October 28, 2014

2014 STOCKHOLDER OUTREACH

SUMMARY OF EXECUTIVE COMPENSATION PROGRAM |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

SCHEDULE 14A

(Rule 14a-101)

Proxy Statement Pursuant to Section 14(a) of the

Securities Exchange Act of 1934

(Amendment No. )

Filed by the Registrant x Filed by a Party other than the Registrant ¨

Check the appropriate box:

| ¨ | Preliminary Proxy Statement | |

| ¨ | Confidential, for Use of the Commission Only (as permitted by Rule 14a-6(e)(2)) | |

| ¨ | Definitive Proxy Statement | |

| x | Definitive Additional Materials | |

| ¨ | Soliciting Material Pursuant to §240.14a-12 | |

SOLERA HOLDINGS, INC.

(Name of Registrant as Specified In Its Charter)

(Name of Person(s) Filing Proxy Statement, if other than the Registrant)

Payment of Filing Fee (Check the appropriate box):

| x | No fee required. | |||

| ¨ | Fee computed on table below per Exchange Act Rules 14a-6(i)(1) and 0-11. | |||

| (1) | Title of each class of securities to which transaction applies:

| |||

| (2) | Aggregate number of securities to which transaction applies:

| |||

| (3) | Per unit price or other underlying value of transaction computed pursuant to Exchange Act Rule 0-11 (set forth the amount on which the filing fee is calculated and state how it was determined):

| |||

| (4) | Proposed maximum aggregate value of transaction:

| |||

| (5) | Total fee paid:

| |||

| ¨ | Fee paid previously with preliminary materials. | |||

| ¨ | Check box if any part of the fee is offset as provided by Exchange Act Rule 0-11(a)(2) and identify the filing for which the offsetting fee was paid previously. Identify the previous filing by registration statement number, or the Form or Schedule and the date of its filing. | |||

| (1) | Amount Previously Paid:

| |||

| (2) | Form, Schedule or Registration Statement No.:

| |||

| (3) | Filing Party:

| |||

| (4) | Date Filed:

| |||

| October 28, 2014

2014 STOCKHOLDER OUTREACH

SUMMARY OF EXECUTIVE COMPENSATION PROGRAM |

SAFE

HARBOR STATEMENT Statements

in

this

presentation

that

are

not

reported

financial

results

or

other

historical

information

are

“forward-looking

statements”

within

the

meaning

of

the

Private

Securities

Litigation

Reform

Act

of

1995.

These

statements

relate

to

analyses

and

other

information

that

are

based

on

forecasts

of

future

results

and

estimates

of

amounts

not

yet

determinable

and

historical

results

or

performance

that

may

suggest

trends

for

our

business.

These

forward-looking

statements

include

statements

about:

Mission

2020,

including

our

ability

to

achieve

Mission

2020;

our

acquisition

strategy;

our

ability

to

continue

to

diversify

our

business;

geographic

expansion;

operating

benefits

emanating

from

our

capital

structure; realizable compensation associated with the Mission 2020 Awards and

historical results that may suggest trends for our business, including our

completed acquisitions, revenue and Adjusted EBITDA results, stockholder returns, our financial and operating performance

relative to our peer group companies and total direct compensation. These

forward-looking statements are based on current plans, estimates

and

expectations,

and

are

not

guarantees

of

future

performance.

They

are

based

on

management’s

expectations

that

involve

a

number

of

business risks and uncertainties, any of which could cause actual results to differ

materially from those expressed in or implied by the forward-

looking

statements.

Factors

that

could

cause

actual

results

to

differ

materially

from

the

forward-looking

statements

include,

but

are

not

limited

to:

our reliance on a limited number of customers for a substantial portion of our

revenues; unpredictability and volatility of our operating results, which

include the volatility associated with foreign currency exchange risks, our sales cycle, seasonality, global economic conditions,

acquisitions and other factors; risks associated with the uncertainty in and

volatility of global economic conditions; risks associated with and possible

negative consequences of acquisitions, joint ventures, divestitures and similar transactions, including regulatory matters and our ability

to successfully integrate our acquired businesses; we may not complete any

subsequent acquisitions of additional equity interests of our Service Repair

Solutions joint venture ("SRS"); the failure to realize the expected benefits from SRS or our investment in or subsequent

acquisition of SRS; our inability to successfully integrate SRS's business,

including SRS's existing employees, infrastructure and service

offerings,

with

our

existing

businesses

at

reasonable

cost,

or

at

all;

our

inability

to

pay

(or

finance,

as

applicable)

the

call

price

or

put

prices

for

additional equity interests in SRS at our expected cost, or at all, and the

possible reduction in our cash balance or increase in outstanding debt after

payment of such call price or put prices; risks associated with entering new

business segments with which we have limited experience or successful

integration of acquired businesses that operate in industries outside of our core market; effects of competition on our software and

service pricing and our business; time and expenses associated with customers

switching from competitive software and services to our software

and

services;

rapid

technology

changes

in

our

industry;

risks

associated

with

operating

in

multiple

countries;

risks

associated

with

a

diversified business; effects of changes in or violations by us or our customers of

government regulations; use of cash to service our debt and effects

on

our

business

of

restrictive

covenants

in

our

bond

indentures;

our

ability

to

obtain

additional

financing

as

necessary

to

support

our

operations, including Mission 2020; our reliance on third-party information for

our software and services; costs and possible future losses or impairments

relating to our acquisitions; the financial impact of future significant restructuring and severance charges; the impact of changes in

our tax provision (benefit) or effective tax rate; our ability to pay dividends or

repurchase shares in future periods; our dependence on a limited number of

key personnel; effects of system failures or security breaches on our business and reputation; and any material adverse impact of

current or future litigation on our results or business, including litigation with

Mitchell International; and other risks and uncertainties that could impact

our operations or financial results and cause our results to differ

materially from those in the forward-looking statements described in our

filings

with

the

Securities

and

Exchange

Commission,

particularly

our

Annual

Report

on

Form

10-K

for

the

year

ended

June

30,

2014.

We

undertake

no

obligation

to

publicly

update

or

revise

any

forward-looking

statement.

This

presentation

includes

a

calculation

of

Adjusted

EBITDA,

a

non-GAAP

financial

measure

that

is

different

from

financial

measures

calculated

in

accordance

with

GAAP

and

may

be

different

from

calculations

of

Adjusted

EBITDA

made

by

other

companies.

A

quantitative

reconciliation

of

Adjusted

EBITDA

to

Net

Income

and

Adjusted

Net

Income

to

GAAP

Net

earnings,

the

most

directly

comparable

GAAP

financial

measures,

was

previously

included

in

our

Q4

fiscal

year

2014

earnings release issued on August 26, 2014.

2 |

Update to

Mission 2020 Mission 2020

$2 billion in revenue and $800 million (subsequently revised to $840 million in Aug

2014) in Adjusted EBITDA by FY2020.

•

Requires significant and long-term commitment to grow the

business. •

Publicly announced in FY13.

•

Uncommon

for

companies

to

publicly

announce

such

long

term

growth

initiatives.

How do we drive the growth required to achieve Mission 2020 and mitigate

risk? •

LDD Strategy:

Leverage

our core business,

Diversify

into new markets and geographies, and

Disrupt

the market with investments in new technologies and businesses.

Mission 2020 Growth Requirements.

•

Based on our FY13 step-off rate (on a straight-line basis):

Requires revenue CAGR of 13.2%, and

Requires Adjusted EBITDA (at $800M) CAGR of 11.6%.

•

Based on our FY14 step-off rate (on a straight-line basis):

Requires revenue CAGR of 12.5%, and

Requires Adjusted EBITDA (at $840M) CAGR of 12.5%.

•

Phase

1

of

Mission

2020

(FY14

through

FY17)

–

“investment

phase”.

Including

this

investment,

annual

Adjusted

EBITDA

targets

during

Phase

1

require

growth

that

is

comparable

to

our

10.9%

compounded

annual

growth

for

three

fiscal

years

ended

June

30,

2013.

3 |

FY 2014

Accomplishments Solera

and

NEOs

delivered

strong

operating

results

and

strategic

results

in

FY14:

•

On a constant currency basis:

Grew

revenue

by

16.8%

FY13 revenue growth over FY12 results was 8.5%.

Grew

Adjusted

EBITDA

by

11.3%

over

FY13

results.

FY13 Adjusted EBITDA growth over FY12 results was 6.7%.

Adjusted

EBITDA

margin

was

42.2%

•

Completed seven acquisition transactions and announced two additional acquisition

transactions that were completed in Q1 2015, which:

Contributed approximately $242 million in annual revenue on a run-rate basis,

Strengthened

our

core

business,

and

Diversified

our

portfolio

of

businesses.

Mitigates business risk by reducing reliance on any one market or solution.

Entered

new

market

segments

(ex:

SMR,

property

and

glass

claims)

and

five

new

geographic

markets.

Non-claims revenue in FY14 was 39% of total revenue vs 27% of total revenue in

FY13. •

Completed senior notes offerings totaling $1 billion, enabling us to redeem $850 million of existing notes.

More flexible covenant package provides additional freedom to operate to

facilitate Mission 2020. •

Increased

FY14

annualized

dividend

by

36%

vs

FY13

dividend

•

Returned

to

stockholders

about

$75

million

in

value

through

dividends

and

stock

repurchases.

•

Delivered

a

TSR

of

22.0%

during

FY14,

bringing

our

five-year

compound

annual

TSR

to

22.5%.

4

(despite increased investments in the business).

over

FY13

results. |

Culture

of Meritocracy. •Well

known

and

understood

by

our

investors,

and

reflected

in

our

pay-

for-performance compensation philosophy, strategy and design.

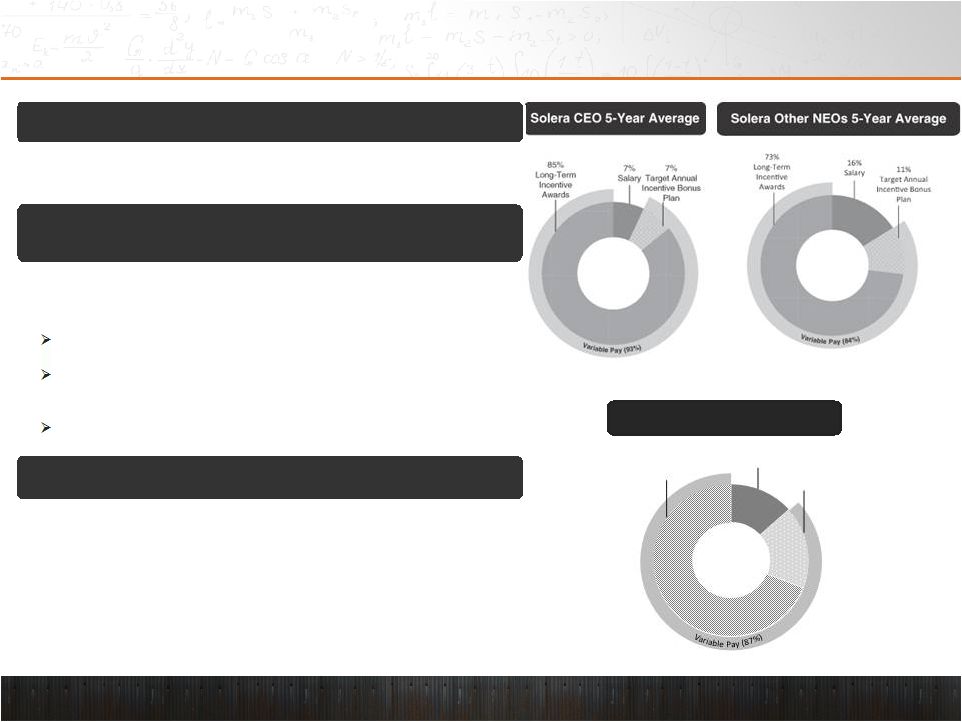

Variable vs Non-Variable Compensation.

•Non-Variable: Annual base salary.

•Variable: Annual cash bonus and LTI equity awards.

•CEO compensation (during the last five years):

93% variable vs 87% variable for similar positions in our FY15

peer group.

79% specific to performance-based equity awards or stock

options vs only 52% for FY15 peer group.

•Other NEOs (during the last five years):

84%

variable

-

Similar

strong

emphasis

on

performance-based

equity awards and stock options.

Other Effective Design Components.

•Balance

of

performance

metrics

-

shareholder

return

relative

to

peers, revenue and adjusted EBITDA growth, and ROIC.

•Severance and almost all equity awards are “double trigger”.

•No tax gross-ups in the event of a change-in-control.

•Stock ownership guidelines for all NEOs.

•NEOs subject to clawback policy.

Our Pay for Performance Philosophy, Strategy and Design

Peer Group CEOs

5

-Term

13%

Salary

18%

Annual Target

Bonus

69%

Long

Incentive

Awards |

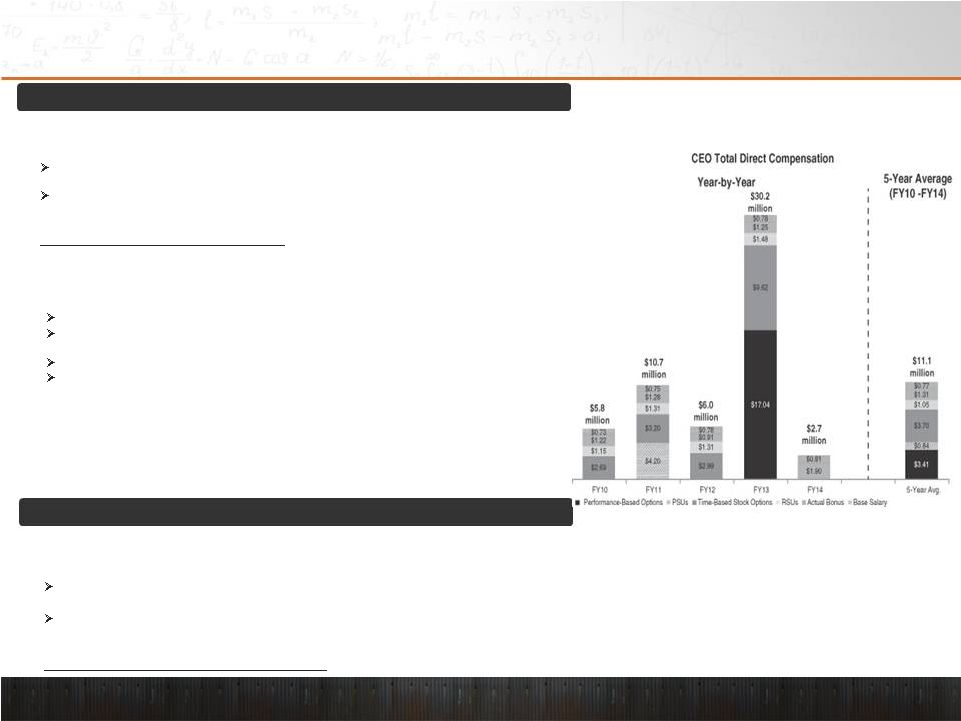

NEO Pay at

a Glance CEO Pay

•

$2.7

million

–

CEO

FY14

total

direct

compensation

(“TDC”)

reported

in

proxy

statement.

•

Consists of base salary and annual cash incentive.

•

No equity awards granted to CEO in FY14.

Mission 2020 Awards are by design significant relative to competitive practice for

annual awards.

In

recognition

of

this

dynamic,

the

Committee

does

not

intend

to

grant

any

additional

equity

to

the CEO until Q4 of FY16.

CEO

FY14

TDC

was

well

below

the

median

for

similarly

situated

positions

at

peers.

Average

CEO

TDC

during

five

years

ended

June

30,

2014

–

$11.1

million.

•

TDC not a reflection of realizable compensation.

•

FY11:

Road

to

$1

Billion

PSUs

granted

(40%

of

TDC).

Due

to

tough

relative

TSR

performance

hurdles,

only

4%

of

PSUs

were

earned

and

96%

of

the

PSUs

were

forfeited.

FY13:

Mission

2020

Awards

granted

(80%

of

TDC).

The FY14 tranche of the Mission 2020 Awards has not been earned as relative TSR vesting

hurdle has not yet been achieved.

Other NEOs Pay

•$730,000

to

$1.3

million

–

Other

NEO

FY14

TDC.

•Consists of base salary and annual cash incentive payment.

•No equity awards granted to Other NEOs in FY14.

Mission 2020 Awards granted to the Other NEOs represented a portion of their equity

awards associated with Mission 2020.

Other NEO equity awards granted in October 2014 represent the balance of the

equity award opportunity associated with Mission 2020 and take into consideration

the increased Adjusted EBITDA target for Mission 2020.

•Other

NEOs’

TDC

was

well

below

the

median

for

similarly

situated

positions

at

peers.

6

The Committee remains committed to ensuring that CEO compensation design and

opportunities are aligned with retaining and motivating Mr. Aquila to continue his

strong performance and contributions.

Highest TDC years were FY11 and FY13

•

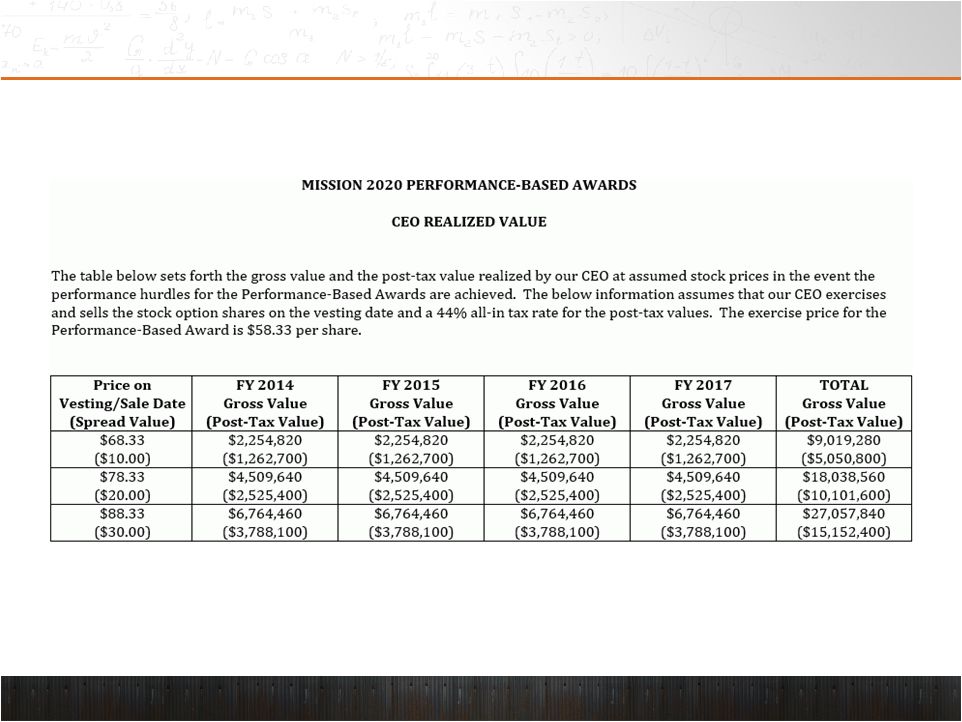

Realizable compensation does not approach summary compensation table value

until stock price reaches mid-$70s. See Annex B.

|

2013

Annual Meeting and Say-on-Pay Vote; Stockholder Engagement 2013

Annual Meeting Results. •Approx. 51.5% of the votes cast were cast FOR

MSOP. •Down from about 94% of the votes cast FOR MSOP at our 2012 Annual

Meeting. Stockholder Outreach.

•We engaged in a concerted stockholder outreach effort during FY14 and

FY15. Ensure stockholders were being heard and to address their

concerns. Connected with stockholders representing approximately 72% of

outstanding shares (including 17 of our 20 largest investors).

Consistent Feedback Themes from Stockholders.

•Consistent Theme No. 1: Consider a different financial metric as a new

vesting hurdle for the Mission 2020 Awards. •Consistent

Theme

No.

2:

Too

many

of

the

executive

comp

program’s

performance-based

elements

include

Adjusted

EBITDA.

Committee Responses to Consistent Feedback Themes.

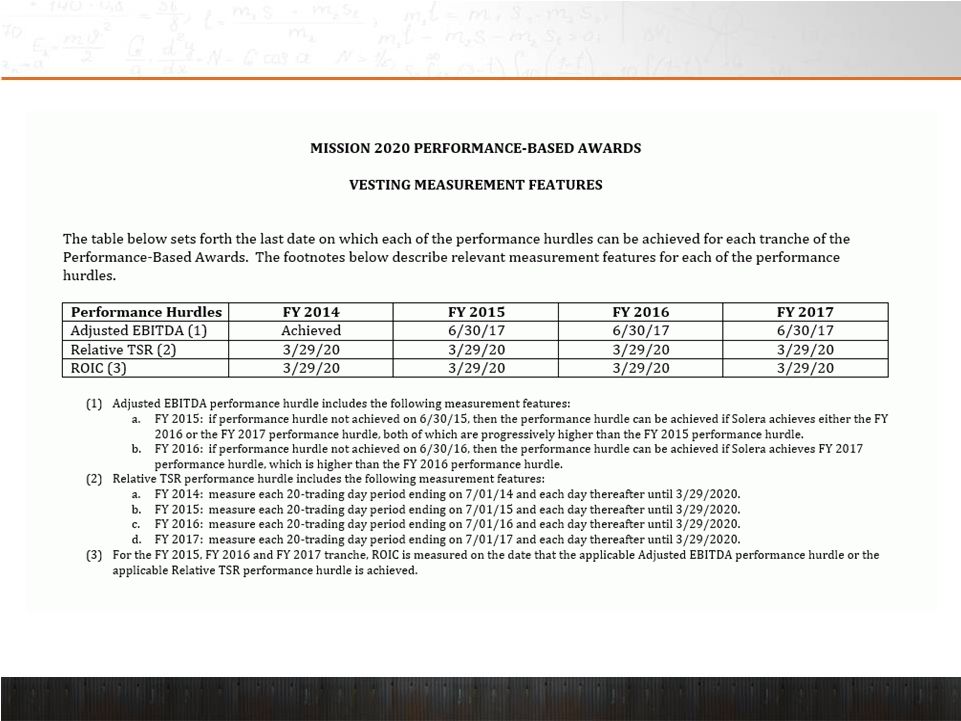

•ROIC Vesting hurdle (approved by Committee October 1, 2014):

ROIC is an additional vesting hurdle, rather than simply replacing an

existing hurdle. Accordingly, the final three tranches of the

Performance-Based Awards require that three vesting hurdles be achieved to earn the

awards

–

Adjusted

EBITDA;

Relative

TSR

(which

requires

60

th

percentile

performance);

and

ROIC.

See Annex A for an illustration of the interplay between the three vesting hurdles

for the final three tranches of the Performance- Based Awards.

•The Performance-Based Awards require exceptional performance to be

earned. Example:

We

achieved

the

Adjusted

EBITDA

vesting

hurdle

for

the

FY14

tranche

and

achieved

TSR

of

22%

in

FY14;

we

have

not

achieved

the

applicable

required

Relative

TSR

vesting

hurdle

Therefore,

this

tranche

has

not

yet

vested.

NEO and Investor Interests are Aligned.

•Mission 2020 Awards are stock options with an exercise price of $58.33.

•NEOs

will

only

realize

value

as

stock

price

appreciates,

aligning

the

interests

of

the

NEOs

and

our

investors.

7 |

Other

Feedback

from

Stockholder

Advisory

Firms

and

Investors

and

Our

Responses

Topic: NEO compensation opportunities exceed peer median levels.

•

Performance

has

historically

exceeded

peer

median

levels,

supporting

above-median

pay.

•

CEO’s FY14 TDC was well below the median for peers.

•

Rigorous performance-based compensation:

Example -

Only 4% of the Road to $1 Billion PSUs were earned and 96% were forfeited.

Example -

FY14 tranche of the Mission 2020 Awards has not been earned.

•

NEOs were not granted any equity awards during FY14.

•

We

do

more

with

less

–

Only

three

NEOs

each

with

roles

that

are

broader

than

their

peers.

Similar

dynamic

exists

across

all

management

levels

at

Solera

Result

=

Aggregate

compensation

expense

remains

modest.

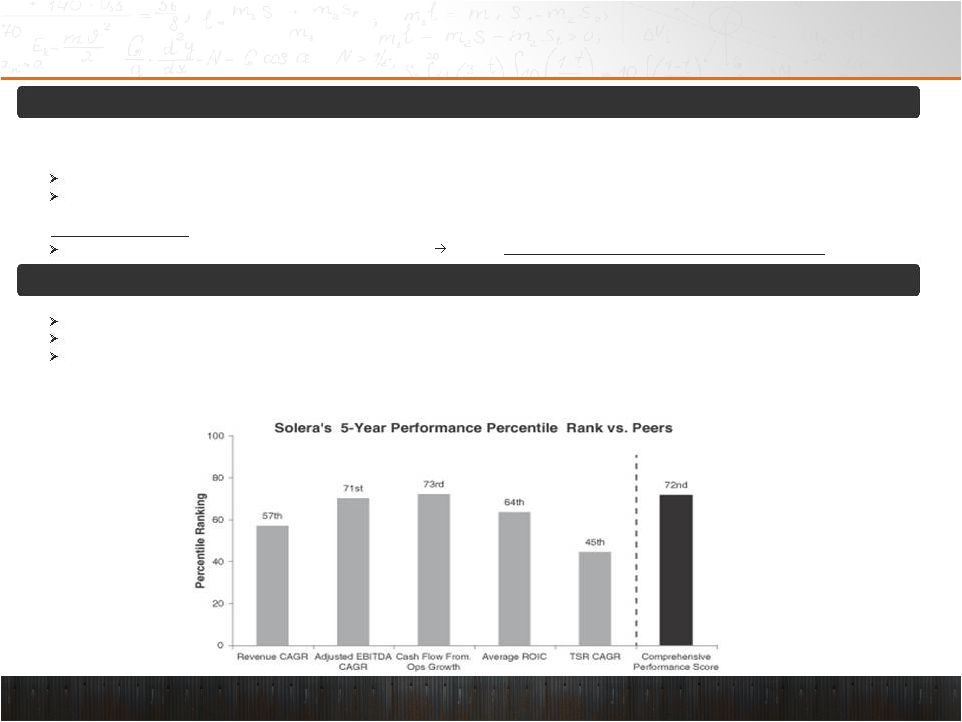

Topic: CEO pay and Company performance are not aligned.

Comprehensive approach

pay-for-performance alignment, focusing on:

Long-term performance

(five years versus three years or one year);

Evaluation of performance metrics in addition to TSR; and

Realizable compensation versus TDC

calculated in accordance with SEC regulations.

•

CEO

realizable

compensation

approximated

the

90

percentile,

our

comprehensive

performance

approximated

the

72

percentile

and

our

stockholder

value

created

approximated

the

69

percentile.

•

Difference

of

25

points

or

less

between

realizable

compensation

and

comprehensive

performance

score

suggests

reasonable

alignment.

8

th

th

nd |

Other

Feedback

from

Stockholder

Advisory

Firms

and

Investors

and

Our

Responses

Topic: Mission 2020 Awards have multiple vesting opportunities.

•Mission 2020 is an eight-year performance period

that requires growth and investment to facilitate that growth.

•Performance outcomes may be volatile in the short/medium term,

especially in regards to acquisitions, their timing and impact on our results.

•Provides ongoing incentive to achieve clear financial performance

hurdles and create stockholder value, even if early hurdles are missed.

•Progressively

higher

Adjusted

EBITDA

vesting

hurdles

–

require

an

aggressive

performance

path

and

value

creation.

•Relative

TSR

hurdles

and

the

ROIC

hurdles

reinforce

alignment

with

our

stockholders’

interests.

•Performance-Based Awards vest only if all of the vesting hurdles are

achieved. Topic: Maximum discretionary multiplier has been applied to

the CEO’s annual cash incentive. •Discretionary multiplier

provides an opportunity to recognize performance beyond that which is captured by our ABIP.

Examples: market segment and geographic diversification; business risk

mitigation; M&A execution and integration; product research and

development;

management

development

and

succession

planning;

and

enhancements

to

capital

structure.

•Discretion may be applied to either increase or decrease

compensation. •Discretion requires Committee to conduct a more

thorough assessment of CEO performance than what is captured by financial formulae.

9 |

Conclusion and Takeaways

10

Road to $1B Awards: Relative TSR performance hurdles.

Mission 2020 Awards: Relative TSR and ROIC performance hurdles; awards are stock

options. CEO and Other NEOs’

FY14 TDC well below the median.

No equity awards granted to NEOs during FY14.

CEO compensation:

Road to $1B PSUs -

due to rigorous relative TSR performance hurdles, only 4% of PSUs were earned and 96% of the PSUs were forfeited.

FY14 tranche of Mission 2020 Awards not earned

as relative TSR performance hurdle has not yet been achieved.

Based on our five-year measure of comprehensive performance and stockholder

value creation, CEO realizable pay and Company performance

are within relative alignment band.

Mission 2020 Awards: Added ROIC as an additional performance hurdle,

resulting in more rigorous performance standards

Other

Elements

of

Compensation

Program:

increased

dialogue

with

stockholders;

enhanced

explanations

of

Committee

decisions

and

rationales. |

11

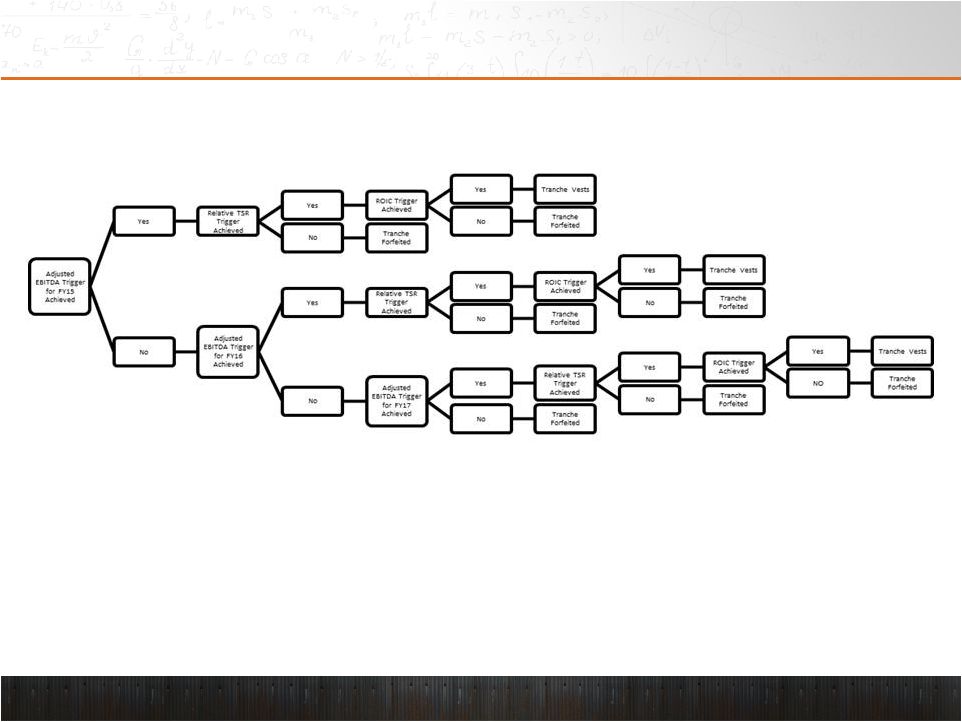

Annex A – Mission 2020 Vesting Hurdles for Second Tranche of Performance-Based Awards ROIC

Trigger– Achieve ROIC in excess our weighted average

cost of capital plus a one percent premium. ROIC Trigger must be achieved when either the

applicable Adjusted EBITDA Vesting Trigger or the applicable Relative

TSR Trigger is achieved. Relative TSR Trigger

–

Achieve greater than 60th percentile TSR rank vs. the S&P 400

midcap index constituents. Beginning point for all measurements is

March

29, 2013 and measurements consider 20 trading day trailing average

stock price. Ending date for measurement may be any 20 trading day period

ending the first day of the fiscal year (July 1) following the

applicable tranche (e.g., July 1, 2015 following the second tranche) or ending any day thereafter

through March

29, 2020.

Adjusted EBITDA

–

Calculated in a manner identical to the Adjusted EBITDA calculation in

our earnings press releases, except that we deduct non-

controlling interests as required by the Performance-Based Award

Agreement. |

Annex

B

–

Mission

2020

Performance-Based

Awards

12 |

Annex B

– (continued)

13 |