.2

| 0 Supplemental Financial Presentation May 2026 Offering everyone a piece of the American spirit—one handshake at a time. |

| 1 Important Information Forward-Looking Statements This presentation contains forward-looking statements that are subject to risks and uncertainties. All statements other than statements of historical fact included in this presentation are forward-looking statements. Forward-looking statements refer to Boot Barn Holdings, Inc.’s (the “Company,” “Boot Barn,” “BOOT,” “we,” “us,” and “our”) current expectations and projections relating to, by way of example and without limitation, the Company’s financial condition, liquidity, profitability, results of operations, margins, plans, objectives, strategies, future performance, business, and industry. You can identify forward-looking statements by the fact that they generally do not relate strictly to historical or current facts. These statements may include words such as “anticipate”, “estimate”, “expect”, “project”, “plan“, “intend”, “believe”, “may”, “might”, “will”, “could”, “should”, “can have”, “likely”, “outlook”, and other words and terms of similar meaning in connection with any discussion of the timing or nature of future operating or financial performance or other events, but not all forward-looking statements contain these identifying words. These forward-looking statements are based on assumptions that the Company’s management has made in light of their industry experience and on their perceptions of historical trends, current conditions, expected future developments and other factors that they believe are appropriate under the circumstances. As you consider this presentation, you should understand that these statements are not guarantees of performance or results. They involve risks, uncertainties (some of which are beyond the Company’s control), and assumptions. These risks, uncertainties, and assumptions include, but are not limited to, the following: decreases in consumer spending due to declines in consumer confidence, local economic conditions, or changes in consumer preferences; the impact that import tariffs and other trade restrictions imposed by the U.S., or other countries have had, and may continue to have, on our product costs and changes to U.S. or other countries’ trade policies and tariff and import/export regulations; the Company’s ability to effectively execute on its growth strategy; and the Company’s failure to maintain and enhance its strong brand image, to compete effectively, to maintain good relationships with its key suppliers, and to improve and expand its exclusive product offerings. The Company discusses the foregoing risks and other risks in greater detail under the heading “Risk factors” in the periodic reports filed by the Company with the Securities and Exchange Commission. Although the Company believes that these forward-looking statements are based on reasonable assumptions, you should be aware that many factors could affect the Company’s actual financial results and cause them to differ materially from those anticipated in the forward-looking statements. Because of these factors, the Company cautions that you should not place undue reliance on any of these forward-looking statements. New risks and uncertainties arise from time to time, and it is impossible for the Company to predict those events or how they may affect the Company. Further, any forward-looking statement speaks only as of the date on which it is made. Except as required by law, the Company does not intend to update or revise the forward-looking statements in this presentation after the date of this presentation. Industry and Market Information Statements in this presentation concerning our industry and the markets in which we operate, including our general expectations and competitive position, business opportunity and market size, growth and share, are based on information from independent industry organizations and other third-party sources, data from our internal research, and management estimates. Management estimates are derived from publicly available information and the information and data referred to above and are based on assumptions and calculations made by us based upon our interpretation of such information and data. The information and data referred to above are imprecise and may prove to be inaccurate because the information cannot always be verified with complete certainty due to the limitations on the availability and reliability of raw data, the voluntary nature of the data gathering process, and other limitations and uncertainties. As a result, please be aware that the data and statistical information in this presentation may differ from information provided by our competitors or from information found in current or future studies conducted by market research institutes, consultancy firms, or independent sources. Recent Developments Our business and opportunities for growth depend on consumer discretionary spending, and as such, our results are particularly sensitive to economic conditions and consumer confidence. Inflation, changes to U.S. or other countries’ trade policies and tariff and import/export regulations, and other challenges affecting the global economy could impact our operations and will depend on future developments, which are uncertain. These and other effects make it more challenging for us to estimate the future performance of our business, particularly over the near-to-medium term. For further discussion of the uncertainties and business risks affecting the Company, see the sections captioned “Risk factors” in our periodic reports filed with the Securities and Exchange Commission. |

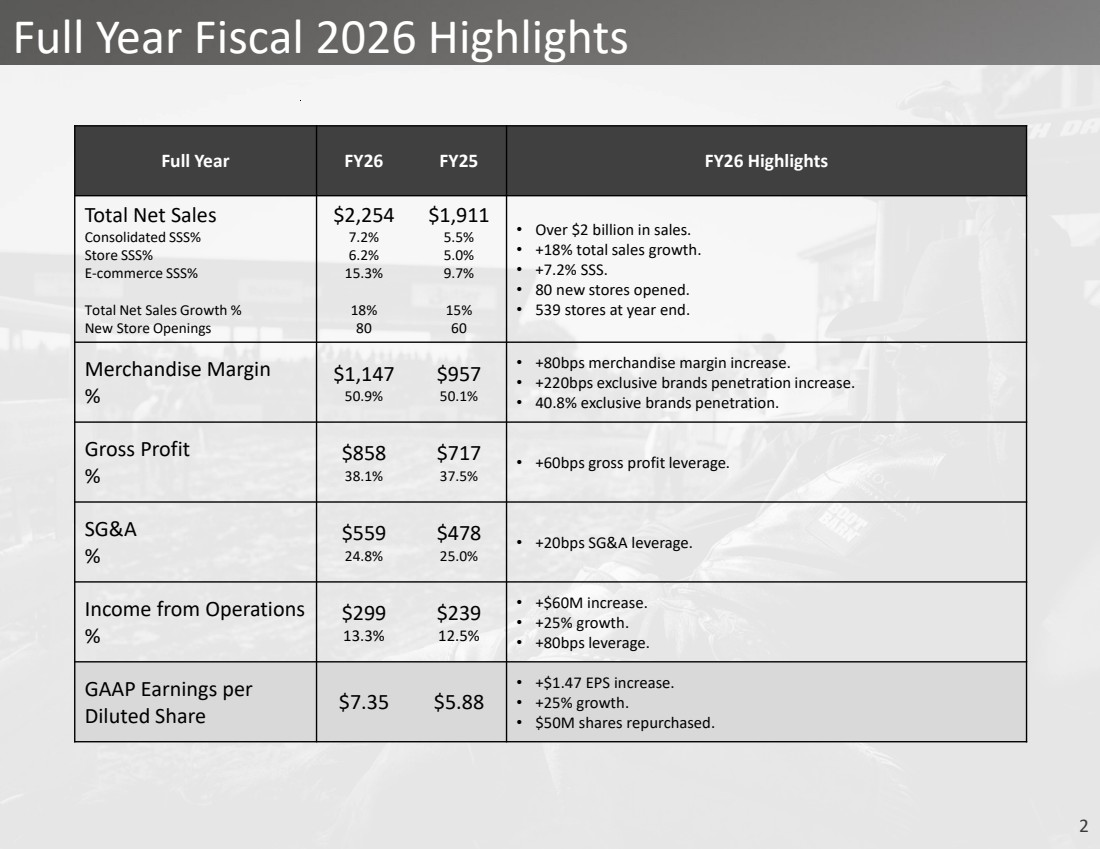

| 2 Full Year Fiscal 2026 Highlights Full Year FY26 FY25 FY26 Highlights Total Net Sales Consolidated SSS% Store SSS% E-commerce SSS% Total Net Sales Growth % New Store Openings $2,254 7.2% 6.2% 15.3% 18% 80 $1,911 5.5% 5.0% 9.7% 15% 60 • Over $2 billion in sales. • +18% total sales growth. • +7.2% SSS. • 80 new stores opened. • 539 stores at year end. Merchandise Margin % $1,147 50.9% $957 50.1% • +80bps merchandise margin increase. • +220bps exclusive brands penetration increase. • 40.8% exclusive brands penetration. Gross Profit % $858 38.1% $717 37.5% • +60bps gross profit leverage. SG&A % $559 24.8% $478 25.0% • +20bps SG&A leverage. Income from Operations % $299 13.3% $239 12.5% • +$60M increase. • +25% growth. • +80bps leverage. GAAP Earnings per Diluted Share $7.35 $5.88 • +$1.47 EPS increase. • +25% growth. • $50M shares repurchased. |

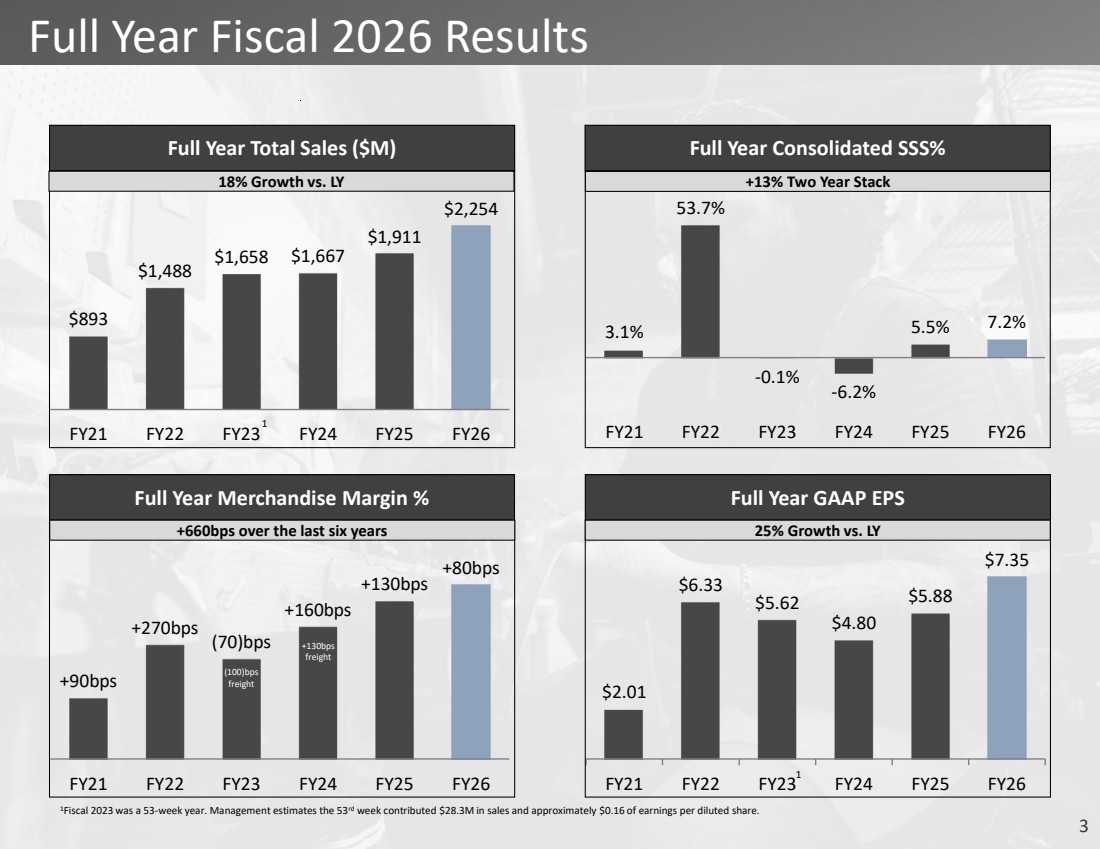

| 3 $2.01 $6.33 $5.62 $4.80 $5.88 $7.35 FY21 FY22 FY23 FY24 FY25 FY26 $893 $1,488 $1,658 $1,667 $1,911 $2,254 FY21 FY22 FY23 FY24 FY25 FY26 Full Year Fiscal 2026 Results 1Fiscal 2023 was a 53-week year. Management estimates the 53rd week contributed $28.3M in sales and approximately $0.16 of earnings per diluted share. 1 1 Full Year Total Sales ($M) 3.1% 53.7% -0.1% -6.2% 5.5% 7.2% FY21 FY22 FY23 FY24 FY25 FY26 Full Year Consolidated SSS% +90bps +270bps (70)bps +160bps +130bps +80bps FY21 FY22 FY23 FY24 FY25 FY26 Full Year Merchandise Margin % Full Year GAAP EPS (100)bps freight +130bps freight +660bps over the last six years 18% Growth vs. LY 25% Growth vs. LY +13% Two Year Stack |

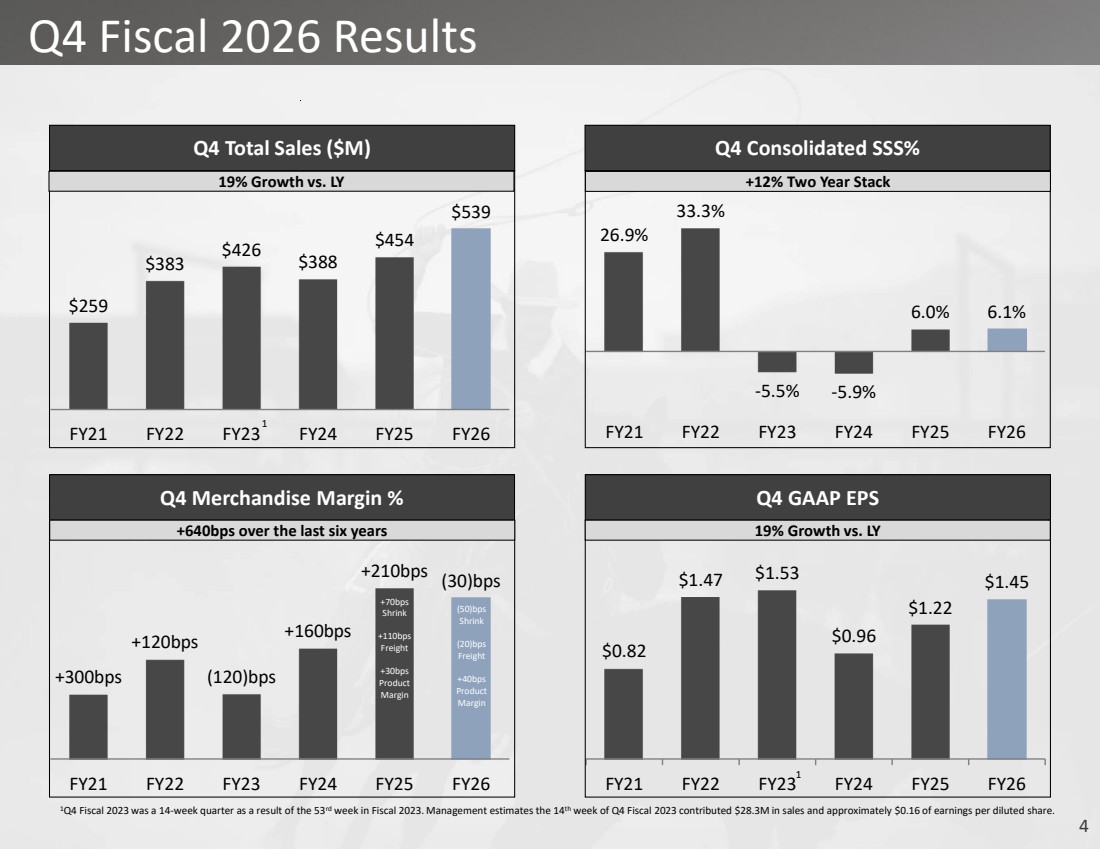

| 4 Q4 Fiscal 2026 Results 1Q4 Fiscal 2023 was a 14-week quarter as a result of the 53rd week in Fiscal 2023. Management estimates the 14th week of Q4 Fiscal 2023 contributed $28.3M in sales and approximately $0.16 of earnings per diluted share. $259 $383 $426 $388 $454 $539 FY21 FY22 FY23 FY24 FY25 FY26 Q4 Total Sales ($M) 26.9% 33.3% -5.5% -5.9% 6.0% 6.1% FY21 FY22 FY23 FY24 FY25 FY26 Q4 Consolidated SSS% +300bps +120bps (120)bps +160bps +210bps (30)bps FY21 FY22 FY23 FY24 FY25 FY26 Q4 Merchandise Margin % $0.82 $1.47 $1.53 $0.96 $1.22 $1.45 FY21 FY22 FY23 FY24 FY25 FY26 Q4 GAAP EPS +640bps over the last six years 19% Growth vs. LY 19% Growth vs. LY +12% Two Year Stack (50)bps Shrink (20)bps Freight +40bps Product Margin +70bps Shrink +110bps Freight +30bps Product Margin 1 1 |

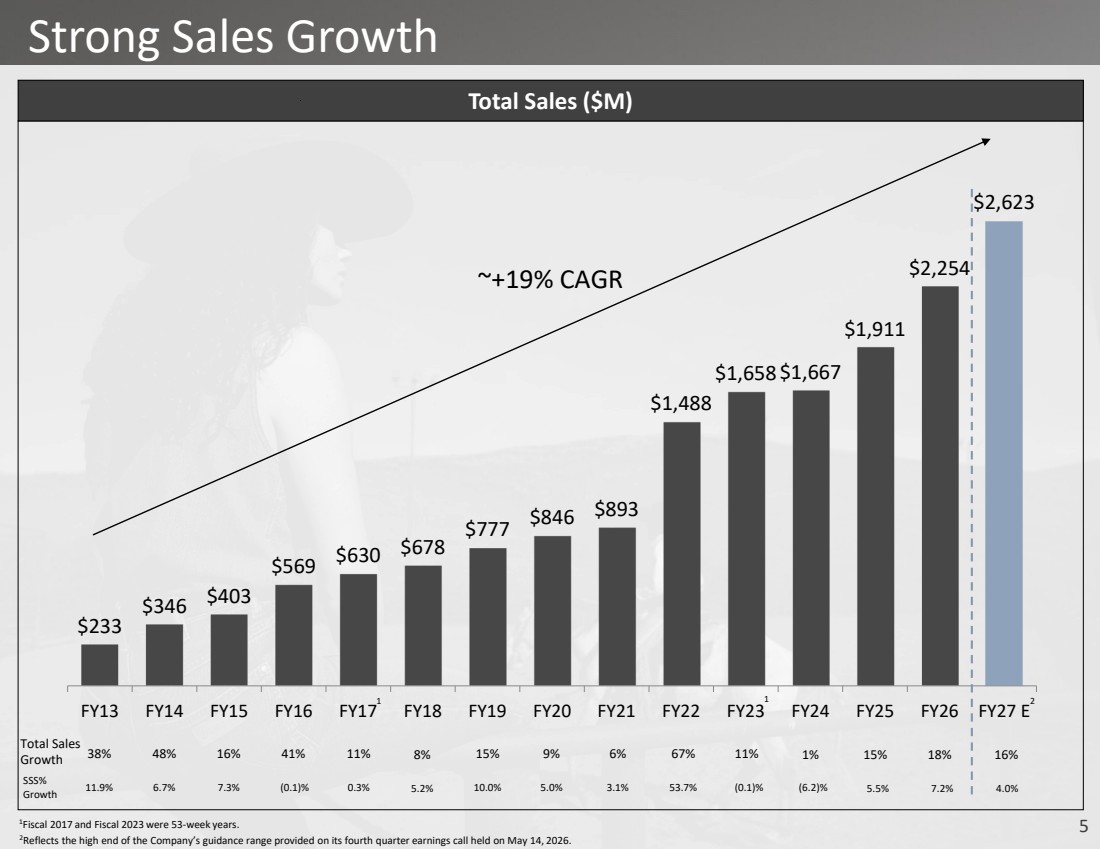

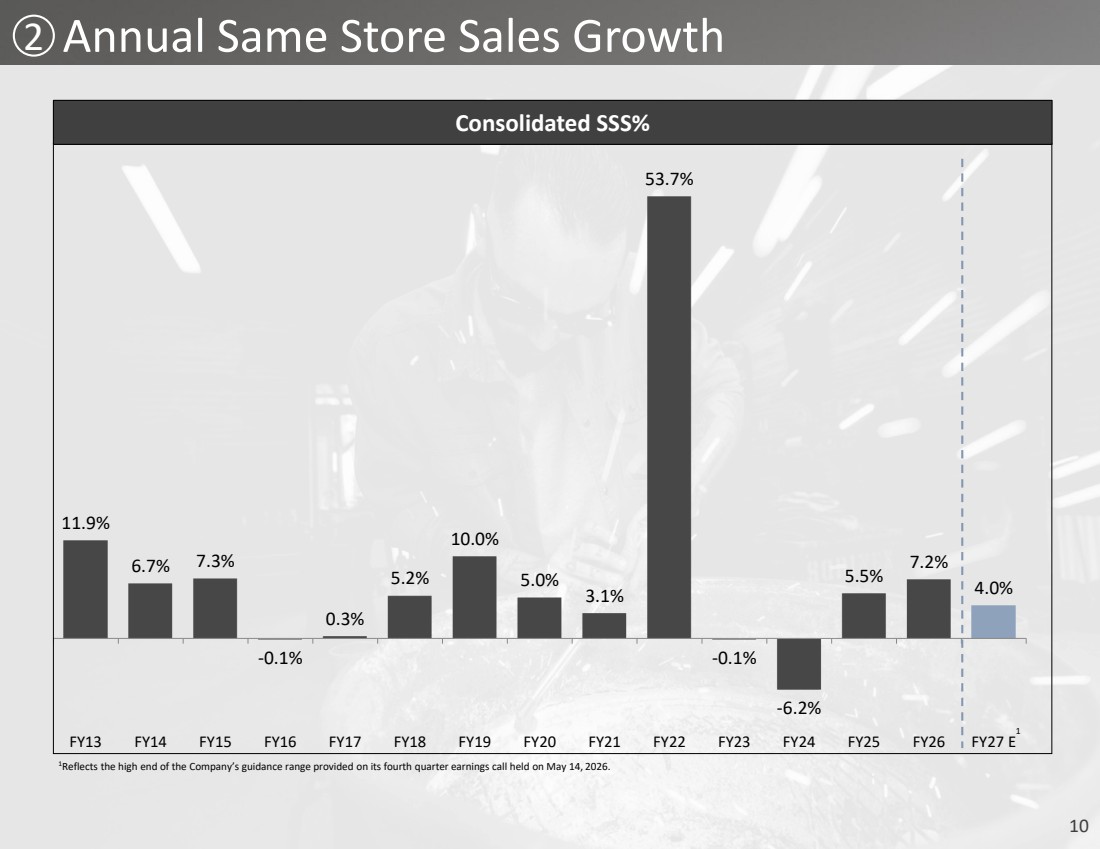

| 5 $233 $346 $403 $569 $630 $678 $777 $846 $893 $1,488 $1,658 $1,667 $1,911 $2,254 $2,623 FY13 FY14 FY15 FY16 FY17 FY18 FY19 FY20 FY21 FY22 FY23 FY24 FY25 FY26 FY27 E Total Sales ($M) Total Sales Growth 38% 48% 16% 41% 11% 8% 15% 9% 6% 67% 11% Strong Sales Growth 1 1 1Fiscal 2017 and Fiscal 2023 were 53-week years. 1% ~+19% CAGR SSS% Growth 11.9% 6.7% 7.3% (0.1)% 0.3% 5.2% 10.0% 5.0% 3.1% 53.7% (0.1)% (6.2)% 15% 5.5% 18% 7.2% 16% 4.0% 2 2Reflects the high end of the Company’s guidance range provided on its fourth quarter earnings call held on May 14, 2026. |

| 6 Strategic Initiatives Update 1 2 3 4 New Stores Same Store Sales Omni-Channel Merchandise Margin & Exclusive Brands |

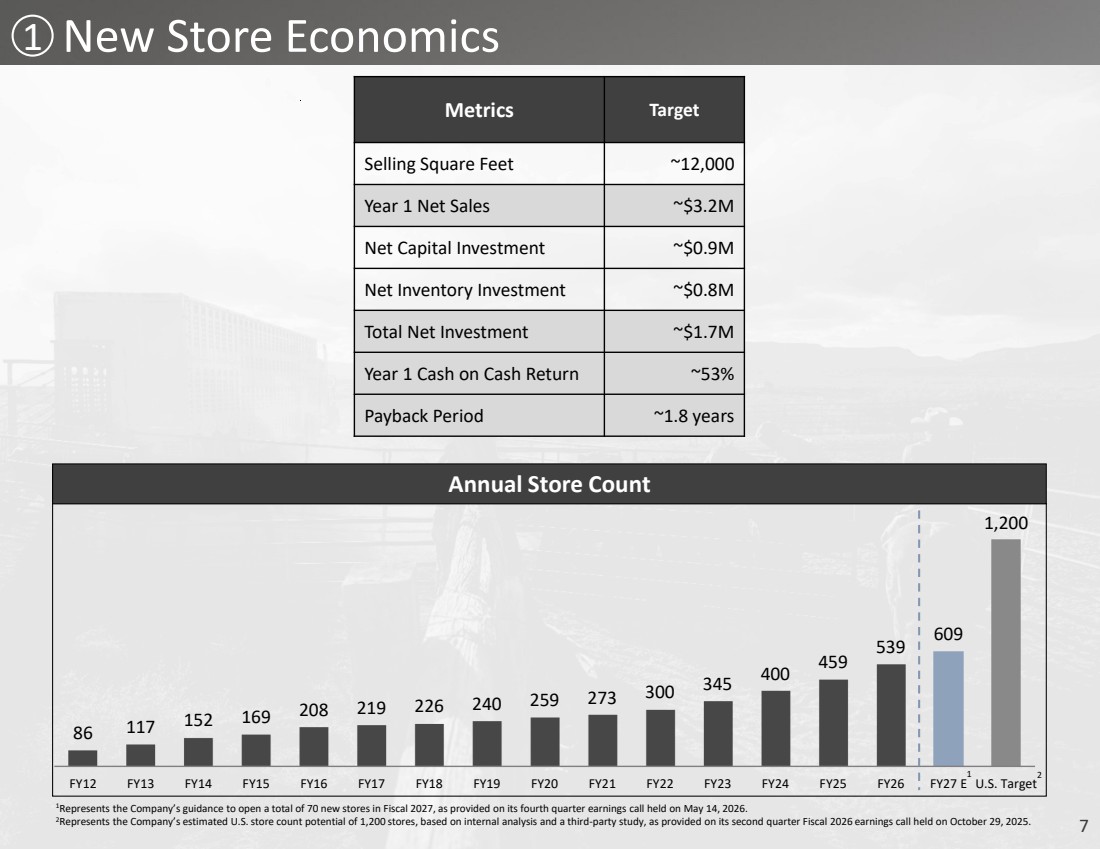

| 7 1 New Store Economics 1Represents the Company’s guidance to open a total of 70 new stores in Fiscal 2027, as provided on its fourth quarter earnings call held on May 14, 2026. 2Represents the Company’s estimated U.S. store count potential of 1,200 stores, based on internal analysis and a third-party study, as provided on its second quarter Fiscal 2026 earnings call held on October 29, 2025. 86 117 152 169 208 219 226 240 259 273 300 345 400 459 539 609 1,200 FY12 FY13 FY14 FY15 FY16 FY17 FY18 FY19 FY20 FY21 FY22 FY23 FY24 FY25 FY26 FY27 E U.S. Target Annual Store Count 1 Metrics Target Selling Square Feet ~12,000 Year 1 Net Sales ~$3.2M Net Capital Investment ~$0.9M Net Inventory Investment ~$0.8M Total Net Investment ~$1.7M Year 1 Cash on Cash Return ~53% Payback Period ~1.8 years 2 |

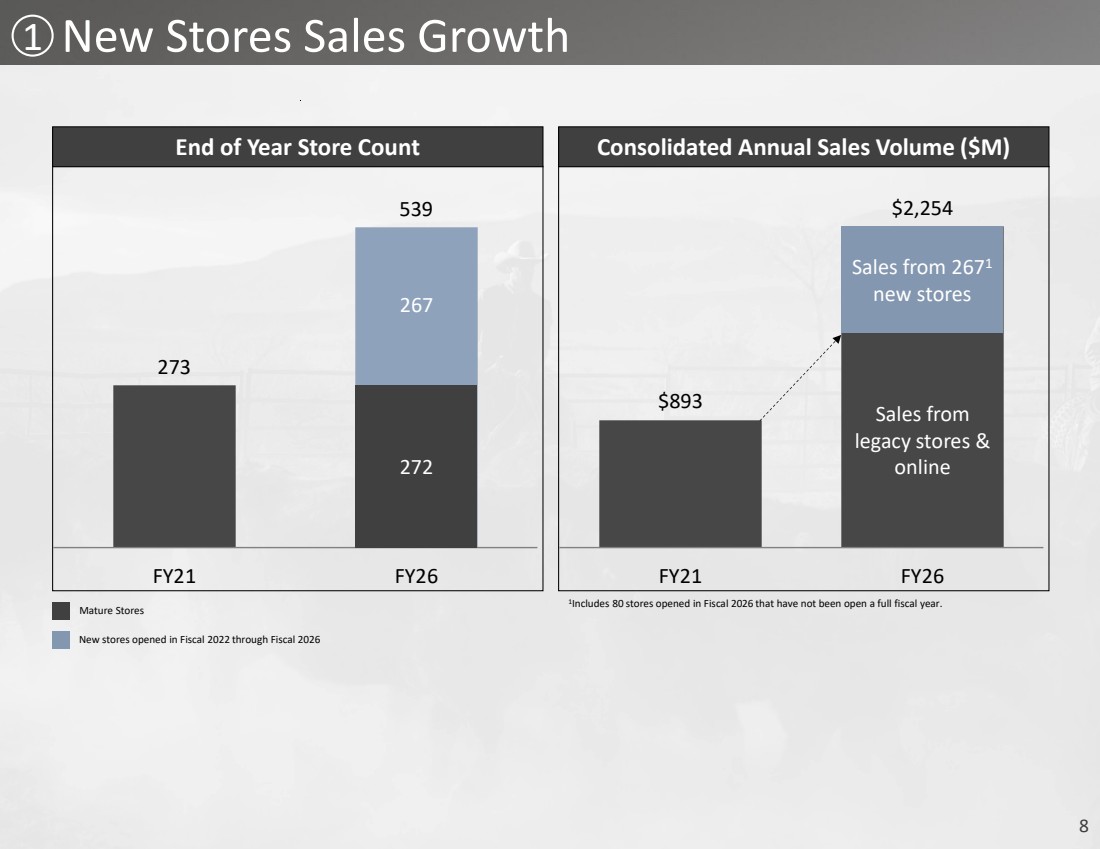

| 8 1 New Stores Sales Growth 273 539 FY21 FY26 End of Year Store Count $893 $2,254 FY21 FY26 Consolidated Annual Sales Volume ($M) Sales from 2671 new stores Sales from legacy stores & 272 online 267 1 Includes 80 stores opened in Fiscal 2026 that have not been open a full fiscal year. Mature Stores New stores opened in Fiscal 2022 through Fiscal 2026 |

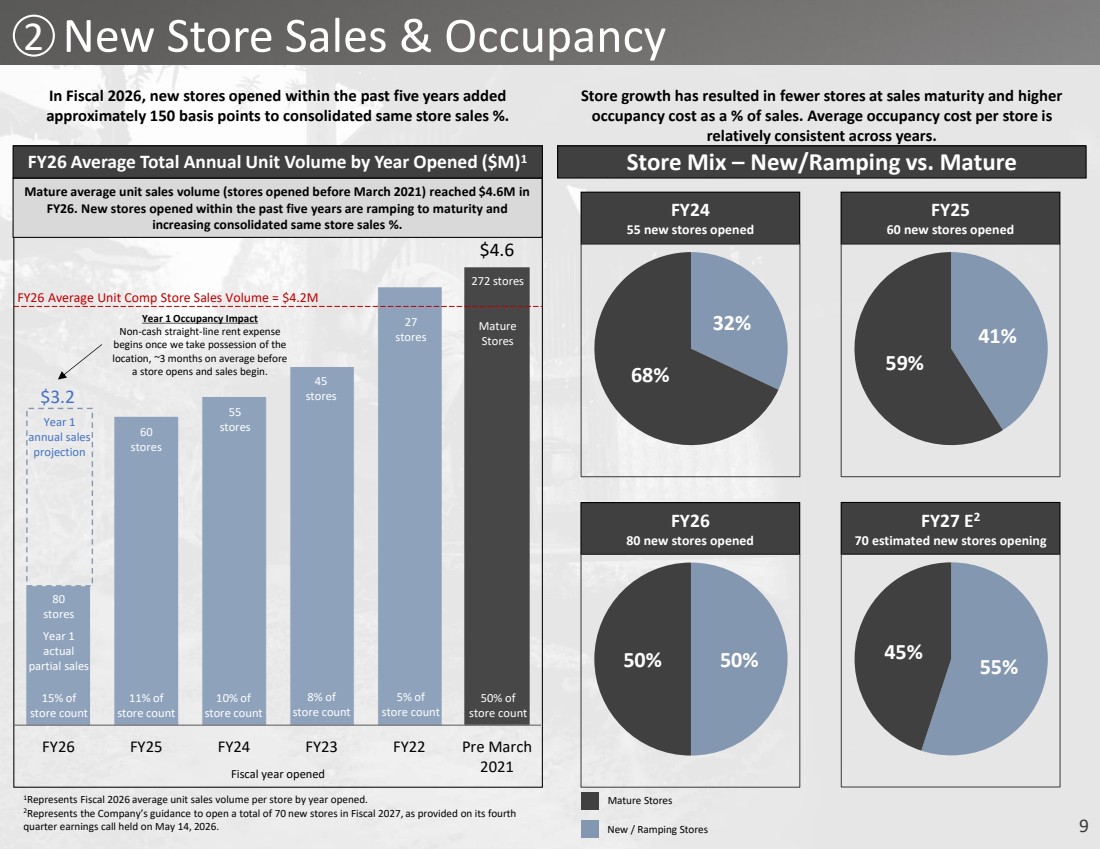

| 9 2 New Store Sales & Occupancy $4.6 FY26 FY25 FY24 FY23 FY22 Pre March 2021 FY26 Average Total Annual Unit Volume by Year Opened ($M)1 272 stores Mature Stores 27 stores 45 stores 55 stores 60 stores 80 stores Year 1 actual partial sales Year 1 annual sales projection 11% of store count 15% of store count 8% of store count 10% of store count 50% of store count 5% of store count Store Mix – New/Ramping vs. Mature FY24 55 new stores opened 32% 68% FY25 60 new stores opened 41% 59% FY26 80 new stores opened 50% 50% FY27 E2 70 estimated new stores opening 55% 45% In Fiscal 2026, new stores opened within the past five years added approximately 150 basis points to consolidated same store sales %. Store growth has resulted in fewer stores at sales maturity and higher occupancy cost as a % of sales. Average occupancy cost per store is relatively consistent across years. Fiscal year opened Year 1 Occupancy Impact Non-cash straight-line rent expense begins once we take possession of the location, ~3 months on average before a store opens and sales begin. Mature average unit sales volume (stores opened before March 2021) reached $4.6M in FY26. New stores opened within the past five years are ramping to maturity and increasing consolidated same store sales %. Mature Stores New / Ramping Stores $3.2 1Represents Fiscal 2026 average unit sales volume per store by year opened. 2Represents the Company’s guidance to open a total of 70 new stores in Fiscal 2027, as provided on its fourth quarter earnings call held on May 14, 2026. FY26 Average Unit Comp Store Sales Volume = $4.2M |

| 10 2 11.9% 6.7% 7.3% -0.1% 0.3% 5.2% 10.0% 5.0% 3.1% 53.7% -0.1% -6.2% 5.5% 7.2% 4.0% FY13 FY14 FY15 FY16 FY17 FY18 FY19 FY20 FY21 FY22 FY23 FY24 FY25 FY26 FY27 E Consolidated SSS% 1 1Reflects the high end of the Company’s guidance range provided on its fourth quarter earnings call held on May 14, 2026. Annual Same Store Sales Growth |

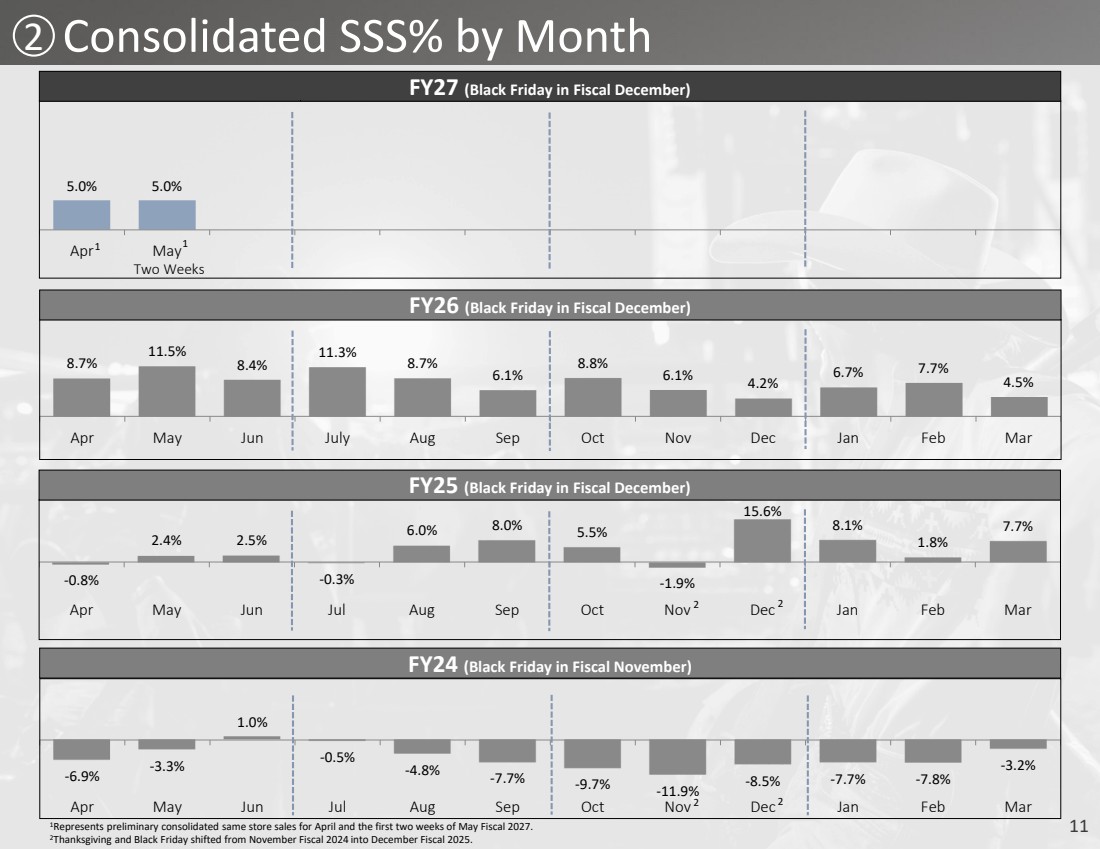

| 11 2 1Represents preliminary consolidated same store sales for April and the first two weeks of May Fiscal 2027. 2Thanksgiving and Black Friday shifted from November Fiscal 2024 into December Fiscal 2025. 8.7% 11.5% 8.4% 11.3% 8.7% 6.1% 8.8% 6.1% 4.2% 6.7% 7.7% 4.5% Apr May Jun July Aug Sep Oct Nov Dec Jan Feb Mar FY26 (Black Friday in Fiscal December) -0.8% 2.4% 2.5% -0.3% 6.0% 8.0% 5.5% -1.9% 15.6% 8.1% 1.8% 7.7% Apr May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar FY25 (Black Friday in Fiscal December) FY24 (Black Friday in Fiscal November) -6.9% -3.3% 1.0% -0.5% -4.8% -7.7% -9.7% -11.9% -8.5% -7.7% -7.8% -3.2% Apr May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar 2 2 2 2 5.0% 5.0% Apr May FY27 (Black Friday in Fiscal December) 1 1 Two Weeks Consolidated SSS% by Month |

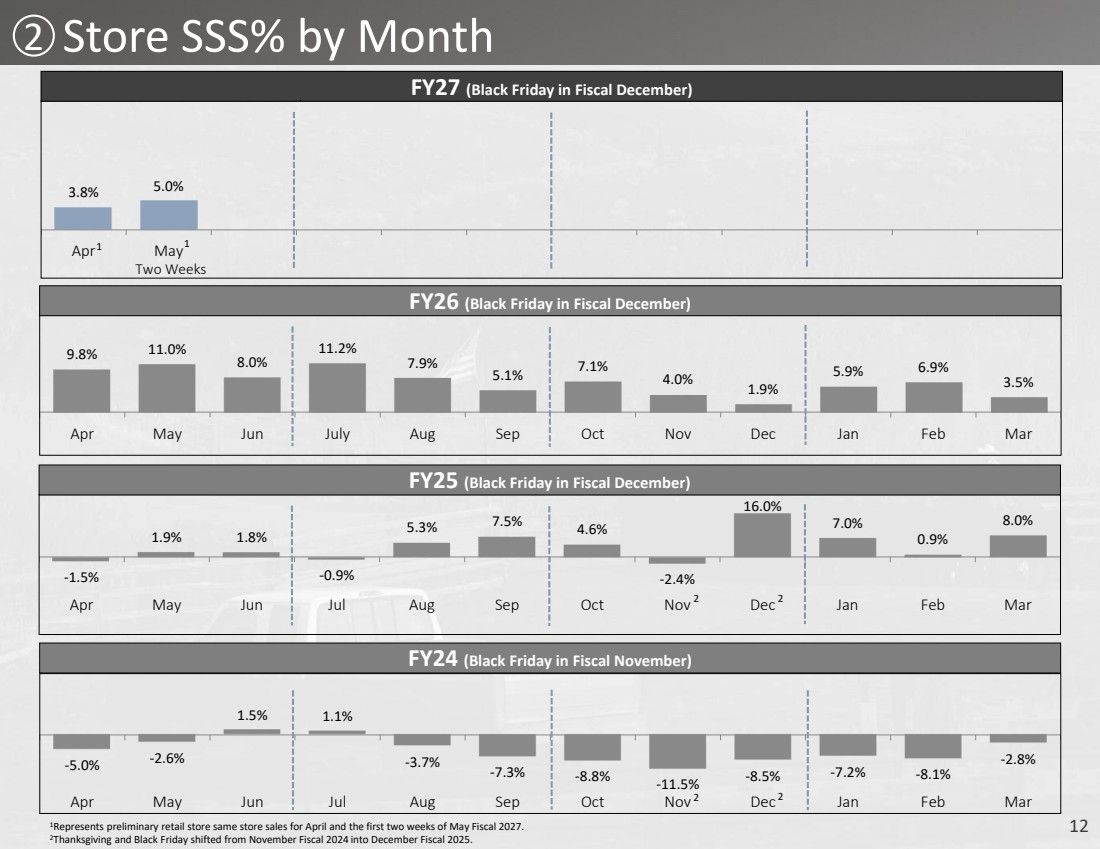

| 12 2 1Represents preliminary retail store same store sales for April and the first two weeks of May Fiscal 2027. 2Thanksgiving and Black Friday shifted from November Fiscal 2024 into December Fiscal 2025. 9.8% 11.0% 8.0% 11.2% 7.9% 5.1% 7.1% 4.0% 1.9% 5.9% 6.9% 3.5% Apr May Jun July Aug Sep Oct Nov Dec Jan Feb Mar FY26 (Black Friday in Fiscal December) -1.5% 1.9% 1.8% -0.9% 5.3% 7.5% 4.6% -2.4% 16.0% 7.0% 0.9% 8.0% Apr May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar FY25 (Black Friday in Fiscal December) FY24 (Black Friday in Fiscal November) -5.0% -2.6% 1.5% 1.1% -3.7% -7.3% -8.8% -11.5% -8.5% -7.2% -8.1% -2.8% Apr May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar 2 2 2 2 3.8% 5.0% Apr May FY27 (Black Friday in Fiscal December) 1 1 Two Weeks Store SSS% by Month |

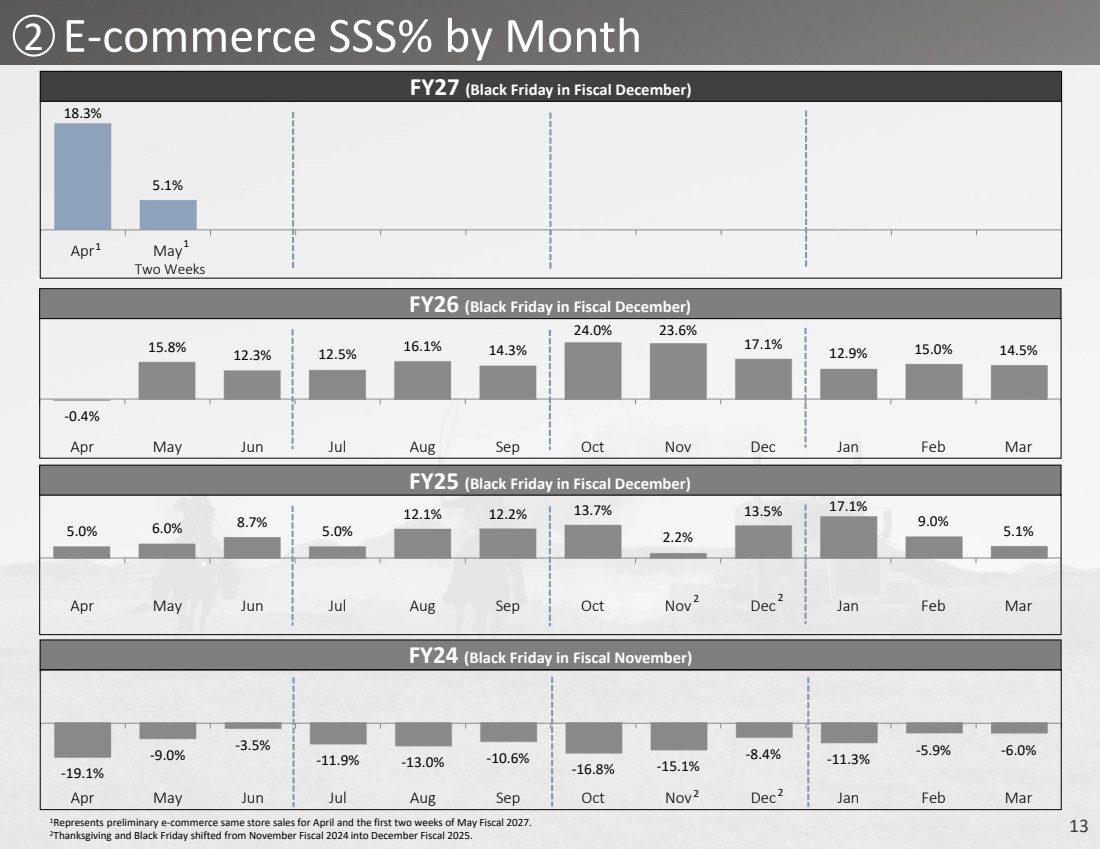

| 13 2 -0.4% 15.8% 12.3% 12.5% 16.1% 14.3% 24.0% 23.6% 17.1% 12.9% 15.0% 14.5% Apr May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar FY26 (Black Friday in Fiscal December) 5.0% 6.0% 8.7% 5.0% 12.1% 12.2% 13.7% 2.2% 13.5% 17.1% 9.0% 5.1% Apr May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar FY25 (Black Friday in Fiscal December) FY24 (Black Friday in Fiscal November) -19.1% -9.0% -3.5% -11.9% -13.0% -10.6% -16.8% -15.1% -8.4% -11.3% -5.9% -6.0% Apr May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar 1Represents preliminary e-commerce same store sales for April and the first two weeks of May Fiscal 2027. 2Thanksgiving and Black Friday shifted from November Fiscal 2024 into December Fiscal 2025. 2 2 2 2 18.3% 5.1% Apr May FY27 (Black Friday in Fiscal December) 1 1 Two Weeks E-commerce SSS% by Month |

| 14 2 Stagecoach Sponsorship & On-Site Events |

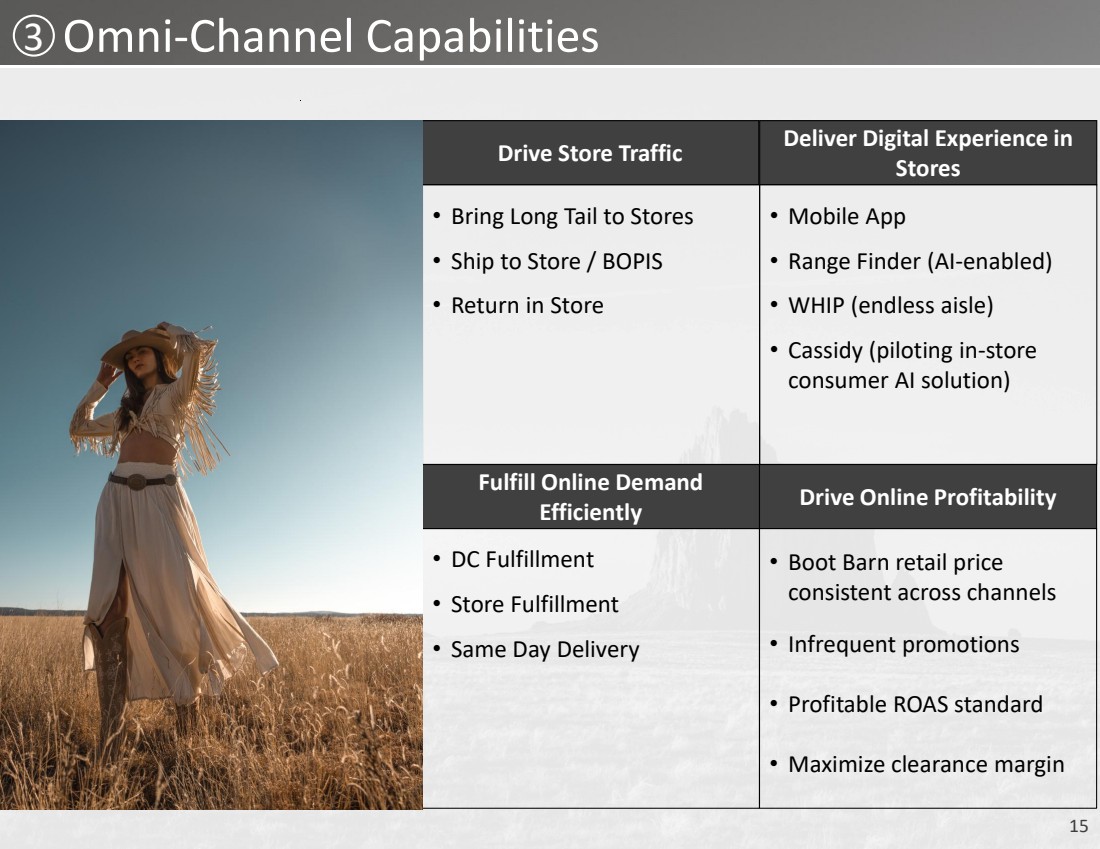

| 15 3 Drive Store Traffic • Bring Long Tail to Stores • Ship to Store / BOPIS • Return in Store Deliver Digital Experience in Stores • Mobile App • Range Finder (AI-enabled) • WHIP (endless aisle) • Cassidy (piloting in-store consumer AI solution) Fulfill Online Demand Efficiently • DC Fulfillment • Store Fulfillment • Same Day Delivery Drive Online Profitability • Boot Barn retail price consistent across channels • Infrequent promotions • Profitable ROAS standard • Maximize clearance margin Omni-Channel Capabilities |

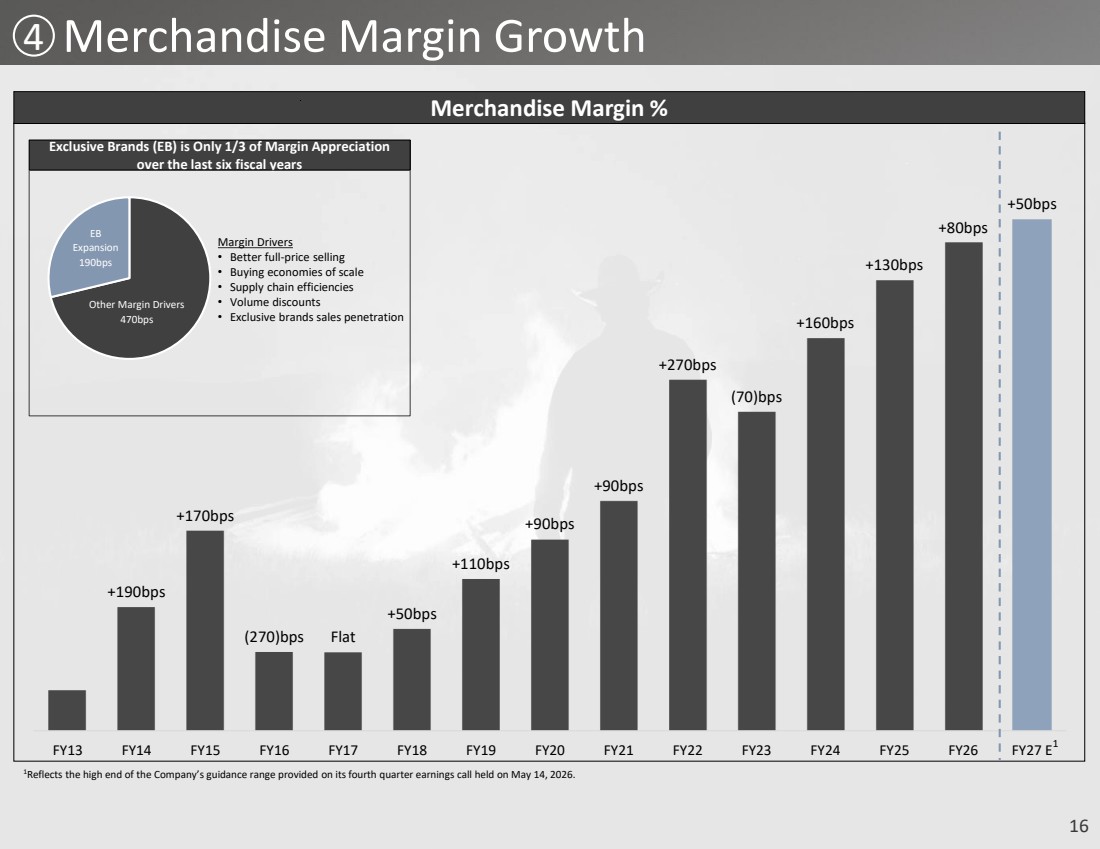

| 16 4 1Reflects the high end of the Company’s guidance range provided on its fourth quarter earnings call held on May 14, 2026. +190bps +170bps (270)bps Flat +50bps +110bps +90bps +90bps +270bps (70)bps +160bps +130bps +80bps +50bps FY13 FY14 FY15 FY16 FY17 FY18 FY19 FY20 FY21 FY22 FY23 FY24 FY25 FY26 FY27 E Merchandise Margin % 1 Merchandise Margin Growth Exclusive Brands (EB) is Only 1/3 of Margin Appreciation over the last six fiscal years Margin Drivers • Better full-price selling • Buying economies of scale • Supply chain efficiencies • Volume discounts • Exclusive brands sales penetration EB Expansion 190bps Other Margin Drivers 470bps |

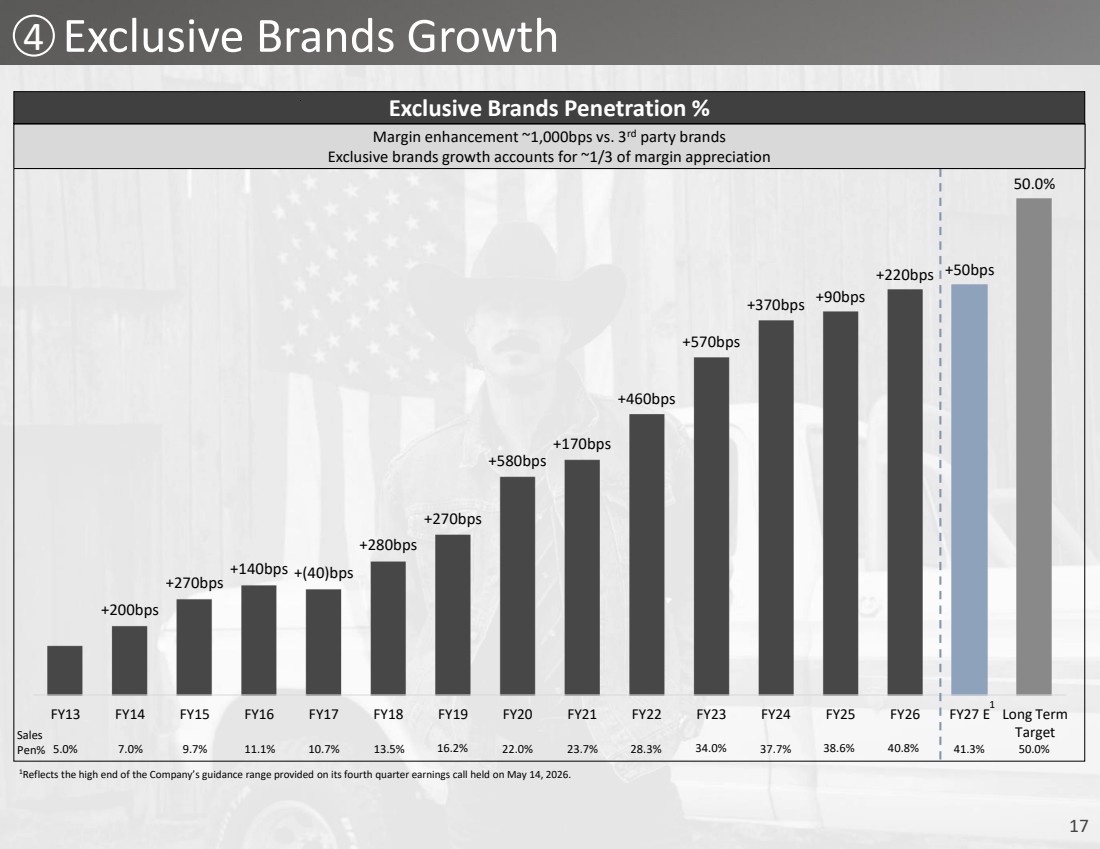

| 17 4 1Reflects the high end of the Company’s guidance range provided on its fourth quarter earnings call held on May 14, 2026. +200bps +270bps +140bps +(40)bps +280bps +270bps +580bps +170bps +460bps +570bps +370bps +90bps +220bps +50bps FY13 FY14 FY15 FY16 FY17 FY18 FY19 FY20 FY21 FY22 FY23 FY24 FY25 FY26 FY27 E Exclusive Brands Penetration % Sales Pen% 5.0% 7.0% 9.7% 11.1% 10.7% 13.5% 16.2% 22.0% 23.7% 28.3% 34.0% 37.7% 38.6% 40.8% 41.3% Long Term Target Margin enhancement ~1,000bps vs. 3rd party brands Exclusive brands growth accounts for ~1/3 of margin appreciation 1 Exclusive Brands Growth 50.0% 50.0% |

| 18 4 Best in Class Exclusive Brands |

| 19 4 Exclusive Brands Marketing & Websites |

| 20 FY27 Guidance |

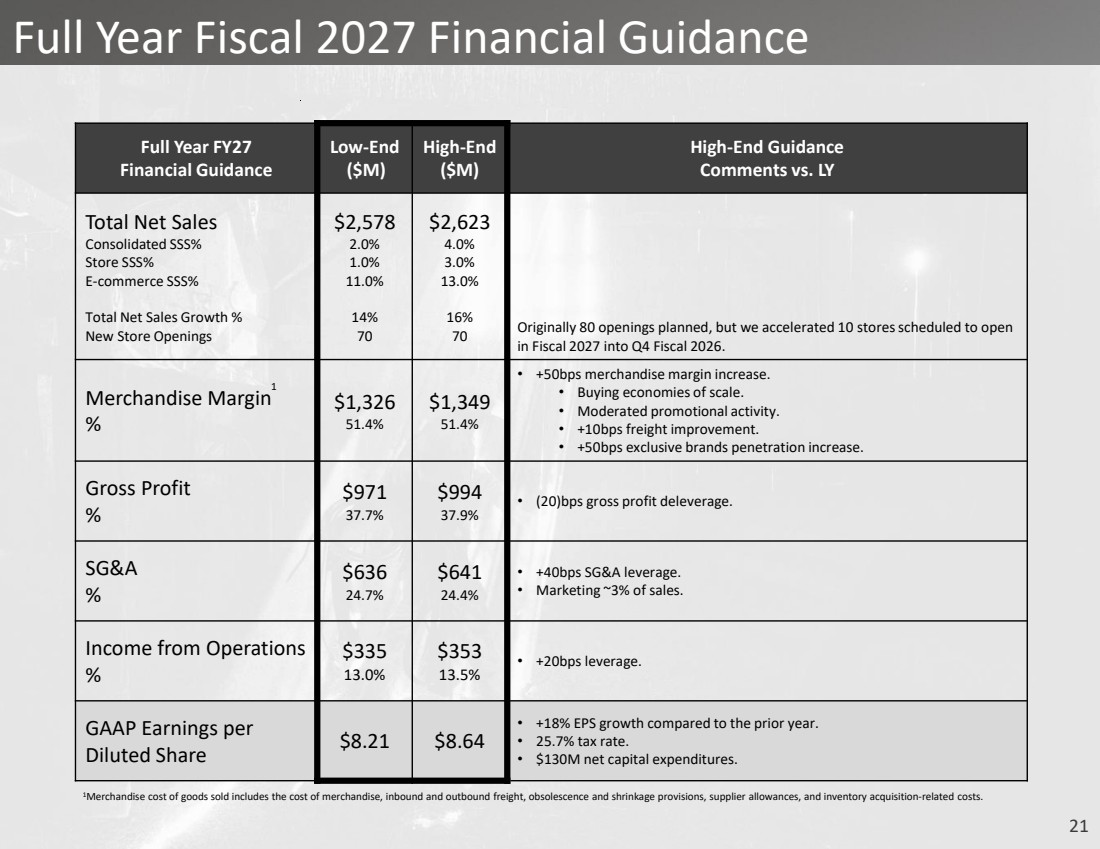

| 21 Full Year Fiscal 2027 Financial Guidance Full Year FY27 Financial Guidance Low-End ($M) High-End ($M) High-End Guidance Comments vs. LY Total Net Sales Consolidated SSS% Store SSS% E-commerce SSS% Total Net Sales Growth % New Store Openings $2,578 2.0% 1.0% 11.0% 14% 70 $2,623 4.0% 3.0% 13.0% 16% 70 Originally 80 openings planned, but we accelerated 10 stores scheduled to open in Fiscal 2027 into Q4 Fiscal 2026. Merchandise Margin % $1,326 51.4% $1,349 51.4% • +50bps merchandise margin increase. • Buying economies of scale. • Moderated promotional activity. • +10bps freight improvement. • +50bps exclusive brands penetration increase. Gross Profit % $971 37.7% $994 37.9% • (20)bps gross profit deleverage. SG&A % $636 24.7% $641 24.4% • +40bps SG&A leverage. • Marketing ~3% of sales. Income from Operations % $335 13.0% $353 13.5% • +20bps leverage. GAAP Earnings per Diluted Share $8.21 $8.64 • +18% EPS growth compared to the prior year. • 25.7% tax rate. • $130M net capital expenditures. 1 1Merchandise cost of goods sold includes the cost of merchandise, inbound and outbound freight, obsolescence and shrinkage provisions, supplier allowances, and inventory acquisition-related costs. |

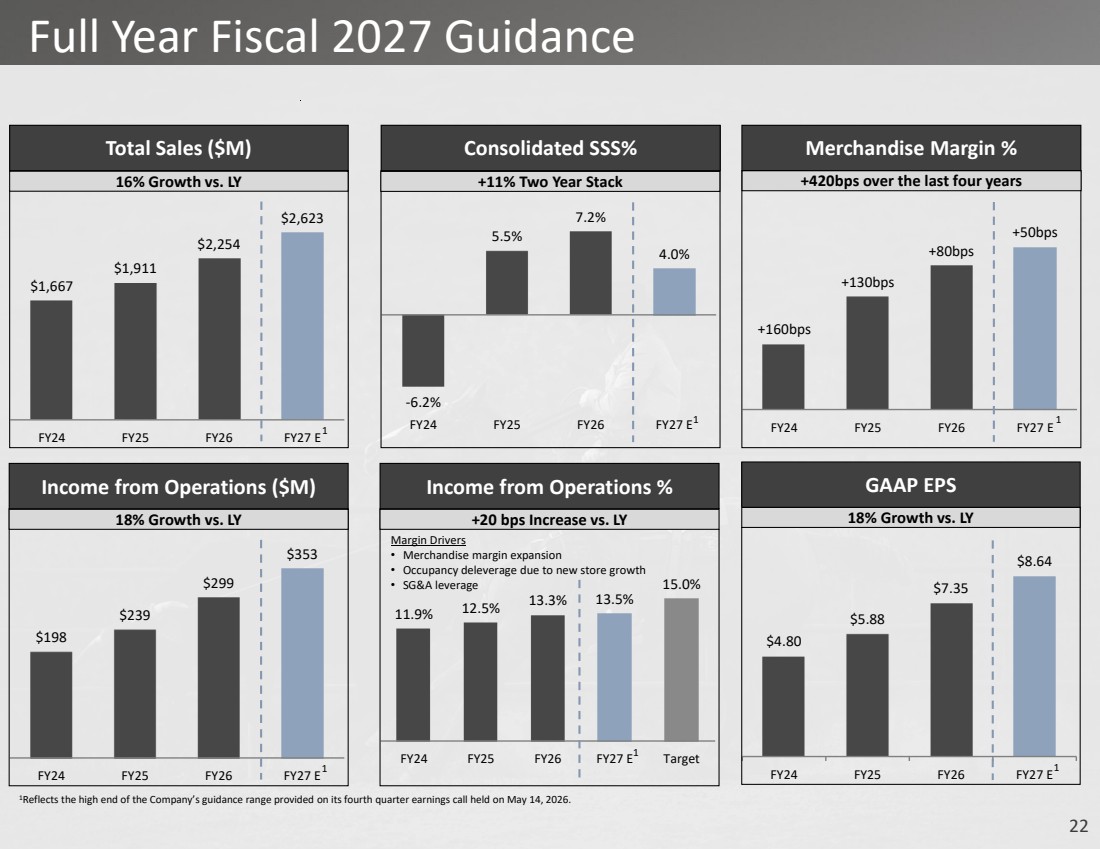

| 22 $4.80 $5.88 $7.35 $8.64 FY24 FY25 FY26 FY27 E $1,667 $1,911 $2,254 $2,623 FY24 FY25 FY26 FY27 E Full Year Fiscal 2027 Guidance Total Sales ($M) -6.2% 5.5% 7.2% 4.0% FY24 FY25 FY26 FY27 E Consolidated SSS% +160bps +130bps +80bps +50bps FY24 FY25 FY26 FY27 E Merchandise Margin % GAAP EPS 16% Growth vs. LY +420bps over the last four years 18% Growth vs. LY +11% Two Year Stack $198 $239 $299 $353 FY24 FY25 FY26 FY27 E Income from Operations ($M) 18% Growth vs. LY 11.9% 12.5% 13.3% 13.5% 15.0% FY24 FY25 FY26 FY27 E Target Income from Operations % +20 bps Increase vs. LY Margin Drivers • Merchandise margin expansion • Occupancy deleverage due to new store growth • SG&A leverage 1Reflects the high end of the Company’s guidance range provided on its fourth quarter earnings call held on May 14, 2026. 1 1 1 1 1 1 |

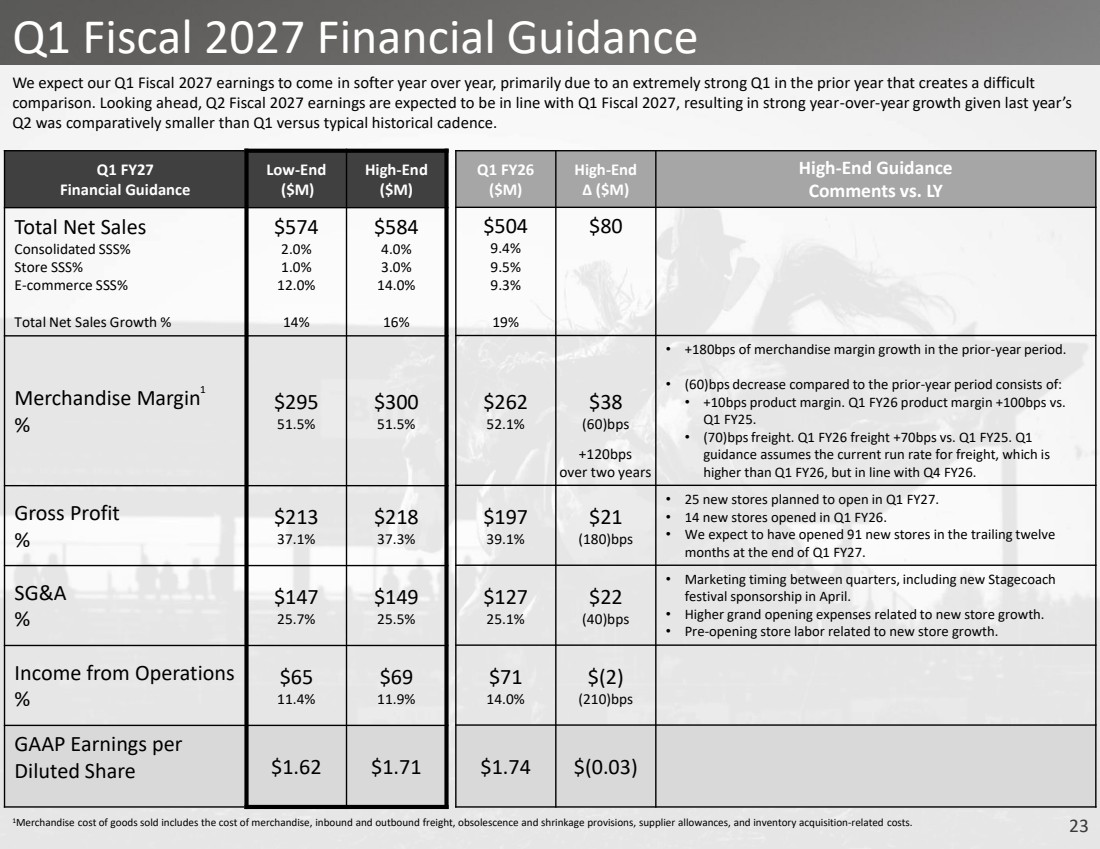

| 23 Q1 Fiscal 2027 Financial Guidance Q1 FY27 Financial Guidance Low-End ($M) High-End ($M) Total Net Sales Consolidated SSS% Store SSS% E-commerce SSS% Total Net Sales Growth % $574 2.0% 1.0% 12.0% 14% $584 4.0% 3.0% 14.0% 16% Merchandise Margin % $295 51.5% $300 51.5% Gross Profit % $213 37.1% $218 37.3% SG&A % $147 25.7% $149 25.5% Income from Operations % $65 11.4% $69 11.9% GAAP Earnings per Diluted Share $1.62 $1.71 1 1Merchandise cost of goods sold includes the cost of merchandise, inbound and outbound freight, obsolescence and shrinkage provisions, supplier allowances, and inventory acquisition-related costs. Q1 FY26 ($M) High-End Δ ($M) High-End Guidance Comments vs. LY $504 9.4% 9.5% 9.3% 19% $80 $262 52.1% $38 (60)bps • +180bps of merchandise margin growth in the prior-year period. • (60)bps decrease compared to the prior-year period consists of: • +10bps product margin. Q1 FY26 product margin +100bps vs. Q1 FY25. • (70)bps freight. Q1 FY26 freight +70bps vs. Q1 FY25. Q1 guidance assumes the current run rate for freight, which is higher than Q1 FY26, but in line with Q4 FY26. $197 39.1% $21 (180)bps • 25 new stores planned to open in Q1 FY27. • 14 new stores opened in Q1 FY26. • We expect to have opened 91 new stores in the trailing twelve months at the end of Q1 FY27. $127 25.1% $22 (40)bps • Marketing timing between quarters, including new Stagecoach festival sponsorship in April. • Higher grand opening expenses related to new store growth. • Pre-opening store labor related to new store growth. $71 14.0% $(2) (210)bps $1.74 $(0.03) +120bps over two years We expect our Q1 Fiscal 2027 earnings to come in softer year over year, primarily due to an extremely strong Q1 in the prior year that creates a difficult comparison. Looking ahead, Q2 Fiscal 2027 earnings are expected to be in line with Q1 Fiscal 2027, resulting in strong year-over-year growth given last year’s Q2 was comparatively smaller than Q1 versus typical historical cadence. |

| 24 investor.bootbarn.com |