UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

SCHEDULE 14A

Proxy Statement Pursuant to Section 14(a) of

the Securities Exchange Act of 1934

Filed by the Registrant x

Filed by a Party other than the Registrant ¨

Check the appropriate box:

| ¨ | Preliminary Proxy Statement |

| ¨ | Confidential, for Use of the Commission Only (as permitted by Rule 14a-6(e)(2)) |

| ¨ | Definitive Proxy Statement |

| x | Definitive Additional Materials |

| ¨ | Soliciting Material under §240.14a-12 |

PACIRA BIOSCIENCES, INC.

(Name of Registrant as Specified in Its Charter)

(Name of Person(s) Filing Proxy Statement, if other than the Registrant)

Payment of Filing Fee (Check all boxes that apply):

| x | No fee required. |

| ¨ | Fee paid previously with preliminary materials. |

| ¨ | Fee computed on table in exhibit required by Item 25(b) per Exchange Act Rules 14a6(i)(1) and 0-11. |

On May 19, 2026, Pacira BioSciences, Inc. published the following investor presentation in connection with its 2026 Annual Meeting of Stockholders:

Delivering Long - Term Value for All Stockholders May 2026

Better is possible. 2 Forward - looking Statements and Where to Find Additional Information Any statements in this document about Pacira’s future expectations, plans, trends, outlook, projections and prospects, and ot her statements containing the words “believes,” “anticipates,” “plans,” “estimates,” “expects,” “intends,” “may,” “will,” “would,” “could,” “can” and similar expressions, constitute forward - looking st atements within the meaning of Section 21E of the Securities Exchange Act of 1934, as amended (the “Exchange Act”), and the Private Securities Litigation Reform Act of 1995, including, without li mit ation, statements related to: the 2026 annual meeting of stockholders; Pacira’s board of directors and the contributions of new directors and director nominees; ‘5x30’, our growth an d b usiness strategy, our future outlook, the strength and efficacy of our intellectual property protection and patent terms, our future growth potential and future financial and operating results and tr ends, our plans, objectives, expectations (financial or otherwise) and intentions, including our plans with respect to the repayment of our indebtedness, anticipated product portfolio and product dev elopment programs, strategic alliances, plans with respect to the Non - Opioids Prevent Addiction in the Nation (“NOPAIN”) Act and any other statements that are not historical facts. For this purp ose, any statement that is not a statement of historical fact should be considered a forward - looking statement. We cannot assure you that our estimates, assumptions and expectations will prove to h ave been correct. Actual results may differ materially from these indicated by such forward - looking statements as a result of various important factors, including risks relating to, among others : risks associated with acquisitions, such as the risk that the acquired businesses and/or assets will not be integrated successfully, that such integration may be more difficult, time - consuming or cos tly than expected or that the expected benefits of the transaction will not occur; our manufacturing and supply chain, global and United States economic conditions (including tariffs, inflation and ri sing interest rates), and our business, including our revenues, financial condition, cash flows and results of operations; the success of our sales and manufacturing efforts in support of t he commercialization of EXPAREL® (bupivacaine liposome injectable suspension), ZILRETTA® (triamcinolone acetonide extended - release injectable suspension) and iovera ® ° ; the rate and degree of market acceptance of EXPAREL, ZILRETTA and iovera ° ; the size and growth of the potential markets for EXPAREL, ZILRETTA and iovera ° and our ability to serve those markets; our plans to expand the use of EXPAREL, ZILRETTA and iovera ° to additional indications and opportunities, and the timing and success of any related clinical trials for EXPAREL, ZILRETTA, iovera ° and any of our other product candidates, including but not limited to PCRX - 201 ( enekinragene inzadenovec ) and PCRX - 2002; the commercial success of EXPAREL, ZILRETTA and iovera ° ; the related timing and success of United States Food and Drug Administration supplemental New Drug Applications and premarket notification 510(k)s; the related timing and success of European Medicines A gen cy Marketing Authorization Applications; our plans to evaluate, develop and pursue additional product candidates utilizing our proprietary high - capacity adenovirus (“ HCAd ”) vector platform; the approval of the commercialization of our products in other jurisdictions (by either us or our partners); clinical trials in support of an existing or potential HCAd - based product candidate; our commercialization and marketing capabilities; our ability to successfully complete capital projects; the outcome of any litigation; the recoverability of our deferred tax assets; assumpt ion s associated with contingent consideration payments; assumptions used for estimated future cash flows associated with determining the fair value of the company; the anticipated funding or be nef its of our share repurchase program; and factors discussed in the “Risk Factors” of Pacira’s most recent Annual Report on Form 10 - K and in other filings that it periodically makes with the U.S. Securities and Exchange Commission (the “SEC”). In addition, the forward - looking statements included in this document represent Pacira’s views as of the date of this document. Important factors could cause actual results to differ materially from those indicated or implied by forward - looking statements, and as such Pacira anticipates that subsequent events and developments will cause its views to change. Except as required by applicable law, Pacira undertakes no intention or obligation to update or revise any forward - looking statements, whether as a result of new information , future events or otherwise, and readers should not rely on these forward - looking statements as representing Pacira’s views as of any date subsequent to the date of this document. These forward - looking statements involve known and unknown risks, uncertainties and other factors that may cause Pacira’s actual results, levels of activity, performance or achievements to differ materially from those expressed or implied by these statements. These factors include the matters discussed and referenced in th e “Risk Factors” of Pacira’s most recent Annual Report on Form 10 - K and in other filings that Pacira periodically makes with the SEC.

Better is possible. 3 Table of Contents 4 Executive Summary 7 Overview of Pacira BioSciences 14 Pacira is Successfully Executing on Its Long - Term Strategy to Drive Value for All Stockholders 29 Pacira’s Highly Qualified Board is Effectively Overseeing Our Long - Term Strategy and Committed to Good Corporate Governance 38 DOMA’s Campaign is Highly Misguided and Not in the Best Interest of All Stockholders 50 Conclusion 54 Appendix

Better is possible. 4 Executive Summary

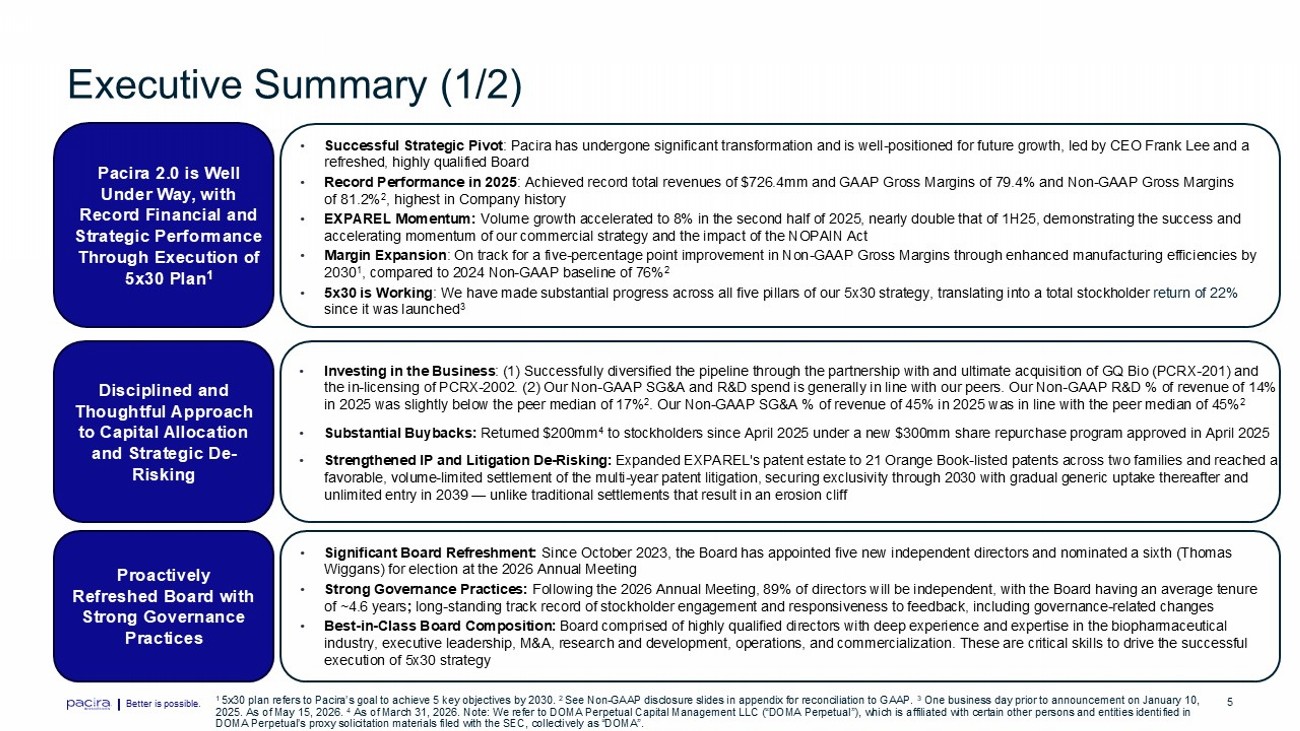

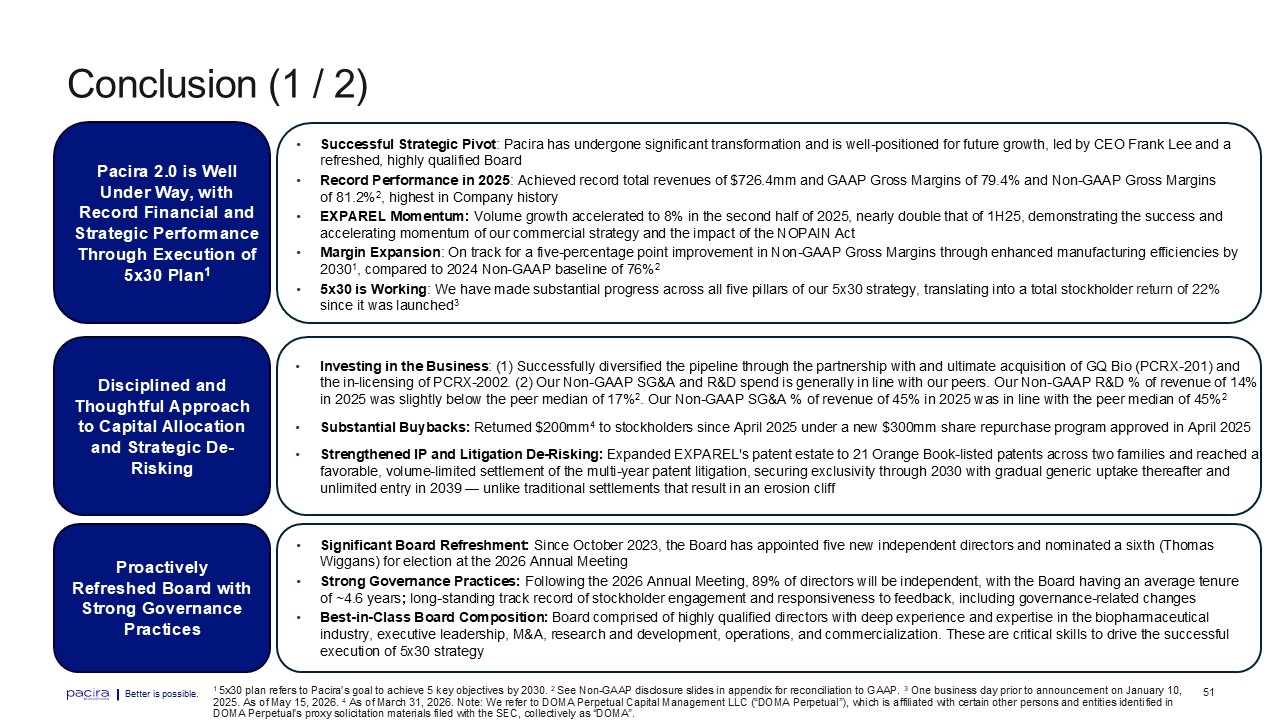

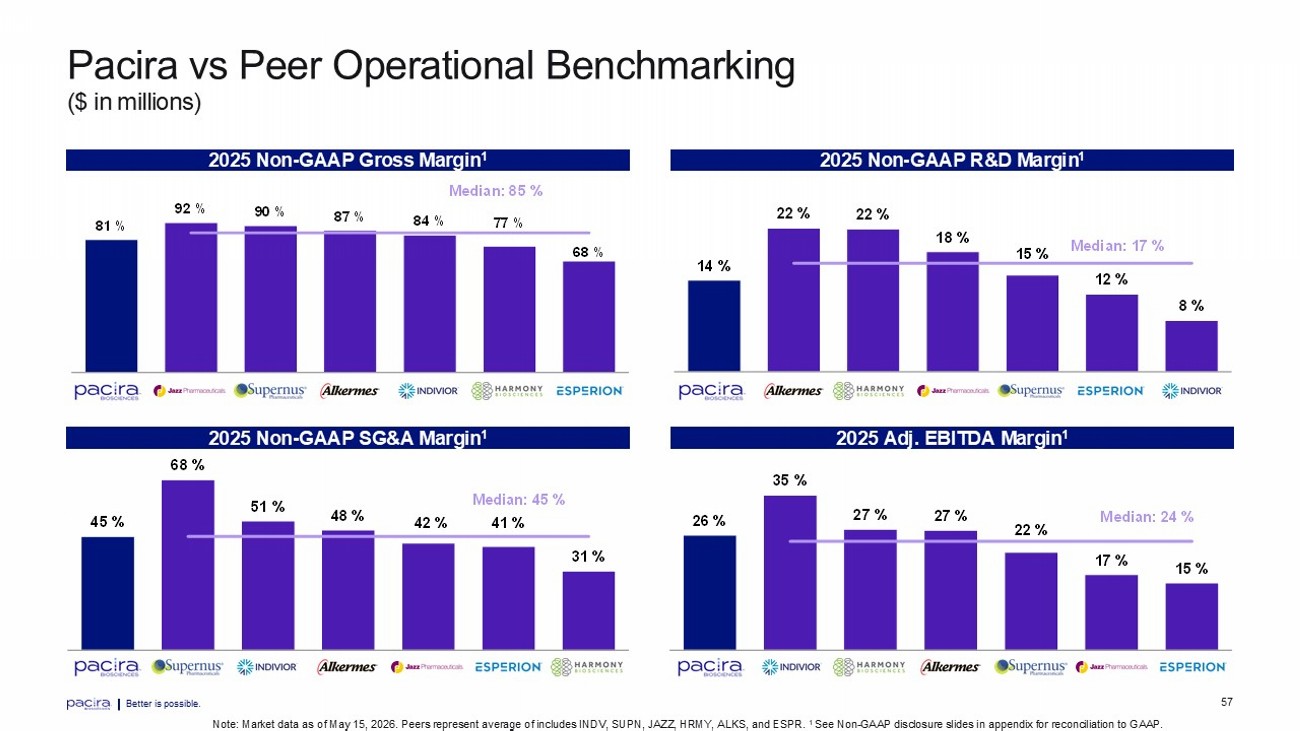

Better is possible. 5 Executive Summary (1/2) Disciplined and Thoughtful Approach to Capital Allocation and Strategic De - Risking • Investing in the Business : (1) Successfully diversified the pipeline through the partnership with and ultimate acquisition of GQ Bio (PCRX - 201) and the in - licensing of PCRX - 2002. (2) Our Non - GAAP SG&A and R&D spend is generally in line with our peers. Our Non - GAAP R&D % of re venue of 14% in 2025 was slightly below the peer median of 17% 2 . Our Non - GAAP SG&A % of revenue of 45% in 2025 was in line with the peer median of 45% 2 • Substantial Buybacks: Returned $200mm 4 to stockholders since April 2025 under a new $300mm share repurchase program approved in April 2025 • Strengthened IP and Litigation De - Risking: Expanded EXPAREL's patent estate to 21 Orange Book - listed patents across two families and reached a favorable, volume - limited settlement of the multi - year patent litigation, securing exclusivity through 2030 with gradual generic uptake thereafter and unlimited entry in 2039 — unlike traditional settlements that result in an erosion cliff Pacira 2.0 is Well Under Way, with Record Financial and Strategic Performance Through Execution of 5x30 Plan 1 • Successful Strategic Pivot : Pacira has undergone significant transformation and is well - positioned for future growth, led by CEO Frank Lee and a refreshed, highly qualified Board • Record Performance in 2025 : Achieved record total revenues of $726.4mm and GAAP Gross Margins of 79.4% and Non - GAAP Gross Margins of 81.2% 2 , highest in Company history • EXPAREL Momentum: Volume growth accelerated to 8% in the second half of 2025, nearly double that of 1H25, demonstrating the success and accelerating momentum of our commercial strategy and the impact of the NOPAIN Act • Margin Expansion : On track for a five - percentage point improvement in Non - GAAP Gross Margins through enhanced manufacturing efficiencies by 2030 1 , compared to 2024 Non - GAAP baseline of 76% 2 • 5x30 is Working : We have made substantial progress across all five pillars of our 5x30 strategy, translating into a total stockholder return of 22% since it was launched 3 Proactively Refreshed Board with Strong Governance Practices • Significant Board Refreshment: Since October 2023, the Board has appointed five new independent directors and nominated a sixth (Thomas Wiggans) for election at the 2026 Annual Meeting • Strong Governance Practices: Following the 2026 Annual Meeting, 89% of directors will be independent, with the Board having an average tenure of ~4.6 years ; long - standing track record of stockholder engagement and responsiveness to feedback, including governance - related changes • Best - in - Class Board Composition: Board comprised of highly qualified directors with deep experience and expertise in the biopharmaceutical industry, executive leadership, M&A, research and development, operations, and commercialization. These are critical skills t o d rive the successful execution of 5x30 strategy 1 5x30 plan refers to Pacira’s goal to achieve 5 key objectives by 2030. 2 See Non - GAAP disclosure slides in appendix for reconciliation to GAAP. 3 One business day prior to announcement on January 10, 2025. As of May 15, 2026. 4 As of March 31, 2026. Note: We refer to DOMA Perpetual Capital Management LLC (“DOMA Perpetual”), which is affiliated with ce rt ain other persons and entities identified in DOMA Perpetual’s proxy solicitation materials filed with the SEC, collectively as “DOMA”.

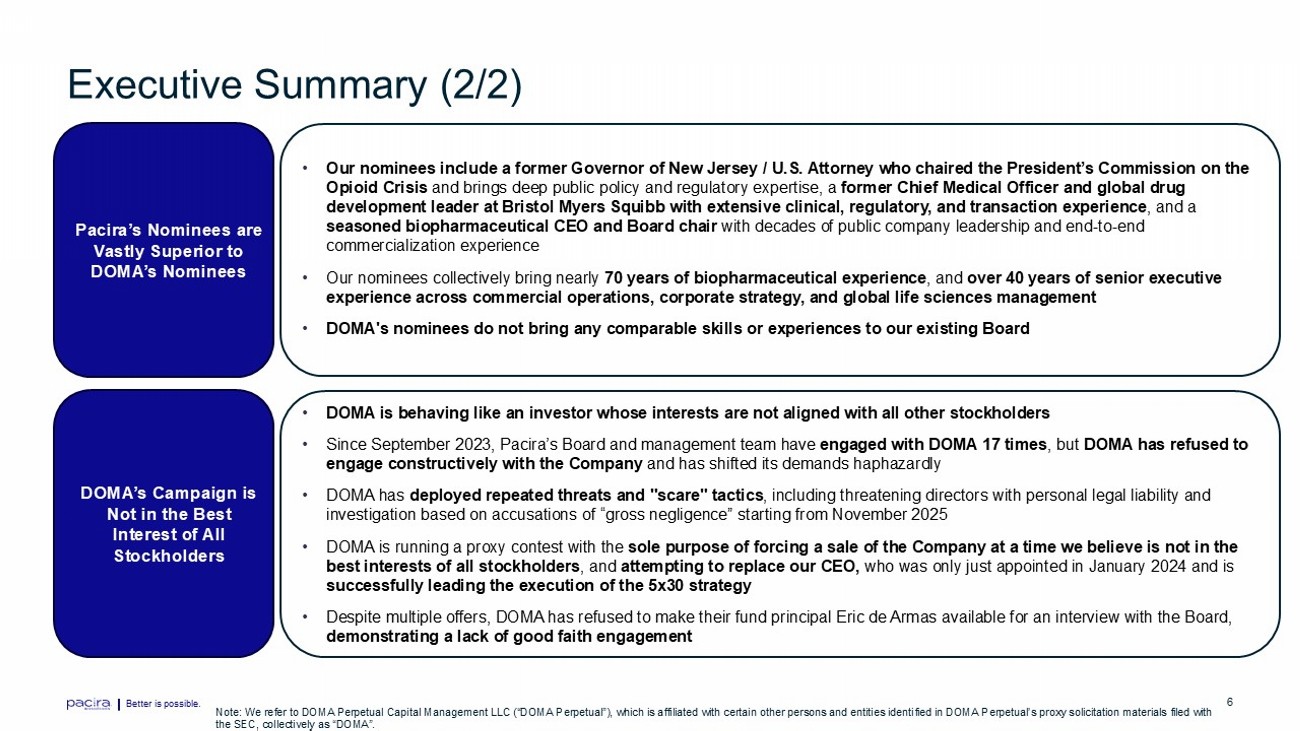

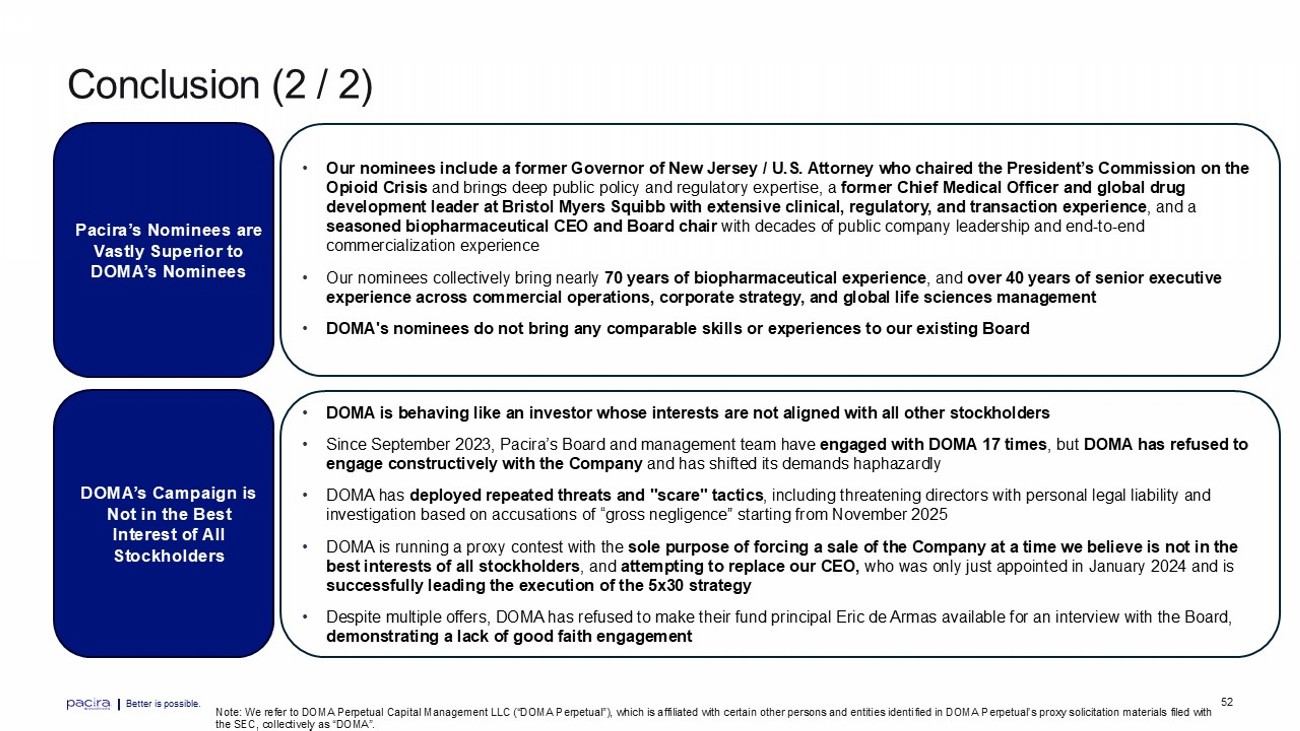

Better is possible. 6 Executive Summary (2/2) Pacira’s Nominees are Vastly Superior to DOMA’s Nominees Note: We refer to DOMA Perpetual Capital Management LLC (“DOMA Perpetual”), which is affiliated with certain other persons an d e ntities identified in DOMA Perpetual’s proxy solicitation materials filed with the SEC, collectively as “DOMA”. DOMA’s Campaign is Not in the Best Interest of All Stockholders • Our nominees include a former Governor of New Jersey / U.S. Attorney who chaired the President’s Commission on the Opioid Crisis and brings deep public policy and regulatory expertise, a former Chief Medical Officer and global drug development leader at Bristol Myers Squibb with extensive clinical, regulatory, and transaction experience , and a seasoned biopharmaceutical CEO and Board chair with decades of public company leadership and end - to - end commercialization experience • Our nominees collectively bring nearly 70 years of biopharmaceutical experience , and over 40 years of senior executive experience across commercial operations, corporate strategy, and global life sciences management • DOMA's nominees do not bring any comparable skills or experiences to our existing Board • DOMA is behaving like an investor whose interests are not aligned with all other stockholders • Since September 2023, Pacira’s Board and management team have engaged with DOMA 17 times , but DOMA has refused to engage constructively with the Company and has shifted its demands haphazardly • DOMA has deployed repeated threats and "scare" tactics , including threatening directors with personal legal liability and investigation based on accusations of “gross negligence” starting from November 2025 • DOMA is running a proxy contest with the sole purpose of forcing a sale of the Company at a time we believe is not in the best interests of all stockholders , and attempting to replace our CEO, who was only just appointed in January 2024 and is successfully leading the execution of the 5x30 strategy • Despite multiple offers, DOMA has refused to make their fund principal Eric de Armas available for an interview with the Boar d, demonstrating a lack of good faith engagement

Better is possible. 7 Overview of Pacira BioSciences

Better is possible. 8 A Leader in Innovative Pain Management MISSION Our mission is to deliver innovative, non - opioid pain therapies to transform the lives of patients. GUIDING PRINCIPLES Our guiding principles are mantras we developed in lockstep with our mission, influencing every decision we make. Better is possible. $726M 800+ 18M+ 10+ ACCELERATING GROWTH IN BASE BUSINESS ADVANCING PIPELINE VALUE 1 More than 3mm patients treated per year 2 Double - digit compounded annual growth rate 3 5 - percentage point N on - GAAP G ross M argin improvements over 2024 1 4 Clinical pipeline expansion with 5 novel programs in development 5 Establishing 5 partnerships including pipeline and commercial agreements Executing on Our 5 - Year Plan to Achieve 5 Key Objectives by 2030 1 See Non - GAAP disclosure slides in appendix for reconciliation to GAAP.

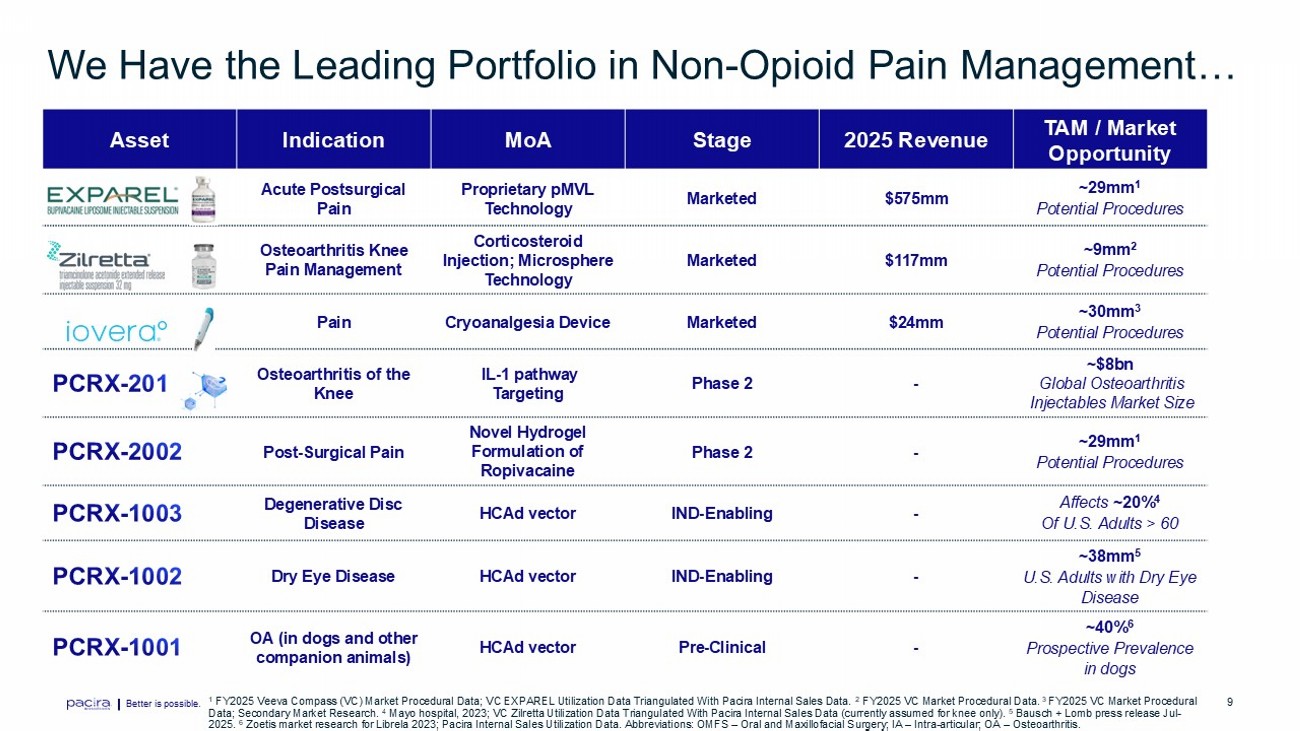

Better is possible. 9 We Have the Leading Portfolio in Non - Opioid Pain Management… Better is possible. TAM / Market Opportunity 2025 Revenue Stage MoA Indication Asset ~29mm 1 Potential Procedures $575mm Marketed Proprietary pMVL Technology Acute Postsurgical Pain EXPAREL ~9mm 2 Potential Procedures $117mm Marketed Corticosteroid Injection; Microsphere Technology Osteoarthritis Knee Pain Management ZILRETTA ~30mm 3 Potential Procedures $24mm Marketed Cryoanalgesia Device Pain IOVERA ~$8bn Global Osteoarthritis Injectables Market Size - Phase 2 IL - 1 pathway Targeting Osteoarthritis of the Knee ~29mm 1 Potential Procedures - Phase 2 Novel Hydrogel Formulation of Ropivacaine Post - Surgical Pain Affects ~20% 4 Of U.S. Adults > 60 - IND - Enabling HCAd vector Degenerative Disc Disease ~38mm 5 U.S. Adults with Dry Eye Disease - IND - Enabling HCAd vector Dry Eye Disease ~40% 6 Prospective Prevalence in dogs - Pre - Clinical HCAd vector OA (in dogs and other companion animals) 1 FY2025 Veeva Compass (VC) Market Procedural Data; VC EXPAREL Utilization Data Triangulated With Pacira Internal Sales Data. 2 FY2025 VC Market Procedural Data. 3 FY2025 VC Market Procedural Data; Secondary Market Research. 4 Mayo hospital, 2023; VC Zilretta Utilization Data Triangulated With Pacira Internal Sales Data (currently assumed for knee only). 5 Bausch + Lomb press release Jul - 2025. 6 Zoetis market research for Librela 2023; Pacira Internal Sales Utilization Data. Abbreviations: OMFS – Oral and Maxillofacial Surgery; IA – Intra - articular; OA – Osteoarthritis.

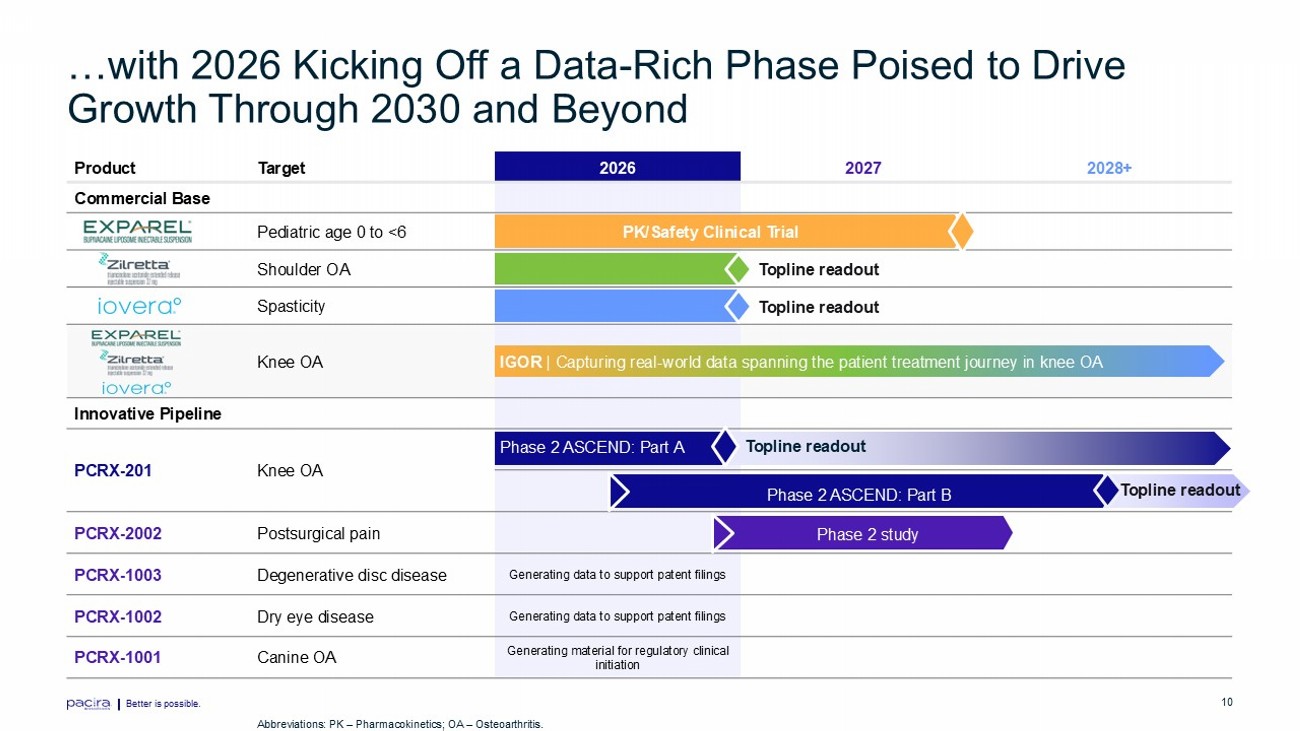

Better is possible. 10 …with 2026 Kicking Off a Data - Rich Phase Poised to Drive Growth Through 2030 and Beyond 2028+ 2027 2026 Target Product Commercial Base Pediatric age 0 to <6 Shoulder OA Spasticity Knee OA Innovative Pipeline Knee OA PCRX - 201 Postsurgical pain PCRX - 2002 Generating data to support patent filings Degenerative disc disease PCRX - 1003 Generating data to support patent filings Dry eye disease PCRX - 1002 Generating material for regulatory clinical initiation Canine OA PCRX - 1001 PK/Safety Clinical Trial Topline readout Phase 2 study IGOR | Capturing real - world data spanning the patient treatment journey in knee OA Phase 2 ASCEND: Part A Topline readout Phase 2 ASCEND: Part B Topline readout Better is possible. Abbreviations: PK – Pharmacokinetics; OA – Osteoarthritis. Topline readout

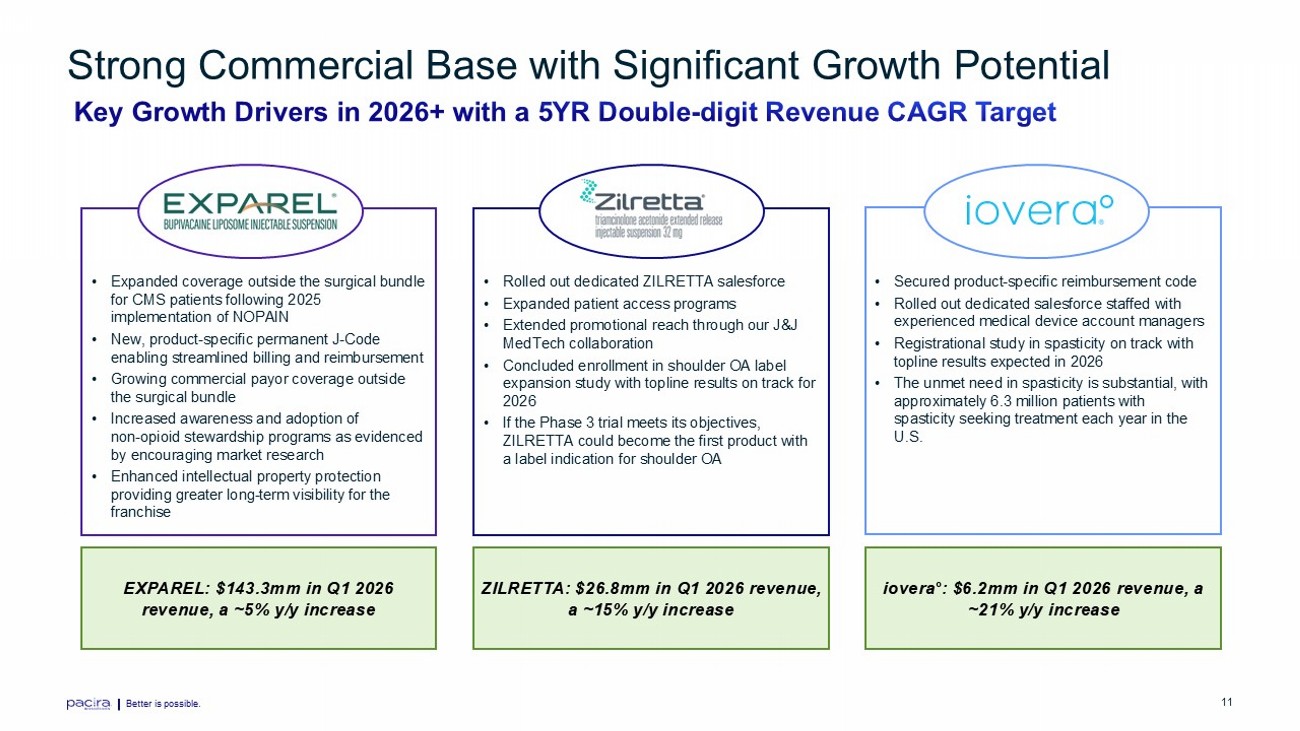

Better is possible. 11 Strong Commercial Base with Significant Growth Potential Better is possible. EXPAREL: $143.3mm in Q1 2026 revenue, a ~5% y/y increase ZILRETTA: $26.8mm in Q1 2026 revenue, a ~15% y/y increase iovera ° : $6.2mm in Q1 2026 revenue, a ~21% y/y increase • Expanded coverage outside the surgical bundle for CMS patients following 2025 implementation of NOPAIN • New, product - specific permanent J - Code enabling streamlined billing and reimbursement • Growing commercial payor coverage outside the surgical bundle • Increased awareness and adoption of non - opioid stewardship programs as evidenced by encouraging market research • Enhanced intellectual property protection providing greater long - term visibility for the franchise • Rolled out dedicated ZILRETTA salesforce • Expanded patient access programs • Extended promotional reach through our J&J MedTech collaboration • Concluded enrollment in shoulder OA label expansion study with topline results on track for 2026 • If the Phase 3 trial meets its objectives, ZILRETTA could become the first product with a label indication for shoulder OA • Secured product - specific reimbursement code • Rolled out dedicated salesforce staffed with experienced medical device account managers • Registrational study in spasticity on track with topline results expected in 2026 • The unmet need in spasticity is substantial, with approximately 6.3 million patients with spasticity seeking treatment each year in the U.S.

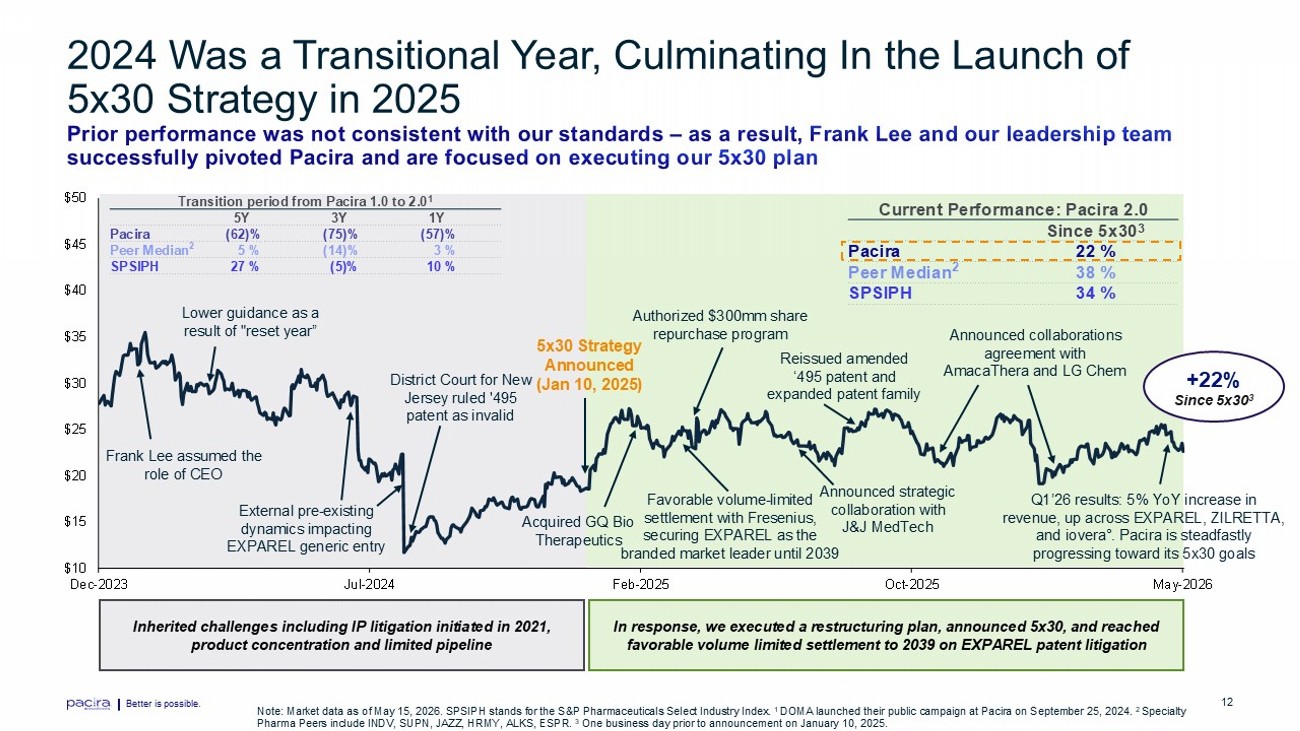

Better is possible. 12 $10 $15 $20 $25 $30 $35 $40 $45 $50 Dec-2023 Jul-2024 Feb-2025 Oct-2025 May-2026 2024 Was a Transitional Year, Culminating In the Launch of 5x30 Strategy in 2025 External pre - existing dynamics impacting EXPAREL generic entry 5x30 Strategy Announced (Jan 10, 2025) Lower guidance as a result of "reset year” Frank Lee assumed the role of CEO Inherited challenges including IP litigation initiated in 2021, product concentration and limited pipeline In response, we executed a restructuring plan, announced 5x30, and reached favorable volume limited settlement to 2039 on EXPAREL patent litigation Authorized $300mm share repurchase program Announced strategic collaboration with J&J MedTech Announced collaborations agreement with AmacaThera and LG Chem Current Performance: Pacira 2.0 Since 5x30 3 22 % Pacira 38 % Peer Median 2 34 % SPSIPH Note: Market data as of May 15, 2026. SPSIPH stands for the S&P Pharmaceuticals Select Industry Index. 1 DOMA launched their public campaign at Pacira on September 25, 2024. 2 Specialty Pharma Peers include INDV, SUPN, JAZZ, HRMY, ALKS, ESPR. 3 One business day prior to announcement on January 10, 2025. Acquired GQ Bio Therapeutics Transition period from Pacira 1.0 to 2.0 1 1Y 3Y 5Y (57)% (75)% (62)% Pacira 3 % (14)% 5 % Peer Median 2 10 % (5)% 27 % SPSIPH District Court for New Jersey ruled '495 patent as invalid Reissued amended ‘495 patent and expanded patent family Favorable volume - limited settlement with Fresenius, securing EXPAREL as the branded market leader until 2039 + 22 % Since 5x30 3 Q1’26 results: 5% YoY increase in revenue, up across EXPAREL, ZILRETTA, and iovera ° . Pacira is steadfastly progressing toward its 5x30 goals

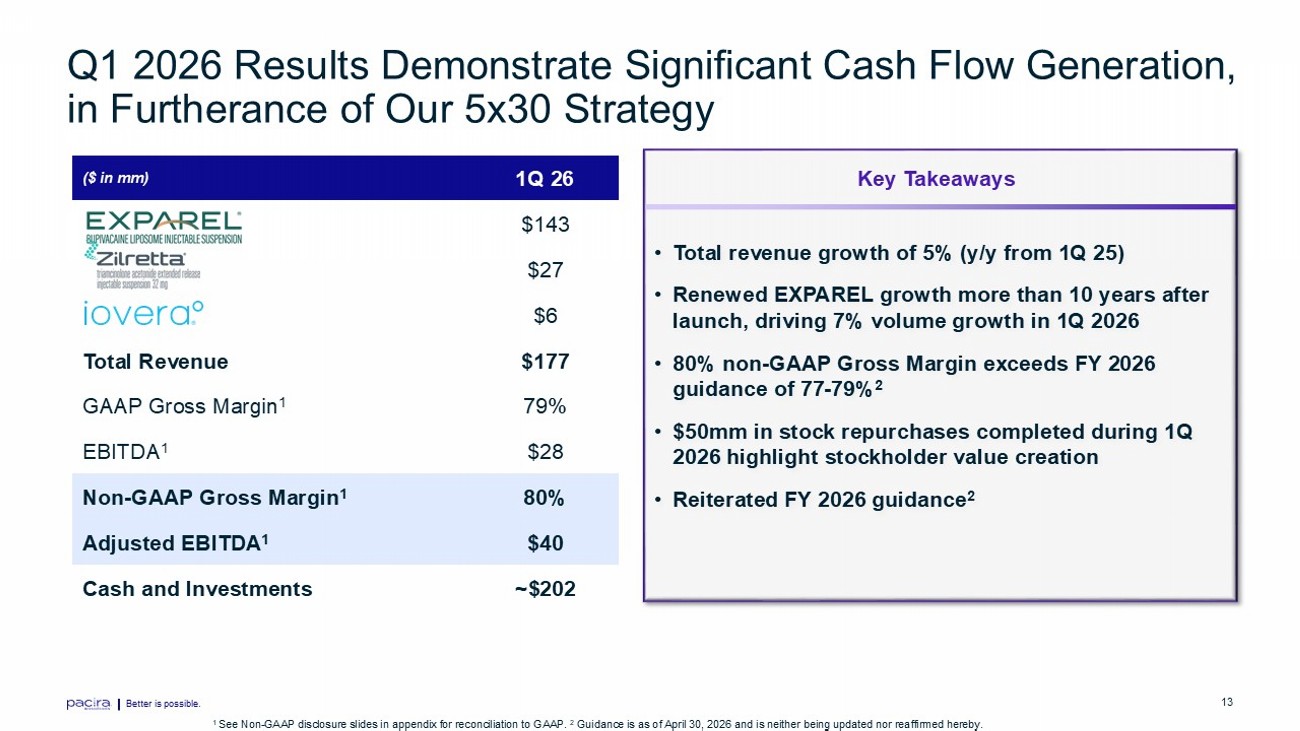

Better is possible. 13 Q1 2026 Results Demonstrate Significant Cash Flow Generation, in Furtherance of Our 5x30 Strategy Better is possible. 1 See Non - GAAP disclosure slides in appendix for reconciliation to GAAP. 2 Guidance is as of April 30, 2026 and is neither being updated nor reaffirmed hereby. 1Q 26 ($ in mm) $143 $27 $6 $177 Total Revenue 79% GAAP Gross Margin 1 $28 EBITDA 1 80% Non - GAAP Gross Margin 1 $40 Adjusted EBITDA 1 ~$202 Cash and Investments • Total revenue growth of 5% (y/y from 1Q 25) • Renewed EXPAREL growth more than 10 years after launch, driving 7% volume growth in 1Q 2026 • 80% non - GAAP Gross Margin exceeds FY 2026 guidance of 77 - 79% 2 • $50mm in stock repurchases completed during 1Q 2026 highlight stockholder value creation • Reiterated FY 2026 guidance 2 Key Takeaways

Better is possible. 14 Pacira is Successfully Executing on Its Long - Term Strategy to Drive Value for All Stockholders

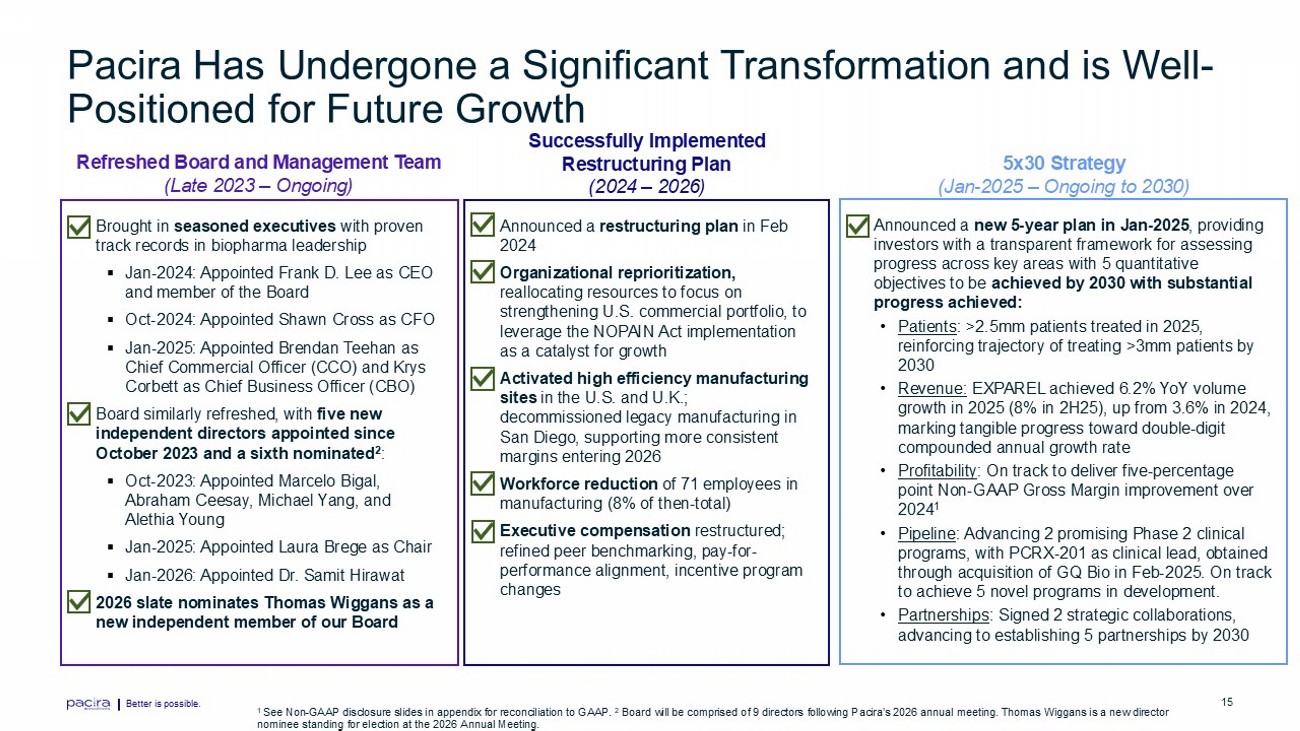

Better is possible. 15 Pacira Has Undergone a Significant Transformation and is Well - Positioned for Future Growth x Announced a restructuring plan in Feb 2024 x Organizational reprioritization, reallocating resources to focus on strengthening U.S. commercial portfolio, to leverage the NOPAIN Act implementation as a catalyst for growth x Activated high efficiency manufacturing sites in the U.S. and U.K.; decommissioned legacy manufacturing in San Diego, supporting more consistent margins entering 2026 x Workforce reduction of 71 employees in manufacturing (8% of then - total) x Executive compensation restructured; refined peer benchmarking, pay - for - performance alignment, incentive program changes x Brought in seasoned executives with proven track records in biopharma leadership ▪ Jan - 2024: Appointed Frank D. Lee as CEO and member of the Board ▪ Oct - 2024: Appointed Shawn Cross as CFO ▪ Jan - 2025: Appointed Brendan Teehan as Chief Commercial Officer (CCO) and Krys Corbett as Chief Business Officer (CBO) x Board similarly refreshed, with five new independent directors appointed since October 2023 and a sixth nominated 2 : ▪ Oct - 2023: Appointed Marcelo Bigal , Abraham Ceesay, Michael Yang, and Alethia Young ▪ Jan - 2025: Appointed Laura Brege as Chair ▪ Jan - 2026: Appointed Dr. Samit Hirawat x 2026 slate nominates Thomas Wiggans as a new independent member of our Board x Announced a new 5 - year plan in Jan - 2025 , providing investors with a transparent framework for assessing progress across key areas with 5 quantitative objectives to be achieved by 2030 with substantial progress achieved: • Patients : >2.5mm patients treated in 2025, reinforcing trajectory of treating >3mm patients by 2030 • Revenue: EXPAREL achieved 6.2% YoY volume growth in 2025 (8% in 2H25), up from 3.6% in 2024, marking tangible progress toward double - digit compounded annual growth rate • Profitability : On track to deliver five - percentage point Non - GAAP Gross Margin improvement over 2024 1 • Pipeline : Advancing 2 promising Phase 2 clinical programs, with PCRX - 201 as clinical lead, obtained through acquisition of GQ Bio in Feb - 2025. On track to achieve 5 novel programs in development. • Partnerships : Signed 2 strategic collaborations, advancing to establishing 5 partnerships by 2030 Successfully Implemented Restructuring Plan (2024 – 2026) Refreshed Board and Management Team (Late 2023 – Ongoing) 5x30 Strategy (Jan - 2025 – Ongoing to 2030) 1 See Non - GAAP disclosure slides in appendix for reconciliation to GAAP. 2 Board will be comprised of 9 directors following Pacira’s 2026 annual meeting. Thomas Wiggans is a new director nominee standing for election at the 2026 Annual Meeting.

Better is possible. 16 Frank D . Lee, MBA, Chief Executive Officer • Joined Pacira as CEO and Board member in January 2024 • Accomplished biopharmaceutical leader, who brings nearly three decades of global experience and a strong track record of product development and commercial success across both small biotech and large pharmaceutical organizations • Most recently he served as CEO and member of the board of directors of Forma Therapeutics from March 2019 through its acquisition by Novo Nordisk in October 2022 • Transformed the Company from early - stage drug discovery into clinical development of lead assets in rare hematologic disorders and cancer • Prior to Forma, served as Senior Vice President, Global Product Strategy, Immunology, Ophthalmology, and Infectious Diseases at Genentech, a member of the Roche Group • Responsible for driving development and commercial strategy for a broad portfolio of molecules in development and for global in - line product sales of $ 11 bn • 13 - year career path at Genentech included leadership positions of increasing scope and responsibility for delivering transformative medicines to patients • Currently serves on the Board of Bausch Health Companies (NYSE: BHC) Our CEO Established a New Vision and the 5x30 Strategy for Growth and Value Creation Better is possible. Prior Leadership Roles . Prior Commercialization Experience . • Sold to Novo N ordisk for $1.1bn • Raised capital through series D crossover round and for the IPO • Novo Nordisk announced positive Phase 3 data for Forma’s lead asset etavopivat in April 2026

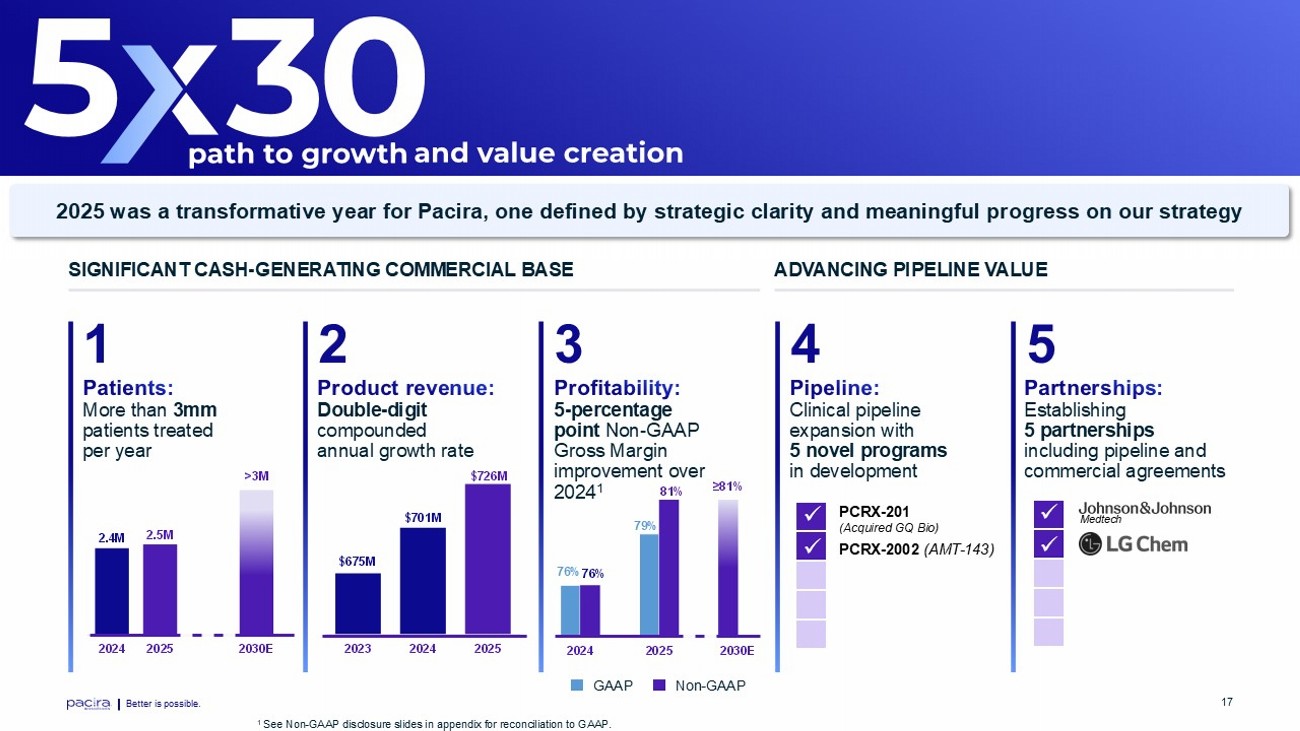

Better is possible. 17 Better is possible. SIGNIFICANT CASH - GENERATING COMMERCIAL BASE ADVANCING PIPELINE VALUE 1 2 3 4 5 More than 3mm patients treated per year Double - digit compounded annual growth rate 5 - percentage point N on - GAAP G ross M argin improvement over 2024 1 Clinical pipeline expansion with 5 novel programs in development Establishing 5 partnerships including pipeline and commercial agreements 2.4 M 2.5 M >3M 2024 2025 2030E $675M $701M $726M 2023 2024 2025 x x x x PCRX - 201 (Acquired GQ Bio) PCRX - 2002 (AMT - 143) Medtech 2025 was a transformative year for Pacira, one defined by strategic clarity and meaningful progress on our strategy 1 See Non - GAAP disclosure slides in appendix for reconciliation to GAAP. 76% 81% ≥ 81% 2024 2025 2030E 76% 79% Non - GAAP GAAP

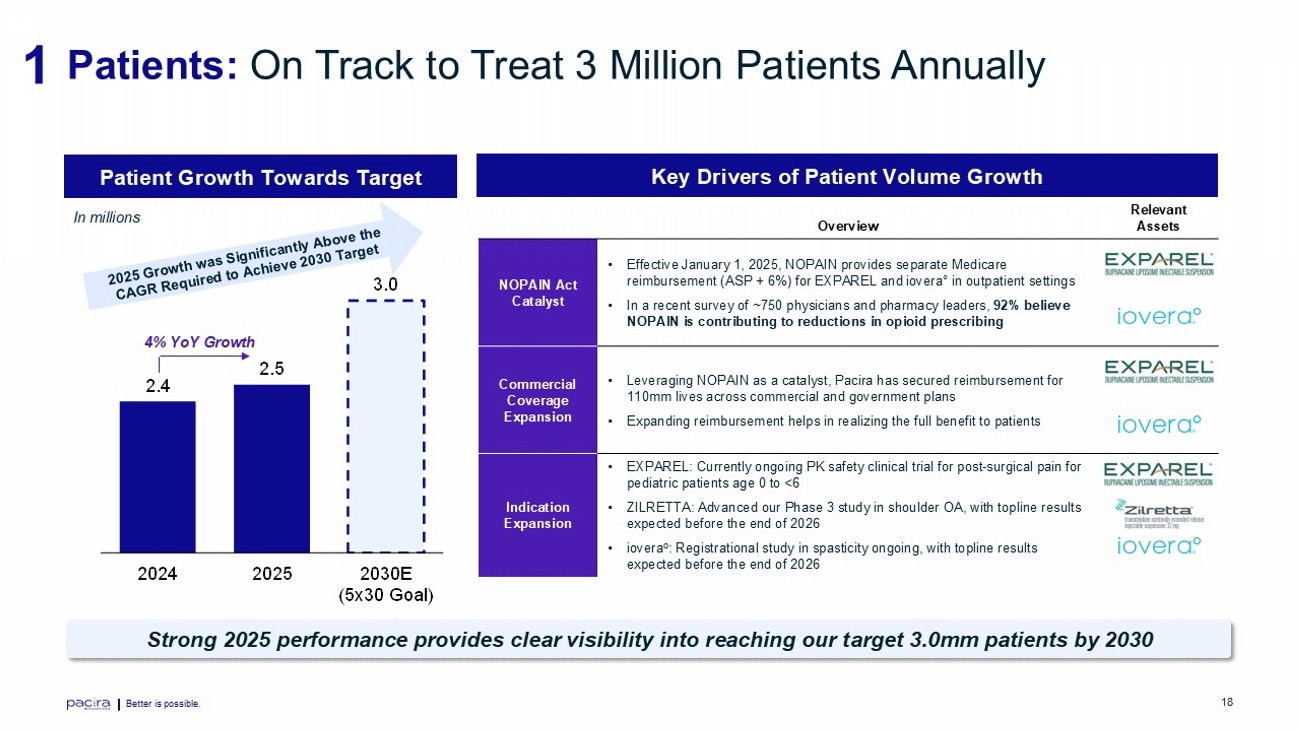

Better is possible. 18 2.4 2.5 3.0 2024 2025 2030E (5x30 Goal) 1 Patients: On Track to Treat 3 Million Patients Annually Patient Growth Towards Target Key Drivers of Patient Volume Growth Relevant Assets Overview • Effective January 1, 2025, NOPAIN provides separate Medicare reimbursement (ASP + 6%) for EXPAREL and iovera ° in outpatient settings • In a recent survey of ~750 physicians and pharmacy leaders, 92% believe NOPAIN is contributing to reductions in opioid prescribing NOPAIN Act Catalyst • Leveraging NOPAIN as a catalyst, Pacira has secured reimbursement for 110mm lives across commercial and government plans • Expanding reimbursement helps in realizing the full benefit to patients Commercial Coverage Expansion • EXPAREL: Currently ongoing PK safety clinical trial for post - surgical pain for pediatric patients age 0 to <6 • ZILRETTA: Advanced our Phase 3 study in shoulder OA, with topline results expected before the end of 2026 • iovera o : Registrational study in spasticity ongoing, with topline results expected before the end of 2026 Indication Expansion Strong 2025 performance p rovides clear v isibility into reaching o ur t arget 3.0mm patients by 2030 In millions 4% YoY Growth

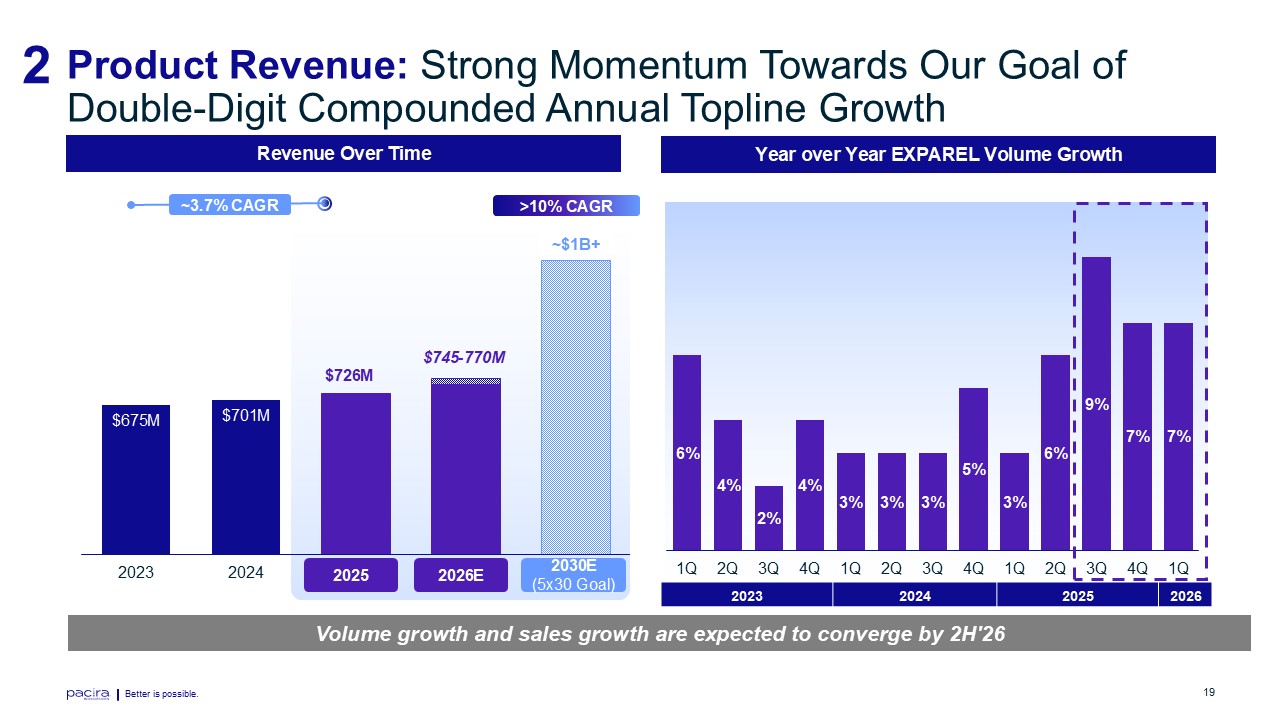

Better is possible. 19 2 Product Revenue: Strong Momentum Towards Our Goal of Double - Digit Compounded Annual Topline Growth Revenue Over Time Year over Year EXPAREL Volume Growth $726M ~2.6% CAGR >10% CAGR >$1.1B $745 - 770M $675M $701M 2023 2024 2025 2026 2030 2025 2030E (5x30 Goal) 2026E 6% 4% 2% 4% 3% 3% 3% 5% 3% 6% 9% 7% 7% 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2026 2025 2024 2023 Volume growth and sales growth are expected to converge by 2H'26

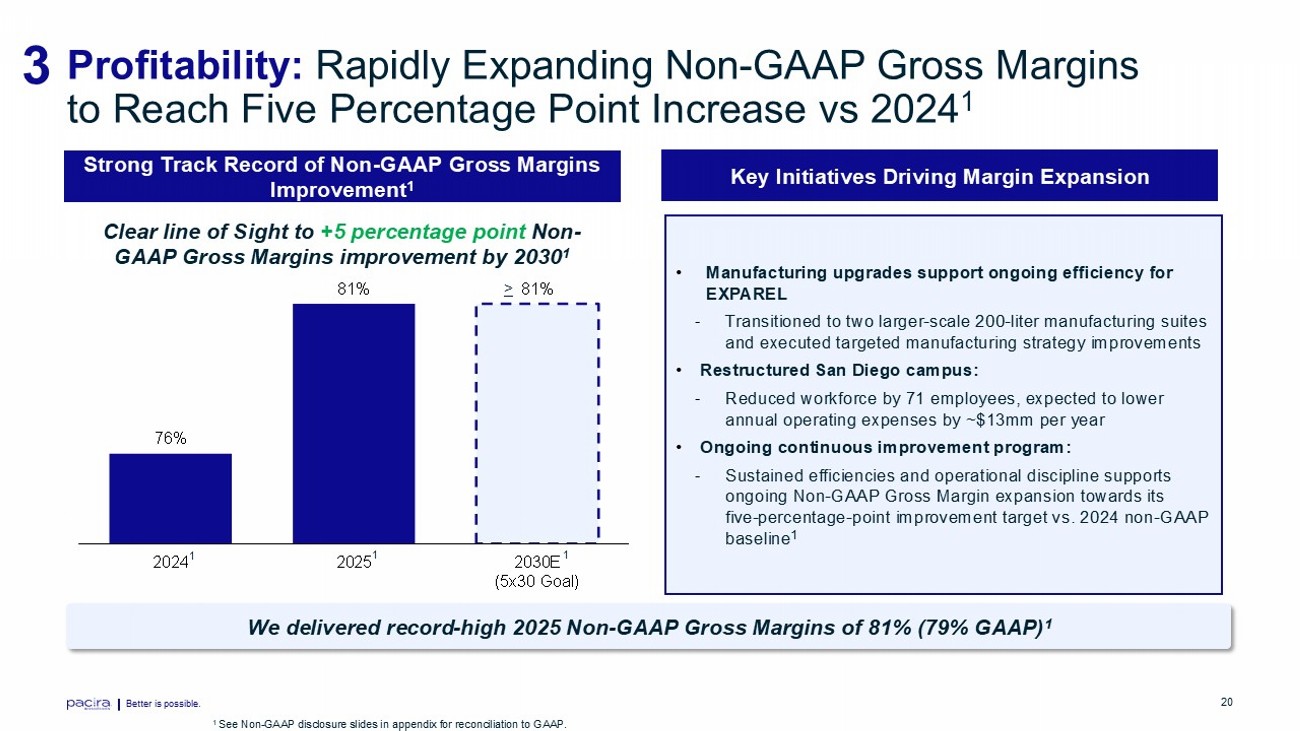

Better is possible. 20 • Manufacturing upgrades support ongoing efficiency for EXPAREL - Transitioned to two larger - scale 200 - liter manufacturing suites and executed targeted manufacturing strategy improvements • Restructured San Diego campus: - Reduced workforce by 71 employees, expected to lower annual operating expenses by ~$13mm per year • Ongoing continuous improvement program: - Sustained efficiencies and operational discipline supports ongoing Non - GAAP Gross Margin expansion towards its five - percentage - point improvement target vs. 2024 non - GAAP baseline 1 76% 81% 81% 2024 2025 2030E (5x30 Goal) Clear line of Sight to +5 percentage point Non - GAAP Gross Margins improvement by 2030 1 3 Profitability: Rapidly Expanding Non - GAAP Gross Margins to Reach Five Percentage Point Increase vs 2024 1 Strong Track Record of Non - GAAP Gross Margins Improvement 1 Key Initiatives Driving Margin Expansion We delivered record - high 2025 Non - GAAP Gross Margins of 81% (79% GAAP) 1 1 1 > 1 See Non - GAAP disclosure slides in appendix for reconciliation to GAAP. 1

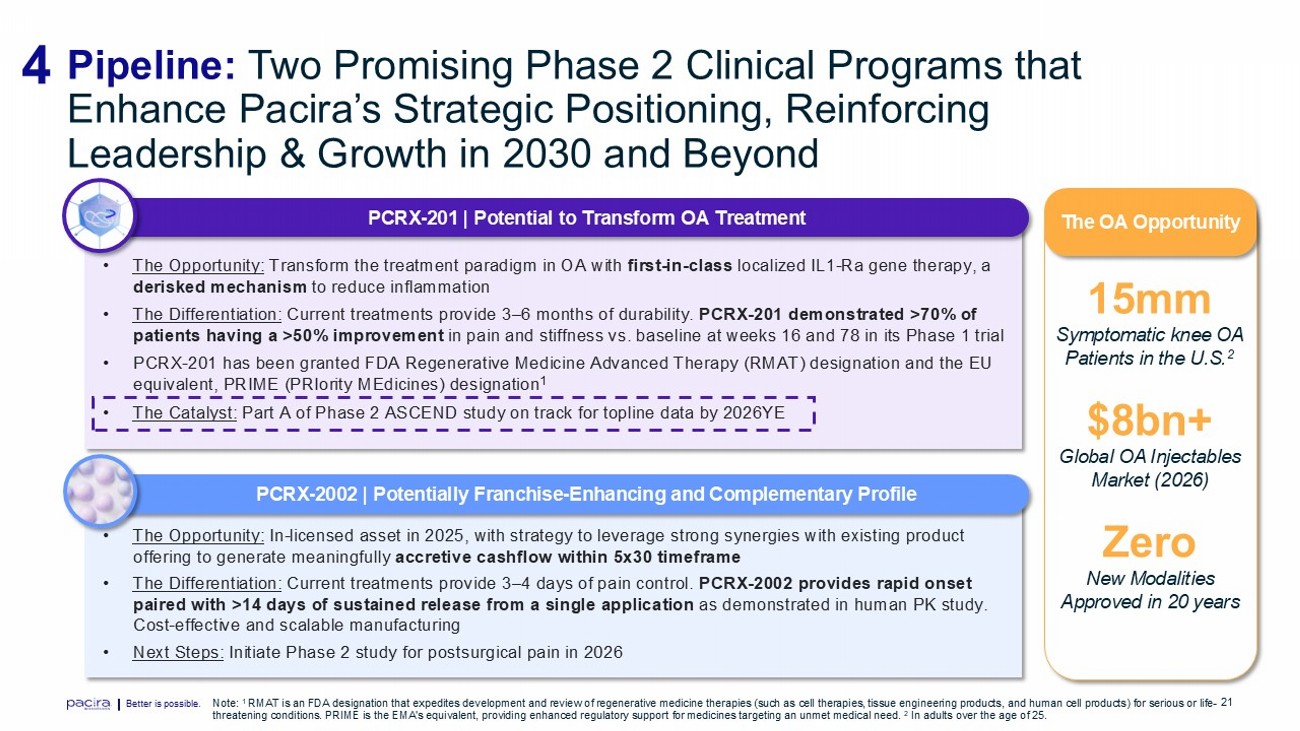

Better is possible. 21 4 Pipeline: Two Promising Phase 2 Clinical Programs that Enhance Pacira’s Strategic Positioning, Reinforcing Leadership & Growth in 2030 and Beyond Note: 1 RMAT is an FDA designation that expedites development and review of regenerative medicine therapies (such as cell therapies, tis sue engineering products, and human cell products) for serious or life - threatening conditions. PRIME is the EMA's equivalent, providing enhanced regulatory support for medicines targeting an unmet me dical need. 2 In adults over the age of 25. PCRX - 201 | Potential to Transform OA Treatment PCRX - 2002 | Potentially Franchise - Enhancing and Complementary Profile • The Opportunity: Transform the treatment paradigm in OA with first - in - class localized IL1 - Ra gene therapy, a derisked mechanism to reduce inflammation • The Differentiation: Current treatments provide 3 – 6 months of durability. PCRX - 201 demonstrated >70% of patients having a >50% improvement in pain and stiffness vs. baseline at weeks 16 and 78 in its Phase 1 trial • PCRX - 201 has been granted FDA Regenerative Medicine Advanced Therapy (RMAT) designation and the EU equivalent, PRIME ( PRIority MEdicines ) designation 1 • The Catalyst: Part A of Phase 2 ASCEND study on track for topline data by 2026YE • The Opportunity: In - licensed asset in 2025, with strategy to leverage strong synergies with existing product offering to generate meaningfully accretive cashflow within 5x30 timeframe • The Differentiation: Current treatments provide 3 – 4 days of pain control. PCRX - 2002 provides rapid onset paired with >14 days of sustained release from a single application as demonstrated in human PK study. Cost - effective and scalable manufacturing • Next Steps: Initiate Phase 2 study for postsurgical pain in 2026 The OA Opportunity Zero New Modalities Approved in 20 years 15mm Symptomatic knee OA Patients in the U.S. 2 $8bn+ Global OA Injectables Market (2026)

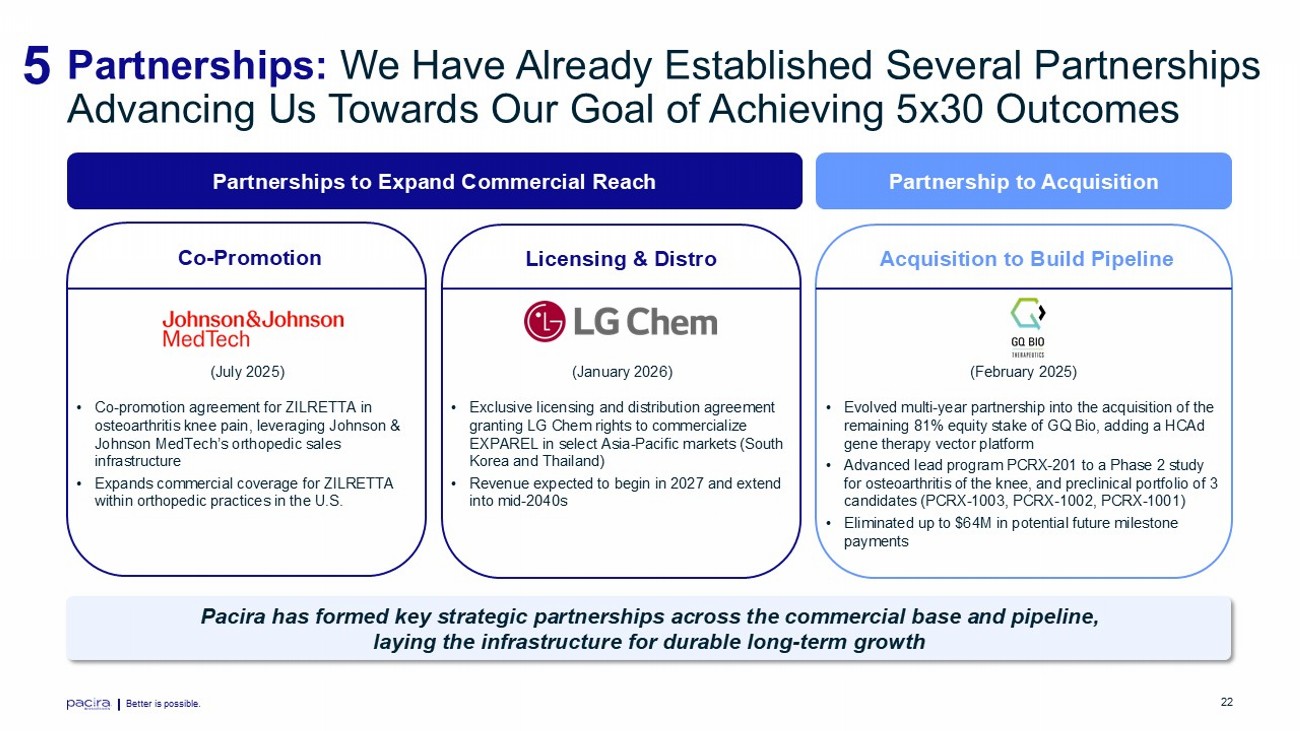

Better is possible. 22 Acquisition to Build Pipeline Pacira has formed key strategic partnerships across the commercial base and pipeline, laying the infrastructure for durable long - term growth Partnerships to Expand Commercial Reach Partnership to Acquisition Co - Promotion Licensing & Distro (July 2025) • Co - promotion agreement for ZILRETTA in osteoarthritis knee pain, leveraging Johnson & Johnson MedTech’s orthopedic sales infrastructure • Expands commercial coverage for ZILRETTA within orthopedic practices in the U.S. (February 2025) • Evolved multi - year partnership into the acquisition of the remaining 81% equity stake of GQ Bio, adding a HCAd gene therapy vector platform • Advanced lead program PCRX - 201 to a Phase 2 study for osteoarthritis of the knee, and preclinical portfolio of 3 candidates (PCRX - 1003, PCRX - 1002, PCRX - 1001) • Eliminated up to $64M in potential future milestone payments (January 2026) • Exclusive licensing and distribution agreement granting LG Chem rights to commercialize EXPAREL in select Asia - Pacific markets (South Korea and Thailand) • Revenue expected to begin in 2027 and extend into mid - 2040s 5 Partnerships: We Have Already Established Several Partnerships Advancing Us Towards Our Goal of Achieving 5x30 Outcomes

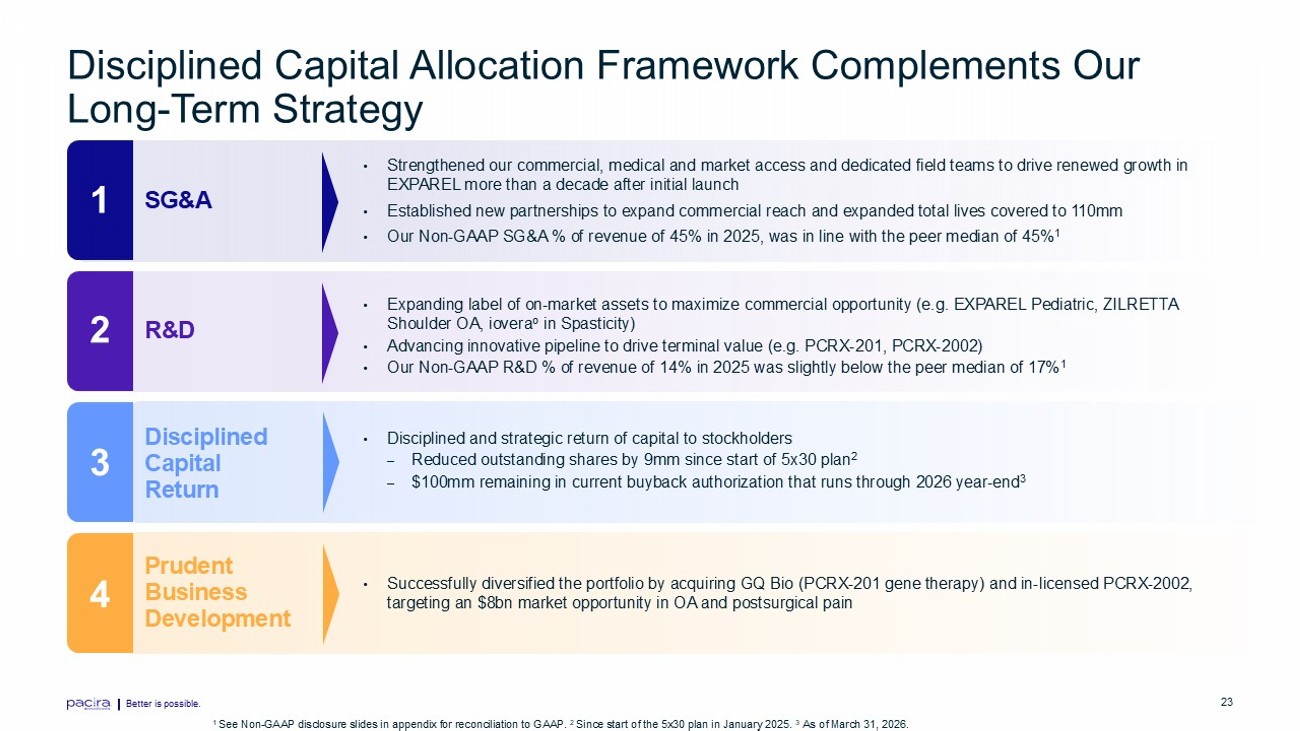

Better is possible. 23 Disciplined Capital Allocation Framework Complements Our Long - Term Strategy SG&A • Strengthened our commercial, medical and market access and dedicated field teams to drive renewed growth in EXPAREL more than a decade after initial launch • Established new partnerships to expand commercial reach and expanded total lives covered to 110mm • Our Non - GAAP SG&A % of revenue of 45% in 2025, was in line with the peer median of 45% 1 • Expanding label of on - market assets to maximize commercial opportunity (e.g. EXPAREL Pediatric, ZILRETTA Shoulder OA, iovera o in Spasticity) • Advancing innovative pipeline to drive terminal value (e.g. PCRX - 201, PCRX - 2002) • Our Non - GAAP R&D % of revenue of 14% in 2025 was slightly below the peer median of 17% 1 • Disciplined and strategic return of capital to stockholders – Reduced outstanding shares by 9mm since start of 5x30 plan 2 – $100mm remaining in current buyback authorization that runs through 2026 year - end 3 R&D Disciplined Capital Return 1 2 3 Better is possible. 1 See Non - GAAP disclosure slides in appendix for reconciliation to GAAP. 2 Since start of the 5x30 plan in January 2025. 3 As of March 31, 2026. • Successfully diversified the portfolio by acquiring GQ Bio (PCRX - 201 gene therapy) and in - licensed PCRX - 2002, targeting an $8bn market opportunity in OA and postsurgical pain Prudent Business Development 4

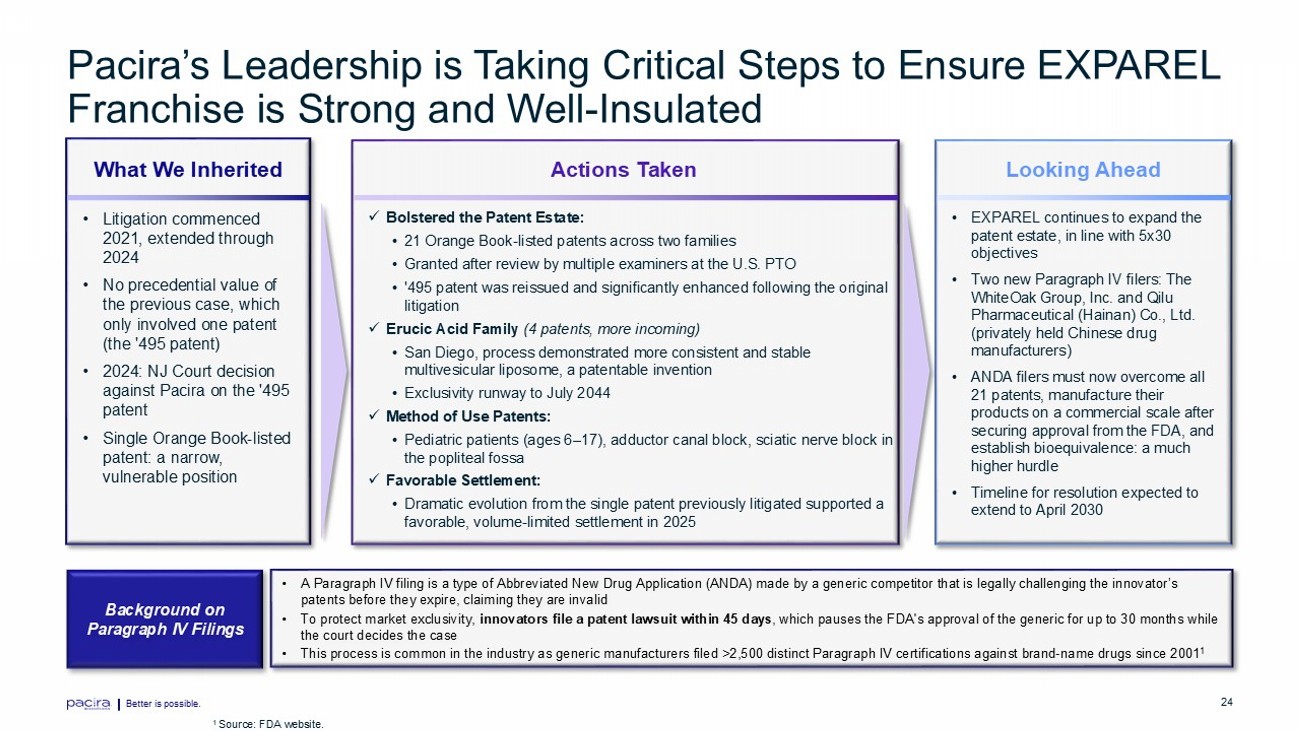

Better is possible. 24 What We Inherited Actions Taken Looking Ahead • Litigation commenced 2021, extended through 2024 • No precedential value of the previous case, which only involved one patent (the '495 patent) • 2024: NJ Court decision against Pacira on the '495 patent • Single Orange Book - listed patent: a narrow, vulnerable position x Bolstered the Patent Estate: • 21 Orange Book - listed patents across two families • Granted after review by multiple examiners at the U.S. PTO • '495 patent was reissued and significantly enhanced following the original litigation x Erucic Acid Family (4 patents, more incoming) • San Diego, process demonstrated more consistent and stable multivesicular liposome, a patentable invention • Exclusivity runway to July 2044 x Method of Use Patents: • Pediatric patients (ages 6 – 17), adductor canal block, sciatic nerve block in the popliteal fossa x Favorable Settlement: • Dramatic evolution from the single patent previously litigated supported a favorable, volume - limited settlement in 2025 • EXPAREL continues to expand the patent estate, in line with 5x30 objectives • Two new Paragraph IV filers: The WhiteOak Group, Inc. and Qilu Pharmaceutical (Hainan) Co., Ltd. (privately held Chinese drug manufacturers) • ANDA filers must now overcome all 21 patents, manufacture their products on a commercial scale after securing approval from the FDA, and establish bioequivalence: a much higher hurdle • Timeline for resolution expected to extend to April 2030 Pacira’s Leadership is Taking Critical Steps to Ensure EXPAREL Franchise is Strong and Well - Insulated • A Paragraph IV filing is a type of Abbreviated New Drug Application (ANDA) made by a generic competitor that is legally chall eng ing the innovator’s patents before they expire, claiming they are invalid • To protect market exclusivity, innovators file a patent lawsuit within 45 days , which pauses the FDA's approval of the generic for up to 30 months while the court decides the case • This process is common in the industry as generic manufacturers filed >2,500 distinct Paragraph IV certifications against bra nd - name drugs since 2001 1 Background on Paragraph IV Filings 1 Source: FDA website.

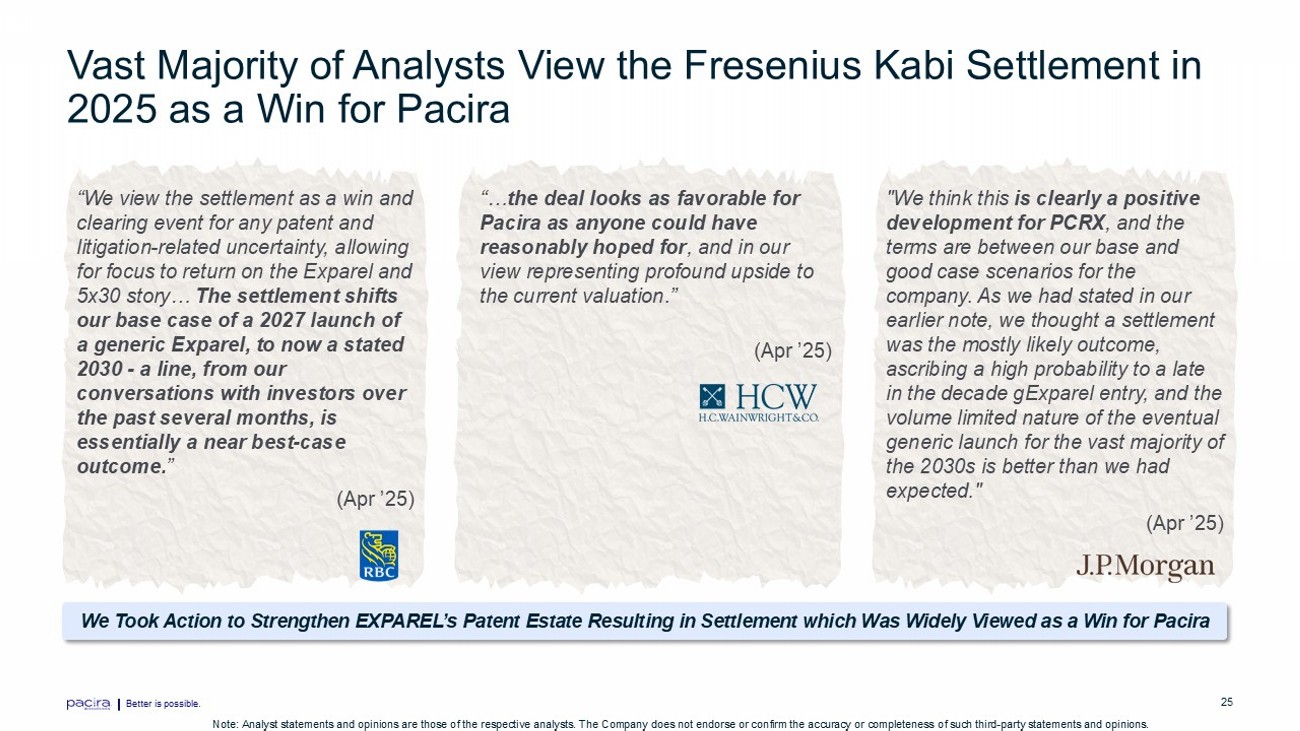

Better is possible. 25 Vast Majority of Analysts View the Fresenius Kabi Settlement in 2025 as a Win for Pacira “We view the settlement as a win and clearing event for any patent and litigation - related uncertainty, allowing for focus to return on the Exparel and 5x30 story… The settlement shifts our base case of a 2027 launch of a generic Exparel, to now a stated 2030 - a line, from our conversations with investors over the past several months, is essentially a near best - case outcome. ” (Apr ’25) “… the deal looks as favorable for Pacira as anyone could have reasonably hoped for , and in our view representing profound upside to the current valuation.” (Apr ’25) "We think this is clearly a positive development for PCRX , and the terms are between our base and good case scenarios for the company. As we had stated in our earlier note, we thought a settlement was the mostly likely outcome, ascribing a high probability to a late in the decade gExparel entry, and the volume limited nature of the eventual generic launch for the vast majority of the 2030s is better than we had expected." (Apr ’25) Note: Analyst statements and opinions are those of the respective analysts. The Company does not endorse or confirm the accur acy or completeness of such third - party statements and opinions. We Took Action to Strengthen EXPAREL’s Patent Estate Resulting in Settlement which Was Widely Viewed as a Win for Pacira

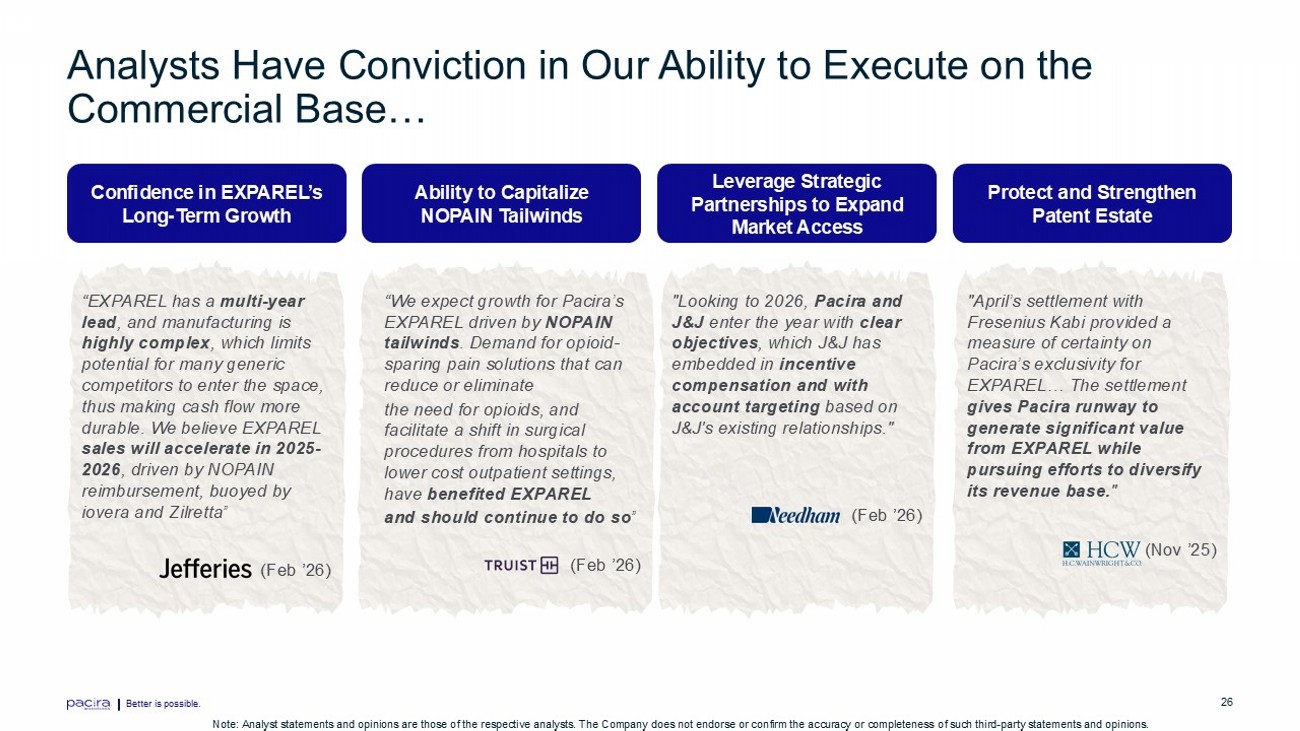

Better is possible. 26 Analysts Have Conviction in Our Ability to Execute on the Commercial Base… Confidence in EXPAREL’s Long - Term Growth Ability to Capitalize NOPAIN Tailwinds “EXPAREL has a multi - year lead , and manufacturing is highly complex , which limits potential for many generic competitors to enter the space, thus making cash flow more durable. We believe EXPAREL sales will accelerate in 2025 - 2026 , driven by NOPAIN reimbursement, buoyed by iovera and Zilretta ” (Feb ’26) “We expect growth for Pacira’s EXPAREL driven by NOPAIN tailwinds . Demand for opioid - sparing pain solutions that can reduce or eliminate the need for opioids, and facilitate a shift in surgical procedures from hospitals to lower cost outpatient settings, have benefited EXPAREL and should continue to do so ” (Feb ’26) Leverage Strategic Partnerships to Expand Market Access "Looking to 2026, Pacira and J&J enter the year with clear objectives , which J&J has embedded in incentive compensation and with account targeting based on J&J's existing relationships." (Feb ’26) Protect and Strengthen Patent Estate "April’s settlement with Fresenius Kabi provided a measure of certainty on Pacira’s exclusivity for EXPAREL… The settlement gives Pacira runway to generate significant value from EXPAREL while pursuing efforts to diversify its revenue base. " (Nov ’25) Note: Analyst statements and opinions are those of the respective analysts. The Company does not endorse or confirm the accur acy or completeness of such third - party statements and opinions.

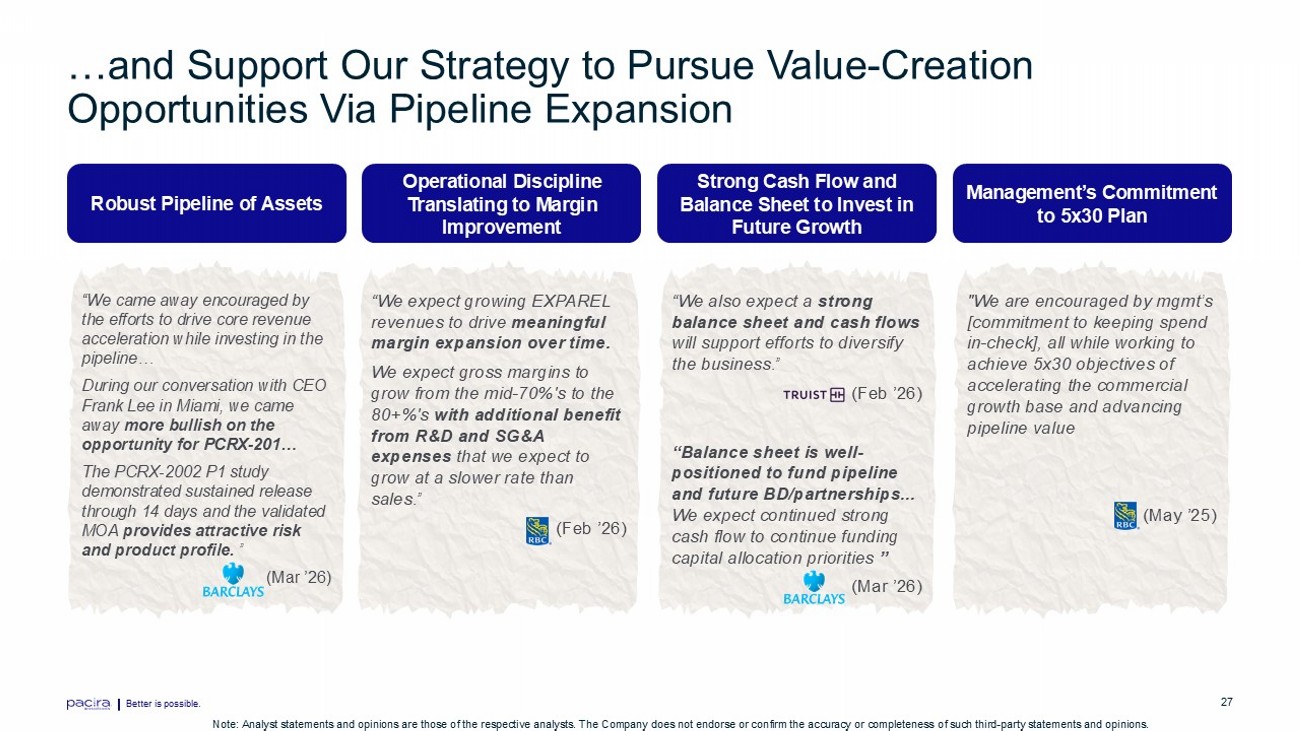

Better is possible. 27 …and Support Our Strategy to Pursue Value - Creation Opportunities Via Pipeline Expansion Robust Pipeline of Assets Operational Discipline Translating to Margin Improvement “We came away encouraged by the efforts to drive core revenue acceleration while investing in the pipeline… During our conversation with CEO Frank Lee in Miami, we came away more bullish on the opportunity for PCRX - 201… The PCRX - 2002 P1 study demonstrated sustained release through 14 days and the validated MOA provides attractive risk and product profile. ” (Mar ’26) “We expect growing EXPAREL revenues to drive meaningful margin expansion over time. We expect gross margins to grow from the mid - 70%'s to the 80+%'s with additional benefit from R&D and SG&A expenses that we expect to grow at a slower rate than sales.” (Feb ’26) Strong Cash Flow and Balance Sheet to Invest in Future Growth “We also expect a strong balance sheet and cash flows will support efforts to diversify the business.” (Feb ’26) “Balance sheet is well - positioned to fund pipeline and future BD/partnerships... We expect continued strong cash flow to continue funding capital allocation priorities ” (Mar ’26) Management’s Commitment to 5x30 Plan "We are encouraged by mgmt’s [commitment to keeping spend in - check], all while working to achieve 5x30 objectives of accelerating the commercial growth base and advancing pipeline value (May ’25) Note: Analyst statements and opinions are those of the respective analysts. The Company does not endorse or confirm the accur acy or completeness of such third - party statements and opinions.

Better is possible. 28 Seasoned Management Team with Deep Experience and Expertise Frank D. Lee Chief Executive Officer & Director Brendan Teehan Chief Commercial Officer Kristen Williams, Esq. Chief Administrative Officer & Secretary Jonathan Slonin , MD Chief Medical Officer Shawn Cross Chief Financial Officer Christopher Young Chief Manufacturing Officer Anthony Molloy III, Esq. Chief Legal & Compliance Officer Krys Corbett Chief Business Officer CEO, Forma Therapeutics 13+ years Genentech/Roche 13+ years Novartis/Janssen/Eli Lilly 6+ years Acadia Pharmaceuticals 13+ years Johnson & Johnson 11+ years Amgen/ Tesaro / RainTree 3 years Bioenvision Inc. 5 years Paul Hastings LLP 20 years board - certified anesthesiologist 20+ years biopharmaceutical investment banking experience 14+ years Actavis 4+ years Akorn Inc. 4+ years Alvogen Inc. 7+ years Patton Boggs LLP 6+ years The Okonite Company 10+ years Genentech/Roche 4+ years Lyell Immunopharma 2+ years ORIC Pharmaceuticals Select Prior Experience: Select Prior Experience: Select Prior Experience: Select Prior Experience: Select Prior Experience: Select Prior Experience: Select Prior Experience: Select Prior Experience:

Better is possible. 29 Pacira’s Highly Qualified Board is Effectively Overseeing Our Long - Term Strategy and Committed to Good Corporate Governance

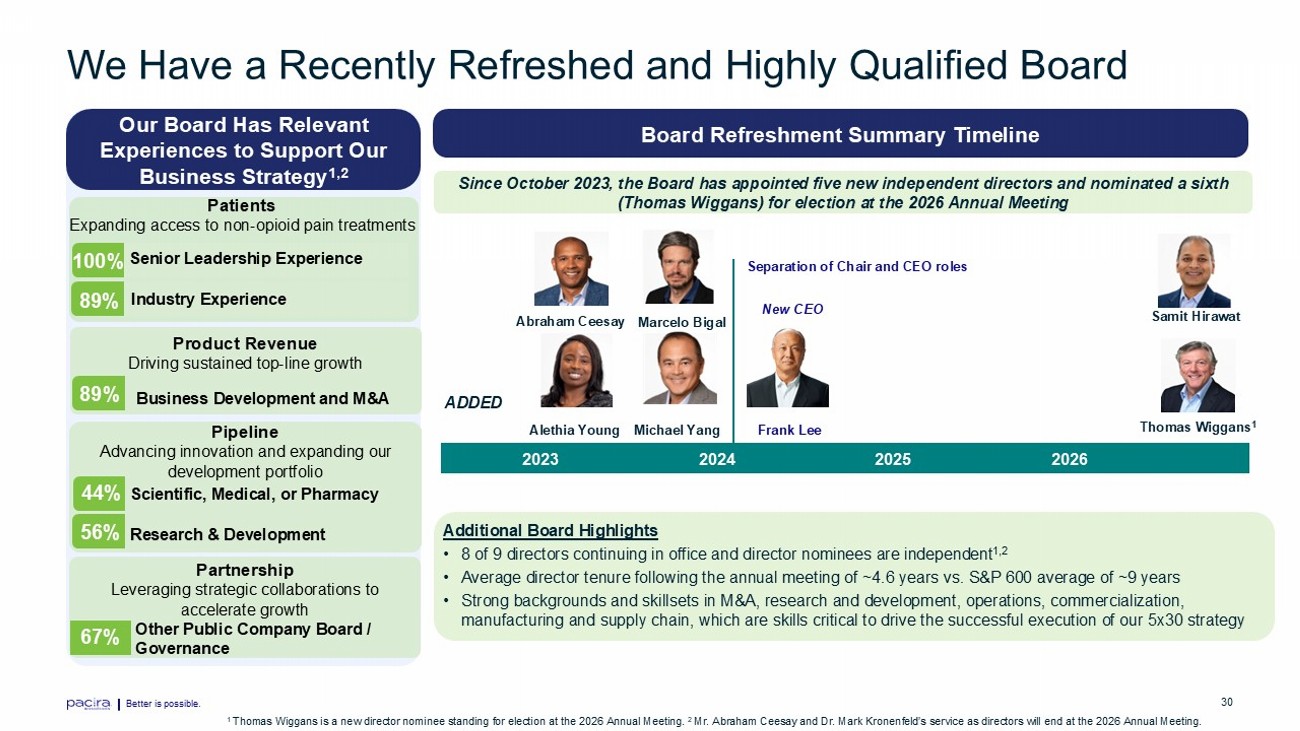

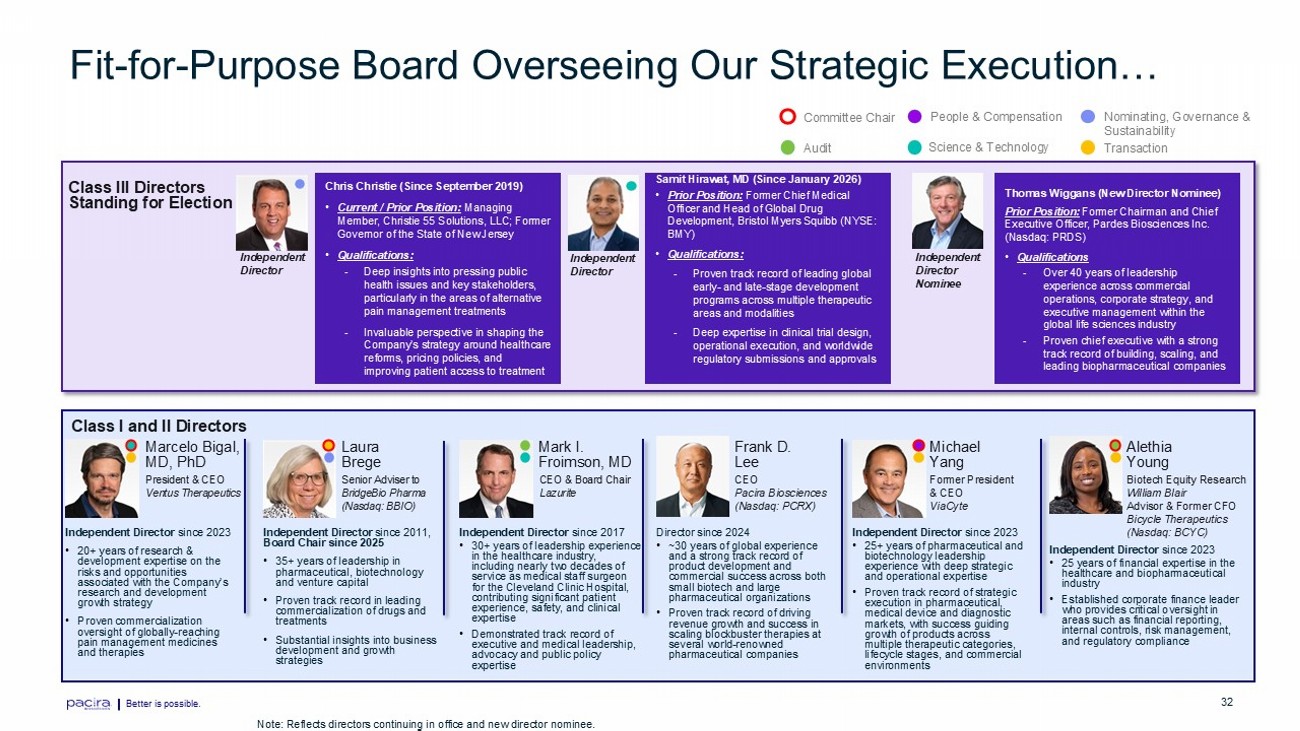

Better is possible. 30 We Have a Recently Refreshed and Highly Qualified Board Our Board Has Relevant Experiences to Support Our Business Strategy 1,2 Since October 2023, the Board has appointed five new independent directors and nominated a sixth (Thomas Wiggans) for election at the 2026 Annual Meeting 2023 2024 2025 2026 Alethia Young Michael Yang Marcelo Bigal Thomas Wiggans 1 Samit Hirawat 100% Senior Leadership Experience ADDED Frank Lee New CEO Separation of Chair and CEO roles 1 Thomas Wiggans is a new director nominee standing for election at the 2026 Annual Meeting. 2 Mr. Abraham Ceesay and Dr. Mark Kronenfeld’s service as directors will end at the 2026 Annual Meeting. Board Refreshment Summary Timeline Additional Board Highlights • 8 of 9 directors continuing in office and director nominees are independent 1,2 • Average director tenure following the annual meeting of ~4.6 years vs. S&P 600 average of ~9 years • Strong backgrounds and skillsets in M&A, research and development, operations, commercialization, manufacturing and supply chain, which are skills critical to drive the successful execution of our 5x30 strategy 89 % Industry Experience Patients Expanding access to non - opioid pain treatments 89 % Business Development and M&A Product Revenue Driving sustained top - line growth 44 % Scientific , Medical, or Pharmacy Pipeline Advancing innovation and expanding our development portfolio 67 % Other Publi c Company Board / Governance Partnership Leveraging strategic collaborations to accelerate growth Abraham Ceesay 56 % Research & Development

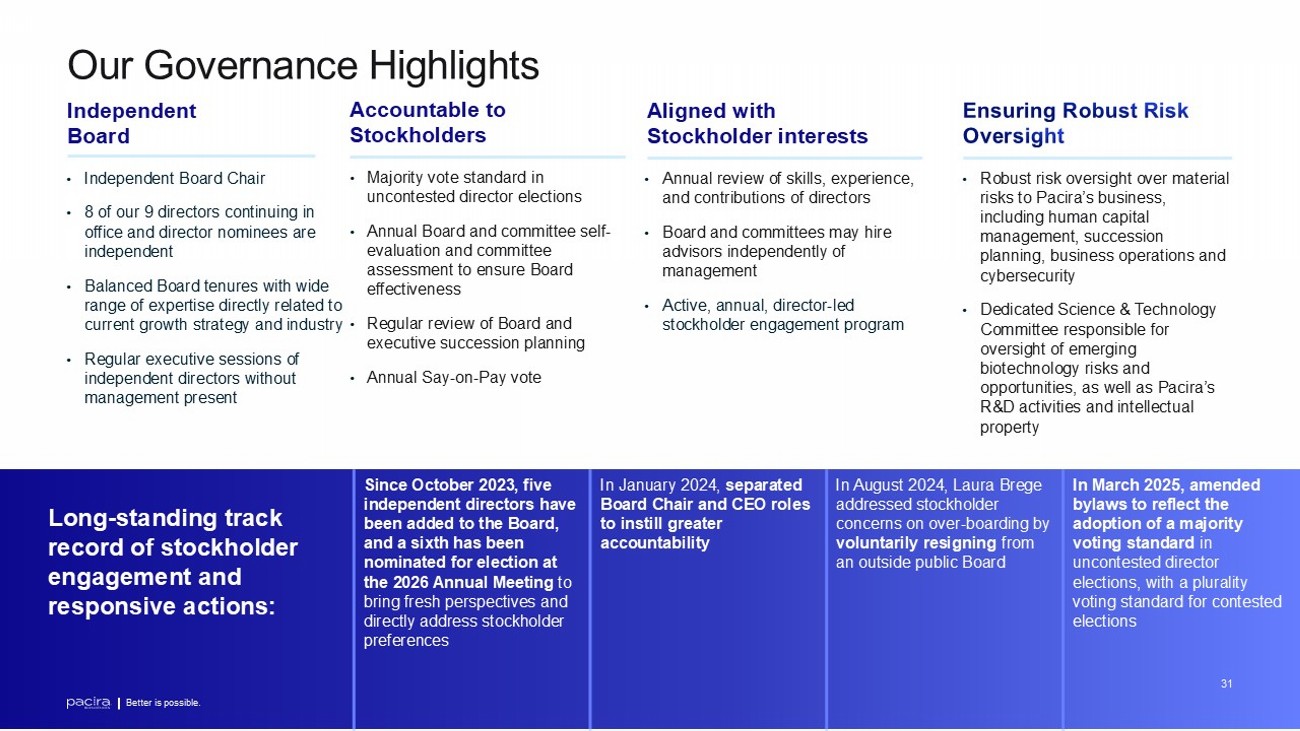

Better is possible. 31 • Independent Board Chair • 8 of our 9 directors continuing in office and director nominees are independent • Balanced Board tenures with wide range of expertise directly related to current growth strategy and industry • Regular executive sessions of independent directors without management present Independent Board Accountable to Stockholders Aligned with Stockholder interests • Majority vote standard in uncontested director elections • Annual Board and committee self - evaluation and committee assessment to ensure Board effectiveness • Regular review of Board and executive succession planning • Annual Say - on - Pay vote • Annual review of skills, experience, and contributions of directors • Board and committees may hire advisors independently of management • Active, annual, director - led stockholder engagement program • Robust risk oversight over material risks to Pacira’s business, including human capital management, succession planning, business operations and cybersecurity • Dedicated Science & Technology Committee responsible for oversight of emerging biotechnology risks and opportunities, as well as Pacira’s R&D activities and intellectual property Long - standing track record of stockholder engagement and responsive actions: In March 2025, amended bylaws to reflect the adoption of a majority voting standard in uncontested director elections, with a plurality voting standard for contested elections In August 2024, Laura Brege addressed stockholder concerns on over - boarding by voluntarily resigning from an outside public Board In January 2024, separated Board Chair and CEO roles to instill greater accountability Since October 2023, five independent directors have been added to the Board, and a sixth has been nominated for election at the 2026 Annual Meeting to bring fresh perspectives and directly address stockholder preferences 31 Better is possible. Our Governance Highlights

Better is possible. 32 Fit - for - Purpose Board Overseeing Our Strategic Execution… Committee Chair Class III Directors Standing for Election Class I and II Directors Senior Adviser to BridgeBio Pharma (Nasdaq: BBIO) Independent Director since 2011, Board Chair since 2025 • 35+ years of leadership in pharmaceutical, biotechnology and venture capital • Proven track record in leading commercialization of drugs and treatments • Substantial insights into business development and growth strategies President & CEO Ventus Therapeutics Independent Director since 2023 • 20+ years of research & development expertise on the risks and opportunities associated with the Company’s research and development growth strategy • P roven commercialization oversight of globally - reaching pain management medicines and therapies Marcelo Bigal , MD, PhD Mark I. Froimson , MD CEO & Board Chair Lazurite Independent Director since 2017 • 30+ years of leadership experience in the healthcare industry, including nearly two decades of service as medical staff surgeon for the Cleveland Clinic Hospital, contributing significant patient experience, safety, and clinical expertise • Demonstrated track record of executive and medical leadership, advocacy and public policy expertise Laura Brege Director since 2024 • ~30 years of global experience and a strong track record of product development and commercial success across both small biotech and large pharmaceutical organizations • Proven track record of driving revenue growth and success in scaling blockbuster therapies at several world - renowned pharmaceutical companies Frank D. Lee CEO Pacira Biosciences (Nasdaq: PCRX) Former President & CEO ViaCyte Independent Director since 2023 • 25+ years of pharmaceutical and biotechnology leadership experience with deep strategic and operational expertise • Proven track record of strategic execution in pharmaceutical, medical device and diagnostic markets, with success guiding growth of products across multiple therapeutic categories, lifecycle stages, and commercial environments Michael Yang Biotech Equity Research William Blair Advisor & Former CFO Bicycle Therapeutics (Nasdaq: BCYC) Independent Director since 2023 • 25 years of financial expertise in the healthcare and biopharmaceutical industry • Established corporate finance leader who provides critical o versight in areas such as financial reporting, internal controls, risk management, and regulatory compliance Alethia Young Chris Christie (Since September 2019) • Current / Prior Position: Managing Member, Christie 55 Solutions, LLC; Former Governor of the State of New Jersey • Qualifications: - Deep insights into pressing public health issues and key stakeholders, particularly in the areas of alternative pain management treatments - Invaluable perspective in shaping the Company’s strategy around healthcare reforms, pricing policies, and improving patient access to treatment Samit Hirawat , MD (Since January 2026) • Prior Position: Former Chief Medical Officer and Head of Global Drug Development, Bristol Myers Squibb (NYSE: BMY) • Qualifications: - Proven track record of leading global early - and late - stage development programs across multiple therapeutic areas and modalities - Deep expertise in clinical trial design, operational execution, and worldwide regulatory submissions and approvals Thomas Wiggans (New Director Nominee) Prior Position: Former Chairman and Chief Executive Officer, Pardes Biosciences Inc. (Nasdaq: PRDS) • Qualifications - Over 40 years of leadership experience across commercial operations, corporate strategy, and executive management within the global life sciences industry - Proven chief executive with a strong track record of building, scaling, and leading biopharmaceutical companies Audit People & Compensation Science & Technology Nominating, Governance & Sustainability Transaction Independent Director Independent Director Independent Director Nominee Note: Reflects directors continuing in office and new director nominee. Better is possible.

Better is possible. 33 Total Young Yang Wiggans Lee Hirawat Froimson Christie Brege Bigal Director Skills and Experience 3 / 9 Academia 4 / 9 Accounting & Finance 8 / 9 Business Development / M&A 6 / 9 Corporate Governance / Public Board Service 3 / 9 Cybersecurity & Information Technology 4 / 9 Government, Public Policy & Regulatory Affairs 9 / 9 Human Capital Management 8 / 9 Industry Experience 3 / 9 Operations, Manufacturing & Supply Chain 5 / 9 Research & Development 4 / 9 Scientific, Medical & Pharmacy 9 / 9 Senior Leadership ...with a Mix of Complementary Skillsets Note: Reflects directors continuing in office and new director nominee.

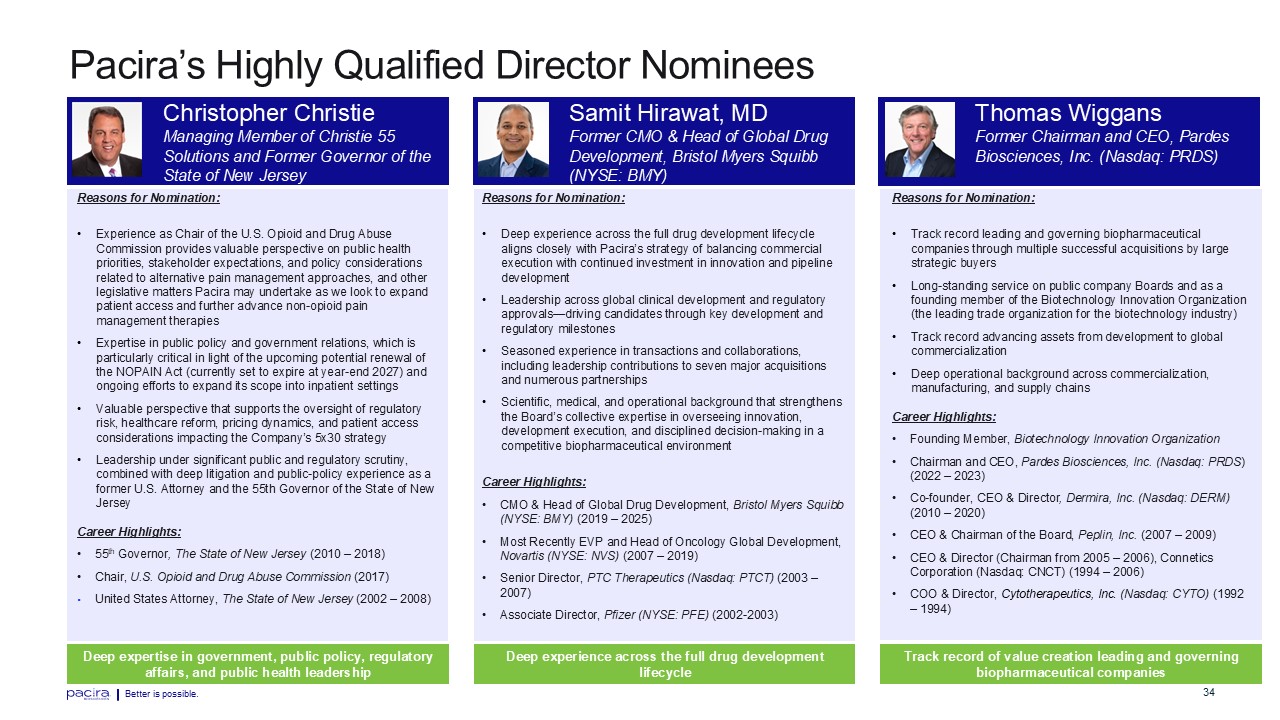

Better is possible. 34 Christopher Christie Managing Member of Christie 55 Solutions and Former Governor of the State of New Jersey Deep expertise in government, public policy, regulatory affairs, and public health leadership Samit Hirawat , MD Former CMO & Head of Global Drug Development, Bristol Myers Squibb (NYSE: BMY) Deep experience across the full drug development lifecycle Thomas Wiggans Former Chair man and CEO, Pardes Biosciences, Inc. (Nasdaq: PRDS) Track record of value creation leading and governing biopharmaceutical companies Reasons for Nomination: • Experience as Chair of the U.S. Opioid and Drug Abuse Commission provides valuable perspective on public health priorities, stakeholder expectations, and policy considerations related to alternative pain management approaches, and other legislative matters Pacira may undertake as we look to expand patient access and further advance non - opioid pain management therapies • Valuable perspective that supports the oversight of regulatory risk, healthcare reform, pricing dynamics, and patient access considerations impacting the Company’s 5x30 strategy • Leadership under significant public and regulatory scrutiny, combined with deep litigation and public - policy experience as a former U.S. Attorney and the 55th Governor of the State of New Jersey Career Highlights: • 55 th Governor , The State of New Jersey ( 2010 – 2018) • Chair, U.S. Opioid and Drug Abuse Commission (2017) • United States Attorney, The State of New Jersey (2002 – 2008) Reasons for Nomination: • Deep experience across the full drug development lifecycle aligns closely with Pacira’s strategy of balancing commercial execution with continued investment in innovation and pipeline development • Leadership across global clinical development and regulatory approvals — driving candidates through key development and regulatory milestones • Seasoned experience in transactions and collaborations, including leadership contributions to seven major acquisitions and numerous partnerships • Scientific, medical, and operational background that strengthens the Board’s collective expertise in overseeing innovation, development execution, and disciplined decision - making in a competitive biopharmaceutical environment Career Highlights: • CMO & Head of Global Drug Development, Bristol Myers Squibb (NYSE: BMY) (2019 – 2025) • Most Recently EVP and Head of Oncology Global Development, Novartis (NYSE: NVS) (2007 – 2019) • Senior Director, PTC Therapeutics (Nasdaq: PTCT) (2003 – 2007) • Associate Director, Pfizer (NYSE: PFE) (2002 - 2003) Reasons for Nomination: • Track record leading and governing biopharmaceutical companies through multiple successful acquisitions by large strategic buyers • Long - standing service on public company Boards and as a founding member of the Biotechnology Innovation Organization (the leading trade organization for the biotechnology industry) • Track record advancing assets from development to global commercialization • Deep operational background across commercialization, manufacturing, and supply chains Career Highlights: • Founding Member, Biotechnology Innovation Organization (1993 – Present) • Chairman and CEO, Pardes Biosciences, Inc. (Nasdaq: PRDS ) (2022 – 2023) • Co - founder, CEO & Director , Dermira , Inc. (Nasdaq: DERM) (2010 – 2020) • CEO & Chairman of the Board, Peplin, Inc. (2007 – 2009) • Most recently CEO & Chairman, Connetics Corporation (Nasdaq: CNCT) (1994 – 2006) • COO & Director, Cytotherapeutics , Inc . (Nasdaq: CYTO) (1992 – 1994) Pacira’s Highly Qualified Director Nominees

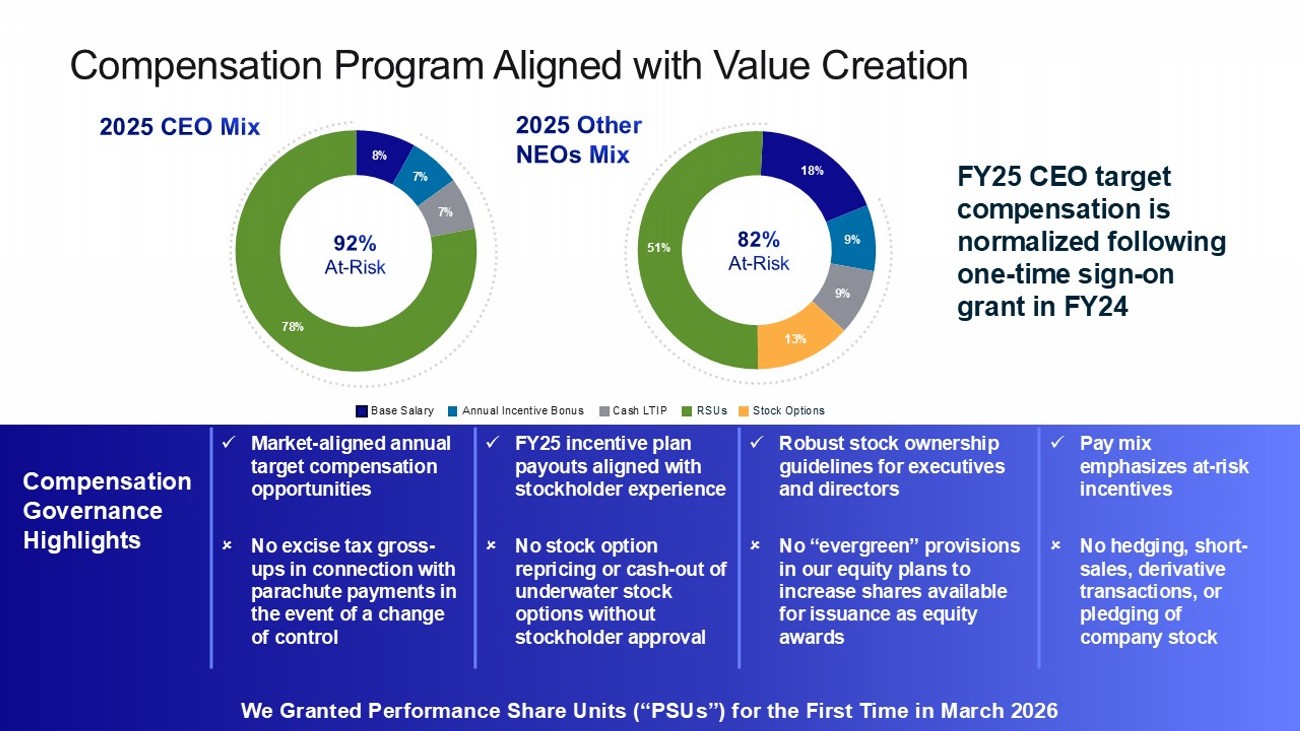

Better is possible. 35 8 % 7 % 7 % 78 % 18 % 9 % 9 % 13 % 51 % Compensation Governance Highlights x Pay mix emphasizes at - risk incentives x Robust stock ownership guidelines for executives and directors x FY25 incentive plan payouts aligned with stockholder experience x Market - aligned annual target compensation opportunities No hedging, short - sales, derivative transactions, or pledging of company stock No “evergreen” provisions in our equity plans to increase shares available for issuance as equity awards No stock option repricing or cash - out of underwater stock options without stockholder approval No excise tax gross - ups in connection with parachute payments in the event of a change of control ■ Base Salary ■ Annual Incentive Bonus ■ Cash LTIP ■ RSUs ■ Stock Options FY25 CEO target compensation is normalized following one - time sign - on grant in FY24 Compensation Program Aligned with Value Creation We Granted Performance Share Units (“PSUs”) for the First Time in March 2026

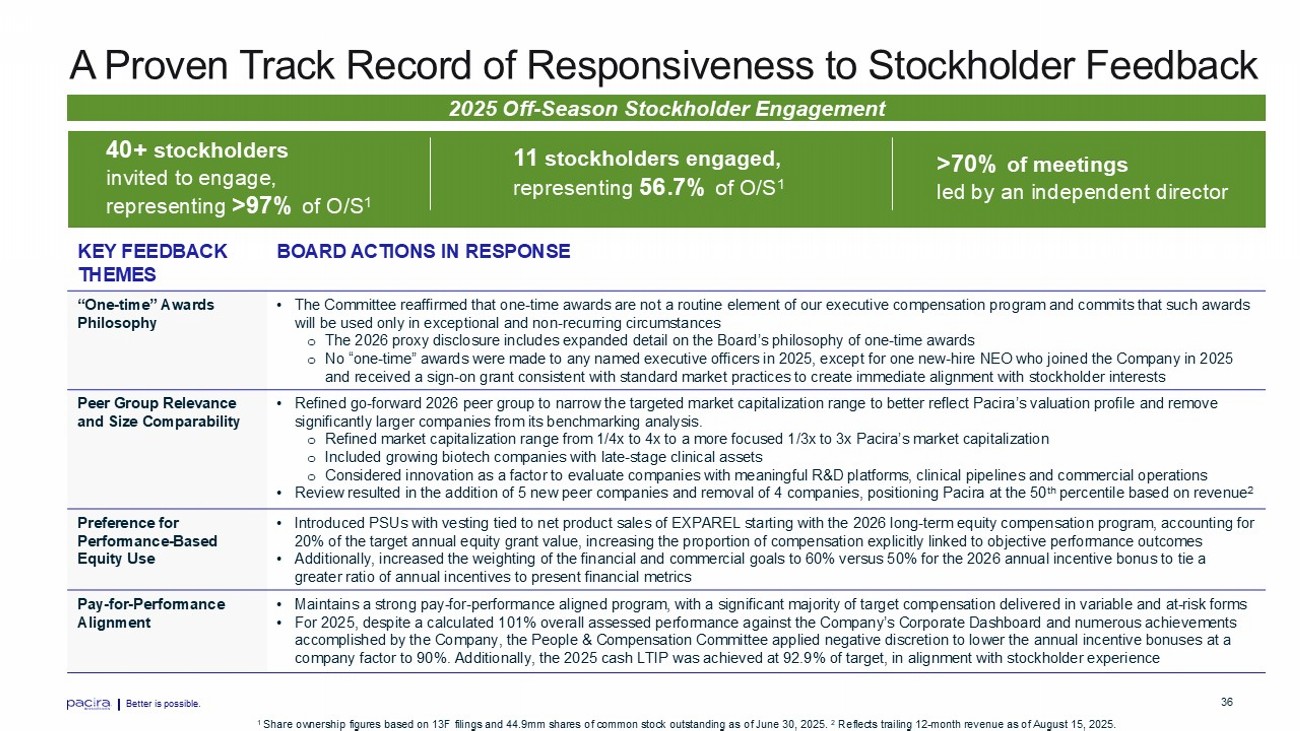

Better is possible. 36 BOARD ACTIONS IN RESPONSE KEY FEEDBACK THEMES • The Committee reaffirmed that one - time awards are not a routine element of our executive compensation program and commits that s uch awards will be used only in exceptional and non - recurring circumstances o The 2026 proxy disclosure includes expanded detail on the Board’s philosophy of one - time awards o No “one - time” awards were made to any named executive officers in 2025, except for one new - hire NEO who joined the Company in 20 25 and received a sign - on grant consistent with standard market practices to create immediate alignment with stockholder interests “One - time” Awards Philosophy • Refined go - forward 2026 peer group to narrow the targeted market capitalization range to better reflect Pacira’s valuation profi le and remove significantly larger companies from its benchmarking analysis. o Refined market capitalization range from 1/4x to 4x to a more focused 1/3x to 3x Pacira’s market capitalization o Included growing biotech companies with late - stage clinical assets o Considered innovation as a factor to evaluate companies with meaningful R&D platforms, clinical pipelines and commercial oper ati ons • Review resulted in the addition of 5 new peer companies and removal of 4 companies, positioning Pacira at the 50 th percentile based on revenue 2 Peer Group Relevance and Size Comparability • Introduced PSUs with vesting tied to net product sales of EXPAREL starting with the 2026 long - term equity compensation program, accounting for 20% of the target annual equity grant value, increasing the proportion of compensation explicitly linked to objective perform anc e outcomes • Additionally, increased the weighting of the financial and commercial goals to 60% versus 50% for the 2026 annual incentive b onu s to tie a greater ratio of annual incentives to present financial metrics Preference for Performance - Based Equity Use • Maintains a strong pay - for - performance aligned program, with a significant majority of target compensation delivered in variable and at - risk forms • For 2025, despite a calculated 101% overall assessed performance against the Company’s Corporate Dashboard and numerous achie vem ents accomplished by the Company, the People & Compensation Committee applied negative discretion to lower the annual incentive bo nus es at a company factor to 90%. Additionally, the 2025 cash LTIP was achieved at 92.9% of target, in alignment with stockholder experi enc e Pay - for - Performance Alignment 40+ stockholders invited to engage, representing >97% of O/S 1 11 stockholders engaged, representing 56.7 % of O /S 1 >70% of meetings led by an independent director 2025 Off - Season Stockholder Engagement A Proven Track Record of Responsiveness to Stockholder Feedback 1 Share ownership figures based on 13F filings and 44.9mm shares of common stock outstanding as of June 30, 2025. 2 Reflects trailing 12 - month revenue as of August 15, 2025.

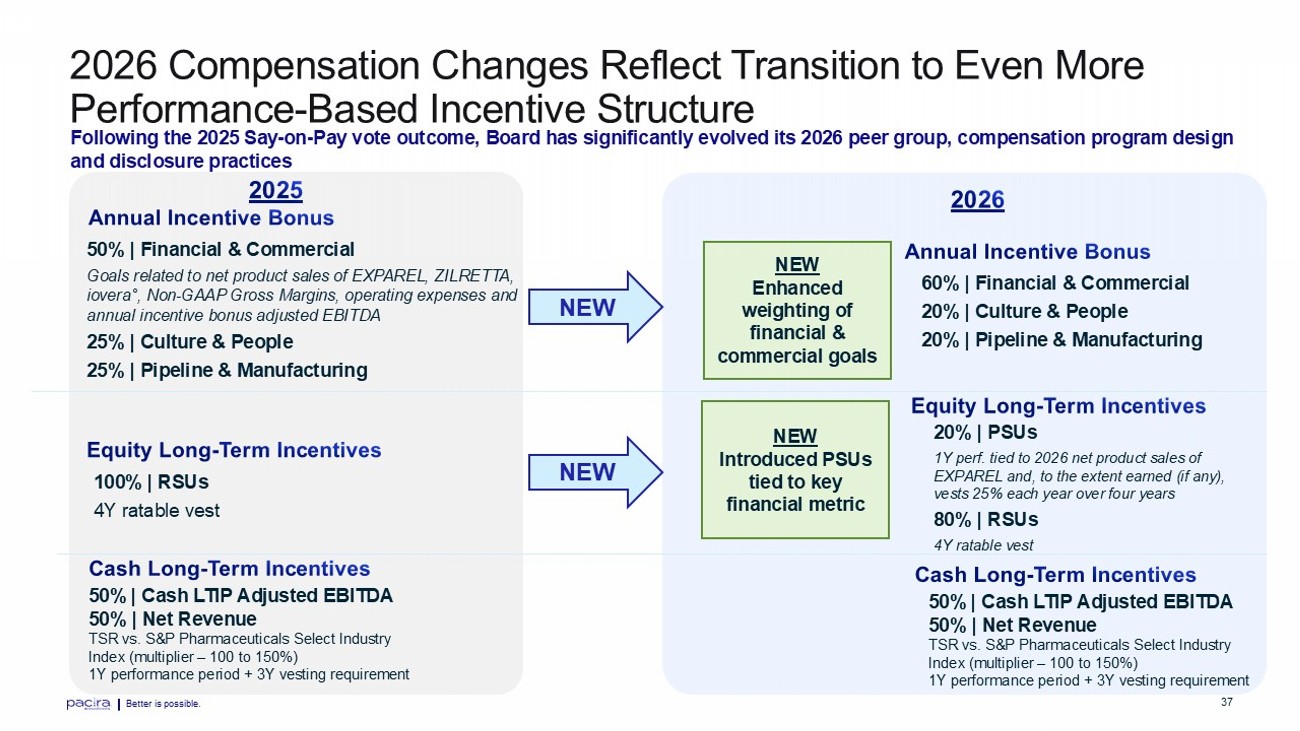

Better is possible. 37 20% | PSUs 1Y perf. tied to 2026 net product sales of EXPAREL and, to the extent earned (if any), vests 25% each year over four years 80 % | RSUs 4Y ratable vest Following the 2025 Say - on - Pay vote outcome, Board has significantly evolved its 2026 peer group, compensation program design and disclosure practices NEW Enhanced weighting of financial & commercial goals 50% | Cash LTIP Adjusted EBITDA 50% | Net Revenue TSR vs. S&P Pharmaceuticals Select Industry Index (multiplier – 100 to 150%) 1Y performance period + 3Y vesting requirement 100% | RSUs 4Y ratable vest 50% | Financial & Commercial Goals related to net product sales of EXPAREL, ZILRETTA, iovera ° , Non - GAAP Gross Margins, operating expenses and annual incentive bonus adjusted EBITDA 25% | Culture & People 25% | Pipeline & Manufacturing 60% | Financial & Commercial 20% | Culture & People 20% | Pipeline & Manufacturing NEW NEW Introduced PSUs tied to key financial metric NEW 50% | Cash LTIP Adjusted EBITDA 50% | Net Revenue TSR vs. S&P Pharmaceuticals Select Industry Index (multiplier – 100 to 150%) 1Y performance period + 3Y vesting requirement 2026 Compensation Changes Reflect Transition to Even More Performance - Based Incentive Structure

Better is possible. 38 DOMA’s Campaign is Highly Misguided and Not in the Best Interest of All Stockholders

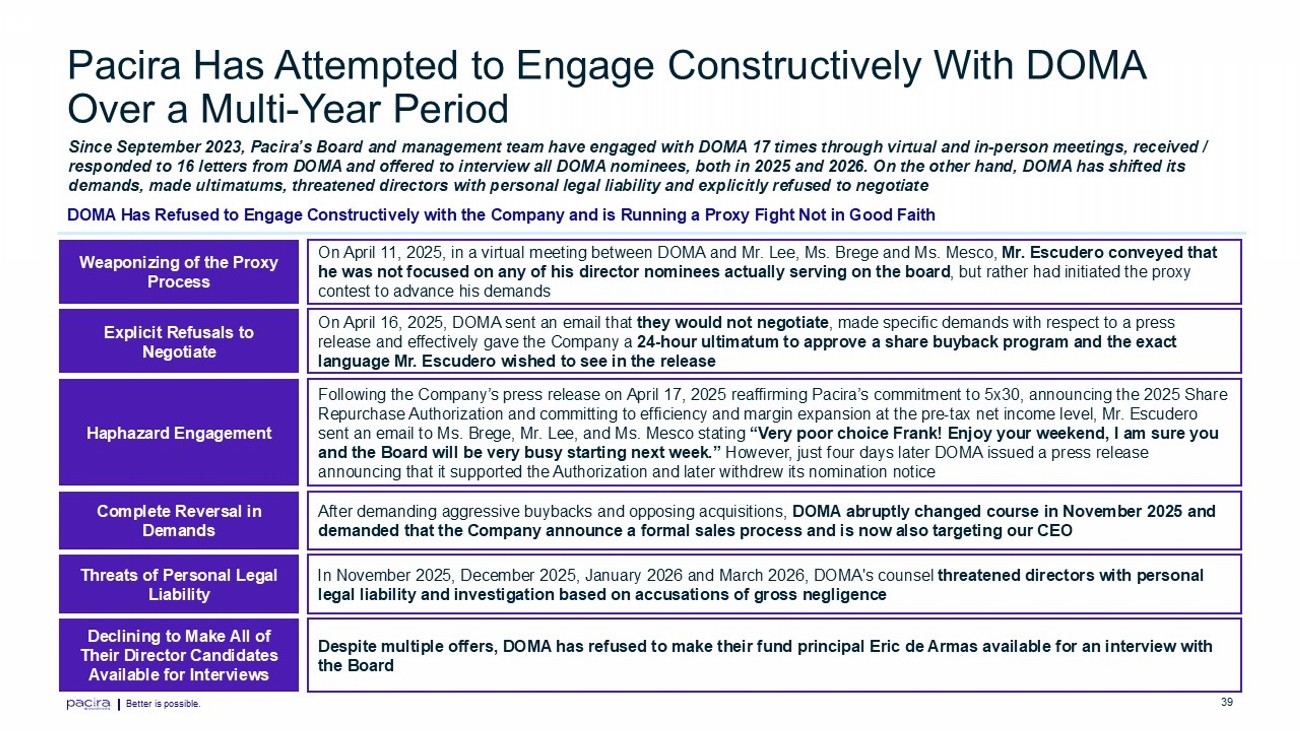

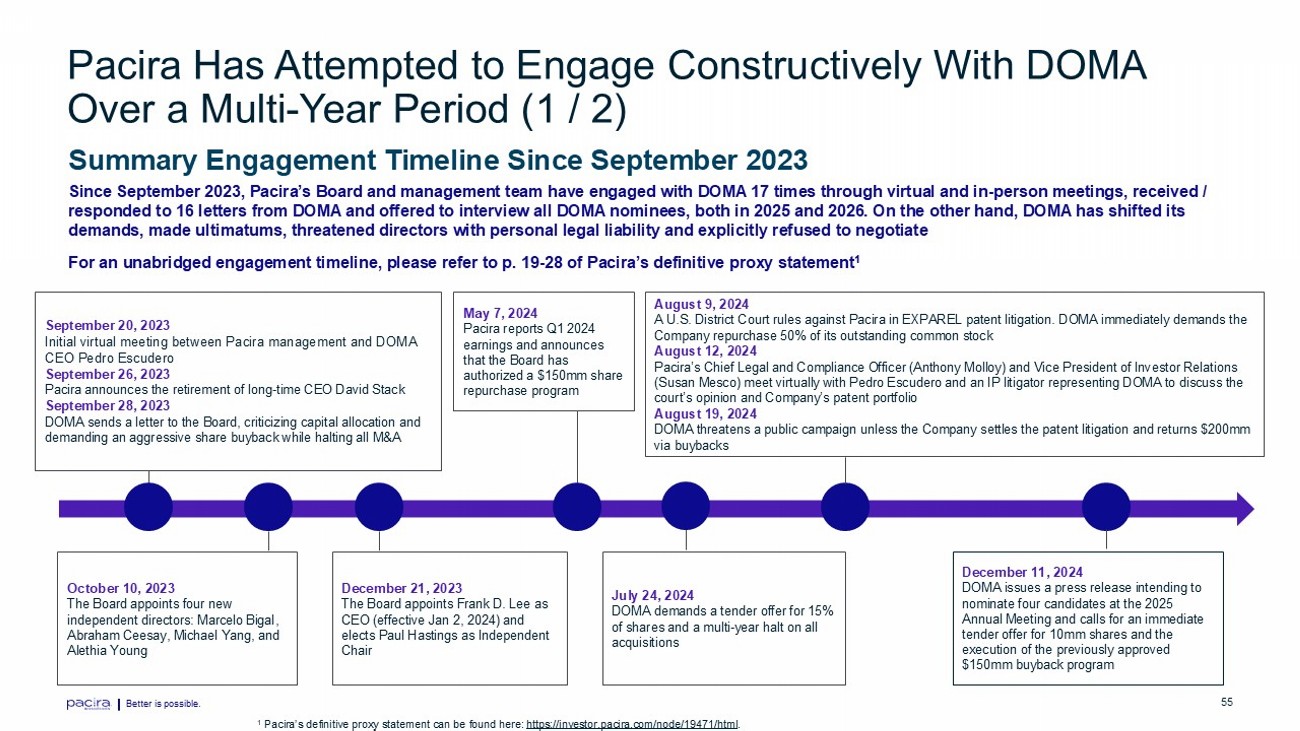

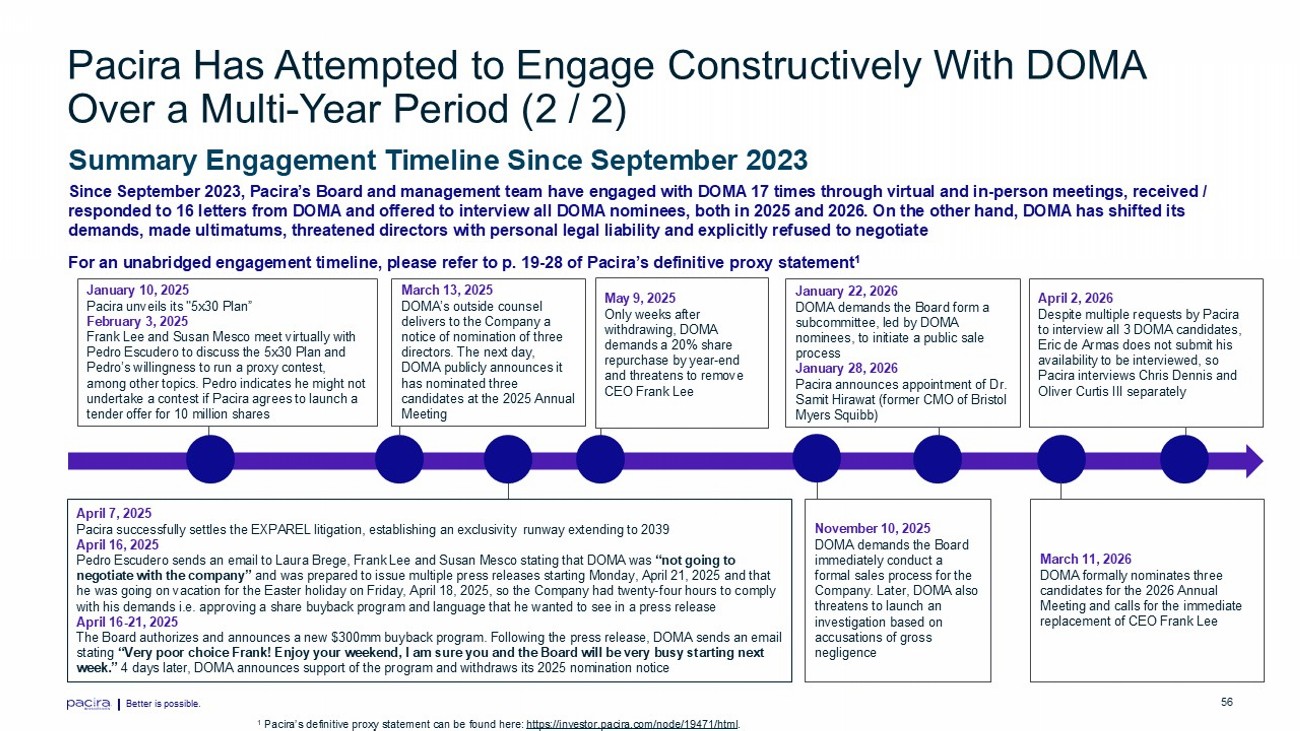

Better is possible. 39 Pacira Has Attempted to Engage Constructively With DOMA Over a Multi - Year Period Since September 2023, Pacira’s Board and management team have engaged with DOMA 17 times through virtual and in - person meetings, received / responded to 16 letters from DOMA and offered to interview all DOMA nominees, both in 2025 and 2026. On the other hand, DOMA has shifted its demands, made ultimatums, threatened directors with personal legal liability and explicitly refused to negotiate DOMA Has Refused to Engage Constructively with the Company and is Running a Proxy Fight Not in Good Faith Weaponizing of the Proxy Process On April 11, 2025, in a virtual meeting between DOMA and Mr. Lee, Ms. Brege and Ms. Mesco, Mr. Escudero conveyed that he was not focused on any of his director nominees actually serving on the board , but rather had initiated the proxy contest to advance his demands Explicit Refusals to Negotiate On April 16, 2025, DOMA sent an email that they would not negotiate , made specific demands with respect to a press release and effectively gave the Company a 24 - hour ultimatum to approve a share buyback program and the exact language Mr. Escudero wished to see in the release Haphazard Engagement Following the Company’s press release on April 17, 2025 reaffirming Pacira’s commitment to 5x30, announcing the 2025 Share Repurchase Authorization and committing to efficiency and margin expansion at the pre - tax net income level, Mr. Escudero sent an email to Ms. Brege, Mr. Lee, and Ms. Mesco stating “Very poor choice Frank! Enjoy your weekend, I am sure you and the Board will be very busy starting next week.” However, just four days later DOMA issued a press release announcing that it supported the Authorization and later withdrew its nomination notice Complete Reversal in Demands After demanding aggressive buybacks and opposing acquisitions, DOMA abruptly changed course in November 2025 and demanded that the Company announce a formal sales process and is now also targeting our CEO Threats of Personal Legal Liability In November 2025, December 2025, January 2026 and March 2026, DOMA's counsel threatened directors with personal legal liability and investigation based on accusations of gross negligence Declining to Make All of Their Director Candidates Available for Interviews Despite multiple offers, DOMA has refused to make their fund principal Eric de Armas available for an interview with the Board

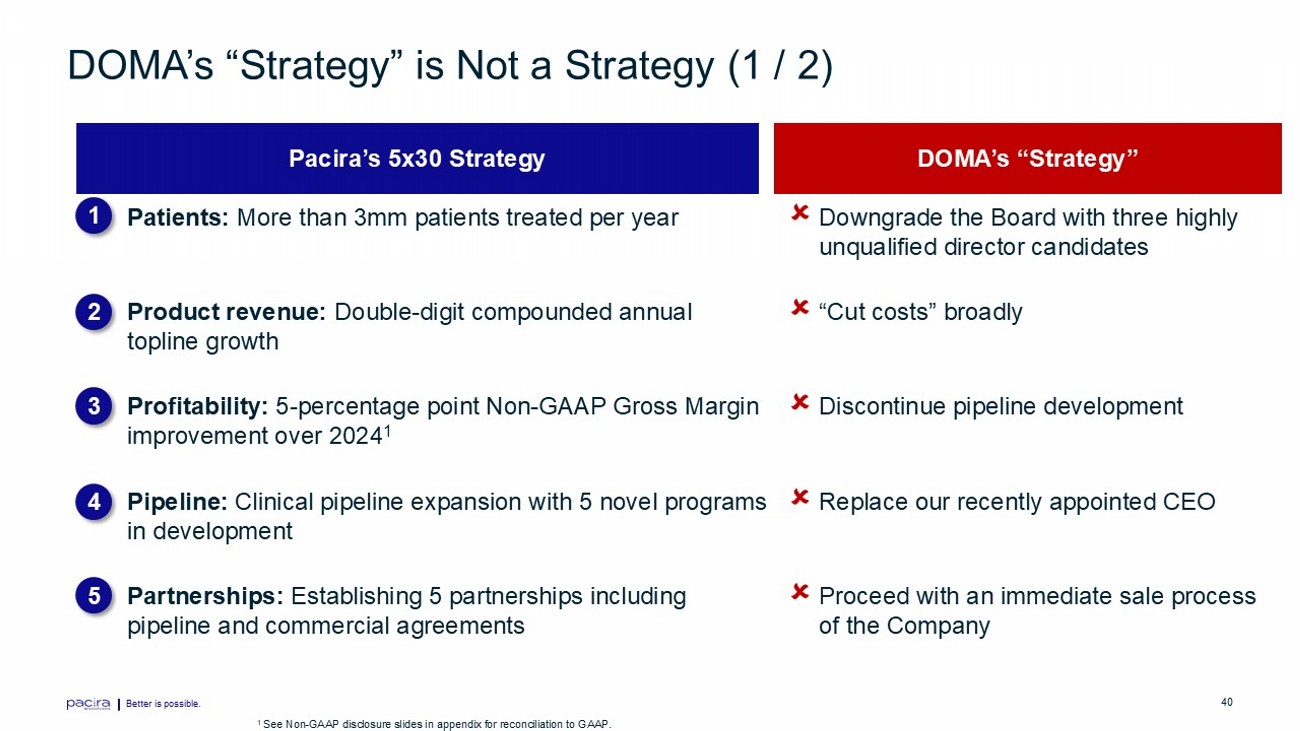

Better is possible. 40 DOMA’s “Strategy” is Not a Strategy (1 / 2) Pacira’s 5x30 Strategy DOMA’s “Strategy” 1 2 3 4 5 1 See Non - GAAP disclosure slides in appendix for reconciliation to GAAP. Downgrade the Board with three highly unqualified director candidates Patients: More than 3mm patients treated per year “Cut costs” broadly Product revenue: Double - digit compounded annual topline growth Discontinue pipeline development Profitability: 5 - percentage point Non - GAAP Gross Margin improvement over 2024 1 Replace our recently appointed CEO Pipeline: Clinical pipeline expansion with 5 novel programs in development Proceed with an immediate sale process of the Company Partnerships: Establishing 5 partnerships including pipeline and commercial agreements

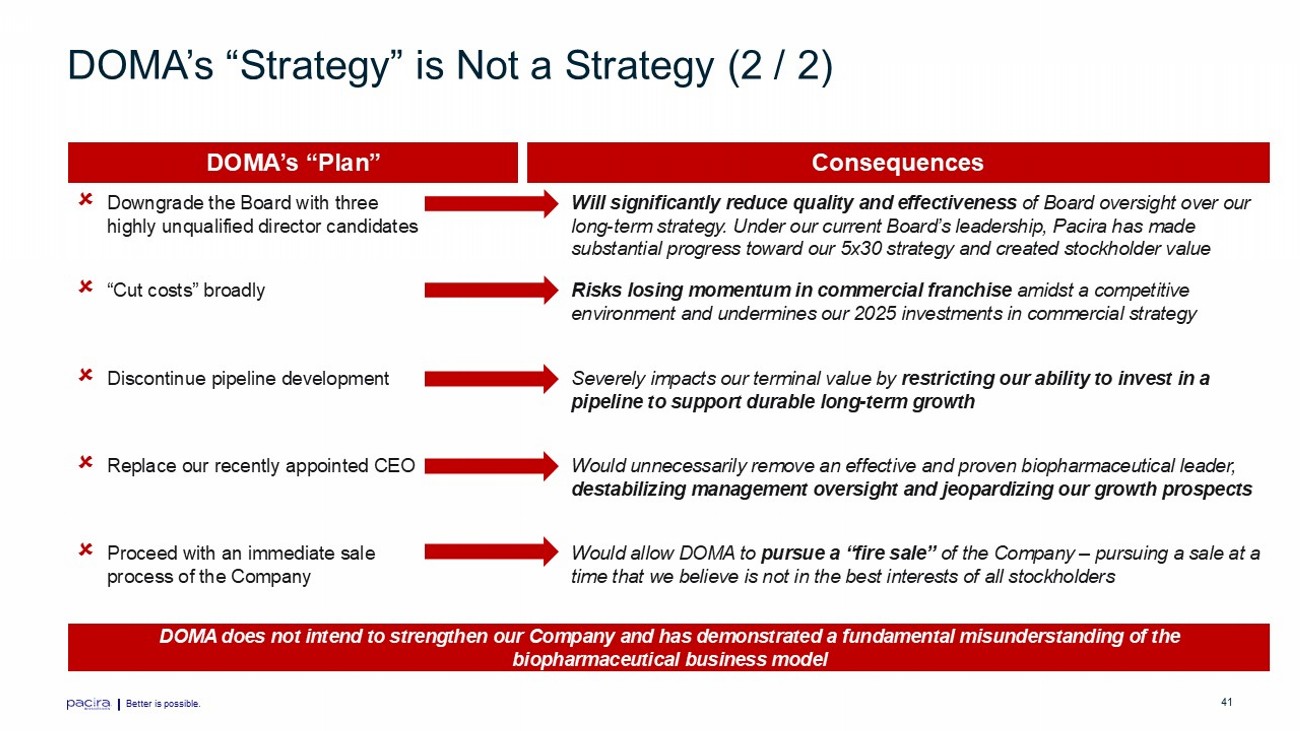

Better is possible. 41 DOMA’s “Strategy” is Not a Strategy (2 / 2) DOMA’s “Plan” Consequences Will significantly reduce quality and effectiveness of Board oversight over our long - term strategy. Under our current Board’s leadership, Pacira has made substantial progress toward our 5x30 strategy and created stockholder value Downgrade the Board with three highly unqualified director candidates Risks losing momentum in commercial franchise amidst a competitive environment and undermines our 2025 investments in commercial strategy “Cut costs” broadly Severely impacts our terminal value by restricting our ability to invest in a pipeline to support durable long - term growth Discontinue pipeline development Would unnecessarily remove an effective and proven biopharmaceutical leader, destabilizing management oversight and jeopardizing our growth prospects Replace our recently appointed CEO Would allow DOMA to pursue a “fire sale” of the Company – pursuing a sale at a time that we believe is not in the best interests of all stockholders Proceed with an immediate sale process of the Company DOMA does not intend to strengthen our Company and has demonstrated a fundamental misunderstanding of the biopharmaceutical business model

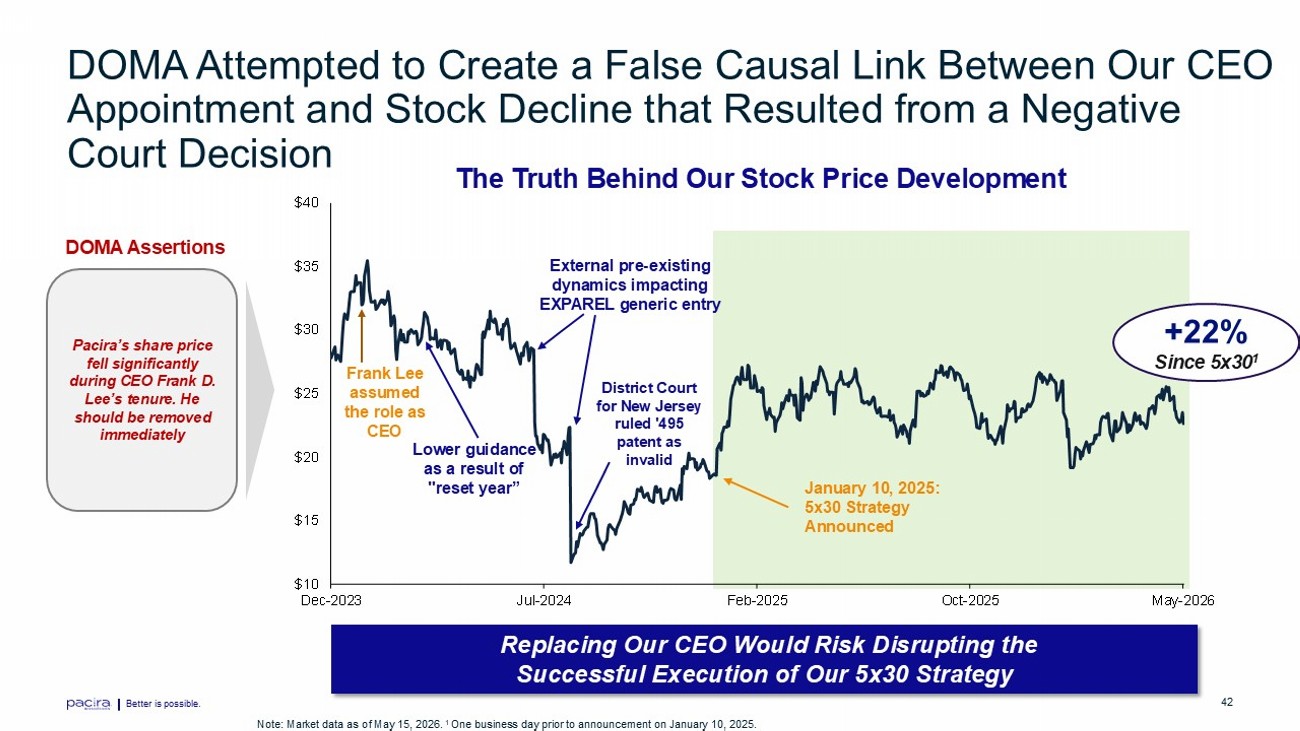

Better is possible. 42 $10 $15 $20 $25 $30 $35 $40 Dec-2023 Jul-2024 Feb-2025 Oct-2025 May-2026 Pacira’s share price fell significantly during CEO Frank D. Lee’s tenure. He should be removed immediately DOMA Attempted to Create a False Causal Link Between Our CEO Appointment and Stock Decline that Resulted from a Negative Court Decision Replacing Our CEO Would Risk Disrupting the Successful Execution of Our 5x30 Strategy External pre - existing dynamics impacting EXPAREL generic entry January 10, 2025: 5x30 Strategy Announced DOMA Assertions The Truth Behind Our Stock Price Development Lower guidance as a result of "reset year” Frank Lee assumed the role as CEO Note: Market data as of May 15, 2026. 1 One business day prior to announcement on January 10, 2025. + 22 % Since 5x30 1 District Court for New Jersey ruled '495 patent as invalid

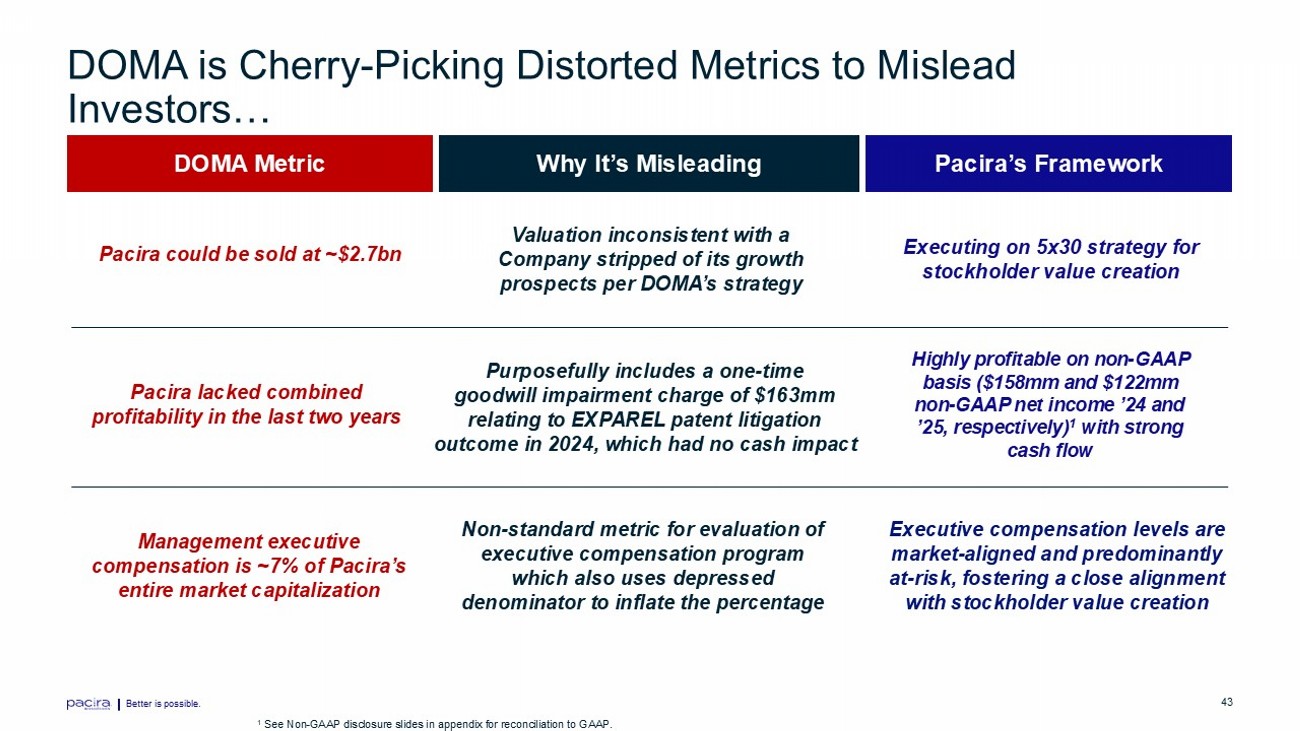

Better is possible. 43 DOMA is Cherry - Picking Distorted Metrics to Mislead Investors… DOMA Metric Why It’s Misleading Pacira’s Framework Pacira lacked combined profitability in the last two years Purposefully includes a one - time goodwill impairment charge of $163mm relating to EXPAREL patent litigation outcome in 2024, which had no cash impact Highly profitable on non - GAAP basis ($158mm and $122mm non - GAAP net income ’24 and ’25, respectively) 1 with strong cash flow Non - standard metric for evaluation of executive compensation program which also uses depressed denominator to inflate the percentage Management executive compensation is ~7% of Pacira’s entire market capitalization Pacira could be sold at ~$2.7bn Valuation inconsistent with a Company stripped of its growth prospects per DOMA’s strategy Executing on 5x30 strategy for stockholder value creation Executive compensation levels are market - aligned and predominantly at - risk, fostering a close alignment with stockholder value creation 1 See Non - GAAP disclosure slides in appendix for reconciliation to GAAP.

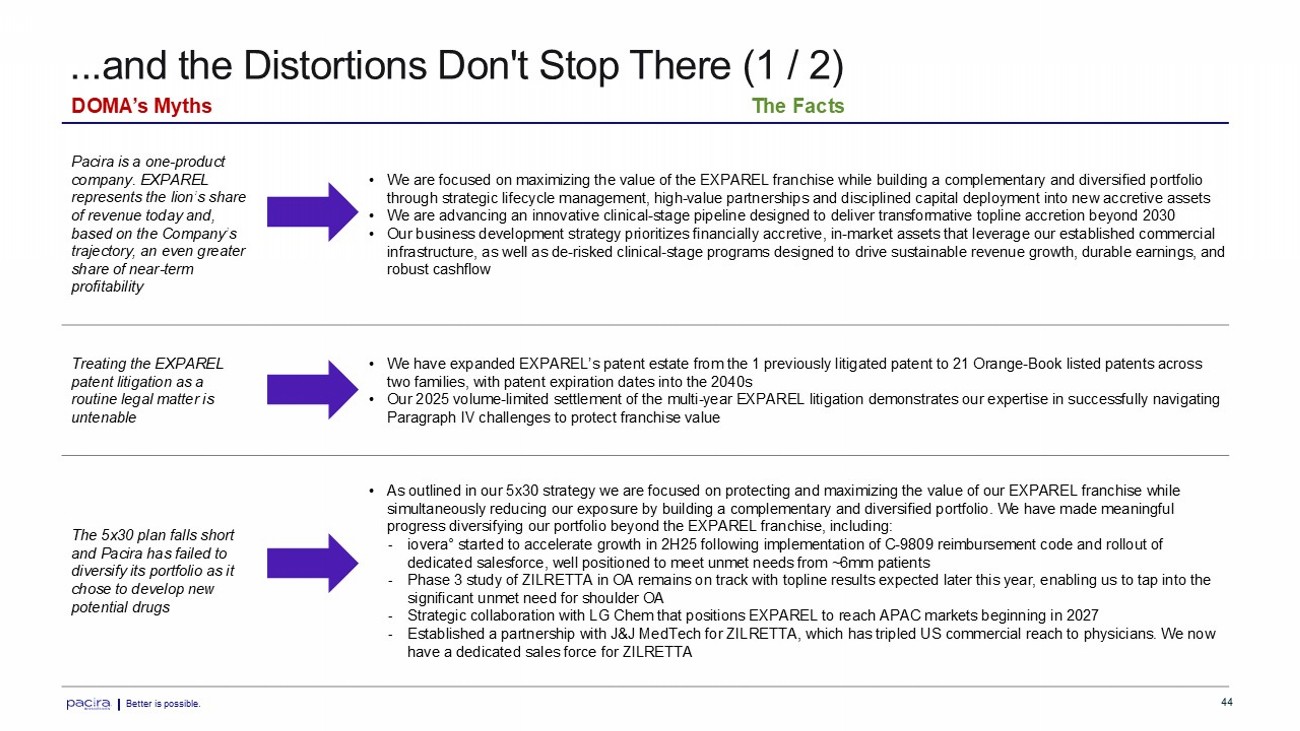

Better is possible. 44 The Facts DOMA’s Myths • We are focused on maximizing the value of the EXPAREL franchise while building a complementary and diversified portfolio through strategic lifecycle management, high - value partnerships and disciplined capital deployment into new accretive assets • We are advancing an innovative clinical - stage pipeline designed to deliver transformative topline accretion beyond 2030 • Our business development strategy prioritizes financially accretive, in - market assets that leverage our established commercial infrastructure, as well as de - risked clinical - stage programs designed to drive sustainable revenue growth, durable earnings, and robust cashflow Pacira is a one - product company. EXPAREL represents the lion’s share of revenue today and, based on the Company’s trajectory, an even greater share of near - term profitability • We have expanded EXPAREL’s patent estate from the 1 previously litigated patent to 21 Orange - Book listed patents across two families, with patent expiration dates into the 2040s • Our 2025 volume - limited settlement of the multi - year EXPAREL litigation demonstrates our expertise in successfully navigating Paragraph IV challenges to protect franchise value Treating the EXPAREL patent litigation as a routine legal matter is untenable • As outlined in our 5x30 strategy we are focused on protecting and maximizing the value of our EXPAREL franchise while simultaneously reducing our exposure by building a complementary and diversified portfolio. We have made meaningful progress diversifying our portfolio beyond the EXPAREL franchise, including: - iovera ° started to accelerate growth in 2H25 following implementation of C - 9809 reimbursement code and rollout of dedicated salesforce, well positioned to meet unmet needs from ~6mm patients - Phase 3 study of ZILRETTA in OA remains on track with topline results expected later this year, enabling us to tap into the significant unmet need for shoulder OA - Strategic collaboration with LG Chem that positions EXPAREL to reach APAC markets beginning in 2027 - Established a partnership with J&J MedTech for ZILRETTA, which has tripled US commercial reach to physicians. We now have a dedicated sales force for ZILRETTA The 5x30 plan falls short and Pacira has failed to diversify its portfolio as it chose to develop new potential drugs ...and the Distortions Don't Stop There ( 1 / 2 )

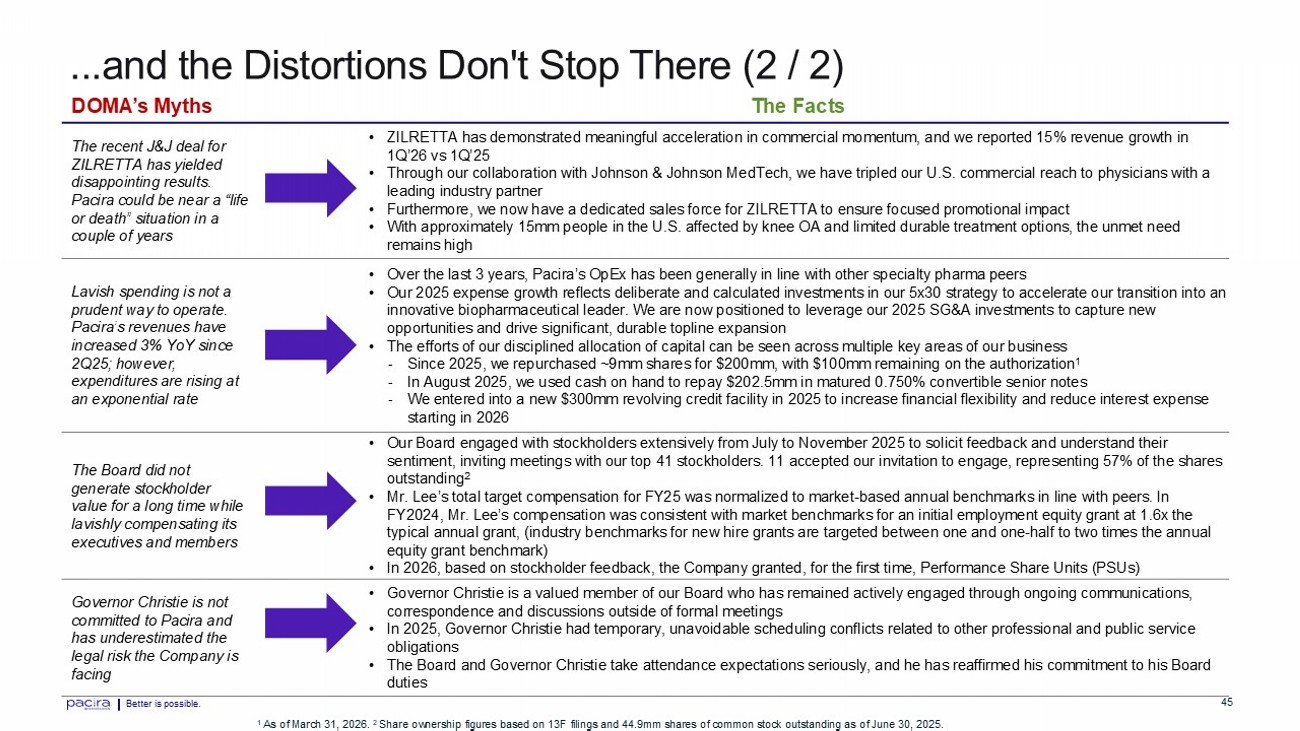

Better is possible. 45 The Facts DOMA’s Myths • ZILRETTA has demonstrated meaningful acceleration in commercial momentum, and we reported 15% revenue growth in 1Q’26 vs 1Q’25 • Through our collaboration with Johnson & Johnson MedTech, we have tripled our U.S. commercial reach to physicians with a leading industry partner • Furthermore, we now have a dedicated sales force for ZILRETTA to ensure focused promotional impact • With approximately 15mm people in the U.S. affected by knee OA and limited durable treatment options, the unmet need remains high The recent J&J deal for ZILRETTA has yielded disappointing results. Pacira could be near a “life or death” situation in a couple of years • Over the last 3 years, Pacira’s OpEx has been generally in line with other specialty pharma peers • Our 2025 expense growth reflects deliberate and calculated investments in our 5x30 strategy to accelerate our transition into an innovative biopharmaceutical leader. We are now positioned to leverage our 2025 SG&A investments to capture new opportunities and drive significant, durable topline expansion • The efforts of our disciplined allocation of capital can be seen across multiple key areas of our business - Since 2025, we repurchased ~9mm shares for $200mm, with $100mm remaining on the authorization 1 - In August 2025, we used cash on hand to repay $202.5mm in matured 0.750% convertible senior notes - We entered into a new $300mm revolving credit facility in 2025 to increase financial flexibility and reduce interest expense starting in 2026 Lavish spending is not a prudent way to operate. Pacira’s revenues have increased 3% YoY since 2Q25; however, expenditures are rising at an exponential rate • Our Board engaged with stockholders extensively from July to November 2025 to solicit feedback and understand their sentiment, inviting meetings with our top 41 stockholders. 11 accepted our invitation to engage, representing 57% of the shar es outstanding 2 • Mr. Lee’s total target compensation for FY25 was normalized to market - based annual benchmarks in line with peers. In FY2024, Mr. Lee’s compensation was consistent with market benchmarks for an initial employment equity grant at 1.6x the typical annual grant, (industry benchmarks for new hire grants are targeted between one and one - half to two times the annual equity grant benchmark) • In 2026, based on stockholder feedback, the Company granted, for the first time, Performance Share Units (PSUs) The Board did not generate stockholder value for a long time while lavishly compensating its executives and members • Governor Christie is a valued member of our Board who has remained actively engaged through ongoing communications, correspondence and discussions outside of formal meetings • In 2025, Governor Christie had temporary, unavoidable scheduling conflicts related to other professional and public service obligations • The Board and Governor Christie take attendance expectations seriously, and he has reaffirmed his commitment to his Board duties Governor Christie is not committed to Pacira and has underestimated the legal risk the Company is facing ...and the Distortions Don't Stop There (2 / 2 ) 1 As of March 31, 2026. 2 Share ownership figures based on 13F filings and 44.9mm shares of common stock outstanding as of June 30, 2025.

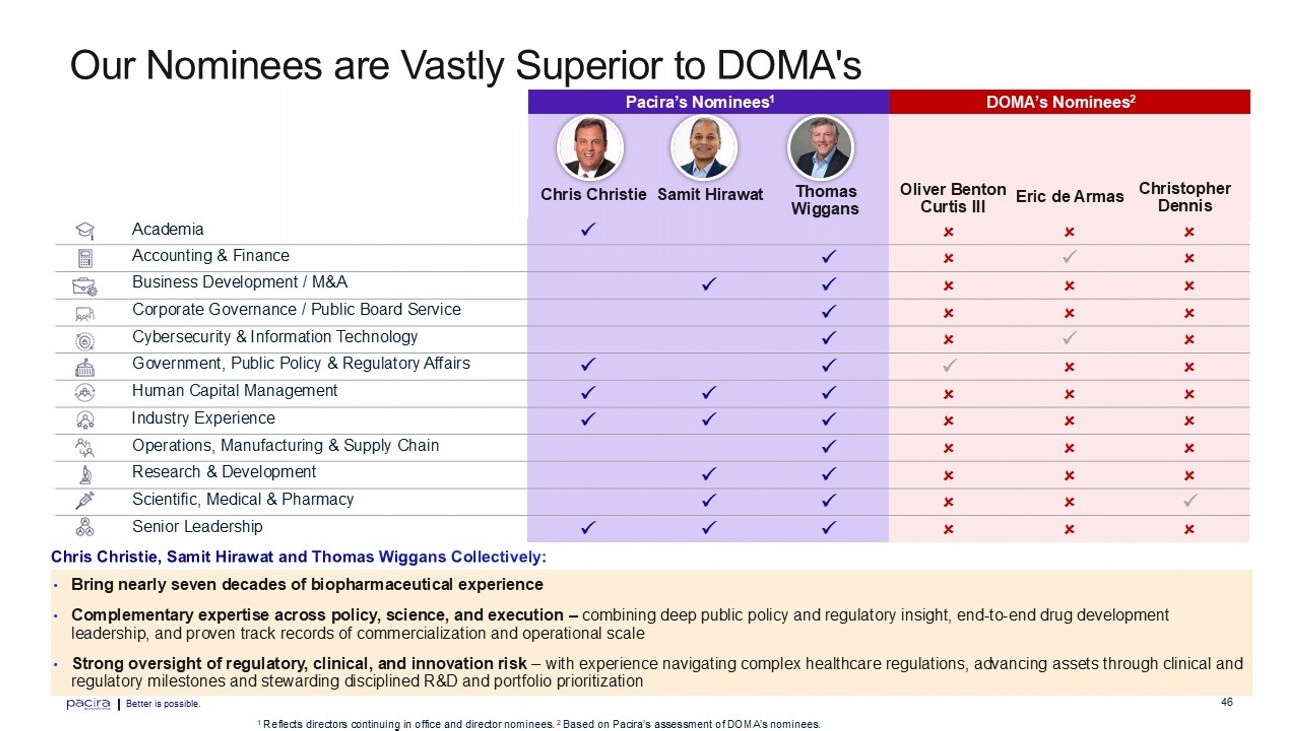

Better is possible. 46 DOMA’s Nominees 2 Academia Accounting & Finance Business Development / M&A Corporate Governance / Public Board Service Cybersecurity & Information Technology Government, Public Policy & Regulatory Affairs Human Capital Management Industry Experience Operations, Manufacturing & Supply Chain Research & Development Scientific, Medical & Pharmacy Senior Leadership Our Nominees are Vastly Superior to DOMA's 1 Reflects directors continuing in office and director nominees. 2 Based on Pacira’s assessment of DOMA’s nominees. Chris Christie Samit Hirawat Thomas Wiggans Pacira’s Nominees 1 Oliver Benton Curtis III Eric de Armas Christopher Dennis • Bring nearly seven decades of biopharmaceutical experience • Complementary expertise across policy, science, and execution – combining deep public policy and regulatory insight, end - to - end drug development leadership, and proven track records of commercialization and operational scale • Strong oversight of regulatory, clinical, and innovation risk – with experience navigating complex healthcare regulations, advancing assets through clinical and regulatory milestones and stewarding disciplined R&D and portfolio prioritization

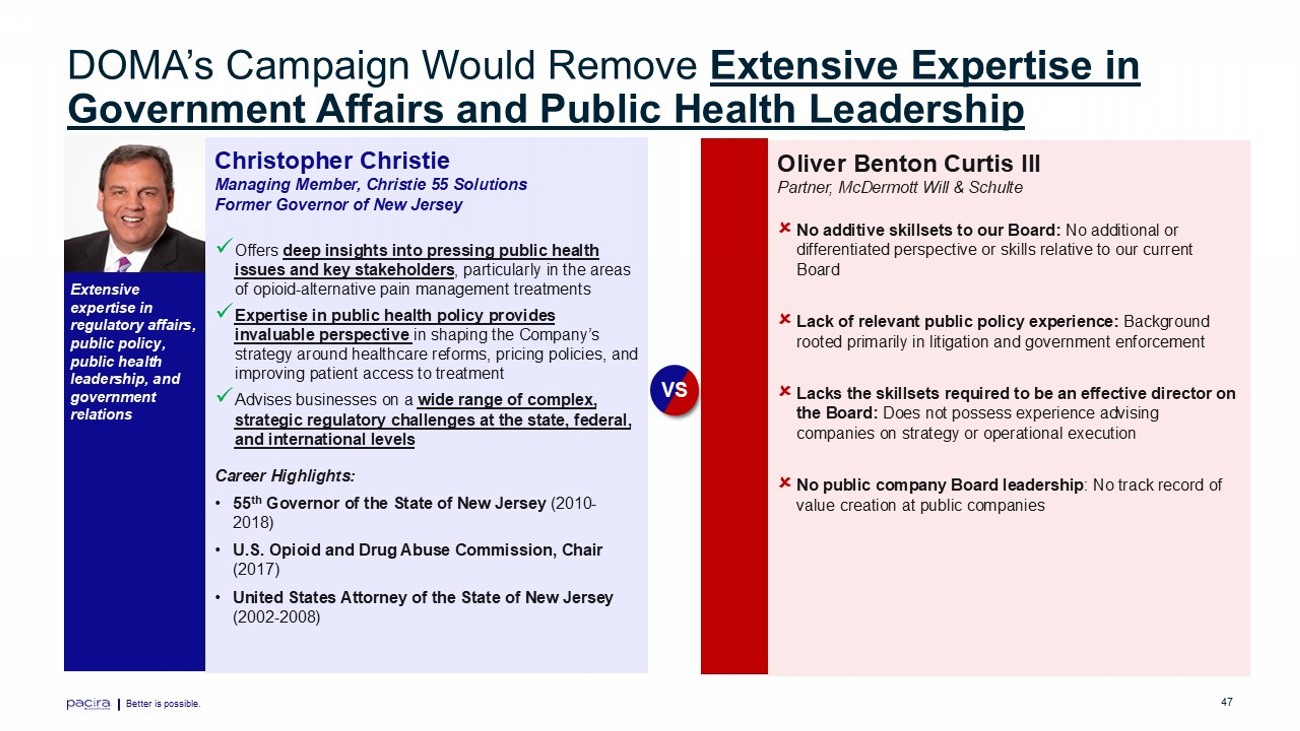

Better is possible. 47 DOMA’s Campaign Would Remove Extensive Expertise in Government Affairs and Public Health Leadership Christopher Christie Managing Member, Christie 55 Solutions Former Governor of New Jersey x Offers deep insights into pressing public health issues and key stakeholders , particularly in the areas of opioid - alternative pain management treatments x Expertise in public health policy provides invaluable perspective in shaping the Company’s strategy around healthcare reforms, pricing policies, and improving patient access to treatment x Advises businesses on a wide range of complex, strategic regulatory challenges at the state, federal, and international levels Oliver Benton Curtis III Partner, McDermott Will & Schulte No additive skillsets to our Board: No additional or differentiated perspective or skills relative to our current Board Lack of relevant public policy experience: Background rooted primarily in litigation and government enforcement Lacks the skillsets required to be an effective director on the Board: Does not possess experience advising companies on strategy or operational execution No public company Board leadership : No track record of value creation at public companies Extensive expertise in regulatory affairs, public policy, public health leadership, and government relations Career Highlights: • 55 th Governor of the State of New Jersey (2010 - 2018) • U.S. Opioid and Drug Abuse Commission, Chair (2017) • United States Attorney of the State of New Jersey (2002 - 2008) VS

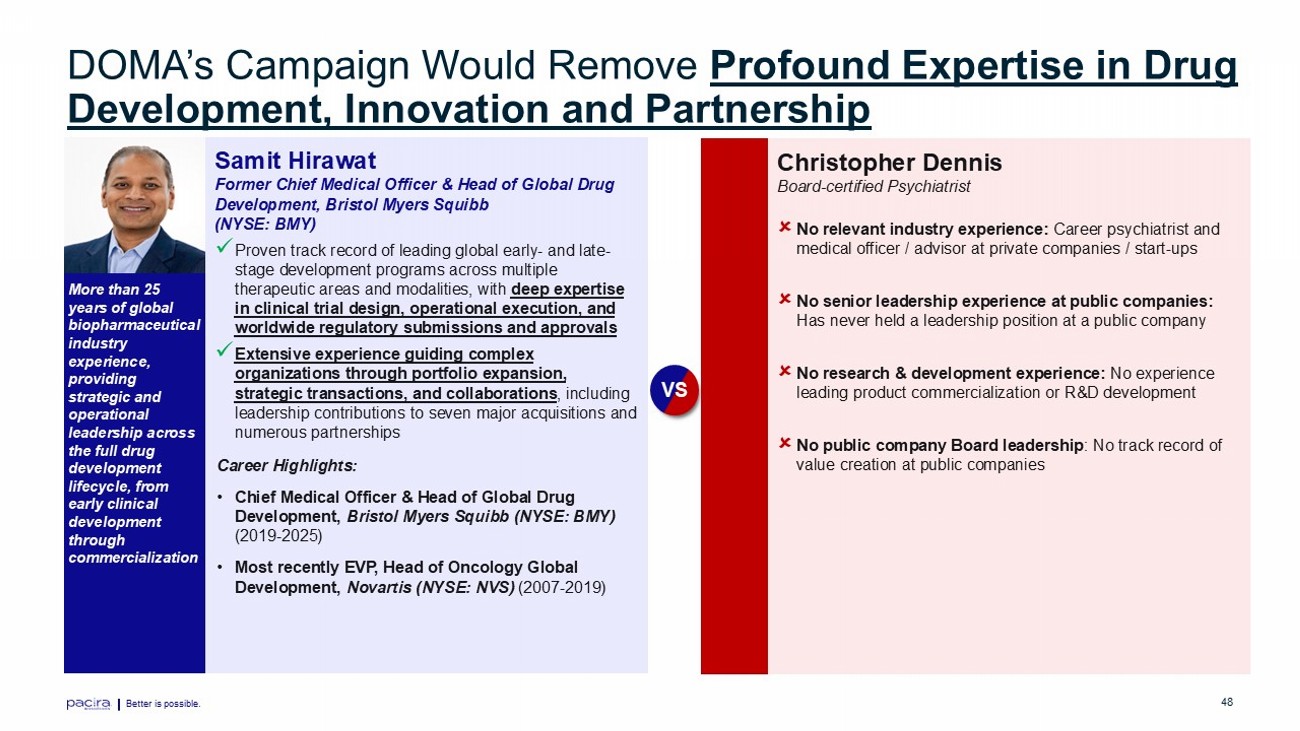

Better is possible. 48 DOMA’s Campaign Would Remove Profound Expertise in Drug Development, Innovation and Partnership Samit Hirawat Former Chief Medical Officer & Head of Global Drug Development, Bristol Myers Squibb (NYSE: BMY) x Proven track record of leading global early - and late - stage development programs across multiple therapeutic areas and modalities, with deep expertise in clinical trial design, operational execution, and worldwide regulatory submissions and approvals x Extensive experience guiding complex organizations through portfolio expansion, strategic transactions, and collaborations , including leadership contributions to seven major acquisitions and numerous partnerships More than 25 years of global biopharmaceutical industry experience, providing strategic and operational leadership across the full drug development lifecycle, from early clinical development through commercialization Career Highlights: • Chief Medical Officer & Head of Global Drug Development, Bristol Myers Squibb (NYSE: BMY) (2019 - 2025) • Most recently EVP, Head of Oncology Global Development, Novartis (NYSE: NVS) (2007 - 2019) Christopher Dennis Board - certified Psychiatrist No relevant industry experience: Career psychiatrist and medical officer / advisor at private companies / start - ups No senior leadership experience at public companies: Has never held a leadership position at a public company No research & development experience: No experience leading product commercialization or R&D development No public company Board leadership : No track record of value creation at public companies VS

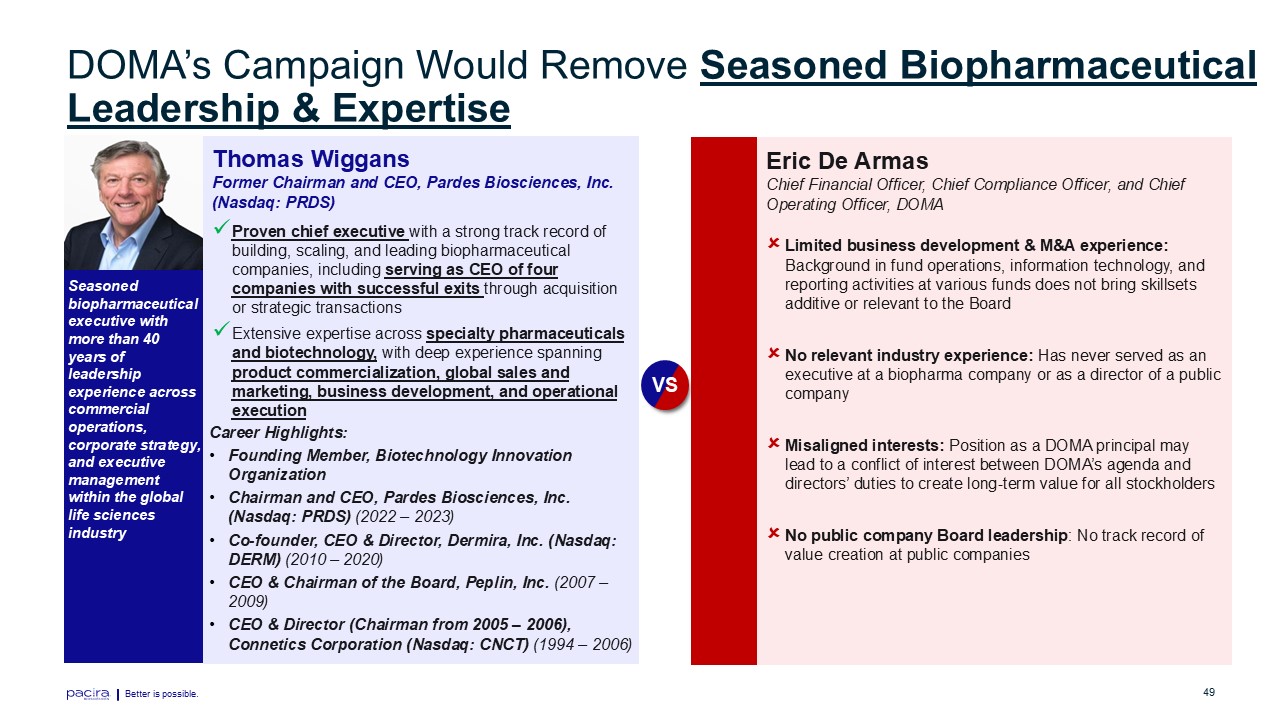

Better is possible. 49 DOMA’s Campaign Would Remove Seasoned Biopharmaceutical Leadership & Expertise Thomas Wiggans Former Chairman and CEO, Pardes Biosciences, Inc. (Nasdaq: PRDS) x Proven chief executive with a strong track record of building, scaling, and leading biopharmaceutical companies, including serving as CEO of four companies with successful exits through acquisition or strategic transactions x Extensive expertise across specialty pharmaceuticals and biotechnology, with deep experience spanning product commercialization, global sales and marketing, business development, and operational execution Seasoned biopharmaceutical executive with more than 40 years of leadership experience across commercial operations, corporate strategy, and executive management within the global life sciences industry Career Highlights: • Founding Member, Biotechnology Innovation Organization (1993 – Present) • Chairman and CEO, Pardes Biosciences, Inc. (Nasdaq: PRDS) (2022 – 2023) • Co - founder, CEO & Director, Dermira , Inc. (Nasdaq: DERM) (2010 – 2020) • CEO & Chairman of the Board, Peplin, Inc. (2007 – 2009) • Most Recently CEO & Chairman, Connetics Corporation (Nasdaq: CNCT) (1994 – 2006) Eric De Armas Chief Financial Officer, Chief Compliance Officer, and Chief Operating Officer, DOMA Limited business development & M&A experience: Background in fund operations, information technology, and reporting activities at various funds does not bring skillsets additive or relevant to the Board No relevant industry experience: Has never served as an executive at a biopharma company or as a director of a public company Misaligned interests: Position as a DOMA principal may lead to a conflict of interest between DOMA’s agenda and directors’ duties to create long - term value for all stockholders No public company Board leadership : No track record of value creation at public companies VS

50 Better is possible. Conclusion