Please wait

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

___________________________________________________________

FORM 6-K

___________________________________________________________

Report of Foreign Private Issuer

Pursuant to Rule 13a-16 or 15d-16 under

the Securities Exchange Act of 1934

For the quarterly period ended March 31, 2026

Commission file number 1-33867

___________________________________________________________

TEEKAY TANKERS LTD.

(Exact name of Registrant as specified in its charter)

___________________________________________________________

2nd Floor, Swan Building, 26 Victoria Street, Hamilton, HM 12, Bermuda

(Address of principal executive office)

___________________________________________________________

Indicate by check mark whether the registrant files or will file annual reports under cover of Form 20-F or Form 40-F.

Form 20-F ý Form 40-F ¨

TEEKAY TANKERS LTD.

REPORT ON FORM 6-K FOR THE QUARTERLY PERIOD ENDED MARCH 31, 2026

INDEX

PART I – FINANCIAL INFORMATION

ITEM 1 – FINANCIAL STATEMENTS

TEEKAY TANKERS LTD. AND SUBSIDIARIES

UNAUDITED CONSOLIDATED STATEMENTS OF INCOME (note 1)

(in thousands of U.S. Dollars, except share and per share amounts)

| | | | | | | | | | | | | | | | | | |

| | Three months ended March 31, | | |

| | 2026 | | 2025 | | | | |

| | $ | | $ | | | | |

| | | | | | | | |

Voyage charter revenues (note 3) | | 231,093 | | 192,643 | | | | |

Time-charter revenues (note 3) | | 13,755 | | 6,314 | | | | |

Bareboat-charter revenues (note 3) | | 2,877 | | — | | | | |

Other revenues (note 3) | | 38,369 | | 32,682 | | | | |

| Total revenues | | 286,094 | | 231,639 | | | | |

| | | | | | | | |

Voyage expenses (note 6) | | (57,615) | | (86,867) | | | | |

Vessel operating expenses | | (61,217) | | (61,168) | | | | |

Charter hire expenses (note 8) | | (9,678) | | (14,409) | | | | |

| Depreciation and amortization | | (22,188) | | (23,240) | | | | |

| General and administrative expenses | | (10,380) | | (9,712) | | | | |

Gain on sale and write-down of assets (note 12) | | 22,656 | | 38,163 | | | | |

| | | | | | | | |

| Income from operations | | 147,672 | | 74,406 | | | | |

| | | | | | | | |

| Interest income | | 8,046 | | 5,857 | | | | |

| Interest expense | | (489) | | (773) | | | | |

| | | | | | | | |

Gain on distribution and equity income from equity-accounted investment (note 13) | | 1,500 | | 230 | | | | |

Other income (expense) (note 14) | | 821 | | (4,158) | | | | |

| Net income before income tax | | 157,550 | | 75,562 | | | | |

Income tax (expense) recovery (note 15) | | (3,999) | | 470 | | | | |

| Net income | | 153,551 | | 76,032 | | | | |

| | | | | | | | |

| | | | | | | | |

Per common share amounts (note 16) | | | | | | | | |

| - Basic earnings per share | | $4.42 | | $2.20 | | | | |

| - Diluted earnings per share | | $4.40 | | $2.19 | | | | |

| - Cash dividends declared | | $0.25 | | $0.25 | | | | |

| | | | | | | | |

Weighted-average number of Class A and Class B common shares outstanding (note 16) | | | | | | | | |

| - Basic | | 34,758,582 | | 34,482,849 | | | | |

| - Diluted | | 34,909,856 | | 34,666,717 | | | | |

| | | | | | | | |

Related party transactions (note 11) | | | | | | | | |

The accompanying notes are an integral part of the unaudited consolidated financial statements.

TEEKAY TANKERS LTD. AND SUBSIDIARIES

UNAUDITED CONSOLIDATED BALANCE SHEETS (note 1)

(in thousands of U.S. Dollars)

| | | | | | | | | | | | | | |

| | As at | | As at |

| | March 31, 2026 | | December 31, 2025 |

| | $ | | $ |

| ASSETS | | | | |

| Current | | | | |

| Cash and cash equivalents | | 722,009 | | 830,569 |

Short-term investments (note 9) | | 274,142 | | 22,000 |

Restricted cash – current (note 17) | | — | | 692 |

| | | |

| Accounts receivable, net of allowance of $4.8 million (2025 - $4.4 million) | | 113,001 | | 82,781 |

Assets held for sale (note 12) | | 61,036 | | 26,834 |

Due from affiliates (note 11) | | 3,642 | | 2,804 |

| Bunker and lube oil inventory | | 28,719 | | 29,409 |

| Prepaid expenses | | 17,195 | | 17,013 |

| | | | |

| Accrued revenue | | 36,168 | | 52,005 |

Other current assets (note 5) | | 14,288 | | 15,351 |

| Total current assets | | 1,270,200 | | 1,079,458 |

| | | | |

| Vessels and equipment | | | | |

At cost, less accumulated depreciation of $494.3 million (2025 - $487.7 million) (notes 3, 5, 7 and 12) | | 1,053,098 | | 1,000,483 |

| | | | |

Operating lease right-of-use assets (note 8) | | 32,998 | | 38,161 |

| Total vessels and equipment | | 1,086,096 | | 1,038,644 |

| | | | |

| | | | |

Goodwill and intangible assets (note 5) | | 10,481 | | 2,426 |

Other non-current assets (note 5) | | 23,742 | | 121,146 |

| | | | |

| Total assets | | 2,390,519 | | 2,241,674 |

| LIABILITIES AND EQUITY | | | | |

| Current | | | | |

| Accounts payable | | 28,085 | | 19,926 |

Accrued liabilities (note 6) | | 75,365 | | 84,724 |

| | | | |

| | | | |

| | | | |

| | | | |

Current portion of operating lease liabilities (note 8) | | 19,422 | | 21,107 |

Due to affiliates (note 11) | | 410 | | 595 |

Other current liabilities (note 3) | | 11,868 | | 8,938 |

| Total current liabilities | | 135,150 | | 135,290 |

| | | | |

| | | | |

Long-term operating lease liabilities (note 8) | | 13,577 | | 17,054 |

| | | | |

Other long-term liabilities (note 6) | | 51,880 | | 45,714 |

| Total liabilities | | 200,607 | | 198,058 |

Commitments and contingencies (notes 7, 8, 9 and 18) | | | | |

| Equity | | | | |

Common shares and additional paid-in capital (585.0 million shares authorized, 30.0 million Class A and 4.6 million Class B shares issued and outstanding as of March 31, 2026, and 585.0 million shares authorized, 29.9 million Class A and 4.6 million Class B shares issued and outstanding as at December 31, 2025) (note 10) | | 1,316,092 | | 1,314,640 |

| Accumulated surplus | | 873,820 | | 728,976 |

| Total equity | | 2,189,912 | | 2,043,616 |

| Total liabilities and equity | | 2,390,519 | | 2,241,674 |

Subsequent events (note 19)

The accompanying notes are an integral part of the unaudited consolidated financial statements.

TEEKAY TANKERS LTD. AND SUBSIDIARIES

UNAUDITED CONSOLIDATED STATEMENTS OF CASH FLOWS (note 1)

(in thousands of U.S. Dollars)

| | | | | | | | | | | | | | |

| | Three Months Ended March 31, |

| | 2026 | | 2025 |

| | $ | | $ |

| Cash, cash equivalents and restricted cash provided by (used for) | | | | |

| OPERATING ACTIVITIES | | | | |

| Net income | | 153,551 | | 76,032 |

| Non-cash items: | | | | |

| Depreciation and amortization | | 22,188 | | 23,240 |

Gain on sale and write-down of assets (note 12) | | (22,656) | | (38,163) |

| | | | |

Gain on distribution and equity income from equity-accounted investment (note 13) | | (1,500) | | (230) |

| Provision (recovery) for uncertain tax position | | 260 | | (2,221) |

| | | | |

| Other | | (388) | | 5,652 |

| Change in operating assets and liabilities | | (29,158) | | (6,019) |

| Expenditures for dry docking | | (2,691) | | (667) |

| Net operating cash flow | | 119,606 | | 57,624 |

| | | | |

| FINANCING ACTIVITIES | | | | |

| | | | |

| | | | |

| | | | |

| | | | |

| | | | |

| | | | |

| | | | |

| | | | |

| | | | |

| Issuance of common shares upon exercise of stock options | | 1,072 | | 872 |

| | | |

| Cash dividends paid | | (8,661) | | (8,596) |

| Other | | — | | (803) |

| Net financing cash flow | | (7,589) | | (8,527) |

| | | | |

| INVESTING ACTIVITIES | | | | |

Proceeds from sale of vessels (note 12) | | 72,332 | | 120,834 |

Distribution from equity-accounted joint venture (note 13) | | 1,500 | | — |

| Expenditures for vessels and equipment | | (510) | | (306) |

| | | | |

| Purchase of short-term investments | | (274,142) | | — |

| Proceeds from short-term investments | | 22,000 | | — |

| Vessel acquisitions | | (42,449) | | — |

| Purchase of marketable securities | | — | | (2,348) |

| | | | |

| Deposit for vessel purchase | | — | | (6,300) |

| Net investing cash flow | | (221,269) | | 111,880 |

| | | | |

| (Decrease) increase in cash, cash equivalents and restricted cash | | (109,252) | | 160,977 |

| Cash, cash equivalents and restricted cash, beginning of the period | | 831,261 | | 515,561 |

| Cash, cash equivalents and restricted cash, end of the period | | 722,009 | | 676,538 |

Supplemental cash flow information (note 17)

The accompanying notes are an integral part of the unaudited consolidated financial statements.

TEEKAY TANKERS LTD. AND SUBSIDIARIES

UNAUDITED CONSOLIDATED STATEMENTS OF CHANGES IN EQUITY (note 1)

(in thousands of U.S. Dollars, except share amounts)

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | Common Shares and Additional

Paid-in Capital | | | | |

| | | | | Thousands of Common Shares # | | Class A Common Shares $ | | Class B Common Shares $ | | Accumulated Surplus

$ | | Total $ |

| Balance as at December 31, 2025 | | | | 34,548 | | 1,226,108 | | 88,532 | | 728,976 | | 2,043,616 |

| Net income | | | | — | | — | | — | | 153,551 | | 153,551 |

| Dividends declared | | | | — | | — | | — | | (8,707) | | (8,707) |

Equity-based compensation (note 10) | | | | 96 | | 1,452 | | — | | — | | 1,452 |

| Balance as at March 31, 2026 | | | | 34,644 | | 1,227,560 | | 88,532 | | 873,820 | | 2,189,912 |

| | | | | | | | | | | | |

| | | | | | | | | | | | |

| | | | | | | | | | | | |

| | | | | | | | | | | | |

| | | | | | | | | | | | |

| | | | | | | | | | | | |

| | | | | | | | | | | | |

| | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | Common Shares and Additional

Paid-in Capital | | | | |

| | | | | Thousands of Common Shares # | | Class A Common Shares $ | | Class B Common Shares $ | | Accumulated

Surplus

$ | | Total $ |

| Balance as at December 31, 2024 | | | | 34,361 | | 1,220,963 | | 88,532 | | 447,055 | | 1,756,550 |

| Net income | | | | — | | — | | — | | 76,032 | | 76,032 |

| Dividends declared | | | | — | | — | | — | | (8,626) | | (8,626) |

Equity-based compensation (note 10) | | | | 72 | | 263 | | — | | — | | 263 |

| Balance as at March 31, 2025 | | | | 34,433 | | 1,221,226 | | 88,532 | | 514,461 | | 1,824,219 |

| | | | | | | | | | | | |

| | | | | | | | | | | | |

| | | | | | | | | | | | |

| | | | | | | | | | | | |

| | | | | | | | | | | | |

| | | | | | | | | | | | |

| | | | | | | | | | | | |

| | | | | | | | | | | | |

| | | | | | | | | | | | |

| | | | | | | | | | | | |

| | | | | | | | | | | | |

The accompanying notes are an integral part of the unaudited consolidated financial statements.

TEEKAY TANKERS LTD. AND SUBSIDIARIES

NOTES TO THE UNAUDITED CONSOLIDATED FINANCIAL STATEMENTS

(all tabular amounts stated in thousands of U.S. Dollars, other than share or per share data)

1.Basis of Presentation

The unaudited interim consolidated financial statements (or unaudited consolidated financial statements) have been prepared in accordance with United States generally accepted accounting principles (or GAAP). These unaudited consolidated financial statements include the accounts of Teekay Tankers Ltd. (or Teekay Tankers), which is incorporated under the laws of Bermuda, its wholly-owned subsidiaries and equity-accounted joint venture (collectively, the Company).

Certain information and footnote disclosures required by GAAP for complete annual financial statements have been omitted and, therefore, these unaudited consolidated financial statements should be read in conjunction with the Company’s audited consolidated financial statements for the year ended December 31, 2025, filed on Form 20-F with the U.S. Securities and Exchange Commission (or the SEC) on March 13, 2026. In the opinion of management, these unaudited consolidated financial statements reflect all normal recurring adjustments necessary to present fairly, in all material respects, the Company’s unaudited consolidated financial position, results of operations, cash flows and changes in equity for the interim periods presented. The results of operations for the interim periods presented are not necessarily indicative of those for a full fiscal year. Intercompany balances and transactions have been eliminated upon consolidation. The preparation of financial statements in conformity with GAAP requires management to make estimates and assumptions that affect the amounts reported in the unaudited consolidated financial statements and accompanying notes. Actual results could differ from those estimates.

2. Recent Accounting Pronouncements

In November 2024, the Financial Accounting Standards Board (or FASB) issued Accounting Standards Update (or ASU) 2024-03, Income Statement—Reporting Comprehensive Income—Expense Disaggregation Disclosures (Subtopic 220-40) Disaggregation of Income Statement Expenses, which requires disclosure, in the notes to financial statements, of specified information about certain costs and expenses. The amendments require that, for each interim and annual reporting period, an entity:

•Disclose the amounts of (a) purchases of inventory, (b) employee compensation, (c) depreciation, and (d) intangible asset amortization included in each relevant expense caption on the face of the income statement within continuing operations;

•Include certain amounts that are already required to be disclosed under current GAAP in the same disclosure as the other disaggregation requirements;

•Disclose a qualitative description of the amounts remaining in relevant expense captions that are not separately disaggregated quantitatively; and

•Disclose the total amount of selling expenses and, in annual reporting periods, an entity’s definition of selling expenses.

The amendments in the standard are effective for annual periods beginning after December 15, 2026 and for interim reporting periods beginning after December 15, 2027. Early adoption is permitted and should be applied prospectively, with retrospective application permitted. The Company expects to adopt this standard in its annual period beginning January 1, 2027. The Company is evaluating the impact of this standard on its consolidated financial statements.

3. Revenues

The Company’s primary source of revenue is from chartering its vessels (Suezmax tankers, Aframax tankers, Long Range 2 (or LR2) tankers and a Very Large Crude Carrier (or VLCC) tanker) to its customers and providing operational and maintenance marine services through its Australian operations. The Company utilizes two primary forms of contracts, consisting of voyage charters and time charters, and to a lesser extent bareboat charters from time to time.

The extent to which the Company employs its vessels on voyage charters versus time charters and bareboat charters is dependent upon the Company’s chartering strategy and the availability of time charters and bareboat charters. Spot market rates for voyage charters are volatile from period to period, whereas time charters provide a stable source of monthly revenue. During 2026, the Company has three vessels on short-term bareboat contracts that relate to the acquisitions of such vessels completed in January 2026. These bareboat charters are charters under which the customer pays a fixed daily rate for a fixed period of time for use of the vessel, and the customer also pays for all costs of operating the vessel, including voyage and vessel operating expenses. The Company also provides ship-to-ship (or STS) support services, which include managing the process of transferring cargo between seagoing ships positioned alongside each other, as well as management services to third-party owners of vessels. For descriptions of voyage charters and time charters, see "Item 18 – Financial Statements: Note 4" in the Company’s audited consolidated financial statements filed with its Annual Report on Form 20-F for the year ended December 31, 2025.

TEEKAY TANKERS LTD. AND SUBSIDIARIES

NOTES TO THE UNAUDITED CONSOLIDATED FINANCIAL STATEMENTS

(all tabular amounts stated in thousands of U.S. Dollars, other than share or per share data)

The following tables contain a breakdown of the Company's revenue by segment and contract type for the three months ended March 31, 2026 and March 31, 2025. The Company’s lease income consists of the revenue from its voyage charters, time charters and bareboat charters.

| | | | | | | | | | | | | | | | | | | | | | | |

| Three Months Ended March 31, 2026 | | Three Months Ended March 31, 2025 |

| Tankers | Marine

Services and

Other | Total | | Tankers | Marine

Services and

Other | Total |

| $ | $ | $ | | $ | $ | $ |

| Voyage charter revenues | | | | | | | |

| Suezmax | 114,172 | — | 114,172 | | 108,765 | — | 108,765 |

| Aframax / LR2 | 109,952 | — | 109,952 | | 83,878 | — | 83,878 |

VLCC (1) | 6,969 | — | 6,969 | | — | — | — |

| Total | 231,093 | — | 231,093 | | 192,643 | — | 192,643 |

| | | | | | | |

| Time-charter revenues | | | | | | | |

| Suezmax | 6,092 | — | 6,092 | | — | — | — |

| Aframax / LR2 | 5,439 | — | 5,439 | | 4,478 | — | 4,478 |

Bunker tanker (2) | — | 2,224 | 2,224 | | — | 1,836 | 1,836 |

| Total | 11,531 | 2,224 | 13,755 | | 4,478 | 1,836 | 6,314 |

| | | | | | | |

| Bareboat-charter revenues | | | | | | | |

| Aframax / LR2 | 2,877 | — | 2,877 | | — | — | — |

| Total | 2,877 | — | 2,877 | | — | — | — |

| | | | | | | |

Other revenues (3) | | | | | | | |

| Vessel operational and maintenance services | 486 | 29,493 | 29,979 | | 501 | 26,587 | 27,088 |

| Ship-to-ship support services | 2,411 | — | 2,411 | | 4,882 | — | 4,882 |

Management fees and other (4) | 5,473 | 506 | 5,979 | | — | 712 | 712 |

| Total | 8,370 | 29,999 | 38,369 | | 5,383 | 27,299 | 32,682 |

| | | | | | | |

| Total revenues | 253,871 | 32,223 | 286,094 | | 202,504 | 29,135 | 231,639 |

(1)Includes one VLCC tanker, which was acquired by the Company from its 50/50 joint venture in August 2025 and is trading in a pooling arrangement managed by a third-party.

(2)Includes variable lease payments of $nil and $1.0 million for the three months ended March 31, 2026 and 2025, respectively, related to the reimbursement for certain operating expenditures received from the Company's customer relating to such costs incurred by the Company to operate the vessel.

(3)Relates to non-lease revenues.

(4)Tankers segment includes in-process revenue related to the acquisitions of three 2016-built Aframax / LR2 tankers that were completed in January 2026. For more details, see "In-process Revenue" subsection of this Note 4 below.

Charters-out

As at March 31, 2026, six (December 31, 2025 - four) of the Company’s vessels operated under fixed-rate time-charter contracts, which are scheduled to expire between September 2026 and May 2029. As at March 31, 2026, the minimum scheduled future revenues to be received by the Company under time charters then in place were approximately $64.9 million (remainder of 2026), $10.8 million (2027), $8.0 million (2028), and $2.7 million (2029). The hire payments should not be construed to reflect a forecast of total charter hire revenue for any of the periods. Future hire payments do not include any hire payments generated from new contracts entered into after March 31, 2026 or from variable consideration, if any, under contracts. In addition, future hire payments presented above have been reduced by estimated off-hire time for required periodic maintenance and do not reflect the impact of any applicable revenue sharing

TEEKAY TANKERS LTD. AND SUBSIDIARIES

NOTES TO THE UNAUDITED CONSOLIDATED FINANCIAL STATEMENTS

(all tabular amounts stated in thousands of U.S. Dollars, other than share or per share data)

arrangements whereby time-charter revenues are shared with other revenue sharing arrangement participants. Actual amounts may vary given future events such as unplanned vessel maintenance.

Bareboat Charters-out

As at March 31, 2026, three (December 31, 2025 - none) of the Company’s vessels operated under fixed-rate bareboat-charter contracts, which are scheduled to expire between May 2026 and July 2026. As at March 31, 2026, the minimum scheduled future revenues to be received by the Company under bareboat charters then in place were approximately $2.5 million (remainder of 2026). The hire payments should not be construed to reflect a forecast of total charter hire revenue for such periods. Future hire payments do not include any hire payments generated from new contracts entered into after March 31, 2026 or from variable consideration, if any, under contracts.

Contract Liabilities

As at March 31, 2026, the Company had $3.6 million (December 31, 2025 - $5.8 million) of advanced payments recognized as contract liabilities that are expected to be recognized as time-charter revenues or voyage charter revenues in subsequent periods and which are included in other current liabilities in the Company's unaudited consolidated balance sheets.

In-process Revenue

In January 2026, the Company completed the acquisitions of three 2016-built Aframax / LR2 tankers. As part of the Company’s acquisitions of these tankers, the Company bareboat chartered out each tanker to the seller for a short-term period with rates that are less favorable than prevailing market rates; as a result, the Company paid a purchase price that is less than the estimated fair value of each vessel. As at March 31, 2026, the Company has recorded both an asset and a liability based on the difference between the fair value and the purchase price for each of the vessels. The Company is amortizing the assets, which are included as part of vessels and equipment in the Company's unaudited consolidated balance sheets, over each vessel’s estimated remaining useful life, and the Company is amortizing the liabilities, which are included as part of other current liabilities in the Company's unaudited consolidated balance sheets, over the estimated remaining term of the short-term bareboat contracts, which are expected to expire prior to the end of the third quarter of 2026.

For the three months ended March 31, 2026, amortization of the liabilities was $5.5 million (2025 - $nil), which is classified as in-process revenue and included as part of other revenues in the Company's unaudited consolidated statements of income. The liabilities are expected to be fully amortized by the end of the third quarter of 2026.

4. Segment Reporting

The Company allocates capital and assesses performance from the perspective of the Company's lines of business. The Company has two primary lines of business: 1) tankers and 2) marine services. The primary focus of the Company’s organizational structure, internal reporting and allocation of resources by the chief operating decision maker (or CODM) is based on the two lines of business, and its segments are presented accordingly on this basis. The CODM is the President and Chief Executive Officer of the Company. The CODM uses income from operations to assess the performance of each segment and to make decisions about allocating resources. The CODM does not assess the performance of each segment by geographic regions.

The Company's two operating segments include: 1) tankers, which consists of the operation of all of the Company's tankers (including the operations from those tankers employed on full service lightering contracts), and the Company's U.S. based ship-to-ship support service operations (including its lightering support services provided as part of full service lightering operations); and 2) marine services, which consists of operational and maintenance marine services provided to the Australian government, Australian energy companies and other third parties.

The accounting policies of the two segments are the same as those described in the summary of significant accounting policies. For more details, see "Item 18 – Financial Statements: Note 1" in the Company’s audited consolidated financial statements filed with its Annual Report on Form 20-F for the year ended December 31, 2025. The measure of segment assets is reported on the balance sheet as total consolidated assets.

TEEKAY TANKERS LTD. AND SUBSIDIARIES

NOTES TO THE UNAUDITED CONSOLIDATED FINANCIAL STATEMENTS

(all tabular amounts stated in thousands of U.S. Dollars, other than share or per share data)

The following tables include the Company’s revenues, expenses, other segment items, income from operations, and gain on distribution and equity income from equity-accounted investment by segment, and reconciles such amounts to the Company’s consolidated net income before income tax for the periods presented in these financial statements:

| | | | | | | | | | | | | | | | | | | | | | |

| Three Months Ended March 31, 2026 | | | |

| Tankers

$ | | Marine

Services and Other

$ | | | | Total

$ | | |

| Revenues | 253,871 | | 32,223 | | | | 286,094 | | | |

| Voyage expenses | (57,615) | | — | | | | (57,615) | | | |

| Vessel operating expenses | (31,013) | | (30,204) | | | | (61,217) | | | |

| Charter hire expenses | (9,058) | | (620) | | | | (9,678) | | | |

| Depreciation and amortization | (22,188) | | — | | | | (22,188) | | | |

| General and administrative expenses | (10,380) | | — | | | | (10,380) | | | |

| Gain on sale of vessels | 22,656 | | — | | | | 22,656 | | | |

| | | | | | | | | | |

| Income from operations | 146,273 | | 1,399 | | | | 147,672 | | | |

| | | | | | | | | | |

| Gain on distribution from equity-accounted investment | 1,500 | | — | | | | 1,500 | | | |

| Non-segment reconciling items: | | | | | | | | | | |

| Interest income | | | | | | | 8,046 | | | |

| Interest expense | | | | | | | (489) | | | |

| | | | | | | | | | |

| Other income | | | | | | | 821 | | | |

| Net income before income tax | | | | | | | 157,550 | | | |

| | | | | | | | | | | | | | | | | | | | | | |

| Three Months Ended March 31, 2025 | | | |

| Tankers

$ | | Marine

Services and Other

$ | | | | Total

$ | | |

| Revenues | 202,504 | | 29,135 | | | | 231,639 | | | |

| Voyage expenses | (86,867) | | — | | | | (86,867) | | | |

| Vessel operating expenses | (35,747) | | (25,421) | | | | (61,168) | | | |

| Charter hire expenses | (13,789) | | (620) | | | | (14,409) | | | |

| Depreciation and amortization | (23,240) | | — | | | | (23,240) | | | |

| General and administrative expenses | (9,712) | | — | | | | (9,712) | | | |

| Gain on sale and write-down of assets | 38,163 | | — | | | | 38,163 | | | |

| | | | | | | | | | |

| Income from operations | 71,312 | | 3,094 | | | | 74,406 | | | |

| | | | | | | | | | |

| Equity income | 230 | | — | | | | 230 | | | |

| Non-segment reconciling items: | | | | | | | | | | |

| Interest income | | | | | | | 5,857 | | | |

| Interest expense | | | | | | | (773) | | | |

| | | | | | | | | | |

| Other expense | | | | | | | (4,158) | | | |

| Net income before income tax | | | | | | | 75,562 | | | |

TEEKAY TANKERS LTD. AND SUBSIDIARIES

NOTES TO THE UNAUDITED CONSOLIDATED FINANCIAL STATEMENTS

(all tabular amounts stated in thousands of U.S. Dollars, other than share or per share data)

A reconciliation of total segment assets to total assets, presented in the accompanying unaudited consolidated balance sheets is as follows:

| | | | | | | | | | | | | | |

| March 31, 2026 (1) | | December 31, 2025 (1) | | | |

| $ | | $ | | |

| Tankers | 1,347,310 | | | 1,341,547 | | | | |

| Marine Services and Other | 43,416 | | | 44,754 | | | | |

| Due from affiliates | 3,642 | | | 2,804 | | | | |

| Cash and cash equivalents | 722,009 | | | 830,569 | | | | |

| Short-term investments | 274,142 | | | 22,000 | | | | |

| Total assets | 2,390,519 | | | 2,241,674 | | | | |

(1)There are no differences between the measurements of the segment assets and the Company’s consolidated total assets.

5. Intangible Assets and Other Non-Current Assets

Intangible Assets

Intangible assets are included in goodwill and intangible assets on the Company's unaudited consolidated balance sheets.

As part of the European Union Emissions Trading System (or EU ETS) requirements, as at March 31, 2026, the Company had a balance of European Union allowances (or EUAs) totaling $19.1 million (December 31, 2025 - $11.6 million), which was recorded as indefinite-lived intangible assets. As at March 31, 2026, $11.0 million (December 31, 2025 - $11.6 million) of these intangible assets are presented as other current assets in the unaudited consolidated balance sheets as these EUAs are related to the Company's 2025 emissions levels and will be surrendered within one year from the balance sheet date, and the remaining $8.1 million (December 31, 2025 - $nil) of EUAs are related to the Company's 2026 emissions levels and will be surrendered more than one year from the balance sheet date.

The carrying amount of intangible assets, excluding EUAs classified as other current assets, is as follows:

| | | | | | | | | | | |

| As at |

| March 31, 2026 | | December 31, 2025 |

| $ | | $ |

| EUAs, at cost | 8,055 | | — |

| | | |

| 8,055 | | — |

Other Non-Current Assets

In December 2025, the Company signed agreements to acquire three 2016-built Aframax / LR2 tankers for a total purchase price of $141.5 million. The full purchase price of $94.3 million related to two of the tankers and a deposit of $4.7 million related to the remaining tanker were placed in an escrow account, which was recorded in other non-current assets in the Company's unaudited consolidated balance sheet as at December 31, 2025. The acquisition of the three tankers was completed during the first quarter of 2026, and the total payment of $99.0 million, which was previously recorded in other non-current assets, is included as part of vessels and equipment in the Company's unaudited consolidated balance sheet as at March 31, 2026.

TEEKAY TANKERS LTD. AND SUBSIDIARIES

NOTES TO THE UNAUDITED CONSOLIDATED FINANCIAL STATEMENTS

(all tabular amounts stated in thousands of U.S. Dollars, other than share or per share data)

6. Accrued Liabilities and Other Long-Term Liabilities

The following tables present the components of accrued liabilities and other long-term liabilities on the Company's unaudited consolidated balance sheets.

| | | | | | | | | | | |

Accrued Liabilities | As at |

| March 31, 2026 | | December 31, 2025 |

| $ | | $ |

| Voyage and vessel | 38,584 | | 41,020 |

| Payroll and benefits | 23,546 | | 30,750 |

| Obligation related to EU ETS | 11,020 | | 11,020 |

| | | |

| Other accrued liabilities | 2,215 | | 1,934 |

| Accrued liabilities | 75,365 | | 84,724 |

Obligation Related to EU ETS

As at March 31, 2026, the Company has recorded an obligation of $15.6 million (December 31, 2025 - $11.0 million) related to its emissions levels, of which $11.0 million (December 31, 2025 - $11.0 million) is related to the Company's 2025 emissions levels and was included as part of accrued liabilities and the remaining $4.6 million (December 31, 2025 - $nil) is related to the Company's 2026 emissions levels and is included as part of other-long term liabilities in the unaudited consolidated balance sheets. During the three months ended March 31, 2026, the Company also recognized expenses related to EU ETS of $4.6 million (2025 - $2.7 million) as part of voyage expenses in the unaudited consolidated statements of income.

| | | | | | | | | | | |

Other Long-Term Liabilities | As at |

| March 31, 2026 | | December 31, 2025 |

| $ | | $ |

Freight tax provision (note 15) | 31,423 | | 31,073 |

| Office lease liability - long term | 10,267 | | 8,216 |

Obligation related to EU ETS | 4,555 | | — |

| | | |

| Defined contribution pension liability | 3,980 | | 4,818 |

| Other | 1,655 | | 1,607 |

| Other long-term liabilities | 51,880 | | 45,714 |

7. Long-Term Debt

As at March 31, 2026, the Company had one revolving credit facility (or the 2023 Revolver), which, as at such date, provided for aggregate borrowings of up to $171.7 million (December 31, 2025 - $171.7 million), of which $171.7 million (December 31, 2025 - $171.7 million) was undrawn. The 2023 Revolver matures in May 2029, and interest payments are based on the Secured Overnight Financing Rate (or SOFR) plus a margin of 2.00%, which, if the 2023 Revolver had been drawn, would have resulted in an interest rate of 5.7% as of March 31, 2026 (December 31, 2025 - 5.7%). The Company is required to pay a commitment fee which is calculated based on 0.7% of the undrawn portion of the 2023 Revolver. During the three months ended March 31, 2026, total commitment fees paid were $0.3 million (2025 - $0.4 million), which is recorded as part of interest expense in the Company's unaudited consolidated statements of income. As of March 31, 2026, the total amount available under the 2023 Revolver was scheduled to decrease by $57.2 million (remainder of 2026), $49.7 million (2027), $43.3 million (2028), $21.5 million (2029). As of March 31, 2026, the 2023 Revolver was collateralized by 17 of the Company's vessels, together with other related security (note 19).

The 2023 Revolver requires the Company to maintain a minimum hull coverage ratio of 125% of the total outstanding drawn balance for the facility. This requirement is assessed on a semi-annual basis with reference to vessel valuations compiled by two or more agreed upon third parties. Should this ratio drop below the required amount, the lenders may request that the Company either prepay a portion of the loan in the amount of the shortfall or provide additional collateral in the amount of the shortfall, at the Company's option. As at March 31, 2026, the hull coverage ratio for the 2023 Revolver was not applicable due to no balance being drawn. In addition, the Company is required to maintain a minimum liquidity (cash, cash equivalents and undrawn committed revolving credit lines with at least six months to maturity) of the greater of $35.0 million and at least 5% of the Company's total consolidated debt. As at March 31, 2026, the Company was in compliance with all covenants in respect of the 2023 Revolver.

TEEKAY TANKERS LTD. AND SUBSIDIARIES

NOTES TO THE UNAUDITED CONSOLIDATED FINANCIAL STATEMENTS

(all tabular amounts stated in thousands of U.S. Dollars, other than share or per share data)

8. Operating Leases

The Company charters-in vessels from other vessel owners on time charter-in contracts, whereby the vessel owner provides use and technical operation of the vessel for the Company, and also on bareboat-in contracts, whereby the registered owner provides the vessel to the Company during which the Company is entirely responsible for the operation of the vessel, including technical services and the crew required for operation. Time charter-in contracts and bareboat-in contracts are typically for a fixed period of time, although in certain cases the Company may have the option to extend the charter. The Company typically pays the owner a daily hire rate that is fixed over the duration of the charter. Under time charter-in contracts, the Company is generally not required to pay the daily hire rate during periods the vessel is not able to operate, whereas this does not generally apply to bareboat-in contracts.

As at March 31, 2026, minimum commitments to be incurred by the Company under time charter-in contracts and bareboat-in contracts were approximately $27.3 million (remainder of 2026), $15.3 million (2027), $8.5 million (2028), and $7.4 million (2029).

9. Fair Value Measurements

For a description of how the Company estimates fair value and for a description of the fair value hierarchy levels, see "Item 18 – Financial Statements: Note 12" to the Company’s audited consolidated financial statements filed with its Annual Report on Form 20-F for the year ended December 31, 2025.

The following table includes the estimated fair value, carrying value and categorization using the fair value hierarchy of those assets and liabilities that are measured at their estimated fair value on a recurring and non-recurring basis, as well as certain financial instruments that are not measured at fair value on a recurring basis.

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | March 31, 2026 | | December 31, 2025 |

| | | Fair Value Hierarchy Level | | Carrying

Amount

Asset / (Liability)

$ | | Fair

Value

Asset / (Liability)

$ | | Carrying Amount Asset / (Liability) $ | | Fair Value Asset / (Liability) $ |

| Recurring: | | | | | | | | | | |

Cash, cash equivalents and restricted cash (note 17) | | Level 1 | | 722,009 | | 722,009 | | 831,261 | | 831,261 |

Short-term investments | | Level 1 | | 274,142 | | 274,142 | | 22,000 | | 22,000 |

| | | | | | | | | |

Obligation related to EU ETS (note 6) (1) | | Level 1 | | (15,575) | | Note (1) | | (11,020) | | Note (1) |

| | | | | | | | | | |

| | | | | | | | | | |

| | | | | | | | | | |

| | | | | | | | | | |

| | | | | | | | | | |

| | | | | | | | | | |

| | | | | | | | | | |

| | | | | | | | | | |

| | | | | | | | | | |

| | | | | | | | | | |

| | | | | | | | | | |

| | | | | | | | | | |

| | | | | | | | | | |

| | | | | | | | | | |

| | | | | | | | | | |

| | | | | | | | | | |

| | | | | | | | | | |

(1)As at March 31, 2026, the Company has recorded an obligation related to EU ETS for $15.6 million, of which $11.0 million (December 31, 2025 - $11.0 million) was included as part of accrued liabilities and the remaining balance of $4.6 million (December 31, 2025 - $nil) was included as part of other-long term liabilities in the unaudited consolidated balance sheets. This amount can include an accrual representing the difference between the total emissions liability and the carrying value of the EUAs held as at the end of the reporting period. The fair value of the accrual is estimated using the fair market value of an EUA that is traded on a regulated energy exchange at the end of the reporting period. As at March 31, 2026, no such accrual was made as the total emissions liability was less than the carrying value of the EUAs held (December 31, 2025 - $nil).

The Company is exposed to credit loss in the event of non-performance by the financial institutions and the U.S. Government where its cash, cash equivalents and short-term investments are held. In order to minimize credit risk, the Company only places deposits and short-term investments with counterparties that are rated A- or better by Standard & Poor’s or A3 or better by Moody’s at the time of the transaction. In addition, to the extent practical, cash deposits and short-term investments are held by and entered into with different counterparties to reduce concentration risk.

10. Share Capital and Equity-Based Compensation

The authorized share capital of the Company at March 31, 2026 and December 31, 2025 was 100.0 million preference shares, with a par value of $0.01 per share, 485.0 million Class A common shares, with a par value of $0.01 per share, and 100.0 million Class B common shares, with a par value of $0.01 per share. A Class A common share entitles the holder to one vote per share while a Class B common share entitles the holder to five votes per share, subject to a 49% aggregate Class B common share voting power maximum. As of March 31, 2026, the Company had 30,017,861 Class A common shares (December 31, 2025 – 29,921,732), 4,625,997 Class B common shares (December 31, 2025 – 4,625,997) and no preference shares (December 31, 2025 – nil) issued and outstanding.

During the three months ended March 31, 2026 and 2025, the Company recognized $0.3 million and $0.2 million, respectively, of expenses related to restricted stock units in general and administrative expenses. During the three months ended March 31, 2025, a total of 2,905 restricted stock units with a market value of $0.1 million vested and 1,272 shares of Class A common stock, net of withholding taxes, were concurrently issued to the grantees.

TEEKAY TANKERS LTD. AND SUBSIDIARIES

NOTES TO THE UNAUDITED CONSOLIDATED FINANCIAL STATEMENTS

(all tabular amounts stated in thousands of U.S. Dollars, other than share or per share data)

11. Related Party Transactions

a.The Company and its subsidiaries have entered into management services agreements with Teekay and its affiliates (other than Teekay Tankers Ltd. and its subsidiaries) pursuant to which the Company provides services to Teekay and its affiliates in return for a management fee paid to the Company by Teekay. Amounts (paid) received by the Company for related party transactions for the periods indicated below were as follows:

| | | | | | | | | | | | | | | |

| | Three Months Ended March 31, | | |

| | 2026 | | 2025 | | | | |

| $ | | $ | | | | |

Transaction fee related to the sale of certain vessels (i) | (400) | | (700) | | | | |

Management fee revenues (ii) | 274 | | 489 | | | | |

| | | | | | | |

| | | | | | | |

| | | | | | | |

| | | | | | | |

| | | | | | | |

| | | | | | | |

| | | | | | | |

| | | | | | | |

| | | | | | | |

| | | | | | | |

| | | | | | | |

| | | | | | | |

| | | | | | | |

| | | | | | | |

(i)The Company pays a transaction fee to Teekay upon the sale of vessels that were previously owned by Tanker Investments Ltd., which the Company acquired in 2017. This fee is equal to 1.0% of the aggregate consideration payable to the Company pursuant to a sale contract. During the three months ended March 31, 2026, this fee was related to the sale of one vessel (2025 - two vessels).

(ii)The Company receives management fees from Teekay for time spent on Teekay matters by employees of the Company.

b.Teekay and its subsidiaries (other than Teekay Tankers Ltd. and its subsidiaries) may collect certain cash receipts and remit payments for certain expenses incurred by the Company. Such amounts, which are presented on the Company's unaudited consolidated balance sheets in "due from affiliates" or "due to affiliates", as applicable, are without interest or stated terms of repayment.

12. Vessel Sales and Write-down of Assets

During the three months ended March 31, 2026, the Company completed the sales of two Suezmax tankers for a total price of $73.0 million, with the Company recognizing an aggregate gain on sales of $22.7 million. One of the tankers as well as its related bunker and lube oil inventories were classified as held for sale as at December 31, 2025.

During the three months ended March 31, 2026, the Company agreed to sell one VLCC tanker for a price of $84.5 million, and the tanker as well as its related lube oil inventory were classified as held for sale as at March 31, 2026.

During the three months ended March 31, 2025, the Company completed the sales of two Aframax / LR2 tankers and two Suezmax tankers for a total price of for $120.5 million, with the Company recognizing an aggregate gain on sales of $39.0 million.

During the three months ended March 31, 2025, the Company recorded a write-down of $0.8 million on its operating lease right-of-use assets, which were written-down to their estimated fair values based on prevailing charter rates for comparable periods, due to a reduction in these charter rates.

13. Gain on Distribution and Equity Income from Equity-Accounted Investment

The Company has a 50% economic interest in a joint venture arrangement (or High-Q joint venture), which is jointly controlled by the Company and Wah Kwong Maritime Transport Holdings Limited. As at March 31, 2026, the High-Q joint venture no longer had any operational activities and is expected to be unwound during 2026.

During the three months ended March 31, 2026, the Company received a cash distribution from the High-Q joint venture in the amount of $1.5 million (2025 - $nil), which was recognized as part of gain on distribution and equity income from equity-accounted investment in the Company's unaudited consolidated statements of income. The Company does not have a contractual obligation to return any of the distribution received or provide additional financial support to the High-Q joint venture.

For the three months ended March 31, 2026, the Company recorded equity income of $nil (2025 - $0.2 million) which comprises its share of net income from the High-Q joint venture.

TEEKAY TANKERS LTD. AND SUBSIDIARIES

NOTES TO THE UNAUDITED CONSOLIDATED FINANCIAL STATEMENTS

(all tabular amounts stated in thousands of U.S. Dollars, other than share or per share data)

14. Other Income (Expense)

The components of other income (expense) are as follows:

| | | | | | | | | | | | | | | |

| Three Months Ended March 31, | | |

| 2026 | | 2025 | | | | |

| $ | | $ | | | | |

| Foreign exchange gain | 1,126 | | 431 | | | | |

Unrealized loss on marketable securities (1) | — | | (4,721) | | | | |

| | | | | | | |

| Other (expense) income | (305) | | 132 | | | | |

| Total | 821 | | (4,158) | | | | |

(1)The Company sold its entire investment in marketable securities during the fourth quarter of 2025.

15. Income Tax (Expense) Recovery

The components of the provision for income tax (expense) recovery are as follows:

| | | | | | | | | | | | | | | |

| Three Months Ended March 31, | | |

| 2026 | | 2025 | | | | |

| $ | | $ | | | | |

Current | (2,680) | | 424 | | | | |

Deferred | (1,319) | | 46 | | | | |

Income tax (expense) recovery | (3,999) | | 470 | | | | |

The following table reflects changes in uncertain tax positions relating to freight tax liabilities, which are recorded in other long-term liabilities in the Company's unaudited consolidated balance sheets:

| | | | | | | | | | | |

| Three Months Ended March 31, |

| 2026

$ | | 2025

$ |

| Balance as at January 1 | 31,073 | | 41,404 |

| Increases for positions related to the current year | 828 | | 170 |

| Increases for positions related to prior years | 927 | | 1,452 |

| | | |

| | | |

| Decreases related to expiry of limitation period | (1,494) | | (3,843) |

| Foreign exchange loss | 89 | | 1 |

| Balance as at March 31 | 31,423 | | 39,184 |

Included in the Company's current income tax (expense) recovery are provisions for uncertain tax positions relating to freight taxes. Positions relating to freight taxes can vary each period depending on the trading patterns of the Company's vessels.

The Company reviews its freight tax obligations on a regular basis and may update its assessment of its tax positions based on available information at that time. Such information may include legal advice as to the applicability of freight taxes in relevant jurisdictions. Freight tax regulations are subject to change and interpretation; therefore, the amounts recorded by the Company may change accordingly.

TEEKAY TANKERS LTD. AND SUBSIDIARIES

NOTES TO THE UNAUDITED CONSOLIDATED FINANCIAL STATEMENTS

(all tabular amounts stated in thousands of U.S. Dollars, other than share or per share data)

16. Earnings Per Share

The net income available for common shareholders and earnings per common share are presented in the table below:

| | | | | | | | | | | | | | | |

| | Three Months Ended March 31, | | |

| | 2026 | | 2025 | | | | |

| $ | | $ | | | | |

| Net income | 153,551 | | 76,032 | | | | |

| | | | | | | |

Weighted average number of common shares - basic (1) | 34,758,582 | | 34,482,849 | | | | |

| Dilutive effect of stock-based awards | 151,274 | | 183,868 | | | | |

| Weighted average number of common shares - diluted | 34,909,856 | | 34,666,717 | | | | |

| | | | | | | |

| Earnings per common share: | | | | | | | |

| – Basic | 4.42 | | 2.20 | | | | |

| – Diluted | 4.40 | | 2.19 | | | | |

(1) Includes unissued common shares related to non-forfeitable stock-based compensation.

Stock-based awards that have an anti-dilutive effect on the calculation of diluted earnings per common share are excluded from this calculation. In the periods where a loss attributable to shareholders has been incurred, all stock-based awards are anti-dilutive. For the three months ended March 31, 2026 and 2025, a total of 75,000 and 4,920 restricted stock units, respectively, had anti-dilutive effects on the calculation of diluted earnings per common share. For the three months ended March 31, 2026 and 2025, there were no options that had an anti-dilutive effect on the calculation of diluted earnings per common share.

17. Supplemental Cash Flow Information

Total cash and cash equivalents and restricted cash are as follows:

| | | | | | | | | | | | | | | | | | | | | | | |

| As at | | As at | | As at | | As at |

| March 31, 2026 | | December 31, 2025 | | March 31, 2025 | | December 31, 2024 |

| $ | | $ | | $ | | $ |

Cash and cash equivalents | 722,009 | | 830,569 | | 675,420 | | 511,888 |

Restricted cash – current (1) | — | | 692 | | 1,118 | | 3,673 |

| | | | | | | |

| | | | | | | |

| | | | | | | |

| 722,009 | | 831,261 | | 676,538 | | 515,561 |

(1) The Company maintained restricted cash deposits for the purpose of acquiring EUAs (note 5) and for the purpose of entering into forward freight agreements (or FFAs). As at December 31, 2025, the Company no longer maintained restricted cash deposits relating to FFAs.

The Company entered into new operating leases or extended existing operating leases for office premises and in-chartered vessels which resulted in the recognition of additional operating lease right-of-use assets and operating lease liabilities each in the amount of $3.5 million during the three months ended March 31, 2026 (2025 - $0.3 million). The increases to these balances had no cash impact.

18. Commitments and Contingencies

a)Liquidity

Management is required to assess if the Company will have sufficient liquidity to continue as a going concern for the one-year period following the issuance of these unaudited consolidated financial statements. Based on the Company's liquidity as at the date these unaudited consolidated financial statements were issued, and from the expected cash flows from the Company's operations over the following year, the Company estimates that it will have sufficient liquidity to meet its minimum liquidity requirements under its financial covenants and to continue as a going concern for at least a one-year period following the issuance of these unaudited consolidated financial statements.

b)Legal Proceedings and Claims

The Company may, from time to time, be involved in legal proceedings and claims that arise in the ordinary course of business. The Company believes that any adverse outcome of existing claims, individually or in the aggregate, would not have a material effect on its financial position, results of operations or cash flows, when taking into account its insurance coverage and indemnifications from charterers.

TEEKAY TANKERS LTD. AND SUBSIDIARIES

NOTES TO THE UNAUDITED CONSOLIDATED FINANCIAL STATEMENTS

(all tabular amounts stated in thousands of U.S. Dollars, other than share or per share data)

c)Other

The Company enters into indemnification agreements with certain officers and directors. In addition, the Company enters into other indemnification agreements in the ordinary course of business. The maximum potential amount of future payments required under these indemnification agreements is unlimited. However, the Company maintains what it believes is appropriate liability insurance that reduces its exposure and, subject to policy terms, would enable the Company to recover future amounts paid up to the maximum amount of the insurance coverage, less any deductible amounts pursuant to the terms of the respective policies, the amounts of which are not considered material.

19. Subsequent Events

a.In April 2026, eight tankers were released from collateral securing obligations under the 2023 Revolver, and the aggregate amount of borrowings available under the 2023 Revolver has been reduced by $60.5 million to $111.2 million (note 7).

b.In April 2026, the Company entered into an agreement to sell one 2009-built Suezmax tanker for $53.5 million. The tanker was delivered to its purchaser in May 2026.

c.In April 2026, the Company agreed to acquire two resale Suezmax tanker shipbuilding contracts for a total cost of $190.0 million. The vessels are being built at a South Korean shipyard and are expected to be delivered in 2027. The transaction will be completed upon the successful novation of the shipbuilding contracts and refund guarantees, which is expected to occur in May or June 2026.

d.In May 2026, the Company's Board of Directors declared a fixed quarterly cash dividend in the amount of $0.25 per outstanding common share for the quarter ended March 31, 2026. In addition, the Board of Directors declared a special cash dividend of $1.00 per common share. These dividends are payable on June 2, 2026 to all of Teekay Tankers Ltd.'s shareholders of record on May 26, 2026.

TEEKAY TANKERS LTD. AND SUBSIDIARIES

March 31, 2026

PART I - FINANCIAL INFORMATION

ITEM 2 – MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

The following Management’s Discussion and Analysis of Financial Condition and Results of Operations should be read in conjunction with the unaudited consolidated financial statements and accompanying notes contained in "Item 1 – Financial Statements" of this Report on Form 6-K and with our audited consolidated financial statements contained in "Item 18 – Financial Statements" and "Management’s Discussion and Analysis of Financial Condition and Results of Operations" in "Item 5 – Operating and Financial Review and Prospects" of our Annual Report on Form 20-F for the year ended December 31, 2025.

OVERVIEW

Our primary business is to own and operate crude oil and product tankers, and we employ a chartering strategy that seeks to capture upside opportunities in the tanker spot market while using fixed-rate charters and full service lightering (or FSL) contracts to reduce potential downside risks. Our mix of vessels trading in the spot market or subject to fixed-term charters will change from time to time. In addition to our core business, we also provide operational and maintenance marine services and ship-to-ship (or STS) support services, along with our tanker commercial management and technical management operations. As at March 31, 2026, our fleet consisted of 39 vessels, including five chartered-in vessels. The following table summarizes our fleet as at March 31, 2026:

| | | | | | | | | | | |

| Owned

Vessels | Chartered-in Vessels | Total |

|

| Fixed-rate: | | | |

| Suezmax Tankers | 3 | — | 3 |

Aframax Tankers / LR2 Product Tankers (1) | 5 | — | 5 |

| Total Fixed-Rate Fleet | 8 | — | 8 |

| | | |

| Spot-rate: | | | |

Suezmax Tankers (2)(3) | 12 | 1 | 13 |

Aframax Tankers / LR2 Product Tankers (4)(5) | 13 | 2 | 15 |

Very Large Crude Carrier (or VLCC) Tanker (6) | 1 | — | 1 |

Total Spot Fleet (7) | 26 | 3 | 29 |

STS Support and Bunker Tanker Vessels (8) | — | 2 | 2 |

| Total Teekay Tankers Fleet | 34 | 5 | 39 |

(1)Includes three Aframax tankers subject to bareboat charter-out contracts that are scheduled to expire during the second and third quarters of 2026. In May 2026, one of the tankers was redelivered to us following the expiry of its bareboat charter-out contract.

(2)Includes one owned Suezmax tanker for which an agreement was put in place in April 2026 to sell the vessel. The tanker was delivered to its purchaser in May 2026.

(3)One Suezmax tanker is time chartered-in for a period of 54 months expiring in June 2027 with an option to extend for one year.

(4)One Aframax / LR2 tanker is time chartered-in for a period expiring in February 2027 with no option to extend. One 2023-built Aframax / LR2 tanker is time chartered-in for a period expiring in January 2030 with three one-year extension option periods and a purchase option at the end of the second extension option period.

(5)Includes one owned Aframax / LR2 tanker for which a time charter-out contract was entered into us in May 2026 and which is scheduled to commence in late May 2026.

(6)Includes one owned VLCC tanker for which an agreement was put in place in February 2026 to sell the vessel. The tanker is trading on spot voyage charters in a pooling arrangement managed by a third party and is expected to be delivered to its purchaser in June 2026. The tanker is classified as held for sale as at March 31, 2026.

(7)As at March 31, 2026, a total of 28 of our owned and chartered-in vessels, as well as two vessels not in our fleet and owned by third parties, were subject to revenue sharing agreements (or RSAs).

(8)Includes one bunker tanker which we chartered-in for a period expiring in May 2029. This bunker tanker is also chartered-out by us for the same corresponding period.

ITEMS YOU SHOULD CONSIDER WHEN EVALUATING OUR RESULTS

There are a number of factors that should be considered when evaluating our historical financial performance and assessing our future prospects, and we use a variety of financial and operational terms and concepts when analyzing our results of operations. These items can be found in "Item 5 – Operating and Financial Review and Prospects" in our Annual Report on Form 20-F for the year ended December 31, 2025.

SIGNIFICANT DEVELOPMENTS IN 2026

Global Tariffs and Trade

During 2025 and 2026, the U.S. administration and other governments have announced or taken actions to implement new or increased tariffs on foreign imports and port fees. These actions have resulted and may result in additional retaliatory tariffs being levied on various goods and commodities, which may trigger trade wars. Additionally, in early 2026, the U.S. Supreme Court struck certain of the tariffs implemented by the U.S. administration, who thereafter reimplemented certain tariffs in response, which may cause additional uncertainty and increase geopolitical tensions. These activities have disrupted global markets, resulting in an increase in general global economic uncertainty, including an increased risk of economic recessions. In 2025, the U.S. and China announced new port fees that would apply to port calls of certain Chinese and U.S.-related tankers, respectively, which could be disruptive to our industry. These port fees subsequently have been suspended until October 2026. As a result of the rapidly changing and unpredictable geopolitical climate, the shipping industry is experiencing uncertainty as to future vessel demand, trade routes, rates and operating costs.

Geopolitical Conflicts

Geopolitical conflicts and related sanctions, export controls, and price caps have significantly affected us and our industry, including by disrupting energy supply chains and trading patterns, and causing instability and volatility in the global economy. These conflicts include, among others, Russia’s ongoing invasion of Ukraine, Houthi rebel attacks on vessels in the Red Sea area, U.S. action in Venezuela and the subsequent shift in trade towards the compliant fleet of tankers, and the recent U.S.-Israel war with Iran which has led to the effective closure of the Strait of Hormuz and a U.S. blockade of ships calling at Iranian ports. The latter conflict is particularly impactful for global oil and tanker markets as it has led to a virtual stoppage of tanker transits through the Strait of Hormuz and a significant decline in crude oil and refined product exports from the Middle East Gulf region. Resultant trading inefficiencies in the first two months of the conflict have supported spot tanker rates. However, a prolonged closure of the Strait of Hormuz could lead to a sustained shortage of global oil supply relative to demand, leading to high crude oil prices, oil demand destruction, and lower crude oil tanker demand. The escalation and expansion of hostilities in the Middle East and the possibility of continuing instability or further escalation in Ukraine, Venezuela or elsewhere could continue to affect the price of crude oil and the oil industry, the tanker industry and demand for our services.

Vessel Sales

During the first quarter of 2026, we sold two Suezmax tankers for a total price of $73.0 million, which resulted in an aggregate gain on sales of $22.7 million during the three months ended March 31, 2026. Both tankers were delivered to their purchasers during the first quarter of 2026.

In February 2026 and April 2026, we entered into agreements to sell one 2013-built VLCC tanker and one 2009-built Suezmax tanker, respectively, for a combined sales price of $138.0 million. The Suezmax tanker was delivered to its purchaser during the second quarter of 2026, and the VLCC tanker is expected to be delivered to its purchaser in June 2026.

Vessel Acquisitions

In January 2026, we completed the acquisitions of three 2016-bulit Aframax / LR2 tankers for a total purchase price of $141.5 million. Upon the completion of these purchases, we bareboat chartered out each tanker to the seller for periods between four months and eight months, after which we will assume commercial and technical management of the vessels. In May 2026, one of the tankers was redelivered to us following the expiry of its bareboat charter-out contract.

In April 2026, we agreed to acquire two resale Suezmax tanker shipbuilding contracts for a total cost of $190.0 million. The vessels are being built at a South Korean shipyard and are expected to be delivered in 2027. The transaction will be completed upon the successful novation of the shipbuilding contracts and refund guarantees, which is expected to occur in May or June 2026.

Time Chartered-in Vessel

During the first quarter of 2026, one chartered-in lightering support vessel was redelivered to its owner following the expiry of its time chartered-in contract.

Time Chartered-out Vessels

During the first and second quarters of 2026, we entered into time charter-out contracts for two Suezmax tankers and one Aframax / LR2 tanker for terms between 10 months and 12 months at an average rate of $64,000 per day, two of which charters commenced in the first quarter of 2026, while the remaining charter is scheduled to commence in the second quarter of 2026.

Special Cash Dividend Declaration

In May 2026, our Board of Directors declared a special cash dividend of $1.00 per common share. This dividend is payable on June 2, 2026 to all of Teekay Tankers Ltd.'s shareholders of record on May 26, 2026.

Revolving Credit Facility

In April 2026, eight tankers were released from collateral securing obligations under the 2023 Revolver, and the aggregate amount of borrowings available under the 2023 Revolver has been reduced by $60.5 million to $111.2 million.

RESULTS OF OPERATIONS

In accordance with GAAP, we report gross revenues in our unaudited consolidated statements of income and include voyage expenses among our operating expenses. However, ship-owners base economic decisions regarding the deployment of their vessels upon anticipated time-charter equivalent (or TCE) rates, which represent net revenues (or income or loss from operations before vessel operating expenses, charter hire expenses, depreciation and amortization, general and administrative expenses, and gain or loss on sale and write-down of assets), which includes voyage expenses, divided by revenue days; in addition, industry analysts typically measure bulk shipping freight and hire rates in terms of TCE rates. This is because under time charter-out and bareboat charter-out contracts, the customer usually pays the voyage expenses, while under voyage charters the ship-owner usually pays the voyage expenses, which typically are added to the hire rate at an approximate cost. Accordingly, the discussion of revenue below focuses on net revenues and TCE rates (both of which are non-GAAP financial measures) where applicable.

The results of operations that follow have been divided into (a) tankers, which consists of the operation of all of our Suezmax, Aframax / LR2 and VLCC tankers (including the operations from those of our tankers employed on full service lightering contracts), and our U.S. based ship-to-ship support service operations (including our lightering support services provided as part of full service lightering operations); and (b) marine services and other, which consists of operational and maintenance marine services provided to the Australian government, Australian energy companies and other third parties, as well as management services provided to Teekay and third parties.

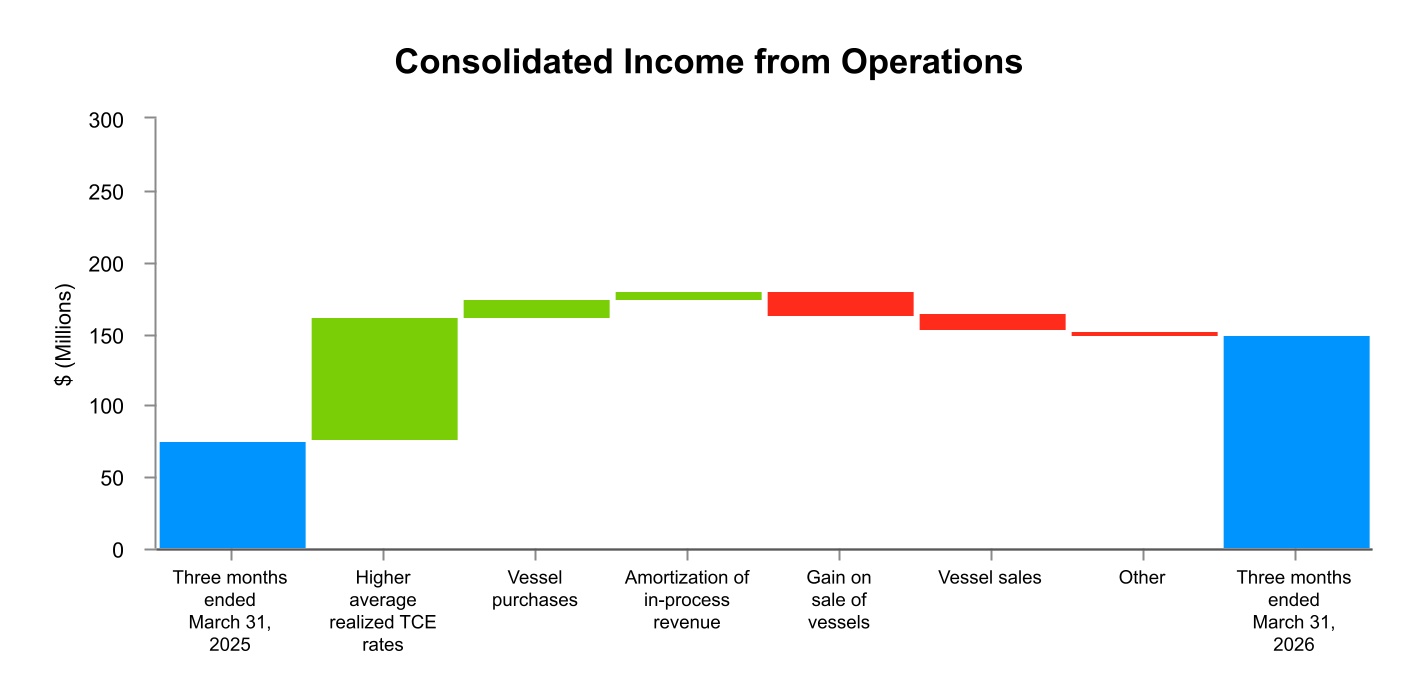

Summary

Our consolidated income from operations was $147.7 million for the three months ended March 31, 2026, compared to $74.4 million in the same period last year. The primary reasons for this increase in income are as follows:

•an increase of $85.8 million as a result of higher overall average realized spot TCE rates earned by our Suezmax tankers and Aframax / LR2 tankers in the first quarter of 2026 compared to the same period in the prior year;

•an increase of $13.2 million due to the acquisitions of four Aframax / LR2 tankers, one Suezmax tanker, and one VLCC tanker between the start of the second quarter of 2025 and the end of the first quarter of 2026; and

•an increase of $5.5 million due to the amortization of in-process revenue related to the acquisition of the three Aframax / LR2 tankers in the first quarter of 2026;

partially offset by:

•a decrease of $16.3 million due to the gain on sales of two Suezmax tankers in the first quarter of 2026 compared to the gain on sales of two Aframax / LR2 tankers and two Suezmax tankers in the first quarter of 2025; and

•a decrease of $11.5 million due to the sales of 10 Suezmax tankers and three Aframax / LR2 tankers between the start of the first quarter of 2025 and the end of first quarter of 2026.

Details of the changes to our results of operations for the three months ended March 31, 2026, compared to the three months ended March 31, 2025, are provided below.

Three Months Ended March 31, 2026 versus Three Months Ended March 31, 2025

Tankers - Operating Results

We own and operate crude oil and product tankers that (i) are subject to long-term, fixed-rate time-charter contracts (which have an original term of one year or more), (ii) operate in the spot tanker market, (iii) are subject to time charters that are priced on a spot market basis or are short-term, fixed-rate contracts (which have original terms of less than one year), including those employed on FSL contracts, or (iv) are subject to short-term bareboat charter contracts. In addition, we provide STS support services, along with our tanker commercial management and technical management services.

The following table presents the Tankers' operating results for the three months ended March 31, 2026 and 2025, and includes a comparison of net revenues(1), a non-GAAP financial measure, for those periods to income from operations, the most directly comparable GAAP financial measure:

| | | | | | | | | | | | | | | | | | | | | | | |

| Three Months Ended March 31, | | |

| (in thousands of U.S. Dollars, except percentage changes) | 2026 | | 2025 | | % Change | | | | | | |

| Revenues | 253,871 | | | 202,504 | | | 25.4 | % | | | | | | |

| Voyage expenses | (57,615) | | | (86,867) | | | (33.7) | % | | | | | | |

Net revenues(1) | 196,256 | | | 115,637 | | | 69.7 | % | | | | | | |

| | | | | | | | | | | |

| Vessel operating expenses | (31,013) | | | (35,747) | | | (13.2) | % | | | | | | |

| Charter hire expenses | (9,058) | | | (13,789) | | | (34.3) | % | | | | | | |

| Depreciation and amortization | (22,188) | | | (23,240) | | | (4.5) | % | | | | | | |

| General and administrative expenses | (10,380) | | | (9,712) | | | 6.9 | % | | | | | | |

| Gain on sale and write down of assets | 22,656 | | | 38,163 | | | (40.6) | % | | | | | | |

| | | | | | | | | | | |

| Income from operations | 146,273 | | | 71,312 | | | 105.1 | % | | | | | | |

| | | | | | | | | | | |

| | | | | | | | | | | |

| | | | | | | | | | | |

| Gain on distribution and equity income from equity-accounted investment | 1,500 | | | 230 | | | 552.2 | % | | | | | | |

| | | | | | | | | | | |

| | | | | | | | | | | |

| | | | | | | | | | | |

| | | | | | | | | | | |

(1)This is a non-GAAP financial measure. Please refer to "Item 2 – Management's Discussion and Analysis of Financial Condition and Results of Operations - Non-GAAP Financial Measure" for a definition and reconciliation of this non-GAAP financial measure to the most directly comparable financial measure calculated and presented in accordance with GAAP.

Net Revenues. Net revenues were $196.3 million for the three months ended March 31, 2026, compared to $115.6 million for the same period in the prior year.

The net increase for the three months ended March 31, 2026 compared to the same period in the prior year was primarily the result of:

•an increase of $85.8 million for the three months ended March 31, 2026 due to higher overall average realized spot TCE rates earned by our Suezmax tankers and Aframax / LR2 tankers compared to the same period in the prior year;

•an increase of $5.5 million for the three months ended March 31, 2026 due to the amortization of in-process revenue related to the acquisition of the three Aframax / LR2 tankers in the first quarter of 2026; and

•an increase of $2.7 million for the three months ended March 31, 2026 primarily due to certain vessels commencing on time charter-out contracts at various times and earning a higher average rate compared to the rate from the comparative period;

partially offset by:

•a net decrease of $10.0 million for the three months ended March 31, 2026 due to the sales of 10 Suezmax tankers and three Aframax / LR2 tankers between the start of the first quarter of 2025 and the end of first quarter of 2026, as well as the redeliveries of two chartered-in tankers to their owners between the start of the first quarter of 2025 and the end of the third quarter of 2025, partially offset by the acquisitions of four Aframax / LR2 tankers, one Suezmax tanker, and one VLCC tanker between the start of the second quarter of 2025 and the end of the first quarter of 2026;

•a decrease of $2.5 million for the three months ended March 31, 2026 due to lower revenues related to certain STS support service activities compared to the same period in the prior year; and

•a decrease of $0.8 million for the three months ended March 31, 2026 due to more dry-docking related off-hire days and higher off-hire bunker expenses related to the timing of dry dockings compared to the same period in the prior year.

Vessel Operating Expenses. Vessel operating expenses were $31.0 million for the three months ended March 31, 2026, compared to $35.7 million for the same period in the prior year.

The net decrease for the three months ended March 31, 2026 compared to the same period in the prior year was primarily the result of:

•a net decrease of $4.7 million resulting from the sales of ten Suezmax tankers and three Aframax / LR2 tankers between the start of the first quarter of 2025 and the end of the first quarter of 2026, partially offset by the acquisition of one Aframax / LR2 tanker, one Suezmax tanker and one VLCC tanker between the start of the second quarter of 2025 and the end of the third quarter of 2025; and

•a decrease of $0.5 million resulting from lower expenditures related to certain STS support service activities during the first quarter of 2026;

partially offset by:

•an increase of $0.6 million resulting from higher repair and maintenance related expenditures during the first quarter of 2026.

Charter Hire Expenses. Charter hire expenses were $9.1 million for the three months ended March 31, 2026, compared to $13.8 million for the same period in the prior year. The decrease was primarily due to the redeliveries of two chartered-in tankers to their owners between the start of the first quarter of 2025 and the end of the third quarter of 2025.

Depreciation and Amortization. Depreciation and amortization was $22.2 million for the three months ended March 31, 2026, compared to $23.2 million for the same period in the prior year. The net decrease was primarily due to the sales of ten Suezmax tankers and three Aframax / LR2 tankers between the start of the first quarter of 2025 and the end of the first quarter of 2026, partially offset by the acquisitions of four Aframax / LR2 tankers, one Suezmax tanker and one VLCC tanker between the start of the second quarter of 2025 and the end of the first quarter of 2026, as well as the dry docks of certain vessels that are subject to a shorter amortization period compared to the previous dry docks.

General and Administrative Expenses. General and administrative expenses were $10.4 million for the three months ended March 31, 2026, compared to $9.7 million for the same period in the prior year. The increase was primarily due to higher costs related to compensation and benefits, partially offset by lower general corporate expenditures.

Gain on Sale and Write-Down of Assets. The gain on sale of assets of $22.7 million for the three months ended March 31, 2026 was related to the sales of two Suezmax tankers.

The gain on sale and write-down of assets of $38.2 million for the three months ended March 31, 2025 was related to:

•the sales of two Aframax / LR2 tankers and two Suezmax tankers, which resulted in an aggregate gain on sales of $39.0 million during the first quarter of 2025;

partially offset by:

•the impairment recorded for two of our operating lease right-of-use assets resulting from a decline in the prevailing short-term time-charter rates, which resulted in a write-down of $0.8 million during the first quarter of 2025.

Gain on Distribution and Equity Income from Equity-accounted Investment. Gain on distribution from equity-accounted investment was $1.5 million for the three months ended March 31, 2026, compared to equity income of $0.2 million for the same period in the prior year. The increase was primarily due to a $1.5 million gain recognized on the receipt of a cash distribution from the equity-accounted joint venture in the first quarter of 2026.

Tanker Market

The effective closure of the Strait of Hormuz due to conflict in the Middle East has led to unprecedented disruption to global oil and tanker markets. As a result, mid-size crude tanker spot rates rose to the second highest level for a first quarter on record during the first quarter of 2026, with rates increasing further to all-time highs at the start of the second quarter of 2026.

Prior to the conflict in the Middle East, mid-size crude tanker spot rates were already at very firm levels due to a combination of rising seaborne oil trade volumes, a tightening of sanctions against Russia, Iran, and Venezuela (which pushed more trade volumes away from the “dark fleet” towards the compliant fleet of tankers), and the impact of fleet consolidation in the VLCC sector. This was further amplified at the start of 2026 with the removal of Venezuelan President Nicolás Maduro by the United States and the subsequent freeing up of Venezuelan crude oil exports to move on compliant tonnage to destinations such as the U.S. Gulf, Europe, and India, to the benefit of mid-size crude tanker demand.

However, it is the recent events in the Middle East which have propelled spot tanker rates to new highs. Following the commencement on February 28, 2026 of attacks by the United States and Israel against Iran, Iran has responded by attacking a range of military and civilian assets across the Middle East region, including vessels transiting the Strait of Hormuz. The U.S. has also imposed a blockade on the strait. This has led to a significant drop in vessel traffic through the Strait of Hormuz due to safety concerns, which in turn has led to a sharp decline in Middle East oil production and exports. While Saudi Arabia and the UAE have been able to divert some of their export volumes to ports outside of the Middle East Gulf, total crude oil exports from the region have fallen by approximately 10 million barrels per day (mb/d) compared to pre-war levels.

Ordinarily, an oil supply loss of this magnitude would likely be negative for tanker demand due to the steep drop in cargo supply. However, a series of trading inefficiencies have coincided to boost spot tanker rates in the weeks following the start of the conflict.