Please wait

| | | | | |

| Eversheds Sutherland (US) LLP 700 Sixth Street, NW, Suite 700 Washington, DC 20001-3980 D: +1 202.383.0218 F: +1 202.637.3593 cynthiakrus@eversheds-sutherland.com |

September 25, 2024

Via EDGAR

U.S. Securities and Exchange Commission

Division of Investment Management

Attention: Ms. Anu Dubey and Mr. John Kernan

100 F Street, N.E.

Washington, D.C. 20549

| | | | | |

| Re: | Blue Owl Capital Corporation – Registration Statement on Form N-14 (File No. 333-281609) |

Dear Ms. Dubey and Mr. Kernan:

On behalf of Blue Owl Capital Corporation (the “Company” or “OBDC”), set forth below is the Company’s response to the oral comments provided by the staff of the Division of Investment Management (the “Staff”) of the U.S. Securities and Exchange Commission (the “SEC”), on September 10, 2024 and September 12, 2024, regarding the Company’s registration statement on Form N-14 (the “Registration Statement”), and the joint proxy statement/prospectus contained therein, as initially filed with the SEC on August 16, 2024. Each of the Staff’s comments is set forth below and followed by the Company’s response. Unless otherwise indicated, all page references are to page numbers in the Registration Statement. Capitalized terms used herein but not defined shall have the meanings ascribed to them in the Registration Statement.

Legal

1.Comment: In the OBDC Shareholder Letter, please disclose the limited purposes for which the Advisers are party to the Merger Agreement.

Response: The Company has revised the third through sixth paragraphs of the OBDC Shareholder Letter to add the language underlined below:

At the OBDC Special Meeting, you will be asked to:

(i)approve the issuance of shares of OBDC common stock, par value $0.01 per share (“OBDC Common Stock”) pursuant to the Agreement and Plan of Merger dated as of August 7, 2024 (the “Merger Agreement”) by and among OBDC, a Maryland corporation, Cardinal Merger Sub Inc., a Maryland corporation and

1

Eversheds Sutherland (US) LLP is part of a global legal practice, operating through various separate and distinct legal entities, under Eversheds Sutherland. For a full description of the structure and a list of offices, please visit www.eversheds-sutherland.com.

wholly owned subsidiary of OBDC (“Merger Sub”), Blue Owl Capital Corporation III, a Maryland corporation (“OBDE”), Blue Owl Credit Advisors LLC, a Delaware limited liability company (“OBDC Adviser”) (for the limited purposes set forth therein and described below) and Blue Owl Diversified Credit Advisors LLC, a Delaware limited liability company (“OBDE Adviser”) (for the limited purposes set forth therein and described below) (such proposal is referred to herein as the “Merger Stock Issuance Proposal”);

(ii)approve the Fourth Amended and Restated Investment Advisory Agreement between OBDC and OBDC Adviser (the “New OBDC Investment Advisory Agreement”) on the terms described in the accompanying joint proxy statement/prospectus (such proposal is referred to herein as the “Advisory Agreement Amendment Proposal”). The New OBDC Investment Advisory Agreement is amended to exclude the impact of purchase accounting adjustments resulting from any purchase premium or discount paid for the acquisition of assets in a merger from the calculation of the income incentive fee and the capital gains incentive fee, and to delete certain provisions and remove references to items which by their terms are not applicable to OBDC as a result of OBDC’s listing on the New York Stock Exchange.

The Board, including all of the independent directors, and upon recommendation of a committee of the Board comprised solely of the independent directors, unanimously recommends that you vote “FOR” the approval of the Merger Stock Issuance Proposal. The Board, including all of the independent directors, also unanimously recommends that you vote “FOR” the approval of the Advisory Agreement Amendment Proposal.

The approval of the Merger Stock Issuance Proposal is not contingent on the approval of the Advisory Agreement Amendment Proposal and the approval of the Advisory Agreement Amendment Proposal is not contingent on the approval of the Merger Stock Issuance Proposal. Closing of the Mergers (as defined below) is contingent upon OBDC Shareholder approval of the Merger Stock Issuance Proposal, approval by the holders of common stock of OBDE (“OBDE Shareholders”) of a proposal to adopt the Merger Agreement and certain other closing conditions.

OBDC and OBDE are proposing a combination of both companies by a series of mergers and related transactions pursuant to the Merger Agreement pursuant to which Merger Sub will merge with and into OBDE with OBDE continuing as the surviving company (the “Initial Merger”). Immediately following the Initial Merger, OBDE, as the surviving company, would merge with and into OBDC with OBDC continuing as the surviving company (the “Second Merger” and together, with the Initial Merger, the “Mergers”). OBDC Adviser and OBDE Adviser are each a party to the Merger Agreement for the following limited purpose: to (i) deliver the calculation of the Closing OBDC NAV (as defined below) or the Closing OBDE NAV (as defined below), as applicable, and (ii) make customary representations and warranties. OBDC Adviser is also party to the

Merger Agreement because it has agreed to reimburse each of OBDC and OBDE for 50% of all fees and expenses incurred and payable by each party in connection with the Mergers, subject to certain terms, conditions and limitations included in the Merger Agreement. OBDE Adviser is also party to the Merger Agreement because it is a party to the investment advisory agreement and administration agreement with OBDE, which the Merger Agreement stipulates will be automatically terminated immediately after the Effective Time and immediately prior to the Second Merger.

2.Comment: In the OBDE Notice of Special Meeting of Shareholders, disclose why there is an Initial Merger and a Second Merger.

Response: The Company has revised the fourth paragraph of the OBDE Notice of Special Meeting of Shareholders to add the language underlined below:

Pursuant to the Merger Agreement, Merger Sub will merge with and into OBDE, with OBDE continuing as the surviving company (the “Initial Merger”), followed immediately by the merger of OBDE with and into OBDC, with OBDC as the surviving company (the “Second Merger” and together, with the Initial Merger, the “Mergers”) (such proposal is referred to herein as the “Merger Proposal”). The Mergers are taking place in two steps: (1) to allow the Mergers, taken as a whole, to qualify as a reorganization within the meaning of Section 368(a) of the Internal Revenue Code of 1986, as amended (the “Code”); and (2) to preclude imposition of corporate-level income tax should the transaction fail to qualify as a “reorganization” under Section 368(a) of the Code and OBDE fail to qualify as a regulated investment company for any reason. Subject to the terms and conditions of the Merger Agreement, if the Initial Merger is completed, each holder of OBDE common stock, par value $0.01 per share (“OBDE Common Stock”), issued and outstanding immediately prior to the effective time of the Initial Merger will have the right to receive, for each share of OBDE Common Stock, a number of shares of OBDC common stock, par value $0.01 per share (“OBDC Common Stock”) equal to the Exchange Ratio (as defined below), provided, that the Exchange Ratio shall be adjusted if, between the Determination Date (as defined below) and the effective time of the Mergers, the respective outstanding shares of OBDC Common Stock or OBDE Common Stock shall have been increased or decreased or changed into or exchanged for a different number or kind of shares or securities, in each case, as a result of any reclassification, recapitalization, stock split, reverse stock split, split-up, merger, issue tender or exchange offer, combination or exchange of shares, or similar transaction, or if a stock dividend or dividend payable in any other securities or similar distribution shall be authorized and declared with a record date within such period.

3.Comment: Explain why it is appropriate for OBDE Shareholders to vote on the Mergers when such shareholders do not know which investment advisory agreement will be in effect for the surviving fund because it depends on whether the New OBDC Investment Advisory Agreement will be approved.

Response: The Company respectfully advises the Staff that it is appropriate for OBDE Shareholders to vote on the Mergers because (1) the changes being proposed in the New

OBDC Investment Advisory Agreement are not material, and (2) the Registration Statement contains sufficient information about the changes being proposed in the New OBDC Investment Advisory agreement for an OBDE Shareholder to evaluate the Mergers and consider whether to approve the Merger Proposal regardless of whether the proposed changes are approved.

As described in the section of the Registration Statement entitled “Accounting Treatment of the Mergers,” ASC 805-50, Business Combinations—Related Issues (“ASC 805-50”) requires the Company to treat the Merger as an asset acquisition. The asset acquisition method of accounting requires OBDC to, among other things, record on its books the assets acquired from OBDE at fair market value. Because ASC 805-50 also requires OBDC to allocate any purchase premium or purchase discount to each asset acquired from OBDE, the Merger may result in amortization or accretion to interest income and in OBDC immediately recognizing on its financial statements any unrealized depreciation and / or unrealized appreciation attributable to OBDE’s former assets. Although there is no expected change in the asset composition of the combined OBDC/OBDE entity, since OBDC’s Current OBDC Investment Advisory Agreement calculates incentive fees based on these inputs, the required asset acquisition accounting treatment could alter (i.e., increase or decrease) the amount of incentive fees due to OBDC Adviser solely as a result of the Merger, as described further in the Registration Statement.

One of the purposes of the New OBDC Investment Advisory Agreement is to adjust the calculations of OBDC’s capital gains incentive fee and income incentive fee to exclude the impact of any amortization or accretion of any purchase premium or purchase discount resulting solely from the purchase accounting required in a merger. The Company believes that the New OBDC Investment Advisory Agreement would better align the incentive fees with the economic realities of a merger that results in a combined entity with substantially the same assets. In other words, the New OBDC Investment Advisory Agreement is intended to make the calculation of the incentive fees neutral with respect to a merger. Since OBDC and OBDE shareholders’ capital gains and income incentive fees are otherwise exactly the same, and since such shareholders’ fees would not be altered solely as a result of the merger transaction, the Company does not believe that changes to the income and capital gain incentive fees included in the New OBDC Investment Advisory Agreement are material.

The Registration Statement discloses that, if the Mergers had been completed on June 30, 2024, the New OBDC Investment Advisory Agreement would have resulted in a $0.1 million quarterly decrease in the income incentive fee due to the Adviser, and no additional capital gains incentive fees due to the Adviser. The Company believes that the pro forma decrease in income incentive fees as of June 30, 2024 is immaterial given the income incentive fees that OBDC historically paid. For example, for the fiscal year ended December 31, 2023, the $0.1 million decrease in income incentive fee per quarter would have represented a 0.25% overall decrease in the amount of incentive fees paid based on the $159.9 million in annual income incentive fees paid by OBDC in that year.

The second purpose of the New OBDC Investment Advisory Agreement is to remove certain provisions relating to the NASAA Omnibus Guidelines and provisions that were solely applicable to OBDC prior to the listing of its Common Stock on the NYSE. As these provisions have never applied to the Company, the Company does not believe that removing these provisions would be material to any OBDE Shareholder considering whether to approve the Merger.

In addition to the changes included in the New OBDC Investment Advisory Agreement not being material, the Company believes that it has provided OBDE Shareholders with sufficient information to determine how OBDC would operate, regardless of whether OBDC’s Shareholders approve the New OBDC Investment Advisory Agreement. As noted in the Registration Statement, there is no material difference in the rate of ongoing management and incentive fees to be paid by, nor the services that the OBDC Adviser expects to provide to, shareholders of the combined company. As discussed above, the Company has fully disclosed the potential impact on the incentive fees of the approval of the New OBDC Investment Advisory Agreement, and that removal of provisions related to the NASAA Omnibus Guidelines and periods prior to the listing of OBDC’s Common Stock on the NYSE is not expected to have any impact on the Company. As a result, the Company believes that the OBDE shareholders have sufficient information to fully evaluate the expected operations of the combined company following the Mergers.

4.Comment: Explain why the vote required for the Merger Proposal is not a majority of outstanding voting securities as required by Rule 17a-8(a)(3)(ii) under the 1940 Act.

Response: The Company respectfully advises the Staff that the voting standard in Rule 17a-8(a)(3)(ii) is not required because the transaction satisfies the conditions set forth therein. Specifically, the investment advisory contract between OBDC and OBDC Adviser is not materially different from the advisory contract between OBDE and OBDE Adviser, except for the identity of the adviser party thereto. The services to be provided by OBDC Adviser are the same services that OBDE Adviser currently provides to OBDE. Specifically, both OBDE Adviser and OBDC Adviser have the same employees, investment committees, portfolio managers, and processes for sourcing and monitoring investment opportunities. Moreover, the termination provisions of each of their investment advisory agreements are the same, and the management fee and incentive fee rates under each agreement are the same.

As such, the majority voting standard under the 1940 Act is not required with respect to the Merger Proposal and the Maryland state law voting requirement is sufficient for approval of the Merger Proposal.

5.Comment: Please describe with specificity what happens in the Initial Merger and whose shares are exchanged for whose shares and whether this exchange is it at NAV, and please also explain what legal approvals, if any, are required for the initial merger.

Response: The Company respectfully advises the Staff that subject to the terms and conditions of the Merger Agreement, at the effective time of the Initial Merger, (i) each share of common stock of Merger Sub (all of which are owned by the Company) will be converted into one validly issued, fully paid and nonassessable share of common stock of OBDE and (ii) shares of OBDE Common Stock (other than those held by the Company or any of its consolidated subsidiaries) will be converted into the right to receive, the number of shares of OBDC Common Stock equal to the Exchange Ratio (the “Merger Consideration”). As a result of the Initial Merger, all shares of OBDE Common Stock shall no longer be outstanding and shall automatically be cancelled and shall only represent the right to receive the Merger Consideration, cash in lieu of fractional shares and any dividends or other distributions payable pursuant to the Merger Agreement.

The Initial Merger requires the following approvals: (1) approval by the OBDC Board in accordance with Section 3-105(b) of the MGCL; (2) approval by OBDC in its capacity as the sole shareholder of Merger Sub in accordance with Section 4A-702(f) of the Maryland Limited Liability Company Act; and (3) the approval of the holders of a majority of the outstanding shares of OBDE Common Stock entitled to be cast at the OBDE Special Meeting, pursuant to Section 2-104(b)(5) of the MGCL and the OBDE Charter. The Company received the approvals referenced in clauses (1) and (2) on August 6, 2024 and OBDE is seeking the approval referenced in clause (3) at the OBDE Special Meeting.

6.Comment: On page 10, in the answer to the question “Is the Exchange Ratio subject to any adjustment?”, please disclose an explanation as to how the Exchange Ratio will be “appropriately adjusted” if these occurrences happen.

Response: The Company has revised the answer to this question to add the language underlined below:

Yes. As described in more detail in this joint proxy statement/prospectus, the Exchange Ratio is calculated by taking into account the OBDC Per Share NAV and the OBDE Per Share NAV, as well as the OBDC Common Stock Price. The Exchange Ratio is determined as of the Determination Date. The Exchange Ratio will be appropriately adjusted If, between the Determination Date and the Effective Time, the respective outstanding shares of OBDC Common Stock or OBDE Common Stock has been increased or decreased or changed into or exchanged for a different number or kind of shares or securities, in each case, as a result of any reclassification, recapitalization, stock split, reverse stock split, split-up, combination or exchange of shares, or if a stock dividend or dividend payable in any other securities has been declared with a record date within such period, the OBDC Per Share NAV and the OBDE Per Share NAV used to calculated the Exchange Ratio will be adjusted to account for such increase, decrease or change, as applicable, in shares outstanding (to the extent not already taken into account in determining the Closing OBDE Net Asset Value and/or the Closing OBDC Net Asset Value, if applicable). This adjustment will be made to provide OBDE Shareholders and

OBDC Shareholders the same economic effect as contemplated by the Merger Agreement prior to such increase, decrease or change, as applicable.

7.Comment: On page 10, in the answer to the question “Who is responsible for paying the expenses relating to completing the Mergers?”, disclose the approximate dollar costs associated with the Mergers and identify who will bear those approximate dollar costs.

Response: The Company respectively advises the Staff that it has already disclosed in the answer to the relevant question, that if the Mergers are consummated, it is anticipated that OBDC will bear expenses of approximately $4.9 million in connection with the Mergers, and OBDE will bear expenses of approximately $2.3 million in connection with the Mergers. OBDC Adviser will reimburse up to 50% of such fees and expenses (up to $4.25 million) with the reimbursed amount to be allocated among OBDC and OBDE in a mutually agreeable manner.

8.Comment: On page 11, in the answer to the question, “How will the combined company be managed following the Second Merger?”, please clarify in the answer if OBDC and OBDE will have the same directors and officers both before and after the Initial Merger and the Second Merger.

Response: The Company has revised the answer to this question to add the language underlined below:

OBDC and OBDE have the same directors and officers and OBDC will continue to have the same directors and officers following the Mergers. The directors of OBDC immediately prior to the Second Merger will remain the directors of OBDC and will hold office until their respective successors are duly elected and qualify, or their earlier death, resignation or removal. The officers of OBDC immediately prior to the Second Merger will remain the officers of OBDC and will hold office until their respective successors are duly appointed and qualify, or their earlier death, resignation or removal. OBDE Adviser is affiliated with OBDC Adviser. Following the Second Merger, OBDC Adviser will continue to be the investment adviser of OBDC.

9.Comment: On page 12, in the answer to the question, “How will management and incentive fees at the combined company compare to management and incentive fees at OBDE?”, please explain in plain English how the calculation of incentive fee on income and on capital gains will change in the New OBDC Investment Advisory Agreement compared to the Current OBDC Investment Advisory Agreement.

Response: The Company has revised the answer to this question to add the language underlined below:

The contractual management and incentive fees of OBDC and OBDE are identical. See “Item 1. Business – Investment Advisory Agreement – Compensation of the Adviser” respectively in Part I of each of OBDC’s Annual Report on Form 10-K and

OBDE’s Annual Report on Form 10-K for the fiscal year ended December 31, 2023 for additional information on the calculation of each of OBDC’s and OBDE’s management fee under the OBDC Investment Advisory Agreement and the OBDE Investment Advisory Agreement. If the New OBDC Investment Advisory Agreement is approved, upon its effectiveness, the base management fee rate, capital gains incentive fee rate, and hurdle rate payable by OBDC will be the same as the base management fee rate, capital gains incentive fee rate, and hurdle rate paid by OBDE prior to the Mergers under the OBDE Investment Advisory Agreement. Pursuant to the New OBDC Investment Advisory Agreement, the calculation of the incentive fee based on income will be adjusted to exclude any amounts resulting solely from the new cost basis of the acquired OBDE investments established by ASC-805 as a result of the Mergers any amortization or accretion of any purchase premium or purchase discount to interest income resulting solely from the purchase accounting for any premium or discount paid for the acquisition of assets in a merger (the “New Income Incentive Fee”) and the calculation of the incentive fee on capital gains will be adjusted to exclude realized capital gains, realized capital losses or unrealized capital appreciation or depreciation resulting solely from the purchase accounting for any premium or discount paid for the acquisition of assets in a merger (the “New Capital Gains Incentive Fee”). In contrast, in the Current OBDC Investment Advisory Agreement, the calculations for the income incentive fee and capital gains incentive fee paid to the OBDC Adviser take into account the foregoing purchase accounting adjustments, and as a result, the accounting treatment of the Merger could alter (i.e., increase or decrease) the amount of incentive fees due to the OBDC Adviser under the Current OBDC Investment Advisory Agreement. For a more fulsome description of these changes, see “OBDC Proposal II: Approval of the Advisory Agreement Amendment Proposal.” For a comparison of the fees paid by OBDC, OBDE, and on a pro forma basis for the combined company, see “Comparative Fees and Expenses.” As described in the footnotes to the Comparative Fees and Expenses table, the table shows consistent fees payable on a pro forma basis for the combined company because OBDC and OBDE have substantially similar leverage and leverage targets, and the fees shown in the table are calculated, as is required by the relevant SEC rules applicable to the disclosure in the table, as a percentage of net assets attributable to common stock, rather than how they are calculated under the applicable investment advisory agreement. Under each of the New OBDC Investment Advisory Agreement, the Current OBDC Investment Advisory Agreement, and the OBDE Investment Advisory Agreement, base management fees are based on average adjusted gross assets at the end of the two most recently completed calendar quarters (excluding cash and cash equivalents and adjusted for any share issuances or repurchases during the applicable calendar quarter). 10.Comment: The Staff advises you that any attempt to seek payment of the Termination Fee would be a violation of Section 17(d) and Rule 17d-1 under the 1940 Act. The Staff also advises you that with respect to any future merger, entry into an agreement that provides for payment of a termination fee to an entity that would be an affiliated person or principal underwriter referenced in Rule 17d-1(a) in connection with a merger by a registered investment company or a company that has elected to be

regulated as a BDC would be a violation of 17(d) and Rule 17d-1 at the time the agreement is made.

Response: The Company respectfully submits that Section 17(d) and Rule 17d-1 under the 1940 Act do not apply to the provisions requiring the payment of the Termination Fee under the Merger Agreement. Section 17(d) prohibits joint transactions between registered investment companies and affiliated persons and Rule 17d-1 prohibits affiliated persons of registered investment companies from participating in any “joint enterprise or other joint arrangement or profit-sharing plan” in which any such registered investment company is a participant. Rule 17d-1(c) defines “joint enterprise or other joint arrangement or profit-sharing plan” as:

any written or oral plan, contract, authorization or arrangement, or any practice or understanding concerning an enterprise or undertaking whereby a registered investment company or a controlled company thereof and any affiliated person of or a principal underwriter for such registered investment company, or any affiliated person of such a person or principal underwriter, have a joint or a joint and several participation, or share in the profits of such enterprise or undertaking, including, but not limited to, any stock option or stock purchase plan, but shall not include an investment advisory contract subject to section 15 of the Act.

The Company respectfully advises the Staff that pursuant to the Merger Agreement, should the Merger Agreement be terminated, an unaffiliated third party may be required to pay a Termination Fee to the Company or OBDE, in certain circumstances if the termination is a result of certain actions by that unaffiliated third party. In no instance can the Termination Fee be paid by an affiliated person (or principal underwriter) of the Company or OBDE pursuant to the terms of the Merger Agreement. As such, the payment, if any, of the Termination Fee cannot result in a joint transaction between the Company and OBDE or any affiliated person (or principal underwriter) of either entity and does not qualify as a “joint enterprise or other joint arrangement or profit-sharing plan” because it is not an arrangement between either the Company or OBDE and an affiliated person (or principal underwriter) of either entity.

11.Comment: Please tell the Staff if Merger Sub is a BDC, and if so, if the Maryland Control Share Act applies to Merger Sub.

Response: The Company respectfully advises the Staff that Merger Sub is not a BDC.

12.Comment: On page 35, in the Comparative Fees and Expenses table, include a pro forma column that assumes the Advisory Agreement Amendment Proposal is not approved since the Merger Proposal and Advisory Agreement Proposal are independent of each other.

Response: The Company has revised the Registration Statement accordingly. A copy of the Comparative Fees and Expenses table marked to show these changes is attached hereto as Annex A.

13.Comment: On page 52, in the fourth paragraph, please remove the underlining in the third sentence.

Response: The Company has revised the Registration Statement accordingly.

14.Comment: Please update the exhibit list to reflect that Stradley Ronan Stevens & Young LLP will not be providing a Form of Opinion and Consent supporting tax matters and clarify for which entities Eversheds Sutherland (US) LLP will be providing a Form of Opinion and Consent supporting tax matters.

Response: The Company has revised the Registration Statement accordingly. The Company confirms that Eversheds Sutherland (US) LLP has acted as special tax counsel to both OBDC and OBDE in connection with the Mergers and will be providing a Form of Opinion and Consent supporting tax matters for both companies, pursuant to sections 8.02(e) and 8.03(d) of the Merger Agreement, as applicable.

15.Comment: Explain whether OBDE Adviser will receive any compensation as part of the termination of the OBDE Investment Advisory Agreement and the OBDE Administration Agreement.

Response: The Company respectfully advises the Staff that OBDE Adviser will not receive any compensation in connection with the termination of the OBDE Investment Advisory Agreement other than any compensation that is otherwise payable to OBDE Adviser under the terms of the agreement as a result of its termination. As the OBDE Investment Advisory Agreement will automatically terminate upon the consummation of the Mergers and, in connection with such termination, OBDE will make a final payment of fees owed under the terms of the OBDE Investment Advisory Agreement to OBDE Adviser as of the date of its termination. As a result, unless such date occurs at the end of a calendar quarter or calendar year, fees otherwise payable at quarter-end or year-end, as applicable, will be payable as of the termination date (instead of at quarter-end or year-end, as applicable). Thus, the Mergers may accelerate the payment of fees previously earned, but will not otherwise cause the payment of an incentive fee. Furthermore, OBDE confirms that the Mergers will not result in OBDE Adviser receiving any other incentive fee or other compensation which it would not receive absent the Mergers.

16.Comment: On page 109, delete the word “certain” from the heading “Certain Material U.S. Federal Income Tax Considerations.” See Staff Legal Bulletin 19(iii)(C)(1).

Response: The Company has revised the Registration Statement accordingly.

17.Comment: On page 110, delete the word “certain” from the heading “Certain Material U.S. Federal Income Tax Considerations.” See Staff Legal Bulletin 19(iii)(C)(1).

Response: The Company has revised the Registration Statement accordingly.

18.Comment: On page 123, in the section “The New Income Fee and Capital Gains Incentive Fee Calculation,” explain why these changes are taking place as a result of the Mergers.

Response: The Company has revised this section of the Registration Statement to include a cross reference to the section “Reasons for the New OBDC Investment Advisory Agreement,” and has changed the heading of this section to “New Income Incentive Fee Calculation and Capital Gains Incentive Fee Calculation.”

In addition, the Company respectfully advises the Staff, on a supplemental basis, that these changes are not taking place as a result of the Mergers, as the Advisory Agreement proposal is separate and non-contingent.

19.Comment: Tell the Staff whether the Form(s) of Opinion and Consent supporting tax matters will be filed in a pre-effective amendment. If not, please provide an undertaking that these will be filed in a post-effective amendment.

Response: The Company confirms that the Forms of Opinion and Consent supporting tax matters will be filed in a pre-effective amendment to the Registration Statement.

20.Comment: Please provide the Staff with exhibits 17(c) and 17(d) as part of correspondence for the Staff to review.

Response: The Company has provided copies of exhibits 17(c) and 17(d) attached hereto as Annex B and Annex C.

21.Comment: Please file the Power of Attorney as an exhibit. See Rule 483(b).

Response: The Company undertakes to file the Power of Attorney as an exhibit in a pre-effective amendment to the Registration Statement.

22.Comment: Please supplementally tell the Staff whether the fund, its adviser, or any of the fund’s affiliates have entered a standstill agreement with respect to the fund and a third party. If yes, provide the Staff with a copy of the agreement or tell us where the agreement is filed on EDGAR. It is our intention to review any such agreements and we may have additional comments. For purposes of this comment, a standstill agreement is an agreement whereby a third party agrees to take or not take one or more specified actions with respect to the fund.

Response: The Company confirms that none of the Company, OBDC Adviser, or any of the Company’s affiliates have entered a standstill agreement with respect to the Company and a third party.

Accounting

1.Comment: Please consider adding disclosure to clarify if any repositioning of the acquired fund’s investment portfolio is anticipated outside of the normal course of investment operations.

Response: The Company has revised the answer to “How does OBDC’s investment objective and strategy differ from OBDE’s?” to add the language underlined below:

As a result of these commonalities, OBDC Adviser and OBDE Adviser do not anticipate any repositioning of OBDE’s investment portfolio outside of the normal course of investment operations. Additionally, the Mergers will not result in a material change to OBDE’s investment portfolio due to investment restrictions or a change in accounting policies.

2.Comment: Please consider adding supplemental financial information disclosure pursuant to Rule 6-11(d)(2) of Regulation S-X to state for the avoidance of doubt that the reorganization will not result in (1) a material change in the acquired fund’s investment portfolio due to investment restrictions or (2) a change in accounting policies.

Response: The Company has revised the Registration Statement accordingly. See the Company’s response to Accounting Comment 1.

3.Comment: In correspondence, please confirm that the current financial condition of the Merger Sub does not trigger any financial information disclosure requirements within the form.

Response: The Company confirms that the current financial condition of Merger Sub does not trigger any financial information disclosure requirements within Form N-14.

4.Comment: Subject to the termination fee’s permissibility under Section 17(d) and Rule 17d-1 under the 1940 Act, please review the termination fee disclosure included on page 32 for consistency with disclosure included on page 25 as the fees payable to the respective parties appear to have been flipped.

Response: The Company has revised the Registration Statement accordingly.

* * *

Please do not hesitate to contact me at (202) 383-0218, Kristin Burns at (212) 287-7023 or Dwaune Dupree (202) 383-0206 if you should need further information or clarification.

| | |

| Sincerely, |

|

| /s/ Cynthia M. Krus |

| Cynthia M. Krus |

Annex A

COMPARATIVE FEES AND EXPENSES

Comparative Fees and Expenses Relating to the Mergers

The following tables are intended to assist OBDC Shareholders and OBDE Shareholders in understanding the costs and expenses that an investor in shares of OBDC Common Stock or OBDE Common Stock bears directly or indirectly and, based on the assumptions set forth below, the pro forma costs and expenses estimated to be incurred by the combined company in the first year following completion of the Mergers. OBDC and OBDE caution you that some of the percentages indicated in the table below are estimates and may vary. Actual expenses may be greater or less than shown. Except where the context suggests otherwise, whenever this document contains a reference to fees or expenses paid or to be paid by “you,” “OBDC” or “OBDE,” investors will indirectly bear such fees or expenses as shareholders of OBDC or OBDE, as applicable. The table below is based on information as of June 30, 2024 (except as noted below) and includes expenses of the applicable consolidated subsidiaries.

| | | | | | | | | | | | | | | | | | | | |

| | Actual | | Pro Forma |

| Shareholder transaction expenses: | | OBDC | | OBDE | | OBDC |

| Sales load (as a percentage of offering price) | | None(1) | | None(1) | | None(1) |

| Offering expenses (as a percentage of offering price) | | None(1) | | None(1) | | None(1) |

| Dividend reinvestment plan fees | | None(2) | | None(2) | | None(2) |

Total shareholder transaction expenses (as a percentage of offering price) | | None | | None | | None |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Estimated annual expenses (as a percentage of net assets attributable to common stock(3)): | | Actual | | Pro Forma | |

| OBDC | | OBDE | | OBDC | | OBDC | |

Base management fees(4) | | 3.1 | % | | 3.1 | % | | 3.1 | % | | 3.1 | % | |

Incentive fees (OBDC: 17.5%; OBDE: 17.5%)(5) | | 2.5 | % | | 2.1 | % | | 2.4 | % | (10) | 2.4 | % | (11) |

Interest payments on borrowed funds (including other costs of servicing and offering debt securities)(6) | | 7.4 | % | | 9.0 | % | | 7.8 | % | | 7.8 | % | |

Other expenses(7) | | 0.5 | % | | 0.7 | % | | 0.4 | % | | 0.4 | % | |

Acquired fund fees and expenses(8) | | 0.8 % | | — % | | 0.6 | % | | 0.6 % | |

Total annual expenses(9) | | 14.3 % | | 14.9 % | | 14.4 % | (10) | 14.4 % | (11) |

______________

(1)Purchases of shares of OBDC Common Stock or OBDE Common Stock on the secondary market are not subject to sales load, but may be subject to brokerage commissions or other charges. The table does not include any sales load (underwriting discounts or commissions) that shareholders may have paid in connection with their purchase of shares of OBDC Common Stock or OBDE Common Stock.

(2)The expenses of administering the OBDC and OBDE dividend reinvestment plans are included in “Other expenses.” For additional information, see “OBDC Dividend Reinvestment Plan” and “OBDE Dividend Reinvestment Plan.”

(3)For the pro forma column, the combined net assets of OBDC and OBDE on a pro forma basis as of June 30, 2024 were used.

(4)For OBDC, the base management fee is 1.50% of OBDC’s average gross assets (excluding cash and cash equivalents but including assets purchased with borrowed amounts); provided however, the base management fee is 1.00% of OBDC’s average gross assets (excluding cash and cash equivalents but including assets purchased with borrowed amounts) that is below an asset coverage ratio of 200% calculated in accordance with Sections 18 and 61 of the 1940 Act, in each case, at the end of the two most recently completed calendar quarters. The management fee for any partial month or quarter, as the case may be, will be appropriately prorated and adjusted for any share issuances or repurchases during the relevant calendar months or quarters, as the case may be. The management fee reflected in the table is calculated by determining the ratio that the management fee bears to OBDC’s net assets attributable to common stock (rather than its gross assets).

For OBDE, the base management fee is 1.50% of OBDE’s average gross assets (excluding cash and cash equivalents but including assets purchased with borrowed amounts); provided however, the base management fee is 1.00% of OBDE’s average gross assets (excluding cash and cash equivalents but including assets purchased with borrowed amounts) that is below an asset coverage ratio of 200% calculated in accordance with Sections 18 and 61 of the 1940 Act, in each case, at the end of the two most recently completed calendar quarters. The management fee for any partial month or quarter, as the case may be, will be appropriately prorated and adjusted for any share issuances or

repurchases during the relevant calendar months or quarters, as the case may be. The management fee reflected in the table is calculated by determining the ratio that the management fee bears to OBDE’s net assets attributable to common stock (rather than its gross assets).

Following completion of the Mergers, the combined company will be externally managed by OBDC Adviser. The pro forma base

management fee is the same under both the New OBDC Investment Advisory Agreement and Current OBDC Investment Advisory Agreement. The pro forma base management fee referenced in the table above is based on the combined gross assets (excluding cash andcash equivalents) of OBDC and OBDE on a pro forma basis as of June 30, 2024. For a discussion of the New OBDC Investment Advisory Agreement, see “OBDC Proposal II: Approval of the Advisory Agreement Amendment Proposal.”

(5)For OBDC, the incentive fee consists of two components that are independent of each other, with the result that one component may be payable even if the other is not. A portion of the incentive fee is based on OBDC’s income and a portion is based on OBDC’s capital gains, For more detailed information about OBDC’s incentive fee, see “Part I, Item 1 BUSINESS – Investment Advisory Agreement” in OBDC’s Annual Report on Form 10-K for the fiscal year ended December 31, 2023. For OBDE, the incentive fee consists of two components that are independent of each other, with the result that one component may be payable even if the other is not. A portion of the incentive fee is based on OBDE’s income and a portion is based on OBDE’s capital gains. For more detailed information about the incentive fee, see “Part I, Item 1 BUSINESS – Investment Advisory Agreement” in OBDE’s Annual Report on Form 10-K for the fiscal year ended December 31, 2023. Following completion of the Mergers, the combined company will be externally managed by OBDC Adviser. The pro forma incentive fee has been calculated in accordance with the terms of the New OBDC Investment Advisory Agreement and assumes that the Advisory Agreement Amendment Proposal is approved by OBDC Shareholders. The pro forma incentive fee referenced in the table above is based on the actual amounts of the income component of the incentive fee for OBDC and OBDE on a pro forma basis for the six months ended June 30, 2024, annualized for a full year and calculated under the New OBDC Investment Advisory Agreement and the amount payable under the New OBDC Investment Advisory Agreement for the capital gains component as of June 30, 2024, assuming the Mergers closed on June 30, 2024.

(6)For OBDC, the figure in the table represents OBDC’s interest expenses based on actual interest and credit facility expenses incurred for the six months ended June 30, 2024, which includes the impact of interest rate swaps. During the six months ended June 30, 2024, OBDC’s average borrowings outstanding were $7.3 billion and OBDC’s interest expense incurred was $228.3 million. OBDC had outstanding borrowings of approximately $7.5 billion as of June 30, 2024. Interest payments on borrowed funds represents an estimate of OBDC’s annualized interest expense based on borrowings under the OBDC Revolving Credit Facility, the SPV Asset Facility, the 2025 Notes, July 2025 Notes, the 2026 Notes, the July 2026 Notes, the 2027 Notes, the 2028 Notes, the 2029 Notes, the CLO I Transaction, the CLO II Transaction, the CLO III Transaction, the CLO IV Transaction, the CLO V Transaction, the CLO VII Transaction and the CLO X Transaction. The assumed weighted average interest rate on OBDC’s total debt outstanding was 5.7%. OBDC may borrow additional funds from time to time to make investments to the extent OBDC determines that the economic situation is conducive to doing so. OBDC may also issue additional debt securities or preferred stock, subject to OBDC’s compliance with applicable requirements under the 1940 Act.

For OBDE, the figure in the table represents OBDE’s interest expenses based on actual interest and credit facility expenses incurred for the six months ended June 30, 2024. During the six months ended June 30, 2024, OBDE’s average borrowings outstanding were $2.1 billion and OBDE’s interest expense incurred was $78.5 million. OBDE had outstanding borrowings of approximately $2.5 billion as of June 30, 2024. Interest payments on borrowed funds represents an estimate of OBDE’s annualized interest expense based on borrowings under the OBDE Revolving Credit Facility, SPV Asset Facility I, SPV Asset Facility II, SPV Asset Facility III, 2027 Notes, July 2025 Notes, July 2027 Notes, Series 2023A Notes and CLO XIV Transaction. The assumed weighted average interest rate on OBDE’s total debt outstanding was 7.1%. OBDE may borrow additional funds from time to time to make investments to the extent OBDE determines that the economic situation is conducive to doing so. OBDE may also issue additional debt securities or preferred stock, subject to OBDE compliance with applicable requirements under the 1940 Act.

The “Pro Forma” column assumes the sum of amounts of average borrowings during the six months ended June 30, 2024 for each of OBDC and OBDE for the combined company following the Mergers.

(7)“Other expenses” are based on estimated amounts for the current fiscal year for each of OBDC and OBDE. These expenses include certain expenses allocated to the applicable company under the Current OBDC Investment Advisory Agreement and the OBDE Investment Advisory Agreement, as applicable. The “Pro Forma” column assumes the sum of amounts estimated for each of OBDC and OBDE for the combined company following the Mergers and reflects decreases in duplicative costs such as professional fees for legal, audit and tax fees, directors’ fees, and other redundant administrative and operating expenses directly related to the Mergers. “Other expenses” does not reflect any potential provision (benefit) for income taxes because of the uncertainties associated with determining such amounts in future periods.

(8)OBDC Shareholders indirectly bear the expenses of underlying funds or other investment vehicles that would be an investment company under section 3(a) of the 1940 Act but for the exceptions to that definition provided for in sections 3(c)(1) and 3(c)(7) of the 1940 Act in which OBDC invests.

For OBDC, this amount includes the annual expenses of OBDC SLF LLC (“OBDC SLF”). There are no fees paid by OBDC SLF to OBDC. See note 4 in the notes to the Consolidated Financial Statements in OBDC’s Annual Report on Form 10-K for the fiscal year ended December 31, 2023 for more information on OBDC SLF. OBDE has no such investments.

The “Pro Forma” column assumes the sum of amounts for each of OBDC and OBDE for the combined company following the Mergers.

(9)“Total annual expenses” is presented as a percentage of net assets attributable to holders of common stock because OBDC Shareholders and OBDE Shareholders bear all of the fees and expenses of the respective company. “Total annual expenses” does not reflect any potential provision (benefit) for income taxes because of the uncertainties associated with determining such amounts in future periods.

(10)Following completion of the Mergers, the combined company will be externally managed by OBDC Adviser. The pro forma incentive fee has been calculated in accordance with the terms of the New OBDC Investment Advisory Agreement and assumes that the Advisory Agreement Amendment Proposal is approved by OBDC Shareholders. The pro forma incentive fee as a percentage of NAV is 2.39% rounded to two decimal places and is based on the actual amounts of the income component of the incentive fee for OBDC and OBDE on a pro forma basis for the six months ended June 30, 2024, annualized for a full year and calculated under the New OBDC Investment Advisory Agreement and the amount payable under the New OBDC Investment Advisory Agreement for the capital gains component as of

June 30, 2024, assuming the Mergers closed on June 30, 2024. The resulting proforma total annual expense is 14.39% rounded to two decimal places.

(11)Following completion of the Mergers, the combined company will be externally managed by OBDC Adviser. The pro forma incentive fee has been calculated in accordance with the terms of the Current OBDC Investment Advisory Agreement and assumes that the Advisory Agreement Amendment Proposal is not approved by OBDC Shareholders. The pro forma incentive fee as a percentage of NAV is 2.44% rounded to two decimal places and is based on the actual amounts of the income component of the incentive fee for OBDC and OBDE on a pro forma basis for the six months ended June 30, 2024, annualized for a full year and calculated under the Current OBDC Investment Advisory Agreement and the amount payable under the Current OBDC Investment Advisory Agreement for the capital gains component as of June 30, 2024, assuming the Mergers closed on June 30, 2024. The resulting proforma total annual expense is 14.44% rounded to two decimal places.

Example

The following example demonstrates the projected dollar amount of total cumulative expenses that would be incurred over various periods with respect to a hypothetical investment in OBDC, OBDE or the combined company’s common stock following completion of the Mergers on a pro forma basis, in each case assuming that OBDC, OBDE and the combined company hold no cash or liabilities other than debt. In calculating the following expense amounts, each of OBDC and OBDE has assumed that it would have no additional leverage and that its annual operating expenses would remain at the levels set forth in the tables above. Calculations for the pro forma combined company following the Mergers assume that the Mergers closed on June 30, 2024 and that the leverage and operating expenses of OBDC and OBDE remain at the levels set forth in the tables above. Transaction expenses related to the Mergers are not included in the following examples.

| | | | | | | | | | | | | | | | | | | | | | | |

| 1 year | | 3 years | | 5 years | | 10 years |

You would pay the following expenses on a $1,000 investment: | | | | | | | |

| OBDC, assuming a 5% annual return (assumes no return from net realized capital gains) | $ | 110 | | | $ | 330 | | | $ | 550 | | | $ | 1,100 | |

| OBDE, assuming a 5% annual return (assumes no return from net realized capital gains) | $ | 128 | | | $ | 377 | | | $ | 618 | | | $ | 1,183 | |

| OBDC, assuming a 5% annual return (assumes return entirely from realized capital gains) | $ | 128 | | | $ | 378 | | | $ | 618 | | | $ | 1,179 | |

| OBDE, assuming a 5% annual return (assumes return entirely from realized capital gains) | $ | 146 | | | $ | 423 | | | $ | 680 | | | $ | 1,243 | |

| | | | | | | | | | | | | | | | | | | | | | | |

| 1 year | | 3 years | | 5 years | | 10 years |

Pro forma combined company following the Mergers You would pay the following expenses on a $1,000 investment: | | | | | | | |

Assuming a 5% annual return (assumes no return from net realized capital gains) | $ | 114 | | | $ | 340 | | | $ | 564 | | | $ | 1,120 | |

Assuming a 5% annual return (assumes return entirely from realized capital gains) | $ | 132 | | | $ | 387 | | | $ | 631 | | | $ | 1,194 | |

The foregoing tables are intended to assist you in understanding the various costs and expenses that an investor in OBDC, OBDE or, following the Mergers, the combined company will bear directly or indirectly. While the example assumes, as required by the SEC, a 5% annual return, performance of OBDC, OBDE and the combined company will vary and may result in a return greater or less than 5%. The incentive fee based on pre-incentive fee NII under each of the Current OBDC Investment Advisory Agreement, the New OBDC Investment Advisory Agreement and the OBDE Investment Advisory Agreement, which, assuming a 5% annual return, would either not be payable or would have an insignificant impact on the expense amounts shown above, is not included in the example. If sufficient returns are achieved on investments, including through the realization of capital gains, to trigger an incentive fee of a material amount, expenses, and returns to investors, would be higher. This example assumes that, as of June 30, 2024, the sum of realized capital losses and unrealized capital depreciation on a cumulative basis since IPO for OBDC and since the OBDE Exchange Listing for OBDE is zero. In addition, while

the example assumes reinvestment of all distributions at NAV, participants in OBDC’s dividend reinvestment plan will receive a number of shares of OBDC Common Stock determined by dividing the total dollar amount of the cash distribution payable to a participant by either (i) the greater of (a) the current NAV per share of OBDC Common Stock and (b) 95% of the market price per share of OBDC Common Stock at the close of trading on the payment date fixed by the OBDC Board in the event that newly issued shares are used to satisfy the share requirements of the dividend reinvestment plan or (ii) the average purchase price, excluding any brokerage charges or other charges, of all shares of OBDC Common Stock purchased by the administrator of the dividend reinvestment plan in the event that shares are purchased in the open market to satisfy the share requirements of the dividend reinvestment plan, which may be at, above or below NAV.

The example and the expenses in the table above should not be considered a representation of OBDC’s, OBDE’s, or, following completion of the Mergers, the combined company’s, future expenses, and actual expenses may be greater or less than those shown.

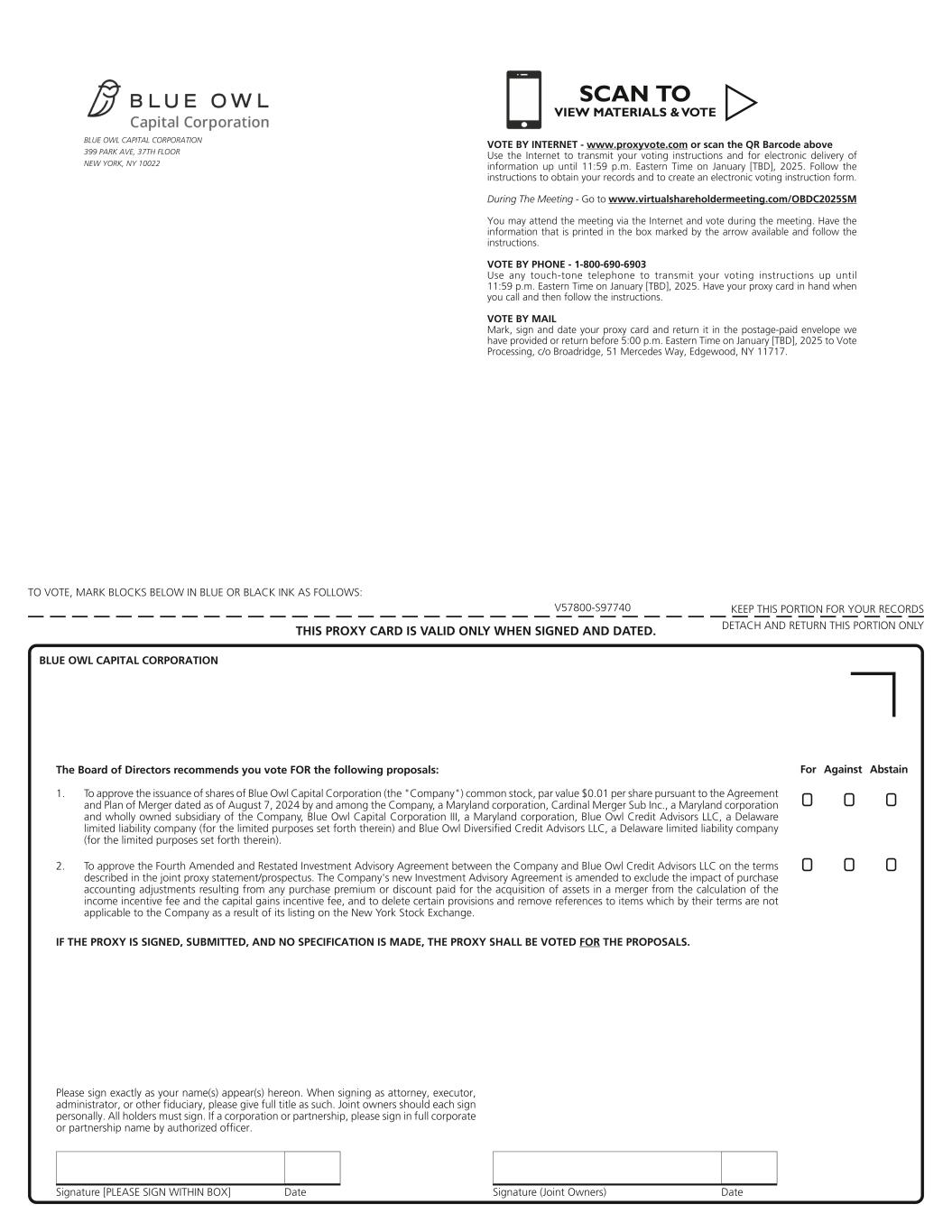

Annex B

Signature [PLEASE SIGN WITHIN BOX] Date Signature (Joint Owners) Date TO VOTE, MARK BLOCKS BELOW IN BLUE OR BLACK INK AS FOLLOWS: KEEP THIS PORTION FOR YOUR RECORDS DETACH AND RETURN THIS PORTION ONLYTHIS PROXY CARD IS VALID ONLY WHEN SIGNED AND DATED. V57800-S97740 BLUE OWL CAPITAL CORPORATION 399 PARK AVE, 37TH FLOOR NEW YORK, NY 10022 BLUE OWL CAPITAL CORPORATION The Board of Directors recommends you vote FOR the following proposals: Please sign exactly as your name(s) appear(s) hereon. When signing as attorney, executor, administrator, or other fiduciary, please give full title as such. Joint owners should each sign personally. All holders must sign. If a corporation or partnership, please sign in full corporate or partnership name by authorized officer. IF THE PROXY IS SIGNED, SUBMITTED, AND NO SPECIFICATION IS MADE, THE PROXY SHALL BE VOTED FOR THE PROPOSALS. 1. To approve the issuance of shares of Blue Owl Capital Corporation (the "Company") common stock, par value $0.01 per share pursuant to the Agreement and Plan of Merger dated as of August 7, 2024 by and among the Company, a Maryland corporation, Cardinal Merger Sub Inc., a Maryland corporation and wholly owned subsidiary of the Company, Blue Owl Capital Corporation III, a Maryland corporation, Blue Owl Credit Advisors LLC, a Delaware limited liability company (for the limited purposes set forth therein) and Blue Owl Diversified Credit Advisors LLC, a Delaware limited liability company (for the limited purposes set forth therein). ! !! ! !! For Against Abstain 2. To approve the Fourth Amended and Restated Investment Advisory Agreement between the Company and Blue Owl Credit Advisors LLC on the terms described in the joint proxy statement/prospectus. The Company's new Investment Advisory Agreement is amended to exclude the impact of purchase accounting adjustments resulting from any purchase premium or discount paid for the acquisition of assets in a merger from the calculation of the income incentive fee and the capital gains incentive fee, and to delete certain provisions and remove references to items which by their terms are not applicable to the Company as a result of its listing on the New York Stock Exchange. SCAN TO VIEW MATERIALS & VOTEw VOTE BY INTERNET - www.proxyvote.com or scan the QR Barcode above Use the Internet to transmit your voting instructions and for electronic delivery of information up until 11:59 p.m. Eastern Time on January [TBD], 2025. Follow the instructions to obtain your records and to create an electronic voting instruction form. During The Meeting - Go to www.virtualshareholdermeeting.com/OBDC2025SM You may attend the meeting via the Internet and vote during the meeting. Have the information that is printed in the box marked by the arrow available and follow the instructions. VOTE BY PHONE - 1-800-690-6903 Use any touch-tone telephone to transmit your voting instructions up until 11:59 p.m. Eastern Time on January [TBD], 2025. Have your proxy card in hand when you call and then follow the instructions. VOTE BY MAIL Mark, sign and date your proxy card and return it in the postage-paid envelope we have provided or return before 5:00 p.m. Eastern Time on January [TBD], 2025 to Vote Processing, c/o Broadridge, 51 Mercedes Way, Edgewood, NY 11717.

V57801-S97740 Important Notice Regarding the Availability of Proxy Materials for the Special Meeting: The Notice and Joint Prospectus/Proxy Statement are available at www.proxyvote.com. NOTICE IS HEREBY GIVEN THAT the special meeting of shareholders (the “Special Meeting”) of Blue Owl Capital Corporation, a Maryland corporation (the "Company"), will be held on January [TBD], 2025 at 9:00 a.m. Eastern Time. The Special Meeting will be a completely virtual meeting, which will be conducted via live webcast. You will be able to attend the Special Meeting online and submit your questions during the meeting by visiting www.virtualshareholdermeeting.com/OBDC2025SM. BLUE OWL CAPITAL CORPORATION Special Meeting of Shareholders January [TBD], 2025 at 9:00 A.M. Eastern Time This proxy is solicited by the Board of Directors The undersigned shareholder of Blue Owl Capital Corporation hereby appoints Neena A. Reddy and Jonathan Lamm, or either of them, as proxies for the undersigned, with full power of substitution in either of them, to attend the Special Meeting of Shareholders of Blue Owl Capital Corporation to be held on January [TBD], 2025 at 9:00 A.M. Eastern Time, virtually at www.virtualshareholdermeeting.com/OBDC2025SM, and any and all adjournments and postponements thereof, with all power possessed by the undersigned as if personally present and to vote in their discretion on such other matters as may properly come before the meeting. The undersigned hereby acknowledges receipt of the Notice of Special Meeting of Shareholders and the accompanying Joint Prospectus/Proxy Statement, and revokes any proxy heretofore given with respect to such meeting. This proxy is solicited on behalf of the Blue Owl Capital Corporation board of directors. In their discretion, the proxies are authorized to vote upon such other business as may properly come before the Special Meeting of Shareholders or any adjournments or postponements thereof in accordance with the recommendation of the board of directors or, in the absence of such a recommendation, in their discretion, including, but not limited to, matters incident to the conduct of the meeting or a motion to adjourn or postpone the meeting to another time and/or place for the purpose of soliciting additional proxies for any or all of the proposals referenced herein. If you sign, date, and return this proxy, it will be voted as directed or, if no direction is indicated, will be voted in accordance with the Board of Directors' recommendations. Continued and to be signed on reverse side YOUR VOTE IS VERY IMPORTANT! Your immediate response will help avoid potential delays and may save the Company significant additional expenses associated with soliciting Shareholder votes.

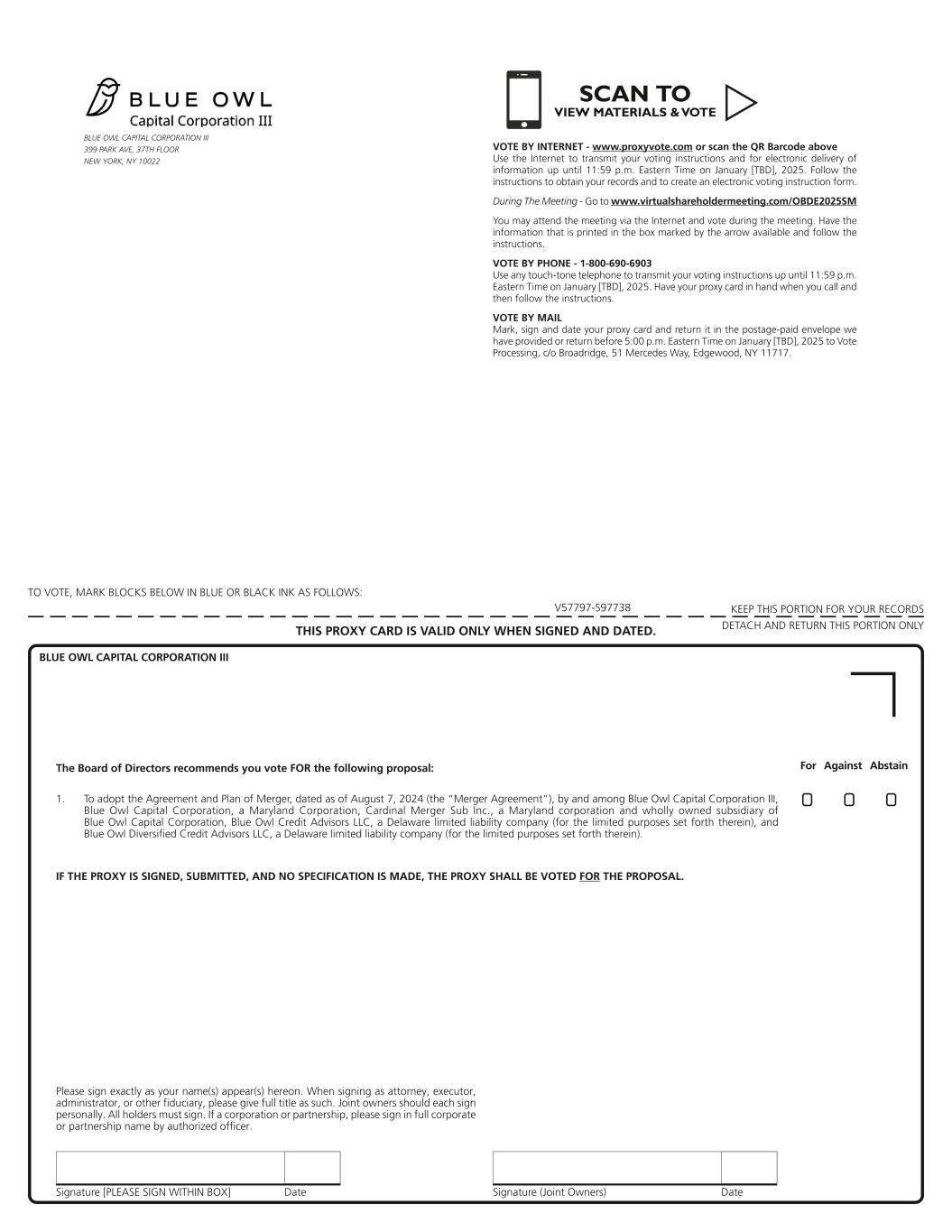

Annex C

Signature [PLEASE SIGN WITHIN BOX] Date Signature (Joint Owners) Date TO VOTE, MARK BLOCKS BELOW IN BLUE OR BLACK INK AS FOLLOWS: KEEP THIS PORTION FOR YOUR RECORDS DETACH AND RETURN THIS PORTION ONLYTHIS PROXY CARD IS VALID ONLY WHEN SIGNED AND DATED. V57797-S97738 BLUE OWL CAPITAL CORPORATION III 399 PARK AVE, 37TH FLOOR NEW YORK, NY 10022 For Against Abstain BLUE OWL CAPITAL CORPORATION III 1. To adopt the Agreement and Plan of Merger, dated as of August 7, 2024 (the “Merger Agreement”), by and among Blue Owl Capital Corporation III, Blue Owl Capital Corporation, a Maryland Corporation, Cardinal Merger Sub Inc., a Maryland corporation and wholly owned subsidiary of Blue Owl Capital Corporation, Blue Owl Credit Advisors LLC, a Delaware limited liability company (for the limited purposes set forth therein), and Blue Owl Diversified Credit Advisors LLC, a Delaware limited liability company (for the limited purposes set forth therein). Please sign exactly as your name(s) appear(s) hereon. When signing as attorney, executor, administrator, or other fiduciary, please give full title as such. Joint owners should each sign personally. All holders must sign. If a corporation or partnership, please sign in full corporate or partnership name by authorized officer. The Board of Directors recommends you vote FOR the following proposal: IF THE PROXY IS SIGNED, SUBMITTED, AND NO SPECIFICATION IS MADE, THE PROXY SHALL BE VOTED FOR THE PROPOSAL. ! !! VOTE BY INTERNET - www.proxyvote.com or scan the QR Barcode above Use the Internet to transmit your voting instructions and for electronic delivery of information up until 11:59 p.m. Eastern Time on January [TBD], 2025. Follow the instructions to obtain your records and to create an electronic voting instruction form. During The Meeting - Go to www.virtualshareholdermeeting.com/OBDE2025SM You may attend the meeting via the Internet and vote during the meeting. Have the information that is printed in the box marked by the arrow available and follow the instructions. VOTE BY PHONE - 1-800-690-6903 Use any touch-tone telephone to transmit your voting instructions up until 11:59 p.m. Eastern Time on January [TBD], 2025. Have your proxy card in hand when you call and then follow the instructions. VOTE BY MAIL Mark, sign and date your proxy card and return it in the postage-paid envelope we have provided or return before 5:00 p.m. Eastern Time on January [TBD], 2025 to Vote Processing, c/o Broadridge, 51 Mercedes Way, Edgewood, NY 11717. SCAN TO VIEW MATER

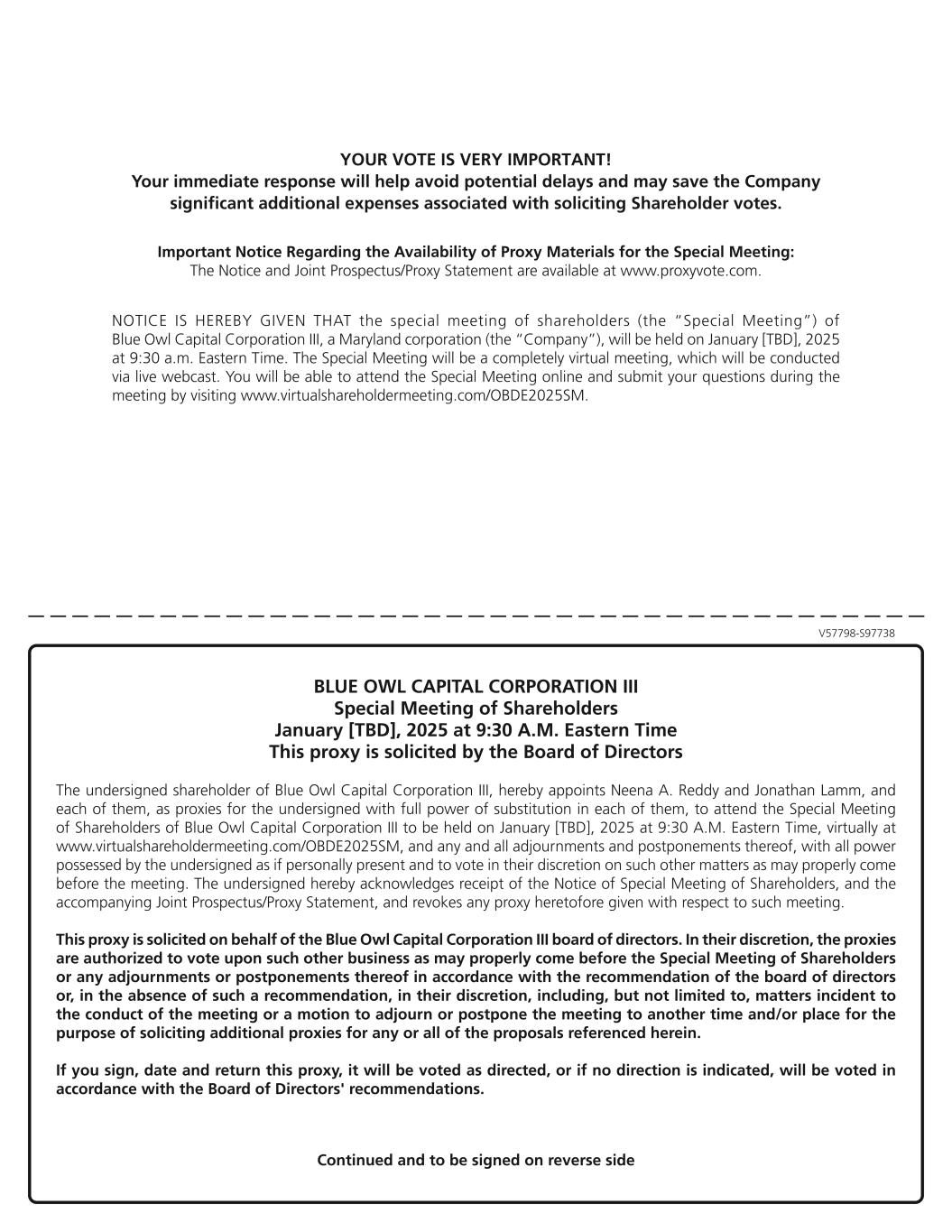

V57798-S97738 NOTICE IS HEREBY GIVEN THAT the special meeting of shareholders (the “Special Meeting”) of Blue Owl Capital Corporation III, a Maryland corporation (the “Company”), will be held on January [TBD], 2025 at 9:30 a.m. Eastern Time. The Special Meeting will be a completely virtual meeting, which will be conducted via live webcast. You will be able to attend the Special Meeting online and submit your questions during the meeting by visiting www.virtualshareholdermeeting.com/OBDE2025SM. Important Notice Regarding the Availability of Proxy Materials for the Special Meeting: The Notice and Joint Prospectus/Proxy Statement are available at www.proxyvote.com. YOUR VOTE IS VERY IMPORTANT! Your immediate response will help avoid potential delays and may save the Company significant additional expenses associated with soliciting Shareholder votes. BLUE OWL CAPITAL CORPORATION III Special Meeting of Shareholders January [TBD], 2025 at 9:30 A.M. Eastern Time This proxy is solicited by the Board of Directors The undersigned shareholder of Blue Owl Capital Corporation III, hereby appoints Neena A. Reddy and Jonathan Lamm, and each of them, as proxies for the undersigned with full power of substitution in each of them, to attend the Special Meeting of Shareholders of Blue Owl Capital Corporation III to be held on January [TBD], 2025 at 9:30 A.M. Eastern Time, virtually at www.virtualshareholdermeeting.com/OBDE2025SM, and any and all adjournments and postponements thereof, with all power possessed by the undersigned as if personally present and to vote in their discretion on such other matters as may properly come before the meeting. The undersigned hereby acknowledges receipt of the Notice of Special Meeting of Shareholders, and the accompanying Joint Prospectus/Proxy Statement, and revokes any proxy heretofore given with respect to such meeting. This proxy is solicited on behalf of the Blue Owl Capital Corporation III board of directors. In their discretion, the proxies are authorized to vote upon such other business as may properly come before the Special Meeting of Shareholders or any adjournments or postponements thereof in accordance with the recommendation of the board of directors or, in the absence of such a recommendation, in their discretion, including, but not limited to, matters incident to the conduct of the meeting or a motion to adjourn or postpone the meeting to another time and/or place for the purpose of soliciting additional proxies for any or all of the proposals referenced herein. If you sign, date and return this proxy, it will be voted as directed, or if no direction is indicated, will be voted in accordance with the Board of Directors' recommendations. Continued and to be signed on reverse side