Annual Report

2025

Annual Report

2025

DOCVARIABLE ndGeneratedStamp \* MERGEFORMAT 4903-5206-7992, v. 1

ANNUAL REPORT

2025

SECTION I

STATEMENT OF RESPONSIBILITY

"This document contains true and sufficient information regarding the business development of INTERCORP FINANCIAL SERVICES INC. (hereinafter "IFS") throughout the year 2025.

Without prejudice to the liability of the issuer, the signatories are responsible for its contents in accordance with the applicable legal provisions. This document is issued in compliance with CONASEV Resolution No. 141-1998-EF/94.10 - Regulations for the Preparation and Submission of Annual Reports and its amending rules, and by General Management’s Resolution of the Superintendency of the Securities Market (SMV) No. 211-98-EF/94. 11 - Manual for the Preparation of Annual Reports and Common Rules for the Determination of the Contents of Informative Documents and its amending rules, and SMV Resolution No. 013-2023-SMV/01 - Standards on the Preparation, Reporting and Communication of Financial Statements, Annual Report and Management Report applicable to entities supervised by the Superintendency of Securities Market.”

Luis Felipe Castellanos López - Torres

Chief Executive Officer

Lima, March 18, 2026

DOCVARIABLE ndGeneratedStamp \* MERGEFORMAT 4903-5206-7992, v. 1

SECTION II

BUSINESS

Intercorp Financial Services Inc. (IFS)

Initially incorporated as Intergroup Financial Services Corp., its name was later changed to Intercorp Financial Services Inc. by resolution of the Extraordinary General Shareholders' Meeting dated June 8, 2012, recorded in Public Deed No. 16,063, dated June 22, 2012, issued before the Tenth Notaries’ Office of the Circuit of Panama, by Ricardo A. Landero M., recorded in Card No. 539106, Redi Document No. 2197803 of the Commercial Section of the Public Records Office of Panama; which was later rectified by Public Deed No. 17,416, dated July 5, 2012, issued before the Tenth Notaries’ Office of the Circuit of Panama, by Ricardo A. Landero M., recorded in Card No. 539106, Redi Document No. 2208035 of the Commercial Section of the Public Records Office of Panama.

The company’s registered office is located at Calle 74, San Francisco Edificio P.H. 909, Piso 15, Panama City, Republic of Panama. The company’s offices in Peru can be reached by phone at + (511) 219-2000 and by fax at +(511) 219-2346.

IFS was incorporated on September 19, 2006, starting operations on January 19, 2007. Its incorporation is recorded in Public Deed No. 22,758 issued before the First Notaries’ Office of the Circuit of Panama, by Boris Barrios Gonzáles, recorded in Card No. 539106, Redi Document No. 1014737 of the Commercial Section of the Public Records Office of Panama. IFS is a limited liability holding company, incorporated as a result of the structure reorganization of its main shareholder Intercorp Perú Ltd. (hereinafter "Intercorp", a holding company incorporated in 1997 in The Bahamas) in 2007.

IFS is part of the following Business Group as of December 31, 2025:

DOCVARIABLE ndGeneratedStamp \* MERGEFORMAT 4903-5206-7992, v. 1

Name of the Group’s Main Companies |

Corporate Purpose of the Group’s Main Companies |

ADMINISTRACIÓN FOOD REGIONAL S.A.C. (previously Servicios Food Retail S.A.C. and previously Back Office Peruana S.A.C.) |

A company engaged in the provision of administrative services. |

AGORA SERVICIOS DIGITALES S.A.C. |

A company engaged in the development, management and operation of digital services, as well as in the retail and/or wholesale purchase and sale of various goods. |

ALAMEDA COLONIAL S.A.C. |

A company engaged in real estate investment. |

ALMACÉN GURÚ PERÚ S.A.C. (En Liquidación) |

A company engaged in managing and executing technological solutions for the marketing of goods and organization of deliveries. |

BANCO INTERNACIONAL DEL PERÚ S.A.A.-INTERBANK |

A multibank. |

BEACON HEALTHCARE S.A.C. |

A company engaged in the investment and investment management in different sectors, including the health sector. |

BOTICAS IP S.A.C. |

Retail sale of pharmaceutical and medicinal products, cosmetics and toiletries |

CALLAO GLOBAL OPPORTUNITIES CORP. |

A company engaged in the investment in the distribution of personal property in general. |

CASH-&-CARRY ECUADOR S.A.S. (In liquidation) |

A company engaged in the development of all types of activities related to the real estate business in Ecuador. |

CENTROS DE SALUD PERUANOS S.A.C. |

A company engaged in the provision of health services, including prevention and recovery services. |

CHELSEA NATIONAL CORP. |

A company engaged in investing in the digital services business. |

COLEGIOS COLOMBIANOS S.A.S. |

A company engaged in the provision of educational services in Colombia. |

COLEGIOS COLOMBIANOS HOLDING S.A.S. |

A holding company of Colegios Colombianos S.A.S. |

COLEGIOS DE ECUADOR COLDEC S.A.S. |

A company engaged in the provision of educational services in Ecuador. |

COLEGIOS PERUANOS S.A. |

A company engaged in the provision of regular basic education services at the pre-school, elementary and high school levels. |

COMPAÑÍA DE SERVICIOS CONEXOS EXPRESSNET S.A.C. |

A company engaged in the credit card operations business. |

COMPAÑÍA FOOD RETAIL S.A.C. |

A company engaged in non-specialized wholesale and retail sales and road freight. |

COMPAÑÍA HARD DISCOUNT S.A.C. |

A company engaged in retail sales in non-specialized stores. |

CORPORACIÓN EDUCATIVA HISPANOAMERICANA S.C. |

A company engaged in the provision of educational services in Mexico. |

DESARROLLADORA DE STRIP CENTERS S.A.C. |

A company engaged in the development of all types of activities related to the real estate business. |

DOCVARIABLE ndGeneratedStamp \* MERGEFORMAT 4903-5206-7992, v. 1

Name of the Group’s Main Companies |

Corporate Purpose of the Group’s Main Companies |

DIGITAL FOOD S.A.C. (formerly JOKR PERU S.A.C.) |

A company involved in managing and implementing technological solutions for commercialization of goods and organization of deliveries. |

DOMUS HOGARES DEL NORTE S.A.C. |

A company engaged in real estate investment. |

EDUCACIÓN 23 S.A.C. |

A company engaged in the provision of higher education (educational and cultural activities) services. |

EMPRESA PRODUCTORA DE ALIMENTOS S.A.C. (formerly SUPERMERCADO SUR DEL PERU S.A.C., INMOBILIARIA FOOD RETAIL S.A.C. and ELECTRO OH! SA.C.) |

A company engaged in retail sales through non-specialized stores. |

FARMACIAS PERUANAS S.A.C. |

A company engaged in the provision of administrative and management services. |

FINANCIERA OH! S.A. |

A company specializing in financial intermediation. |

FOOD RETAIL CHILE SPA (formerly Hard Discount Investments SPA) |

A company engaged in the holding of securities. |

FP MAYORISTA S.A.C. (previously FP SERVICIOS GENERALES S.A.C.) |

A company engaged in providing shared services. |

HOLDING SEH S.A.S. |

A company engaged in the holding of securities. |

HOMECENTERS ECUATORIANOS S.A.S. |

A company engaged in the home improvement business. |

HOMECENTERS PERUANOS ORIENTE S.A.C. |

A company engaged in the home improvement business. |

HOMECENTERS PERUANOS S.A. |

A company engaged in the home improvement business. |

HPSA ECUADOR S.A.S. |

A company engaged in the holding of securities. |

HPSA CORP. |

A company dedicated to investing in the home improvement business. |

IDAT S.A.C. |

A company engaged in higher education services. |

IFH CAPITAL CORP. |

A company engaged in the investment business. |

IFH RETAIL CORP. |

A company engaged in retail investments. |

IFS GLOBAL STRATEGY S.L.U. |

A company engaged in the holding of foreign securities. |

IFS MANAGEMENT S.A.C. (previously IFS DIGITAL S.A.C.) |

A company engaged in providing management services. |

INDIGITAL XP S.A.C. |

A company dedicated to the provision of digital product development services. |

INMOBILIARIA MILENIA S.A. |

A company engaged in real estate activities. |

INMOBILIARIA NEPTUNO INMONEP S.A.S. |

A company engaged in the development of all types of activities related to the real estate business in Ecuador. |

INMOBILIARIA PUERTA DEL SOL S.A.C. |

A company engaged in the business of shopping centers. |

INRETAIL PERÚ CORP. |

A company engaged in investments in retail business. |

INRETAIL PHARMA S.A. |

A company engaged in the pharmaceutical business. |

DOCVARIABLE ndGeneratedStamp \* MERGEFORMAT 4903-5206-7992, v. 1

Name of the Group’s Main Companies |

Corporate Purpose of the Group’s Main Companies |

INRETAIL REAL ESTATE CORP. |

A company engaged in real estate investment. |

INTELIGO BANK LTD. |

Bank authorized to operate by the Commonwealth of the Bahamas. |

INTELIGO GROUP CORP. |

A company engaged in the investment business. |

INTELIGO PERÚ HOLDINGS S.A.C. |

A company dedicated to investments in the financial sector. |

INTELIGO SOCIEDAD AGENTE DE BOLSA S.A. |

A broker-dealer company. |

INTELIGO USA INC. |

A company engaged in the investment business. |

INTERBANK - Peru Representações e Participações Brasil Ltda. |

An Interbank Representative Office in Brazil. |

INTERCORP CAPITAL INVESTMENTS INC. |

A company engaged in the investment business. |

INTERCORP CONNECTIVITY INC. |

A holding company engaged in the investments business |

INTERCORP EDUCATION HOLDINGS S.A. |

A company engaged in education investment (Other financial intermediation n.c.p.). |

INTERCORP EDUCATION SERVICES S.L.U. |

A holding company of Transformando la Educación de México S.A. de C.V. |

INTERCORP FINANCIAL SERVICES INC. |

A holding company in the financial sector. |

INTERCORP MANAGEMENT S.A.C. |

A company engaged in the provision of management services. |

INTERCORP PERÚ LTD. |

A company engaged in the investment business. |

INTERCORP PERÚ TRADING (SHANGHAI) COMPANY LTD. |

A company engaged in the investment business. |

INTERCORP PERÚ TRADING (HONG KONG) COMPANY LTD. |

A company engaged in the investment business. |

INTERCORP RETAIL INC. |

A company dedicated to investments. A parent company in retail investments. |

INTERCORP RETAIL SPAIN CORP. S.L. (formerly HPSA Spain Corp. S.L.U. and Esslemon Invest S.L.) |

A company engaged in the management and administration of securities. |

INTERFONDOS S.A. SOCIEDAD ADMINISTRADORA DE FONDOS |

A company that manages mutual funds and investment funds. |

INTERNACIONAL DE TÍTULOS SOCIEDAD TITULIZADORA S.A. - INTERTÍTULOS |

A securitization company. |

INTERSEGURO COMPAÑÍA DE SEGUROS S.A. |

A company authorized to sell life insurance, general insurance and annuities. |

INVERSIONES REAL STATE S.A.C |

A company engaged in real estate investment. |

IR INTERNATIONAL CORP. S.L. (formerly Highburyland S.L.U.) |

A company engaged in the holding of securities. |

IR MANAGEMENT S.R.L. |

A company engaged in the provision of management services. |

DOCVARIABLE ndGeneratedStamp \* MERGEFORMAT 4903-5206-7992, v. 1

Name of the Group’s Main Companies |

Corporate Purpose of the Group’s Main Companies |

IXP HOLDING CORP. |

A company engaged in the holding of securities. |

IZIPAY S.A.C. |

A company engaged in the provision of payment processing services. |

IZIPAY ECUADOR S.A. |

A company engaged in the provision of auxiliary services in the financial system and provision of services as a manager of the auxiliary payment system. |

JORSA DE LA SELVA S.A.C. |

A company engaged in the wholesale and retail marketing and import of pharmaceutical products. |

LA PUNTA GLOBAL OPPORTUNITIES CORP. |

A company engaged in the investment business. |

LINCE GLOBAL OPPORTUNITIES CORP. |

A company engaged in the investment business. |

MAKRO SUPERMAYORISTA S.A. |

A company engaged in the wholesale of groceries and food products. |

MIFARMA S.A.C. |

A company engaged in the wholesale and retail marketing and import of pharmaceutical products. |

NEGOCIOS E INMUEBLES S.A. |

A company engaged in real estate activities for remuneration. |

NG EDUCATION HOLDINGS CORP. |

A company specialized in investing in educational businesses. |

NG EDUCATION HOLDINGS II CORP. |

A company specialized in investing in educational businesses. |

NG EDUCATION HOLDINGS III CORP. |

A company specialized in investing in educational businesses. |

NG EDUCATION S.A.C. |

A company specialized in investing in educational businesses. |

OPERADORA DE SERVICIOS LOGÍSTICOS S.A.C. |

A company engaged in providing comprehensive logistics services, among others. |

OPORTO INMOBILIARIA S.A.C. |

A company engaged in real estate activities. |

PATRIMONIO EN FIDEICOMISO D.S. 093-2002-EF-INRETAIL CONSUMER |

A trust fund of investment in the retail trade sector. |

PATRIMONIO EN FIDEICOMISO D.S. 093-2002-EF-INRETAIL SHOPPING MALLS |

A trust fund of investment in real estate projects. |

PATRIMONIO EN FIDEICOMISO D.S. 093-2002-EF-INTERPROPERTIES HOLDING |

A trust fund of investment in real estate projects. |

PATRIMONIO EN FIDEICOMISO D.S. 093-2002-EF-INTERPROPERTIES HOLDING II |

A trust fund of investment in real estate projects. |

PATRIMONIO EN FIDEICOMISO D.S. 093-2002-EF-INTERPROPERTIES PERÚ |

A trust fund of investment in real estate projects. |

PINAPP USA LLC |

A company engaged in the investment business. |

PLAZA VEA ORIENTE S.A.C. |

A company engaged in the supermarket business in the Peruvian Amazon rainforest. |

DOCVARIABLE ndGeneratedStamp \* MERGEFORMAT 4903-5206-7992, v. 1

Name of the Group’s Main Companies |

Corporate Purpose of the Group’s Main Companies |

PROCESOS DE MEDIOS DE PAGO S.A. |

A company engaged in the provision of payment processing services. |

PROMOTORA DE LA UNIVERSIDAD TECNOLÓGICA DE CHICLAYO S.A.C. |

A company engaged in the business of education. |

PUNTO DE ACCESO ESPAÑA S.L.U. |

A company engaged in the holding of foreign securities. |

PUNTO DE ACCESO GUATEMALA S.A. |

A company engaged in the telecommunications business. |

PUNTO DE ACCESO HONDURAS II S.A. de C.V. |

A company engaged in the telecommunications business. |

PUNTO DE ACCESO JAMAICA LIMITED |

An internet service provider. |

PUNTO DE ACCESO PERÚ S.A.C. |

A company engaged in the provision of telecommunications services (internet access). |

QUICORP S.A. |

A holding company |

QUIFATEX S.A. |

A company engaged in the marketing and distribution of pharmaceutical and consumer products in Ecuador. |

REAL PLAZA S.R.L. |

A company engaged in the shopping center business. |

SAN BORJA GLOBAL OPPORTUNITIES S.A.C. |

A company engaged in e-commerce. |

SAN MIGUEL GLOBAL OPPORTUNITIES S.A.C. |

A company engaged in real estate investment. |

SERVICIO EDUCATIVO EMPRESARIAL S.A.C. |

A company engaged in the provision of higher education services |

SERVICIOS ADMINISTRATIVOS TRANSFORMANDO LA EDUCACIÓN DE MÉXICO, S.C. |

A company engaged in the provision of educational services in Mexico. |

SOCIEDAD COMERCIALIZADORA DE PRODUCTOS A DETALLE S.A. |

A company engaged in the retail sale in non-specialized commerce. |

SUPERMERCADOS CHILENOS SPA |

A company engaged in, among others, the commercialization of all kind of goods. |

SUPERMERCADOS PERUANOS S.A. |

A company engaged in the business of hypermarkets, supermarkets and other retail formats. |

TIENDAS PERUANAS ORIENTE S.A.C. |

A company engaged in the business of retail marketing of clothing and household goods. |

TIENDAS PERUANAS S.A. |

A company involved in the business of retail marketing of clothing and household goods. |

TRANSFORMANDO LA EDUCACIÓN DE MÉXICO S.A. DE C.V. |

A holding company for Administrative Services Transforming Education in Mexico S.C. |

UNIVERSIDAD TECNOLÓGICA DEL PERÚ S.A.C. |

A company engaged in the provision of higher education services. |

DOCVARIABLE ndGeneratedStamp \* MERGEFORMAT 4903-5206-7992, v. 1

Name of the Group’s Main Companies |

Corporate Purpose of the Group’s Main Companies |

URBI PROPIEDADES S.A.C. |

A company engaged in real estate investment and management. |

URBI PROYECTOS S.A.C. |

A company engaged in activities related to the structuring, management, representation, advisory, consulting, execution, development, operation and/or financing of investment projects. |

VANTTIVE CIA. LTDA. |

Company engaged in the import, export, distribution, and commercialization of all types of products in Ecuador. |

VELTRIA ADVISORS CORP. (formerly ASB Consultores LLC) |

Businesses related to Chapter 607 of the Florida Statutes. |

The amount of paid-in capital stock is US$ 1,122,151,692.60 represented by 115,447,705 shares at an issue price of US$ 9.72 each.

As of December 31, 2025, the main shareholder of IFS is as follows:

Names and surnames |

Number of shares |

Percentage (%) |

Nationality |

Business Group |

Intercorp Perú Ltd.

|

62,012,134 |

53.71% |

Bahamas |

Grupo Intercorp |

At December 31, 2025, the capital stock of IFS was represented by 115,447,705 shares with a market value of US$ 42.36 each on the Lima Stock Exchange, and US$ 42.12 each on the New York Stock Exchange, of which Intercorp Peru Ltd. holds 62,012,134 shares representing 53.71% of the issued capital stock of IFS.

IFS belongs to ISIC 6420, corresponding to companies of "Activities of Holding Company". The corporate purpose of IFS is to serve as holding company for the Financial Division of the Intercorp Group.

DOCVARIABLE ndGeneratedStamp \* MERGEFORMAT 4903-5206-7992, v. 1

The duration of the company is perpetual.

IFS, headquartered in Panama, was established in 2006 as part of the corporate reorganization of Intercorp Group. The reorganization simplified the Group's structure and created IFS to bring together the assets operated by the Group in the Peruvian financial service industry: Interbank and Interseguro.

In June 2007, the initial public offering of IFS shares was successfully completed. The transaction resulted in the implicit valuation of IFS by US$ 1,300 million.

In September 2008, IFS launched a public offering to exchange Interbank shares for IFS shares. Its main goal was to generate greater value for Interbank's minority shareholders. Interbank's float decreased from 3.12% to 0.71%, and IFS shareholding in Interbank increased from 96.88% to 99.29%.

On August 01, 2014, Inteligo Group Corp. was fully acquired by Intercorp Financial Services Inc. as part of a corporate restructuring.

On May 31, 2017, the acquisition of Seguros Sura and Hipotecaria Sura was announced. It was approved on September 28, 2017.

In January 2019, Inteligo wealth management business was reorganized by transferring Interfondos, a mutual funds subsidiary of Interbank, to Inteligo Group, a company primarily focused on asset management.

In July 2019, IFS debuted in the New York Stock Exchange (NYSE) with an initial public offering of approximately nine million shares at US$ 46 per share. The securities were offered by IFS, Interbank, Intercorp Perú and a non-affiliated third party.

In April 2022, IFS completed the acquisition of 50% shareholding in Izipay, which, together with the 50% the bank already owned, gave it the opportunity to develop the payment processing business more strongly.

IFS shares are traded under the “IFS” mnemonic code, both in the Lima Stock Exchange and the New York Stock Exchange. Moreover, IFS has two ticker symbols in Bloomberg, IFS PE and IFS US, one for each market where its shares are traded. To date, approximately 29.38% of IFS shares are traded publicly in Peru and the United States. As of December 31, 2025, Intercorp Perú directly and indirectly holds 53.71% and 70.62% of issued and outstanding IFS capital stock, respectively.

DOCVARIABLE ndGeneratedStamp \* MERGEFORMAT 4903-5206-7992, v. 1

Brief History of Interbank

Interbank was incorporated in Lima, Peru, in 1897, under the business names “Banco Internacional del Perú” and “Interbanc”. International Petroleum Company acquired Interbank in 1944 and held ownership until 1967, when it executed a joint venture agreement with Chemical Bank New York Trust & Co. In 1970, Interbank was transferred to the Peruvian government as part of the banking system reform carried out by the military government of the time. In August 1994, in line with the government's privatization efforts, 91% of Interbank's capital stock was acquired by Corporación Interbanc, which subsequently transferred its Interbank portfolio to Intercorp Perú Ltd. The remaining shares of Interbank's capital stock were sold, mainly to Interbank's employees.

Following the acquisition by Intercorp Perú Ltd. in 1994, Interbank started its operations under the “Interbank” business name in line with its effort to renew the brand and modernize the company. Since then, Interbank continued growing and became one of the main consumer credit providers in Peru, and one of the most innovative banks in the country, mainly focusing on personal bank operations and the development of convenient distribution channels.

Brief History of Interseguro

Interseguro was incorporated in June 16, 1998, from the partnership between Intercorp Group and Bankers Trust. In 2007, Intercorp Group created a financial holding, Intergroup Financial Services Corp., now Intercorp Financial Services Inc. (IFS), consolidating ownership of Interbank, Interseguro and Inteligo. Interseguro is currently one of the main Peruvian insurance firms, specialized in Life Annuities. In addition to its competitive position in the Life Annuity market, Interseguro offers other products, such as life insurance, and low-cost mass insurance sold mainly through Intercorp Group's distribution channels.

Brief History of Inteligo

Inteligo Group Corp. was incorporated under the laws of the Republic of Panama in 2006. It has five subsidiaries: Inteligo Bank Ltd., Inteligo Sociedad Agente de Bolsa, Inteligo Perú Holdings, Inteligo USA and Veltria Advisors Corp.

Incorporated under the laws of the Commonwealth of The Bahamas in 1995, is engaged in the business of financial advisory and wealth management. It is supervised by the Central Bank of The Bahamas and the Securities Commission of The Bahamas. Additionally, it has a branch in Panama, established in 1997, which operates under an international license granted by the Superintendency of Banks of Panama and is also supervised by the Superintendency of the Securities Market of Panama.

DOCVARIABLE ndGeneratedStamp \* MERGEFORMAT 4903-5206-7992, v. 1

Incorporated under the laws of the Republic of Peru in 1996 and operating since 1997 with authorization from the Superintendency of the Securities Market of Peru, the Company’s main activities include the purchase and sale of securities traded in both the exchange and over-the-counter markets, as well as providing advisory services to investors in the securities market..

Incorporated under the laws of the Republic of Peru in 2018, it is the holding company and main shareholder of Interfondos S.A. - Sociedad Administradora de Fondos. Inteligo Perú Holdings provides corporate services to companies of Inteligo Group.

Interfondos was incorporated under the laws of the Republic of Peru in 1994 and acquired by Inteligo Perú Holdings on January 8, 2019. The company's main activity is management of mutual funds and investment funds domiciled in Peru, particularly for local clients. Is supervised by the Superintendency of the Securities Market of Peru.

Incorporated under the laws of the City of New York in 2019, Inteligo USA offers financial services in the United States.

Veltria is a registered investment advisor (Registered Investment Adviser – RIA), established in 2014 and incorporated into Inteligo Group in 2025. It is regulated by the U.S. Securities and Exchange Commission (SEC) and the Financial Industry Regulatory Authority (FINRA). Veltria has an office in the City of Miami and provides customized portfolio management services from the United States.

Macroeconomic Environment

Peru recorded GDP growth of 3.3% in 2025, primarily driven by the strong performance of primary sectors, such as agriculture and mining, as well as manufacturing, construction and trade; and by non-primary sectors, supported by the recovery in domestic demand, as a result of higher consumption and private investment.

Inflation stood at 1.5% in 2025, within the Central Reserve Bank of Peru’s (BCRP) target range. In this context, the BCRP reduced its benchmark interest rate from 5.00% at the end of 2024 to 4.25% at year-end 2025.

Finally, the Peruvian sol appreciated by approximately 10% against the U.S. dollar during 2025.

DOCVARIABLE ndGeneratedStamp \* MERGEFORMAT 4903-5206-7992, v. 1

.

Banking System

Net income of the banking system increased by 37% in 2025, while return on equity (ROE) improved to 19.0% in 2025, above the 15.3% recorded in 2024. Gross loans at the banking system level grew by 5.4% in 2025, exceeding the 0.2% growth reported in 2024.

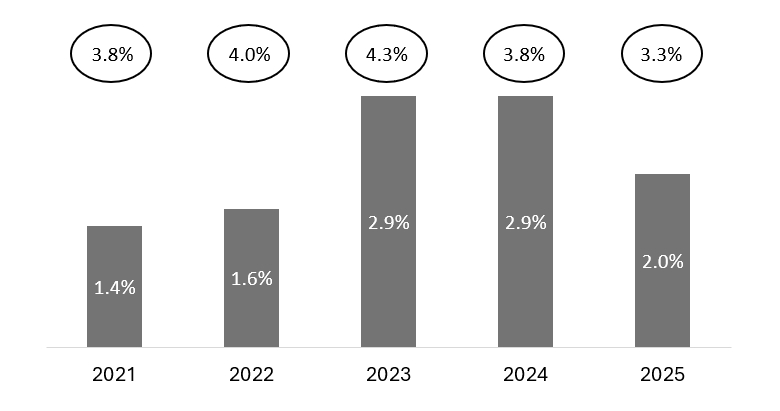

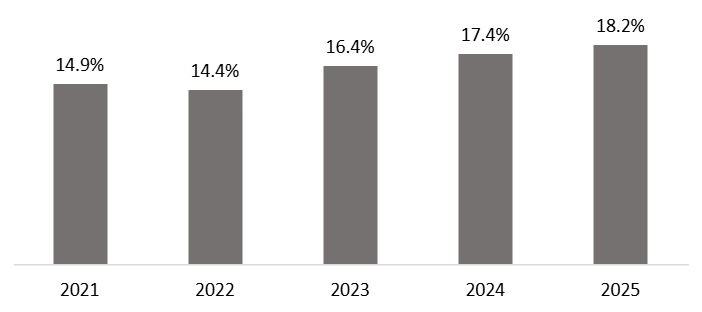

The banking system reduced delinquency levels, ending 2025 at 3.3%, lower than the 3.8% reported in 2024. Meanwhile, the coverage ratio of the system stood at 171.06% in 2025, up from 156.1% in 2024, remaining at healthy levels. Regarding capitalization levels, the system remained solid, closing 2025 at 17.9%, compared to 17.4% in 2024.

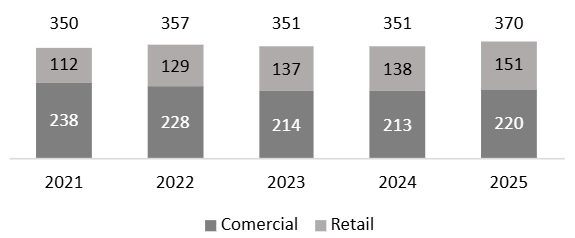

Main Banking System Indicators

Gross Placements (S/ billion)

Source: SBS

DOCVARIABLE ndGeneratedStamp \* MERGEFORMAT 4903-5206-7992, v. 1

Cost of Risk and Default Ratio (%)

Default Ratio

Cost of Risk

Source: SBS

Capitalization (%)

Source: SBS

DOCVARIABLE ndGeneratedStamp \* MERGEFORMAT 4903-5206-7992, v. 1

Peruvian Insurance Market

The Peruvian insurance sector includes 17 companies: six exclusively focused on general insurance, one on life insurance, and ten focused on both categories.

The most representative insurance products, in terms of annual premiums, were Individual Annuities, which accounted for 16.1% of total insurance sales in 2025 and 27.6% of the Life segment. In addition, the industry’s sales mix shows that 58.3% of premiums written corresponded to the Life segment, 31.0% to General Insurance, and 10.8% to Accident and Health Insurance.

Overall, as of year-end 2025, the industry’s return on equity (ROE) was 20.0%, lower than the 24.5% recorded at the end of 2024. Return on assets (ROA) stood at 3.0%, in line with the 3.0% reported in 2024. In the case of Interseguro, return on equity (ROE) was 28.0%, slightly above the 27.9% recorded at year-end 2024, while return on assets (ROA) reached 2.5%, higher than the 2.4% reported in 2024.

Both the industry's and the company's outlook in the medium and long term are favorable, being mainly based on a still low penetration level of insurance in Peru (as a percentage of GDP) as compared to other countries in the region, and on better conditions in financial markets. Similarly, there is room to continue developing new channels and products, as well as bancassurance with Interbank.

Financial Advisory, Wealth Management and Stock Broker Markets

The financial advisory and wealth management businesses are highly competitive. This sector includes local and international companies and, in recent years, it has seen an increase of independent advisors.

Inteligo Bank Ltd.'s main international competitors are UBS and Credit Suisse, among others. The products offered per each asset class include fixed income and variable income instruments, and alternative investments; both in the local and international market.

Inteligo Sociedad Agente de Bolsa provides custody and brokerage services in the Lima Stock Exchange. Interfondos provides mutual fund and investment fund management services in the Peruvian market.

Since 2019, Inteligo USA provides financial advisory and transaction management services in the US market.

As of December 31, 2025 and 2024, IFS owns 99.31% of Interbank's outstanding capital stock, 99.85% of Interseguro Compañía de Seguros S.A.'s outstanding capital stock, and 100.00% of Inteligo Group Corp.'s capital stock. The operations of IFS and its subsidiaries focus on Peru and the Republic of Panama.

DOCVARIABLE ndGeneratedStamp \* MERGEFORMAT 4903-5206-7992, v. 1

The accompanying financial statements reflect the individual activity of IFS, and do not include the effects of the consolidation of these financial statements with those of its subsidiaries, pursuant to the legal provisions and financial reporting standards in Peru.

The separate audited financial statements of IFS are presented below:

DOCVARIABLE ndGeneratedStamp \* MERGEFORMAT 4903-5206-7992, v. 1

Intercorp Financial Services Inc.

Separate Statement of Financial Position

As of December 31, 2025 and 2024

|

2025 |

2024 |

|

S/(000) |

S/(000) |

|

|

|

Asset |

|

|

Current asset |

|

|

Available cash |

314,565 |

181,971 |

Accounts receivable from subsidiary and related party |

1,331 |

1,531 |

Other accounts receivable |

165 |

195 |

Investments at fair value through profit or loss |

179,302 |

156,529 |

|

___________ |

___________ |

Total current asset |

495,363 |

340,226 |

|

|

|

Investments at fair value through other comprehensive profit or loss |

41,487 |

39,966 |

Investments in subsidiaries |

12,848,096 |

11,608,593 |

Other assets |

13,039 |

55,088 |

|

___________ |

___________ |

Total non-current asset |

12,902,622 |

11,703,647 |

|

___________ |

___________ |

|

|

|

Total asset |

13,397,985 |

12,043,873 |

|

___________ |

___________ |

|

|

|

Liability |

|

|

Interests, dividend tax provision, other accounts payable and provisions |

92,514 |

58,977 |

|

___________ |

___________ |

Total current liability |

92,514 |

58,977 |

|

|

|

Corporate bond |

956,880 |

1,069,661 |

|

___________ |

___________ |

Total liability |

1,049,394 |

1,128,638 |

|

|

|

Net equity |

|

|

Capital stock |

1,038,017 |

1,038,017 |

Treasury shares |

(469,546) |

(206,997) |

Capital premium |

532,771 |

532,771 |

Reserves |

9,100,000 |

8,300,000 |

Unrealized gains and losses |

(36,034) |

(187,830) |

Retained earnings |

2,183,383 |

1,439,274 |

|

___________ |

___________ |

Total net equity |

12,348,591 |

10,915,235 |

|

___________ |

___________ |

|

|

|

Total liability and net equity |

13,397,985 |

12,043,873 |

|

___________ |

___________ |

DOCVARIABLE ndGeneratedStamp \* MERGEFORMAT 4903-5206-7992, v. 1

Intercorp Financial Services Inc.

Separate Income Statement

For the years ended on December 31, 2025 and 2024

|

2025 |

2024 |

|

S/(000) |

S/(000) |

|

|

|

Share of profit or loss of Subsidiaries, net |

1,978,644 |

1,383,105 |

|

__________ |

__________ |

|

|

|

(Expenses) income |

|

|

Financial expenses, net |

(48,127) |

(52,238) |

Net gain (loss) in derivative financial instruments for trade |

2,779 |

(239) |

Net gain in valuation of investments at fair value through profit or loss |

81,011 |

34,179 |

General and operating expenses |

(47,377) |

(35,618) |

Exchange difference, net |

5,603 |

(3,442) |

Other income |

17 |

181 |

|

__________ |

__________ |

|

(6,094) |

(57,177) |

|

__________ |

__________ |

Profit before income tax on dividends |

1,972,550 |

1,325,928 |

|

|

|

Provision for income tax on dividends |

(40,080) |

(25,850) |

|

__________ |

__________ |

|

|

|

Net profit for the year |

1,932,470 |

1,300,078 |

|

__________ |

__________ |

|

|

|

Earnings per basic and diluted share (in Soles) |

17.299 |

11.376 |

|

__________ |

__________ |

|

|

|

Weighted average of outstanding shares (in thousand) |

111,713 |

114,287 |

|

__________ |

__________ |

DOCVARIABLE ndGeneratedStamp \* MERGEFORMAT 4903-5206-7992, v. 1

Analysis of the company's separate financial statements 2024

Regarding Intercorp Financial Services' individual performance, net income reached S/ 1,932.5 million in 2025, representing a 48.6% increase compared to 2024. This was mainly driven by a 43.1% increase in the net contribution of subsidiaries' results, as well as a higher valuation of investments at fair value through profit or loss.

Profit or loss of main subsidiaries:

Bank Segment

Interbank’s net income amounted to S/ 1,475 million in 2025, an increase of S/ 467.6 million, equivalent to 46.4% year-over-year.

Annual performance was mainly driven by a reduction of S/ 583.2 million in loan loss provisions, reflecting improved performance across all segments. Other income increased by S/ 106.7 million, primarily due to higher income from foreign exchange transactions and higher valuation of investments. Fee income from financial transactions rose by S/ 92.8 million, mainly explained by higher credit card fees, driven by increased transaction volumes. Results also benefited from an increase of S/ 82.6 million in net interest income, associated with a 40 basis point decrease in the cost of funds, in line with a 12.7% increase in efficient funding.

These effects were partially offset by a S/ 216.3 million increase in income tax expense, driven by a 52.7% increase in pre-tax income, and by a S/ 192.1 million increase in other expenses.

As a result, Interbank’s ROE reached 15.5% in 2025, above the 12.2% reported in 2024.

Interest-Earning Assets

Interbank’s earning assets reached S/ 74,197 million as of December 31, 2025, representing a 5.0% year-over-year increase.

The Bank’s earning asset portfolio is primarily composed of loans, segmented by risk characteristics in accordance with IFRS 9. For impairment loss estimation purposes, the portfolio is grouped into three segments: Retail Banking (consumer and mortgage), Commercial Banking (corporate and middle-market), and Small Business (small and micro enterprises).

Gross loans recorded year-over-year growth, driven by the positive performance of the main segments. Retail banking led growth, while commercial loans expanded at a more moderate pace.

In retail, performance was mainly driven by strong mortgage growth, together with increases in credit cards and personal loans, partially offset by a contraction in

DOCVARIABLE ndGeneratedStamp \* MERGEFORMAT 4903-5206-7992, v. 1

payroll-deducted loans. Credit cards and personal loans continue to represent a significant portion of the total portfolio.

Meanwhile, the commercial portfolio showed mixed performance: strong growth in small and micro enterprises stood out, accompanied by more limited expansion in middle-market companies, while corporate loans recorded a slight decline. From an economic perspective, excluding foreign exchange effects, total loan portfolio growth would have been 6.5%, and commercial loans would have grown by 8.2%, reflecting stronger underlying expansion in business lending.

Funding Structure

The Bank’s total funding increased by 3.1% year-over-year. This was driven by a 4.9% increase in deposits and obligations, partially offset by decreases of 2.6% in due to banks and correspondents and interbank funds, and of 8.1% in bonds, notes and other obligations, the latter mainly impacted by foreign exchange depreciation.

The annual increase in deposits of S/ 2,155.0 million was mainly driven by growth of 8.2% in retail deposits and 2.2% in commercial deposits. By type, savings deposits increased by 13.0% and demand deposits by 3.2%, partially offset by a 2.3% decrease in time deposits. The Bank remains strongly focused on promoting efficient funding, which increased by 12.7% year-over-year.

As of December 31, 2025, deposits and obligations represented 82.9% of total funding, above the 81.5% reported in 4Q25.

Financial Margin

Gross financial margin increased by 2.2%, as a result of a 2.6% decrease in financial income, partially offset by a 10.7% reduction in financial expenses.

Lower financial income was mainly explained by an 18.6% decrease in interest on cash and interbank funds, a 5.1% decline in interest on investments, and a 1.4% decrease in interest on loans.

The reduction in interest on cash was driven by a 70 basis point decrease in the average yield, in line with lower benchmark rates in both soles and U.S. dollars, partially offset by an 8.1% increase in average volume, consistent with higher deposits held at the Central Reserve Bank of Peru (BCRP).

Lower interest on loans was attributable to a 60 basis point decrease in the average yield, partially offset by a 5.2% increase in average volume. The reduction in the average rate was mainly related to lower rates in the retail loan portfolio, in line with the declining interest rate cycle and changes in product mix. As for average volume, this was driven by a 9.5% increase in the commercial portfolio, as well as a 1.5% increase in the retail portfolio. The increase in average volume in the commercial portfolio was related

DOCVARIABLE ndGeneratedStamp \* MERGEFORMAT 4903-5206-7992, v. 1

to higher working capital loans, trade finance placements, and financial lease operations.

The average yield on loans decreased from 10.4% in 2024 to 9.8% in 2025, mainly due to lower implied rates in the consumer and commercial portfolios, while remaining stable in the mortgage portfolio.

As a result of the above, the return on average interest-earning assets decreased by 60 basis points, from 8.4% in 2024 to 7.8% in 2025.

The decrease in financial expenses was mainly explained by a 16.6% reduction in interest and fees on deposits and a 14.1% decrease in interest and fees on borrowings and interbank funds, partially offset by a 22.5% increase in interest and fees on bonds, associated with the subordinated bond issued in January 2025.

The reduction in interest on deposits was driven by a 60 basis point decrease in the average cost, partially offset by a 5.5% increase in average volume. The average cost declined from 2.9% in 2024 to 2.3% in 2025, as a result of lower rates paid on institutional, commercial, and retail deposits, reflecting lower BCRP and international benchmark rates. At the same time, average volume increased due to higher balances of institutional, retail, and commercial deposits.

The average cost of funds decreased by 40 basis points, from 3.4% in 2024 to 3.0% in 2025, driven by the lower implicit cost of borrowings and deposits, as well as an improvement in the funding structure. The share of deposits in total funding increased from 81.5% in 2024 to 82.9% in 2025.

Provisions

The loan provision, net of recoveries, decreased by 33.9% due to lower provisioning requirements in the retail and commercial loan portfolios, driven by improved payment capacity from clients.

Financial Services Fees and Commissions

Net income from financial services increased by 14.7%, driven by higher fees from financial services, as well as higher credit card fees. These effects were partially offset by lower fees from bill collection services and lower fees from contingent operations. The growth in financial services fees was mainly driven by increases in insurance income, transfer and savings services, financial advisory fees, and maintenance fees.

Capitalization

The Bank’s global capital ratio stood at 16.0% as of December 31, 2025, above the 15.8% reported as of December 31, 2024.

DOCVARIABLE ndGeneratedStamp \* MERGEFORMAT 4903-5206-7992, v. 1

As of 4Q25, risk-weighted assets (RWAs) increased by 0.5% quarter-over-quarter, driven by higher capital requirements for credit risk. The increase in credit risk RWAs was mainly attributable to higher RWAs from loans. In turn, regulatory capital increased by 1.9% quarter-over-quarter, driven by net income generated in 4Q25.

The year-over-year increase in the capital ratio was driven by an 8.2% increase in regulatory capital, partially offset by a 7.5% increase in RWAs. The increase in RWAs was the result of higher capital requirements for credit risk, explained by growth in corporate and mortgage lending.

The year-over-year increase in regulatory capital was mainly driven by the capitalization of earnings from fiscal year 2024, net income generated in 2025, as well as improvements in unrealized results from the available-for-sale investment portfolio.

The minimum global capital ratio requirement is 10%. Additionally, the regulator requires capital buffers for conservation, the economic cycle, market concentration, and other risks. As of 4Q25, the total additional requirement amounted to 3.6%, resulting in a total regulatory minimum of 13.6%.

Insurance Segment

Interseguro’s net income reached S/ 274.5 million in 2025, representing an increase of S/ 72.6 million, or 36.0%, compared to 2024.

Annual net income performance was mainly driven by an increase of S/ 150.8 million in other income, primarily related to higher mark-to-market valuations, particularly in real estate investments. In addition, insurance results improved by S/ 122.0 million, driven by higher CSM release in life insurance and annuities, as well as improved performance of the Disability and Survivorship (D&S) portfolio, acquired through a two-year bidding process from the Peruvian private pension system.

Furthermore, increases of S/ 45.1 million in translation gains were recorded, in line with exchange rate movements, and of S/ 19.8 million in net interest income, mainly related to higher dividends received. These effects were partially offset by impairment losses on financial investments in Rutas de Lima and Telefónica del Perú amounting to S/ 218.2 million.

As a result, Interseguro’s ROE was 39.5% in 2025, compared to 41.6% in 2024.

Wealth Management Segment

Inteligo’s net income amounted to S/ 231.1 million in 2025, an increase of S/ 93.8 million compared to the previous year.

This growth was mainly driven by higher mark-to-market gains on proprietary portfolio investments, which increased by S/ 77.3 million, as well as by a S/ 25.0 million increase in fee income. The latter was primarily supported by the strong performance of

DOCVARIABLE ndGeneratedStamp \* MERGEFORMAT 4903-5206-7992, v. 1

Interfondos, the local mutual fund subsidiary, whose revenues grew in line with a 31.9% expansion in assets under management (AUM). These positive effects were partially offset by a S/ 8.2 million decrease in net interest income, mainly due to lower yields on balances with banks and on interbank funds and loans.

From a business development perspective, Inteligo’s client acquisition initiatives continued to deliver solid results, reflected in sustained growth in new account openings and AUM across both Private Wealth Management and mutual funds, as well as in the acquisition of Veltria, a firm focused on providing services to high-net-worth families. As of December 31, 2025, total AUM increased by 17.2% year-over-year in U.S. dollar terms.

Inteligo’s return on equity (ROE) stood at 21.5% in 2025, above the 14.2% reported in 2024.

As of December 31, 2025, IFS does not have its own personnel, since its operations are carried out by personnel from the different subsidiaries of Intercorp Group.

IFS has not received any relevant loans during fiscal year 2024.

2.2.3.6 Judicial, administrative or arbitration proceedings

IFS is not involved in any judicial, administrative or arbitration proceedings that could be considered to have a significant impact on IFS results of operations and financial position.

Interbank is involved in a number of legal proceedings in the ordinary course of its banking operations. In addition, Interbank has legal proceedings related to labor discrepancies with former employees and tax discrepancies with the tax authority.

Interseguro is routinely involved in legal and/or arbitration proceedings in connection with claims that are routinely made in relation to policy coverage. These liabilities are taken into account for the constitution of Interseguro’s technical reserves.

Inteligo Bank Ltd. Is involved in legal proceedings in the ordinary course of its banking business.

Bachelor's Degree in Social Sciences – University of California, Berkeley

DOCVARIABLE ndGeneratedStamp \* MERGEFORMAT 4903-5206-7992, v. 1

Master of Business Administration – Dartmouth College

Chairman of the Board

Since 2007

Bachelor’s Degree in Economics – Universidad del Pacífico

Master in Business Management – Universidad de Piura

Master in Business Administration– University of Birmingham

Since 2019

Bachelor’s Degree in Economics – Universidad del Pacífico

Master in Finance – The American University

Master in Economics – University of Pittsburgh

Since 2007

Attorney-at-Law – Pontificia Universidad Católica del Perú

Master’s Degree in Business Administration – Universidad Adolfo Ibañez, Chile.

Since 2019

Bachelor’s Degree in Economics – Universidad del Pacífico

Ph.D. – Washington University, St. Louis

Since 2019

Bachelor’s Degree in Economics – Universidad Católica de Chile

Master in Business Administration – Chicago University

Master in Economics – London School of Economics

Since 2019

Bachelor’s Degree in Economics – Universidad del Pacífico

Master in Business Administration – Stanford Graduate School of Business

Since 2025

CEO

Bachelor’s Degree in Business Administration – Universidad del Pacífico

Master in Business Administration – Dartmouth College

D/CEO

DOCVARIABLE ndGeneratedStamp \* MERGEFORMAT 4903-5206-7992, v. 1

Bachelor’s Degree in Business Administration – Universidad del Pacífico

Master in Business Administration – Harvard University

Chief Financial Officer

Bachelor’s Degree in Business Administration – Universidad de Lima

Master in Business Administration – SDA Bocconi

Legal Department Manager and Stock Exchange Representative

Attorney-at-Law – Pontificia Universidad Católica del Perú

L.L.M Master in Law – University of Virginia

Master in Business Management– Universidad Adolfo Ibañez, Chile

Chief Accountant

Accountant– Pontificia Universidad Católica del Perú

Master in Business Administration – INCAE Business School

Investor Relations Officer

Bachelor’s Degree in Economics – Universidad de Lima

Master in Finance – London Business School

Chief Compliance Officer

Bachelor’s Degree in Business Administration – Florida International University

Master in Business Administration – Nova Southeastern University

Internal Auditor

Bachelor’s Degree in Economics – Universidad del Pacífico

Master in Business Administration – Cornell University

Sustainability Officer

Bachelor’s Degree in Law – Universidad Católica Andrés Bello

Master in Comparative Jurisprudence – New York University

Master in International Banking Law – Morin Center for Banking and Financial Law at Boston University

Master in Business Administration – Management School at Universidad de Piura

DOCVARIABLE ndGeneratedStamp \* MERGEFORMAT 4903-5206-7992, v. 1

SECTION III

FINANCIAL INFORMATION

3.1. Management's Discussion and Analysis of the Results of Operations and the Economic-Financial Situation

The profit sharing of Subsidiaries in 2025 shows an increase of 43.1% compared to those in 2024.

Intercorp Financial Services Inc.

Audited Income Statement

For the years ended on December 31, 2025 and 2024

|

|

|

|

2025 |

2024 |

|

S/(000) |

S/(000) |

|

|

|

Share of profit or loss of Subsidiaries, net |

1,978,644 |

1,383,105 |

|

__________ |

__________ |

|

|

|

(Expenses) income |

|

|

Financial expenses, net |

(48,127) |

(52,238) |

Net gain (loss) in derivative financial instruments for trade |

2,779 |

(239) |

Net gain in valuation of investments at fair value through profit or loss |

81,011 |

34,179 |

General and operating expenses |

(47,377) |

(35,618) |

Exchange difference, net |

5,603 |

(3,442) |

Other income |

17 |

181 |

|

__________ |

__________ |

|

(6,094) |

(57,177) |

|

__________ |

__________ |

Profit before income tax on dividends |

1,972,550 |

1,325,928 |

|

|

|

Provision for income tax on dividends |

(40,080) |

(25,850) |

|

__________ |

__________ |

|

|

|

Net profit for the year |

1,932,470 |

1,300,078 |

|

__________ |

__________ |

|

|

|

Earnings per basic and diluted share (in Soles) |

17.299 |

11.376 |

|

__________ |

__________ |

|

|

|

Weighted average of outstanding shares (in thousand) |

111,713 |

114,287 |

|

__________ |

__________ |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

DOCVARIABLE ndGeneratedStamp \* MERGEFORMAT 4903-5206-7992, v. 1

SECTION IV

ANNEX I

Information regarding monthly quotations for 2025 on the Lima Stock Exchange 1:

Year-Month |

Opening |

Closing |

Maximum |

Minimum |

January |

29.43 |

29.50 |

29.94 |

29.43 |

February |

31.92 |

32.00 |

32.00 |

31.79 |

March |

33.55 |

33.33 |

33.55 |

33.33 |

April |

33.50 |

33.50 |

33.50 |

33.50 |

May |

34.95 |

34.95 |

34.95 |

34.95 |

June |

37.65 |

37.80 |

37.80 |

37.65 |

July |

35.93 |

36.17 |

36.17 |

35.93 |

August |

39.78 |

39.90 |

39.90 |

39.78 |

September |

40.00 |

40.00 |

40.00 |

40.00 |

October |

42.90 |

43.00 |

43.00 |

42.90 |

November |

39.01 |

40.00 |

40.00 |

39.01 |

December |

42.20 |

42.12 |

42.20 |

42.12 |

Information regarding monthly quotations for 2025 on the New York Stock Exchange 2:

Year-Month |

Opening |

Closing |

Maximum |

Minimum |

January |

29.65 |

29.78 |

30.00 |

29.44 |

February |

31.98 |

32.04 |

32.12 |

31.64 |

March |

33.12 |

33.13 |

33.30 |

32.86 |

April |

33.60 |

33.87 |

33.95 |

33.25 |

May |

35.20 |

34.61 |

35.20 |

34.20 |

June |

37.80 |

38.13 |

38.15 |

37.48 |

July |

35.88 |

36.06 |

36.35 |

35.88 |

August |

39.98 |

39.72 |

40.02 |

39.68 |

September |

40.10 |

40.34 |

40.44 |

39.73 |

1 Maximums and minimums considering the close of each day of the month.

2 Maximums and minimums considering the close of each day of the month.

DOCVARIABLE ndGeneratedStamp \* MERGEFORMAT 4903-5206-7992, v. 1

October |

42.81 |

43.03 |

43.34 |

42.60 |

November |

40.39 |

40.29 |

40.50 |

40.15 |

December |

42.02 |

42.36 |

42.40 |

41.90 |

DOCVARIABLE ndGeneratedStamp \* MERGEFORMAT 4903-5206-7992, v. 1

REPORT ON SHAREHOLDING STRUCTURE PER TYPE OF INVESTOR (10190)

INTERCORP FINANCIAL SERVICES INC. Name:

2025Year:

METHODOLOGY:

The information to be submitted refers to those shares or securities representing equity of the Company that have been part of the S&P/BVL Peru Select Index, according to the information disclosed on the website of the Lima Stock Exchange at the end of the year reported.

The composition of the shareholding structure per type of shareholder must be indicated by the Company for each share or security representative thereof, belonging to the aforementioned index.

IFS

Share: [ISIN code o mnemonic code of equity]

Holding per type of shareholders of the share or equity security comprising the S&P/BVL Perú Select Index (at year-end) |

Number of shareholders |

% of ownership3 |

1. Members of the board of directors and senior management of the company, including relatives1. |

2 |

0.03% |

2. Employees of the company, not included in item 1 above. |

- |

0.00% |

3. Individuals, not included in items 1 and 2. |

1,200 |

0.74% |

4. Pension funds managed by Pension Fund Administrators under the supervision of the Superintendence of Banking, Insurance, and Pension Funds. |

3 |

1.94% |

DOCVARIABLE ndGeneratedStamp \* MERGEFORMAT 4903-5206-7992, v. 1

5. Pension fund administered by the Pension Standardization Bureau (ONP in Spanish) |

- |

0.00% |

6. Peruvian State Entities, except for the case included in item 5. |

- |

0.00% |

7. Banks, financial institutions, municipal savings and loan associations, small and medium-sized enterprises (EDPYMES), rural savings and loan associations and savings and loan cooperatives under the supervision of the Superintendence of Banking, Insurance and Pension Fund Management |

2 |

0.04% |

8. Insurance companies under supervision of the Superintendence of Banking, Insurance and Pension Funds. |

- |

0.00% |

9. Brokerage agents, under the supervision of the SMV. |

- |

0.00% |

10. Investment funds, mutual funds and trust funds within the scope of the Securities Market Law and the Investment Funds and bank trusts Law within the scope of the General Law of the Financial System. |

9 |

0.17% |

11. Autonomous estates and banking trusts abroad, to the extent that they can be identified. |

- |

0.00% |

12. Foreign depositaries listed as holders of the share in the ADR or ADS programs. |

- |

0.00% |

13. Foreign depositaries listed as holders of shares not included in item 12. |

1 |

26.02% |

14. Foreign custodians listed as shareholders |

- |

0.00% |

15. Entities not included in the preceding items2. |

19 |

71.06% |

16. Shares belonging to the S&P/BVL Perú Select Index or a security representing these shares in the company's portfolio. |

1 |

0.00% |

Total |

1,237 |

100.0% |

Holding by holders of the shares or representative equity securities comprising the S&P/BVL Peru Select Index, according to residence (at year-end) |

Number of shareholders |

% of ownership 3 |

Domiciled |

1,204 |

2.87% |

Non-domiciled |

33 |

97.13% |

Total |

1,237 |

100.0% |

DOCVARIABLE ndGeneratedStamp \* MERGEFORMAT 4903-5206-7992, v. 1

DOCVARIABLE ndGeneratedStamp \* MERGEFORMAT 4903-5206-7992, v. 1