REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR (g) OF THE SECURITIES EXCHANGE ACT OF 1934

OR

☒

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 2024

OR

☐

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

OR

☐

SHELL COMPANY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

Date of event requiring this shell company report ………………………….

Commission file number 001-38965

INTERCORP FINANCIAL SERVICES INC.

(Exact name of Registrant as specified in its charter)

INTERCORP FINANCIAL SERVICES INC.

(Translation of Registrant’s name into English)

REPUBLIC OF PANAMA

(Jurisdiction of incorporation or organization)

Intercorp Financial Services Inc.

Torre Interbank, Av. Carlos Villarán 140

La Victoria

Lima13, Peru

(Address of principal executive offices)

Michela Casassa Ramat

Intercorp Financial Services Inc.

Torre Interbank, Av. Carlos Villarán 140

La Victoria

Lima13, Peru

Telephone: (511) 219-2000 ext. 22110

E-mail: mcasassa@intercorp.com.pe

(Name, telephone, e-mail and/or facsimile number and address of company contact person)

Securities registered or to be registered pursuant to Section 12(b) of the Act:

Title of each class

Trading

Symbol(s)

Name of each exchange on which registered

Common Shares

IFS

NYSE and Lima

Securities registered or to be registered pursuant to Section 12(g) of the Act:

None

(Title of Class)

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act:

None

(Title of Class)

Indicate the number of outstanding shares of each of the issuer’s classes of capital or common stock as of the close of the period covered by the annual report:

Common shares outstanding as of December 31, 2024: 113,288,457

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

☒Yes ☐ No

If this report is an annual or transition report, indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15 (d) of the Securities Exchange Act of 1934.

☐ Yes ☒No

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

☒Yes ☐ No

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files)

☒Yes☐ No

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or an emerging growth company. See definition of “large accelerated filer,” “accelerated filer,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer☒

Accelerated filer ☐

Non-accelerated filer ☐

Emerging growth company ☐

If an emerging growth company that prepares its financial statements in accordance with U.S. GAAP, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards† provided pursuant to Section 13(a) of the Exchange Act. ☐

† The term “new or revised financial accounting standard” refers to any update issued by the Financial Accounting Standards Board to its Accounting Standards Codification after April 5, 2012.

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☒

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. ☐

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). ☐

Indicate by check mark which basis of accounting the registrant has used to prepare the financial statements included in this filing:

U.S. GAAP ☐

International Financial Reporting Standards as issued

Other ☐

by the International Accounting Standards Board

☒

If “Other” has been checked in response to the previous question, indicate by check mark which financial statement item the registrant has elected to follow.

☐ Item 17 ☐ Item 18

If this is an annual report, indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

☐ Yes ☒ No

(APPLICABLE ONLY TO ISSUERS INVOLVED IN BANKRUPTCY PROCEEDINGS DURING THE PAST FIVE YEARS)

Indicate by check mark whether the registrant has filed all documents and reports required to be filed by Sections 12, 13 or 15(d) of the Securities Exchange Act of 1934 subsequent to the distribution of securities under a plan confirmed by a court. ☐ Yes ☐ No

All references to “we”, “us”, “our company”, and “IFS” in this Annual Report on Form 20-F are to Intercorp Financial Services Inc., a corporation (sociedad anónima) organized under the laws of the Republic of Panama (“Panama”).

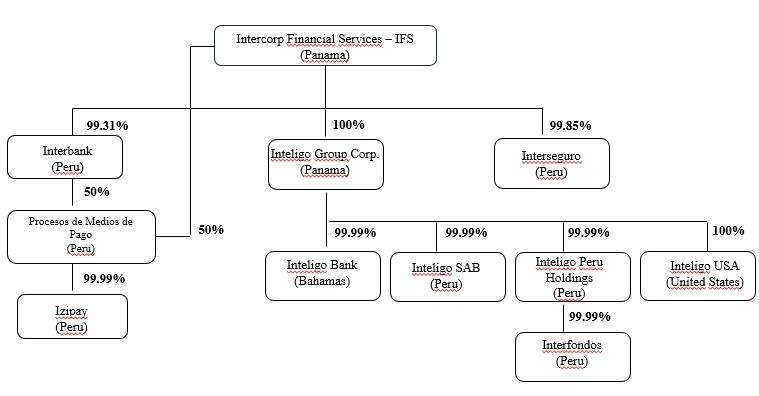

In this Annual Report on Form 20-F, we refer to and the discussion of our business includes the business of our principal subsidiaries as follows: (i) in our banking segment: Banco Internacional del Perú, S.A.A.—Interbank, an open-stock corporation (sociedad anónima abierta) organized under the laws of Peru, as “Interbank”; (ii) in our insurance segment: Interseguro Compañía de Seguros, S.A., a corporation (sociedad anónima) organized under the laws of Peru, as “Interseguro”; (iii) in our wealth management segment: Inteligo Group Corp., a corporation (sociedad anónima) organized under the laws of Panama, as “Inteligo”; Inteligo Bank Ltd., a corporation organized under the laws of The Bahamas, as “Inteligo Bank”; Inteligo Sociedad Agente de Bolsa S.A., a corporation (sociedad anónima) organized under the laws of Peru, as “Inteligo SAB”; Inteligo USA Inc., a corporation organized under the laws of New York, as “Inteligo USA,” and Interfondos S.A. Sociedad Administradora de Fondos, a corporation organized under the laws of Peru, as “Interfondos SAFM” or “Interfondos”; and (iv) Procesos de Medios de Pago S.A., a corporation (sociedad anónima) organized under the laws of Peru, as “PMP” and its subsidiary Izipay S.A.C., a closed-stock corporation (sociedad anónima cerrada) organized under the laws of Peru, as “Izipay,” both of which are IFS’ consolidated subsidiaries since April 2022. Except otherwise provided, references to Izipay shall include PMP.

In this Annual Report on Form 20-F, we also refer to our parent company, Intercorp Perú Ltd. (“Intercorp Peru” or “Intercorp”), a holding company for a group of companies operating mainly in Peru under the name “Intercorp”. Intercorp Peru’s main subsidiaries include our company and Intercorp Retail Inc. (“Intercorp Retail”). Intercorp Retail acts as a holding company for the retail and real estate operations of Intercorp Peru in Peru. Through its subsidiary, InRetail Peru Corp., whose shares are listed on the Lima Stock Exchange under the symbol “INRETC1,” Intercorp Retail has controlling stakes in (i) Supermercados Peruanos S.A. (“Supermercados Peruanos”), an operating supermarket chain that consolidates other operating companies, primarily operating under the: “Plaza Vea,” “Vivanda,” “MASS” and “Makro” brands, (ii) InRetail Pharma S.A., a holding company consisting of a chain of pharmacies operating under the “Inkafarma” and “MiFarma” brands with a distribution and marketing business as well as manufacturing some pharmaceutical products and (iii) InRetail Real Estate Corp., an owner, developer and operator of shopping malls under the “Real Plaza” brand. Intercorp Retail also controls directly (a) Tiendas Peruanas S.A., a department store chain operating under the “Oechsle” brand that started operations in 2009, (b) Financiera Oh! S.A., a consumer finance company that started operations in 2010, and (c) Homecenters Peruanos S.A. (“Homecenters Peruanos”), a home improvement company operating under the “Promart” brand. Our parent company Intercorp Peru also controls the following companies involved in the private education and healthcare businesses under the following brands: “Innova Schools,” “Zegel,” “UTP,” “IDAT” and “Aviva”.

1

SUMMARY OF RISK FACTORS

An investment in our common shares is subject to a number of risks, including risks relating to the nature of our business as a holding company of banking, insurance, financial institutions, and payments institutions, our operations in Peru and our common shares. The following list summarizes some, but not all, of these risks. Please read the information in the section entitled “Risk Factors” for a more thorough description of these and other risks.

Risks Relating to Our Businesses

•

We are a holding company and all of our operations are conducted through our subsidiaries. Our ability to pay corporate expenses and to pay dividends, if any, to holders of our common shares depends on the ability of our subsidiaries to pay dividends and make other distributions to us.

•

As a holding company, our right to receive any distribution of assets of our subsidiaries will be effectively subordinated to the rights of our subsidiaries’ creditors, and holders of our common shares may have limited recourse against our subsidiaries’ assets in case of our liquidation.

•

Our subsidiaries are subject to extensive regulation and supervision, and changes in existing regulations or the implementation of future regulations may have a material adverse effect on our financial condition and results of operations.

•

Enhanced ESG and climate change disclosure may impose additional costs on us or our subsidiaries.

•

The operations of our subsidiaries require the maintenance of banking, insurance and other licenses and any non-compliance with applicable licenses and operating obligations could have a material adverse effect on our business, financial condition and results of operations.

•

Under certain circumstances, the SBS, the SMV, the Superintendency of Banks of Panama or the Central Bank of The Bahamas, as applicable, may intervene in our subsidiaries’ operations in order to prevent, control and reduce the effects of a failure of our operations.

•

The adoption of new international banking and insurance guidelines may cause our subsidiaries to require additional capital and could cause their cost of funds to increase, which could have a material adverse effect on our financial condition and results of operations.

•

We are subject to regulatory capital requirements imposed by the SBS, and failure to comply with these requirements could have a material adverse effect on our financial condition and results of operations.

•

Our subsidiaries face intense competition from other banking, insurance and financial institutions, and from other players including providers of emerging financial technologies and failure to compete successfully could have a material adverse effect on our financial condition and results of operations.

•

The failure of our subsidiaries to effectively anticipate or adapt to emerging technologies or changes in customer behavior could have a material adverse effect on our financial conditions and results of operations.

•

The banking and insurance markets are exposed to macroeconomic shocks that could have a material adverse effect on our financial condition and results of operations.

•

We could sustain losses if Interbank’s asset quality declines.

•

Reduced diversification in Interbank’s loan portfolio could have a material adverse effect on our financial condition and results of operations.

•

Interbank’s provisions for loan losses may not be adequate to cover the future losses to its loan portfolio or other assets, which could have a material adverse effect on our financial condition and results of operations.

2

•

Interbank may be unable to realize the collateral or guarantees securing its loans to cover the outstanding principal and interest balance of those loans, which may adversely affect our results of operations and financial condition.

•

Our financial results may be negatively affected by changes to International Financial Reporting Standards ("IFRS Accounting Standards").

•

Our financial results may be negatively affected by investment losses.

•

Interest rate changes could have a material adverse effect on our financial condition and results of operations.

•

Interseguro is exposed to the impact of changes in interest rates on other comprehensive income.

•

Actual mortality and morbidity rates and other factors may differ from those assumed in the calculation of technical reserves and may have a material adverse effect on Interseguro’s financial condition and results of operations.

•

Interbank may not be able to obtain the funding required to support growth and implement its strategy.

•

A reduction in our subsidiaries’ credit ratings could increase their cost of borrowing funds and make their ability to raise new funds and renew maturing debt more difficult.

•

Interseguro’s failure to underwrite and price insurance premiums accurately for the products it offers would have a material adverse effect on its financial condition and results of operations.

•

Interbank’s and Interseguro’s reliance on Peruvian sovereign and global bonds in their respective investment portfolios leaves us vulnerable to a default on such debt.

•

Interseguro may suffer losses in its investment portfolio because of risks associated with its real estate investments.

•

Tax exemptions applicable to a substantial portion of Interseguro’s investment earnings could be changed in the future.

•

We and our subsidiaries are dependent on key personnel.

•

Interruption, mismanagement or failure in our subsidiaries’ information technology systems may adversely affect their operations.

•

Cybersecurity events could negatively affect our reputation or results of operations and may result in litigation.

•

Our subsidiaries are susceptible to fraud, unauthorized transactions and operational errors.

•

Our existing insurance coverage may be insufficient and future coverage may be difficult or expensive to obtain.

•

Our subsidiaries' employees could join labor unions and our subsidiaries could be subject to organized labor actions, including work stoppages that could have a material adverse effect on their business.

•

Our trademarks and trade names may be misappropriated or challenged by others.

•

Any failure to comply with anti-corruption, anti-bribery, anti-money laundering and anti-terrorist financing and antitrust laws and regulations could damage our reputation or expose us to penalties.

•

We and our subsidiaries are subject to litigation and other legal, administrative and regulatory proceedings.

•

Legal restrictions on our clients may reduce the demand for our services.

•

Our risk management structure may not be fully effective.

3

•

Implementation of tax laws related to the global minimum tax may increase our subsidiaries’ tax liabilities, and, as a result, have a material and adverse effect on us.

•

Disruptive innovation by fintechs and insurtechs may result in increased competition, and as a result, have a material and adverse effect on our subsidiaries.

•

Transition to a low-carbon economy may have a material and adverse effect on our subsidiaries’ results of operations.

•

Public health crises and epidemics/pandemics could adversely affect our and our subsidiaries’ business, financial condition and results of operations.

Risks Relating to Peru

•

Economic, social and political developments in Peru, including political instability, social unrest, inflation and unemployment, could have a material adverse effect on our businesses.

•

Fluctuations in the value of the sol could have a material adverse effect on our financial condition and results of operations.

•

A downgrade in Peru’s credit ratings may affect the perception of Peru and its economy and consequently adversely affect us.

•

Potential exchange controls implemented by the Peruvian government could adversely affect our ability to pay dividends and have a material adverse effect on our financial condition and results of operations.

•

Increased inflation in Peru could have an adverse effect on the Peruvian long-term credit market as well as the Peruvian economy generally and, therefore, on our financial condition and results of operations.

•

The stability of the Peruvian financial system depends on public confidence in Peruvian banking and financial institutions.

•

The Peruvian economy could be adversely affected by economic developments in regional or global markets.

•

A decline in the prices of certain commodities in the international markets could have a material adverse effect on our financial condition and results of operations.

•

The market volatility generated by distortions in the international financial markets may affect the Peruvian capital markets and the Peruvian banking system.

•

The operations of Interbank, Interseguro, Interfondos, Inteligo SAB and Izipay could be adversely affected by earthquakes, floodings or other natural disasters.

•

Corruption and ongoing high profile corruption investigations may hinder the growth of the Peruvian economy and have a negative impact on our business and operations.

•

Changes in tax laws may increase our tax liabilities and, as a result, have a material and adverse effect on us.

•

The dollarization of the Peruvian economy hampers monetary policy, which in turn may have an effect on our business.

•

The 2026 general elections in Peru may result in political and electoral uncertainty in Peru.

Risks Relating to the Common Shares

•

There may be a lack of liquidity and market for our common shares.

•

The price of our common shares may be volatile.

•

We may raise additional capital in the future through the issuance of equity securities, which may result in dilution of the interests of our shareholders.

4

•

The significant share ownership of our controlling shareholder may conflict with the interests of the holders of our common shares and may have an adverse effect on the future market price of our shares.

•

Holders of our common shares may have fewer and less well-defined rights than shareholders of a company organized in other jurisdictions, such as the United States.

•

Holders of our common shares may have difficulty enforcing judgments against us, our officers and directors.

•

Judgments of Peruvian courts with respect to our common shares will be payable only in soles.

•

We are subject to different corporate disclosure and accounting standards than those holders of our common shares may be familiar with in the United States.

•

We could be considered a passive foreign investment company ("PFIC") for U.S. federal income tax purposes, which could result in adverse U.S. tax consequences for U.S. investors.

•

One or more of our subsidiaries could be classified as a PFIC for U.S. federal income tax purposes.

•

If we are unable to maintain effective internal control over financial reporting in the future, our results of operations and the price of our common shares could be adversely affected.

•

The requirements of being a public company may strain our resources, divert management’s attention and affect our ability to attract and retain qualified board members or executive officers.

•

Our status as a foreign private issuer allows us to follow alternate standards to the corporate governance standards of the NYSE, which may limit the protections afforded to investors.

•

If securities or industry analysts do not actively follow our business, or if they publish unfavorable research about our business, the price and trading volume of our common shares could decline.

•

Future offerings of debt or preferred securities may limit our operating and financial flexibility and may materially adversely affect the market price of, and dilute the value of, the common shares.

•

Peruvian corporations, including our subsidiaries, may be jointly and severally liable for any unpaid Peruvian capital gains tax related to the transfer of the common shares.

5

FORWARD-LOOKING STATEMENTS

This Annual Report on Form 20-F contains forward-looking statements. All statements other than statements of historical facts included in this Annual Report on Form 20-F regarding our business, financial condition, results of operations and certain of our plans, objectives, assumptions, projections, expectations or beliefs and statements regarding other future events or prospects are forward-looking statements. These statements include, without limitation, those concerning: our strategy and our ability to achieve it; expectations regarding sales, profitability and growth; our possible or assumed future results of operations; capital expenditures and investment plans; adequacy of capital; and financing plans. In addition, this Annual Report on Form 20-F includes forward-looking statements relating to our potential exposure to various types of market risks, such as macroeconomic risk, Peru specific risks, foreign exchange rate risk, interest rate risks and other risks related to our financial performance. The words “aim,” “may,” “will,” “expect,” “is expected to,” “anticipate,” “believe,” “future,” “continue,” “help,” “estimate,” “plan,” “schedule,” “intend,” “should,” “would be,” “seeks,” “estimates,” “shall,” or the negative or other variations thereof, as well as other similar expressions regarding matters that are not historical facts, are or may indicate forward–looking statements.

We have based these forward-looking statements on our management’s current views with respect to future events and financial performance. These views reflect the best judgment of our management but involve a number of risks and uncertainties which could cause actual results to differ materially from those predicted in our forward–looking statements and from past results, performance or achievements. Although we believe that the estimates reflected in the forward-looking statements are reasonable, such estimates may prove to be incorrect. By their nature, forward-looking statements involve risk and uncertainty because they relate to events and depend on circumstances that will occur in the future. There are a number of factors that could cause actual results and developments to differ materially from those expressed or implied by these forward-looking statements. These factors include, among other things:

•

our holding company structure;

•

economic, business and political developments in Peru and globally, including corruption scandals involving the Peruvian government and related political instability;

•

economic and geopolitical developments in regional or global markets, including the new administration of the United States, Russia’s continued invasion of Ukraine and the military conflict between Israel and Hamas, as well as between Israel and Iran and Hezbollah;

•

the financial market volatility and market turmoil generated by trade policies, bank failures or similar developments in the United States and other regions;

•

health epidemics and pandemics and other outbreaks, government measures to contain the spread of these pandemics or outbreaks, their effects on the economy of Peru, and their impact on global and regional economic growth prospects, creditworthiness, counter-party risk, as well as any logistical, operational or labor disruptions, among others;

•

protests and social unrest in Peru against government economic policies, violent crime, corruption scandals and social inequality;

•

changes in Peruvian, Panamanian and Bahamian and other foreign laws and regulations including the adoption of new capital requirements for banks or insurance companies, as well as interest rate caps for banks;

•

the dollarization of the Peruvian economy;

•

increased competition in the Peruvian financial services and insurance markets;

•

increased inflation;

•

exchange rate instability and government measures to control foreign exchange rates;

•

developments affecting the purchasing power of middle-income consumers or consumer spending generally;

•

changes in interest rates;

•

downturns in the capital markets and changes in capital markets in general that affect policies or attitudes towards lending to Peru or Peruvian companies or securities issued by Peruvian companies;

6

•

our ability to keep up with technological changes and integrate new businesses into our operations;

•

the inability to obtain the capital we need for further expansion of our businesses;

•

the inability to attract and retain key personnel;

•

any future acquisitions may not bring anticipated benefits;

•

changes in tax laws;

•

severe weather, adverse climate changes and natural disasters (including El Niño and La Niña);

•

changes and volatility in regional or global markets;

•

dependence on sovereign debt in our investment portfolios;

•

credit and other risks of lending, such as increases in defaults of borrowers, and increases in the provision for loan losses;

•

increased costs of funding or inability of our subsidiaries to obtain additional debt or equity financing on attractive terms or at all;

•

a deterioration in the quality of our assets;

•

our provisions for impairment losses or the provisions from impairment losses of our subsidiaries may be inadequate;

•

changes to accounting standards;

•

changes in actuarial assumptions upon which our annuity business is based;

•

failure to adequately price insurance premiums;

•

decreases in the spread between investment yields and implied interest rates in annuities;

•

dependence on information technology (“IT”) systems and cybersecurity risks; and

•

other risks and uncertainties described in “Item 3. Key Information—Risk Factors.”

We urge holders of our common shares to read the sections of this Annual Report on Form 20-F entitled “Item 3. Key Information—Risk Factors”, “Item 4. Information on the Company— Business Overview” and “Item 5. Operating and Financial Review and Prospects” for a more complete discussion of the factors that could affect our future performance and the industries in which we operate. Additionally, new risks and uncertainties can emerge from time to time, and it is not possible for us to predict all future risks and uncertainties, nor can we assess their potential impact. Accordingly, holders of our common shares should not place undue reliance on forward-looking statements as a prediction of actual results.

All forward-looking statements included in this Annual Report on Form 20-F are based on information available to us on the date of this Annual Report on Form 20-F. We undertake no obligation to update publicly or revise any forward-looking statement, whether as a result of new information, future events or otherwise, except as may be required by applicable law. All other written and oral forward-looking statements attributable to us or persons acting on our behalf are expressly qualified in their entirety by the cautionary statements contained throughout this Annual Report on Form 20-F.

7

PRESENTATION OF FINANCIAL INFORMATION

Our audited annual consolidated financial statements as of December 31, 2024 and 2023 and for each of the three years ended December 31, 2024, 2023 and 2022 included in this Annual Report on Form 20-F have been prepared in soles and in accordance with IFRS Accounting Standards as issued by the International Accounting Standards Board (“IASB”) and audited by Tanaka, Valdivia & Asociados Sociedad Civil de Responsabilidad Limitada, PCAOB ID 1315, Lima, Peru, a member firm of Ernst & Young Global Limited (“EY Peru”).

For a description of our significant accounting policies, see Note 3 to our audited annual consolidated financial statements.

For regulatory purposes, including regulations of the Banco Central de Reserva del Perú (the “Central Reserve Bank of Peru” or “BCRP”) and regulations and the reporting requirements of the Superintendencia del Mercado de Valores (the “SMV”), our Peruvian subsidiaries, Interbank and Interseguro, also prepare in Spanish and make available to shareholders statutory financial statements as prescribed by the Peruvian Superintendency of Banks, Insurance and Private Pension Fund Administrators (Superintendencia de Banca, Seguros y Administradoras de Fondos de Pensiones, or “SBS”), hereinafter “SBS GAAP”.

We have included in this Annual Report on Form 20-F certain information reported by the SBS for the Peruvian banking and insurance sectors as a whole as well as for individual financial institutions in Peru, including Interbank and Interseguro, which report to the SBS in SBS GAAP. The information under SBS GAAP has been presented for comparative market purposes. All statements in this Annual Report on Form 20-F regarding our relative market position and financial performance vis-à-vis the financial services and insurance sectors in Peru are based, out of necessity, on information obtained from the SBS and the SMV. With respect to comparative banking information, we typically compare ourselves against certain peer banks or against the system as a whole. With respect to comparative insurance information, we typically compare ourselves against the industry as a whole. Statements in this Annual Report on Form 20-F regarding our relative market position and financial performance, however, do not include information relating to Inteligo as Inteligo is not regulated by and does not report to the SBS or the SMV.

Certain comparative financial information related to our compound annual growth rate (“CAGR”) included in this Annual Report on Form 20-F has been prepared based on information reported pursuant to SBS GAAP, except for Inteligo. Compound Annual Growth Rate (“CAGR”) is calculated by (i) dividing the value of a variable on year X (ending value) by the value of this same variable on year Y (beginning value), then (ii) raising this to an exponent of one divided by (X-Y) and (iii) subtracting one from the result. In addition, our Peruvian subsidiaries pay dividends to us on the basis of the SBS GAAP financial statements as further described in this Annual Report on Form 20-F. See “Item 8 Financial Information—Consolidated Statements and Other Financial Information—Dividends and dividends policy” and “Item 3. Key Information—Risk Factors—We are a holding company and all of our operations are conducted through our subsidiaries. Our ability to pay dividends to holders of our common shares depends on the ability of our subsidiaries to pay dividends and make other distributions to us.”

IFRS Accounting Standards differs in certain significant respects from SBS GAAP. Consequently, information presented in this Annual Report on Form 20-F in accordance with SBS GAAP or based on information from the SBS or SMV may not be comparable with our financial information prepared in accordance with IFRS Accounting Standards. Unless otherwise indicated, all financial information provided in this Annual Report on Form 20-F has been prepared in accordance with IFRS Accounting Standards.

Change in Accounting Policies and Estimates

Generally, we have only adopted standards, interpretations or amendments that were effective in each year. Therefore, standards, interpretations or amendments that become effective in 2025 or later have not been early adopted.

On January 1, 2024, we adopted the following standards, interpretations, or amendments: (i) in connection with lease liability in a sale and leaseback, amendments to IFRS 16 "Leases," (ii) in connection with classification of liabilities as current or non-current, amendments to IAS 1 "Presentation of Financial Statements” and (iii) in connection with supplier finance arrangements, amendments to IAS 7 "Statements of Cash Flows" and IFRS 7"Financial instruments: Disclosures". Such standards, interpretations or amendments have not had a significant impact on our consolidated financial statements. See Note 3.2 to our audited annual consolidated financial statements.

On January 1, 2023, we adopted the following standards, interpretations, or amendments: (i) IFRS 17 "Insurance Contracts", (ii) in connection with the definition of Accounting Estimates, an amendment to IAS 8 “Accounting Policies, Changes in Accounting Estimates and Errors,” (ii) in connection with the disclosure of Accounting Policies, amendments to IAS 1 “Presentation of Financial Statements” and IFRS Practice Statement 2 “Making Materiality Judgements,” (iii) in connection with Deferred Tax related to Assets and Liabilities arising from a Single Transaction, amendments to IAS 12 “Income Taxes,” and (iv) in connection

8

with the International Tax Reform – Pillar Two Model Rules, amendments to IAS 12 “Income Taxes.” Such standards, interpretations or amendments, except for IFRS 17, have not had a significant impact on our consolidated financial statements.

On January 1, 2022, we adopted the following standards, interpretations, or amendments: (i) in connection with costs of fulfilling a contract, an amendment to IAS 37 “Provisions, Contingent Liabilities and Contingent Assets,” (ii) amendments to IFRS 3 “Business Combinations,” (iii) in connection with proceeds before intended use of property, plant and equipment, an amendment to IAS 16 “Property, Plant and Equipment,” (iv) in connection with a subsidiary as a first time adopter, an amendment to IFRS 1 “First-time Adoption of International Financial Reporting Standards,” and (v) in connection with fees in the “10 per cent” test for derecognition of financial liabilities, an amendment to IFRS 9 “Financial Instruments.” Such standards, interpretations or amendments have not had a significant impact on our consolidated financial statements.

Currency Translation

The term “sol” and the symbol “S/” refer to the legal currency of Peru, and the term “U.S. dollar” and the symbol “U.S.$” refer to the legal currency of the United States.

We have translated some of the soles amounts contained in this Annual Report on Form 20-F into U.S. dollars for convenience purposes only. Unless otherwise indicated or the context otherwise requires, the rate used to translate soles amounts to U.S. dollars as of December 31, 2024 was S/3.764 = U.S.$1.00, which was the exchange rate reported for December 31, 2024 by the SBS. The Federal Reserve Bank of New York does not report a noon buying rate for soles. The U.S. dollar equivalent information presented in this Annual Report on Form 20-F is provided solely for convenience of investors and should not be construed as implying that the soles or other currency amounts represent, or could have been or could be converted into, U.S. dollars at such rates or at any other rate.

Effect of Rounding

Certain figures included in this Annual Report on Form 20-F and in our consolidated financial statements have been rounded for ease of presentation. Percentage figures included in this Annual Report on Form 20-F have not in all cases been calculated on the basis of such rounded figures but on the basis of such amounts prior to rounding. For this reason, percentage amounts in this Annual Report on Form 20-F may vary from those obtained by performing the same calculations using the figures in our consolidated financial statements. Certain numerical figures shown as totals in some tables may not be an arithmetic aggregation of the figures that preceded them due to rounding.

Market and Industry Data

In this Annual Report on Form 20-F, unless otherwise indicated, all macroeconomic data relating to Peru is based on information published by the SBS, the Central Reserve Bank of Peru, the Peruvian Ministry of the Economy and Finance (Ministerio de Economía y Finanzas, or “MEF”), and the Peruvian National Institute of Statistics and Information Processing (Instituto Nacional de Estadística e Informática, or “INEI”). References in this Annual Report on Form 20-F to “GDP” refer to real gross domestic product, except for GDP per capita and penetration ratios of loan products.

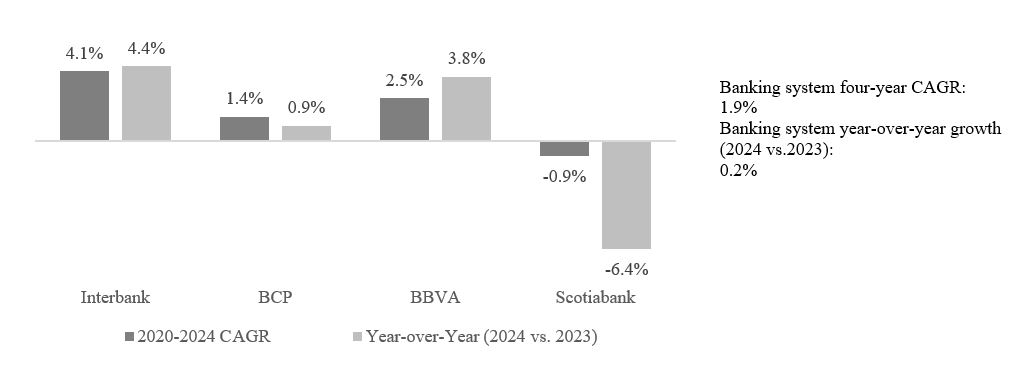

References in this Annual Report on Form 20-F to “peer countries” in Latin America refer to Brazil, Chile, Colombia and Mexico. Certain information about peer countries in Latin America have been derived from the Economist Intelligence Unit (“EIU”), the Chilean Superintendency of Banks and Financial Institutions (Superintendencia de Bancos e Instituciones Financieras, or “SBIF”), the Central Bank of Brazil (Banco Central do Brasil), the Colombian Financial Superintendency (Superintendencia Financiera de Colombia), and the Mexican Commission for Banking and Securities (Comisión Nacional Bancaria y de Valores). References in this Annual Report on Form 20-F to the “four largest banks in Peru” or the “four largest Peruvian banks” refer to Banco de Crédito del Perú (“BCP”), BBVA Continental, Interbank and Scotiabank Perú S.A.A.

Unless otherwise indicated, statistical information in this Annual Report on Form 20-F relating to our Peruvian subsidiaries Interbank and Interseguro, regarding market share, ranking, and other measures, as well as information on other Peruvian financial institutions and the Peruvian financial system generally, has been derived from reports and information published by the SBS, the SMV, the Central Reserve Bank of Peru, the Association of Peruvian Banks (Asociación de Bancos del Perú, or “ASBANC”) or from other publicly available sources and industry publications.

9

Socioeconomic levels are determined based on the data collected by INEI in their national annual survey Encuesta Nacional de Hogares (“ENAHO”). INEI assigns a score to each household based on their ranking on the following four factors: (i) characteristics of the household living space, (ii) level of living space overcrowding, (iii) level of education of household head and (iv) ownership of durable goods/properties; and then groups them in five socioeconomic segments (A, B, C, D, E).

Other market share information and other statistical information and quantitative statements in this Annual Report on Form 20-F regarding our market position relative to our competitors, except where otherwise indicated, is not based on published statistical data or information obtained from independent third parties. Rather, such information and statements reflect management estimates based upon our internal records and surveys, statistics published by providers of industry data, information published by our competitors, and information published by trade and business organizations and associations and other sources within the industry in which we operate. We have not independently verified any data produced by third parties or industry or general publications, although we believe such data and publications are reliable. In addition, while we believe our internal data and surveys to be reliable, such data and surveys have not been verified by any independent sources.

Loan Portfolio Data

Unless otherwise indicated, references in this Annual Report on Form 20-F to performing loans refer to loans in compliance with their original contractual obligations. References to past-due loans refer to overdue loans defined as follows: commercial loans are considered past-due once amortization payments are 15 days overdue; loans to micro-businesses are considered past-due once amortization payments are 30 days overdue; and in the case of consumer, mortgage and leasing loans, the amortization portion of a coupon is considered past-due once 30 days overdue and the total amount of the loan is considered past-due once an amortization payment is 90 days overdue. For IFRS 7 and IFRS 9 disclosure purposes, the entire loan balance is considered past due when debtors have failed to make a payment when contractually due. Past-due loans do not include refinanced and restructured loans. References to total gross loans include total loans outstanding, including past-due loans, refinanced loans and restructured loans, and references to total net loans refer to gross loans plus accrued interest less allowances for loan losses and deferred interest.

Interbank has rescheduled loans, and such rescheduling has involved modifying payment schedules, granting grace periods, and lowering interest rates, among other measures. As showed in the audited financial statements in Note 29.1 (d.7), there were three types of rescheduling: (1) reschedules due to the Covid-19 pandemic, (2) reschedules due to the “Reactiva Peru” program, a credit guarantee program launched by the Peruvian government (“Reactiva Peru”), and (3) rescheduling due to local political and social conflicts.

Changes in Operating Segments

During the second quarter of 2024, we changed the reporting structure of IFS’s operating segments compared with that presented in our annual report on Form 20-F for the year ended December 31, 2023 (the “2023 Form 20-F”), mainly as a consequence of the elimination of the payments segment, since its revenues and income do not meet the thresholds established by IFRS 8 "Operating Segments", as those represent less than 10% of IFS consolidated results. Therefore, since the second quarter 2024, the results of the businesses that previously comprised the payments segment ceased being reported separately to the board and Izipay, our payments subsidiary, was reclassified under “Holding, Other Subsidiaries and Eliminations”. For additional information on our current segments, see “Item 4. Information on the Company-Business Overview” and Note 27 to our audited annual consolidated financial statements.

In order to make the information as of and for the years ended December 31, 2023 and 2022 comparable with the information as of and for the year ended December 31, 2024, as required by IFRS 8 “Information by business segments”, figures as of and for the years ended December 31, 2023 and 2022 were recast in conformity with the new operating segment reporting structure.

Certain Financial Definitions and Conventions

We present return on assets, or “ROA”, return on equity or “ROE”, net interest margin or “NIM”, risk adjusted net interest margin or “risk adjusted NIM”, cost of risk and efficiency ratio in this Annual Report on Form 20-F. We define our ROA as net profit for the period divided by average total assets; our ROE as net profit for the period divided by average total equity; NIM as (x) net interest and similar income divided (y) average interest earning assets; risk adjusted NIM as net interest margin after impairment loss on loans, net of recoveries; cost of risk is defined as impairment loss on loans, net of recoveries divided by average gross loans. Efficiency ratio as the division of (x) salaries and employee benefits plus administrative expenses plus depreciation and amortization by (y) net interest and similar income plus other income, plus net premiums earned.

We present average balances and nominal average interest rates in this Annual Report on Form 20-F. Except as otherwise indicated, average balances are based on quarterly balances. Nominal average interest rates have been calculated by dividing interest earned on assets or paid on liabilities by the corresponding average balances on such assets or liabilities.

10

Non-GAAP Financial Measures

In this Annual Report on Form 20-F, we present adjusted net profit, adjusted ROE and adjusted ROA, which are non-GAAP financial measures. A non-GAAP financial measure does not have a standardized meaning prescribed by IFRS Accounting Standards. A non-GAAP financial measure is generally defined as a numerical measure of an issuer’s historical or future financial performance, financial position or cash flows that: (i) excludes amounts, or is subject to adjustments that have the effect of excluding amounts, that are included in the most directly comparable measure calculated and presented in accordance with IFRS Accounting Standards in the statement of income, balance sheet or statement of cash flows (or equivalent statements) of the issuer; or (ii) includes amounts, or is subject to adjustments that have the effect of including amounts, that are excluded from the most directly comparable measure so calculated and presented.

We believe that the presentation of these non-GAAP measures provides additional useful information to investors regarding our performance and trends related to our results of operations. Accordingly, we believe that when non-GAAP financial information is viewed with IFRS Accounting Standards' financial information, investors are provided with a more meaningful understanding of our ongoing operating performance and financial results.

ROE is calculated by dividing net profit for the year by average total equity. ROA is calculated by dividing net profit for the year by average total assets. Adjusted net profit is defined as net profit excluding non-operating and/or non-recurring gain or losses.

For the years ended December 31, 2024 and 2023, we did not make adjustments to our net profit, ROE or ROA. For the year ended December 31, 2022, we made adjustments to our net profit, to ROE and to ROA, as we defined our adjusted net profit (used for the calculation of adjusted ROE and adjusted ROA) as net profit excluding the gain recognized as a result of the step acquisition of Izipay, which management believes is non-recurring in nature. See Note 1(b) to our Audited Annual Consolidated Financial Statements.

We believe that the adjustment to our net profit provided useful metrics because by excluding the fair value adjustment of the 50% ownership interest held by Interbank in Izipay before the acquisition of the remaining 50% equity interest in Izipay in April 2022, it deducted from our net profit pre-acquisition effects that our management believes to be non-operating and/or non-recurring in nature and in so doing, allows us to better assess the performance of our operating activities. Adjusted net income, adjusted ROE and adjusted ROA do not have a standardized meaning and are not recognized measures under IFRS Accounting Standards. Adjusted net income, adjusted ROE and adjusted ROA should not each be considered by itself or as a substitute for net income or other measures of operating performance. Our definition of adjusted net income, adjusted ROE and adjusted ROA may differ from those used by other companies.

For a discussion on the non-GAAP financial measures and reconciliation of these measures to IFRS Accounting Standards' financial measures, see “Item 4. Information on the Company—Business Overview—Non-GAAP Financial Measures” and “Item 5. Operating and Financial Review and Prospects—Operating Results.”

There may be limits in the usefulness of these measures to investors. As a result, we encourage readers to consider the consolidated financial statements and other financial information contained in this Annual Report on Form 20-F in their entirety, and not to rely on any single financial measure.

11

PART I

ITEM 1. IDENTITY OF DIRECTORS, SENIOR MANAGEMENT AND ADVISERS

Not Applicable.

ITEM 2. OFFER STATISTICS AND EXPECTED TIMETABLE

Not Applicable.

ITEM 3. KEY INFORMATION

A.

[RESERVED]

B.

Capitalization and Indebtedness

Not Applicable.

C.

Reasons for the Offer and Use of Proceeds

Not Applicable.

D.

Risk Factors

An investment in our common shares involves a high degree of risk. In addition to the other information contained in this Annual Report on Form 20-F, holders of our common shares should carefully consider the following risk factors before purchasing our common shares. If any of the possible events described below occurs, our businesses, financial condition, results of operations or prospects could be materially and adversely affected. As a result, the market prices of our common shares could decline and holders of our common shares could lose all or part of their investment. The risks and uncertainties below are those known to us and that we currently believe may materially affect us and our common shares. We may face additional risks and uncertainties not currently known to us or which as of the date of this Annual Report on Form 20-F we might not consider significant, which may also adversely affect our businesses.

Risks Relating to Our Businesses

We are a holding company and all of our operations are conducted through our subsidiaries. Our ability to pay corporate expenses and to pay dividends, if any, to holders of our common shares depends on the ability of our subsidiaries to pay dividends and make other distributions to us.

As a holding company, all of our operations are conducted through our subsidiaries. Accordingly, our ability to pay corporate expenses and to pay dividends, if any, to holders of our common shares, depends on our receipt of dividends and other distributions from our subsidiaries.

There are various regulatory restrictions in Peru and other jurisdictions that may limit our subsidiaries’ ability to pay dividends or make other payments to us, such as their obligations to maintain minimum regulatory capital and minimum liquidity. See “—Public health crises and epidemics/pandemics could adversely affect our and our subsidiaries’ business, financial condition and results of operations”.

In addition, some of our Peruvian subsidiaries pay dividends to us on the basis of the SBS GAAP financial statements, which differ from IFRS Accounting Standards. For example, for the year ended December 31, 2024, Interseguro had a net profit of S/201.9 million under IFRS Accounting Standards and of S/376.3 million under SBS GAAP, which resulted in a dividend payment to us of S/125.0 million in 2025. Therefore, there is no assurance that the differences in accounting treatment will not render the opposite result, namely that lower or no dividends would be payable to us by any of our Peruvian subsidiaries under SBS GAAP than what it would appear to be able to pay under IFRS Accounting Standards, or that dividends will continue to be payable under SBS GAAP in the future.

Furthermore, our subsidiaries may incur indebtedness or enter into other arrangements containing terms that may restrict or prohibit the payment of dividends, the making of other distributions, or the making of loans to us. We cannot assure holders of our common shares that the agreements governing the future indebtedness of our subsidiaries will permit them to provide us with sufficient dividends, distributions or the making of loans to fund dividend payments.

12

To the extent our subsidiaries do not have funds available or are otherwise restricted from paying dividends to us, our ability to pay dividends to our shareholders will be adversely affected.

As a holding company, our right to receive any distribution of assets of our subsidiaries will be effectively subordinated to the rights of our subsidiaries’ creditors, and holders of our common shares may have limited recourse against our subsidiaries’ assets in case of our liquidation.

As a holding company, our right to receive any distribution of assets of our subsidiaries upon any subsidiary’s liquidation or reorganization or otherwise will be subject to the prior claims of creditors of that subsidiary, except to the extent that any claims by us as a creditor of such subsidiary may be recognized as such. Accordingly, holders of our common shares will have rights that will effectively be subordinated to all existing and future indebtedness of our subsidiaries, and, in the event of any claim against us, our shareholders may have recourse only against our assets, and not those of our subsidiaries, for payments. The only significant assets that we currently hold are our equity interests in our subsidiaries.

Our subsidiaries are subject to extensive regulation and supervision, and changes in existing regulations or the implementation of future regulations may have a material adverse effect on our financial condition and results of operations.

Interbank and Interseguro are subject to extensive regulation and supervision by the SBS. The SBS also oversees all of Interbank’s and Interseguro’s subsidiaries and their operations. Interbank is also subject to regulation and oversight by the Central Reserve Bank of Peru, which, together with the SBS, have general administrative responsibilities over banks and other financial institutions, including the authority to set loan loss provisions, limits on interest rates and fees, regulatory capital requirements and other minimum capital adequacy and reserve requirements. In addition, banks are required to provide the SBS, on a periodic basis, with all information necessary to allow for its evaluation of the bank’s financial performance. Similarly, insurance companies are required to periodically provide the SBS, with all information necessary for the SBS to evaluate the company’s management, measure systems, solvency, profitability and liquidity.

Similarly, Inteligo’s subsidiaries are regulated by governmental entities and other financial services regulators in The Bahamas, Panama and Peru. Inteligo Bank is subject to the regulation and supervision of the Central Bank of The Bahamas. Additionally, Inteligo Bank’s asset management activities and securities custody and trading activities are subject to supervision by the Securities Commission of The Bahamas. Inteligo Bank holds licenses from the Securities Commission of The Bahamas for dealing in securities as agent or principal, arranging deals, managing securities and advising on securities. Inteligo Bank is licensed to undertake all securities-related activities ancillary to its banking business. Inteligo Bank and its branch are subject to regulation by the Superintendency of Banks of Panama (Superintendencia de Bancos de Panamá). Inteligo Bank is also subject to regulation by the Securities Commission of Panama (Superintendencia del Mercado de Valores de Panama) since June 18, 2021, when it obtained its investment advisory license. On January 3, 2022, Inteligo Bank began its operations under such license. Inteligo SAB and Interfondos are subject to the regulation and supervision of the SMV in Peru. Also, Interbank and Interseguro are subject to the regulations of the SMV. PMP and Izipay are mainly subject to the regulations of the Central Reserve Bank of Peru. In addition, IFS, Interbank, Interseguro, Inteligo Bank and Inteligo SAB are subject to other regulations, such as the U.S. Foreign Account Tax Compliance Act (“FATCA”), which could increase compliance costs and, in case of non-compliance could result in liability, additional costs or sanctions imposed by the U.S. Internal Revenue Service.

Changes in the regulation and/or supervision of Interbank, Interseguro, Inteligo and/or Izipay or the implementation of future regulations could have a material adverse effect on our financial condition and results of operations by restricting our existing operations, limiting the expansion of our business and requiring extensive system and operating changes that may be difficult or costly to implement. For example, the SBS and the Central Reserve Bank of Peru regulate, and have in the past changed, capital structure and deposit reserve requirements, interest paid on deposit reserves, the amount of deposit reserves for which no interest is payable, rules regarding provisions for loan losses and legal lending limits applicable to Peruvian commercial banks. Furthermore, Interbank could be required to increase its level of provisions in response to pro-cyclical provisioning requirements or be required to increase capital levels in response to pro-cyclical buffers that could be activated by regulators under certain favorable macroeconomic conditions. As an example, additional changes in the regulation and supervision of our subsidiaries were imposed as a result of the COVID-19 pandemic and as a result of social unrest, which Interbank complied with, but we cannot predict whether and to what extent new laws and regulations will be imposed in case of other periods of crisis.

Moreover, changes in consumer protection regulation and protection of personal data may also affect our business. In March 2021, the Peruvian Congress approved Law No. 31143 under which (i) the Central Reserve Bank of Peru will semi-annually establish caps on interest rates (including default interest rates) that banks can charge to consumers and small businesses, and (ii) in cases of default, the debtor shall only pay interest which may not be capitalized and may not be charged with commissions or additional expenses. Since its approval, such new regulation limiting the interest that can be charged to clients of banking entities, such as Interbank, has negatively impacted its financial results. In addition, Interbank could be subject to limits on fees or commissions charged to clients. If legislation or governmental or regulatory action is enacted limiting the amount of ATM fees or

13

surcharges that Interbank may receive or on its ability to charge overdraft or other fees, it could adversely impact our financial results. Furthermore, during 2022, Legislative Decree No. 1531 amended the Peruvian Banking and Insurance Law (Ley General del Sistema Financiero y del Sistema de Seguros y Orgánica de la Superintendencia de Banca y Seguros), approved by Law No. 26702 (as amended, the “Peruvian Banking and Insurance Law”) to more closely align the Peruvian regulatory framework and its regulations applicable to the companies of the financial system to the Basel Committee’s 2011 agreement regarding the overall design of the capital and liquidity reform package (now referred to as “Basel III”), including changes related to the composition of the effective equity (which changes to effective equity came into effect as of January 1, 2023). Interbank has already implemented most of these requirements, with no adverse effect to its financial condition or operations, but as it continues to implement such additional requirements imposed by Legislative Decree No. 1531 and the other resolutions aimed at adapting the regulatory framework of the financial system more generally to the Basel III principles, we cannot guarantee that no such effects will impact its financial condition or results of operations. Similarly, in September 2024, Legislative Decree No. 1646 amended the Peruvian Banking and Insurance Law mainly to adjust lending limits based on concentration risk according to international standards to safeguard the solvency and stability of the Peruvian financial system. This legislation is expected to come into effect in June 2025 and be implemented in stages and subject to further regulations to be approved by the SBS. Likewise, also in September 2024, Legislative Decree No. 1665 amended Law No. 29440 (the Payments and Securities Settlement Systems Law) to grant new regulatory and sanctioning powers to the Central Reserve Bank of Peru (e.g., imposition of fines, and suspensions and cancellations of licenses, as the governing body of the Peruvian Payments and Securities Settlement Systems System), among other regulatory changes.

Since 1998, Interseguro has been subjected to strict local regulations that required significant changes in reserve requirements. For example, in March 2018, changes by the SBS to mortality tables used for calculating reserves for new annuities resulted in a higher reserve requirement, which in turn could adversely affect Interseguro’s results of operations or could result in lowered implied interest rates on Interseguro’s annuities. New legislation or regulations applicable to the insurance industry may adversely affect Interseguro’s ability to underwrite and price risks accurately as well as affect its revenues and net income. For example, whereas retirees formerly had to choose between remaining with their pension fund or choosing an annuity, since 2016 a law has allowed retirees to withdraw 95.5% of their capital accumulated in cash upon retirement, which has resulted in a significant reduction of annuities sold by Peruvian insurance companies, including Interseguro. In addition, considering that the SBS regulates the types of and limits on eligible investments that insurance companies, such as Interseguro, are allowed to make, in case the SBS enacts new regulations that further restricts such eligible investments, Interseguro could be compelled to liquidate current investments on less favorable terms than if they were held to maturity and restrict Interseguro from making investments that its management deems to be beneficial. Likewise, at the end of 2022, in order to adjust the fair value of real estate investments, the SBS established new requirements for valuation specialists or entities requiring capacitation in specific valuation matters that are not lectured in Peru, which created hurdles to such valuations and increased operating costs. Any failure to comply with these new requirements may increase costs and result in potential sanctions by the SBS. Moreover, in the past and as a response to the COVID-19 pandemic, the Peruvian government permitted companies to suspend employee contracts without pay in certain cases until the end of the COVID-19 pandemic, which caused these companies to stop making the corresponding monthly contribution to the pension funds of their worker, affecting the private pension system. In addition, the Peruvian government eased pension fund regulations, including measures permitting extraordinary withdrawals of funds from the private pension system, which in turn reduced pension funds collected by Interseguro. In September 2024, the Peruvian government enacted Law No. 32123, which established a reform of the Peruvian pension system. This law is expected to become effective in July 2025 and to limit extraordinary withdrawals of funds from the private pension system, which in turn may potentially reduce the demand for Interseguro’s annuities. Furthermore, Interseguro may face competition from private pension funds (Pension Funds Administrators, or “AFPs”) and Peruvian commercial banks, which could be allowed to offer annuities in the future. While this law provides insurance companies with the opportunity to manage private pension funds, any adverse impact on Interseguro resulting from increased competition or reform of the private pension system could have a material adverse effect on our financial condition and results of operations.

The Bahamas has repealed and replaced the Commercial Entities Economic Substance Requirements Act, 2018 with the Commercial Entities (Substance Requirements) Act, 2023 which requires substantial economic presence in The Bahamas for certain Bahamas incorporated or registered entities that conduct relevant activities. A relevant activity includes the business of banking as conducted by Inteligo Bank. Inteligo Bank has made the appropriate registration and it is exempt from the main substance requirements of the Commercial Entities (Substance Requirements) Act, 2023 due to its asserted tax residency outside of The Bahamas. If The Bahamas in the future changes such regulation such that Inteligo Bank is no longer considered to be exempt from the substance requirements, it would have to enhance its economic and business presence in The Bahamas in order to comply with the Commercial Entities (Substance Requirements) Act, 2023, which increased presence may result in increased costs—financial, compliance or otherwise, which could impact Inteligo Bank’s profitability and our results of operations.

We cannot predict whether and to what extent new laws and regulations, or changes to existing laws and regulations, affecting our subsidiaries’ business may be adopted in the future, the timing of any such adoption and what effect such events would have on our financial condition and results of operations.

14

Enhanced ESG and climate change disclosure may impose additional costs on us or our subsidiaries.

In recent years, various guidelines and regulations have been issued recommending or requiring companies to adopt policies and procedures with the purpose of enhancing the approach to environmental, governance and social (ESG) matters. In March 2024, the SEC adopted rules aimed at enhancing and standardizing climate-related disclosures. The rules require registrants to include certain climate-related information in their registration statements and annual reports, including data regarding greenhouse gas emissions and information regarding climate-related risks and opportunities and related financial impacts, governance and strategy. Several lawsuits have been filed against such rules and, unless they prevail, we would be subject to certain of these requirements commencing with the fiscal year ending on December 31, 2025. On April 4, 2024, the SEC voluntarily stayed the rules, pending judicial review, and on March 27, 2025, the SEC dropped the defense of the rules in court.

Although the SEC’s climate rules proposed in 2024 did not prosper, we cannot rule out future attempts to enact rules requiring climate-related disclosures. The adoption of new guidelines and regulations on ESG matters could limit our business or the businesses of our subsidiaries, restrict our ability or the ability of our subsidiaries to recruit new customers, increase compliance requirements or result in higher operating or funding costs, among other effects in the future that we cannot predict now, given the still-developing and evolving regulatory environment related to ESG matters.

The operations of our subsidiaries require the maintenance of banking, insurance and other licenses and any non-compliance with applicable licenses and operating obligations could have a material adverse effect on our business, financial condition and results of operations.

All banks and insurance companies established in Peru require certain authorizations issued by the SBS in order to operate in Peru. In addition, all brokerage firms operating in Peru require certain authorizations issued by the SMV in order to operate in Peru.Service providers (such as Izipay), collecting agents or processing agents in the payment industry are not required to obtain prior licenses. However, recent regulations imposed certain obligations to such entities (including anti-money laundering (“AML”) obligations) and required that they register with the Central Reserve Bank of Peru; furthermore, the Central Reserve Bank of Peru has established minimum quality levels for such entities. In The Bahamas and Panama, all banks require a license to operate. Governmental authorities, such as the SBS or the Central Reserve Bank of Peru, the Central Bank of The Bahamas, or the Superintendency of Banks of Panama, have general administrative responsibilities over banks and other financial institutions, including authority to set loan loss provisions, limits on fees, regulatory capital requirements and other minimum capital adequacy and reserve requirements. In addition, banks are generally required to provide the relevant banking supervisory agency, on a periodic basis, with all information that is necessary to allow for its evaluation of a bank’s financial performance. Insurance companies are regulated and supervised by the SBS which has the ability, among other things, to set reserve requirements for insurance companies. Similarly, the SMV and the Securities Commission of The Bahamas have general administrative responsibilities over brokerage firms, including the authority to set minimum capital requirements.

Our subsidiaries currently have the required licenses or applicable registrations in order to conduct their operations in their corresponding jurisdictions for all of their operations. Although we believe our subsidiaries are currently in compliance with their respective existing material license and reporting obligations, there is no assurance that our subsidiaries will be able to maintain the necessary licenses in the future. We can offer no assurance that future changes to existing laws and regulations, or stricter interpretation or enforcement of existing laws and regulations, will not impair our ability to comply with such laws and regulations and thus with the terms of our licenses.

The loss of a license, a breach of the terms of a license by any of our subsidiaries or the failure to obtain any further required licenses in the future could have a material adverse effect on our business, financial condition and results of operations. If any of our subsidiaries loses its licenses or is required to seek additional licenses, then such subsidiary will be unable to perform its operations as it is currently authorized and as it is currently doing.

Under certain circumstances, the SBS, the SMV, the Superintendency of Banks of Panama or the Central Bank of The Bahamas, as applicable, may intervene in our subsidiaries’ operations in order to prevent, control and reduce the effects of a failure of our operations.

Under the Peruvian Banking and Insurance Law and the regulations thereunder, the SBS may intervene in Interbank’s and Interseguro’s operations upon the occurrence of any of the following events:

•

Interbank or Interseguro suspends payment of its obligations or is unable to pay its obligations as they come due;

•

Interbank or Interseguro breaches any of their respective commitments to the SBS under a surveillance regime (régimen de vigilancia) imposed by the SBS;

15

•

Interbank’s regulatory capital is less than 50% of the minimum regulatory capital required under the Peruvian Banking and Insurance Law;

•

Interbank or Interseguro experiences a deficit or reduction of more than 50% of its regulatory capital during the preceding 12-month period; or

•

Interseguro experiences a deficit or reduction of the regulatory capital of more than 50% of its solvency equity.

In the event of an intervention, the SBS has the power to institute measures, such as limiting the decisions that could be taken at a shareholders’ meeting, suspending our normal activities and segregating certain of Interbank’s or Interseguro’s assets and liabilities for transfer to third parties, among others. Furthermore, the SBS has the power under the Peruvian Banking and Insurance Law to declare the wind-up or liquidation of any bank or insurance company if an intervention extends for longer than 45 days, which period may be extended one time for another 45 days at the sole discretion of the SBS, and/or upon the occurrence of a wind-up or liquidation pursuant to the Peruvian General Corporations Law (Ley General de Sociedades). For further detail, see “Item 4. Information on the Company—Business Overview—Regulation and Supervision—The Peruvian Financial and Insurance Systems — Intervention by the SBS and Liquidation”.

Under Peruvian capital markets laws and the regulations thereunder, the SMV may revoke the license of Inteligo SAB and/or Interfondos, among others, upon the occurrence of (i) significant irregularities that put the companies at risk to carry out their operations as permitted by law or (ii) significant violations of the law, statutes and regulations promulgated by the SMV.

Under Bahamian banking regulations, the Central Bank of The Bahamas may intervene in Inteligo Bank’s operations upon the occurrence of any of the following events:

•

Inteligo Bank carries on its business in a manner detrimental to the public interest or the interests of its depositors or other creditors; or

•

Inteligo Bank contravenes the provisions of Bahamian banking law or any other law, order or regulation made thereunder, or any term or condition subject to which its license was issued, either in The Bahamas or elsewhere.

In addition, under Bahamian securities laws and regulations, the Securities Commission of the Bahamas may revoke Inteligo Bank’s registration and license to deal in securities, arrange deals, manage securities and/or advise on securities for noncompliance with laws and regulations.

Under Law Decree 9 of 1998, as amended, the Superintendency of Banks of Panama may seize administrative and operating control of the branch of Inteligo Bank in Panama, based on any of the following grounds:

•

upon a reasoned request of Inteligo Bank itself;

•

if Inteligo Bank cannot continue operations without endangering the interests of the depositors;

•

as a consequence of the evaluation of the report submitted by an appointed advisor;

•

non-compliance with the corrective measures ordered by the Superintendency of Banks of Panama;

•

if Inteligo Bank carries out its operations in an illegal, negligent or fraudulent manner;

•

if Inteligo Bank has suspended payment on its obligations; or

•

if the Superintendency of Banks of Panama confirms that the capital adequacy, solvency or liquidity of Inteligo Bank has deteriorated so as to require action by the Superintendency of Banks of Panama.

The adoption of new international banking and insurance guidelines may cause our subsidiaries to require additional capital and could cause their cost of funds to increase, which could have a material adverse effect on our financial condition and results of operations.

In December 2009, the Basel Committee announced its intention to issue a new framework related to the regulation, supervision and risk management of the banking industry. This was followed by the Basel III principles, which revises and strengthens the three pillars established by Basel II.

16

Starting in 2011, the SBS issued different regulations to schedule additional capital requirements to be implemented in Peru, which, although not completely consistent with Basel III, included requirements to cover concentration, interest rate and systemic risk, as well as certain pro-cyclical capital requirements. In March 2022, the Peruvian government issued Legislative Decree 1531, which revised the regulatory capital definition rules in the Peruvian Banking and Insurance Law. This legislative decree became effective on January 1, 2023, aiming at a better alignment with the standards established by Basel III. Consistent with certain aspects of Basel III, the SBS issued in 2022, SBS Resolution No. 03953-2022 and SBS Resolution No. 03954-2022 in order to update the methodologies for calculating the individual and sector concentration risk buffers (including regional and economic sector concentration) eliminating the capital buffer requirement for risk appetite and maintaining the requirement for measuring the interest rate risk of the banking book. Legislative Decree No. 1531 and SBS Resolution No. 03954-2022 aligned the capital conservation buffer in the Peruvian regulation, to the Basel III principles.

In February 2016, the SBS issued SBS Resolution No. 975-2016 (as amended from time to time), which aimed to improve the quality of the total regulatory capital (patrimonio efectivo) and align Peruvian regulations towards Basel III. This resolution changed the conditions that subordinated debt must meet in order to be considered in the calculation of additional capital and the calculation methodology applicable to risk-weighted assets. In December 2022, as part of the implementation of the Basel III standards, the SBS issued SBS Resolution No. 03950-2022, which replaced the regulations applicable to subordinated debt related to its computation at the different levels and sublevels of the regulatory capital. This resolution became effective on January 1, 2023 and is applicable to subordinated debt incurred or created from the date of its effectiveness. However, as established in this new regulation, subordinated debt incurred or created prior to its effectiveness is still considered in the calculation of regulatory capital. Although the main changes became effective on January 1, 2023, other relevant regulation were also passed by the SBS by end of 2022 to implement the aforementioned law and provided certain adequacy periods until 2026. We cannot assure whether the implementation and further supervision of the above-mentioned new regulations may result in increased costs, financial, compliance or otherwise, which could impact our profitability and our results of operations. For further details, see “Item 4. Information on the Company—Business Overview—Regulation and Supervision—The Peruvian Financial and Insurance Systems”. As of the date of this Annual Report on Form 20-F, Interbank is fully compliant with applicable capital regulatory requirements. While Interbank expects to continue to be in compliance with current and upcoming capital requirements, Interbank’s assumptions with respect to compliance may turn out to be incorrect, and, consequently, have a material adverse effect on its financial condition and results of operations.