| Confidential, Preliminary & Highly Illustrative for Discussion Purposes Materials for the Special Committee Goldman Sachs & Co. LLC January 29th, 2026 Goldman Sachs does not provide accounting, tax, or legal advice. Notwithstanding anything in this document to the contrary, and except as required to enable compliance with applicable securities law, you (and each of your employees, representatives, and other agents) may disclose to any and all persons the US federal income and state tax treatment and tax structure of the transaction and all materials of any kind (including tax opinions and other tax analyses) that are provided to you relating to such tax treatment and tax structure, without Goldman Sachs imposing any limitation of any kind. |

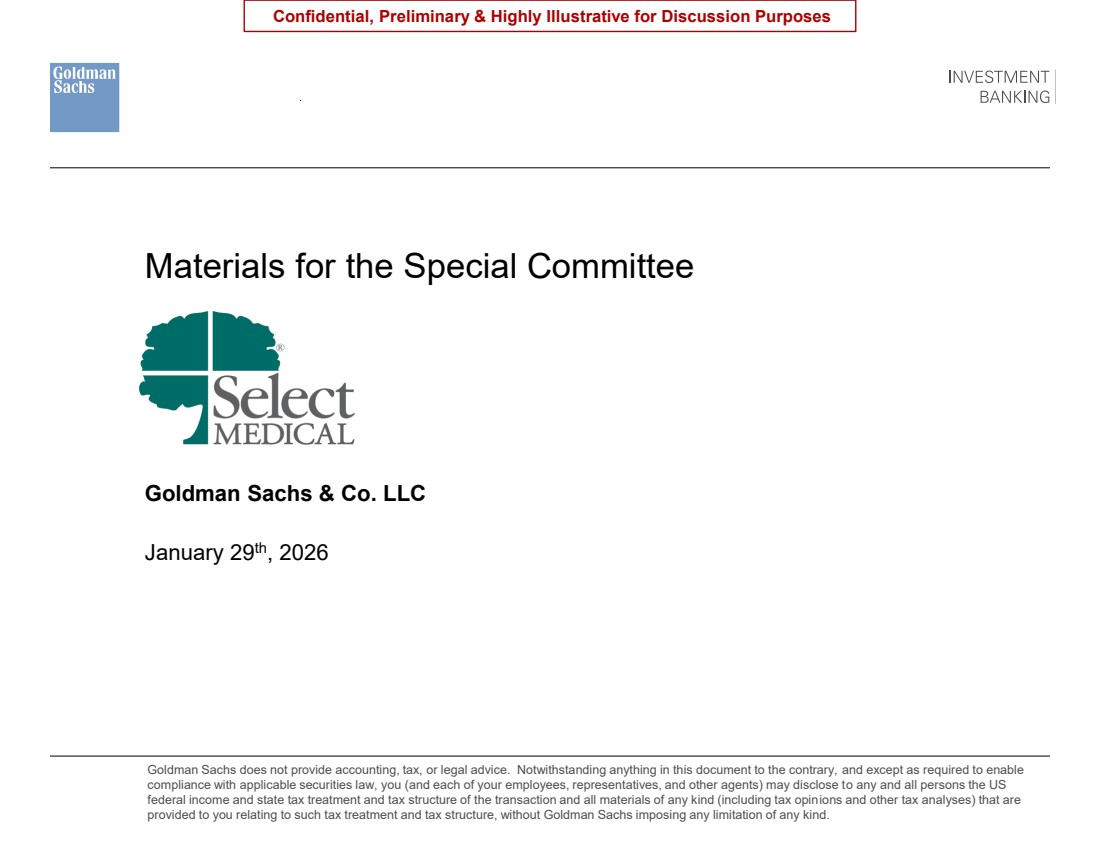

| 1 Confidential, Preliminary & Highly Illustrative for Discussion Purposes 2027 MA Advance Notice Has Resulted in a Material Pullback Across Healthcare Source: FactSet, Market data as of 28-Jan-26 1 Represents delta between closing prices on 26-Jan-26 and 28-Jan-26. 2 Acute care peers include HCA, Tenet, UHS, Community Health, and Ardent. 3 Post acute peers include Encompass, USPH, Enhabit, Addus, Aveanna, OptionCare, Surgery Partners, Davita, and Fresenius. Market Reaction to 2027 MA Advance Notice Key Commentary 2D Stock Price Reaction1 2D EV / NTM EBITDA Delta (2.8)% (0.1)x (9.5)% (1.1)x (2.9)% (0.2)x (11.7)% (0.7)x (9.3)% (0.8)x (26.4)% (2.3)x (7.0)% (0.7)x (16.4)% (1.9)x Acute Care Peer Median2 (1.5)% (0.0)x Post Acute Peer Median3 (3.8)% (0.5)x “CMS released its proposed 2027 Medicare Advantage and Part D Advance Notice on January 26, projecting an average payment increase of just 0.09%, or about $700 million across the Medicare Advantage (MA) program. The proposal fell short on Wall Street’s expectations and quickly influenced insurer stock prices, flagging how closely the industry tracks even small changes in federal payment policy” - Managed Healthcare Executive, 27-Jan-26 “Looking briefly to 2027, the advanced notice published yesterday simply doesn't reflect the reality of medical utilization and cost trends. We will continue to work with CMS to ensure an appropriate final growth rate calculation to avoid a profoundly negative impact on seniors' benefits and access to care. That would be a deeply unfortunate result for a program that already is under funding pressure from the previous administration, despite its track record of success serving seniors and taxpayers” - Timothy Noel, CEO UnitedHealthcare, 27-Jan-26 “These proposed payment policies are about making sure Medicare Advantage works better for the people it serves. By strengthening payment accuracy and modernizing risk adjustment, CMS is helping ensure beneficiaries continue to have affordable plan choices and reliable benefits, while protecting taxpayers from unnecessary spending that is not oriented towards addressing real health needs.” - Dr. Mehmet Oz, CMS Administrator, 27-Jan-26 |

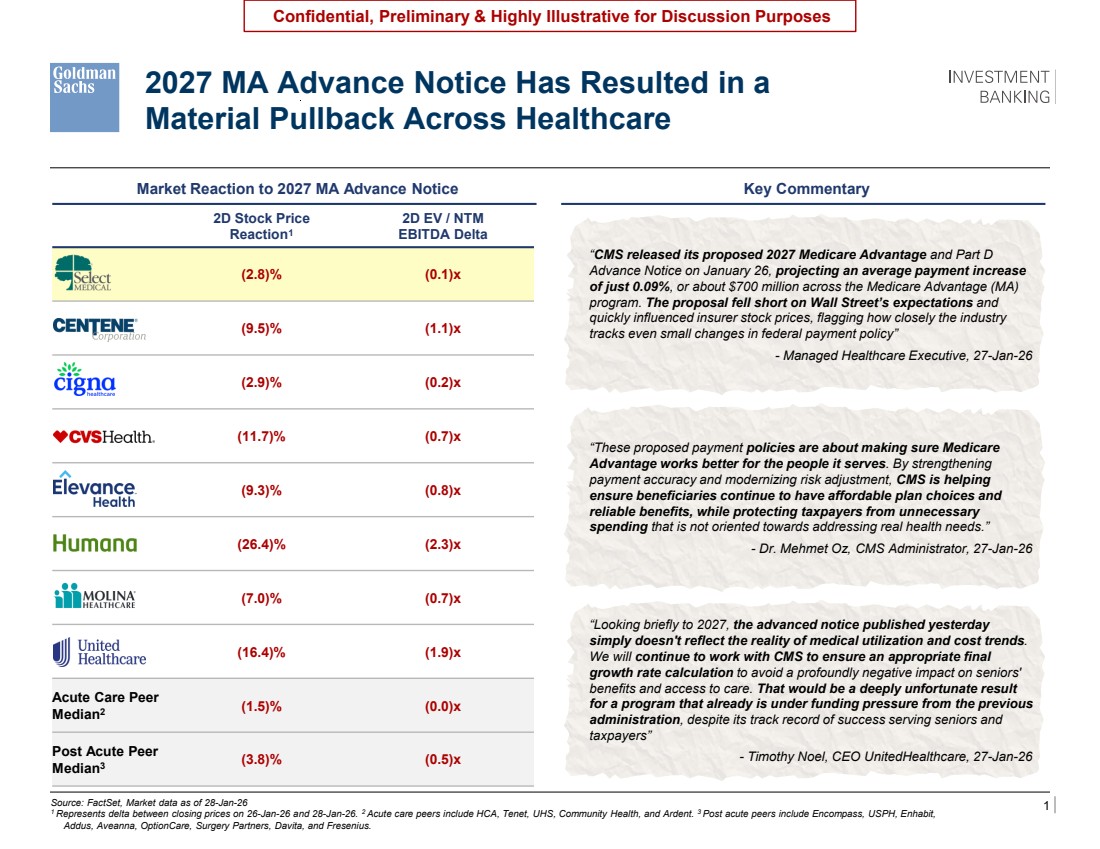

| 2 Confidential, Preliminary & Highly Illustrative for Discussion Purposes Stallion Buyer Consortium Has Been Engaged in Diligence Since Data Room Opened 15-Jan Initial Indication of Interest ◼ $16.00 – $16.20 VDR Users ◼ WCAS: 6 ◼ JP Morgan: 6 ◼ Wells Fargo: 5 ◼ Barclays: 4 ◼ Ropes Gray: 12 ◼ Cravath: 7 ◼ PwC: 8 Documents Available ◼ 8,352 Diligence Calls ✓ 1/27-1/28: Management Presentation ◼ TBC: Discussion on separability of business segments ◼ TBD: Additional calls requests across functional areas (legal, regulatory, tech, etc.) ◼ Operational — Capacity and occupancy metrics — De-novo, JV partnerships, and acquisition pipeline — Clinical quality metrics — Third-party vendor spend ◼ Finance & Accounting — Segment level financials — Financial forecast and underlying assumptions — Corporate costs — Growth vectors across each segment — Strategic JV expansions ◼ Human Resources — Labor productivity metrics — Labor inflation and wage growth — Employee census — Employment-related claims ◼ Legal / Compliance / Tax — Legal structure — Tax returns — Intercompany transactions — LTACH compliance ◼ Technology — Product and service roadmaps — IT spend — Cybersecurity practices — AI strategy Diligence Process Summary Key Areas of Focus \\firmwide.corp.gs.com\ibdroot\projects\IBD-NY\sapient2025\977110_1\Presentations\8. Special Committee Process Update\Excel\Content Engagement Report.xlsx 63% of Diligence Requests Have Been Closed To-Date (160 of 254 Total Requests) |

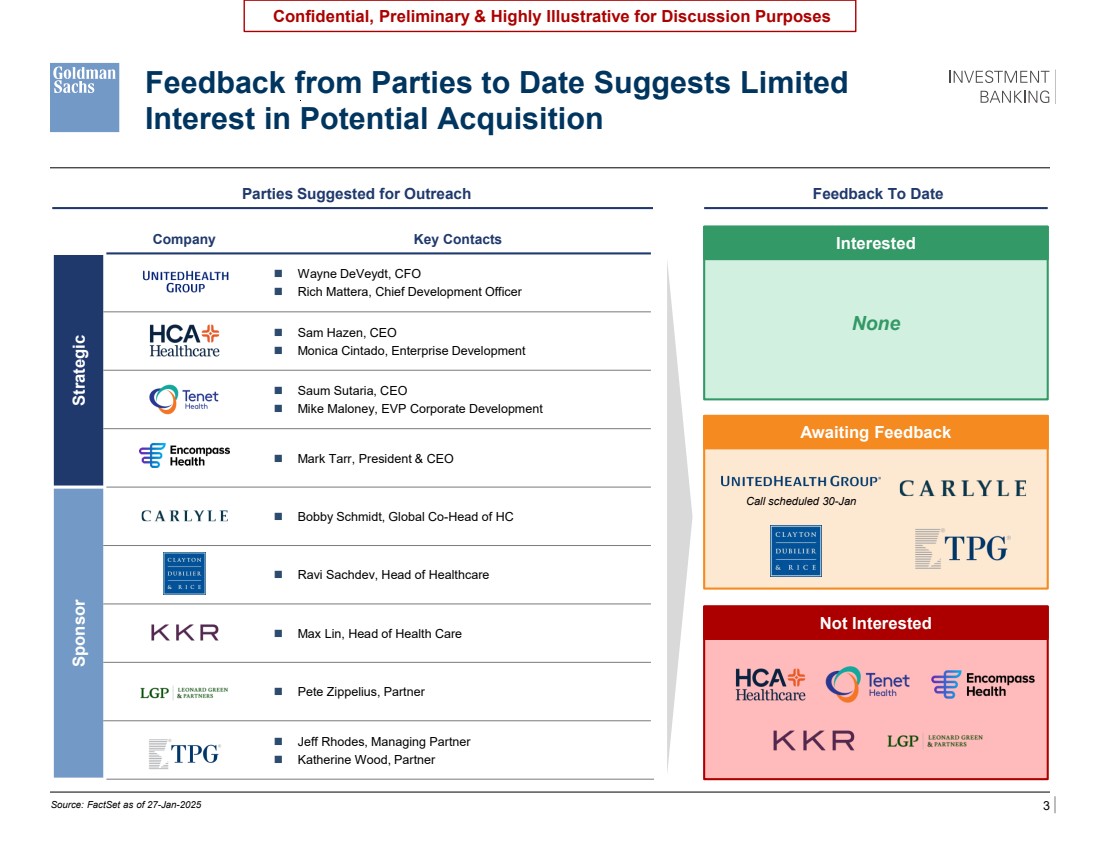

| 3 Confidential, Preliminary & Highly Illustrative for Discussion Purposes Company Key Contacts Strategic UNH ◼ Wayne DeVeydt, CFO ◼ Rich Mattera, Chief Development Officer HCA ◼ Sam Hazen, CEO ◼ Monica Cintado, Enterprise Development THC ◼ Saum Sutaria, CEO ◼ Mike Maloney, EVP Corporate Development Encompass ◼ Mark Tarr, President & CEO Sponsor Carlyle ◼ Bobby Schmidt, Global Co-Head of HC CD&R ◼ Ravi Sachdev, Head of Healthcare KKR ◼ Max Lin, Head of Health Care LGP ◼ Pete Zippelius, Partner TPG ◼ Jeff Rhodes, Managing Partner ◼ Katherine Wood, Partner Would have strategics / sponsors on LHS that we suggested for outreach And then bifurcate RHS into 3 buckets: Interested / Not interested / Awaiting feedback First bucket would have no names Encompass a pass Speaking to United on Friday Tenet encompass and HCA all no LGP and KKR a no so far Cd&r also a no Source: FactSet as of 27-Jan-2025 Parties Suggested for Outreach Feedback To Date Interested None Awaiting Feedback Not Interested Feedback from Parties to Date Suggests Limited Interest in Potential Acquisition Call scheduled 30-Jan |

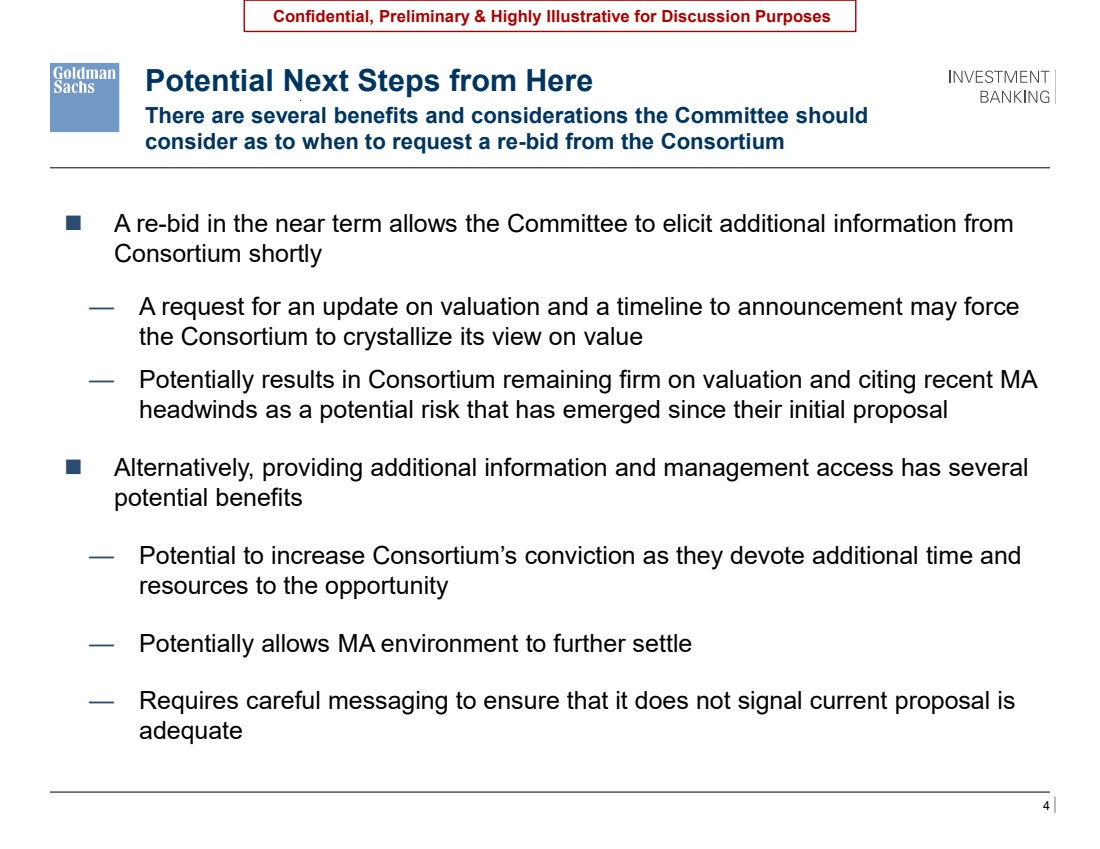

| 4 Confidential, Preliminary & Highly Illustrative for Discussion Purposes Potential Next Steps from Here ◼ Requires buyer consortium to formalize a revised view on value based on information provided since initial bid was submitted in November 2025, indicating their seriousness and conviction in their offer — Allows consortium to outline remaining diligence required to reach announcement ◼ Potential to accelerate overall M&A timeline, with clarity around what additional information and time commitment from management may be needed to complete process Benefits of Requesting Consortium to Re-Bid Based on Diligence to Date Considerations Around Requesting Consortium to Re-Bid Based on Diligence to Date ◼ Potential for buyer consortium to maintain initial bid range without completing thorough due diligence across all functional areas — Additional diligence may be needed for consortium to uncover all potential synergies, growth opportunities, and value creation opportunities with a separation of CIRH ◼ Consortium may view timeline as rushed, with only 1 in-person management presentation completed to date ◼ Additional time could allow consortium to investment more significant time and financial resources into extensive due diligence, demonstrating a higher level of commitment to the transaction, and therefore come back with a potentially higher and more informed bid — Revised bid that results from extensive diligence may be perceived as more credible There are several benefits and considerations the Committee should consider as to when to request a re-bid from the Consortium ◼ A re-bid in the near term allows the Committee to elicit additional information from Consortium shortly — A request for an update on valuation and a timeline to announcement may force the Consortium to crystallize its view on value — Potentially results in Consortium remaining firm on valuation and citing recent MA headwinds as a potential risk that has emerged since their initial proposal ◼ Alternatively, providing additional information and management access has several potential benefits — Potential to increase Consortium’s conviction as they devote additional time and resources to the opportunity — Potentially allows MA environment to further settle — Requires careful messaging to ensure that it does not signal current proposal is adequate |

| 5 Confidential, Preliminary & Highly Illustrative for Discussion Purposes Disclaimer These materials have been prepared and are provided by Goldman Sachs on a confidential basis solely for the information and assistance of the Special Committee of Select Medical Holdings Corporation (the "Company") in connection with their consideration of the matters referred to herein. These materials and Goldman Sachs’ presentation relating to these materials (the “Confidential Information”) may not be disclosed to the third party or circulated or referred to publicly or used for or relied upon for any other purpose without the prior written consent of Goldman Sachs. The Confidential Information was not prepared with a view to public disclosure or to conform to any disclosure standards under any state, federal or international securities laws or other laws, rules or regulations, and Goldman Sachs does not take any responsibility for the use of the Confidential Information by persons other than those set forth above. Notwithstanding anything in this Confidential Information to the contrary, the Company may disclose to any person the US federal income and state income tax treatment and tax structure of any transaction described herein and all materials of any kind (including tax opinions and other tax analyses) that are provided to the Company relating to such tax treatment and tax structure, without Goldman Sachs imposing any limitation of any kind. The Confidential Information has been prepared by Goldman Sachs Investment Banking and is not a product of Goldman Sachs Global Investment Research. Goldman Sachs and its affiliates are engaged in advisory, underwriting and financing, principal investing, sales and trading, research, investment management and other financial and non-financial activities and services for various persons and entities. Goldman Sachs and its affiliates and employees, and funds or other entities they manage or in which they invest or have other economic interest or with which they co-invest, may at any time purchase, sell, hold or vote long or short positions and investments in securities, derivatives, loans, commodities, currencies, credit default swaps and other financial instruments of the Company, any other party to any transaction and any of their respective affiliates or any currency or commodity that may be involved in any transaction. Goldman Sachs Investment Banking maintains regular, ordinary course client service dialogues with clients and potential clients to review events, opportunities, and conditions in particular sectors and industries and, in that connection, Goldman Sachs may make reference to the Company, but Goldman Sachs will not disclose any confidential information received from the Company. The Confidential Information has been prepared based on historical financial information, forecasts and other information obtained by Goldman Sachs from publicly available sources, the management of the Company or other sources (approved for our use by the Company in the case of information from management and non-public information). In preparing the Confidential Information, Goldman Sachs has relied upon and assumed, without assuming any responsibility for independent verification, the accuracy and completeness of all of the financial, legal, regulatory, tax, accounting and other information provided to, discussed with or reviewed by us, and Goldman Sachs does not assume any liability for any such information. Goldman Sachs does not provide accounting, tax, legal or regulatory advice. Goldman Sachs has not made an independent evaluation or appraisal of the assets and liabilities (including any contingent, derivative or off-balance sheet assets and liabilities) of the Company or any other party to any transaction or any of their respective affiliates and has no obligation to evaluate the solvency of the Company or any other party to any transaction under any state or federal laws relating to bankruptcy, insolvency or similar matters. The analyses contained in the Confidential Information do not purport to be appraisals nor do they necessarily reflect the prices at which businesses or securities actually may be sold or purchased. Goldman Sachs’ role in any due diligence review is limited solely to performing such a review as it shall deem necessary to support its own advice and analysis and shall not be on behalf of the Company. Analyses based upon forecasts of future results are not necessarily indicative of actual future results, which may be significantly more or less favorable than suggested by these analyses, and Goldman Sachs does not assume responsibility if future results are materially different from those forecast. The Confidential Information does not address the underlying business decision of the Company to engage in any transaction, or the relative merits of any transaction or strategic alternative referred to herein as compared to any other transaction or alternative that may be available to the Company. The Confidential Information is necessarily based on economic, monetary, market and other conditions as in effect on, and the information made available to Goldman Sachs as of, the date of such Confidential Information and Goldman Sachs assumes no responsibility for updating or revising the Confidential Information based on circumstances, developments or events occurring after such date. The Confidential Information does not constitute any opinion, nor does the Confidential Information constitute a recommendation to the Board, any security holder of the Company or any other person as to how to vote or act with respect to any transaction or any other matter. The Confidential Information, including this disclaimer, are subject to, and governed by, any written agreement between the Company, the Board and/or any committee thereof, on the hand, and Goldman Sachs, on the other hand. The Confidential Information does not address, nor does Goldman Sachs express any view as to, the potential effects of volatility in the credit, financial and stock markets on the Company, any other party to any transaction or any transaction. |