Management's Discussion and Analysis of

Results of Operations and Financial Condition

For the year ended

December 31, 2025

February 19, 2026

INTRODUCTION

This Management's Discussion and Analysis ("MD&A") dated February 19, 2026 is intended to supplement Hudbay Minerals Inc.'s consolidated financial statements and related notes for the year ended December 31, 2025 and 2024 (the "consolidated financial statements"). The consolidated financial statements have been prepared in accordance with IFRS® Accounting Standards ("IFRS" or "GAAP") as issued by the International Accounting Standards Board ("IASB").

References to "Hudbay" or the "Company" refer to Hudbay Minerals Inc. and its direct and indirect subsidiaries as at December 31, 2025.

Readers should be aware that:

- This MD&A contains certain "forward-looking statements" and "forward-looking information" (collectively, "forward-looking information") that are subject to risk factors set out in a cautionary note contained in Hudbay's MD&A.

- This MD&A has been prepared in accordance with the requirements of the securities laws in effect in Canada, which may differ materially from the requirements of United States securities laws applicable to US issuers.

- Hudbay uses a number of non-GAAP financial performance measures in Hudbay's MD&A, which do not have standardized meaning under IFRS. For further information and detailed reconciliations of such measures, please see the discussion under the "Non-GAAP Financial Performance Measures" section herein.

- The technical and scientific information in this MD&A has been approved by qualified persons based on a variety of assumptions and estimates. Please see the discussion under the "Qualified Persons and NI 43-101" section herein.

Readers are also urged to review the "Notes to Reader" section beginning on page 83 of this MD&A.

Additional information regarding Hudbay, including the risks related to its business and those that are reasonably likely to affect its consolidated financial statements in the future, is contained in Hudbay's continuous disclosure materials, including its most recent Annual Information Form, consolidated financial statements and Management Information Circular available on SEDAR+ at www.sedarplus.ca and on EDGAR at www.sec.gov.

All amounts are in US dollars unless otherwise noted.

HUDBAY'S BUSINESS

Hudbay is a copper-focused critical minerals company with three long-life operations and a world-class pipeline of copper growth projects in tier-one mining jurisdictions of Canada, Peru and the United States. Hudbay's operating portfolio includes the Constancia mine in Cusco (Peru), the Snow Lake operations in Manitoba (Canada) and the Copper Mountain mine in British Columbia (Canada). Copper is the primary metal produced by the Company, which is complemented by meaningful gold production and by-product zinc, silver and molybdenum. The Company's growth pipeline includes the Copper World project in Arizona (United States), the Mason project in Nevada (United States), the Llaguen project in La Libertad (Peru) and several expansion and exploration opportunities near its existing operations. Hudbay is governed by the Canada Business Corporations Act and its shares are listed under the symbol "HBM" on the Toronto Stock Exchange, New York Stock Exchange and Bolsa de Valores de Lima.

HUDBAY'S PURPOSE

The value Hudbay creates and the impact it has is embodied in its purpose statement: "We care about our people, our communities and our planet. Hudbay provides the metals the world needs. We work sustainably, transform lives and create better futures for communities."

Hudbay transforms lives: Hudbay invests in its employees, their families and local communities through long-term employment, local procurement and economic development to improve their quality of life and ensure the communities benefit from the Company's presence.

Hudbay operates responsibly: From exploration to closure, Hudbay operates safely and responsibly, welcomes innovation and strives to minimize its environmental footprint while following leading operating practices in all facets of mining.

Hudbay provides critical metals: Hudbay produces copper and other metals needed for everyday products and essential for applications to support the energy transition toward a more sustainable future.

HUDBAY'S STRATEGY

Hudbay's mission is to create sustainable value and strong returns by leveraging its core strengths in community relations, focused exploration, mine development and efficient operations.

The Company believes that copper is the commodity with the best long-term supply/demand fundamentals and offers shareholders the greatest opportunity for sustained risk-adjusted returns. Copper is essential for achieving energy transition and AI technology needs - it is one of the most heavily utilized metals in renewable energy systems and is a key component for power networks, circuit boards and cooling systems in data processing centres. Through the discovery and successful development of economic mineral deposits, and through highly efficient low-cost operations to extract the metals, Hudbay believes sustainable value will be created for all stakeholders.

Hudbay's successful development, ramp-up and operation of the Constancia open-pit mine in Peru, the Company's long history of underground mining and full life-cycle experience in northern Manitoba, its track record of reserve expansion through effective exploration, and its organic pipeline of copper development projects including Copper World and Mason provide the Company with a competitive advantage to deliver sustainable value relative to other mining companies of similar scale.

Over the past decade, Hudbay has built a world-class asset portfolio by executing a consistent long-term growth strategy focused on copper. The Company continuously works to generate strong free cash flow and optimize the value of its producing assets through exploration, brownfield expansion projects and efficient and safe operations. Furthermore, Hudbay intends to sustainably grow through the exploration and development of its robust project pipeline, as well as through the acquisition of other properties that fit the Company's stringent strategic criteria.

To ensure that any investment in existing assets or acquisition of other mineral assets is consistent with the Company's purpose and mission, Hudbay has established a number of criteria for evaluating these opportunities. The criteria include the following:

- Sustainability: Hudbay is focused on jurisdictions that support responsible mining activity. The current geographic focus is on select investment grade countries in the Americas, with strong rule of law and respect for human rights consistent with the Company's long-standing focus on environmental, social and governance ("ESG") principles;

- Copper Focus: Hudbay believes copper is the commodity with the best long-term supply/demand fundamentals. Global copper mine supply is challenged due to declining industry grades, major disruptions at large mines, limited exploration success and an insufficient pipeline of development-ready projects, while demand is expected to continue to increase through global decarbonization initiatives and the rapid growth in AI data processing centres. Hudbay believes this long-term supply/demand gap will create opportunities for increased risk-adjusted returns. While the Company's primary focus is on copper, it recognizes and values the polymetallic nature of copper deposits and, in particular, the complementary benefits of gold in the Company's portfolio;

- Quality: Hudbay is focused on investing in long-life, low-cost, expandable, high-quality assets that can capture peak pricing of multiple commodity price cycles and can generate free cash flow through the troughs of price cycles;

- Potential: Hudbay considers the full spectrum of acquisition and investment opportunities, from early-stage exploration to producing assets, that offer significant incremental potential for exploration, development, expansion and optimization beyond the stated resources and mine plan;

- Process: Hudbay develops a clear understanding of how an investment or acquisition can create value through its robust due diligence and capital allocation process that applies the Company's technical, social, operational and project execution expertise;

- Operatorship: Hudbay believes value is created through leveraging its competitive advantages in safe and efficient operations, effective exploration, proven project development and strong community relations. While operatorship is a key criterion, Hudbay is open to joint ventures and partnerships that de-risk its portfolio and increase risk-adjusted returns; and

- Capital Allocation: Hudbay pursues investments and acquisitions that are accretive on a per share basis. Given that the Company's strategic focus includes allocating capital to assets at various stages of development, when evaluating accretion, it will consider measures such as internal rate of return ("IRR"), return on invested capital ("ROIC"), net asset value per share and the contained value of reserves and resources per share.

Hudbay's key objectives for 2026 are focused on continued operational excellence, advancement of organic growth opportunities and prudent capital allocation to deliver attractive high-return growth:

1. Demonstrate continued operational excellence to generate substantial free cash flow through consistent copper and gold production, industry-leading cost performance and high-return brownfield reinvestment opportunities.

◦ Increase mill throughput at Constancia to approximately 90,000 tonnes per day in the second half of 2026 through the installation of two pebble crushers.

◦ Continue mill throughput improvements at New Britannia and recovery enhancements at the Stall mill.

◦ Advance the 1901 deposit towards full production by the end of 2027.

◦ Ramp up mill throughput at Copper Mountain to its permitted capacity of 50,000 tonnes per day in the second half of 2026.

2. Advance attractive organic growth opportunities to deliver significant increase in long-term production.

◦ Complete the definitive feasibility study at Copper World in mid-2026 with final sanctioning decision expected in 2026.

◦ Progress New Ingerbelle permitting and development activities to add production and mine life extension at Copper Mountain.

◦ Advance economic evaluations of regional satellite properties in Snow Lake, including the Talbot copper-gold-zinc deposit and the New Britanna gold deposit, to further optimize the mine plan and extend mine life.

◦ Execute extensive Snow Lake exploration program to look for new anchor deposits to meaningfully extend mine life.

◦ Initiate pre-feasibility study activities at Mason to de-risk project development.

◦ Advance Flin Flon tailings reprocessing opportunities through pre-feasibility analysis.

◦ Prepare for exploration activities at Maria Reyna and Caballito to identify high-grade satellite deposits within trucking distance of Constancia's milling infrastructure and provide significant long-term upside potential in Peru.

3. Implement the Capital Allocation Framework to maintain strong financial discipline and maximize returns.

◦ Continue to reduce total debt outstanding and maintain significant financial flexibility throughout Copper World project build.

◦ Source the most efficient project level financing for Copper World as part of the Company's prudent financial plan for developing the project.

◦ Evaluate all types of capital redeployment opportunities, including reinvestments and shareholder returns to generate the highest risk-adjusted returns.

SUMMARY

Delivered Record Annual Revenue and Adjusted EBITDA; Achieved 2025 Consolidated Copper and Gold Production and Cost Guidance

• Achieved record annual revenue of $2,211.0 million and record annual adjusted EBITDA1 of $1,060.9 million in 2025, demonstrating the resilience and strength of Hudbay's diversified operating platform.

• Achieved full year consolidated copper and gold production guidance, with 118,188 tonnes of copper and 267,934 ounces of gold, despite mandatory wildfire evacuations in Manitoba and temporary operational interruptions in Peru resulting in production deferrals during the year.

• 2025 represents the 11th consecutive year in which Hudbay achieved its annual consolidated copper production guidance, since Constancia declared commercial production, and the 5th consecutive year achieving its annual consolidated gold production guidance, since establishing standalone gold production guidance4.

• Significantly outperformed the twice-improved 2025 consolidated cash cost guidance driven by strong cost control, higher metal prices and meaningful exposure to gold by-product credits resulting in consolidated cash cost1 and sustaining cash cost1, net of by-product credits, of $(0.22) and $1.30 per pound of copper, respectively, in 2025, an improvement of 148% and 20%, respectively, compared to 2024.

• Peru operations produced 85,155 tonnes of copper and 74,480 ounces of gold in 2025 with full year copper production within the 2025 guidance range while gold production far exceeded the top end of the annual guidance range. This production output was attributable to the optimization of the mine plan in 2025 by prioritizing Pampacancha mining activities and fully depleting the high-grade satellite deposit in December. Peru also leveraged the use of stockpiled ore during the third quarter of 2025 as the Company adapted its mine plan due to the social unrest experienced in the region. Peru full year cash cost1 of $1.08 per pound of copper outperformed the low end of the 2025 annual guidance range of $1.35 to $1.65 per pound as a result of stable operating cost performance and higher by-product credits.

• Manitoba operations produced 173,453 ounces of gold, 9,249 tonnes of copper, 17,646 tonnes of zinc and 800,198 ounces of silver in 2025. Production was below the low end of the guidance range for gold and zinc, while copper and silver production was within the guidance range in 2025. These production levels were achieved despite the impacts of over two months of production deferrals due to wildfire evacuations, ramp-up activities throughout the summer and unexpected downtime from an eight day weather-related power outage in October. In addition, zinc production was lower than the guidance range as gold production was prioritized in Manitoba. Manitoba full year cash cost1 of $549 per ounce of gold outperformed the low end of the 2025 annual guidance range of $650 to $850 per ounce as a result of productivity gains and lower treatment and refining charges.

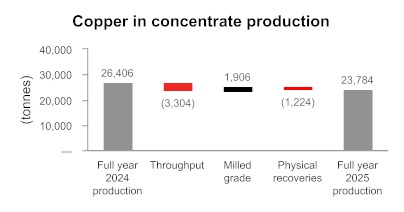

• British Columbia operations produced 23,784 tonnes of copper, 20,001 ounces of gold and 252,811 ounces of silver in 2025. Copper production was below the low end of the production guidance range, while the operations achieved full year 2025 production guidance for gold and silver. Copper production in 2025 was impacted by reduced throughput at the primary semi-autogenous grinding ("SAG") mill in the fourth quarter of 2025 and a higher portion of low-grade stockpiles utilized as ore feed in 2025. British Columbia full year cash cost1 of $3.06 per pound of copper achieved the 2025 annual cost guidance range of $2.45 to $3.45 per pound.

Delivered Strong Fourth Quarter Financial Results Driven by Resilient Operating Performance

• Achieved record quarterly revenue of $732.9 million and record quarterly adjusted EBITDA1 of $385.9 million in the fourth quarter of 2025.

• Demonstrated strong operational performance in the fourth quarter of 2025 as operations normalized after temporary production interruptions in the third quarter with consolidated copper production of 33,069 tonnes and consolidated gold production of 84,298 ounces.

• Maintained industry-leading cost performance in the fourth quarter with consolidated cash cost1 and sustaining cash cost1 per pound of copper produced, net of by-product credits, of $(0.63) and $0.94, respectively.

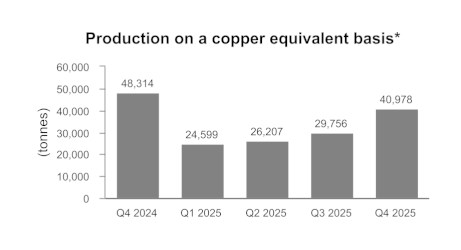

• Peru operations had the strongest quarter of the year in the fourth quarter with production of 25,038 tonnes of copper, 32,865 ounces of gold and 731,017 ounces of silver as strong copper and gold grades were mined from Pampacancha and less ore was processed from low-grade stockpiles. Hudbay continued to optimize the mine plan during the quarter with more ore mined from Pampacancha than previously expected, resulting in the accelerated depletion of Pampacancha, in late December compared to early 2026. Peru cash cost1, net of by-product credits, was $0.57 per pound of copper in the fourth quarter, outperforming the low end of the annual cost guidance range.

• Manitoba operations produced 47,423 ounces of gold in the fourth quarter, slightly lower than quarterly cadence expectations due to unplanned down time in October from an eight-day weather-related power outage, offset by record monthly throughput at the New Britannia mill in December. Manitoba operations also produced 3,326 tonnes of copper, 5,703 tonnes of zinc and 214,493 ounces of silver in the fourth quarter. Manitoba cash cost1, net of by-product credits, was $705 per ounce of gold in the fourth quarter, well within the annual cost guidance range.

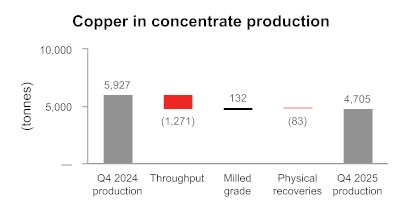

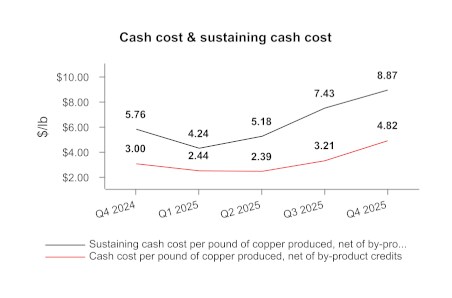

• British Columbia operations produced 4,705 tonnes of copper, 4,010 ounces of gold and 57,475 ounces of silver in the fourth quarter. While the operations completed construction of the permanent feed system for the new second SAG mill in December, total throughput in the fourth quarter was constrained by the primary SAG mill requiring unplanned maintenance early in the fourth quarter of 2025. British Columbia cash cost1, net of by-product credits, was $4.82 per pound of copper in the fourth quarter, reflecting the production impacts from the primary SAG mill maintenance.

• Fourth quarter net earnings attributable to owners and earnings per share attributable to owners were $128.0 million and $0.32, respectively, reflecting the strong gross margins as a result of higher metal prices and a $25.0 million business interruption insurance recovery related to the mandatory wildfire evacuations in Manitoba during the year. After adjusting for the insurance recovery and other non-cash items, fourth quarter adjusted earnings1 per share attributable to owners was $0.22.

• The strong gross margins achieved in the fourth quarter of 2025 resulted in higher employee profit sharing expenses of $36.1 million recorded within cost of sales.

Achieved Deleveraging Targets Ahead of Schedule

• Hudbay's unique copper and gold diversification across its operations provides exposure to higher copper and gold prices, which together with a focus on cost control across the business, continues to expand margins and generate attractive free cash flow.

• While the majority of Hudbay's revenue continues to be derived from copper production, revenue from gold production continues to represent a growing portion of total revenues at 38% of total revenue in 2025, including 41% of revenue in the fourth quarter, compared to 35% in 2024.

• Delivered another quarter of record free cash flow1 generation with $228.2 million achieved during the fourth quarter of 2025, resulting in $387.9 million in free cash flow in 2025.

• Achieved adjusted EBITDA1 of $385.9 million in the fourth quarter of 2025, resulting in record annual adjusted EBITDA1 of $1,060.9 million.

• Repurchased and retired an additional $39.3 million of senior unsecured notes through open market purchases at a discount to par during the fourth quarter of 2025 reducing total debt to $1.0 billion as of December 31, 2025. Since the end of 2024, Hudbay has reduced its long-term debt by $185.1 million.

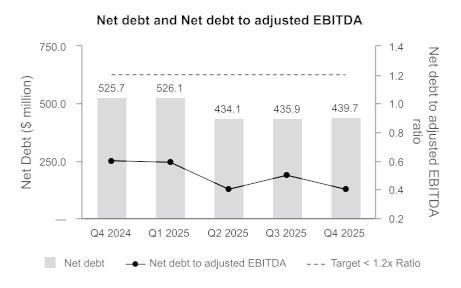

• Net debt1 decreased by $86.0 million to $439.7 million as at December 31, 2025 compared to $525.7 million at December 31, 2024.

• Net debt to adjusted EBITDA ratio1 was 0.4x at the end of the fourth quarter of 2025, a further improvement from 0.6x at the end of the fourth quarter of 2024.

• After giving effect to the recent closing of the Copper World joint venture transaction, which occurred in January 2026, Hudbay's post-closing adjusted cash and cash equivalents as at December 31, 2025 were approximately $992 million3. In addition, Hudbay had undrawn availability of $424.8 million under its revolving credit facilities as of December 31, 2025, increasing its total post-closing adjusted liquidity to over $1.4 billion3.

Implementing Holistic Capital Allocation Framework to Maintain Strong Financial Discipline, Deliver Growth Initiatives and Maximize Long-term Risk-adjusted Returns

• Enhanced Capital Allocation Framework embedded into Hudbay's annual financial planning cycle to provide a holistic approach to capital allocation decisions, including capital deployment into brownfield projects, greenfield projects and strategic investments, while considering debt repurchases, share buybacks and dividends.

• Hudbay's recent financial transformation has positioned the Company to introduce a new quarterly dividend of C$0.01 per share, an annual increase of 100% compared to its former semi-annual C$0.01 per share dividend, representing the Company's first dividend increase in its history.

• Closed the accretive $600 million joint venture transaction with Mitsubishi Corporation ("Mitsubishi") in January 2026, securing a premier, long-term 30% strategic partner for the development of Copper World. Definitive feasibility study on track for completion in mid-2026 with a sanctioning decision expected in 2026.

• Ongoing optimization efforts at Copper Mountain include executing an accelerated stripping campaign to deliver higher grades starting in 2027 and mill improvement initiatives to achieve the permitted mill throughput capacity of 50,000 tonnes per day in the second half of 2026.

• Expected to deliver higher mill throughput rates at Constancia in the second half of 2026 with the installation of pebble crushers.

• Continued large Snow Lake exploration program to further increase near-term production and mineral reserves, test regional satellite deposits for additional mill feed to utilize available capacity at Stall and explore the large land package for a new anchor deposit to meaningfully extend mine life.

• Underground infrastructure established at the 1901 deposit to enable exploration drilling throughout 2026 and prepare for full production by the end of 2027.

• Drilling activities have increased at the copper-gold-zinc Talbot deposit near Snow Lake with six drill rigs deployed and several step-out drill holes indicating resource expansion potential.

• Engineering work advances on the Flin Flon tailings reprocessing opportunity to assess the economic viability of producing critical minerals and precious metals and the potential to reduce the overall environmental footprint.

• Advancing plans to initiate a pre-feasibility study for the Mason copper project in Nevada.

2026 Guidance Reflects Stable Copper and Gold Production at Industry-leading Margins

• Consolidated copper production of 124,000 tonnes, based on the midpoint of the 2026 guidance range, is expected to increase by 5% compared to 2025 levels, reflecting higher expected production in British Columbia with the anticipated mill throughput ramp-up to the targeted 50,000 tonnes per day in the second half of 2026, partially offset by lower grades in Peru with the depletion of Pampacancha in 2025.

• Consolidated gold production of 244,500 ounces, based on the midpoint of the 2026 guidance range, is expected to be lower than 2025 production, reflecting the depletion of Pampacancha in 2025, but higher in unstreamed gold ounces with higher gold production in Manitoba from mill throughput at New Britannia continuing to exceed expectations.

• Consolidated cash cost1, net of by-product credits, in 2026 is expected to be within ($0.30) to ($0.10) per pound of copper, benefiting from higher gold production and a continued focus on maintaining stable operating costs across the business, driving industry-leading margins.

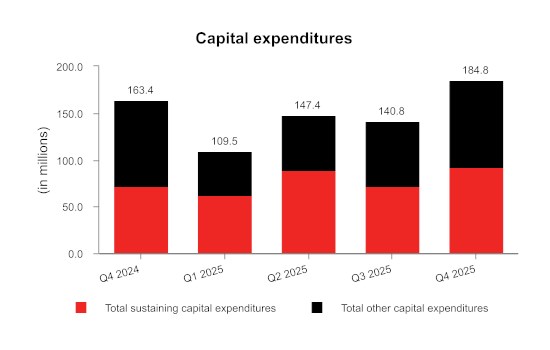

• Total sustaining capital expenditures are expected to be $435 million in 2026, reflecting approximately $38 million in deferrals from 2025 and $44 million in one-time sustaining capital projects at the operations.

• As the Company embarks on generational reinvestments, total growth capital expenditures at the operations are expected to be $140 million in 2026, including approximately $23 million in deferrals from 2025, to advance several high-return growth projects in 2026 to deliver increased copper exposure, including Peru mill throughput enhancement projects, early works at the New Ingerbelle expansion project in British Columbia, and excludes growth capital related to the Copper World joint venture.

• Growth capital expenditures at Copper World are expected to be $135 million in 2026 for project feasibility, de-risking and pre-sanctioning costs, which have been fully funded by the proceeds received from Mitsubishi as part of the closing of the Copper World joint venture transaction in January 2026, and include approximately $60 million for accelerated long lead items and de-risking activities and $35 million of capital deferrals from 2025.

Summary of Fourth Quarter Results

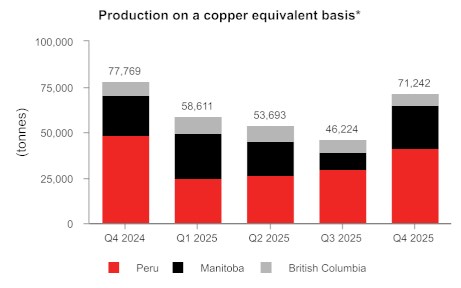

Hudbay's diversified asset portfolio delivered consolidated copper production of 33,069 tonnes and consolidated gold production of 84,298 ounces in the fourth quarter of 2025. Consolidated copper and gold production was higher than the third quarter of 2025 due to strong copper and gold grades from Pampacancha and less ore processed from low-grade stockpiles compared to the third quarter. Consolidated gold production also benefitted from the ramp-up to full operations in Snow Lake after the mandatory wildfire evacuations were lifted in the third quarter of 2025 and record monthly throughput at the New Britannia mill in December. Consolidated silver production of 1,002,985 ounces and zinc production of 5,703 tonnes in the fourth quarter of 2025 were also higher than the third quarter of 2025 for the aforementioned reasons.

Cash generated from operating activities of $209.4 million decreased compared to the same period in 2024 as the strong gross margins during the quarter was offset by the impacts of changes in non-cash working capital from a higher receivable balance as a result of the timing of sales as well as higher cash taxes paid compared to the same period in 2024. Cash generated from operating activities increased compared to the third quarter of 2025 as a result of higher gross margins driven by strong metal prices and higher sales volumes compared to the third quarter which was impacted by mandatory wildfire evacuations in Manitoba and a temporary operational interruption in Peru. Operating cash flow before change in non-cash working capital was $336.9 million during the fourth quarter of 2025, reflecting an increase of $266.6 million from the third quarter of 2025. This significant increase reflects higher copper and gold sales volumes from normalized operations after temporary interruptions and higher metal prices.

Adjusted EBITDA1 was $385.9 million in the fourth quarter of 2025, an increase compared to $142.6 million in the third quarter of 2025 as higher realized metal prices and higher copper and gold sales volume resulted in strong gross margins during the quarter.

Net earnings attributable to owners was $128.0 million, or $0.32 per share, in the fourth quarter of 2025 compared to $222.4 million, or $0.56 per share, in the third quarter of 2025 and $21.2 million, or $0.05 per share, in the fourth quarter of 2024. The decrease in earnings compared to the third quarter of 2025 is a result of a non-cash after-tax gain of $242.7 million from a full impairment reversal relating to Hudbay's Copper World project that occurred in the third quarter. The increase in earnings compared to the fourth quarter of 2024 is driven by higher realized metal prices resulting in strong gross margin as well as a $25.0 million business interruption insurance recovery related to the Manitoba mandatory wildfire evacuation shutdowns.

Adjusted net earnings attributable to owners1 and adjusted net earnings per share attributable to owners1 in the fourth quarter of 2025 were $86.0 million and $0.22 per share, respectively, after adjusting for various non-cash items on a pre-tax basis including a $25.0 million business interruption insurance recovery related to the Manitoba mandatory wildfire evacuations during the year, a $5.7 million mark-to-market revaluation gain on various instruments such as investments and share-based compensation, and a non-cash $5.4 million foreign exchange gain, among other items. This compares to adjusted net earnings attributable to owners1 and net earnings per share attributable to owners1 of $70.3 million and $0.18 per share in the fourth quarter of 2024 and $10.1 million and $0.03 per share in the third quarter of 2025. The increase compared to the fourth quarter of 2024 is for the same reasons discussed above for net earnings. The increase compared to the third quarter of 2025 is a result of higher realized metal prices and higher sales volumes.

Consolidated cash cost1, net of by-product credits, in the fourth quarter of 2025 was $(0.63) per pound of copper, compared to $0.42 per pound in the third quarter of 2025 and $0.45 in the fourth quarter of 2024, as Hudbay continued to demonstrate strong cost control across its operations. The decrease in cash cost from the comparative periods was a result of higher by-product credits reflecting the benefits of Hudbay's diversified asset portfolio with higher realized prices across all metals.

Consolidated sustaining cash cost1, net of by-product credits, in the fourth quarter of 2025 was $0.94 per pound of copper, compared to $2.09 per pound in the third quarter of 2025 and $1.37 per pound in the fourth quarter of 2024. The decrease was primarily due to the same factors impacting consolidated cash cost noted above, partially offset by planned higher cash sustaining capital expenditures.

Consolidated all-in sustaining cash cost1, net of by-product credits, in the fourth quarter of 2025 was $1.43 per pound of copper, lower than the third quarter of 2025 and the fourth quarter of 2024 mainly due to the same reasons noted above, partially offset by higher corporate general and administrative ("G&A") costs from the revaluation of Hudbay's stock-based compensation due to a higher share price.

As at December 31, 2025, total liquidity was $993.7 million, including $568.9 million in cash and cash equivalents, and undrawn availability of $424.8 million under Hudbay's revolving credit facilities. Net debt1 at the end of the fourth quarter was $439.7 million, marking an $86.0 million improvement from fourth quarter of 2024 as a result of deleveraging activities which included the repurchase and retirement of senior unsecured notes. After giving effect to the closing of the Copper World joint venture transaction, post-closing adjusted cash and cash equivalents as of December 31, 2025 are approximately $992 million3, total post-closing adjusted liquidity increases to over $1.4 billion3 and post-closing net debt1 is approximately zero. Hudbay expects that the current liquidity, together with cash flows from operations, will be sufficient to meet the Company's liquidity needs for the year.

Summary of Full Year Results

Hudbay achieved 2025 consolidated production guidance for copper and gold, with full year production of 118,188 tonnes of copper and 267,934 ounces of gold. In 2025, the operations also produced 17,646 tonnes of zinc, 3,468,143 ounces of silver and 1,282 tonnes of molybdenum. 2025 represents the 11th consecutive year in which Hudbay achieved its annual consolidated copper production guidance, since Constancia declared commercial production, and 5th consecutive year achieving its annual consolidated gold production guidance, since establishing standalone gold production guidance.

With respect to Hudbay's operating business units, Peru exceeded the top end of the gold production guidance and achieved the guidance ranges for copper despite the impact from the temporary operational interruption due to social unrest. While Hudbay was previously tracking within the guidance ranges in Manitoba despite the wildfires, gold and zinc production fell below the low end of the respective ranges as a result of an eight-day weather-related power outage in October. Manitoba achieved guidance for copper and silver production despite these interruptions. British Columbia achieved guidance for gold and silver production, while copper production fell below the low end of the guidance range, primarily due to unplanned maintenance at the primary SAG mill in the fourth quarter and a higher portion of low-grade stockpiles utilized as ore feed in 2025.

Cash generated from operating activities increased to $707.3 million in 2025 from $666.2 million in 2024. Operating cash flow before change in non-cash working capital increased to a record $764.3 million in 2025 from $691.1 million in 2024. The increase in operating cash flow before changes in working capital was primarily the result of higher gross margins driven by higher metal prices and stable cost performance despite temporary operational interruptions during the year. This was partially offset by a significant increase in cash taxes paid of $268.4 million, compared to $132.5 million in 2024 reflecting earlier periods of high taxable income mainly at the Peru and Manitoba operations.

Net earnings attributable to owners were $568.5 million, or $1.44 per share, in 2025, compared to $76.7 million, or $0.20 per share, in 2024. Net earnings were positively impacted by higher realized prices for all metals and a non-cash charge of $242.7 million relating to an impairment reversal with respect to the Copper World project in 2025, partially offset by higher mining and income tax expenses.

Adjusted net earnings attributable to owners1 and adjusted net earnings per share attributable to owners1 in 2025 were $265.5 million and $0.67 per share, respectively, after adjusting for items on a pre-tax basis such as a $322.3 million impairment reversal with respect to the Copper World project, $25.0 million in business interruption insurance recovery related to the Manitoba wildfires, $18.6 million in foreign exchange gains, and $14.9 million in consideration received from sale of a non-core project, among other items. This compares to adjusted net earnings attributable to owners1 and net earnings per share attributable to owners1 of $181.4 million and $0.48 per share in 2024.

Adjusted EBITDA1 was $1,060.9 million in 2025, a 29% increase compared to $822.5 million in 2024, achieving a new annual record. The increase was the result of higher realized metal prices and stable operating performance, driving strong cost control across the business.

Consolidated cash cost1, net of by-product credits, in the fourth quarter of 2025 was $(0.22) per pound of copper, compared to $0.46 per pound of copper in 2024. Hudbay significantly outperformed its twice-improved 2025 consolidated cash cost guidance as a result of higher metal prices with a significant increase in gold by-product credits, partially offset by higher G&A due to higher employee profit sharing in Peru and Manitoba.

Consolidated sustaining cash cost1, net of by-product credits1, in the fourth quarter of 2025 was $1.30 per pound of copper in 2025 decreased from $1.62 per pound of copper in 2024 due to the same reasons affecting cash cost, partially offset by higher cash sustaining capital expenditures. Hudbay outperformed the improved 2025 consolidated sustaining cash cost guidance as a result of the same reasons driving the outperformance on cash cost guidance.

Consolidated all-in sustaining cash cost1, net of by-product credits, in the fourth quarter of 2025 was $1.74 per pound of copper in 2025, lower than $1.88 per pound of copper in 2024 as a result of the same reasons outlined above, partially offset by higher corporate selling and administrative costs primarily due to a revaluation of share-based compensation associated with a higher share price.

*Copper equivalent production is calculated using the quarter average LME prices for each metal.

1 Adjusted net earnings - attributable to owners and adjusted net earnings per share - attributable to owners, adjusted EBITDA, cash cost, sustaining cash cost, all-in sustaining cash cost per pound of copper produced, net of by-product credits, cash cost, sustaining cash cost per ounce of gold produced, net of by-product credits, combined unit cost, net debt, net debt to adjusted EBITDA ratio and free cash flow are non-GAAP financial performance measures with no standardized definition under IFRS. For further information and a detailed reconciliation, please see the discussion under the "Non-GAAP Financial Performance Measures" section of this MD&A.

2 Liquidity includes $568.9 million in cash and cash equivalents as well as undrawn total availability of $424.8 million under Hudbay's revolving credit facilities.

3 The post-closing adjusted year-end cash and cash equivalents of $992 million includes December 31, 2025 cash and cash equivalents balance of $568.9 million and approximately $420 million of cash at the Copper World LLC level, which is designated for exclusive use by the Copper World joint venture. Post-closing adjusted liquidity includes the pro-forma cash and cash equivalent plus the undrawn availability of $424.8 million under Hudbay's revolving credit facilities.

4 In 2020, Hudbay's consolidated copper production guidance range was revised during the year due to the impact of COVID-19 at the operations. Hudbay's copper production was within the revised guidance ranges. Prior to 2021, Hudbay provided guidance on a precious metal equivalent instead of gold as a standalone metal.

KEY FINANCIAL RESULTS

| Financial Condition | ||||||

| (in $ millions, except net debt to adjusted EBITDA ratio) | Dec. 31, 2025 | Dec. 31, 2024 | ||||

| Cash and cash equivalents and short-term investments | $ | 568.9 | $ | 581.8 | ||

| Total long-term debt | 1,008.6 | 1,107.5 | ||||

| Net debt1 | 439.7 | 525.7 | ||||

| Working capital2 | (65.6 | ) | 511.3 | |||

| Total assets | 6,223.3 | 5,487.6 | ||||

| Equity attributable to owners of the Company | 3,231.0 | 2,553.2 | ||||

| Net debt to adjusted EBITDA 1 | 0.4 | 0.6 |

1 Net debt and net debt to adjusted EBITDA are non-GAAP financial performance measures with no standardized definition under IFRS. For further information and a detailed reconciliation, please see discussion under the "Non-GAAP Financial Performance Measures" section of this MD&A.

2 Working capital is determined as total current assets less total current liabilities as defined under IFRS and disclosed on the consolidated financial statements. Working capital as of December 31, 2025 was impacted by an increase in the current portion of long-term debt of $472.1 million as the 2026 Notes are now maturing within one year.

| Financial Performance | Three months ended | Year ended | |||||||||||||

| (in $ millions, except per share amounts or as noted below) | Dec. 31, 2025 |

Sep. 30, 2025 |

Dec. 31, 2024 |

Dec. 31, 2025 |

Dec. 31, 2024 |

||||||||||

| Revenue | $ | 732.9 | $ | 346.8 | $ | 584.9 | $ | 2,211.0 | $ | 2,021.2 | |||||

| Cost of sales | 462.8 | 281.5 | 400.5 | 1,467.8 | 1,467.4 | ||||||||||

| Earnings before tax | 257.1 | 330.5 | 103.7 | 912.0 | 251.6 | ||||||||||

| Net earnings | 128.0 | 222.4 | 19.3 | 564.3 | 67.8 | ||||||||||

| Net earnings attributable to owners | 128.0 | 222.4 | 21.2 | 568.5 | 76.7 | ||||||||||

| Basic and diluted earnings per share - attributable | 0.32 | 0.56 | 0.05 | 1.44 | 0.20 | ||||||||||

| Adjusted earnings per share - attributable1 | 0.22 | 0.03 | 0.18 | 0.67 | 0.48 | ||||||||||

| Operating cash flow before change in non-cash working capital | 336.9 | 70.3 | 231.5 | 764.3 | 691.1 | ||||||||||

| Adjusted EBITDA1 | 385.9 | 142.6 | 257.3 | 1,060.9 | 822.5 | ||||||||||

| Free cash flow1 | 228.2 | (15.2 | ) | 149.0 | 387.9 | 368.0 | |||||||||

1 Adjusted earnings per share - attributable to owners, adjusted EBITDA and free cash flow are non-GAAP financial performance measures with no standardized definition under IFRS. For further information and a detailed reconciliation, please see discussion under the "Non-GAAP Financial Performance Measures" section of this MD&A.

KEY PRODUCTION RESULTS

| Three months ended | Year ended | Guidance | |||||

| Dec. 31, 2025 |

Sep. 30, 2025 |

Dec. 31, 2024 |

Dec. 31, 2025 |

Dec. 31, 2024 |

Annual 2025 | ||

| Contained metal in concentrate and doré produced1 | |||||||

| Copper | tonnes | 33,069 | 24,205 | 43,262 | 118,188 | 137,943 | 117,000 - 149,000 |

| Gold | oz | 84,298 | 53,581 | 94,161 | 267,934 | 332,240 | 247,500 - 308,000 |

| Silver | oz | 1,002,985 | 730,394 | 1,311,658 | 3,468,143 | 3,983,851 | 3,520,000 - 4,390,000 |

| Zinc | tonnes | 5,703 | 548 | 8,385 | 17,646 | 33,339 | 21,000 - 27,000 |

| Molybdenum | tonnes | 325 | 185 | 195 | 1,282 | 1,323 | 1,300 - 1,500 |

| Payable metal sold | |||||||

| Copper | tonnes | 34,132 | 18,280 | 37,927 | 114,534 | 125,094 | |

| Gold2 | oz | 84,424 | 38,279 | 92,734 | 260,261 | 335,342 | |

| Silver2 | oz | 871,006 | 418,418 | 1,150,518 | 3,190,552 | 3,549,816 | |

| Zinc | tonnes | 3,972 | 3,452 | 5,261 | 15,152 | 25,120 | |

| Molybdenum | tonnes | 190 | 269 | 182 | 1,334 | 1,287 | |

1 Metal reported in concentrate is prior to deductions associated with smelter contract terms and includes other secondary products.

2 Includes total payable gold and silver in concentrate and in doré sold and other secondary products.

KEY COST RESULTS

| Three months ended | Year ended | Guidance | |||||

| Dec. 31, 2025 |

Sep. 30, 2025 |

Dec. 31, 2024 |

Dec. 31, 2025 |

Dec. 31, 2024 |

Annual 20252 |

||

| Peru cash cost per pound of copper produced | |||||||

| Cash cost1 | $/lb | 0.57 | 1.30 | 1.00 | 1.08 | 1.18 | 1.35 - 1.65 |

| Sustaining cash cost1 | $/lb | 1.53 | 2.11 | 1.48 | 2.02 | 1.86 | |

| Manitoba cash cost per ounce of gold produced | |||||||

| Cash cost1 | $/oz | 705 | 379 | 607 | 549 | 606 | 650 - 850 |

| Sustaining cash cost1 | $/oz | 1,110 | 762 | 908 | 875 | 868 | |

| British Columbia cash cost per pound of copper produced | |||||||

| Cash cost1 | $/lb | 4.82 | 3.21 | 3.00 | 3.06 | 2.74 | 2.45 - 3.45 |

| Sustaining cash cost1 | $/lb | 8.87 | 7.43 | 5.76 | 6.12 | 5.29 | |

| Consolidated cash cost per pound of copper produced | |||||||

| Cash cost1 | $/lb | (0.63) | 0.42 | 0.45 | (0.22) | 0.46 | 0.15 - 0.35 |

| Sustaining cash cost1 | $/lb | 0.94 | 2.09 | 1.37 | 1.30 | 1.62 | 1.85 - 2.25 |

| All-in sustaining cash cost1 | $/lb | 1.43 | 2.78 | 1.53 | 1.74 | 1.88 | |

1 Cash cost, sustaining cash cost, all-in sustaining cash cost per pound of copper produced, net of by-product credits, gold cash cost, sustaining cash cost per ounce of gold produced, and net of by-product credits are non-GAAP financial performance measures with no standardized definition under IFRS. For further information and a detailed reconciliation, please see the discussion under the "Non-GAAP Financial Performance Measures" section of this MD&A.

2 Improved full year 2025 consolidated copper cash cost guidance range to $0.15 to $0.35 per pound from prior guidance of $0.65 to $0.85 per pound and the original guidance range of $0.80 to $1.00 per pound. Improved full year 2025 consolidated sustaining copper cash cost guidance range to $1.85 to $2.25 per pound from the original guidance range of $2.25 to $2.65 per pound.

RECENT DEVELOPMENTS

Continued Free Cash Flow Generation Driving Further Debt Reduction and Significant Financial Flexibility

Hudbay has delivered several quarters of meaningful free cash flow generation as a result of steady operating performance, expanding margins from strong copper and gold exposure and a focus on cost control across the business. This has resulted in Hudbay achieving record annual adjusted EBITDA of $1,060.9 million and record annual free cash flow of $387.9 million in 2025.

As a result of the strong operating and financial performance, Hudbay continued its prudent balance sheet management and further reduced overall debt levels in the fourth quarter of 2025, resulting in a total of $102.5 million in debt repayments during the full year 2025. These deleveraging efforts have reduced total principal debt to $1,008.6 million as of December 31, 2025.

As of December 31, 2025, Hudbay had approximately $569 million in cash and cash equivalents, resulting in a reduction in net debt to $439.7 million compared to $525.7 million at December 31, 2024. Similarly, Hudbay reduced its net debt to adjusted EBITDA ratio to 0.4x at the end of the fourth quarter of 2025, a further improvement from 0.6x at the end of fourth quarter of 2024.

After giving effect to the closing of the Copper World joint venture transaction, as described below, Hudbay's post-closing adjusted cash and cash equivalents as at December 31, 2025 was approximately $992 million3. In addition, Hudbay had undrawn availability of $425 million under Hudbay's revolving credit facilities as of December 31, 2025, increasing total post-closing adjusted liquidity to over $1.4 billion3. Hudbay is well-positioned to advance Copper World and fund its several other high-return growth opportunities across the business.

Prudently Advancing Copper World Towards a Sanction Decision in 2026

In January 2026, Hudbay announced the closing of the joint venture transaction ("JV Transaction") with Mitsubishi, securing a premier, long-term strategic partner for the development of Copper World. The Company continues to progress the detailed engineering work to de-risk Copper World ahead of a sanction decision later this year.

• Realized Accretive JV Transaction - On January 12, 2026, Hudbay announced the closing of the highly accretive $600 million JV Transaction, which represents a significant de-risking milestone in advancing Copper World and further validates the premium long-term value of this world-class asset. The $420 million of proceeds received at closing from Mitsubishi will be used to directly fund the remaining definitive feasibility study ("DFS") costs and pre-sanctioning costs in addition to the initial project development costs for Copper World. Mitsubishi will contribute an additional $180 million within 18 months of closing to complete its 30% minority investment and will also fund its pro-rata 30% share of future equity capital contributions. The JV Transaction increases the project IRR to Hudbay to approximately 90% based on pre-feasibility study ("PFS") estimates2.

• Secured Premier Strategic Joint Venture Partner - Mitsubishi is one of the largest Japanese trading houses with a global mining presence and a significant U.S.-based business. Mitsubishi is the partner of choice with investments in a world-class portfolio of large and high-quality copper assets, including five of the top twenty copper mines globally by 2024 production. This partnership validates the attractive long-term value of Copper World as a world-class copper asset and endorses the strong technical capabilities of Hudbay. It also represents the beginning of a long-term strategic partnership, and the parties are identifying other opportunities for collaboration to advance their respective copper growth strategies.

• Achieved Key Elements of Hudbay's Three Prerequisites (3-P) Plan - Hudbay has achieved the final key elements of its prudent 3-P financial strategy for the development of Copper World with the closing of the JV Transaction and the achievement of stated balance sheet targets. After accounting for proceeds from the JV Transaction, Hudbay has post-closing adjusted cash and cash equivalents of $992 million3 and reduced its post-closing net debt to adjusted EBITDA ratio to 0.0x, far exceeding the stated balance sheet targets. The Mitsubishi initial investment and its future pro-rata equity capital contributions, together with the Wheaton Precious Metals Corp. stream, provide significant financial flexibility by reducing Hudbay's estimated share of the remaining capital contributions to approximately $200 million based on PFS estimates and deferring Hudbay's first capital contribution to 2028 at the earliest.

• Feasibility Study and Detailed Engineering Underway - Feasibility activities for Copper World are well underway with expected completion of the DFS in mid-2026. Hudbay has continued to execute detailed engineering work and other de-risking activities, in preparation for a Copper World sanctioning decision expected in 2026.

Manitoba Exploration Update

Large Exploration Drill Program Continues in Snow Lake

Hudbay continues to execute the largest exploration program in Snow Lake in the Company's history through extensive geophysical surveying and multi-phased drilling campaigns as part of Hudbay's threefold exploration strategy:

• Near-mine Exploration at Lalor and 1901 to Further Increase Near-term Production and Extend Mine Life - Hudbay completed the development of the initial exploration drift at the 1901 deposit in 2025 and the development of the haulage drift is underway. Hudbay received positive initial step-out drilling results from the exploration drift, and during the second half of 2025, some zinc development ore was delivered for processing at Stall. Activities at 1901 over the next two years will focus on exploration, definition drilling, orebody access, and establishing critical infrastructure for full production in late 2027. Exploration activities at 1901 will target additional step-out drilling to potentially extend the orebody and infill drilling to convert inferred mineral resources in the gold lenses to mineral reserves.

• Testing Regional Satellite Deposits to Utilize Available Processing Capacity and Increase Production - Hudbay increased its regional land package by more than 250% in 2023 through the acquisition of Rockcliff Metals Corp. ("Rockcliff"), which included the addition of several known deposits located within trucking distance of the Snow Lake processing infrastructure. The deposits acquired as part of the Rockcliff acquisition, together with several deposits already owned by Hudbay in Snow Lake, have created an attractive portfolio of regional deposits in Snow Lake, including the Talbot, New Britannia, Rail, Pen II, Watts, 3 Zone and WIM deposits. The continued strong performance from the New Britannia mill has freed up processing capacity at the Stall mill, where there is approximately 1,500 tonnes per day of available capacity which could be utilized by the regional satellite deposits to increase production and extend the life of the Snow Lake operations beyond 2037.

• Exploring Large Land Package for a New Anchor Deposit to Significantly Extend Mine Life - A majority of the land claims acquired as part of the Rockcliff acquisition have been untested by modern deep geophysics, which was the discovery method for the Lalor deposit. A large geophysics program is currently underway consisting of surface electromagnetic surveys using cutting edge techniques that enable the team to detect targets at depths of almost 1,000 metres below surface. The planned geophysics program is the largest geophysics program in Hudbay's history and includes 800 kilometres of ground electromagnetic surveys and an extensive airborne geophysics survey.

Talbot Initial Drilling Results Confirm Resource Expansion Potential

Talbot is a copper-zinc-gold rich VMS deposit located within trucking distance to existing processing infrastructure in Snow Lake. Successful drilling campaigns could expand the resource base and support a PFS to upgrade the mineral resources to reserves, extending the overall mine life of the Snow Lake operations. In April 2025, Hudbay announced the signing of the exploration agreement with the Mosakahiken Cree Nation on exploration activities in their traditional and ancestral territory, including at Talbot.

In July 2025, Hudbay commenced an extensive summer drill program at Talbot focused on expanding the known mineralization at depth, testing geophysical targets as well as conducting an infill drill program in the upper part of the ore body to support a PFS. As part of the initial drilling program in 2025, Hudbay drilled six holes to test the continuity of the Talbot deposit at depth, with all the holes yielding positive results and four of them returning mineralized intercepts with economic potential (see table of intercepts below). The 2026 drilling program has now commenced with six drill rigs deployed, including one drill rig focused on continuing to expand the footprint of the deposit at depth. In addition to the intercepts below, another hole provided a significant intercept of copper mineralization over an estimated length of 19.7 metres from core logging and for which assay results are pending.

| Hole ID | From (m) | To (m) | Intercept (m) |

Estimated true width (m)1 |

Cu (%)2 | Au (g/t)2 | Ag (g/t)2 | Zn (%)2 | CuEq. (%)3,4 |

| TLS024 | 1556.0 | 1567.5 | 11.5 | 10.4 | 2.4 | 1.8 | 55.1 | 0.8 | 4.2 |

| TLS025 top | 1435.3 | 1449.5 | 14.2 | 13.2 | 1.2 | 0.8 | 17.8 | 0.5 | 2.0 |

| TLS025 bottom | 1459.0 | 1465.0 | 6.0 | 5.6 | 2.0 | 0.7 | 16.9 | 0.5 | 2.6 |

| TLS026 | 1265.5 | 1273.4 | 7.8 | 7.1 | 1.4 | 0.9 | 18.4 | 0.3 | 2.2 |

| TLS027W02 | 1252.8 | 1271.5 | 18.8 | 16.3 | 1.4 | 0.8 | 18.9 | 1.3 | 2.4 |

1.True widths are estimated based on drill angle and intercept geometry of mineralization.

2 All copper, gold, silver and zinc values are uncut.

3 Copper-equivalent ("CuEq") grade calculated using the following long-term commodity price assumptions: $4.40 per pound copper, $2,800 per ounce gold, $32.00 per ounce silver and $1.25 per pound zinc.

4 Using the combined recoveries of New Britannia and Stall mills of 89% copper, 89% gold, 81% silver and 84% zinc.

In 2026, the Company plans on progressing a PFS and preparing an updated mineral resource estimate for Talbot using Hudbay standard methods that have demonstrated high reserve conversion rates.

Expanded Flin Flon Exploration Partnership with Marubeni and JOGMEC

On January 22, 2026, the Company announced the signing of an amended and restated option agreement with Japan Organization for Metals and Energy Security ("JOGMEC") and Marubeni Corporation ("Marubeni"), where Hudbay granted JOGMEC an option to acquire a 10% interest in three projects located within trucking distance of Hudbay's processing facilities in Flin Flon, Manitoba. In order to exercise its option, JOGMEC is required to fund at least C$6 million in exploration expenditures over a period of approximately three years, with Hudbay acting as the operator carrying out the exploration activities. The agreement is an amendment and restatement of the option agreement with Marubeni from March 2024, pursuant to which Marubeni's wholly-owned Canadian subsidiary was granted an option to acquire a 20% interest in the three projects, provided it, funds at least C$12 million in exploration expenditures over the designated earn-in period, which is inclusive of past contributions made by Marubeni since March 2024.

The option agreement focuses on three projects in the Flin Flon region, namely Cuprus-White Lake, Westarm and North Star, which were selected by Marubeni prior to the original March 2024 agreement and following a period of detailed due diligence. All three properties hold past producing mines that generated meaningful production with attractive grades of both base metals and precious metals. The properties remain highly prospective with potential for further discovery based on the attractive geological setting, limited historical deep drilling and promising geochemical and geophysical targets. Cuprus-White Lake, Westarm and North Star are all within 20 kilometres of Hudbay's Flin Flon milling complex.

Senior Management Team Appointments

In January 2026, Hudbay appointed Audra Walsh to the role of Vice President, South America Business Unit. Ms.Walsh joined Hudbay as acting Vice President in Peru in August 2025 and has transitioned to the permanent role as a testament to her exceptional talent as a professional engineer with over 30 years of technical, operating, management, executive and board experience in the mining industry. As leader of the South America Business Unit, Ms. Walsh is responsible for the strategic performance of Hudbay's operational and exploration activities in Peru and exploration activities in Chile.

Ms. Walsh's leadership experience and deep expertise will be instrumental in helping Hudbay achieve regional milestones and drive growth in Peru with the long-life operations at Constancia, the future development of Caballito and Maria Reyna and further regional exploration.

Holistic Capital Allocation Framework to Deliver Growth and Maximize Long-Term Risk-Adjusted Returns

Hudbay has a proven track record of prudently allocating capital to high-return brownfield investments, such as the New Britannia gold mill refurbishment project and the development of the high-grade Pampacancha satellite deposit, which have delivered significant free cash flows and contributed to Company's deleveraging efforts.

Hudbay has completed a financial transformation over the past three years. The Company has moved from being overleveraged and capital constrained to a preferred position where it can strategically allocate capital across the portfolio to maximize value and generate the highest risk-adjusted returns, creating long-term sustainable value for stakeholders.

Prudent strategic financial planning and execution of the Company's 3-P plan has achieved the Company's balance sheet deleveraging goals and has lowered its cost of capital. With its strongest balance sheet in more than a decade and peer-leading credit metrics, together with the strategic investment by Mitsubishi, Hudbay is very well positioned to sanction the Copper World project and embark on generational investments in the Company's operating portfolio in 2026. These generational investments include allocating capital to high-return brownfield projects at the Company's three operating mines and advance its world-class development and exploration pipeline.

To provide transparency and continued financial discipline, Hudbay has implemented an enhanced Capital Allocation Framework to provide a holistic approach around capital allocation decisions, including with respect to the deployment of capital into the business through near-term brownfield projects, longer-term greenfield projects, strategic investments and exploration, while considering debt repurchases, share buybacks and dividends.

Hudbay's holistic Capital Allocation Framework is embedded into the Company's annual financial planning cycle and includes the following key elements:

• Preserving Balance Sheet Strength - Aligning with successful deleveraging efforts to maintaining net debt to adjusted EBITDA ratios of less than 1.0x throughout the investment and development cycle, continuing to lower the Company's cost of capital and considering unique (non-dilutive) sources of project funding available.

• Strategic Fit for Growth and Diversification - Expanding and optimizing production and mine life from the existing asset base, enhancing Hudbay's strategic commodity exposure to copper and complementary gold, targeting 400,000 tonnes of annual copper-equivalent production, increasing long-term portfolio diversification across tier-1 jurisdictions and aligning with the Company's sustainability goals.

• Accretive Across Key Financial Metrics - Pursuing investment opportunities that are accretive to a mix of key financial performance metrics - Hudbay's net present value per share, copper-equivalent mineral resources per share, return on invested capital and cash flow yields, as well as demonstrating robust internal rate of returns and project paybacks to maximize value and long-term sustainable returns for all stakeholders.

• Rigorous Risk Assessment - Considering risk-adjusted returns based on project-specific characteristics, applying varying discount rates, commodity price scenarios and sensitivity analysis, as well as key qualitative risk considerations.

• Accountable Investment Governance - Integrating detailed project reviews as part of the annual budgeting process and executing investment decisions subject to a formal internal tollgate process, requiring Executive Committee and Board approval, followed by comprehensive post-project reviews to drive continuous improvement.

Increased Annual Dividend

Following Hudbay's recent financial transformation and consistent with its Capital Allocation Framework, the Company has commenced an increase in shareholder returns in the form of a quarterly dividend. Hudbay's Board of Directors approved the introduction of a new quarterly dividend of C$0.01 per share as the Company has achieved certain financial milestones ahead of schedule and has significantly improved its financial position. The new total annual dividend amount of C$0.04 per share represents an increase of 100% or C$0.02 per share over the previous annual dividend, which was paid semi-annually, representing the first dividend increase in the Company's history.

A quarterly dividend of C$0.01 per share was declared on February 19, 2026. The dividend will be paid out on March 27, 2026 to shareholders of record as of close of business on March 10, 2026.

1 Adjusted EBITDA, net debt, net debt to adjusted EBITDA ratio and free cash flow are non-GAAP financial performance measures with no standardized definition under IFRS. For further information and a detailed reconciliation, please see the discussion under the "Non-GAAP Financial Performance Measures" section of this MD&A.

2 Based on the initial capital investment and the $3.75 per pound copper price used in the PFS published on September 8, 2023 with assumptions of approximately $145 million for pre-sanctioning costs, $230 million from the precious metals stream, $350 million from project-level financing and approximately $700 million from Mitsubishi's $420 million initial investment, $180 million investment within 18 months and its pro-rata 30% share of future equity capital contributions.

3 The post-closing adjusted year-end cash and cash equivalents includes approximately $420 million of cash at the Copper World LLC level, including close adjustments received as part of the recent closing of the Copper World joint venture transaction, which is designated for exclusive use by the Copper World joint venture.

CLIMATE CHANGE INITIATIVES

Since inception of Hudbay's climate change strategy in 2022, the Company continues to implement initiatives to reduce its greenhouse gas ("GHG") footprint. The Company strives to measure efficiency against key process drivers, while recognizing the unique characteristics of each business unit, such as fluctuating strip ratios in open pit mines and changing development profiles at underground mines. In 2025, Hudbay updated its climate change targets with new 2030 GHG emissions reduction targets specific to each business unit and focused on areas where the Company believes it can achieve the biggest impact.

The Company has made significant progress towards achieving its climate change goals, including:

• Peru - Hudbay's new 10-year power purchase agreement with ENGIE Energía Perú for access to a 100% renewable energy supply to Constancia came into effect in January 2026. This is expected to be a key contributing factor towards the Peru operations reaching its 2030 target of a 99% reduction in Scope 2 GHG emissions intensity (tonnes of Scope 2 emissions per kilotonne of ore processed) compared to a 2022 baseline.

• Manitoba - Hudbay continues to expand its fleet of electric equipment for use at its underground operations. Following the successful initial trial of an electric Epiroc scooptram ST14 SG at the Lalor mine in 2023, the Company has seen reduced carbon intensity and improved ventilation due to temperature reductions in the deeper areas of the mine. Today, Hudbay has expanded the fleet of battery electric vehicles at Lalor to 10 with two more being added in 2026. Continuing to expand the electric equipment fleet and other operational efficiency initiatives will progress the Snow Lake operations towards its 2030 target of a 25% reduction in Scope 1 GHG emissions intensity (tonnes of Scope 1 emissions per kilometre) compared to a 2022 baseline.

• British Columbia - At the Copper Mountain mine, efforts to drive operational efficiency continue to be a core focus and will enable the B.C. operations to progress towards its 2030 target of 5% reduction in Scope 1 GHG emissions intensity (tonnes of Scope 1 emissions per kilometre) compared to a 2024 baseline. Hudbay utilizes several pieces of electric equipment at Copper Mountain, including, three electric shovels and three electric rotary blasthole drills, which reduces carbon intensity by displacing existing diesel equipment. Additionally, the Company took steps to implement renewable diesel, also known as hydrotreated vegetable oil (HVO) fuel, to power more than 50% of the haul truck fleet in 2025.

• Corporate - Hudbay integrated Scope 1 and Scope 2 GHG emissions into its long-range financial plans to support GHG reduction decision making and alignment with the Company's 2030 goals. The Company also implemented sustainability reporting software to standardize the sustainability data collection process. In January 2025, the Company established an ESG Steering Committee consisting of the COO, CFO and three SVPs to provide enhanced oversight of the Company's sustainability initiatives, procedures and disclosures.Hudbay plans to advance its Scope 3 data collection process in 2026 through supplier and customer engagement to drive transparency and influence positive GHG behaviours throughout the value chain.

PERU OPERATIONS REVIEW

| Three months ended | Year ended | |||||

| Dec. 31, 2025 | Sep. 30, 2025 | Dec. 31, 2024 | Dec. 31, 2025 | Dec. 31, 2024 | ||

| Constancia ore mined1 | tonnes | 5,610,915 | 564,579 | 4,186,058 | 21,539,089 | 15,046,190 |

| Copper | % | 0.31 | 0.25 | 0.40 | 0.31 | 0.34 |

| Gold | g/tonne | 0.03 | 0.02 | 0.04 | 0.03 | 0.04 |

| Silver | g/tonne | 3.27 | 1.92 | 3.88 | 3.18 | 3.08 |

| Molybdenum | % | 0.01 | 0.01 | 0.02 | 0.02 | 0.01 |

| Pampacancha ore mined1 | tonnes | 4,152,000 | 4,260,081 | 4,037,264 | 9,563,442 | 9,317,499 |

| Copper | % | 0.43 | 0.38 | 0.63 | 0.40 | 0.55 |

| Gold | g/tonne | 0.27 | 0.31 | 0.38 | 0.29 | 0.32 |

| Silver | g/tonne | 4.84 | 4.87 | 6.43 | 4.78 | 5.61 |

| Molybdenum | % | 0.01 | 0.01 | 0.00 | 0.01 | 0.01 |

| Total ore mined | tonnes | 9,762,915 | 4,824,660 | 8,223,322 | 31,102,531 | 24,363,689 |

| Strip ratio2 | 0.57 | 1.38 | 1.22 | 1.04 | 1.78 | |

| Ore milled | tonnes | 7,627,853 | 6,991,744 | 7,999,453 | 30,292,668 | 31,933,624 |

| Copper | % | 0.39 | 0.31 | 0.48 | 0.33 | 0.36 |

| Gold | g/tonne | 0.18 | 0.16 | 0.20 | 0.11 | 0.14 |

| Silver | g/tonne | 4.19 | 3.94 | 5.28 | 3.72 | 3.84 |

| Molybdenum | % | 0.01 | 0.01 | 0.01 | 0.01 | 0.01 |

| Copper concentrate | tonnes | 110,431 | 82,796 | 148,283 | 380,211 | 452,473 |

| Concentrate grade | % Cu | 22.67 | 21.88 | 22.92 | 22.40 | 21.88 |

| Copper recovery | % | 84.5 | 83.2 | 87.8 | 84.3 | 85.0 |

| Gold recovery | % | 74.7 | 72.1 | 73.3 | 69.2 | 70.7 |

| Silver recovery | % | 71.1 | 65.2 | 71.4 | 66.7 | 68.8 |

| Molybdenum recovery | % | 38.8 | 33.9 | 37.1 | 37.4 | 41.7 |

| Combined unit operating costs3,4,5 | $/tonne | 14.51 | 13.03 | 15.25 | 13.02 | 12.91 |

1 Reported tonnes and grade for ore mined are estimates based on mine plan assumptions and may not reconcile fully to ore milled.

2 Strip ratio is calculated as waste mined divided by ore mined.

3 Reflects combined mine, mill and general and administrative ("G&A") costs per tonne of ore milled. Reflects the deduction of expected capitalized stripping costs.

4 Combined unit costs is a non-GAAP financial performance measure with no standardized definition under IFRS. For further information and a detailed reconciliation, please see the discussion under the "Non-GAAP Financial Performance Measures" section of this MD&A.

5 Excludes approximately $1.3 million or $0.17 per tonne of overhead costs incurred during temporary suspension during the three months ended December 31, 2025, $7.3 million or $1.04 per tonne for the three months ended September 30, 2025 and $8.6 million or $0.28 per tonne during year ended December 31, 2025.

| Three months ended | Year ended | |||||

| Dec. 31, 2025 | Sep. 30, 2025 | Dec. 31, 2024 | Dec. 31, 2025 | Dec. 31, 2024 | ||

| Contained metal in concentrate produced | ||||||

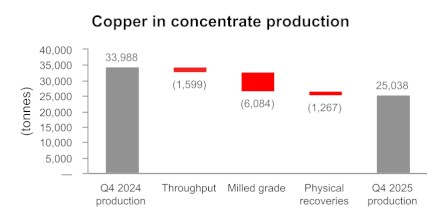

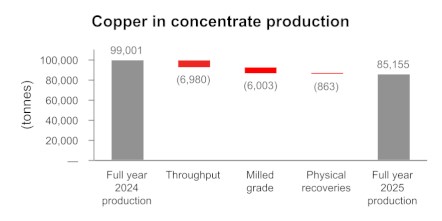

| Copper | tonnes | 25,038 | 18,114 | 33,988 | 85,155 | 99,001 |

| Gold | oz | 32,865 | 26,380 | 38,079 | 74,480 | 98,226 |

| Silver | oz | 731,017 | 577,446 | 969,502 | 2,415,134 | 2,708,262 |

| Molybdenum | tonnes | 325 | 185 | 195 | 1,282 | 1,323 |

| Payable metal sold | ||||||

| Copper | tonnes | 28,361 | 11,769 | 28,775 | 84,438 | 88,138 |

| Gold | oz | 37,874 | 9,798 | 37,459 | 71,755 | 103,364 |

| Silver | oz | 650,384 | 258,215 | 824,613 | 2,239,832 | 2,343,820 |

| Molybdenum | tonnes | 190 | 269 | 182 | 1,334 | 1,287 |

| Cost per pound of copper produced | ||||||

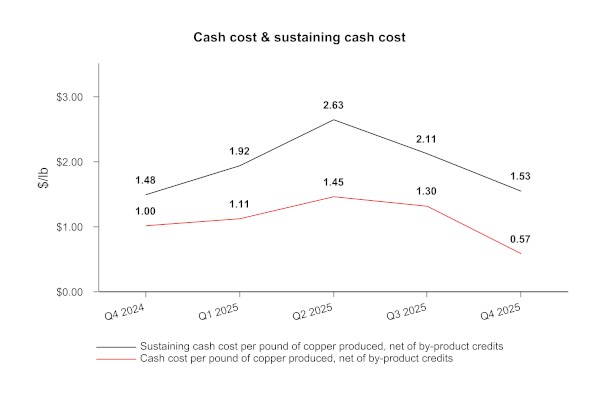

| Cash cost1,2 | $/lb | 0.57 | 1.30 | 1.00 | 1.08 | 1.18 |

| Sustaining cash cost1 | $/lb | 1.53 | 2.11 | 1.48 | 2.02 | 1.86 |

1 Cash cost and sustaining cash costs, net of by-product credits, per pound of copper produced are not recognized under IFRS. For more detail on these non-GAAP financial performance measures, please see the discussion under the "Non-GAAP Financial Performance Measures" section of this MD&A.

2 Excludes approximately $1.3 million or $0.02 per pound of overhead costs incurred during temporary suspension during the three months ended December 31, 2025, $7.3 million or $0.19 per pound during the three months ended September 30, 2025 and $8.6 million or $0.05 per pound during the year ended December 31, 2025.

Overview

Peru operations had its strongest quarter of the year in the fourth quarter, with continued strong copper and gold grades from Pampacancha and less ore processed from low-grade stockpiles compared to the third quarter of 2025. The Company continued to optimize the mine plan in the fourth quarter with more ore mined from Pampacancha than previously expected, resulting in the accelerated depletion of Pampacancha in late December as opposed to early 2026 and enabling Hudbay to exceed the top end of the 2025 Peru gold guidance range.

Despite the impacts from social unrest in the third quarter, Hudbay achieved its 2025 production guidance for copper and gold in Peru, with gold production exceeding the top end of the 2025 guidance range by 24%. Production of silver and molybdenum fell slightly short of the lower end of guidance.

As mentioned above, mining activities in the Pampacancha pit were completed during the fourth quarter and remaining stockpiled Pampacancha ore has been fully processed during January 2026.

The Company continues to advance the installation of pebble crushers in Peru to increase mill throughput rates starting in the second half of 2026, which will allow Constancia to deliver steady annual copper production despite lower grades from the depletion of Pampacancha. Hudbay's efforts to increase mill throughput align with the Peru Ministry of Energy and Mines regulatory change to allow mining companies to operate up to 10% above permitted levels.

Mining Activities

Total ore mined in the fourth quarter was 102% higher than the third quarter of 2025, a sizable increase due to the impacts from social unrest during the third quarter. Mining activities in the Pampacancha pit were completed during the fourth quarter and the remaining stockpiled Pampacancha ore was fully processed during January 2026. Total ore mined in Peru in the fourth quarter of 2025 was 19% higher than the same period in 2024, despite the ramp up required in October following the temporary operational interruption due to social unrest.

Total ore mined in Peru for the full year of 2025 was 28% higher than the same period in 2024 due to elevated waste stripping in 2024, which was partially offset by the impacts of the temporary interruption of certain mining activities during the third quarter of 2025.

Milling Activities

Total mill throughput increased to 7.6 million tonnes during the fourth quarter of 2025, higher than the third quarter of 2025 due to higher mechanical availability as the prior quarter was impacted by the temporary operational interruption due to social unrest, partially offset by a scheduled semi-annual mill maintenance shutdown in the fourth quarter of 2025. Milled copper grades increased by 26% compared to the third quarter 2025, primarily due to higher grades from Pampacancha and less ore processed from stockpiles. Milled gold grades increased compared to the third quarter of 2025 due to a higher portion of ore feed from Pampacancha where the gold grades are meaningfully higher than at Constancia. Milled gold grades decreased compared to the same period in 2024 since additional gold benches were mined as planned during the comparable quarter last year. Copper recoveries of 85% in the fourth quarter of 2025 were higher compared to the third quarter of 2025 but lower compared to the same period in 2024 due to the different proportions of ore feed from stockpiles and pits. Recoveries of gold and silver during the fourth quarter of 2025 were in line with Hudbay's metallurgical models for the ore that was being processed.

Full year ore milled was 5% lower compared to the same period in 2024 mainly due to the aforementioned social issues in the third quarter of 2025. Full year milled copper grades were 8% lower than the same period in 2024 and milled gold grades decreased by 21% due to lower grades in ore feed from the Constancia pit and lower grades in ore feed from stockpiles, both of which made up a higher proportion of ore feed. Recoveries of copper during the year were 84%, representing a decrease of 1% compared to the 2024 period due to lower head grades primarily from stockpiles. Gold and silver recoveries during the year were 69% and 67%, respectively, representing a decrease of 2% and 3%, respectively, due to ore feed from stockpiles.

Production and Sales Performance

The Peru operations produced 25,038 tonnes of copper, 32,865 ounces of gold, 731,017 ounces of silver and 325 tonnes of molybdenum during the fourth quarter of 2025. Production of copper was higher in the fourth quarter of 2025 compared to the third quarter of 2025 and lower compared to the same period in 2024. The increase in copper production compared to the third quarter of 2025 is primarily due to higher ore milled as the third quarter was impacted by a temporary operational interruption due to social unrest. The decrease in copper production compared to the same quarter last year is mainly the result of higher grades from Pampacancha in the prior year. Production of gold and silver was higher than the third quarter of 2025 but lower than the same period in 2024 for the same reasons as the variance in copper production. Production of molybdenum was higher in the fourth quarter of 2025 compared with both comparable periods due to higher recoveries and additional tonnes of ore milled in the molybdenum plant.

Full year production of copper, gold, silver and molybdenum in 2025 was 85,155 tonnes, 74,480 ounces, 2,415,134 ounces, and 1,282 tonnes, respectively, representing a decrease of 14%, 24%, 11% and 3%, respectively, from the comparative 2024 period primarily due to fewer tonnes of ore milled in the current period due to the aforementioned temporary operational interruption in the third quarter of 2025 and lower grades from higher amounts of ore processed from stockpile.

Fourth quarter copper, gold and silver metal sold was higher than the third quarter of 2025 primarily due to the shifting of copper concentrate sales at the end of the third quarter into early in the fourth quarter as a result of ocean swells at the port in late September. While copper concentrate inventory levels normalized at the end of December 2025, the concentrate contained higher levels of precious metals due to a higher portion of Pampacancha production in the second half of the year, resulting in a shift of some precious metals sales from December 2025 to January 2026.

Full year copper metal sold in 2025 was slightly lower than the comparable period but reflected normal levels of unsold copper concentrate inventory at December 31, 2025. Quantities of gold sold during 2025 were lower than 2024 due to lower production levels and the timing of precious metal sales as mentioned above.

*Copper equivalent production is calculated using the quarter average LME prices for each metal excluding molybdenum.

Cost Performance

Combined mine, mill and G&A unit operating cost in the fourth quarter of 2025 was $14.51 per tonne, 5% lower than the same period in 2024 primarily from reduced drilling and blasting together with a lower strip ratio during the current quarter. Combined mine, mill and G&A unit operating cost was 11% higher than the third quarter of 2025 due to higher fuel consumption associated with additional tonnes of material moved, higher water management and dewatering costs, and higher milling costs associated with the scheduled semi-annual mill maintenance program, partially offset by additional tonnes milled.

Combined mine, mill and G&A unit operating cost for the full year 2025 was $13.02 per tonne, which was consistent with 2024.