|

|

Exhibit (c)(9)

Project Pony

Prepared for Board of Directors

September 7, 2016

|

|

Situational Overview

Management has completed a comprehensive strategic

review of its MLP interests in TC PipeLines, LP and Columbia

Pipeline Partners LP (“CPPL”)

Recommendation: Buyback CPPL

Transaction Structure

Reverse triangular merger

All cash offer expected

Offer expected to be made by the end of September

| 2 |

|

TransCanada Date: September 7, 2016 |

|

|

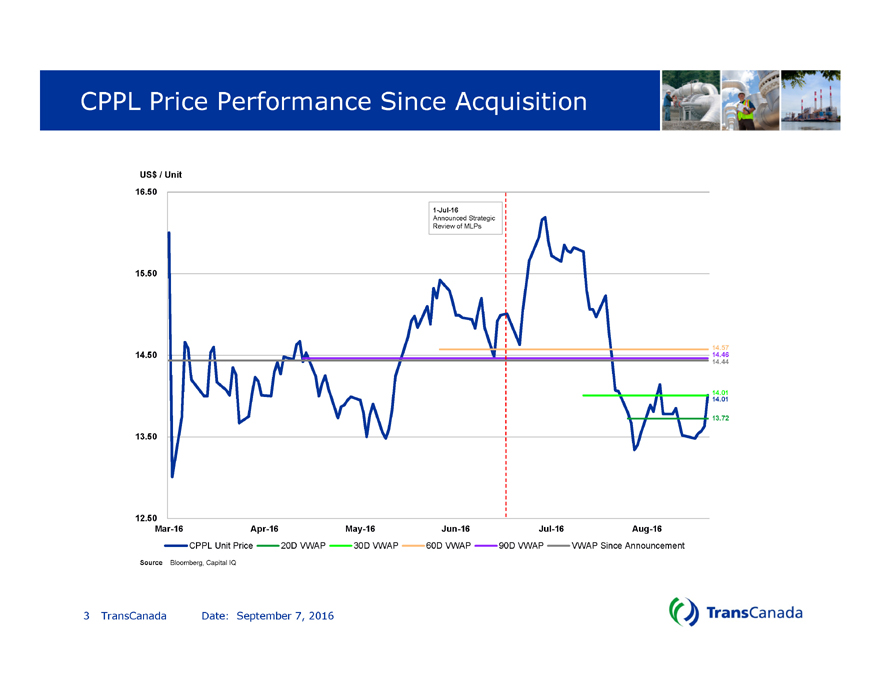

CPPL Price Performance Since Acquisition

US$ / Unit16.5015.50

16.50

Mar-16 Apr-16 May-16 Jun-16 Jul-16 Aug-16

CPPL Unit Price 20D VWAP 30D VWAP 60D VWAP 90D VWAP VWAP Since Announcement

US$ / Unit

13.72

14.57

14.01

14.46

1-Jul-16

Announced Strategic

Review of MLP14.5013.50Source Bloomberg, Capital IQ

| 3 |

|

TransCanada Date: September 7, 2016 |

|

|

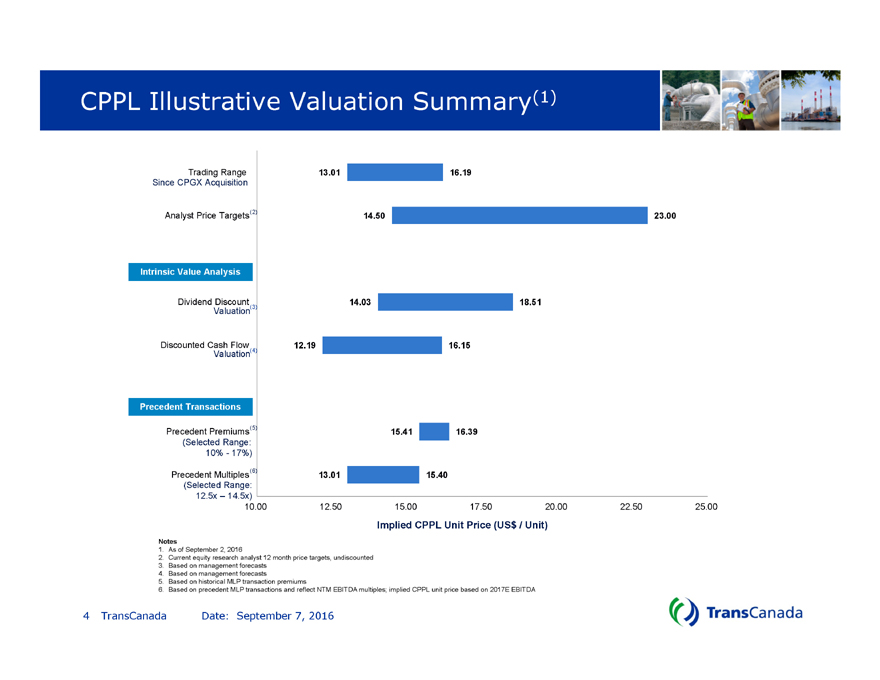

CPPL Illustrative Valuation Summary(1)

13.01

14.50

14.03

12.19

15.41

13.01

16.19

23.00

18.51

16.15

16.39

15.40

10.00 12.50 15.00 17.50 20.00 22.50 25.00

Trading Range

Analyst Price Targets

Dividend Discount

Discounted Cash Flow

Precedent Premiums

Precedent Multiples

Implied CPPL Unit Price (US$ / Unit)

Since CPGX Acquisition

(Selected Range:

10%—17%)

(Selected Range:

12.5x – 14.5x)

| (6) |

|

Intrinsic Value Analysis

Precedent Transactions

| (5) |

|

| (4) |

|

| (3) |

|

| (2) |

|

Valuation

Valuation

Notes

1. As of September 2, 2016

2. Current equity research analyst 12 month price targets, undiscounted

3. Based on management forecasts

4. Based on management forecasts

5. Based on historical MLP transaction premiums

6. Based on precedent MLP transactions and reflect NTM EBITDA multiples; implied CPPL unit price based on 2017E EBITDA

| 4 |

|

TransCanada Date: September 7, 2016 |

|

|

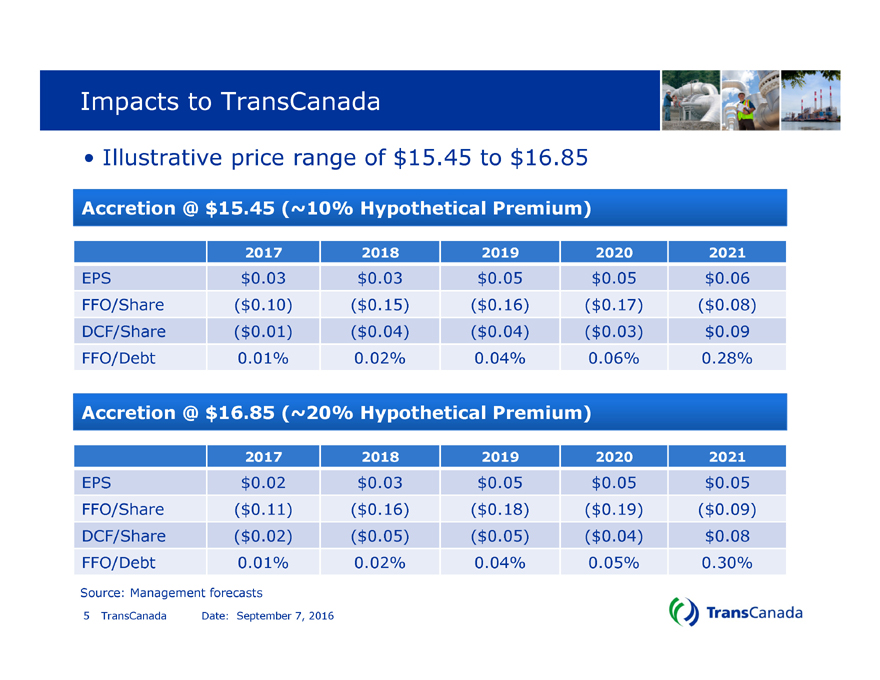

Impacts to TransCanada

Illustrative price range of $15.45 to $16.85

2017 2018 2019 2020 2021

EPS $0.03 $0.03 $0.05 $0.05 $0.06

FFO/Share ($0.10) ($0.15) ($0.16) ($0.17) ($0.08)

DCF/Share ($0.01) ($0.04) ($0.04) ($0.03) $0.09

FFO/Debt 0.01% 0.02% 0.04% 0.06% 0.28%

Accretion @ $15.45 (~10% Hypothetical Premium)

2017 2018 2019 2020 2021

EPS $0.02 $0.03 $0.05 $0.05 $0.05

FFO/Share ($0.11) ($0.16) ($0.18) ($0.19) ($0.09)

DCF/Share ($0.02) ($0.05) ($0.05) ($0.04) $0.08

FFO/Debt 0.01% 0.02% 0.04% 0.05% 0.30%

Source: Management forecasts

| 5 |

|

TransCanada Date: September 7, 2016 |

|

|

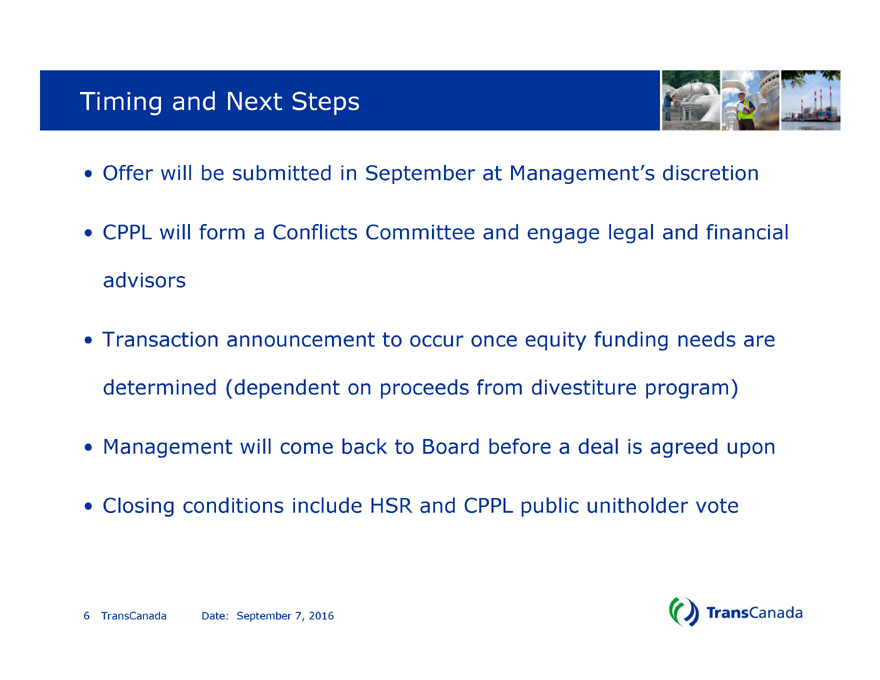

Timing and Next Steps

Offer will be submitted in September at Management’s discretion

CPPL will form a Conflicts Committee and engage legal and financial

advisors

Transaction announcement to occur once equity funding needs are

determined (dependent on proceeds from divestiture program)

Management will come back to Board before a deal is agreed upon

Closing conditions include HSR and CPPL public unitholder vote

| 6 |

|

TransCanada Date: September 7, 2016 |

|

|

Appendix

| 7 |

|

TransCanada Date: September 7, 2016 |

|

|

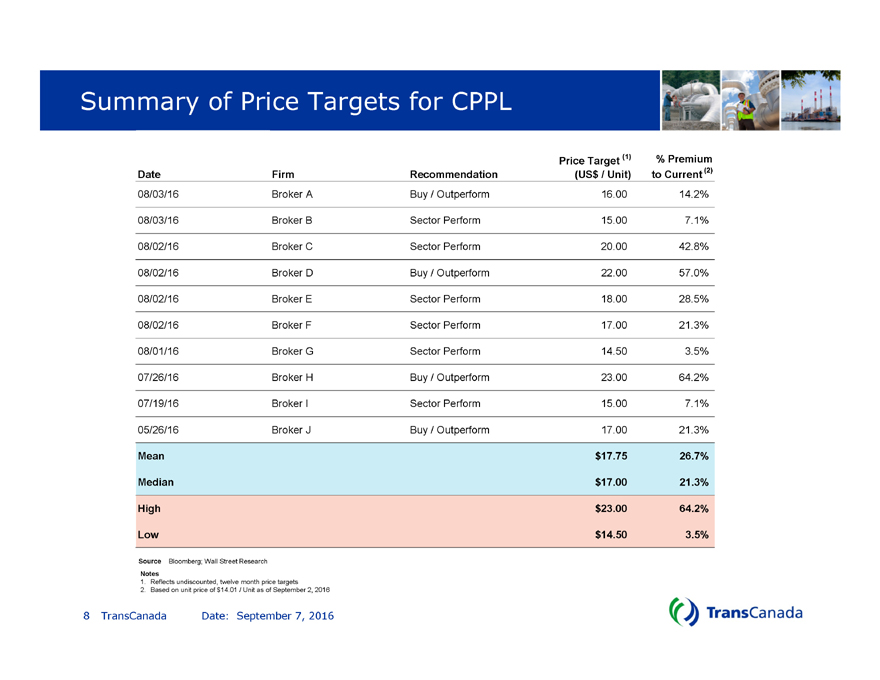

Summary of Price Targets for CPPL

Date Firm Recommendation

Price Target (1)

(US$ / Unit)

% Premium

to Current (2)

08/03/16 Broker A Buy / Outperform 16.00 14.2%

08/03/16 Broker B Sector Perform 15.00 7.1%

08/02/16 Broker C Sector Perform 20.00 42.8%

08/02/16 Broker D Buy / Outperform 22.00 57.0%

08/02/16 Broker E Sector Perform 18.00 28.5%

08/02/16 Broker F Sector Perform 17.00 21.3%

08/01/16 Broker G Sector Perform 14.50 3.5%

07/26/16 Broker H Buy / Outperform 23.00 64.2%

07/19/16 Broker I Sector Perform 15.00 7.1%

05/26/16 Broker J Buy / Outperform 17.00 21.3%

Mean $17.75 26.7%

Median $17.00 21.3%

High $23.00 64.2%

Low $14.50 3.5%

Source Bloomberg; Wall Street Research

Notes

1. Reflects undiscounted, twelve month price targets

2. Based on unit price of $14.01 / Unit as of September 2, 2016

| 8 |

|

TransCanada Date: September 7, 2016 |

|

|

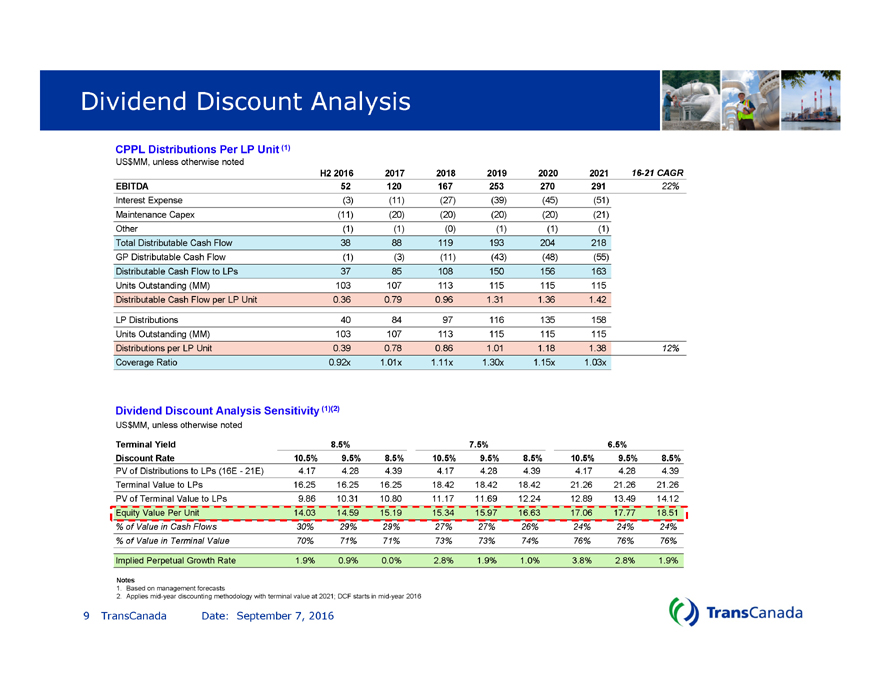

Dividend Discount Analysis

CPPL Distributions Per LP Unit (1)

US$MM, unless otherwise noted

H2 2016 2017 2018 2019 2020 2021 16-21 CAGR

EBITDA 52 120 167 253 270 291 22%

Interest Expense (3) (11) (27) (39) (45) (51)

Maintenance Capex (11) (20) (20) (20) (20) (21)

Other (1) (1) (0) (1) (1) (1)

Total Distributable Cash Flow 38 88 119 193 204 218

GP Distributable Cash Flow (1) (3) (11) (43) (48) (55)

Distributable Cash Flow to LPs 37 85 108 150 156 163

Units Outstanding (MM) 103 107 113 115 115 115

Distributable Cash Flow per LP Unit 0.36 0.79 0.96 1.31 1.36 1.42

LP Distributions 40 84 97 116 135 158

Units Outstanding (MM) 103 107 113 115 115 115

Distributions per LP Unit 0.39 0.78 0.86 1.01 1.18 1.38 12%

Coverage Ratio 0.92x 1.01x 1.11x 1.30x 1.15x 1.03x

Dividend Discount Analysis Sensitivity (1)(2)

US$MM, unless otherwise noted

Terminal Yield 8.5% 7.5% 6.5%

Discount Rate 10.5% 9.5% 8.5% 10.5% 9.5% 8.5% 10.5% 9.5% 8.5%

PV of Distributions to LPs (16E—21E) 4.17 4.28 4.39 4.17 4.28 4.39 4.17 4.28 4.39

Terminal Value to LPs 16.25 16.25 16.25 18.42 18.42 18.42 21.26 21.26 21.26

PV of Terminal Value to LPs 9.86 10.31 10.80 11.17 11.69 12.24 12.89 13.49 14.12

Equity Value Per Unit 14.03 14.59 15.19 15.34 15.97 16.63 17.06 17.77 18.51

% of Value in Cash Flows 30% 29% 29% 27% 27% 26% 24% 24% 24%

% of Value in Terminal Value 70% 71% 71% 73% 73% 74% 76% 76% 76%

Implied Perpetual Growth Rate 1.9% 0.9% 0.0% 2.8% 1.9% 1.0% 3.8% 2.8% 1.9%

Notes

1. Based on management forecasts

2. Applies mid-year discounting methodology with terminal value at 2021; DCF starts in mid-year 2016

9 TransCanada Date: September 7, 2016

|

|

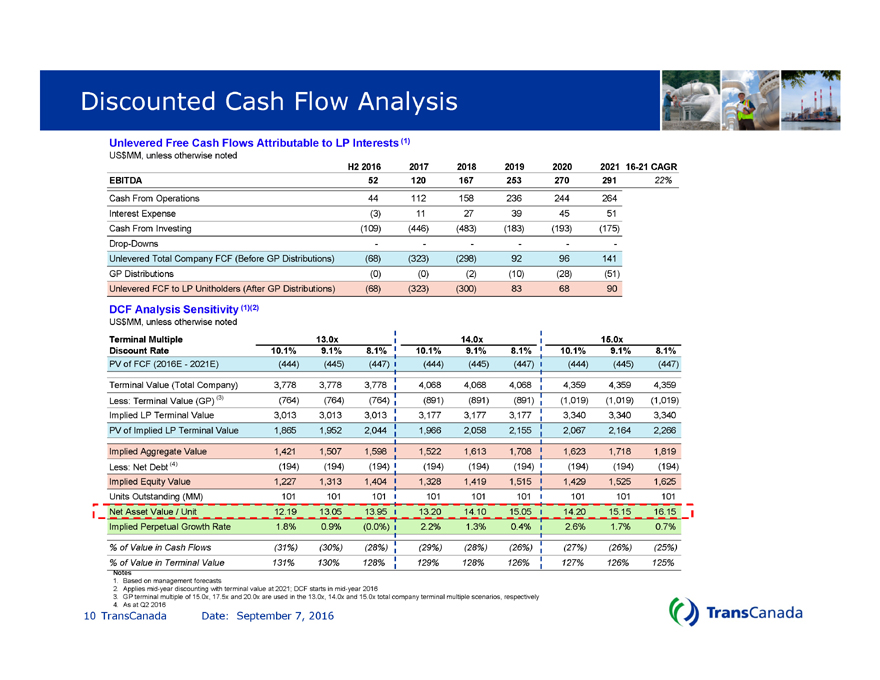

Discounted Cash Flow

Unlevered Free Cash Flows Attributable to LP Interests (1)Analysis

US$MM, unless otherwise noted

Terminal Multiple 13.0x 14.0x 15.0x

Discount Rate 10.1% 9.1% 8.1% 10.1% 9.1% 8.1% 10.1% 9.1% 8.1%

PV of FCF (2016E—2021E) (444) (445) (447) (444) (445) (447) (444) (445) (447)

Terminal Value (Total Company) 3,778 3,778 3,778 4,068 4,068 4,068 4,359 4,359 4,359

Less: Terminal Value (GP) (3) (764) (764) (764) (891) (891) (891) (1,019) (1,019) (1,019)

Implied LP Terminal Value 3,013 3,013 3,013 3,177 3,177 3,177 3,340 3,340 3,340

PV of Implied LP Terminal Value 1,865 1,952 2,044 1,966 2,058 2,155 2,067 2,164 2,266

Implied Aggregate Value 1,421 1,507 1,598 1,522 1,613 1,708 1,623 1,718 1,819

Less: Net Debt (4) (194) (194) (194) (194) (194) (194) (194) (194) (194)

Implied Equity Value 1,227 1,313 1,404 1,328 1,419 1,515 1,429 1,525 1,625

Units Outstanding (MM) 101 101 101 101 101 101 101 101 101

Net Asset Value / Unit 12.19 13.05 13.95 13.20 14.10 15.05 14.20 15.15 16.15

Implied Perpetual Growth Rate 1.8% 0.9% (0.0%) 2.2% 1.3% 0.4% 2.6% 1.7% 0.7%

% of Value in Cash Flows (31%) (30%) (28%) (29%) (28%) (26%) (27%) (26%) (25%)

% of Value in Terminal Value 131% 130% 128% 129% 128% 126% 127% 126% 125%

DCF Analysis Sensitivity (1)(2)

Notes

1. Based on management forecasts

2. Applies mid-year discounting with terminal value at 2021; DCF starts in mid-year 2016

3. GP terminal multiple of 15.0x, 17.5x and 20.0x are used in the 13.0x, 14.0x and 15.0x total company terminal multiple scenarios, respectively

4. As at Q2 2016

US$MM, unless otherwise noted

H2 2016 2017 2018 2019 2020 2021 16-21 CAGR

EBITDA 52 120 167 253 270 291 22%

Cash From Operations 44 112 158 236 244 264

Interest Expense (3) 11 27 39 45 51

Cash From Investing (109) (446) (483) (183) (193) (175)

Drop-Downs — — —

Unlevered Total Company FCF (Before GP Distributions) (68) (323) (298) 92 96 141

GP Distributions (0) (0) (2) (10) (28) (51)

Unlevered FCF to LP Unitholders (After GP Distributions) (68) (323) (300) 83 68 90

10 TransCanada Date: September 7, 2016

|

|

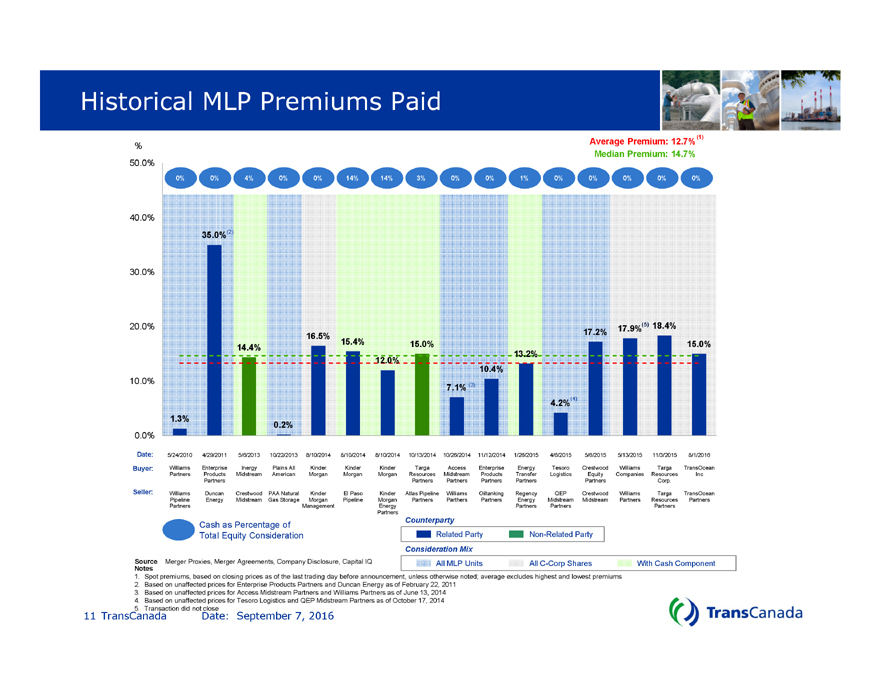

Historical MLP Premiums Paid

Notes

1. Spot premiums, based on closing prices as of the last trading day before announcement, unless otherwise noted; average excludes highest and lowest premiums

2. Based on unaffected prices for Enterprise Products Partners and Duncan Energy as of February 22, 2011

3. Based on unaffected prices for Access Midstream Partners and Williams Partners as of June 13, 2014

4. Based on unaffected prices for Tesoro Logistics and QEP Midstream Partners as of October 17, 2014

5. Transaction did not close

Average Premium: 12.7%

Date:

Buyer:

Seller:

Median Premium: 14.7%

All MLP Units All C-Corp Shares With Cash Component

Consideration Mix

Cash as Percentage of

Total Equity Consideration

| (2) |

|

| (3) |

|

0% 0% 4% 0% 0% 14% 14% 3% 0% 0% 1% 0% 0% 0% 0% 0%

Related Party Non-Related Party

Counterparty

Source Merger Proxies, Merger Agreements, Company Disclosure, Capital IQ

1.3% 35.0% 14.4% 0.2% 16.5% 15.4% 12.0% 15.0% 7.1% 10.4% 13.2% 4.2% 17.2% 17.9% 18.4% 15.0% 0.0% 10.0%

20.0% 30.0% 40.0% 50.0% 5/24/2010 Williams Partners Williams Pipeline Partners 4/29/2011 Enterprise Products Partners Duncan Energy

5/6/2013 Inergy Midstream Crestwood Midstream 10/22/2013 Plains All American PAA Natural Gas Storage 8/10/2014 Kinder Morgan Kinder

Morgan Management 8/10/2014 Kinder Morgan El Paso Pipeline 8/10/2014 Kinder Morgan Kinder Morgan Energy Partners 10/13/2014

Targa Resources Partners Atlas Pipeline Partners 10/26/2014 Access Midstream Partners Williams Parthers 11/12/2014 Enterprise Products

Partners Oiltanking Partners 1/26/2015 Energy Transfer Partners Regency Energy Partners 4/6/2015 Tesoro Logistics QEP Midstream

Partners 5/6/2015 Crestwood Equity Partners Crestwood Midstream 5/13/2015 Williams Companies Williams Partners 11/3/2015 Targa

Resources Corp. Targa Resources Partners 8/1/2016 TransOcean Inc TransOcean 11 TransCanada Date: September 7, 2016

|

|

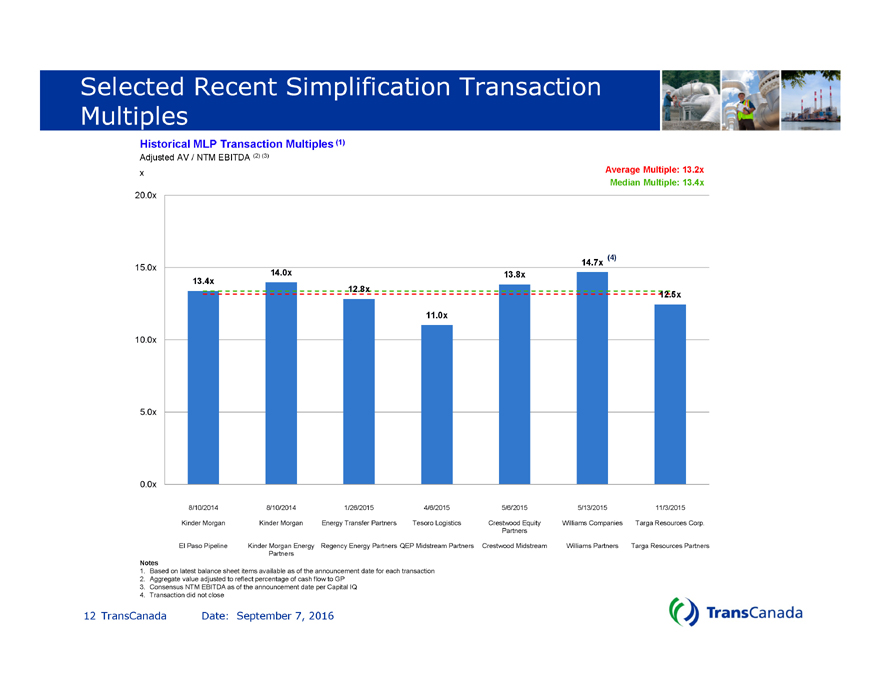

Selected Recent Simplification Transaction

Multiples

13.4x

14.0x

12.8x

11.0x

13.8x

14.7x

12.5x

0.0x

5.0x

10.0x

15.0x

20.0x

8/10/2014

Kinder Morgan

El Paso Pipeline

8/10/2014

Kinder Morgan

Kinder Morgan Energy

Partners

1/26/2015

Energy Transfer Partners

Regency Energy Partners

4/6/2015

Tesoro Logistics

QEP Midstream Partners

5/6/2015

Crestwood Equity

Partners

Crestwood Midstream

5/13/2015

Williams Companies

Williams Partners

11/3/2015

Targa Resources Corp.

Targa Resources Partners

Historical MLP Transaction Multiples (1)

Adjusted AV / NTM EBITDA (2) (3)

x

Notes

1. Based on latest balance sheet items available as of the announcement date for each transaction

2. Aggregate value adjusted to reflect percentage of cash flow to GP

3. Consensus NTM EBITDA as of the announcement date per Capital IQ

4. Transaction did not close

Average Multiple: 13.2x

Median Multiple: 13.4x

12 TransCanada Date: September 7, 2016