ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 2025

OR

☐

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from to

Commission File Number: 001-33708

PHILIP MORRIS INTERNATIONAL INC.

(Exact name of registrant as specified in its charter)

Virginia

13-3435103

(State or other jurisdiction of incorporation or organization)

(I.R.S. Employer Identification No.)

677 Washington Blvd, Suite 1100

Stamford

Connecticut

06901

(Address of principal executive offices)

(Zip Code)

203-905-2410

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

Title of each class

Trading Symbol(s)

Name of each exchange on which registered

Common Stock, no par value

PM

New York Stock Exchange

2.750% Notes due 2026

PM26A

New York Stock Exchange

2.875% Notes due 2026

PM26

New York Stock Exchange

0.125% Notes due 2026

PM26B

New York Stock Exchange

3.125% Notes due 2027

PM27

New York Stock Exchange

3.125% Notes due 2028

PM28

New York Stock Exchange

2.875% Notes due 2029

PM29

New York Stock Exchange

3.375% Notes due 2029

PM29A

New York Stock Exchange

2.750% Notes due 2029

PM29D

New York Stock Exchange

3.750% Notes due 2031

PM31B

New York Stock Exchange

0.800% Notes due 2031

PM31

New York Stock Exchange

3.250% Notes due 2032

PM32

New York Stock Exchange

3.125% Notes due 2033

PM33

New York Stock Exchange

2.000% Notes due 2036

PM36

New York Stock Exchange

1.875% Notes due 2037

PM37A

New York Stock Exchange

6.375% Notes due 2038

PM38

New York Stock Exchange

1.450% Notes due 2039

PM39

New York Stock Exchange

4.375% Notes due 2041

PM41

New York Stock Exchange

Title of each class

Trading Symbol(s)

Name of each exchange on which registered

4.500% Notes due 2042

PM42

New York Stock Exchange

3.875% Notes due 2042

PM42A

New York Stock Exchange

4.125% Notes due 2043

PM43

New York Stock Exchange

4.875% Notes due 2043

PM43A

New York Stock Exchange

4.250% Notes due 2044

PM44

New York Stock Exchange

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.Yes☑No☐

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes☐No☑

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes☑No☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes☑No☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer☑Accelerated filer ☐

Non-accelerated filer ☐ Smaller reporting company ☐

Emerging growth company ☐

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☑

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. ☐

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes☐No☑

As of June 30, 2025, the aggregate market value of the registrant’s common stock held by non-affiliates of the registrant was approximately $283 billion based on the closing sale price of the common stock as reported on the New York Stock Exchange.

Class

Outstanding at

January 30, 2026

Common Stock, no par value

1,556,679,579

shares

DOCUMENTS INCORPORATED BY REFERENCE

Parts Into Which Incorporated

Portions of the registrant’s definitive proxy statement for use in connection with its annual meeting of shareholders to be held on May 6, 2026, to be filed with the Securities and Exchange Commission on or about March 26, 2026.

In this report, “PMI,” “we,” “us” and “our” refers to Philip Morris International Inc. and its subsidiaries.

Trademarks and service marks in this report are the registered property of, or licensed by, the subsidiaries of Philip Morris International Inc. and are italicized.

PART I

Item 1.Business.

General Development of Business

General

Philip Morris International Inc. is a Virginia holding company incorporated in 1987. In March 2008, we became a U.S. public company listed on the New York Stock Exchange and subject to the rules of the U.S. Securities and Exchange Commission (the "SEC"). We are a leading international consumer goods company, actively delivering a smoke-free future and evolving our portfolio for the long term to include products outside of the tobacco and nicotine sector. Our current product portfolio primarily consists of cigarettes and smoke-free products, including heat-not-burn, nicotine pouch and e-vapor products. Since 2008, we have invested over $16 billion to develop, scientifically substantiate and commercialize innovative smoke-free products for adults who would otherwise continue to smoke, with the goal of completely ending the sale of cigarettes. This investment includes the building of world-class scientific assessment capabilities, notably in the areas of pre-clinical systems toxicology, clinical and behavioral research, as well as post-market studies. In November 2022, we acquired Swedish Match AB ("Swedish Match") – a leader in oral nicotine delivery – creating a global smoke-free combination led by the companies’ IQOS and ZYN brands. As of April 30, 2024, we hold the full rights to commercialize IQOS in the U.S. after reaching an agreement to end our U.S. commercial relationship covering IQOS with Altria Group, Inc. in 2022. Following a robust science-based review, the U.S. Food and Drug Administration (the "FDA") has authorized the marketing of Swedish Match’s General snus and ZYN nicotine pouches and versions of PMI’s IQOS devices and consumables - the first-ever such authorizations in their respective categories. Versions of IQOS devices and consumablesand General snus also obtained the first-ever Modified Risk Tobacco Product ("MRTP") authorizations from the FDA. We describe the MRTP orders in more detail in the "Business Environment" section of Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations.

With a strong foundation and significant expertise in life sciences, PMI has a long-term ambition to expand into wellness areas. The business strategy of our wellness unit, Aspeya, currently focuses on developing and commercializing primarily oral consumer wellness offerings. This includes medical and non-recreational cannabinoid products (including CBD), in line with applicable regulatory requirements, though any revenue related to cannabinoids is expected to be negligible in the near to medium term.

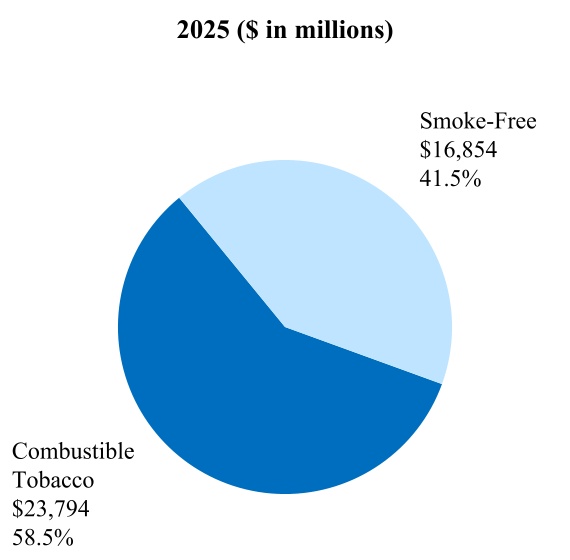

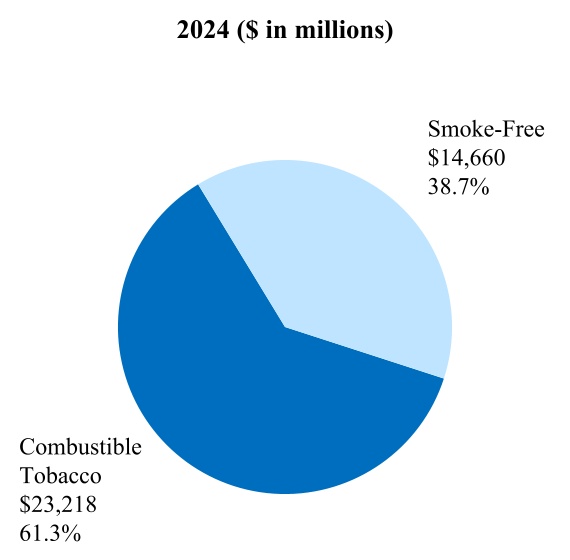

Smoke-Free Business ("SFB”) is the term PMI uses to refer to all of its smoke-free products. SFB also includes wellness products, as well as consumer accessories, such as lighters and matches.

Smoke-free products (also referred to herein as "SFPs") is the term PMI uses to refer to all of its products that provide nicotine without combusting tobacco, such as heat-not-burn, e-vapor, and oral smokeless, and that therefore generate far lower levels of harmful chemicals. As such, these products have the potential to present less risk of harm versus continued smoking.

We have a range of SFPs in various stages of development, scientific assessment and commercialization. Our smoke-free products are designed for, and directed toward, current adult smokers and adult users of nicotine-containing products. We put significant effort to restrict access of our products from underage persons. We believe regulation must include measures designed to prevent youth initiation; and we also support and engage with relevant authorities to seek sensible regulation of flavors, mandated health warnings and minimum age laws.

Our IQOS smoke-freeproduct brand portfolio includes heated tobacco and nicotine-containing vapor products. It uses a precisely controlled heating device into which a specially designed and proprietary tobacco unit is inserted and heated to generate an aerosol. Heated tobacco units ("HTUs") is the term we use to refer to heated tobacco consumables, which include our BLENDS, DELIA, HEETS, HEETS Creations (defined collectively as "HEETS"), SENTIA, TEREA,TEREA CRAFTED and TEREA Dimensions, as well as the KT&G-licensed brands, Fiit and Miix (outside of South Korea). HTUs also include zero tobacco heat-not-burn consumables (LEVIA). IQOS was first introduced in Nagoya, Japan, in 2014.

IQOS,ZYN and VEEV are the leading brands in our SFPs portfolio. As of December 31, 2025, our smoke-free products were available for sale in 106 markets. With regard to modern oral pouches, we increased our presence to 56 markets.

Our cigarettes are sold in approximately 170 markets, and in many of these markets they hold the number one or number two market share position. We have a wide range of premium, mid-price and low-price brands. Our portfolio comprises both international and local brands and is led by Marlboro, the world’s best-selling international cigarette, which accounted for approximately 43% of our total 2025 cigarette shipment volume. Marlboro is complemented in the premium-price category by Parliament. Our other leading

1

international cigarette brands are Chesterfield, L&M, and Philip Morris. These five international cigarette brands contributed 81% of our cigarette shipment volume in 2025. We also own a number of important local cigarette brands, such as Dji Sam Soe and Sampoerna A in Indonesia, and Fortune and Jackpot in the Philippines.

Source of Funds — Dividends

We are a legal entity separate and distinct from our direct and indirect subsidiaries. Accordingly, our right, and thus the right of our creditors and stockholders, to participate in any distribution of the assets or earnings of any subsidiary is subject to the prior rights of creditors of such subsidiary, except to the extent that claims of our company itself as a creditor may be recognized. As a holding company, our principal sources of funds, including funds to make payment on our debt securities, are from the receipt of dividends and repayment of debt from our subsidiaries. Our principal wholly owned and majority-owned subsidiaries currently are not limited by long-term debt or other agreements in their ability to pay cash dividends or to make other distributions that are otherwise compliant with law, including governmental capital and foreign currency exchange controls.

Description of Business

Following the sale of Vectura Group Ltd. on December 31, 2024, we updated our segment reporting in January 2025 by including the ongoing Wellness results (previously referred to as Wellness & Healthcare) in the Europe segment. In addition, we renamed our “PMI Duty Free” business to “PMI Global Travel Retail” effective in the first quarter of 2025. As a result of this change, our segment that includes our duty free business was renamed East Asia, Australia & PMI Global Travel Retail (“EA, AU & PMI GTR”).

As of December 31, 2025, our four geographical segments were as follows:

•Europe Region is headquartered in Lausanne, Switzerland, and covers all the European Union countries, Switzerland, the United Kingdom, and also Ukraine, Moldova and Southeast Europe; it also includes our Wellness business;

•South and Southeast Asia, Commonwealth of Independent States, Middle East and Africa Region ("SSEA, CIS & MEA") is headquartered in Dubai, United Arab Emirates. It covers South and Southeast Asia, the African continent, the Middle East, Turkey, as well as Israel, Central Asia, Caucasus and Russia;

•East Asia, Australia, and PMI Global Travel Retail ("EA, AU & PMI GTR") is headquartered in Hong Kong, and includes the consolidation of our global travel retail business with East Asia & Australia; and

•Americas Region is headquartered in Stamford, Connecticut, and covers the United States, Canada and Latin America.

As communicated in the fourth quarter of 2025, with our smoke-free business now operating at scale across our regions, including substantial growth from our U.S. business, we have implemented an evolved organizational model with two primary business units: International and U.S. The updated organizational structure is designed to enhance our agility and to support our journey to become a smoke-free company under the leadership of Jacek Olczak, Group CEO of PMI. This change was implemented effective January 1, 2026, and as a result we realigned our reportable segments accordingly. The four geographic segments have been replaced with three new reportable segments: International Smoke-Free, International Combustibles, and U.S. As of the first quarter of 2026, our reporting will reflect these changes.

Our shipment volume in 2025, including cigarettes and smoke-free products (in equivalent units) were as follows:

Full-Year 2025

Total PMI

SFP

HTU

Oral SFP

E-vapor

Cigarettes

Total Shipment Volume

(equivalent units in billions)

786.5

179.1

155.1

20.7

3.3

607.4

vs. 2024

1.4%

12.8%

11.0%

18.5%

+100%

(1.5)%

Oral smoke-free products conversion: (i) nicotine pouches (units): 15 pouches per can in the U.S. and approximately 20 pouches per can outside the U.S.; (ii) snus products: weighted average 21 pouches equivalent per can; (iii) moist snuff products: weighted average 17 pouches equivalent per can; (iv) tobacco bits products: weighted average 30 pouches equivalent per can; (v) chew bags products: weighted average 20 pouches per can.

E-vapor products conversion: one milliliter of e-vapor liquid equivalent to 10 units.

2

References in this Form 10-K to total international market, defined as worldwide cigarette and heated tobacco unit volume, excluding the United States, total industry (or total market) and market shares, are our estimates for tax-paid and Global Travel Retail products based on data from a number of internal and external sources, and may, in defined instances, exclude China. Past reported periods may be updated to ensure comparability and to incorporate the most current information for industry and market share reporting.

Unless otherwise stated, references to total industry and our market share performance reflect cigarettes and heated tobacco units.

Key data regarding total market and market share were as follows:

2025

2024

2023

Total Market, billion units (excluding China and the U.S.)

2,587

2,596

2,560

Total International Market Share (1)

29.2%

29.0%

28.6%

Cigarettes

23.4%

23.7%

23.8%

HTU

5.8%

5.3%

4.7%

PMI Cigarette over Cigarette Market Share (2)

25.3%

25.5%

25.4%

Marlboro Cigarette over Cigarette Market Share (3)

10.7%

10.2%

9.8%

(1) Defined as PMI's cigarette and heated tobacco unit in-market sales volume as a percentage of total industry cigarette and heated tobacco unit sales volume, excluding China and the U.S., including cigarillos in Japan

(2) Defined as PMI's cigarette in-market sales volume as a percentage of total industry cigarette sales volume, excluding China and the U.S., including cigarillos in Japan

(3) Defined as Marlboro's cigarette in-market sales volume as a percentage of total industry cigarette sales volume, excluding China and the U.S., including cigarillos in Japan

Note: Sum of share of market by product categories might not foot to total due to roundings

We have a market share of at least 15% in approximately 100 markets, including Algeria, Argentina, Australia, Austria, Brazil, the Czech Republic, Egypt, France, Germany, Greece, Hong Kong, Hungary, Indonesia, Italy, Japan, Kazakhstan, Mexico, the Netherlands, the Philippines, Poland, Portugal, Romania, Russia, Saudi Arabia, the Slovak Republic, South Korea, Spain, Switzerland and Turkey.

Distribution & Sales

Our main types of distribution and sales are tailored to the characteristics of each market and are often used simultaneously:

•Direct sales and distribution, where we sell directly to the retailers;

•Distribution through independent distributors that often distribute other fast-moving consumer goods and are responsible for distribution in a particular market;

•Exclusive zonified distribution, where the dedicated multicategory product distributors are assigned to exclusive territories within a market;

•Distribution through national or regional wholesalers that then supply the retail trade;

•Our own e-commerce infrastructure for product sales to trade partners and to consumers; and

•Our own brand retail infrastructure for our SFPs and accessories for sales to consumers.

3

Competition

We are subject to highly competitive conditions in all aspects of our business. We compete primarily on the basis of product quality, brand recognition, brand loyalty, taste, R&D, innovation, packaging, customer service, marketing, advertising and retail price.

The competitive environment and our competitive position can be significantly influenced by weak economic conditions; erosion of consumer confidence; competitors' introduction of lower-price products or innovative products; adult smoker willingness to convert to our SFPs; higher product taxes; higher absolute prices and larger gaps between retail price categories; and product regulation that diminishes the ability to differentiate products, restricts adult consumer access to truthful and non-misleading information about our SFPs, or disproportionately impacts the commercialization of our products in relation to our competitors.

Competitors in our industry include Altria Group, Inc., British American Tobacco plc, Japan Tobacco Inc., Imperial Brands plc, new market entrants, particularly with respect to innovative products, several regional and local tobacco companies and, in some instances, state-owned tobacco enterprises, principally in Algeria, Egypt, China, Taiwan, Thailand and Vietnam. Some of our competitors have different profit, volume and regulatory objectives, and some international competitors may be less susceptible than PMI to changes in currency exchange rates. Some market participants who sell products that directly compete with ours are circumventing applicable regulations or adopting regulatory interpretations that, in the absence of regulatory intervention and/or enforcement, could lead to an unfair competitive environment in certain markets where we operate. Certain SFP competitors may alienate consumers from innovative products through inappropriate marketing campaigns, messaging and inferior product satisfaction, and without scientific substantiation based on appropriate R&D protocols and standards. The growing use of digital media could increase the speed and extent of the dissemination of inaccurate and misleading information about our SFPs, all of which could have a material adverse effect on our profitability and results of operations.

Procurement and Raw Materials

We purchase tobacco leaf of various types, grades and styles throughout the world, mostly through independent international tobacco suppliers. In 2025, we also contracted directly with farmers in several countries, including Argentina, Brazil, Italy, Pakistan and Poland. In 2025, direct sourcing from farmers represented approximately 23% of PMI’s global leaf requirements. The largest supplies of tobacco leaf are sourced from Argentina, Brazil, China, India, Italy, Indonesia (mostly for domestic use in kretek products), Malawi, Mozambique, the Philippines, Turkey and the United States. We believe that there is a sufficient supply of tobacco leaf in the world markets to satisfy our current and anticipated production requirements.

Given the global reach of our value chain, properly managing land and water resources and utilizing a geographically diversified sourcing strategy for agricultural products are priorities as we seek to increase the resilience of our production systems and minimize operational risks. We conduct a global water risk assessment annually in tobacco-growing regions to identify potential hotspots for physical water risks that require adaptation measures. Our water stewardship strategy includes guidance for applying a landscape approach to water optimization projects, protecting natural resources and recharge areas, and improving the efficiency of irrigation systems to integrate better farm water management.

In 2025, we purchased a wide variety of direct materials from a total of approximately 350 suppliers. The four most significant direct materials that we purchase are printed paper board used in packaging, acetate tow used in filter making, fine paper used in the manufacturing of cigarettes and heated tobacco units, and susceptors used for TEREA and other consumables. In addition, the adequate supply and procurement of cloves are of particular importance to our Indonesian business. For our oral smoke-free products, direct materials include plastic cans and lids for nicotine pouches and traditional snus products, nicotine salt or nicotine premix for nicotine pouches, pouch material for individual pouchmaking and additives. In 2025, our top ten suppliers of direct materials combined represented approximately 60% of our total direct materials purchases.

Additionally, we purchase electronic devices, which are made by various electronic manufacturing services providers ("EMS"). The components used in the assembly of these devices can be made by the EMS or purchased from other suppliers. These components include mechanical parts, electrical and electromechanical components, batteries, semiconductors, and packaging materials.

We discuss the details of our supply chain for our SFPs in Item 7. Management's Discussion and Analysis of Financial Condition and Results of Operations of this Annual Report on Form 10-K (“Item 7”) in Business Environment—Reduced-Risk Products.

Business Environment

Information called for by this Item is hereby incorporated by reference to the paragraphs in Item 7, Business Environment to this Annual Report on Form 10-K.

4

Other Matters

Customers

As described in more detail in “Distribution & Sales” above, in many of our markets we sell our products to distributors. In 2025, sales to a distributor in the Europe Region and a distributor in the EA, AU & PMI GTR Region each amounted to 10 percent or more of our consolidated net revenues. See Item 8, Note 11. Segment Reporting for more information. We believe that none of our business segments is dependent upon a single customer or a few customers, the loss of which would have a material adverse effect on our consolidated results of operations. In some of our markets, particularly in the Europe, SSEA, CIS & MEA, and EA, AU & PMI GTR Regions, a loss of a distributor may result in a temporary market disruption.

Human Capital

Our Workforce. At December 31, 2025, we employed approximately 84,900 people worldwide, including full-time, temporary and part-time staff. Our businesses are subject to a number of laws and regulations relating to our relationship with our employees. Generally, these laws and regulations are specific to the location of each business. We engage with legally recognized employee representative bodies and we have collective bargaining agreements in several of the countries in which we operate. In addition, in accordance with E.U. requirements, we have established a European Works Council composed of management and elected members of our workforce. We believe we maintain good relations with our employees and their representative organizations.

Our Internal Transformation. To be successful in our transformation to a smoke-free future, we must continue transforming our culture and ways of working, align our talent with our business needs, successfully integrate acquired businesses and innovate to become a truly consumer-centric business. To achieve our strategic goals, we need to attract, retain, develop and motivate the best global talent, talent that is diverse and has the right degree of experience, competencies and skills. Our compensation and benefit programs are set at the levels that we believe are necessary to attract the best talent and remain competitive with other consumer product companies.

Oversight and Management. Our Board of Directors (the "Board") provides oversight of various matters pertaining to our workforce. The Compensation and Leadership Development Committee of the Board is responsible for executive compensation matters and oversight of the risks and programs related to human capital management. Our Code of Conduct and Corporate Governance Guidelines highlight our commitment to ethical business conduct and honesty, respect, and fairness.

Collaborative Culture. We are proud of the global reach of our company, with approximately 170 markets where we have sold our products, and with employees representing more than 130 nationalities as of December 31, 2025. We reflect the demographics of the countries, communities, and consumers we serve, which is key to the variety of thought, innovation, and consumer-centric approach that enables us to deliver a smoke-free future.

Our focus is on fostering a performance-driven and collaborative culture, recognizing the value of our global workforce and their contributions. We remain committed to the impact, growth, and well-being of our employees, providing them with the right environment, support, and resources for their careers and professional development.

These principles are codified in our cultural values, which we call the PMI DNA, and we embed these principles throughout our people and business guidelines, practices, and systems.

As the first multinational company to receive a global EQUAL-SALARY certification from the EQUAL-SALARY Foundation in 2019, we completed another year of market level reviews with success and maintained our global certification. We believe this certification is a valuable component in our reputation as an employer.

Government Regulation

As a company with global operations in a heavily regulated industry, we are subject to multiple laws and regulations of the jurisdictions in which we operate. We discuss our regulatory environment in Item 7, Business Environment.

The regulatory landscape related to environmental matters is rapidly evolving. We closely monitor these developments and implement initiatives addressing PMI’s priorities in line with our sustainability strategy. In particular, we are subject to international, national, and local environmental laws and regulations in the countries in which we do business. We have specific programs across our business units designed to meet, and where required, report on, applicable environmental compliance requirements.

Our environmental and occupational health and safety management program takes into account our policies, standard practices and procedures at our manufacturing centers, and, where required, we obtain external third party certification to validate the effectiveness

5

of our management programs. Our subsidiaries expect to continue to make investments in order to drive improved performance and maintain compliance with environmental laws and regulations. We assess and report to our management the compliance status of our legal entities on a regular basis. Based on current regulations, the management and controls we have in place and our review of environmental risks, expenditures related to such matters have not had, and are not expected to have, a material adverse effect on our consolidated results of operations, capital expenditures, financial position, earnings or competitive position.

In Item 1A. Risk Factors, we provide additional details related to risks that could significantly affect our financial results, including regulatory initiatives that could result in a significant decrease in demand for our brands or increase our cost of operation.

We discuss additional information regarding regulatory matters relating to environmental matters in Item 7, Environmental and Social Laws and Regulations.

Information About Our Executive Officers

The disclosure regarding executive officers is hereby incorporated by reference to the discussion under the heading “Information about our Executive Officers as of February 6, 2026” in Part III, Item 10. Directors, Executive Officers and Corporate Governance of this Annual Report on Form 10-K (“Item 10”).

Intellectual Property

Our trademarks are valuable assets, and their protection and reputation are essential to us. We own the trademark rights to all of our principal brands, including Marlboro (outside of the U.S.), HEETS, IQOS, IQOS ILUMA,TEREA, VEEV and ZYN, or have the right to use them in all countries in which these brands are advertised or sold.

In addition, we have a large number of granted patents and pending patent applications worldwide. Our patent portfolio, as a whole, is material to our business. However, no one patent, or group of related patents, is material to us. We also have registered industrial designs, as well as unregistered proprietary trade secrets, technology, know-how, processes and other unregistered intellectual property rights.

Effective January 1, 2008, PMI entered into an Intellectual Property Agreement with Philip Morris USA Inc., a wholly owned subsidiary of Altria Group, Inc. (“PM USA”). The Intellectual Property Agreement allocates ownership of jointly funded intellectual property as follows:

•PMI owns all rights to jointly funded intellectual property outside the United States, its territories and possessions; and

•PM USA owns all rights to jointly funded intellectual property in the United States, its territories and possessions.

The parties agreed to submit disputes under the Intellectual Property Agreement first to negotiation between senior executives and then to binding arbitration.

An agreement was reached with PM USA in 2022 relating to IQOS commercialization rights in the U.S. including, among other things, an agreement relating to intellectual property rights consistent with the commercialization rights for relevant IQOS products.

On February 1, 2024, Philip Morris Products S.A., an indirect, wholly-owned subsidiary of PMI, and Nicoventures Trading Limited, an indirect, wholly-owned subsidiary of British American Tobacco p.l.c., entered into a settlement agreement (the “Settlement Agreement”) for an eight-year term, under which, among other things: (i) certain pending legal proceedings (the “Proceedings”) between them concerning certain of their respective products were dismissed with prejudice, subject to certain limited exceptions, and without admission of liability; (ii) the Limited Exclusion Order and Cease and Desist Order issued by the International Trade Commission on September 29, 2021, prohibiting the importation of certain heat-not-burn products by PMI and its affiliates into the United States was rescinded; and (iii) any injunctions granted to either party in the Proceedings were fully and finally discharged, without admission of liability.

The parties have also agreed to certain covenants not to sue on a perpetual, royalty-free basis or on a royalty-bearing basis, subject to the terms and conditions set forth in the Settlement Agreement, and, among other things, both parties may introduce certain heat-not-burn and vapor products under the Settlement Agreement (including certain evolutions of the existing heat-not-burn and e-vapor products, and certain variants and product line extensions of heat-not-burn and e-vapor products), which products may be royalty-bearing or royalty-free depending on the patents of the other party that may have been used in the development thereof.

6

Seasonality

Our business segments are not significantly affected by seasonality, although in certain markets cigarette consumption may be lower during the winter months due to the cold weather and may rise during the summer months due to outdoor use, longer daylight, and tourism. However, we typically experience higher SFP adult user growth in the first half of each year versus the second half of each year due to seasonal influences.

Available Information

We are required to file with the SEC annual, quarterly and current reports, proxy statements and other information required by the Securities Exchange Act of 1934, as amended (the “Exchange Act”). The SEC maintains an Internet website at http://www.sec.gov that contains reports, proxy and information statements, and other information regarding issuers that file electronically with the SEC, from which investors can electronically access our SEC filings.

We make available free of charge on, or through, our website at www.pmi.com our Annual Report on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K and amendments to those reports filed or furnished pursuant to Section 13(a) or 15(d) of the Exchange Act as soon as reasonably practicable after we electronically file such material with, or furnish it to, the SEC. Investors can access our filings with the SEC by visiting www.pmi.com.

The information on our website is not, and shall not be deemed to be, a part of this report or incorporated into any other filings we make with the SEC.

Item 1A. Risk Factors.

The following risk factors should be read carefully in connection with evaluating our business and the forward-looking statements contained in this Annual Report on Form 10-K. Any of the following risks could materially adversely affect our business, our operating results, our financial condition and the actual outcome of matters as to which forward-looking statements are made in this Annual Report on Form 10-K.

Forward-Looking and Cautionary Statements

We may from time to time make written or oral forward-looking statements, including statements contained in this Annual Report on Form 10-K and other filings with the SEC, in reports to investors and in press releases and investor webcasts. You can identify these forward-looking statements by use of words such as "strategy," "expects," "continues," "plans," "anticipates," "believes," "will," "aspires," "estimates," "intends," "projects," "aims," "goals," "targets," "forecasts" and other words of similar meaning. You can also identify them by the fact that they do not relate strictly to historical or current facts.

We cannot guarantee that any forward-looking statement will be realized, although we believe we have been prudent in our plans and assumptions. Achievement of future results is subject to risks, uncertainties and inaccurate assumptions. Should known or unknown risks or uncertainties materialize, or should underlying assumptions prove inaccurate, actual results could vary materially from those anticipated, estimated or projected. Investors should bear this in mind as they consider forward-looking statements and whether to invest in or remain invested in our securities. In connection with the “safe harbor” provisions of the Private Securities Litigation Reform Act of 1995, we are identifying important factors that, individually or in the aggregate, could cause actual results and outcomes to differ materially from those contained in any forward-looking statements made by us; any such statement is qualified by reference to the following cautionary statements. We elaborate on these and other risks we face throughout this document, particularly in Item 7, Business Environment. You should understand that it is not possible to predict or identify all risk factors. Consequently, you should not consider the following to be a complete discussion of all potential risks or uncertainties. We do not undertake to update any forward-looking statement that we may make from time to time, except in the normal course of our public disclosure obligations.

Overall Business Risks

We may be unsuccessful in our efforts to introduce, commercialize, and grow smoke-free products in existing and new markets, and regulators may prohibit or significantly restrict the commercialization of these products or the communication of scientifically substantiated information and claims.

Our strategic priority is the continued introduction, commercialization, and growth of our SFPs and if these efforts are not successful, in key markets or systematically, our financial results and future growth prospects may be materially adversely impacted. If other market participants are more successful in these efforts or if SFP categories where we hold a competitive advantage are inequitably regulated compared to cigarettes or other SFP categories without regard to the totality of the scientific evidence available for such products, we may be at a competitive disadvantage. In addition, actions of some market participants, such as the inappropriate

7

marketing of e-vapor products to youth, as well as alleged health consequences associated with the use of certain SFPs, may unfavorably impact public opinion and/or mischaracterize the health consequences of our SFPs to consumers, regulators and policy makers without regard to the totality of scientific evidence available for specific products. This may impede our efforts to advocate for the development and maintenance of science-based regulatory frameworks for the development and commercialization of SFPs. We cannot predict the extent to which regulators will permit — or continue to permit — the sale and/or marketing of SFPs and regulatory restrictions have, and could further limit, the commercialization of our SFPs.

Additionally, any claims, regardless of merit, challenging our research and clinical data available to date, may impact the development and maintenance of science-based regulatory frameworks for the commercialization of the SFP category and the commercialization of the SFP category in general.

Our SFPs and commercial activities for these products are designed for, and directed toward, current adult smokers and adult users of nicotine-containing products. We also put significant effort to restrict access of our products from underage persons. Despite our efforts, technological, operational, regulatory and/or commercial developments might impact the implementation or effectiveness of youth access prevention mechanisms and surrounding infrastructure. If there is significant usage, whether actual or perceived, of our products or competitive products among youth or non-nicotine users, even in situations over which we have no control, our reputation and credibility may suffer, the regulatory approach to our products may become more restrictive, and our efforts to advocate for the development of science-based regulatory frameworks for the development and commercialization of SFPs may be significantly impacted.

Consumption of tax-paid cigarettes continues to decline in many of our markets.

This decline is due to multiple factors, including increased taxes and pricing, governmental actions, the diminishing social acceptance of smoking, health concerns, competition, continuing economic and geopolitical uncertainty, and the continuing prevalence of illicit products. These factors and their potential consequences are discussed more fully below and in Item 7, Business Environment. The decline in the consumption of cigarettes could have a material adverse effect on our revenues, cash flows and profitability, which in turn may have a material adverse effect on our ability to fund our smoke-free transformation.

Our business faces significant governmental actions aimed at increasing regulatory requirements with the goal of reducing or preventing the use of tobacco or nicotine-containing products.

Governmental actions, combined with the diminishing social acceptance of smoking and private actions to restrict smoking, have resulted in reduced industry volumes for our combustible products in many of our markets, and we expect that such factors will continue to reduce combustible consumption levels and will increase down-trading and the risk of counterfeiting, contraband, illicit trade and cross-border purchases.

Governmental actions to restrict or entirely prohibit the use of certain SFP categories have also been considered or adopted in various jurisdictions. A significant factor influencing these developments are reports issued by the World Health Organization (the "WHO”) and Framework Convention on Tobacco Control (the "FCTC"), and related proposals, which make a number of policy recommendations on SFPs that, if implemented, could restrict both the availability of these products and the access to accurate information about them. These reports and proposals are not binding on the WHO Member States or on parties to the FCTC, and so it is not possible to predict the extent to which any of the reports or proposals are implemented into regulations by Member States. However, these proposed guidance documents could ultimately lead to restrictions on the availability of certain of our SFPs or access to accurate information about them in one or more of our current or future markets, which could have a material adverse effect on our financial results and growth prospects.

We anticipate that significant regulatory restrictions will continue to be considered and adopted in many markets. Regulatory initiatives that have been contemplated, proposed, introduced, or enacted by governmental authorities in various jurisdictions include:

•

restrictions on or licensing of outlets permitted to sell tobacco or nicotine-containing products;

•

the levying of substantial and increasing tax and duty charges;

•

restrictions or bans on advertising, marketing and sponsorship;

•

the display of larger health warnings, graphic health warnings and other labeling requirements;

•

restrictions on packaging design, including the use of colors, and mandating plain packaging;

8

•

restrictions on packaging and cigarette formats and dimensions;

•

restrictions or bans on the display of product packaging at the point of sale and restrictions or bans on vending machines;

•

generation sales bans, under which the sale of certain tobacco or nicotine-containing products to people born after a certain year would be prohibited;

Classification of the product as food such that any nicotine amounts beyond de minimis content de facto bans the nicotine product from the market

•

requirements regarding testing, disclosure and performance standards for tar, nicotine, carbon monoxide and/or other smoke or product constituents;

•

disclosure, restrictions, or bans of tobacco and nicotine-containing product ingredients, components or other product features, including bans on the flavors of certain tobacco and nicotine-containing products, and restrictions on certain device features;

•

increased restrictions on smoking and use of tobacco and nicotine-containing products in public or private spaces, both indoors or outdoors;

•

restrictions or prohibitions of novel tobacco or nicotine-containing products or related devices;

•

elimination of duty free sales and duty free allowances for travelers;

•

restrictions in terms of importing or exporting our products impacting our logistics activities and ability to ship our products;

•

encouraging litigation against tobacco companies; and

•

excluding tobacco companies from transparent public dialogue regarding public health and other policy matters.

Our financial results could be materially affected by regulatory initiatives resulting in a significant decrease in demand for our brands. More specifically, requirements that lead to a commoditization of tobacco products or impede adult consumers' ability to access and convert to our SFPs, as well as any significant increase in the cost of complying with new regulatory requirements, could have a material adverse effect on our financial results and growth prospects.

The success of our business in the United States is dependent on an evolving legal and regulatory framework.

Federal, state or local government action, including regulatory actions and inaction by the FDA, may have a material adverse impact on our commercialization of SFPs and in our business in the United States. The FDA’s premarket tobacco product and modified risk tobacco product authorizations of two versions of our IQOS product as well as the premarket tobacco authorizations of 20 varieties of ZYN nicotine pouches are subject to strict marketing, reporting and other requirements. Although we have received these authorizations from the FDA, there is no guarantee that the products will remain authorized for sale in the United States, or that new versions of IQOS or other ZYN products will receive authorizations, particularly if there is a significant uptake in youth or non-nicotine user initiation.

The commercialization of our products in the United States is dependent on successfully managing compliance with federal, state, and local laws, regulations, legal agreements, and related interpretations. Failure to successfully manage compliance and to resolve any disputes that may arise regarding the application of legal and administrative requirements to our products could negatively impact the timing, manner, or success of our SFP commercialization in the United States, which could in turn have a material adverse effect on our results of operations, revenues, cash flows, or profitability.

We face intense competition, and our failure to compete effectively could have a material adverse effect on our profitability and results of operations.

We are subject to highly competitive conditions in all aspects of our business. See Item 1, Business—Competition for a description of the competitive environment in which we operate. The competitive environment and our competitive position can be significantly influenced by weak economic conditions; erosion of consumer confidence; competitors' introduction of lower-price products or innovative products; adult smoker willingness to convert to our SFPs; higher product taxes; higher absolute prices and larger gaps between retail price categories; unfair competition; and product regulation that diminishes the ability to differentiate products, restricts adult consumer access to truthful and non-misleading information about our SFPs, or disproportionately impacts the commercialization of our products in relation to our competitors.

Some of our competitors have different profit, volume and regulatory objectives, some international competitors may be less susceptible than PMI to changes in currency exchange rates, and some competitors may sell products in circumvention of applicable regulations that compete directly with our products. Certain SFP competitors may alienate consumers from innovative products through inappropriate marketing campaigns, messaging and inferior product satisfaction, and without scientific substantiation based on

9

appropriate R&D protocols and standards, all of which could have a material adverse effect on our profitability and results of operations.

We may be unable to anticipate changes in adult consumer preferences.

Our business is subject to changes in adult consumer preferences and if we do not accurately assess market trends, are unable to adapt our product offerings to evolving consumer demands, or face challenges in product development, we could experience missed opportunities, supply chain challenges, reduced competitiveness, inefficient expenditures, and potential impacts on our customer base and brand reputation. Furthermore, restrictions pertaining to packaging, labeling, or promotional and advertising activities may limit our ability to effectively communicate product innovations intended to address changing adult consumer preferences. Any of these factors could have a material adverse effect on our results of operations, revenues, cash flows, profitability, and prospects for growth.

The financial and business performance of our smoke-free products is less predictable than our cigarette business.

Our SFPs compete in relatively new categories, and the pace at which adult smokers adopt them may vary, depending on the competitive, regulatory, fiscal and cultural environment, and other factors in a specific market. There may be periods of accelerated growth and periods of slower growth for these products, the timing and drivers of which may be more difficult for us to predict versus our mature cigarette business. The impact of this lower predictability on our projected results for a specific period may be significant, due to geopolitical or macroeconomic events that negatively impact SFP availability or adoption, which in turn may have a material adverse effect on our results of operations.

Our ability to grow profitability may be limited by our inability to introduce new products, enter new markets, maintain sufficient production capacity, or improve our margins through higher pricing and improvements in our brand and geographic mix.

Our profit growth may be materially adversely impacted if we are unable to introduce new products or enter new markets successfully, to meet the demand for our products with increased production capacity, to raise prices, or to improve the proportion of our sales of higher margin products and in higher margin geographies.

Our management uses certain key business metrics to evaluate our business, measure our performance, identify trends affecting our business, formulate financial projections and make strategic decisions and such metrics may not accurately reflect all of the aspects of our business needed to make such evaluations and decisions, in particular as our business continues to evolve.

In addition to our consolidated financial results, our management regularly reviews a number of operating, performance, risk, and financial metrics, including various revenue, user and sales metrics (such as market shares, in-market sales, adjusted in-market sales, and SFP users) to evaluate our business, measure our performance, identify trends affecting our business, formulate financial projections and make strategic decisions. We believe that these metrics are representative of our current business; however, these metrics may not accurately reflect all aspects of our business and we anticipate that these metrics may change or may be substituted for additional or different metrics as our business evolves. Furthermore, in some instances the metrics are based upon a number of assumptions and estimates that, while presented with numerical specificity, are inherently subject to significant uncertainties and contingencies. If our management fails to account for other relevant information or to substitute the key business metrics they review as our business changes or if the assumptions or estimates underlying the metrics are inaccurate, their ability to accurately formulate financial projections and make strategic decisions may be compromised and our business, financial results and future growth prospects may be adversely impacted.

Our ability to achieve our strategic goals may be impaired if we fail to attract, motivate and retain the best global talent and effectively align our organizational design with the goals of our transformation.

To be successful, we must continue evolving our culture and ways of working, align our talent and organizational design with our increasingly complex business needs, and innovate and transform to a consumer-centric business. We compete for talent with companies in the consumer products, technology, pharmaceutical and other sectors that enjoy greater societal acceptance. As a result, we may be unable to attract, motivate and retain the best global talent with the right degree of diversity, experience and skills to achieve our strategic goals.

Risks Related to Taxation and Finance

Cigarettes are subject to substantial taxes. Significant increases in cigarette-related taxes have been proposed or enacted and are likely to continue to be proposed or enacted in numerous jurisdictions. These tax increases may disproportionately affect our profitability and make us less competitive versus certain of our competitors.

Tax regimes, including excise taxes, sales taxes and import duties, can disproportionately affect the retail price of cigarettes versus other combustible tobacco products, or disproportionately affect the relative retail price of our cigarette brands versus cigarette brands

10

manufactured by certain of our competitors. Because our portfolio is weighted toward the premium-price cigarette category, tax regimes based on sales price can place us at a competitive disadvantage in certain markets. Furthermore, our volume and profitability may be adversely affected in these markets.

In addition, increases in cigarette taxes are expected to continue to have an adverse impact on our sales of cigarettes, due to resulting lower consumption levels, a shift in sales from manufactured cigarettes to other combustible tobacco products and from the premium-price to the mid-price or low-price cigarette categories, where we may be under-represented, from local sales to cross-border purchases of lower price products, or to illicit products such as contraband, counterfeit and other non-compliant or otherwise illicit products.

Each of these risks could have a material adverse effect on our business, operations, results of operations, revenues, cash flows and profitability.

We may be unsuccessful in our efforts to differentiate smoke-free products and cigarettes with respect to taxation.

To date, we have been largely successful in demonstrating to regulators that our SFPs are not cigarettes due to the absence of combustion, and accordingly they are frequently taxed either as a separate category or as other tobacco products, which typically yields more favorable tax rates than cigarettes. Nevertheless, some jurisdictions have considered or adopted taxation regimes with SFP taxation rates approaching or equal to cigarettes and we are unable to predict whether new regulations, or reinterpretations of existing regulations, will result in SFPs being taxed in line with other tobacco products such as conventional cigarettes in additional jurisdictions, on a prospective or retroactive basis. If we are not successful in our efforts to maintain differentiation, SFP unit margins may be materially adversely affected, which in turn may have a material adverse effect on our results of operations, revenues, cash flows, and profitability.

Changes in the earnings mix and changes in tax laws may result in significant variability in our effective tax rates. Our ability to receive payments from foreign subsidiaries or to repatriate royalties and dividends could be restricted by local country currency exchange controls and other regulations.

We are subject to income tax laws in the United States and numerous foreign jurisdictions. Changes in the tax laws of foreign jurisdictions could arise as a result of the base erosion and profit shifting project undertaken by the Organisation for Economic Co-operation and Development (the "OECD"), which could have a material adverse impact on our effective tax rate thereby reducing our net earnings. Such changes, as well as changes in taxing jurisdictions’ administrative interpretations, decisions, policies, or positions, could also have a material adverse impact on our effective tax rate thereby reducing our net earnings. Currently, many countries have enacted or taken actions to align with the OECD’s framework on a global minimum tax (referred to as “Pillar Two”), effective for taxable years beginning after December 31, 2023. In future periods, our ability to recover deferred tax assets could be subject to additional uncertainty as a result of such developments. Furthermore, changes in the earnings mix or applicable foreign tax laws may result in significant variability in our effective tax rates.

Unstable geopolitical conditions or events in certain markets, including international conflicts, civil unrest, acts of war, terrorism, governmental changes, or changes in international relations could result in negative tax impacts. As a result of Russia’s invasion of Ukraine, certain taxing jurisdictions, including the U.S., have proposed punitive tax legislation applicable to companies doing business in Russia, which could also have a material adverse impact on our effective tax rate if enacted thereby reducing our net earnings.

We are a U.S. holding company whose most significant source of funds is distributions from our non-U.S. subsidiaries. Certain countries in which we operate have adopted or could institute currency exchange controls and other regulations or policies that limit or prohibit our local subsidiaries' ability to convert local currency into U.S. dollars or to make payments outside the country. This could subject us to the risks of local currency devaluation and business disruption.

Disruptions in the credit markets or changes to our credit ratings may adversely affect our business.

We currently generate significant cash flows from ongoing operations and have access to global credit markets through our various short- and long- term financing activities. Our financial performance, our credit ratings, interest rates, the stability of financial institutions with which we partner, geopolitical or national developments, the stability and liquidity of the credit markets and the state of the global economy could affect the availability and cost of financing.

Disruption in the credit markets, limitations on our ability to borrow, slower than anticipated debt deleveraging, or a downgrade of our current credit rating could increase our future borrowing costs which could materially and adversely affect our financial condition and results of operations. In addition, tighter or more volatile credit markets may lead to business disruptions for certain of our suppliers, contract manufacturers or trade customers which could, in turn, adversely impact our business, results of operations, cash flows and financial condition.

11

We may be required to write down assets due to impairment, which could have a material adverse effect on our results of operations or financial position.

We continuously monitor the values of our long-lived assets, reporting units, intangible assets, as well as investments in equity securities, to determine whether events or changes in circumstances indicate that an impairment exists. We also test goodwill and non-amortizable intangible assets for impairment annually. The values of these assets may be affected by several factors, including general macroeconomic and geopolitical conditions; regulatory and legal developments; changes in product volume growth rates; changes in pricing strategies and cost bases; discount rates; success of planned new product expansions; competitive activity; and income and excise taxes. If an impairment is determined to exist, we will incur impairment losses, which could have a material adverse effect on our results of operations or financial position. See Item 7, Management’s Discussion and Analysis of Financial Condition and Results of Operations—Critical Accounting Estimates for additional information concerning impairment determination and calculation.

Risks Related to the Impact of the War in Ukraine on our Business

Our business, results of operations, cash flows and financial position may be adversely impacted by the continuation and consequences of the war in Ukraine.

In 2025, Russia accounted for around 9% of our total cigarette and heated tobacco unit shipment volume, and around 6% of our total net revenues. Ukraine accounted for around 2% of our total cigarette and heated tobacco unit shipment volume, and around 1% of our total net revenues.

The full implications of the Russian invasion of Ukraine for our operations in those countries are impossible to predict at this time. The likelihood of action by the Russian government against PMI, including the possibility of legal action against us or our employees; the deprivation of rights in, or access to, our Russian or Russia-related assets; or nationalization of foreign businesses or assets (including cash reserves held in Russia and intangible assets such as trademarks), is impossible to predict. We are continuously assessing the evolving situation in Russia, including regulatory constraints in the market entailing very complex terms and conditions that must be met for any divestment transaction to be granted approval by the authorities, and restrictions resulting from international regulations. In the event of a divestment, our ability to fully realize the value of the business would likely be subject to material impairment. The deprivation of rights in, or access to, our Russian or Russia-related assets could also result in a material impairment and could cause the deconsolidation of our Russian business. In Ukraine, it is not possible to know when and to what extent we will be able to fully normalize our operations or to what extent our workforce, facilities, inventory, and other assets will remain intact. These developments have and will continue to have a material adverse impact on our business, results of operations, cash flows and financial position, and may result in further impairment charges.

The conflict also continues to elevate the likelihood of supply chain disruptions, both in the region and globally, and may inhibit our ability to timely source materials and services needed to make and sell our products. Furthermore, the imposition of various restrictions on transactions with parties from certain jurisdictions, the ban on exports of various products, and other economic and financial restrictions may adversely affect us or certain third parties with which we do business in Russia, such as customers, suppliers, intermediaries, service providers and banks.

The broader consequences of the invasion are also impossible to predict, but could include reputational consequences; further sanctions, financial or currency restrictions, punitive tax law changes, embargoes, regional instability, or geopolitical shifts; and adverse effects on macroeconomic conditions, security conditions, currency exchange rates, and financial markets. Given the nature of our business and global operations, such geo-political instability and uncertainty could increase the costs of our materials and operations; reduce demand for our products; have a negative impact on our supply chains, manufacturing capabilities, or distribution capabilities; increase our exposure to currency fluctuations; constrain our liquidity or our ability to access capital markets; create staffing or operations difficulties; or subject us to increased cyber-attacks. While we will continue to monitor this fluid situation and develop contingency plans as necessary to address any disruptions to our business operations as they develop, the extent of the conflict’s effect on our business and results of operations as well as the global economy, cannot be predicted.

The conflict may also heighten many other risks disclosed in this Form 10-K, any of which could adversely affect our business, results of operations, cash flows or financial position. Such risks could affect, without limitation, the achievement of our strategic priorities, including achievement of our smoke-free business growth targets; the availability of third-party manufacturing resources; the availability of attractive acquisition and strategic business opportunities and our ability to fully realize the benefits of these transactions; our ability to attract, motivate, and retain the best global talent; and our loss of revenue from counterfeiting and similar illicit activities.

12

Risks Related to Sourcing, Distribution and Quality of Products, Services and Materials

Use of third-parties may negatively impact the distribution, quality, and availability of our products and services, and we may be required to replace third-party contract distributors, manufacturers or service providers.

We increasingly rely on third-parties and their subcontractors/suppliers, sometimes concentrated in a specific geographic area, for product distribution and to manufacture some of our products and product parts (particularly, electronic devices and accessories), as well as to provide services, including to support our finance, commercialization and information technology processes. While many of these arrangements improve efficiency and decrease our operating costs, they also diminish our direct control. Such diminished control may lead to disruption in the distribution of our products and may have a material adverse effect on the quality and availability of products or services, our supply chain, and the speed and flexibility in our response to changing market conditions and adult consumer preferences, all of which may place us at a competitive disadvantage or negatively impact our reputation. In addition, we may be unable to renew these agreements on satisfactory terms for numerous reasons, including government regulations, and the distribution of our products may be disrupted in certain markets or our costs may increase significantly if we must replace such third parties with other partners or our own resources.

Additionally, we expect that these third parties adhere to our applicable standards and to applicable laws related to product quality, responsible marketing, data protection, labor practices, and other areas. Our ability to monitor and enforce compliance is inherently limited and these parties may fail to comply with our standards or to operate in accordance with our expectations or legal requirements, which could expose us to operational disruptions, legal or regulatory liabilities, reputational damage, or financial losses.

Risks related to the natural environment and related legal or regulatory developments may have a negative impact on our business and results of operations.

While we seek to mitigate the physical risks to our business associated with the natural environment through a comprehensive strategy that includes the development and implementation of robust mitigation and adaptation measures, we recognize that there are residual risks that lie beyond our operational control. For example, increased frequency and intensity of extreme droughts, floods, and/or heatwaves could negatively affect our manufacturing operations, tobacco-growing areas, third-party operators and third-party manufacturers sites, and supply regions for products and raw materials, all of which may lead to disruption of our supply chain and of operations at factories, warehouses and other premises.

Furthermore, there is a continued and, in some cases, increased focus by certain regulatory and legislative bodies on environmental policies, including by the governmental authorities in certain international jurisdictions where we operate.These policies include, among others, carbon emissions and other environmentally focused taxation and fees as well as disclosure requirements, which could lead to additional taxation; energy price increases; disclosure and data assurance risks; new compliance costs; increased distribution and supply chain costs; and other expenses impacting our cost of operations. Moreover, given that the regulatory landscape in this regard is highly dynamic and fragmented across the many jurisdictions where we operate, additional uncertainties may be driven by regulatory changes with limited time for implementation and by contradictory requirements across jurisdictions, which could elevate the cost or complexity of our operations or create compliance risks. Additionally, government authorities, non-governmental organizations and other external stakeholders are increasingly filing lawsuits or initiating regulatory actions, alleging that public statements regarding sustainability-related matters and practices are misleading or false.

Government mandated prices, production control programs, and shifts in crops driven by economic conditions may increase the cost or reduce the quality of tobacco and other agricultural products used to manufacture our products.

As with other agricultural products, the price of tobacco leaf and cloves can be influenced by imbalances in supply and demand and the impacts of natural disasters and pandemics such as COVID-19. Tobacco production in certain countries is subject to a variety of controls, including government mandated prices and production control programs. Changes in the patterns of demand for agricultural products could cause farmers to produce less tobacco or cloves. Any significant change in tobacco leaf and clove prices, quality and quantity could affect our profitability and our business.

Additionally, we source the vast majority of our tobacco from a global network of farmers across multiple countries, rather than through commodity markets, which helps ensure the consistency, quality, and traceability of our tobacco supply. However, this model also means that disruptions to farmer livelihoods, if not actively mitigated, could lead to supply chain disruption through farmer exit, reduced crop quality, unsustainable farming practices, increased regulatory scrutiny, and reputational risks.

A prolonged disruption of facilities used to produce our products could have a material adverse effect on our business, financial condition and results of operations.

A prolonged disruption at or shut-down of one or more of the facilities where our products or product components are produced, or sourced from, especially our ZYN production facility in Kentucky, U.S., which currently supplies substantially all of our capacity for ZYN sales in the U.S., due to natural- or man-made disasters or other events outside of our control, such as equipment malfunction or widespread outbreaks of acute illness, including COVID-19, supply chain constraints, a cybersecurity incident, or for any other reason, could limit our capacity to meet customer demands. Such an event could disrupt our operations; delay production, shipments and

13

revenue; and result in significant expense to repair or replace affected facilities. As a result, we could forgo revenue opportunities and potentially lose market share, which could materially and adversely affect our business, financial condition and results of operations.

We could decide, or be required to, recall products, which could have a material adverse effect on our business, reputation, results of operations, cash flows or financial position.

We could decide - or laws, regulations, or administrative action could require us - to recall products due to the failure, or alleged failure, to meet quality or safety standards or specifications, suspected or confirmed and deliberate or unintentional product contamination, manufacturing defects, or other product safety concerns, adulteration, misbranding or tampering. A product recall or a product liability or other claim (even if unsuccessful or without merit) could generate negative publicity about us and our products, and our reputation or that of our brands may be adversely affected. In addition, if another company recalls or experiences negative publicity related to a product in a category in which we compete, adult nicotine consumers might reduce their overall consumption of products in that product category. Any of these events could have a material adverse effect on our business, reputation, results of operations, cash flows or financial position.

Risks Related to our International Operations

Because we have operations in numerous countries, our results may be adversely impacted by economic, regulatory and political developments, natural disasters, pandemics or conflicts.

Some of the countries in which we operate face the threat of civil unrest and can be subject to regime changes. In others, nationalization, terrorism, conflict and the threats of war or acts of war may have a significant impact on the business environment. Factors beyond our control, such as, without limitation, natural disasters; extreme weather events; pandemics; adverse economic, political or regulatory events; acts of war or threats of war; formal or informal bans or boycotts or changes in consumer preferences resulting from geopolitical developments; geopolitical instability affecting international trade; or other developments, could disrupt or increase the expenses related to our supply chain, manufacturing capabilities, distribution capabilities, or the energy and other utility services required to operate our factories, warehouses, and other premises. Our business continuity plans and other safeguards might not always be effective to fully mitigate their impact. Additionally, while we do not now expect that the recent and currently anticipated trade tariffs imposed by the U.S. and other countries will materially impact our business, the global tariff environment is volatile and further tariff or trade related developments could result in risks to PMI’s business, including increased production costs; limited market access; supplier financial condition degradation resulting in reduced or interrupted supplies; and price increases or other economic impacts that could reduce consumer demand. Any of these developments could cause significant volume declines in our Global Travel Retail business and certain other key markets; disrupt or delay our distribution, manufacturing or supply chain; increase currency volatility; increase costs of our materials and operations and lead to loss of property or equipment that are critical to our business in certain markets and difficulty in staffing and managing our operations, all of which could have a material adverse effect on our business, operations, volumes, revenues, cash flows, financial position, net earnings and profitability. We discuss additional risks associated with Russia's invasion of Ukraine above.

In certain markets, we are dependent on governmental approvals of various actions such as price changes, and failure to obtain such approvals could impair growth of our profitability.

In addition, despite our high ethical standards and rigorous controls and compliance policies aimed at preventing and detecting unlawful conduct, given the breadth and scope of our international operations, we may not be able to detect all potential improper or unlawful conduct by our employees and partners. Such improper or unlawful conduct (actual or alleged) could lead to litigation and regulatory action, cause damage to our reputation and that of our brands, and result in substantial costs.

Our reported results could be adversely affected by unfavorable currency exchange rates and currency fluctuations could impair our competitiveness. Our results could also be adversely affected by capital controls or by foreign currency exchange constraints or devaluations.

We conduct our business primarily in local currency and, for purposes of financial reporting, the local currency results are translated into U.S. dollars based on average exchange rates prevailing during a reporting period. Foreign currencies may fluctuate significantly against the U.S. dollar, reducing our net revenues, operating income and EPS. Our primary local currency cost bases may be different from our primary currency revenue markets, and U.S. dollar fluctuations against various currencies may have disproportionate negative impact on cash flows and on net revenues as compared to our gross profit and operating income margins.

Capital controls and/or foreign currency exchange constraints may affect the ability of our subsidiaries in impacted jurisdictions to settle foreign currency denominated imports of goods and services and/or to pay dividends and royalties. These factors may also increase foreign currency devaluation risks, which may have a negative impact on our net assets and results of operations in these jurisdictions. All of which could have a material adverse effect on our financial condition, including our leverage ratios, cash flows, liquidity, net earnings, and profitability.

14

A sustained period of elevated inflation across the markets in which we operate could result in higher operating and financing costs and lead to reduced demand for our products.