QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the quarterly period ended June 29, 2025

or

☐

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from ______ to ______

Commission File Number: 001-35625

BLOOMIN’ BRANDS, INC.

(Exact name of registrant as specified in its charter)

Delaware

20-8023465

(State or other jurisdiction of incorporation or organization)

(IRS Employer Identification No.)

2202 North West Shore Boulevard, Suite 500, Tampa, FL33607

(Address of principal executive offices) (Zip Code)

(813) 282-1225

(Registrant’s telephone number, including area code)

N/A

(Former name, former address and former fiscal year, if changed since last report)

Securities registered pursuant to Section 12(b) of the Act:

Title of each class

Trading Symbol(s)

Name of each exchange on which registered

Common Stock

$0.01 par value

BLMN

The Nasdaq Stock Market LLC

(Nasdaq Global Select Market)

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes☒ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes☒ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer☒ Accelerated filer☐ Non-accelerated filer ☐

Smaller reporting company ☐ Emerging growth company ☐

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐No ☒

As of August 4, 2025, 85,068,422 shares of common stock of the registrant were outstanding.

Current assets of discontinued operations held for sale

—

22,989

Total current assets

331,964

320,519

Property, fixtures and equipment, net

941,676

948,521

Operating lease right-of-use assets

1,015,518

1,012,857

Goodwill

213,323

213,323

Intangible assets, net

427,179

429,091

Deferred income tax assets, net

205,993

185,522

Equity method investment

61,702

—

Other assets, net

110,193

74,471

Non-current assets of discontinued operations held for sale

—

200,501

Total assets

$

3,307,548

$

3,384,805

LIABILITIES AND STOCKHOLDERS’ EQUITY

Current liabilities

Accounts payable

$

142,521

$

153,161

Current operating lease liabilities

162,509

158,806

Accrued and other current liabilities

163,752

178,314

Unearned revenue

308,416

374,099

Current liabilities of discontinued operations held for sale

—

87,956

Total current liabilities

777,198

952,336

Non-current operating lease liabilities

1,077,983

1,088,518

Deferred income tax liabilities, net

23,610

33,822

Long-term debt, net

917,073

1,027,398

Other long-term liabilities, net

110,390

93,420

Non-current liabilities of discontinued operations held for sale

—

49,865

Total liabilities

2,906,254

3,245,359

Commitments and contingencies (Note 15)

Stockholders’ equity

Bloomin’ Brands stockholders’ equity

Preferred stock, $0.01 par value, 25,000,000 shares authorized; no shares issued and outstanding as of June 29, 2025 and December 29, 2024

—

—

Common stock, $0.01 par value, 475,000,000 shares authorized; 85,062,439 and 84,854,768 shares issued and outstanding as of June 29, 2025 and December 29, 2024, respectively

851

849

Additional paid-in capital

1,250,403

1,273,288

Accumulated deficit

(858,263)

(925,834)

Accumulated other comprehensive income (loss)

4,246

(212,793)

Total Bloomin’ Brands stockholders’ equity

397,237

135,510

Noncontrolling interests

4,057

3,936

Total stockholders’ equity

401,294

139,446

Total liabilities and stockholders’ equity

$

3,307,548

$

3,384,805

The accompanying notes are an integral part of these unaudited consolidated financial statements.

1. Description of the Business and Basis of Presentation

Description of the Business - Bloomin’ Brands (“Bloomin’ Brands” or the “Company”) owns and operates casual, upscale casual and fine dining restaurants. OSI Restaurant Partners, LLC (“OSI”) is the Company’s primary operating entity. The Company’s restaurant portfolio includes Outback Steakhouse, Carrabba’s Italian Grill, Bonefish Grill and Fleming’s Prime Steakhouse & Wine Bar. Additional Outback Steakhouse, Carrabba’s Italian Grill and Bonefish Grill restaurants are operated under franchise agreements.

Basis of Presentation - The accompanying interim unaudited condensed consolidated financial statements have been prepared by the Company pursuant to the rules and regulations of the Securities and Exchange Commission. Accordingly, they do not include all the information and footnotes required by generally accepted accounting principles in the United States (“U.S. GAAP”) for complete financial statements. In the opinion of the Company, all adjustments necessary for fair statement of results for the periods presented have been included and are of a normal, recurring nature. The results of operations for interim periods are not necessarily indicative of the results to be expected for the full year. Unless otherwise noted, disclosures within these Notes to Consolidated Financial Statements relate solely to the Company’s continuing operations. These financial statements should be read in conjunction with the audited financial statements and notes thereto included in the Company’s Annual Report on Form 10-K for the year ended December 29, 2024.

Recently Issued Financial Accounting Standards Not Yet Adopted - In December 2023, the FASB issued ASU No. 2023-09, “Income Taxes (Topic 740): Improvements to Income Tax Disclosures,” (“ASU No. 2023-09”) which expands existing income tax disclosures, including disaggregation of the Company’s effective income tax rate reconciliation table and income taxes paid disclosures. ASU No. 2023-09 is effective for the Company beginning with the 2025 Form 10-K, with early adoption permitted, and may be applied either prospectively for reporting periods after the effective date or retrospectively to prior periods presented. The Company is currently evaluating the impact ASU No. 2023-09 will have on its disclosures.

In November 2024, the FASB issued ASU No. 2024-03, “Income Statement - Reporting Comprehensive Income (Subtopic 220-40): Disaggregation of Income Statement Expenses,” (“ASU No. 2024-03”) which requires detailed disclosures in the notes to financial statements of expense categories within relevant income statement captions including purchases of inventory, employee compensation, depreciation and intangible asset amortization. ASU No. 2024-03 is effective for the Company beginning with the 2027 Form 10-K, with early adoption permitted, and may be applied either prospectively for reporting periods after the effective date or retrospectively to prior periods presented. The Company is currently evaluating the impact ASU No. 2024-03 will have on its disclosures.

Recent accounting guidance not discussed herein is not applicable, did not have or is not expected to have a material impact to the Company.

Reclassifications - The Company reclassified certain immaterial amounts in prior period financial statements to conform to the current period’s presentation. These reclassifications had no effect on previously reported Net income (loss).

2. Discontinued Operations

On December 30, 2024 (the “Closing Date”), an indirect wholly owned subsidiary of the Company (the “Seller”) completed the sale of 67% of the ownership interest in its business in Brazil (the “Disposal Group”) to a fund managed by an affiliate of Vinci Partners Investments Ltd. (the “Buyer”) (the “Brazil Sale Transaction”). Following the closing, the Brazil restaurants began operating as unconsolidated franchisees.

The aggregate consideration paid to the Seller consisted of 67% of the enterprise valuation of the Disposal Group in the amount of R$2.06 billion Brazilian Reais, which equaled R$1.4 billion Brazilian Reais (approximately $225.3 million in U.S. Dollars based on the exchange rate on the Closing Date), subject to customary adjustments, and withholding for Brazilian taxes (the “Purchase Price”). On December 30, 2024, the Company received cash proceeds, net of withheld income taxes, of $103.9 million, in U.S. dollars based on the exchange rate on the Closing Date, representing 52% of the Purchase Price. The proceeds were applied to the Company’s revolving credit facility during the thirteen weeks ended March 30, 2025. The second installment payment, representing 48% of the Purchase Price, is due on the first anniversary of the Closing Date (based on the exchange rate on the date of payment) and will generate interest income based on the interbank deposit rate in Brazil until paid.

The sale represents a strategic shift to a primarily franchised model for the Company’s international operations. The assets and liabilities of the Disposal Group were classified as held for sale on the Company’s Consolidated Balance Sheet as of December 29, 2024. For the thirteen and twenty-six weeks ended June 29, 2025 and June 30, 2024, all sales, direct costs and expenses and income taxes attributable to restaurants classified as discontinued operations have been aggregated to a single caption titled Net income from discontinued operations, net of tax in the Company’s Consolidated Statements of Operations and Comprehensive Income (Loss) for all periods presented.

As of the Closing Date, the fair value of the Company’s retained interest was $59.9 million based on the proportional enterprise valuation of the Disposal Group, adjusted for debt used by the Buyer to fund a portion of the Purchase Price and to be pushed down to the operating entity subsequent to the second installment payment. See Note 3 - Equity Method Investment for additional details regarding the Company’s retained interest in its Brazil operations.

Net income from discontinued operations, net of tax, in the Company’s Consolidated Statements of Operations and Comprehensive Income (Loss) includes the following for the periods indicated:

THIRTEEN WEEKS ENDED

TWENTY-SIX WEEKS ENDED

(dollars in thousands)

JUNE 29, 2025

JUNE 30, 2024

JUNE 29, 2025

JUNE 30, 2024

Revenues

$

—

$

125,799

$

—

$

258,609

Operating costs and expenses

—

123,226

—

249,800

Gain on sale of Brazil business (1)

1,672

—

4,575

—

Income from operations

1,672

2,573

4,575

8,809

Provision (benefit) for income taxes

893

(1,082)

4,050

2,246

Net income from discontinued operations, net of tax

$

779

$

3,655

$

525

$

6,563

____________________

(1)The thirteen and twenty-six weeks ended June 29, 2025 include $1.3 million and $2.9 million, respectively, of net foreign currency translation gains on contingent consideration assets and indemnification liabilities, as discussed below.

Contingent Consideration Assets and Indemnification Liabilities - On the Closing Date, the Company recognized contingent consideration assets of $29.3 million, primarily judicial deposits, and indemnification liabilities of $6.9 million, primarily labor and tax exposures, within Other assets, net and Other long-term liabilities, net, respectively, on the Company’s Consolidated Balance Sheet in connection with the Brazil Sale Transaction. As of June 29, 2025, the Company’s balance of contingent consideration assets and indemnification liabilities, which are denominated in Brazilian Reais, increased to $33.1 million and $7.8 million, respectively, as a result of fluctuations in foreign exchange rates. All post-closing adjustments related to contingent consideration assets and indemnification liabilities will be reflected in discontinued operations.

The Company retained a 33% interest in the franchisee of the Company’s restaurants in Brazil subsequent to the sale, which is accounted for using the equity method of accounting. To ensure timely reporting, the Company records the results of the equity method investment in Brazil on a calendar basis one-month lag.

As of June 29, 2025, the carrying value of the Company’s equity method investment was $61.7 million and is recorded in Equity method investment on its Consolidated Balance Sheet. The Company’s proportionate share of net loss from its equity interest was $1.8 millionand $3.1 millionfor the thirteen and twenty-six weeks ended June 29, 2025, respectively, and is recorded within Loss from equity method investment, net of tax in the Consolidated Statements of Operations and Comprehensive Income (Loss).

4. Revenue Recognition

The following tables include the disaggregation of Restaurant sales and franchise revenues by restaurant concept and segment for the periods indicated:

THIRTEEN WEEKS ENDED

JUNE 29, 2025

JUNE 30, 2024

(dollars in thousands)

RESTAURANT SALES

FRANCHISE REVENUES

RESTAURANT SALES

FRANCHISE REVENUES

U.S.

Outback Steakhouse

$

571,897

$

7,800

$

562,904

$

8,076

Carrabba’s Italian Grill

181,141

573

174,576

752

Bonefish Grill

126,671

89

134,279

128

Fleming’s Prime Steakhouse & Wine Bar

95,586

—

88,390

—

Other

—

—

1,939

18

U.S. total

975,295

8,462

962,088

8,974

International Franchise (1)

—

7,051

—

9,444

Other (2)

9,476

10

15,691

—

Total

$

984,771

$

15,523

$

977,779

$

18,418

TWENTY-SIX WEEKS ENDED

JUNE 29, 2025

JUNE 30, 2024

(dollars in thousands)

RESTAURANT SALES

FRANCHISE REVENUES

RESTAURANT SALES

FRANCHISE REVENUES

U.S.

Outback Steakhouse

$

1,169,378

$

15,969

$

1,166,517

$

16,396

Carrabba’s Italian Grill

365,471

1,235

359,005

1,488

Bonefish Grill

262,662

193

278,782

288

Fleming’s Prime Steakhouse & Wine Bar

197,914

—

184,552

—

Other

—

—

4,128

56

U.S. total

1,995,425

17,397

1,992,984

18,228

International Franchise (1)

—

16,334

—

19,556

Other (2)

18,863

32

31,485

—

Total

$

2,014,288

$

33,763

$

2,024,469

$

37,784

________________

(1)Includes intercompany royalties from Brazil prior to the sale and royalties from Brazil after the sale.

(2)Includes Restaurant sales for Company-owned restaurants in Hong Kong.

The following table includes a detail of assets and liabilities from contracts with customers included on the Company’s Consolidated Balance Sheets as of the periods indicated:

(dollars in thousands)

JUNE 29, 2025

DECEMBER 29, 2024

Other current assets, net

Deferred gift card sales commissions

$

12,554

$

16,935

Unearned revenue

Deferred gift card revenue

$

299,636

$

366,059

Deferred loyalty revenue

6,892

6,073

Deferred franchise fees - current

530

490

Other

1,358

1,477

Total Unearned revenue

$

308,416

$

374,099

Other long-term liabilities, net

Deferred franchise fees - non-current

$

4,360

$

3,901

The following table is a rollforward of deferred gift card sales commissions for the periods indicated:

THIRTEEN WEEKS ENDED

TWENTY-SIX WEEKS ENDED

(dollars in thousands)

JUNE 29, 2025

JUNE 30, 2024

JUNE 29, 2025

JUNE 30, 2024

Balance, beginning of the period

$

13,127

$

13,520

$

16,935

$

18,081

Deferred gift card sales commissions amortization

(4,870)

(5,163)

(11,767)

(12,661)

Deferred gift card sales commissions capitalization

4,900

4,942

8,873

8,856

Other

(603)

(649)

(1,487)

(1,626)

Balance, end of the period

$

12,554

$

12,650

$

12,554

$

12,650

The following table is a rollforward of unearned gift card revenue for the periods indicated:

The components of Provision for impaired assets and restaurant closings are as follows for the periods indicated:

THIRTEEN WEEKS ENDED

TWENTY-SIX WEEKS ENDED

(dollars in thousands)

JUNE 29, 2025

JUNE 30, 2024

JUNE 29, 2025

JUNE 30, 2024

Impairment losses

U.S.

$

5,680

$

—

$

6,266

$

1,852

Other

—

12,471

—

12,471

Total impairment losses

$

5,680

$

12,471

$

6,266

$

14,323

Restaurant closure (benefits) charges

U.S.

$

(3,726)

$

2,135

$

(3,670)

$

11,219

Other

(414)

78

(706)

15

Total restaurant closure (benefits) charges

(4,140)

2,213

(4,376)

11,234

Provision for impaired assets and restaurant closings (1)

$

1,540

$

14,684

$

1,890

$

25,557

________________

(1)For the thirteen and twenty-six weeks ended June 30, 2024, primarily related to the Q2 2024 decision to close nine restaurants in Hong Kong and the closure of 36 predominantly older, underperforming U.S. restaurants (the “2023 Restaurant Closures”).

The following table presents the computation of basic and diluted earnings (loss) per share for the periods indicated:

THIRTEEN WEEKS ENDED

TWENTY-SIX WEEKS ENDED

(in thousands, except per share data)

JUNE 29, 2025

JUNE 30, 2024

JUNE 29, 2025

JUNE 30, 2024

Net income (loss) attributable to Bloomin’ Brands

$

25,419

$

28,403

$

67,571

$

(55,469)

Net income from discontinued operations, net of tax

779

3,655

525

6,563

Net income (loss) attributable to Bloomin’ Brands from continuing operations

$

24,640

$

24,748

$

67,046

$

(62,032)

Basic weighted average common shares outstanding

85,041

86,688

84,971

86,856

Effect of dilutive securities:

Stock-based compensation awards

99

290

151

—

Convertible senior notes (1)

—

1,005

13

—

Warrants (1)

—

649

—

—

Diluted weighted average common shares outstanding

85,140

88,632

85,135

86,856

Basic earnings (loss) per share:

Continuing operations

$

0.29

$

0.29

$

0.79

$

(0.71)

Discontinued operations

0.01

0.04

0.01

0.08

Net basic earnings (loss) per share

$

0.30

$

0.33

$

0.80

$

(0.64)

Diluted earnings (loss) per share:

Continuing operations

$

0.29

$

0.28

$

0.79

$

(0.71)

Discontinued operations

0.01

0.04

0.01

0.08

Net diluted earnings (loss) per share

$

0.30

$

0.32

$

0.79

$

(0.64)

Antidilutive stock-based compensation awards

1,754

998

1,953

1,193

Antidilutive convertible senior notes and warrants (2)

1,682

—

1,835

4,554

________________

(1)During the thirteen weeks ended June 29, 2025, the 2025 Notes matured and were settled in cash and the proportional warrants were terminated. See Note 9 - Convertible Senior Notes for additional details.

(2)For the thirteen and twenty-six weeks ended June 29, 2025, the Company’s share price was lower than the conversion and strike price related to the 2025 Notes and related warrants, respectively, which resulted in antidilutive shares. For the twenty-six weeks ended June 30, 2024, as a result of the loss from continuing operations, securities are classified as antidilutive.

The following table presents a summary of the Company’s performance-based share units (“PSUs”) and restricted stock units (“RSUs”) activity:

WEIGHTED AVERAGE GRANT DATE FAIR VALUE PER UNIT

AGGREGATE INTRINSIC VALUE (1)

(in thousands, except per unit data)

PSUs

RSUs

PSUs

RSUs

PSUs

RSUs

Outstanding as of December 29, 2024

722

1,044

$

27.42

$

19.80

$

8,860

$

12,814

Granted (2)

312

922

$

7.75

$

7.83

Performance adjustment (3)

(229)

—

$

26.10

$

—

Vested

—

(266)

$

—

$

24.13

Forfeited

(176)

(154)

$

27.53

$

21.53

Outstanding as of June 29, 2025

629

1,546

$

18.13

$

11.75

$

5,445

$

13,387

Expected to vest as of June 29, 2025 (4)

309

1,546

$

2,678

$

13,387

________________

(1)Based on the $12.27 and $8.66 share price of the Company’s common stock on December 27, 2024 and June 27, 2025, the last trading day of the year ended December 29, 2024 and the twenty-six weeks ended June 29, 2025, respectively.

(2)The weighted average dividend yield was 6.40% and 6.60% for PSUs and RSUs, respectively. For PSUs, a new performance structure was used for grants beginning in 2025. The new structure contains separate performance goals that are set at the beginning of each of the three annual performance periods and units earned based on performance will cliff vest after three years.

(3)Represents adjustment to 0% payout for PSUs granted during 2022.

(4)For PSUs, the estimated number of units to be issued upon the vesting of outstanding PSUs is based on Company performance projections of performance criteria set forth in the 2023, 2024 and 2025 PSU award agreements.

The following represents unrecognized stock-based compensation expense and the remaining weighted average recognition period as of June 29, 2025:

UNRECOGNIZED COMPENSATION EXPENSE (dollars in thousands)

REMAINING WEIGHTED AVERAGE RECOGNITION PERIOD (in years)

Performance-based share units

$

2,132

2.7

Restricted stock units

$

13,842

2.0

8. Supplemental Balance Sheet Information

Other current assets, net, consisted of the following as of the periods indicated:

Goodwill and Intangible Assets - The Company performs its annual assessment for impairment of goodwill and other indefinite-lived intangible assets during its second fiscal quarter. During the thirteen weeks ended June 29, 2025, the Company performed a quantitative impairment analysis due to the recent decline in the Company’s market capitalization, while its 2024 assessment was qualitative. In connection with these assessments, the Company did not record any impairment charges.

The goodwill analysis indicated that all reporting units had fair values that exceeded their carrying values. However, the Outback Steakhouse and Bonefish Grill reporting units had fair values that decreased to approximately 10% above their respective carrying values. The fair values for the Outback Steakhouse and Bonefish Grill reporting units decreased primarily due to lower cash flow estimates, increased discount rates, lower market multiples, and additionally for Bonefish Grill, a lower long-term growth rate, compared to the last quantitative impairment analysis performed during the quarter ended June 25, 2023.

The quantitative impairment analysis for indefinite-lived intangible assets indicated that all trade names had fair values exceeding their carrying values; however, the Outback Steakhouse trade name’s fair value decreased to approximately 15% above its carrying value. Similar to the goodwill analysis, the fair value of the Outback Steakhouse trade name decreased primarily due to lower projected system-wide sales and an increased discount rate.

Fair value determinations require considerable judgement and are sensitive to changes in underlying assumptions, estimates and market factors.Key assumptions include cash flow estimates (including sales and operating profit), long-term growth rates, discount rates, royalty rates, market multiples and other market factors. Sales declines, unplanned increases in commodity or labor costs, decreases to the market multiples, increases in discount rates, deterioration in overall economic conditions and challenges in the restaurant industry or any such event may impact the Company’s fair value determinations and may result in future impairment charges. It is possible that changes in circumstances or changes in assumptions and estimates could result in impairment of the Company’s goodwill or other intangible assets. Further, as a result of the decreased fair values, the Outback Steakhouse and Bonefish Grill reporting units and the Outback Steakhouse trade name are at a higher risk of future impairment.

Other assets, net, consisted of the following as of the periods indicated:

The Company’s 5.00% convertible senior notes due in 2025 (the “2025 Notes”) matured on May 1, 2025, and were settled in cash for $20.7 million, excluding accrued interest. In connection with the maturity of the 2025 Notes, the related convertible note hedges entered into with certain purchasers of the 2025 Notes and/or their respective affiliates and other financial institutions expired. On May 16, 2025, the Company terminated the remaining proportional warrants in cash for $0.4 million.

The following table includes the outstanding principal amount and carrying value of the2025 Notes as of the period indicated:

(dollars in thousands)

DECEMBER 29, 2024

Principal

$

20,724

Less: unamortized debt issuance costs

(56)

Net carrying amount

$

20,668

Following is a summary of interest expense for the 2025 Notes by component for the periods indicated:

THIRTEEN WEEKS ENDED

TWENTY-SIX WEEKS ENDED

(dollars in thousands)

JUNE 29, 2025

JUNE 30, 2024

JUNE 29, 2025

JUNE 30, 2024

Coupon interest

$

86

$

259

$

345

$

1,265

Debt issuance cost amortization

14

40

56

198

Total interest expense (1)

$

100

$

299

$

401

$

1,463

________________

(1)The effective rate of the 2025 Notes was 5.85%.

10. Stockholders’ Equity

Dividends - The Company declared and paid dividends per share during fiscal year 2025 as follows:

(dollars in thousands, except per share data)

DIVIDENDS PER SHARE

AMOUNT

First fiscal quarter

$

0.15

$

12,747

Second fiscal quarter

0.15

12,759

Total cash dividends declared and paid

$

0.30

$

25,506

In July 2025, the Company’s Board of directors (the “Board”) declared a quarterly cash dividend of $0.15 per share, payable on September 3, 2025 to shareholders of record at the close of business on August 19, 2025.

Accumulated Other Comprehensive Income (Loss) - The following table is a rollforward of the components of Accumulated Other Comprehensive Income (Loss) for the periods indicated:

THIRTEEN WEEKS ENDED

TWENTY-SIX WEEKS ENDED

(dollars in thousands)

JUNE 29, 2025

JUNE 30, 2024

JUNE 29, 2025

JUNE 30, 2024

Foreign currency translation:

Balance, beginning of the period

$

3,023

$

(179,620)

$

(212,172)

$

(177,689)

Foreign currency translation adjustment (1)

1,731

(9,858)

(622)

(11,789)

Reclassification of foreign currency translation adjustments into earnings due to sale of business

—

—

217,548

—

Balance, end of the period

$

4,754

$

(189,478)

$

4,754

$

(189,478)

(Loss) gain on derivatives, net of tax:

Balance, beginning of the period

$

(798)

$

542

$

(621)

$

(615)

Change in fair value of derivatives, net of tax

263

898

63

2,333

Reclassification realized in Net income (loss), net of tax

27

(568)

50

(846)

Balance, end of the period

$

(508)

$

872

$

(508)

$

872

Accumulated other comprehensive income (loss):

Balance beginning of the period

$

2,225

$

(179,078)

$

(212,793)

$

(178,304)

Other comprehensive income (loss) attributable to Bloomin' Brands

2,021

(9,528)

217,039

(10,302)

Balance, end of the period

$

4,246

$

(188,606)

$

4,246

$

(188,606)

____________________

(1)For the thirteen and twenty-six weeks ended June 29, 2025, represents foreign currency translation adjustments primarily related to the Company’s equity method investment.

11. Derivative Instruments and Hedging Activities

Cash Flow Hedges of Interest Rate Risk - In March 2024 and December 2023, OSI entered into 11 interest rate swap agreements with ten counterparties (the “Swap Transactions”) to manage its exposure to fluctuations in variable interest rates that include one and two-year tenors. The remaining Swap Transactions have an aggregate notional amount of $275.0 million with the following terms:

NOTIONAL AMOUNT

WEIGHTED AVERAGE FIXED INTEREST RATE (1)

EFFECTIVE DATE

TERMINATION DATE

$

100,000,000

4.34%

December 29, 2023

December 31, 2025

175,000,000

4.40%

March 29, 2024

March 31, 2026

$

275,000,000

4.38%

____________________

(1)The weighted average fixed interest rate excludes the term SOFR adjustment and interest rate spread described below.

In connection with the remaining Swap Transactions, the Company effectively converted $275.0 million of its outstanding indebtedness from SOFR, plus a term SOFR adjustment of 0.10% and a spread of 150 to 250 basis points, to the weighted average fixed interest rates within the table above, plus a term SOFR adjustment of 0.10% and a spread of 150 to 250 basis points. The Swap Transactions have an embedded floor of minus 0.10%.

The Swap Transactions have been designated and qualify as cash flow hedges, are recognized on the Company’s Consolidated Balance Sheets at fair value and are classified based on the instruments’maturity dates. The Company estimates $0.7 million of interest expense will be reclassified from Accumulated Other Comprehensive Income (Loss) to Interest expense, net over the next 12 months related to the Swap Transactions.

The following table presents the fair value and classification of the Company’s swap agreements as of the periods indicated:

(dollars in thousands)

CONSOLIDATED BALANCE SHEETS CLASSIFICATION

JUNE 29, 2025

DECEMBER 29, 2024

Interest rate swaps - liability

Accrued and other current liabilities

$

683

$

579

Interest rate swaps - liability

Other long-term liabilities, net

—

255

Total fair value of derivative instruments - liabilities (1)

$

683

$

834

____________________

(1)See Note 13 - Fair Value Measurements for fair value discussion of the interest rate swaps.

By utilizing the interest rate swaps, the Company is exposed to credit-related losses in the event that the counterparty fails to perform under the terms of the derivative contract. To mitigate this risk, the Company enters into derivative contracts with major financial institutions based upon credit ratings and other factors. The Company continually assesses the creditworthiness of its counterparties. As of June 29, 2025, all counterparties to the Swap Transactions performed in accordance with their contractual obligations.

The Swap Transactions contain provisions whereby the Company could be declared in default on its derivative obligations if the repayment of the underlying indebtedness is accelerated by the lender due to the Company’s default on indebtedness. If the Company had breached any of these provisions as of June 29, 2025 and December 29, 2024, it could have been required to settle its obligations under the Swap Transactions at their termination value of $0.7 million and $0.8 million, respectively. As of June 29, 2025 and December 29, 2024, the Company has not posted any collateral related to the Swap Transactions.

Non-Designated Hedges

During the fourth quarter of 2024, the Company entered into foreign currency forward contracts to partially offset the foreign currency exchange gains and losses generated by the Brazilian Reais rate risk associated with the purchase price installment payments from the Brazil Sale Transaction. As of June 29, 2025, the Company had R$720.0 million Brazilian Reais (approximately $130.6 million U.S. Dollars) of outstanding notional amounts related to its foreign currency forward contracts. The asset related to the foreign exchange forward contracts as of June 29, 2025 and December 29, 2024 is not material as they are short term and typically mature monthly. As of June 29, 2025 and December 29, 2024, the Company has not posted any collateral related to the foreign currency forward contracts.

The following table summarizes the effects of the Company’s foreign exchange forward contracts on the Consolidated Statements of Operations and Comprehensive Income (Loss) for the periods indicated:

CONSOLIDATED STATEMENTS OF OPERATIONS AND COMPREHENSIVE INCOME (LOSS) CLASSIFICATION

THIRTEEN WEEKS ENDED

TWENTY-SIX WEEKS ENDED

(dollars in thousands)

JUNE 29, 2025

JUNE 29, 2025

Loss on foreign currency forward contracts (1)

General and administrative

$

8,461

$

18,711

____________________

(1)The loss on foreign currency forward contracts is materially offset within General and administrative expense by the gains on foreign currency exchange related to the installment receivable from the Brazil Sale Transaction.

The Company’s interest rate swaps and foreign currency forward contracts are subject to master netting arrangements. As of June 29, 2025, the Company elected not to offset derivative positions in its Consolidated Balance Sheet with the same counterparty under the same agreement.

The following table includes a detail of lease assets and liabilities included on the Company’s Consolidated Balance Sheets as of the periods indicated:

(dollars in thousands)

CONSOLIDATED BALANCE SHEETS CLASSIFICATION

JUNE 29, 2025

DECEMBER 29, 2024

Operating lease right-of-use assets

Operating lease right-of-use assets

$

1,015,518

$

1,012,857

Finance lease right-of-use assets (1)

Property, fixtures and equipment, net

13,433

10,058

Total lease assets, net

$

1,028,951

$

1,022,915

Current operating lease liabilities

Current operating lease liabilities

$

162,509

$

158,806

Current finance lease liabilities

Accrued and other current liabilities

3,668

2,618

Non-current operating lease liabilities

Non-current operating lease liabilities

1,077,983

1,088,518

Non-current finance lease liabilities

Other long-term liabilities, net

11,589

8,359

Total lease liabilities

$

1,255,749

$

1,258,301

________________

(1)Net of accumulated amortization of $5.3 million and $4.0 million as of June 29, 2025 and December 29, 2024, respectively.

Following is a summary of expenses and income related to leases recognized in the Company’s Consolidated Statements of Operations and Comprehensive Income (Loss) for the periods indicated:

CONSOLIDATED STATEMENTS OF OPERATIONS AND COMPREHENSIVE INCOME (LOSS) CLASSIFICATION

THIRTEEN WEEKS ENDED

TWENTY-SIX WEEKS ENDED

(dollars in thousands)

JUNE 29, 2025

JUNE 30, 2024

JUNE 29, 2025

JUNE 30, 2024

Operating lease cost (1)

Other restaurant operating

$

42,623

$

42,364

$

84,928

$

85,296

Variable lease cost

Other restaurant operating

1,294

941

2,486

1,995

Finance lease costs:

Amortization of leased assets

Depreciation and amortization

750

511

1,440

1,024

Interest on lease liabilities

Interest expense, net

261

169

500

344

Sublease revenue

Franchise and other revenues

(1,745)

(1,832)

(3,447)

(3,567)

Lease costs, net

$

43,183

$

42,153

$

85,907

$

85,092

________________

(1)Excludes rent expense for office facilities and closed or subleased properties of $3.4 million and $3.6 million for the thirteen weeks ended June 29, 2025 and June 30, 2024, respectively, and $7.0 million for the twenty-six weeks ended June 29, 2025 and June 30, 2024, which is included in General and administrative expense.

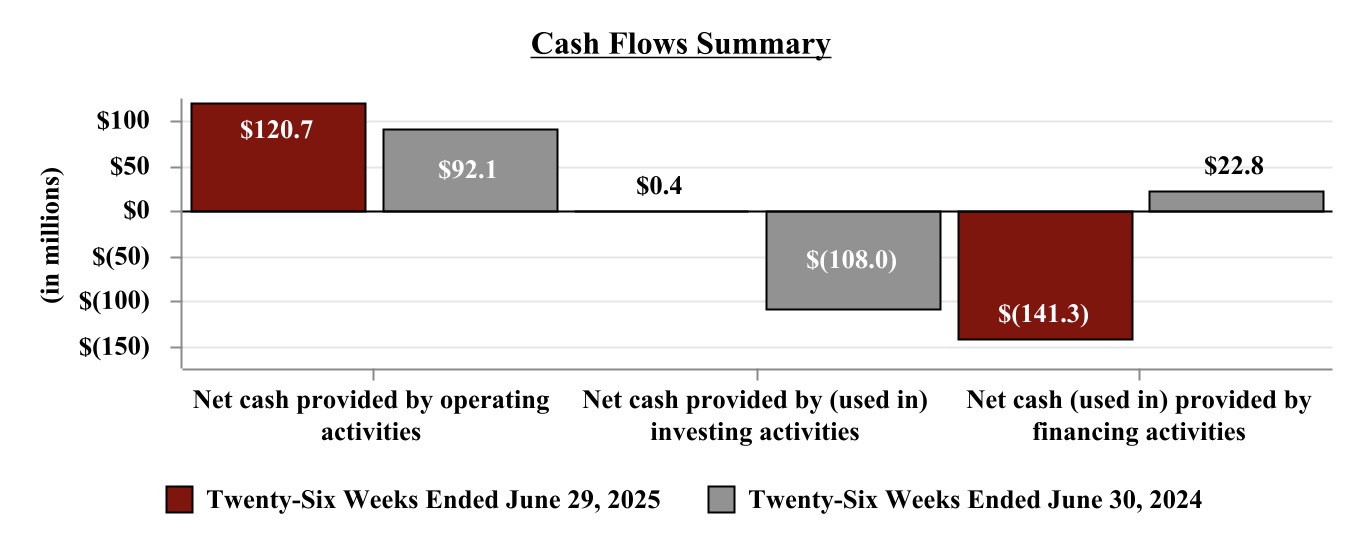

The following table is a summary of cash flow impacts to the Company’s Consolidated Financial Statements related to its leases for the periods indicated:

TWENTY-SIX WEEKS ENDED

(dollars in thousands)

JUNE 29, 2025

JUNE 30, 2024

Cash flows from operating activities:

Cash paid for amounts included in the measurement of operating lease liabilities

Fair value is the price that would be received for an asset or paid to transfer a liability, or the exit price, in an orderly transaction between market participants on the measurement date. Fair value is categorized into one of the following three levels based on the lowest level of significant input:

Level 1

Unadjusted quoted market prices in active markets for identical assets or liabilities

Level 2

Observable inputs available at measurement date other than quoted prices included in Level 1

Level 3

Unobservable inputs that cannot be corroborated by observable market data

Fair Value Measurements on a Recurring Basis - The following table summarizes the Company’s financial assets and liabilities measured at fair value by hierarchy level on a recurring basis as of the periods indicated:

CONSOLIDATED BALANCE SHEETS CLASSIFICATION

MEASUREMENT LEVEL

FAIR VALUE

(dollars in thousands)

JUNE 29, 2025

DECEMBER 29, 2024

Assets:

Short-term investments

Cash and cash equivalents

Level 1

$

5,026

$

11,868

Foreign currency forward contracts

Other current assets, net

Level 2

$

282

$

304

Liabilities:

Interest rate swaps

Accrued and other current liabilities

Level 2

$

683

$

579

Interest rate swaps

Other long-term liabilities

Level 2

$

—

$

255

Fair value of each class of financial instruments is determined based on the following:

FINANCIAL INSTRUMENT

METHODS AND ASSUMPTIONS

Short-term investments

Carrying value approximates fair value because maturities are less than three months.

Derivative instruments

The Company’s derivative instruments include interest rate swaps and foreign currency forward contracts. Fair value measurements are based on the contractual terms of the derivatives and observable market-based inputs. Interest rate swaps are valued using a discounted cash flow analysis on the expected cash flows of each derivative using observable inputs including interest rate curves and credit spreads. Foreign currency forwards are valued by comparing the contracted forward exchange rate to the current market forward exchange rate. Key inputs for the valuation of the foreign currency forwards are spot rates, foreign currency forward rates and the interest rate curve of the domestic currency. The Company also considers its own nonperformance risk and the respective counterparty’s nonperformance risk in the fair value measurements. As of June 29, 2025 and December 29, 2024, the Company determined that the credit valuation adjustments were not significant to the overall valuation of its derivatives.

Interim Disclosures about Fair Value of Financial Instruments - The Company’s non-derivative financial instruments consist of cash equivalents, accounts receivable, accounts payable and long-term debt. The fair values of cash equivalents, accounts receivable, including the second installment receivable related to the Brazil Sale Transaction, and accounts payable approximate their carrying amounts reported on the Company’s Consolidated Balance Sheets due to their short duration.

Debt is carried at amortized cost; however, the Company estimates the fair value of debt for disclosure purposes. The following table includes the carrying value and fair value of the Company’s debt by hierarchy level as of the periods indicated:

(1)On May 1, 2025, the 2025 Notes matured and were settled in cash. See Note 9 - Convertible Senior Notes for additional details.

14. Income Taxes

THIRTEEN WEEKS ENDED

TWENTY-SIX WEEKS ENDED

(dollars in thousands)

JUNE 29, 2025

JUNE 30, 2024

JUNE 29, 2025

JUNE 30, 2024

Income (loss) before (benefit) provision for income taxes

$

18,951

$

28,756

$

64,995

$

(49,800)

(Benefit) provision for income taxes

$

(8,748)

$

2,780

$

(7,845)

$

9,422

Effective income tax rate

(NM)

9.7

%

(12.1)

%

(18.9)

%

________________

NM Not meaningful.

For the thirteen weeks ended June 29, 2025 and June 30, 2024, the (benefit) provision for income taxes includes the impact of changes to the estimate of forecasted annual pre-tax book income relative to the prior quarter in each respective year and the benefit of FICA tax credits on certain tipped wages.

The effective income tax rate for the twenty-six weeks ended June 29, 2025 includes the benefit of FICA tax credits on certain tipped wages relative to forecasted annual pre-tax book income which resulted in a negative effective income tax rate.

The effective income tax rate for the twenty-six weeks ended June 30, 2024 includes the impact of the non-deductible losses associated with the repurchase of $83.6 million of the outstanding 2025 Notes (the “Second 2025 Notes Partial Repurchase”) recorded in the twenty-six weeks ended June 30, 2024, which, relative to a pre-tax book loss, resulted in a negative effective income tax rate.

In the U.S., a restaurant company employer may claim a credit against its federal income taxes for FICA taxes paid on certain tipped wages (the “FICA tax credit”). The level of FICA tax credits is primarily driven by U.S. Restaurant sales and is not impacted by costs incurred that may reduce Income (loss) before (benefit) provision for income taxes.

The effective income tax rates for the thirteen weeks ended June 29, 2025 and June 30, 2024 and the twenty-six weeks ended June 29, 2025 were lower than the Company’s blended federal and state statutory rate of approximately 26% primarily due to the benefit of FICA tax credits on certain tipped wages. The effective income tax rate for the twenty-six weeks ended June 30, 2024 was lower than the Company’s blended federal and state statutory rate of approximately 26% primarily due to the impact of the non-deductible losses associated with the Second 2025 Notes Partial Repurchase partially offset by the benefit of FICA tax credits on certain tipped wages, which, relative to a pre-tax book loss, resulted in a negative effective income tax rate.

On July 4, 2025, the One Big Beautiful Bill Act (“OBBBA”) was signed into law, which enacted or modified, among other things, several business tax rules. The Company is currently evaluating the potential impact of the OBBBA and does not anticipate it will have a material impact on the Company’s financial statements.

15. Commitments and Contingencies

Litigation and Other Matters - The Company recorded reserves of $2.1 million and $2.3 million for certain of its outstanding legal proceedings as of June 29, 2025 and December 29, 2024, respectively, within Accrued and other current liabilities on its Consolidated Balance Sheets. While the Company believes that additional losses beyond these accruals are reasonably possible, it cannot estimate a possible loss contingency or range of reasonably possible loss contingencies beyond these accruals.

Lease Guarantees - The Company assigned its interest, and is contingently liable, under certain real estate leases. These leases have varying terms, the latest of which expires in 2032. As of June 29, 2025, the undiscounted payments that the Company could be required to make in the event of non-payment by the primary lessees was $11.3 million. The present value of these potential payments discounted at the Company’s incremental borrowing rate as of June 29, 2025 was $8.7 million. In the event of default, the indemnity clauses in the Company’s purchase and sale agreements generally govern its ability to pursue and recover damages incurred. As of June 29, 2025 and December 29, 2024, the Company’s recorded contingent lease liability was $1.7 million and $1.6 million, respectively.

16. Segment Reporting

The following is a summary of reportable segments:

REPORTABLE SEGMENT

CONCEPT

GEOGRAPHIC LOCATION

U.S. (1)

Outback Steakhouse

United States of America

Carrabba’s Italian Grill

Bonefish Grill

Fleming’s Prime Steakhouse & Wine Bar

International Franchise

Outback Steakhouse

12 Franchise Markets

Carrabba’s Italian Grill (Abbraccio)

_________________

(1)Includes franchise locations.

Segment accounting policies are the same as those described in Note 2 - Summary of Significant Accounting Policies in the Company’s Annual Report on Form 10-K for the year ended December 29, 2024. Revenues for all segments include only transactions with customers and exclude intersegment revenues. There were no material transactions among reportable segments. Excluded from Income from operations for U.S. are certain legal and corporate costs not directly related to the performance of the segment, most stock-based compensation expenses, a portion of insurance expenses and certain bonus expenses. The below segment disclosures have been recast to include amounts that relate solely to the Company’s continuing operations. In the tables below, “other” includes amounts related to its Hong Kong subsidiary.

The following table is a reconciliation of segment income from operations to Income (loss) before (benefit) provision for income taxes for the periods indicated:

THIRTEEN WEEKS ENDED

TWENTY-SIX WEEKS ENDED

(dollars in thousands)

JUNE 29, 2025

JUNE 30, 2024

JUNE 29, 2025

JUNE 30, 2024

Total segment income from operations

$

75,299

$

88,727

$

171,973

$

195,900

Unallocated corporate operating expense

(46,422)

(32,286)

(86,190)

(68,025)

Other income (loss) from operations

773

(12,389)

1,098

(12,906)

Total income from operations

29,650

44,052

86,881

114,969

Loss on extinguishment of debt

—

—

—

(135,797)

Interest expense, net

(10,699)

(15,296)

(21,886)

(28,972)

Income (loss) before (benefit) provision for income taxes

$

18,951

$

28,756

$

64,995

$

(49,800)

The following table is a summary of depreciation and amortization by segment for the periods indicated:

THIRTEEN WEEKS ENDED

TWENTY-SIX WEEKS ENDED

(dollars in thousands)

JUNE 29, 2025

JUNE 30, 2024

JUNE 29, 2025

JUNE 30, 2024

Depreciation and amortization

U.S.

$

42,145

$

40,616

$

83,758

$

80,584

Corporate

2,205

2,214

4,289

4,267

Other

248

560

498

1,239

Total depreciation and amortization

$

44,598

$

43,390

$

88,545

$

86,090

The following table is a summary of capital expenditures by segment, excluding non-cash activity, for the periods indicated:

TWENTY-SIX WEEKS ENDED

(dollars in thousands)

JUNE 29, 2025

JUNE 30, 2024

Capital expenditures

U.S.

$

76,906

$

103,691

Corporate

7,380

3,836

Other

11

715

Total capital expenditures

$

84,297

$

108,242

The following table sets forth Total assets by segment as of the periods indicated:

(dollars in thousands)

JUNE 29, 2025

DECEMBER 29, 2024

Assets

U.S.

$

2,630,373

$

2,735,251

International Franchise

105,776

103,242

Total segment assets

2,736,149

2,838,493

Corporate

494,822

306,560

Other (1)

76,577

16,262

Assets of discontinued operations held for sale

—

223,490

Total assets

$

3,307,548

$

3,384,805

_________________

(1)Includes the Company’s equity method investment in Brazil.

Item 2. Management’s Discussion and Analysis of Financial Condition and Results of Operations

Management’s discussion and analysis of financial condition and results of operations should be read in conjunction with our unaudited consolidated financial statements and the related notes. Unless the context otherwise indicates, as used in this report, the term the “Company,” “we,” “us,” “our” and other similar terms mean Bloomin’ Brands, Inc. and its subsidiaries.

Cautionary Statement

This Quarterly Report on Form 10-Q (the “Report”) includes statements that express our opinions, expectations, beliefs, plans, objectives, assumptions or projections regarding future events or future results and therefore are, or may be deemed to be, “forward-looking statements” within the meaning of Section 27A of the Securities Act of 1933, as amended (the “Securities Act”), and Section 21E of the Securities Exchange Act of 1934, as amended (the “Exchange Act”). These forward-looking statements can generally be identified by the use of forward-looking terminology, including the terms “believes,” “estimates,” “anticipates,” “expects,” “feels,” “seeks,” “forecasts,” “projects,” “intends,” “plans,” “may,” “will,” “should,” “could” or “would” or, in each case, their negative or other variations or comparable terminology, although not all forward-looking statements are accompanied by such terms. These forward-looking statements include all matters that are not historical facts. They appear in a number of places throughout this Report and include statements regarding our intentions, beliefs or current expectations concerning, among other things, our results of operations, financial condition, liquidity, prospects, growth, strategies and the industry in which we operate.

By their nature, forward-looking statements involve risks and uncertainties because they relate to events and depend on circumstances that may or may not occur in the future. Although we base these forward-looking statements on assumptions that we believe are reasonable when made, we caution you that forward-looking statements are not guarantees of future performance and that our actual results of operations, financial condition and liquidity, and industry developments may differ materially from statements made in or suggested by the forward-looking statements contained in this Report. In addition, even if our results of operations, financial condition and liquidity, and industry developments are consistent with the forward-looking statements contained in this Report, those results or developments may not be indicative of results or developments in subsequent periods. Important factors that could cause actual results to differ materially from statements made or suggested by forward-looking statements include, but are not limited to, the following:

(i)Consumer reactions to public health and food safety issues;

(ii)Minimum wage increases, additional mandated employee benefits and fluctuations in the cost and availability of employees;

(iii)Our ability to recruit and retain high-quality leadership, restaurant-level management and team members;

(iv)Economic and geopolitical conditions, including recent tariff developments, and their effects on consumer confidence and discretionary spending, consumer traffic, the cost and availability of credit and interest rates;

(v)Our ability to compete in the highly competitive restaurant industry with many well-established competitors and new market entrants;

(vi)Our ability to protect our information technology systems from interruption or security breach, including cybersecurity threats, and to protect consumer data and personal employee information;

FINANCIAL CONDITION AND RESULTS OF OPERATIONS - Continued

(vii)Fluctuations in the price and availability of commodities, including supplier freight charges and restaurant distribution expenses, and other impacts of inflation and our dependence on a limited number of suppliers and distributors to meet our beef, pork, chicken and other major product supply needs;

(viii)Our ability to preserve and grow the reputation and value of our brands, particularly in light of changes in consumer engagement with social media platforms and limited control with respect to the operations of our franchisees;

(ix)The effects of international economic, political and social conditions and legal systems on our foreign operations and on foreign currency exchange rates;

(x)The impacts of our operations in Brazil as a minority investor and franchisor following our recent sale transaction;

(xi)Our ability to comply with corporate citizenship and sustainability reporting requirements and investor expectations or our failure to achieve any goals, targets or objectives that we establish with respect to corporate citizenship and sustainability matters;

(xii)Our ability to effectively respond to changes in patterns of consumer traffic, including by maintaining relationships with third-party delivery apps and services, consumer tastes and dietary habits;

(xiii)Our ability to comply with governmental laws and regulations, the costs of compliance with such laws and regulations and the effects of changes or uncertainty with respect to applicable laws and regulations, including tax laws and unanticipated liabilities, and the impact of any litigation;

(xiv)Our ability to implement our remodeling, relocation and expansion plans, due to uncertainty in locating and acquiring attractive sites on acceptable terms, obtaining required permits and approvals, recruiting and training necessary personnel, obtaining adequate financing and estimating the performance of newly opened, remodeled or relocated restaurants, and our cost savings plans to enable reinvestment in our business, due to uncertainty with respect to macroeconomic conditions and the efficiency that may be added by the actions we take;

(xv)Seasonal and periodic fluctuations in our results and the effects of significant adverse weather conditions and other disasters or unforeseen events;

(xvi)The effects of our leverage and restrictive covenants in our various credit facilities on our ability to raise additional capital to fund our operations, to make capital expenditures to invest in new or renovate restaurants and to react to changes in the economy or our industry;

(xvii)Any impairment in the carrying value of our goodwill or other intangible or long-lived assets and its effect on our financial condition and results of operations; and

(xviii)Such other factors as discussed in Part I, Item IA. Risk Factors of our Annual Report on Form 10-K for the year ended December 29, 2024.

Given these risks and uncertainties, we caution you not to place undue reliance on these forward-looking statements. Any forward-looking statement that we make in this Report speaks only as of the date of such statement, and we undertake no obligation to update any forward-looking statement or to publicly announce the results of any revision to any of those statements to reflect future events or developments. Comparisons of results for current and any prior

FINANCIAL CONDITION AND RESULTS OF OPERATIONS - Continued

periods are not intended to express any future trends or indications of future performance, unless specifically expressed as such, and should only be viewed as historical data.

Overview

We are one of the largest casual dining restaurant companies in the world with a portfolio of leading, differentiated restaurant concepts. As of June 29, 2025, we owned and operated 985 restaurants and franchised 494 restaurants across 46 states, Guam and 12 countries. Our restaurant portfolio includes: Outback Steakhouse, Carrabba’s Italian Grill, Bonefish Grill and Fleming’s Prime Steakhouse & Wine Bar.

Financial Overview - Our financial overview for the thirteen weeks ended June 29, 2025 includes the following:

•U.S. combined and Outback Steakhouse comparable restaurant sales of (0.1)% and (0.6)%, respectively;

•Increase in Total revenues of 0.3% as compared to the second quarter of 2024;

•Operating income and restaurant-level operating margins of 3.0% and 12.0%, respectively, as compared to 4.4% and 14.0%, respectively, for the second quarter of 2024;

•Operating income of $29.7 million as compared to $44.1 million in the second quarter of 2024; and

•Diluted earnings per share of $0.29 as compared to $0.28 for the second quarter of 2024.

Key Financial Performance Indicators - Key measures that we use in evaluating our restaurants and assessing our business include the following:

•Average restaurant unit volumes—average sales (excluding gift card breakage) per restaurant to measure changes in customer traffic, pricing and development of the brand.

•Comparable restaurant sales—year-over-year comparison of the change in sales volumes (excluding gift card breakage) for Company-owned restaurants that are open 18 months or more in order to remove the impact of new restaurant openings in comparing the operations of existing restaurants.

•System-wide sales—total restaurant sales volume for all Company-owned and franchise restaurants, regardless of ownership, to interpret the overall health of our brands.

•Restaurant-level operating margin, Income from operations, Net income (loss) and Diluted earnings (loss) per share—financial measures utilized to evaluate our operating performance.

Restaurant-level operating margin is a non-GAAP financial measure widely regarded in the industry as a useful metric to evaluate restaurant-level operating efficiency and performance of ongoing restaurant-level operations, and we use it for these purposes. Our restaurant-level operating margin is expressed as the percentage of our Restaurant sales that Food and beverage costs, Labor and other related expense and Other restaurant operating expense (including advertising expenses) represent, in each case as such items are reflected in our Consolidated Statements of Operations and Comprehensive Income (Loss). The following categories of revenue and operating expenses are not included in restaurant-level operating income and the corresponding margin because we do not consider them reflective of operating performance at the restaurant-level within a period:

(i)Franchise and other revenues, which are earned primarily from franchise royalties and other non-food and beverage revenue streams, such as rental and sublease income;

(ii)Depreciation and amortization, which, although substantially all of which is related to restaurant-level assets, represent historical sunk costs rather than cash outlays for the restaurants;

FINANCIAL CONDITION AND RESULTS OF OPERATIONS - Continued

(iii)General and administrative expense, which includes primarily non-restaurant-level costs associated with support of the restaurants and other activities at our corporate offices; and

(iv)Asset impairment charges and restaurant closing costs, which are not reflective of ongoing restaurant performance in a period.

Restaurant-level operating margin excludes various expenses, as discussed above, that are essential to supporting the operations of our restaurants and may materially impact our Consolidated Statements of Operations and Comprehensive Income (Loss). As a result, restaurant-level operating margin is not indicative of our consolidated results of operations and is presented exclusively as a supplement to, and not a substitute for, Net income (loss) or Income from operations. In addition, our presentation of restaurant-level operating margin may not be comparable to similarly titled measures used by other companies in our industry.

•Adjusted restaurant-level operating margin, Adjusted income from operations, Adjusted net income and Adjusted diluted earnings per share—non-GAAP financial measures utilized to evaluate our operating performance.

We believe that our use of these non-GAAP financial measures permits investors to assess the operating performance of our business relative to our performance based on U.S. GAAP results and relative to other companies within the restaurant industry by isolating the effects of certain items that may vary from period to period without correlation to core operating performance or that vary widely among similar companies. However, our inclusion of these adjusted measures should not be construed as an indication that our future results will be unaffected by unusual or infrequent items or that the items for which we have made adjustments are unusual or infrequent or will not recur. We believe that the disclosure of these non-GAAP measures is useful to investors as they form part of the basis for how our management team and Board evaluate our operating performance, allocate resources and administer employee incentive plans.

FINANCIAL CONDITION AND RESULTS OF OPERATIONS - Continued

Selected Operating Data - The table below presents the number of our restaurants in operation as of the periods indicated:

Number of restaurants (at end of the period):

JUNE 29, 2025

JUNE 30, 2024

U.S.

Outback Steakhouse

Company-owned

557

549

Franchised

121

125

Total

678

674

Carrabba’s Italian Grill

Company-owned

191

192

Franchised

17

18

Total

208

210

Bonefish Grill

Company-owned

162

162

Franchised

4

4

Total

166

166

Fleming’s Prime Steakhouse & Wine Bar

Company-owned

65

63

Aussie Grill

Company-owned

—

4

Franchised

1

2

Total

1

6

U.S. total

1,118

1,119

International Franchise

Outback Steakhouse - Brazil (1)

185

—

Outback Steakhouse - South Korea

100

93

Other (1)

66

50

International Franchise total

351

143

International other - Company-owned

Outback Steakhouse - Hong Kong/China

10

20

Outback Steakhouse - Brazil (1)

—

165

Other - Brazil (1)

—

18

System-wide total

1,479

1,465

System-wide total - Company-owned

985

1,173

System-wide total - Franchised

494

292

____________________

(1)The June 30, 2024 restaurant counts for Brazil, are reported as of May 31, 2024, to correspond with the balance sheet date of this subsidiary. Following the close of the Brazil Sale Transaction on December 30, 2024, all restaurants in that market operate as unconsolidated franchisees and the related store count is no longer reported on a one-month lag. See Note 2 - Discontinued Operations of the Notes to Consolidated Financial Statements for further details.

FINANCIAL CONDITION AND RESULTS OF OPERATIONS - Continued

Results of Operations

REVENUES

Restaurant Sales - Following is a summary of the change in Restaurant sales for the periods indicated:

(dollars in millions)

THIRTEEN WEEKS ENDED

TWENTY-SIX WEEKS ENDED

For the periods ended June 30, 2024

$

977.8

$

2,024.5

Change from:

Restaurant openings (1)

19.0

35.4

Restaurant closures (2)

(12.9)

(40.4)

Comparable restaurant sales

(0.2)

(5.5)

Other

1.1

0.3

For the periods ended June 29, 2025

$

984.8

$

2,014.3

________________

(1)The thirteen and twenty-six weeks ended June 29, 2025 include restaurant sales from 32 new restaurants not included in our comparable restaurant sales base.

(2)The thirteen and twenty-six weeks ended June 29, 2025 include the restaurant sales impact from the closure of 23 and 60 restaurants since March 31, 2024 and December 31, 2023, respectively.

Average Restaurant Unit Volumes and Operating Weeks - Following is a summary of the average restaurant unit volumes and operating weeks for the periods indicated:

FINANCIAL CONDITION AND RESULTS OF OPERATIONS - Continued

Comparable Restaurant Sales, Traffic and Average Check Per Person (Decreases) Increases - Following is a summary of comparable restaurant sales, traffic and average check per person (decreases) increases for the periods indicated:

THIRTEEN WEEKS ENDED

TWENTY-SIX WEEKS ENDED

JUNE 29, 2025

JUNE 30, 2024

JUNE 29, 2025

JUNE 30, 2024

Year over year percentage change:

Comparable restaurant sales (restaurants open 18 months or more):

U.S. (1)

Outback Steakhouse

(0.6)

%

(0.1)

%

(0.9)

%

(0.7)

%

Carrabba’s Italian Grill

3.9

%

2.0

%

2.6

%

1.2

%

Bonefish Grill

(5.8)

%

(2.0)

%

(4.9)

%

(3.5)

%

Fleming’s Prime Steakhouse & Wine Bar

3.8

%

(1.1)

%

4.5

%

(1.5)

%

Combined U.S.

(0.1)

%

(0.1)

%

(0.3)

%

(0.9)

%

Traffic:

U.S.

Outback Steakhouse

(1.0)

%

(4.1)

%

(2.6)

%

(4.1)

%

Carrabba’s Italian Grill

0.7

%

(1.8)

%

0.2

%

(2.3)

%

Bonefish Grill

(11.4)

%

(4.8)

%

(10.4)

%

(6.0)

%

Fleming’s Prime Steakhouse & Wine Bar

(0.6)

%

(8.2)

%

(0.5)

%

(6.5)

%

Combined U.S.

(2.0)

%

(3.8)

%

(3.0)

%

(4.1)

%

Average check per person (2):

U.S.

Outback Steakhouse

0.4

%

4.0

%

1.7

%

3.4

%

Carrabba’s Italian Grill

3.2

%

3.8

%

2.4

%

3.5

%

Bonefish Grill

5.6

%

2.8

%

5.5

%

2.5

%

Fleming’s Prime Steakhouse & Wine Bar

4.4

%

7.1

%

5.0

%

5.0

%

Combined U.S.

1.9

%

3.7

%

2.7

%

3.2

%

____________________

(1)Relocated restaurants closed more than 60 days are excluded from comparable restaurant sales until at least 18 months after reopening.

(2)Includes the impact of menu pricing changes, product mix and discounts.

FINANCIAL CONDITION AND RESULTS OF OPERATIONS - Continued

COSTS AND EXPENSES

The following table sets forth the percentages of certain items in our Consolidated Statements of Operations in relation to Restaurant sales or Total revenues for the periods indicated:

THIRTEEN WEEKS ENDED

TWENTY-SIX WEEKS ENDED

JUNE 29, 2025

JUNE 30, 2024

JUNE 29, 2025

JUNE 30, 2024

Revenues

Restaurant sales

98.2

%

97.8

%

98.2

%

97.9

%

Franchise and other revenues

1.8

2.2

1.8

2.1

Total revenues

100.0

100.0

100.0

100.0

Costs and expenses

Food and beverage (1)

30.3

30.1

30.4

30.1

Labor and other related (1)

32.0

30.7

31.3

30.4

Other restaurant operating (1)

25.7

25.2

25.4

24.7

Depreciation and amortization

4.4

4.3

4.3

4.2

General and administrative

5.9

5.6

5.9

5.6

Provision for impaired assets and restaurant closings

0.2

1.5

0.1

1.2

Total costs and expenses

97.0

95.6

95.8

94.4

Income from operations

3.0

4.4

4.2

5.6

Loss on extinguishment of debt

—

—

—

(6.6)

Interest expense, net

(1.1)

(1.5)

(1.0)

(1.4)

Income (loss) before (benefit) provision for income taxes

1.9

2.9

3.2

(2.4)

(Benefit) provision for income taxes

(0.9)

0.3

(0.4)

0.5

Loss from equity method investment, net of tax

(0.2)

—

(0.2)

—

Net income (loss) from continuing operations

2.6

2.6

3.4

(2.9)

Net income from discontinued operations, net of tax

0.1

0.4

*

0.4

Net income (loss)

2.7

3.0

3.4

(2.5)

Less: net income attributable to noncontrolling interests

0.2

0.2

0.1

0.2

Net income (loss) attributable to Bloomin’ Brands

2.5

%

2.8

%

3.3

%

(2.7)

%

____________________

(1)As a percentage of Restaurant sales.

* Less than 1/10th of one percent of Total revenues.

Thirteen weeks ended June 29, 2025 as compared to thirteen weeks ended June 30, 2024

Food and beverage cost increased as a percentage of Restaurant sales primarily due to 1.1% from commodity inflation and 0.2% from unfavorable product cost mix. These increases were partially offset by decreases as a percentage of Restaurant sales of 0.9% from an increase in average check per person, primarily due to menu pricing, and 0.3% from cost-saving and productivity initiatives.

Labor and other related expense increased as a percentage of Restaurant sales primarily due to 1.7% from higher hourly and field management labor costs, mainly due to wage rate inflation and health insurance, partially offset by a decrease of 0.4% from an increase in average check per person.

Other restaurant operating expense increased as a percentage of Restaurant sales primarily due to 0.8% from higher restaurant-level operating and supply expenses, mainly due to inflation, and 0.5% from higher insurance expense. These increases were partially offset by decreases as a percentage of Restaurant sales of 0.6% from lower advertising expense and 0.3% from an increase in average check per person.

Depreciation and amortization expense increased primarily due to new restaurant development.

FINANCIAL CONDITION AND RESULTS OF OPERATIONS - Continued

General and administrative expense increased primarily due to costs associated with our foreign currency forward contracts.

Provision for impaired assets and restaurant closings decreased primarily due to lapping impairment and closure charges in connection with the Q2 2024 decision to close nine restaurants in Hong Kong and the 2023 Restaurant Closures.

Interest expense, net decreased primarily due to interest income on the second installment receivable related to the Brazil Sale Transaction.

(Benefit) provision for income taxes for the thirteen weeks ended June 29, 2025 and June 30, 2024 includes the impact of changes to the estimate of forecasted annual pre-tax book income relative to the prior quarter in each respective year and the benefit of FICA tax credits on certain tipped wages.

Twenty-six weeks ended June 29, 2025 as compared to twenty-six weeks ended June 30, 2024

Food and beverage cost increased as a percentage of Restaurant sales primarily due to 1.0% from commodity inflation and 0.5% from unfavorable product cost mix. These increases were partially offset by decreases as a percentage of Restaurant sales of 1.0% from an increase in average check per person, primarily due to menu pricing, and 0.3% from cost-saving and productivity initiatives.

Labor and other related expense increased as a percentage of Restaurant sales primarily due to 1.4% from higher hourly and field management labor costs, mainly due to wage rate inflation and health insurance, partially offset by a decrease of 0.4% from an increase in average check per person.

Other restaurant operating expense increased as a percentage of Restaurant sales primarily due to 0.9% from higher restaurant-level operating and supply expenses, mainly due to inflation, and 0.2% from higher insurance expense. These increases were partially offset by decreases as a percentage of Restaurant sales of 0.3% from lower advertising expense and 0.3% from an increase in average check per person.

Depreciation and amortization expense increased primarily due to restaurant development.

General and administrative expense increased primarily due to costs associated with our foreign currency forward contracts and severance partially offset by lower compensation and related expenses.

Provision for impaired assets and restaurant closings decreased primarily due to lapping impairment and closure charges in connection with the 2023 Restaurant Closures and the Q2 2024 decision to close nine restaurants in Hong Kong.

Loss on extinguishment of debt during the twenty-six weeks ended June 30, 2024 was in connection with the Second 2025 Notes Partial Repurchase.

Interest expense, net decreased primarily due to interest income on the second installment receivable related to the Brazil Sale Transaction.

Benefit for income taxes for the twenty-six weeks ended June 29, 2025 includes the benefit of FICA tax credits on certain tipped wages relative to forecasted annual pretax book income. Provision for income taxes for the twenty-six weeks ended June 30, 2024 includes the impact of the non-deductible losses associated with the Second 2025 Notes Partial Repurchase, partially offset by the benefit of FICA tax credits on certain tipped wages.

FINANCIAL CONDITION AND RESULTS OF OPERATIONS - Continued

SEGMENT PERFORMANCE

Revenues for both segments include transactions with customers and royalties from franchisees. There were no material transactions among reportable segments. Excluded from Income from operations for U.S. are certain legal and corporate costs not directly related to the performance of the segments, most stock-based compensation expenses, a portion of insurance expenses and certain bonus expenses. The below segment disclosures have been recast to include amounts that relate solely to our continuing operations.

Refer to Note 16 - Segment Reporting of the Notes to Consolidated Financial Statements for reconciliations of segment income from operations to the consolidated operating results.