---Unofficial translation for convenience purposes---

OPC ENERGY LTD.

Report of the Board of Directors regarding the Company’s Matters

for the three months ended March 31, 2026

The Board of Directors of OPC Energy Ltd. (hereinafter – “the Company”) is pleased to present herein the Report of the Board of

Directors regarding the activities of the Company and its investee companies (hereinafter together – “the Group”), as at March 31, 2026 and for the three months then ended (“the Period of the Report”).

Except for the data reviewed in the Company’s consolidated financial statements as at March 31, 2026 (hereinafter – “the Interim

Statements”) that is included in this report below, the data appearing in the Report of the Board of Directors has not been audited or reviewed by the Company’s auditing CPAs.

This Report of the Board of Directors is submitted on the assumption that the interim reports and all parts of

the Company’s Periodic Report for 2025, which was published on March 12, 2026 (Reference No.: (2026‑01‑021904) (“the Periodic Report for 2025”), are before the reader and references to the Company’s reports include the information presented therein

by means of reference.

1

---Unofficial translation for convenience purposes---

OPC Energy Ltd.

Report of the Board of Directors

| 1. |

Executive Summary1

|

| A. |

Brief description of the areas of activity

|

The Company is a public company the securities of which are listed for trading on the Tel‑Aviv Stock Exchange

Ltd.

For details regarding the Group’s activity segments in the Period of the Report – see Section 1A of the Report

of the Board of Directors that is included in the Periodic Report for 2025 (“the Report of the Board of Directors for 2025”) and Note 25 to the financial statements as at December 31, 2025 that are included in the Periodic Report for 2025 (“the

Annual Financial Statements”).

| B. |

Change in the Company’s presentation currency from the shekel to the U.S. dollar

|

Starting from January 1, 2026, the Company presents all its financial results, including its financial

statements, in U.S. dollars (“the Dollar”)2. The comparative data was translated for comparison purposes while using the same translation rules (translation into the presentation currency pursuant to the provisions of IAS 21). For

additional details – see Note 2B to the Interim Statements.

| 1 |

The executive summary below is presented solely for convenience and it is not a substitute for reading the full detail (including with reference to the matters referred to in the summary) as stated in this

report with all its parts (including warnings relating to “forward‑looking” information as it is defined in the Securities Law, 1968 (“the Securities Law”), definitions or explanations with respect to the indices for measurement of the

results and including the information included by means of reference, as applicable). This summary includes estimates, plans and assessment of the Company, which constitute “forward‑looking” information regarding which there is no certainty

they will materialize and the readers are directed to the detail presented in the relevant sections.

|

| 2 |

It is noted that the Company’s presentation currency does not impact its functional currency and the functional currency of its significant subsidiaries. Accordingly, as at the date of the report, the functional currency of the Company

and the companies operating in Israel (OPC Power and its subsidiaries) continues to be the shekel whereas the functional currency of the companies operating in the United States (ICG and its subsidiaries and the CPV Group) continues to be

the Dollar.

|

2

---Unofficial translation for convenience purposes---

OPC Energy Ltd.

Report of the Board of Directors

| 1. |

Executive Summary1 (Cont.)

|

| C. |

Main financial parameters (in millions of dollars)

|

|

For the

|

||||

|

Three Months Ended

|

||||

|

March 31

|

||||

|

2026

|

2025

|

%

|

||

|

Consolidated

|

EBITDA after proportionate consolidation

|

124

|

113

|

10%

|

|

Net income

|

14

|

25

|

(44%)

|

|

|

Adjusted net income

|

33

|

28

|

18%

|

|

|

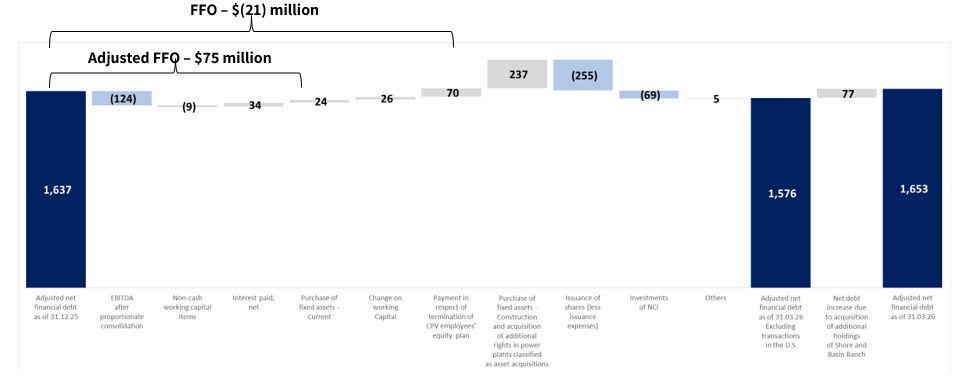

FFO

|

(21)

|

89

|

(124%)

|

|

|

Adjusted FFO

|

75

|

69

|

9%

|

|

|

Israel

|

EBITDA

|

44

|

38

|

16%

|

|

FFO

|

24

|

53

|

(55%)

|

|

|

Adjusted FFO

|

27

|

29

|

(7%)

|

|

|

U.S.

|

EBITDA after proportionate consolidation

|

83

|

77

|

8%

|

|

FFO

|

(34)

|

41

|

(183%)

|

|

|

Adjusted FFO

|

53

|

48

|

10%

|

|

|

EBITDA after proportionate consolidation –

Energy Transition

|

88

|

77

|

14%

|

|

|

EBITDA after proportionate consolidation –

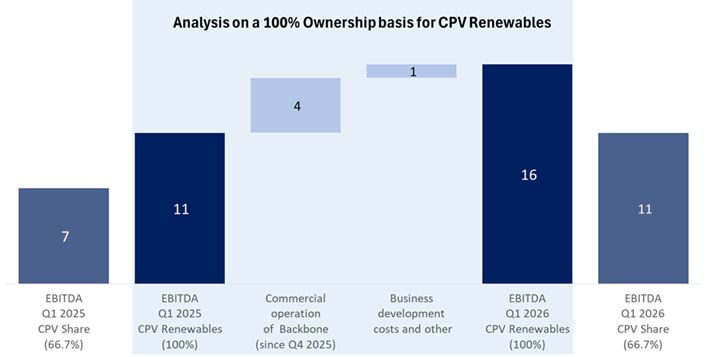

Renewable Energies

|

11

|

7

|

57%

|

|

| * |

EBITDA, EBITDA after proportionate consolidation, adjusted net income, FFO and adjusted FFO (Funds From Operations) are non‑IFRS financial measures – for definitions and the manner of their calculation – see Sections 4B and 4A(3) below.

|

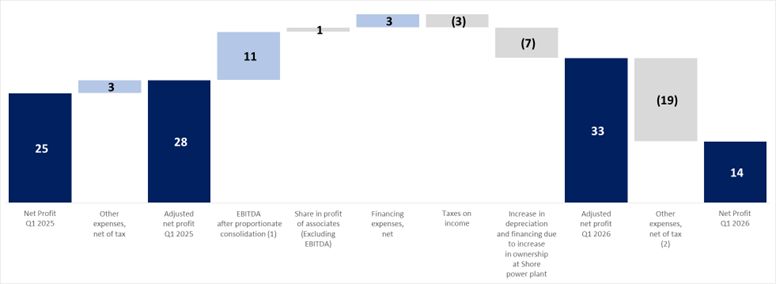

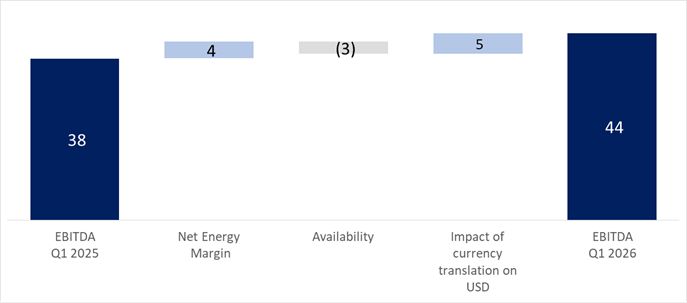

As detailed in the above table, in the first quarter of 2026, the EBITDA after

proportionate consolidation increased by about 10% over the corresponding quarter last year, as a result of an increase of 8% in the EBITDA after proportionate consolidation in the United States, primarily due to an increase in the energy margins

and the capacity prices in the PJM market and an increase in the holding rates in the Shore power plant, as well as due to an increase of about 16% in the EBITDA in Israel mainly against the background of the increase in the energy margins and due

to the impacts of the translation on the results of the activities in Israel to the presentation currency (the dollar), which weakened significantly against the shekel (which is the functional currency in Israel).

In the first quarter of 2026, the consolidated Adjusted Net Income rose by about 18%

compared with the corresponding quarter last year, against the background of the increase in the adjusted EBITDA.

In the first quarter of 2026, the consolidated adjusted FFO rose by about 9% compared with

the corresponding quarter last year, primarily due to the increase in the adjusted EBITDA.

3

---Unofficial translation for convenience purposes---

OPC Energy Ltd.

Report of the Board of Directors

| 1. |

Executive Summary1 (Cont.)

|

| D. |

Main developments in the first quarter of 2026 and thereafter

|

|

Israel

|

Hadera expansion project in advanced development (combined cycle) with a capacity of 850 megawatts – in February 2026, the

Company signed a binding agreement for acquisition of the main equipment and a maintenance agreement with GE and is taking action to complete the undertaking in the other project agreements (equipment, construction, and financing) and to

complete receipt of all the required approvals and permits and to reach the financial closing (some of which had received as at the approval date of the report) by the end of the second quarter of 2026. For details – see Section 5A(2)

below.

|

|

Ramat Beka project in advanced development (solar with a capacity of about 550 megawatts with integrated storage of about 3,850

megawatt-hours) – in March 2026, the approved plan was published by the government in the Official Records. The Company is taking action to complete the undertaking in the project agreements (construction, equipment and financing)

and to obtain all the required approvals and permits, and it expects to make the payment to Israel Lands Authority for the project’s areas by the end of the second quarter of 2026. For details – see Section 5A(2) below.

|

|

|

Expansion of activities in the area of supply of electricity to Data Centers – undertaking in a long‑term PPA agreement with a

leading consumer in the area with a capacity that could gradually reach about 460 megawatts in the upcoming years.

|

|

|

Natural gas activities with carbon capture potential in the U.S.

|

Acquisition of the remaining rights (30%) in the Basin Ranch – in February 2026 the acquisition was completed and starting from

this date the project is consolidated in the CPV Group’s and the Company’s financial statements. In this regard, the corporate loan of the CPV Group from Bank Leumi was increased by about $300 million to about $430 million. For details –

see Section 5B(1) below.

|

|

Increase in the pipeline (backlog) of natural gas projects to about 8.7 gigawatts (the share of the CPV Group – about 7.4 gigawatts)

alongside the continued accelerated development of the Shay Project in the PJM market (combined cycle with a capacity of 2.1 gigawatts in West Virginia – the share of CPV is 70%), which is being advanced in licensing and

grid interconnection processes and is expected to enter into an interconnection agreement in early 2027. In addition, a slot reservation agreement for significant equipment has been signed and CPV Group is evaluating and taking actions to

position the project to meet the eligibility requirements for participation in the RBP mechanism. For further details, see Section 5B(2) below.

|

4

---Unofficial translation for convenience purposes---

OPC Energy Ltd.

Report of the Board of Directors

| 1. |

Executive Summary1 (Cont.)

|

| D. |

Main developments in the first quarter of 2026 and thereafter (Cont.)

|

|

Energy Transition in the U.S.

|

Execution of the strategy to increase the holdings and obtain control over natural gas‑fired power plants: (1) in January

2026, acquisition of the remaining rights (11%) in the Shore power plant (a combined cycle power plant with a capacity of 725 megawatts in PJM); and (2) in May 2026, acquisition of the remaining interest (25%) in the Maryland power plant

(combined cycle with a capacity of 745 megawatts in PJM) in exchange for sale of the rights (10%) in the Three Rivers power plant (combined cycle with a capacity of 1,258 megawatts in PJM) with payment of an immaterial amount.

|

|

Refinancing of the Valley power plant (combined cycle with a capacity of 720 megawatts in New York) – in February 2026, a

refinancing transaction was completed whereby the margin was reduced to 2.75%, the cash sweep rate was reduced from 100% to a leverage‑based mechanism as is customary in the TLB market, and a dividend was distributed to the partners /

shareholders’ loans were repaid, in the amount of about $100 million (the CPV Group’s share – about $50 million). For additional details – see Section 6A(3) below.

|

|

|

Capacity auctions and regulatory processes in PJM – in April 2026, FERC approved the extension of the maximum and minimum limits

(collar) for two additional capacity auctions in the period from June 1, 2028 through May 31, 2030. In addition, in April 2026 PJM published an initial proposal for an emergency procurement for acquisition of additional available capacity

through a Reliability Backstop Procurement (“RBP”), in order to provide a response to the expected shortage of capacity deriving from an increase in the demand for electricity. The proposal includes procurement processes of about

15 gigawatts for capacity contracts for periods of up to 15 years. The RBP design has not yet been formulated and is subject to, among other things, regulatory approvals. For details – see Section 3C below.

|

|

|

Renewable Energies in the U.S.

|

As at the approval date of the report, the CPV Group took action in an attempt to assure compliance with Safe Harbor conditions for projects in the scope of

1.9 gigawatts (share of the CPV Group – about 1.3 gigawatts). For details – see Section 5C(2) below.

|

|

U.S.

headquarters

|

Long‑term incentive plan for employees of the CPV Group – as part of the plan, which was granted in 2021 and vested over a

period of five years, in March 2026 profit participation units were exercised that were granted to employees of the CPV Group, in the amount of about $70 million. In addition, a new long‑term incentive plan was approved for employees of the

CPV Group with vesting periods up to the beginning of 2031. For details – see Note 7F to the Interim Statements.

|

5

---Unofficial translation for convenience purposes---

OPC Energy Ltd.

Report of the Board of Directors

| 1. |

Executive Summary1 (Cont.)

|

| D. |

Main developments in the first quarter of 2026 and thereafter (Cont.)

|

|

Group

headquarters

|

Raising of capital – in March 2026, the Company completed a capital raise with gross proceeds of about $257 million (about

NIS 800 million). The proceeds of the issuances were designated for the continued growth and development of the Company’s business.

|

|

Increase of the investment commitment in the CPV Group – in March 2026, a process was completed of increase of the investment

commitment of the Company and the other partners in the CPV Group in connection with the financial close of the Basin Ranch power plant and transactions for increasing the holdings in the natural gas‑fired power plants, in the aggregate

amount of about $502 million. For details – see Note 23A(3) to the Annual Financial Statements.

|

|

|

Improvement of the credit rating – in May 2026, Midroog affirmed the credit rating of the Company and of its debentures at the

level of A1.il and updated the rating outlook from stable to positive in light of the strengthening of the Company’s financial profile. For details – see Section 6C below.

|

|

|

Early partial redemption (prepayment) of the debentures (Series B) – in May 2026, the Company’s Board of Directors decided to make a partial early prepayment of

the debentures (Series B), in the total amount of about $70 million (about NIS 200 million), to be executed in the beginning of June 2026.

|

6

---Unofficial translation for convenience purposes---

OPC Energy Ltd.

Report of the Board of Directors

| 1. |

Executive Summary1 (Cont.)

|

| E. |

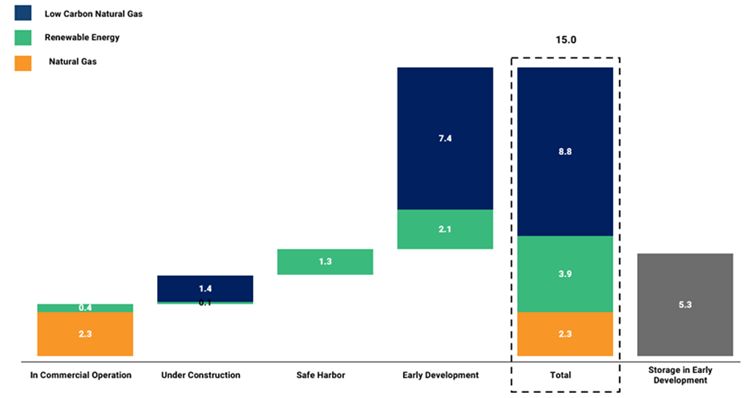

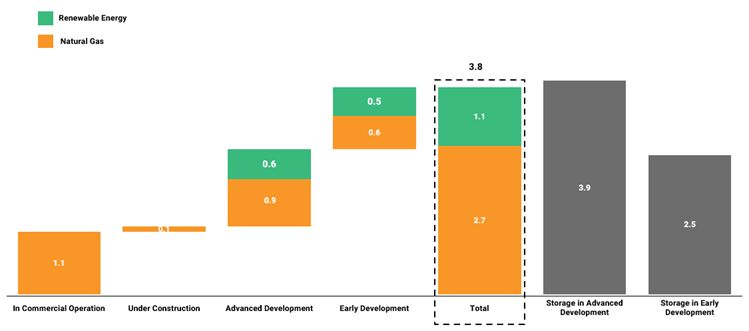

Portfolio of about 18.83 GW and about 11.7 GWh of storage (for details – see Section 5 below)

|

United States (1)(2)

| (1) |

The projects in the United States that are held by associated companies are presented according to the CPV’s Group relative ownership interest in each project.

|

| (2) |

The Maryland and Three Rivers power plants are presented based on the share of the CPV Group as at the approval date of the report (which is 100% and 0%, respectively).

|

| 3 |

The data included in this report relating to the capacity of the renewable‑energy projects using solar technology is in MWdc.

|

7

---Unofficial translation for convenience purposes---

OPC Energy Ltd.

Report of the Board of Directors

| 1. |

Executive Summary1 (Cont.)

|

| E. |

Portfolio of about 18.83 GW and about 11.7 GWh of storage (for details – see Section 5 below) (Cont.)

|

Israel

That stated with respect to the development stages, capacities and/or expectations regarding

construction of the development (pipeline) projects in Israel and in the U.S. constitutes “forward‑looking” information as it is defined in the Securities Law, 1968 (“the Securities Law”), which is based on the Company’s estimates at the approval

date of the report and regarding which there is no certainty they will be realized. Ultimately, there could be changes in the characteristics of the projects and/or delays or changes due to regulatory, operating, commercial factors and/or

realization of one or more of the risk factors to which the Company is exposed, as stated in Part A of the Periodic Report for 2025. Advancement of the pipeline projects (or any one of them) is subject to the discretion of the Company’s competent

organs and existence (fulfillment) of additional conditions, as stated in Part A of the Periodic Report for 2025.

For definitions of the development stages – see Section 5 below.

8

---Unofficial translation for convenience purposes---

OPC Energy Ltd.

Report of the Board of Directors

| 2. |

Main Developments in the Business and Regulatory Environment in Israel

|

| A. |

Update of electricity tariffs

|

In December 2025, the generation component for 2026 was set (subject to a periodic update, as detailed in

Section 2A(1) of the Report of the Board of Directors for 2025) at 28.90 agurot per kilowatt hour (assuming a shekel/dollar exchange rate of U.S.$1 = NIS 3.3), a decline of 1.66% compared with the average generation component for 2025.

Set forth below is data regarding the weighted‑average annual generation component (the prices are

denominated in agurot per kilowatt hour):

|

Period

|

2026

|

2025

|

Change

|

|

January–March average

|

28.90

|

29.39

|

(2.4%)

|

In the Company’s estimation, update of the tariff for 2026 is not expected to have a significant impact on its

results4.

| B. |

Security, Political and Geopolitical Instability in Israel

|

Further to that stated in Section 2B of the Report of the Board of Directors for 2025 and

Section 6.1.1 of Part A of the Periodic Report for 2025, on February 28, 2026, there was a significant escalation in the regional geopolitical situation upon the outbreak of an additional serious military confrontation between Israel and the United

States versus Iran, which also included attacks by Iran on additional Middle‑Eastern countries (the “Roaring Lion” Operation). As a consequence of the “Roaring Lion” military operation, among other things, Israeli airspace was closed and a general

emergency situation was announced for the Israeli home front in such a manner that significantly limits the activities (traffic/movement) in public areas – this being together with a large mobilization of military reserves.

During the “Roaring Lion” Operation, all the gas rigs were shut down (including the Karish

reserve) for varying time periods and temporary use of diesel oil was made in the Company’s power plants, where as at the approval date of the report the three gas reservoirs had returned to full activities. The shutdown of the Tamar gas reserve

lasted only several days at the beginning of the “Roaring Lion” Operation such that upon its operation, all of the Company’s gas needs were supplied, while some of the gas was purchased at a price higher than the alternative price from the Karish

reserve with only an insignificant impact as at the approval date of the report.

Furthermore, due to the emergency situation declared in the Israeli economy, there was a

certain decline in demand for a short period of time, the impact of which was not significant. Also, force majeure notifications were received from suppliers and contractors along with limited availability

of foreign work teams and experts on the Company’s activity sites in Israel, including on the Sorek 2 site (which is undergoing acceptance tests).

| 4 |

The Company’s estimates with respect to the impact of the Decision is “forward‑looking” information as it is defined in the Securities Law, for which there is no certainty of their realization.

Ultimately, the impacts could be different due to, among other things, the market conditions, changes impacting the components of the tariffs, regulator changes/factors that impact the electricity market.

|

9

---Unofficial translation for convenience purposes---

OPC Energy Ltd.

Report of the Board of Directors

| 2. |

Main Developments in the Business and Regulatory Environment in Israel (Cont.)

|

| B. |

Security, Political and Geopolitical Instability in Israel (Cont.)

|

On April 8, 2026, a temporary ceasefire was announced with Iran, while the marine blockade

continued in the Strait of Hormuz with respect to movement of oil and natural gas tankers (containers). On April 17, 2026, a temporary ceasefire was announced with Lebanon, where as at the approval date of the report the attacks of the Hezbollah

organization from Lebanon are continuing and, accordingly, the restrictions relating to the emergency situation in the northern part of Israel were reinstated to a certain extent.

As at the approval date of the report the “Lion’s Roar” Operation did not

have a significant impact on the business activities and/or the financial results. Nonetheless, as at the approval date of the report there is a significant concern that the combat with Iran will be rekindled and the fighting in Lebanon will

continue.

It is noted that the above‑mentioned events involve significant uncertainty and could

impact the macro‑economic and geopolitical environment in both Israel and the U.S., including an adverse impact on the strength of the Israeli economy, as well as on the global economic activities (for a short or even possibility a long period of

time). A rekindling of the fighting and/or a worsening of the security/defense situation could negatively affect the Company’s activities, mainly in Israel, including the activities of its customers and suppliers in Israel, and could also have an

unfavorable effect on the results of the Company’s operations, the availability and cost of capital and financing sources required for the Group’s activities. For additional details regarding the possible impacts of the security/defense and

geopolitical situations and the related risk factors – see Sections 6.1 and 19.1 of the Part A of the Periodic Report for 2025.

For additional details regarding the structure and manner of determination of the

electricity tariff for customers of Israel Electric Company, the price of natural gas and the carbon tax, availability/capacity revenues and supply to customers, as well as with respect to the Government’s decision concerning advancement of the

construction of Data Centers – see Section 2A of the Report of the Board of Directors for 2025 and Section 7.3 of Part A of the Periodic Report for 2025.

| 3. |

Main Developments in the Business and Regulatory Environment in the U.S.

|

| A. |

Electricity and natural gas prices

|

The results of the activities of the CPV Group are impacted to a significant extent by the

electricity prices in effect in the areas in which the Group’s power plants operate. The main factors impacting the electricity prices are demand for electricity, available generation (supply) and the natural gas price in the area in which the

power plant operates.

For more information regarding the trend of the supply and demand of electricity in the

U.S, including in the PJM and ERCOT markets and with respect to fluctuations of the gas and electricity prices, along with the factors affecting it – see Section 3A of the Report of the Board of Directors for 2025.

10

---Unofficial translation for convenience purposes---

OPC Energy Ltd.

Report of the Board of Directors

| 3. |

Main Developments in the Business and Regulatory Environment in the U.S. (Cont.)

|

| A. |

Electricity and natural gas prices (Cont.)

|

Natural gas prices

|

Set forth below are the average natural gas prices in each of the main markets in which the power plants of the CPV Group operate (the prices are denominated in dollars per MMBtu)*:

|

|

For the three months ended

|

|||||

|

Region

|

March 31

|

||||

|

(Power Plant)

|

2026

|

2025

|

Change

|

||

|

Texas Eastern M‑3 (Shore, Valley – 70%)

|

9.61

|

6.42

|

50%

|

||

|

Transco Zone 5 North (Maryland)

|

8.36

|

6.06

|

38%

|

||

|

Dominion South Pt (Valley – 30%)

|

4.73

|

3.74

|

26%

|

||

|

Algonquin City Gate (Towantic)

|

14.08

|

11.83

|

19%

|

||

|

Texas Eastern M‑3 and Texas Eastern M‑2 (Fairview)**

|

9.61

|

3.83

|

151%

|

||

|

Chicago City Gate (Three Rivers)

|

5.34

|

4.00

|

34%

|

||

|

Waha (Basin Ranch)***

|

(1.09)

|

1.81

|

(160%)

|

||

| * |

Source: The Day‑Ahead prices at gas Midpoints as reported in Platt’s Gas Daily. It is clarified that the actual gas prices of the power plants of the CPV Group could be significantly different.

|

| ** |

Commencing from the third quarter of 2025, Fairview has started acquiring natural gas that is priced based on the Texas Eastern M‑3 transmission region. Accordingly, the comparison between the gas prices in the first quarter of 2026 and

the corresponding quarter last year reflects prices from two different transmission regions – Texas Eastern M-‑3 compared with Texas Eastern M-‑2, respectively. For additional details – see Appendix A below.

|

| *** |

The Basin Ranch project is under construction. For details – see Section 5B(1) below.

|

In the estimation of the CPV Group, the significant increase in the natural gas prices in

the Period of the Report is mainly due to the continuing cold weather conditions in the United States, including with respect to the corresponding period last year, which led to a significant rise in demand for natural gas and an increase in the

prices in the regions in which the CPV Group’s power plants operate. Nonetheless, the inventory levels of the natural gas in the U.S. have remained historically high, which moderated the impact of the winter weather conditions on future gas prices.

Regarding the Fairview power plant, the unusual increase in the natural gas prices also stems from transition to the Texas Eastern M‑3 transmission region, which is more significantly impacted by high demand for natural gas under cold weather

conditions than the Texas Eastern M‑2 transmission region.

Regarding the natural gas distribution region in Waha Texas, which is expected to serve as

a source for supply to the Basin Ranch power plant, which is presently under construction, the region is affected by different market dynamics and different weather conditions, and similar price increases have not been recorded therein. Production

of natural gas in this region constitutes a by‑product of oil production, and the high demand for oil led to high levels of gas production, along with limitations on the transmission capacity outside of the Waha basin which, in turn, caused a

surplus local supply of gas and downward pressure on prices.

11

---Unofficial translation for convenience purposes---

OPC Energy Ltd.

Report of the Board of Directors

| 3. |

Main Developments in the Business and Regulatory Environment in the U.S. (Cont.)

|

| A. |

Electricity and natural gas prices (Cont.)

|

Electricity prices

The following table summarizes the average electricity prices in each of the regions in

which the power plants in the area of energy transition activities of the CPV Group are active (the prices are denominated in dollars per megawatt hour)*:

|

For the Three Months Ended

|

|||||

|

Region

|

March 31

|

||||

|

(Power Plant)

|

2026

|

2025

|

Change

|

||

|

PJM West (Shore, Maryland)

|

97.42

|

53.90

|

81%

|

||

|

New York Zone G (Valley)

|

119.58

|

88.85

|

35%

|

||

|

Mass Hub (Towantic)

|

117.36

|

102.78

|

14%

|

||

|

PJM AEP Dayton (Fairview)

|

70.66

|

47.91

|

47%

|

||

|

PJM ComEd (Three Rivers)

|

51.13

|

35.24

|

45%

|

||

|

ERCOT West Hub (Basin Ranch)**

|

39.42

|

35.24

|

12%

|

||

| * |

Based on Day‑Ahead prices as published by the relevant ISO.

|

| ** |

The Basin Ranch power plant, the construction of which commenced in October 2025. For details – see Section 5B(1) below.

|

It is noted that the actual electricity prices of the power plants of the CPV Group could

be higher or lower than the regional price shown in the above table due to the existence of a Power Basis (the difference between the power plant’s specific electricity price and the regional price). The Power Basis is a function of transmission

constraints, local cost of electricity generation, local demand for electricity, loss of electricity in the transmission lines and additional factors. For details regarding the Power Basis data – see Section 3A to the Report of the Board of

Directors for 2025.

In the Period of the Report, there was a significant increase in the electricity prices

compared with the corresponding period last year, which in the estimation of the CPV Group derives mainly from an increase in the natural‑gas prices in the areas in which the power plants of the CPV Group are located, as detailed above.

12

---Unofficial translation for convenience purposes---

OPC Energy Ltd.

Report of the Board of Directors

| 3. |

Main Developments in the Business and Regulatory Environment in the U.S. (Cont.)

|

| A. |

Electricity and natural gas prices (Cont.)

|

Spark Spreads in the operating markets of the CPV Group

Spark Spread represents the difference between the price of the electricity in the relevant

area (zone) and the price of the natural gas used for generation of the electricity in the relevant area (zone) (it is clarified that RGGI is not included in calculation of the Spark Spread but rather in the Energy Margin as detailed in

Section 4D(3) below).

The Spark Spread is calculated based on the following formula:

Spark Spread ($/MWh) = price of the electricity ($/MWh) – [the gas price ($/MMBtu) x

thermal conversion ratio (heat rate) (MMBtu/MWh)]

Set forth below are the average Spark Spread margins for each of the main markets in which

the power plants of the CPV Group are operating (the prices are denominated in dollars per megawatt/hour)*:

|

For the Three Months Ended

|

|||

|

March 31

|

|||

|

Power Plant5

|

2026

|

2025

|

Change

|

|

Shore

|

31.11

|

9.60

|

224%

|

|

Maryland

|

39.74

|

12.09

|

229%

|

|

Valley

|

63.37

|

50.10

|

26%

|

|

Towantic

|

25.84

|

25.89

|

0%

|

|

Fairview**

|

8.20

|

23.02

|

(64%)

|

|

Three Rivers

|

16.42

|

9.24

|

78%

|

|

Basin Ranch***

|

46.51

|

19.47

|

139%

|

| * |

Based on electricity prices as shown in the above table, with assuming a thermal conversion ratio (heat rate) of 6.9 MMBtu/MWh for Maryland, Shore and Valley, and a thermal conversion ratio of 6.5 MMBtu/MWh for Three Rivers, Fairview,

Towantic and Basin Ranch. It is clarified that the actual energy margins of the power plants of the CPV Group could be significantly different due to, among other things, the existence of Power Basis and a different breakdown in the scope

of the electricity sold in the peak and off‑peak hours in CPV’s power plants and that shown above (which was calculated in the above table based on the assumption of generation in all the hours of the 24‑hour period).

|

| ** |

Commencing from the third quarter of 2025, Fairview has started acquiring natural gas that is priced based on the Texas Eastern M‑3 transmission region. Accordingly, the above table presents the electricity margin in the Period of the

Report, which is calculated on the basis of the gas price in the Texas Eastern M‑3 transmission region, compared with the electricity margin in the corresponding period last year, which is calculated on the basis of the gas price in the

Texas Eastern M‑2 transmission region.

|

| *** |

The Basin Ranch power plant is under construction. For details – see Section 5B(1) below.

|

In the Period of the Report, there was a significant increase in the Spark Spreads in most

of the active power plants of the CPV Group, compared with the corresponding period last year, stemming from a combination of unusual weather conditions – temperatures lower than the average, as stated above, plus a continuing increase in the

demand for electricity in the areas in which the power plants of the CPV Group are located.

5 For additional details regarding the energy margin of the CPV Group – see

Section 4D(3) below.

13

---Unofficial translation for convenience purposes---

OPC Energy Ltd.

Report of the Board of Directors

| 3. |

Main Developments in the Business and Regulatory Environment in the U.S. (Cont.)

|

| A. |

Electricity and natural gas prices (Cont.)

|

Spark Spreads in the operating markets of the CPV Group (Cont.)

Regarding the Towantic power plant, which operates in the ISO‑NE market, no increase was

recorded in the electricity margins compared with the corresponding period last year, this being mainly due a change in market rules in the ISO‑NE market, which shifts some of the fluctuations in the energy prices, which derive from unusual demand,

to the ancillary service market (that is, an increase in other income against the spark spread margin – for additional details, see the breakdown of the EBITDA data in Section 4D(2) below). Regarding the Fairview power plant, the decline derives

mainly from to the transition to the Texas Eastern M‑3 natural gas transmission region, as noted above.

It is noted that hedging programs in the CPV Group’s natural gas-fired power plants are

intended to reduce the fluctuations of the CPV Group’s electricity margin resulting from changes in the natural gas and electricity prices in the energy market. For details regarding hedging agreements related to the electricity margin at CPV

Group’s active power plants – see Section 4D(3) below. Regarding the Gas Netback agreements and fixed-price electricity sales, which hedge a significant portion of the Basin Ranch power plant’s net energy margin – see Section 5B(1), below).

For details regarding the Company’s forecasted electricity and natural gas forward market

prices (received from EOX) up to the end of 2026 and for 2027 and 2028 – see Appendix A below.

| B. |

Carbon Emissions Tax – Regional Greenhouse Gas Initiative (RGGI)

|

The RGGI regulation applies to the Maryland, Shore, Valley and Towantic power plants (which

belong to the Energy Transition segment of the CPV Group). For additional details regarding the RGGI regulation – see Section 8.1.4B of Part A of the Periodic Report for 2025.

Set forth below are details regarding the prices of the carbon‑emission allowances (carbon emission tax) from

the RGGI auctions. In general, the auctions take place four times a year, in March, June, September and December.

|

Average for the

|

|||

|

Three Months Ended

|

|||

|

March 31

|

|||

|

2026

|

2025

|

Change

|

|

|

Price of carbon emission tax in the RGGI auctions

($ per short ton / 2,000 pounds)*

|

26.73

|

20.05

|

33%

|

|

Cost of the carbon emission tax (in terms of gas cost)

($ per MMBtu)**

|

1.59

|

1.19

|

33%

|

| * |

The prices of the carbon emissions tax are presented under the assumption that the price of the auction that is held prior to a certain quarter represents the price of the carbon emissions tax for the subsequent quarter. For example, the

auction held in December 2025 represents the price for the first quarter of 2026. It is noted that the actual price of the carbon emissions tax could be different than the auction prices as a result of transactions made in the secondary

market.

|

| ** |

The cost of the carbon emissions tax (in terms of gas cost) is calculated under the assumption of emissions of carbon dioxide with a reference (ratio) of 119 MMBtu/lbs. It is noted that the actual carbon dioxide emissions ratio varies

between the different power plants, and in the estimation of the CPV Group a ratio of 119 MMBtu/lbs. is a representative ratio for natural gas-fired power plants.

|

14

---Unofficial translation for convenience purposes---

OPC Energy Ltd.

Report of the Board of Directors

| 3. |

Main Developments in the Business and Regulatory Environment in the U.S. (Cont.)

|

| B. |

Carbon Emissions Tax – Regional Greenhouse Gas Initiative (RGGI) (Cont.)

|

It is noted that from time to time, usually for short periods, the RGGI

market could experience price volatility stemming mainly from regulatory factors and supply and demand with respect to emissions’ permits.

| C. |

Capacity revenues

|

Capacity is an additional significant income component of the CPV Group’s active power

plants that operate in the PJM, NYISO and ISO‑NE markets, where normally an increase in the capacity prices has a favorable impact on CPV’s results, and vice‑versa. The extent of the impact on the overall results changes as a function of the energy

margins, which is the most significant component of the gross profit (margin for generation of the electricity and the sale thereof).

PJM market

In the PJM market, the capacity payments vary between the market’s sub‑regions, as a function of local supply

and demand and transmission capabilities. In general, the capacity auctions are made once a year for an annual supply period (June – May) in a format of three years in advance. Due to regulatory delays, the current schedule includes an auction once

every six months, with the goal of returning to annual auctions in 2027 – subject to regulatory changes. Set forth below are the capacity tariffs in the sub‑regions that are relevant to the CPV Group’s power plants and in the general market (the

prices are denominated in dollars per megawatt per day).

|

Sub-region

|

CPV Power Plants

|

(3)2027/2028

|

(2)2026/2027

|

(1)2025/2026

|

2024/2025

|

|

PJM RTO

|

Three Rivers, Backbone

|

333.44

|

329.17

|

269.92

|

28.92

|

|

PJM MAAC

|

Fairview, Maryland,

Maple Hill

|

333.44

|

329.17

|

269.92

|

49.49

|

|

PJM EMAAC

|

Shore

|

333.44

|

329.17

|

269.92

|

54.95

|

|

Source: PJM

|

| (1) |

Reflects estimated additional revenues for the CPV Group for the period of the auction compared with the corresponding period last year of about $98 million6.

|

| (2) |

Reflects estimated additional revenues for the CPV Group in the 2026/2027 auction compared with the 2025/2026 auction of about $18 million6.

|

| (3) |

Reflects estimated additional revenues for the CPV Group in the 2027/2028 auction compared with the 2026/2027 auction of about $2 million6.

|

| 6 |

That stated in this section with respect to the estimates of the CPV Group constitutes “forward‑looking” information as it is defined in the Securities Law, regarding which there is no certainty it will be

realized. Ultimately, the revenues of the CPV Group from capacity could change (even significantly) as a result of, among other things, regulatory changes, operational factors, regulatory arrangements applicable to capacity regarding fines

or bonuses, changes in the business environment and/or the occurrence of one or more of the risk factors the CPV Group is exposed to.

|

15

---Unofficial translation for convenience purposes---

OPC Energy Ltd.

Report of the Board of Directors

| 3. |

Main Developments in the Business and Regulatory Environment in the U.S. (Cont.)

|

| C. |

Capacity revenues (Cont.)

|

It is noted that the capacity prices set in the 2026/2027 and 2027/2028 auctions, as shown above, were

determined in accordance with the ceiling prices approved by PJM and approved by FERC for these two capacity auctions (with the necessary adjustments). In addition, the unforced capacity (UCAP) relative to installed capacity (ICAP) for combined

cycle gas plants were updated which led to a decrease in the UCAP that is provided for sale by the CPV Group’s natural‑gas power plants of this type from about 96% to about 79% (in the 2025/2026 auction) and from about 79% to about 74% (in the

2026/2027 auction and thereafter). It is further noted that based on PJM publications, the theoretical prices derived from the results of the auctions, had it not been for the said ceiling, would have been about $389 per megawatt/day and about $530

per megawatt/day, respectively. In April 2026, FERC approved PJM’s request to extend the maximum and minimum limits (collar) of $325 per megawatt/day and $175 per megawatt/day (adjusted for the UCAP to ICAP ratio), respectively, for two additional

capacity auctions for the 2028/2029 and 2029/2030 periods.

Subject to additional changes in the timetables, if any, as at the approval date of the report, the next PJM

capacity auction for the 2028/2029 capacity year is planned for June 2026.

The significant increase in the capacity tariffs in the latest auctions, as shown in the table above, relates

to, among other things, a continuing increase in electricity demand, anticipated growth in future demand, higher reserve requirements, and a decline in the aggregate supply due to a change in the methods used to calculate capacities and demand

capability of PJM’s generation sources.

Reliability Backstop Procurement (RBP) – in April 2026, PJM published an initial RBP7 proposal

for an emergency procurement of additional available capacity, for the purpose of providing a response to an anticipated capacity deficiency stemming from an increase in the demand for electricity. The proposal includes procurement in an initial

scope of about 15 gigawatts and is based on a two‑stage format:

| – |

Stage 1 – Bilateral arrangements between generators and consumers, facilitated by PJM, which is expected to take place between September 2026 and March 2027; and

|

| – |

Stage 2 – Centralized procurement led by PJM, which is expected to begin in March 2027, for the balance of the available capacity that is not secured though the bilateral stage. The centralized procurement is expected to include

contracts for capacity only for periods of up to 15 years, where the eligibility is expected to be limited solely to new resources, including new-build generation, upgrades, conversions and demand response solutions, which are expected to

reach commercial operation by June 1, 2031.

|

PJM has started a formal process with the interested parties and is expected to submit a proposal to FERC in

June 2026. As at the approval date of the report, the final RBP, its scope and timetables have not yet been finally formulated, and they are subject to, among other things, regulatory approvals and changes. Accordingly, in the estimation of the CPV

Group, at this stage it is not possible to assess the impact of the RBP on the market, particularly its impact with respect to future capacity tariffs.

| 7 |

For further details, see PJM’s publication dated April 16, 2026: https://www.pjm.com/-/media/DotCom/committees-groups/cifp-rbp/2026/20260416/20260416-item-05---pjm-reliability-backstop-procurement-proposal---paper.pdf

|

16

---Unofficial translation for convenience purposes---

OPC Energy Ltd.

Report of the Board of Directors

| 3. |

Main Developments in the Business and Regulatory Environment in the U.S. (Cont.)

|

| C. |

Capacity revenues (Cont.)

|

The CPV Group is examining and taking action with respect to some of its development projects, particularly the

Shay project (as detailed in Section 5B(2) below), to position them as projects that may meet the eligibility conditions for participation in the RBP – to the extent this procurement is implemented, and taking into account changes that could be

made thereto prior to its final formulation. It is clarified that participation in the RBP, if ultimately advanced, could involve provision of collaterals in significant amounts, which could be impacted by, among other things, the number of

projects and the length of the availability period.

In addition, on May 6, 2026, PJM published a document8 whereby it examines possible future reforms in

the capacity (availability) market. For additional details regarding the latest developments in the PJM capacity market – see Section 3C of the Report of the Board of Directors for 2025 and Section 8.1.2.1A of Part A of the Periodic Report for

2025.

NYISO market

For details regarding capacity auctions in the NYISO market – see Section 3C of the Report of the Board of

Directors for 2025.

Set forth below are the capacity prices determined in the seasonal auctions in the NYISO market (the prices are

denominated in dollars per megawatt per day):

|

Sub-Area

|

CPV Power

Plants

|

Summer 2026

|

Winter 2025/2026

|

Summer 2025

|

Winter 2024/2025

|

|

NYISO

Rest of the Market

|

–

|

174.46

|

89.83

|

153.26

|

66.30

|

|

Lower Hudson Valley

|

Valley

|

174.46

|

89.83

|

153.26

|

66.30

|

Source: NYISO – Converted from dollars for kilowatt per month to dollars for megawatt per day.

It is noted that the Valley power plant is located in Area G (Lower Hudson Valley) and the actual capacity

prices for the Valley power plants are impacted by the seasonal auctions, the monthly auctions and the SPOT prices, with variable capacity prices every month, as well as bilateral agreements with energy suppliers in the market.

| 8 |

For further details, see PJM’s publication dated May 6, 2026:

https://www.pjm.com/-/media/DotCom/library/reports-notices/special-reports/2026/20260506-powering-reliability-through-market-design.pdf

|

17

---Unofficial translation for convenience purposes---

OPC Energy Ltd.

Report of the Board of Directors

| 3. |

Main Developments in the Business and Regulatory Environment in the U.S. (Cont.)

|

| C. |

Capacity revenues (Cont.)

|

ISO‑NE market

For details regarding capacity auctions in the ISO‑NE market and a planned reform in the structure of the

capacity market – see Section 3C of the Report of the Board of Directors for 2025 and Section 8.1.2.1C of Part A of the Periodic Report.

Up to May 2025, the tariff applicable for the Towantic power plant was $313.97 MW/day (linked to the

Handy-Whitman Price Index from 2019).

Set forth below are the capacity payments determined in the sub‑regions that are relevant to the Towantic power

plant (the prices are denominated in dollars per megawatt per day):

|

Sub-Region

|

CPV Power Plants

|

2027/2028

|

2026/2027

|

2025/2026

|

|

ISO-NE

Rest of the Market

|

Towantic

|

117.70

|

85.15

|

85.15

|

Source: ISO-NE – the Company’s processing in order to convert from dollars for kilowatt per month to dollars for

megawatt per day.

It is noted that as at the approval date of the report the actual capacity prices for the Towantic power plant

are impacted by forward auctions, supplementary annual auctions, monthly auctions with capacity prices that change every month and bilateral agreements with energy suppliers in the market.

| D. |

Changes in the government’s policies and legislation of the One Big Beautiful Bill in the U.S. – for additional information regarding the impacts of the changes in the federal policies of the U.S. government, including with

respect to reduction of the government’s support of renewable energies, changes in the federal tax benefits, imposition of tariffs and the uncertainty created thereby, as well as the impacts of legislation of the One Big Beautiful Bill on

the activities of the CPV Group in the areas of natural gas and renewable energies – see Section 3D of the Report of the Board of Directors for 2025 and Section 8.1.3.1 of Part A of the Periodic Report for 2025. For additional details

regarding the possible impact on development projects, including on the forecasted start dates of the construction and the feasibility of the projects – see also Section 5C(2) below.

|

18

---Unofficial translation for convenience purposes---

OPC Energy Ltd.

Report of the Board of Directors

| 4. |

Analysis of the results of operations for the Three Months Ended March 31, 2026 (in millions of dollars)

|

| A. |

Consolidated statement of income

|

|

Section

|

For the Three Months Ended

|

|

|

March 31

|

||

|

*2026

|

2025

|

|

|

Revenues from sales and provision of services (1)

|

317

|

183

|

|

Cost of sales and provision of services (without depreciation and amortization) (2)

|

(245)

|

(139)

|

|

Depreciation and amortization

|

(24)

|

(17)

|

|

Gross profit

|

48

|

27

|

|

Share in earnings of associated companies

|

34

|

38

|

|

Administrative and general expenses

|

(23)

|

(15)

|

|

Business development expenses

|

(2)

|

(1)

|

|

Other expenses, net

|

(17)

|

(3)

|

|

Operating income

|

40

|

46

|

|

Financing expenses, net

|

(20)

|

(13)

|

|

Income before taxes on income

|

20

|

33

|

|

Income tax expenses

|

(6)

|

(8)

|

|

Net income for the period (3)

|

14

|

25

|

|

Attributable to:

|

||

|

The Company’s shareholders

|

12

|

18

|

|

Holders of non‑controlling interests

|

2

|

7

|

| * |

Starting from January and February 2026, the Company has commenced consolidating the Shore and Basin Ranch (under construction) power plants, respectively, in its financial

statements. For additional details – see Notes 6A and 6B to the Interim Statements.

|

19

---Unofficial translation for convenience purposes---

OPC Energy Ltd.

Report of the Board of Directors

| 4. |

Analysis of the results of operations for the Three Months Ended March 31, 2026 (in millions of dollars) (Cont.)

|

| A. |

Consolidated statement of income (Cont.)

|

(1) Changes in revenues:

|

Revenues

|

For the Three

|

Board’s Explanations

|

|

|

Months Ended

|

|||

|

March 31

|

|||

|

2026

|

2025

|

||

|

Revenues in Israel

|

|||

|

Revenues from sale of energy to private customers

|

96

|

78

|

An increase, in the amount of about $22 million, compared with the corresponding period last year,

stems mainly from an increase of about $10 million relating to an increase in customer consumption, and an increase of about $12 million due to a sharp drop in the average shekel/dollar exchange rate.

|

|

Revenues from sale of energy to the System Operator and to other suppliers

|

15

|

14

|

|

|

Revenues in respect of capacity payments

|

10

|

9

|

|

|

Revenues from sale of energy at cogeneration tariff

|

3

|

5

|

|

|

Revenues from sale of steam

|

4

|

4

|

|

|

Total revenues from sale of energy and others in Israel (without infrastructure services)

|

128

|

110

|

|

|

Revenues from private customers in respect of infrastructure services

|

53

|

36

|

An increase, in the amount of about $17 million, compared with the corresponding period last year,

stems mainly from an average increase in the tariffs at the rate of about 15%.

|

|

Total revenues in Israel

|

181

|

146

|

|

|

Revenues in the U.S.

|

|||

|

Revenues from generation and sale of electricity (Energy Transition)

|

84

|

–

|

The increase stems from the first‑time consolidation of the Shore power plant starting from January

2026.

|

|

Revenues in respect of capacity payments (Energy Transition)

|

14

|

–

|

The increase stems from the first‑time consolidation of the Shore power plant starting from January

2026.

|

|

Realization of derivatives for hedging electricity prices (Energy Transition)

|

(30)

|

–

|

The increase stems from the first‑time consolidation of the Shore power plant starting from January

2026.

|

|

Revenues from sale of electricity (Retail) activities

|

56

|

25

|

The increase stems mainly from an increase in the scope of the retail activities.

|

|

Revenues from provision of services and others

|

12

|

12

|

|

|

Total revenues in the U.S.

|

136

|

37

|

|

|

Total revenues

|

317

|

183

|

|

20

---Unofficial translation for convenience purposes---

OPC Energy Ltd.

Report of the Board of Directors

| 4. |

Analysis of the results of operations for the Three Months Ended March 31, 2026 (in millions of dollars) (Cont.)

|

| A. |

Consolidated statement of income (Cont.)

|

| (2) |

Changes in the consolidated cost of sales and provision of services:

|

|

Cost of Sales and

Provision of Services

|

For the Three

Months Ended

|

Board’s Explanations

|

|

|

March 31

|

|||

|

2026

|

2025

|

||

|

Cost of sales in Israel

|

|||

|

Natural gas and diesel oil

|

51

|

47

|

|

|

Expenses in respect of acquisition of energy

|

12

|

7

|

|

|

Cost of transmission of gas

|

4

|

4

|

|

|

Salaries and related expenses

|

4

|

2

|

|

|

Operating expenses

|

7

|

8

|

|

|

Total cost of sales in Israel without infrastructure services

|

78

|

68

|

|

|

Expenses in respect of infrastructure services

|

53

|

36

|

For details – see the explanation of the change in the revenues in respect of infrastructure services.

|

|

Total cost of sales in Israel

|

131

|

104

|

|

|

Cost of sales and services in the U.S.

|

|||

|

Cost of natural gas including RGGI (Energy Transition)

|

73

|

–

|

The increase stems from the first‑time consolidation of the Shore power plant starting from January 2026.

|

|

Operating expenses

(Energy Transition)

|

5

|

–

|

The increase stems from the first‑time consolidation of the Shore power plant starting from January 2026.

|

|

Realization of derivatives for hedging gas prices (Energy Transition)

|

(33)

|

-

|

The increase stems from the first‑time consolidation of the Shore power plant starting from January 2026.

|

|

Cost of sales in respect of sale of electricity (Retail)

|

58

|

24

|

The increase stems mainly from an increase in the scope of the retail activities.

|

|

Cost of sales in respect of provision of services and others

|

11

|

11

|

|

|

Total cost of sales and provision of services in the U.S.

|

114

|

35

|

|

|

Total cost of sales and provision of services

|

245

|

139

|

|

21

---Unofficial translation for convenience purposes---

OPC Energy Ltd.

Report of the Board of Directors

| 4. |

Analysis of the results of operations for the Three Months Ended March 31, 2026 (in millions of dollars) (Cont.)

|

| A. |

Consolidated statement of income (Cont.)

|

| (3) |

Consolidated net income and consolidated adjusted net income

|

| 1. |

Definitions

|

Adjusted net income or loss – net income or loss in accordance with IFRS plus or minus other expenses

and income, events of a non‑recurring nature, such as, impairment losses and reversals and transactions that are not in the ordinary course of business.

It is emphasized that the said adjusted net income or loss item in this report is not an item that is

recognized under IFRS or other generally accepted accounting standards as an index for measuring financial performances and is not intended to be considered as a substitute for income or loss or other terms provided pursuant to IFRS. It is possible

that the Company’s definitions of adjusted income or loss are different than those used by other companies. Nonetheless, the Company believes that the adjusted income or loss provides useful information to management and investors by excluding

certain items that management believes do not constitute an indication of the Company’s regular and ongoing business activities.

22

---Unofficial translation for convenience purposes---

OPC Energy Ltd.

Report of the Board of Directors

| 4. |

Analysis of the results of operations for the Three Months Ended March 31, 2026 (in millions of dollars) (Cont.)

|

| A. |

Consolidated statement of income (Cont.)

|

| (3) |

Consolidated net income and consolidated adjusted net income (Cont.)

|

| 2. |

Analysis of the change (in millions of dollars)

|

| (1) |

For an analysis of the change in the EBITDA after proportionate consolidation in the various segments in the Period of the Report compared with the corresponding period last year, see Sections B - E below.

|

| (2) |

Stems mainly from a loss, in the amount of about $12 million (after taxes), resulting from reclassification of balances of capital reserves and other comprehensive income (mostly in respect of hedging the electricity margin) to the

statement of profit and loss due to the initial consolidation of the Shore power plant and a loss of a non‑recurring nature in associated companies.

|

23

---Unofficial translation for convenience purposes---

OPC Energy Ltd.

Report of the Board of Directors

| 4. |

Analysis of the results of operations for the Three Months Ended March 31, 2026 (in millions of dollars) (Cont.)

|

| B. |

EBITDA, FFO (Funds From Operations) and net cash flows after debt service

|

| 1. |

Definitions

|

| – |

EBITDA indices

|

“EBITDA in the consolidated financial statements”9: net income (loss) for the period

before depreciation and amortization, financing expenses or income, net, taxes on income and other income (expenses), net.

“EBITDA after proportionate consolidation”: – “EBITDA in the consolidated financial statements” less the

share of the income (loss) of associated companies and plus a proportionate consolidation of the EBITDA of the associated companies based on the rate of the holdings of the CPV Group therein.

| – |

“FFO” (Funds From Operations) – with respect to active projects – cash flows from current operating activities for the period (including changes in working capital) and less investments in property, plant and equipment and

periodic maintenance costs that are not included in the operating activities and less net interest payments. With respect to the rest of the Group’s activities – cash flows from current operating activities for the period (including changes

in working capital) and less net interest payments (to the extent they do not relate to projects under construction). It is clarified that investments in property, plant and equipment (under construction and/or in development) including the

net interest payments in respect thereof, are not included in FFO.

|

| – |

“Adjusted FFO” – the “FFO” less the impacts of changes in working capital and receipts or payments of a non‑recurring nature or that are not in the ordinary course of business.

|

| – |

“Net cash flows after service of debt” – the “FFO” less/plus payment of principal in respect of financial debt or taking out of project debt and non‑project debt (loans and/or debentures), and after adjustments for a change in

other credit from banks and a change in cash, including cash restricted for debt service and deposits.

|

The said non‑IFRS measures are not recognized as indices for measurement of financial

performances and are not intended to be considered a replacement for gross profit or loss and operating income, cash flows from operating activities or other terms relating to operating performances or liquidity indices in accordance with IFRS.

It is noted that the EBITDA indices are not intended to present an approximate of the free cash flows from the

Group’s operating activities or to present cash available for distribution of dividends or other uses (particularly in light of provisions of the project financing agreements for some of the Group’s power plants), since such cash may be used for

debt service, capital investments, working capital and other liabilities. Moreover, the EBITDA indices are characterized by restrictions that limit the use thereof as indices for analyzing the Company’s profitability, since they do not take into

account certain income and expenses deriving from the Company’s business that could have a material impact on its net income or loss, such as depreciation expenses, financing expenses or income and taxes on income.

| 9 |

It is clarified that income in respect of lost profits is included in EBITDA in the consolidated statements.

|

24

---Unofficial translation for convenience purposes---

OPC Energy Ltd.

Report of the Board of Directors

| 4. |

Analysis of the results of operations for the Three Months Ended March 31, 2026 (in millions of dollars) (Cont.)

|

| B. |

EBITDA, FFO (Funds From Operations) and net cash flows after debt service (Cont.)

|

| 1. |

Definitions (Cont.)

|

The Company believes that the data items “EBITDA after proportionate consolidation” and “FFO”10

(including the adjusted) provide useful and transparent information to investors when reviewing the Company’s operating performances and current cash flows and when comparing such performances to performances of other companies in the same sector

or in other industries (having different capital structures, different levels of debt and/or different income tax rates) as well as when comparing performances between periods. It is noted that the “EBITDA after proportionate consolidation” data

item also serves the Company’s management when analyzing the Company’s performances.

The data item “net cash flows after debt service” provides additional information regarding the Group’s net

cash flows that are available for its use for purposes of growth and making of new investments, along with distribution of dividends to the shareholders (subject to compliance with the provisions of law, the trust certificates and non‑project

financing agreements and in accordance with the Company’s dividend distribution policy11).

| 10 |

It is noted that other companies might define EBITDA and FFO indices differently.

|

| 11 |

Pursuant to the Company’s dividend distribution policy, which was adopted by a decision of the Company’s Board of Directors in July 2017, it was determined that the Company will distribute, subject to the provisions of law and the

discretion of the Board of Directors, an annual dividend at the rate of at least 50% of the net after‑tax income. In 2024, the Company’s Board of Directors decided to suspend implementation of the dividend distribution policy for a period

of two years, in light of the Company’s growth strategy and the targets for expansion of its activities, while taking into account its business needs and preservation of its financial strength. In the decision of the Company’s Board of

Directors in March 2026, the suspension of the dividend distribution policy was extended for an additional at least two years, that is, at least up to March 2028, where at the end of this period the Board of Directors will consider

restarting of the said policy and the conformance thereof to the circumstances as they will be.

|

25

---Unofficial translation for convenience purposes---

OPC Energy Ltd.

Report of the Board of Directors

| 4. |

Analysis of the results of operations for the Three Months Ended March 31, 2026 (in millions of dollars) (Cont.)

|

| B. |

EBITDA, FFO (Funds From Operations) and net cash flows after debt service (Cont.)

|

| 2. |

Calculation of EBITDA

|

EBITDA calculations in the consolidated statement, including EBITDA after proportionate consolidation (in

millions of dollars):

|

For the

|

||

|

Three Months Ended

|

||

|

March 31

|

||

|

Revenues from sales and provision of services

|

317

|

183

|

|

Cost of sales (without depreciation and amortization)

|

(245)

|

(139)

|

|

Share in income of associated companies

|

34

|

38

|

|

Administrative and general expenses (without depreciation and

amortization)

|

(22)

|

(14)

|

|

Business development expenses

|

(2)

|

(1)

|

|

Consolidated EBITDA

|

82

|

67

|

|

Elimination of the share in income of associated companies

|

(34)

|

(38)

|

|

Plus – Group’s share of the proportionate EBITDA of associated companies in the Energy Transition segment

|

65

|

77

|

|

Plus – Group’s share of the proportionate EBITDA of activities

in the Renewable Energies segment in the U.S.

|

11

|

7

|

|

EBITDA after proportionate consolidation

|

124

|

113

|

| * |

Starting from January and February 2026, the Company has commenced consolidating the Shore and Basin Ranch (under construction) power plants, respectively, in its financial

statements. For additional details – see Notes 6A and 6B to the Interim Statements.

|

26

---Unofficial translation for convenience purposes---

OPC Energy Ltd.

Report of the Board of Directors

| 4. |

Analysis of the results of operations for the Three Months Ended March 31, 2026 (in millions of dollars) (Cont.)

|

| B. |

EBITDA, FFO (Funds From Operations) and net cash flows after debt service (Cont.)

|

Set forth below is a breakdown of the EBITDA after proportionate consolidation data broken down by subsidiaries

(on a consolidated basis) and the associated companies (on a proportionate basis, based on the rate of the holdings of the CPV Group therein) as well as FFO and cash flows after service of debt data (in millions of dollars):

|

Main projects in operation

|

For the three months ended

|

For the three months ended

|

|||||

|

Basis of

|

March 31, 2026

|

March 31, 2025

|

|||||

|

presentation

|

|||||||

|

in the

|

EBITDA

|

EBITDA

|

|||||

|

Company’s

|

after

|

Net cash

|

after

|

Net cash

|

|||

|

financial

|

proportionate

|

flows after

|

proportionate

|

flows after

|

|||

|

statements

|

consolidation

|

FFO(6)

|

debt service

|

consolidation

|

FFO(6)

|

debt service

|

|

|

Total operating projects in Israel and accompanying business activities (1)

|

Consolidated

|

45

|

36

|

33

|

38

|

61

|

57

|

|

Business development costs, headquarters in Israel and other costs

|

Consolidated

|

(1)

|

(12)

|

(18)

|

–

|

(8)

|

(9)

|

|

Total Israel (2)

|

44

|

24

|

15

|

38

|

53

|

48

|

|

|

Total operating projects (3)

|

Associated + consolidated

|

88

|

49

|

74

|

77

|

51

|

(37)

|

|

Other expenses

|

Consolidated

|

–

|

(1)

|

(1)

|

–

|

(1)

|

(1)

|

|

Total energy transition in the U.S.

|

88

|

48

|

73

|

77

|

50

|

(38)

|

|

|

Total operating projects

|

Associated

|

12

|

7

|

3

|

9

|

6

|

–

|

|

Business development and other costs

|

Associated

|

(1)

|

(1)

|

(1)

|

(2)

|

(1)

|

(1)

|

|

Total renewable energy in the U.S.

|

11

|

6

|

2

|

7

|

5

|

(1)

|

|

|

Total activities as part of the “others” segment (4)

|

Consolidated

|

(6)

|

(10)

|

(5)

|

(2)

|

(2)

|

(2)

|

|

Headquarters in the United States (5) (6)

|

Consolidated

|

(10)

|

(78)

|

(78)

|

(5)

|

(12)

|

(12)

|

|

Total United States

|

83

|

(34)

|

(8)

|

77

|

41

|

(53)

|

|

|

Company headquarters (not allocated to the segments) (5)

|

Consolidated

|

(3)

|

(11)

|

(49)

|

(2)

|

(5)

|

(1)

|

|

Total consolidated

|

124

|

(21)

|

(42)

|

113

|

89

|

(6)

|

|

| (1) |

The accompanying business activities in Israel include mainly virtual supply activities through OPC Israel, and sale/purchase of natural gas, including with third parties through OPC Natural Gas.

|

| (2) |

Not including intercompany activities between the headquarters and the subsidiaries in Israel.

|

| (3) |

For details regarding active projects in the Energy Transition segment in the U.S. – see Section 4D below.

|

| (4) |

Includes mainly business development and other costs in the area of initiation and development of high‑efficiency natural gas-fired power plants, with future carbon capture potential, and the results of the retail activities in the

U.S.

|

| (5) |

After elimination of management fees between the CPV Group and the Company, in the amounts of about $3 million and about $2 million for the periods ended March 31, 2026 and 2025, respectively.

|

| (6) |

Set forth below are additional details regarding the FFO (in millions of dollars):

|

27

---Unofficial translation for convenience purposes---

OPC Energy Ltd.

Report of the Board of Directors

| 4. |

Analysis of the results of operations for the Three Months Ended March 31, 2026 (in millions of dollars) (Cont.)

|

| B. |

EBITDA, FFO (Funds From Operations) and net cash flows after debt service (Cont.)

|

|

For the three months ended March 31, 2026

|

For the three months ended March 31, 2025

|

|||||||

|

Working

|

Working

|

|||||||

|

capital

|

Other

|

Adjusted

|

capital

|

Other

|

Adjusted

|

|||

|

FFO

|

changes

|

changes*

|

FFO

|

FFO

|

changes

|

changes

|

FFO

|

|

|

Israel

|

24

|

3

|

–

|

27

|

53

|

(24)

|

–

|

29

|

|

U.S.

|

(34)

|

17

|

70

|

53

|

41

|

7

|

–

|

48

|

|

Company headquarters

|

(11)

|

6

|

–