Please wait

GUERNSEY POWER HOLDINGS, LLC

AND SUBSIDIARY

Consolidated Financial Statements

December 31, 2024

(With Independent Auditors’ Report Thereon)

[KPMG LOGO]

KPMG LLP

Suite 4000

1735 Market Street

Philadelphia, PA 19103-7501

Independent Auditors’ Report

The Member

Guernsey Power Holdings, LLC and Subsidiary:

Opinion

We have audited the consolidated financial statements of Guernsey Power Holdings, LLC and its Subsidiary (the Company), which comprise the consolidated balance sheet as of December 31, 2024, and the related consolidated statements of operations, member’s capital, and cash flows for the year then ended, and the related notes to the consolidated financial statements.

In our opinion, the accompanying consolidated financial statements present fairly, in all material respects, the financial position of the Company as of December 31, 2024, and the results of its operations and its cash flows for the year then ended in accordance with U.S. generally accepted accounting principles.

Basis for Opinion

We conducted our audit in accordance with auditing standards generally accepted in the United States of America (GAAS). Our responsibilities under those standards are further described in the Auditors’ Responsibilities for the Audit of the Consolidated Financial Statements section of our report. We are required to be independent of the Company and to meet our other ethical responsibilities, in accordance with the relevant ethical requirements relating to our audit. We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinion.

Responsibilities of Management for the Consolidated Financial Statements

Management is responsible for the preparation and fair presentation of the consolidated financial statements in accordance with U.S. generally accepted accounting principles, and for the design, implementation, and maintenance of internal control relevant to the preparation and fair presentation of consolidated financial statements that are free from material misstatement, whether due to fraud or error.

In preparing the consolidated financial statements, management is required to evaluate whether there are conditions or events, considered in the aggregate, that raise substantial doubt about the Company’s ability to continue as a going concern for one year after the date that the consolidated financial statements are issued.

Auditors’ Responsibilities for the Audit of the Consolidated Financial Statements

Our objectives are to obtain reasonable assurance about whether the consolidated financial statements as a whole are free from material misstatement, whether due to fraud or error, and to issue an auditors’ report that includes our opinion. Reasonable assurance is a high level of assurance but is not absolute assurance and therefore is not a guarantee that an audit conducted in accordance with GAAS will always detect a material misstatement when it exists. The risk of not detecting a material misstatement resulting from fraud is higher than for one resulting from error, as fraud may involve collusion, forgery, intentional omissions, misrepresentations, or the override of internal control. Misstatements are considered material if there is a substantial likelihood that, individually or in the aggregate, they would influence the judgment made by a reasonable user based on the consolidated financial statements.

In performing an audit in accordance with GAAS, we:

•Exercise professional judgment and maintain professional skepticism throughout the audit.

•Identify and assess the risks of material misstatement of the consolidated financial statements, whether due to fraud or error, and design and perform audit procedures responsive to those risks. Such procedures include examining, on a test basis, evidence regarding the amounts and disclosures in the consolidated financial statements.

•Obtain an understanding of internal control relevant to the audit in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the Company’s internal control. Accordingly, no such opinion is expressed.

•Evaluate the appropriateness of accounting policies used and the reasonableness of significant accounting estimates made by management, as well as evaluate the overall presentation of the consolidated financial statements.

•Conclude whether, in our judgment, there are conditions or events, considered in the aggregate, that raise substantial doubt about the Company’s ability to continue as a going concern for a reasonable period of time.

We are required to communicate with those charged with governance regarding, among other matters, the planned scope and timing of the audit, significant audit findings, and certain internal control related matters that we identified during the audit.

/s/KPMG LLP

Philadelphia, Pennsylvania

September 12, 2025

GUERNSEY POWER HOLDINGS, LLC

AND SUBSIDIARY

Consolidated Balance Sheet

December 31, 2024

(Dollars in thousands)

GUERNSEY POWER HOLDINGS, LLC

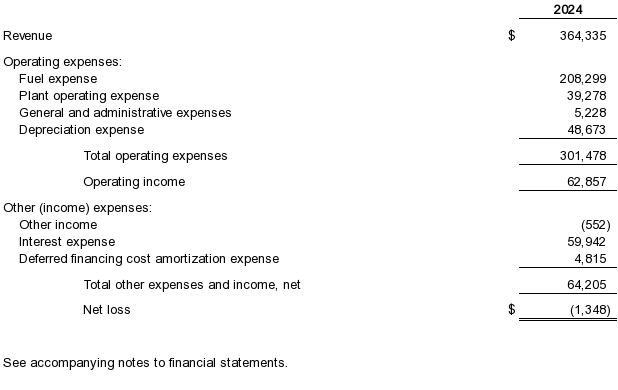

AND SUBSIDIARY

Consolidated Statement of Operations

Year ended December 31, 2024

(Dollars in thousands)

GUERNSEY POWER HOLDINGS, LLC

AND SUBSIDIARY

Consolidated Statement of Member’s Capital

Year ended December 31, 2024

(Dollars in thousands)

GUERNSEY POWER HOLDINGS, LLC

AND SUBSIDIARY

Consolidated Statement of Cash Flows

Year ended December 31, 2024

(Dollars in thousands)

GUERNSEY POWER HOLDINGS, LLC

AND SUBSIDIARY

Notes to Consolidated Financial Statements

December 31, 2024

(Dollars in thousands)

(1)Organization and Operation of the Company

Guernsey Power Holdings, LLC (GPH or the Company) was formed on July 12, 2016, as a Delaware limited liability company, to act as a holding company for Guernsey Power Station, LLC (the Project Company), which was formed to develop, finance, construct, own, and operate a gas-fired combined-cycle power generation facility with a capacity of approximately 1,875 MW located in Guernsey County, Ohio (the Project or Facility). The Company is wholly owned by Caithness Apex Guernsey, LLC (Member), and is governed by a limited liability company agreement that contains customary industry terms.

On August 29, 2019, Caithness Guernsey Holdings, LLC (CGH) an indirect owner of the Company made non-cash contributions to the Company in an amount equal to $19,873, which consisted of (i) $16,664 which represented the amount owed to CGH in accordance with the Project Development Loan and Development Service Agreement (DSA), which was deemed repaid in full at that time and (ii) $2,000, which was a special distribution that was simultaneously contributed to CGH per the DSA and (iii) $1,209 for additional project development cost. All those costs were recorded at their historical amounts.

The Project Company began development of the Project during 2016 and achieved commercial operations on May 1, 2023. The Project Company secured all land rights, interconnection and transmission rights, and material permits (which are non-appealable) required for construction. The Project Company also executed multiple contracts, including, but not limited to, the following: the Operation and Maintenance Agreement (OMA), Purchase of Power Generation Equipment and Related Services (ESA), the Assignment, Assumption and Consent Agreement, Contractual Service Agreement (CSA), Firm Gas Transportation Agreements (GTA), Contracts for the Sale and Purchase of Natural Gas (GSA), and the Engineering Procurement and Construction Contract (EPC) (note 8).

On August 29, 2019, the Company along with its owners entered into an Equity Contribution Agreement and Guarantee (ECCA) that established guarantees to provide additional funding for the project to reach completion. These contributions which ended on March 30, 2023, along with the Project Debt (note 5) were used to fund the construction of the Facility.

(2)Summary of Significant Accounting Policies

(a)Basis of Accounting and Presentation

The accompanying consolidated financial statements have been prepared in accordance with U.S. generally accepted accounting principles (U.S. GAAP) and reflects all adjustments, which the Company believes are necessary to fairly present the consolidated financial position, results of operations, and cash flows of the Company for the year ended December 31, 2024.

(b)Reclassifications and Immaterial Error Corrections

The Company identified immaterial errors in the presentation of unrealized gains and losses in previously issued financial statements that have been corrected.

(c)Principles of Consolidation

The accompanying consolidated financial statements include the accounts of the Company and its wholly owned subsidiary. All intercompany balances and transactions have been eliminated in consolidation.

(d)Accounts Receivable and Revenue Recognition

Accounts receivable primarily consist of receivables from PJM Interconnection, LLC (PJM) for capacity, energy, and ancillary services payments. The Company also has receivables from sales from commodity contracts. The Company earns merchant revenue for incremental capacity, energy, and ancillary services provided to PJM. Merchant capacity, energy, and ancillary services revenue is recorded as electricity sales at the end of each operating period based upon energy delivered and services provided during the period.

GUERNSEY POWER HOLDINGS, LLC

AND SUBSIDIARY

Notes to Consolidated Financial Statements

December 31, 2024

(Dollars in thousands)

In the normal course of business, the Company has future performance obligations for capacity sales awarded through market-based capacity auctions and (or) for capacity sales under bilateral contractual arrangements.

The PJM Base Residual Auction (BRA) for the 2025/2026 PJM Capacity Year was held in July 2024. The Company cleared a total of 1,395 MW at a clearing price of $269.92 per MW-day for the PJM RTO locational delivery areas.

As of December 31, 2024, the expected future period capacity revenues subject to unsatisfied or partially unsatisfied performance obligations were:

The PJM BRA for delivery year 2026/2027 was held in July 2025. The Company cleared a total of 1,323 MW at a clearing price of $329.17 per MW-day.

The Company’s revenue includes sales from commodity contracts with Large Creditworthy Financial Institutions (collectively known as Power Swaps), that are accounted for under ASC 815, Derivatives and Hedging (ASC 815). Revenue from commodity contracts primarily relates to forward sales of commodities merchant energy prices, which are accounted for as derivatives at fair value under ASC 815. These forward sales meet the definition of a derivative under ASC 815 as they have an underlying (e.g. the price of gas), a notional amount (e.g. tons), no initial net investment and can be net settled since the commodity is readily convertible to cash. Revenue from commodity contracts is recognized in Electricity sales for the contracted amount when the contracts are settled at a point in time by transferring control of the commodity to the customer, similarly to revenue recognized from contracts with customers under ASC 606. From inception through settlement, these forward sales arrangements are recorded at fair value under ASC 815 with unrealized gains and losses recognized in the respective statement of operations caption and carried on the consolidated balance sheet as assets or liabilities (see Note 6: Derivative Instruments and Hedging Activities), respectively. Further information about the fair value of these contracts is presented in Note 4: Fair Value Measurements.

The following table represents merchant capacity, energy, ancillary services sales, realized and unrealized gain (loss) on commodity contracts at December 31, 2024.

GUERNSEY POWER HOLDINGS, LLC

AND SUBSIDIARY

Notes to Consolidated Financial Statements

December 31, 2024

(Dollars in thousands)

(e)Cash and Cash Equivalents

The Company considers all liquid investments purchased with an original maturity of three months or less to be cash equivalents. The carrying amount of these instruments approximates fair value because of their short-term maturity.

(f)Restricted Cash

Restricted cash and investments are short term in nature and are specifically designated for the Company’s obligations, as defined in the Project Debt footnote (note 5). Restricted cash represents amounts that are required to be maintained in separate accounts in connection with the Project Debt, significant scheduled construction requirements, and for other general purposes.

All funds are held in highly rated money market accounts, and the carrying value approximates fair value as of December 31, 2024.

(g)Income Taxes

The Company and the Project Company are each disregarded entities for tax purposes. Accordingly, any effect of income taxes is recognized at their indirect parent.

(h)Use of Estimates

The preparation of the consolidated financial statements in conformity with U.S. GAAP requires management to make estimates and assumptions that affect the reported amounts of assets, liabilities, and member’s capital and disclosure of contingent assets and liabilities at the date of the consolidated financial statements and the reported amounts of revenue, expenses, and allocation of profits and losses during the reporting period. Actual results could differ from those estimates. The Company is unaware of any change of conditions or situations that would cause any material change in estimates used to prepare the consolidated financial statements.

(i)Leases

The Company accounts for leases in accordance with Topic 842. The Company reviews its arrangements at contract inception to determine if it is or contains a lease. As of December 31, 2024 the Company has not entered into any material leases.

(j)Asset Retirement Obligations

The Company has no legal or constructive obligations related to the closure of the Facility, and accordingly, no asset retirement obligation is recorded in the consolidated financial statements.

(k)Impairment of Long-Lived Assets

Long-lived assets, such as property, plant, and equipment, and purchased intangibles that are subject to amortization, are reviewed for impairment whenever events or changes in circumstances indicate that the carrying amount of an asset may not be recoverable. Recoverability of assets to be held and used is measured by a comparison of the carrying amount of an asset to estimated undiscounted future cash flows expected to be generated by the asset. If the carrying amount of an asset exceeds its estimated future cash flows, an impairment charge is recognized by the amount by which the carrying amount of the asset exceeds fair value of the asset. Assets to be disposed of would be separately presented in the consolidated balance sheets and reported at the lower of the carrying amount or fair value less costs to sell and are not depreciated. The assets and liabilities of a disposed group classified as held-for-sale would be presented separately in the appropriate asset and liability sections of the consolidated balance sheets.

GUERNSEY POWER HOLDINGS, LLC

AND SUBSIDIARY

Notes to Consolidated Financial Statements

December 31, 2024

(Dollars in thousands)

(l)Fair Value of Financial Instruments

The carrying amounts of cash and cash equivalents, restricted cash, accounts payable, accrued liabilities, other long-term liabilities and amounts due to related parties approximated fair value as of December 31, 2024 because of the relatively short-term maturity of these instruments. The fair value of debt instruments is disclosed in note 4.

(m)Deferred Financing Costs and Amortization Expense

Deferred financing costs represent costs related to the issuance of the Project Debt (note 5) and are amortized using the effective-interest method over the term of the Notes. Deferred financing costs have been netted against Project Debt, which at December 31, 2024 consist of the following:

For the year ended December 31, 2024, the Company incurred amortization expense of $4,815, which was expensed on the consolidated statement of operations.

(n)Derivative and Hedging Activities

The Company recognizes derivative instruments as either assets or liabilities in the consolidated balance sheets at their respective fair values unless they qualify for the normal purchase-normal sale exemption. These instruments are reported gross on the Company's balance sheet. The Company uses derivative instruments to manage its exposure to interest rate risk and merchant power price risk and does not hold or issue derivatives for speculative or trading purposes.

The Company did not elect hedge accounting from inception for all its derivatives. The Company carries the derivatives at their fair value on the consolidated balance sheets and recognizes any subsequent changes in their fair value in earnings.

(o)Concentration of Credit Risk

Financial instruments that potentially subject the Company to concentrations of credit risk consist of accounts receivable, which are concentrated within the energy industry and derivative financial instruments with large creditworthy financial institutions. These industry concentrations may impact the Company’s overall exposure to credit risk, either positively or negatively, in that the customers may be similarly affected by changes in economic, industry or other conditions. Receivables and other contractual arrangements are subject to collateral requirements under the terms of enabling agreements. However, the Company believes that the credit risk posed by industry concentration is offset by the diversification and creditworthiness of its potential customer base. As of December 31, 2024, substantially all the Company’s revenue and accounts receivable is with one counterparty.

(p)Property, Plant, and Equipment, Net

The Company’s property, plant, and equipment are stated at cost net of accumulated depreciation. Depreciation is recorded on a straight-line basis over the estimated useful life of the related assets.

GUERNSEY POWER HOLDINGS, LLC

AND SUBSIDIARY

Notes to Consolidated Financial Statements

December 31, 2024

(Dollars in thousands)

The following table provides the depreciable lives used for each asset class:

(q)Materials and Supplies

Materials and supplies in the amount of $1,090 as of December 31, 2024, are stated at the lower of the average cost or net realizable value. The Material and Supplies are included in Prepaid Expenses and Other Assets on the Company's consolidated balance sheet.

(r)Interest Expense

Interest payments are reported as interest expense on the consolidated statements of operations. Total interest expense was $59,942 as of December 31, 2024. Interest expense includes interest on debt, commitment fees, interest rate swap settlements, and corresponding changes in fair value. The interest rate swaps are derivative financial instruments and are recorded on the consolidated balance sheets at fair value.

(3)Property, Plant, and Equipment, Net

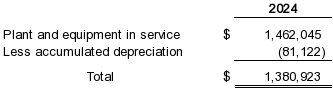

Property, plant and equipment, net at December 31, 2024 consist of the following:

Depreciation expense was $48,673 for the year ended December 31, 2024.

(4)Fair Value Measurement

ASC Topic 820, Fair Value Measurement, establishes a fair value hierarchy that prioritizes the inputs to valuation techniques used to measure fair value. The hierarchy gives the highest priority to unadjusted quoted prices in active markets for identical assets or liabilities (Level 1 measurements) and the lowest priority to measurements involving significant unobservable inputs (Level 3 measurements).

Assets and liabilities measured at fair value on a recurring basis as of December 31, 2024 are summarized below under the three-level hierarchy established by ASC Topic 820, which defines the levels within the hierarchy as follows:

•Level 1 – assets or liabilities whose value is based on unadjusted quoted prices in active markets at the measurement date

•Level 2 – assets or liabilities valued using industry standard models and based on prices, other than quoted prices within Level 1, that are either directly or indirectly observable as of the measurement date

•Level 3 – assets or liabilities whose fair value is estimated based on internally developed models or methodologies using inputs that are generally less readily observable and supported by little, if any, market activity at the measurement date.

GUERNSEY POWER HOLDINGS, LLC

AND SUBSIDIARY

Notes to Consolidated Financial Statements

December 31, 2024

(Dollars in thousands)

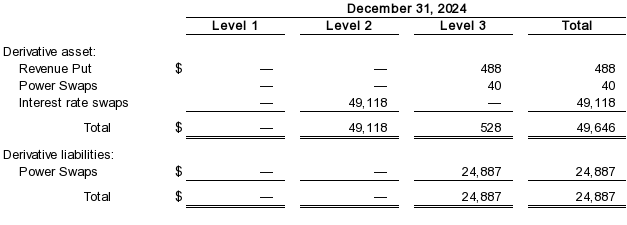

The following tables set forth by level within the fair value hierarchy the financial assets and liabilities that were accounted for at fair value on a recurring basis as of December 31, 2024. These financial assets and liabilities are classified in their entirety based on the lowest level of input that is significant to the fair value measurement. The Company’s assessment of the significance of a particular input to the fair value measurement requires judgment and may affect the fair value of assets and liabilities and their placement within the fair value hierarchy levels, as follows:

The valuation techniques used to measure the fair value of the Level 2 Interest Rate Swaps above in which the counterparties have high credit ratings were derived using the income approach from discounted cash flow pricing models, with all significant inputs derived from or corroborated by observable market data. The Company’s discounted cash flow techniques use observable market inputs, such as LIBOR-based yield curves in the past and SOFR-based yield curves going forward.

The Power swaps referenced above have been designated as Level 3 derivative financial instruments due to their illiquidity. The power node in which the Company delivers energy has no broker or InterContinental Exchange quotes available, no bid/ask from brokers and no information on where broker last saw inter and intra-market spreads and their knowledge of year-on-year calendar spreads. The power node prices for the Company are derived by assessing more liquid zones for correlation, basis in the Fixed Transmission Rights market, and forward projections based on historical assessment. The power swaps have been entered into with counterparties with high credit ratings.

The Revenue Put referenced above have been designated as a Level 3 derivative financial instrument due to its illiquidity.

(a)Additional Information Regarding Level 3 Measurements

For valuations that include both observable and unobservable inputs, if the unobservable input is determined to be significant to the overall inputs, the entire valuation is categorized in Level 3. This includes derivatives valued using indicative price quotations for contracts with tenors that extend into periods with no observable pricing. The Company would include the Revenue Put, which, given the inputs listed below, would have a

GUERNSEY POWER HOLDINGS, LLC

AND SUBSIDIARY

Notes to Consolidated Financial Statements

December 31, 2024

(Dollars in thousands)

direct impact on the fair value if they were adjusted. For the year ended December 31, 2024, the significant unobservable inputs used in the fair value measurement of the Revenue Put Option are as follows:

The following table presents the activity for the Revenue Put Option for the year ended December 31, 2024:

(b)Valuation Techniques

The fair value measurement accounting guidance describes three main approaches to measuring the fair value of assets and liabilities: (1) market approach, (2) income approach, and (3) cost approach. The market approach uses prices and other relevant information generated from market transactions involving identical or comparable assets or liabilities. The income approach uses valuation techniques to convert future amounts to a single present value amount. The measurement is based on current market expectations of the return on those future amounts.

The Company measures its interest rate swaps, power derivatives and revenue put at fair value on a recurring basis. The fair value of its interest rate swap derivatives is determined using the income approach by a third-party service provider. The service provider utilizes a standard model and observable inputs to estimate the fair value of the interest rate swaps. The Company performs analytical procedures and makes comparisons to other third-party information in order to assess the reasonableness of the fair value. The fair value of its Revenue Put Option is determined using the income approach based on externally developed models and methodologies utilizing significant inputs that are less readily observable from objective sources. The Company performs analytical procedures and makes comparisons to third-party information when available in order to assess the reasonableness of the fair value.

GUERNSEY POWER HOLDINGS, LLC

AND SUBSIDIARY

Notes to Consolidated Financial Statements

December 31, 2024

(Dollars in thousands)

(5)Long-Term Debt

The Company’s long-term debt is nonrecourse to the Member, which includes the following terms:

On August 29, 2019, the Company entered into a $950 million floating rate Construction and Term Loan Facility (CT Loan) to finance the construction of the Project and a $125 million Revolving Credit/Letter of Credit Facility (RCF) (collectively known as the Project Debt). The Project Debt did not require principal repayments until the time it was converted from construction loan to term loan.

On May 5, 2023, the Project Debt was converted from a construction loan to a term loan. At such time all terms and requirements under the term loan became effective. On June 4, 2023, the Company amended the Project Debt documents to reference SOFR and remove LIBOR.

The RCF has two primary uses: (i) to issue letters of credit and (ii) make working capital loans. Any working capital loans drawn require interest payments at SOFR +351 bps that must be fully repaid for five consecutive days during a twelve month period (“WC Clean Up”). Repayments of working capital loans may be borrowed again after the WC Clean Up is satisfied. As of December 31, 2024, there were no draws against the RCF.

The Project Debt agreements contain certain restrictive covenants that, among other things, limit the Company’s ability to incur additional indebtedness, maintain reserve accounts, make distributions, and the requirement to hedge the majority of interest rate risk. The Project Debt was being drawn, subject to the satisfaction of certain conditions precedent, on a monthly basis during the available draw period.

The annual maturities of the long-term Project Debt based on schedule of targeted principal payments are as follows:

GUERNSEY POWER HOLDINGS, LLC

AND SUBSIDIARY

Notes to Consolidated Financial Statements

December 31, 2024

(Dollars in thousands)

(6)Derivative Instruments and Hedging Activities

The Company uses interest rate derivative instruments to manage its exposure to changes in the interest rate on its variable rate debt instruments. In addition, from time to time the Company uses power swaps and a revenue put to manage its merchant power price risk.

By using derivative financial instruments to hedge exposures to changes in interest rates and fluctuating power prices the Company exposes itself to credit risk and market risk. Credit risk is the failure of the counterparty to perform under the terms of the derivative contract. When the fair value of a derivative contract is positive, the counterparty owes the Company, which creates credit risk for the Company. When the fair value of a derivative contract is negative, the Company owes the counterparty, and therefore, the Company is not exposed to the counterparty’s credit risk in those circumstances. The Company minimizes counterparty credit risk in derivative instruments by entering transactions with high quality counterparties.

Market risk is the adverse effect on the value of a derivative instrument that results from a change in interest rates or merchant power prices. The market risk associated with interest rate contracts and power swap contracts is managed by establishing and monitoring parameters that limit the types and degree of market risk that may be undertaken.

The tables listed below provide a reconciliation of the beginning and ending net balances for the derivative instruments measured at fair value. All interest rate swaps are classified as Level 2 in the fair value hierarchy and all power swaps are classified as Level 3 in the fair value hierarchy:

For the year ended December 31, 2024 the Company received $29,923 of interest swap settlements, which were recognized on the consolidated statement of operations.

GUERNSEY POWER HOLDINGS, LLC

AND SUBSIDIARY

Notes to Consolidated Financial Statements

December 31, 2024

(Dollars in thousands)

The following table summarizes the fair value within the derivative instruments valuation on the consolidated balance sheets as of December 31, 2024:

(a)Interest Rate Swaps

On August 29, 2019, the Company entered into four interest rate swap agreements, each with the same terms, which are the forecasted interest payments for 75% of the expected outstanding Project Debt under the credit facility. The interest rate swaps are in effect from June 30, 2021, to October 31, 2027 and effectively convert the floating rate of the Project Debt to a fixed interest rate. The interest rate swaps are derivative financial instruments and are recorded on the consolidated balance sheets at fair value. The following table summarizes the interest rate swap rates:

(b)Commodity Derivatives

During 2024 the Company entered into various Commodity Swap Transactions. These swaps lock in various fixed pricing of the Projects output. The notional volume of the Company’s open derivative transactions is 2,151,590 MWH’s for the year ended December 31, 2024. The commodity swaps are derivative financial instruments and are recorded on the consolidated balance sheets at fair value.

The Company also executed a Revenue Put, on August 29, 2019 with Morgan Stanley Capital Group (Morgan Stanley), who was paid a one-time $35,000 option premium in exchange for a revenue guarantee of $26,000 in annual energy margin of 500 megawatts (MW) for the five annual periods starting on September 1, 2022. At the end of each quarter, a proxy energy margin for 500 MW of capability is calculated based upon a defined PJM proxy power price less calculated operating costs based on a proxy gas price index applied to a theoretical plant heat rate with defined O&M cost adders. If the quarterly calculated energy margin is less than $6,500, Morgan Stanley pays the Company the shortfall amount. At the end of

GUERNSEY POWER HOLDINGS, LLC

AND SUBSIDIARY

Notes to Consolidated Financial Statements

December 31, 2024

(Dollars in thousands)

each annual period the quarterly payments are trued up so that Morgan Stanley meets but does not exceed the $26,000 annual energy margin for that period. The Company is not required to pay Morgan Stanley any excess revenue with the exception of reimbursement of the amount that the sum of the quarterly payments exceeds the $26,000 annual revenue strike. The initial one-time payment was classified as a long term derivative asset on the accompanying balance sheet. For the year ended December 31, 2024, the Company recorded an unrealized loss in the consolidated statement of operations of $840, related to the Revenue Put.

(7)Related Parties

(a)Administrative Management Agreement (AMA)

The Company executed an AMA with Caithness Guernsey Administrative Management, LLC on August 29, 2019 to act as an independent contractor who will perform operational management and general administrative services. The services and fees under the AMA, began on August 1, 2022 and continue throughout operations of the Project. The Company will pay an annual fee of $3,000 for performance under the AMA, with the monthly fee subject to annual increases based on the Consumer Price Index increase for the immediately preceding 12-month period. For the year ended December 31, 2024, the Company incurred $3,594 which was expensed in general administrative expenses.

(b)Amounts Due From and Due To Related Parties

Amounts due to related parties pertain to payments of normal course of business expenses paid on behalf of the Company and intercompany loans. The amounts due to related parties as of December 31, 2024 are comprised of the following:

(8)Commitments and Contingencies

The Company routinely obtains Lines of Credit (LOCs) to satisfy the obligations for various requirements. The table below summarizes the LOC outstanding as of December 31, 2024:

GUERNSEY POWER HOLDINGS, LLC

AND SUBSIDIARY

Notes to Consolidated Financial Statements

December 31, 2024

(Dollars in thousands)

The table below summarizes the Company’s commitment fee as of December 31, 2024:

The Company also pays a .125% fronting fee associated with the LOCs. For the year ended December 31, 2024, the LOCs and commitment fees were $2,746 which was included in interest expense on the statement of operations.

(a)Operation and Maintenance Agreement (OMA)

On May 13, 2019, the Company entered into an OMA with Ethos Energy Power Plant Services, LLC (EEP), which provides for the operation and maintenance of the Facility. Prior to COD, EEP performed all the necessary services to bring the Facility to commercial operations (the Mobilization Phase), including recruiting and staffing, budgeting, developing and administering necessary operations programs, and all other services needed to assist the Company with accepting the Facility from the EPC contractor. Subsequent to the Mobilization Phase is the Operational Phase, where EEP provided appropriate staffing and performs the day-to-day operations, routine testing, maintenance, repair of the Facility, and other services required for electrical energy production. EEP will procure all goods, services, accessories, consumables, parts and equipment, as needed to perform their duties as operator and will receive payment for all payroll costs for on-site staffing as well as an annual fee to cover all costs to perform their duties as operator. The OMA is due to expire on the earlier of (i) 5 years after the Operational Phase, subject to extension upon mutual agreement of the Company and EEP and (ii) termination of the agreement by the Company or EEP. The terms of the OMA permit the Company to terminate the agreement at any time during the Operational Phase without cause upon giving 60 days’ written notice to EEP.

Contract pricing under the terms of the OMA are as follows:

•Mobilization Phase: $10 each month, plus reimbursement of payroll costs and other operating expenses

•Operational Phase: $305 annual fee paid in 12 monthly installments, plus reimbursement of payroll costs and other operating expenses.

The OMA also provides for an annual performance adjustment, which if positive, will consist of a payment by the Company to EEP or if negative, will consist of a payment from EEP to the Company. The terms of the performance adjustment are as follows:

•Annual base amount of $183, escalated.

•Consideration of Operator performance in Safety, Environmental and Budget compliance and Facility Availability (all as defined in the OMA).

For the year ended December 31, 2024, the fees incurred under the OMA were $424.

(b)Contract for the Purchase of Power Generation Equipment and Related Services and the Assignment, Assumption and Consent Agreement

On January 31, 2019, the Company entered into the ESA with General Electric Company (GE) for the procurement, manufacture, fabrication, delivery, and supply of power train equipment for three power generation units (Power Blocks) for an approximately 1,875-megawatt combined cycle natural gas fired, electrical generating facility. Each delivered unit includes the gas turbine, heat recovery steam generator,

GUERNSEY POWER HOLDINGS, LLC

AND SUBSIDIARY

Notes to Consolidated Financial Statements

December 31, 2024

(Dollars in thousands)

steam turbine and all necessary supporting equipment for installation and operation. The contract price for the ESA is approximately $381,364, which was assigned to Gemma Power Systems, LLC (Gemma) under the Assignment, Assumption and Consent Agreement (AACA) dated January 31, 2019 by and among the Company, Gemma and GE. Under the AACA, Gemma assumes responsibility for GE’s performance and stands in front of GE and the Company. Under the AACA the Company retains certain rights and responsibilities such as the responsibility to make payments, and requires the Company to deposit amounts properly invoiced by GE into an escrow account. Gemma is responsible to release the funds from escrow to GE upon Gemma’s agreement that the funds are due and owing. Under the AACA the Company is indemnified in the event of a dispute over payments to GE as long as the Company made the escrow deposit.

GE was subject to liquidated damages (25% of contract price for delay, 15% of contract price for performance, cumulatively capped at 35% of the contract price) for failure to meet the guaranteed delivery dates set forth in the ESA. Liquidated Damages for delays in delivering drawings, Major Components (as defined in the agreement) and Minor Components are set forth in the agreement and may vary based on the duration of the delay subject to daily and cumulative caps. For example, liquidated damages for delays in delivery beyond 60 days for Major Components and Minor Components are $90 and $20 per day respectively and all delivery delay liquidated damages are capped at a maximum of $270 per day. Since the ESA is assigned to Gemma, any liquidated damages owing by GE are paid to Gemma. Gemma may or may not have corresponding obligations to the Company for liquidated damages under the EPC agreement. GE continues to have performance requirements to the Company after the commercial operation date.

(c)Contractual Service Agreement (CSA)

On June 28, 2019, the Company entered into a CSA with General Electric International, Inc. (GEI), pursuant to which they will provide certain parts and services for the installed gas turbines, steam turbines generators, and other associated components of the turbines. The CSA will cover maintenance, repair of collateral damage, initial spare parts, monitoring systems, unscheduled outage obligations, non-hazardous clean-up and permits having to do with the installed turbines. The initial term of the contract is for 25 years.

The contract includes $20,000 plus escalation paid over four annual payment dates, for the delivery of the initial spare parts. The first payment for the initial spare parts is due when the initial spare parts are received. The initial spare parts were received during 2024 and on October 31, 2024, the first payment of $5,944 was made. The spare parts associated with the CSA are recorded in other long term assets on the accompanying balance sheets. The next contract payment of $5,000, is included in accrued liabilities and the remaining two payments are included in other long term liabilities on the accompanying balance sheets.

In addition, there will be a monthly fixed fee of $25 and variable fees of $0.5 per gas turbine fired hour with an annual 2.5% escalation on both fees.

(d)Contracts for Sale and Purchase of Natural Gas and Firm Gas Transportation Agreements

On October 9, 2018 the Company entered into the GSA with Equinor Natural Gas, LLC (ENG), which was amended on June 2, 2019, July 8, 2019, July 26, 2019, and July 14, 2022 for the firm supply of up to 160,000 dekatherm (dth)/day of natural gas for a period covering 10 years from the in service date. ENG will have the option to decrease volumes beginning in year 6.

The Company must take full contract gas volumes every day. If all or a portion of the plant is in an Excused Outage, then the Company is excused from taking the amount of gas it cannot burn due to the Excused Outage.

On August 22, 2019 the Company entered into a GSA with Shell Energy North America (US), L.P. (SENA) for the firm supply of up to 80,000 dth/day of natural gas for a period of 5 years from the in service date. The

GUERNSEY POWER HOLDINGS, LLC

AND SUBSIDIARY

Notes to Consolidated Financial Statements

December 31, 2024

(Dollars in thousands)

Company must take full contract gas volumes every day but may reduce the volume during an Excused Outage. SENA will also schedule and balance gas supply under the Company’s GTAs. The Company has determined that the price of gas in these contracts is a market price for gas in the location received. The Company has concluded that these long-term gas supply contracts are not derivatives as the price at which they purchase gas is the market price of gas at that location. If this was not a market price and these were derivatives the Company would apply the normal purchase normal sales exclusion as they are using the gas in their operations and do not anticipate any net settlements of gas.

On August 22, 2019, the Company entered into a Fuel Management Services Agreement (FMA) with Shell Energy North America (US), L.P. (SENA) for fuel management and consulting services for a period of 5 years from the in-service date. Under the FMA, the Company will pay SENA $0.005 per dth for managing third-party supplied gas or approximately $24 per month.On June 20, 2019, the Company entered into a Gas Transportation Agreement with Rockies Express Pipeline LLC (REX) for firm gas transportation of 240,000 dth/day for a period of 20 years from the in-service date. REX will transport gas from the pipeline receipt points in the Clarington production area to a delivery point at Aspire’s metering station at the plant. Under the REX GTA, the Company will pay REX an annual demand charge of $11,388 plus variable charges for gas actually transported for the Company.

On December 21, 2017, the Company entered into a Firm Transportation Service Agreement with Aspire Energy Express, LLC (Aspire) for firm gas transportation of 300,000 dth/day for a period of 10 years from the in-service date. Aspire built and will own and operate a metering station to receive gas from REX at the plant site and deliver it to the Company. Under the Aspire GTA, the Company will pay Aspire an annual demand charge of $1,476.

(e)Turnkey, Engineering, Procurement and Construction Agreement (Switchyard EPC)

On August 9, 2019, the Company executed the Switchyard EPC with EPC Services Company, LLC for the design, engineering, procurement, and construction of a 765 kV switching station and generator tie line. The facility will use this switching station to interconnect with the American Electric Power (AEP) transmission system along the Kammer and Vassel 765 kV line. Full notice to proceed was issued under the Switchyard EPC on August 29, 2019. The Switchyard EPC contract cost was $44,737, subject to change orders and was subject to payment by the Company with customary terms and conditions. On January 20, 2023, the Company transferred ownership of the Switchyard EPC to AEP for no consideration. The Company will continue to carry and depreciate these capitalized costs. This will have no effect on the Company’s current or future financial statements.

(9)Subsequent Events

On July 17, 2025, Caithness Apex Guernsey, LLC, the sole owner of the Company entered into an agreement to sell 100% of their interest in the Company to an unrelated third party. The transaction will not have any impact on the financial position of the Company. Subsequent events have been evaluated and disclosed as required through the report issuance date of September 12, 2025.