|

|

|

|

|

|

|

|

|

|

|

|

|

| |

|

2015 Y |

|

|

2016 Y |

|

|

2017 Y |

|

| Period Ended |

|

|

12/31/2015 |

|

|

|

12/31/2016 |

|

|

|

12/31/2017 |

|

| Net Investment Income |

|

|

15,932 |

|

|

|

15,987 |

|

|

|

15,290 |

|

| Realized Capital Gains |

|

|

229 |

|

|

|

(301 |

) |

|

|

42 |

|

| Unrealized Capital Gains |

|

|

(662 |

) |

|

|

640 |

|

|

|

(179 |

) |

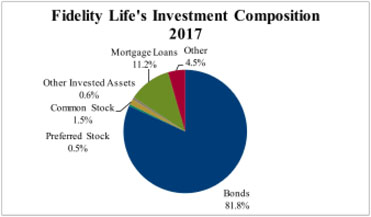

| Investment Portfolio Composition (%) |

|

|

|

|

|

|

|

|

|

|

|

|

| Total Cash & Investments |

|

|

405,223 |

|

|

|

384,863 |

|

|

|

384,013 |

|

| Affiliated Cash & Investments |

|

|

0 |

|

|

|

0 |

|

|

|

0 |

|

| Unaff. Bonds / Unaff. Investments |

|

|

85.57 |

|

|

|

83.13 |

|

|

|

81.76 |

|

| Unaff. Preferred Stocks / Unaff. Investments |

|

|

0.12 |

|

|

|

0.13 |

|

|

|

0.49 |

|

| Unaff. Common Stocks / Unaff. Investments |

|

|

1.09 |

|

|

|

1.63 |

|

|

|

1.49 |

|

| Unaff. Mortgage Loans / Unaff. Investments |

|

|

7.25 |

|

|

|

8.39 |

|

|

|

11.16 |

|

| Real Estate / Unaff. Investments |

|

|

0.00 |

|

|

|

0.00 |

|

|

|

0.00 |

|

| Contract Loans / Unaff. Investments |

|

|

1.67 |

|

|

|

1.50 |

|

|

|

1.55 |

|

| Unaff. Cash & Short Term / Unaff. Investments |

|

|

3.37 |

|

|

|

4.41 |

|

|

|

2.73 |

|

| Unaff. Other Investments / Unaff. Investments |

|

|

0.94 |

|

|

|

0.80 |

|

|

|

0.83 |

|

| Investment Yields by Type (%) |

|

|

|

|

|

|

|

|

|

|

|

|

| Net Yield on Invested Assets |

|

|

3.98 |

|

|

|

4.07 |

|

|

|

3.99 |

|

| Gross Yield - Bonds (excl affiliates) |

|

|

4.45 |

|

|

|

4.52 |

|

|

|

4.48 |

|

| Gross Yield - Preferred Stocks (excl affiliates) |

|

|

6.37 |

|

|

|

6.38 |

|

|

|

4.66 |

|

| Gross Yield - Common Stocks (excl affiliates) |

|

|

3.80 |

|

|

|

5.93 |

|

|

|

6.22 |

|

| Gross Yield - Mortgage Loans |

|

|

5.23 |

|

|

|

5.08 |

|

|

|

5.39 |

|

| Gross Yield - Real Estate |

|

|

NA |

|

|

|

NA |

|

|

|

NA |

|

| Gross Yield - Contract Loans |

|

|

6.53 |

|

|

|

5.67 |

|

|

|

3.58 |

|

| Gross Yield - Cash and Short Term |

|

|

0.01 |

|

|

|

0.17 |

|

|

|

0.48 |

|

| Gross Yield - All Other Inv. Assets |

|

|

5.24 |

|

|

|

7.10 |

|

|

|

7.94 |

|

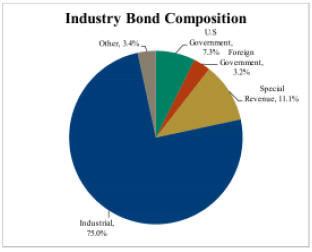

| Bond Portfolio Composition (%) |

|

|

|

|

|

|

|

|

|

|

|

|

| Total Bonds (incl Short-Term) ($000) |

|

|

346,901 |

|

|

|

319,933 |

|

|

|

313,950 |

|

| U.S Government / Total Bonds |

|

|

1.59 |

|

|

|

1.29 |

|

|

|

2.30 |

|

| Foreign Government / Total Bonds |

|

|

0.04 |

|

|

|

0.04 |

|

|

|

0.04 |

|

| States, Territories & Possessions / Total Bonds |

|

|

0.32 |

|

|

|

0.34 |

|

|

|

0.35 |

|

| Political Subdivisions / Total Bonds |

|

|

0.30 |

|

|

|

0.32 |

|

|

|

0.48 |

|

| Special Revenue / Total Bonds |

|

|

18.41 |

|

|

|

17.23 |

|

|

|

17.62 |

|

| Public Utilities / Total Bonds |

|

|

NA |

|

|

|

NA |

|

|

|

NA |

|

| Industrial / Total Bonds |

|

|

79.34 |

|

|

|

80.73 |

|

|

|

78.86 |

|

| Credit Tenant Loans / Total Bonds |

|

|

NA |

|

|

|

NA |

|

|

|

NA |

|

| Affiliated / Total Bonds |

|

|

0.00 |

|

|

|

0.00 |

|

|

|

0.00 |

|

| Privately Placed Bonds / Total Bonds |

|

|

26.55 |

|

|

|

27.66 |

|

|

|

28.62 |

|

| Privately Placed Bonds / C&S |

|

|

68.43 |

|

|

|

66.93 |

|

|

|

70.41 |

|

| Bond Average Asset Quality (NAIC Des # 1-6) |

|

|

|

|

|

|

|

|

|

|

|

|

| U.S Government |

|

|

1.00 |

|

|

|

1.00 |

|

|

|

1.00 |

|

| Foreign Government |

|

|

2.00 |

|

|

|

2.00 |

|

|

|

2.00 |

|

| States, Territories & Possessions |

|

|

1.00 |

|

|

|

1.00 |

|

|

|

1.00 |

|

| Political Subdivisions |

|

|

1.47 |

|

|

|

1.48 |

|

|

|

1.32 |

|

| Special Revenue |

|

|

1.00 |

|

|

|

1.00 |

|

|

|

1.00 |

|

| Public Utilities |

|

|

NA |

|

|

|

NA |

|

|

|

NA |

|

| Industrial |

|

|

1.47 |

|

|

|

1.53 |

|

|

|

1.56 |

|

| Credit Tenant Loans |

|

|

NA |

|

|

|

NA |

|

|

|

NA |

|

| Affiliated |

|

|

NA |

|

|

|

NA |

|

|

|

NA |

|

| Total Bonds |

|

|

1.38 |

|

|

|

1.43 |

|

|

|

1.45 |

|

| Bonds Rated 3-6 / Total Bonds |

|

|

5.52 |

|

|

|

7.90 |

|

|

|

9.40 |

|

| Bonds Rated 3-6 / C&S |

|

|

14.24 |

|

|

|

19.12 |

|

|

|

23.12 |

|

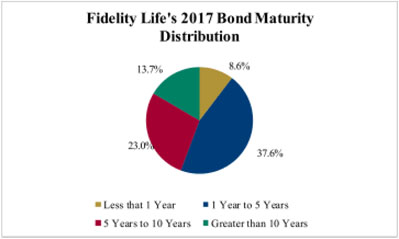

| Bond Maturity Distribution (%) |

|

|

|

|

|

|

|

|

|

|

|

|

| < 1 Year / Total Bonds |

|

|

12.79 |

|

|

|

6.91 |

|

|

|

8.59 |

|

| 1 - 5 Years / Total Bonds |

|

|

41.02 |

|

|

|

45.35 |

|

|

|

37.57 |

|

| 5 - 10 Years / Total Bonds |

|

|

23.92 |

|

|

|

20.93 |

|

|

|

23.00 |

|

| 10 - 20 Years / Total Bonds |

|

|

7.01 |

|

|

|

11.89 |

|

|

|

13.72 |

|

| > 20 Years / Total Bonds |

|

|

15.26 |

|

|

|

14.92 |

|

|

|

17.12 |

|

| Preferred Stock Portfolio Composition (%) |

|

|

|

|

|

|

|

|

|

|

|

|

| Total Preferred Stock (incl Nonadmitted) ($000) |

|

|

500 |

|

|

|

500 |

|

|

|

1,890 |

|

| Public Utilities / Total Preferred |

|

|

NA |

|

|

|

NA |

|

|

|

NA |

|

| Banks, Trust & Unaffil Insurance / Total Preferred |

|

|

NA |

|

|

|

NA |

|

|

|

NA |

|

| Industrial & Misc / Total Preferred |

|

|

100.00 |

|

|

|

100.00 |

|

|

|

100.00 |

|

| Affiliated / Total Preferred |

|

|

0.00 |

|

|

|

0.00 |

|

|

|

0.00 |

|

| Common Stock Portfolio Composition (%) |

|

|

|

|

|

|

|

|

|

|

|

|

| Total Common Stock (incl Nonadmitted) ($000) |

|

|

4,401 |

|

|

|

6,286 |

|

|

|

5,705 |

|

| Public Utilities / Total Common |

|

|

NA |

|

|

|

NA |

|

|

|

NA |

|

| Banks, Trust & Unaffil Insurance / Total Common |

|

|

NA |

|

|

|

NA |

|

|

|

NA |

|

| Industrial & Misc / Total Common |

|

|

100.00 |

|

|

|

100.00 |

|

|

|

100.00 |

|

| Affiliated / Total Common |

|

|

0.00 |

|

|

|

0.00 |

|

|

|

0.00 |

|

| Mortgage Loan Portfolio Composition (%) |

|

|

|

|

|

|

|

|

|

|

|

|

| Total Mortgage Loans (incl Nonadmitted) ($000) |

|

|

29,929 |

|

|

|

32,785 |

|

|

|

43,120 |

|

| Mortgages in Good Standing / Total |

|

|

95.33 |

|

|

|

95.97 |

|

|

|

98.37 |

|

| Restructured Mortgages / Total |

|

|

4.67 |

|

|

|

3.83 |

|

|

|

1.63 |

|

| Mortgages 90+ Due / Total |

|

|

0.00 |

|

|

|

0.00 |

|

|

|

0.00 |

|

| Mortgages in Foreclosure / Total |

|

|

0.00 |

|

|

|

0.20 |

|

|

|

0.00 |

|

| Mortgages in Foreclosure / C&S |

|

|

0.00 |

|

|

|

0.05 |

|

|

|

0.00 |

|

| Real Estate Composition (%) |

|

|

|

|

|

|

|

|

|

|

|

|

| Total Real Estate (incl Nonadmitted) ($000) |

|

|

0 |

|

|

|

0 |

|

|

|

0 |

|

| Real Estate Occupied / Total |

|

|

NA |

|

|

|

NA |

|

|

|

NA |

|

| Income Producing Real Estate / Total |

|

|

NA |

|

|

|

NA |

|

|

|

NA |

|

| Real Estate Held for Sale / Total |

|

|

NA |

|

|

|

NA |

|

|

|

NA |

|