.2

February 26, 2026 Natera, Inc. Q4’2025 Earnings Presentation

This presentation contains forward - looking statements under the meaning of the Private Securities Litigation Reform Act of 1995 . All statements other than statements of historical facts contained in this presentation, including statements regarding our market opportunity, our anticipated products and launch schedules, our reimbursement coverage and our product costs, our commercial and strategic partnerships and potential acquisitions, our user experience, our clinical trials and studies, our strategies, our goals and general business and market conditions, are forward - looking statements . These forward - looking statements are subject to known and unknown risks and uncertainties that may cause actual results to differ materially, including : we face numerous uncertainties and challenges in achieving our financial projections and goals ; we may be unable to further increase the use and adoption of our products through our direct sales efforts or through our laboratory partners ; we have incurred net losses since our inception and we anticipate that we will continue to incur net losses for the foreseeable future ; our quarterly results may fluctuate from period to period ; unless otherwise indicated, all financial data for the current and prior quarters are unaudited and subject to adjustment in connection with the completion of Natera’s quarterly and annual financial reporting processes ; our estimates of market opportunity and forecasts of market growth may prove to be inaccurate ; we may be unable to compete successfully with existing or future products or services offered by our competitors ; we may engage in acquisitions, dispositions or other strategic transactions that may not achieve our anticipated benefits and could otherwise disrupt our business, cause dilution to our stockholders or reduce our financial resources ; our products may not perform as expected ; the results of our clinical studies may not support the use and reimbursement of our tests, particularly for microdeletions screening, and may not be able to be replicated in later studies required for regulatory approvals or clearances ; if either of our primary CLIA - certified laboratories becomes inoperable, we will be unable to perform our tests and our business will be harmed ; we rely on a limited number of suppliers or, in some cases, single suppliers, for some of our laboratory instruments and materials and may not be able to find replacements or immediately transition to alternative suppliers ; if we are unable to successfully scale our operations, our business could suffer ; the marketing, sale, and use of Panorama and our other products could result in substantial damages arising from product liability or professional liability claims that exceed our resources ; we may be unable to expand, obtain or maintain third - party payer coverage and reimbursement for our tests, and we may be required to refund reimbursements already received ; third - party payers may withdraw coverage or provide lower levels of reimbursement due to changing policies, billing complexities or other factors ; we could incur substantial costs and delays complying with governmental regulations ; litigation and other regulatory or governmental proceedings, related to our intellectual property or the commercialization of our tests, are costly, time - consuming, could result in our obligation to pay material judgments or incur material settlement costs, and could limit our ability to commercialize our tests ; and any inability to effectively protect our proprietary technology could harm our competitive position or our brand . We discuss these and other risks and uncertainties in greater detail in the sections entitled “Risk Factors” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations” in our periodic reports on Forms 10 - K and 10 - Q and in other filings we make with the SEC from time to time . Moreover, we operate in a very competitive and rapidly changing environment . New risks emerge from time to time . It is not possible for our management to predict all risks, nor can we assess the impact of all factors on our business or the extent to which any factor, or combination of factors, may cause actual results to differ materially from those contained in any forward - looking statement . In light of these risks, uncertainties and assumptions, the forward - looking events and circumstances discussed in this presentation may not occur and our actual results could differ materially and adversely from those anticipated or implied . As a result, you should not place undue reliance on our forward - looking statements . Except as required by law, we undertake no obligation to update publicly any forward - looking statements for any reason after the date of this presentation to conform these statements to actual results or to changes in our expectations . We file reports, proxy statements, and other information with the SEC . Such reports, proxy statements, and other information concerning us is available at http : //www . sec . gov . Requests for copies of such documents should be directed to our Investor Relations department at Natera , Inc . , 13011 McCallen Pass, Building A Suite 100 , Austin, TX 78753 . Our telephone number is ( 650 ) 980 - 9190 . 2 Safe harbor statement Not for reproduction or further distribution.

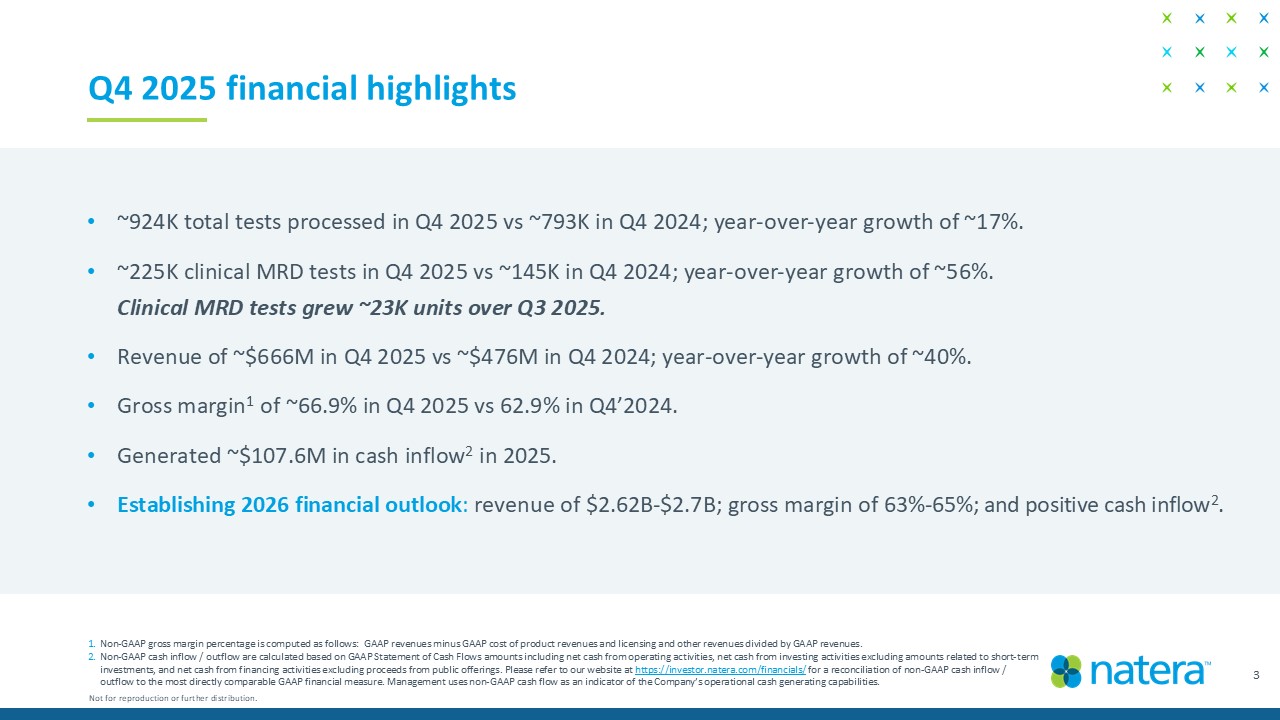

3 Q4 2025 financial highlights Not for reproduction or further distribution. 1. Non - GAAP gross margin percentage is computed as follows: GAAP revenues minus GAAP cost of product revenues and licensing and ot her revenues divided by GAAP revenues. 2. Non - GAAP cash inflow / outflow are calculated based on GAAP Statement of Cash Flows amounts including net cash from operating ac tivities, net cash from investing activities excluding amounts related to short - term investments, and net cash from financing activities excluding proceeds from public offerings. Please refer to our website at https://investor.natera.com/financials/ for a reconciliation of non - GAAP cash inflow / outflow to the most directly comparable GAAP financial measure. Management uses non - GAAP cash flow as an indicator of the Compan y’s operational cash generating capabilities. • ~924K total tests processed in Q4 2025 vs ~793K in Q4 2024; year - over - year growth of ~17%. • ~225K clinical MRD tests in Q4 2025 vs ~145K in Q4 2024; year - over - year growth of ~56%. Clinical MRD tests grew ~23K units over Q3 2025. • Revenue of ~$666M in Q4 2025 vs ~$476M in Q4 2024; year - over - year growth of ~40%. • Gross margin 1 of ~66.9% in Q4 2025 vs 62.9% in Q4’2024 • Generated ~$107.6M in cash inflow 2 in 2025. • Establishing 2026 financial outlook : revenue of $2.60B - $2.68B; gross margin of 63 % – 65%; and positive cash inflow 2 .

2025 business highlights 4 Not for reproduction or further distribution. Launch: Signatera TM Genome for RUO Readout: DEFINE - HT at International Society for Heart & Lung Transplantation Medicare Coverage: Signatera in Lung Cancer Surveillance Paper: Prospera Heart TM with DQS in American Journal of Transplantation Medicare Coverage: Signatera Genome Launch: Latitude TM Tissue - Free MRD Paper: PEDAL in American Journal of Transplantation Launch: Proprietary AI Foundation Models Launch: Fetal Focus TM Single - Gene Non - Invasive Prenatal Test (NIPT) Paper: IMvigor011 in New England Journal of Medicine Readout: AA Data from PROCEED Trial Acquisition: Foresight Diagnostics Paper: CALGB (Alliance)/ SWOG 80702 in JAMA Oncology Q1 Q2 Q3 Q4

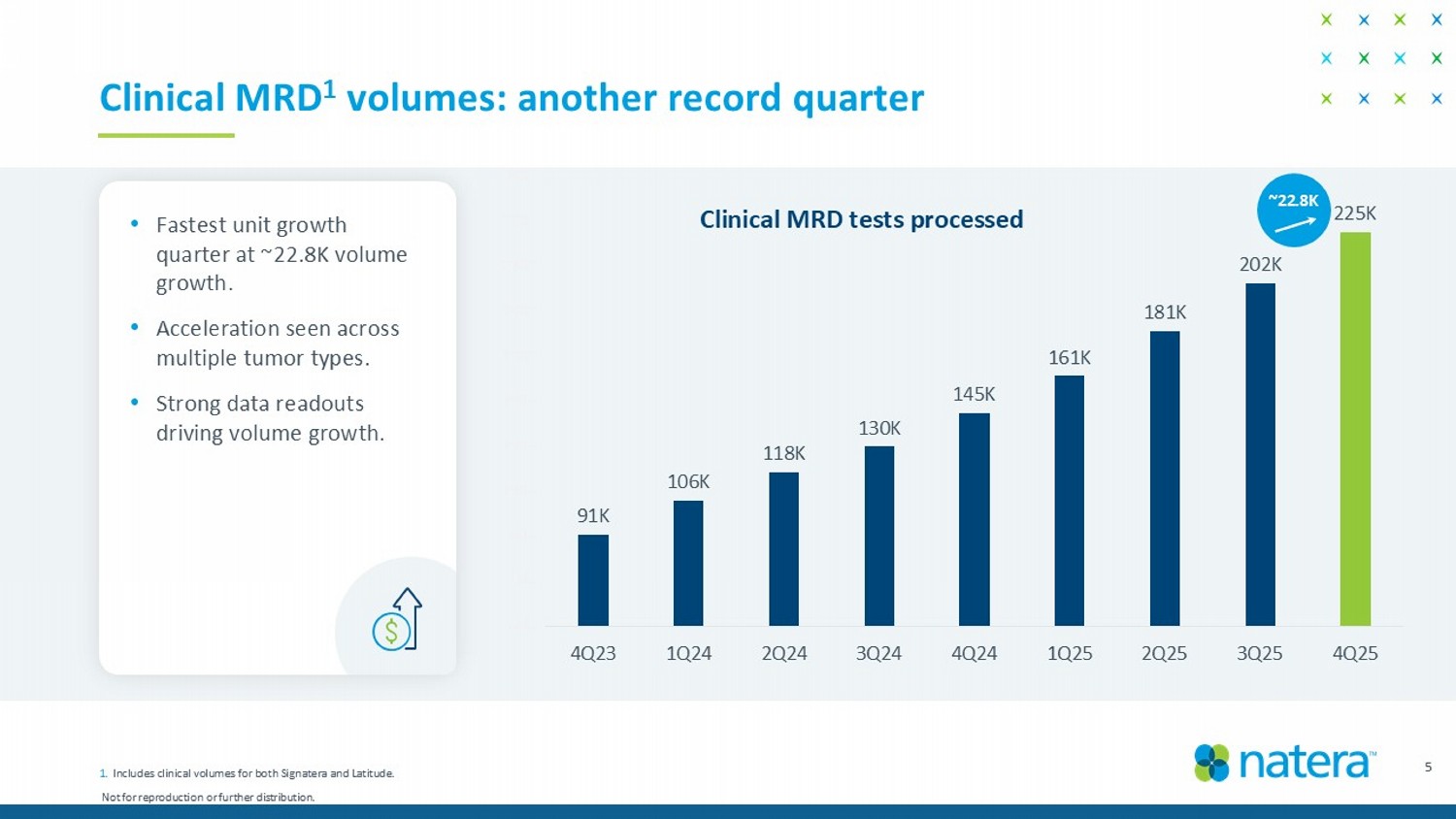

Not for reproduction or further distribution. 91K 106K 118K 130K 145K 161K 181K 202K 225K 50K 70K 90K 110K 130K 150K 170K 190K 210K 230K 250K 4Q23 1Q24 2Q24 3Q24 4Q24 1Q25 2Q25 3Q25 4Q25 5 Clinical MRD 1 volumes: another record quarter Clinical MRD tests processed ~22.8K • Fastest unit growth quarter at ~22.8K volume growth. • Acceleration seen across multiple tumor types. • Strong data readouts driving volume growth. 1. Includes clinical volumes for both Signatera and Latitude.

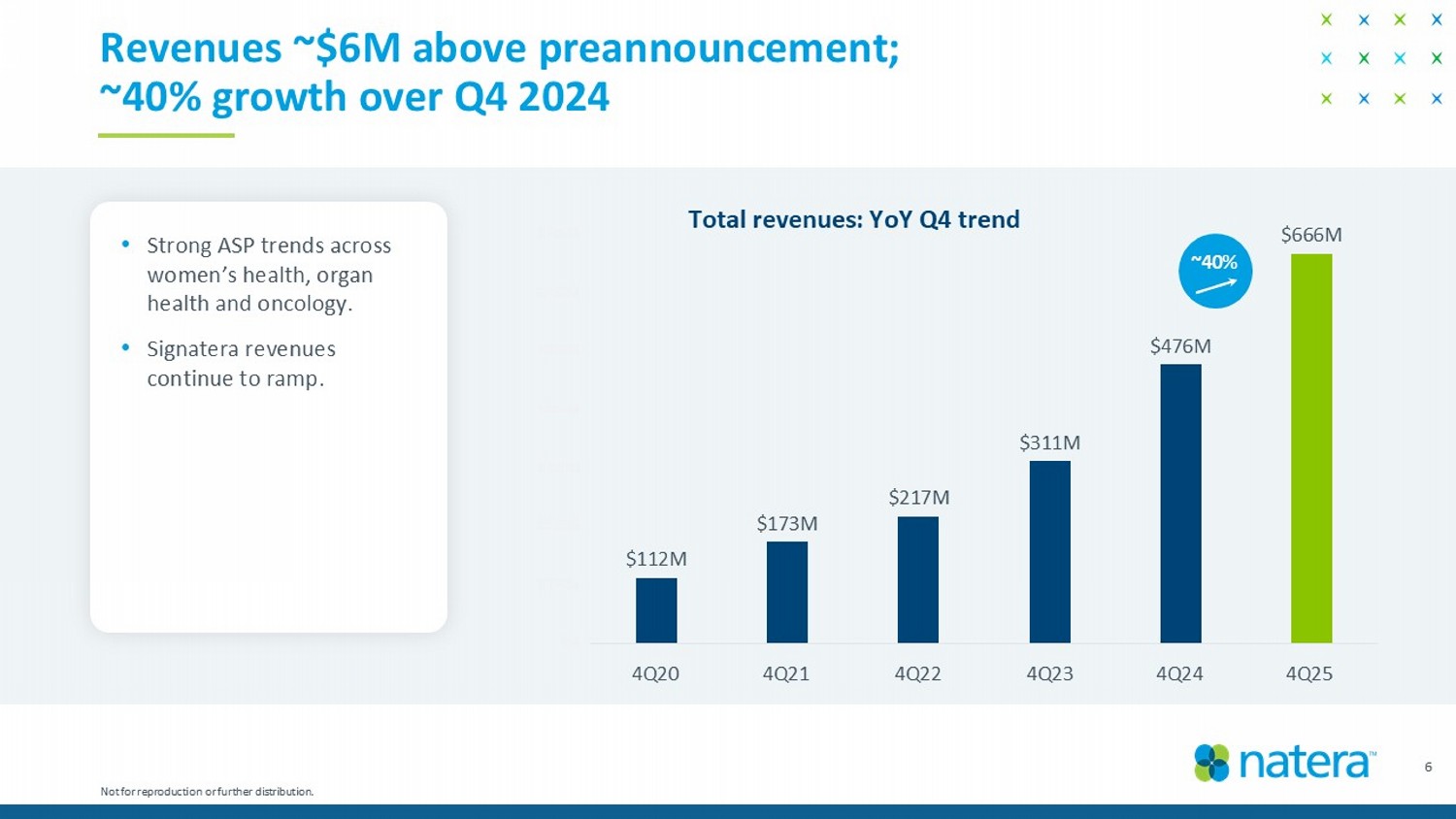

$112M $173M $217M $311M $476M $666M $M $100M $200M $300M $400M $500M $600M $700M 4Q'20 4Q'21 4Q'22 4Q'23 4Q'24 4Q'25 6 Revenues ~$6M above preannouncement; ~40% growth over Q4 2024 Total revenues: YoY Q4 trend Not for reproduction or further distribution. ~40% • Strong ASP trends across women’s health, organ health and oncology. • Signatera revenues continue to ramp. 4Q20 4Q21 4Q22 4Q23 4Q24 4Q25

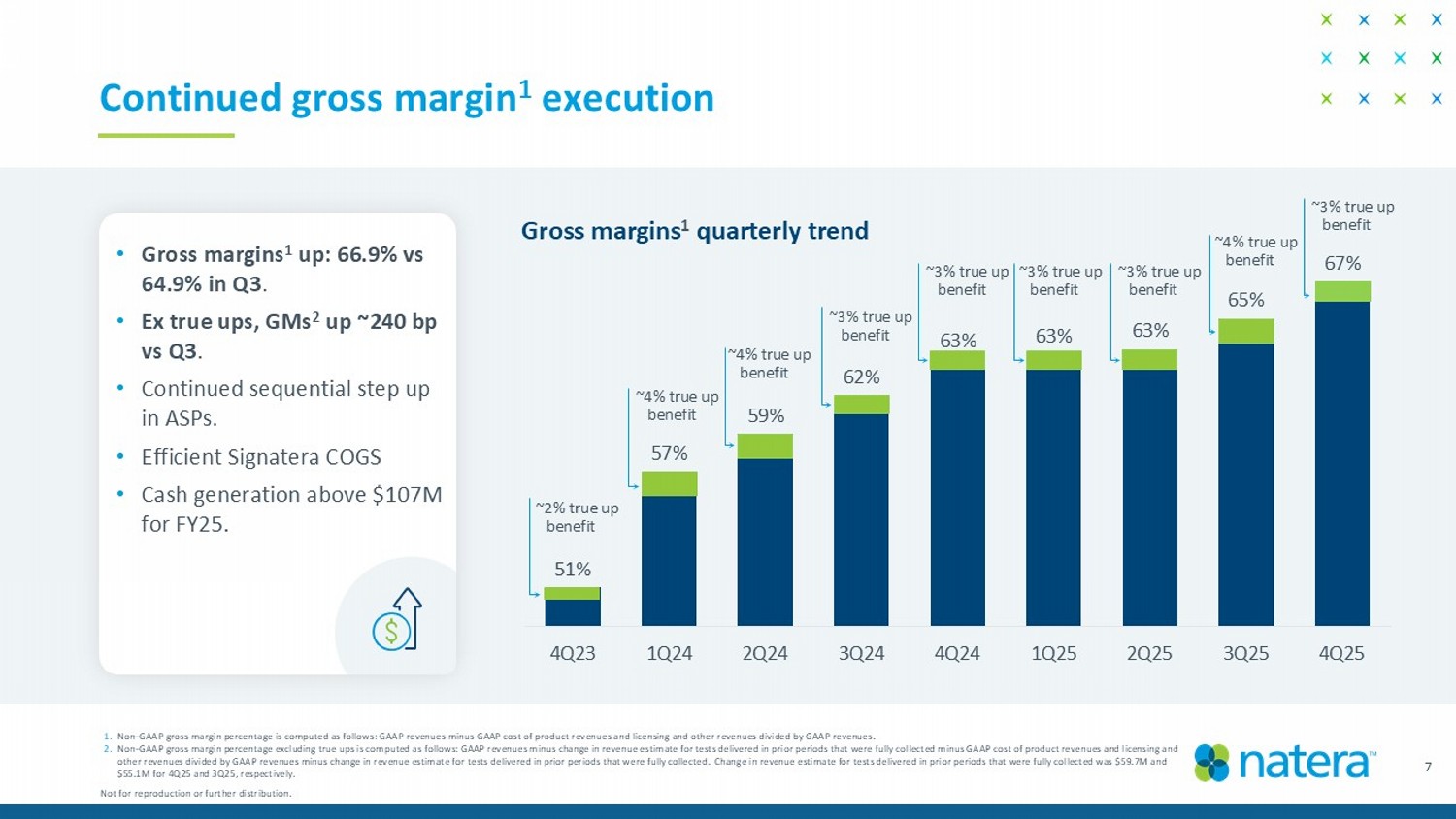

51% 57% 59% 62% 63% 63% 63% 65% 67% 4Q23 1Q24 2Q24 3Q24 4Q24 1Q25 2Q25 3Q25 4Q25 ~ 2 % true up benefit ~4% true up benefit ~4% true up benefit ~3% true up benefit ~3% true up benefit ~3% true up benefit ~3% true up benefit ~4% true up benefit 7 Continued gross margin 1 execution • Gross margins 1 up: 66.9% vs 64.9% in Q3 . • Ex true ups, GMs 2 up ~240 bp vs Q3 . • Continued sequential step up in ASPs. • Efficient Signatera COGS • Cash generation above $107M for FY25. 1. Non - GAAP gross margin percentage is computed as follows: GAAP revenues minus GAAP cost of product revenues and licensing and oth er revenues divided by GAAP revenues. 2. Non - GAAP gross margin percentage excluding true ups is computed as follows: GAAP revenues minus change in revenue estimate for t ests delivered in prior periods that were fully collected minus GAAP cost of product revenues and licensing and other revenues divided by GAAP revenues minus change in revenue estimate for tests delivered in prior periods that were fully co llected. Change in revenue estimate for tests delivered in prior periods that were fully collected was $59.7M and $55.1M for 4Q25 and 3Q25, respectively. Gross margins 1 quarterly trend Not for reproduction or further distribution. ~3% true up benefit

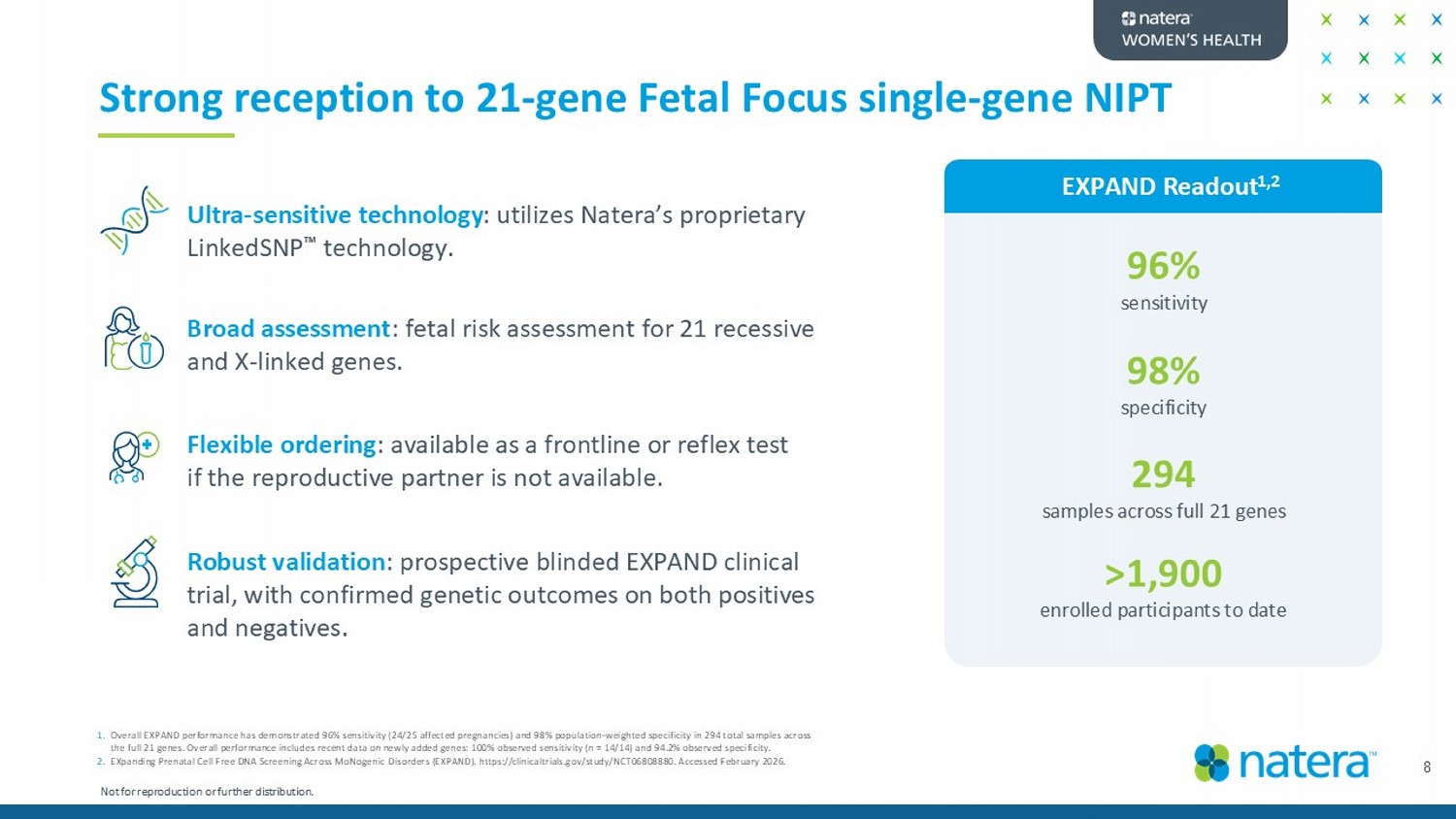

Strong reception to 21 - gene Fetal Focus single - gene NIPT Robust validation : prospective blinded EXPAND clinical trial, with confirmed genetic outcomes on both positives and negatives. Broad assessment : fetal risk assessment for 21 recessive and X - linked genes. Flexible ordering : available as a frontline or reflex test if the reproductive partner is not available. Ultra - sensitive technology : utilizes Natera’s proprietary LinkedSNP technology. 96% sensitivity 98% specificity >1,900 enrolled participants to date 294 samples across full 21 genes 1. Overall EXPAND performance has demonstrated 96% sensitivity (24/25 affected pregnancies) and 98% population - weighted specificity in 294 total samples across the full 21 genes. Overall performance includes recent data on newly added genes: 100% observed sensitivity (n = 14/14) and 9 4.2 % observed specificity. 2. EXpanding Prenatal Cell Free DNA Screening Across MoNogenic Disorders (EXPAND). https:// clinicaltrials.gov /study/NCT06808880. Accessed February 2026. 8 EXPAND Readout 1,2 Not for reproduction or further distribution.

9 EXPAND clinical trial selected for oral plenary at SMFM Not for reproduction or further distribution. • First single - gene NIPT study to be selected for an oral plenary and presented at the Society for Maternal - Fetal Medicine ( SMFM ) Meeting. • Underscores the scientific rigor and clinical relevance of the trial. • Largest prospective study on single - gene NIPT in the U.S. • Demonstrated excellent performance.

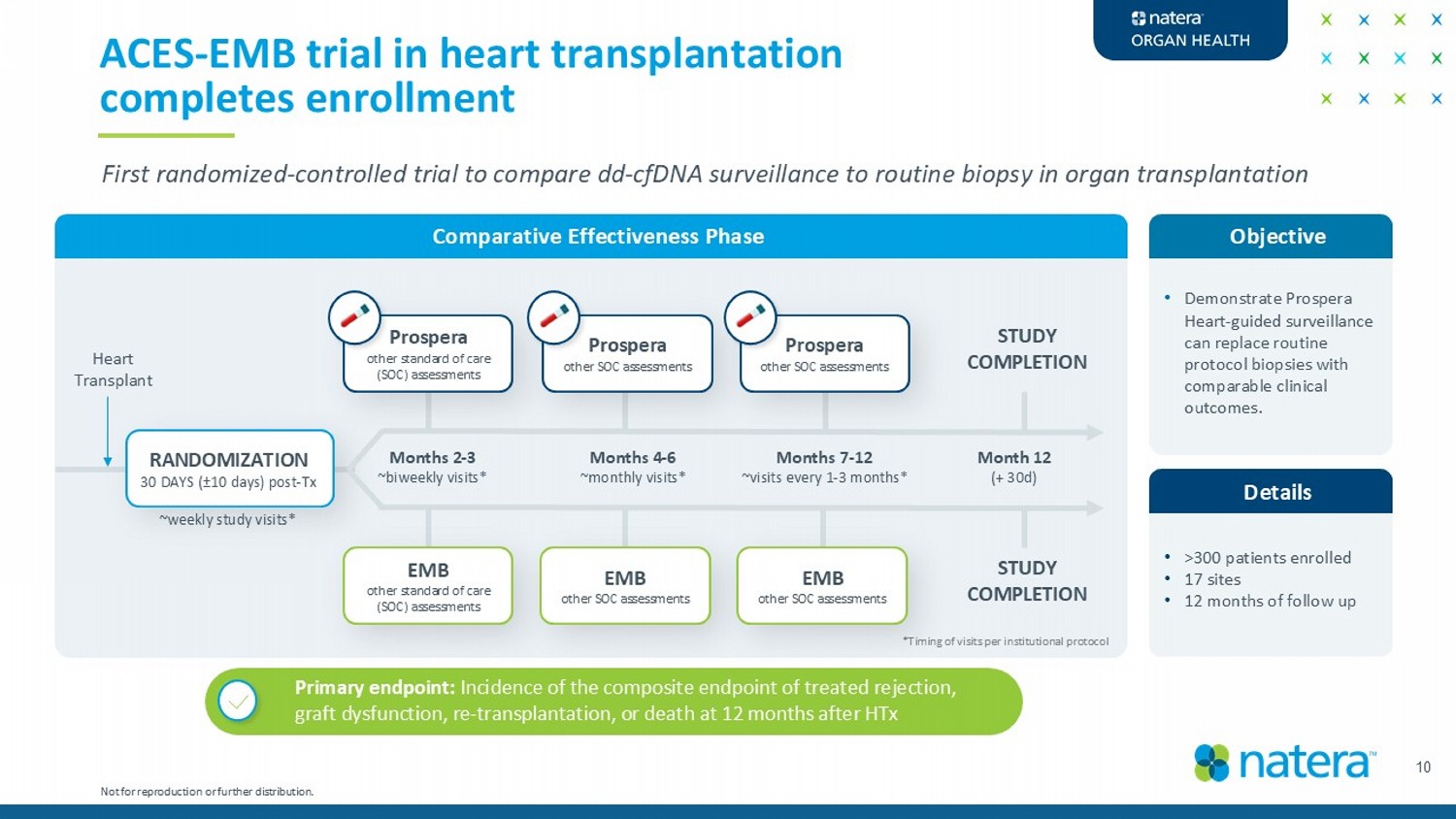

Details 10 ACES - EMB trial in heart transplantation completes enrollment Objective • Demonstrate Prospera Heart - guided surveillance can replace routine protocol biopsies with comparable clinical outcomes. Comparative Effectiveness Phase RANDOMIZATION 30 DAYS ( ± 10 days) post - Tx Months 2 - 3 ~biweekly visits* First randomized - controlled trial to compare dd - cfDNA surveillance to routine biopsy in organ transplantation EMB other standard of care (SOC) assessments Prospera other standard of care (SOC) assessments Months 4 - 6 ~monthly visits* EMB other SOC assessments Months 7 - 12 ~visits every 1 - 3 months* EMB other SOC assessments Prospera other SOC assessments Prospera other SOC assessments STUDY COMPLETION Month 12 (+ 30d) STUDY COMPLETION Heart Transplant Primary endpoint: Incidence of the composite endpoint of treated rejection, graft dysfunction, re - transplantation, or death at 12 months after HTx *Timing of visits per institutional protocol • >300 patients enrolled • 17 sites • 12 months of follow up ~weekly study visits* Not for reproduction or further distribution.

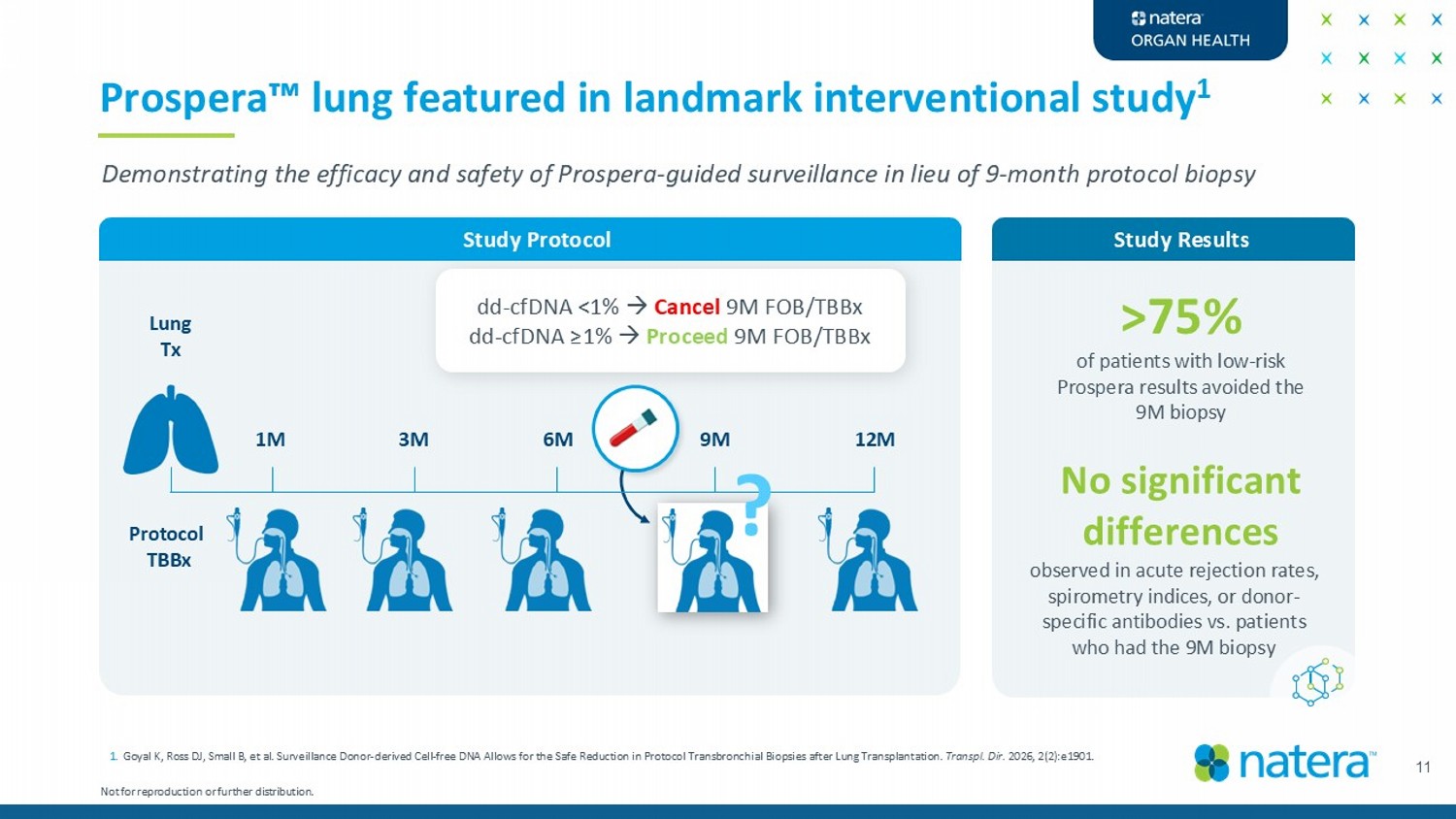

11 Prospera lung featured in landmark interventional study 1 Lung Tx 1M 3M 6M 12M 9M Protocol TBBx dd - cfDNA <1% Cancel 9M FOB/TBBx dd - cfDNA ≥ 1% Proceed 9M FOB/TBBx ? Study Results >75% of patients with low - risk Prospera results avoided the 9M biopsy Not for reproduction or further distribution. No significant differences Study Protocol Demonstrating the efficacy and safety of Prospera - guided surveillance in lieu of 9 - month protocol biopsy 1. Goyal K, Ross DJ, Small B, et al. Surveillance Donor - derived Cell - free DNA Allows for the Safe Reduction in Protocol Transbronch ial Biopsies after Lung Transplantation. Transpl . Dir. 2026, 2(2):e1901. observed in acute rejection rates, spirometry indices, or donor - specific antibodies vs. patients who had the 9M biopsy

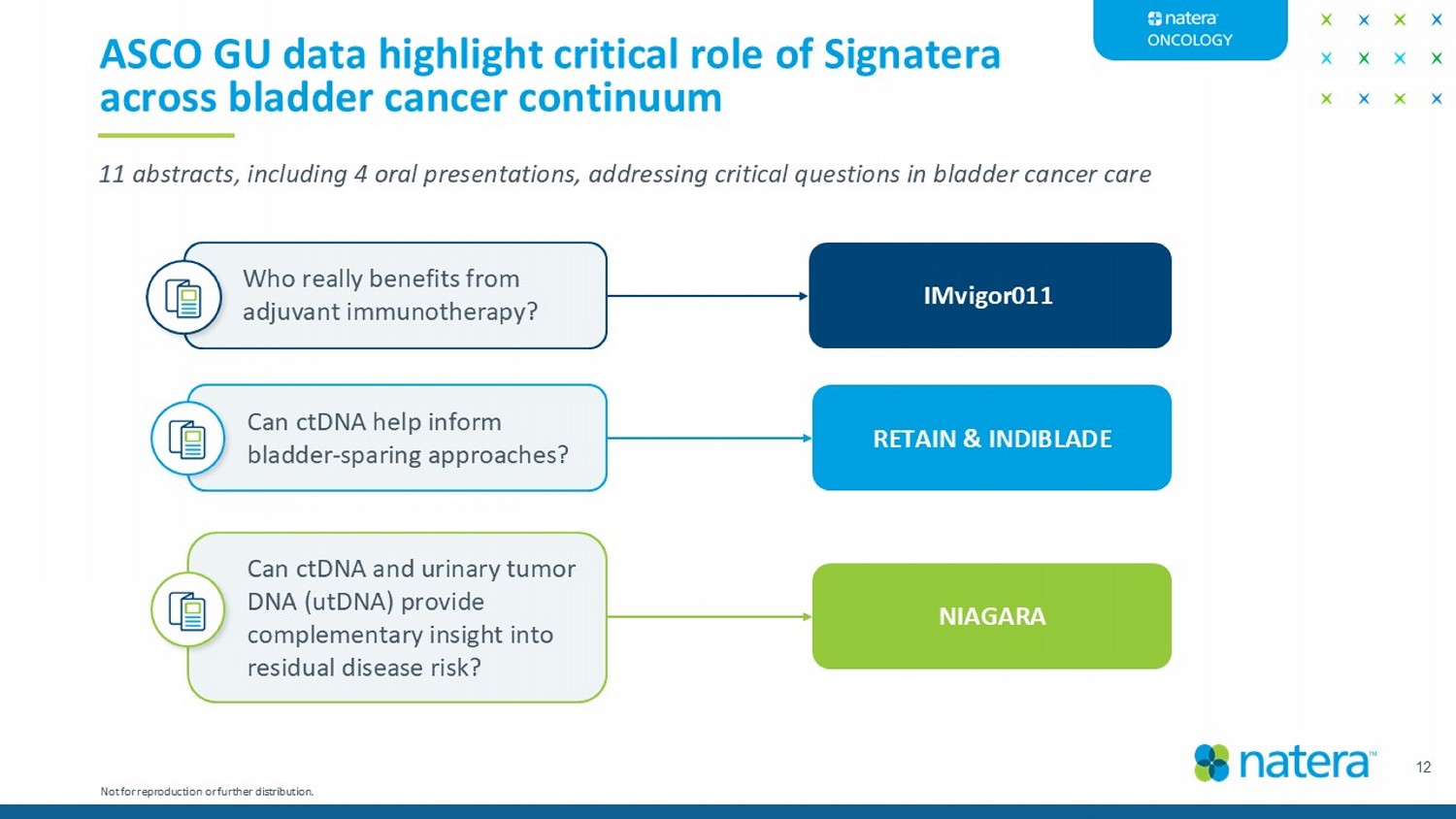

12 ASCO GU data highlight critical role of Signatera across bladder cancer continuum 11 abstracts, including 4 oral presentations, addressing critical questions in bladder cancer care Can ctDNA help inform bladder - sparing approaches? Who really benefits from adjuvant immunotherapy? Can ctDNA and urinary tumor DNA (utDNA) provide complementary insight into residual disease risk? RETAIN & INDIBLADE IMvigor011 NIAGARA Not for reproduction or further distribution.

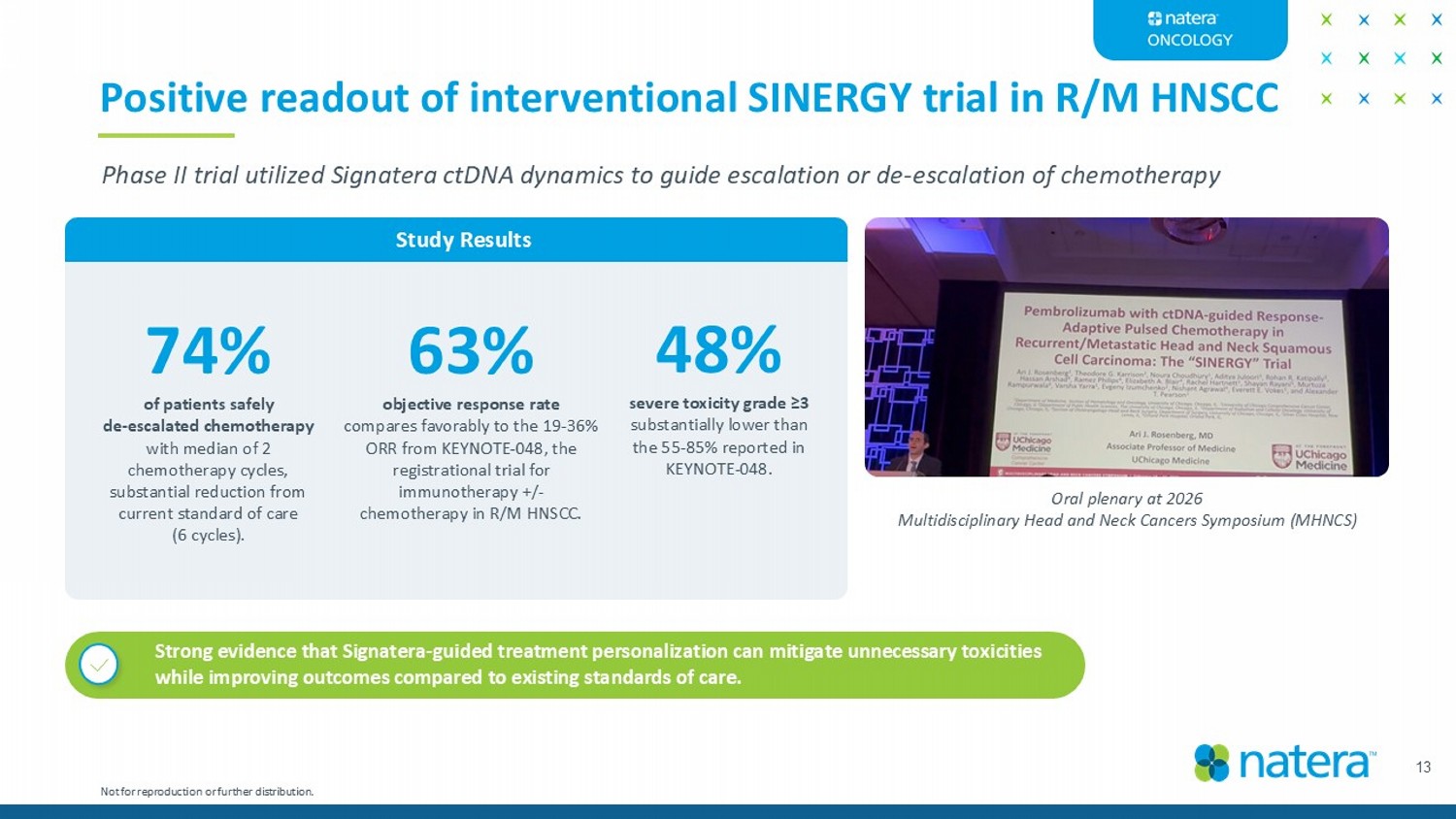

13 Positive readout of interventional SINERGY trial in R/M HNSCC Phase II trial utilized Signatera ctDNA dynamics to guide escalation or de - escalation of chemotherapy 74% of patients safely de - escalated chemotherapy with median of 2 chemotherapy cycles, substantial reduction from current standard of care (6 cycles). 63% objective response rate compares favorably to the 19 - 36% ORR from KEYNOTE - 048, the registrational trial for immunotherapy +/ - chemotherapy in R/M HNSCC . 48% severe toxicity grade ≥3 substantially lower than the 55 - 85% reported in KEYNOTE - 048. Oral plenary at 2026 Multidisciplinary Head and Neck Cancers Symposium (MHNCS) Study Results Strong evidence that Signatera - guided treatment personalization can mitigate unnecessary toxicities while improving outcomes compared to existing standards of care. Not for reproduction or further distribution.

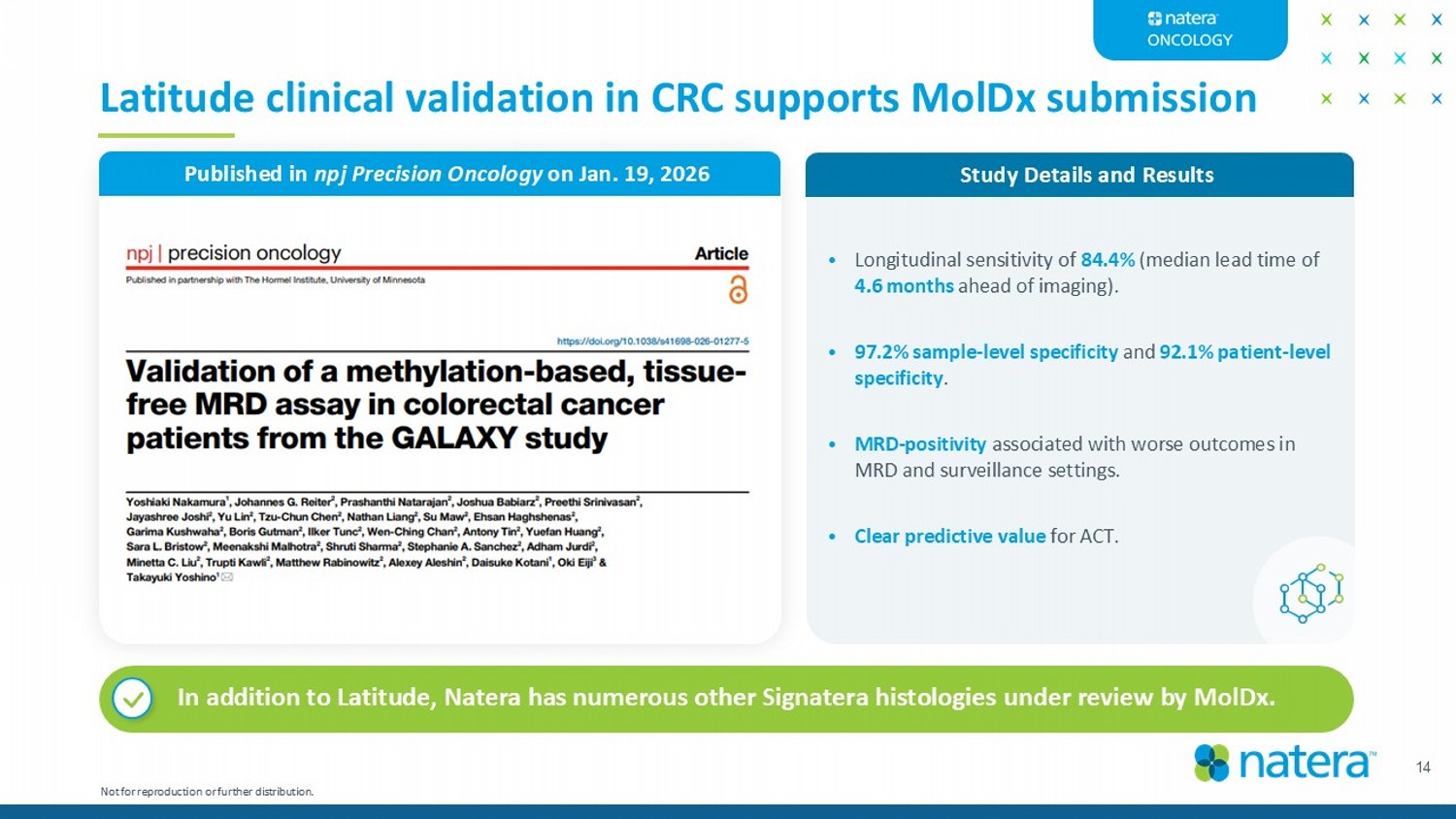

14 Latitude clinical validation in CRC supports MolDx submission In addition to Latitude, Natera has numerous other Signatera histologies under review by MolDx . Study Details and Results • Longitudinal sensitivity of 84.4% (median lead time of 4.6 months ahead of imaging). • 97.2% sample - level specificity and 92.1% patient - level specificity . • MRD - positivity associated with worse outcomes in MRD and surveillance settings. • Clear predictive value for ACT. Published in npj Precision Oncology on Jan. 19, 2026 Not for reproduction or further distribution.

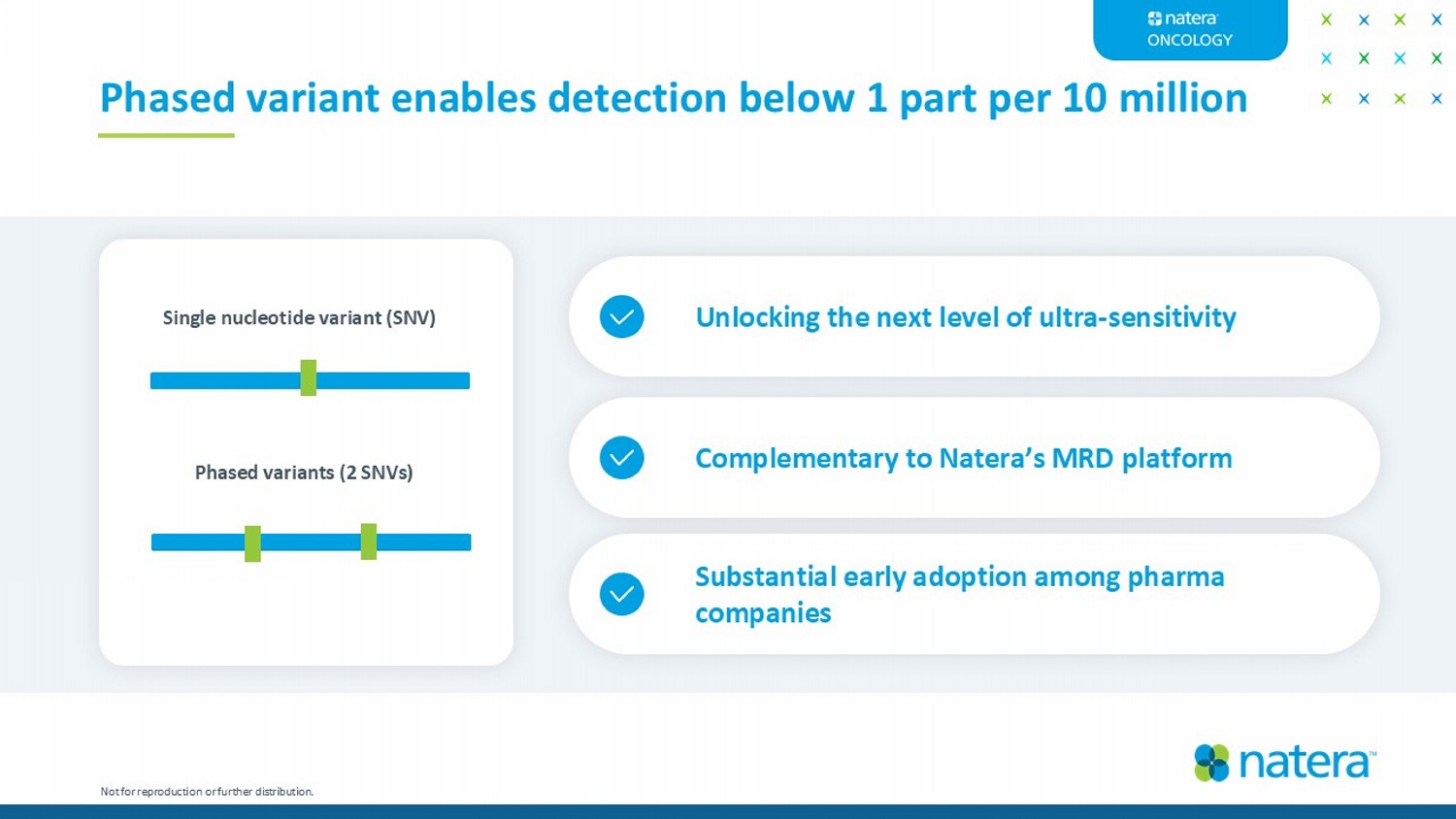

Phased variant enables detection below 1 part per 10 million Unlocking the next level of ultra - sensitivity Complementary to Natera’s MRD platform Substantial early adoption among pharma companies Single nucleotide variant (SNV) Phased variants (2 SNVs) Not for reproduction or further distribution.

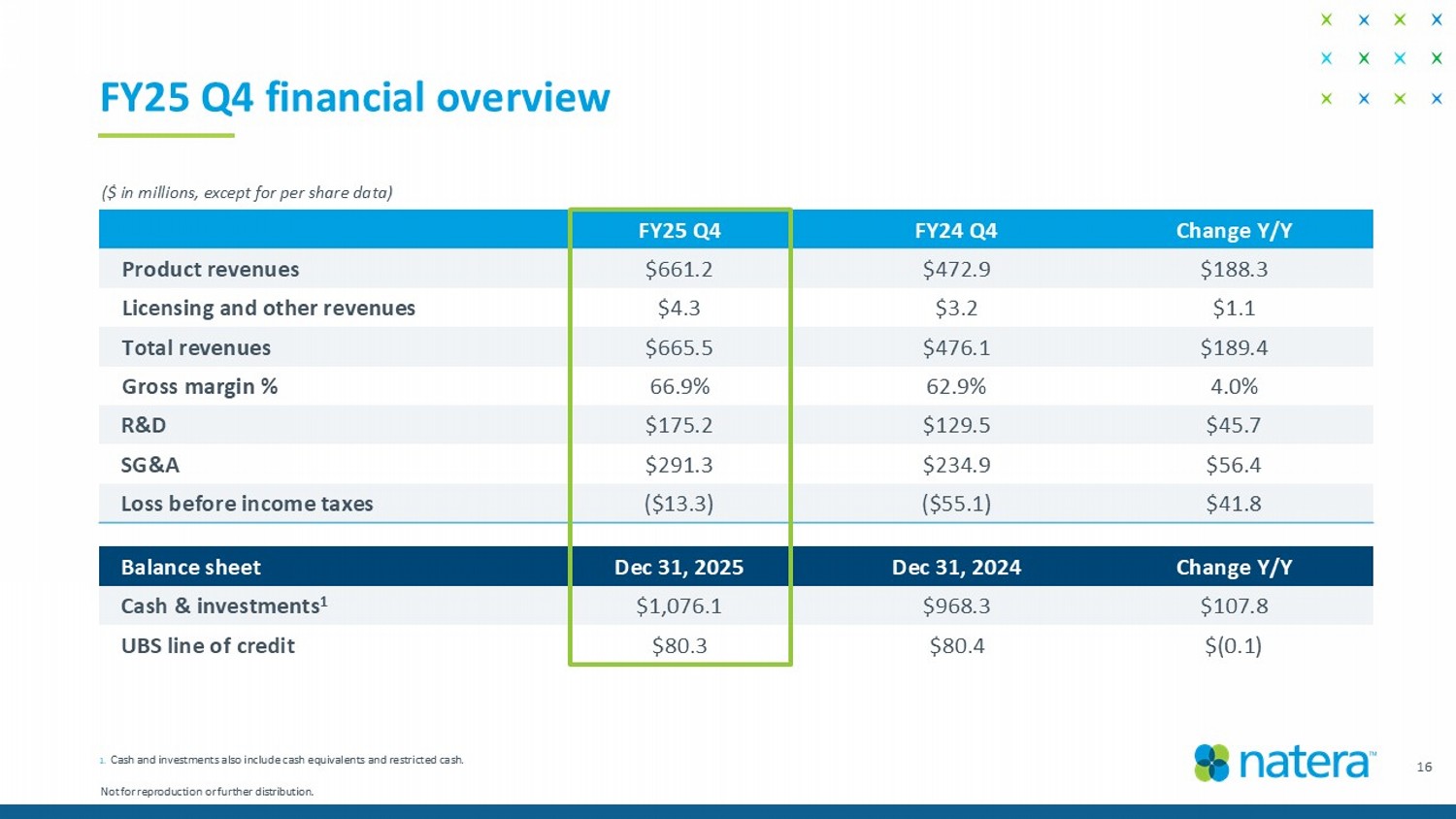

FY25 Q4 financial overview 1. Cash and investments also include cash equivalents and restricted cash. ($ in millions, except for per share data) Change Y/Y Dec 31, 2024 Dec 31, 2025 Balance sheet $107.8 $968.3 $1,076.1 Cash & investments 1 $(0.1) $80.4 $80.3 UBS line of credit Change Y/Y FY24 Q4 FY25 Q4 $188.3 $472.9 $661.2 Product revenues $1.1 $3.2 $4.3 Licensing and other revenues $189.4 $476.1 $665.5 Total revenues 4.0% 62.9% 66.9% Gross margin % $45.7 $129.5 $175.2 R&D $56.4 $234.9 $291.3 SG&A $41.8 ($55.1) ($13.3) Loss before income taxes 16 Not for reproduction or further distribution.

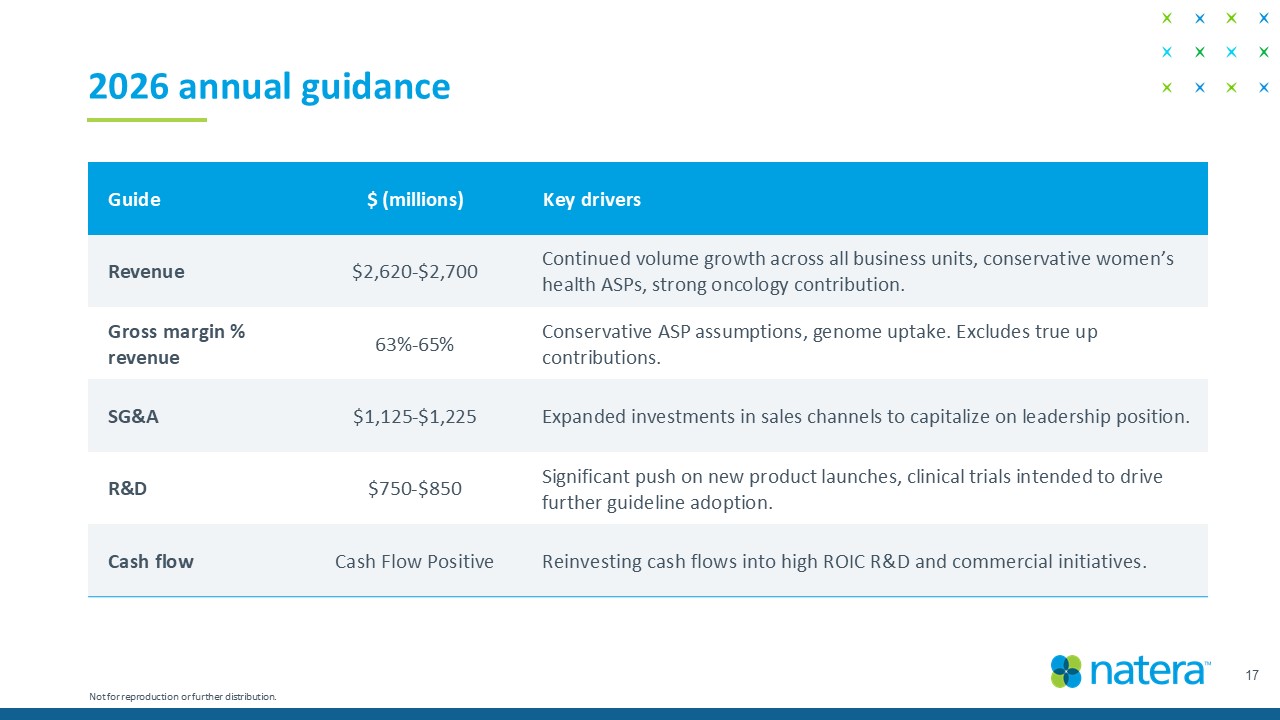

Key drivers $ (millions) Guide Continued volume growth across all business units, conservative women’s health ASPs, strong oncology contribution. $ 2,600 - $2,680 Revenue Conservative ASP assumptions, genome uptake. Excludes true up contributions. 63 % - 65 % Gross margin % revenue Expanded investments in sales channels to capitalize on leadership position. $ 1,125 - $ 1,225 SG&A Significant push on new product launches, clinical trials intended to drive further guideline adoption. $ 750 - $850 R&D Reinvesting cash flows into high ROIC R&D and commercial initiatives. Cash Flow Positive Cash flow 2026 annual guidance 17 Not for reproduction or further distribution.

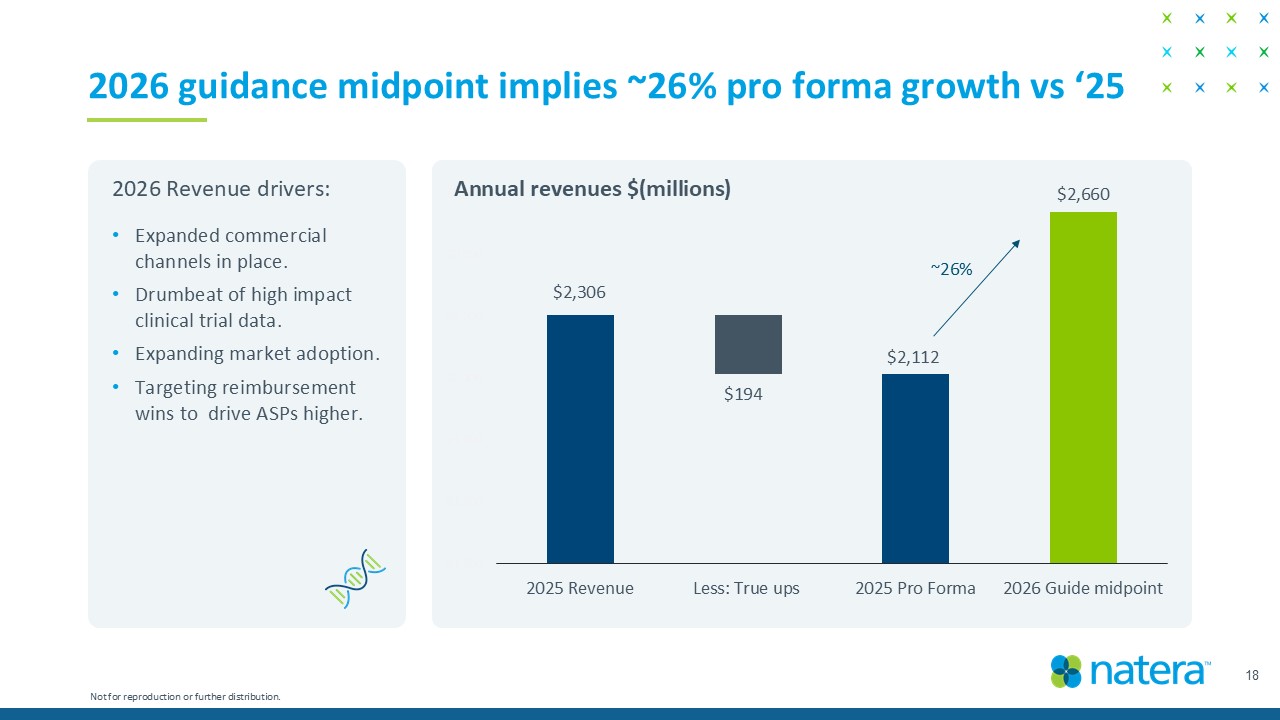

$1,500 $1,700 $1,900 $2,100 $2,300 $2,500 $2,700 2025 Revenue Less: True ups 2025 Pro Forma 2026 Guide midpoint 18 2026 guidance midpoint implies ~25% pro forma growth vs ‘25 • Expanded commercial channels in place. • Drumbeat of high impact clinical trial data. • Expanding market adoption. • Targeting reimbursement wins to drive ASPs higher. Annual revenues $(millions) ~25% 2026 Revenue drivers: Not for reproduction or further distribution. $2,306 $194 $2,112 $2,640

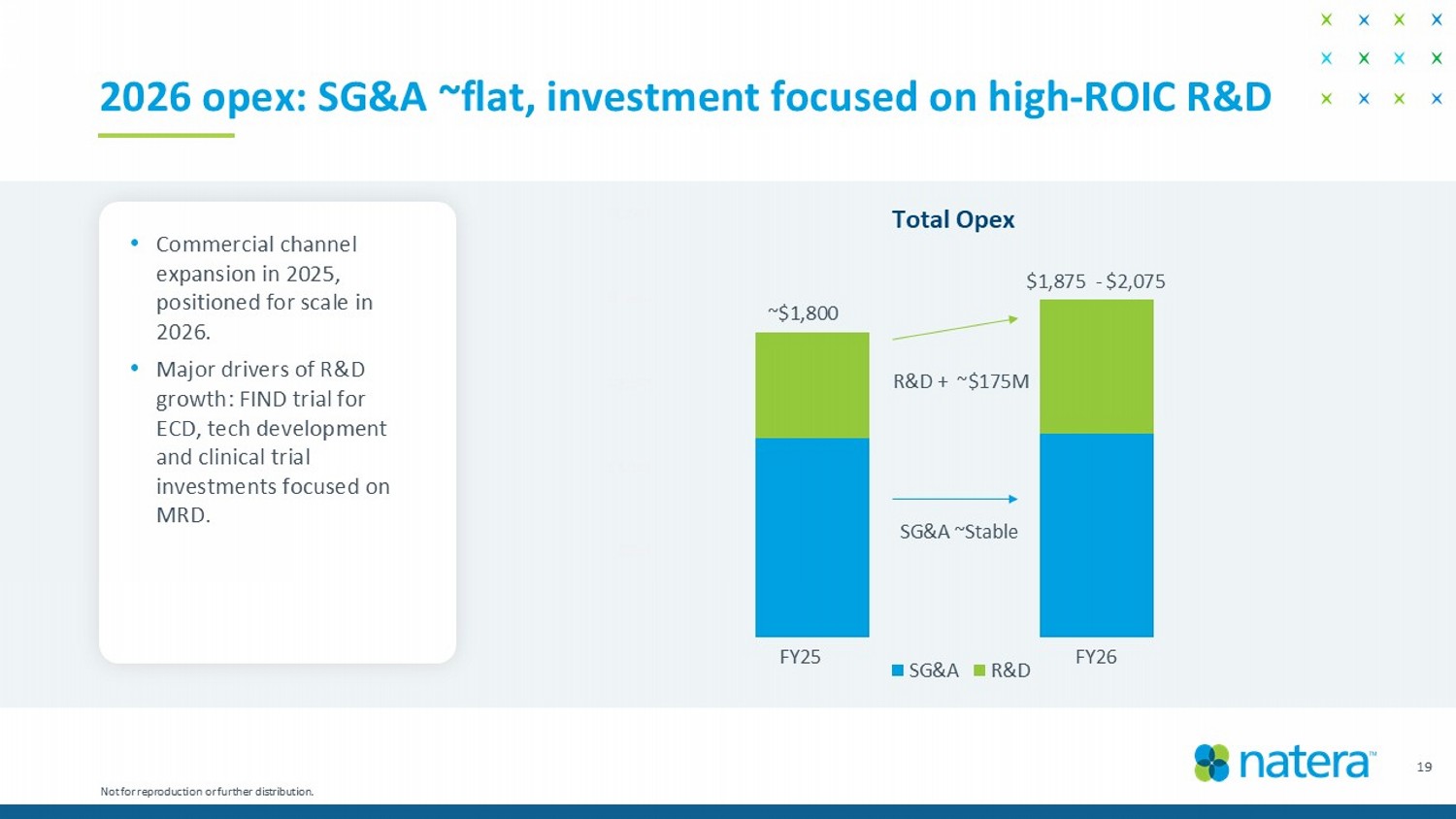

– $500 $1,000 $1,500 $2,000 $2,500 SG&A R&D 19 2026 opex: SG&A ~flat, investment focused on high - ROIC R&D $1,875 - $2,075 R&D + ~$175M SG&A ~Stable Total Opex • Commercial channel expansion in 2025, positioned for scale in 2026. • Major drivers of R&D growth: FIND trial for ECD, tech development and clinical trial investments focused on MRD . FY25 FY26 Not for reproduction or further distribution. ~$1,800

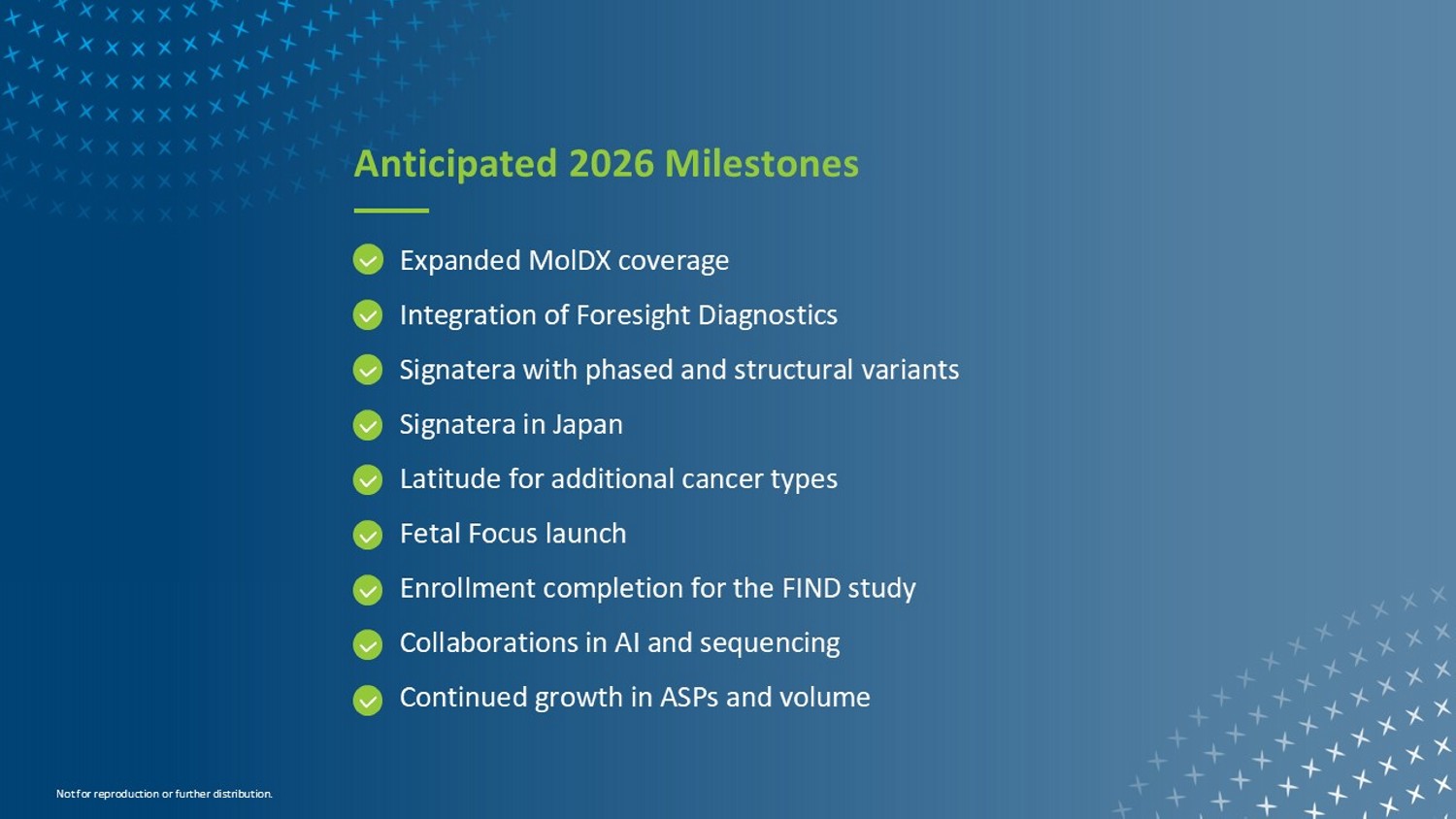

Anticipated 2026 Milestones Expanded MolDX coverage Integration of Foresight Diagnostics Signatera with phased and structural variants Signatera in Japan Latitude for additional cancer types Fetal Focus launch Enrollment completion for the FIND study Collaborations in AI and sequencing Continued growth in ASPs and volume Not for reproduction or further distribution.

©202 5 Natera, Inc. All Rights Reserved. Not for reproduction or further distribution. ®