Item 1. |

Reports to Stockholders. |

|

Closed-End Funds |

December 31, 2025 |

Nuveen

Closed-End Funds

| Nuveen Multi-Asset Income Fund |

NMAI | |

| Nuveen Real Asset Income and Growth Fund |

JRI | |

| Nuveen Real Estate Income Fund |

JRS | |

Annual

Report

IMPORTANT DISTRIBUTION NOTICE

for Shareholders of the Nuveen Real Estate Income Fund (JRS)

Annual Shareholder Report for the period ending December 31, 2025

The Nuveen Real Estate Income Fund (JRS) seek to offer attractive cash flow to its shareholders, by converting the expected long-term total return potential of the Fund’s investments in REITs into regular quarterly distributions. Following is a discussion of the Managed Distribution Policy the Fund uses to achieve this.

The Fund pays quarterly common share distributions that seek to convert the Fund’s expected long-term total return potential into regular cash flow. As a result, the Fund’s regular common share distributions (presently $0.1700 per share) may be derived from a variety of sources, including:

| • | distributions from portfolio companies (REITs), |

| • | realized capital gains or, |

| • | Possibly, returns of capital representing in certain cases unrealized capital appreciation. |

Such distributions are sometimes referred to as “managed distributions.” The Fund seeks to establish a distribution rate that roughly corresponds to the Adviser’s projections of the total return that could reasonably be expected to be generated by the Fund over an extended period of time. The Adviser may consider many factors when making such projections, including, but not limited to, long-term historical returns for the asset classes in which the Fund invests. As portfolio and market conditions change, the distribution amount and distribution rate on the Common Shares under the Fund’s Managed Distribution Policy could change.

When it pays a distribution, the Fund provides holders of its Common Shares a notice of the estimated sources of the Fund’s distributions (i.e., what percentage of the distributions is estimated to constitute ordinary income, short-term capital gains, long-term capital gains, and/or a non-taxable return of capital) on a year-to-date basis. It does this by posting the notice on its website (www.nuveen.com/cef), and by sending it in written form.

You should not draw any conclusions about the Fund’s investment performance from the amount of this distribution or from the terms of the Fund’s Managed Distribution Policy. The Fund’s actual financial performance will likely vary from month-to-month and from year-to-year, and there may be extended periods when the distribution rate will exceed the Fund’s actual total returns. The Managed Distribution Policy provides that the Board may amend or terminate the Policy at any time without prior notice to Fund shareholders. There are presently no reasonably foreseeable circumstances that might cause the Fund to terminate its Managed Distribution Policy.

2 |

Table

of Contents

4 |

||||

5 |

||||

10 |

||||

13 |

||||

14 |

||||

22 |

||||

23 |

||||

71 |

||||

72 |

||||

73 |

||||

75 |

||||

78 |

||||

81 |

||||

97 |

||||

135 |

||||

137 |

||||

138 |

||||

139 |

||||

3 |

Important Notices

NMAI - Portfolio manager updates:

Effective January 7, 2026, Mark Zheng, CFA, James Kim and John Tribolet were added as portfolio managers of the Fund and Nathan Shetty and Anurag Dugar were removed as portfolio manager of the Fund. JRI - Portfolio manager updates:

Effective February 11, 2025, James Kim has been added as a portfolio manager of the Fund. Effective April 1, 2025, Jean Lin retired and is no longer a portfolio manager of the Fund. JRI – Rights Offering:

On January 15, 2026, the Board approved the terms of the issuance of Rights to the holders of the Fund’s Common Shares as of February 6, 2026 (the “Record Date”). Holders of Rights will be entitled to subscribe for additional Common shares (the “Offer”) at a discount to the market price of the Common Shares. After considering a number of factors, including potential benefits and costs, the Board and the Adviser, determined that the Offer will benefit both the Fund and its common shareholders and increase the assets of the Fund available to take advantage of existing investment opportunities, consistent with the Fund’s investment objective of providing shareholders with a high level of current income and long-term capital appreciation.

Certain key terms of the Offer include:

• Holders of Common Shares on the Record Date (“Record Date Shareholders”) will receive one Right for each outstanding Common Share owned on the Record Date. The Rights entitle the holders to purchase one new Common Share for every four Rights held (1-for-4).

• The subscription price per Common Share (the “Subscription Price”) will be determined based upon a formula equal to 95% of the average of the last reported sales price of the Common Shares on the NYSE on the Expiration Date and each of the four preceding trading days (the “Formula Price”). If, however, the Formula Price is less than 90% of the net asset value per Common Share at the close of trading on the NYSE on the Expiration Date, then the Subscription Price will be 90% of the Fund’s net asset value per Common Share at the close of trading on the NYSE on the Expiration Date. The Rights offering will expire at 5:00 p.m., Eastern time, on March 9, 2026 (the “Expiration Date”).

• Record Date Shareholders who fully exercise all Rights issued to them can subscribe, subject to certain limitations and allotment, for any additional Common Shares which were not subscribed for by other holders of Rights at the Subscription Price, subject to the right of the Board to eliminate this over-subscription privilege. Investors who are not Record Date Shareholders but who otherwise acquire Rights in the secondary market are not entitled to participate in the over-subscription privilege. If these requests exceed available Common Shares, they will be allocated pro rata among those fully exercising Record Date Shareholders who over-subscribe based on the number of Rights originally issued to them by the Fund.

• Rights are transferable and were admitted for trading on the NYSE under the symbol “JRI RTWI” initially trading “when-issued” on February 5, 2026. The Rights then began trading with regular settlement under the symbol “JRI RT” on February 10, 2026, and will cease trading at the close on March 6, 2026, one day before the Offer’s Expiration Date. During this time, Record Date Shareholders may also choose to sell their Rights.

More details about the Fund’s rights offering are available on www.nuveen.com/cef.

4 |

Discussion of Fund Performance

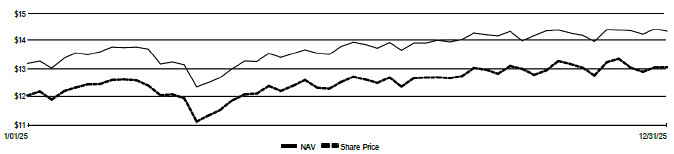

Nuveen Multi-Asset Income Fund (NMAI)

Nuveen Real Asset Income and Growth Fund (JRI)

Nuveen Real Estate Income Fund (JRS)

The Nuveen Multi-Asset Income Fund (NMAI) features features portfolio management by Nuveen Asset Management, LLC (NAM), Teachers Advisors, LLC (TAL) and Winslow Capital Management LLC (Winslow). NAM, TAL and Winslow each serve as a sub-adviser to the Fund and are each an affiliate of Nuveen Fund Advisors, LLC, the Fund’s investment adviser. Subsequent to the close of the reporting period, effective January 7, 2026, the Fund’s portfolio managers are Mark Zheng, CFA, FRM, James Kim and John Tribolet.

The Nuveen Real Asset Income and Growth Fund (JRI) features portfolio management by Nuveen Asset Management, LLC (NAM), an affiliate of Nuveen Fund Advisors, LLC, the Fund’s investment adviser. The Fund’s portfolio managers are Tryg Sarsland, Brenda Langenfeld, CFA, Benjamin Kerl, Noah Hauser, CFA and James Kim.

The Nuveen Real Estate Income Fund (JRS) features portfolio management by a team of real estate investment professionals at Security Capital Research & Management Incorporated (Security Capital), a wholly owned subsidiary of JPMorgan Chase & Company. Anthony Manno Jr., Kevin Bedell and Nathan Gear, CFA, lead the investment and portfolio management team.

Below is a discussion of Fund performance and the factors that contributed and detracted during the 12-month reporting period ended December 31, 2025. For more information on each Fund’s investment objectives and policies, please refer to the Shareholder Update section at the end of the report.

Nuveen Multi-Asset Income Fund (NMAI)

What factors affected markets during the reporting period?

| • | Global equities posted healthy gains in 2025, led by non-U.S. developed markets, with emerging markets performing nearly as well. Both topped U.S. shares, as measured by the S&P 500 Index, by double digits for the first time since 2006, driven partly by a weaker U.S. dollar. In the U.S., large-cap growth stocks outperformed large-cap value. |

| • | U.S. Treasury yields broadly fell and the yield curve steepened during the reporting period. Intermediate-duration fixed income assets generally outperformed shorter-duration assets of similar credit rating, while very long-dated fixed income instruments underperformed. Additionally, the anticipation and announcements of tariffs by the U.S. on its trading partners contributed to volatility in April 2025 and weakened the U.S. dollar. |

| • | Credit spreads tightened during the reporting period. High-yield bonds, emerging markets debt, and preferred securities outperformed investment-grade bonds, while senior loans lagged. |

What key strategies were used to manage the Fund during the reporting period?

| • | The Fund seeks to provide attractive total return through high current income and capital appreciation. The Fund dynamically invests in a portfolio of equity and debt securities of issuers located around the world. |

| • | During the first quarter 2025, the Fund reduced its interest rates exposure by trimming the allocations to emerging markets debt and TIPS (Treasury inflation-protected securities), while increasing exposure to floating-rate loans. Additionally, after having reduced the equity exposure around mid-February 2025 via real assets and international developed stocks, the Fund added back some equity exposure in March 2025 via U.S. large-cap value and dividend growth stocks. |

| • | Early in the second quarter 2025, the Fund increased exposure to U.S. dividend growth stocks to take advantage of the April sell-off and began to wind down the Fund’s call overwriting overlay. Later in the quarter, the Fund reduced exposure to public real assets – both U.S. real estate investment trusts (REITs) and global infrastructure stocks – and to emerging markets equities, while increasing exposure to core U.S. and international developed market equities. In fixed income, the Fund reduced the floating-rate loans, preferred securities and mortgage-backed securities (MBS) allocations and increased the core bond and high yield bond allocations. |

5 |

Discussion of Fund Performance (continued)

| • | After September’s strong interest rate rally, the Fund reduced exposure to MBS and added an allocation to energy infrastructure master limited partnerships (MLPs), which helped lower the Fund’s interest rate sensitivity while enhancing the expected portfolio yield. |

| • | In the fourth quarter 2025, the Fund reduced exposure to floating-rate senior loans and increased allocation to equities as the Federal Reserve cut interest rates. |

How did the Fund perform and what factors affected relative performance?

For the 12-month reporting period ended December 31, 2025, NMAI returned 19.23%. The Fund outperformed the returns of the NMAI Blended Benchmark, which returned 15.16%. The NMAI Blended Benchmark, effective June 17, 2025, consists of 1) 50% MSCI ACWI Index (Net), 2) 35% Bloomberg U.S. Corporate high Yield Bond Index and 3) 15% Bloomberg U.S. Aggregate Bond Index. Prior to June 17, 2025, the NMAI Blended Benchmark consisted of 1) 50% MSCI ACWI (Net), and 2) 50% Bloomberg U.S. Corporate high Yield Bond Index.

Top contributors to relative performance

| • | The Fund’s use of leverage through bank borrowings and reverse repurchase agreements. |

| • | Within equities, an overweight allocation to international equities. |

| • | Within fixed income, an out-of-benchmark allocation to preferred securities. |

Top detractors from relative performance

| • | Within equities, an overweight allocation to U.S. equities. |

| • | Within fixed income, an overweight allocation to U.S. investment-grade bonds |

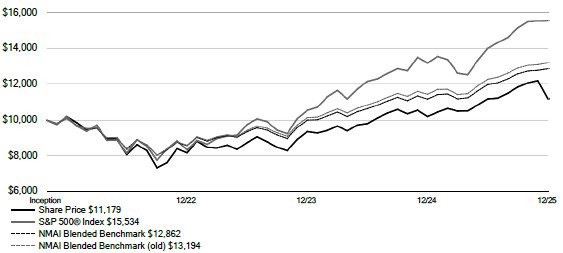

Nuveen Real Asset Income and Growth Fund (JRI)

What factors affected markets during the reporting period?

| • | The U.S. economy continued to expand, and pricing pressures generally eased, but inflation remained higher than the central bank’s 2% target. The labor market began to show signs of weakening toward the end of the reporting period. |

| • | Most global central banks continued to ease monetary policy. After holding steady throughout the first eight months of 2025, the Federal Reserve lowered rates by 25 basis points in September, October and December, bringing the federal funds rate to a range of 3.50%-3.75%. |

| • | In the United States, rates fell across all but the longest 30-year segment of the Treasury yield curve, but more so at the short end, causing the yield curve to steepen. The 10-year U.S. Treasury yield ended the reporting period 40 basis points lower at 4.18%. |

| • | Of the five segments within the JRI Blended Benchmark, global infrastructure common equities performed best during the reporting period, followed by the real estate common equity segment. |

| • | High yield bonds also rallied throughout the reporting period due to stronger-than-expected U.S. economic growth and consumer spending that supported credit spreads. |

| • | Despite looser monetary policy, the rate-sensitive real estate preferred securities sector within the JRI Blended Benchmark underperformed during the reporting period. |

6 |

What key strategies were used to manage the Fund during the reporting period?

| • | The Fund generally maintained a more defensive posture throughout its portfolio given ongoing geopolitical risks, along with uncertainty surrounding global growth, inflation and interest rates. The portfolio management team favored sectors that tend to have more resilient business models and greater earnings visibility, while also maintaining some cyclical exposure. |

| • | In the equity portion of the Fund, global infrastructure common shares represented the Fund’s largest overweight. Exposure increased in the more defensive and essential electric utilities sector because of these companies’ more visible cash flows and earnings, and importance in fulfilling the increased demand for power to develop generative artificial intelligence (AI). |

| • | Real estate common equity exposure also remained a modest overweight. Much of this sector continued to be attractive from a valuation standpoint relative to the broader equity market after underperforming due to higher interest rates. |

| • | The debt portion of the Fund remained an overweight at the end of the reporting period because of the potential for continued stock market volatility following three straight years of strong equity market advances. Additionally, the debt segment of the capital structure continued to offer attractive yields and pricing. |

| • | Within the debt portfolio, the portfolio management team made some opportunistic additions in commercial mortgage-backed securities (CMBS), largely due to relatively attractive spreads in the sector. While the majority of the Fund’s debt exposure remained in high yield bonds, the portfolio management team maintained modest exposure to higher-quality, investment-grade credits to allow for broader sector diversification than what was available in the high yield market. |

| • | The Fund maintained underweight exposures to preferred securities throughout the reporting period. Real estate preferreds remained the Fund’s largest underweight due to much lighter issuance and tight spreads in the sector. Global infrastructure preferreds also remained an underweight, with purchases focused on $1000 par institutional securities and hybrid structures within the group. |

| • | The portfolio management team maintained the Fund’s overweight to U.S. versus non-U.S. exposure throughout the reporting period because it found incrementally more attractive opportunities in the United States. |

How did the Fund perform and what factors affected relative performance?

For the 12-month reporting period ended December 31, 2025, JRI returned 14.15%. The Fund outperformed the returns of the JRI Blended Benchmark, which returned 10.82%. The JRI Blended Benchmark consists of 1) 25% FTSE EPRA Nareit Developed Index (Net), 2) 22% S&P Global Infrastructure Index (Net), 3) 20% ICE Hybrid & Preferred Infrastructure 7% Issuer Constrained Custom Index, 4) 13% FTSE Nareit Preferred Stock Index and 5) 20% Bloomberg U.S. Corporate High Yield Bond Index.

Top contributors to relative performance

| • | Security selection in real estate common equity, led by industrial companies, including an overweight position in LXP Industrial Trust. |

| • | Security selection in the gas utilities sector within the global infrastructure common equity segment, led by an out-of-benchmark position in Snam S.p.A. |

| • | An overweight to the electric transmission sector within the global infrastructure common equity segment, led by an overweight to National Grid. |

| • | An underweight to real estate preferred securities, including an underweight to hotel real estate investment trust (REIT) preferreds. |

7 |

Discussion of Fund Performance (continued)

| • | The Fund’s use of leverage through bank borrowings. In addition, the Fund’s use of leverage was accretive to overall common share income. |

Top detractors from relative performance

| • | An underweight to the airport sector within the global infrastructure common equity segment. |

| • | Security selection and an overweight position in real asset debt, including overweights to the rail, pipeline and technology infrastructure sectors. |

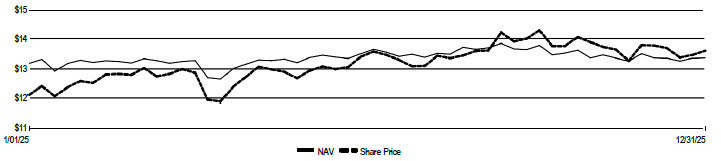

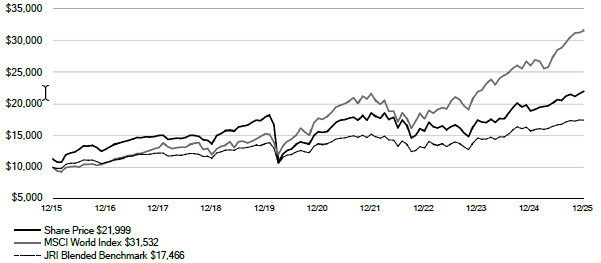

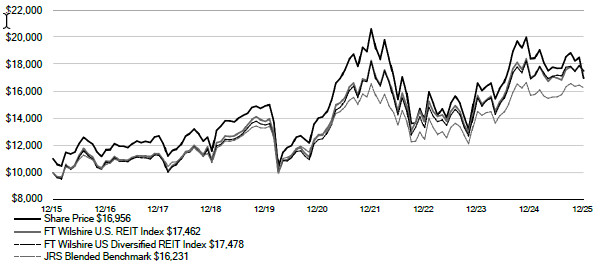

Nuveen Real Estate Income Fund (JRS)

What factors affected markets during the reporting period?

| • | The U.S. economy continued to expand, and pricing pressures generally eased, but inflation remained higher than the central bank’s 2% target. The labor market began to show signs of weakening toward the end of the reporting period. |

| • | Most global central banks continued to ease monetary policy. After holding rates steady throughout the first eight months of 2025, the Federal Reserve lowered rates three times between September and December, bringing the federal funds rate to a range of 3.50%-3.75%. |

| • | In the United States, rates fell across all but the longest 30-year segment of the Treasury yield curve, but more so at the short end, causing the curve to steepen over the reporting period. The 10-year U.S. Treasury yield ended the year 40 basis points lower at 4.18%. |

| • | Despite looser monetary policy, the real estate sector underperformed broader equity markets in 2025. Economic uncertainty and still-elevated interest rates hampered new real estate development, while investors favored technology-focused companies more closely tied to artificial intelligence (AI) spending throughout the reporting period. |

What key strategies were used to manage the Fund during the reporting period?

| • | The portfolio management team sought to maintain significant property type and geographic diversification while considering company credit quality and security type allocations. |

| • | Investment decisions were based on a multi-layered analysis of the company, the real estate it owns, its management and the relative price of the security. |

| • | The portfolio management team used fundamental security research to identify securities that it believed would be best positioned to generate sustainable income and potential price appreciation. |

| • | To manage risk at the portfolio level during the reporting period, the team continued to adjust the Fund’s exposures in common equity versus preferred securities, senior unsecured bonds, and cash. In general, during times of strong economic growth, the portfolio management team increased the Fund’s allocation to common equity. In less certain times, the portfolio management team tended to increase the Fund’s allocation toward preferred securities. |

How did the Fund perform and what factors affected relative performance?

For the 12-month reporting period ended December 31, 2025, JRS returned -1.70%. The Fund underperformed the returns of the JRS Blended Benchmark, which returned 3.44%. The JRS Blended Benchmark consists of 1) 60% FT Wilshire U.S. REIT Index and 2) 40% FTSE Nareit Preferred Stock Index.

8 |

Top contributors to relative performance

| • | An overweight to health care company Ventas Inc. |

| • | An overweight to industrial company First Industrial Realty Trust. |

Top detractors from relative performance

| • | An underweight to health care REIT Welltower Inc. |

| • | An overweight to Alexandria Real Estate Equities Inc. |

| • | An overweight to Healthpeak Properties Inc. |

| • | The Fund’s use of leverage through bank borrowings. |

This material is not intended to be a recommendation or investment advice, does not constitute a solicitation to buy, sell or hold a security or an investment strategy, and is not provided in a fiduciary capacity. The information provided does not take into account the specific objectives or circumstances of any particular investor, or suggest any specific course of action. Investment decisions should be made based on an investor’s objectives and circumstances and in consultation with his or her advisors.

Certain statements in this report are forward-looking statements. Discussions of specific investments are for illustration only and are not intended as recommendations of individual investments. The forward-looking statements and other views expressed herein are those of the portfolio managers as of the date of this report. Actual future results or occurrences may differ significantly from those anticipated in any forward-looking statements, and the views expressed herein are subject to change at any time, due to numerous market and other factors. The Funds disclaim any obligation to update publicly or revise any forward-looking statements or views expressed herein.

Each Fund uses credit quality ratings for its portfolio securities provided by Moody’s Investors Service, Inc. (Moody’s), Standard & Poor’s (S&P) and Fitch, Inc. (Fitch). For NMAI, if all three of Moody’s, S&P, and Fitch provide a rating for a security, the middle rating is used; if two of the three agencies rate a security, the lower rating is used; and if only one rating agency rates a security, that rating is used. For JRI and JRS, the highest rating given by Moody’s, S&P and Fitch is used. This treatment of split-rated securities may differ from that used for other purposes, such as for Fund investment policies. AAA, AA, A, and BBB are investment grade ratings; BB, B, CCC/CC/C and D are below-investment grade ratings. Holdings designated N/R are not rated by these national rating agencies.

Refer to the Glossary of Terms Used in this Report for further definition of the terms used within this section.

9 |

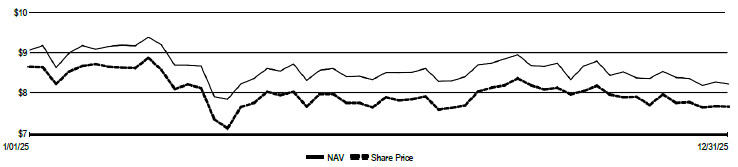

Common Share Information

NMAI and JRI DISTRIBUTION INFORMATION

The following information regarding the distributions for NMAI and JRI are as of December 31, 2025, the Funds’ fiscal and tax year end, and may differ from previously issued distribution notices.

Each Fund’s distribution policy, which may be changed by the Board, is to make regular monthly cash distributions to holders of its common shares (stated in terms of a fixed cents per common share dividend distribution rate which may be set from time to time). Each Fund intends to distribute all or substantially all of its net investment income each year through its regular monthly distribution and to distribute realized capital gains at least annually. In addition, in any monthly period, to maintain its declared per common share distribution amount, Each Fund may distribute more or less than its net investment income during the period. In the event a Fund distributes more than its net investment income during any yearly period, such distributions may also include realized gains and/or a return of capital. To the extent that a distribution includes a return of capital the NAV per share may erode. The practice of maintaining a stable distribution level had no material effect on the Fund’s investment strategy during the most recent fiscal period and is not expected to have such an effect in future periods, however, distributions in excess of Fund returns will cause its NAV per share to erode. For additional information, refer to the distribution information section below and in the Notes to Financial Statements herein.

The following table provides the sources of distributions and may include amounts attributed to realized gains and/or returns of capital. A return of capital may occur, for example, when some or all of the money that you invested in a Fund is paid back to you. A return of capital distribution does not necessarily reflect a Fund’s investment performance and should not be confused with “yield” or “income.” The Funds attribute these estimates equally to each regular distribution throughout the year.

The amounts and sources of distributions reported in this notice are for financial reporting purposes and are not being provided for tax reporting purposes. The actual amounts and character of the distributions for tax reporting purposes will be reported to shareholders on Form 1099-DIV, which will be sent to shareholders shortly after calendar year-end. Because distribution source estimates are updated throughout the current fiscal year based on the Fund’s performance, those estimates may differ from both the tax information reported to you in your Fund’s 1099 statement, as well as the ultimate economic sources of distributions over the life of your investment. The figures in the table below provide the sources of distributions and may include amounts attributed to realized gains and/or returns of capital. More details about the Fund’s distributions are available on www.nuveen.com/en-us/closed-end-funds.

Data as of December 31, 2025

Per Share Sources of Distribution |

Percentage of Distributions |

|||||||||||||||||||||||||||||||||||

Per Share Distribution |

Net Investment Income |

Long-Term Gains |

Short-Term Gains |

Return of Capital |

Net Investment Income |

Long-Term Gains |

Short-Term Gains |

Return of Capital |

||||||||||||||||||||||||||||

| NMAI (FYE 12/31) |

||||||||||||||||||||||||||||||||||||

| Current Distribution |

$ |

0.1160 |

$ |

0.0357 |

$ |

0.0000 |

$ |

0.0000 |

$ |

0.0803 |

30.80 |

% |

0.00 |

% |

0.00 |

% |

69.20 |

% | ||||||||||||||||||

| Fiscal YTD |

$ |

1.2895 |

$ |

0.3973 |

$ |

0.0000 |

$ |

0.0000 |

$ |

0.8922 |

30.80 |

% |

0.00 |

% |

0.00 |

% |

69.20 |

% | ||||||||||||||||||

| JRI (FYE 12/31) |

||||||||||||||||||||||||||||||||||||

| Current Distribution |

$ |

0.1335 |

$ |

0.0681 |

$ |

0.0000 |

$ |

0.0000 |

$ |

0.0654 |

51.00 |

% |

0.00 |

% |

0.00 |

% |

49.00 |

% | ||||||||||||||||||

| Fiscal YTD |

$ |

1.6020 |

$ |

0.8166 |

$ |

0.0000 |

$ |

0.0000 |

$ |

0.7854 |

51.00 |

% |

0.00 |

% |

0.00 |

% |

49.00 |

% | ||||||||||||||||||

JRS DISTRIBUTION INFORMATION

The following 19(a) Notice presents JRS’s most current distribution information as of December 31, 2025 as required by certain exempted regulatory relief the Fund has received.

Because the ultimate tax character of your distributions depends on the Fund’s performance for its entire fiscal year (which is the calendar year for the Fund) as well as certain fiscal year-end (FYE) tax adjustments, estimated distribution source information you receive with each distribution may differ from the tax information reported to you on your Fund’s IRS Form 1099 statement.

10 |