| 1 Evotec Group Group Policy on Insider Information Document: Revision version No. 2 Effective Date: 19 April 2024 Author: Legal & Compliance Department Reviewed by: Management Board and Supervisory Board Approved by: Management Board and Supervisory Board on: 19 April 2024 Group Policy on Insider Information 1. PURPOSE ................................................................................1 2. APPLICATION FIELD ..................................................................2 3. RESPONSIBILITIES ...................................................................2 4. WHAT IS INSIDER INFORMATION ...............................................2 5. POLICY ...................................................................................4 5.1 Insider Rules .....................................................................4 5.2 Projects ............................................................................4 5.3 Pre-Clearance Procedures ...................................................4 5.4 Trading Prohibition During Blackout Periods: ..........................5 5.4.1 Financial Reporting Blackout Periods .........................5 5.4.2 Event-Specific Blackout Periods ................................5 5.4.3 Exceptions ............................................................5 5.5 Rule 10b5-1 Plans ..............................................................6 6. CONSEQUENCES OF VIOLATIONS & QUESTIONS ...........................7 7. DOCUMENT HISTORY ................................................................7 1. PURPOSE As the shares of Evotec SE (“Company”) are admitted to trading on the Frankfurt Stock Exchange and the American Depositary Shares are listed on Nasdaq, all securities transactions are subject to securities legislation, including the EU Market Abuse Regulation (596/2014) and the German Securities Trading Act (WpHG) as well as the securities laws and regulations of the United States. These laws regulate the disclosure/publication and prohibit the unlawful use of insider information for securities trading. The Management Board has issued this Group policy (the “Policy”) on insider information in order to protect the Company’s employees and the Company. Improper disclosure/publication and use of insider information is prohibited by German, European and US legislation, as well as by many others, and is subject to criminal proceedings. The Company and its employees are required to comply with all applicable laws and regulations. The Policy was created for information purposes and aims to ensure compliance with these laws and regulations within the Company group worldwide. The Company also intends not to unreasonably restrict the free trading of affected persons. The Policy is applied according to the specific circumstances at hand. The Company's independent consultants and (potential) cooperation or business partners are personally responsible for ensuring the proper handling of insider information. |

| Group Policy on Insider Information 2 2. APPLICATION FIELD This Policy applies to all members of the Management and Supervisory Board as well as all other employees of the Company and its subsidiaries, including family members, household members and entities controlled by persons subject to this Policy. This Policy applies to any transactions in the Company’s securities (collectively referred to in this Policy as “Company Securities”), including the Company’s common stock, options to purchase common stock, American Depositary Shares, or any other type of securities that the Company may issue, including (but not limited to) preferred stock, convertible debentures and warrants, as well as derivative securities that are not issued by the Company, such as exchange-traded put or call options or swaps relating to Company Securities. Transactions subject to this Policy include purchases, sales and bona fide gifts of Company Securities. Transactions by family members and others This Policy applies to your family members who reside with you (including a spouse, a child, a child away at college, stepchildren, grandchildren, parents, stepparents, grandparents, siblings and in-laws), anyone else who lives in your household, and any family members who do not live in your household but whose transactions in Company Securities are directed by you or are subject to your influence or control, such as parents or children who consult with you before they trade in Company Securities (collectively referred to as “Family Members”). You are responsible for the transactions of these other persons and therefore should make them aware of the need to confer with you before they trade in Company Securities, and you should treat all such transactions for the purposes of this Policy and applicable securities laws as if the transactions were for your own account. This Policy does not, however, apply to personal securities transactions of Family Members where the purchase or sale decision is made by a third party not controlled by, influenced by or related to you or your Family Members. Transactions by entities that you influence or control This Policy applies to any entities that you influence or control, including any corporations, partnerships or trusts (collectively referred to as “Controlled Entities”), and transactions by these Controlled Entities should be treated for the purposes of this Policy and applicable securities laws as if they were for your own account. 3. RESPONSIBILITIES Every person who comes into contact with insider information is obligated ethically and legally to take all appropriate measures to ensure the confidentiality and non-use of insider information relating to the Company or the Company's securities. Each person is responsible for making sure that he or she complies with this Policy, and that any Family Member or Controlled Entity whose transactions are subject to this Policy, as discussed below, also complies with this Policy. The circle of insiders must be kept as small as possible based on the strict application of the need-to-know principle as well as by screening for possible conflicts and establishing organizational separations such as "firewalls" between the various departments (such as between the M&A and Partnership/Licensing/Business Development departments and the Treasury department). The responsibility for determining whether a person is in possession of material nonpublic information rests with that individual, and any action on the part of the Company, the General Counsel or any other employee or member of the Management or Supervisory Board pursuant to this Policy (or otherwise) does not in any way constitute legal advice or insulate an individual from liability or criminal prosecution under applicable securities laws. This Policy continues to apply to transactions in Company securities even after a person's termination of service to the Company. If a person is in possession of material nonpublic information when his or her service terminates, that individual may not trade in Company securities until that information has become public or is no longer material. The pre-clearance procedures specified under the heading "Pre-Clearance Procedures" below, however, will cease to apply to transactions in Company Securities upon the expiration of any Blackout Period or other Company-imposed trading restrictions applicable at the time of the termination of service. 4. WHAT IS INSIDER INFORMATION Insider information is any material information that has not been publicly disclosed ("material nonpublic information") relating, directly or indirectly, to the Company and/or its securities that if published, is likely to have a material impact on the price of securities of the Company, whether negative or positive. Information |

| Group Policy on Insider Information 3 is considered "material" if a reasonable investor would consider that information important in making a decision to buy, hold or sell securities. There is no bright-line standard for assessing materiality; rather, materiality is based on an assessment of all of the facts and circumstances. Information may also be material if it indicates future circumstances reasonably expected to occur, where it is specific enough to enable a conclusion to be drawn as to the possible effect of the circumstances or event on the prices of the securities of the Company. In a protracted process the intermediate steps may also constitute insider information. On this basis, the Company's insider information includes the knowledge of Management Board members, Supervisory Board members, administration, executives, employees and consultants of the Company about material nonpublic information that they gain within the context of their activities for the Company, where publication of such knowledge would likely have a considerable impact on the Company's stock price. Insider information of this kind can arise particularly within the context of work on projects, such as company mergers, company acquisitions, disposals of assets, capital increases, important capital markets transactions, important license agreements or other collaborations, major clinical trials, etc., and prior to the proper publication of the Company’s financial key figures (quarterly results, interim results and annual results). The events specified below are also usually considered insider information: • projections of future earnings or losses, or other earnings guidance, or any material changes thereto (to the extent not already made public); • bank borrowings or other financing transactions out of the ordinary course of business; • issue of new shares (e.g. capital increase, granting stock options); • capital reductions, stock-splits, or share repurchase programmes; • other material changes in the capital structure, such as unforeseeable and extraordinary revenue gains or losses, or events that will likely result in a change of this type to the earnings performance (e.g. a major product liability case, extremely high restructuring costs, etc.); • company mergers, company acquisitions, disposals of assets, spin-off of a company division, loss of a material business segment; • restructuring or bankruptcy of the Company or the Company group; • conclusion or cancellation of an important strategic alliance; • development or purchase of products or technologies with high market value; • material related party transactions; • the gain or loss of material license agreements or other collaborations, or of customers or suppliers; • results of larger clinical trials; • material changes in the Company's market position; • material changes in senior management, the Management Board or the Supervisory Board; • unexpected changes in auditors or notification that an auditor report may no longer be relied upon; • material pending or threatened litigation, or the resolution of such litigation; • the imposition of a ban on trading in the Company's securities; and • a significant cybersecurity incident experienced by the Company that has not yet been made public. If you are unsure whether information is material, you should either consult the General Counsel before making any decision to trade in or recommend trading in securities to which that information relates or assume that the information is material. When information is considered publicly disclosed: Information that has not been disclosed to the public is generally considered to be nonpublic information. In order to establish that the information has been disclosed to the public, it may be necessary to demonstrate that the information has been "widely disseminated.” Information generally would be considered widely disseminated if it has been disclosed through a broadly distributed press release or public disclosure of documents filed with the SEC that are available on the SEC's website. By contrast, information would likely not be considered widely disseminated if it is available only to the Company's employees, or if it is only available to a select group of analysts, brokers and institutional investors. Under the provisions of European and German law on the disclosure of material nonpublic information, information generally would be considered widely disseminated if it has been disclosed through a media cluster. |

| Group Policy on Insider Information 4 5. POLICY 5.1 Insider Rules Any person with Company insider information, an insider, must adhere to the following rules: i.) Obligation to maintain confidentiality: Insider information must be treated as strictly confidential and may not be made accessible to non- insiders inside or outside of the Company, including but not limited to, family or household members, friends, business associates, investors and expert consulting firms. The disclosure of any insider information to persons inside or outside of the Company must be strictly limited to persons who require this information to do their jobs and made in accordance with the securities laws and Company’s policies regarding the protection or authorized external disclosure of information regarding the Company. ii.) Trading ban: Insiders may not buy, sell or otherwise trade Company Securities and/or the securities of other listed companies in which the Company holds an investment as published in the Company’s financial statements for themselves or for a third party in their own name or on behalf of a third party. Additionally, no member of the Management Board or Supervisory Board or any other employee of the Company who, in the course of working for the Company, learns of material nonpublic information about a company with which the Company does business, including a customer or supplier of the Company, may trade in that company's securities until the information becomes public or is no longer material. iii.) No trading recommendations: Trading recommendations (whether express or implied) to non-insiders to purchase or sell any Company Securities are not permitted. Non-insiders who trade based on the insider information and the insider who provided the information may also be subject to criminal proceedings. iv.) No exceptions: There are no exceptions to this Policy, except as specifically noted herein. Transactions that may be necessary or justifiable for independent reasons (such as the need to raise money for an emergency expenditure), or small transactions, are not exempted from this Policy. The securities laws do not recognize any mitigating circumstances, and, in any event, even the appearance of an improper transaction must be avoided to preserve the Company’s reputation for adhering to the highest standards of conduct. Persons subject to this policy may not assist anyone engaged in unlawfully trading on the basis of material nonpublic information. Such Insider Rules set forth above shall apply equally to any trading in other companies’ securities if the insider obtains material nonpublic information about another company in the course of its employment or other relationship with the Company. 5.2 Projects Any time information (e.g., about a certain project) reaches a level where it is likely to affect the Company's share price, the responsible “Ad-hoc Committee” (a specific committee consisting of participants from Company’s Management Board, Legal department, Finance and Communication/Investor Relations) needs to be informed by the relevant project leader and the Ad-hoc Committee shall compile an insider list and inform the relevant persons (e.g., project participants) about their inclusion on the list. However, the mere inclusion of information on the insider list does not mean that the Company suspects the existence of insider information at that time which would, in principle, make an ad-hoc publication necessary. When informing individuals on the insider list of the insider rules, particularly the obligation to maintain confidentiality and the trading ban, emphasis shall be made that these rules should be strictly complied with in order to avoid any possible penalties. The Ad-hoc Committee is responsible for maintaining insider project lists with the relevant status and for extending the insider group as may be needed. All insider lists shall be archived and the Company's Management Board shall maintain a list of all insider projects of the Company group with the relevant status, which shall be updated on a continuous basis. 5.3 Pre-Clearance Procedures The Company has established the following additional procedures in order to assist the Company in the |

| Group Policy on Insider Information 5 administration of this Policy, to facilitate compliance with laws prohibiting insider trading while in possession of material nonpublic information, and to avoid the appearance of any impropriety. Persons discharging managerial responsibilities, i.e. Supervisory Board members, Management Board members, as well as senior executives who have regular access to material nonpublic information and are authorized to make significant business decisions at the group level, such as the CFO leadership team, CBO leadership team, COO leadership team, CSO leadership team, Group Accounting, Group Controlling, Group Risk Management, Investor Relations, Corporate Communications, ("Covered Senior Persons") and any persons designated by the General Counsel as being subject to these procedures, as well as the Family Members and Controlled Entities of such persons, may not engage in any transaction in Company Securities without first obtaining pre-clearance of the transaction from the General Counsel. A request for pre-clearance should be submitted to the General Counsel in the form attached hereto, see Schedule A: INSIDER TRADING PRE-CLEARANCE REQUEST & RULE 10B5-1 PLAN FORM, at least two business days in advance of the proposed transaction. The General Counsel is under no obligation to approve a transaction submitted for pre-clearance and may determine not to permit the transaction. If a person seeks pre- clearance and permission to engage in the transaction is denied, then he or she must refrain from initiating any transaction in Company securities and not inform any other person of the restriction. Before a request for pre-clearance is made, the requestor should carefully consider whether he or she may be aware of any material nonpublic information about the Company and shall describe fully those circumstances to the General Counsel. The requestor shall also indicate whether he or she has effected any non-exempt "opposite-way" transactions within the past six months, and should be prepared to report the proposed transaction on an appropriate Form 4 or Form 5. The requestor should also be prepared to comply with SEC Rule 144 and file a Form 144, if applicable. If a person seeks pre-clearance and permission to engage in the transaction is granted, then such trade must be effected within three business days of receipt of pre-clearance unless an exception is granted. Such person must promptly (within 24 hours) notify the General Counsel following the completion of the transaction, or instruct its bank/broker to do so. A person who has not effected a transaction within the time limit may not engage in such transaction without again obtaining pre-clearance of the transaction from the General Counsel. 5.4 Trading Prohibition During Blackout Periods: 5.4.1 Financial Reporting Blackout Periods Covered Senior Persons may not conduct any transactions involving the Company's securities (other than as specified by this Policy), during a "Blackout Period”. Blackout Periods include: the period of time from two weeks prior to the end of a quarter and ending after the first business day after the day the relative interim financial statement, quarterly report, or annual financial statement is published. In other words, these persons may only conduct transactions in Company Securities during the “Window Period” beginning after the close of trading on the first full trading day following the public release of the Company’s quarterly earnings and ending fourteen days prior to the close of the next fiscal quarter. 5.4.2 Event-Specific Blackout Periods From time to time, an event may occur that is material to the Company and is known by only a few members of the Supervisory Board, Management Board and/or employees, such as a cybersecurity incident or planned material transaction. So long as the event remains material and nonpublic, the persons designated by the Ad-hoc Committee may not trade Company Securities. In addition, if the Company's financial results may be sufficiently material in a particular fiscal quarter that, in the judgment of the Ad-hoc Committee, designated persons should refrain from trading in Company securities even sooner than the typical Blackout Period described above. In that situation, the Ad-hoc Committee shall notify these persons that they should not trade in Company Securities, without disclosing the reason for the restriction. The existence of an event-specific trading restriction period or extension of a Blackout Period will not be announced to the Company as a whole and should be communicated only to those on a need-to-know basis. 5.4.3 Exceptions The quarterly trading restrictions and event-driven trading restrictions do not apply to those transactions to which this Policy does not apply, as described below. Further, the requirement for pre-clearance, the quarterly trading restrictions and event-driven trading restrictions do not apply to transactions conducted pursuant to approved Rule 10b5-1 plans, described under the heading “Rule 10b5-1 Plans.” This Policy does not apply in the case of the following transactions, except as specifically noted: |

| Group Policy on Insider Information 6 i.) Restricted Stock Awards / Share Performance Awards: This Policy does not apply to the vesting of restricted stock or restricted stock units, or the exercise of a tax withholding right pursuant to which you elect to have the Company withhold shares of stock to satisfy tax withholding requirements upon the vesting of any restricted stock or restricted stock units. The Policy does apply, however, to any market sale of the Company Securities received upon such vesting. ii.) 401(k) Plan: This Policy does not apply to purchases of Company Securities in the Company’s 401(k) plan resulting from your periodic contribution of money to the plan pursuant to your payroll deduction election. This Policy does apply, however, to certain elections you may make under the 401(k) plan, including: (a) an election to increase or decrease the percentage of your periodic contributions that will be allocated to the Company stock fund; (b) an election to make an intra-plan transfer of an existing account balance into or out of the Company stock fund; (c) an election to borrow money against your 401(k) plan account if the loan will result in a liquidation of some or all of your Company stock fund balance; and (d) an election to pre-pay a plan loan if the pre-payment will result in allocation of loan proceeds to the Company stock fund 5.5 Rule 10b5-1 Plans Rule 10b5-1 under the Exchange Act provides an affirmative defense to insider trading allegations under federal law. In order to be eligible to rely on this defense, a person subject to this Policy must enter into a Rule 10b5-1 plan for transactions in Company Securities that meets the conditions specified in the Rule (a “Rule 10b5-1 Plan”). If the plan meets the requirements of Rule 10b5-1, Company Securities may be purchased or sold without regard to certain insider trading restrictions described in this Policy. To comply with the Policy, the adoption, modification or early termination of a Rule 10b5-1 Plan must be approved by the General Counsel, and all Rule 10b5-1 Plans must meet the requirements of Rule 10b5- 1. Any Rule 10b5-1 Plan must be submitted for approval five days prior to the entry into the Rule 10b5- 1 Plan, and any proposed modifications or terminations thereof must be submitted for approval at least three days prior to the consummation of such actions. No further pre-approval of transactions conducted pursuant to the Rule 10b5-1 Plan will be required. In addition, a Rule 10b5-1 Plan may be entered into or modified only (i) at a time when the person entering into, or modifying the plan is not aware of material nonpublic information about the Company or Company Securities and (ii) in the case of Covered Senior Persons, during an open Window Period. Once the plan is adopted, the person must not exercise any influence over the amount of securities to be traded, the price at which they are to be traded or the date of the trade. The plan must either specify the amount, pricing and timing of transactions in advance or delegate discretion on these matters to an independent third party. Once a Rule 10b5-1 Plan is pre-cleared and is adopted or modified, it is subject to a “cooling-off” period before execution of the first trade. The “cooling-off” period for directors and officers subject to Section 16 of the Exchange Act ends on the later of: (1) 90 days following the Rule 10b5-1 Plan adoption or modification or (2) two business days following the disclosure in Form 10-Q or Form 10-K of the Company’s financial results for the fiscal quarter in which the Rule 10b5-1 Plan was adopted or modified (however, the cooling-off period will not exceed 120 days following plan adoption or modification). For all other individuals, a 30 day cooling-off period is required. A person may not enter into overlapping Rule 10b5-1 Plans (subject to certain exceptions) and may only enter into one single-trade Rule 10b5-1 Plan during any 12-month period (subject to certain exceptions). Directors and officers subject to Section 16 of the Exchange Act must include a representation in their Rule 10b5-1 Plan certifying that: (i) they are not aware of any material nonpublic information; and (ii) they are adopting the Rule 10b5-1 Plan in good faith and not as part of a plan or scheme to evade the prohibitions in Rule 10b-5. All persons entering into a Rule 10b5-1 Plan must act in good faith with respect to that plan. * * * Note: Where reference to General Counsel is made, the General Counsel may be substituted with a person with whom the General Counsel delegates to act on their behalf. |

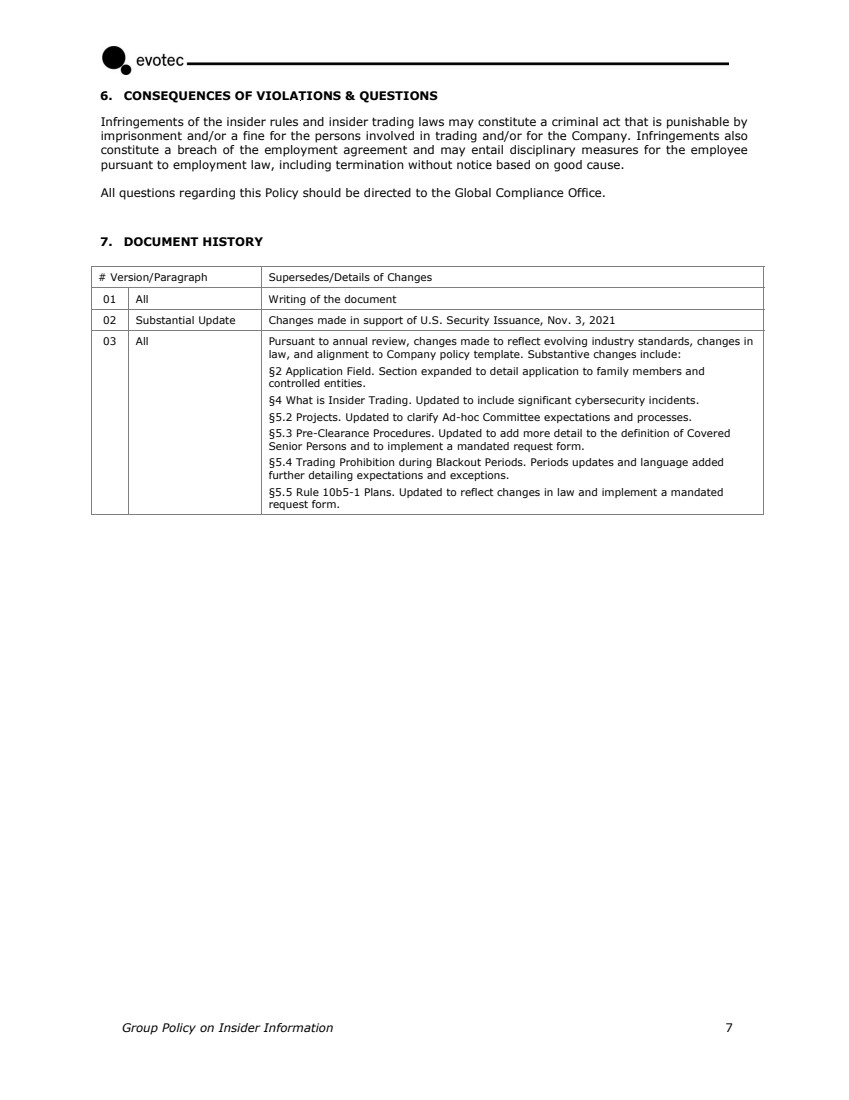

| Group Policy on Insider Information 7 6. CONSEQUENCES OF VIOLATIONS & QUESTIONS Infringements of the insider rules and insider trading laws may constitute a criminal act that is punishable by imprisonment and/or a fine for the persons involved in trading and/or for the Company. Infringements also constitute a breach of the employment agreement and may entail disciplinary measures for the employee pursuant to employment law, including termination without notice based on good cause. All questions regarding this Policy should be directed to the Global Compliance Office. 7. DOCUMENT HISTORY # Version/Paragraph Supersedes/Details of Changes 01 All Writing of the document 02 Substantial Update Changes made in support of U.S. Security Issuance, Nov. 3, 2021 03 All Pursuant to annual review, changes made to reflect evolving industry standards, changes in law, and alignment to Company policy template. Substantive changes include: §2 Application Field. Section expanded to detail application to family members and controlled entities. §4 What is Insider Trading. Updated to include significant cybersecurity incidents. §5.2 Projects. Updated to clarify Ad-hoc Committee expectations and processes. §5.3 Pre-Clearance Procedures. Updated to add more detail to the definition of Covered Senior Persons and to implement a mandated request form. §5.4 Trading Prohibition during Blackout Periods. Periods updates and language added further detailing expectations and exceptions. §5.5 Rule 10b5-1 Plans. Updated to reflect changes in law and implement a mandated request form. |