| Confidential, Preliminary & Highly Illustrative for Discussion Purposes Materials for the Special Committee Goldman Sachs & Co. LLC February 25th , 2026 Goldman Sachs does not provide accounting, tax, or legal advice. Notwithstanding anything in this document to the contrary, and except as required to enable compliance with applicable securities law, you (and each of your employees, representatives, and other agents) may disclose to any and all persons the US federal income and state tax treatment and tax structure of the transaction and all materials of any kind (including tax opinions and other tax analyses) that are provided to you relating to such tax treatment and tax structure, without Goldman Sachs imposing any limitation of any kind. |

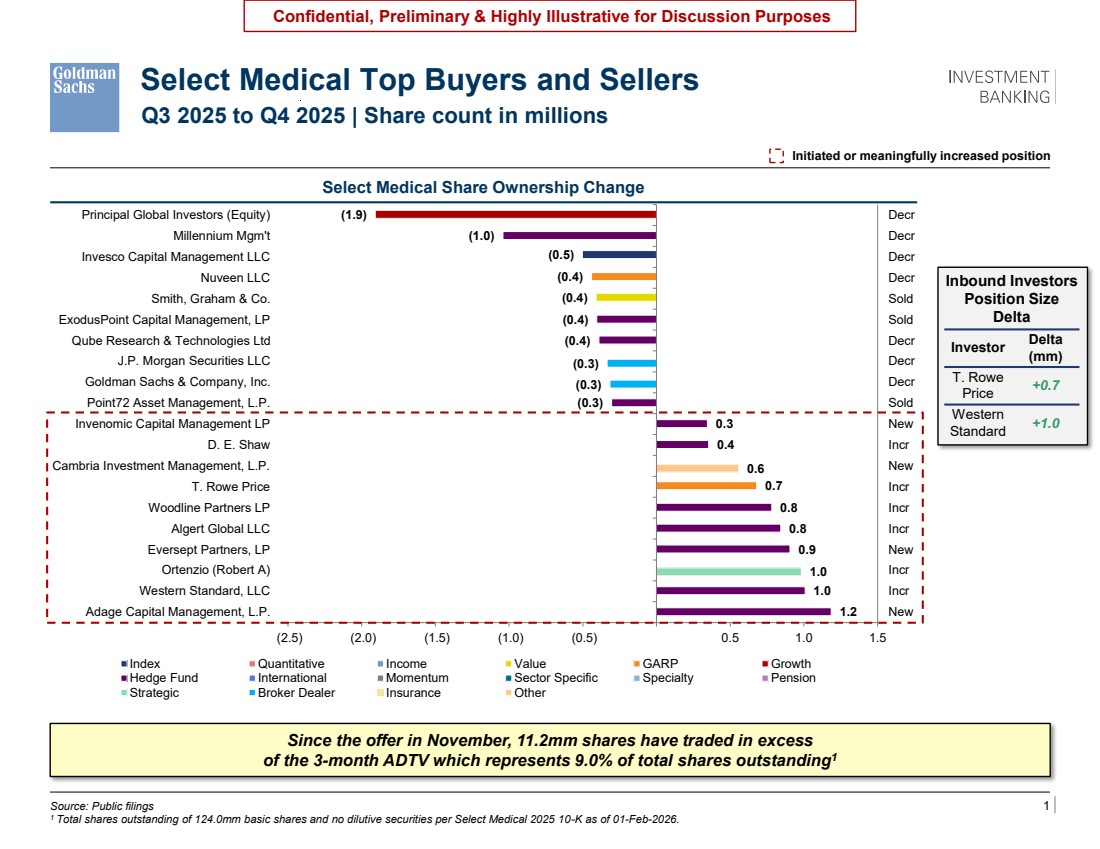

| 1 Confidential, Preliminary & Highly Illustrative for Discussion Purposes Select Medical Top Buyers and Sellers Q3 2025 to Q4 2025 | Share count in millions Inbound Investors Position Size Delta Investor Delta (mm) T. Rowe Price +0.7 Western Standard +1.0 0.6 (0.3) (0.3) 1.0 1.2 1.0 0.9 0.8 0.8 0.4 0.3 (0.3) (0.4) (0.4) (1.0) (1.9) 0.7 (0.4) (0.4) (0.5) New Incr Incr New Incr Incr Incr New Incr New Sold Decr Decr Decr Sold Sold Decr Decr Decr Decr (2.5) (2.0) (1.5) (1.0) (0.5) 0.5 1.0 1.5 Adage Capital Management, L.P. Western Standard, LLC Ortenzio (Robert A) Eversept Partners, LP Algert Global LLC Woodline Partners LP T. Rowe Price Cambria Investment Management, L.P. D. E. Shaw Invenomic Capital Management LP Point72 Asset Management, L.P. Goldman Sachs & Company, Inc. J.P. Morgan Securities LLC Qube Research & Technologies Ltd ExodusPoint Capital Management, LP Smith, Graham & Co. Nuveen LLC Invesco Capital Management LLC Millennium Mgm't Principal Global Investors (Equity) Index Quantitative Income Value GARP Growth Hedge Fund International Momentum Sector Specific Specialty Pension Strategic Broker Dealer Insurance Other Sizes Investor Position Size (mm) DE Shaw 2.2 Woodline 1.3 Adage 1.2 Total 4.7 3.8 %1 Source: Public filings 1 Total shares outstanding of 124.0mm basic shares and no dilutive securities per Select Medical 2025 10-K as of 01-Feb-2026. Select Medical Share Ownership Change Initiated or meaningfully increased position Since the offer in November, 11.2mm shares have traded in excess of the 3-month ADTV which represents 9.0% of total shares outstanding1 |

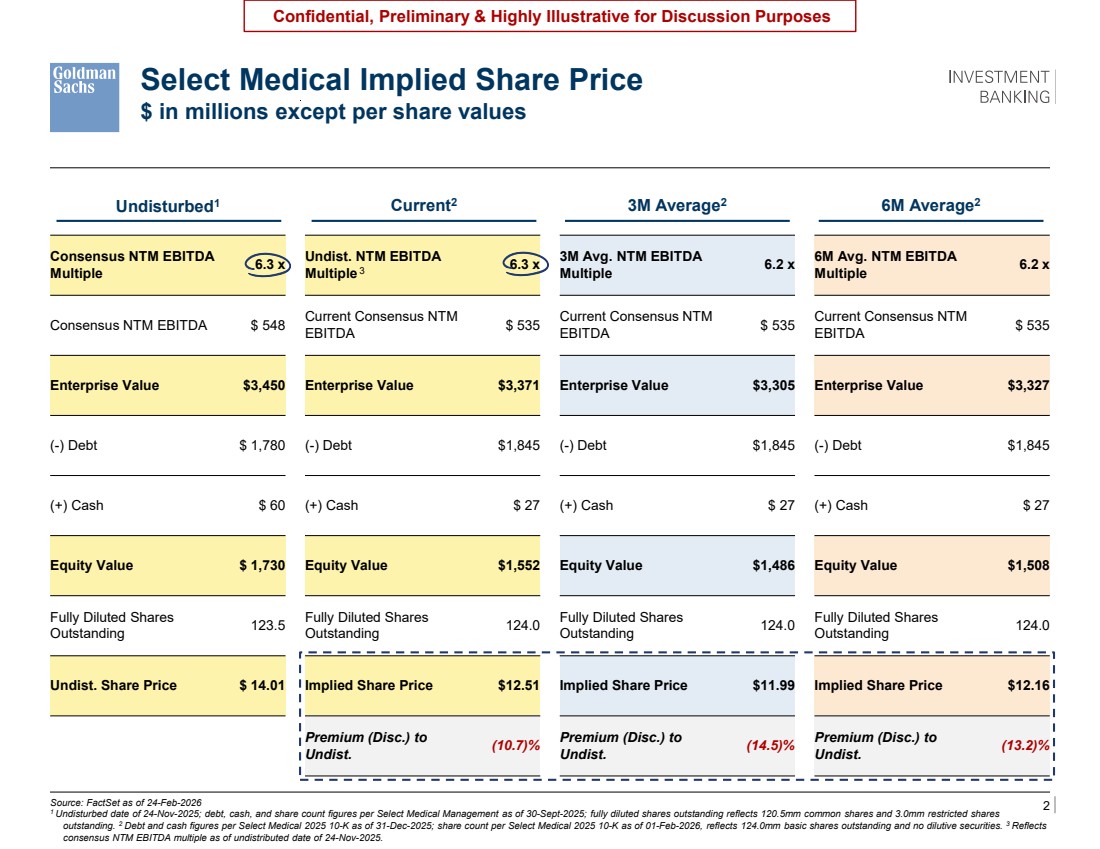

| 2 Confidential, Preliminary & Highly Illustrative for Discussion Purposes Select Medical Implied Share Price $ in millions except per share values Source: FactSet as of 24-Feb-2026 1 Undisturbed date of 24-Nov-2025; debt, cash, and share count figures per Select Medical Management as of 30-Sept-2025; fully diluted shares outstanding reflects 120.5mm common shares and 3.0mm restricted shares outstanding. 2 Debt and cash figures per Select Medical 2025 10-K as of 31-Dec-2025; share count per Select Medical 2025 10-K as of 01-Feb-2026, reflects 124.0mm basic shares outstanding and no dilutive securities. 3 Reflects consensus NTM EBITDA multiple as of undistributed date of 24-Nov-2025. Since the offer in November, 11.2mm shares have traded in excess of the 3-month ADTV which represents 9.0% of total shares outstanding4 Consensus NTM EBITDA Multiple 6.3 x Undist. NTM EBITDA Multiple 6.3 x 3M Avg. NTM EBITDA Multiple 6.2 x 6M Avg. NTM EBITDA Multiple 6.2 x Consensus NTM EBITDA $ 548 Current Consensus NTM EBITDA $ 535 Current Consensus NTM EBITDA $ 535 Current Consensus NTM EBITDA $ 535 Enterprise Value $3,450 Enterprise Value $3,371 Enterprise Value $3,305 Enterprise Value $3,327 (-) Debt $ 1,780 (-) Debt $1,845 (-) Debt $1,845 (-) Debt $1,845 (+) Cash $ 60 (+) Cash $ 27 (+) Cash $ 27 (+) Cash $ 27 Equity Value $ 1,730 Equity Value $1,552 Equity Value $1,486 Equity Value $1,508 Fully Diluted Shares Outstanding 123.5 Fully Diluted Shares Outstanding 124.0 Fully Diluted Shares Outstanding 124.0 Fully Diluted Shares Outstanding 124.0 Undist. Share Price $ 14.01 Implied Share Price $12.51 Implied Share Price $11.99 Implied Share Price $12.16 Premium (Disc.) to Undist. (10.7)% Premium (Disc.) to Undist. (14.5)% Premium (Disc.) to Undist. (13.2)% Undisturbed1 Current2 3M Average2 6M Average2 3 Excel: \\firmwide.corp.gs.com\ibdroot\projects\IBD-NY\sawbones2024\925030_1\Presentations\2025.11.XX Pitch\Excel\Peers_TSR_2025YTD_5Dec2025.XLSM |

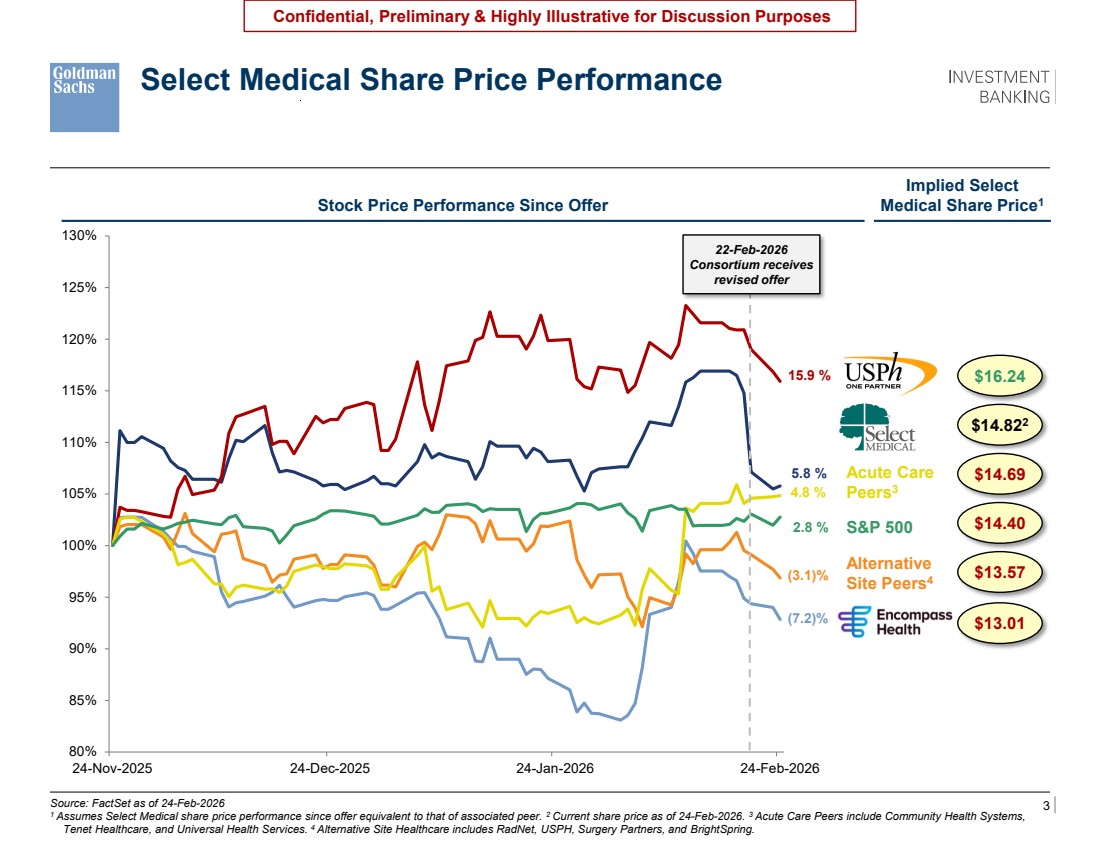

| 3 Confidential, Preliminary & Highly Illustrative for Discussion Purposes Select Medical Share Price Performance Source: FactSet as of 24-Feb-2026 1 Assumes Select Medical share price performance since offer equivalent to that of associated peer. 2 Current share price as of 24-Feb-2026. 3 Acute Care Peers include Community Health Systems, Tenet Healthcare, and Universal Health Services. 4 Alternative Site Healthcare includes RadNet, USPH, Surgery Partners, and BrightSpring. Stock Price Performance Since Offer S&P 500 Acute Care Peers3 80% 85% 90% 95% 100% 105% 110% 115% 120% 125% 130% 24-Nov-2025 24-Dec-2025 24-Jan-2026 24-Feb-2026 4.8 % 2.8 % 5.8 % (3.1)% 15.9 % (7.2)% Alternative Site Peers4 Implied Select Medical Share Price1 $16.24 $14.822 $14.69 $14.40 $13.57 $13.01 05-Feb-2026 Encompass reports 4Q 2025 earnings 22-Feb-2026 Consortium receives revised offer |

| Confidential, Preliminary & Highly Illustrative for Discussion Purposes Materials for the Special Committee Goldman Sachs & Co. LLC February 25 th , 2026 Goldman Sachs does not provide accounting, tax, or legal advice. Notwithstanding anything in this document to the contrary, and except as required to enable compliance with applicable securities law, you (and each of your employees, representatives, and other agents) may disclose to any and all persons the US federal income and state tax treatment and tax structure of the transaction and all materials of any kind (including tax opinions and other tax analyses) that are provided to you relating to such tax treatment and tax structure, without Goldman Sachs imposing any limitation of any kind. |

| 1 Confidential, Preliminary & Highly Illustrative for Discussion Purposes Would have strategics / sponsors on LHS that we suggested for outreach And then bifurcate RHS into 3 buckets: Interested / Not interested / Awaiting feedback First bucket would have no names Encompass a pass Speaking to United on Friday Tenet encompass and HCA all no LGP and KKR a no so far Cd&r also a no Illustrative Talking Points and Potential Q&A ◼ Talking points for Dan in call with Bob — Thank you for your time the other day—it was very helpful for me and for us on the committee — We met as a special committee yesterday to discuss your latest $16 offer, and formally concluded we won’t do a deal at that price — However, we remain open to considering any improved proposal you have — I want to remind you that we have studied value and continue to see value well in excess of your original range — As I mentioned, several of our shareholders share that perspective and have proactively reached out to us to let us know — I also appreciate that this is hard for you, but please remember this is incredibly hard for us on the SC. Doing a deal in and around your original range just isn’t right for all our shareholders. [If appropriate: You yourself have acknowledged you wouldn’t sell at $16] ◼ Potential Q&A — What is it going to take? I told you $17 isn’t ever going to happen. And, maybe I could get to a number a few pennies above our range, but that was it. So, I hope you have thought about that as you answer my question — Option 1: I heard you the other day about where you see value. And I hope you heard me also. I wasn’t negotiating; we think any deal below $17 is incredibly hard. In that light, while we haven’t talked about exactly what number we would accept, nobody on the Committee is comfortable in the low $16’s, and I don’t think we could have a more constructive Committee discussion below the mid-$16’s — Option 2: I heard you very clearly the other day, but I hope you heard me, too. Anything below $17 is hard for us. But at the moment, you are at $16, I told you we are at $17. There is $60mm mid-way between those two points, which is a less than 2% difference from your $16 proposal. If you can’t find $60mm, I doubt we could ever get comfortable. [If appropriate: I’m sure WCAS will be tempted to chisel and test that, but I’m telling you Bob, you are better off getting there, or shutting this down] — It’s not about $60mm, anything above $16/share would require me to find additional equity to fund this transaction and I don’t think that’s feasible based on my conversations with WCAS. They are serious about not having any appetite to go further here — I hear you, and I appreciate that color. However, I’d like to remind you again that my job on the special committee is to do what’s in the best interest of our shareholders – if you’re telling me that based on what I’ve said that there’s not a deal to be done here, I would understand that |

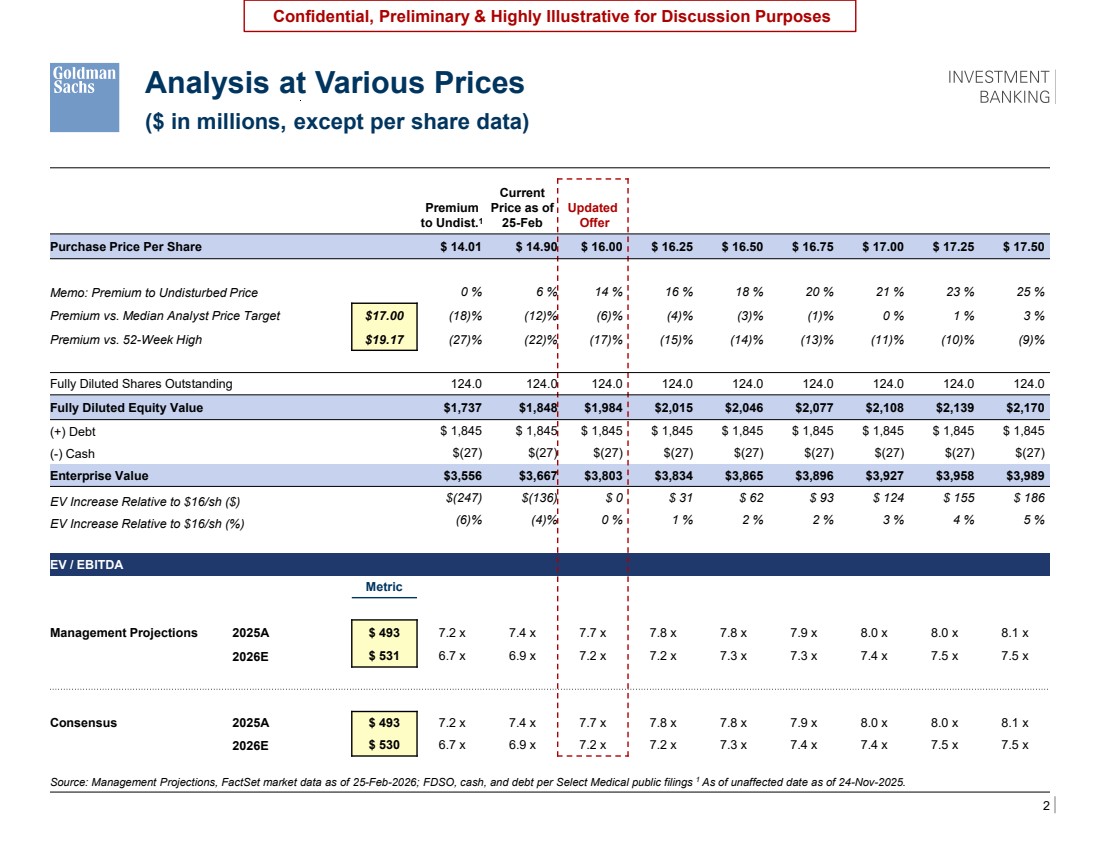

| 2 Confidential, Preliminary & Highly Illustrative for Discussion Purposes Source: Management Projections, FactSet market data as of 25-Feb-2026; FDSO, cash, and debt per Select Medical public filings 1 As of unaffected date as of 24-Nov-2025. Analysis at Various Prices ($ in millions, except per share data) Premium to Undist.1 Current Price as of 25-Feb Updated Offer Purchase Price Per Share $ 14.01 $ 14.90 $ 16.00 $ 16.25 $ 16.50 $ 16.75 $ 17.00 $ 17.25 $ 17.50 Memo: Premium to Undisturbed Price 0 % 6 % 14 % 16 % 18 % 20 % 21 % 23 % 25 % Premium vs. Median Analyst Price Target $17.00 (18)% (12)% (6)% (4)% (3)% (1)% 0 % 1 % 3 % Premium vs. 52-Week High $19.17 (27)% (22)% (17)% (15)% (14)% (13)% (11)% (10)% (9)% Fully Diluted Shares Outstanding 124.0 124.0 124.0 124.0 124.0 124.0 124.0 124.0 124.0 Fully Diluted Equity Value $1,737 $1,848 $1,984 $2,015 $2,046 $2,077 $2,108 $2,139 $2,170 (+) Debt $ 1,845 $ 1,845 $ 1,845 $ 1,845 $ 1,845 $ 1,845 $ 1,845 $ 1,845 $ 1,845 (-) Cash $(27) $(27) $(27) $(27) $(27) $(27) $(27) $(27) $(27) Enterprise Value $3,556 $3,667 $3,803 $3,834 $3,865 $3,896 $3,927 $3,958 $3,989 EV Increase Relative to $16/sh ($) $(247) $(136) $ 0 $ 31 $ 62 $ 93 $ 124 $ 155 $ 186 EV Increase Relative to $16/sh (%) (6)% (4)% 0 % 1 % 2 % 2 % 3 % 4 % 5 % EV / EBITDA Metric Management Projections 2025A $ 493 7.2 x 7.4 x 7.7 x 7.8 x 7.8 x 7.9 x 8.0 x 8.0 x 8.1 x 2026E $ 531 6.7 x 6.9 x 7.2 x 7.2 x 7.3 x 7.3 x 7.4 x 7.5 x 7.5 x Consensus 2025A $ 493 7.2 x 7.4 x 7.7 x 7.8 x 7.8 x 7.9 x 8.0 x 8.0 x 8.1 x 2026E $ 530 6.7 x 6.9 x 7.2 x 7.2 x 7.3 x 7.4 x 7.4 x 7.5 x 7.5 x |