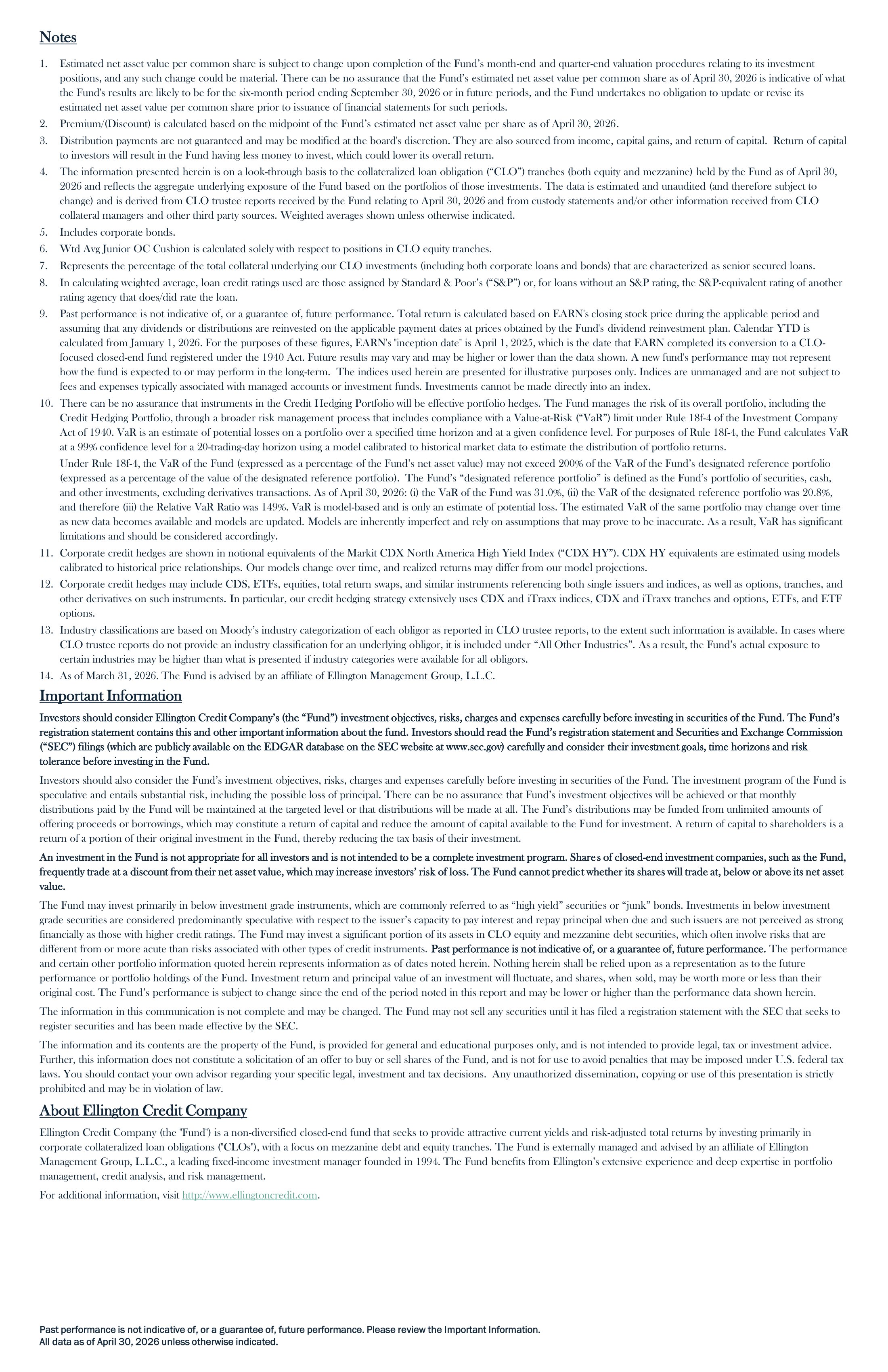

CLO Portfolio Underlying Corporate Loans(5)

Second Lien, Corporate

Floating Rate and Bonds 4% First Lien, Fixed

Rate Leveraged Loans

1%

Asset Type

95% First Lien, Floating Rate Leveraged

Loan Highly Diversified by Industry

A A: High Tech Industries

- 11% B: Services: Business

B C: Healthcare & Pharma

L D: Banking/Finance/Insurance/

32% 10% Real Estate

E: Hotel, Gaming & Leisure F: Construction & Building

Industry (13) 10% C G: Chemicals, Plastics & Rubber

H: Beverage, Food & Tobacco

I: Services: Consumer

3% J: Capital Equipment

K 3% 10% K: Telecommunications

J 4% 5% D L: All Other Industries <3%

4% 4% 4%

I

H G F E

Asset Maturity

30% Wtd Avg Loan

26%

25% Maturity: 4.3

years

20% 19% 18%

15% 14% 14%

10%

5%

5% 3%

1%

0%

2026 2027 2028 2029 2030 2031 2032 2033+ Ratings of Loans Underlying CLO Equity Investments

35% 32.7%

30%

25% 21.0%

20% 16.0%

15% 11.1%

10% 7.7%

4.7%

5% 2.7%

0.6% 0.4% 1.6% 0.6% 0.6% 0.4%

0%

BBB+ BBB BBB- BB+ BB BB- B+ B B- CCC+ CCC CCC- Not

and and Rated

Above Below

Ellington Management Group Profile (14)

$22.2 bn 10 31 20%

Assets Under Management Employee-partners own the firm Years of average industry experience of senior

portfolio managers Employees dedicated to research and engineering

Notes

1. Estimated net asset value per common share is subject to change upon completion of the Fund’s month-end and quarter-end valuation procedures relating to its investment

positions, and any such change could be material. There can be no assurance that the Fund’s estimated net asset value per common share as of April 30, 2026 is indicative of what the Fund's results are likely to be for the six-month period ending September 30, 2026 or in future periods, and the Fund undertakes no obligation to update or revise its estimated net asset value per common share prior to issuance of financial statements for such periods.

2. Premium/(Discount) is calculated based on the midpoint of the Fund’s estimated net asset value per share as of April 30, 2026.

3. Distribution payments are not guaranteed and may be modified at the board's discretion. They are also sourced from income, capital gains, and return of capital. Return of capital to investors will result in the Fund having less money to invest, which could lower its overall return.

4. The information presented herein is on a look-through basis to the collateralized loan obligation (“CLO”) tranches (both equity and mezzanine) held by the Fund as of April 30, 2026 and reflects the aggregate underlying exposure of the Fund based on the portfolios of those investments. The data is estimated and unaudited (and therefore subject to change) and is derived from CLO trustee reports received by the Fund relating to April 30, 2026 and from custody statements and/or other information received from CLO collateral managers and other third party sources. Weighted averages shown unless otherwise indicated.

5. Includes corporate bonds.

6. Wtd Avg Junior OC Cushion is calculated solely with respect to positions in CLO equity tranches.

7. Represents the percentage of the total collateral underlying our CLO investments (including both corporate loans and bonds) that are characterized as senior secured loans.

8. In calculating weighted average, loan credit ratings used are those assigned by Standard & Poor’s (“S&P”) or, for loans without an S&P rating, the S&P-equivalent rating of another rating agency that does/did rate the loan.

9. Past performance is not indicative of, or a guarantee of, future performance. Total return is calculated based on EARN's closing stock price during the applicable period and assuming that any dividends or distributions are reinvested on the applicable payment dates at prices obtained by the Fund's dividend reinvestment plan. Calendar YTD is calculated from January 1, 2026. For the purposes of these figures, EARN's "inception date" is April 1, 2025, which is the date that EARN completed its conversion to a CLO-focused closed-end fund registered under the 1940 Act. Future results may vary and may be higher or lower than the data shown. A new fund's performance may not represent how the fund is expected to or may perform in the long-term. The indices used herein are presented for illustrative purposes only. Indices are unmanaged and are not subject to fees and expenses typically associated with managed accounts or investment funds. Investments cannot be made directly into an index.

10. There can be no assurance that instruments in the Credit Hedging Portfolio will be effective portfolio hedges. The Fund manages the risk of its overall portfolio, including the Credit Hedging Portfolio, through a broader risk management process that includes compliance with a Value-at-Risk (“VaR”) limit under Rule 18f-4 of the Investment Company Act of 1940. VaR is an estimate of potential losses on a portfolio over a specified time horizon and at a given confidence level. For purposes of Rule 18f-4, the Fund calculates VaR at a 99% confidence level for a 20-trading-day horizon using a model calibrated to historical market data to estimate the distribution of portfolio returns.

Under Rule 18f-4, the VaR of the Fund (expressed as a percentage of the Fund’s net asset value) may not exceed 200% of the VaR of the Fund’s designated reference portfolio (expressed as a percentage of the value of the designated reference portfolio). The Fund’s “designated reference portfolio” is defined as the Fund’s portfolio of securities, cash, and other investments, excluding derivatives transactions. As of April 30, 2026: (i) the VaR of the Fund was 31.0%, (ii) the VaR of the designated reference portfolio was 20.8%, and therefore (iii) the Relative VaR Ratio was 149%. VaR is model-based and is only an estimate of potential loss. The estimated VaR of the same portfolio may change over time as new data becomes available and models are updated. Models are inherently imperfect and rely on assumptions that may prove to be inaccurate. As a result, VaR has significant limitations and should be considered accordingly.

11. Corporate credit hedges are shown in notional equivalents of the Markit CDX North America High Yield Index (“CDX HY”). CDX HY equivalents are estimated using models calibrated to historical price relationships. Our models change over time, and realized returns may differ from our model projections.

12. Corporate credit hedges may include CDS, ETFs, equities, total return swaps, and similar instruments referencing both single issuers and indices, as well as options, tranches, and other derivatives on such instruments. In particular, our credit hedging strategy extensively uses CDX and iTraxx indices, CDX and iTraxx tranches and options, ETFs, and ETF options.

13. Industry classifications are based on Moody’s industry categorization of each obligor as reported in CLO trustee reports, to the extent such information is available. In cases where CLO trustee reports do not provide an industry classification for an underlying obligor, it is included under “All Other Industries”. As a result, the Fund’s actual exposure to certain industries may be higher than what is presented if industry categories were available for all obligors.

14. As of March 31, 2026. The Fund is advised by an affiliate of Ellington Management Group, L.L.C.

Important Information

Investors should consider Ellington Credit Company’s (the “Fund”) investment objectives, risks, charges and expenses carefully before investing in securities of the Fund. The Fund’s registration statement contains this and other important information about the fund. Investors should read the Fund’s registration statement and Securities and Exchange Commission (“SEC”) filings (which are publicly available on the EDGAR database on the SEC website at www.sec.gov) carefully and consider their investment goals, time horizons and risk tolerance before investing in the Fund.

Investors should also consider the Fund’s investment objectives, risks, charges and expenses carefully before investing in securities of the Fund. The investment program of the Fund is

speculative and entails substantial risk, including the possible loss of principal. There can be no assurance that Fund’s investment objectives will be achieved or that monthly

distributions paid by the Fund will be maintained at the targeted level or that distributions will be made at all. The Fund’s distributions may be funded from unlimited amounts of offering proceeds or borrowings, which may constitute a return of capital and reduce the amount of capital available to the Fund for investment. A return of capital to shareholders is a return of a portion of their original investment in the Fund, thereby reducing the tax basis of their investment.

An investment in the Fund is not appropriate for all investors and is not intended to be a complete investment program. Shares of closed-end investment companies, such as the Fund, frequently trade at a discount from their net asset value, which may increase investors’ risk of loss. The Fund cannot predic t whether its shares will trade at, below or above its net asset value.

The Fund may invest primarily in below investment grade instruments, which are commonly referred to as “high yield” securities or “junk” bonds. Investments in below investment

grade securities are considered predominantly speculative with respect to the issuer’s capacity to pay interest and repay principal when due and such issuers are not perceived as strong financially as those with higher credit ratings. The Fund may invest a significant portion of its assets in CLO equity and mezzanine debt securities, which often involve risks that are different from or more acute than risks associated with other types of credit instruments. Past performance is not indicative of, or a guarantee of, future performance. The performance and certain other portfolio information quoted herein represents information as of dates noted herein. Nothing herein shall be relied upon as a representation as to the future performance or portfolio holdings of the Fund. Investment return and principal value of an investment will fluctuate, and shares, when sold, may be worth more or less than their

original cost. The Fund’s performance is subject to change since the end of the period noted in this report and may be lower or higher than the performance data shown herein.

The information in this communication is not complete and may be changed. The Fund may not sell any securities until it has filed a registration statement with the SEC that seeks to register securities and has been made effective by the SEC.

The information and its contents are the property of the Fund, is provided for general and educational purposes only, and is not intended to provide legal, tax or investment advice. Further, this information does not constitute a solicitation of an offer to buy or sell shares of the Fund, and is not for use to avoid penalties that may be imposed under U.S. federal tax laws. You should contact your own advisor regarding your specific legal, investment and tax decisions. Any unauthorized dissemination, copying or use of this presentation is strictly prohibited and may be in violation of law.

About Ellington Credit Company

Ellington Credit Company (the "Fund") is a non-diversified closed-end fund that seeks to provide attractive current yields and risk-adjusted total returns by investing primarily in corporate collateralized loan obligations ("CLOs"), with a focus on mezzanine debt and equity tranches. The Fund is externally managed and advised by an affiliate of Ellington Management Group, L.L.C., a leading fixed-income investment manager founded in 1994. The Fund benefits from Ellington’s extensive experience and deep expertise in portfolio management, credit analysis, and risk management.

For additional information, visit http://www.ellingtoncredit.com.