. Overview of any non-disclosed litigation and/or government investigations 5. Summary of joint venture relationships and key terms by customer 6. Joint venture agreements (including any management, put/call and buyout agreements) and an ownership summary for each JV; status of JV put/call options and minority partner buy-out rights 7. Current credit agreements and overview of key covenant terms / CoC provisions 8. Overview of estimated impact of OBBBA for each market 9. Summary of historical acquisitions and dispositions material to the business, including documents relating to any pending or proposed merger, JV, acquisition or disposition 10. Overview of outstanding material litigation Other 1. Overview of historical dialogue with potential strategic and sponsor buyers for both WholeCo or any particular segment 2. Previous Board Presentations a. Management forecasts and sensitivity analysis b. Separation or strategic alternative analysis c. Analysis done on TSAs, intercompany or separation costs d. Corporate expense allocation analysis 3. Overview of shareholder agreements |

| 15 III Working Group List A Appendix |

| 16 Working Group List Company / Address Business Phone Stallion, Inc. 4714 Gettysburg Rd Mechanicsburg, PA 17055 Tel: 717-972-1100 Special Committee Daniel J. Thomas Board Member Email: Dan.Thomas@healthcarehighways.com Katherine Davisson Board Member Email: krdavisson@yahoo.com Jim Ely Board Member Email: jim.ely@pricap.com Stallion Special Committee |

| 17 Working Group List Company / Address Business Phone Goldman Sachs & Co. LLC 200 West Street New York, New York 10282 Tel: 212-902-1000 Fax: 212-902-3000 Healthcare Michael Rimland Managing Director Head of Healthcare Services Asst./Sec: Julie Salter Tel: 212-902-3844 Mob: 917-863-9617 Email: michael.rimland@gs.com Tel: 917-343-1658 Email: Julie.salter@gs.com Peter van der Goes Managing Director Co-Head of Healthcare and Head of Healthcare M&A Asst./Sec: Lina Choi Tel: 212-902-1943 Mob: 917-494-9370 Email: peter.vandergoes@gs.com Tel: 212-357-2107 Email: lina.choi@gs.com Jeff McCown Managing Director Asst./Sec: Alyssa Free Tel: 212-357-2825 Mob: 815-514-5160 Email: jeff.mccown@gs.com Tel: 212-934-0712 Email: Alyssa.free@gs.com Jennifer Austin Vice President Asst./Sec: Maria Luevanos Tel: 212-902-1100 Mob: 714-732-2035 Email: jennifer.austin@gs.com Tel: 415-249-7260 Email: maria.luevanos@gs.com Peter Braun Associate Asst./Sec: Sunny Morris Tel: 212-855-0175 Mob: 651-955-3291 Email: peter.braun@gs.com Tel: 312-384-3002 Email: sunny.morris@gs.com Goldman Sachs |

| 18 Company / Address Business Phone Goldman Sachs & Co. LLC 200 West Street New York, New York 10282 Tel: 212-902-1000 Fax: 212-902-3000 Healthcare (Cont’d) Campbell Moriarty Analyst Asst./Sec: Erica Hayden Tel: 212-855-0347 Mob: 973-494-1900 Email: campbell.moriarty@gs.com Tel: 312-384-3381 Email: erica.hayden@gs.com Ashton Rollins Analyst Asst./Sec: Keili Perez Tel: 212-902-7669 Mob: 201-957-3449 Email: ashton.rollins@gs.com Tel: 312-384-3098 Email: keili.perez@gs.com Working Group List Goldman Sachs |

| 19 Company / Address Business Phone Skadden, Arps, Slate, Meagher & Flom One Manhattan West New York, New York 10001 Tel: 212-735-3000 Fax: 212-735-2000 M&A Allison Schneirov Partner Tel: 212-735-4138 Email: Allison.Schneirov@skadden.com Christopher Barlow Partner Tel: 212-735-3972 Email: Christopher.Barlow@skadden.com Jacob Allely Associate Tel: 212-735-2081 Email: Jacob.Allely@skadden.com Sophie Minter Associate Tel: 212-735-3706 Email: Sophie.Minter@skadden.com Litigation Joe Larkin Partner Tel: 302-651-3124 Email: Joseph.Larkin@skadden.com Working Group List Skadden, Arps, Slate, Meagher & Flom |

| 20 IV WCAS Diligence Workplan A Appendix |

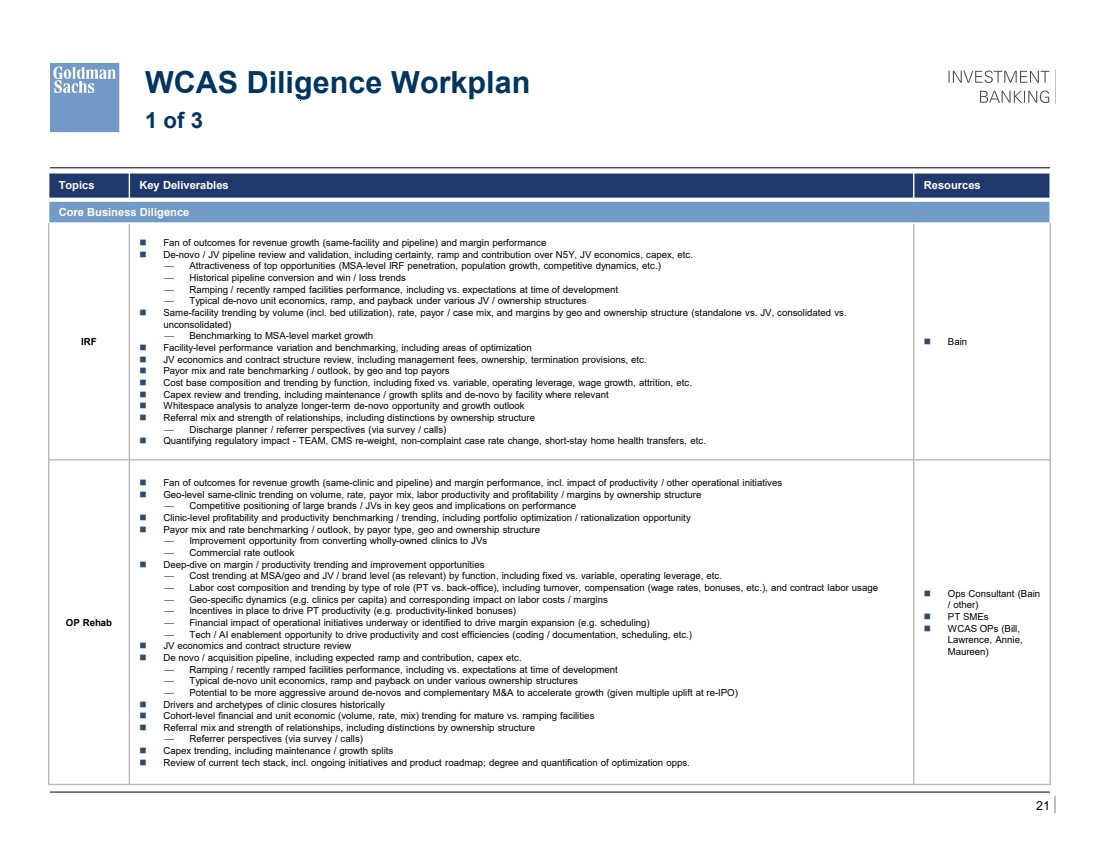

| 21 WCAS Diligence Workplan 1 of 3 Topics Key Deliverables Resources Core Business Diligence IRF ◼ Fan of outcomes for revenue growth (same-facility and pipeline) and margin performance ◼ De-novo / JV pipeline review and validation, including certainty, ramp and contribution over N5Y, JV economics, capex, etc. — Attractiveness of top opportunities (MSA-level IRF penetration, population growth, competitive dynamics, etc.) — Historical pipeline conversion and win / loss trends — Ramping / recently ramped facilities performance, including vs. expectations at time of development — Typical de-novo unit economics, ramp, and payback under various JV / ownership structures ◼ Same-facility trending by volume (incl. bed utilization), rate, payor / case mix, and margins by geo and ownership structure (standalone vs. JV, consolidated vs. unconsolidated) — Benchmarking to MSA-level market growth ◼ Facility-level performance variation and benchmarking, including areas of optimization ◼ JV economics and contract structure review, including management fees, ownership, termination provisions, etc. ◼ Payor mix and rate benchmarking / outlook, by geo and top payors ◼ Cost base composition and trending by function, including fixed vs. variable, operating leverage, wage growth, attrition, etc. ◼ Capex review and trending, including maintenance / growth splits and de-novo by facility where relevant ◼ Whitespace analysis to analyze longer-term de-novo opportunity and growth outlook ◼ Referral mix and strength of relationships, including distinctions by ownership structure — Discharge planner / referrer perspectives (via survey / calls) ◼ Quantifying regulatory impact - TEAM, CMS re-weight, non-complaint case rate change, short-stay home health transfers, etc. ◼ Bain OP Rehab ◼ Fan of outcomes for revenue growth (same-clinic and pipeline) and margin performance, incl. impact of productivity / other operational initiatives ◼ Geo-level same-clinic trending on volume, rate, payor mix, labor productivity and profitability / margins by ownership structure — Competitive positioning of large brands / JVs in key geos and implications on performance ◼ Clinic-level profitability and productivity benchmarking / trending, including portfolio optimization / rationalization opportunity ◼ Payor mix and rate benchmarking / outlook, by payor type, geo and ownership structure — Improvement opportunity from converting wholly-owned clinics to JVs — Commercial rate outlook ◼ Deep-dive on margin / productivity trending and improvement opportunities — Cost trending at MSA/geo and JV / brand level (as relevant) by function, including fixed vs. variable, operating leverage, etc. — Labor cost composition and trending by type of role (PT vs. back-office), including turnover, compensation (wage rates, bonuses, etc.), and contract labor usage — Geo-specific dynamics (e.g. clinics per capita) and corresponding impact on labor costs / margins — Incentives in place to drive PT productivity (e.g. productivity-linked bonuses) — Financial impact of operational initiatives underway or identified to drive margin expansion (e.g. scheduling) — Tech / AI enablement opportunity to drive productivity and cost efficiencies (coding / documentation, scheduling, etc.) ◼ JV economics and contract structure review ◼ De novo / acquisition pipeline, including expected ramp and contribution, capex etc. — Ramping / recently ramped facilities performance, including vs. expectations at time of development — Typical de-novo unit economics, ramp and payback on under various ownership structures — Potential to be more aggressive around de-novos and complementary M&A to accelerate growth (given multiple uplift at re-IPO) ◼ Drivers and archetypes of clinic closures historically ◼ Cohort-level financial and unit economic (volume, rate, mix) trending for mature vs. ramping facilities ◼ Referral mix and strength of relationships, including distinctions by ownership structure — Referrer perspectives (via survey / calls) ◼ Capex trending, including maintenance / growth splits ◼ Review of current tech stack, incl. ongoing initiatives and product roadmap; degree and quantification of optimization opps. ◼ Ops Consultant (Bain / other) ◼ PT SMEs ◼ WCAS OPs (Bill, Lawrence, Annie, Maureen) |

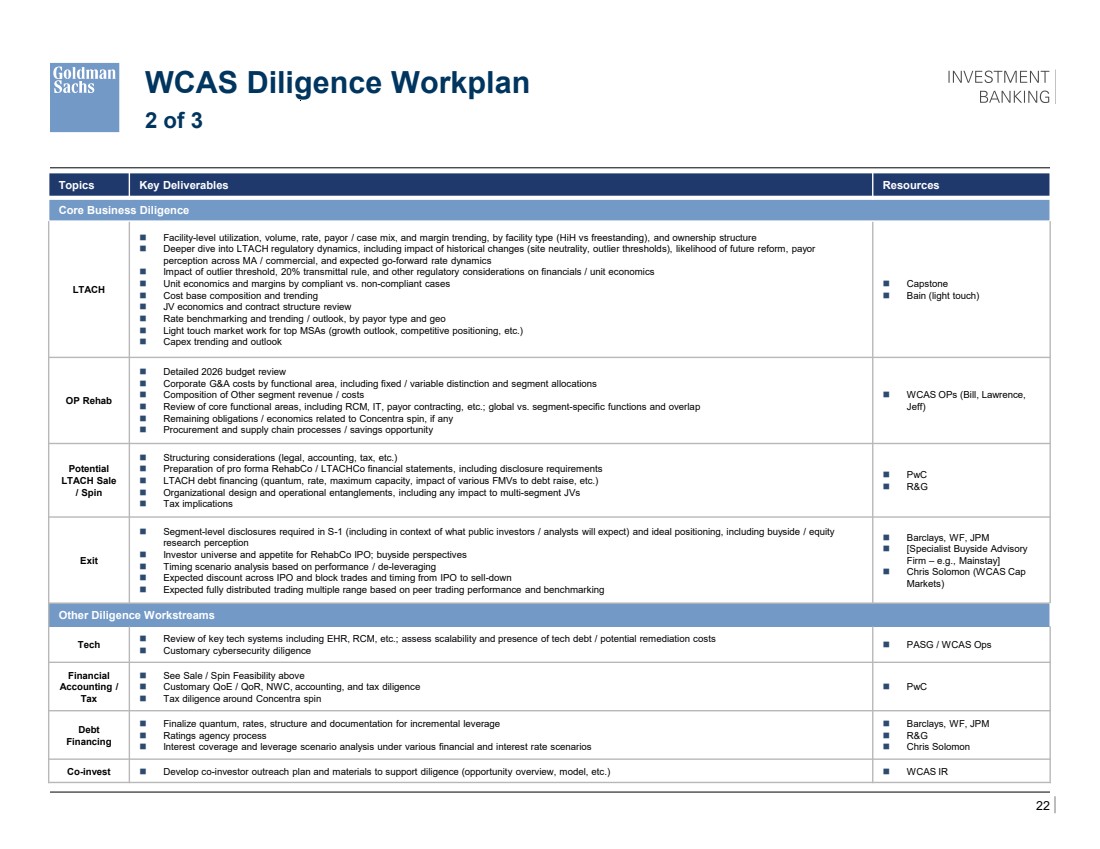

| 22 WCAS Diligence Workplan 2 of 3 Topics Key Deliverables Resources Core Business Diligence LTACH ◼ Facility-level utilization, volume, rate, payor / case mix, and margin trending, by facility type (HiH vs freestanding), and ownership structure ◼ Deeper dive into LTACH regulatory dynamics, including impact of historical changes (site neutrality, outlier thresholds), likelihood of future reform, payor perception across MA / commercial, and expected go-forward rate dynamics ◼ Impact of outlier threshold, 20% transmittal rule, and other regulatory considerations on financials / unit economics ◼ Unit economics and margins by compliant vs. non-compliant cases ◼ Cost base composition and trending ◼ JV economics and contract structure review ◼ Rate benchmarking and trending / outlook, by payor type and geo ◼ Light touch market work for top MSAs (growth outlook, competitive positioning, etc.) ◼ Capex trending and outlook ◼ Capstone ◼ Bain (light touch) OP Rehab ◼ Detailed 2026 budget review ◼ Corporate G&A costs by functional area, including fixed / variable distinction and segment allocations ◼ Composition of Other segment revenue / costs ◼ Review of core functional areas, including RCM, IT, payor contracting, etc.; global vs. segment-specific functions and overlap ◼ Remaining obligations / economics related to Concentra spin, if any ◼ Procurement and supply chain processes / savings opportunity ◼ WCAS OPs (Bill, Lawrence, Jeff) Potential LTACH Sale / Spin ◼ Structuring considerations (legal, accounting, tax, etc.) ◼ Preparation of pro forma RehabCo / LTACHCo financial statements, including disclosure requirements ◼ LTACH debt financing (quantum, rate, maximum capacity, impact of various FMVs to debt raise, etc.) ◼ Organizational design and operational entanglements, including any impact to multi-segment JVs ◼ Tax implications ◼ PwC ◼ R&G Exit ◼ Segment-level disclosures required in S-1 (including in context of what public investors / analysts will expect) and ideal positioning, including buyside / equity research perception ◼ Investor universe and appetite for RehabCo IPO; buyside perspectives ◼ Timing scenario analysis based on performance / de-leveraging ◼ Expected discount across IPO and block trades and timing from IPO to sell-down ◼ Expected fully distributed trading multiple range based on peer trading performance and benchmarking ◼ Barclays, WF, JPM ◼ [Specialist Buyside Advisory Firm – e.g., Mainstay] ◼ Chris Solomon (WCAS Cap Markets) Other Diligence Workstreams Tech ◼ Review of key tech systems including EHR, RCM, etc.; assess scalability and presence of tech debt / potential remediation costs ◼ Customary cybersecurity diligence ◼ PASG / WCAS Ops Financial Accounting / Tax ◼ See Sale / Spin Feasibility above ◼ Customary QoE / QoR, NWC, accounting, and tax diligence ◼ Tax diligence around Concentra spin ◼ PwC Debt Financing ◼ Finalize quantum, rates, structure and documentation for incremental leverage ◼ Ratings agency process ◼ Interest coverage and leverage scenario analysis under various financial and interest rate scenarios ◼ Barclays, WF, JPM ◼ R&G ◼ Chris Solomon Co-invest ◼ Develop co-investor outreach plan and materials to support diligence (opportunity overview, model, etc.) ◼ WCAS IR |

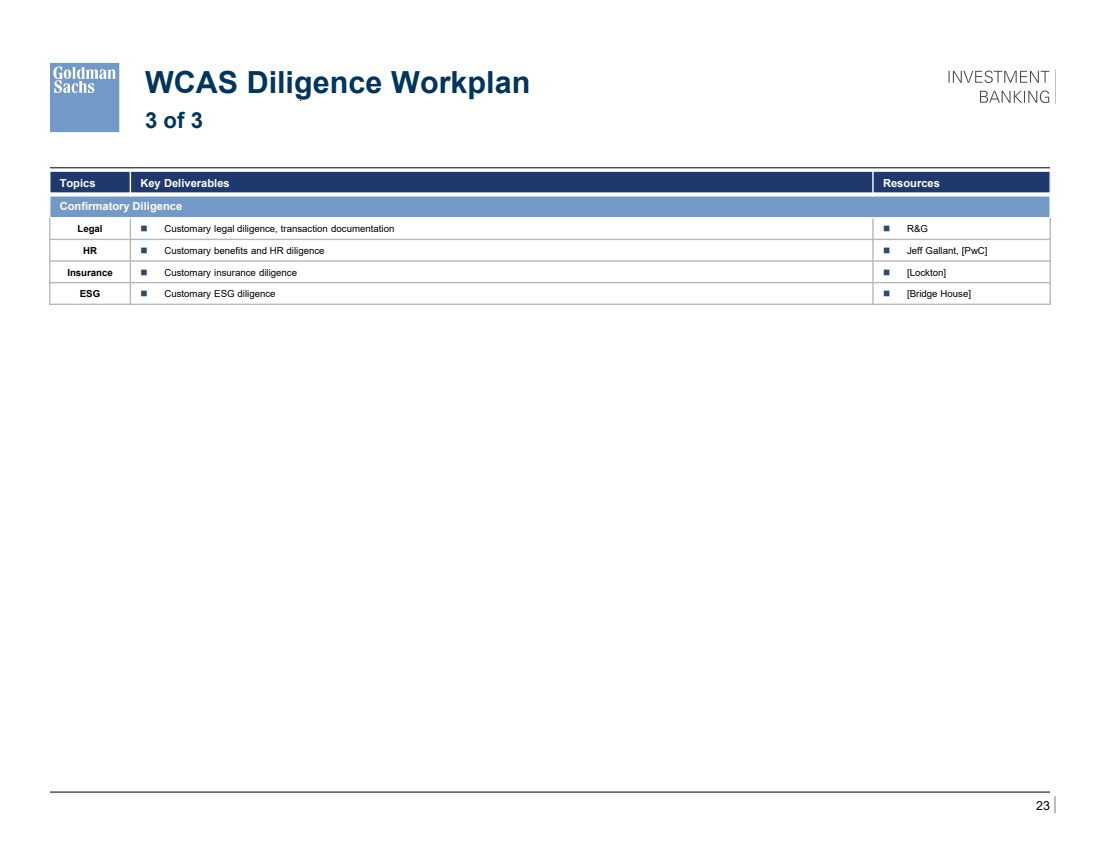

| 23 WCAS Diligence Workplan 3 of 3 Topics Key Deliverables Resources Confirmatory Diligence Legal ◼ Customary legal diligence, transaction documentation ◼ R&G HR ◼ Customary benefits and HR diligence ◼ Jeff Gallant, [PwC] Insurance ◼ Customary insurance diligence ◼ [Lockton] ESG ◼ Customary ESG diligence ◼ [Bridge House] |