There are royalties attached to the mineral concessions, however, the only royalties that affect the Mineral Reserves and have been considered in the economic analysis are:

| · | A 2 % royalty on silver production to Nueva Granada Gold Ltd. (formerly Lemuria Royalties Corp.). |

| · | A 1 % royalty or an effective rate based on operating profit (whichever is greater) to the Peruvian Government has been taken into account in predicting cash flows. |

| · | A Special Tax on Mining based on the quarterly operating profit of the mining concession holder. |

The earliest documented mining activity in the Caylloma District dates back to that of Spanish miners in 1620. English miners carried out activities in the late 1800s and early 1900s. Numerous companies have been involved in mining the district of Caylloma but limited records are available to detail these activities.

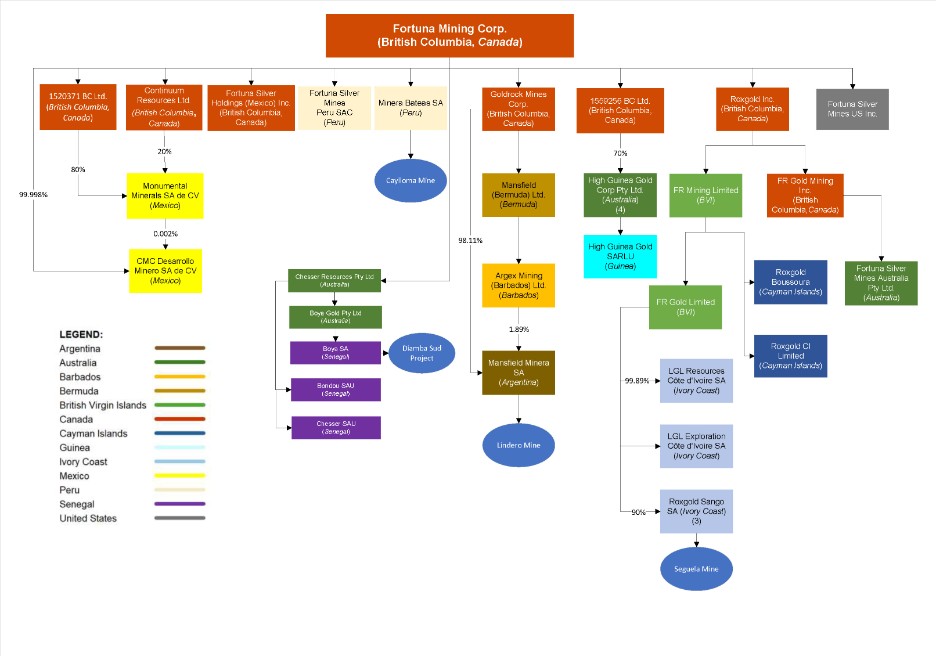

The Caylloma Mine was acquired by Compania Minera Arcata S.A. (CMA), a wholly owned subsidiary of Hochschild Mining plc in 1981. Fortuna acquired the mine from CMA in 2005.

CMA focused exploration on identifying high-grade silver vein structures. Exploration was concentrated in the northern portion of the district and focused on veins including Bateas, El Toro, Paralela, San Pedro, San Cristobal, San Carlos, Don Luis, La Plata, and Apostles.

Production prior to 2005 came primarily from the San Cristobal vein, as well as from the Bateas, Santa Catalina and the northern silver veins (including Paralela, San Pedro, and San Carlos) with production focused on silver ores and no payable credits for base metals. While under CMA management production parameters fluctuated during the late 1990s, as reserves were depleted. Owing to low metal prices, funds were not available to develop the Mineral Resources at depth or extend along the strike of the veins. Ultimately this resulted in production being halted in 2002.

Production under Bateas management focused on the development of polymetallic veins producing lead and zinc concentrates with silver and gold credits. Total production since October 2006 through December 31, 2023, is estimated at 23.4 Moz of silver, 36 koz of gold, 193 kt of lead, and 272 kt of zinc.

1.5 | Geology and mineralization |

The mine is within the historical mining district of Caylloma, northwest of the Caylloma caldera complex and southwest of the Chonta caldera complex. Host rocks at the Caylloma Mine are volcanic in nature, belonging to the Tacaza Group. Mineralization is in the form of low to intermediate sulfidation epithermal vein systems.

Epithermal veins at the Caylloma Mine are characterized by minerals such as pyrite, sphalerite, galena, chalcopyrite, marcasite, native gold, stibnite, argentopyrite, and silver-bearing sulfosalts (tetrahedrite, polybasite, pyrargyrite, stephanite, stromeyerite, jalpite, miargyrite and bournonite). These are accompanied by gangue minerals, such as quartz, rhodonite, rhodochrosite, johannsenite (manganese-pyroxene) and calcite.

There are two different types of mineralization at Caylloma; the first is comprised of silver-rich veins with low concentrations of base metals and includes the Bateas, Bateas Piso, Bateas Techo, La Plata, Cimoide La Plata, San Cristobal, Pilar, Patricia, San Pedro, San Carlos, Paralela, Ramal Piso Carolina, and Don Luis II veins. The second type of vein is polymetallic in nature with elevated lead, zinc, copper, silver and gold grades and includes the Animas, Animas NE, Comoide ASNE, Ramal Techo ASNE, Rosita, Nancy Santa Catalina, Silvia and Soledad veins.

Underground operations are presently focused on mining the Animas, Animas NE, Nancy and associated splay veins.

1.6 | Exploration, drilling and sampling |

CMA implemented a series of exploration programs to complement their mining activities prior to the closure of the operation in 2002. There is no reliable information available to detail the exploration conducted by CMA at the Caylloma Mine. Bateas were able to recover and validate information on 47 diamond drill holes totaling 8,177.67 m drilled by CMA between 1981 and 2003 at the Caylloma Mine.

Since Fortuna took ownership of the property in 2005, the principal exploration conducted at the deposit has been surface and underground drilling, to explore the numerous vein structures identified through surface mapping or geophysical surveys conducted by Bateas, or for infill purposes to increase the confidence level of the Mineral Resource estimates.