OTC: EXXIQ www.energyxxi.com September 21, 2016 Project Bluewater Creditor Presentation Confidential; Do Not Distribute Subject to Material Revision

Confidential; Do Not Distribute Subject to Material Revision Disclaimer This document contains highly confidential information and is solely for informational purposes. You should not rely upon or use it to form the definitive basis for any decision or action whatsoever, with respect to any proposed transaction or otherwise. You and your affiliates and agents must hold this document and any oral information provided in connection with this document, as well as any information derived by you from the information contained herein, in strict con fid ence and may not communicate, reproduce or disclose it to any other person, or refer to it publicly, in whole or in part at any time except with our prior written conse nt. If you are not the intended recipient of this document, please delete and destroy all copies immediately. This document is “as is” and is based, in part, on information obtained from other sources. Our use of such information does not imply that we have independently verified or necessarily agree with any of such information, and we have assumed and relied upon the accuracy and completeness of such inf orm ation for purposes of this document. Neither we nor any of our affiliates or agents, make any representation or warranty, express or implied, in relation to the accuracy or completeness of the information contained in this document or any oral information provided in connection herewith, or any data it generates and expressly disclaim any and all li ability (whether direct or indirect, in contract, tort or otherwise) in relation to any of such information or any errors or omissions therein. Any views or terms contained herein are pr eliminary, and are based on financial, economic, market and other conditions prevailing as of the date of this document and are subject to change. We undertake no obligations or responsibility to update any of the information contained in this document. Past performance does not guarantee or predict future performance. This document does not constitute an offer to sell or the solicitation of an offer to buy any security, nor does it constitut e a n offer or commitment to lend, syndicate or arrange a financing, underwrite or purchase or act as an agent or advisor or in any other capacity with respect to any transaction, or commit capital, or to participate in any trading strategies, and does not constitute legal, regulatory, accounting or tax adv ice to the recipient. This document does not constitute and should not be considered as any form of financial opinion or recommendation by us or any of our affiliates. This document is not a research report nor should it be construed as such. This document may include information from the S&P Capital IQ Platform Service. Such information is subject to the following: “C opyright © 2015, S&P Capital IQ (and its affiliates, as applicable). This may contain information obtained from third parties, including ratings from credit ratings a gen cies such as Standard & Poor’s. Reproduction and distribution of third party content in any form is prohibited except with the prior written permission of the related third p art y. Third party content providers do not guarantee the accuracy, completeness, timeliness or availability of any information, including ratings, and are not responsible for any err ors or omissions (negligent or otherwise), regardless of the cause, or for the results obtained from the use of such content. THIRD PARTY CONTENT PROVIDERS GIVE NO EXPRESS OR IMPLIED WA RRANTIES, INCLUDING, BUT NOT LIMITED TO, ANY WARRANTIES OF MERCHANTABILITY OR FITNESS FOR A PARTICULAR PURPOSE OR USE. THIRD PARTY CONTENT PROVIDERS S HAL L NOT BE LIABLE FOR ANY DIRECT, INDIRECT, INCIDENTAL, EXEMPLARY, COMPENSATORY, PUNITIVE, SPECIAL OR CONSEQUENTIAL DAMAGES, COSTS, E XPE NSES, LEGAL FEES, OR LOSSES (INCLUDING LOST INCOME OR PROFITS AND OPPORTUNITY COSTS OR LOSSES CAUSED BY NEGLIGENCE) IN CONNECTION W ITH ANY USE OF THEIR CONTENT, INCLUDING RATINGS. Credit ratings are statements of opinions and are not statements of fact or recommen dat ions to purchase, hold or sell securities. They do not address the suitability of securities or the suitability of securities for investment purposes, and s hou ld not be relied on as investment advice.” 2

Confidential; Do Not Distribute Subject to Material Revision 3 Table of Contents Discussion Topics Page I Company Overview 4 II Operations 8 III BOEM Update 15 IV Midstream 19 V Reserves 21 VI Recompletions 26 VII Major Fields 30 VIII Exploration Potential 44 IX Financials & Forecast 47

Confidential; Do Not Distribute Subject to Material Revision I. COMPANY OVERVIEW

Confidential; Do Not Distribute Subject to Material Revision Company History 5 August 2015 Acquired equity interests of M21K for $25MM October 2005 Successfully competed $300MM IPO on the London AIM June 2005 Company formation April 2006 Acquired Marlin Energy Offshore, LLC for $448MM June 2006 Acquired South Louisiana properties for $311MM April 2007 Acquired POGO’s GoM assets for $415MM August 2007 NASDAQ listing (Ticker: EXXI) December 2010 Acquired ExxonMobil GoM Shelf properties for $1.01BN September 2012 Implemented horizontal drilling program in the West Delta 73 Field January 2013 Acquired Bayou Carlin Onshore S. Louisiana for $80MM January 2014 Lomond North – Tuscaloosa Discovery March 2014 Acquired EPL Oil & Gas for $2.3BN June 2015 Grand Isle Gathering System closed for $245MM June 2015 Sale of the East Bay Field closed November 2009 Acquired Mit Energy assets for $276MM

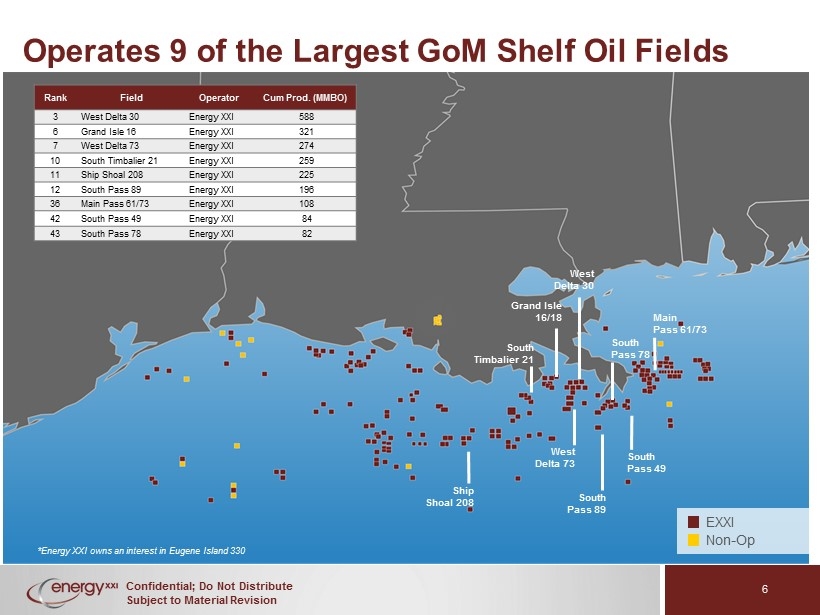

Confidential; Do Not Distribute Subject to Material Revision Grand Isle 16/18 West Delta 30 South Timbalier 21 West Delta 73 South Pass 49 South Pass 78 Ship Shoal 208 South Pass 89 EXXI Non - Op *Energy XXI owns an interest in Eugene Island 330 Main Pass 61/73 6 Rank Field Operator Cum Prod. (MMBO) 3 West Delta 30 Energy XXI 588 6 Grand Isle 16 Energy XXI 321 7 West Delta 73 Energy XXI 274 10 South Timbalier 21 Energy XXI 259 11 Ship Shoal 208 Energy XXI 225 12 South Pass 89 Energy XXI 196 36 Main Pass 61/73 Energy XXI 108 42 South Pass 49 Energy XXI 84 43 South Pass 78 Energy XXI 82 Operates 9 of the Largest GoM Shelf Oil Fields

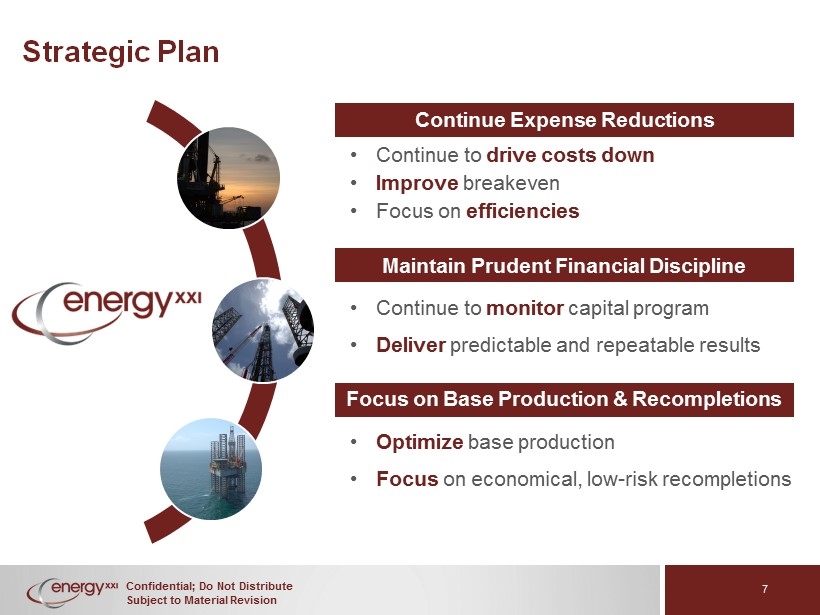

Confidential; Do Not Distribute Subject to Material Revision Strategic Plan • Continue to monitor capital program • Deliver predictable and repeatable results Maintain Prudent Financial Discipline Continue Expense Reductions • Continue to drive costs down • I mprove breakeven • Focus on efficiencies Focus on Base Production & Recompletions • Optimize base production • Focus on economical, low - risk recompletions 7

Confidential; Do Not Distribute Subject to Material Revision II. OPERATIONS

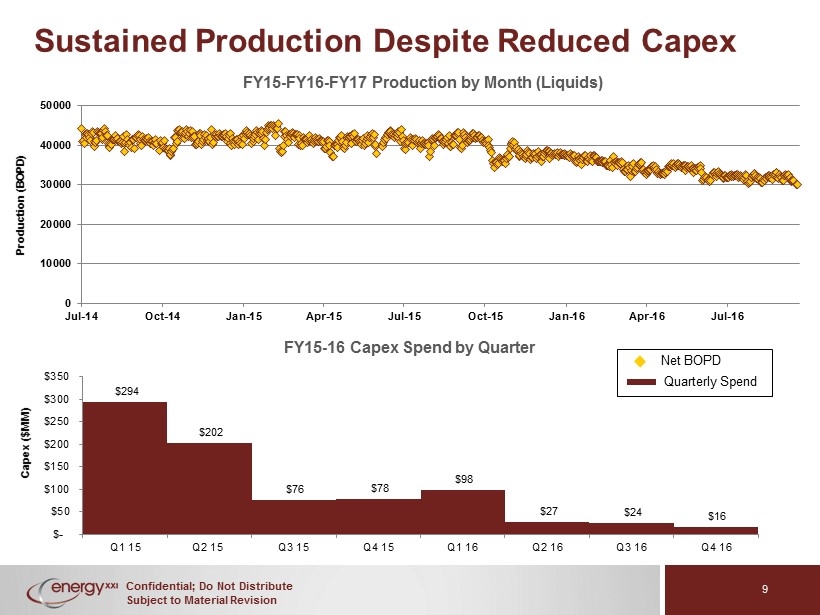

Confidential; Do Not Distribute Subject to Material Revision Net BOPD Quarterly Spend 9 Sustained Production Despite Reduced Capex $294 $202 $76 $78 $98 $27 $24 $16 $- $50 $100 $150 $200 $250 $300 $350 Q1 15 Q2 15 Q3 15 Q4 15 Q1 16 Q2 16 Q3 16 Q4 16 Capex ($MM) FY15 - 16 Capex Spend by Quarter 0 10000 20000 30000 40000 50000 Jul-14 Oct-14 Jan-15 Apr-15 Jul-15 Oct-15 Jan-16 Apr-16 Jul-16 Production (BOPD) FY15 - FY16 - FY17 Production by Month (Liquids)

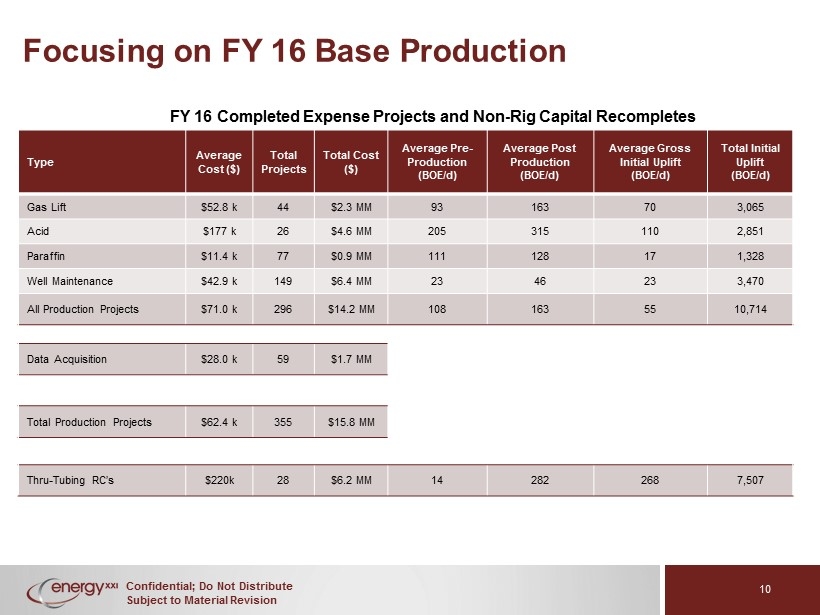

Confidential; Do Not Distribute Subject to Material Revision Focusing on FY 16 Base Production 10 Type Average Cost ($) Total Projects Total Cost ($) Average Pre - Production (BOE/d) Average Pos t Production (BOE/d) Average Gross Initial Uplift (BOE/d) Total Initial Uplift (BOE/d) Gas Lift $52.8 k 44 $2.3 MM 93 163 70 3,065 Acid $177 k 26 $4.6 MM 205 315 110 2,851 Paraffin $11.4 k 77 $0.9 MM 111 128 17 1,328 Well Maintenance $42.9 k 149 $6.4 MM 23 46 23 3,470 All Production Projects $71.0 k 296 $14.2 MM 108 163 55 10,714 Data Acquisition $28.0 k 59 $1.7 MM Total Production Projects $62.4 k 355 $15.8 MM Thru - Tubing RC’s $220k 28 $6.2 MM 14 282 268 7,507 FY 16 Completed Expense Projects and Non - Rig Capital Recompletes

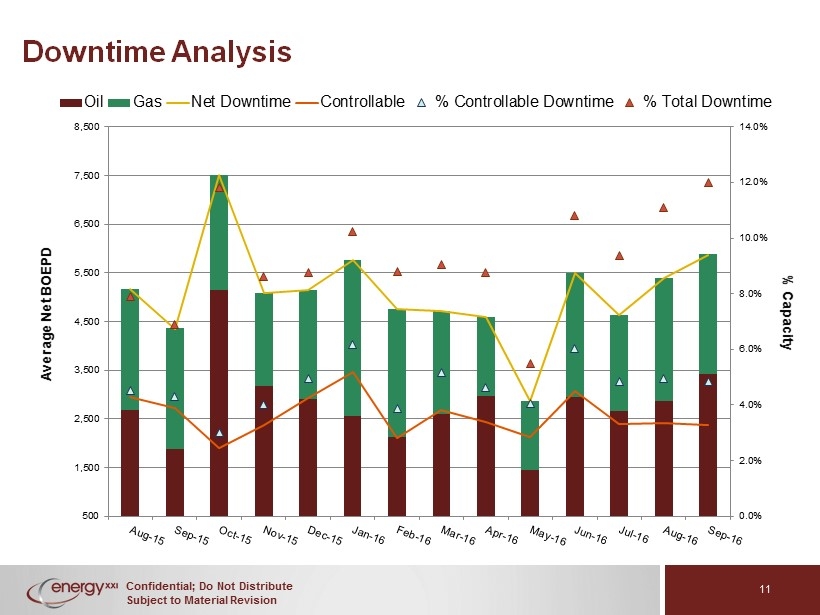

Confidential; Do Not Distribute Subject to Material Revision Downtime Analysis 11 0.0% 2.0% 4.0% 6.0% 8.0% 10.0% 12.0% 14.0% 500 1,500 2,500 3,500 4,500 5,500 6,500 7,500 8,500 % Capacity Average Net BOEPD Oil Gas Net Downtime Controllable % Controllable Downtime % Total Downtime

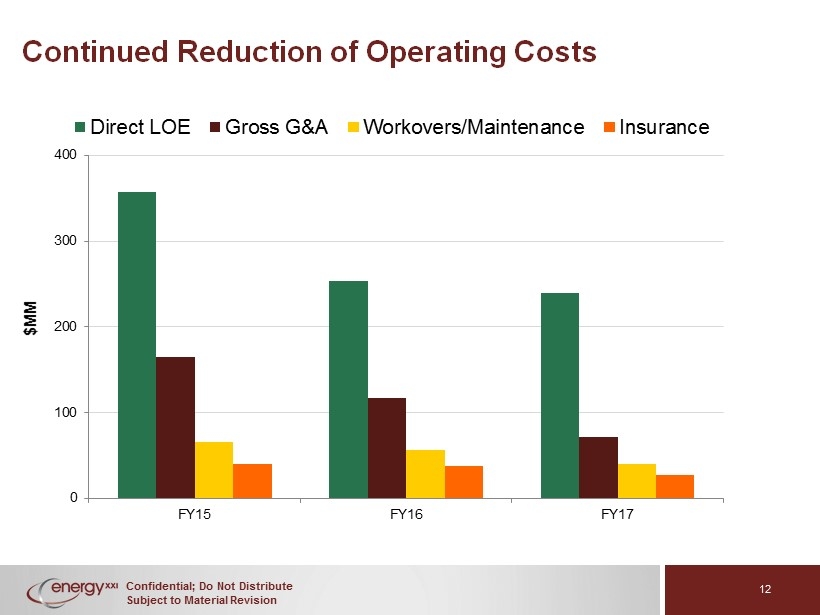

Confidential; Do Not Distribute Subject to Material Revision Continued Reduction of Operating Costs 12 0 100 200 300 400 FY15 FY16 FY17 $MM Direct LOE Gross G&A Workovers/Maintenance Insurance

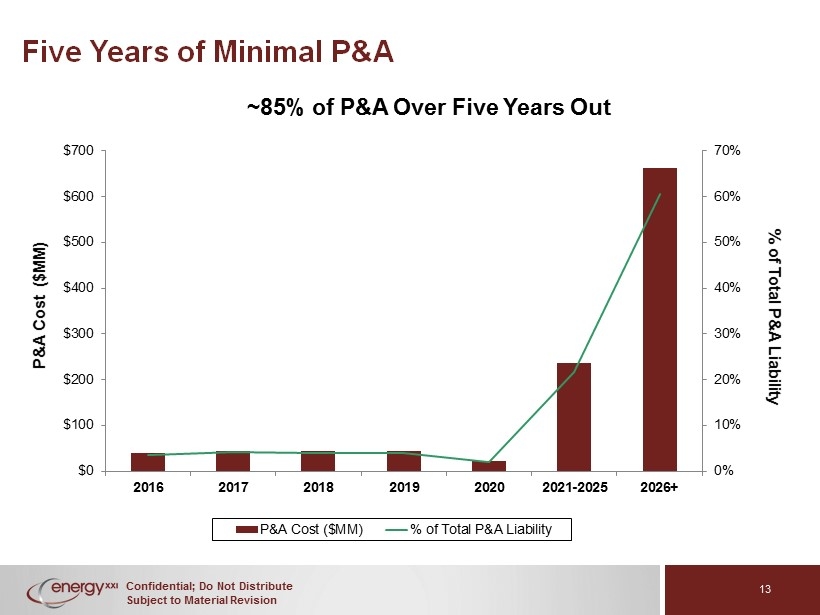

Confidential; Do Not Distribute Subject to Material Revision Five Years of Minimal P&A 0% 10% 20% 30% 40% 50% 60% 70% $0 $100 $200 $300 $400 $500 $600 $700 2016 2017 2018 2019 2020 2021-2025 2026+ % of Total P&A Liability P&A Cost ($MM) P&A Cost ($MM) % of Total P&A Liability ~85% of P&A Over Five Years Out 13

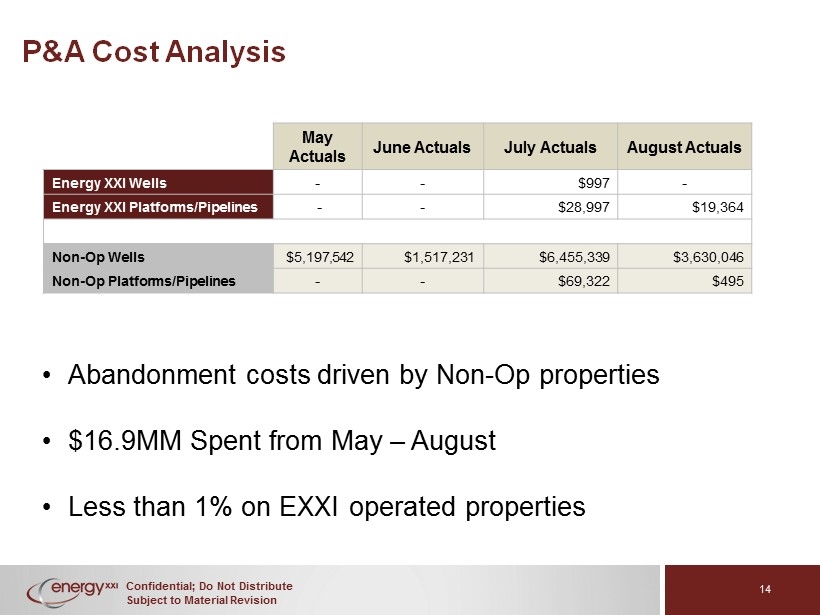

Confidential; Do Not Distribute Subject to Material Revision P&A Cost Analysis 14 May Actuals June Actuals July Actuals August Actuals Energy XXI Wells - - $997 - Energy XXI Platforms/Pipelines - - $28,997 $19,364 Non - Op Wells $5,197,542 $1,517,231 $ 6,455,339 $3,630,046 Non - Op Platforms/Pipelines - - $69,322 $495 • Abandonment costs driven by Non - Op properties • $16.9MM Spent from May – August • Less than 1% on EXXI operated properties

Confidential; Do Not Distribute Subject to Material Revision III. BOEM UPDATE

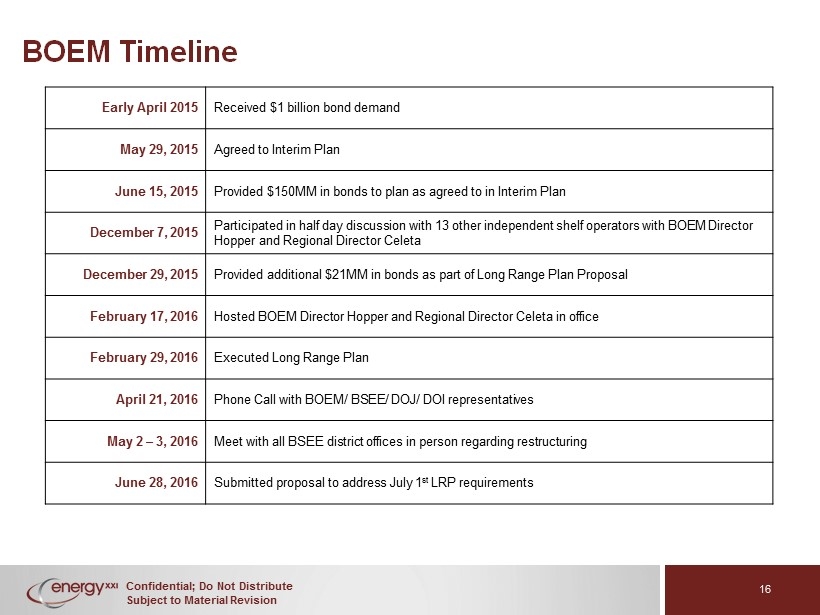

Confidential; Do Not Distribute Subject to Material Revision BOEM Timeline Early April 2015 Received $1 billion bond demand May 29, 2015 Agreed to Interim Plan June 15, 2015 Provided $150MM in bonds to plan as agreed to in Interim Plan December 7, 2015 Participated in half day discussion with 13 other independent shelf operators with BOEM Director Hopper and Regional Director Celeta December 29, 2015 Provided additional $21MM in bonds as part of Long Range Plan Proposal February 17, 2016 Hosted BOEM Director Hopper and Regional Director Celeta in office February 29, 2016 Executed Long Range Plan April 21, 2016 Phone Call with BOEM/ BSEE/ DOJ/ DOI representatives May 2 – 3, 2016 Meet with all BSEE district offices in person regarding restructuring June 28, 2016 Submitted proposal to address July 1 st LRP requirements 16

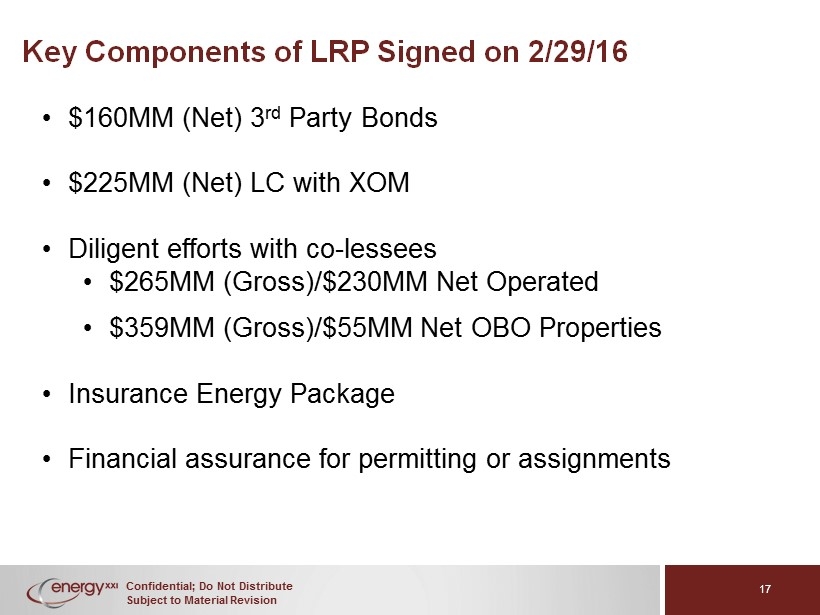

Confidential; Do Not Distribute Subject to Material Revision Key Components of LRP Signed on 2/29/16 • $ 160MM (Net) 3 rd Party Bonds • $ 225MM (Net) LC with XOM • Diligent efforts with co - lessees • $265MM (Gross)/$230MM Net Operated • $359MM (Gross)/$55MM Net OBO Properties • Insurance Energy Package • Financial assurance for permitting or assignments 17 17

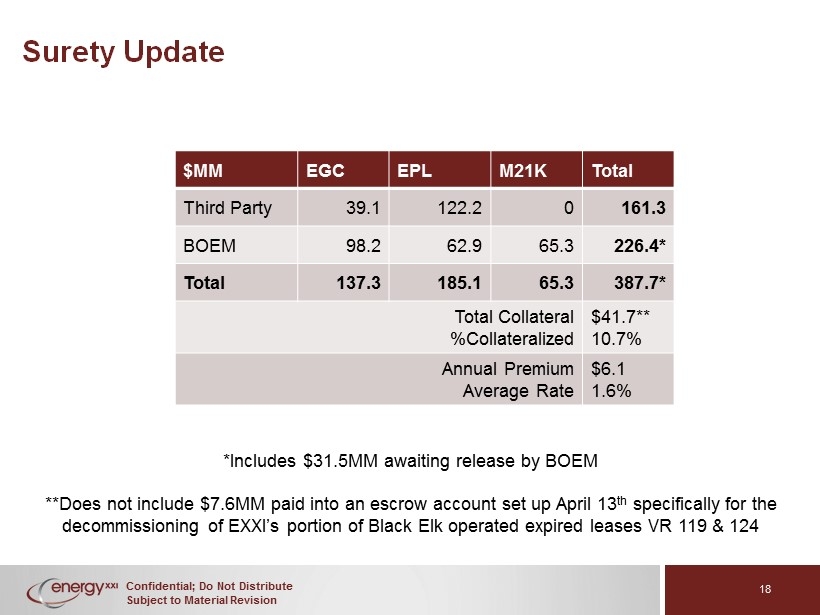

Confidential; Do Not Distribute Subject to Material Revision Surety Update $MM EGC EPL M21K Total Third Party 39.1 122.2 0 161.3 BOEM 98.2 62.9 65.3 226.4* Total 137.3 185.1 65.3 387.7* Total Collateral %Collateralized $41.7** 10.7% Annual Premium Average Rate $6.1 1.6% 18 *Includes $31.5MM awaiting release by BOEM **Does not include $7.6MM paid into an escrow account set up April 13 th specifically for the decommissioning of EXXI’s portion of Black Elk operated expired leases VR 119 & 124

Confidential; Do Not Distribute Subject to Material Revision IV. MIDSTREAM

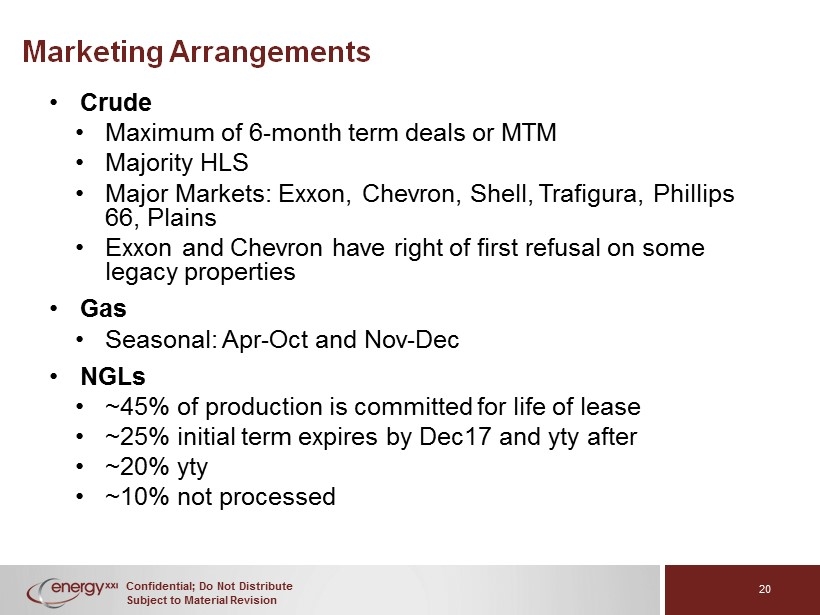

Confidential; Do Not Distribute Subject to Material Revision Marketing Arrangements • Crude • Maximum of 6 - month term deals or MTM • Majority HLS • Major Markets: Exxon, Chevron, Shell, Trafigura, Phillips 66, Plains • Exxon and Chevron have right of first refusal on some legacy properties • Gas • Seasonal: Apr - Oct and Nov - Dec • NGLs • ~45% of production is committed for life of lease • ~25% initial term expires by Dec17 and yty after • ~20% yty • ~10% not processed 20

Confidential; Do Not Distribute Subject to Material Revision V. RESERVES

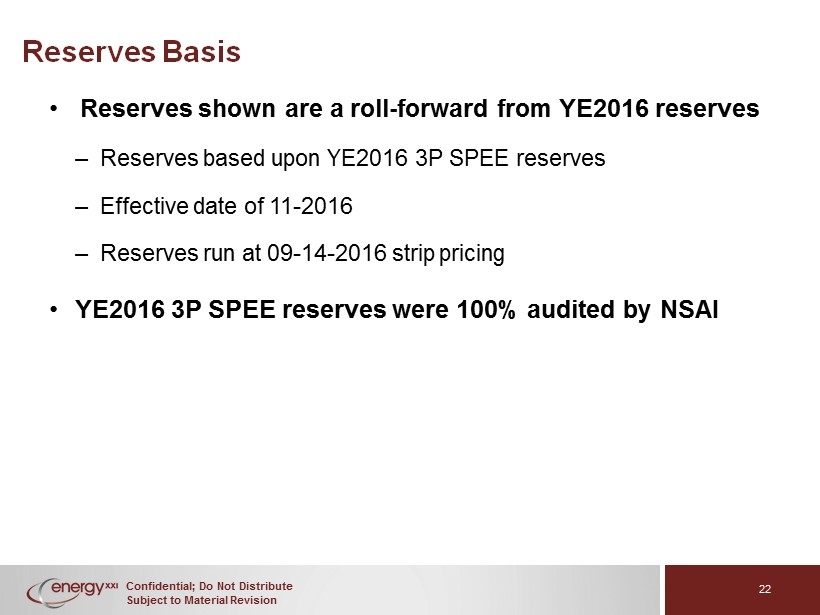

Confidential; Do Not Distribute Subject to Material Revision Reserves Basis • Reserves shown are a roll - forward from YE2016 reserves – Reserves based upon YE2016 3P SPEE reserves – Effective date of 11 - 2016 – Reserves run at 09 - 14 - 2016 strip pricing • YE2016 3P SPEE reserves were 100% audited by NSAI 22

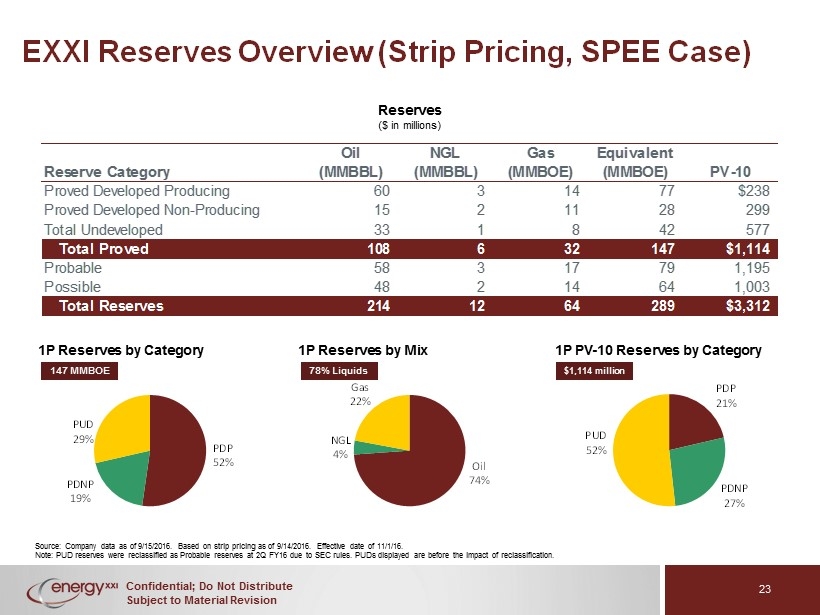

Confidential; Do Not Distribute Subject to Material Revision EXXI Reserves Overview (Strip Pricing, SPEE Case) Source: Company data as of 9/15/2016 . Based on strip pricing as of 9/14/2016 . Effective date of 11/1/16. Note: PUD reserves were reclassified as Probable reserves at 2Q FY16 due to SEC rules. PUDs displayed are before the impact of reclassification. 1P Reserves by Mix 1P PV - 10 Reserves by Category $1,114 million 1P Reserves by Category PDP 52% PDNP 19% PUD 29% Oil 74% NGL 4% Gas 22% PDP 21% PDNP 27% PUD 52% Reserves ($ in millions) 78% Liquids 147 MMBOE Oil NGL Gas Equivalent Reserve Category (MMBBL) (MMBBL) (MMBOE) (MMBOE) PV-10 Proved Developed Producing 60 3 14 77 $238 Proved Developed Non-Producing 15 2 11 28 299 Total Undeveloped 33 1 8 42 577 Total Proved 108 6 32 147 $1,114 Probable 58 3 17 79 1,195 Possible 48 2 14 64 1,003 Total Reserves 214 12 64 289 $3,312 23

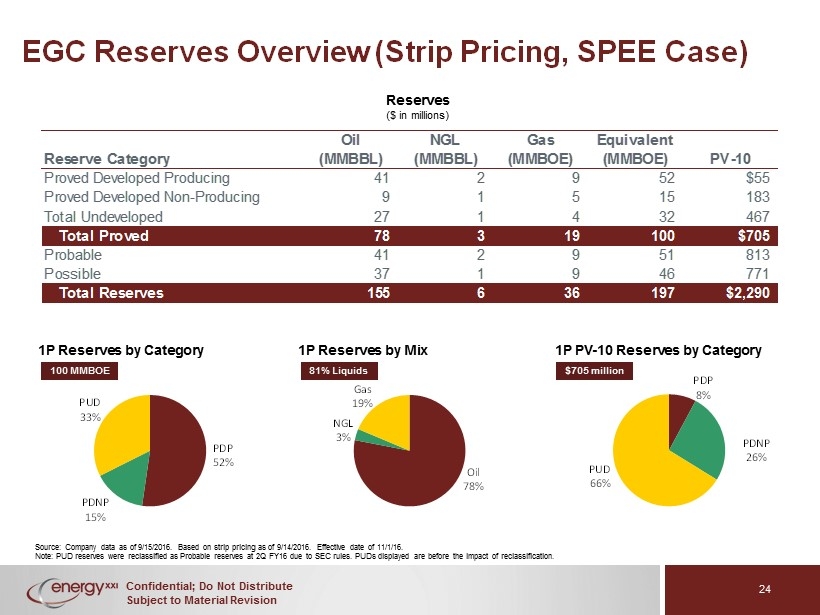

Confidential; Do Not Distribute Subject to Material Revision EGC Reserves Overview ( Strip Pricing, SPEE Case) PDP 52% PDNP 15% PUD 33% Oil 78% NGL 3% Gas 19% PDP 8% PDNP 26% PUD 66% 1P Reserves by Mix 1P PV - 10 Reserves by Category $705 million 1P Reserves by Category Reserves ($ in millions) 81% Liquids 100 MMBOE Source: Company data as of 9/15/2016. Based on strip pricing as of 9/14/2016. Effective date of 11/1/16. Note : PUD reserves were reclassified as Probable reserves at 2Q FY16 due to SEC rules. PUDs displayed are before the impact of re cla ssification. Oil NGL Gas Equivalent Reserve Category (MMBBL) (MMBBL) (MMBOE) (MMBOE) PV-10 Proved Developed Producing 41 2 9 52 $55 Proved Developed Non-Producing 9 1 5 15 183 Total Undeveloped 27 1 4 32 467 Total Proved 78 3 19 100 $705 Probable 41 2 9 51 813 Possible 37 1 9 46 771 Total Reserves 155 6 36 197 $2,290 24

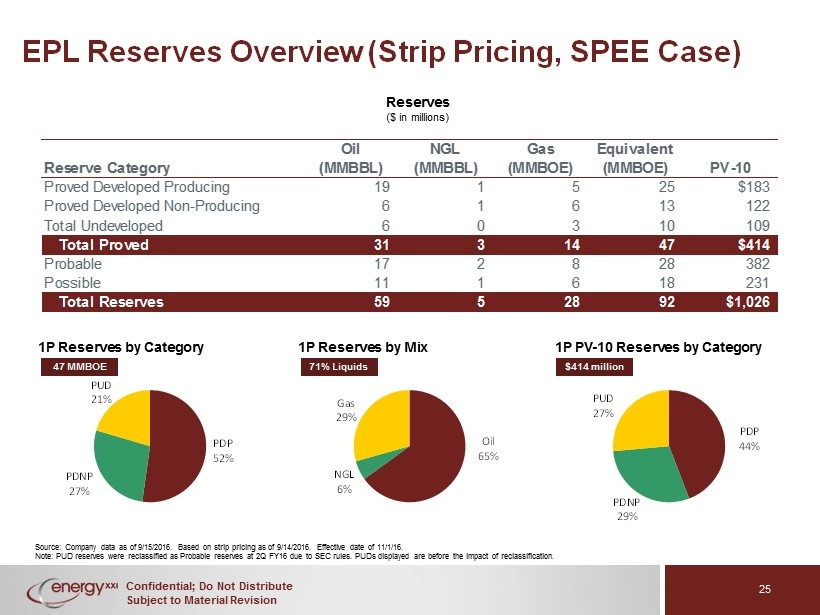

Confidential; Do Not Distribute Subject to Material Revision PDP 44% PDNP 29% PUD 27% EPL Reserves Overview (Strip Pricing, SPEE Case) PDP 52% PDNP 27% PUD 21% Oil 65% NGL 6% Gas 29% Reserves ($ in millions) 71% Liquids 47 MMBOE 1P Reserves by Mix 1P PV - 10 Reserves by Category $414 million 1P Reserves by Category Source: Company data as of 9/15/2016. Based on strip pricing as of 9/14/2016. Effective date of 11/1/16. Note : PUD reserves were reclassified as Probable reserves at 2Q FY16 due to SEC rules. PUDs displayed are before the impact of re cla ssification. Oil NGL Gas Equivalent Reserve Category (MMBBL) (MMBBL) (MMBOE) (MMBOE) PV-10 Proved Developed Producing 19 1 5 25 $183 Proved Developed Non-Producing 6 1 6 13 122 Total Undeveloped 6 0 3 10 109 Total Proved 31 3 14 47 $414 Probable 17 2 8 28 382 Possible 11 1 6 18 231 Total Reserves 59 5 28 92 $1,026 25

Confidential; Do Not Distribute Subject to Material Revision VI. RECOMPLETIONS

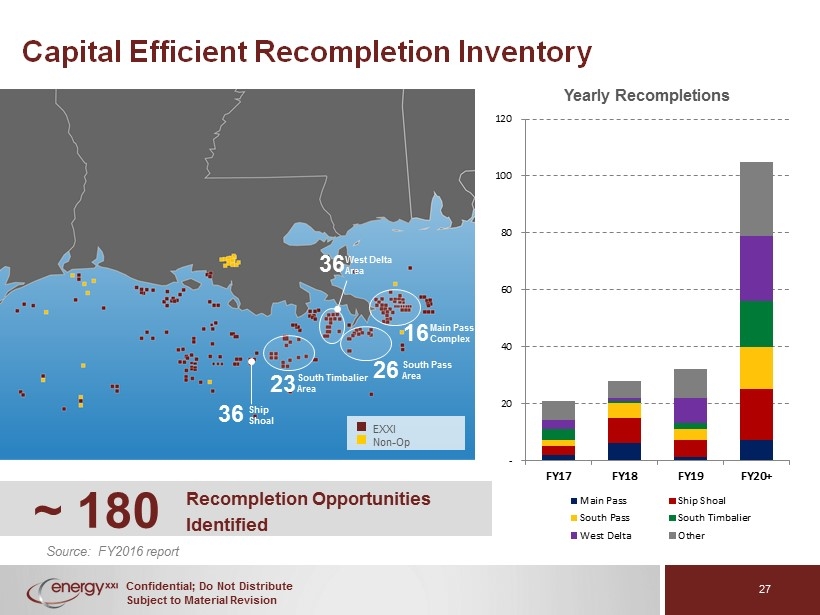

Confidential; Do Not Distribute Subject to Material Revision ~ 180 Recompletion Opportunities Identified Yearly Recompletions West Delta Area South Pass Area South Timbalier Area EXXI Non - Op Main Pass Complex 16 26 36 23 36 Ship Shoal Capital Efficient Recompletion Inventory - 20 40 60 80 100 120 FY17 FY18 FY19 FY20+ Main Pass Ship Shoal South Pass South Timbalier West Delta Other Source: FY2016 report 27

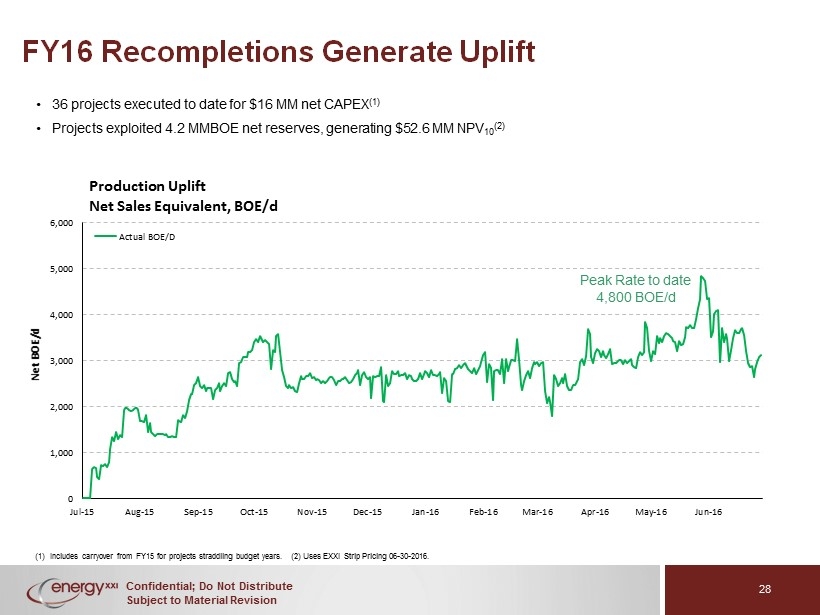

Confidential; Do Not Distribute Subject to Material Revision FY16 Recompletions Generate Uplift • 36 projects executed to date for $16 MM net CAPEX (1) • Projects exploited 4.2 MMBOE net reserves, generating $52.6 MM NPV 10 (2) 0 1,000 2,000 3,000 4,000 5,000 6,000 Jul-15 Aug-15 Sep-15 Oct-15 Nov-15 Dec-15 Jan-16 Feb-16 Mar-16 Apr-16 May-16 Jun-16 Net BOE/d Production Uplift Net Sales Equivalent, BOE/d Actual BOE/D Peak Rate to date 4,800 BOE/d (1) Includes carryover from FY15 for projects straddling budget years . (2) Uses EXXI Strip Pricing 06 - 30 - 2016. 28

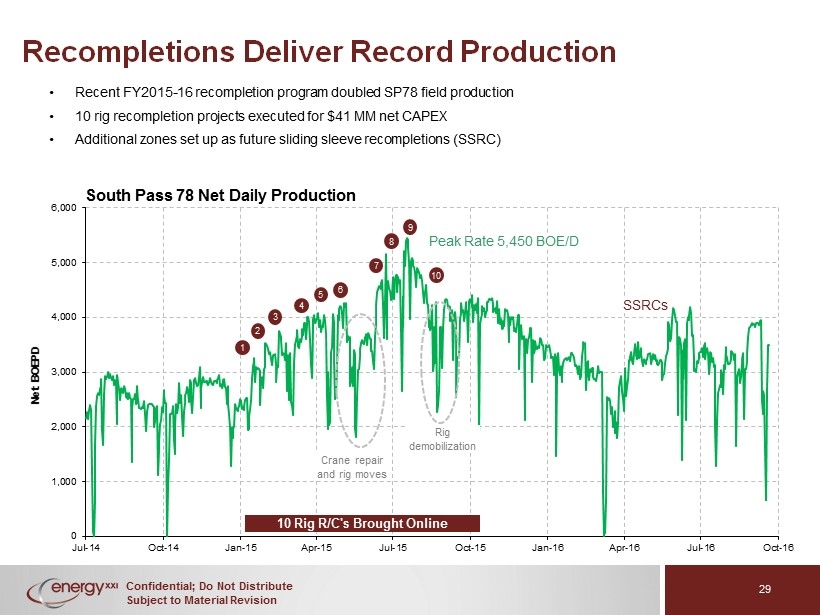

Confidential; Do Not Distribute Subject to Material Revision Recompletions Deliver Record Production • Recent FY2015 - 16 recompletion program doubled SP78 field production • 10 rig recompletion projects executed for $41 MM net CAPEX • Additional zones set up as future sliding sleeve recompletions (SSRC) 0 1,000 2,000 3,000 4,000 5,000 6,000 Jul-14 Oct-14 Jan-15 Apr-15 Jul-15 Oct-15 Jan-16 Apr-16 Jul-16 Oct-16 Net BOEPD South Pass 78 Net Daily Production Peak Rate 5,450 BOE/D 10 Rig R/C's Brought Online SSRCs 1 2 8 7 6 5 4 3 9 Crane repair and rig moves Rig demobilization 10 29

Confidential; Do Not Distribute Subject to Material Revision VII. MAJOR FIELDS

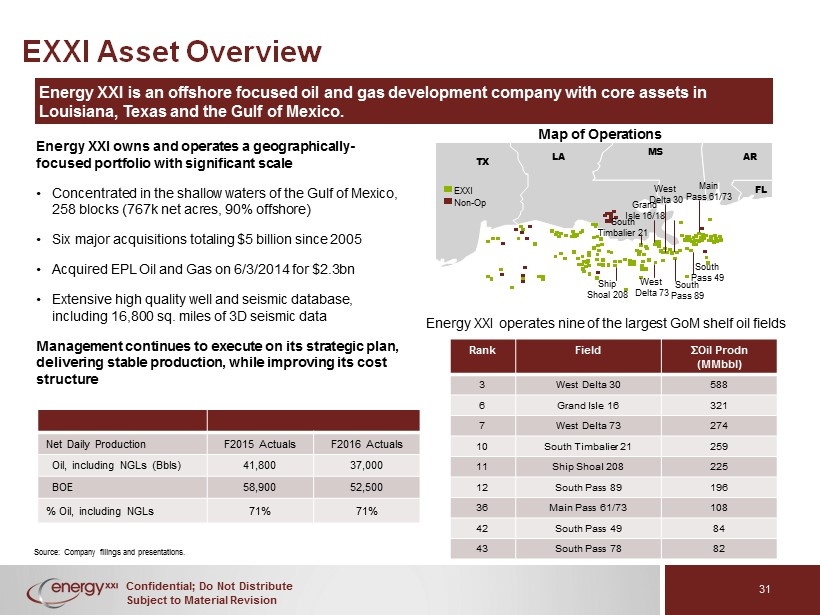

Confidential; Do Not Distribute Subject to Material Revision EXXI Asset Overview Energy XXI is an offshore focused oil and gas development company with core assets in Louisiana, Texas and the Gulf of Mexico . Energy XXI owns and operates a geographically - focused portfolio with significant scale • Concentrated in the shallow waters of the Gulf of Mexico, 258 blocks (767k net acres, 90% offshore) • Six major acquisitions totaling $5 billion since 2005 • Acquired EPL Oil and Gas on 6/3/2014 for $2.3bn • Extensive high quality well and seismic database, including 16,800 sq. miles of 3D seismic data Management continues to execute on its strategic plan, delivering stable production, while improving its cost structure Map of Operations Energy XXI operates nine of the largest GoM shelf oil fields TX LA MS AR FL EXXI Non - Op South Timbalier 21 West Delta 30 Grand Isle 16/18 South Pass 89 Main Pass 61/73 South Pass 49 West Delta 73 Ship Shoal 208 Source: Company filings and presentations . Net Daily Production F2015 Actuals F2016 Actuals Oil, including NGLs (Bbls) 41,800 37,000 BOE 58,900 52,500 % Oil, including NGLs 71% 71% Rank Field S Oil Prodn (MMbbl) 3 West Delta 30 588 6 Grand Isle 16 321 7 West Delta 73 274 10 South Timbalier 21 259 11 Ship Shoal 208 225 12 South Pass 89 196 36 Main Pass 61/73 108 42 South Pass 49 84 43 South Pass 78 82 31

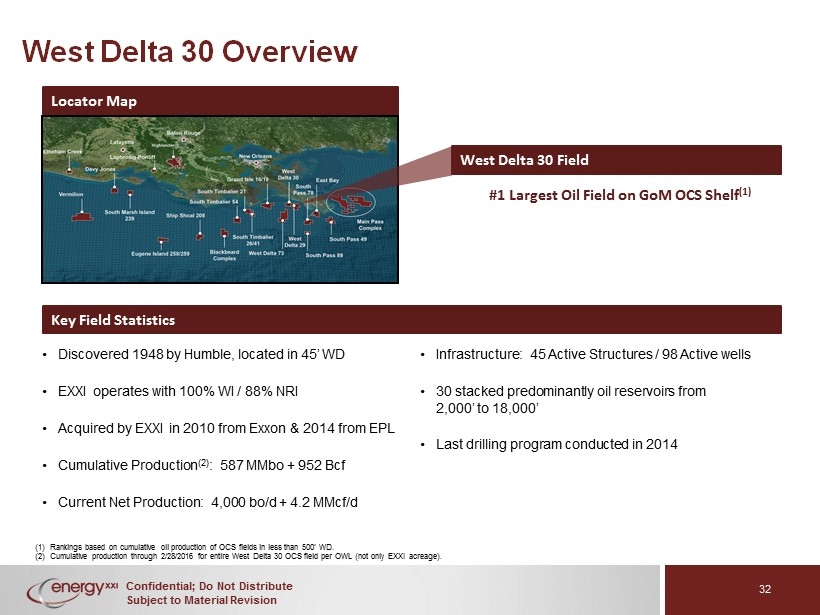

Confidential; Do Not Distribute Subject to Material Revision West Delta 30 Overview (1) Rankings based on cumulative oil production of OCS fields in less than 500’ WD. (2) Cumulative production through 2/28/2016 for entire West Delta 30 OCS field per OWL (not only EXXI acreage). • Discovered 1948 by Humble, located in 45’ WD • EXXI operates with 100% WI / 88% NRI • Acquired by EXXI in 2010 from Exxon & 2014 from EPL • Cumulative Production (2) : 587 MMbo + 952 Bcf • Current Net Production: 4,000 bo/d + 4.2 MMcf/d • Infrastructure: 45 Active Structures / 98 Active wells • 30 stacked predominantly oil reservoirs from 2,000’ to 18,000’ • Last drilling program conducted in 2014 Locator Map West Delta 30 Field #1 Largest Oil Field on GoM OCS Shelf (1) Key Field Statistics 32

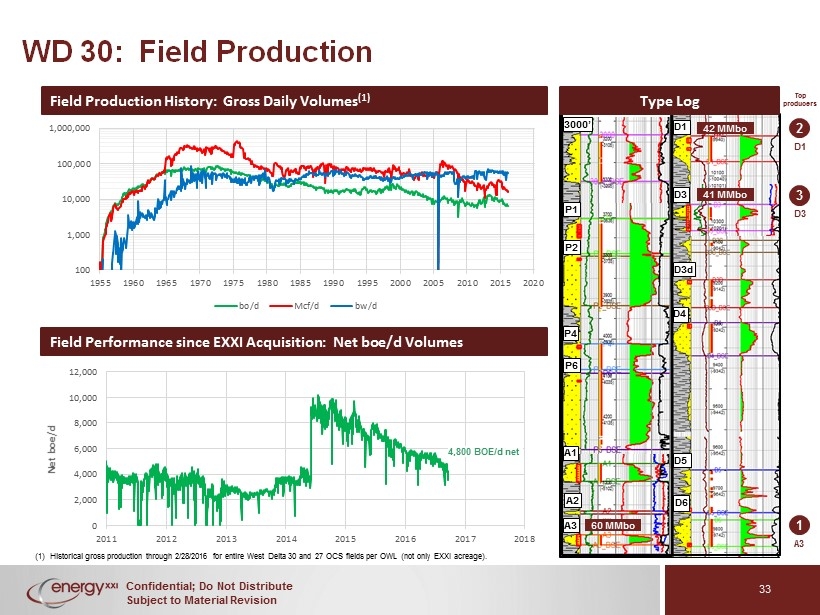

Confidential; Do Not Distribute Subject to Material Revision 0 2,000 4,000 6,000 8,000 10,000 12,000 2011 2012 2013 2014 2015 2016 2017 2018 Net boe/d WD 30: Field Production (1) Historical gross production through 2/28/2016 for entire West Delta 30 and 27 OCS fields per OWL (not only EXXI acreage ). 1 2 3 Top producers D1 D3 A3 3000’ P1 P2 P4 P6 A1 A3 A2 D1 D3 D3d D4 D5 D6 41 MMbo 42 MMbo 60 MMbo Type Log 4,800 BOE/d net 100 1,000 10,000 100,000 1,000,000 1955 1960 1965 1970 1975 1980 1985 1990 1995 2000 2005 2010 2015 2020 bo/d Mcf/d bw/d Field Production History: Gross Daily Volumes (1) Field Performance since EXXI Acquisition: Net boe/d Volumes 33

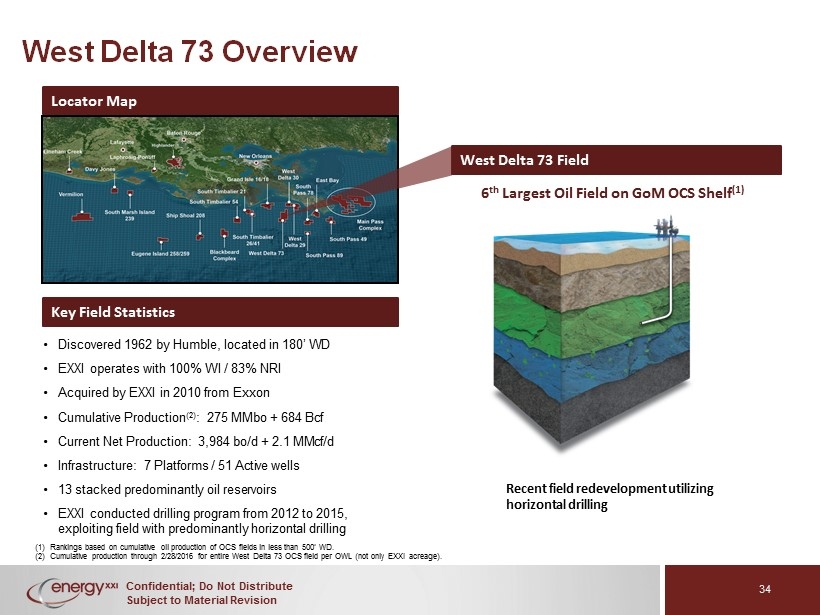

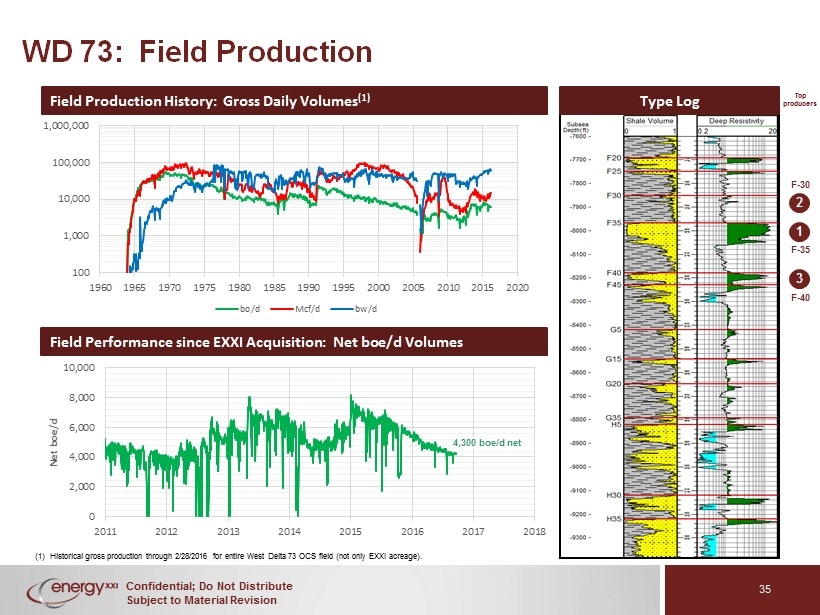

Confidential; Do Not Distribute Subject to Material Revision West Delta 73 Overview (1) Rankings based on cumulative oil production of OCS fields in less than 500’ WD. (2) Cumulative production through 2/28/2016 for entire West Delta 73 OCS field per OWL (not only EXXI acreage ). • Discovered 1962 by Humble, located in 180’ WD • EXXI operates with 100% WI / 83% NRI • Acquired by EXXI in 2010 from Exxon • Cumulative Production (2) : 275 MMbo + 684 Bcf • Current Net Production: 3,984 bo/d + 2.1 MMcf/d • Infrastructure: 7 Platforms / 51 Active wells • 13 stacked predominantly oil reservoirs • EXXI conducted drilling program from 2012 to 2015, exploiting field with predominantly horizontal drilling Locator Map West Delta 73 Field 6 th Largest Oil Field on GoM OCS Shelf (1) Recent field redevelopment utilizing horizontal drilling Key Field Statistics 34

Confidential; Do Not Distribute Subject to Material Revision 0 2,000 4,000 6,000 8,000 10,000 2011 2012 2013 2014 2015 2016 2017 2018 Net boe/d WD 73: Field Production (1) Historical gross production through 2/28/2016 for entire West Delta 73 OCS field ( not only EXXI acreage ). 1 2 3 Top producers 85 MMboe 37 MMboe 23 MMboe F - 35 F - 40 F - 30 4,300 boe/d net 100 1,000 10,000 100,000 1,000,000 1960 1965 1970 1975 1980 1985 1990 1995 2000 2005 2010 2015 2020 bo/d Mcf/d bw/d Field Production History: Gross Daily Volumes (1) Field Performance since EXXI Acquisition: Net boe/d Volumes Type Log 35

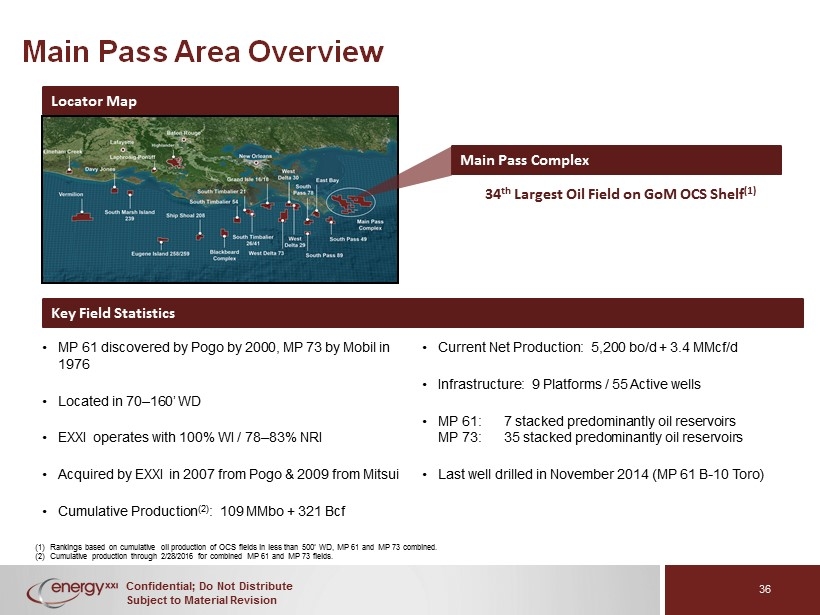

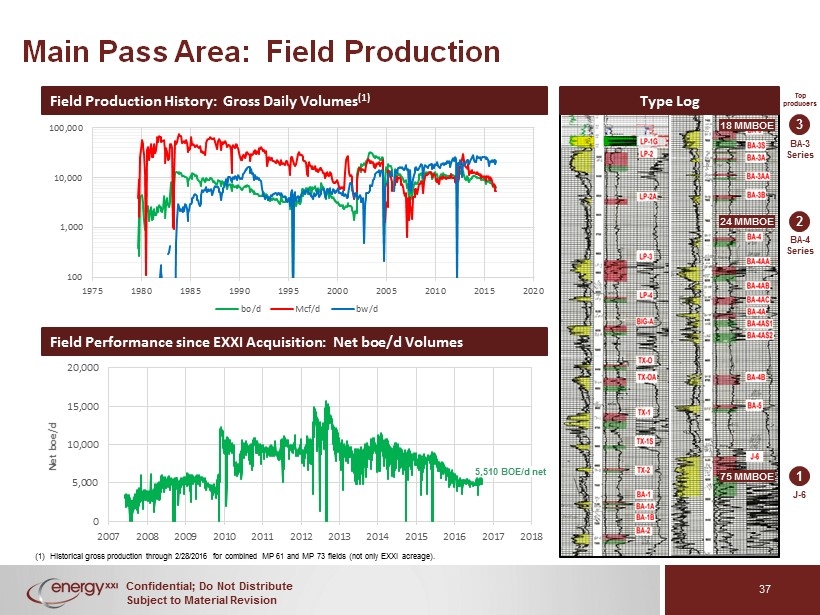

Confidential; Do Not Distribute Subject to Material Revision Main Pass Area Overview (1) Rankings based on cumulative oil production of OCS fields in less than 500’ WD, MP 61 and MP 73 combined. (2) Cumulative production through 2/28/2016 for combined MP 61 and MP 73 fields. • MP 61 discovered by Pogo by 2000, MP 73 by Mobil in 1976 • Located in 70 – 160’ WD • EXXI operates with 100% WI / 78 – 83% NRI • Acquired by EXXI in 2007 from Pogo & 2009 from Mitsui • Cumulative Production (2) : 109 MMbo + 321 Bcf • Current Net Production: 5,200 bo/d + 3.4 MMcf/d • Infrastructure: 9 Platforms / 55 Active wells • MP 61: 7 stacked predominantly oil reservoirs MP 73: 35 stacked predominantly oil reservoirs • Last well drilled in November 2014 (MP 61 B - 10 Toro) Locator Map Main Pass Complex 34 th Largest Oil Field on GoM OCS Shelf (1) Key Field Statistics 36

Confidential; Do Not Distribute Subject to Material Revision 0 5,000 10,000 15,000 20,000 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 Net boe/d Main Pass Area: Field Production (1) Historical gross production through 2/28/2016 for combined MP 61 and MP 73 fields (not only EXXI acreage). 1 3 2 Top producers 75 MMBOE 18 MMBOE 24 MMBOE Type Log BA - 3 Series BA - 4 Series J - 6 5,510 BOE/d net 100 1,000 10,000 100,000 1975 1980 1985 1990 1995 2000 2005 2010 2015 2020 bo/d Mcf/d bw/d Field Production History: Gross Daily Volumes (1) Field Performance since EXXI Acquisition: Net boe/d Volumes 37

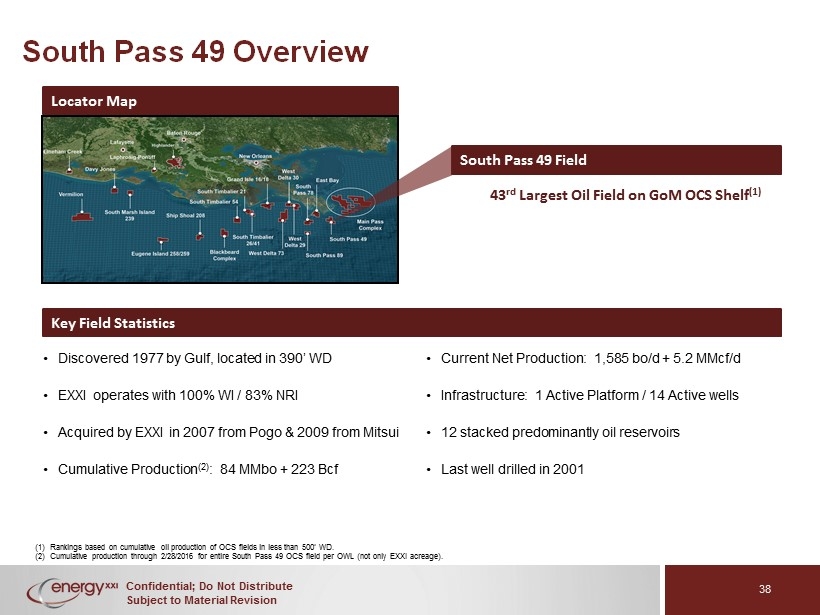

Confidential; Do Not Distribute Subject to Material Revision South Pass 49 Overview (1) Rankings based on cumulative oil production of OCS fields in less than 500’ WD. (2) Cumulative production through 2/28/2016 for entire South Pass 49 OCS field per OWL (not only EXXI acreage ). • Discovered 1977 by Gulf, located in 390’ WD • EXXI operates with 100% WI / 83% NRI • Acquired by EXXI in 2007 from Pogo & 2009 from Mitsui • Cumulative Production (2) : 84 MMbo + 223 Bcf • Current Net Production: 1,585 bo/d + 5.2 MMcf/d • Infrastructure: 1 Active Platform / 14 Active wells • 12 stacked predominantly oil reservoirs • Last well drilled in 2001 Locator Map South Pass 49 Field 43 rd Largest Oil Field on GoM OCS Shelf (1) Key Field Statistics 38

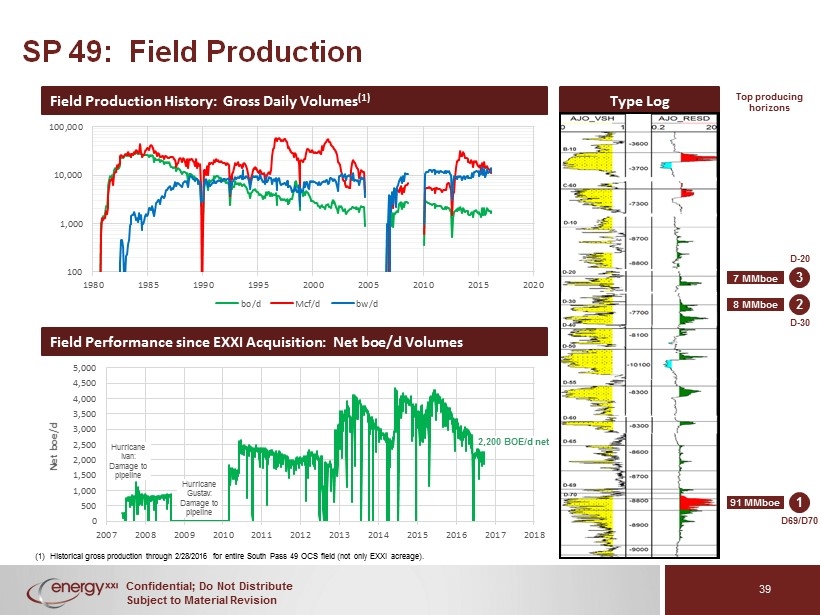

Confidential; Do Not Distribute Subject to Material Revision 0 500 1,000 1,500 2,000 2,500 3,000 3,500 4,000 4,500 5,000 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 Net boe/d SP 49: Field Production (1) Historical gross production through 2/28/2016 for entire South Pass 49 OCS field ( not only EXXI acreage ). 1 2 Top producing horizons 91 MMboe 8 MMboe Type Log D - 30 D69/D70 3 7 MMboe D - 20 Hurricane Gustav: Damage to pipeline 2,200 BOE/d net Hurricane Ivan: D amage to pipeline Hurricane Ivan Hurricane Gustav 100 1,000 10,000 100,000 1980 1985 1990 1995 2000 2005 2010 2015 2020 bo/d Mcf/d bw/d Field Production History: Gross Daily Volumes (1) Field Performance since EXXI Acquisition: Net boe/d Volumes 39

Confidential; Do Not Distribute Subject to Material Revision Ship Shoal 208 Overview (1) Rankings based on cumulative oil production of OCS fields in less than 500’ WD. (2) Cumulative production through 2/28/2016 for entire Ship Shoal 208 OCS field per OWL (not only EXXI acreage ). • Discovered 1963 by Unocal, located in 85 – 100’ WD • EXXI operates with 100% WI / 83% NRI • Acquired by EXXI in 2014 from EPL • Cumulative Production (2) : 224 MMbo + 1.4 Tcf • Current Net Production (3) : 2,700 bo/d + 2.9 MMcf/d • Infrastructure: 11 Platforms / 28 Active wells • 30 stacked predominantly oil reservoirs • Last drilling program conducted in 2014 Locator Map Ship Shoal 208 Field 10 th Largest Oil Field on GoM OCS Shelf (1) Key Field Statistics 40

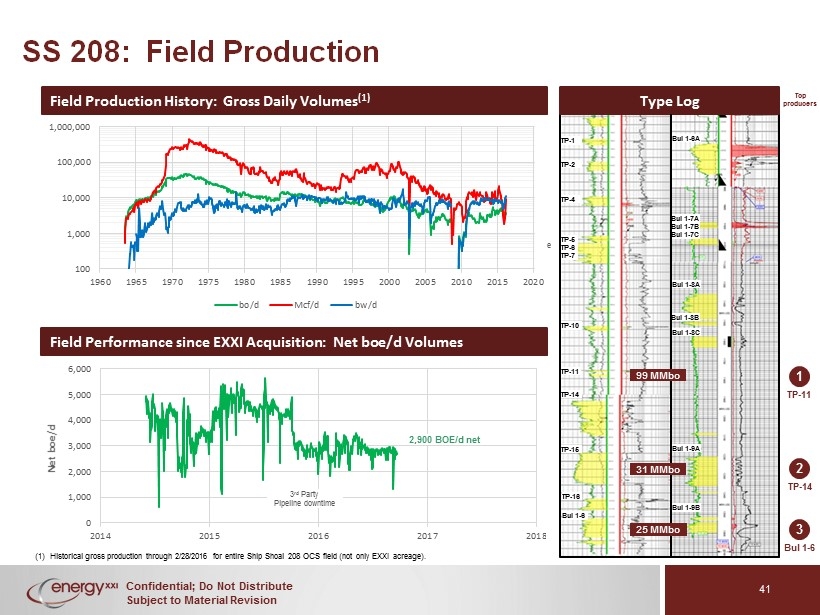

Confidential; Do Not Distribute Subject to Material Revision 0 1,000 2,000 3,000 4,000 5,000 6,000 2014 2015 2016 2017 2018 Net boe/d SS 208: Field Production (1) Historical gross production through 2/28/2016 for entire Ship Shoal 208 OCS field ( not only EXXI acreage ). 1 3 2 Top producers Type Log Bul 1 - 6 TP - 14 TP - 11 TP - 1 TP - 2 TP - 4 TP - 5 TP - 6 TP - 7 TP - 10 TP - 11 TP - 14 TP - 15 TP - 16 Bul 1 - 6 Bul 1 - 6A Bul 1 - 7A Bul 1 - 7B Bul 1 - 7C Bul 1 - 9A Bul 1 - 9B Bul 1 - 8A Bul 1 - 8B Bul 1 - 8C 25 MMbo 31 MMbo 99 MMbo 3 rd Party Pipeline downtime 3 rd Party Pipeline downtime 100 1,000 10,000 100,000 1,000,000 1960 1965 1970 1975 1980 1985 1990 1995 2000 2005 2010 2015 2020 bo/d Mcf/d bw/d Field Production History: Gross Daily Volumes (1) Field Performance since EXXI Acquisition: Net boe/d Volumes 2,900 BOE/d net 41

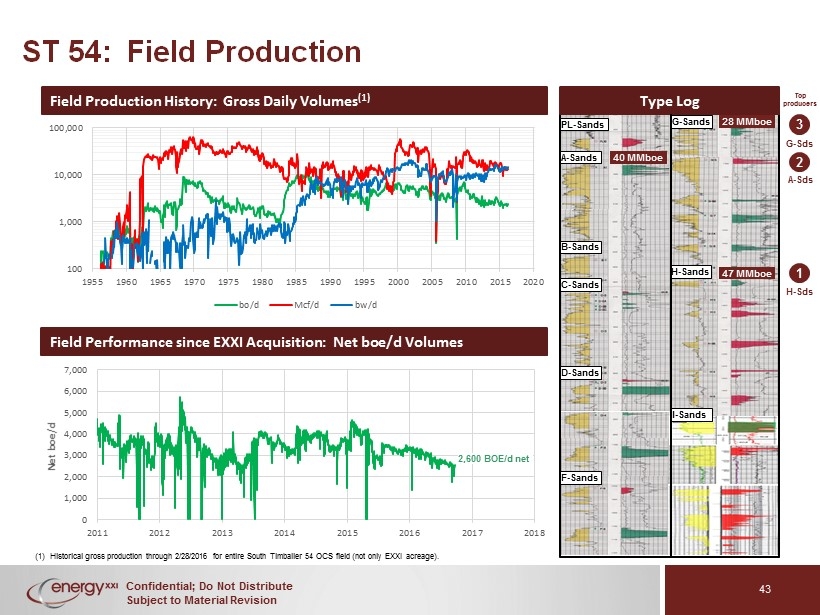

Confidential; Do Not Distribute Subject to Material Revision South Timbalier 54 Overview (1) Rankings based on cumulative oil production of OCS fields in less than 500’ WD. (2) Cumulative production through 2/28/2016 for entire South Timbalier 54 OCS field per OWL (not only EXXI acreage). • Discovered 1956 by Humble, located in 61’ WD • EXXI operates with 100% WI / 83 – 88% NRI • Acquired by EXXI in 2010 from Exxon • Cumulative Production (2) : 76 MMbo + 442 Bcf • Current Net Production: 1,877 bo/d + 5 MMcf /d • Infrastructure: 6 Platforms / 26 Active wells • 7 stacked predominantly oil reservoirs • Last drilling program conducted in January 2015 Locator Map South Timbalier 54 Field 48 th Largest Oil Field on GoM OCS Shelf (1) Key Field Statistics 42

Confidential; Do Not Distribute Subject to Material Revision 0 1,000 2,000 3,000 4,000 5,000 6,000 7,000 2011 2012 2013 2014 2015 2016 2017 2018 Net boe/d ST 54: Field Production (1) Historical gross production through 2/28/2016 for entire South Timbalier 54 OCS field (not only EXXI acreage ). Field Performance since EXXI Acquisition: Net boe/d Volumes 1 3 2 Top producers 47 MMboe 28 MMboe 40 MMboe Type Log G - Sds A - Sds H - Sds 2,600 BOE/d net A - Sands PL - Sands B - Sands C - Sands D - Sands F - Sands G - Sands H - Sands I - Sands 100 1,000 10,000 100,000 1955 1960 1965 1970 1975 1980 1985 1990 1995 2000 2005 2010 2015 2020 bo/d Mcf/d bw/d Field Production History: Gross Daily Volumes (1) 43

Confidential; Do Not Distribute Subject to Material Revision VIII . EXPLORATION POTENTIAL

Confidential; Do Not Distribute Subject to Material Revision Exploration Portfolio • Robust inventory - represents material potential • Extensive seismic database • Multi - well program helps mitigate risk • Both offshore and onshore locations in a variety of plays • Existing facilities expedite discovery to 1st production • Dedicated team and technology • Integrated with internal regional work • Sought exploration JV partner pre - filing 45

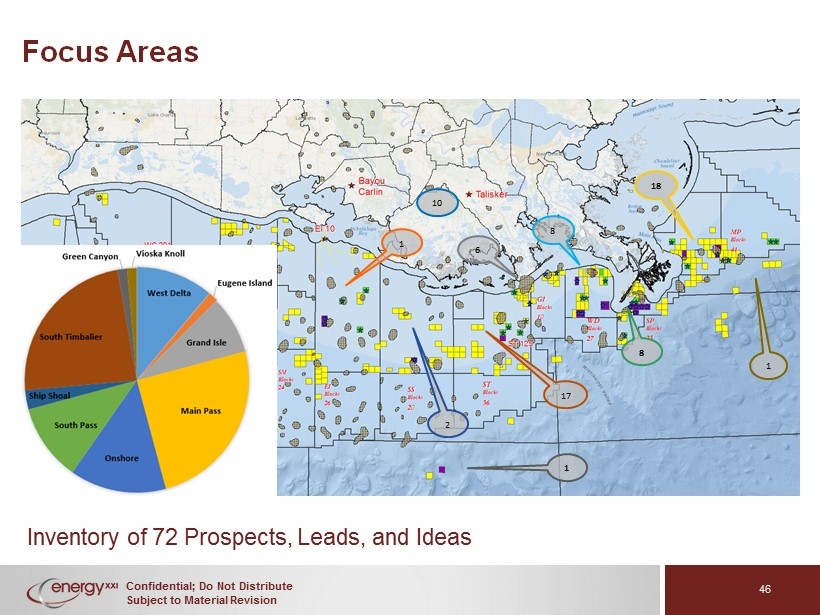

Confidential; Do Not Distribute Subject to Material Revision 6 Focus Areas 8 1 10 18 8 17 2 Inventory of 72 Prospects, Leads, and Ideas 1 1 46

Confidential; Do Not Distribute Subject to Material Revision IX. FINANCIALS & FORECAST

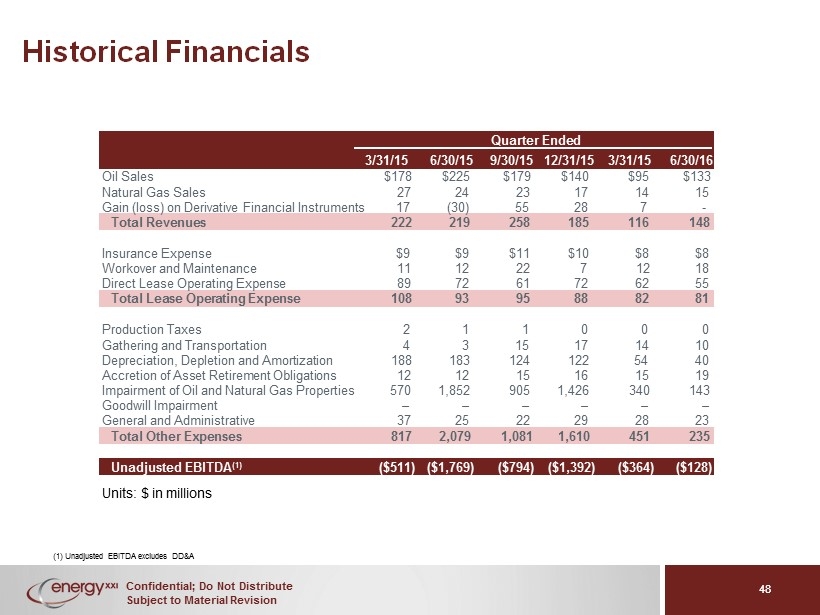

Confidential; Do Not Distribute Subject to Material Revision Historical Financials 48 Quarter Ended 3/31/15 6/30/15 9/30/15 12/31/15 3/31/15 6 /30/16 Oil Sales $178 $ 225 $ 179 $ 140 $95 $ 133 Natural Gas Sales 27 24 23 17 14 15 Gain (loss) on Derivative Financial Instruments 17 (30) 55 28 7 - Total Revenues 222 219 258 185 116 148 Insurance Expense $ 9 $9 $11 $10 $8 $8 Workover and Maintenance 11 12 2 2 7 12 18 Direct Lease Operating Expense 89 72 61 72 62 55 Total Lease Operating Expense 108 93 95 88 82 81 Production Taxes 2 1 1 0 0 0 Gathering and Transportation 4 3 15 17 14 10 Depreciation, Depletion and Amortization 188 183 124 122 54 40 Accretion of Asset Retirement Obligations 12 12 15 16 15 19 Impairment of Oil and Natural Gas Properties 570 1,852 905 1,426 340 143 Goodwill Impairment – – – – – General and Administrative 37 25 22 29 28 23 Total Other Expenses 817 2,079 1,081 1,610 451 235 Unadjusted EBITDA (1) ($ 511) ($ 1,769 ) ($ 794 ) ($ 1,392 ) ($ 364 ) ($ 128 ) – 48 Units: $ in millions (1) Unadjusted EBITDA excludes DD&A

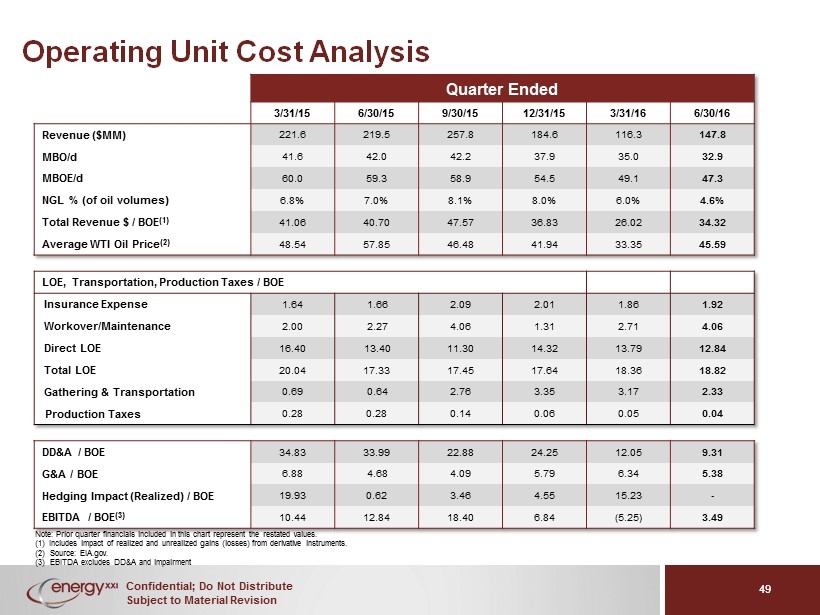

Confidential; Do Not Distribute Subject to Material Revision Operating Unit Cost Analysis Note: Prior quarter financials included in this chart represent the restated values . (1) Includes impact of realized and unrealized gains (losses) from derivative instruments. (2) Source: EIA.gov. (3) EBITDA excludes DD&A and impairment Quarter Ended 3/31/15 6/30/15 9/30/15 12/31/15 3/31/16 6/30/16 Revenue ($MM) 221.6 219.5 257.8 184.6 116.3 147.8 MBO/d 41.6 42.0 42.2 37.9 35.0 32.9 MBOE/d 60.0 59.3 58.9 54.5 49.1 47.3 NGL % (of oil volumes) 6.8% 7.0% 8.1% 8.0% 6.0% 4.6% Total Revenue $ / BOE (1) 41.06 40.70 47.57 36.83 26.02 34.32 Average WTI Oil Price (2) 48.54 57.85 46.48 41.94 33.35 45.59 LOE, Transportation, Production Taxes / BOE Insurance Expense 1.64 1.66 2.09 2.01 1.86 1.92 Workover/Maintenance 2.00 2.27 4.06 1.31 2.71 4.06 Direct LOE 16.40 13.40 11.30 14.32 13.79 12.84 Total LOE 20.04 17.33 17.45 17.64 18.36 18.82 Gathering & Transportation 0.69 0.64 2.76 3.35 3.17 2.33 Production Taxes 0.28 0.28 0.14 0.06 0.05 0.04 DD&A / BOE 34.83 33.99 22.88 24.25 12.05 9.31 G&A / BOE 6.88 4.68 4.09 5.79 6.34 5.38 Hedging Impact (Realized) / BOE 19.93 0.62 3.46 4.55 15.23 - EBITDA / BOE (3) 10.44 12.84 18.40 6.84 (5.25) 3.49 49 49

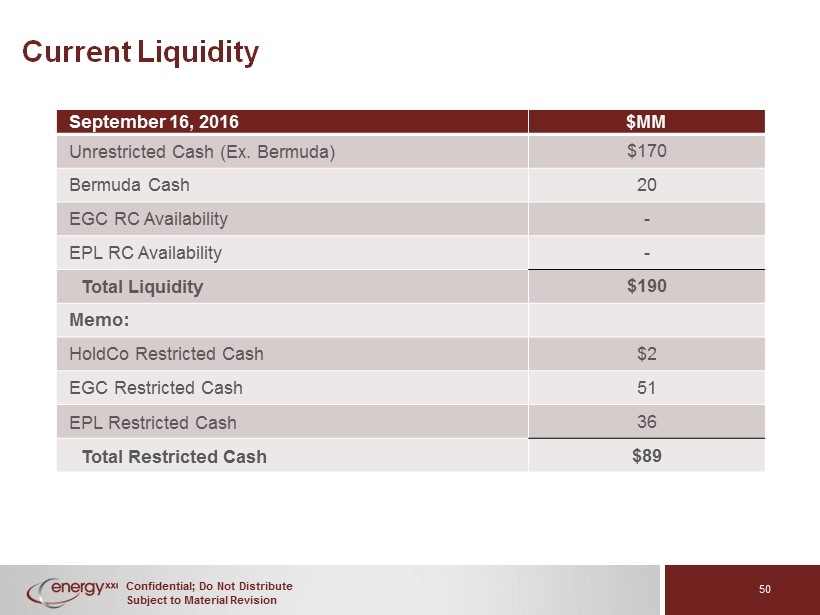

Confidential; Do Not Distribute Subject to Material Revision 50 September 16, 2016 $MM Unrestricted Cash (Ex. Bermuda) $170 Bermuda Cash 20 EGC RC Availability - EPL RC Availability - Total Liquidity $190 Memo: Hold Co Restricted Cash $2 EGC Restricted Cash 51 EPL Restricted Cash 36 Total Restricted Cash $89 Current Liquidity

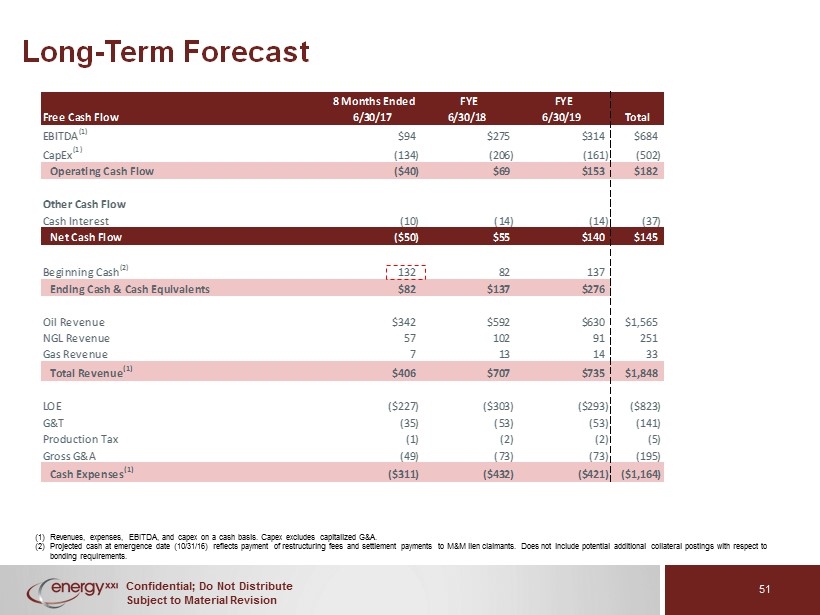

Confidential; Do Not Distribute Subject to Material Revision 8 Months Ended FYE FYE Free Cash Flow 6/30/17 6/30/18 6/30/19 Total EBITDA (1) $94 $275 $314 $684 CapEx (1) (134) (206) (161) (502) Operating Cash Flow ($40) $69 $153 $182 Other Cash Flow Cash Interest (10) (14) (14) (37) Net Cash Flow ($50) $55 $140 $145 Beginning Cash (2) 132 82 137 Ending Cash & Cash Equivalents $82 $137 $276 Oil Revenue $342 $592 $630 $1,565 NGL Revenue 57 102 91 251 Gas Revenue 7 13 14 33 Total Revenue (1) $406 $707 $735 $1,848 LOE ($227) ($303) ($293) ($823) G&T (35) (53) (53) (141) Production Tax (1) (2) (2) (5) Gross G&A (49) (73) (73) (195) Cash Expenses (1) ($311) ($432) ($421) ($1,164) Long - Term Forecast (1) Revenues, expenses, EBITDA, and capex on a cash basis. Capex excludes capitalized G&A. (2) Projected cash at emergence date (10/31/16) reflects payment of restructuring fees and settlement payments to M&M lien claima nts . Does not include potential additional collateral postings with respect to bonding requirements. 51

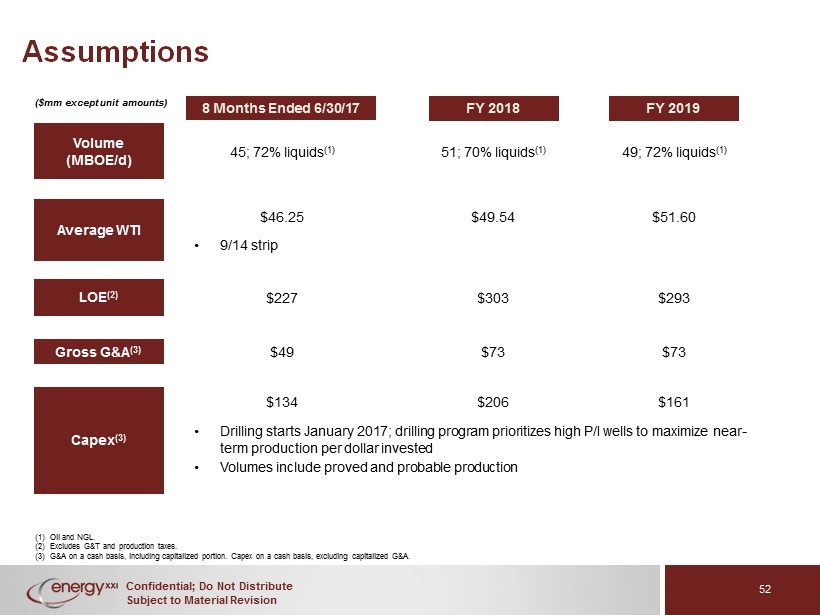

Confidential; Do Not Distribute Subject to Material Revision Capex (3) Assumptions (1) Oil and NGL. (2) Excludes G&T and production taxes . (3) G&A on a cash basis, including capitalized portion. Capex on a cash basis, excluding capitalized G&A. ($mm except unit amounts) • 9/14 strip • Drilling starts January 2017; drilling program prioritizes high P/I wells to maximize near - term production per dollar invested • Volumes include proved and probable production 51; 70% liquids (1) 49; 72% liquids (1) $46.25 $49.54 $51.60 $49 $73 $73 $134 $206 $161 $227 $303 $293 45; 72% liquids (1) Average WTI LOE (2) Gross G&A (3) Volume (MBOE/d) 8 Months Ended 6/30/17 FY 2018 FY 2019 $49 $227 $46.25 52

Confidential; Do Not Distribute Subject to Material Revision Q&A 53

Additional Diligence Materials

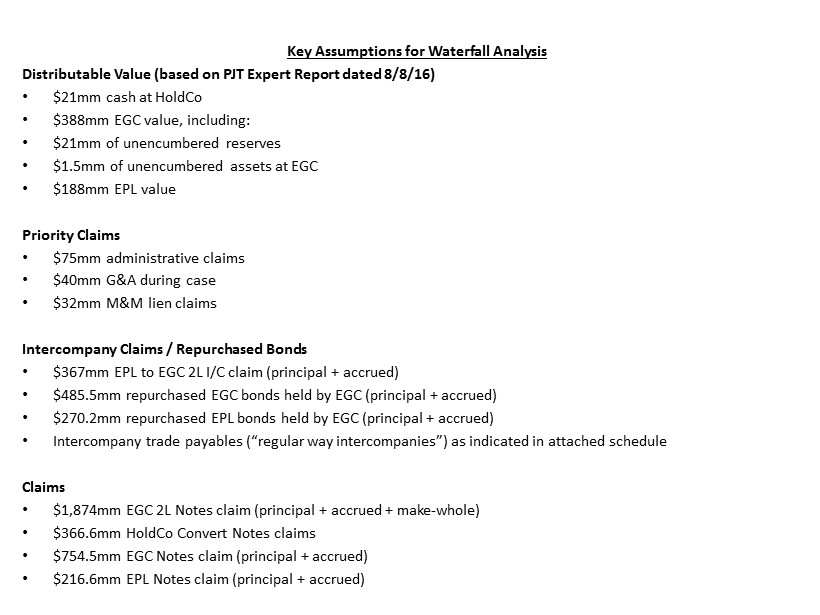

Key Assumptions for Waterfall Analysis Distributable Value (based on PJT Expert Report dated 8/8/16) • $ 21mm cash at HoldCo • $ 388mm EGC value, including: • $ 21mm of unencumbered reserves • $ 1.5mm of unencumbered assets at EGC • $ 188mm EPL value Priority Claims • $ 75mm administrative claims • $ 40mm G&A during case • $ 32mm M&M lien claims Intercompany Claims / Repurchased Bonds • $ 367mm EPL to EGC 2L I/C claim (principal + accrued) • $ 485.5mm repurchased EGC bonds held by EGC (principal + accrued) • $ 270.2mm repurchased EPL bonds held by EGC (principal + accrued) • Intercompany trade payables (“regular way intercompanies ”) as indicated in attached schedule Claims • $ 1,874mm EGC 2L Notes claim (principal + accrued + make - whole) • $ 366.6mm HoldCo Convert Notes claims • $ 754.5mm EGC Notes claim (principal + accrued) • $ 216.6mm EPL Notes claim (principal + accrued)

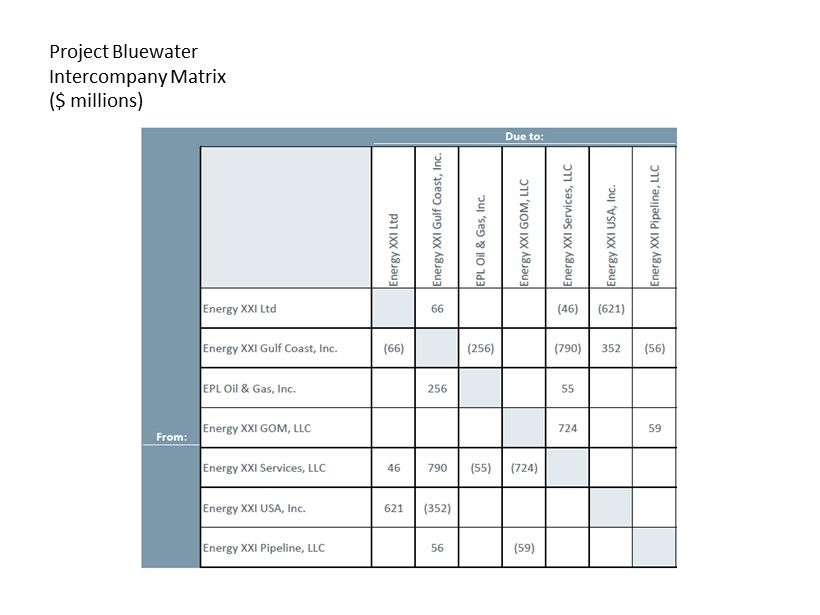

Project Bluewater Intercompany Matrix ($ millions)