Exhibit (c)(14)

Exhibit (c)(14) Discussion Materials Prepared for the Special Committee of the Board of Directors of DCP Midstream GP, LLC January 5, 2023 [Graphic Appears Here] [Graphic Appears Here]

Exhibit (c)(14)

Exhibit (c)(14) Discussion Materials Prepared for the Special Committee of the Board of Directors of DCP Midstream GP, LLC January 5, 2023 [Graphic Appears Here] [Graphic Appears Here]

These materials have been prepared by Evercore Group L.L.C. (“Evercore”) for the Special Committee (the “Special Committee”) of the Board of Directors of DCP Midstream GP, LLC, the general partner of the general partner of DCP Midstream, LP (“DCP” or the “Partnership”), to whom such materials are directly addressed and delivered and may not be used or relied upon for any purpose other than as specifically contemplated. These materials are based on information provided by or on behalf of the Partnership and/or other potential transaction participants, from public sources or otherwise reviewed by Evercore. Evercore assumes no responsibility for independent investigation or verification of such information and has relied on such information being complete and accurate in all material respects. To the extent such information includes estimates and forecasts of future financial performance prepared by or reviewed with the management of the Partnership and/or other potential transaction participants or obtained from public sources, Evercore has assumed that such estimates and forecasts have been reasonably prepared on bases reflecting the best currently available estimates and judgments of such management (or, with respect to estimates and forecasts obtained from public sources, represent reasonable estimates). No representation or warranty, express or implied, is made as to the accuracy or completeness of such information and nothing contained herein is, or shall be relied upon as, a representation, whether as to the past, the present or the future. These materials were designed for use by specific persons familiar with the business and affairs of the Partnership. These materials are not intended to provide the sole basis for evaluating, and should not be considered a recommendation with respect to, any transaction or other matter. These materials have been developed by and are proprietary to Evercore and were prepared exclusively for the benefit and internal use of the Special Committee. These materials were compiled on a confidential basis for use of the Special Committee in evaluating the potential transaction described herein and not with a view to public disclosure or filing thereof under state or federal securities laws, and may not be reproduced, disseminated, quoted or referred to, in whole or in part, without the prior written consent of Evercore. These materials do not constitute an offer or solicitation to sell or purchase any securities and are not a commitment by Evercore (or any affiliate) to provide or arrange any financing for any transaction or to purchase any security in connection therewith. Evercore assumes no obligation to update or otherwise revise these materials. These materials may not reflect information known to other professionals in other business areas of Evercore and its affiliates. Evercore and its affiliates do not provide legal, accounting or tax advice. Accordingly, any statements contained herein as to tax matters were neither written nor intended by Evercore or its affiliates to be used and cannot be used by any taxpayer for the purpose of avoiding tax penalties that may be imposed on such taxpayer. Each person should seek legal, accounting and tax advice based on his, her or its particular circumstances from independent advisors regarding the impact of the transactions or matters described herein.

Table of Contents Section Executive Summary I DCP Situation Analysis II DCP Financial Projections III Preliminary Valuation of the Common Units IV Appendix A. Weighted Average Cost of Capital Analysis B. Supplemental Valuation Materials C. LPG Market Overview

I. Executive Summary

Executive Summary Introduction and Overview of Materials â—¼ Evercore Group L.L.C. (“Evercore”) is pleased to provide the following materials to the Special Committee (the “Special Committee”) of the Board of Directors of DCP Midstream GP, LLC (“DCP GP LLC”), the general partner of DCP Midstream GP, LP (the “General Partner”), which is the general partner of DCP Midstream, LP (“DCP” or the “Partnership”), regarding the proposed acquisition by Phillips 66 and its affiliates (collectively, “PSX,” “Phillips 66” or the “Parent”) of all of the outstanding common units (the “Common Units”) of the Partnership not already owned by Phillips 66, Enbridge, Inc. (“ENB”) and their affiliates (the “Public Common Units” and the holders of such Public Common Units, the “Partnership Unaffiliated Unitholders”) for cash (the “Merger”) ï,„ Pursuant to an agreement and plan of merger by and among the Partnership, DCP GP LLC, the General Partner, the Parent, Phillips 66 Project Development Inc., a wholly-owned subsidiary of the Parent (“PDI”), and Dynamo Merger Sub LLC, a wholly-owned subsidiary of PDI (“Merger Sub”) (the “Merger Agreement”), Merger Sub shall merge with and into the Partnership and each Common Unit owned by a Partnership Unaffiliated Unitholder shall be converted into the right to receive $41.75 in cash (the “Merger Consideration”) • Implies a 20.1% premium to PSX’s offer of $34.75 per Public Common Unit (the “Original Offer”) made as of August 17, 2022 (the “Unaffected Date”) • Represents a 21.2% premium to the 10-day1 VWAP of the Common Units as of the Unaffected Date • Represents a 28.5% premium to the 30-day1 VWAP of the Common Units as of the Unaffected Date • PSX currently owns 43.3% of the Common Units2 A â—¼ The Evercore analysis reviews valuation of the Common Units based on the financial projections for DCP as provided by DCP management (the “DCP Financial Projections” or the “Forecast”) as well as sensitivities based on certain price decks including:ï,„ B A sensitivity case utilizing NYMEX Strip Pricing as of January 3, 2023 (“Sensitivity Case B – NYMEX Strip Pricing Case”)ï,„ A sensitivity case based on assumed pricing higher than that utilized in the DCP Financial Projections (“Sensitivity Case C – C Higher Commodity Prices”) ï,„ A sensitivity case based on assumed pricing lower than that utilized in the DCP Financial Projections (“Sensitivity Case D – D Lower Commodity Prices”) Source: DCP Management, FactSet 1. Trading days 2. As of January 4, 2023

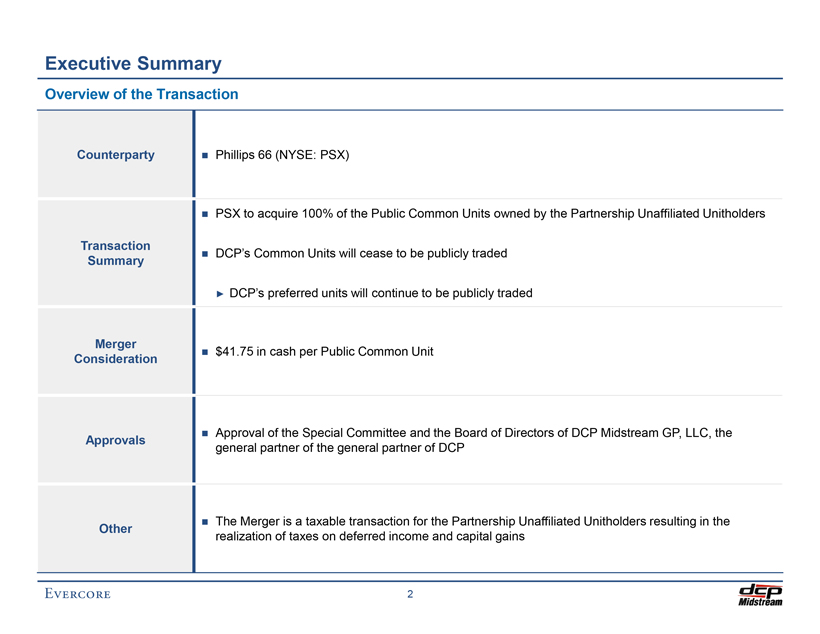

Executive Summary Overview of the Transaction Counterparty â—¼ Phillips 66 (NYSE: PSX) â—¼ PSX to acquire 100% of the Public Common Units owned by the Partnership Unaffiliated Unitholders Transaction â—¼ DCP’s Common Units will cease to be publicly traded Summary â–º DCP’s preferred units will continue to be publicly traded Merger â—¼ $41.75 in cash per Public Common Unit Consideration â—¼ Approval of the Special Committee and the Board of Directors of DCP Midstream GP, LLC, the Approvals general partner of the general partner of DCP â—¼ The Merger is a taxable transaction for the Partnership Unaffiliated Unitholders resulting in the Other realization of taxes on deferred income and capital gains

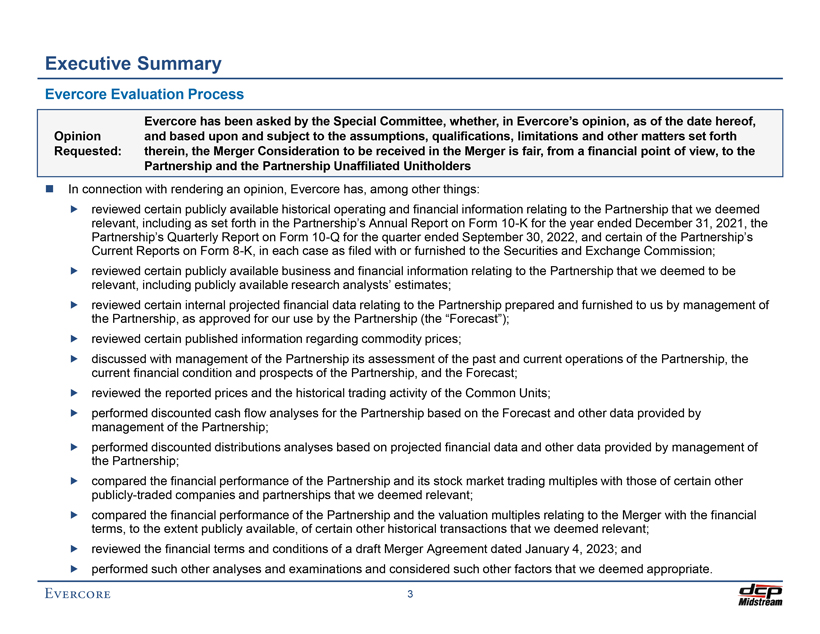

Executive Summary Evercore Evaluation Process Evercore has been asked by the Special Committee, whether, in Evercore’s opinion, as of the date hereof, Opinion and based upon and subject to the assumptions, qualifications, limitations and other matters set forth Requested: therein, the Merger Consideration to be received in the Merger is fair, from a financial point of view, to the Partnership and the Partnership Unaffiliated Unitholders â—¼ In connection with rendering an opinion, Evercore has, among other things: ï,„ reviewed certain publicly available historical operating and financial information relating to the Partnership that we deemed relevant, including as set forth in the Partnership’s Annual Report on Form 10-K for the year ended December 31, 2021, the Partnership’s Quarterly Report on Form 10-Q for the quarter ended September 30, 2022, and certain of the Partnership’s Current Reports on Form 8-K, in each case as filed with or furnished to the Securities and Exchange Commission;ï,„ reviewed certain publicly available business and financial information relating to the Partnership that we deemed to be relevant, including publicly available research analysts’ estimates; ï,„ reviewed certain internal projected financial data relating to the Partnership prepared and furnished to us by management of the Partnership, as approved for our use by the Partnership (the “Forecast”); ï,„ reviewed certain published information regarding commodity prices; ï,„ discussed with management of the Partnership its assessment of the past and current operations of the Partnership, the current financial condition and prospects of the Partnership, and the Forecast;ï,„ reviewed the reported prices and the historical trading activity of the Common Units;ï,„ performed discounted cash flow analyses for the Partnership based on the Forecast and other data provided by management of the Partnership;ï,„ performed discounted distributions analyses based on projected financial data and other data provided by management of the Partnership;ï,„ compared the financial performance of the Partnership and its stock market trading multiples with those of certain other publicly-traded companies and partnerships that we deemed relevant;ï,„ compared the financial performance of the Partnership and the valuation multiples relating to the Merger with the financial terms, to the extent publicly available, of certain other historical transactions that we deemed relevant; ï,„ reviewed the financial terms and conditions of a draft Merger Agreement dated January 4, 2023; andï,„ performed such other analyses and examinations and considered such other factors that we deemed appropriate.

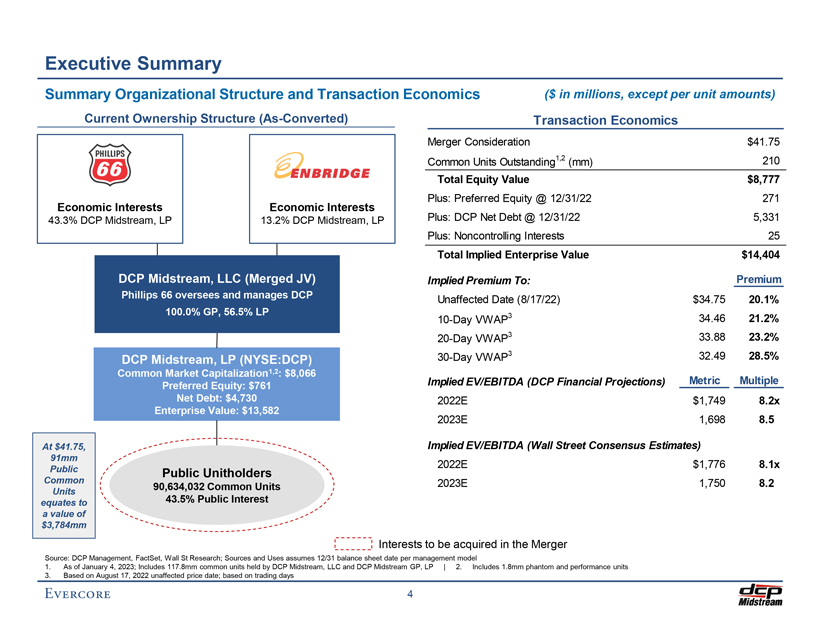

Executive Summary Summary Organizational Structure and Transaction Economics Current Ownership Structure (As-Converted) Economic Interests 43.3% DCP Midstream, LP Economic Interests 13.2% DCP Midstream, LP DCP Midstream, LLC (Merged JV) Phillips 66 oversees and manages DCP 100.0% GP, 56.5% LP DCP Midstream, LP (NYSE:DCP) Common Market Capitalization1,2: $8,066 Preferred Equity: $761 Net Debt: $4,730 Enterprise Value: $13,582 At $41.75, 91mm Public Public Unitholders Common 90,634,032 Common Units Units equates to 43.5% Public Interest a value of $3,784mm ($ in millions, except per unit amounts) Transaction Economics Merger Consideration $41.75 Common Units Outstanding1,2 (mm) 210 Total Equity Value $8,777 Plus: Preferred Equity @ 12/31/22 271 Plus: DCP Net Debt @ 12/31/22 5,331 Plus: Noncontrolling Interests 25 Total Implied Enterprise Value $14,404 Implied Premium To: Premium Unaffected Date (8/17/22) $34.75 20.1% 10-Day VWAP3 34.46 21.2% 20-Day VWAP3 33.88 23.2% 30-Day VWAP3 32.49 28.5% Implied EV/EBITDA (DCP Financial Projections) Metric Multiple 2022E $1,749 8.2x 2023E 1,698 8.5 Implied EV/EBITDA (Wall Street Consensus Estimates) 2022E $1,776 8.1x 2023E 1,750 8.2 Interests to be acquired in the Merger Source: DCP Management, FactSet, Wall St Research; Sources and Uses assumes 12/31 balance sheet date per management model 1. As of January 4, 2023; Includes 117.8mm common units held by DCP Midstream, LLC and DCP Midstream GP, LP | 2. Includes 1.8mm phantom and performance units 3. Based on August 17, 2022 unaffected price date; based on trading days

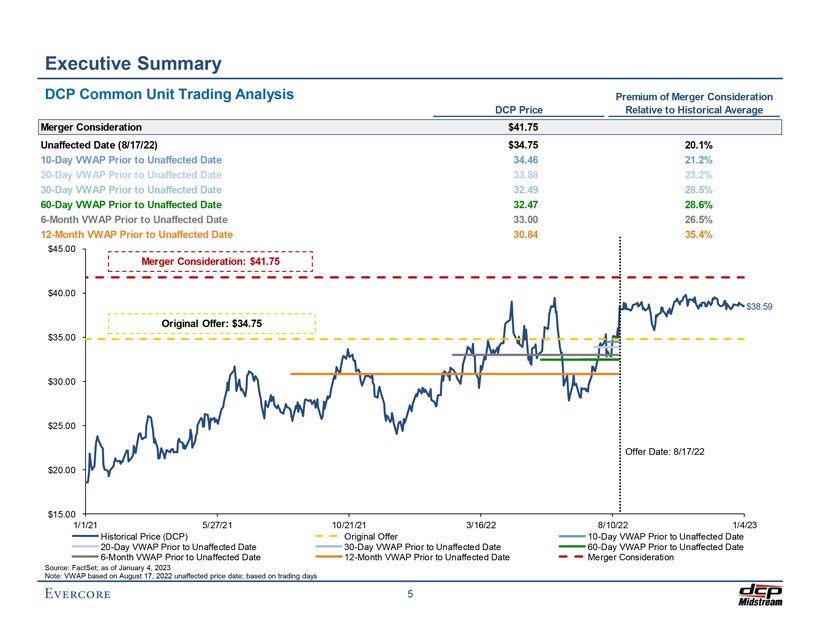

Executive Summary DCP Common Unit Trading Analysis Premium of Merger Consideration DCP Price Relative to Historical Average Merger Consideration $41.75 Unaffected Date (8/17/22) $34.75 20.1% 10-Day VWAP Prior to Unaffected Date 34.46 21.2% 20-Day VWAP Prior to Unaffected Date 33.88 23.2% 30-Day VWAP Prior to Unaffected Date 32.49 28.5% 60-Day VWAP Prior to Unaffected Date 32.47 28.6% 6-Month VWAP Prior to Unaffected Date 33.00 26.5% 12-Month VWAP Prior to Unaffected Date 30.84 35.4% [Graphic Appears Here] Historical Price (DCP) Original Offer 10-Day VWAP Prior to Unaffected Date 20-Day VWAP Prior to Unaffected Date 30-Day VWAP Prior to Unaffected Date 60-Day VWAP Prior to Unaffected Date 6-Month VWAP Prior to Unaffected Date 12-Month VWAP Prior to Unaffected Date Merger Consideration Source: FactSet; as of January 4, 2023 Note: VWAP based on August 17, 2022 unaffected price date; based on trading days

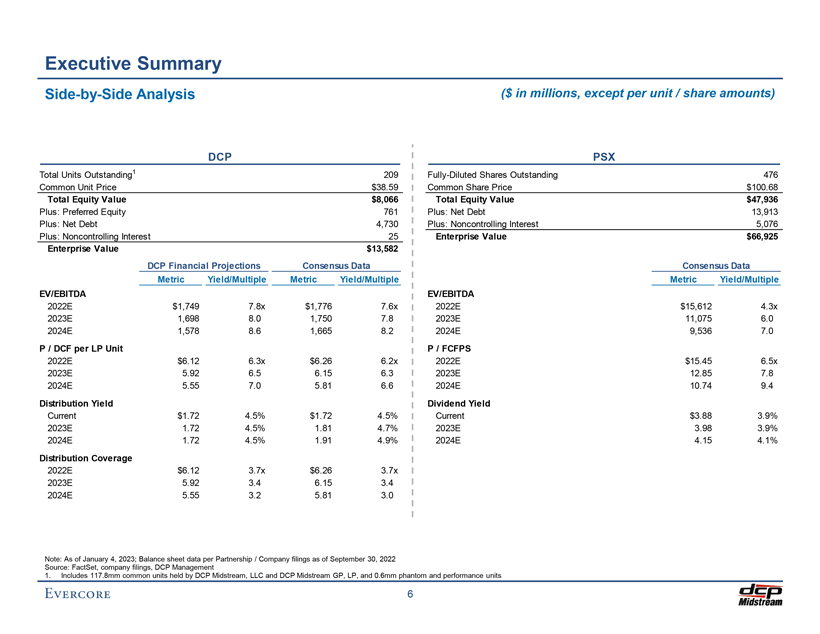

Executive Summary Side-by-Side Analysis ($ in millions, except per unit / share amounts) DCP Total Units Outstanding1 209 Common Unit Price $38.59 Total Equity Value $8,066 Plus: Preferred Equity 761 Plus: Net Debt 4,730 Plus: Noncontrolling Interest 25 Enterprise Value $13,582 DCP Financial Projections Consensus Data Metric Yield/Multiple Metric Yield/Multiple EV/EBITDA 2022E $1,749 7.8x $1,776 7.6x 2023E 1,698 8.0 1,750 7.8 2024E 1,578 8.6 1,665 8.2 P / DCF per LP Unit 2022E $6.12 6.3x $6.26 6.2x 2023E 5.92 6.5 6.15 6.3 2024E 5.55 7.0 5.81 6.6 Distribution Yield Current $1.72 4.5% $1.72 4.5% 2023E 1.72 4.5% 1.81 4.7% 2024E 1.72 4.5% 1.91 4.9% Distribution Coverage 2022E $6.12 3.7x $6.26 3.7x 2023E 5.92 3.4 6.15 3.4 2024E 5.55 3.2 5.81 3.0 PSX Fully-Diluted Shares Outstanding 476 Common Share Price $100.68 Total Equity Value $47,936 Plus: Net Debt 13,913 Plus: Noncontrolling Interest 5,076 Enterprise Value $66,925 Consensus Data Metric Yield/Multiple EV/EBITDA 2022E $15,612 4.3x 2023E 11,075 6.0 2024E 9,536 7.0 P / FCFPS 2022E $15.45 6.5x 2023E 12.85 7.8 2024E 10.74 9.4 Dividend Yield Current $3.88 3.9% 2023E 3.98 3.9% 2024E 4.15 4.1% Note: As of January 4, 2023; Balance sheet data per Partnership / Company filings as of September 30, 2022 Source: FactSet, company filings, DCP Management 1. Includes 117.8mm common units held by DCP Midstream, LLC and DCP Midstream GP, LP, and 0.6mm phantom and performance units

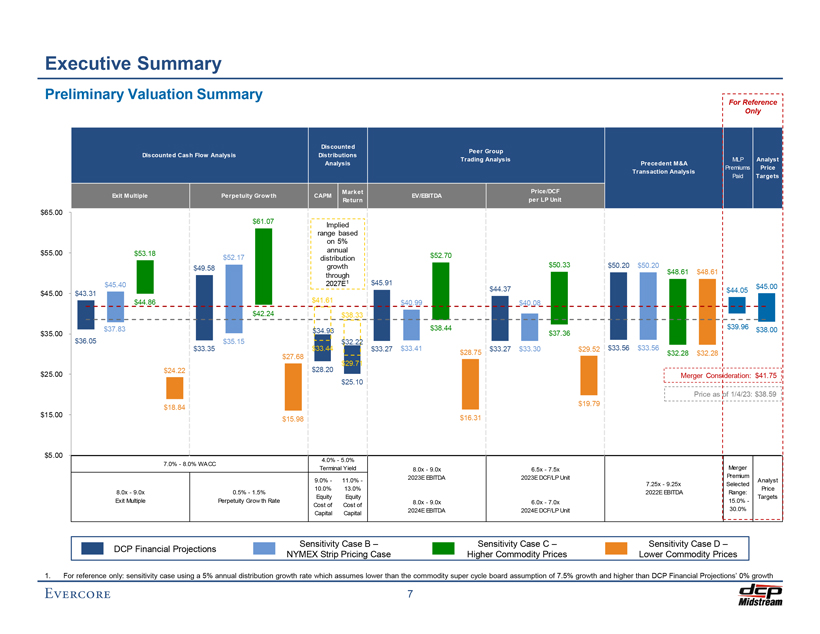

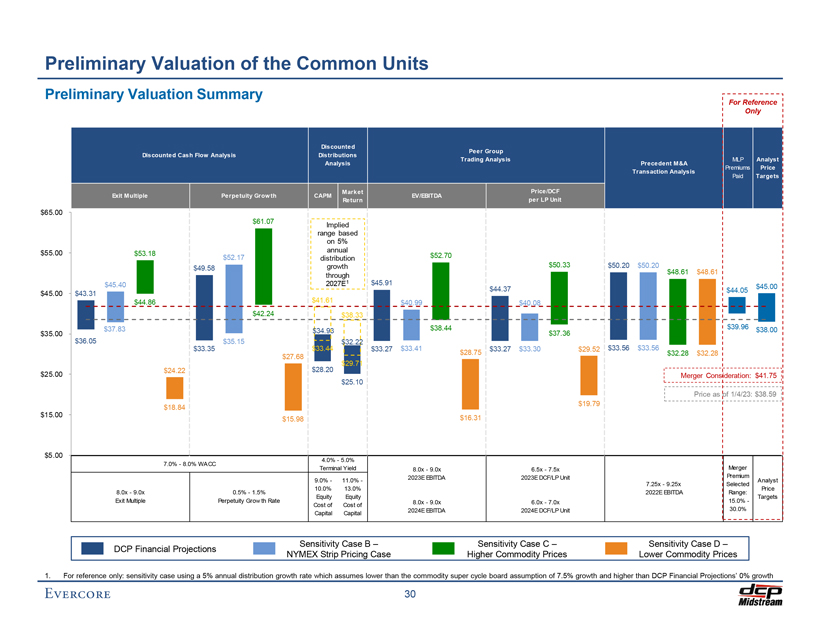

Executive Summary Preliminary Valuation Summary Discounted Peer Group Discounted Cash Flow Analysis Distributions Trading Analysis MLP Analyst Analysis Precedent M&A Premiums Price Transaction Analysis Paid Targets Market Price/DCF Exit Multiple Perpetuity Grow th CAPM EV/EBITDA Return per LP Unit $65.00 $61.07 Implied range based on 5% $55.00 annual $53.18 $52.70 $52.17 distribution growth $50.33 $50.20 $50.20 $49.58 $48.61 $48.61 through $45.40 2027E1 $45.91 $44.37 $45.00 $45.00 $43.31 $44.05 $44.86 $41.61 $40.99 $40.08 $42.24 $38.33 $37.83 $38.44 $39.96 $38.00 $35.00 $34.93 $37.36 $36.05 $35.15 $32.22 $33.35 $33.44 $33.27 $33.41 $33.27 $33.30 $29.52 $33.56 $33.56 $28.75 $32.28 $32.28 $27.68 $28.20 $29.71 $24.22 $25.00 Merger Consideration: $41.75 $25.10 Price as of 1/4/23: $38.59 $19.79 $18.84 $15.00 $16.31 $15.98 $5.00 4.0%—5.0% 7.0%—8.0% WACC Terminal Yield 8.0x—9.0x 6.5x—7.5x Merger 2023E EBITDA 2023E DCF/LP Unit Premium 9.0%—11.0%—Analyst 7.25x—9.25x Selected 10.0% 13.0% Price 8.0x—9.0x 0.5%—1.5% 2022E EBITDA Range: Equity Equity Targets Exit Multiple Perpetuity Grow th Rate 8.0x—9.0x 6.0x—7.0x 15.0%—Cost of Cost of 2024E EBITDA 2024E DCF/LP Unit 30.0% Capital Capital Sensitivity Case B – Sensitivity Case C – Sensitivity Case D –DCP Financial Projections NYMEX Strip Pricing Case Higher Commodity Prices Lower Commodity Prices [Graphic Appears Here] 1. For reference only: sensitivity case using a 5% annual distribution growth rate which assumes lower than the commodity super cycle board assumption of 7.5% growth and higher than DCP Financial Projections’ 0% growth

Executive Summary Benefits to the Partnership of the Merger â—¼ Simplified structure â—¼ Reduced cost of capital under the Parent’s capital structure and improved access to capital â—¼ Reduced pro forma leverage given ability to repay debt on an accelerated basis â—¼ Participation in pro forma cost savings and operating synergies including enhanced connectivity from wellhead to end markets â—¼ Greater flexibility and ability to pursue growth projects and strategic acquisitions â—¼ Reduced reporting requirements as a wholly-owned subsidiary of PSX

II. DCP Situation Analysis

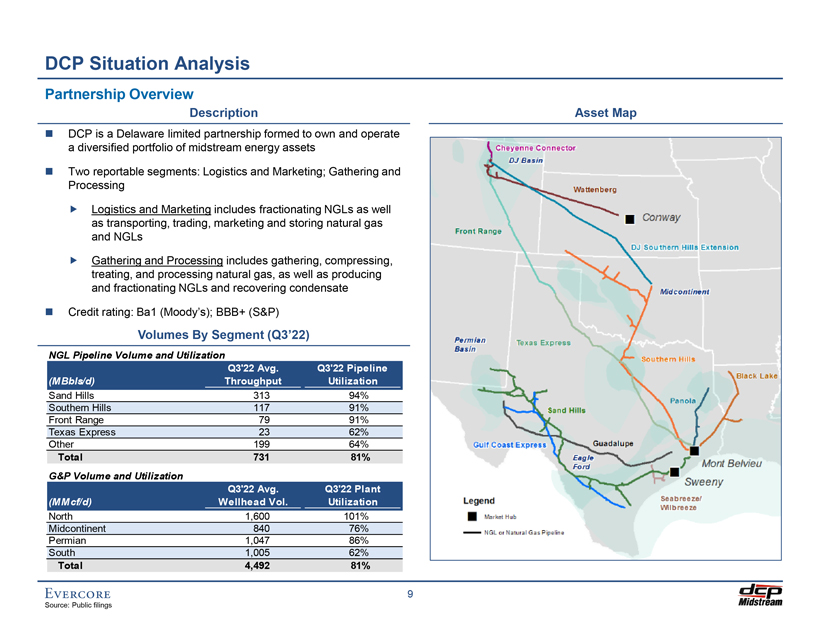

DCP Situation Analysis Partnership Overview Description DCP is a Delaware limited partnership formed to own and operate a diversified portfolio of midstream energy assets Two reportable segments: Logistics and Marketing; Gathering and Processing Logistics and Marketing includes fractionating NGLs as well as transporting, trading, marketing and storing natural gas and NGLs Gathering and Processing includes gathering, compressing, treating, and processing natural gas, as well as producing and fractionating NGLs and recovering condensate Credit rating: Ba1 (Moody’s); BBB+ (S&P) Volumes By Segment (Q3’22) NGL Pipeline Volume and Utilization Q3’22 Avg. Q3’22 Pipeline (MBbls/d) Throughput Utilization Sand Hills 313 94% Southern Hills 117 91% Front Range 79 91% Texas Express 23 62% Other 199 64% Total 731 81% G&P Volume and Utilization Q3’22 Avg. Q3’22 Plant (MMcf/d) Wellhead Vol. Utilization North 1,600 101% Midcontinent 840 76% Permian 1,047 86% South 1,005 62% Total 4,492 81% Asset Map

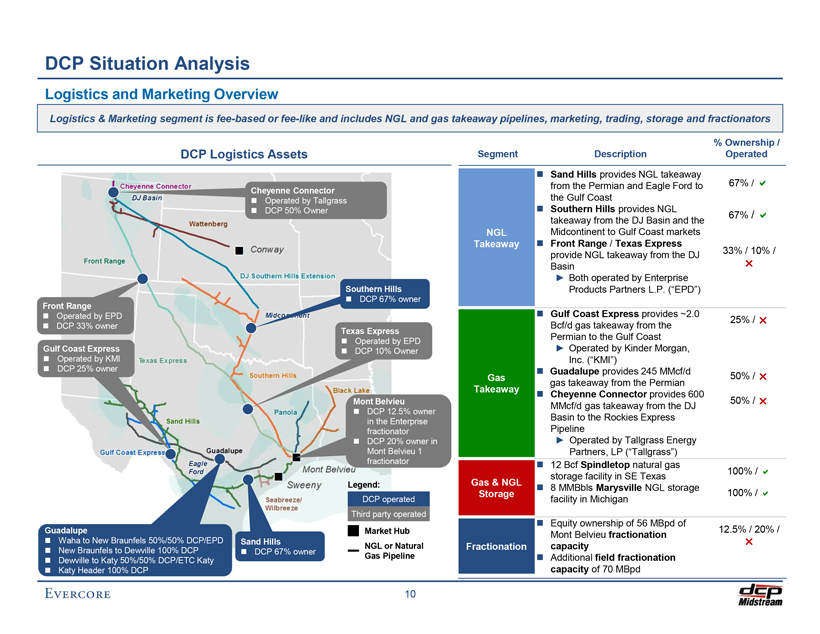

DCP Situation Analysis Logistics and Marketing Overview Logistics & Marketing segment is fee-based or fee-like and includes NGL and gas takeaway pipelines, marketing, trading, storage and fractionators DCP Logistics Assets Cheyenne Connector â—¼ Operated by Tallgrass â—¼ DCP 50% Owner Southern Hills Front Range â—¼ DCP 67% owner â—¼ Operated by EPD â—¼ DCP 33% owner Texas Express Gulf Coast Express â—¼ Operated by EPD â—¼ Operated by KMI â—¼ DCP 10% Owner â—¼ DCP 25% owner Mont Belvieu â—¼ DCP 12.5% owner in the Enterprise fractionator â—¼ DCP 20% owner in Mont Belvieu 1 fractionator Legend: DCP operated Third party operated Guadalupe Market Hub â—¼ Waha to New Braunfels 50%/50% DCP/EPD Sand Hills NGL or Natural â—¼ New Braunfels to Dewville 100% DCP â—¼ DCP 67% owner Gas Pipeline â—¼ Dewville to Katy 50%/50% DCP/ETC Katy â—¼ Katy Header 100% DCP [Graphic Appears Here] % Ownership / Segment Description Operated Sand Hills provides NGL takeaway / from the Permian and Eagle Ford to 67% the Gulf Coast Southern Hills provides NGL 67% / takeaway from the DJ Basin and the NGL Midcontinent to Gulf Coast markets Takeaway Front Range / Texas Express provide NGL takeaway from the DJ 33% / 10% / Basin Both operated by Enterprise Products Partners L.P. (“EPD”) Gulf Coast Express provides ~2.0 25% / Bcf/d gas takeaway from the Permian to the Gulf Coast Operated by Kinder Morgan, Inc. (“KMI”) Guadalupe provides 245 MMcf/d Gas 50% / gas takeaway from the Permian Takeaway Cheyenne Connector provides 600 50% / MMcf/d gas takeaway from the DJ Basin to the Rockies Express Pipeline Operated by Tallgrass Energy Partners, LP (“Tallgrass”) 12 Bcf Spindletop natural gas 100% / storage facility in SE Texas Gas & NGL 8 MMBbls Marysville NGL storage Storage 100% / facility in Michigan Equity ownership of 56 MBpd of 12.5% / 20% / Mont Belvieu fractionation Fractionation capacity Additional field fractionation capacity of 70 MBpd

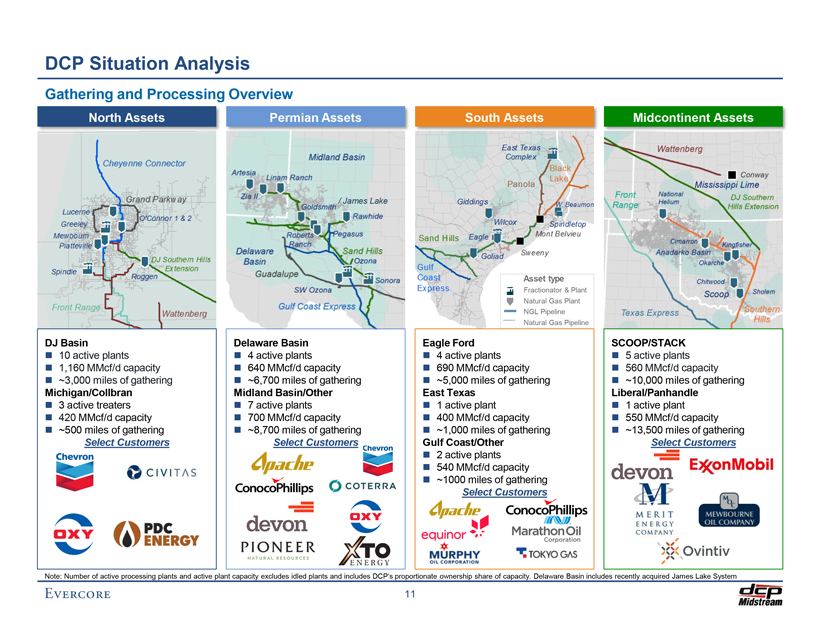

DCP Situation Analysis Gathering and Processing Overview North Assets DJ Basin â—¼ 10 active plants â—¼ 1,160 MMcf/d capacity â—¼ ~3,000 miles of gathering Michigan/Collbran â—¼ 3 active treaters â—¼ 420 MMcf/d capacity â—¼ ~500 miles of gathering Select Customers [Graphic Appears Here] Permian Assets / James Lake Delaware Basin â—¼ 4 active plants â—¼ 640 MMcf/d capacity â—¼ ~6,700 miles of gathering Midland Basin/Other â—¼ 7 active plants â—¼ 700 MMcf/d capacity â—¼ ~8,700 miles of gathering Select Customers [Graphic Appears Here] South Assets Asset type Fractionator & Plant Natural Gas Plant NGL Pipeline Natural Gas Pipeline Eagle Ford â—¼ 4 active plants â—¼ 690 MMcf/d capacity â—¼ ~5,000 miles of gathering East Texas â—¼ 1 active plant â—¼ 400 MMcf/d capacity â—¼ ~1,000 miles of gathering Gulf Coast/Other â—¼ 2 active plants â—¼ 540 MMcf/d capacity â—¼ ~1000 miles of gathering Select Customers [Graphic Appears Here] Midcontinent Assets SCOOP/STACK â—¼ 5 active plants â—¼ 560 MMcf/d capacity â—¼ ~10,000 miles of gathering Liberal/Panhandle â—¼ 1 active plant â—¼ 550 MMcf/d capacity â—¼ ~13,500 miles of gathering Select Customers [Graphic Appears Here] Note: Number of active processing plants and active plant capacity excludes idled plants and includes DCP’s proportionate ownership share of capacity. Delaware Basin includes recently acquired James Lake System

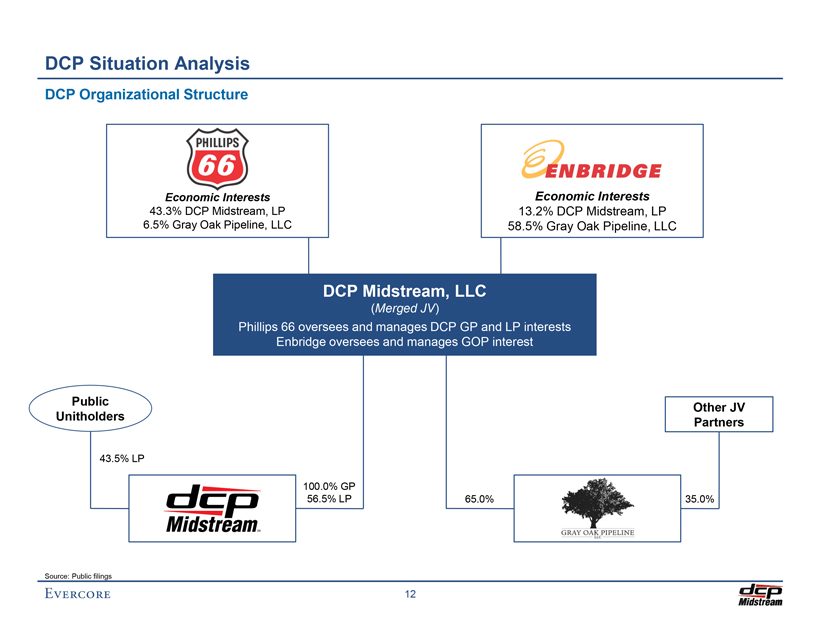

DCP Situation Analysis DCP Organizational Structure [Graphic Appears Here] Economic Interests 43.3% DCP Midstream, LP 6.5% Gray Oak Pipeline, LLC [Graphic Appears Here] Economic Interests 13.2% DCP Midstream, LP 58.5% Gray Oak Pipeline, LLC DCP Midstream, LLC (Merged JV) Phillips 66 oversees and manages DCP GP and LP interests Enbridge oversees and manages GOP interest Public Unitholders 43.5% LP [Graphic Appears Here] 100.0% GP 56.5% LP 65.0% [Graphic Appears Here] Other JV Partners 35.0% Source: Public filings

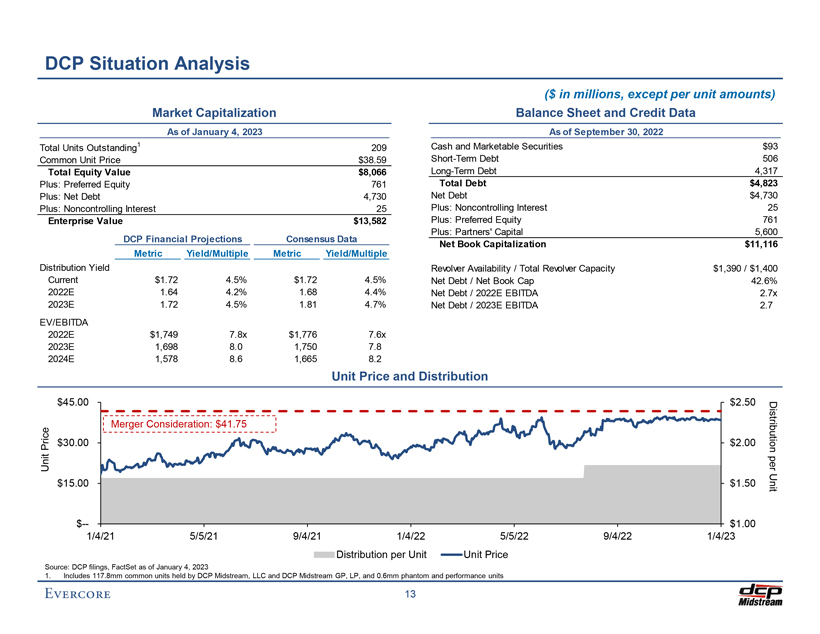

DCP Situation Analysis Market Capitalization As of January 4, 2023 Total Units Outstanding1 209 Common Unit Price $38.59 Total Equity Value $8,066 Plus: Preferred Equity 761 Plus: Net Debt 4,730 Plus: Noncontrolling Interest 25 Enterprise Value $13,582 DCP Financial Projections Consensus Data Metric Yield/Multiple Metric Yield/Multiple Distribution Yield Current $1.72 4.5% $1.72 4.5% 2022E 1.64 4.2% 1.68 4.4% 2023E 1.72 4.5% 1.81 4.7% EV/EBITDA 2022E $1,749 7.8x $1,776 7.6x 2023E 1,698 8.0 1,750 7.8 2024E 1,578 8.6 1,665 8.2 ($ in millions, except per unit amounts) Balance Sheet and Credit Data As of September 30, 2022 Cash and Marketable Securities $93 Short-Term Debt 506 Long-Term Debt 4,317 Total Debt $4,823 Net Debt $4,730 Plus: Noncontrolling Interest 25 Plus: Preferred Equity 761 Plus: Partners’ Capital 5,600 Net Book Capitalization $11,116 Revolver Availability / Total Revolver Capacity $1,390 / $1,400 Net Debt / Net Book Cap 42.6% Net Debt / 2022E EBITDA 2.7x Net Debt / 2023E EBITDA 2.7 Unit Price and Distribution [Graphic Appears Here] Distribution per Unit Unit Price Source: DCP filings, FactSet as of January 4, 2023 1. Includes 117.8mm common units held by DCP Midstream, LLC and DCP Midstream GP, LP, and 0.6mm phantom and performance units

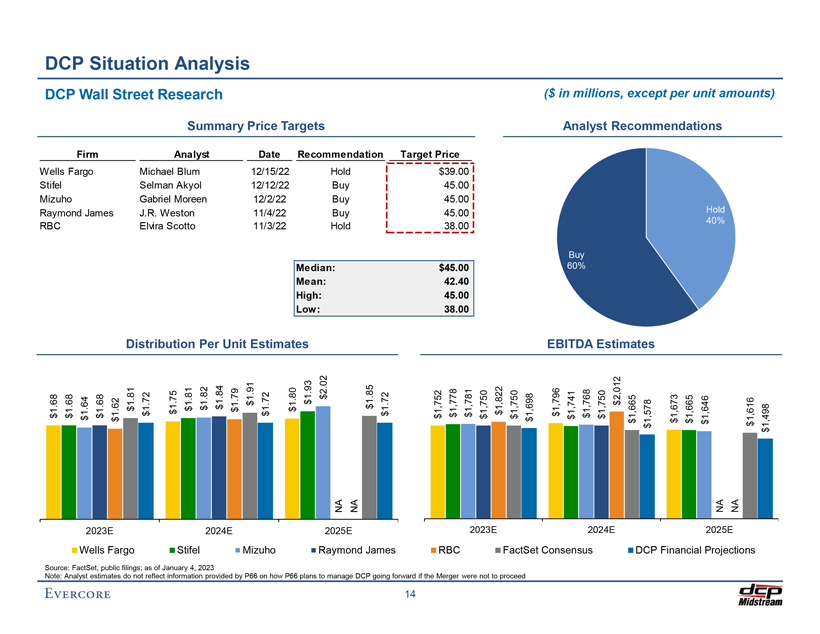

DCP Situation Analysis DCP Wall Street Research Summary Price Targets Firm Analyst Date Recommendation Target Price Wells Fargo Michael Blum 12/15/22 Hold $39.00 Stifel Selman Akyol 12/12/22 Buy 45.00 Mizuho Gabriel Moreen 12/2/22 Buy 45.00 Raymond James J.R. Weston 11/4/22 Buy 45.00 RBC Elvira Scotto 11/3/22 Hold 38.00 Median: $45.00 Mean: 42.40 High: 45.00 Low: 38.00 ($ in millions, except per unit amounts) Analyst Recommendations [Graphic Appears Here] Distribution Per Unit Estimates EBITDA Estimates [Graphic Appears Here] [Graphic Appears Here] 2023E 2024E 2025E Wells Fargo Stifel Mizuho Raymond James 2023E 2024E 2025E RBC FactSet Consensus DCP Financial Projections Source: FactSet, public filings; as of January 4, 2023 Note: Analyst estimates do not reflect information provided by P66 on how P66 plans to manage DCP going forward if the Merger were not to proceed

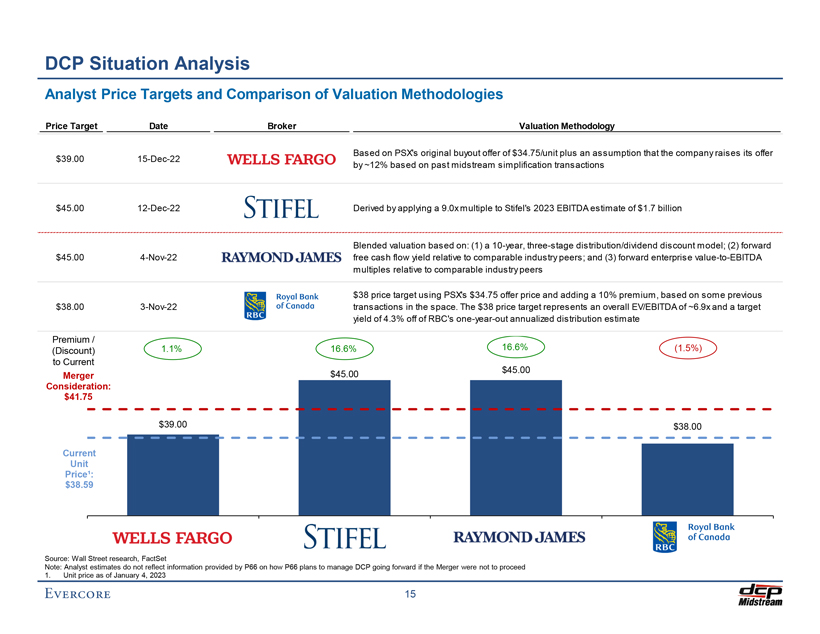

DCP Situation Analysis Analyst Price Targets and Comparison of Valuation Methodologies Price Target Date Broker Valuation Methodology Based on PSX’s original buyout offer of $34.75/unit plus an assumption that the company raises its offer $39.00 15-Dec-22 by ~12% based on past midstream simplification transactions $45.00 12-Dec-22 Derived by applying a 9.0x multiple to Stifel’s 2023 EBITDA estimate of $1.7 billion Blended valuation based on: (1) a 10-year, three-stage distribution/dividend discount model; (2) forward $45.00 4-Nov-22 free cash flow yield relative to comparable industry peers; and (3) forward enterprise value-to-EBITDA multiples relative to comparable industry peers $38 price target using PSX’s $34.75 offer price and adding a 10% premium, based on some previous $38.00 3-Nov-22 transactions in the space. The $38 price target represents an overall EV/EBITDA of ~6.9x and a target yield of 4.3% off of RBC’s one-year-out annualized distribution estimate Premium / 16.6% (Discount) 1.1% 16.6% (1.5%) to Current $45.00 Merger $45.00 Consideration: $41.75 $39.00 $38.00 Current Unit Price¹: $38.59 [Graphic Appears Here] [Graphic Appears Here] Source: Wall Street research, FactSet Note: Analyst estimates do not reflect information provided by P66 on how P66 plans to manage DCP going forward if the Merger were not to proceed 1. Unit price as of January 4, 2023

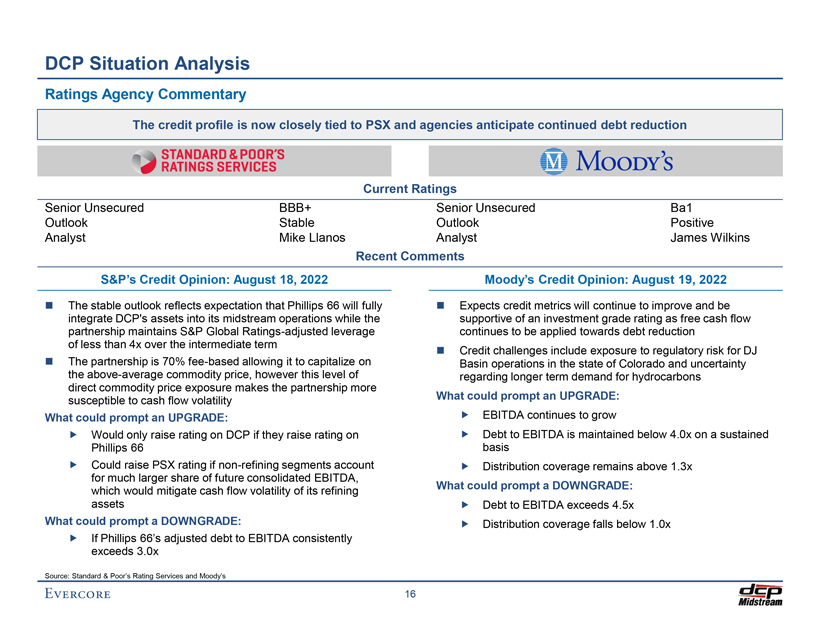

DCP Situation Analysis Ratings Agency Commentary The credit profile is now closely tied to PSX and agencies anticipate continued debt reduction Current Ratings Senior Unsecured BBB+ Senior Unsecured Ba1 Outlook Stable Outlook Positive Analyst Mike Llanos Analyst James Wilkins Recent Comments S&P’s Credit Opinion: August 18, 2022 â—¼ The stable outlook reflects expectation that Phillips 66 will fully integrate DCP’s assets into its midstream operations while the partnership maintains S&P Global Ratings-adjusted leverage of less than 4x over the intermediate term â—¼ The partnership is 70% fee-based allowing it to capitalize on the above-average commodity price, however this level of direct commodity price exposure makes the partnership more susceptible to cash flow volatility What could prompt an UPGRADE: ï,„ Would only raise rating on DCP if they raise rating on Phillips 66ï,„ Could raise PSX rating if non-refining segments account for much larger share of future consolidated EBITDA, which would mitigate cash flow volatility of its refining assets What could prompt a DOWNGRADE: ï,„ If Phillips 66’s adjusted debt to EBITDA consistently exceeds 3.0x Moody’s Credit Opinion: August 19, 2022 â—¼ Expects credit metrics will continue to improve and be supportive of an investment grade rating as free cash flow continues to be applied towards debt reduction â—¼ Credit challenges include exposure to regulatory risk for DJ Basin operations in the state of Colorado and uncertainty regarding longer term demand for hydrocarbons What could prompt an UPGRADE: ï,„ EBITDA continues to grow ï,„ Debt to EBITDA is maintained below 4.0x on a sustained basisï,„ Distribution coverage remains above 1.3x What could prompt a DOWNGRADE: ï,„ Debt to EBITDA exceeds 4.5x ï,„ Distribution coverage falls below 1.0x Source: Standard & Poor’s Rating Services and Moody’s

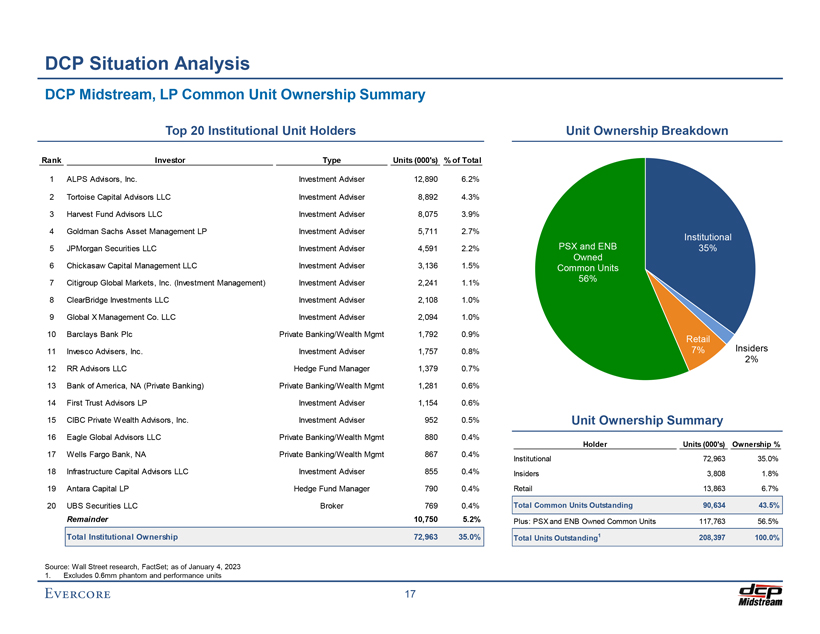

DCP Situation Analysis DCP Midstream, LP Common Unit Ownership Summary Top 20 Institutional Unit Holders Rank Investor Type Units (000’s) % of Total 1 ALPS Advisors, Inc. Investment Adviser 12,890 6.2% 2 Tortoise Capital Advisors LLC Investment Adviser 8,892 4.3% 3 Harvest Fund Advisors LLC Investment Adviser 8,075 3.9% 4 Goldman Sachs Asset Management LP Investment Adviser 5,711 2.7% 5 JPMorgan Securities LLC Investment Adviser 4,591 2.2% 6 Chickasaw Capital Management LLC Investment Adviser 3,136 1.5% 7 Citigroup Global Markets, Inc. (Investment Management) Investment Adviser 2,241 1.1% 8 ClearBridge Investments LLC Investment Adviser 2,108 1.0% 9 Global X Management Co. LLC Investment Adviser 2,094 1.0% 10 Barclays Bank Plc Private Banking/Wealth Mgmt 1,792 0.9% 11 Invesco Advisers, Inc. Investment Adviser 1,757 0.8% 12 RR Advisors LLC Hedge Fund Manager 1,379 0.7% 13 Bank of America, NA (Private Banking) Private Banking/Wealth Mgmt 1,281 0.6% 14 First Trust Advisors LP Investment Adviser 1,154 0.6% 15 CIBC Private Wealth Advisors, Inc. Investment Adviser 952 0.5% 16 Eagle Global Advisors LLC Private Banking/Wealth Mgmt 880 0.4% 17 Wells Fargo Bank, NA Private Banking/Wealth Mgmt 867 0.4% 18 Infrastructure Capital Advisors LLC Investment Adviser 855 0.4% 19 Antara Capital LP Hedge Fund Manager 790 0.4% 20 UBS Securities LLC Broker 769 0.4% Remainder 10,750 5.2% Total Institutional Ownership 72,963 35.0% Unit Ownership Breakdown [Graphic Appears Here] Unit Ownership Summary Holder Units (000’s) Ownership % Institutional 72,963 35.0% Insiders 3,808 1.8% Retail 13,863 6.7% Total Common Units Outstanding 90,634 43.5% Plus: PSX and ENB Owned Common Units 117,763 56.5% Total Units Outstanding1 208,397 100.0% Source: Wall Street research, FactSet; as of January 4, 2023 1. Excludes 0.6mm phantom and performance units

III. DCP Financial Projections

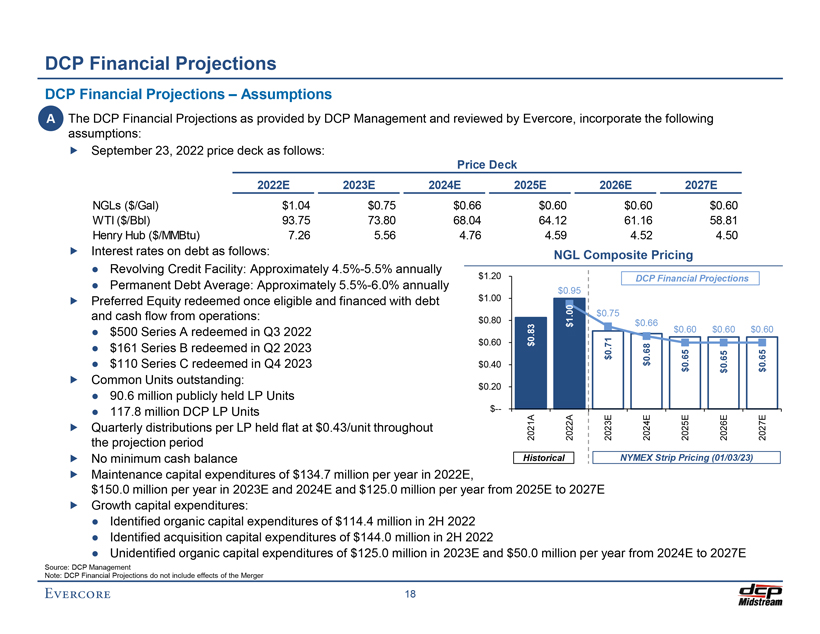

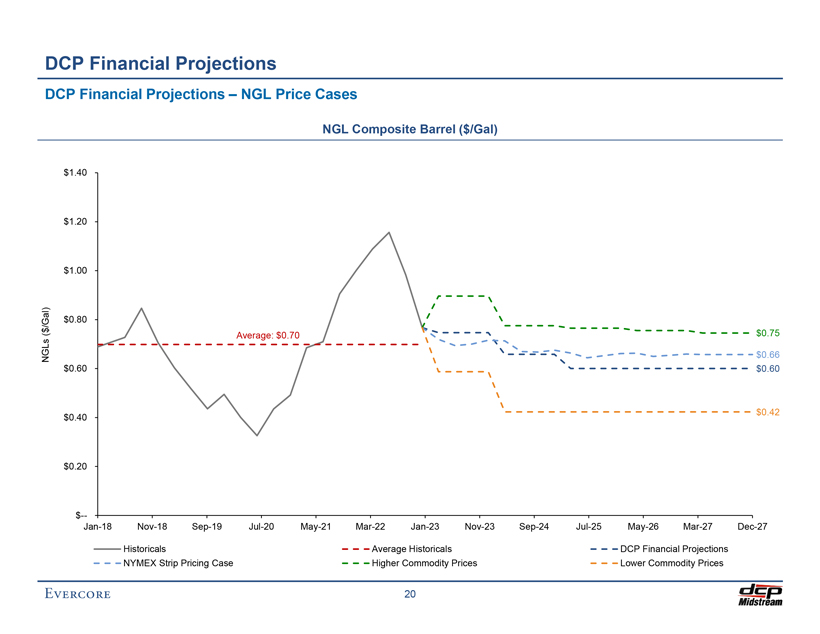

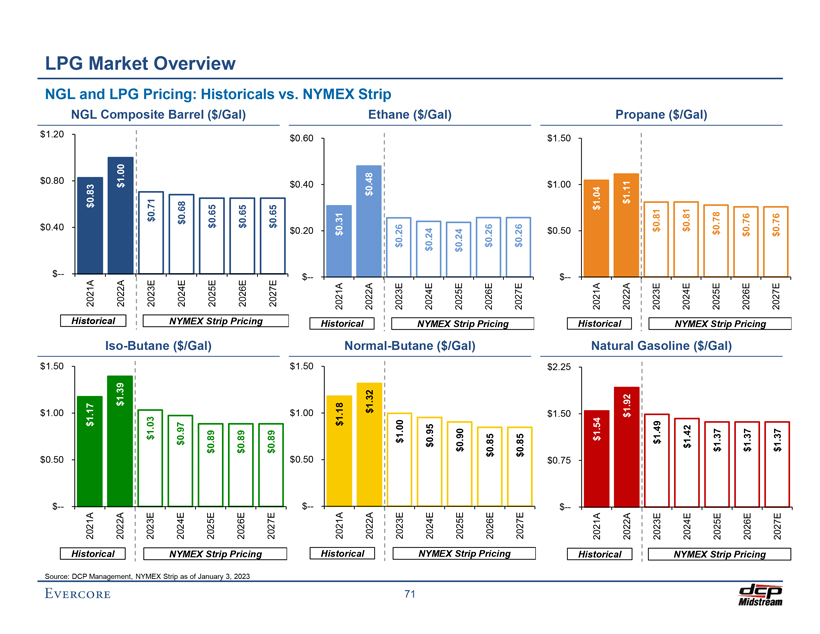

DCP Financial Projections DCP Financial Projections – Assumptions â—¼ A The DCP Financial Projections as provided by DCP Management and reviewed by Evercore, incorporate the following assumptions:ï,„ September 23, 2022 price deck as follows: Price Deck 2022E 2023E 2024E 2025E 2026E 2027E NGLs ($/Gal) $1.04 $0.75 $0.66 $0.60 $0.60 $0.60 WTI ($/Bbl) 93.75 73.80 68.04 64.12 61.16 58.81 Henry Hub ($/MMBtu) 7.26 5.56 4.76 4.59 4.52 4.50 ï,„ Interest rates on debt as follows: • Revolving Credit Facility: Approximately 4.5%-5.5% annually • Permanent Debt Average: Approximately 5.5%-6.0% annuallyï,„ Preferred Equity redeemed once eligible and financed with debt and cash flow from operations: • $500 Series A redeemed in Q3 2022 • $161 Series B redeemed in Q2 2023 • $110 Series C redeemed in Q4 2023ï,„ Common Units outstanding: • 90.6 million publicly held LP Units • 117.8 million DCP LP Units ï,„ Quarterly distributions per LP held flat at $0.43/unit throughout the projection periodï,„ No minimum cash balance ï,„ Maintenance capital expenditures of $134.7 million per year in 2022E, $150.0 million per year in 2023E and 2024E and $125.0 million per year from 2025E to 2027Eï,„ Growth capital expenditures: • Identified organic capital expenditures of $114.4 million in 2H 2022 • Identified acquisition capital expenditures of $144.0 million in 2H 2022 • Unidentified organic capital expenditures of $125.0 million in 2023E and $50.0 million per year from 2024E to 2027E NGL Composite Pricing .20 DCP Financial Projections .00 $0.95 0 . 0 $0.75 .80 1 3 $ $0.66 8 $0.60 $0.60 $0.60 0 . .60 $ 71 8 . 0 . 6 5 5 5 $ 0 . 6 6 .. 6 $ . .40 $ 0 0 $ 0 $ .20 $— A 2021 2022A E 2023 E 2024 2025E E 2026 2027 E Historical NYMEX Strip Pricing (01/03/23) [Graphic Appears Here] Source: DCP Management Note: DCP Financial Projections do not include effects of the Merger

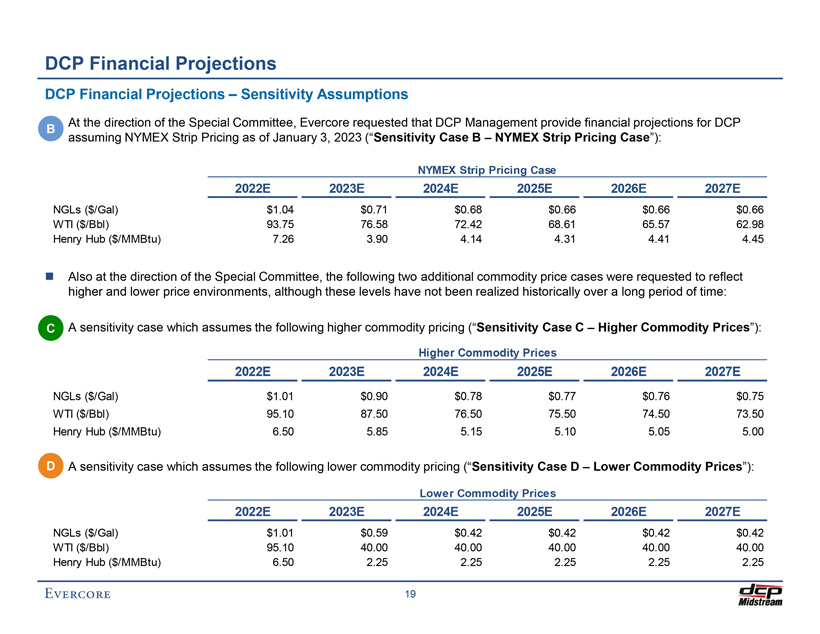

DCP Financial Projections DCP Financial Projections – Sensitivity Assumptions â—¼ At the direction of the Special Committee, Evercore requested that DCP Management provide financial projections for DCP B assuming NYMEX Strip Pricing as of January 3, 2023 (“Sensitivity Case B – NYMEX Strip Pricing Case”): NYMEX Strip Pricing Case 2022E 2023E 2024E 2025E 2026E 2027E NGLs ($/Gal) $1.04 $0.71 $0.68 $0.66 $0.66 $0.66 WTI ($/Bbl) 93.75 76.58 72.42 68.61 65.57 62.98 Henry Hub ($/MMBtu) 7.26 3.90 4.14 4.31 4.41 4.45 â—¼ Also at the direction of the Special Committee, the following two additional commodity price cases were requested to reflect higher and lower price environments, although these levels have not been realized historically over a long period of time: â—¼ C A sensitivity case which assumes the following higher commodity pricing (“Sensitivity Case C – Higher Commodity Prices”): Higher Commodity Prices 2022E 2023E 2024E 2025E 2026E 2027E NGLs ($/Gal) $1.01 $0.90 $0.78 $0.77 $0.76 $0.75 WTI ($/Bbl) 95.10 87.50 76.50 75.50 74.50 73.50 Henry Hub ($/MMBtu) 6.50 5.85 5.15 5.10 5.05 5.00 â—¼ D A sensitivity case which assumes the following lower commodity pricing (“Sensitivity Case D – Lower Commodity Prices”): Lower Commodity Prices 2022E 2023E 2024E 2025E 2026E 2027E NGLs ($/Gal) $1.01 $0.59 $0.42 $0.42 $0.42 $0.42 WTI ($/Bbl) 95.10 40.00 40.00 40.00 40.00 40.00 Henry Hub ($/MMBtu) 6.50 2.25 2.25 2.25 2.25 2.25

DCP Financial Projections DCP Financial Projections – NGL Price Cases NGL Composite Barrel ($/Gal) Historicals Average Historicals DCP Financial Projections NYMEX Strip Pricing Case Higher Commodity Prices Lower Commodity Prices

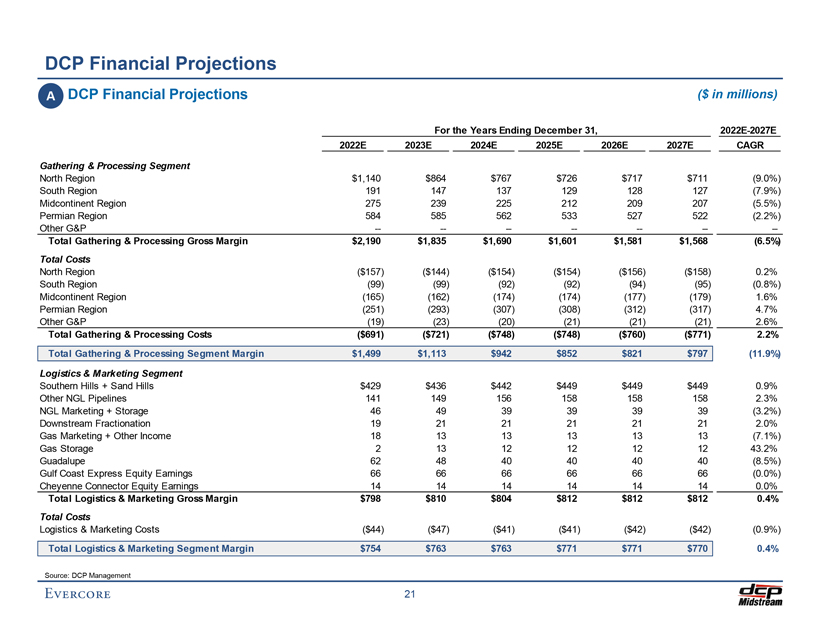

DCP Financial Projections A DCP Financial Projections ($ in millions) For the Years Ending December 31, 2022E-2027E 2022E 2023E 2024E 2025E 2026E 2027E CAGR Gathering & Processing Segment North Region $1,140 $864 $767 $726 $717 $711 (9.0%) South Region 191 147 137 129 128 127 (7.9%) Midcontinent Region 275 239 225 212 209 207 (5.5%) Permian Region 584 585 562 533 527 522 (2.2%) Other G&P -——————- Total Gathering & Processing Gross Margin $2,190 $1,835 $1,690 $1,601 $1,581 $1,568 (6.5%) Total Costs North Region ($157) ($144) ($154) ($154) ($156) ($158) 0.2% South Region (99) (99) (92) (92) (94) (95) (0.8%) Midcontinent Region (165) (162) (174) (174) (177) (179) 1.6% Permian Region (251) (293) (307) (308) (312) (317) 4.7% Other G&P (19) (23) (20) (21) (21) (21) 2.6% Total Gathering & Processing Costs ($691) ($721) ($748) ($748) ($760) ($771) 2.2% Total Gathering & Processing Segment Margin $1,499 $1,113 $942 $852 $821 $797 (11.9%) Logistics & Marketing Segment Southern Hills + Sand Hills $429 $436 $442 $449 $449 $449 0.9% Other NGL Pipelines 141 149 156 158 158 158 2.3% NGL Marketing + Storage 46 49 39 39 39 39 (3.2%) Downstream Fractionation 19 21 21 21 21 21 2.0% Gas Marketing + Other Income 18 13 13 13 13 13 (7.1%) Gas Storage 2 13 12 12 12 12 43.2% Guadalupe 62 48 40 40 40 40 (8.5%) Gulf Coast Express Equity Earnings 66 66 66 66 66 66 (0.0%) Cheyenne Connector Equity Earnings 14 14 14 14 14 14 0.0% Total Logistics & Marketing Gross Margin $798 $810 $804 $812 $812 $812 0.4% Total Costs Logistics & Marketing Costs ($44) ($47) ($41) ($41) ($42) ($42) (0.9%) Total Logistics & Marketing Segment Margin $754 $763 $763 $771 $771 $770 0.4% Source: DCP Management

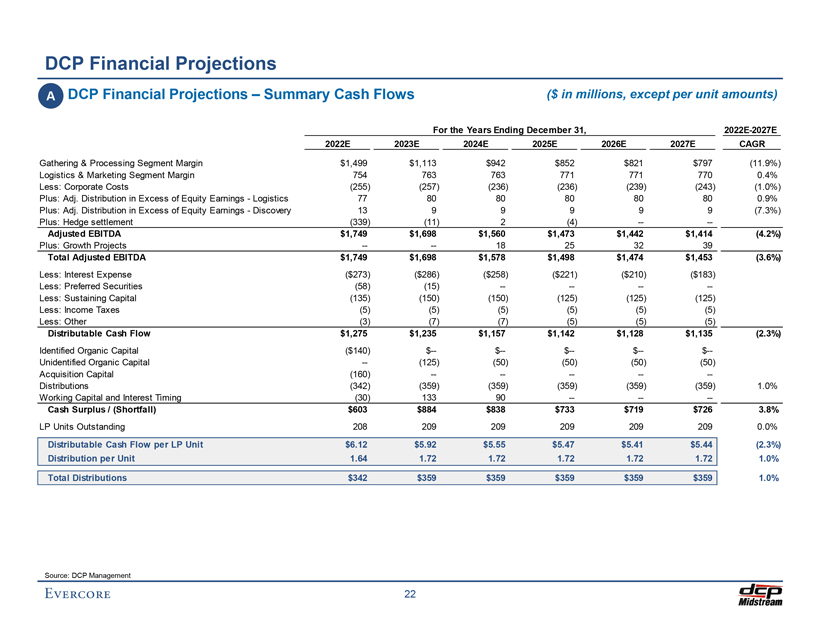

DCP Financial Projections A DCP Financial Projections – Summary Cash Flows ($ in millions, except per unit amounts) For the Years Ending December 31, 2022E-2027E 2022E 2023E 2024E 2025E 2026E 2027E CAGR Gathering & Processing Segment Margin $1,499 $1,113 $942 $852 $821 $797 (11.9%) Logistics & Marketing Segment Margin 754 763 763 771 771 770 0.4% Less: Corporate Costs (255) (257) (236) (236) (239) (243) (1.0%) Plus: Adj. Distribution in Excess of Equity Earnings—Logistics 77 80 80 80 80 80 0.9% Plus: Adj. Distribution in Excess of Equity Earnings—Discovery 13 9 9 9 9 9 (7.3%) Plus: Hedge settlement (339) (11) 2 (4) -—- Adjusted EBITDA $1,749 $1,698 $1,560 $1,473 $1,442 $1,414 (4.2%) Plus: Growth Projects -—- 18 25 32 39 Total Adjusted EBITDA $1,749 $1,698 $1,578 $1,498 $1,474 $1,453 (3.6%) Less: Interest Expense ($273) ($286) ($258) ($221) ($210) ($183) Less: Preferred Securities (58) (15) -———-Less: Sustaining Capital (135) (150) (150) (125) (125) (125) Less: Income Taxes (5) (5) (5) (5) (5) (5) Less: Other (3) (7) (7) (5) (5) (5) Distributable Cash Flow $1,275 $1,235 $1,157 $1,142 $1,128 $1,135 (2.3%) Identified Organic Capital ($140) $— $— $— $— $—Unidentified Organic Capital — (125) (50) (50) (50) (50) Acquisition Capital (160) -————- Distributions (342) (359) (359) (359) (359) (359) 1.0% Working Capital and Interest Timing (30) 133 90 -——- Cash Surplus / (Shortfall) $603 $884 $838 $733 $719 $726 3.8% LP Units Outstanding 208 209 209 209 209 209 0.0% Distributable Cash Flow per LP Unit $6.12 $5.92 $5.55 $5.47 $5.41 $5.44 (2.3%) Distribution per Unit 1.64 1.72 1.72 1.72 1.72 1.72 1.0% Total Distributions $342 $359 $359 $359 $359 $359 1.0% Source: DCP Management

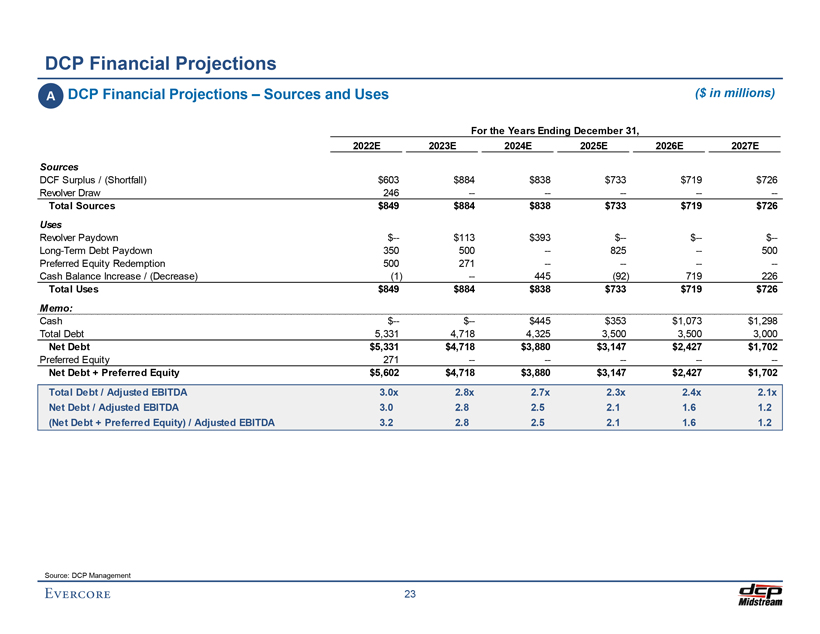

DCP Financial Projections A DCP Financial Projections – Sources and Uses ($ in millions) For the Years Ending December 31, 2022E 2023E 2024E 2025E 2026E 2027E Sources DCF Surplus / (Shortfall) $603 $884 $838 $733 $719 $726 Revolver Draw 246 -————- Total Sources $849 $884 $838 $733 $719 $726 Uses Revolver Paydown $— $113 $393 $— $— $— Long-Term Debt Paydown 350 500 — 825 — 500 Preferred Equity Redemption 500 271 -———-Cash Balance Increase / (Decrease) (1) — 445 (92) 719 226 Total Uses $849 $884 $838 $733 $719 $726 Memo: Cash $— $— $445 $353 $1,073 $1,298 Total Debt 5,331 4,718 4,325 3,500 3,500 3,000 Net Debt $5,331 $4,718 $3,880 $3,147 $2,427 $1,702 Preferred Equity 271 -————- Net Debt + Preferred Equity $5,602 $4,718 $3,880 $3,147 $2,427 $1,702 Total Debt / Adjusted EBITDA 3.0x 2.8x 2.7x 2.3x 2.4x 2.1x Net Debt / Adjusted EBITDA 3.0 2.8 2.5 2.1 1.6 1.2 (Net Debt + Preferred Equity) / Adjusted EBITDA 3.2 2.8 2.5 2.1 1.6 1.2 Source: DCP Management

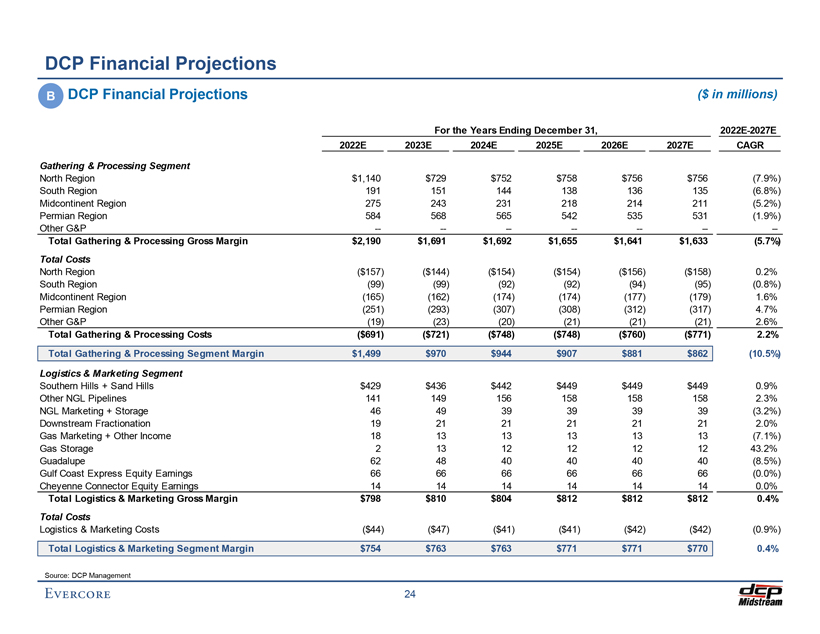

DCP Financial Projections B DCP Financial Projections ($ in millions) For the Years Ending December 31, 2022E-2027E 2022E 2023E 2024E 2025E 2026E 2027E CAGR Gathering & Processing Segment North Region $1,140 $729 $752 $758 $756 $756 (7.9%) South Region 191 151 144 138 136 135 (6.8%) Midcontinent Region 275 243 231 218 214 211 (5.2%) Permian Region 584 568 565 542 535 531 (1.9%) Other G&P -——————- Total Gathering & Processing Gross Margin $2,190 $1,691 $1,692 $1,655 $1,641 $1,633 (5.7%) Total Costs North Region ($157) ($144) ($154) ($154) ($156) ($158) 0.2% South Region (99) (99) (92) (92) (94) (95) (0.8%) Midcontinent Region (165) (162) (174) (174) (177) (179) 1.6% Permian Region (251) (293) (307) (308) (312) (317) 4.7% Other G&P (19) (23) (20) (21) (21) (21) 2.6% Total Gathering & Processing Costs ($691) ($721) ($748) ($748) ($760) ($771) 2.2% Total Gathering & Processing Segment Margin $1,499 $970 $944 $907 $881 $862 (10.5%) Logistics & Marketing Segment Southern Hills + Sand Hills $429 $436 $442 $449 $449 $449 0.9% Other NGL Pipelines 141 149 156 158 158 158 2.3% NGL Marketing + Storage 46 49 39 39 39 39 (3.2%) Downstream Fractionation 19 21 21 21 21 21 2.0% Gas Marketing + Other Income 18 13 13 13 13 13 (7.1%) Gas Storage 2 13 12 12 12 12 43.2% Guadalupe 62 48 40 40 40 40 (8.5%) Gulf Coast Express Equity Earnings 66 66 66 66 66 66 (0.0%) Cheyenne Connector Equity Earnings 14 14 14 14 14 14 0.0% Total Logistics & Marketing Gross Margin $798 $810 $804 $812 $812 $812 0.4% Total Costs Logistics & Marketing Costs ($44) ($47) ($41) ($41) ($42) ($42) (0.9%) Total Logistics & Marketing Segment Margin $754 $763 $763 $771 $771 $770 0.4% Source: DCP Management

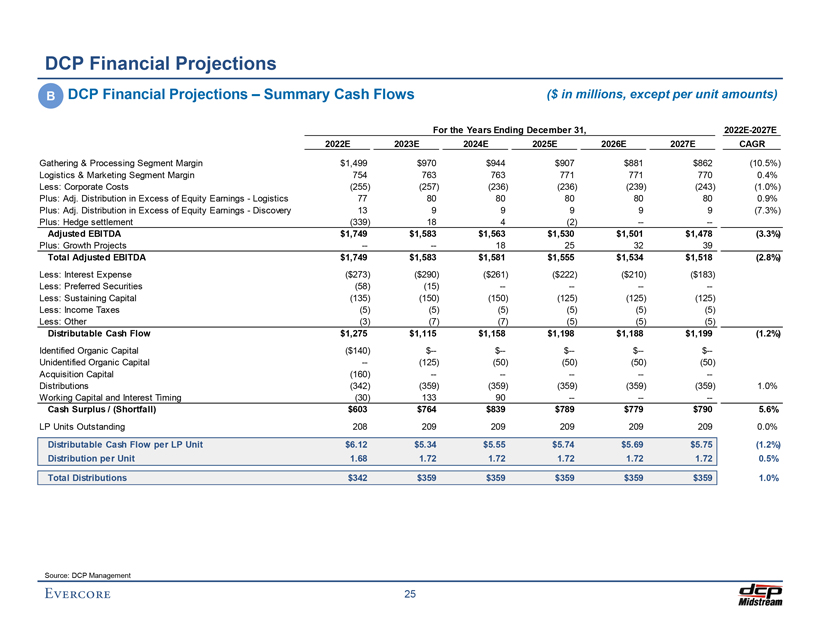

DCP Financial Projections B DCP Financial Projections – Summary Cash Flows ($ in millions, except per unit amounts) For the Years Ending December 31, 2022E-2027E 2022E 2023E 2024E 2025E 2026E 2027E CAGR Gathering & Processing Segment Margin $1,499 $970 $944 $907 $881 $862 (10.5%) Logistics & Marketing Segment Margin 754 763 763 771 771 770 0.4% Less: Corporate Costs (255) (257) (236) (236) (239) (243) (1.0%) Plus: Adj. Distribution in Excess of Equity Earnings—Logistics 77 80 80 80 80 80 0.9% Plus: Adj. Distribution in Excess of Equity Earnings—Discovery 13 9 9 9 9 9 (7.3%) Plus: Hedge settlement (339) 18 4 (2) -—- Adjusted EBITDA $1,749 $1,583 $1,563 $1,530 $1,501 $1,478 (3.3%) Plus: Growth Projects -—- 18 25 32 39 Total Adjusted EBITDA $1,749 $1,583 $1,581 $1,555 $1,534 $1,518 (2.8%) Less: Interest Expense ($273) ($290) ($261) ($222) ($210) ($183) Less: Preferred Securities (58) (15) -———-Less: Sustaining Capital (135) (150) (150) (125) (125) (125) Less: Income Taxes (5) (5) (5) (5) (5) (5) Less: Other (3) (7) (7) (5) (5) (5) Distributable Cash Flow $1,275 $1,115 $1,158 $1,198 $1,188 $1,199 (1.2%) Identified Organic Capital ($140) $— $— $— $— $—Unidentified Organic Capital — (125) (50) (50) (50) (50) Acquisition Capital (160) -————- Distributions (342) (359) (359) (359) (359) (359) 1.0% Working Capital and Interest Timing (30) 133 90 -——- Cash Surplus / (Shortfall) $603 $764 $839 $789 $779 $790 5.6% LP Units Outstanding 208 209 209 209 209 209 0.0% Distributable Cash Flow per LP Unit $6.12 $5.34 $5.55 $5.74 $5.69 $5.75 (1.2%) Distribution per Unit 1.68 1.72 1.72 1.72 1.72 1.72 0.5% Total Distributions $342 $359 $359 $359 $359 $359 1.0% Source: DCP Management

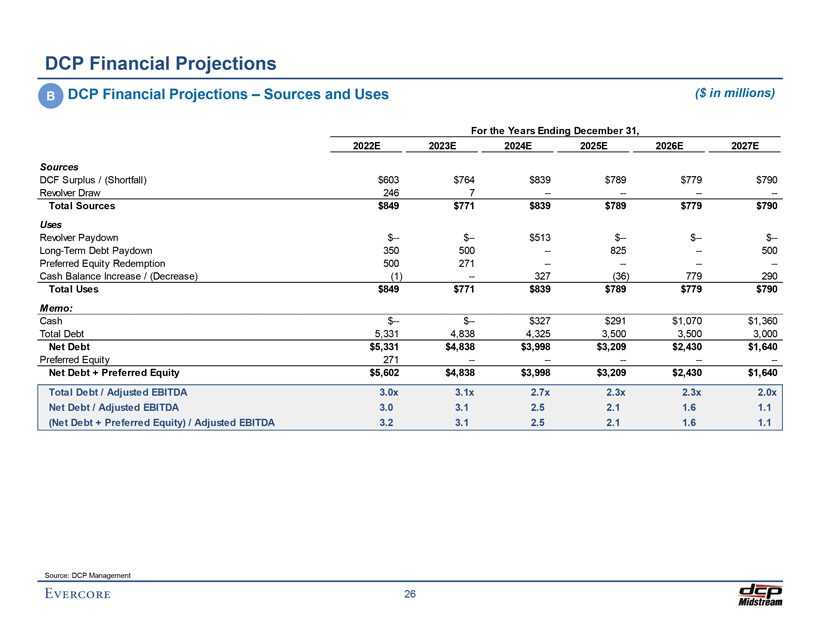

DCP Financial Projections B DCP Financial Projections – Sources and Uses ($ in millions) For the Years Ending December 31, 2022E 2023E 2024E 2025E 2026E 2027E Sources DCF Surplus / (Shortfall) $603 $764 $839 $789 $779 $790 Revolver Draw 246 7 -———- Total Sources $849 $771 $839 $789 $779 $790 Uses Revolver Paydown $— $— $513 $— $— $— Long-Term Debt Paydown 350 500 — 825 — 500 Preferred Equity Redemption 500 271 -———-Cash Balance Increase / (Decrease) (1) — 327 (36) 779 290 Total Uses $849 $771 $839 $789 $779 $790 Memo: Cash $— $— $327 $291 $1,070 $1,360 Total Debt 5,331 4,838 4,325 3,500 3,500 3,000 Net Debt $5,331 $4,838 $3,998 $3,209 $2,430 $1,640 Preferred Equity 271 -————- Net Debt + Preferred Equity $5,602 $4,838 $3,998 $3,209 $2,430 $1,640 Total Debt / Adjusted EBITDA 3.0x 3.1x 2.7x 2.3x 2.3x 2.0x Net Debt / Adjusted EBITDA 3.0 3.1 2.5 2.1 1.6 1.1 (Net Debt + Preferred Equity) / Adjusted EBITDA 3.2 3.1 2.5 2.1 1.6 1.1 Source: DCP Management

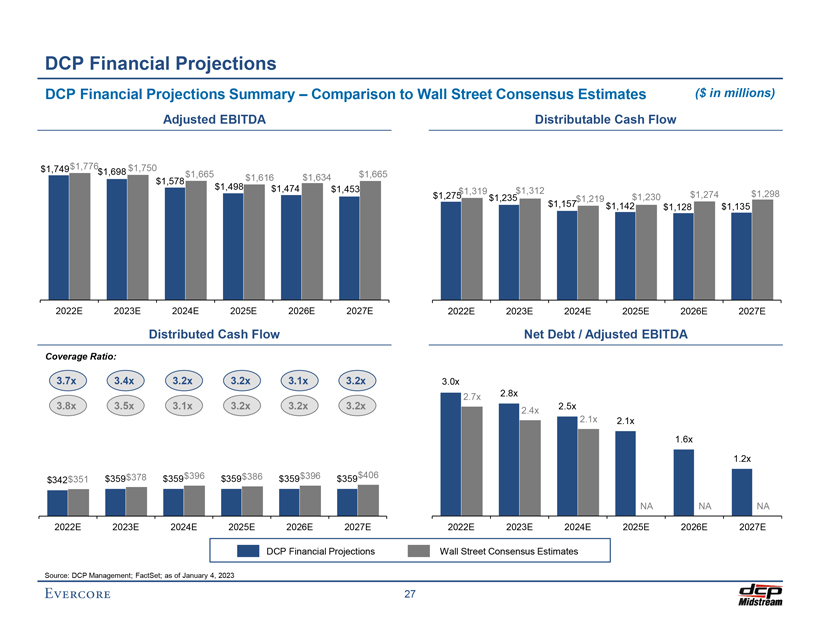

DCP Financial Projections DCP Financial Projections Summary – Comparison to Wall Street Consensus Estimates ($ in millions) Adjusted EBITDA [Graphic Appears Here] Distributed Cash Flow Coverage Ratio: [Graphic Appears Here] [Graphic Appears Here] Distributable Cash Flow [Graphic Appears Here] Net Debt / Adjusted EBITDA [Graphic Appears Here] DCP Financial Projections Wall Street Consensus Estimates Source: DCP Management; FactSet; as of January 4, 2023

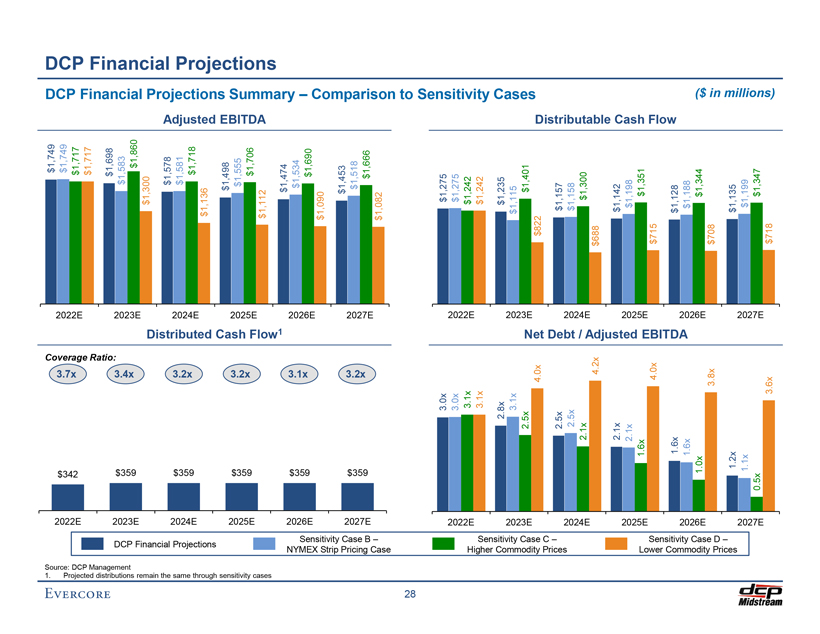

DCP Financial Projections DCP Financial Projections Summary – Comparison to Sensitivity Cases ($ in millions) Adjusted EBITDA [Graphic Appears Here] Distributed Cash Flow1 Coverage Ratio: [Graphic Appears Here] [Graphic Appears Here] Distributable Cash Flow [Graphic Appears Here] Net Debt / Adjusted EBITDA [Graphic Appears Here] Sensitivity Case B – Sensitivity Case C – Sensitivity Case D –DCP Financial Projections NYMEX Strip Pricing Case Higher Commodity Prices Lower Commodity Prices Source: DCP Management 1. Projected distributions remain the same through sensitivity cases

DCP Financial Projections DCP Financial Projections Summary – Comparison to Sensitivity Cases ($ in millions) Adjusted EBITDA [Graphic Appears Here] Distributed Cash Flow1 Coverage Ratio: [Graphic Appears Here] [Graphic Appears Here] Distributable Cash Flow [Graphic Appears Here] Net Debt / Adjusted EBITDA [Graphic Appears Here] Sensitivity Case B – Sensitivity Case C – Sensitivity Case D –DCP Financial Projections NYMEX Strip Pricing Case Higher Commodity Prices Lower Commodity Prices Source: DCP Management 1. Projected distributions remain the same through sensitivity cases IV. Preliminary Valuation of the Common Units

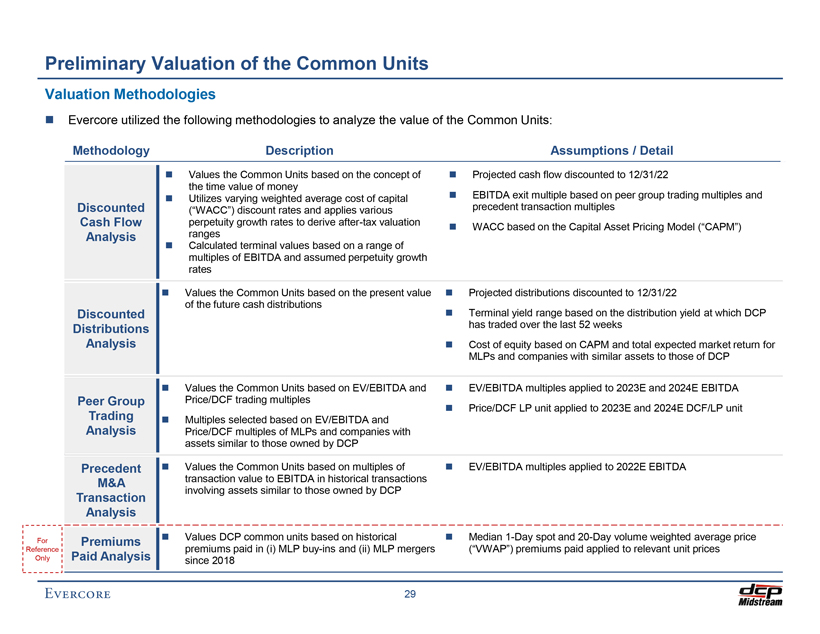

Preliminary Valuation of the Common Units Valuation Methodologies â—¼ Evercore utilized the following methodologies to analyze the value of the Common Units: Methodology Description Assumptions / Detail â—¼ Values the Common Units based on the concept of â—¼ Projected cash flow discounted to 12/31/22 the time value of money â—¼ Utilizes varying weighted average cost of capital â—¼ EBITDA exit multiple based on peer group trading multiples and Discounted (“WACC”) discount rates and applies various precedent transaction multiples Cash Flow perpetuity growth rates to derive after-tax valuation â—¼ WACC based on the Capital Asset Pricing Model (“CAPM”) Analysis ranges â—¼ Calculated terminal values based on a range of multiples of EBITDA and assumed perpetuity growth rates â—¼ Values the Common Units based on the present value â—¼ Projected distributions discounted to 12/31/22 of the future cash distributions Discounted â—¼ Terminal yield range based on the distribution yield at which DCP Distributions has traded over the last 52 weeks Analysis â—¼ Cost of equity based on CAPM and total expected market return for MLPs and companies with similar assets to those of DCP â—¼ Values the Common Units based on EV/EBITDA and â—¼ EV/EBITDA multiples applied to 2023E and 2024E EBITDA Peer Group Price/DCF trading multiples â—¼ Price/DCF LP unit applied to 2023E and 2024E DCF/LP unit Trading â—¼ Multiples selected based on EV/EBITDA and Analysis Price/DCF multiples of MLPs and companies with assets similar to those owned by DCP Precedent â—¼ Values the Common Units based on multiples of â—¼ EV/EBITDA multiples applied to 2022E EBITDA M&A transaction value to EBITDA in historical transactions involving assets similar to those owned by DCP Transaction Analysis For Premiums â—¼ Values DCP common units based on historical â—¼ Median 1-Day spot and 20-Day volume weighted average price Reference premiums paid in (i) MLP buy-ins and (ii) MLP mergers (“VWAP”) premiums paid applied to relevant unit prices Only Paid Analysis since 2018

Preliminary Valuation of the Common Units Preliminary Valuation Summary For Reference Only Discounted Peer Group Discounted Cash Flow Analysis Distributions Trading Analysis MLP Analyst Analysis Precedent M&A Premiums Price Transaction Analysis Paid Targets Market Price/DCF Exit Multiple Perpetuity Grow th CAPM EV/EBITDA Return per LP Unit $65.00 $61.07 Implied range based on 5% $55.00 annual $53.18 $52.70 $52.17 distribution growth $50.33 $50.20 $50.20 $49.58 $48.61 $48.61 through $45.40 2027E1 $45.91 $44.37 $45.00 $45.00 $43.31 $44.05 $44.86 $41.61 $40.99 $40.08 $42.24 $38.33 $37.83 $38.44 $39.96 $38.00 $35.00 $34.93 $37.36 $36.05 $35.15 $32.22 $33.35 $33.44 $33.27 $33.41 $33.27 $33.30 $29.52 $33.56 $33.56 $28.75 $32.28 $32.28 $27.68 $28.20 $29.71 $24.22 $25.00 Merger Consideration: $41.75 $25.10 Price as of 1/4/23: $38.59 $19.79 $18.84 $15.00 $16.31 $15.98 $5.00 4.0%—5.0% 7.0%—8.0% WACC Terminal Yield 8.0x—9.0x 6.5x—7.5x Merger 2023E EBITDA 2023E DCF/LP Unit Premium 9.0%—11.0%—Analyst 7.25x—9.25x Selected 10.0% 13.0% Price 8.0x—9.0x 0.5%—1.5% 2022E EBITDA Range: Equity Equity Targets Exit Multiple Perpetuity Grow th Rate 8.0x—9.0x 6.0x—7.0x 15.0%—Cost of Cost of 2024E EBITDA 2024E DCF/LP Unit 30.0% Capital Capital Sensitivity Case B – Sensitivity Case C – Sensitivity Case D –DCP Financial Projections NYMEX Strip Pricing Case Higher Commodity Prices Lower Commodity Prices 1. For reference only: sensitivity case using a 5% annual distribution growth rate which assumes lower than the commodity super cycle board assumption of 7.5% growth and higher than DCP Financial Projections’ 0% growth

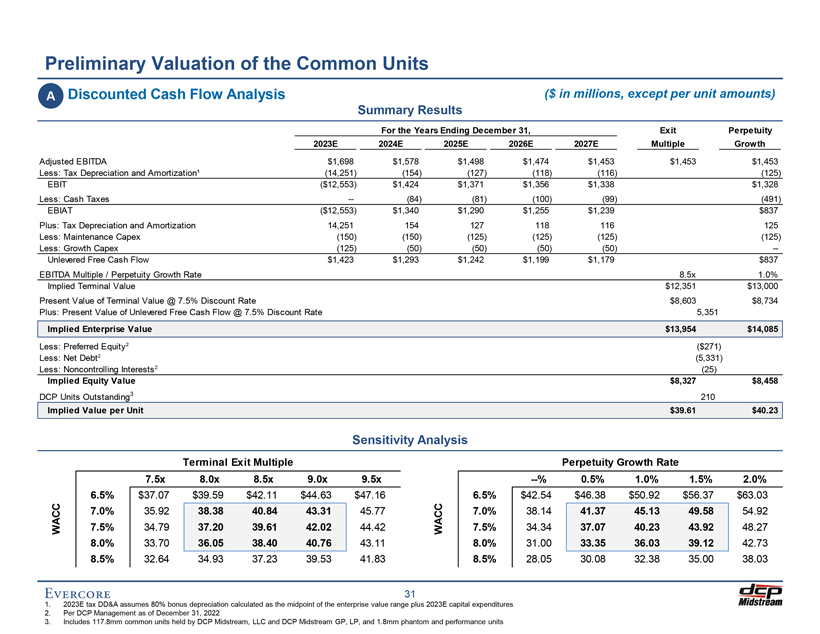

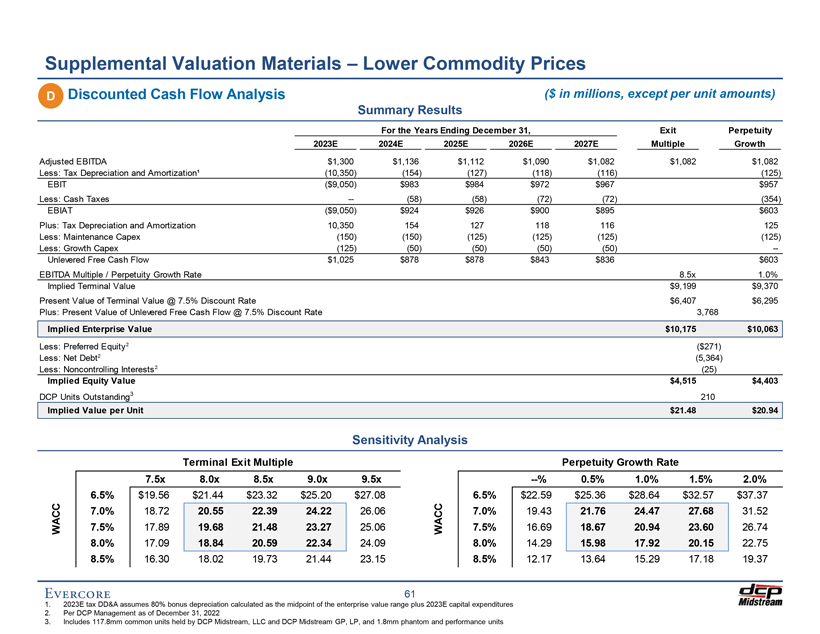

Preliminary Valuation of the Common Units A Discounted Cash Flow Analysis ($ in millions, except per unit amounts) Summary Results For the Years Ending December 31, Exit Perpetuity 2023E 2024E 2025E 2026E 2027E Multiple Growth Adjusted EBITDA $1,698 $1,578 $1,498 $1,474 $1,453 $1,453 $1,453 Less: Tax Depreciation and Amortization¹ (14,251) (154) (127) (118) (116) (125) EBIT ($12,553) $1,424 $1,371 $1,356 $1,338 $1,328 Less: Cash Taxes — (84) (81) (100) (99) (491) EBIAT ($12,553) $1,340 $1,290 $1,255 $1,239 $837 Plus: Tax Depreciation and Amortization 14,251 154 127 118 116 125 Less: Maintenance Capex (150) (150) (125) (125) (125) (125) Less: Growth Capex (125) (50) (50) (50) (50) —Unlevered Free Cash Flow $1,423 $1,293 $1,242 $1,199 $1,179 $837 EBITDA Multiple / Perpetuity Growth Rate 8.5x 1.0% Implied Terminal Value $12,351 $13,000 Present Value of Terminal Value @ 7.5% Discount Rate $8,603 $8,734 Plus: Present Value of Unlevered Free Cash Flow @ 7.5% Discount Rate 5,351 Implied Enterprise Value $13,954 $14,085 Less: Preferred Equity2 ($271) Less: Net Debt2 (5,331) Less: Noncontrolling Interests2 (25) Implied Equity Value $8,327 $8,458 DCP Units Outstanding3 210 Implied Value per Unit $39.61 $40.23 Sensitivity Analysis Terminal Exit Multiple Perpetuity Growth Rate 7.5x 8.0x 8.5x 9.0x 9.5x —% 0.5% 1.0% 1.5% 2.0% 6.5% $37.07 $39.59 $42.11 $44.63 $47.16 6.5% $42.54 $46.38 $50.92 $56.37 $63.03 C C 7.0% 35.92 38.38 40.84 43.31 45.77 C C 7.0% 38.14 41.37 45.13 49.58 54.92 WA 7.5% 34.79 37.20 39.61 42.02 44.42 WA 7.5% 34.34 37.07 40.23 43.92 48.27 8.0% 33.70 36.05 38.40 40.76 43.11 8.0% 31.00 33.35 36.03 39.12 42.73 8.5% 32.64 34.93 37.23 39.53 41.83 8.5% 28.05 30.08 32.38 35.00 38.03 31 1. 2023E tax DD&A assumes 80% bonus depreciation calculated as the midpoint of the enterprise value range plus 2023E capital expenditures 2. Per DCP Management as of December 31, 2022 3. Includes 117.8mm common units held by DCP Midstream, LLC and DCP Midstream GP, LP, and 1.8mm phantom and performance units

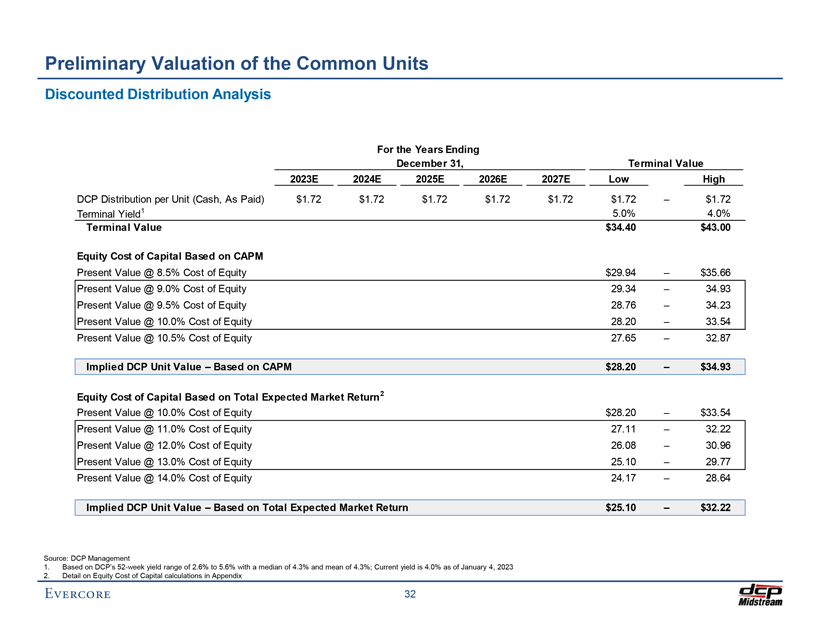

Preliminary Valuation of the Common Units Discounted Distribution Analysis For the Years Ending December 31, Terminal Value 2023E 2024E 2025E 2026E 2027E Low High DCP Distribution per Unit (Cash, As Paid) $1.72 $1.72 $1.72 $1.72 $1.72 $1.72 – $1.72 Terminal Yield1 5.0% 4.0% Terminal Value $34.40 $43.00 Equity Cost of Capital Based on CAPM Present Value @ 8.5% Cost of Equity $29.94 – $35.66 Present Value @ 9.0% Cost of Equity 29.34 – 34.93 Present Value @ 9.5% Cost of Equity 28.76 – 34.23 Present Value @ 10.0% Cost of Equity 28.20 – 33.54 Present Value @ 10.5% Cost of Equity 27.65 – 32.87 Implied DCP Unit Value – Based on CAPM $28.20 – $34.93 Equity Cost of Capital Based on Total Expected Market Return2 Present Value @ 10.0% Cost of Equity $28.20 – $33.54 Present Value @ 11.0% Cost of Equity 27.11 – 32.22 Present Value @ 12.0% Cost of Equity 26.08 – 30.96 Present Value @ 13.0% Cost of Equity 25.10 – 29.77 Present Value @ 14.0% Cost of Equity 24.17 – 28.64 Implied DCP Unit Value – Based on Total Expected Market Return $25.10 – $32.22 Source: DCP Management 1. Based on DCP’s 52-week yield range of 2.6% to 5.6% with a median of 4.3% and mean of 4.3%; Current yield is 4.0% as of January 4, 2023 2. Detail on Equity Cost of Capital calculations in Appendix

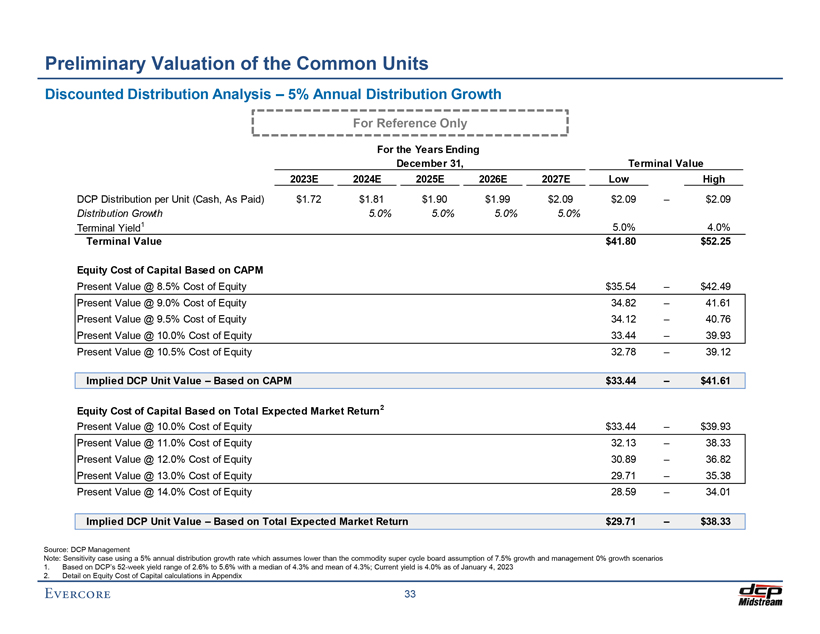

Preliminary Valuation of the Common Units Discounted Distribution Analysis – 5% Annual Distribution Growth For Reference Only For the Years Ending December 31, Terminal Value 2023E 2024E 2025E 2026E 2027E Low High DCP Distribution per Unit (Cash, As Paid) $1.72 $1.81 $1.90 $1.99 $2.09 $2.09 – $2.09 Distribution Growth 5.0% 5.0% 5.0% 5.0% Terminal Yield1 5.0% 4.0% Terminal Value $41.80 $52.25 Equity Cost of Capital Based on CAPM Present Value @ 8.5% Cost of Equity $35.54 – $42.49 Present Value @ 9.0% Cost of Equity 34.82 – 41.61 Present Value @ 9.5% Cost of Equity 34.12 – 40.76 Present Value @ 10.0% Cost of Equity 33.44 – 39.93 Present Value @ 10.5% Cost of Equity 32.78 – 39.12 Implied DCP Unit Value – Based on CAPM $33.44 – $41.61 Equity Cost of Capital Based on Total Expected Market Return2 Present Value @ 10.0% Cost of Equity $33.44 – $39.93 Present Value @ 11.0% Cost of Equity 32.13 – 38.33 Present Value @ 12.0% Cost of Equity 30.89 – 36.82 Present Value @ 13.0% Cost of Equity 29.71 – 35.38 Present Value @ 14.0% Cost of Equity 28.59 – 34.01 Implied DCP Unit Value – Based on Total Expected Market Return $29.71 – $38.33 Source: DCP Management Note: Sensitivity case using a 5% annual distribution growth rate which assumes lower than the commodity super cycle board assumption of 7.5% growth and management 0% growth scenarios 1. Based on DCP’s 52-week yield range of 2.6% to 5.6% with a median of 4.3% and mean of 4.3%; Current yield is 4.0% as of January 4, 2023 2. Detail on Equity Cost of Capital calculations in Appendix

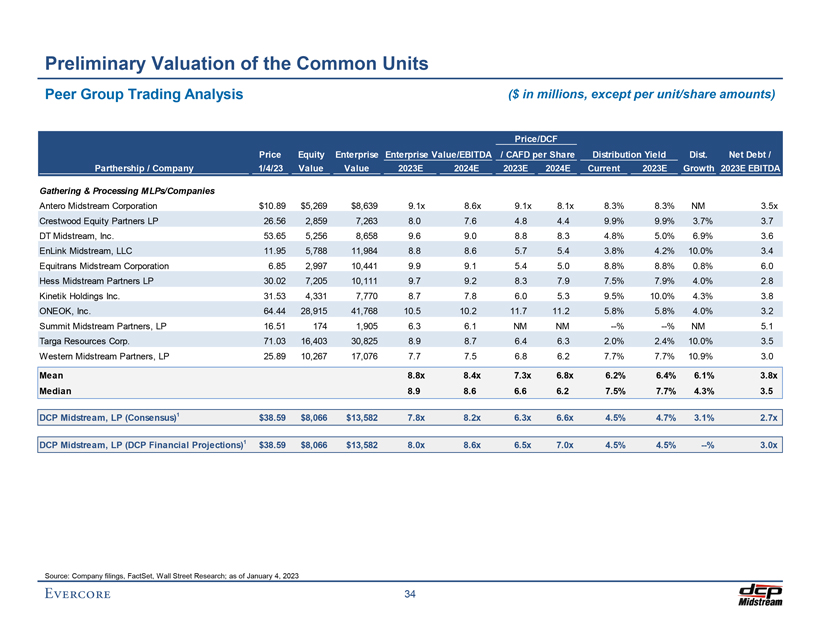

Preliminary Valuation of the Common Units Peer Group Trading Analysis ($ in millions, except per unit/share amounts) Price/DCF Price Equity Enterprise Enterprise Value/EBITDA / CAFD per Share Distribution Yield Dist. Net Debt / Parthership / Company 1/4/23 Value Value 2023E 2024E 2023E 2024E Current 2023E Growth 2023E EBITDA Gathering & Processing MLPs/Companies Antero Midstream Corporation $10.89 $5,269 $8,639 9.1x 8.6x 9.1x 8.1x 8.3% 8.3% NM 3.5x Crestwood Equity Partners LP 26.56 2,859 7,263 8.0 7.6 4.8 4.4 9.9% 9.9% 3.7% 3.7 DT Midstream, Inc. 53.65 5,256 8,658 9.6 9.0 8.8 8.3 4.8% 5.0% 6.9% 3.6 EnLink Midstream, LLC 11.95 5,788 11,984 8.8 8.6 5.7 5.4 3.8% 4.2% 10.0% 3.4 Equitrans Midstream Corporation 6.85 2,997 10,441 9.9 9.1 5.4 5.0 8.8% 8.8% 0.8% 6.0 Hess Midstream Partners LP 30.02 7,205 10,111 9.7 9.2 8.3 7.9 7.5% 7.9% 4.0% 2.8 Kinetik Holdings Inc. 31.53 4,331 7,770 8.7 7.8 6.0 5.3 9.5% 10.0% 4.3% 3.8 ONEOK, Inc. 64.44 28,915 41,768 10.5 10.2 11.7 11.2 5.8% 5.8% 4.0% 3.2 Summit Midstream Partners, LP 16.51 174 1,905 6.3 6.1 NM NM —% —% NM 5.1 Targa Resources Corp. 71.03 16,403 30,825 8.9 8.7 6.4 6.3 2.0% 2.4% 10.0% 3.5 Western Midstream Partners, LP 25.89 10,267 17,076 7.7 7.5 6.8 6.2 7.7% 7.7% 10.9% 3.0 Mean 8.8x 8.4x 7.3x 6.8x 6.2% 6.4% 6.1% 3.8x Median 8.9 8.6 6.6 6.2 7.5% 7.7% 4.3% 3.5 DCP Midstream, LP (Consensus)1 $38.59 $8,066 $13,582 7.8x 8.2x 6.3x 6.6x 4.5% 4.7% 3.1% 2.7x DCP Midstream, LP (DCP Financial Projections)1 $38.59 $8,066 $13,582 8.0x 8.6x 6.5x 7.0x 4.5% 4.5% —% 3.0x Source: Company filings, FactSet, Wall Street Research; as of January 4, 2023

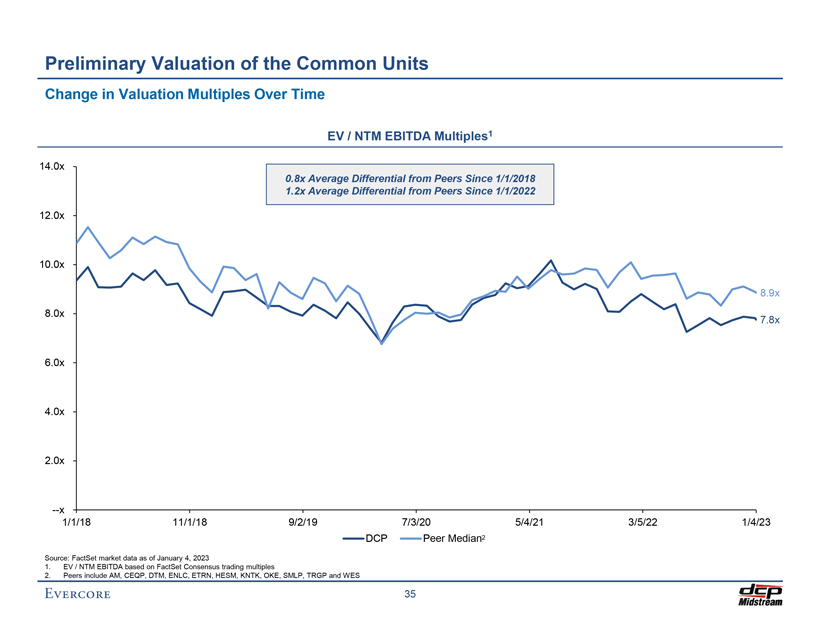

Preliminary Valuation of the Common Units Change in Valuation Multiples Over Time EV / NTM EBITDA Multiples1 14.0x 0.8x Average Differential from Peers Since 1/1/2018 1.2x Average Differential from Peers Since 1/1/2022 12.0x 10.0x 8.9x 8.0x 7.8x 6.0x 4.0x 2.0x --x 1/1/18 11/1/18 9/2/19 7/3/20 5/4/21 3/5/22 1/4/23 DCP Peer Median2 Source: FactSet market data as of January 4, 2023 1. EV / NTM EBITDA based on FactSet Consensus trading multiples 2. Peers include AM, CEQP, DTM, ENLC, ETRN, HESM, KNTK, OKE, SMLP, TRGP and WES

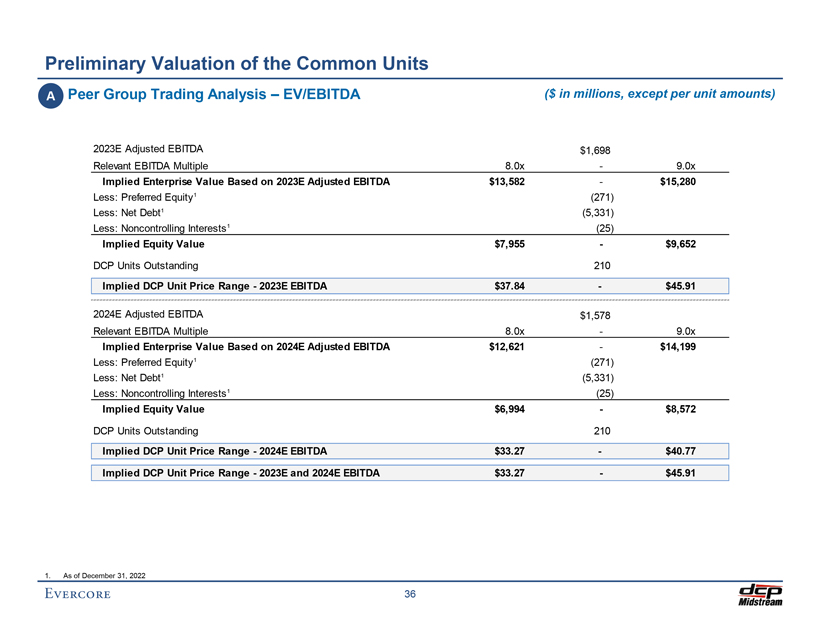

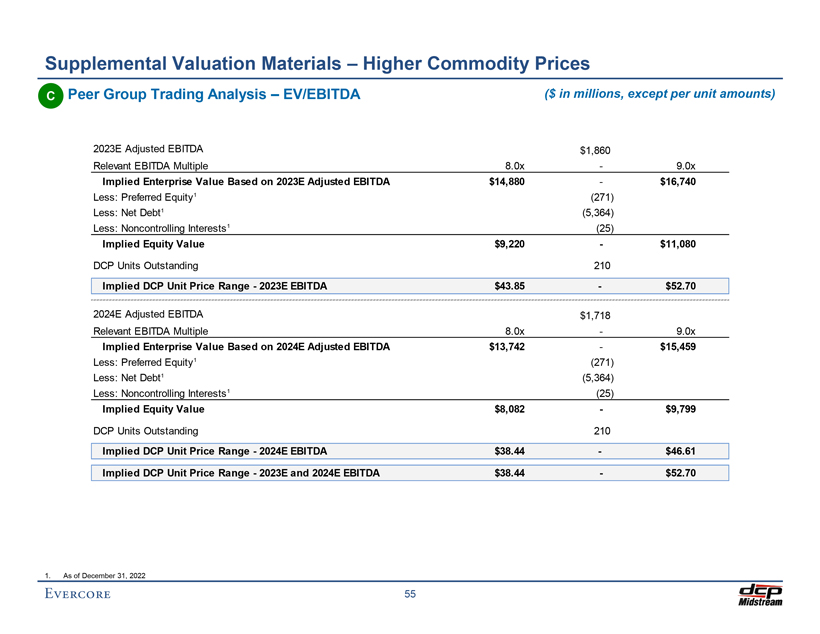

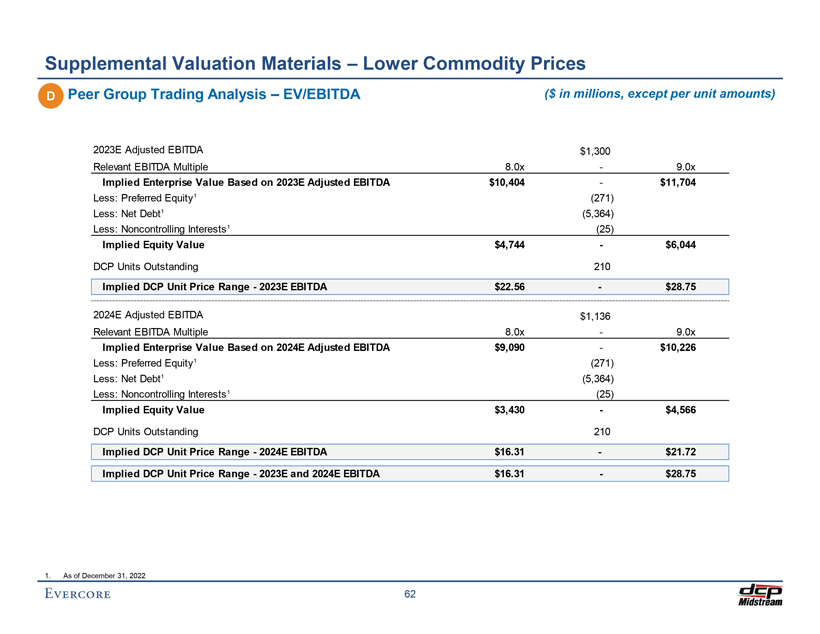

Preliminary Valuation of the Common Units A Peer Group Trading Analysis – EV/EBITDA ($ in millions, except per unit amounts) 2023E Adjusted EBITDA $1,698 Relevant EBITDA Multiple 8.0x—9.0x Implied Enterprise Value Based on 2023E Adjusted EBITDA $13,582—$15,280 Less: Preferred Equity1 (271) Less: Net Debt1 (5,331) Less: Noncontrolling Interests1 (25) Implied Equity Value $7,955—$9,652 DCP Units Outstanding 210 Implied DCP Unit Price Range—2023E EBITDA $37.84—$45.91 2024E Adjusted EBITDA $1,578 Relevant EBITDA Multiple 8.0x—9.0x Implied Enterprise Value Based on 2024E Adjusted EBITDA $12,621—$14,199 Less: Preferred Equity1 (271) Less: Net Debt1 (5,331) Less: Noncontrolling Interests1 (25) Implied Equity Value $6,994—$8,572 DCP Units Outstanding 210 Implied DCP Unit Price Range—2024E EBITDA $33.27—$40.77 Implied DCP Unit Price Range—2023E and 2024E EBITDA $33.27—$45.91 1. As of December 31, 2022

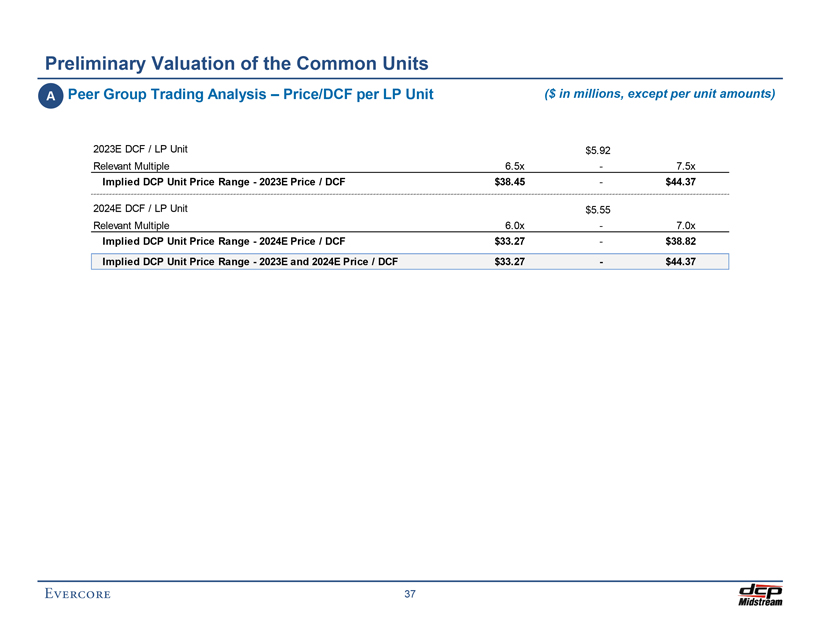

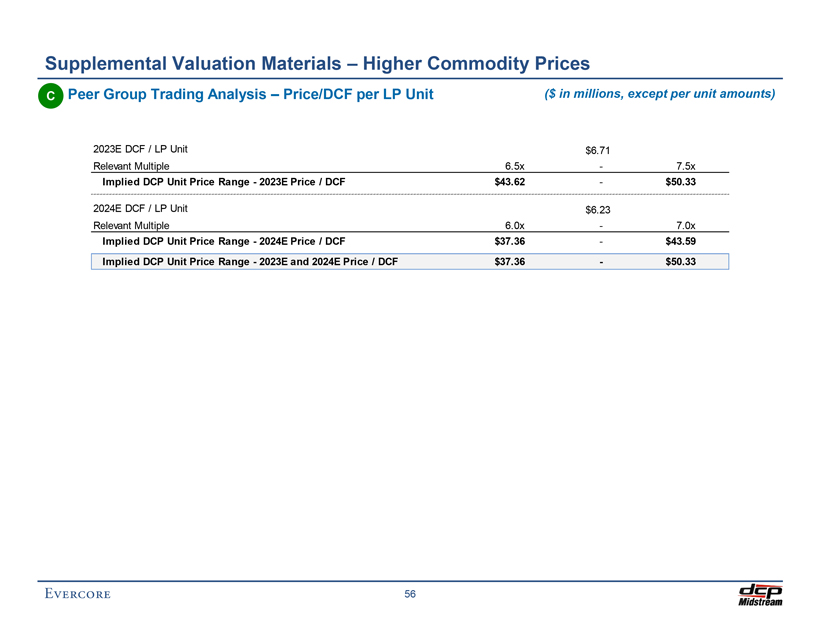

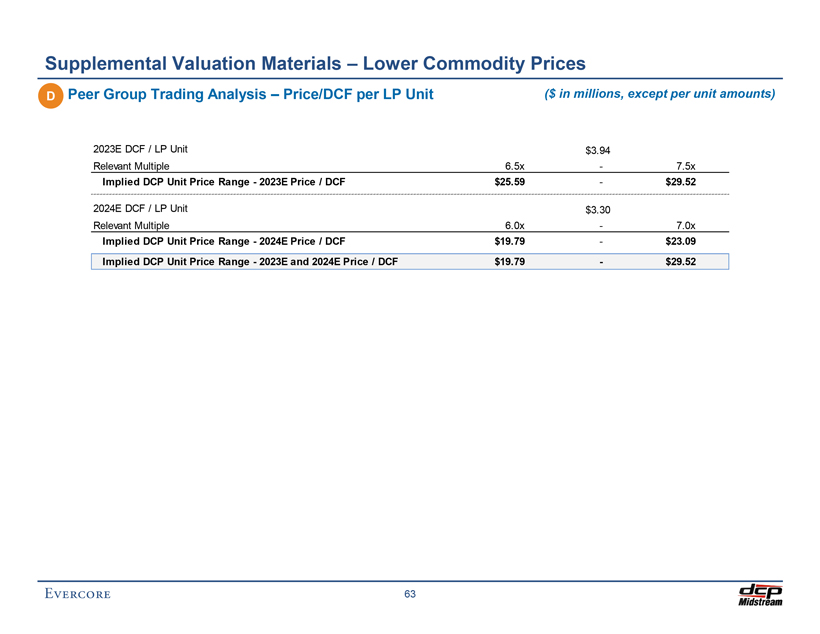

Preliminary Valuation of the Common Units A Peer Group Trading Analysis – Price/DCF per LP Unit ($ in millions, except per unit amounts) 2023E DCF / LP Unit $5.92 Relevant Multiple 6.5x—7.5x Implied DCP Unit Price Range—2023E Price / DCF $38.45—$44.37 2024E DCF / LP Unit $5.55 Relevant Multiple 6.0x—7.0x Implied DCP Unit Price Range—2024E Price / DCF $33.27—$38.82 Implied DCP Unit Price Range—2023E and 2024E Price / DCF $33.27—$44.37

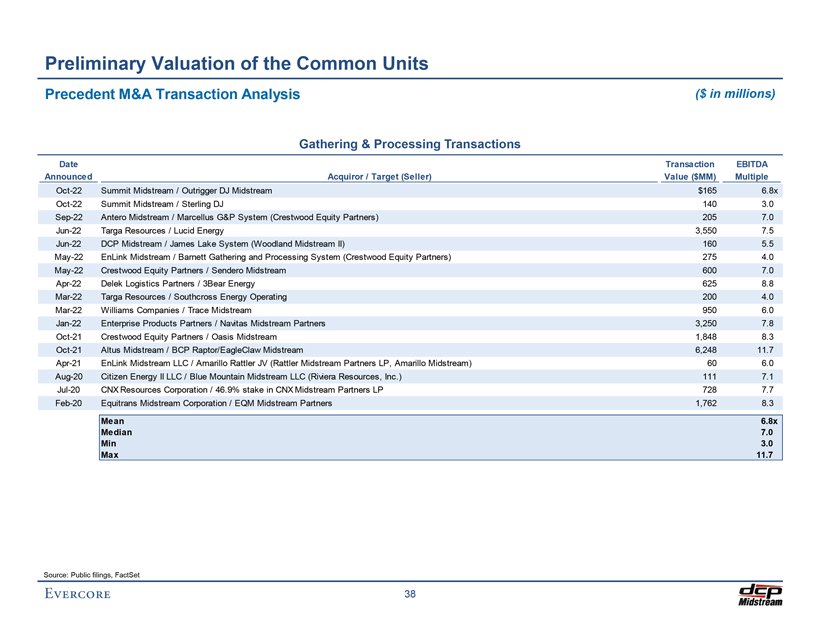

Preliminary Valuation of the Common Units Precedent M&A Transaction Analysis ($ in millions) Gathering & Processing Transactions Date Transaction EBITDA Announced Acquiror / Target (Seller) Value ($MM) Multiple Oct-22 Summit Midstream / Outrigger DJ Midstream $165 6.8x Oct-22 Summit Midstream / Sterling DJ 140 3.0 Sep-22 Antero Midstream / Marcellus G&P System (Crestwood Equity Partners) 205 7.0 Jun-22 Targa Resources / Lucid Energy 3,550 7.5 Jun-22 DCP Midstream / James Lake System (Woodland Midstream II) 160 5.5 May-22 EnLink Midstream / Barnett Gathering and Processing System (Crestwood Equity Partners) 275 4.0 May-22 Crestwood Equity Partners / Sendero Midstream 600 7.0 Apr-22 Delek Logistics Partners / 3Bear Energy 625 8.8 Mar-22 Targa Resources / Southcross Energy Operating 200 4.0 Mar-22 Williams Companies / Trace Midstream 950 6.0 Jan-22 Enterprise Products Partners / Navitas Midstream Partners 3,250 7.8 Oct-21 Crestwood Equity Partners / Oasis Midstream 1,848 8.3 Oct-21 Altus Midstream / BCP Raptor/EagleClaw Midstream 6,248 11.7 Apr-21 EnLink Midstream LLC / Amarillo Rattler JV (Rattler Midstream Partners LP, Amarillo Midstream) 60 6.0 Aug-20 Citizen Energy II LLC / Blue Mountain Midstream LLC (Riviera Resources, Inc.) 111 7.1 Jul-20 CNX Resources Corporation / 46.9% stake in CNX Midstream Partners LP 728 7.7 Feb-20 Equitrans Midstream Corporation / EQM Midstream Partners 1,762 8.3 Mean 6.8x Median 7.0 Min 3.0 Max 11.7

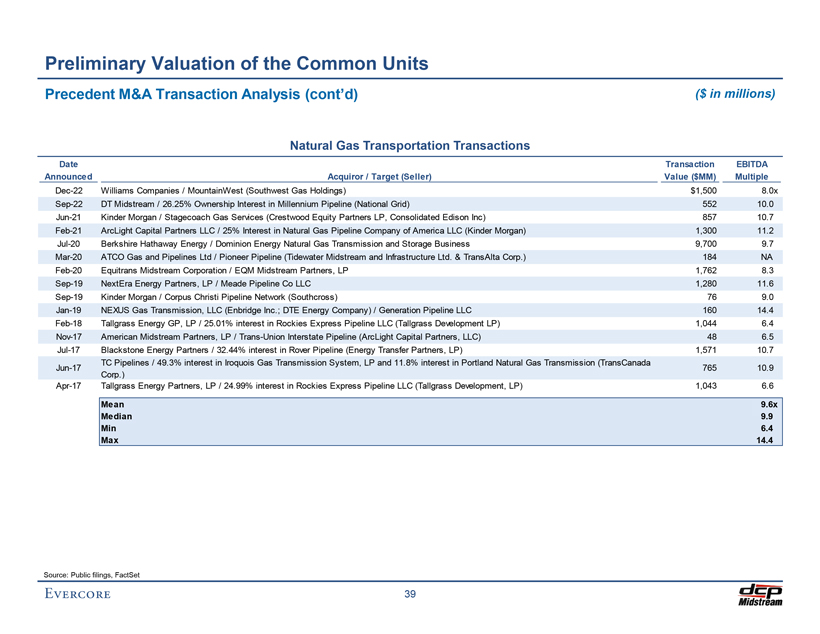

Preliminary Valuation of the Common Units Precedent M&A Transaction Analysis (cont’d) ($ in millions) Natural Gas Transportation Transactions Date Transaction EBITDA Announced Acquiror / Target (Seller) Value ($MM) Multiple Dec-22 Williams Companies / MountainWest (Southwest Gas Holdings) $1,500 8.0x Sep-22 DT Midstream / 26.25% Ownership Interest in Millennium Pipeline (National Grid) 552 10.0 Jun-21 Kinder Morgan / Stagecoach Gas Services (Crestwood Equity Partners LP, Consolidated Edison Inc) 857 10.7 Feb-21 ArcLight Capital Partners LLC / 25% Interest in Natural Gas Pipeline Company of America LLC (Kinder Morgan) 1,300 11.2 Jul-20 Berkshire Hathaway Energy / Dominion Energy Natural Gas Transmission and Storage Business 9,700 9.7 Mar-20 ATCO Gas and Pipelines Ltd / Pioneer Pipeline (Tidewater Midstream and Infrastructure Ltd. & TransAlta Corp.) 184 NA Feb-20 Equitrans Midstream Corporation / EQM Midstream Partners, LP 1,762 8.3 Sep-19 NextEra Energy Partners, LP / Meade Pipeline Co LLC 1,280 11.6 Sep-19 Kinder Morgan / Corpus Christi Pipeline Network (Southcross) 76 9.0 Jan-19 NEXUS Gas Transmission, LLC (Enbridge Inc.; DTE Energy Company) / Generation Pipeline LLC 160 14.4 Feb-18 Tallgrass Energy GP, LP / 25.01% interest in Rockies Express Pipeline LLC (Tallgrass Development LP) 1,044 6.4 Nov-17 American Midstream Partners, LP / Trans-Union Interstate Pipeline (ArcLight Capital Partners, LLC) 48 6.5 Jul-17 Blackstone Energy Partners / 32.44% interest in Rover Pipeline (Energy Transfer Partners, LP) 1,571 10.7 TC Pipelines / 49.3% interest in Iroquois Gas Transmission System, LP and 11.8% interest in Portland Natural Gas Transmission (TransCanada Jun-17 765 10.9 Corp.) Apr-17 Tallgrass Energy Partners, LP / 24.99% interest in Rockies Express Pipeline LLC (Tallgrass Development, LP) 1,043 6.6 Mean 9.6x Median 9.9 Min 6.4 Max 14.4 Source: Public filings, FactSet

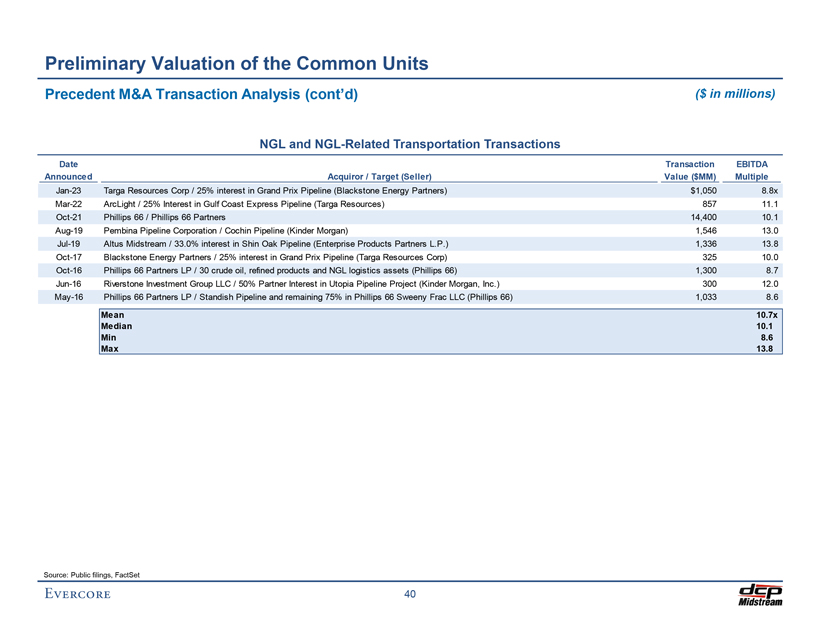

Preliminary Valuation of the Common Units Precedent M&A Transaction Analysis (cont’d) ($ in millions) NGL and NGL-Related Transportation Transactions Date Transaction EBITDA Announced Acquiror / Target (Seller) Value ($MM) Multiple Jan-23 Targa Resources Corp / 25% interest in Grand Prix Pipeline (Blackstone Energy Partners) $1,050 8.8x Mar-22 ArcLight / 25% Interest in Gulf Coast Express Pipeline (Targa Resources) 857 11.1 Oct-21 Phillips 66 / Phillips 66 Partners 14,400 10.1 Aug-19 Pembina Pipeline Corporation / Cochin Pipeline (Kinder Morgan) 1,546 13.0 Jul-19 Altus Midstream / 33.0% interest in Shin Oak Pipeline (Enterprise Products Partners L.P.) 1,336 13.8 Oct-17 Blackstone Energy Partners / 25% interest in Grand Prix Pipeline (Targa Resources Corp) 325 10.0 Oct-16 Phillips 66 Partners LP / 30 crude oil, refined products and NGL logistics assets (Phillips 66) 1,300 8.7 Jun-16 Riverstone Investment Group LLC / 50% Partner Interest in Utopia Pipeline Project (Kinder Morgan, Inc.) 300 12.0 May-16 Phillips 66 Partners LP / Standish Pipeline and remaining 75% in Phillips 66 Sweeny Frac LLC (Phillips 66) 1,033 8.6 Mean 10.7x Median 10.1 Min 8.6 Max 13.8 Source: Public filings, FactSet

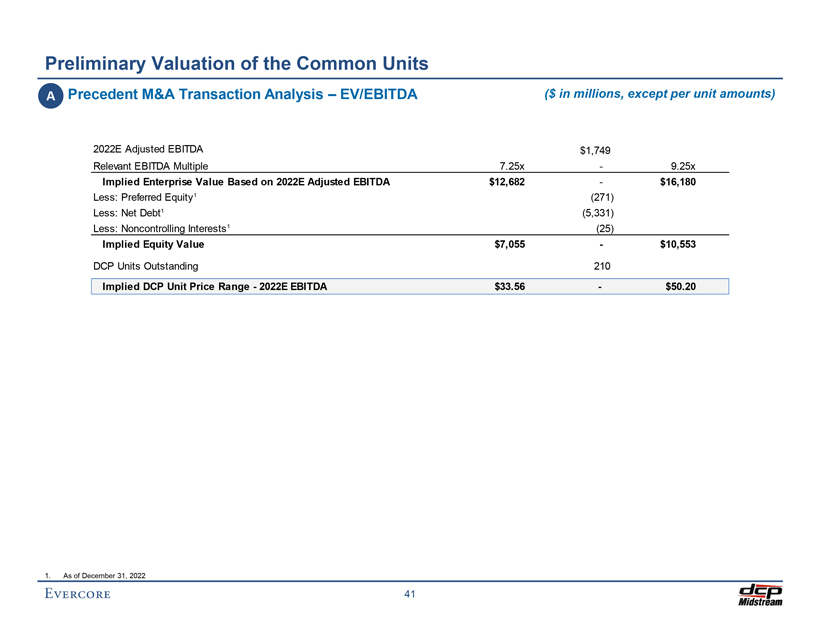

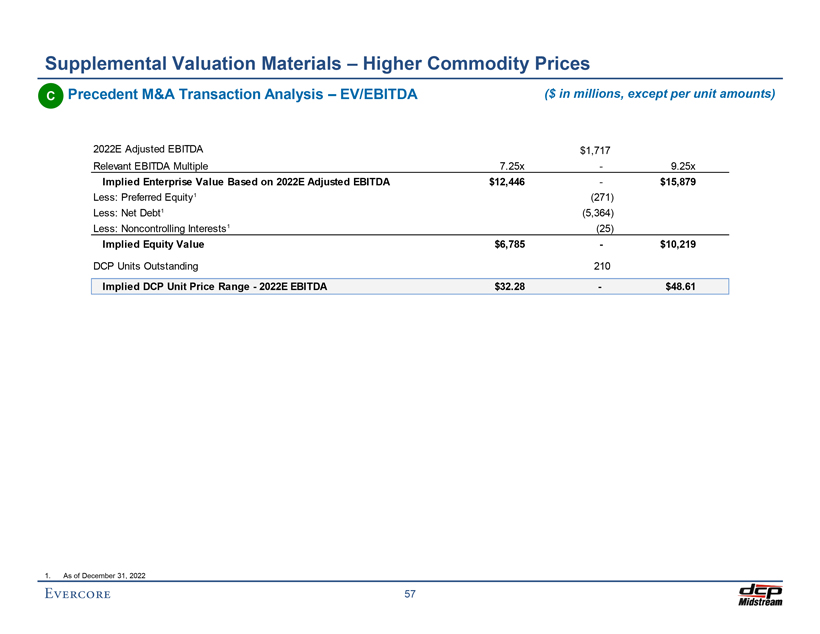

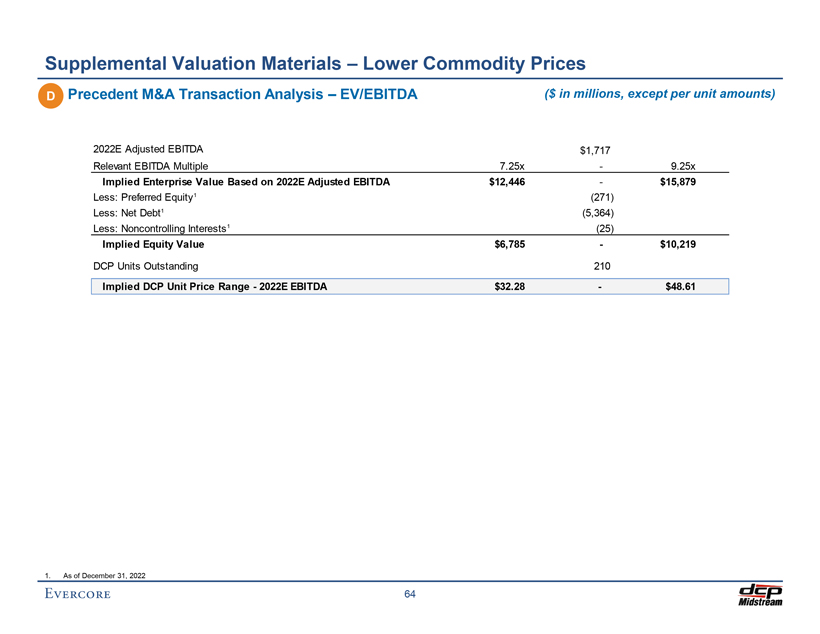

Preliminary Valuation of the Common Units A Precedent M&A Transaction Analysis – EV/EBITDA ($ in millions, except per unit amounts) 2022E Adjusted EBITDA $1,749 Relevant EBITDA Multiple 7.25x—9.25x Implied Enterprise Value Based on 2022E Adjusted EBITDA $12,682—$16,180 Less: Preferred Equity1 (271) Less: Net Debt1 (5,331) Less: Noncontrolling Interests1 (25) Implied Equity Value $7,055—$10,553 DCP Units Outstanding 210 Implied DCP Unit Price Range—2022E EBITDA $33.56—$50.20 1. As of December 31, 2022

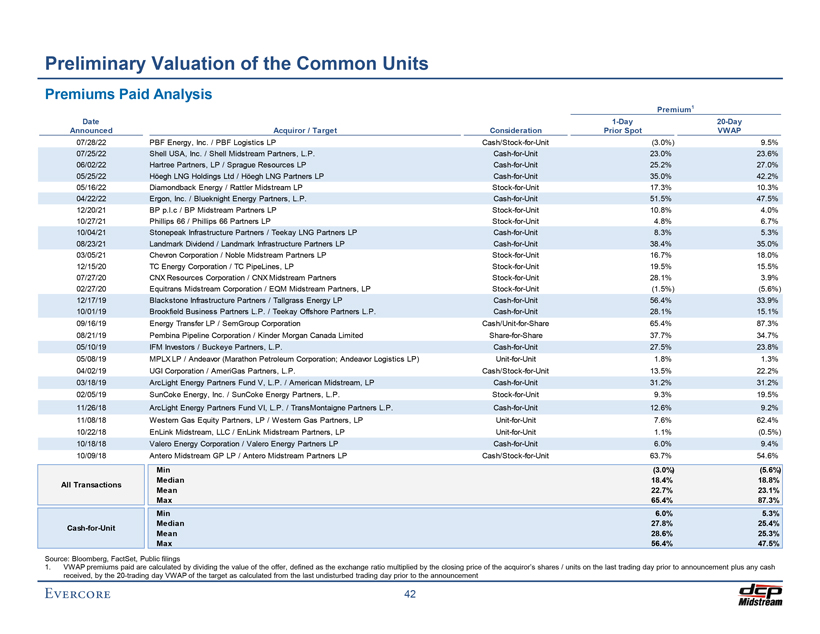

Preliminary Valuation of the Common Units Premiums Paid Analysis Premium1 Date 1-Day 20-Day Announced Acquiror / Target Consideration Prior Spot VWAP 07/28/22 PBF Energy, Inc. / PBF Logistics LP Cash/Stock-for-Unit (3.0%) 9.5% 07/25/22 Shell USA, Inc. / Shell Midstream Partners, L.P. Cash-for-Unit 23.0% 23.6% 06/02/22 Hartree Partners, LP / Sprague Resources LP Cash-for-Unit 25.2% 27.0% 05/25/22 Höegh LNG Holdings Ltd / Höegh LNG Partners LP Cash-for-Unit 35.0% 42.2% 05/16/22 Diamondback Energy / Rattler Midstream LP Stock-for-Unit 17.3% 10.3% 04/22/22 Ergon, Inc. / Blueknight Energy Partners, L.P. Cash-for-Unit 51.5% 47.5% 12/20/21 BP p.l.c / BP Midstream Partners LP Stock-for-Unit 10.8% 4.0% 10/27/21 Phillips 66 / Phillips 66 Partners LP Stock-for-Unit 4.8% 6.7% 10/04/21 Stonepeak Infrastructure Partners / Teekay LNG Partners LP Cash-for-Unit 8.3% 5.3% 08/23/21 Landmark Dividend / Landmark Infrastructure Partners LP Cash-for-Unit 38.4% 35.0% 03/05/21 Chevron Corporation / Noble Midstream Partners LP Stock-for-Unit 16.7% 18.0% 12/15/20 TC Energy Corporation / TC PipeLines, LP Stock-for-Unit 19.5% 15.5% 07/27/20 CNX Resources Corporation / CNX Midstream Partners Stock-for-Unit 28.1% 3.9% 02/27/20 Equitrans Midstream Corporation / EQM Midstream Partners, LP Stock-for-Unit (1.5%) (5.6%) 12/17/19 Blackstone Infrastructure Partners / Tallgrass Energy LP Cash-for-Unit 56.4% 33.9% 10/01/19 Brookfield Business Partners L.P. / Teekay Offshore Partners L.P. Cash-for-Unit 28.1% 15.1% 09/16/19 Energy Transfer LP / SemGroup Corporation Cash/Unit-for-Share 65.4% 87.3% 08/21/19 Pembina Pipeline Corporation / Kinder Morgan Canada Limited Share-for-Share 37.7% 34.7% 05/10/19 IFM Investors / Buckeye Partners, L.P. Cash-for-Unit 27.5% 23.8% 05/08/19 MPLX LP / Andeavor (Marathon Petroleum Corporation; Andeavor Logistics LP) Unit-for-Unit 1.8% 1.3% 04/02/19 UGI Corporation / AmeriGas Partners, L.P. Cash/Stock-for-Unit 13.5% 22.2% 03/18/19 ArcLight Energy Partners Fund V, L.P. / American Midstream, LP Cash-for-Unit 31.2% 31.2% 02/05/19 SunCoke Energy, Inc. / SunCoke Energy Partners, L.P. Stock-for-Unit 9.3% 19.5% 11/26/18 ArcLight Energy Partners Fund VI, L.P. / TransMontaigne Partners L.P. Cash-for-Unit 12.6% 9.2% 11/08/18 Western Gas Equity Partners, LP / Western Gas Partners, LP Unit-for-Unit 7.6% 62.4% 10/22/18 EnLink Midstream, LLC / EnLink Midstream Partners, LP Unit-for-Unit 1.1% (0.5%) 10/18/18 Valero Energy Corporation / Valero Energy Partners LP Cash-for-Unit 6.0% 9.4% 10/09/18 Antero Midstream GP LP / Antero Midstream Partners LP Cash/Stock-for-Unit 63.7% 54.6% Min (3.0%) (5.6%) Median 18.4% 18.8% All Transactions Mean 22.7% 23.1% Max 65.4% 87.3% Min 6.0% 5.3% Median 27.8% 25.4% Cash-for-Unit Mean 28.6% 25.3% Max 56.4% 47.5% Source: Bloomberg, FactSet, Public filings VWAP premiums paid are calculated by dividing the value of the offer, defined as the exchange ratio multiplied by the closing price of the acquiror’s shares / units on the last trading day prior to announcement plus any cash received, by the 20-trading day VWAP of the target as calculated from the last undisturbed trading day prior to the announcement

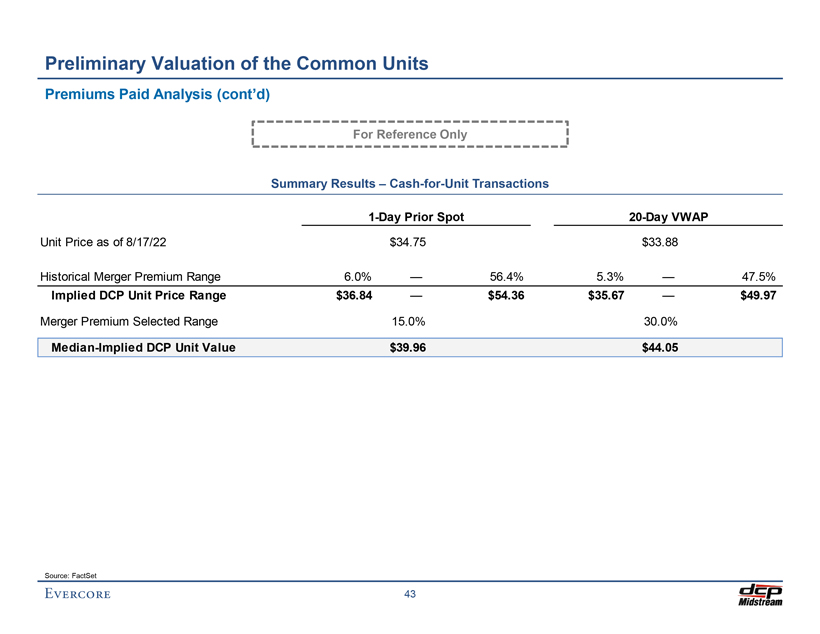

Preliminary Valuation of the Common Units Premiums Paid Analysis (cont’d) For Reference Only Summary Results – Cash-for-Unit Transactions 1-Day Prior Spot 20-Day VWAP Unit Price as of 8/17/22 $34.75 $33.88 Historical Merger Premium Range 6.0% — 56.4% 5.3% — 47.5% Implied DCP Unit Price Range $36.84 — $54.36 $35.67 — $49.97 Merger Premium Selected Range 15.0% 30.0% Median-Implied DCP Unit Value $39.96 $44.05 Source: FactSet

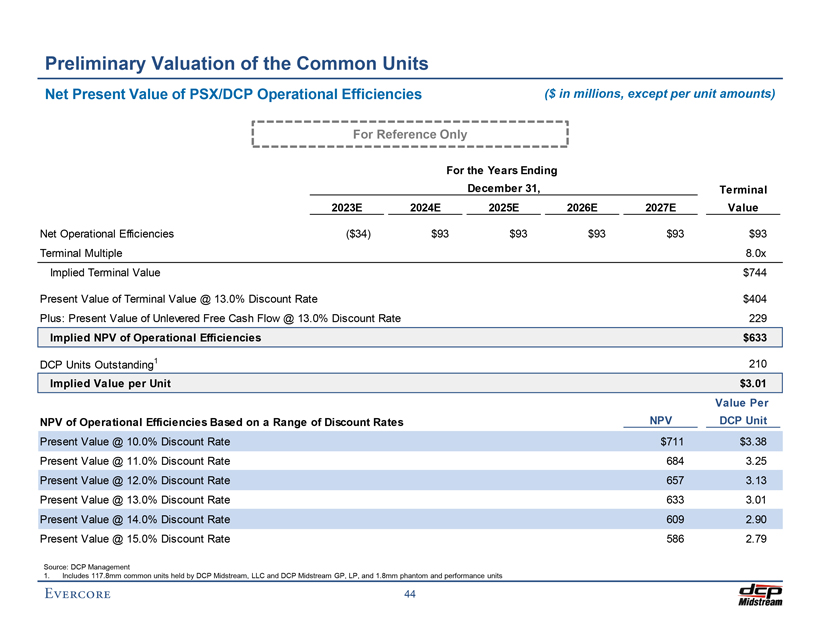

Preliminary Valuation of the Common Units Net Present Value of PSX/DCP Operational Efficiencies ($ in millions, except per unit amounts) For Reference Only For the Years Ending December 31, Terminal 2023E 2024E 2025E 2026E 2027E Value Net Operational Efficiencies ($34) $93 $93 $93 $93 $93 Terminal Multiple 8.0x Implied Terminal Value $744 Present Value of Terminal Value @ 13.0% Discount Rate $404 Plus: Present Value of Unlevered Free Cash Flow @ 13.0% Discount Rate 229 Implied NPV of Operational Efficiencies $633 DCP Units Outstanding1 210 Implied Value per Unit $3.01 Value Per NPV of Operational Efficiencies Based on a Range of Discount Rates NPV DCP Unit Present Value @ 10.0% Discount Rate $711 $3.38 Present Value @ 11.0% Discount Rate 684 3.25 Present Value @ 12.0% Discount Rate 657 3.13 Present Value @ 13.0% Discount Rate 633 3.01 Present Value @ 14.0% Discount Rate 609 2.90 Present Value @ 15.0% Discount Rate 586 2.79 Source: DCP Management 1. Includes 117.8mm common units held by DCP Midstream, LLC and DCP Midstream GP, LP, and 1.8mm phantom and performance units

Appendix

A. Weighted Average Cost of Capital Analysis

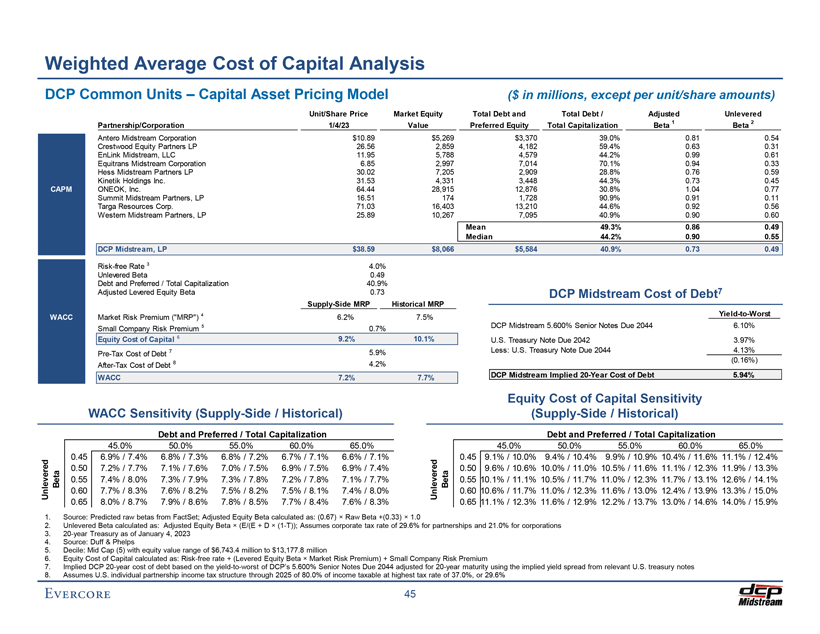

Weighted Average Cost of Capital Analysis DCP Common Units – Capital Asset Pricing Model ($ in millions, except per unit/share amounts) Unit/Share Price Market Equity Total Debt and Total Debt / Adjusted Unlevered 1/4/23 Value Preferred Equity Capitalization Beta 1 2 Partnership/Corporation Total Beta Antero Midstream Corporation $10.89 $5,269 $3,370 39.0% 0.81 0.54 Crestwood Equity Partners LP 26.56 2,859 4,182 59.4% 0.63 0.31 EnLink Midstream, LLC 11.95 5,788 4,579 44.2% 0.99 0.61 Equitrans Midstream Corporation 6.85 2,997 7,014 70.1% 0.94 0.33 Hess Midstream Partners LP 30.02 7,205 2,909 28.8% 0.76 0.59 Kinetik Holdings Inc. 31.53 4,331 3,448 44.3% 0.73 0.45 CAPM ONEOK, Inc. 64.44 28,915 12,876 30.8% 1.04 0.77 Summit Midstream Partners, LP 16.51 174 1,728 90.9% 0.91 0.11 Targa Resources Corp. 71.03 16,403 13,210 44.6% 0.92 0.56 Western Midstream Partners, LP 25.89 10,267 7,095 40.9% 0.90 0.60 Mean 49.3% 0.86 0.49 Median 44.2% 0.90 0.55 DCP Midstream, LP $38.59 $8,066 $5,584 40.9% 0.73 0.49 Risk-free Rate 3 4.0% Unlevered Beta 0.49 Debt and Preferred / Total Capitalization 40.9% Adjusted Levered Equity Beta 0.73 DCP Midstream Cost of Debt7 Supply-Side MRP Historical MRP 4 Yield-to-Worst WACC Market Risk Premium (“MRP”) 6.2% 7.5% Small Company Risk Premium 5 0.7% DCP Midstream 5.600% Senior Notes Due 2044 6.10% Equity Cost of Capital 6 9.2% 10.1% U.S. Treasury Note Due 2042 3.97% 7 5.9% Less: U.S. Treasury Note Due 2044 4.13% Pre-Tax Cost of Debt (0.16%) After-Tax Cost of Debt 8 4.2% WACC 7.2% 7.7% DCP Midstream Implied 20-Year Cost of Debt 5.94% Equity Cost of Capital Sensitivity WACC Sensitivity (Supply-Side / Historical) (Supply-Side / Historical) Debt and Preferred / Total Capitalization Debt and Preferred / Total Capitalization 45.0% 50.0% 55.0% 60.0% 65.0% 45.0% 50.0% 55.0% 60.0% 65.0% ed 0.45 6.9% / 7.4% 6.8% / 7.3% 6.8% / 7.2% 6.7% / 7.1% 6.6% / 7.1% ed 0.45 9.1% / 10.0% 9.4% / 10.4% 9.9% / 10.9% 10.4% / 11.6% 11.1% / 12.4% r 0.50 7.2% / 7.7% 7.1% / 7.6% 7.0% / 7.5% 6.9% / 7.5% 6.9% / 7.4% r 0.50 9.6% / 10.6% 10.0% / 11.0% 10.5% / 11.6% 11.1% / 12.3% 11.9% / 13.3% Beta 0.55 7.4% / 8.0% 7.3% / 7.9% 7.3% / 7.8% 7.2% / 7.8% 7.1% / 7.7% Beta 0.55 10.1% / 11.1% 10.5% / 11.7% 11.0% / 12.3% 11.7% / 13.1% 12.6% / 14.1% nleve U 0.60 7.7% / 8.3% 7.6% / 8.2% 7.5% / 8.2% 7.5% / 8.1% 7.4% / 8.0% U nleve 0.60 10.6% / 11.7% 11.0% / 12.3% 11.6% / 13.0% 12.4% / 13.9% 13.3% / 15.0% 0.65 8.0% / 8.7% 7.9% / 8.6% 7.8% / 8.5% 7.7% / 8.4% 7.6% / 8.3% 0.65 11.1% / 12.3% 11.6% / 12.9% 12.2% / 13.7% 13.0% / 14.6% 14.0% / 15.9% 1. Source: Predicted raw betas from FactSet; Adjusted Equity Beta calculated as: (0.67) × Raw Beta +(0.33) × 1.0 2. Unlevered Beta calculated as: Adjusted Equity Beta × (E/(E + D × (1-T)); Assumes corporate tax rate of 29.6% for partnerships and 21.0% for corporations 3. 20-year Treasury as of January 4, 2023 4. Source: Duff & Phelps 5. Decile: Mid Cap (5) with equity value range of $6,743.4 million to $13,177.8 million 6. Equity Cost of Capital calculated as: Risk-free rate + (Levered Equity Beta × Market Risk Premium) + Small Company Risk Premium 7. Implied DCP 20-year cost of debt based on the yield-to-worst of DCP’s 5.600% Senior Notes Due 2044 adjusted for 20-year maturity using the implied yield spread from relevant U.S. treasury notes 8. Assumes U.S. individual partnership income tax structure through 2025 of 80.0% of income taxable at highest tax rate of 37.0%, or 29.6%

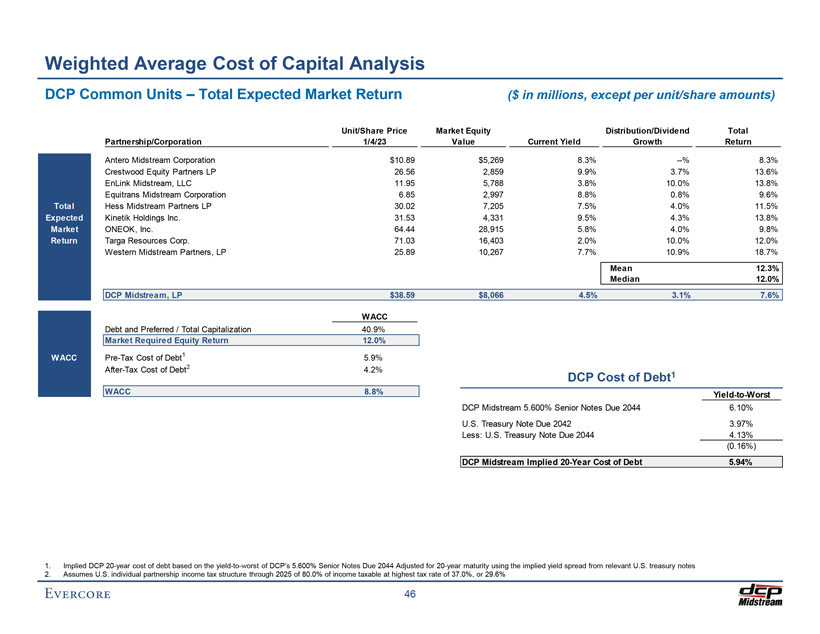

Weighted Average Cost of Capital Analysis DCP Common Units – Total Expected Market Return ($ in millions, except per unit/share amounts) Unit/Share Price Market Equity Distribution/Dividend Total Partnership/Corporation 1/4/23 Value Current Yield Growth Return Antero Midstream Corporation $10.89 $5,269 8.3% —% 8.3% Crestwood Equity Partners LP 26.56 2,859 9.9% 3.7% 13.6% EnLink Midstream, LLC 11.95 5,788 3.8% 10.0% 13.8% Equitrans Midstream Corporation 6.85 2,997 8.8% 0.8% 9.6% Total Hess Midstream Partners LP 30.02 7,205 7.5% 4.0% 11.5% Expected Kinetik Holdings Inc. 31.53 4,331 9.5% 4.3% 13.8% Market ONEOK, Inc. 64.44 28,915 5.8% 4.0% 9.8% Return Targa Resources Corp. 71.03 16,403 2.0% 10.0% 12.0% Western Midstream Partners, LP 25.89 10,267 7.7% 10.9% 18.7% Mean 12.3% Median 12.0% DCP Midstream, LP $38.59 $8,066 4.5% 3.1% 7.6% WACC Debt and Preferred / Total Capitalization 40.9% Market Required Equity Return 12.0% WACC Pre-Tax Cost of Debt1 5.9% After-Tax Cost of Debt2 4.2% DCP Cost of Debt1 WACC 8.8% Yield-to-Worst DCP Midstream 5.600% Senior Notes Due 2044 6.10% U.S. Treasury Note Due 2042 3.97% Less: U.S. Treasury Note Due 2044 4.13% (0.16%) DCP Midstream Implied 20-Year Cost of Debt 5.94% 1. Implied DCP 20-year cost of debt based on the yield-to-worst of DCP’s 5.600% Senior Notes Due 2044 Adjusted for 20-year maturity using the implied yield spread from relevant U.S. treasury notes 2. Assumes U.S. individual partnership income tax structure through 2025 of 80.0% of income taxable at highest tax rate of 37.0%, or 29.6%

B. Supplemental Valuation Materials

B Sensitivity Case B – NYMEX Strip Pricing

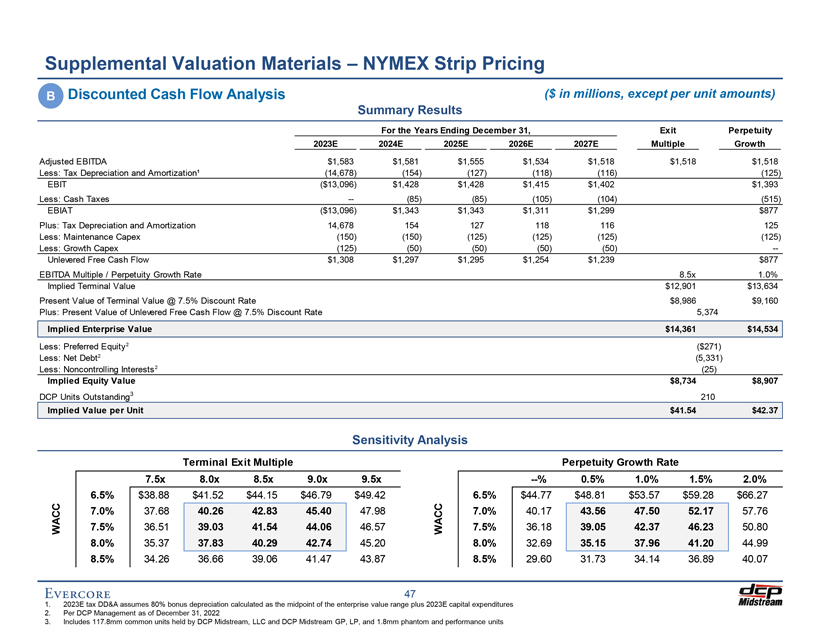

Supplemental Valuation Materials – NYMEX Strip Pricing B Discounted Cash Flow Analysis ($ in millions, except per unit amounts) Summary Results For the Years Ending December 31, Exit Perpetuity 2023E 2024E 2025E 2026E 2027E Multiple Growth Adjusted EBITDA $1,583 $1,581 $1,555 $1,534 $1,518 $1,518 $1,518 Less: Tax Depreciation and Amortization¹ (14,678) (154) (127) (118) (116) (125) EBIT ($13,096) $1,428 $1,428 $1,415 $1,402 $1,393 Less: Cash Taxes — (85) (85) (105) (104) (515) EBIAT ($13,096) $1,343 $1,343 $1,311 $1,299 $877 Plus: Tax Depreciation and Amortization 14,678 154 127 118 116 125 Less: Maintenance Capex (150) (150) (125) (125) (125) (125) Less: Growth Capex (125) (50) (50) (50) (50) —Unlevered Free Cash Flow $1,308 $1,297 $1,295 $1,254 $1,239 $877 EBITDA Multiple / Perpetuity Growth Rate 8.5x 1.0% Implied Terminal Value $12,901 $13,634 Present Value of Terminal Value @ 7.5% Discount Rate $8,986 $9,160 Plus: Present Value of Unlevered Free Cash Flow @ 7.5% Discount Rate 5,374 Implied Enterprise Value $14,361 $14,534 Less: Preferred Equity2 ($271) Less: Net Debt2 (5,331) Less: Noncontrolling Interests2 (25) Implied Equity Value $8,734 $8,907 DCP Units Outstanding3 210 Implied Value per Unit $41.54 $42.37 Sensitivity Analysis Terminal Exit Multiple Perpetuity Growth Rate 7.5x 8.0x 8.5x 9.0x 9.5x —% 0.5% 1.0% 1.5% 2.0% 6.5% $38.88 $41.52 $44.15 $46.79 $49.42 6.5% $44.77 $48.81 $53.57 $59.28 $66.27 7.0% 37.68 40.26 42.83 45.40 47.98 7.0% 40.17 43.56 47.50 52.17 57.76 WACC 7.5% 36.51 39.03 41.54 44.06 46.57 WACC 7.5% 36.18 39.05 42.37 46.23 50.80 8.0% 35.37 37.83 40.29 42.74 45.20 8.0% 32.69 35.15 37.96 41.20 44.99 8.5% 34.26 36.66 39.06 41.47 43.87 8.5% 29.60 31.73 34.14 36.89 40.07 47 1. 2023E tax DD&A assumes 80% bonus depreciation calculated as the midpoint of the enterprise value range plus 2023E capital expenditures 2. Per DCP Management as of December 31, 2022 3. Includes 117.8mm common units held by DCP Midstream, LLC and DCP Midstream GP, LP, and 1.8mm phantom and performance units

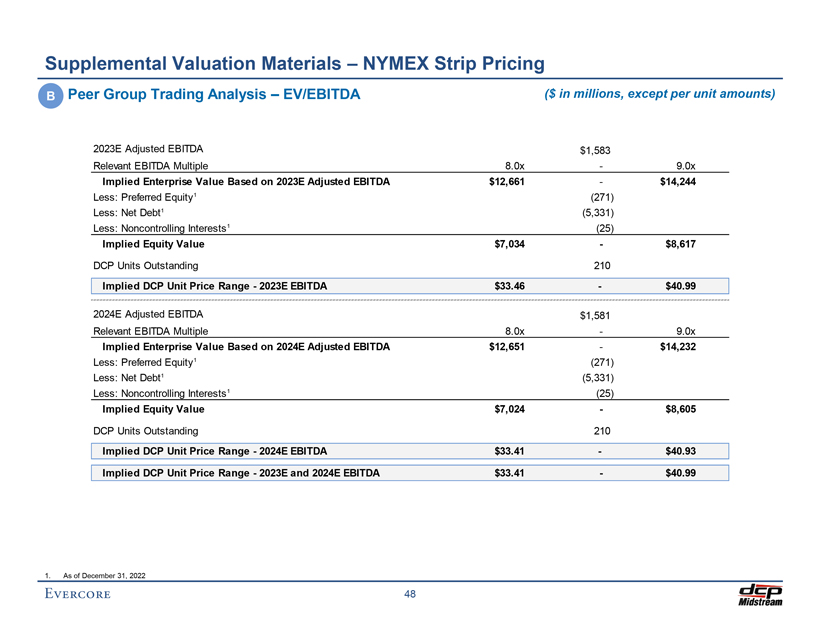

Supplemental Valuation Materials – NYMEX Strip Pricing B Peer Group Trading Analysis – EV/EBITDA ($ in millions, except per unit amounts) 2023E Adjusted EBITDA $1,583 Relevant EBITDA Multiple 8.0x—9.0x Implied Enterprise Value Based on 2023E Adjusted EBITDA $12,661—$14,244 Less: Preferred Equity1 (271) Less: Net Debt1 (5,331) Less: Noncontrolling Interests1 (25) Implied Equity Value $7,034—$8,617 DCP Units Outstanding 210 Implied DCP Unit Price Range—2023E EBITDA $33.46—$40.99 2024E Adjusted EBITDA $1,581 Relevant EBITDA Multiple 8.0x—9.0x Implied Enterprise Value Based on 2024E Adjusted EBITDA $12,651—$14,232 Less: Preferred Equity1 (271) Less: Net Debt1 (5,331) Less: Noncontrolling Interests1 (25) Implied Equity Value $7,024—$8,605 DCP Units Outstanding 210 Implied DCP Unit Price Range—2024E EBITDA $33.41—$40.93 Implied DCP Unit Price Range—2023E and 2024E EBITDA $33.41—$40.99 1. As of December 31, 2022

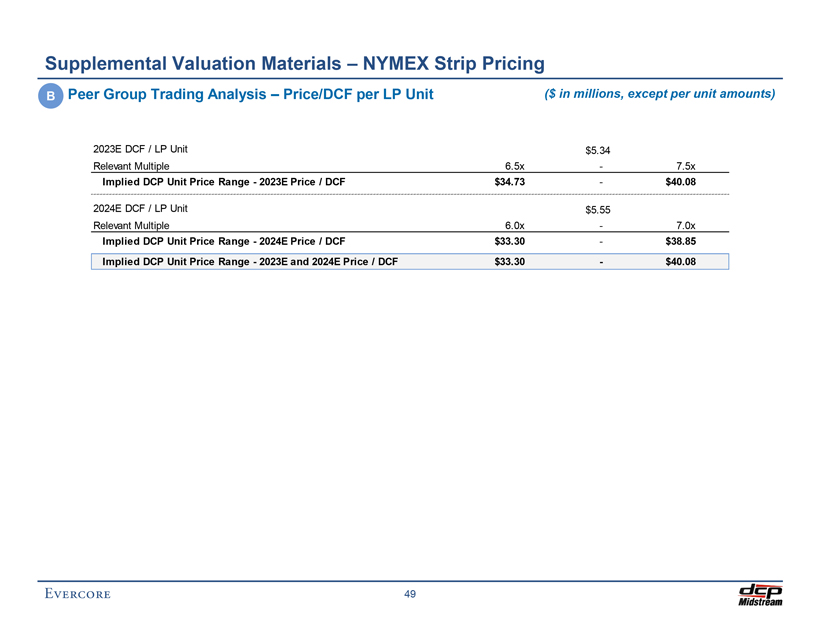

Supplemental Valuation Materials – NYMEX Strip Pricing B Peer Group Trading Analysis – Price/DCF per LP Unit ($ in millions, except per unit amounts) 2023E DCF / LP Unit $5.34 Relevant Multiple 6.5x—7.5x Implied DCP Unit Price Range—2023E Price / DCF $34.73—$40.08 2024E DCF / LP Unit $5.55 Relevant Multiple 6.0x—7.0x Implied DCP Unit Price Range—2024E Price / DCF $33.30—$38.85 Implied DCP Unit Price Range—2023E and 2024E Price / DCF $33.30—$40.08

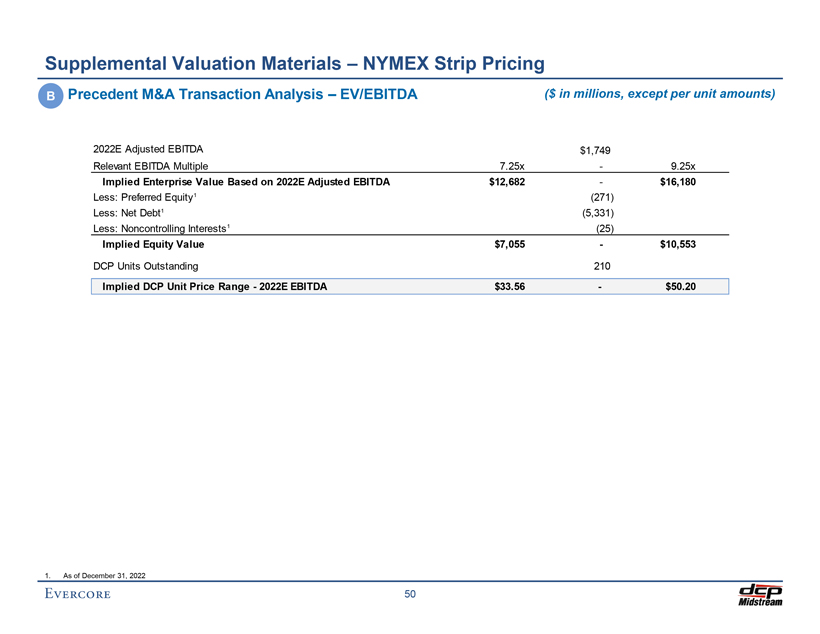

Supplemental Valuation Materials – NYMEX Strip Pricing B Precedent M&A Transaction Analysis – EV/EBITDA ($ in millions, except per unit amounts) 2022E Adjusted EBITDA $1,749 Relevant EBITDA Multiple 7.25x—9.25x Implied Enterprise Value Based on 2022E Adjusted EBITDA $12,682—$16,180 Less: Preferred Equity1 (271) Less: Net Debt1 (5,331) Less: Noncontrolling Interests1 (25) Implied Equity Value $7,055—$10,553 DCP Units Outstanding 210 Implied DCP Unit Price Range—2022E EBITDA $33.56—$50.20 1. As of December 31, 2022

C Sensitivity Case C – Higher Commodity Prices

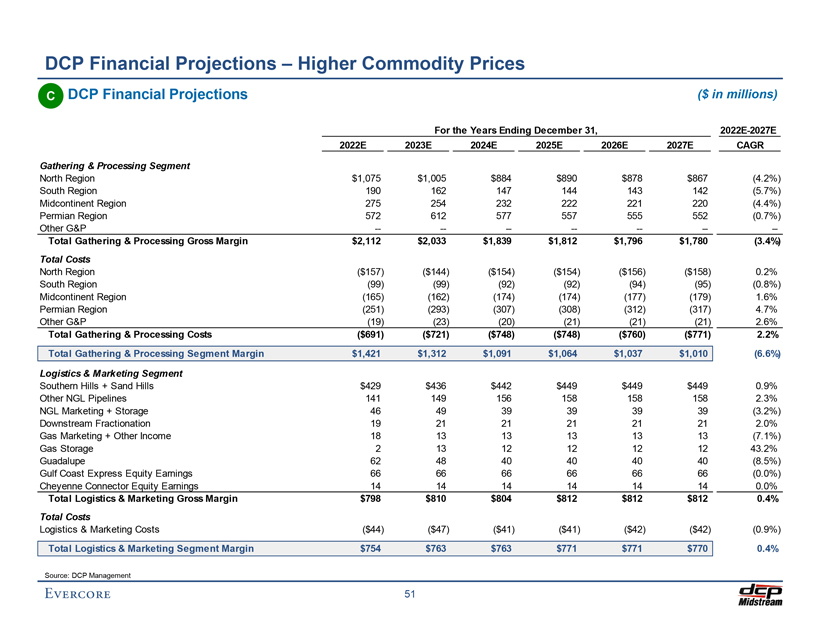

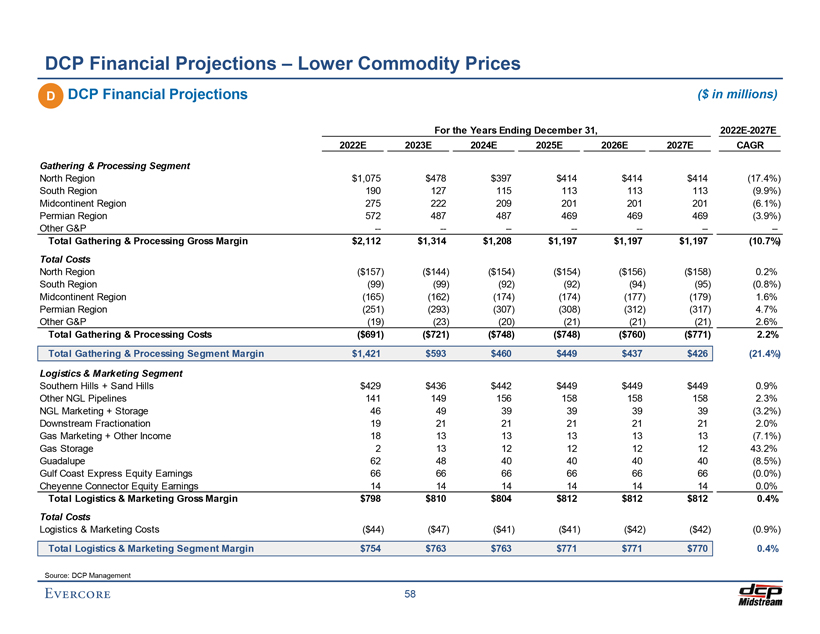

DCP Financial Projections – Higher Commodity Prices C DCP Financial Projections ($ in millions) For the Years Ending December 31, 2022E-2027E 2022E 2023E 2024E 2025E 2026E 2027E CAGR Gathering & Processing Segment North Region $1,075 $1,005 $884 $890 $878 $867 (4.2%) South Region 190 162 147 144 143 142 (5.7%) Midcontinent Region 275 254 232 222 221 220 (4.4%) Permian Region 572 612 577 557 555 552 (0.7%) Other G&P -——————- Total Gathering & Processing Gross Margin $2,112 $2,033 $1,839 $1,812 $1,796 $1,780 (3.4%) Total Costs North Region ($157) ($144) ($154) ($154) ($156) ($158) 0.2% South Region (99) (99) (92) (92) (94) (95) (0.8%) Midcontinent Region (165) (162) (174) (174) (177) (179) 1.6% Permian Region (251) (293) (307) (308) (312) (317) 4.7% Other G&P (19) (23) (20) (21) (21) (21) 2.6% Total Gathering & Processing Costs ($691) ($721) ($748) ($748) ($760) ($771) 2.2% Total Gathering & Processing Segment Margin $1,421 $1,312 $1,091 $1,064 $1,037 $1,010 (6.6%) Logistics & Marketing Segment Southern Hills + Sand Hills $429 $436 $442 $449 $449 $449 0.9% Other NGL Pipelines 141 149 156 158 158 158 2.3% NGL Marketing + Storage 46 49 39 39 39 39 (3.2%) Downstream Fractionation 19 21 21 21 21 21 2.0% Gas Marketing + Other Income 18 13 13 13 13 13 (7.1%) Gas Storage 2 13 12 12 12 12 43.2% Guadalupe 62 48 40 40 40 40 (8.5%) Gulf Coast Express Equity Earnings 66 66 66 66 66 66 (0.0%) Cheyenne Connector Equity Earnings 14 14 14 14 14 14 0.0% Total Logistics & Marketing Gross Margin $798 $810 $804 $812 $812 $812 0.4% Total Costs Logistics & Marketing Costs ($44) ($47) ($41) ($41) ($42) ($42) (0.9%) Total Logistics & Marketing Segment Margin $754 $763 $763 $771 $771 $770 0.4% Source: DCP Management

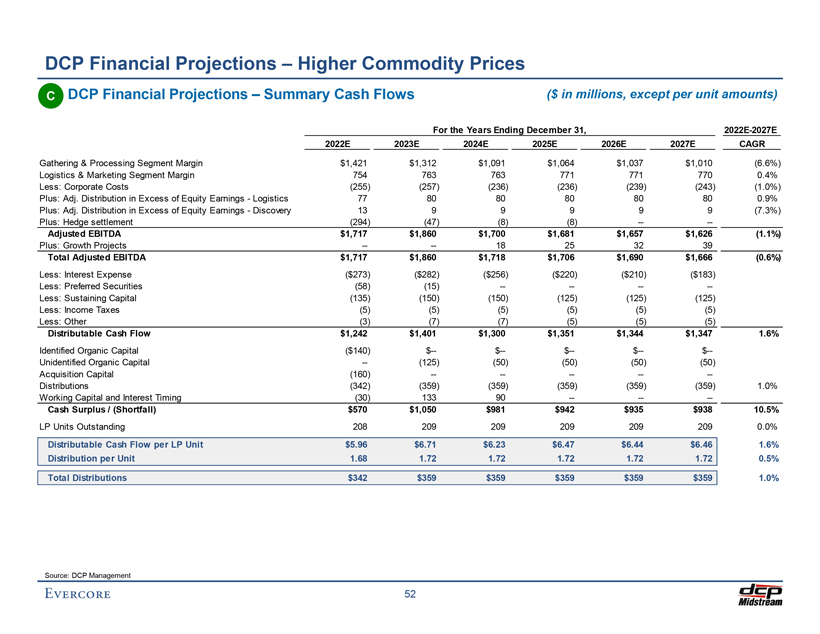

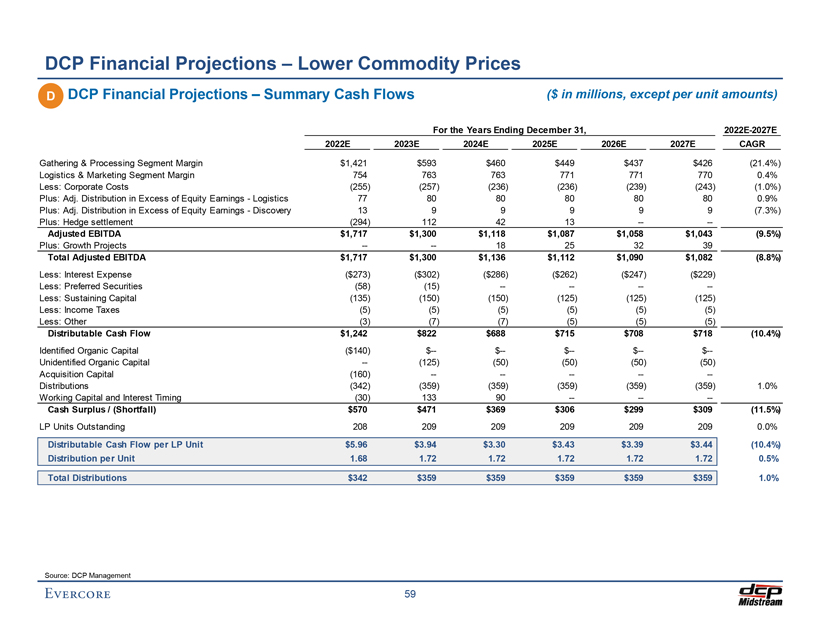

DCP Financial Projections – Higher Commodity Prices C DCP Financial Projections – Summary Cash Flows ($ in millions, except per unit amounts) For the Years Ending December 31, 2022E-2027E 2022E 2023E 2024E 2025E 2026E 2027E CAGR Gathering & Processing Segment Margin $1,421 $1,312 $1,091 $1,064 $1,037 $1,010 (6.6%) Logistics & Marketing Segment Margin 754 763 763 771 771 770 0.4% Less: Corporate Costs (255) (257) (236) (236) (239) (243) (1.0%) Plus: Adj. Distribution in Excess of Equity Earnings—Logistics 77 80 80 80 80 80 0.9% Plus: Adj. Distribution in Excess of Equity Earnings—Discovery 13 9 9 9 9 9 (7.3%) Plus: Hedge settlement (294) (47) (8) (8) -—- Adjusted EBITDA $1,717 $1,860 $1,700 $1,681 $1,657 $1,626 (1.1%) Plus: Growth Projects -—- 18 25 32 39 Total Adjusted EBITDA $1,717 $1,860 $1,718 $1,706 $1,690 $1,666 (0.6%) Less: Interest Expense ($273) ($282) ($256) ($220) ($210) ($183) Less: Preferred Securities (58) (15) -———-Less: Sustaining Capital (135) (150) (150) (125) (125) (125) Less: Income Taxes (5) (5) (5) (5) (5) (5) Less: Other (3) (7) (7) (5) (5) (5) Distributable Cash Flow $1,242 $1,401 $1,300 $1,351 $1,344 $1,347 1.6% Identified Organic Capital ($140) $— $— $— $— $—Unidentified Organic Capital — (125) (50) (50) (50) (50) Acquisition Capital (160) -————- Distributions (342) (359) (359) (359) (359) (359) 1.0% Working Capital and Interest Timing (30) 133 90 -——- Cash Surplus / (Shortfall) $570 $1,050 $981 $942 $935 $938 10.5% LP Units Outstanding 208 209 209 209 209 209 0.0% Distributable Cash Flow per LP Unit $5.96 $6.71 $6.23 $6.47 $6.44 $6.46 1.6% Distribution per Unit 1.68 1.72 1.72 1.72 1.72 1.72 0.5% Total Distributions $342 $359 $359 $359 $359 $359 1.0% Source: DCP Management 52

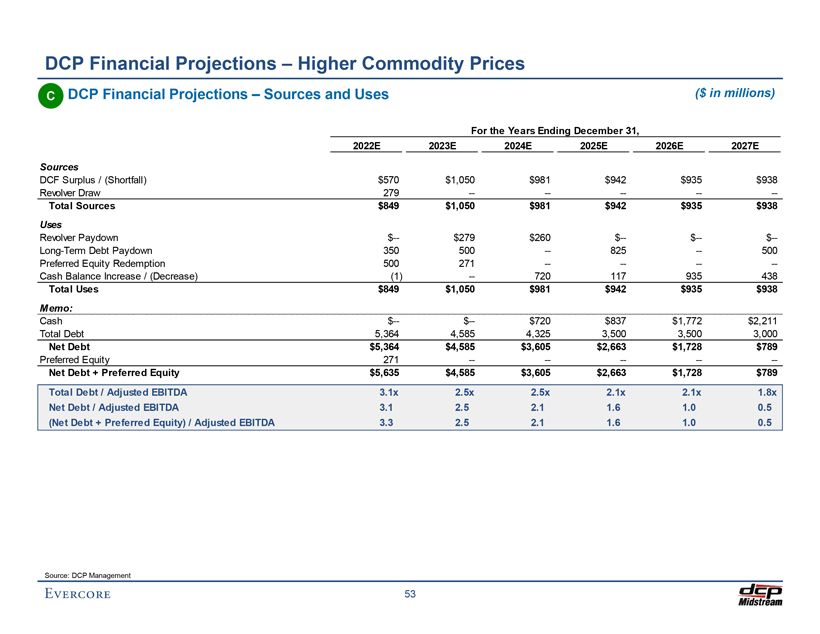

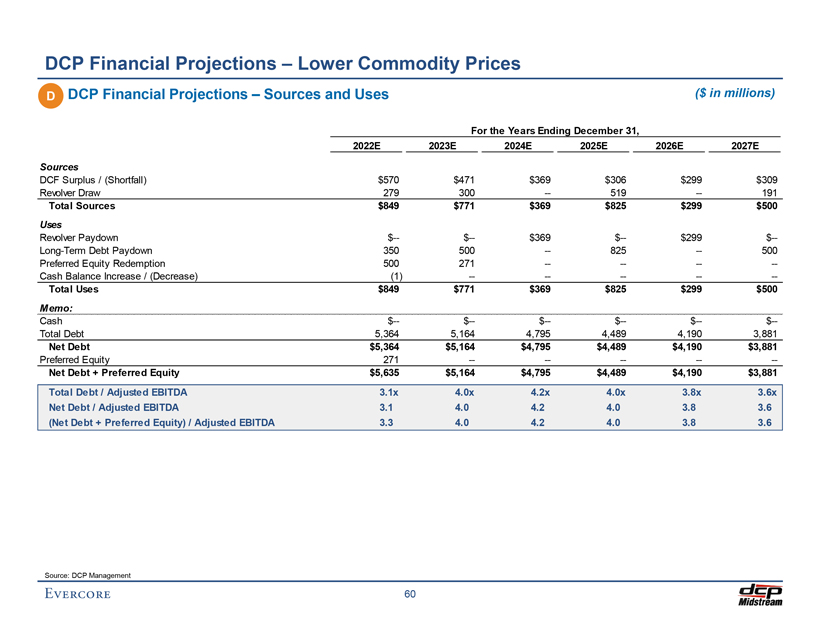

DCP Financial Projections – Higher Commodity Prices C DCP Financial Projections – Sources and Uses ($ in millions) For the Years Ending December 31, 2022E 2023E 2024E 2025E 2026E 2027E Sources DCF Surplus / (Shortfall) $570 $1,050 $981 $942 $935 $938 Revolver Draw 279 -————- Total Sources $849 $1,050 $981 $942 $935 $938 Uses Revolver Paydown $— $279 $260 $— $— $— Long-Term Debt Paydown 350 500 — 825 — 500 Preferred Equity Redemption 500 271 -———-Cash Balance Increase / (Decrease) (1) — 720 117 935 438 Total Uses $849 $1,050 $981 $942 $935 $938 Memo: Cash $— $— $720 $837 $1,772 $2,211 Total Debt 5,364 4,585 4,325 3,500 3,500 3,000 Net Debt $5,364 $4,585 $3,605 $2,663 $1,728 $789 Preferred Equity 271 -————- Net Debt + Preferred Equity $5,635 $4,585 $3,605 $2,663 $1,728 $789 Total Debt / Adjusted EBITDA 3.1x 2.5x 2.5x 2.1x 2.1x 1.8x Net Debt / Adjusted EBITDA 3.1 2.5 2.1 1.6 1.0 0.5 (Net Debt + Preferred Equity) / Adjusted EBITDA 3.3 2.5 2.1 1.6 1.0 0.5 Source: DCP Management 53

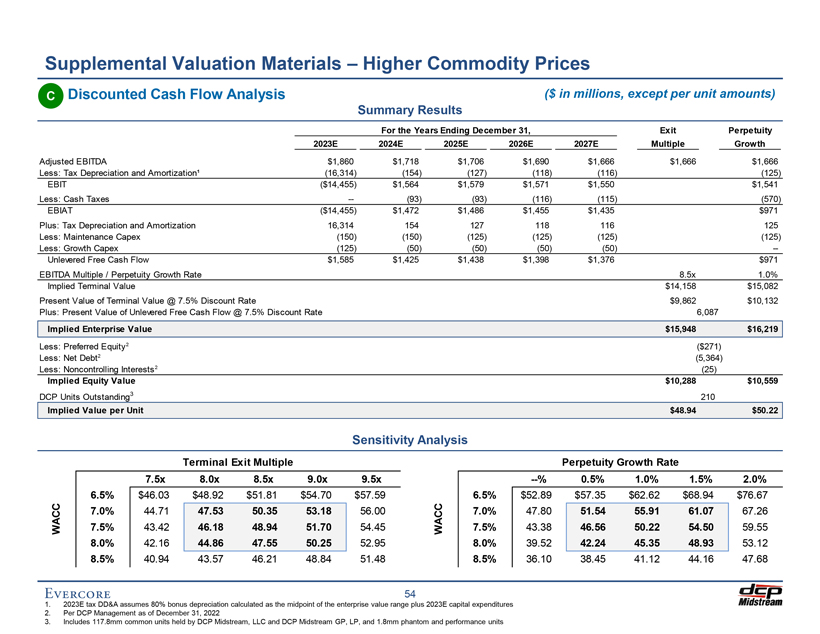

Supplemental Valuation Materials – Higher Commodity Prices C Discounted Cash Flow Analysis ($ in millions, except per unit amounts) Summary Results For the Years Ending December 31, Exit Perpetuity 2023E 2024E 2025E 2026E 2027E Multiple Growth Adjusted EBITDA $1,860 $1,718 $1,706 $1,690 $1,666 $1,666 $1,666 Less: Tax Depreciation and Amortization¹ (16,314) (154) (127) (118) (116) (125) EBIT ($14,455) $1,564 $1,579 $1,571 $1,550 $1,541 Less: Cash Taxes — (93) (93) (116) (115) (570) EBIAT ($14,455) $1,472 $1,486 $1,455 $1,435 $971 Plus: Tax Depreciation and Amortization 16,314 154 127 118 116 125 Less: Maintenance Capex (150) (150) (125) (125) (125) (125) Less: Growth Capex (125) (50) (50) (50) (50) —Unlevered Free Cash Flow $1,585 $1,425 $1,438 $1,398 $1,376 $971 EBITDA Multiple / Perpetuity Growth Rate 8.5x 1.0% Implied Terminal Value $14,158 $15,082 Present Value of Terminal Value @ 7.5% Discount Rate $9,862 $10,132 Plus: Present Value of Unlevered Free Cash Flow @ 7.5% Discount Rate 6,087 Implied Enterprise Value $15,948 $16,219 Less: Preferred Equity2 ($271) Less: Net Debt2 (5,364) Less: Noncontrolling Interests2 (25) Implied Equity Value $10,288 $10,559 DCP Units Outstanding3 210 Implied Value per Unit $48.94 $50.22 Sensitivity Analysis Terminal Exit Multiple Perpetuity Growth Rate 7.5x 8.0x 8.5x 9.0x 9.5x —% 0.5% 1.0% 1.5% 2.0% 6.5% $46.03 $48.92 $51.81 $54.70 $57.59 6.5% $52.89 $57.35 $62.62 $68.94 $76.67 C C 7.0% 44.71 47.53 50.35 53.18 56.00 C C 7.0% 47.80 51.54 55.91 61.07 67.26 WA 7.5% 43.42 46.18 48.94 51.70 54.45 WA 7.5% 43.38 46.56 50.22 54.50 59.55 8.0% 42.16 44.86 47.55 50.25 52.95 8.0% 39.52 42.24 45.35 48.93 53.12 8.5% 40.94 43.57 46.21 48.84 51.48 8.5% 36.10 38.45 41.12 44.16 47.68 54 1. 2023E tax DD&A assumes 80% bonus depreciation calculated as the midpoint of the enterprise value range plus 2023E capital expenditures 2. Per DCP Management as of December 31, 2022 3. Includes 117.8mm common units held by DCP Midstream, LLC and DCP Midstream GP, LP, and 1.8mm phantom and performance units