.2

TABLE OF CONTENTS

|

Company Information & Forward-Looking Statements |

|

|

Earnings Press Release |

|

|

Financial & Operating Highlights |

|

|

Balance Sheets |

|

|

Statements of Operations, Funds from Operations (“FFO”) & Core FFO (“CFFO”) |

|

|

Trailing Five Quarters |

|

|

Three and Nine Months Ended September 30, 2025 and 2024 |

|

|

Adjusted EBITDA Reconciliations and Coverage Ratio |

|

|

Trailing Five Quarters |

|

|

Three and Nine Months Ended September 30, 2025 and 2024 |

|

|

Same-Store Portfolio Net Operating Income (“NOI”) and NOI Bridge |

|

|

Trailing Five Quarters |

|

|

Three and Nine Months Ended September 30, 2025 and 2024 |

|

|

Same-Store Portfolio NOI by Market |

|

|

Three Months Ended September 30, 2025 and 2024 |

|

| Nine Months Ended September 30, 2025 and 2024 | 17 |

|

Property Portfolio NOI Exposure by Market |

|

|

Value Add Summary |

|

|

Investment & Development Activity |

|

|

Debt Summary |

|

|

Debt & Credit Metrics |

|

|

Definitions |

COMPANY INFORMATION

Independence Realty Trust, Inc. (NYSE: IRT), an S&P 400 MidCap Company, is a real estate investment trust (“REIT”) that owns and operates multifamily communities, across non-gateway U.S. markets. IRT’s investment strategy is focused on gaining scale near major employment centers within key amenity rich submarkets that offer good school districts and high-quality retail. IRT’s main objective is to provide attractive risk-adjusted returns to shareholders through diligent portfolio management, strong operational performance, and a consistent return on capital through distributions and capital appreciation. More information may be found on the Company’s website, www.irtliving.com.

|

Corporate Headquarters |

1835 Market Street, Suite 2601 |

|

|

Philadelphia, PA 19103 |

||

|

267.270.4800 |

||

|

Trading Symbol on NYSE |

IRT |

|

| Credit Ratings |

Fitch Ratings |

BBB l Stable |

| Standard & Poors' Ratings Services | BBB l Stable | |

|

Investor Relations |

Stephanie Krewson-Kelly |

|

|

267.270.4815 |

||

|

SKrewson@IRTLiving.com |

This release contains certain forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended. Such forward-looking statements include, but are not limited to, our earnings guidance, and the assumptions underlying such guidance, our planned use of remaining proceeds from our sales of common stock on a forward basis, our expectations with respect to the three properties which are classified as held for sale, the assumptions underlying the determination of the fair value of our impairment charge for our property held for sale as of September 30, 2025, and our expectations with respect to our new joint venture and our expectations with respect to future acquisitions and dispositions. All statements in this release that address financial and operating performance, events or developments that we expect or anticipate will occur or be achieved in the future are forward-looking statements.

Our forward-looking statements are not guarantees of future performance and involve estimates, projections, forecasts and assumptions, including as to matters that are not within our control, and are subject to risks and uncertainties including, without limitation, risks and uncertainties related to changes in market demand for rental apartment homes and pricing pressures, including from competitors, that could lead to declines in occupancy and rent levels, uncertainty and volatility in capital and credit markets, including changes that reduce availability, and increase costs, of capital, unexpected changes in our intention or ability to repay certain debt prior to maturity, increased costs on account of inflation, increased competition in the labor market, our planned use of the remaining proceeds from our sales of common stock on a forward basis, inability to sell certain assets, including those assets designated as held for sale, within the time frames or at the pricing levels expected, failure to achieve expected benefits from the redeployment of proceeds from asset sales, inability or failure to achieve anticipated benefits from future acquisitions and dispositions, delays in completing, and cost overruns incurred in connection with, our value add initiatives and failure to achieve rent increases and occupancy levels on account of the value add initiatives, unexpected impairments or impairments in excess of our estimates, increased regulations generally and specifically on the rental housing market, including legislation that may regulate rents and fees or delay or limit our ability to evict non-paying residents, risks endemic to real estate and the real estate industry generally, the impact of potential outbreaks of infectious diseases and measures intended to prevent the spread or address the effects thereof, economic conditions, including inflation and recessionary conditions and their related impacts on the real estate industry, U.S. and global trade policies and tensions, including changes in, or the imposition of, tariffs and/or trade barriers and the economic impacts, volatility and uncertainty resulting therefrom, the impacts from the U.S. government shutdown, the effects of natural and other disasters, unknown or unexpected liabilities, including the cost of legal proceedings, costs and disruptions as the result of a cybersecurity incident or other technology disruption, including but not limited to a third party's unauthorized access to our data or the data of our residents, unexpected capital needs, inability to obtain appropriate insurance coverages at reasonable rates, or at all, or losses from catastrophes in excess of our insurance coverages, and share price fluctuations. Please refer to the documents filed by us with the SEC, including specifically the “Risk Factors” sections of our Annual Report on Form 10-K for the year ended December 31, 2024 and our Quarterly Report on Form 10-Q for the quarter ended March 31, 2025, and our other filings with the SEC, which identify additional factors that could cause actual results to differ from those contained in forward-looking statements.

These forward-looking statements are based upon the beliefs and expectations of our management at the time of this release and our actual results may differ materially from the expectations, intentions, beliefs, plans or predictions of the future expressed or implied by such forward-looking statements. We undertake no obligation to update these forward-looking statements to reflect events or circumstances after the date hereof or to reflect the occurrence of unanticipated events, except as may be required by law.

Independence Realty Trust Announces Third Quarter 2025 Financial Results

PHILADELPHIA – (BUSINESS WIRE) – October 29, 2025 — Independence Realty Trust, Inc. (“IRT”) (NYSE: IRT), a multifamily apartment REIT, announces its third quarter 2025 financial results.

Q3 2025 EPS of $0.03

Q3 CFFO Per Share of $0.29

In Line with Expectations

2.7% Same-Store NOI Growth in Q3

1.4% Increase in Rental Revenue and 0.7% Decrease in Property Operating Expenses

95.6% Same-Store Occupancy at End of Q3

60.4% Resident Retention Rate in Q3

Completed 788 Renovations in Value Add Program

Achieved Average ROI of 14.8% During Q3

Accretive Investment Activity

Acquired Two Communities in Orlando During Q3 for an Aggregate Purchase Price of $155 million

Capital Recycling Out of Three Communities to Fund Higher Growth Investments is Progressing

Balance Sheet Remains Strong

Conservative Leverage and Ample Liquidity to Fund Growth

Reaffirmed Full Year 2025 Guidance Midpoints

Management Commentary

“Third quarter same-store NOI growth of 2.7% and CFFO per share of $0.29 were in line with our expectations. We remain committed to prioritizing stable occupancy, which will position us to capture improving rental rate growth as supply pressures continue to recede,” said Scott Schaeffer, Chairman and CEO. “I am also pleased to report bad debt during the third quarter improved to less than 1% of same-store revenues driven by improved processes and our investments in technology. We will continue to invest in technologies to drive further operational efficiencies that enhance the resident experience while benefiting shareholders.”

Third Quarter Summary

|

• |

Net income available to common shares of $6.9 million for the quarter ended September 30, 2025 compared to $12.4 million for the quarter ended September 30, 2024. Earnings per diluted share (“EPS”) of $0.03 for the quarter ended September 30, 2025 compared to $0.05 for the quarter ended September 30, 2024. |

|

• |

Same-store portfolio NOI growth of 2.7% for the quarter ended September 30, 2025 compared to the quarter ended September 30, 2024. |

|

• |

Core Funds from Operations (“CFFO”) of $70.0 million for the quarter ended September 30, 2025 compared to $66.8 million for the quarter ended September 30, 2024. CFFO per share was $0.29 for the third quarter of 2025 and for the third quarter of 2024. |

|

• |

Adjusted EBITDA of $92.6 million for the quarter ended September 30, 2025 compared to $87.5 million for the quarter ended September 30, 2024. |

|

• |

Value add program completed renovations of 788 units during the quarter ended September 30, 2025, achieving a weighted average return on investment during the quarter of 14.8%. |

Included later in this press release are definitions of NOI, CFFO, Adjusted EBITDA and other Non-GAAP financial measures and reconciliations of such measures to their most comparable financial measures as calculated and presented in accordance with GAAP, as well as discussion of our same-store methodology.

Same-Store Portfolio(1) Operating Results

|

Three Months Ended |

Nine Months Ended |

|||

|

September 30, 2025 Compared to |

September 30, 2025 Compared to |

|||

|

Three Months Ended |

Nine Months Ended |

|||

|

September 30, 2024 |

September 30, 2024 |

|||

|

Rental and other property revenue |

1.4% increase |

1.6% increase |

||

|

Property operating expenses |

0.7% decrease |

0.1% decrease |

||

|

NOI |

2.7% increase |

2.7% increase |

||

|

Portfolio average occupancy |

10 bps decrease to 95.3% |

40 bps increase to 95.4% |

||

|

Portfolio average rental rate |

0.6% increase to $1,581 |

0.9% increase to $1,577 |

||

|

NOI Margin |

90 bps increase to 63.4% |

60 bps increase to 63.0% |

|

Q2 2025 |

Q3 2025 |

|||||||

|

Same-Store Portfolio(1) |

||||||||

|

Average Occupancy |

95.3 | % | 95.3 | % | ||||

|

Lease Over Lease Effective Rental Rate Growth:(2) |

||||||||

|

New Leases |

(3.1 | )% | (3.5 | )% | ||||

|

Renewal Leases |

3.9 | % | 2.6 | % | ||||

|

Blended |

0.7 | % | 0.1 | % | ||||

|

Resident Retention Rate |

58.4 | % | 60.4 | % | ||||

|

Same-Store Portfolio excluding Ongoing Value Add |

||||||||

|

Average Occupancy |

95.5 | % | 95.8 | % | ||||

|

Lease Over Lease Effective Rental Rate Growth:(2) |

||||||||

|

New Leases |

(3.8 | )% | (4.3 | )% | ||||

|

Renewal Leases |

3.9 | % | 2.5 | % | ||||

|

Blended |

0.4 | % | (0.3 | )% | ||||

|

Resident Retention Rate |

58.7 | % | 60.7 | % | ||||

|

Value Add (34 properties with Ongoing Value Add) |

||||||||

|

Average Occupancy |

95.0 | % | 94.4 | % | ||||

|

Lease Over Lease Effective Rental Rate Growth:(2) |

||||||||

|

New Leases |

(2.1 | )% | (2.2 | )% | ||||

|

Renewal Leases |

3.9 | % | 2.7 | % | ||||

|

Blended |

1.1 | % | 0.7 | % | ||||

|

Resident Retention Rate |

58.0 | % | 59.7 | % | ||||

|

(1) |

Same-store portfolio includes 105 properties, which represent 30,502 units. |

|

(2) |

Lease-over-lease effective rent growth represents the change in effective monthly rent, as adjusted for concessions, for each unit that had a prior lease and current lease that are for a term of 9-14 months. Q2 2025 new, renewal, and blended lease over lease rent growth for all leases was (3.4)%, 4.2%, and 0.7%, respectively. Q3 2025 new, renewal, and blended lease over lease rent growth for all leases was (3.9)%, 2.8% and 0.1%, respectively. |

Value Add Program

We completed renovations of 788 units during the three months ended September 30, 2025, achieving a weighted average return on investment of 14.8%, with an average cost per unit renovated of $20,269, and an average monthly rent increase per unit of $249 over unrenovated comparable units. We completed renovations of 1,517 units during the nine months ended September 30, 2025, achieving a weighted average return on investment of 15.4%, with an average cost per unit renovated of $19,612, and an average monthly rent increase per unit of $252 over unrenovated comparable units. See the Value Add Summary page of our supplemental information for additional information on our projects’ life to date as of September 30, 2025.

Investment Activity

Acquisitions

| • |

On July 31, 2025, we acquired 3030 at Apopka, a 240-unit community in Orlando, Florida, for $60.25 million.

|

|

| • |

On August 14, 2025, we acquired M2 at Millenia 700, a 403-unit community, also in Orlando, Florida for $94.75 million.

|

|

| • |

The aggregate purchase price of these two acquisitions totaled $155.0 million, and the acquisitions increased our exposure in Orlando, Florida from 617 units to 1,260 units.

|

|

| • | We used $101.0 million of proceeds from sales of our common stock under our forward sale agreements to acquire these communities on a leverage-neutral and CFFO accretive basis. |

Properties Held for Sale

As of September 30, 2025, we had three properties classified as held for sale.

|

• |

Jamestown at St. Matthews: During the three months ended June 30, 2025, we classified this property in Louisville, Kentucky, as held for sale. This property is under contract for sale and the sale is expected to close by year end at a gain of approximately $18.0 million.

|

|

| • |

Stonebridge Crossing: During the three months ended June 30, 2025, we classified this property in Memphis, Tennessee as held for sale. We are actively marketing this property for sale and expect it to close in early 2026.

|

|

| • |

Bella Terra at City Center: During the three months ended June 30, 2025, we classified this property in Denver, Colorado as held for sale. We recognized a loss on impairment of $12.8 million in the third quarter of 2025. We expect the sale of this property to occur in 2026.

|

Joint Ventures

| • |

Metropolis at Innsbrook, Richmond, Virginia: On July 21, 2025, the joint venture sold this 402-unit apartment community. We received $31.1 million in proceeds from the sale, comprised of a return of our initial investment of $24.5 million and equity proceeds of $6.6 million. We recognized a gain on sale of $10.4 million in the third quarter of 2025.

|

|

|

• |

The Approach, Indianapolis, Indiana: On October 8, 2025, we entered into a joint venture for the development of a to-be-built multifamily project comprised of 318 units just outside Indianapolis, Indiana. We have committed to invest an aggregate of $20.0 million in this joint venture, and, as of October 8, 2025, had funded $1.7 million on account of this commitment.

|

|

| • |

Views of Music City II, Nashville, Tennessee: On October 9, 2025, our joint venture partner redeemed our investment in this property, comprised of a return of our initial capital of $5.9 million and a preferred return of $3.3 million. We recognized the preferred return of $3.3 million in Income (loss) from unconsolidated real estate entities in October 2025. Under the terms of our joint venture agreement, we are entitled to the right of first refusal on the sale of the property. |

Capital Expenditures

Across our total portfolio for the three months ended September 30, 2025, recurring capital expenditures were $8.6 million, or $246 per unit, value add expenditures were $14.7 million, non-recurring expenditures were $16.9 million and development expenditures were $1.0 million, respectively. For the nine months ended September 30, 2025, recurring capital expenditures were $24.6 million, or $707 per unit, value add expenditures were $31.9 million, non-recurring expenditures were $39.2 million and development expenditures were $9.9 million, respectively.

Capital Markets

In connection with our previously announced public offering of 11,500,000 shares of common stock, in September 2024, we entered into forward sale agreements with Citigroup. On September 29, 2025, we physically settled 5,300,000 of those shares pursuant to the forward sale agreements at a weighted average price of $19.06 per share, resulting in proceeds to us of $101.0 million which we used to fund acquisitions. The scheduled maturity date of our forward sale agreements is December 31, 2025. As of September 30, 2025, there were 300,000 shares of common stock remaining under our forward sale agreements with Citigroup and 2,681,000 shares remaining to be settled pursuant to the forward sale transactions entered into under our At-the-Market offering program, for a combined total of 2,981,600 shares of our common stock. Assuming the 2,981,600 shares were settled at the September 30, 2025 forward sales price, we would receive additional proceeds of approximately $61.7 million.

Balance Sheet and Liquidity

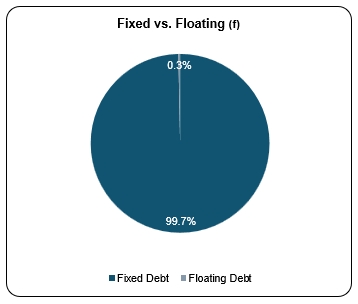

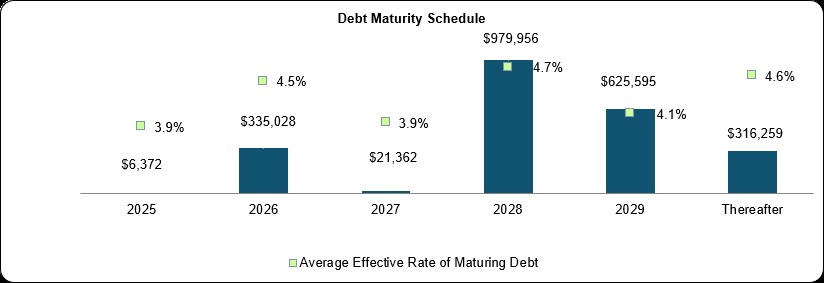

At September 30, 2025, our net debt to Adjusted EBITDA was 6.0x. As of the same date and including the effect of hedges, our weighted average effective interest rate on our consolidated debt was 4.3% with a weighted average maturity of 3.2 years, and 99.7% of our debt was either subject to fixed interest rates or was hedged. Also as of September 30, 2025, we had approximately $628.1 million in liquidity through a combination of unrestricted cash and cash equivalents, unsettled proceeds related to forward sale agreements (assuming the forward sale agreements are physically settled at the forward price determined at the closing of such forward sale agreements), and capacity under our unsecured revolver.

Dividend Distribution

On September 8, 2025, our Board of Directors declared a quarterly dividend of $0.17 per share of common stock. The third quarter dividend was paid on October 24, 2025 to stockholders of record at the close of business on September 30, 2025.

2025 EPS, FFO and CFFO Guidance

|

Previous Guidance |

Current Guidance |

Change at Midpoint |

||||||||||||||||||

|

2025 Full Year EPS and CFFO Guidance(1) |

Low |

High |

Low |

High |

||||||||||||||||

|

Earnings per share (3) |

$ | 0.475 | $ | 0.535 | $ | 0.27 | $ | 0.28 | $ | (0.23 | ) | |||||||||

|

Adjustments: |

||||||||||||||||||||

|

Depreciation and amortization |

1.02 | 1.02 | 1.00 | 1.00 | (0.02 | ) | ||||||||||||||

|

Gains on sale included with income from unconsolidated real estate entities (2) |

(0.04 | ) | (0.04 | ) | (0.04 | ) | (0.04 | ) |

— |

|||||||||||

|

Gain on sale of real estate assets (3) |

(0.25 | ) | (0.30 | ) | (0.03 | ) | (0.03 | ) | 0.25 | |||||||||||

|

FFO per share |

1.195 | 1.215 | 1.20 | 1.21 | — | |||||||||||||||

|

Loan (premium accretion) discount amortization, net |

(0.03 | ) | (0.03 | ) | (0.03 | ) | (0.03 | ) | — | |||||||||||

|

CFFO per share |

$ | 1.165 | $ | 1.185 | $ | 1.17 | $ | 1.18 | $ | — | ||||||||||

| Weighted average shares and units (in millions) | 241.6 | 240.2 | (1.4 | ) | ||||||||||||||||

|

(1)

|

This guidance, including the underlying assumptions presented in the table on the following page, constitutes forward-looking information. Actual full year 2025 EPS, FFO, and CFFO could vary significantly from the projections presented. See “Forward-Looking Statements”. Our guidance is based on the key guidance assumptions detailed below. |

|

(2)

|

Represents income from unconsolidated real estate entities we recognized in the third quarter of 2025 with respect to the Metropolis joint venture sale discussed above.

|

|

(3)

|

Change in EPS at the midpoint is due to fewer gains on sale from lower disposition volume. Gain on sale of real estate assets includes gains on sale (loss on impairment) recognized with respect to the one property in Birmingham, Alabama sold in the first quarter of 2025 and two of the properties classified as held for sale as of September 30, 2025.

|

2025 Guidance Assumptions(1)

Our key guidance assumptions for 2025 are enumerated below. See the definitions at the end of this release for further information regarding our same-store definitions.

|

Same-Store Portfolio: |

Previous 2025 Outlook: |

Current 2025 Outlook: |

Change at Midpoint |

|||

|

Number of properties/units |

105 properties / 30,502 units |

105 properties / 30,502 units |

— | |||

|

Property revenue growth |

1.5% - 1.9% |

1.6% - 1.8% |

— | |||

|

Controllable operating expense growth |

1.7% - 2.1% |

1.8% - 2.0% |

— | |||

|

Real estate tax and insurance expense growth |

(0.8%) - 0.0% |

(0.6%) - (0.2%) |

— | |||

|

Total operating expense growth |

0.7% - 1.3% |

0.9% - 1.1% |

— | |||

|

NOI growth |

1.7% - 2.5% |

1.9% - 2.3% |

— | |||

|

Corporate Expenses ($ in millions) |

||||||

|

General and administrative & property management expenses |

$54 - $56 |

$54 - $55 |

$(0.5) |

|||

|

Interest expense(2) |

$88 - $90 |

$86 - $88 |

$(2.0) | |||

|

Transaction/Investment Volume(3) ($ in millions) |

||||||

|

Acquisition volume |

$580 - $650 |

$215 |

$(400) | |||

|

Disposition volume |

$385 - $435 |

$161 |

$(249) | |||

|

Capital Expenditures ($ in millions) |

||||||

|

Recurring |

$27 - $29 |

$29 - $30 |

$1.5 | |||

|

Value add renovation program |

$38 - $42 |

$38 - $40 |

$(1.0) | |||

|

Non-recurring and revenue enhancing |

$43 - $47 |

$46 - $48 |

$2.0 | |||

|

Development |

$5 - $6 |

$5 - $6 |

— |

|

(1) |

This guidance, including the underlying assumptions, constitutes forward-looking information. Actual results could vary significantly from the projections presented. We undertake no duty to update the assumptions used in our guidance except as required by law. See “Forward-Looking Statements.” |

|

(2) |

Interest expense includes amortization of deferred financing costs but excludes loan premium accretion, net. As a result of purchase accounting we recorded loan premiums, net, that are accreted into and reduce GAAP interest expense over the remaining term of the associated debt. However, loan premium accretion is excluded from CFFO. |

|

(3) |

Acquisition volume reflects one property in Indianapolis, Indiana that was acquired for $59.5 million in the first quarter of 2025 and two properties in Orlando, Florida that were acquired for an aggregate purchase price of $155.0 million in the third quarter of 2025. Disposition volume reflects the sale of one property sold for $111.0 million in the first quarter of 2025 and approximately $50.0 million related to the expected disposition of one of the three properties classified as held for sale as of September 30, 2025. We continue to evaluate our portfolio for capital recycling opportunities so actual acquisition and disposition volume could vary significantly from our projections. |

See the schedules at the end of this earnings release for selected financial information for IRT.

Non-GAAP Financial Measures and Definitions

We disclose the following non-GAAP financial measures in this earnings release: FFO, CFFO, NOI and Adjusted EBITDA. Included at the end of this release are definitions of these non-GAAP financial measures and a reconciliation of our reported net income to our FFO and CFFO, a reconciliation of our same-store NOI to our reported net income, a reconciliation of our Adjusted EBITDA to net income, and management’s rationales for the usefulness of each of these and other non-GAAP financial measures used in this release.

Conference Call

All interested parties can listen to the live conference call webcast at 9:00 AM ET on Thursday, October 30, 2025 from the investor relations section of the IRT website at www.irtliving.com or by dialing 1.888.440.3307, access code 1963990. For those who are not available to listen to the live call, the replay will be available shortly following the live call from the investor relations section of IRT’s website until the next earnings release. A replay of the conference call can also be accessed telephonically until Thursday, November 6, 2025 by dialing 1.800.770.2030, access code 1963990.

Supplemental Information

We produce supplemental information that includes details regarding the performance of the portfolio, financial information, non-GAAP financial measures, same-store portfolio information and other useful information for investors. The supplemental information is available via our website, www.irtliving.com, through the "Investor Relations" section.

About Independence Realty Trust, Inc.

Independence Realty Trust, Inc. (NYSE: IRT), an S&P 400 MidCap Company, is a real estate investment trust (“REIT”) that owns and operates multifamily communities, across non-gateway U.S. markets. IRT’s investment strategy is focused on gaining scale near major employment centers within key amenity rich submarkets that offer good school districts and high-quality retail. IRT’s main objective is to provide attractive risk-adjusted returns to shareholders through diligent portfolio management, strong operational performance, and a consistent return on capital through distributions and capital appreciation. More information may be found on the Company’s website, www.irtliving.com.

Forward-Looking Statements

This release contains certain forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended. Such forward-looking statements include, but are not limited to, our earnings guidance, and the assumptions underlying such guidance, our planned use of remaining proceeds from our sales of common stock on a forward basis, our expectations with respect to the three properties which are classified as held for sale, our expectations with respect to our new joint venture and our expectations with respect to future acquisitions and dispositions. All statements in this release that address financial and operating performance, events or developments that we expect or anticipate will occur or be achieved in the future are forward-looking statements.

Our forward-looking statements are not guarantees of future performance and involve estimates, projections, forecasts and assumptions, including as to matters that are not within our control, and are subject to risks and uncertainties including, without limitation, risks and uncertainties related to changes in market demand for rental apartment homes and pricing pressures, including from competitors, that could lead to declines in occupancy and rent levels, uncertainty and volatility in capital and credit markets, including changes that reduce availability, and increase costs, of capital, unexpected changes in our intention or ability to repay certain debt prior to maturity, increased costs on account of inflation, increased competition in the labor market, our planned use of the remaining proceeds from our sales of common stock on a forward basis, inability to sell certain assets, including those assets designated as held for sale, within the time frames or at the pricing levels expected, failure to achieve expected benefits from the redeployment of proceeds from asset sales, inability or failure to achieve anticipated benefits from future acquisitions and dispositions, delays in completing, and cost overruns incurred in connection with, our value add initiatives and failure to achieve rent increases and occupancy levels on account of the value add initiatives, unexpected impairments or impairments in excess of our estimates, increased regulations generally and specifically on the rental housing market, including legislation that may regulate rents and fees or delay or limit our ability to evict non-paying residents, risks endemic to real estate and the real estate industry generally, the impact of potential outbreaks of infectious diseases and measures intended to prevent the spread or address the effects thereof, economic conditions, including inflation and recessionary conditions and their related impacts on the real estate industry, U.S. and global trade policies and tensions, including changes in, or the imposition of, tariffs and/or trade barriers and the economic impacts, volatility and uncertainty resulting therefrom, the impacts from the U.S. government shutdown, the effects of natural and other disasters, unknown or unexpected liabilities, including the cost of legal proceedings, costs and disruptions as the result of a cybersecurity incident or other technology disruption, including but not limited to a third party's unauthorized access to our data or the data of our residents, unexpected capital needs, inability to obtain appropriate insurance coverages at reasonable rates, or at all, or losses from catastrophes in excess of our insurance coverages, and share price fluctuations. Please refer to the documents filed by us with the SEC, including specifically the “Risk Factors” sections of our Annual Report on Form 10-K for the year ended December 31, 2024 and our Quarterly Report on Form 10-Q for the quarter ended March 31,2025, and our other filings with the SEC, which identify additional factors that could cause actual results to differ from those contained in forward-looking statements.

These forward-looking statements are based upon the beliefs and expectations of our management at the time of this release and our actual results may differ materially from the expectations, intentions, beliefs, plans or predictions of the future expressed or implied by such forward-looking statements. We undertake no obligation to update these forward-looking statements to reflect events or circumstances after the date hereof or to reflect the occurrence of unanticipated events, except as may be required by law.

FINANCIAL & OPERATING HIGHLIGHTS

Dollars in thousands, except per share data

|

For the Three Months Ended |

||||||||||||||||||||

|

September 30, 2025 |

June 30, 2025 |

March 31, 2025 |

December 31, 2024 |

September 30, 2024 |

||||||||||||||||

|

Selected Financial Information: |

||||||||||||||||||||

|

Operating Statistics: |

||||||||||||||||||||

|

Net income (loss) available to common shares |

$ | 6,893 | $ | 8,046 | $ | 8,354 | $ | (1,001 | ) | $ | 12,365 | |||||||||

|

Earnings per share -- diluted |

$ | 0.03 | $ | 0.03 | $ | 0.04 | $ | 0.00 | $ | 0.05 | ||||||||||

|

Rental and other property revenue |

$ | 166,888 | $ | 161,891 | $ | 160,905 | $ | 160,617 | $ | 159,860 | ||||||||||

|

Property operating expenses |

$ | 61,699 | $ | 60,935 | $ | 59,263 | $ | 54,195 | $ | 60,538 | ||||||||||

|

NOI |

$ | 105,189 | $ | 100,956 | $ | 101,642 | $ | 106,422 | $ | 99,322 | ||||||||||

|

NOI margin |

63.0 | % | 62.4 | % | 63.2 | % | 66.3 | % | 62.1 | % | ||||||||||

|

Adjusted EBITDA |

$ | 92,643 | $ | 87,556 | $ | 85,748 | $ | 94,533 | $ | 87,453 | ||||||||||

|

FFO per share |

$ | 0.30 | $ | 0.28 | $ | 0.28 | $ | 0.33 | $ | 0.30 | ||||||||||

|

CFFO per share |

$ | 0.29 | $ | 0.28 | $ | 0.27 | $ | 0.32 | $ | 0.29 | ||||||||||

|

Dividends per share |

$ | 0.17 | $ | 0.17 | $ | 0.16 | $ | 0.16 | $ | 0.16 | ||||||||||

|

CFFO payout ratio |

58.6 | % | 60.7 | % | 59.3 | % | 50.0 | % | 55.2 | % | ||||||||||

|

Portfolio Data: |

||||||||||||||||||||

|

Total gross assets |

$ | 7,058,026 | $ | 6,874,320 | $ | 6,844,114 | $ | 6,882,296 | $ | 6,733,864 | ||||||||||

|

Total number of operating properties (a) |

115 | 113 | 113 | 113 | 110 | |||||||||||||||

|

Total units (a) |

33,818 | 33,175 | 33,175 | 33,615 | 32,670 | |||||||||||||||

|

Portfolio period end occupancy (a) |

95.1 | % | 95.2 | % | 94.9 | % | 95.4 | % | 95.5 | % | ||||||||||

|

Portfolio average occupancy (a) |

94.9 | % | 95.2 | % | 95.3 | % | 95.4 | % | 95.4 | % | ||||||||||

|

Portfolio average effective monthly rent, per unit (a) |

$ | 1,593 | $ | 1,582 | $ | 1,583 | $ | 1,572 | $ | 1,571 | ||||||||||

|

Same-store portfolio period end occupancy (b) |

95.6 | % | 95.4 | % | 95.1 | % | 95.5 | % | 95.6 | % | ||||||||||

|

Same-store portfolio average occupancy (b) |

95.3 | % | 95.3 | % | 95.5 | % | 95.5 | % | 95.4 | % | ||||||||||

|

Same-store portfolio average effective monthly rent, per unit (b) |

$ | 1,581 | $ | 1,575 | $ | 1,573 | $ | 1,571 | $ | 1,571 | ||||||||||

|

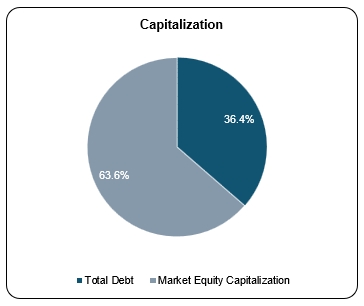

Capitalization: |

||||||||||||||||||||

|

Total debt (c) |

$ | 2,296,202 | $ | 2,249,801 | $ | 2,253,957 | $ | 2,333,683 | $ | 2,286,694 | ||||||||||

|

Common share price, period end |

$ | 16.39 | $ | 17.69 | $ | 21.23 | $ | 19.84 | $ | 20.50 | ||||||||||

|

Market equity capitalization |

$ | 4,016,286 | $ | 4,241,203 | $ | 5,088,933 | $ | 4,697,713 | $ | 4,736,212 | ||||||||||

|

Total market capitalization |

$ | 6,312,488 | $ | 6,491,004 | $ | 7,342,890 | $ | 7,031,396 | $ | 7,022,906 | ||||||||||

|

Total debt/total gross assets |

32.5 | % | 32.7 | % | 32.9 | % | 33.9 | % | 34.0 | % | ||||||||||

|

Net debt to adjusted EBITDA (d) |

6.0x |

6.3x |

6.3x |

5.9x |

6.3x |

|||||||||||||||

|

Interest coverage |

4.5x |

4.7x |

4.4x |

4.8x |

4.8x |

|||||||||||||||

|

Common shares and OP Units: |

||||||||||||||||||||

|

Shares outstanding |

239,103,283 | 233,809,823 | 233,763,180 | 230,838,249 | 225,093,090 | |||||||||||||||

|

OP units outstanding |

5,941,643 | 5,941,643 | 5,941,643 | 5,941,643 | 5,941,643 | |||||||||||||||

|

Common shares and OP units outstanding |

245,044,926 | 239,751,466 | 239,704,823 | 236,779,892 | 231,034,733 | |||||||||||||||

|

Weighted average common shares and OP units |

239,576,189 | 239,438,276 | 236,665,226 | 230,893,621 | 230,762,299 | |||||||||||||||

|

(a) |

Excludes our development projects Destination at Arista and Flatirons Flats, as applicable. See the definitions at the end of this release. Destination at Arista no longer met the definition of a development project in the fourth quarter of 2024. |

|

(b) |

Same-store portfolio consists of 105 properties, which represent 30,502 units. |

|

(c) |

Includes indebtedness associated with real estate held for sale, as applicable. |

|

(d) |

Reflects net debt to Adjusted EBITDA, which is annualized for each period presented, including adjustments for the timing of acquisitions and dispositions impacting quarterly EBITDA. For the five quarters ended September 30, 2025, net debt to Adjusted EBITDA excluding adjustments for timing of acquisitions and dispositions was 6.1x, 6.3x, 6.4x, 6.0x, and 6.4x, respectively. |

Dollars in thousands, except per share data

|

As of |

||||||||||||||||||||

|

September 30, 2025 |

June 30, 2025 |

March 31, 2025 |

December 31, 2024 |

September 30, 2024 |

||||||||||||||||

|

Assets: |

||||||||||||||||||||

|

Real estate held for investment, at cost |

$ | 6,571,161 | $ | 6,356,830 | $ | 6,442,303 | $ | 6,363,936 | $ | 6,341,504 | ||||||||||

|

Less: accumulated depreciation |

(861,370 | ) | (810,042 | ) | (789,619 | ) | (740,957 | ) | (715,702 | ) | ||||||||||

|

Real estate held for investment, net |

5,709,791 | 5,546,788 | 5,652,684 | 5,622,979 | 5,625,802 | |||||||||||||||

|

Real estate held for sale |

107,182 | 119,875 | — | 110,112 | — | |||||||||||||||

|

Real estate under development |

65,628 | 91,849 | 117,802 | 116,861 | 115,221 | |||||||||||||||

|

Cash and cash equivalents |

23,290 | 19,491 | 29,055 | 21,228 | 17,611 | |||||||||||||||

|

Restricted cash |

27,639 | 23,035 | 19,279 | 22,224 | 30,632 | |||||||||||||||

|

Investment in unconsolidated real estate entities |

93,965 | 106,920 | 101,640 | 91,975 | 95,393 | |||||||||||||||

|

Other assets |

47,771 | 38,389 | 39,330 | 39,596 | 43,566 | |||||||||||||||

|

Derivative assets |

11,873 | 14,635 | 20,084 | 29,300 | 18,821 | |||||||||||||||

|

Intangible assets, net |

5,453 | 1,644 | 3,620 | 3,644 | 1,158 | |||||||||||||||

|

Total assets |

$ | 6,092,592 | $ | 5,962,626 | $ | 5,983,494 | $ | 6,057,919 | $ | 5,948,204 | ||||||||||

|

Liabilities and Equity: |

||||||||||||||||||||

|

Indebtedness, net |

$ | 2,296,202 | $ | 2,249,801 | $ | 2,253,957 | $ | 2,274,651 | $ | 2,286,694 | ||||||||||

|

Indebtedness associated with real estate held for sale, net |

— | — | — | 59,032 | — | |||||||||||||||

|

Accounts payable and accrued expenses |

119,513 | 105,576 | 86,399 | 94,670 | 119,286 | |||||||||||||||

|

Accrued interest payable |

10,265 | 7,815 | 10,136 | 8,630 | 6,858 | |||||||||||||||

|

Dividends payable |

41,592 | 40,691 | 37,865 | 37,827 | 36,906 | |||||||||||||||

|

Derivative liabilities |

737 | 233 | 29 | — | 1,779 | |||||||||||||||

|

Other liabilities |

9,023 | 7,550 | 7,929 | 8,035 | 7,966 | |||||||||||||||

|

Total liabilities |

2,477,332 | 2,411,666 | 2,396,315 | 2,482,845 | 2,459,489 | |||||||||||||||

|

Equity: |

||||||||||||||||||||

|

Shareholders' Equity: |

||||||||||||||||||||

|

Preferred shares, $0.01 par value per share |

— | — | — | — | — | |||||||||||||||

|

Common shares, $0.01 par value per share |

2,391 | 2,338 | 2,337 | 2,308 | 2,250 | |||||||||||||||

|

Additional paid in capital |

4,022,309 | 3,920,436 | 3,918,718 | 3,868,006 | 3,755,311 | |||||||||||||||

|

Accumulated other comprehensive income |

9,095 | 12,038 | 17,308 | 26,065 | 13,835 | |||||||||||||||

|

Accumulated deficit |

(548,319 | ) | (514,623 | ) | (482,973 | ) | (454,104 | ) | (416,223 | ) | ||||||||||

|

Total shareholders' equity |

3,485,476 | 3,420,189 | 3,455,390 | 3,442,275 | 3,355,173 | |||||||||||||||

|

Noncontrolling Interests |

129,784 | 130,771 | 131,789 | 132,799 | 133,542 | |||||||||||||||

|

Total equity |

3,615,260 | 3,550,960 | 3,587,179 | 3,575,074 | 3,488,715 | |||||||||||||||

|

Total liabilities and equity |

$ | 6,092,592 | $ | 5,962,626 | $ | 5,983,494 | $ | 6,057,919 | $ | 5,948,204 | ||||||||||

STATEMENTS OF OPERATIONS, FFO & CFFO

TRAILING FIVE QUARTERS

(Dollars in thousands, except per share data)

|

For the Three Months Ended |

||||||||||||||||||||

|

September 30, 2025 |

June 30, 2025 |

March 31, 2025 |

December 31, 2024 |

September 30, 2024 |

||||||||||||||||

|

Revenue: |

||||||||||||||||||||

|

Rental and other property revenue |

$ | 166,888 | $ | 161,891 | $ | 160,905 | $ | 160,617 | $ | 159,860 | ||||||||||

|

Other revenue |

250 | 297 | 338 | 346 | 275 | |||||||||||||||

|

Total revenue |

167,138 | 162,188 | 161,243 | 160,963 | 160,135 | |||||||||||||||

|

Expenses: |

||||||||||||||||||||

|

Property operating expenses |

61,699 | 60,935 | 59,263 | 54,195 | 60,538 | |||||||||||||||

|

Property management expenses |

7,891 | 7,715 | 7,826 | 7,379 | 7,379 | |||||||||||||||

|

General and administrative expenses (a) |

4,905 | 5,982 | 8,406 | 4,856 | 4,765 | |||||||||||||||

|

Depreciation and amortization expense |

61,735 | 59,794 | 58,725 | 57,742 | 55,261 | |||||||||||||||

|

Casualty losses (gains), net |

419 | 255 | (115 | ) | (80 | ) | 1,249 | |||||||||||||

|

Total expenses |

136,649 | 134,681 | 134,105 | 124,092 | 129,192 | |||||||||||||||

|

Interest expense |

(20,455 | ) | (18,773 | ) | (19,348 | ) | (19,770 | ) | (18,308 | ) | ||||||||||

|

(Loss on impairment) gain on sale of real estate assets, net |

(12,841 | ) | — | 1,496 | (20,928 | ) | 688 | |||||||||||||

|

Loss on extinguishment of debt |

— | — | (67 | ) | (2 | ) | — | |||||||||||||

|

Other loss |

(12 | ) | — | (103 | ) | — | — | |||||||||||||

|

Income (loss) from investments in unconsolidated real estate entities |

9,814 | (562 | ) | (590 | ) | 2,729 | (703 | ) | ||||||||||||

|

Net income (loss) |

$ | 6,995 | $ | 8,172 | $ | 8,526 | $ | (1,100 | ) | $ | 12,620 | |||||||||

|

(Income) loss allocated to noncontrolling interests |

(102 | ) | (126 | ) | (172 | ) | 99 | (255 | ) | |||||||||||

|

Net income (loss) available to common shares |

$ | 6,893 | $ | 8,046 | $ | 8,354 | $ | (1,001 | ) | $ | 12,365 | |||||||||

|

Earnings per share - basic |

$ | 0.03 | $ | 0.03 | $ | 0.04 | $ | 0.00 | $ | 0.05 | ||||||||||

|

Weighted-average shares outstanding - Basic |

233,634,546 | 233,496,633 | 230,723,583 | 224,951,978 | 224,820,656 | |||||||||||||||

|

Earnings per share - diluted |

$ | 0.03 | $ | 0.03 | $ | 0.04 | $ | 0.00 | $ | 0.05 | ||||||||||

|

Weighted-average shares outstanding - Diluted |

234,283,170 | 234,131,752 | 231,828,484 | 224,951,978 | 226,058,400 | |||||||||||||||

|

Funds From Operations (FFO): |

||||||||||||||||||||

|

Net income (loss) |

$ | 6,995 | $ | 8,172 | $ | 8,526 | $ | (1,100 | ) | $ | 12,620 | |||||||||

|

Add-Back (Deduct): |

||||||||||||||||||||

|

Real estate depreciation and amortization |

61,282 | 59,372 | 58,308 | 57,332 | 54,880 | |||||||||||||||

|

Our share of real estate depreciation and amortization from investments in unconsolidated real estate entities |

375 | 457 | 457 | (212 | ) | 598 | ||||||||||||||

|

Loss on impairment of real estate assets, net, excluding prepayment gains |

12,841 | — | 73 | 20,928 | 160 | |||||||||||||||

|

Gain on sale of real estate associated with unconsolidated real estate entities |

(10,389 | ) | — | — | — | — | ||||||||||||||

|

FFO |

$ | 71,104 | $ | 68,001 | $ | 67,364 | $ | 76,948 | $ | 68,258 | ||||||||||

|

FFO per share |

$ | 0.30 | $ | 0.28 | $ | 0.28 | $ | 0.33 | $ | 0.30 | ||||||||||

|

CORE Funds From Operations (CFFO): |

||||||||||||||||||||

|

FFO |

$ | 71,104 | $ | 68,001 | $ | 67,364 | $ | 76,948 | $ | 68,258 | ||||||||||

|

Add-Back (Deduct): |

||||||||||||||||||||

|

Other depreciation and amortization |

453 | 422 | 417 | 410 | 382 | |||||||||||||||

|

Casualty losses (gains), net |

419 | 255 | (115 | ) | (80 | ) | 1,249 | |||||||||||||

|

Loan (premium accretion) discount amortization, net |

(2,001 | ) | (1,985 | ) | (2,029 | ) | (2,249 | ) | (2,239 | ) | ||||||||||

|

Prepayment (gains) penalties on asset dispositions |

— | — | (1,569 | ) | — | (848 | ) | |||||||||||||

|

Loss on extinguishment of debt |

— | — | 67 | 2 | — | |||||||||||||||

|

Other loss |

12 | — | 103 | — | — | |||||||||||||||

|

CFFO |

$ | 69,987 | $ | 66,693 | $ | 64,238 | $ | 75,031 | $ | 66,802 | ||||||||||

|

CFFO per share |

$ | 0.29 | $ | 0.28 | $ | 0.27 | $ | 0.32 | $ | 0.29 | ||||||||||

|

Weighted-average shares and units outstanding |

239,576,189 | 239,438,276 | 236,665,226 | 230,893,621 | 230,762,299 | |||||||||||||||

| (a) | Included in the three months ended March 31, 2025 is $2.8 million of stock compensation expense recorded with respect to stock awards granted to retirement eligible employees. |

STATEMENTS OF OPERATIONS, FFO & CFFO

Dollars in thousands, except per share data

|

For the Three Months Ended |

For the Nine Months Ended |

|||||||||||||||

|

September 30, |

September 30, |

|||||||||||||||

|

2025 |

2024 |

2025 |

2024 |

|||||||||||||

|

Revenue: |

||||||||||||||||

|

Rental and other property revenue |

$ | 166,888 | $ | 159,860 | $ | 489,684 | $ | 478,296 | ||||||||

|

Other revenue |

250 | 275 | 885 | 776 | ||||||||||||

|

Total revenue |

167,138 | 160,135 | 490,569 | 479,072 | ||||||||||||

|

Expenses: |

||||||||||||||||

|

Property operating expenses |

61,699 | 60,538 | 181,897 | 181,393 | ||||||||||||

|

Property management expenses |

7,891 | 7,379 | 23,433 | 22,544 | ||||||||||||

|

General and administrative expenses |

4,905 | 4,765 | 19,293 | 19,389 | ||||||||||||

|

Depreciation and amortization expense |

61,735 | 55,261 | 180,256 | 163,112 | ||||||||||||

|

Casualty losses |

419 | 1,249 | 559 | 4,015 | ||||||||||||

|

Total expenses |

136,649 | 129,192 | 405,438 | 390,453 | ||||||||||||

|

Interest expense |

(20,455 | ) | (18,308 | ) | (58,575 | ) | (56,371 | ) | ||||||||

|

(Loss on impairment) gain on sale of real estate assets, net |

(12,841 | ) | 688 | (11,344 | ) | 11,066 | ||||||||||

|

(Loss) gain on extinguishment of debt |

— | — | (67 | ) | 203 | |||||||||||

|

Other loss |

(12 | ) | — | (115 | ) | (1 | ) | |||||||||

|

Income (loss) from investments in unconsolidated real estate entities |

9,814 | (703 | ) | 8,663 | (2,382 | ) | ||||||||||

|

Net income |

6,995 | 12,620 | 23,693 | 41,134 | ||||||||||||

|

Income allocated to noncontrolling interests |

(102 | ) | (255 | ) | (401 | ) | (840 | ) | ||||||||

|

Net income available to common shares |

$ | 6,893 | $ | 12,365 | $ | 23,292 | $ | 40,294 | ||||||||

|

Earnings per share - basic |

$ | 0.03 | $ | 0.05 | $ | 0.10 | $ | 0.18 | ||||||||

|

Weighted-average shares outstanding - Basic |

233,634,546 | 224,820,656 | 232,628,917 | 224,747,327 | ||||||||||||

|

Earnings per share - diluted |

$ | 0.03 | $ | 0.05 | $ | 0.10 | $ | 0.18 | ||||||||

|

Weighted-average shares outstanding - Diluted |

234,283,170 | 226,058,400 | 233,403,810 | 225,530,265 | ||||||||||||

|

Funds From Operations (FFO): |

||||||||||||||||

|

Net income |

$ | 6,995 | $ | 12,620 | $ | 23,693 | $ | 41,134 | ||||||||

|

Add-Back (Deduct): |

||||||||||||||||

|

Real estate depreciation and amortization |

61,282 | 54,880 | 178,964 | 162,028 | ||||||||||||

|

Our share of real estate depreciation and amortization from investments in unconsolidated real estate entities |

375 | 598 | 1,289 | 1,793 | ||||||||||||

|

Loss on impairment (gain on sale) of real estate assets, net, excluding prepayment gains |

12,841 | 160 | 12,914 | (9,113 | ) | |||||||||||

|

Gain on sale of real estate associated with unconsolidated real estate entities |

(10,389 | ) | — | (10,389 | ) | — | ||||||||||

|

FFO |

$ | 71,104 | $ | 68,258 | $ | 206,471 | $ | 195,842 | ||||||||

|

FFO per share |

$ | 0.30 | $ | 0.30 | $ | 0.87 | $ | 0.85 | ||||||||

|

CORE Funds From Operations (CFFO): |

||||||||||||||||

|

FFO |

$ | 71,104 | $ | 68,258 | $ | 206,471 | $ | 195,842 | ||||||||

|

Add-Back (Deduct): |

||||||||||||||||

|

Other depreciation and amortization |

453 | 382 | 1,292 | 1,083 | ||||||||||||

|

Casualty losses |

419 | 1,249 | 559 | 4,015 | ||||||||||||

|

Loan (premium accretion) discount amortization, net |

(2,001 | ) | (2,239 | ) | (6,015 | ) | (6,918 | ) | ||||||||

|

Prepayment (gains) penalties on asset dispositions |

— | (848 | ) | (1,570 | ) | (1,953 | ) | |||||||||

|

Loss (gain) on extinguishment of debt |

— | — | 67 | (203 | ) | |||||||||||

|

Other loss |

12 | — | 115 | 1 | ||||||||||||

|

CFFO |

$ | 69,987 | $ | 66,802 | $ | 200,919 | $ | 191,867 | ||||||||

|

CFFO per share |

$ | 0.29 | $ | 0.29 | $ | 0.84 | $ | 0.83 | ||||||||

|

Weighted-average shares and units outstanding |

239,576,189 | 230,762,299 | 238,570,560 | 230,689,617 | ||||||||||||

ADJUSTED EBITDA RECONCILIATION AND COVERAGE RATIO

Dollars in thousands

|

Three Months Ended |

||||||||||||||||||||

|

September 30, 2025 |

June 30, 2025 |

March 31, 2025 |

December 31, 2024 |

September 30, 2024 |

||||||||||||||||

|

Net income (loss) |

$ | 6,995 | $ | 8,172 | $ | 8,526 | $ | (1,100 | ) | $ | 12,620 | |||||||||

|

Add-Back (Deduct): |

||||||||||||||||||||

|

Interest expense |

20,455 | 18,773 | 19,348 | 19,770 | 18,308 | |||||||||||||||

|

Depreciation and amortization |

61,735 | 59,794 | 58,725 | 57,742 | 55,261 | |||||||||||||||

|

Casualty losses (gains), net |

419 | 255 | (115 | ) | (80 | ) | 1,249 | |||||||||||||

|

Loss on impairment (gain on sale) of real estate assets, net |

12,841 | — | (1,496 | ) | 20,928 | (688 | ) | |||||||||||||

|

Loss on extinguishment of debt |

— | — | 67 | 2 | — | |||||||||||||||

|

(Income) loss from investments in unconsolidated real estate entities |

(9,814 | ) | 562 | 590 | (2,729 | ) | 703 | |||||||||||||

|

Other loss |

12 | — | 103 | — | — | |||||||||||||||

|

Adjusted EBITDA |

$ | 92,643 | $ | 87,556 | $ | 85,748 | $ | 94,533 | $ | 87,453 | ||||||||||

|

INTEREST COST: |

||||||||||||||||||||

|

Interest expense |

$ | 20,455 | $ | 18,773 | $ | 19,348 | $ | 19,770 | $ | 18,308 | ||||||||||

|

INTEREST COVERAGE: |

4.5x |

4.7x |

4.4x |

4.8x |

4.8x |

|||||||||||||||

|

For the Three Months Ended September 30, |

For the Nine Months Ended September 30, |

|||||||||||||||

|

2025 |

2024 |

2025 |

2024 |

|||||||||||||

|

Net income |

$ | 6,995 | $ | 12,620 | $ | 23,693 | $ | 41,134 | ||||||||

|

Add-Back (Deduct): |

||||||||||||||||

|

Interest expense |

20,455 | 18,308 | 58,575 | 56,371 | ||||||||||||

|

Depreciation and amortization |

61,735 | 55,261 | 180,256 | 163,112 | ||||||||||||

|

Casualty losses |

419 | 1,249 | 559 | 4,015 | ||||||||||||

|

Loss on impairment (gain on sale) of real estate assets, net |

12,841 | (688 | ) | 11,344 | (11,066 | ) | ||||||||||

|

Loss (gain) on extinguishment of debt |

— | — | 67 | (203 | ) | |||||||||||

|

(Income) loss from investments in unconsolidated real estate entities |

(9,814 | ) | 703 | (8,663 | ) | 2,382 | ||||||||||

|

Other loss |

12 | — | 115 | 1 | ||||||||||||

|

Adjusted EBITDA |

$ | 92,643 | $ | 87,453 | $ | 265,946 | $ | 255,746 | ||||||||

|

INTEREST COST: |

||||||||||||||||

|

Interest expense |

$ | 20,455 | $ | 18,308 | $ | 58,575 | $ | 56,371 | ||||||||

|

INTEREST COVERAGE: |

4.5x |

4.8x |

4.5x |

4.5x |

||||||||||||

SAME-STORE PORTFOLIO NET OPERATING INCOME & NOI BRIDGE (a) (b)

TRAILING FIVE QUARTERS

Dollars in thousands, except per unit data

|

For the Three Months Ended |

||||||||||||||||||||

|

September 30, 2025 |

June 30, 2025 |

March 31, 2025 |

December 31, 2024 |

September 30, 2024 |

||||||||||||||||

|

Revenue: |

||||||||||||||||||||

|

Rental and other property revenue |

$ | 150,573 | $ | 148,113 | $ | 146,856 | $ | 147,071 | $ | 148,430 | ||||||||||

|

Property Operating Expenses: |

||||||||||||||||||||

|

Real estate taxes |

16,280 | 17,655 | 18,338 | 16,240 | 16,129 | |||||||||||||||

|

Property insurance |

3,107 | 3,381 | 3,716 | 3,719 | 3,713 | |||||||||||||||

|

Personnel expenses |

12,954 | 11,891 | 11,495 | 11,575 | 12,739 | |||||||||||||||

|

Utilities |

7,635 | 7,063 | 7,458 | 7,394 | 7,607 | |||||||||||||||

|

Repairs and maintenance |

5,393 | 5,659 | 4,186 | 2,240 | 6,023 | |||||||||||||||

|

Contract services |

5,788 | 5,825 | 5,500 | 5,140 | 5,616 | |||||||||||||||

|

Advertising expenses |

2,455 | 2,552 | 1,835 | 1,627 | 2,226 | |||||||||||||||

|

Other expenses |

1,571 | 1,620 | 1,564 | 1,492 | 1,537 | |||||||||||||||

|

Total property operating expenses |

55,183 | 55,646 | 54,092 | 49,427 | 55,590 | |||||||||||||||

|

Same-store portfolio NOI |

$ | 95,390 | $ | 92,467 | $ | 92,764 | $ | 97,644 | $ | 92,840 | ||||||||||

|

Same-store portfolio NOI margin |

63.4 | % | 62.4 | % | 63.2 | % | 66.4 | % | 62.5 | % | ||||||||||

|

Average occupancy |

95.3 | % | 95.3 | % | 95.5 | % | 95.5 | % | 95.4 | % | ||||||||||

|

Average effective monthly rent, per unit |

$ | 1,581 | $ | 1,575 | $ | 1,573 | $ | 1,571 | $ | 1,571 | ||||||||||

|

For the Three Months Ended |

||||||||||||||||||||

|

September 30, 2025 |

June 30, 2025 |

March 31, 2025 |

December 31, 2024 |

September 30, 2024 |

||||||||||||||||

|

Rental and other property revenue |

||||||||||||||||||||

|

Same-store portfolio |

$ | 150,573 | $ | 148,113 | $ | 146,856 | $ | 147,071 | $ | 148,430 | ||||||||||

|

Non same-store portfolio |

16,315 | 13,778 | 14,049 | 13,546 | 11,430 | |||||||||||||||

|

Total rental and other property revenue |

166,888 | 161,891 | 160,905 | 160,617 | 159,860 | |||||||||||||||

|

Property operating expenses |

||||||||||||||||||||

|

Same-store portfolio |

55,183 | 55,646 | 54,092 | 49,427 | 55,590 | |||||||||||||||

|

Non same-store portfolio |

6,516 | 5,289 | 5,171 | 4,768 | 4,948 | |||||||||||||||

|

Total property operating expenses |

61,699 | 60,935 | 59,263 | 54,195 | 60,538 | |||||||||||||||

|

NOI |

||||||||||||||||||||

|

Same-store portfolio |

95,390 | 92,467 | 92,764 | 97,644 | 92,840 | |||||||||||||||

|

Non same-store portfolio |

9,799 | 8,489 | 8,878 | 8,778 | 6,482 | |||||||||||||||

|

Total property NOI |

$ | 105,189 | $ | 100,956 | $ | 101,642 | $ | 106,422 | $ | 99,322 | ||||||||||

|

(a) |

Same-store portfolio consists of 105 properties, which represent 30,502 units. |

|

(b) |

See the definitions at the end of this release for a reconciliation from GAAP net income (loss) to NOI. |

SAME-STORE PORTFOLIO NET OPERATING INCOME (a)

THREE AND nine MONTHS ENDED September 30, 2025 AND 2024

Dollars in thousands, except per unit data

|

For the Three Months Ended |

For the Nine Months Ended |

|||||||||||||||||||||||

|

September 30, |

September 30, |

|||||||||||||||||||||||

|

2025 |

2024 |

% change |

2025 |

2024 |

% change |

|||||||||||||||||||

|

Revenue: |

||||||||||||||||||||||||

|

Rental and other property revenue |

$ | 150,573 | $ | 148,430 | 1.4 | % | $ | 445,542 | $ | 438,359 | 1.6 | % | ||||||||||||

|

Property Operating Expenses: |

||||||||||||||||||||||||

|

Real estate taxes |

16,280 | 16,129 | 0.9 | % | 52,274 | 52,294 | 0.0 | % | ||||||||||||||||

|

Property insurance |

3,107 | 3,713 | (16.3 | )% | 10,203 | 11,455 | (10.9 | )% | ||||||||||||||||

|

Personnel expenses |

12,954 | 12,739 | 1.7 | % | 36,341 | 36,493 | (0.4 | )% | ||||||||||||||||

|

Utilities |

7,635 | 7,607 | 0.4 | % | 22,155 | 21,529 | 2.9 | % | ||||||||||||||||

|

Repairs and maintenance |

5,393 | 6,023 | (10.5 | )% | 15,238 | 16,632 | (8.4 | )% | ||||||||||||||||

|

Contract services |

5,788 | 5,616 | 3.1 | % | 17,113 | 16,136 | 6.1 | % | ||||||||||||||||

|

Advertising expenses |

2,455 | 2,226 | 10.3 | % | 6,842 | 5,753 | 18.9 | % | ||||||||||||||||

|

Other expenses |

1,571 | 1,537 | 2.2 | % | 4,755 | 4,717 | 0.8 | % | ||||||||||||||||

|

Total property operating expenses |

55,183 | 55,590 | (0.7 | )% | 164,921 | 165,009 | (0.1 | )% | ||||||||||||||||

|

Same-store portfolio NOI |

$ | 95,390 | $ | 92,840 | 2.7 | % | $ | 280,621 | $ | 273,350 | 2.7 | % | ||||||||||||

|

Same-store portfolio NOI margin |

63.4 | % | 62.5 | % | 0.9 | % | 63.0 | % | 62.4 | % | 0.6 | % | ||||||||||||

|

Average occupancy |

95.3 | % | 95.4 | % | (0.1 | )% | 95.4 | % | 95.0 | % | 0.4 | % | ||||||||||||

|

Average effective monthly rent, per unit |

$ | 1,581 | $ | 1,571 | 0.6 | % | $ | 1,577 | $ | 1,563 | 0.9 | % | ||||||||||||

|

(a) |

Same-store portfolio consists of 105 properties, which represent 30,502 units. |

SAME-STORE PORTFOLIO NET OPERATING INCOME BY MARKET

THREE MONTHS ENDED September 30, 2025

Dollars in thousands, except rent per unit

|

Rental and Other Property Revenue |

Property Operating Expenses |

Net Operating Income |

Average Occupancy |

Average Effective Monthly Rent per Unit |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Market |

Number of Properties |

Units |

2025 |

2024 |

% Change |

2025 |

2024 |

% Change |

2025 |

2024 |

% Change |

2025 |

2024 |

% Change |

2025 |

2024 |

% Change |

|||||||||||||||||||||||||||||||||||||||||||||||||

|

Atlanta, GA |

13 | 5,180 | $ | 25,006 | $ | 24,635 | 1.5 | % | $ | 9,868 | $ | 10,405 | (5.2 | )% | $ | 15,135 | $ | 14,229 | 6.4 | % | 93.5 | % | 94.2 | % | (0.7 | )% | $ | 1,593 | $ | 1,599 | (0.4 | )% | ||||||||||||||||||||||||||||||||||

|

Dallas, TX |

14 | 4,007 | 22,635 | 22,422 | 0.9 | % | 8,535 | 8,120 | 5.1 | % | 14,101 | 14,302 | (1.4 | )% | 96.0 | % | 95.6 | % | 0.4 | % | 1,809 | 1,816 | (0.4 | )% | ||||||||||||||||||||||||||||||||||||||||||

|

Columbus, OH |

10 | 2,510 | 12,014 | 11,528 | 4.2 | % | 4,605 | 4,490 | 2.6 | % | 7,409 | 7,039 | 5.3 | % | 95.5 | % | 95.0 | % | 0.5 | % | 1,539 | 1,493 | 3.1 | % | ||||||||||||||||||||||||||||||||||||||||||

|

Nashville, TN |

5 | 1,508 | 7,712 | 7,640 | 0.9 | % | 1,978 | 2,560 | (22.7 | )% | 5,734 | 5,079 | 12.9 | % | 95.4 | % | 95.5 | % | (0.1 | )% | 1,626 | 1,637 | (0.7 | )% | ||||||||||||||||||||||||||||||||||||||||||

|

Oklahoma City, OK |

8 | 2,147 | 8,665 | 8,427 | 2.8 | % | 2,978 | 2,936 | 1.4 | % | 5,687 | 5,491 | 3.6 | % | 96.4 | % | 95.6 | % | 0.8 | % | 1,254 | 1,225 | 2.4 | % | ||||||||||||||||||||||||||||||||||||||||||

|

Indianapolis, IN |

7 | 1,979 | 9,006 | 8,910 | 1.1 | % | 3,444 | 3,110 | 10.7 | % | 5,562 | 5,800 | (4.1 | )% | 95.8 | % | 96.6 | % | (0.8 | )% | 1,458 | 1,420 | 2.7 | % | ||||||||||||||||||||||||||||||||||||||||||

|

Tampa-St. Petersburg, FL |

5 | 1,503 | 8,830 | 8,449 | 4.5 | % | 3,275 | 2,967 | 10.4 | % | 5,555 | 5,482 | 1.3 | % | 96.0 | % | 93.6 | % | 2.4 | % | 1,869 | 1,839 | 1.6 | % | ||||||||||||||||||||||||||||||||||||||||||

|

Raleigh - Durham, NC |

6 | 1,690 | 8,209 | 8,147 | 0.8 | % | 3,013 | 3,073 | (2.0 | )% | 5,196 | 5,074 | 2.4 | % | 95.5 | % | 95.6 | % | (0.1 | )% | 1,544 | 1,559 | (1.0 | )% | ||||||||||||||||||||||||||||||||||||||||||

|

Denver, CO |

5 | 1,093 | 6,164 | 6,261 | (1.5 | )% | 2,038 | 2,070 | (1.5 | )% | 4,126 | 4,191 | (1.6 | )% | 95.3 | % | 96.4 | % | (1.1 | )% | 1,786 | 1,796 | (0.6 | )% | ||||||||||||||||||||||||||||||||||||||||||

|

Houston, TX |

5 | 1,308 | 6,073 | 5,987 | 1.4 | % | 2,386 | 2,660 | (10.3 | )% | 3,687 | 3,328 | 10.8 | % | 95.6 | % | 96.8 | % | (1.2 | )% | 1,466 | 1,439 | 1.9 | % | ||||||||||||||||||||||||||||||||||||||||||

|

Lexington, KY |

3 | 886 | 4,266 | 4,047 | 5.4 | % | 1,249 | 1,223 | 2.1 | % | 3,017 | 2,824 | 6.8 | % | 96.9 | % | 96.8 | % | 0.1 | % | 1,484 | 1,397 | 6.2 | % | ||||||||||||||||||||||||||||||||||||||||||

|

Huntsville, AL |

4 | 1,051 | 4,712 | 4,951 | (4.8 | )% | 1,747 | 1,744 | 0.2 | % | 2,965 | 3,207 | (7.5 | )% | 95.3 | % | 96.0 | % | (0.7 | )% | 1,418 | 1,481 | (4.3 | )% | ||||||||||||||||||||||||||||||||||||||||||

|

Memphis, TN |

3 | 883 | 4,184 | 4,267 | (1.9 | )% | 1,332 | 1,491 | (10.7 | )% | 2,852 | 2,776 | 2.7 | % | 95.3 | % | 94.7 | % | 0.6 | % | 1,559 | 1,599 | (2.5 | )% | ||||||||||||||||||||||||||||||||||||||||||

|

Charlotte, NC |

3 | 714 | 3,671 | 3,787 | (3.1 | )% | 1,230 | 1,201 | 2.4 | % | 2,440 | 2,586 | (5.6 | )% | 95.7 | % | 95.9 | % | (0.2 | )% | 1,681 | 1,732 | (2.9 | )% | ||||||||||||||||||||||||||||||||||||||||||

|

Louisville, KY |

3 | 794 | 3,502 | 3,412 | 2.6 | % | 1,380 | 1,355 | 1.8 | % | 2,122 | 2,057 | 3.2 | % | 96.2 | % | 96.3 | % | (0.1 | )% | 1,332 | 1,282 | 3.9 | % | ||||||||||||||||||||||||||||||||||||||||||

|

Cincinnati, OH |

2 | 542 | 3,043 | 2,899 | 5.0 | % | 1,115 | 1,100 | 1.4 | % | 1,929 | 1,798 | 7.3 | % | 96.6 | % | 97.2 | % | (0.6 | )% | 1,693 | 1,621 | 4.4 | % | ||||||||||||||||||||||||||||||||||||||||||

|

Charleston, SC |

2 | 518 | 2,841 | 2,762 | 2.9 | % | 1,141 | 1,196 | (4.6 | )% | 1,701 | 1,566 | 8.6 | % | 94.0 | % | 96.2 | % | (2.2 | )% | 1,788 | 1,722 | 3.8 | % | ||||||||||||||||||||||||||||||||||||||||||

|

Myrtle Beach, SC - Wilmington, NC |

3 | 628 | 2,657 | 2,720 | (2.3 | )% | 972 | 939 | 3.5 | % | 1,686 | 1,782 | (5.4 | )% | 95.5 | % | 95.6 | % | (0.1 | )% | 1,388 | 1,410 | (1.6 | )% | ||||||||||||||||||||||||||||||||||||||||||

|

Greenville, SC |

1 | 702 | 2,765 | 2,663 | 3.8 | % | 1,083 | 1,056 | 2.6 | % | 1,682 | 1,607 | 4.7 | % | 92.3 | % | 95.2 | % | (2.9 | )% | 1,321 | 1,303 | 1.4 | % | ||||||||||||||||||||||||||||||||||||||||||

|

Orlando, FL |

1 | 297 | 1,719 | 1,690 | 1.7 | % | 671 | 686 | (2.2 | )% | 1,048 | 1,004 | 4.4 | % | 96.7 | % | 96.0 | % | 0.7 | % | 1,811 | 1,785 | 1.5 | % | ||||||||||||||||||||||||||||||||||||||||||

|

Austin, TX |

1 | 256 | 1,454 | 1,406 | 3.4 | % | 564 | 596 | (5.4 | )% | 890 | 810 | 9.9 | % | 95.2 | % | 94.2 | % | 1.0 | % | 1,797 | 1,801 | (0.2 | )% | ||||||||||||||||||||||||||||||||||||||||||

|

San Antonio, TX |

1 | 306 | 1,445 | 1,420 | 1.8 | % | 579 | 612 | (5.4 | )% | 866 | 808 | 7.2 | % | 96.7 | % | 97.4 | % | (0.7 | )% | 1,462 | 1,456 | 0.4 | % | ||||||||||||||||||||||||||||||||||||||||||

|

Total / Weighted Average |

105 | 30,502 | $ | 150,573 | $ | 148,430 | 1.4 | % | $ | 55,183 | $ | 55,590 | (0.7 | )% | $ | 95,390 | $ | 92,840 | 2.7 | % | 95.3 | % | 95.4 | % | (0.1 | )% | $ | 1,581 | $ | 1,571 | 0.6 | % | ||||||||||||||||||||||||||||||||||

SAME-STORE PORTFOLIO NET OPERATING INCOME BY MARKET

nine MONTHS ENDED September 30, 2025

Dollars in thousands, except rent per unit

|

Rental and Other Property Revenue |

Property Operating Expenses |

Net Operating Income |

Average Occupancy |

Average Effective Monthly Rent per Unit |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Market |

Number of Properties |

Units |

2025 |

2024 |

% Change |

2025 |

2024 |

% Change |

2025 |

2024 |

% Change |

2025 |

2024 |

% Change |

2025 |

2024 |

% Change |

|||||||||||||||||||||||||||||||||||||||||||||||||

|

Atlanta, GA |

13 | 5,180 | $ | 73,228 | $ | 72,710 | 0.7 | % | $ | 28,875 | $ | 29,215 | (1.2 | )% | $ | 44,351 | $ | 43,496 | 2.0 | % | 93.5 | % | 93.5 | % | 0.0 | % | $ | 1,592 | $ | 1,610 | (1.1 | )% | ||||||||||||||||||||||||||||||||||

|

Dallas, TX |

14 | 4,007 | 67,163 | 66,628 | 0.8 | % | 25,557 | 25,714 | (0.6 | )% | 41,606 | 40,914 | 1.7 | % | 96.0 | % | 95.2 | % | 0.8 | % | 1,812 | 1,816 | (0.2 | )% | ||||||||||||||||||||||||||||||||||||||||||

|

Columbus, OH |

10 | 2,510 | 35,594 | 33,553 | 6.1 | % | 13,881 | 12,988 | 6.9 | % | 21,714 | 20,566 | 5.6 | % | 95.7 | % | 94.9 | % | 0.8 | % | 1,529 | 1,458 | 4.9 | % | ||||||||||||||||||||||||||||||||||||||||||

|

Oklahoma City, OK |

8 | 2,147 | 25,485 | 24,514 | 4.0 | % | 8,639 | 8,432 | 2.5 | % | 16,846 | 16,082 | 4.8 | % | 96.1 | % | 95.2 | % | 0.9 | % | 1,248 | 1,206 | 3.5 | % | ||||||||||||||||||||||||||||||||||||||||||

|

Indianapolis, IN |

7 | 1,979 | 26,737 | 26,268 | 1.8 | % | 10,164 | 9,858 | 3.1 | % | 16,573 | 16,410 | 1.0 | % | 95.7 | % | 96.1 | % | (0.4 | )% | 1,455 | 1,398 | 4.1 | % | ||||||||||||||||||||||||||||||||||||||||||

|

Tampa-St. Petersburg, FL |

5 | 1,503 | 26,066 | 24,930 | 4.6 | % | 9,522 | 9,134 | 4.2 | % | 16,543 | 15,795 | 4.7 | % | 96.0 | % | 92.8 | % | 3.2 | % | 1,859 | 1,836 | 1.3 | % | ||||||||||||||||||||||||||||||||||||||||||

|

Nashville, TN |

5 | 1,508 | 22,793 | 22,711 | 0.4 | % | 7,237 | 7,737 | (6.5 | )% | 15,556 | 14,974 | 3.9 | % | 95.7 | % | 95.1 | % | 0.6 | % | 1,620 | 1,635 | (0.9 | )% | ||||||||||||||||||||||||||||||||||||||||||

|

Raleigh - Durham, NC |

6 | 1,690 | 24,352 | 24,100 | 1.0 | % | 9,115 | 9,032 | 0.9 | % | 15,238 | 15,068 | 1.1 | % | 95.1 | % | 94.9 | % | 0.2 | % | 1,548 | 1,551 | (0.2 | )% | ||||||||||||||||||||||||||||||||||||||||||

|

Denver, CO |

5 | 1,093 | 18,365 | 18,456 | (0.5 | )% | 5,739 | 5,790 | (0.9 | )% | 12,626 | 12,666 | (0.3 | )% | 95.0 | % | 96.4 | % | (1.4 | )% | 1,802 | 1,768 | 1.9 | % | ||||||||||||||||||||||||||||||||||||||||||

|

Houston, TX |

5 | 1,308 | 17,897 | 17,673 | 1.3 | % | 7,381 | 7,979 | (7.5 | )% | 10,517 | 9,694 | 8.5 | % | 96.3 | % | 95.7 | % | 0.6 | % | 1,443 | 1,433 | 0.7 | % | ||||||||||||||||||||||||||||||||||||||||||

|

Huntsville, AL |

4 | 1,051 | 14,238 | 14,655 | (2.8 | )% | 5,219 | 5,174 | 0.9 | % | 9,019 | 9,482 | (4.9 | )% | 95.5 | % | 95.4 | % | 0.1 | % | 1,432 | 1,486 | (3.6 | )% | ||||||||||||||||||||||||||||||||||||||||||

|

Lexington, KY |

3 | 886 | 12,472 | 11,791 | 5.8 | % | 3,653 | 3,659 | (0.2 | )% | 8,819 | 8,132 | 8.4 | % | 96.7 | % | 97.0 | % | (0.3 | )% | 1,451 | 1,360 | 6.7 | % | ||||||||||||||||||||||||||||||||||||||||||

|

Memphis, TN |

3 | 883 | 12,687 | 12,697 | (0.1 | )% | 4,161 | 4,452 | (6.5 | )% | 8,526 | 8,245 | 3.4 | % | 95.1 | % | 94.6 | % | 0.5 | % | 1,581 | 1,590 | (0.6 | )% | ||||||||||||||||||||||||||||||||||||||||||

|

Charlotte, NC |

3 | 714 | 11,116 | 11,369 | (2.2 | )% | 3,642 | 3,597 | 1.3 | % | 7,473 | 7,772 | (3.8 | )% | 95.8 | % | 95.4 | % | 0.4 | % | 1,701 | 1,741 | (2.3 | )% | ||||||||||||||||||||||||||||||||||||||||||

|

Louisville, KY |

3 | 794 | 10,339 | 9,977 | 3.6 | % | 4,055 | 3,978 | 1.9 | % | 6,284 | 5,999 | 4.8 | % | 96.4 | % | 95.8 | % | 0.6 | % | 1,308 | 1,266 | 3.3 | % | ||||||||||||||||||||||||||||||||||||||||||

|

Cincinnati, OH |

2 | 542 | 8,879 | 8,499 | 4.5 | % | 3,284 | 3,204 | 2.5 | % | 5,595 | 5,294 | 5.7 | % | 96.7 | % | 96.2 | % | 0.5 | % | 1,663 | 1,603 | 3.7 | % | ||||||||||||||||||||||||||||||||||||||||||

|

Myrtle Beach, SC - Wilmington, NC |

3 | 628 | 7,998 | 8,151 | (1.9 | )% | 2,803 | 2,721 | 3.0 | % | 5,195 | 5,430 | (4.3 | )% | 95.2 | % | 95.2 | % | 0.0 | % | 1,387 | 1,411 | (1.7 | )% | ||||||||||||||||||||||||||||||||||||||||||

|

Charleston, SC |

2 | 518 | 8,402 | 8,204 | 2.4 | % | 3,342 | 3,478 | (3.9 | )% | 5,061 | 4,725 | 7.1 | % | 94.8 | % | 96.2 | % | (1.4 | )% | 1,771 | 1,704 | 3.9 | % | ||||||||||||||||||||||||||||||||||||||||||

|

Greenville, SC |

1 | 702 | 8,061 | 7,948 | 1.4 | % | 3,153 | 3,104 | 1.6 | % | 4,908 | 4,844 | 1.3 | % | 93.0 | % | 94.3 | % | (1.3 | )% | 1,290 | 1,306 | (1.2 | )% | ||||||||||||||||||||||||||||||||||||||||||

|

Orlando, FL |

1 | 297 | 5,103 | 4,993 | 2.2 | % | 2,007 | 2,146 | (6.5 | )% | 3,096 | 2,847 | 8.7 | % | 96.5 | % | 94.6 | % | 1.9 | % | 1,805 | 1,794 | 0.6 | % | ||||||||||||||||||||||||||||||||||||||||||

|

Austin, TX |

1 | 256 | 4,283 | 4,239 | 1.0 | % | 1,736 | 1,788 | (2.9 | )% | 2,547 | 2,451 | 3.9 | % | 95.5 | % | 94.6 | % | 0.9 | % | 1,796 | 1,804 | (0.4 | )% | ||||||||||||||||||||||||||||||||||||||||||

|

San Antonio, TX |

1 | 306 | 4,284 | 4,293 | (0.2 | )% | 1,756 | 1,829 | (4.0 | )% | 2,528 | 2,464 | 2.6 | % | 97.3 | % | 96.9 | % | 0.4 | % | 1,447 | 1,469 | (1.5 | )% | ||||||||||||||||||||||||||||||||||||||||||

|

Total/Weighted Average |

105 | 30,502 | $ | 445,542 | $ | 438,359 | 1.6 | % | $ | 164,921 | $ | 165,009 | (0.1 | )% | $ | 280,621 | $ | 273,350 | 2.7 | % | 95.4 | % | 95.0 | % | 0.4 | % | $ | 1,577 | $ | 1,563 | 0.9 | % | ||||||||||||||||||||||||||||||||||

CONSOLIDATED PROPERTY PORTFOLIO (a)

NET OPERATING INCOME EXPOSURE BY MARKET

Dollars in thousands, except rent per unit

|

For the Three Months Ended |

||||||||||||||||||||||||||||

|

September 30, 2025 |

||||||||||||||||||||||||||||

|

Market |

Number of Properties |

Units |

Gross Real Estate Assets |

Period of Occupancy |

Average Effective Monthly Rent per Unit |

NOI |

% of NOI |

|||||||||||||||||||||

|

Atlanta, GA |

13 | 5,180 | $ | 1,127,199 | 95.0 | % | $ | 1,582 | $ | 15,136 | 14.4 | % | ||||||||||||||||

|

Dallas, TX |

14 | 4,007 | 894,828 | 96.0 | % | 1,811 | 14,101 | 13.4 | % | |||||||||||||||||||

|

Columbus, OH |

10 | 2,510 | 385,920 | 96.0 | % | 1,538 | 7,409 | 7.2 | % | |||||||||||||||||||

|

Tampa-St. Petersburg, FL |

6 | 1,791 | 398,604 | 95.7 | % | 1,924 | 6,823 | 6.5 | % | |||||||||||||||||||

|

Indianapolis, IN |

8 | 2,259 | 360,891 | 95.0 | % | 1,477 | 6,387 | 6.1 | % | |||||||||||||||||||

|

Denver, CO (a)(b)(c) |

7 | 1,722 | 489,720 | 93.5 | % | 1,811 | 6,303 | 6.0 | % | |||||||||||||||||||

|

Nashville, TN |

5 | 1,508 | 379,015 | 96.0 | % | 1,617 | 5,734 | 5.5 | % | |||||||||||||||||||

|

Oklahoma City, OK |

8 | 2,147 | 345,498 | 96.7 | % | 1,260 | 5,687 | 5.4 | % | |||||||||||||||||||

|

Raleigh - Durham, NC |

6 | 1,690 | 258,498 | 94.2 | % | 1,544 | 5,196 | 4.9 | % | |||||||||||||||||||

|

Memphis, TN (c) |

4 | 1,383 | 160,635 | 90.7 | % | 1,478 | 3,860 | 3.7 | % | |||||||||||||||||||

|

Houston, TX |

5 | 1,308 | 217,545 | 96.9 | % | 1,446 | 3,687 | 3.5 | % | |||||||||||||||||||

|

Orlando, FL |

4 | 1,260 | 282,928 | 89.0 | % | 1,899 | 3,551 | 3.4 | % | |||||||||||||||||||

|

Charlotte, NC |

4 | 1,014 | 263,359 | 95.4 | % | 1,672 | 3,498 | 3.3 | % | |||||||||||||||||||

|

Lexington, KY |

3 | 886 | 167,612 | 97.7 | % | 1,485 | 3,017 | 2.9 | % | |||||||||||||||||||

|

Louisville, KY (c) |

4 | 1,150 | 143,874 | 95.3 | % | 1,367 | 2,981 | 2.8 | % | |||||||||||||||||||

|

Huntsville, AL |

4 | 1,051 | 242,661 | 95.4 | % | 1,416 | 2,942 | 2.8 | % | |||||||||||||||||||

|

Cincinnati, OH |

2 | 542 | 127,053 | 97.4 | % | 1,676 | 1,929 | 1.8 | % | |||||||||||||||||||

|

Charleston, SC |

2 | 518 | 83,676 | 95.3 | % | 1,776 | 1,701 | 1.6 | % | |||||||||||||||||||

|

Myrtle Beach, SC - Wilmington, NC |

3 | 628 | 69,636 | 96.2 | % | 1,387 | 1,686 | 1.6 | % | |||||||||||||||||||

|

Greenville, SC |

1 | 702 | 127,593 | 95.1 | % | 1,282 | 1,682 | 1.6 | % | |||||||||||||||||||

|

Austin, TX |

1 | 256 | 61,425 | 94.1 | % | 1,806 | 890 | 0.8 | % | |||||||||||||||||||

|

San Antonio, TX |

1 | 306 | 57,685 | 97.7 | % | 1,440 | 866 | 0.8 | % | |||||||||||||||||||

|

Total / Weighted Average |

115 | 33,818 | $ | 6,645,855 | 95.1 | % | $ | 1,593 | $ | 105,066 | 100.0 | % | ||||||||||||||||

|

(a) |

Excludes our development project Flatiron Flats. See the definitions at the end of this release. |

|

(b) |

Includes properties in our Fort Collins, CO and Colorado Springs, CO markets. |

| (c) | Includes one property that was held for sale as of September 30, 2025. |

PROJECT LIFE TO DATE AS OF September 30, 2025

| Total | Total Units To Be | Units | Units | Rent Premium | % Rent | Renovation Costs per Unit (b) | ROI - Interior Costs | ROI - Total Costs | ||||||||||||||||||||||||||||||||||||

|

Market |

Properties |

Renovated |

Complete |

Leased |

(a) |

Increase |

Interior |

Exterior |

Total |

(c) |

(c) |

|||||||||||||||||||||||||||||||||

|

ONGOING |

||||||||||||||||||||||||||||||||||||||||||||

|

Atlanta, GA |

8 | 3,678 | 1,619 | 1,599 | $ | 226 | 16.6 | % | $ | 18,594 | $ | 2,815 | $ | 21,409 | 14.6 | % | 12.7 | % | ||||||||||||||||||||||||||

|

Dallas, TX |

7 | 1,925 | 851 | 858 | 300 | 20.7 | % | 19,651 | 2,316 | 21,967 | 18.3 | % | 16.4 | % | ||||||||||||||||||||||||||||||

|

Oklahoma City, OK |

5 | 1,430 | 688 | 681 | 183 | 18.2 | % | 17,288 | 2,204 | 19,492 | 12.7 | % | 11.2 | % | ||||||||||||||||||||||||||||||

|

Columbus, OH |

4 | 1,098 | 742 | 741 | 252 | 20.1 | % | 15,267 | 1,431 | 16,698 | 19.8 | % | 18.1 | % | ||||||||||||||||||||||||||||||

|

Denver, CO |

2 | 492 | 164 | 161 | 284 | 22.0 | % | 14,231 | 3,089 | 17,320 | 23.9 | % | 19.7 | % | ||||||||||||||||||||||||||||||

|

Raleigh-Durham, NC |

2 | 489 | 63 | 51 | 264 | 19.3 | % | 19,334 | 2,669 | 22,003 | 16.4 | % | 14.4 | % | ||||||||||||||||||||||||||||||

|

Indianapolis, IN |

2 | 460 | 19 | 25 | 254 | 17.6 | % | 19,833 | 2,783 | 22,616 | 15.4 | % | 13.5 | % | ||||||||||||||||||||||||||||||

|

Lexington, KY |

1 | 436 | 164 | 163 | 352 | 29.8 | % | 17,792 | 2,038 | 19,830 | 23.8 | % | 21.3 | % | ||||||||||||||||||||||||||||||

|

Nashville, TN |

1 | 418 | 325 | 328 | 177 | 12.9 | % | 17,378 | 1,321 | 18,699 | 12.2 | % | 11.3 | % | ||||||||||||||||||||||||||||||

|

Tampa-St. Petersburg, FL |

1 | 348 | 287 | 279 | 323 | 22.2 | % | 16,946 | 1,875 | 18,821 | 22.9 | % | 20.6 | % | ||||||||||||||||||||||||||||||

|

Charleston, SC |