Please wait

| | | | | | | | | | | |

REPORT TO SHAREHOLDERS | | |

Year ended December 31, 2025 | |

| | | |

| MANAGEMENT'S DISCUSSION AND ANALYSIS | |

| | | |

| | | |

Table of Contents | | | |

| | | |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| | | |

| | | |

| | | |

Basis of Presentation

The following Management's Discussion and Analysis ("MD&A") of the financial and operating results of Pembina Pipeline Corporation ("Pembina" or the "Company") is dated February 26, 2026, and is supplementary to, and should be read in conjunction with, Pembina's audited consolidated financial statements as at and for the year ended December 31, 2025 ("Consolidated Financial Statements"). The Consolidated Financial Statements have been prepared in accordance with International Financial Reporting Standards ("IFRS") as issued by the International Accounting Standards Board, using the accounting policies described in Note 3 of the Consolidated Financial Statements. All dollar amounts contained in this MD&A are expressed in Canadian dollars unless otherwise noted. For further details on Pembina and Pembina's significant assets, including definitions for capitalized terms used herein and not otherwise defined, refer to Pembina's annual information form ("AIF") for the year ended December 31, 2025. Additional information about Pembina filed with Canadian and U.S. securities commissions, including quarterly and annual reports, annual information forms (filed with the U.S. Securities and Exchange Commission under Form 40-F) and management information circulars, can be found online at www.sedarplus.ca, www.sec.gov and through Pembina's website at www.pembina.com. Information contained in or otherwise accessible through Pembina's website does not form part of this MD&A and is not incorporated into this document by reference.

Abbreviations

For a list of abbreviations that may be used in this MD&A, refer to the "Abbreviations" section of this MD&A.

Non-GAAP and Other Financial Measures

Pembina has disclosed certain financial measures and ratios within this MD&A that management believes provide meaningful information in assessing Pembina's underlying performance, but which are not specified, defined or determined in accordance with the Canadian generally accepted accounting principles ("GAAP") and which are not disclosed in Pembina's Consolidated Financial Statements. Such non-GAAP financial measures and non-GAAP ratios do not have any standardized meaning prescribed by IFRS and may not be comparable to similar financial measures or ratios disclosed by other issuers. Refer to the "Non-GAAP & Other Financial Measures" section of this MD&A for additional information regarding these non-GAAP financial measures and non-GAAP ratios.

Risk Factors and Forward-Looking Information

Management has identified the primary risk factors that could have a material impact on the financial results and operations of Pembina. Such risk factors are presented in the "Risk Factors" section of this MD&A and are also included in Pembina's AIF. The Company's financial and operational performance is potentially affected by a number of factors, including, but not limited to, the factors described within the "Forward-Looking Statements & Information" section of this MD&A. This MD&A contains forward-looking statements based on Pembina's current expectations, estimates, projections and assumptions. This information is provided to assist readers in understanding the Company's future plans and expectations and may not be appropriate for other purposes.

Pembina Pipeline Corporation 2025 Annual Report 1

1. ABOUT PEMBINA

Pembina Pipeline Corporation is a leading energy transportation and midstream service provider that has served North America's energy industry for more than 70 years. Pembina owns an extensive network of strategically located assets, including hydrocarbon liquids and natural gas pipelines, gas gathering and processing facilities, oil and natural gas liquids infrastructure and logistics services, and an export terminals business. Through our integrated value chain, we seek to provide safe and reliable energy solutions that connect producers and consumers across the world, support a more sustainable future and benefit our customers, investors, employees and communities. For more information, please visit www.pembina.com.

Pembina's Purpose and Strategy

We deliver extraordinary energy solutions so the world can thrive.

Pembina will build on its strengths by continuing to invest in and grow the core businesses that provide critical transportation and midstream services to help ensure reliable and secure energy supply. Pembina will capitalize on exciting opportunities to leverage its assets and expertise into new service offerings that enable the transition to a lower-carbon economy. In continuing to meet global energy demand and its customers' needs, while ensuring Pembina's long-term success and resilience, the Company has established four strategic priorities:

1.To be resilient, we will sustain, decarbonize, and enhance our businesses. This priority is focused on strengthening and growing our existing franchise and demonstrating environmental leadership.

2.To thrive, we will invest in the energy transition to improve the basins in which we operate. We will prioritize lighter commodities as we continue to invest in new infrastructure and expand our portfolio to include new businesses associated with lower-carbon commodities.

3.To meet global demand, we will transform and export our products. We will continue our focus on supporting the transformation of Western Canadian Sedimentary Basin commodities into higher margin products and enabling more coastal egress.

4.To set ourselves apart, we will create a differentiated experience for our stakeholders. We remain committed to delivering excellence for our four key stakeholder groups meaning that:

a.Employees say we are the 'employer of choice' and value our safe, respectful, collaborative, and inclusive work culture.

b.Communities welcome us and recognize the net positive impact of our social and environmental commitment.

c.Customers choose us first for reliable and value-added services.

d.Investors receive sustainable industry-leading total returns.

2 Pembina Pipeline Corporation 2025 Annual Report

2. FINANCIAL & OPERATING OVERVIEW

Consolidated Financial Overview for the Three Months Ended December 31

Results of Operations

| | | | | | | | | | | | |

| ($ millions, except where noted) | 2025 | 2024 | Change | |

| Revenue | 1,913 | | 2,145 | | (232) | | |

Net revenue(1) | 1,139 | | 1,383 | | (244) | | |

| Operating expenses | 241 | | 270 | | (29) | | |

Gross profit | 827 | | 1,024 | | (197) | | |

Adjusted EBITDA(1) | 1,075 | | 1,254 | | (179) | | |

| | | | |

Earnings | 489 | | 572 | | (83) | | |

Earnings per common share – basic and diluted (dollars) | 0.78 | | 0.92 | | (0.14) | | |

| | | | |

| Cash flow from operating activities | 861 | | 902 | | (41) | | |

Cash flow from operating activities per common share – basic (dollars) | 1.48 | | 1.55 | | (0.07) | | |

Adjusted cash flow from operating activities(1) | 731 | | 922 | | (191) | | |

Adjusted cash flow from operating activities per common share – basic (dollars)(1) | 1.26 | | 1.59 | | (0.33) | | |

| Capital expenditures | 235 | | 242 | | (7) | | |

| | | | |

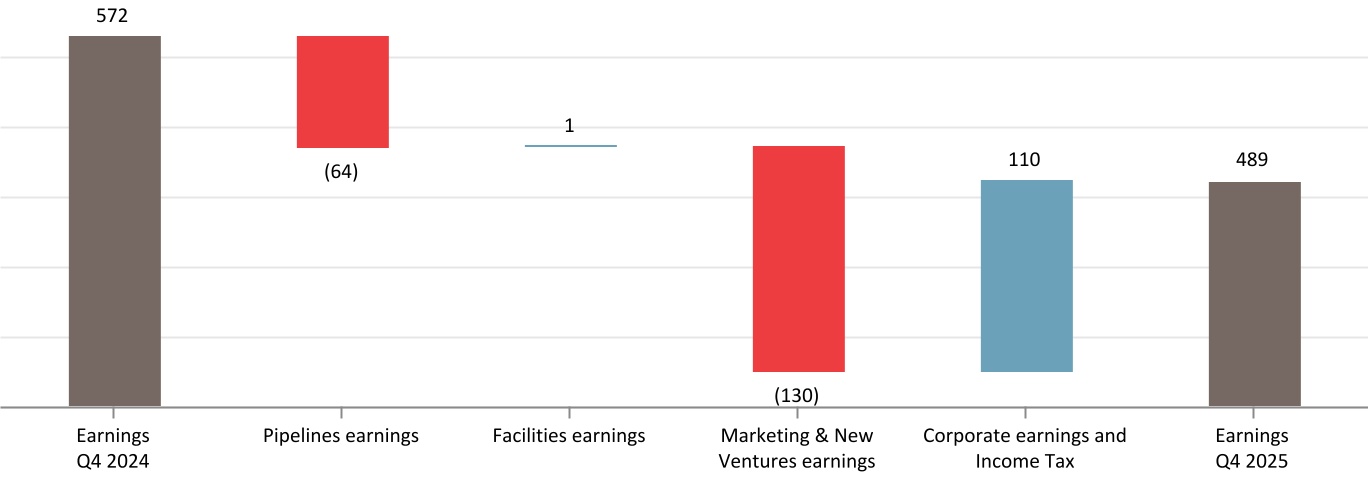

Change in Earnings ($ millions)

Earnings Overview

Earnings in the fourth quarter of 2025 decreased by $83 million compared to the prior period. The change primarily reflects narrower WCSB and U.S. NGL frac spreads as well as lower revenue from derivative contracts within the Marketing & New Ventures Division. Results also include the impact of a new toll structure and revenue sharing mechanism on the Alliance Pipeline, and period specific capital recoveries that impacted the fourth quarter of 2024 with no similar impact in the same period in 2025. These factors were offset by a gain on a land sale recognized within the Corporate and Marketing & New Ventures Division, as well as volume growth and solid performance across the Pipelines and Facilities Divisions. Further details by division are outlined below:

•Pipelines: Decrease largely due to lower revenue on the Canadian portion of the Alliance Pipeline as a result of reduced long-term firm tolls and impacts from the new revenue-sharing mechanism resulting from the negotiated settlement between Alliance and its shippers effective November 2025 ("Alliance Negotiated Settlement"), partially offset by higher seasonal revenue on the Alliance Pipeline. Lower earnings was also due to the recognition of period specific capital recoveries that impacted certain Pipelines assets in the fourth quarter of 2024 with no similar impact in the same period in 2025, lower volumes on the Cochin Pipeline, and higher depreciation and amortization expense. These decreases were offset in part by higher revenue on the Peace Pipeline system and lower operating expenses on the Cochin Pipeline.

•Facilities: Consistent with prior period as a higher share of profit from PGI due to an increase in contributions from certain PGI assets was largely offset by minor decreases in revenue across certain other Facilities assets.

Pembina Pipeline Corporation 2025 Annual Report 3

•Marketing & New Ventures: Decrease primarily due to lower net revenue as a result of narrower WCSB and U.S. NGL frac spreads in the fourth quarter of 2025 compared to the same period in 2024, lower net revenue from risk management and other derivative contracts primarily due to an unrealized loss on the embedded derivative arising from the Cedar LNG capacity commercial arrangement entered into during the fourth quarter of 2025, combined with lower unrealized gains recognized by Cedar LNG, partially offset by a higher share of profit from Greenlight due to a gain on the sale of land to a third-party potential customer.

•Corporate and Income Tax: Higher largely due to a gain on the sale of land to a third-party potential customer of Greenlight in the fourth quarter of 2025, combined with lower net finance costs, income tax expense, as well as acquisition and integration costs, partially offset by higher long-term incentive and restructuring costs.

Adjusted EBITDA(1) Overview

Adjusted EBITDA in the fourth quarter of 2025 decreased by $179 million compared to the prior period. The change primarily reflects a lower contribution from the Marketing & New Ventures Division, the impact of a new toll structure and revenue sharing mechanism on the Alliance Pipeline, and period specific capital recoveries that impacted 2024 with no similar impact in 2025, partially offset by volume growth and solid performance across the Pipelines and Facilities Divisions. Further details by division are outlined below:

•Pipelines: Decrease largely due to lower revenue on the Canadian portion of the Alliance Pipeline as a result of the Alliance Negotiated Settlement, partially offset by higher seasonal revenue on the Alliance Pipeline. Lower results were also due to period specific capital recoveries that impacted certain Pipelines assets in the fourth quarter of 2024 with no similar impact in the same period in 2025 and lower volumes on the Cochin Pipeline. These decreases were offset in part by higher revenue on the Peace Pipeline system and lower operating expenses on the Cochin Pipeline.

•Facilities: Consistent with prior period. Higher contributions from certain PGI assets due to an increase in volumes and the positive impact of PGI's acquisition of a 50 percent working interest in Whitecap Resources Inc.'s ("Whitecap") Kaybob Complex in the fourth quarter of 2024, were largely offset by lower revenue due to period specific capital recoveries that impacted certain PGI assets in the fourth quarter of 2024 with no similar impact in the same period in 2025 and minor decreases in revenue across certain other Facilities assets.

•Marketing & New Ventures: Decrease primarily due to narrower WCSB and U.S. NGL frac spreads in the fourth quarter of 2025 compared to the same period in 2024 and lower realized gains on crude oil-based derivatives due to lower volumes and narrower crude oil price spreads, partially offset by realized gains on NGL-based derivatives in the fourth quarter of 2025 compared to losses in the same period in 2024.

•Corporate: Lower primarily due to higher long-term incentive costs, partially offset by lower non-compensation related general and administrative costs.

Further details and additional factors impacting earnings and adjusted EBITDA by divisions are discussed in the "Segment Results" section of this MD&A.

Cash Flow Measures

| | | | | | |

For the Three Months Ended December 31 |

| | |

| | |

| | |

| | |

| | |

| | |

| Cash flow from operating activities | | $41 million decrease, primarily driven by lower earnings adjusted for items not involving cash and higher taxes paid, partially offset by the change in non-cash operating working capital primarily driven by movements in trade accounts receivable resulting from commodity price and volume fluctuations, as well as higher distributions received from equity accounted investees. |

Adjusted cash flow from operating activities(1) | | $191 million decrease, primarily due to the same items impacting cash flow from operating activities, discussed above, excluding the change in non-cash working capital and taxes paid, combined with higher current income tax expense and accrued share-based payment expense. |

Adjusted cash flow from operating activities per common share – basic (dollars)(1) | | $0.33 decrease, primarily due to the factors impacting adjusted cash flow from operating activities, discussed above, while outstanding common shares remained consistent with prior period. |

| | |

| | |

(1) Refer to the "Non-GAAP & Other Financial Measures" section of this MD&A.

4 Pembina Pipeline Corporation 2025 Annual Report

Consolidated Financial Overview for the Twelve Months Ended December 31

Results of Operations

| | | | | | | | | | | | |

| ($ millions, except where noted) | 2025 | 2024 | Change | |

| Revenue | 7,778 | | 7,384 | | 394 | | |

Net revenue(1) | 4,877 | | 4,776 | | 101 | | |

| Operating expenses | 961 | | 976 | | (15) | | |

Gross profit | 3,193 | | 3,316 | | (123) | | |

Adjusted EBITDA(1) | 4,289 | | 4,408 | | (119) | | |

| | | | |

Earnings | 1,694 | | 1,874 | | (180) | | |

Earnings per common share – basic (dollars) | 2.67 | | 3.00 | | (0.33) | | |

Earnings per common share – diluted (dollars) | 2.66 | | 3.00 | | (0.34) | | |

| Cash flow from operating activities | 3,301 | | 3,214 | | 87 | | |

Cash flow from operating activities per common share – basic (dollars) | 5.68 | | 5.61 | | 0.07 | | |

Adjusted cash flow from operating activities(1) | 2,854 | | 3,265 | | (411) | | |

Adjusted cash flow from operating activities per common share – basic (dollars)(1) | 4.91 | | 5.70 | | (0.79) | | |

| Capital expenditures | 784 | | 955 | | (171) | | |

| | | | |

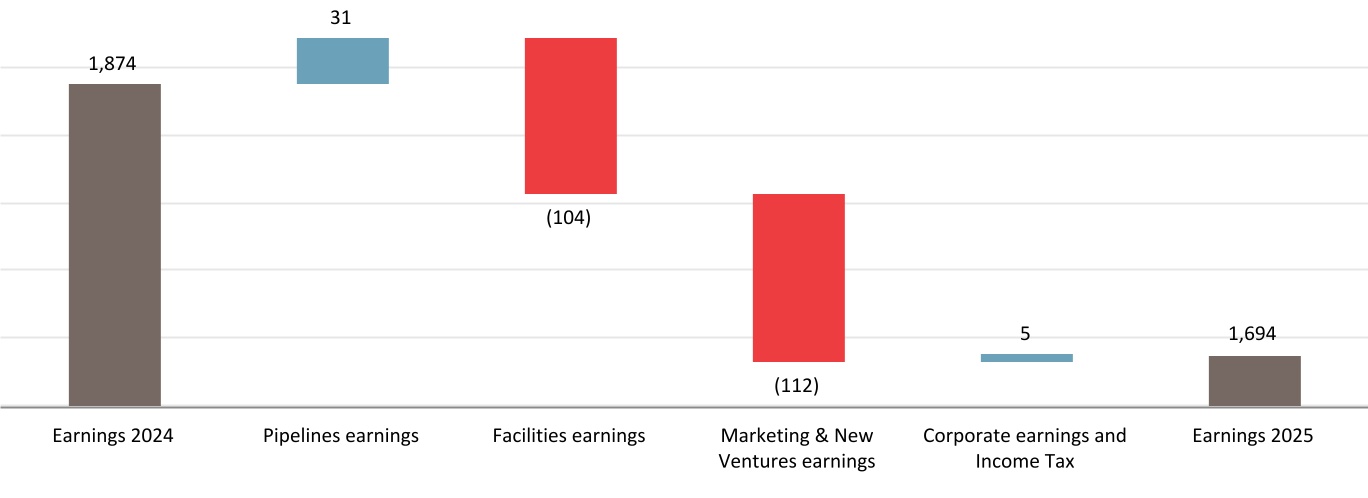

Change in Earnings ($ millions)

Earnings Overview

Earnings during 2025 decreased by $180 million compared to the prior year. The change primarily reflects narrower WCSB and U.S. NGL frac spreads, impairment recognized within PGI share of profit, the impact of a new toll structure and revenue sharing mechanism on the Alliance Pipeline, and period specific capital recoveries that impacted 2024 with no similar impact in 2025. These factors were partially offset by gains recognized within each division and higher revenue from derivative contracts within the Marketing & New Ventures Division, as well as volume growth and solid performance across the Pipelines and Facilities Divisions. Further details by division are outlined below:

•Pipelines: Increase largely due to the positive impacts from Pembina acquiring a controlling ownership interest in Alliance on April 1, 2024, combined with higher seasonal revenue, partially offset by the impacts of the Alliance Negotiated Settlement. Additionally, earnings were impacted by higher revenue on the Peace Pipeline system due to increased volumes and higher tolls mainly related to contractual inflation adjustments, higher revenue on the Nipisi Pipeline, and the recognition of a gain on the sale of the North segment of the Western Pipeline in the third quarter of 2025. These impacts were partially offset by lower net revenue on the Cochin Pipeline, Vantage Pipeline, and at the Edmonton Terminals, along with a decrease in revenue on certain Pipeline assets due to period specific capital recoveries that impacted 2024 with no similar impact in 2025, as well as higher depreciation and amortization expense.

•Facilities: Decrease largely due to lower share of profit from PGI primarily due to an impairment of certain PGI assets and higher depreciation and amortization expense. These results were partially offset by the positive impacts of Pembina acquiring a controlling ownership interest in Aux Sable on April 1, 2024, the recognition of a gain following the amendment of PGI's credit facility, and higher contributions from certain PGI assets.

Pembina Pipeline Corporation 2025 Annual Report 5

•Marketing & New Ventures: Lower primarily due to narrower WCSB and U.S. NGL frac spreads in 2025 compared to 2024 and lower other income, partially offset by the positive impacts from Pembina acquiring a controlling ownership interest in Aux Sable on April 1, 2024, a higher share of profit from Greenlight due to a gain on the sale of land to a third-party potential customer in the fourth quarter of 2025, and higher revenue from risk management and other derivative contracts.

•Corporate and Income Tax: Consistent with prior year. A gain on the sale of land to a third-party potential customer of Greenlight in the fourth quarter of 2025 combined with lower acquisition and integration costs compared to those incurred in 2024, were largely offset by higher income tax expense, net finance costs, general and administrative expenses, and restructuring costs, along with no similar net gain on acquisition to that recognized in the second quarter of 2024 following Pembina acquiring a controlling ownership interest in Alliance and Aux Sable on April 1, 2024.

Adjusted EBITDA(1) Overview

Adjusted EBITDA during 2025 decreased by $119 million compared to the prior year. The change primarily reflects lower contribution from the Marketing & New Ventures Division, the impact of a new toll structure and revenue sharing mechanism on the Alliance Pipeline, and period specific capital recoveries that impacted 2024 with no similar impact in 2025. These factors were partially offset by volume growth and solid performance across the Pipelines and Facilities Divisions. Further details by division are outlined below:

•Pipelines: Positive impacts from Pembina acquiring a controlling ownership interest in Alliance on April 1, 2024, combined with higher seasonal revenue, partially offset by the impacts of the Alliance Negotiated Settlement. Additionally, earnings were impacted by higher revenue on the Peace Pipeline system due to increased volumes and higher tolls mainly related to contractual inflation adjustments, higher revenue on the Nipisi Pipeline, and the recognition of a gain on the sale of the North segment of the Western Pipeline in the third quarter of 2025. These impacts were partially offset by lower net revenue on the Cochin Pipeline, Vantage Pipeline, and at the Edmonton Terminals, along with a decrease in revenue on certain Pipeline assets due to period specific capital recoveries that impacted 2024 with no similar impact in 2025.

•Facilities: Increase largely due to the net positive impacts from Pembina acquiring a controlling ownership interest in Aux Sable on April 1, 2024, combined with higher contributions from certain PGI assets related to an increase in volumes and the net impact of PGI's acquisition of a 50 percent working interest in Whitecap's Kaybob Complex and PGI’s acquisition of Whitecap's Gold Creek and Karr oil batteries in the fourth quarter of 2024 (collectively, the "Whitecap Transactions"). These increases were partially offset by lower volumes at certain PGI assets due to outages in 2025 and third-party downstream restrictions.

•Marketing & New Ventures: Decrease primarily due to narrower NGL frac spreads in 2025 compared to 2024 and lower realized gains on crude oil-based derivatives due to lower volumes and narrower crude oil price spreads. These decreases were partially offset by the net positive impacts from Pembina acquiring a controlling ownership interest in Aux Sable on April 1, 2024 and lower realized losses on NGL-based derivatives.

•Corporate: Consistent with prior year. Higher incentive costs as well as salaries and wages were largely offset by lower other expenses.

Further details and additional factors impacting on earnings and adjusted EBITDA by divisions are discussed in the "Segment Results" section of this MD&A.

Cash Flow Metrics

| | | | | | |

For the Twelve Months Ended December 31 |

| | |

| | |

| | |

| | |

| | |

| Cash flow from operating activities | | $87 million increase, primarily driven by the change in non-cash operating working capital largely driven by movements in trade accounts receivable resulting from commodity price and volume fluctuations and lower taxes paid. These increases were partially offset by lower distributions received from equity accounted investees and higher net interest paid, both largely the result of Pembina acquiring a controlling ownership interest in Alliance and Aux Sable on April 1, 2024, as well as the net change in contract liabilities. |

Adjusted cash flow from operating activities(1) | | $411 million decrease, primarily driven by the same factors impacting cash flow from operating activities, discussed above. However, when excluding the change in non-cash working capital and taxes paid, the adjusted result reflects a decrease. The decrease was further impacted by higher current income tax expense. |

Adjusted cash flow from operating activities per common share – basic (dollars)(1) | | $0.79 decrease, primarily due to the factors impacting adjusted cash flow from operating activities, discussed above, as well as an increase in outstanding common shares following the conversion of subscription receipts into common shares, concurrent with the closing of Pembina's acquisition of a controlling ownership interest in Alliance and Aux Sable on April 1, 2024. |

| | |

| | |

(1) Refer to the "Non-GAAP & Other Financial Measures" section of this MD&A.

6 Pembina Pipeline Corporation 2025 Annual Report

3. SEGMENT RESULTS

Business Overview

The Pipelines Division provides customers with pipeline transportation, terminalling, and storage in key market hubs in Canada and the United States for crude oil, condensate, natural gas liquids and natural gas. Through Pembina's wholly-owned and joint venture assets, the Pipelines Division manages pipeline transportation capacity of approximately 3.0 mmboe/d(1) and above ground storage capacity of approximately 10 mmbbls(1) within its conventional, oil sands and heavy oil, and transmission assets. The conventional assets include strategically located pipelines and terminalling hubs that gather and transport light and medium crude oil, condensate and natural gas liquids from western Alberta and northeast British Columbia to downstream pipelines and processing facilities in the Edmonton, Alberta area. The oil sands and heavy oil assets transport heavy and synthetic crude oil produced within Alberta to the Edmonton, Alberta area and offer associated storage and terminalling services. The transmission assets transport natural gas, ethane and condensate throughout Canada and the United States on long haul pipelines linking various key market hubs. In addition, the Pipelines Division assets provide linkages to Pembina's Facilities Division assets across North America, enabling flexibility and optionality in the Company's customer service offerings. Together, these assets supply products from hydrocarbon producing regions to refineries, fractionators and market hubs in Alberta, British Columbia, and Illinois, as well as other regions throughout North America.

The Facilities Division includes infrastructure that provides Pembina's customers with natural gas, condensate and NGL services. Through its wholly-owned assets and its interest in PGI, Pembina's natural gas gathering and processing facilities are strategically positioned in active, liquids-rich areas of the WCSB and Williston Basin and may be serviced by the Company's other businesses. Pembina provides its customers with sweet and sour gas gathering, compression, condensate stabilization, and both shallow cut and deep cut gas processing services with a total capacity of approximately 6.7 bcf/d(1). Condensate and NGL extracted at virtually all Canadian-based facilities have access to transportation on Pembina's pipelines. In addition, all NGL transported along the Alliance Pipeline are extracted through the Channahon Facility at the terminus. The Facilities Division includes approximately 430 mbpd(1) of NGL fractionation capacity, 21 mmbbls(1) of cavern storage capacity, various oil batteries, associated pipeline and rail terminalling facilities and a liquefied propane export facility on Canada's West Coast. These facilities are accessible to Pembina's other strategically-located assets and pipeline systems, providing customers with flexibility and optionality to access a comprehensive suite of services to enhance the value of their hydrocarbons. In addition, Pembina owns a bulk marine import/export terminal in Vancouver, British Columbia.

The Marketing & New Ventures Division leverages Pembina's integrated value chain and existing network of pipelines, facilities, and energy infrastructure assets to maximize the value of hydrocarbon liquids and natural gas originating in the basins where the Company operates. Pembina pursues the creation of new markets, and further enhances existing markets, to support both the Company's and its customers' business interests. In particular, Pembina seeks to identify opportunities to connect hydrocarbon production to new demand locations through the development of infrastructure. The division also focuses on developing new business platforms and undertaking initiatives that seek to reduce the GHG emissions of Pembina's and its customers' operations.

Within the Marketing & New Ventures Division, Pembina undertakes value-added commodity marketing activities, including buying and selling products (natural gas, ethane, propane, butane, condensate, crude oil, electricity, and carbon credits), commodity arbitrage, and optimizing storage opportunities. The marketing business enters into contracts for capacity on both Pembina's and third-party infrastructure, handles proprietary and customer volumes and aggregates production for onward sale. Through this infrastructure capacity, including Pembina's Prince Rupert Terminal and 30,000 bdp of export capacity secured at AltaGas' Ridley Island facilities, as well as utilizing the Company's expansive rail fleet and logistics capabilities, Pembina's marketing business adds incremental value to the commodities by accessing high value markets across North America and globally.

The Marketing & New Ventures Division is also responsible for the development of new large-scale, or value chain extending projects, including those that provide enhanced access to global markets and support a transition to a lower-carbon economy. Currently, Pembina is pursuing opportunities associated with LNG, natural gas-fired power generation, and large-scale GHG emissions reductions.

(1)Net capacity.

Pembina Pipeline Corporation 2025 Annual Report 7

Financial and Operational Overview by Division

| | | | | | | | | | | | | | | | | | | | | | | | |

| 3 Months Ended December 31 |

| 2025 | 2024 |

($ millions, except where noted) | Volumes(1) | Earnings (loss) | | | Adjusted EBITDA(2) | Volumes(1) | Earnings (loss) | | | Adjusted EBITDA(2) |

| Pipelines | 2,815 | | 470 | | | | 643 | | 2,790 | | 534 | | | | 686 | |

| Facilities | 898 | | 178 | | | | 366 | | 877 | | 177 | | | | 373 | |

Marketing & New Ventures | 337 | | 115 | | | | 116 | | 349 | | 245 | | | | 234 | |

| Corporate | — | | (126) | | | | (50) | | — | | (212) | | | | (39) | |

| | | | | | | | | | |

| Income tax expense | — | | (148) | | | | — | | — | | (172) | | | | — | |

| Total | | 489 | | | | 1,075 | | | 572 | | | | 1,254 | |

| | | | | | | | | | |

| |

| | |

| | | | | | | | | | |

| | | | | | | | | | |

| | | | | | | | | | |

| | | | | | | | | | |

| | | | | | | | | | |

| | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | |

| 12 Months Ended December 31 |

| 2025 | 2024 |

($ millions, except where noted) | Volumes(1) | Earnings (loss) | | | Adjusted EBITDA(2) | Volumes(1) | Earnings (loss) | | | Adjusted EBITDA(2) |

| Pipelines | 2,786 | | 1,938 | | | | 2,596 | | 2,711 | | 1,907 | | | | 2,533 | |

| Facilities | 871 | | 562 | | | | 1,396 | | 837 | | 666 | | | | 1,347 | |

Marketing & New Ventures | 339 | | 457 | | | | 499 | | 327 | | 569 | | | | 724 | |

| Corporate | — | | (750) | | | | (202) | | — | | (1,422) | | | | (196) | |

| | | | | | | | | | |

| Income tax (expense) recovery | — | | (513) | | | | — | | — | | 154 | | | | — | |

| Total | | 1,694 | | | | 4,289 | | | 1,874 | | | | 4,408 | |

| | | | | | | | | | |

| |

| | |

| | | | | | | | | | |

| | | | | | | | | | |

| | | | | | | | | | |

| | | | | | | | | | |

| | | | | | | | | | |

| | | | | | | | | | |

(1) Volumes in mboe/d. See the "Abbreviations" section of this MD&A for definition. Volumes for Pipelines and Facilities divisions are revenue volumes, which are physical volumes plus volumes recognized from take-or-pay commitments. Volumes for Marketing & New Ventures are marketed crude oil and NGL volumes.

(2) Refer to the "Non-GAAP & Other Financial Measures" section of this MD&A.

Equity Accounted Investees Overview by Division

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| 3 Months Ended December 31 |

| | | | |

| 2025 | 2024 |

| ($ millions, except where noted) | Share of profit | Adjusted EBITDA(5) | Contributions | Distributions | Volumes(6) | Share of profit | Adjusted EBITDA(5) | Contributions | Distributions | Volumes(6) |

Pipelines(1) | 1 | | 1 | | — | | — | | — | | — | | — | | — | | — | | — | |

Facilities(2) | 74 | | 200 | | 45 | | 148 | | 386 | | 59 | | 195 | | — | | 131 | | 358 | |

| | | | | | | | | | |

| | | | | | | | | | |

| | | | | | | | | | |

Marketing & New Ventures(3) | 96 | | (1) | | 82 | | — | | — | | 74 | | — | | — | | — | | — | |

| Total | 171 | | 200 | | 127 | | 148 | | 386 | | 133 | | 195 | | — | | 131 | | 358 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| 12 Months Ended December 31 |

| | | | |

| 2025 | 2024 |

| ($ millions, except where noted) | Share of profit | Adjusted EBITDA(5) | Contributions | Distributions | Volumes(6) | Share of profit | Adjusted EBITDA(5) | Contributions | Distributions | Volumes(6) |

| | | | | | | | | | |

| | | | | | | | | | |

| | | | | | | | | | |

Pipelines(1)(4) | 1 | | 4 | | — | | — | | — | | 42 | | 88 | | 5 | | 80 | | 37 | |

| | | | | | | | | | |

| | | | | | | | | | |

| | | | | | | | | | |

Facilities(2) | 134 | | 744 | | 243 | | 544 | | 364 | | 231 | | 717 | | 124 | | 515 | | 358 | |

| | | | | | | | | | |

| | | | | | | | | | |

| | | | | | | | | | |

| | | | | | | | | | |

Marketing & New Ventures(3)(4) | 74 | | (4) | | 168 | | — | | — | | 55 | | 39 | | 242 | | 31 | | 9 | |

| Total | 209 | | 744 | | 411 | | 544 | | 364 | | 328 | | 844 | | 371 | | 626 | | 404 | |

(1) Pipelines includes Grand Valley.

(2) Facilities includes PGI and Fort Corp.

(3) Marketing and New Ventures includes Greenlight in 2025, Cedar LNG and ACG.

(4) For the comparative 2024 period, the results of Alliance and Aux Sable are equity-accounted for the first quarter of 2024. Pembina owned a 50 percent interest in Alliance, an approximately 42.7 percent interest in Aux Sable's U.S operations, and a 50 percent interest in Aux Sable's Canadian operations up to the closing of the acquisition on April 1, 2024. Following the closing of the acquisition, the results of Alliance and Aux Sable are fully consolidated and incorporated into Pembina's financial results.

(5) Refer to the "Non-GAAP & Other Financial Measures" section of this MD&A.

(6) Volumes in mboe/d. See the "Abbreviations" section of this MD&A for definition.

Refer to the "Segment Results – Changes in Results" sections of this MD&A under each of the divisions for additional information.

In 2025, contributions in the Facilities Division were made to PGI to partially fund growth capital projects. Contributions in Marketing & New Ventures in 2025 and 2024 were made to Greenlight and Cedar LNG to fund ongoing project development costs. Refer to the "Segment Results – Marketing & New Ventures Division – Projects & New Developments" sections of this MD&A for additional information.

8 Pembina Pipeline Corporation 2025 Annual Report

Pipelines

Financial Overview for the Three Months Ended December 31

Results of Operations

| | | | | | | | | | | | |

| ($ millions, except where noted) | 2025 | 2024 | Change | |

| | | | |

| | | | |

| | | | |

Pipelines revenue(1) | 871 | | 948 | | (77) | | |

Cost of goods sold(1) | 14 | | 5 | | 9 | | |

Net revenue(1)(2) | 857 | | 943 | | (86) | | |

Operating expenses(1) | 200 | | 231 | | (31) | | |

| Depreciation and amortization included in gross profit | 164 | | 147 | | 17 | | |

| Share of profit from equity accounted investees | 1 | | — | | 1 | | |

| Gross profit | 494 | | 565 | | (71) | | |

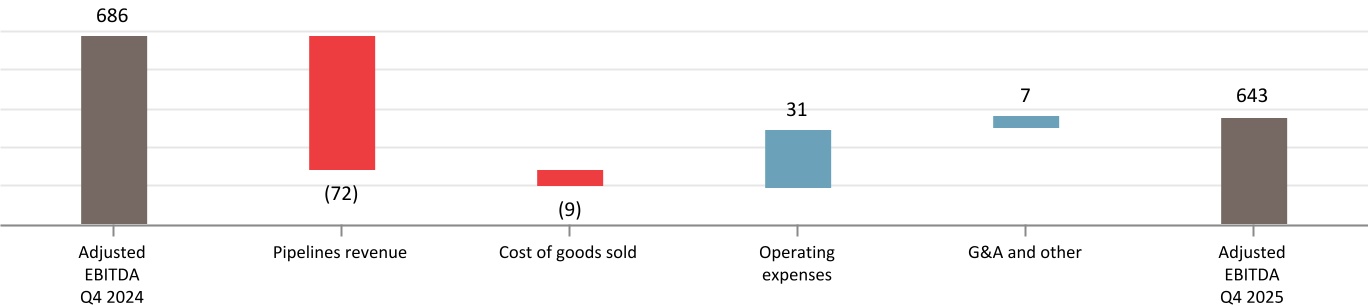

| Earnings | 470 | | 534 | | (64) | | |

Adjusted EBITDA(2) | 643 | | 686 | | (43) | | |

Volumes(3) | 2,815 | | 2,790 | | 25 | | |

| | | | | | |

| Change in Results | | |

| | |

| | |

| | |

Net revenue(1)(2) | | Decrease largely due to lower revenue as a result of the impacts of the Alliance Negotiated Settlement ($33 million) and the presentation of certain flow-through costs on a net basis, with an offsetting decrease to operating expenses for the Alliance Pipeline ($18 million). These impacts were partially offset by higher demand on seasonal contracts on the Alliance Pipeline ($19 million). Lower net revenue due to period specific capital recoveries that impacted certain Pipelines assets in the fourth quarter of 2024 with no similar impact in the same period in 2025 ($23 million), lower interruptible volumes on the Cochin Pipeline driven by narrower condensate price differentials, the sale of the North segment of the Western Pipeline in the third quarter of 2025, and lower revenue at the Edmonton Terminals largely due to lower fees. These decreases were partially offset by higher volumes on the Peace Pipeline system. |

| | |

Operating expenses(1) | | Decrease largely due to the presentation of certain flow-through costs now netted within revenue in 2025 for the Alliance Pipeline. Lower operating expenses were also due to the sale of the North segment of the Western Pipeline in third quarter of 2025 and lower repairs and maintenance costs on the Cochin Pipeline. |

| Depreciation and amortization included in gross profit | | Higher primarily due to a change in estimate related to the decommissioning provision of certain assets and a decrease in the estimated useful life of an intangible asset. |

| | |

| Earnings | | Decrease largely due to the impacts of the Alliance Negotiated Settlement, partially offset by higher seasonal revenue on the Alliance Pipeline. Lower earnings were also driven by period specific capital recoveries that impacted certain Pipelines assets in the fourth quarter of 2024 with no similar impact in the same period in 2025, lower interruptible volumes on the Cochin Pipeline, and higher depreciation and amortization expense. These decreases were partially offset by higher volumes on the Peace Pipeline system and lower operating expenses on the Cochin Pipeline. |

Adjusted EBITDA(2) | | Decrease largely due to the same factors impacting earnings, discussed above, excluding the change in depreciation and amortization expense. |

Volumes(3) | | Higher largely due to higher interruptible and contracted volumes on the Peace Pipeline system, an increase in volumes on AEGS as the fourth quarter in 2024 was impacted by third-party outages, and an increase in contracted volumes on the Nipisi Pipeline. This is partially offset by narrower condensate price differentials resulting in lower interruptible volumes on the Cochin Pipeline and the sale of the North segment of the Western Pipeline in third quarter of 2025. |

Change in Adjusted EBITDA ($ millions)(1)(2)

(1) Includes inter-segment transactions. See Note 5 to the Consolidated Financial Statements.

(2) Refer to the "Non-GAAP & Other Financial Measures" section of this MD&A.

(3) Revenue volumes in mboe/d. See the "Abbreviations" section of this MD&A for definition.

Pembina Pipeline Corporation 2025 Annual Report 9

Financial Overview for the Twelve Months Ended December 31

Results of Operations

| | | | | | | | | | | | |

| ($ millions, except where noted) | 2025 | 2024 | Change | |

| | | | |

| | | | |

| | | | |

Pipelines revenue(1) | 3,521 | | 3,386 | | 135 | | |

Cost of goods sold(1) | 51 | | 40 | | 11 | | |

Net revenue(1)(2) | 3,470 | | 3,346 | | 124 | | |

Operating expenses(1) | 804 | | 832 | | (28) | | |

| Depreciation and amortization included in gross profit | 641 | | 557 | | 84 | | |

| Share of profit from equity accounted investees | 1 | | 42 | | (41) | | |

| Gross profit | 2,026 | | 1,999 | | 27 | | |

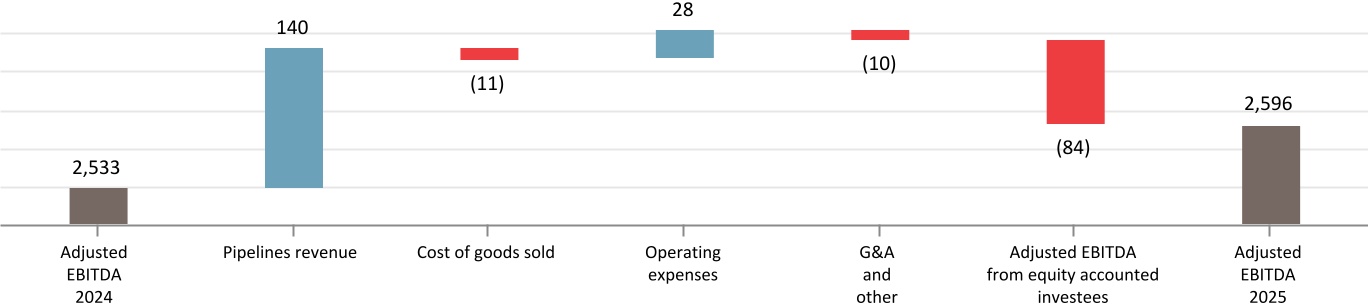

| Earnings | 1,938 | | 1,907 | | 31 | | |

Adjusted EBITDA(2) | 2,596 | | 2,533 | | 63 | | |

Volumes(3) | 2,786 | | 2,711 | | 75 | | |

| | | | | | |

| Change in Results | | |

| | |

| | |

| | |

Net revenue(1)(2) | | Increase largely due to higher net revenue on the Alliance Pipeline resulting from Pembina acquiring a controlling ownership interest in Alliance on April 1, 2024, and higher demand on seasonal contracts ($60 million), partially offset by the impacts of the Alliance Negotiated Settlement ($33 million). Also contributing to the increase were higher interruptible and contracted volumes on the Peace Pipeline system, higher contracted volumes on the Nipisi Pipeline, and higher tolls on the Peace Pipeline system mainly related to contractual inflation adjustments. Higher net revenue on the NEBC Pipelines in 2025 due to the NEBC MPS Expansion being placed into service in November 2024, along with favourable U.S. dollar foreign exchange rate impacts on certain assets, contributed to an increase to net revenue.

These increases were offset in part by lower net revenue on the Cochin Pipeline largely due to lower tolls as a result of the replacement of long-term contracts that expired in mid-July 2024 and lower volumes due to narrower condensate price differentials. Revenue was also lower due to the presentation of certain flow-through costs on a net basis, with an offsetting decrease to operating expenses for the Alliance Pipeline ($39 million), as well as lower revenue due to period specific capital recoveries that impacted 2024 with no similar impact in 2025 ($23 million). In addition, lower tolls and volumes on the Vantage Pipeline, lower revenue on the Western Pipeline due to the sale of the North segment of the Western Pipeline in the third quarter of 2025, lower revenue at the Edmonton Terminals largely due to lower fees and the decommissioning of the Edmonton South Rail Terminal in the second quarter of 2024, and lower recoverable power and geotechnical costs, contributed to a decrease to net revenue. |

| | |

Operating expenses(1) | | Decrease largely due to the presentation of certain flow-through costs now netted within revenue in 2025 for the Alliance Pipeline and the sale of the North segment of the Western Pipeline in third quarter of 2025. Additionally, there were lower geotechnical spend on certain Pipelines assets and lower power costs resulting from a lower power pool price during 2025, both of which were partially recovered in revenue. The decreases were offset in part by higher costs related to Pembina acquiring a controlling ownership interest in Alliance on April 1, 2024. |

Depreciation and amortization included in gross profit | | Higher largely due to Pembina acquiring a controlling ownership interest in Alliance on April 1, 2024, new assets placed into service in the second half of 2024, a change in estimate related to the decommissioning provision of certain assets, and a decrease in the estimated useful life of an intangible asset in 2025. |

Share of profit from equity accounted investees | | Following Pembina acquiring a controlling ownership interest in Alliance on April 1, 2024, the results from Alliance are no longer accounted for in share of profit and are fully consolidated. |

| Earnings | | Increase largely due to higher net revenue on the Alliance Pipeline as a result of the net positive impacts of Pembina acquiring a controlling ownership interest in Alliance on April 1, 2024 and higher seasonal revenue, partially offset by the impacts of the Alliance Negotiated Settlement. Additionally, higher net revenue on the Peace Pipeline system, Nipisi Pipeline, and NEBC Pipelines, also contributed to the increase in earnings, as well as the recognition of a gain on the sale of the North segment of the Western Pipeline in the third quarter of 2025 and favourable foreign exchange rate impacts on certain assets. These factors were partially offset by lower tolls and volumes on the Cochin Pipeline and Vantage Pipeline, along with a decrease in revenue on certain Pipeline assets due to period specific capital recoveries that impacted 2024 with no similar impact in 2025. Furthermore, lower revenue at the Edmonton Terminals along with higher depreciation and amortization expense, contributed to the offsetting decrease. |

Adjusted EBITDA(2) | | Increase largely due to the same factors impacting earnings, discussed above, excluding the gain on the sale of the North segment of the Western Pipeline and the change in depreciation and amortization expense. |

Volumes(3) | | Higher largely due to Pembina acquiring a controlling ownership interest in Alliance on April 1, 2024. Additionally, higher contracted volumes on the Peace Pipeline system and the Nipisi Pipeline, and higher interruptible volumes on the Peace Pipeline system in the 2025 period compared to the same period in 2024 which was impacted by planned outages for the commissioning of the Phase VIII Peace Pipeline Expansion, contributed to an increase to volumes. These increases were offset in part by lower volumes on the Cochin Pipeline due to narrower condensate price differentials and lower interruptible volumes on the Vantage Pipeline. |

(1) Includes inter-segment transactions. See Note 5 to the Consolidated Financial Statements.

(2) Refer to the "Non-GAAP & Other Financial Measures" section of this MD&A.

(3) Revenue volumes in mboe/d. See the "Abbreviations" section of this MD&A for definition.

10 Pembina Pipeline Corporation 2025 Annual Report

Change in Adjusted EBITDA ($ millions)(1)(2)

Financial and Operational Overview

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| 3 Months Ended December 31 | 12 Months Ended December 31 |

| | |

| 2025 | 2024 | 2025 | 2024 |

| ($ millions, except where noted) | Volumes(3) | Earnings | Adjusted EBITDA(2) | Volumes(3) | Earnings | Adjusted EBITDA(2) | Volumes(3) | Earnings | Adjusted EBITDA(2) | Volumes(3) | Earnings | Adjusted EBITDA(2) |

Pipelines(4) | | | | | | | | | | | | |

| Conventional | 1,059 | | 317 | | 379 | | 1,034 | | 321 | | 373 | | 1,025 | | 1,223 | | 1,439 | | 1,001 | | 1,149 | | 1,370 | |

| Transmission | 705 | | 115 | | 193 | | 720 | | 160 | | 224 | | 717 | | 576 | | 891 | | 687 | | 592 | | 865 | |

Oil Sands &

Heavy Oil | 1,051 | | 38 | | 71 | | 1,036 | | 53 | | 89 | | 1,044 | | 139 | | 266 | | 1,023 | | 166 | | 298 | |

| | | | | | | | | | | | |

| Total | 2,815 | | 470 | | 643 | | 2,790 | | 534 | | 686 | | 2,786 | | 1,938 | | 2,596 | | 2,711 | | 1,907 | | 2,533 | |

(1) Includes inter-segment transactions. See Note 5 to the Consolidated Financial Statements.

(2) Refer to the "Non-GAAP & Other Financial Measures" section of this MD&A.

(3) Revenue volumes in mboe/d. See the "Abbreviations" section of this MD&A for definition.

(4) Includes values attributed to Pembina's conventional, transmission and oil sands and heavy oil assets within the Pipelines Division. Refer to Pembina's AIF for the year ended December 31, 2025.

Projects & New Developments(1)

The following table outlines the projects which have recently come into service within the Pipelines Division:

| | | | | |

| Significant Projects | In-service Date |

| Phase VIII Peace Pipeline Expansion | May 2024 |

| NEBC MPS Expansion | November 2024 |

|

(1) For further details on Pembina's significant assets, including definitions for capitalized terms used herein that are not otherwise defined, refer to Pembina's AIF for the year ended December 31, 2025 filed at www.sedarplus.ca (filed with the U.S. Securities and Exchange Commission at www.sec.gov under Form 40-F) and on Pembina's website at www.pembina.com.

The Pipelines Division continues to grow its transportation assets to service customer demand. The following outlines the projects and new developments within the Pipelines Division:

| | | | | | | | |

| Fox Creek-to-Namao Expansion | | |

Capital Budget: $200 million | In-service Date(1): Q1 2027 | Status: Recently sanctioned |

Pembina is developing an expansion of the Peace Pipeline system that, through the addition of three new midpoint pump stations and upgrades to the existing three pump stations, will add approximately 70,000 bpd of propane-plus capacity to the market delivery pipelines from Fox Creek, Alberta to Namao, Alberta, while also increasing operational and logistical flexibility. This expansion will increase the total capacity of the Peace and Northern Pipeline systems to approximately 1.2 mbpd. The project was sanctioned in December 2025. |

| | | | | | | | |

| Birch-to-Taylor Expansion | | |

Capital Budget: $310 million | In-service Date(1): Q4 2027 | Status: Recently sanctioned |

The Birch-to-Taylor Expansion includes a new 95-kilometre pipeline and facility upgrades that will add approximately 120,000 bpd of propane-plus and condensate capacity to that corridor. Plateau Pipe Line Ltd., a subsidiary of Pembina, has obtained all necessary permits to begin preliminary construction activities in 2026. |

Pembina Pipeline Corporation 2025 Annual Report 11

| | | | | | | | |

| Taylor-to-Gordondale Expansion | | |

Capital Budget: $115 million | In-service Date(1): Q1 2027 | Status: Recently sanctioned |

The Taylor-to-Gordondale Expansion will further accommodate growing volumes in northeast British Columbia and Alberta. Pembina and Plateau Pipe Line Ltd., a subsidiary of Pembina, are proceeding with the initial scope of this project, which includes new and upgraded pump stations downstream of Taylor, British Columbia and a new 16-kilometre pipeline connecting production in Alberta to the Gordondale pump station. |

(1) Subject to environmental and regulatory approvals. See the "Forward-Looking Statements & Information" section of this MD&A.

Pembina is proceeding with a phased approach to the Taylor-to-Gordondale Expansion, which is being optimized to meet customers' near-term transportation needs while maintaining Pembina's track record of disciplined capital investment. Pembina continues to evaluate additional scope under the Taylor-to-Gordondale Expansion, including an approximately 89 kilometer, 16-inch pipeline being proposed by Pouce Coupé Pipe Line Ltd., a subsidiary of Pembina, to connect mostly condensate volumes from Taylor, British Columbia to the Gordondale, Alberta area. On February 10, 2026, the CER issued a Certificate of Public Convenience and Necessity for the CER regulated Taylor-to-Gordondale Pipeline Project. This was the final federal regulatory approval required for the pipeline. Pembina will continue to evaluate the incremental scope in conjunction with the timing of customers' egress requirements.

12 Pembina Pipeline Corporation 2025 Annual Report

Facilities

Financial Overview for the Three Months Ended December 31

Results of Operations | | | | | | | | | | | | |

| ($ millions, except where noted) | 2025 | 2024 | Change | |

| | | | |

| | | | |

Facilities revenue(1) | 326 | | 320 | | 6 | | |

| | | | |

| | | | |

Operating expenses(1) | 153 | | 138 | | 15 | | |

Depreciation and amortization included in gross profit | 57 | | 55 | | 2 | | |

Share of profit from equity accounted investees | 74 | | 59 | | 15 | | |

| Gross profit | 190 | | 186 | | 4 | | |

| Earnings | 178 | | 177 | | 1 | | |

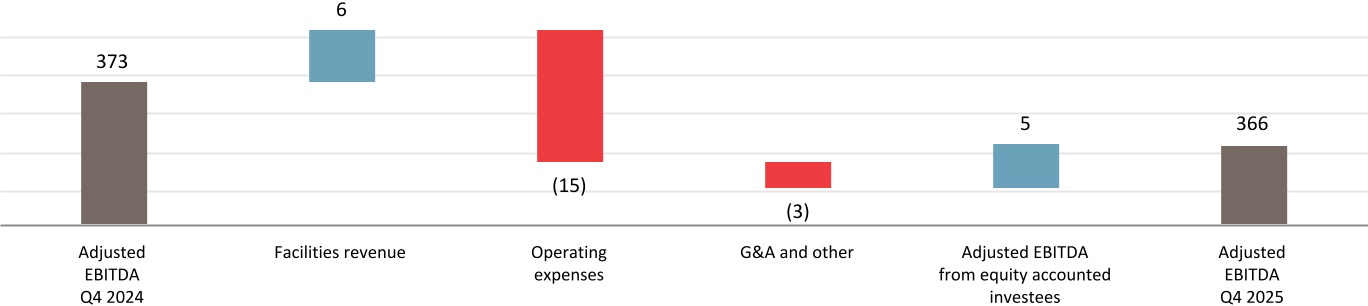

Adjusted EBITDA(2) | 366 | | 373 | | (7) | | |

Volumes(3) | 898 | | 877 | | 21 | | |

| | | | | | |

| Changes in Results | | |

| | |

| | |

Revenue(1) | | Consistent with prior period. Higher operating recoveries at the fractionation facilities within the Redwater Complex, largely offset by minor decreases in revenue across certain other Facilities assets. |

Operating expenses(1) | | Increase primarily due to higher operating expenses related to repairs and maintenance costs at the Redwater Complex in the fourth quarter of 2025 compared to the same period in 2024, the majority of which were recovered in revenue. |

| | |

| Share of profit from equity accounted investees | | Higher earnings from PGI due to an increase in volumes on certain PGI assets and the net impact of PGI's acquisition of a 50 percent working interest in Whitecap's Kaybob Complex in the fourth quarter of 2024. Additionally, there was lower other expense as the fourth quarter of 2024 was impacted by costs related to asset disposals, partially offset by lower revenue due to period specific capital recoveries that impacted certain PGI assets in the fourth quarter of 2024 with no similar impact in the same period in 2025. |

| Earnings | | Consistent with prior period. A higher share of profit from PGI, discussed above, was largely offset by minor decreases in revenue across certain other Facilities assets. |

Adjusted EBITDA(2) | | Consistent with prior period. Higher contributions from certain PGI assets related to an increase in volumes and the net positive impact of the acquisition of Whitecap's Kaybob Complex in the fourth quarter of 2024, were largely offset by minor decreases in revenue across certain other Facilities assets, and lower revenue due to period specific capital recoveries that impacted certain PGI assets in the fourth quarter of 2024 with no similar impact in the same period in 2025. Included in adjusted EBITDA is $198 million (2024: $193 million) related to PGI. |

| | |

Volumes(3) | | Increase is primarily due to higher volumes as a result of the acquisition of Whitecap's Kaybob Complex in the fourth quarter of 2024, higher volumes at the Dawson Assets due to higher natural gas prices, and higher volumes at the Duvernay Complex. This is partially offset by a decrease in Aux Sable volumes due to lower ethane margins. Volumes include 386 mboe/d (2024: 358 mboe/d) related to PGI. |

Change in Adjusted EBITDA ($ millions)(1)(2)

(1) Includes inter-segment transactions. See Note 5 to the Consolidated Financial Statements.

(2) Refer to the "Non-GAAP & Other Financial Measures" section of this MD&A.

(3) Revenue volumes in mboe/d. See the "Abbreviations" section of this MD&A for definition.

Pembina Pipeline Corporation 2025 Annual Report 13

Financial Overview for the Twelve Months Ended December 31

Results of Operations

| | | | | | | | | | | | |

($ millions, except where noted) | 2025 | 2024 | Change | |

| | | | |

| | | | |

Facilities revenue(1) | 1,228 | | 1,127 | | 101 | | |

| | | | |

| | | | |

Operating expenses(1) | 553 | | 474 | | 79 | | |

Depreciation and amortization included in gross profit | 209 | | 183 | | 26 | | |

Share of profit from equity accounted investees | 134 | | 231 | | (97) | | |

| Gross profit | 600 | | 701 | | (101) | | |

| Earnings | 562 | | 666 | | (104) | | |

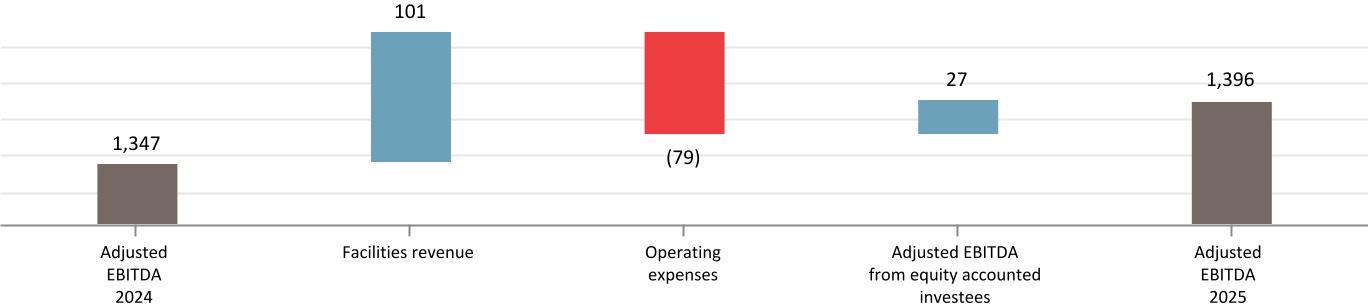

Adjusted EBITDA(2) | 1,396 | | 1,347 | | 49 | | |

Volumes(3) | 871 | | 837 | | 34 | | |

| | | | | | |

| Changes in Results | | |

| | |

| | |

Revenue(1) | | Increase largely due to Pembina acquiring a controlling ownership interest in Aux Sable on April 1, 2024, combined with higher operating recoveries at the fractionation facilities within the Redwater Complex, partially offset by the impact of a planned outage at the Redwater Complex related to an asset upgrade in the second quarter of 2025. |

Operating expenses(1) | | Increase largely due to Pembina acquiring a controlling ownership interest in Aux Sable on April 1, 2024, combined with higher repairs and maintenance costs at the Redwater Complex, the majority of which were recovered in revenue, along with minor increases across multiple other operating costs. |

| Depreciation and amortization included in gross profit | | Higher largely due to Pembina acquiring a controlling ownership interest in Aux Sable on April 1, 2024, combined with an asset upgrade and associated retirement at the Redwater Complex in the second quarter of 2025, resulting in a planned outage during the same period. |

| | |

| | |

| Share of profit from equity accounted investees | | Decrease due to lower earnings from PGI largely the result of impairment of $146 million (net to Pembina, after tax) recognized on certain PGI assets. Additionally, lower revenue driven by outages at certain PGI assets in 2025 and third-party downstream restrictions impacting the Dawson Assets, contributed to a decrease in share of profit from PGI. This was partially offset by the recognition of a $23 million gain (net to Pembina, after tax) following the amendment of PGI's credit facility, gains recognized by PGI on interest rate derivative financial instruments in 2025 compared to losses in 2024, and lower other expense as 2024 was impacted by costs related to asset disposals. Additionally, higher contributions due to the Whitecap Transactions and higher volumes at the Duvernay Complex, contributed to the offsetting increase to share of profit from PGI. |

| Earnings | | Decrease primarily due to lower share of profit from PGI and higher depreciation and amortization expense. This was partially offset by the net positive impacts of Pembina acquiring a controlling ownership interest in Aux Sable on April 1, 2024. |

Adjusted EBITDA(2) | | Increase primarily due to the net positive impacts of Pembina acquiring a controlling ownership interest in Aux Sable on April 1, 2024, combined with higher contributions from PGI largely the result of the Whitecap Transactions and higher volumes at the Duvernay Complex. This was partially offset by outages at certain PGI assets in 2025 and third-party downstream restrictions impacting the Dawson Assets. Included in adjusted EBITDA is $735 million (2024: $709 million) related to PGI. |

Volumes(3) | | Higher largely due to Pembina acquiring a controlling ownership interest in Aux Sable on April 1, 2024, partially offset by a decrease in volumes due to lower ethane margins and lower utilization in 2025 compared to 2024 due to third-party restrictions and planned outages at the Channahon Facility in the second quarter of 2025. Additionally, higher volumes at the Redwater Complex and Younger were due to a planned outage and a rail strike impacting the Redwater Complex that occurred in the third quarter of 2024, which resulted in volume curtailments. Higher volumes on certain PGI assets due to the Whitecap Transactions and higher volumes at the Duvernay Complex, were largely offset by volume curtailments at certain PGI assets resulting from a turnaround that began in the second quarter of 2025 and continued into the third quarter, combined with third-party downstream restrictions impacting the Dawson Assets. Volumes include 364 mboe/d (2024: 358 mboe/d) related to PGI. |

(1) Includes inter-segment transactions. See Note 5 to the Consolidated Financial Statements.

(2) Refer to the "Non-GAAP & Other Financial Measures" section of this MD&A.

(3) Revenue volumes in mboe/d. See the "Abbreviations" section of this MD&A for definition.

14 Pembina Pipeline Corporation 2025 Annual Report

Change in Adjusted EBITDA ($ millions)(1)(2)

Financial and Operational Overview

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| 3 Months Ended December 31 | 12 Months Ended December 31 |

| 2025 | 2024 | 2025 | 2024 |

| ($ millions, except where noted) | Volumes(3) | Earnings | Adjusted EBITDA(2) | Volumes(3) | Earnings | Adjusted EBITDA(2) | Volumes(3) |

Earnings | Adjusted EBITDA(2) | Volumes(3) | Earnings | Adjusted EBITDA(2) |

Facilities(4) | | | | | | | | | | | | |

| Gas Services | 631 | | 91 | | 226 | | 597 | | 77 | | 222 | | 610 | | 209 | | 849 | | 598 | | 299 | | 817 | |

| NGL Services | 267 | | 87 | | 140 | | 280 | | 100 | | 151 | | 261 | | 353 | | 547 | | 239 | | 367 | | 530 | |

| | | | | | | | | | | | |

| Total | 898 | | 178 | | 366 | | 877 | | 177 | | 373 | | 871 | | 562 | | 1,396 | | 837 | | 666 | | 1,347 | |

(1) Includes inter-segment transactions. See Note 5 to the Consolidated Financial Statements.

(2) Refer to the "Non-GAAP & Other Financial Measures" section of this MD&A.

(3) Revenue volumes in mboe/d. See the "Abbreviations" section of this MD&A for definition.

(4) Includes values attributed to Pembina's gas services and NGL services assets within the Facilities operating segment. For a description of Pembina's gas and NGL assets, refer to Pembina's AIF for the year ended December 31, 2025.

Projects & New Developments(1)

The Facilities Division continues to grow its natural gas and NGL processing and fractionation assets to service customer demand. The following outlines the projects and new developments within the Facilities Division:

| | | | | | | | |

| RFS IV | | |

Capital Budget: $525 million | | |

Revised Capital Cost: $500 million | In-service Date(2): Q2 2026 | Status: On time, trending under budget |

RFS IV is a 55,000 bpd propane-plus fractionator at the existing Redwater fractionation and storage complex (the "Redwater Complex"). The project includes additional rail loading capacity and will leverage the design, engineering, and operating best practices of the existing facilities at the Redwater Complex. With the addition of RFS IV, the fractionation capacity at the Redwater Complex will total 256,000 bpd. Pembina has entered into a lump-sum engineering, procurement and construction agreement in respect of the project, for more than 70 percent of the project cost. Engineering, procurement, and fabrication is substantially complete, while field construction has progressed to approximately 90 percent complete. |

| | | | | | | | |

| Wapiti Expansion | | |

Capital Budget: $140 million (net to Pembina) | In-service Date(2): End of Q1 2026 | Status: On time, trending on budget |

PGI is developing an expansion that will increase natural gas processing capacity at the Wapiti Plant by 115 MMcf/d (gross to PGI). The expansion opportunity is driven by strong customer demand supported by growing Montney production and is fully underpinned by long-term, take-or-pay contracts. The project includes a new sales gas pipeline and other related infrastructure. Commissioning is underway and the expansion is expected to be in-service at the end of the first quarter. |

| | | | | | | | |

| K3 Cogeneration Facility | | |

Capital Budget: $70 million (net to Pembina) | In-service Date(2): End of Q1 2026 | Status: On time, trending under budget |

PGI is developing a 28 MW cogeneration facility at its K3 Plant, which is expected to reduce overall operating costs by providing power and heat to the gas processing facility, while reducing customers' exposure to power prices. The K3 Cogeneration Facility is expected to fully supply the K3 Plant's power requirements, with excess power sold to the grid at market rates. Further, through the utilization of the cogeneration waste heat and the low-emission power generated, the project is expected to contribute to a reduction in annual emissions compliance costs at the K3 Plant. Commissioning is underway and the project is expected to be in-service at the end of the first quarter. |

Pembina Pipeline Corporation 2025 Annual Report 15

| | | | | | | | |

| Prince Rupert Terminal Optimization | | |

Capital Budget: $145 million | In-service Date(2): Mid-2028 | Status: Recently sanctioned |

| Pembina is optimizing its Prince Rupert Terminal ("PRT"), primarily through increasing storage capacity, that will allow PRT to accommodate medium gas carrier vessels. The PRT optimization is expected to expand access to additional markets with higher realized propane prices, while significantly reducing shipping costs per unit, thereby improving netbacks for Pembina and its customers. Earthworks at site are nearing completion, and engineering activities and procurement of long-lead equipment has commenced. |

(1) For further details on Pembina's significant assets, including definitions for capitalized terms used herein that are not otherwise defined, refer to Pembina's AIF for the year ended December 31, 2025 filed at www.sedarplus.ca (filed with the U.S. Securities and Exchange Commission at www.sec.gov under Form 40-F) and on Pembina's website at www.pembina.com.

(2) Subject to environmental and regulatory approvals. See the "Forward-Looking Statements & Information" section of this MD&A.

Pursuant to an agreement with Whitecap, PGI has committed to support infrastructure development in the Lator area, including a new battery and gathering laterals (the "Lator Infrastructure"), which PGI will own. PGI anticipates funding up to $400 million ($240 million net to Pembina) for the battery and gathering laterals within the first phase of the Lator Infrastructure development, with all gas volumes flowing to PGI's Musreau facility upon startup, which is expected in the fourth quarter of 2026, supporting long-term plant utilization. Site grading and piling installation for the battery was completed in the fourth quarter of 2025, and Pembina's pipeline execution scope is approximately 60 percent complete.

Pursuant to an agreement with Whitecap, PGI has committed to fund capital up to $300 million ($180 million net to Pembina) for battery and gathering infrastructure in the Gold Creek and Karr areas, which is expected to be in service in the second quarter of 2026. The gathering pipeline infrastructure has been completed and battery construction is approximately 50 percent complete.

Pursuant to an agreement with a Montney producer, PGI has committed to fund and acquire an under-construction battery and additional infrastructure (the "North Gold Creek Battery") in the Wapiti/North Gold Creek Montney area for a capital commitment up to $150 million ($90 million net to Pembina). The North Gold Creek Battery will be operated by the producer and highly contracted under a long-term, take-or-pay agreement. Pipeline installations are complete and all equipment has been installed at the North Gold Creek Battery, with electrical and instrumentation work progressing. The expected in-service date of the North Gold Creek Battery is the second quarter of 2026.

16 Pembina Pipeline Corporation 2025 Annual Report

Marketing & New Ventures

Financial Overview for the Three Months Ended December 31

Results of Operations | | | | | | | | | | | | |

| ($ millions, except where noted) | 2025 | 2024 | Change | |

Marketing & New Ventures revenue(1) | 985 | | 1,133 | | (148) | | |

Cost of goods sold(1) | 927 | | 919 | | 8 | | |

Net revenue(1)(2) | 58 | | 214 | | (156) | | |

Operating expenses(1) | 6 | | 12 | | (6) | | |

| Depreciation and amortization included in gross profit | 18 | | 17 | | 1 | | |

| Share of profit from equity accounted investees | 96 | | 74 | | 22 | | |

| Gross profit | 130 | | 259 | | (129) | | |

| Earnings | 115 | | 245 | | (130) | | |

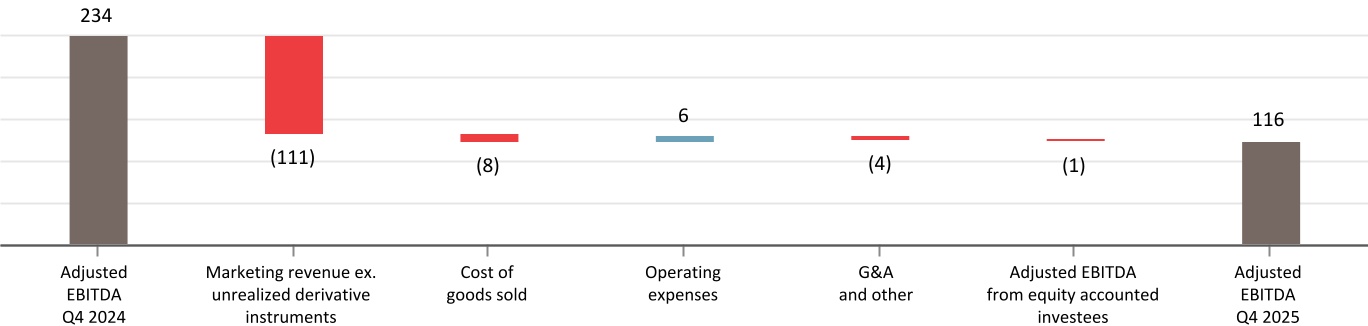

Adjusted EBITDA(2) | 116 | | 234 | | (118) | | |

Crude oil sales volumes(3) | 77 | | 96 | | (19) | | |

NGL sales volumes(3) | 260 | | 252 | | 8 | | |

| | | | | | |

| Change in Results | | |

| | |

| | |

Net revenue(1)(2) | | Lower NGL net revenue from contracts with customers was driven primarily by lower NGL margins due to narrower WCSB and U.S. NGL frac spreads in the fourth quarter of 2025 compared to the same period in 2024. Crude net revenue from contracts with customers remained consistent for the fourth quarter of 2025 compared to the fourth quarter of 2024.

Lower revenue from risk management and other derivative contracts was primarily due to an unrealized loss on the embedded derivative arising from the Cedar LNG capacity commercial arrangement entered into during the fourth quarter of 2025 (refer to the "Other - Risk Management - Financial Instruments" section of this MD&A), lower realized gains on crude oil-based derivatives due to lower volumes and narrower crude oil price spreads, and unrealized losses on renewable power purchase agreements in the fourth quarter of 2025 compared to gains in the fourth quarter of 2024. These decreases were partially offset by gains on NGL-based derivatives in the fourth quarter of 2025 compared to losses in the same period of 2024. The fourth quarter of 2025 included unrealized losses on derivative instruments of $78 million (2024: $41 million loss) and realized gains on derivative instruments of $35 million (2024: $52 million gain). |

| | |

| | |

| | |

| | |

| | |

| Share of profit from equity accounted investees | | Increase largely due to a gain of $62 million (net to Pembina, pre-tax) recognized by Greenlight on the sale of land to a third-party potential customer in the fourth quarter of 2025, partially offset by lower share of profit from Cedar LNG due to lower unrealized gains on interest rate derivative financial instruments, offset in part by unrealized foreign exchange gains on U.S. dollar denominated debt recognized by Cedar LNG in the fourth quarter of 2025 compared to losses in the fourth quarter of 2024. |

| Earnings | | Decrease primarily due to narrower WCSB and U.S. NGL frac spreads in the fourth quarter of 2025 compared to the same period in 2024, and lower net revenue from risk management and other derivative contracts, discussed above. These decreases were partially offset by higher share of profit from Greenlight due to a gain on sale of land to a third-party potential customer, offset in part by lower share of profit from Cedar LNG. |

Adjusted EBITDA(2) | | Decrease largely due to narrower WCSB and U.S. NGL frac spreads in the fourth quarter of 2025 compared to the same period in 2024, as well as lower realized gains on crude oil-based derivatives due to lower volumes and narrower crude oil price spreads, partially offset by realized gains on NGL-based derivatives in the fourth quarter of 2025 compared to losses in the fourth quarter of 2024. |

Crude oil sales volumes(3) | | Lower primarily due to decreased blending opportunities. |

| | |

Change in Adjusted EBITDA ($ millions)(1)(2)

(1) Includes inter-segment transactions. See Note 5 to the Consolidated Financial Statements.

(2) Refer to the "Non-GAAP & Other Financial Measures" section of this MD&A.

(3) Marketed crude oil and NGL volumes in mboe/d. See the "Abbreviations" section of this MD&A for definition.

Pembina Pipeline Corporation 2025 Annual Report 17

Financial Overview for the Twelve Months Ended December 31

Results of Operations

| | | | | | | | | | | | |

| ($ millions, except where noted) | 2025 | 2024 | Change | |

Marketing & New Ventures revenue(1) | 4,065 | | 3,796 | | 269 | | |

Cost of goods sold(1) | 3,524 | | 3,198 | | 326 | | |

Net revenue(1)(2) | 541 | | 598 | | (57) | | |

Operating expenses(1) | 30 | | 25 | | 5 | | |

| Depreciation and amortization included in gross profit | 71 | | 64 | | 7 | | |

| Share of profit from equity accounted investees | 74 | | 55 | | 19 | | |

| Gross profit | 514 | | 564 | | (50) | | |

| Earnings | 457 | | 569 | | (112) | | |

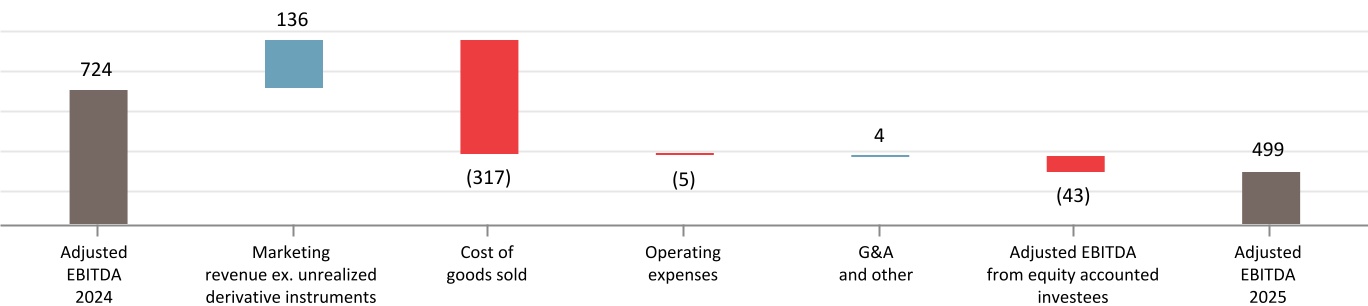

Adjusted EBITDA(2) | 499 | | 724 | | (225) | | |

Crude oil sales volumes(3) | 93 | | 99 | | (6) | | |

NGL sales volumes(3) | 246 | | 228 | | 18 | | |

| | | | | | |

| Change in Results | | |

| | |

| | |

Net revenue(1)(2) | | Lower net revenue from contracts with customers was largely driven by lower NGL margins due to narrower WCSB and U.S. NGL frac spreads in 2025 compared to 2024. This was partially offset by Pembina acquiring a controlling ownership interest in Aux Sable on April 1, 2024 and no similar impact to the nine-day unplanned outage at Aux Sable in July 2024.

Higher revenue from risk management and other derivative contracts was primarily due to lower unrealized losses on renewable power purchase agreements, largely due to improved forward power prices, and unrealized gains on NGL-based derivatives in 2025, compared to losses in 2024. In addition, lower realized losses on NGL-based derivatives, contributed to an increase in net revenue. These increases were partially offset by lower realized gains on crude oil-based derivatives due to lower volumes and narrower crude oil price spreads and an unrealized loss on the embedded derivative arising from the Cedar LNG capacity commercial arrangement entered into during the fourth quarter of 2025 (refer to the "Other - Risk Management - Financial Instruments" section of this MD&A). The 2025 year included unrealized losses on derivative instruments of $37 million (2024: $170 million loss) and realized gains on derivative instruments of $133 million (2024: $241 million gain). |

| | |

| | |

| | |

| Share of profit from equity accounted investees | | Increase largely due to a gain of $62 million (net to Pembina, pre-tax) recognized by Greenlight on the sale of land to a third-party potential customer in the fourth quarter of 2025, combined with unrealized foreign exchange gains on U.S. dollar denominated debt recognized by Cedar LNG in 2025 compared to losses in 2024. These increases were partially offset by unrealized losses on interest rate derivative financial instruments recognized by Cedar LNG in 2025 compared to gains in 2024, as well as the results from Aux Sable from the first quarter of 2024, which are fully consolidated following Pembina acquiring a controlling ownership interest on April 1, 2024. |

| | |

| Earnings | | Decrease primarily due to narrower WCSB and U.S. NGL frac spreads in 2025 compared to 2024, as well as no similar gain to that recognized in the 2024 period associated with the derecognition of the provision related to financial assurances provided by Pembina which were assumed by Cedar LNG following the positive final investment decision in June 2024 in respect of the Cedar LNG project, a floating LNG export facility currently under construction (the "Cedar LNG Project"). This was partially offset by the net positive impacts of Pembina acquiring a controlling ownership interest in Aux Sable on April 1, 2024, higher share of profit from Greenlight, and higher revenue from risk management and other derivative contracts. |

Adjusted EBITDA(2) | | Decrease primarily due to narrower WCSB and U.S. NGL frac spreads in 2025 compared to 2024 and lower realized gains on crude oil-based derivatives due to lower volumes and narrower crude oil price spreads, partially offset by the net positive impacts of Pembina acquiring a controlling ownership interest in Aux Sable on April 1, 2024, and lower realized losses on NGL-based derivatives. |

| | |

NGL sales volumes(3) | | Increase due to higher WCSB ethane volumes, combined with higher ethane, propane, and butane volumes at Aux Sable largely due to the increase in Pembina's ownership interest in Aux Sable and no similar impact to the nine-day unplanned outage in July 2024. |

(1) Includes inter-segment transactions. See Note 5 to the Consolidated Financial Statements.

(2) Refer to the "Non-GAAP & Other Financial Measures" section of this MD&A.

(3) Marketed crude oil and NGL volumes in mboe/d. See the "Abbreviations" section of this MD&A for definition.

18 Pembina Pipeline Corporation 2025 Annual Report

Change in Adjusted EBITDA ($ millions)(1)(2)

Financial and Operational Overview

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| 3 Months Ended December 31 | 12 Months Ended December 31 |

| 2025 | 2024 | 2025 | 2024 |

| ($ millions, except where noted) | Volumes(3) | Earnings | Adjusted EBITDA(2) | Volumes(3) | Earnings | Adjusted EBITDA(2) | Volumes(3) | Earnings | Adjusted EBITDA(2) | Volumes(3) | Earnings | Adjusted EBITDA(2) |

Marketing & New Ventures(4) | | | | | | | | | | | | |

| Marketing | 337 | | 86 | | 122 | | 349 | | 174 | | 237 | | 339 | | 467 | | 521 | | 327 | | 510 | | 731 | |

New Ventures(5) | — | | 29 | | (6) | | — | | 71 | | (3) | | — | | (10) | | (22) | | — | | 59 | | (7) | |

| | | | | | | | | | | | |

| | | | | | | | | | | | |

| Total | 337 | | 115 | | 116 | | 349 | | 245 | | 234 | | 339 | | 457 | | 499 | | 327 | | 569 | | 724 | |

(1) Includes inter-segment transactions. See Note 5 to the Consolidated Financial Statements.

(2) Refer to the "Non-GAAP & Other Financial Measures" section of this MD&A.

(3) Marketed crude oil and NGL volumes in mboe/d. See the "Abbreviations" section of this MD&A for definition.

(4) Includes values attributed to Pembina's marketing activities and new ventures projects within the Marketing & New Ventures operating segment. For further details on Pembina's marketing activities and projects, refer to Pembina's AIF for the year ended December 31, 2025.

(5) All New Ventures projects have not yet commenced operations and therefore have no volumes.

Projects & New Developments(1)

The New Ventures group is responsible for the development of new large-scale, or value chain extending projects, including those that provide enhanced access to global markets and support a transition to a lower-carbon economy.

| | | | | | | | |

| Cedar LNG | | |

Capital Budget: U.S. $2 billion (net) | In-service Date: Late-2028 | Status: On time, on budget |

The Haisla Nation and Pembina are partners in Cedar LNG Partners LP ("Cedar LNG"), which is constructing the Cedar LNG Project, a floating LNG facility with a nameplate capacity of 3.3 million tonnes per annum ("mtpa"), located in the traditional territory of the Haisla Nation, on Canada's West Coast. The project is strategically positioned to leverage Canada's abundant natural gas supply and deliver a lower-carbon energy option to global markets. The facility will be powered by renewable electricity from BC Hydro, making it one of the lowest emitting LNG facilities in the world. At the end of December 2025, construction of the floating LNG vessel was over 35 percent complete. In addition, significant progress has been made towards the onshore scope of work, including completion of all horizontal directional drills on the Cedar Pipeline and clearing of the transmission line right-of-way. 2026 is expected to be the largest single capital investment year for the project, with a focus on progressing construction of the floating LNG vessel, completing the substation and mooring foundations at the marine terminal site, commencing installation of the transmission line, and achieving mechanical completion of the Cedar Pipeline. |

| Cedar LNG has secured a 20-year take-or-pay, fixed toll contract with ARC Resources Ltd. for 1.5 mtpa of LNG. Pembina previously signed a 20-year take-or-pay liquefaction tolling service agreement for 1.5 mtpa of LNG to support the final investment decision on Cedar LNG in June 2024 with the expectation of remarketing the capacity at a later stage. During the fourth quarter of 2025, Pembina announced a 20-year take-or-pay agreement with PETRONAS related to 1.0 mtpa of liquefaction capacity, and a 12-year take-or-pay agreement with Ovintiv related to 0.5 mtpa of liquefaction capacity at Cedar LNG, which completes Pembina's remarketing efforts. |

(1) For further details on Pembina's significant assets, including definitions for capitalized terms used herein that are not otherwise defined, refer to Pembina's AIF for the year ended December 31, 2025 filed at www.sedarplus.ca (filed with the U.S. Securities and Exchange Commission at www.sec.gov under Form 40-F) and on Pembina's website at www.pembina.com.