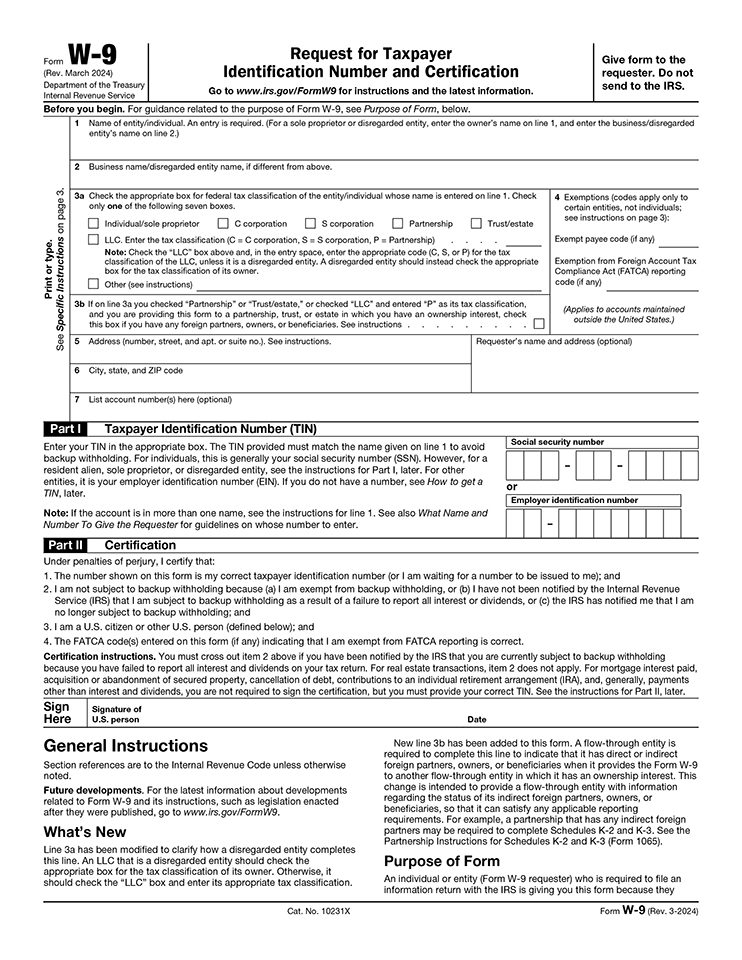

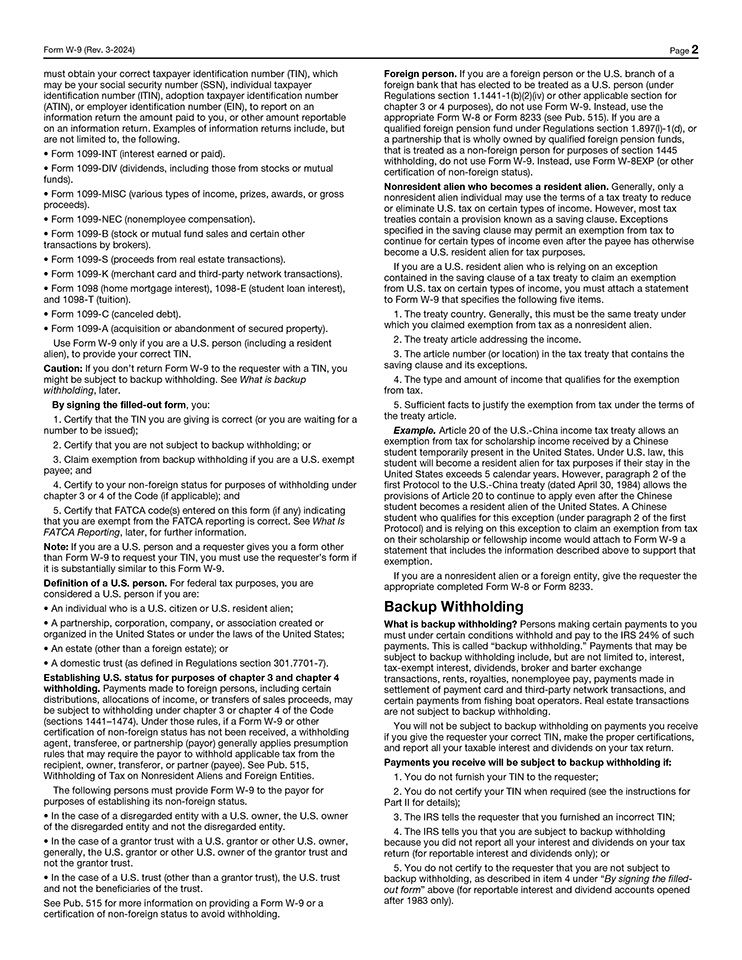

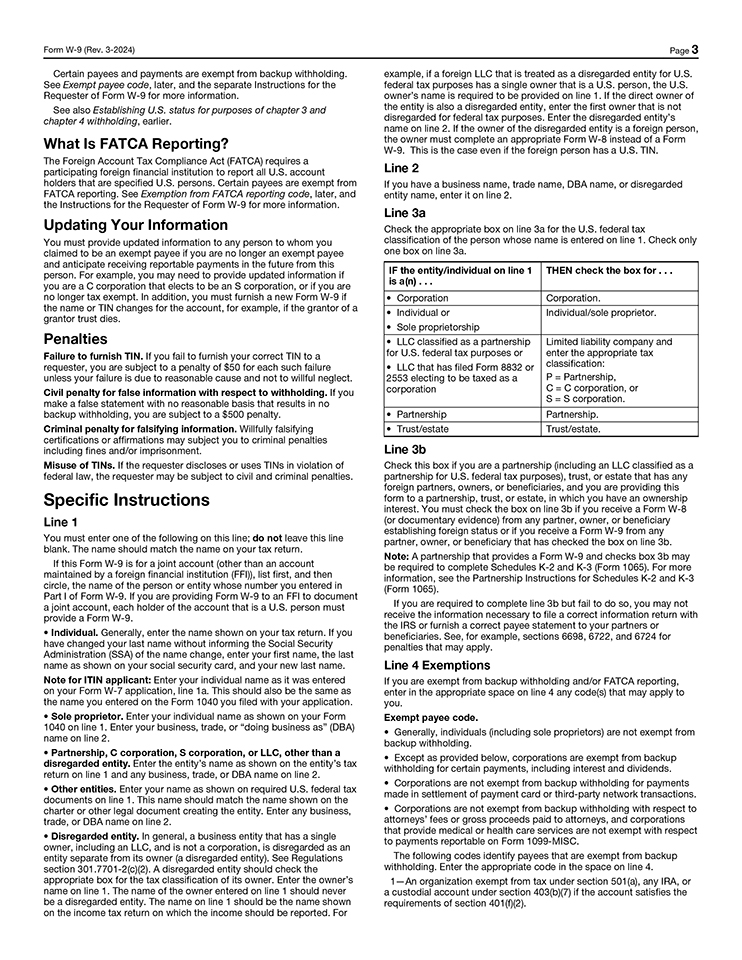

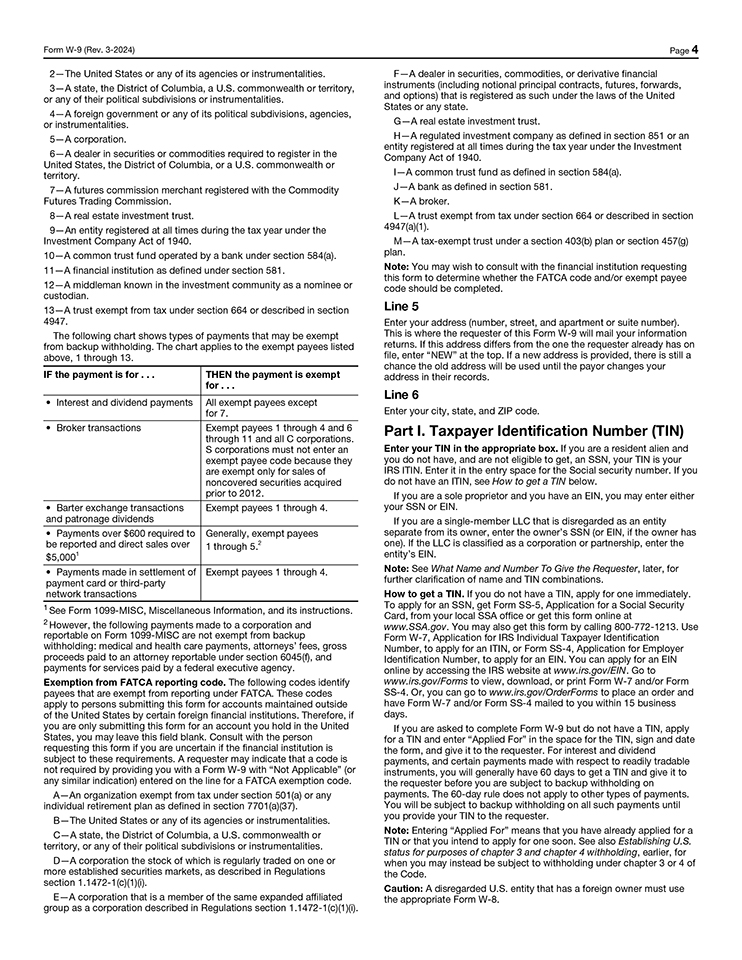

.3

THE INSTRUCTIONS ACCOMPANYING THIS LETTER OF TRANSMITTAL SHOULD BE READ CAREFULLY BEFORE THIS LETTER OF TRANSMITTAL IS COMPLETED. YOU ARE STRONGLY URGED TO READ THE ACCOMPANYING MANAGEMENT INFORMATION CIRCULAR BEFORE COMPLETING THIS LETTER OF TRANSMITTAL. THE DEPOSITARY OR YOUR BROKER OR OTHER FINANCIAL ADVISOR WILL ASSIST YOU IN COMPLETING THIS LETTER OF TRANSMITTAL. ALL DEPOSITS UNDER THIS LETTER OF TRANSMITTAL ARE IRREVOCABLE AND MAY NOT BE WITHDRAWN.

THIS LETTER OF TRANSMITTAL IS FOR USE ONLY IN CONJUNCTION WITH THE PLAN OF ARRANGEMENT INVOLVING SANDSTORM GOLD LTD., ITS SHAREHOLDERS, INTERNATIONAL ROYALTY CORPORATION AND ROYAL GOLD, INC.

THIS LETTER OF TRANSMITTAL MUST BE VALIDLY COMPLETED, DULY EXECUTED AND RETURNED TO THE DEPOSITARY, COMPUTERSHARE INVESTOR SERVICES INC. IT IS IMPORTANT THAT YOU VALIDLY COMPLETE, DULY EXECUTE AND RETURN THIS LETTER OF TRANSMITTAL ON A TIMELY BASIS IN ACCORDANCE WITH THE INSTRUCTIONS CONTAINED HEREIN.

LETTER OF TRANSMITTAL

FOR COMMON SHARES

OF

SANDSTORM GOLD LTD.

This Letter of Transmittal, properly completed and duly executed, together with all other required documents, must accompany certificate(s) or Direct Registration System advice(s) (“DRS Advice(s)”) for common shares (the “Company Shares”) of Sandstorm Gold Ltd. (“Sandstorm”) deposited in connection with the proposed arrangement (the “Arrangement”) involving, among others, Sandstorm and Royal Gold, Inc. (“Royal Gold”) pursuant to an arrangement agreement dated July 6, 2025 (the “Arrangement Agreement”), a copy of which is available under Sandstorm’s profile on SEDAR+ at www.sedarplus.ca and on EDGAR at http://www.sec.gov. The Arrangement is being submitted for approval at the special meeting of shareholders of Sandstorm (the “Shareholders”) that is scheduled to be held on October 9, 2025, or any adjournment or postponement thereof (the “Meeting”), as more particularly described in the management information circular of Sandstorm dated September 8, 2025 (the “Circular”).

Pursuant to the Arrangement, Royal Gold, through International Royalty Corporation, a wholly-owned subsidiary of Royal Gold (“AcquireCo”), will acquire all of the issued and outstanding Company Shares, and each holder of Company Shares will be entitled to receive, in exchange for each one (1) Company Share held by such holder, 0.0625 of a share of Royal Gold common stock (each whole share, a “Purchaser Share”) (the “Consideration”), subject to adjustment pursuant to section 2.17 of the Arrangement Agreement. Royal Gold will not issue any fractional Purchaser Shares in connection with the Arrangement. Where the aggregate number of Purchaser Shares issuable to a Shareholder as Consideration would result in a fraction of a Purchaser Share being issuable, such Shareholder shall receive the nearest whole number of Purchaser Shares. For greater certainty, where such fractional interest represents 0.5 or more of a Purchaser Share, the number of Purchaser Shares to be issued will be rounded up to the nearest whole number, and where such fractional interest represents less than 0.5 of a Purchaser Share, the number of Purchaser Shares to be issued will be rounded down to the nearest whole number. Shareholders should refer to the full text of the plan of arrangement (the “Plan of Arrangement”) which is appended to the Circular as Appendix B.

Capitalized terms used but not defined in this Letter of Transmittal have the meanings set out in the Circular. Registered Shareholders are encouraged to carefully review the Circular in its entirety and should consult their tax advisors prior to submitting a Letter of Transmittal.

1