Please wait

May 7, 2025

VIA EDGAR

U.S. Securities and Exchange Commission

Division of Corporation Finance

Office of Life Sciences

100 F Street, NE

Washington, D.C. 20549

Attention: Jenn Do

Vanessa Robertson

Re: Vaxcyte, Inc.

Form 10-K for the fiscal year ended December 31, 2024

Filed February 25, 2025

File No. 001-39323

Dear Ms. Do and Ms. Robertson,

Vaxcyte, Inc. (the “Company,” “we,” or “our”) acknowledges receipt of your comment letter (the “Comment Letter”) dated April 10, 2025 from the staff (the “Staff”) of the U.S. Securities and Exchange Commission (the “SEC” or the “Commission”) regarding the above-referenced Form 10-K, as filed on February 25, 2025. As such, set forth below is the Company’s response to the comment contained in the Comment Letter. To facilitate the Staff’s review, the text of the Staff’s comment is set forth below in bold.

Form 10-K for the fiscal year ended December 31, 2024

Management's Discussion and Analysis of Financial Condition and Results of Operations, page 99

Results of Operations, page 109

1.You disclose on page 106 that do not allocate all of your costs by vaccine candidates, as your research and development expenses include internal costs, such as payroll and other personnel expenses, which are not tracked by vaccine candidate. Please provide revised disclosure to be included in future filings to address the following:

•Clarify which expenses you do allocate by project and clarify if you track any expenses by candidate. To the extent you do track any research and development expenses by program, provide a breakdown of the expenses tracked by project.

•If you do not track external expenses by program, break out external research and development costs by clinical and preclinical. If you cannot disaggregate these amounts, please disclose that fact and explain why not.

•For all other research and development expenses. provide us with other quantitative or qualitative disclosure that provides more transparency as to the type of research and development expenses incurred (i.e. by nature or type of expense) which should reconcile to total research and development expense on the Statements of Operations. We note that you included a break out of research and development expenses by type in the 10-K for the year ended December 31, 2023.

Response: The Company acknowledges the Staff’s comment and respectfully advises the Staff that we track our research and development (“R&D”) expenses by major types of expense, and we do not have a systematic approach to allocate R&D expenses by candidate, program and/or project. Our R&D expenses include:

1)External costs:

a)Product manufacturing costs: This includes costs related to acquiring, developing, and manufacturing supplies for clinical trials and to prepare for potential future commercial launches, including fees paid to contract manufacturing organizations.

b)Clinical costs: This includes costs and expenses related to agreements with contract research organizations, investigator sites, and consultants to conduct clinical trials.

c)R&D consumables costs, laboratory supplies and equipment costs.

d)Facility and allocated costs.

e)Other expenses, which primarily include professional and consulting services costs.

2)Internal personnel-related costs: This includes salaries, employee benefits, and stock-based compensation for our personnel in R&D functions.

Our pneumococcal conjugate vaccine (“PCV”) programs include VAX-31 and VAX-24, and our non-PCV programs include VAX-A1, VAX-PG, VAX-GI, and other discovery-stage programs. The majority of our external costs relate to our PCV programs, including both VAX-31 and VAX-24, compared to the costs related to VAX-A1 and other non-PCV programs.

Most of the external costs associated with our vaccine candidates, particularly our PCV programs, are common in nature, and can be deployed across multiple candidates or redeployed as our vaccine development strategy evolves; as a result, we do not have a systematic approach to track external costs

precisely by candidate, program or project, nor are we able to allocate these costs across programs in sufficiently reliable detail for reporting purposes, other than clinical costs that are conducted on a program-by-program basis. However, as clinical costs only account for a small portion of the total R&D expenses, we do not believe providing clinical costs by program would materially enhance an investor’s understanding of our total R&D expenses or provide a more meaningful level of disclosure for investors to understand our results of operations. Further, we do not allocate internal personnel-related costs by program or project because several of our departments support multiple vaccine candidate R&D programs, and the hours are not tracked separately by program. While the Company may have the ability to retrospectively provide the R&D expenses on a program-by-program basis by means of manually allocating the costs with certain assumptions, the allocation could be arbitrary and provide less meaningful or potentially misleading information to investors. Moreover, we are also concerned that public disclosure of the R&D expenses by candidate, program or project would result in competitive harm to the Company in a variety of ways, adversely impacting our competitive position, and as a result, our stockholders. For instance, we believe that such disclosure may weaken our ability to negotiate competitive terms with external vendors with which we may contract from time to time for services in support of our vaccine programs because they may be able to determine the amounts we pay for certain work related to a program and leverage this commercially sensitive information against us in the negotiation of contractual terms. This may negatively impact our ability to secure agreements with such vendors on optimal terms or could even make certain proposed arrangements commercially prohibitive to the Company.

Our PCV programs are in the clinical stages, and non-PCV programs are in preclinical stages. The majority of our external costs relate to our PCV programs, including both VAX-31 and VAX-24, compared to the costs related to VAX-A1 and other non-PCV programs. Costs associated with preclinical programs are relatively small and insignificant to the overall financial statements. Further, other than certain clinical trial expenses, the majority of the expenses are shared among various vaccine programs and not tracked separately, and we are not able to disclose such expenses by clinical and preclinical stages in sufficiently reliable detail for reporting purposes. We have determined that the expenses related to preclinical stage programs are not material to an understanding of the Company’s results of operations at this time and therefore do not warrant separate disclosure. If, and to the extent, we determine such expenses are material to the understanding of the Company’s results of operations, such expenses will be tracked and separately disclosed in future periodic reports.

The Company does track product manufacturing costs and clinical costs separately. As the Company continues progressing in the clinic to Phase 3 and the clinical costs continue to grow, we believe it is meaningful to present the two types of external expenses separately, in addition to other external costs and internal personnel-related costs, to provide more transparency to investors. Therefore, the Company

has revised the disclosure in our Quarterly Report on Form 10-Q filed on May 7, 2025, to present product manufacturing costs, clinical costs, other external costs and internal personnel-related costs separately, as set forth on Exhibit A hereto.

The Company respectfully acknowledges the Staff’s comment and advises the Staff that the Company has revised the disclosure in our Quarterly Report on Form 10-Q filed on May 7, 2025 in response to the Staff’s comment to provide additional qualitative and quantitative disclosure that provides more transparency as to the type of R&D expenses incurred, as set forth on Exhibit A hereto (changes that are in response to the Staff’s comment are marked). We will include disclosure in our future filings that is similar to the disclosure in our Quarterly Report on Form 10-Q filed on May 7, 2025. We believe these revisions reflect the way management views and manages our R&D activities and business. We also believe these revisions will provide further context to enhance an investor’s understanding of our use and expected use of resources in connection with our R&D activities and provide greater clarity and transparency in our financial disclosures.

We hope that the foregoing has been responsive to the Staff’s comments. Please do not hesitate to contact the undersigned with any questions or comments regarding this letter.

Sincerely,

| | |

|

| Andrew Guggenhime |

| President and Chief Financial Officer |

|

| | | | | |

| cc: | Mikhail Eydelman, Vaxcyte, Inc. |

| Robert Bitman, Vaxcyte, Inc. |

| Raquel Fox, Skadden, Arps, Slate, Meagher & Flom LLP |

Exhibit A

Components of Results of Operations

Operating Expenses

Research and Development

Research and development expenses represent costs incurred in performing research, development and manufacturing activities in support of our own product development efforts. TheseOur research and development expenses include internal personnel-related costs (including salaries, employee benefits and stock-based compensation) for our personnel in research and development functions, and external costs related to (including (i) product manufacturing costs, primarily related to acquiring, developing and manufacturing supplies for preclinical studies, clinical trials and other studies, to prepare for potential future commercial launches, including fees paid to contract manufacturing organizations; (ii) clinical costs related to agreements with contract research organizations, investigative sites and consultants to conduct non-clinical and preclinical studies and clinical trials; (iii) professional and consulting services; (iv) research and development consumables; (v), laboratory supplies and equipment; and (vi costs; (iv) facility and other allocated shared services; and (v) other expenses primarily including professional and consulting services costs.

Our pneumococcal conjugate vaccine (“PCV”) programs include VAX-31 and VAX-24, and our non-PCV programs include VAX-A1, VAX-PG, VAX-GI, and other discovery-stage programs. The majority of our external costs relate to our PCV programs, including both VAX-31 and VAX-24, compared to the costs related to VAX-A1 and other non-PCV programs. Most of the external costs associated with our vaccine candidates, particularly our PCV programs, are common in nature, and can be deployed across multiple candidates or redeployed as our vaccine development strategy evolves; as a result, we do not track external costs by candidate, program or project. We do not allocate internal personnel-related costs by program or project because several of our departments support multiple vaccine candidate programs and the hours are not tracked separately by program. We do not allocate all of our costs by vaccine candidates, as our research and development expenses include internal costs, such as payroll and other personnel expenses, which are not tracked by vaccine candidate. In particular, with respect to internal costs, several of our departments support multiple vaccine candidate research and development programs.

Our PCV programs are in the clinical stages, and non-PCV programs are in preclinical stages. The majority of our external costs relate to our PCV programs, including both VAX-31 and VAX-24, compared to the costs related to VAX-A1 and other non-PCV programs. Costs associated with preclinical

programs are relatively small and insignificant to the overall financial statements. Further, several expenses are shared among various vaccine programs and, as such, we do not separately track external costs by clinical and preclinical stages.

Results of Operations

Comparison of the Three Months Ended March 31, 2025 and 2024

Operating Expenses

Research and Development Expenses

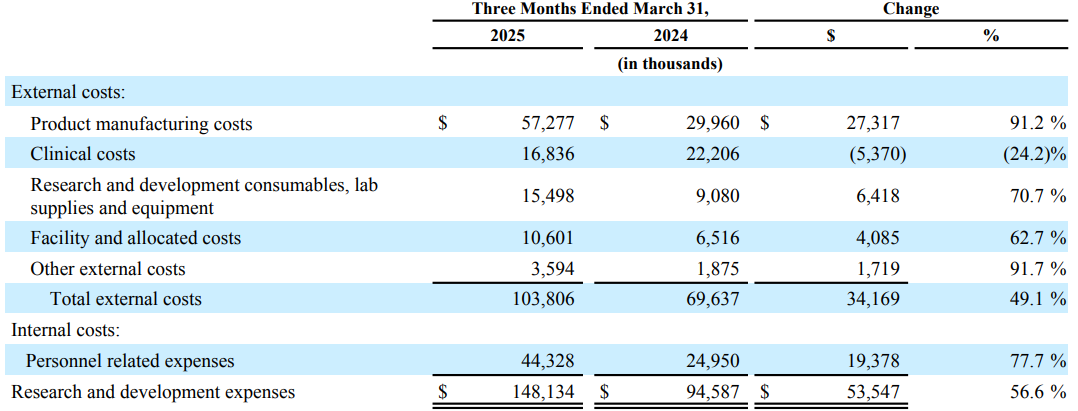

Research and development expenses increased by 53.5 million, or 56.6%, during the three months ended March 31, 2025 compared to the corresponding period in 2024. The increase was driven by external costs, which grew by $34.2 million largely due to increased development and manufacturing activities in connection with the adult and infant PCV programs and to support the potential future commercial launches. Product manufacturing costs increased by $27.3 million, research and development consumables, lab supplies and equipment increased by $6.4 million, facility and allocated costs increased by $4.1 million and other external costs increased by $1.7 million, partially offset by a decrease of $5.4 million in clinical costs primarily due to reduced clinical trial activities compared to the prior period. The increase was further driven by internal personnel-related costs, which grew by $19.3 million largely due to headcount growth.