Please wait

.3

| | | | | | | | |

| Interim Management Discussion and Analysis |

| | | | | | | | | | | | | | |

| Contents |

| About Fortis | 1 | | Cash Flow Summary | 13 |

| Performance at a Glance | 2 | | Contractual Obligations | 15 |

| Business Unit Performance | 5 | | Capital Structure and Credit Ratings | 15 |

| ITC | 5 | | Capital Plan | 16 |

| UNS Energy | 5 | | Business Risks | 19 |

| Central Hudson | 6 | | Accounting Matters | 19 |

| FortisBC Energy | 7 | | Financial Instruments | 20 |

| FortisAlberta | 7 | | Long-Term Debt and Other | 20 |

| FortisBC Electric | 8 | | Derivatives | 20 |

| Other Electric | 8 | | Summary of Quarterly Results | 20 |

| Corporate and Other | 9 | | Related-Party and Inter-Company Transactions | 21 |

| Non-U.S. GAAP Financial Measures | 9 | | Outlook | 21 |

| Regulatory Matters | 10 | | Forward-Looking Information | 22 |

| Financial Position | 11 | | Glossary | 23 |

| Liquidity and Capital Resources | 12 | | Condensed Consolidated Interim Financial Statements (Unaudited) | F-1 |

| Cash Flow Requirements | 12 | | | |

| | | | |

Dated November 3, 2025

This Interim MD&A has been prepared in accordance with National Instrument 51-102 - Continuous Disclosure Obligations. It should be read in conjunction with the Interim Financial Statements, the 2024 Annual Financial Statements and the 2024 Annual MD&A and is subject to the cautionary statement and disclaimer provided under "Forward-Looking Information" on page 22. Further information about Fortis, including its Annual Information Form can be accessed at www.fortisinc.com, www.sedarplus.ca, or www.sec.gov.

Financial information herein has been prepared in accordance with U.S. GAAP (except for indicated Non-U.S. GAAP Financial Measures) and, unless otherwise specified, is presented in Canadian dollars based, as applicable, on the following U.S. dollar-to-Canadian dollar exchange rates: (i) average of 1.38 and 1.36 for the quarters ended September 30, 2025 and 2024, respectively; (ii) average of 1.40 and 1.36 year-to-date September 30, 2025 and 2024, respectively; (iii) 1.39 and 1.35 as at September 30, 2025 and 2024, respectively; (iv) 1.44 as at December 31, 2024; (v) 1.38 for the 2025 annual forecast; and (vi) 1.35 for all other forecast periods. Certain terms used in this Interim MD&A are defined in the "Glossary" on page 23.

ABOUT FORTIS

Fortis (TSX/NYSE: FTS) is a diversified leader in the North American regulated electric and gas utility industry, with 2024 revenue of $12 billion and total assets of $75 billion as at September 30, 2025. The Corporation's 9,600 employees serve 3.5 million utility customers in five Canadian provinces, ten U.S. states and the Caribbean.

For additional information on the Corporation's operations, reportable segments and strategy, refer to the "About Fortis" section of the 2024 Annual MD&A and Note 1 to the Interim Financial Statements.

| | | | | | | | | | | |

1 | FORTIS INC. | SEPTEMBER 30, 2025 QUARTER REPORT | |

| | | | | | | | |

| Interim Management Discussion and Analysis | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| PERFORMANCE AT A GLANCE | | | | | | |

| Key Financial Metrics | | | |

| Periods ended September 30 | Quarter | | Year-to-Date |

($ millions, except as indicated) | 2025 | | | 2024 | | | Variance | | 2025 | | | 2024 | | | Variance |

| Revenue | 2,938 | | | 2,771 | | | 167 | | | 9,091 | | | 8,559 | | | 532 | |

| Common Equity Earnings | | | | | | | | | | | |

| Actual | 409 | | | 420 | | | (11) | | | 1,292 | | | 1,210 | | | 82 | |

Adjusted (1) | 441 | | | 420 | | | 21 | | | 1,324 | | | 1,210 | | | 114 | |

Basic EPS ($) | | | | | | | | | | | |

| Actual | 0.81 | | | 0.85 | | | (0.04) | | | 2.57 | | | 2.45 | | | 0.12 | |

Adjusted (1) | 0.87 | | | 0.85 | | | 0.02 | | | 2.63 | | | 2.45 | | | 0.18 | |

Dividends paid per common share ($) | 0.615 | | | 0.590 | | | 0.025 | | | 1.845 | | | 1.770 | | | 0.075 | |

Weighted average number of common shares outstanding (# millions) | 504.5 | | | 496.2 | | | 8.3 | | | 502.5 | | | 493.9 | | | 8.6 | |

| Operating Cash Flow | 1,027 | | | 1,338 | | | (311) | | | 3,044 | | | 2,920 | | | 124 | |

Capital Expenditures (1) | 1,316 | | | 1,300 | | | 16 | | | 4,171 | | | 3,554 | | | 617 | |

(1)See "Non-U.S. GAAP Financial Measures" on page 9

Revenue

The increase in revenue for the quarter was due to: (i) Rate Base growth; (ii) higher flow-through costs in customer rates; (iii) higher customer delivery rates, as approved by the PSC effective July 1, 2025 in relation to Central Hudson's 2025 general rate application; and (iv) the higher U.S. dollar-to-Canadian dollar exchange rate.

The increase in revenue year to date was due to: (i) Rate Base growth; (ii) higher flow-through costs in customer rates; (iii) higher customer delivery rates effective July 1, 2024 and 2025 as approved by the PSC; and (iv) the higher U.S. dollar-to-Canadian dollar exchange rate. The increase was partially offset by lower wholesale sales revenue at UNS Energy, reflecting a reduction in short-term wholesale electricity sales as well as lower pricing due to market conditions.

Earnings and EPS

Common Equity Earnings decreased by $11 million compared to the third quarter of 2024. The decrease was due to income taxes and closing costs totalling $32 million associated with the disposition of FortisTCI in September 2025.

Excluding the above-noted item, Common Equity Earnings increased by $21 million compared to the third quarter of 2024. The increase was primarily due to Rate Base growth across the utilities, including AFUDC associated with Major Capital Projects. The higher U.S. dollar-to-Canadian dollar exchange rate also contributed to the increase in earnings. The increase was partially offset by higher costs associated with Rate Base growth not yet reflected in customer rates at UNS Energy, the expiration of a regulatory incentive and a lower allowed ROE at FortisAlberta, and higher holding company finance costs.

On a year-to-date basis, and excluding the impact of the disposition of FortisTCI as discussed above, Common Equity Earnings increased by $114 million compared to the prior year. The increase was due to the factors discussed for the quarter, and also reflected growth at Central Hudson due to the rebasing of costs and a higher allowed ROE effective July 1, 2024 and the timing of operating costs in 2025. The increase was partially offset by lower margin on wholesale sales at UNS Energy and the timing of operating costs at FortisAlberta.

In addition to the above-noted items impacting earnings, the change in basic EPS for the quarter and year-to-date periods reflected an increase in the weighted average number of common shares outstanding, largely associated with the Corporation's DRIP.

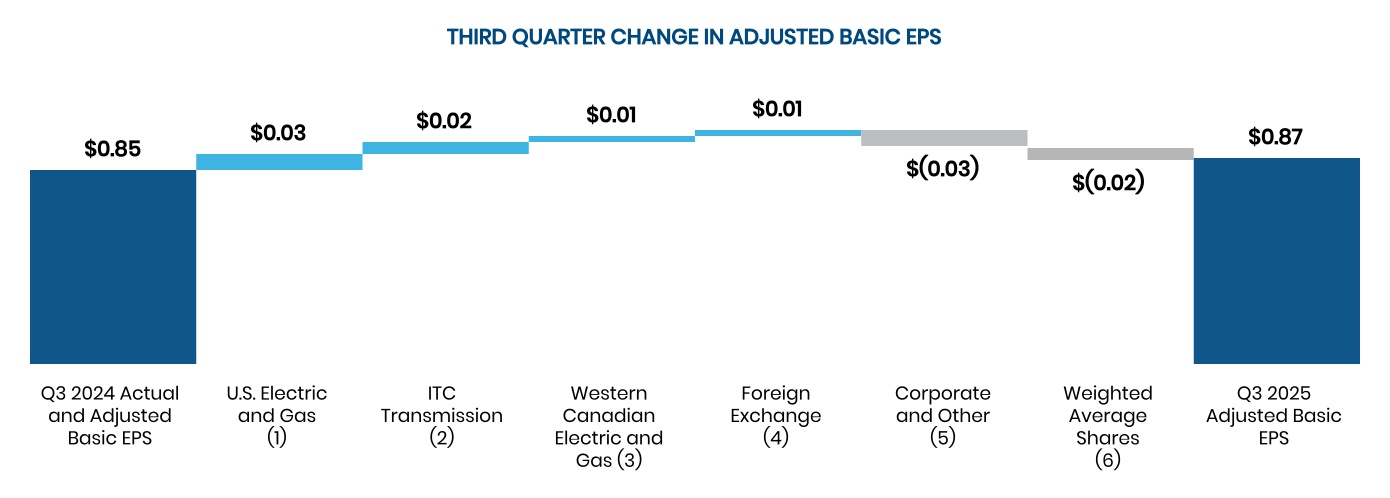

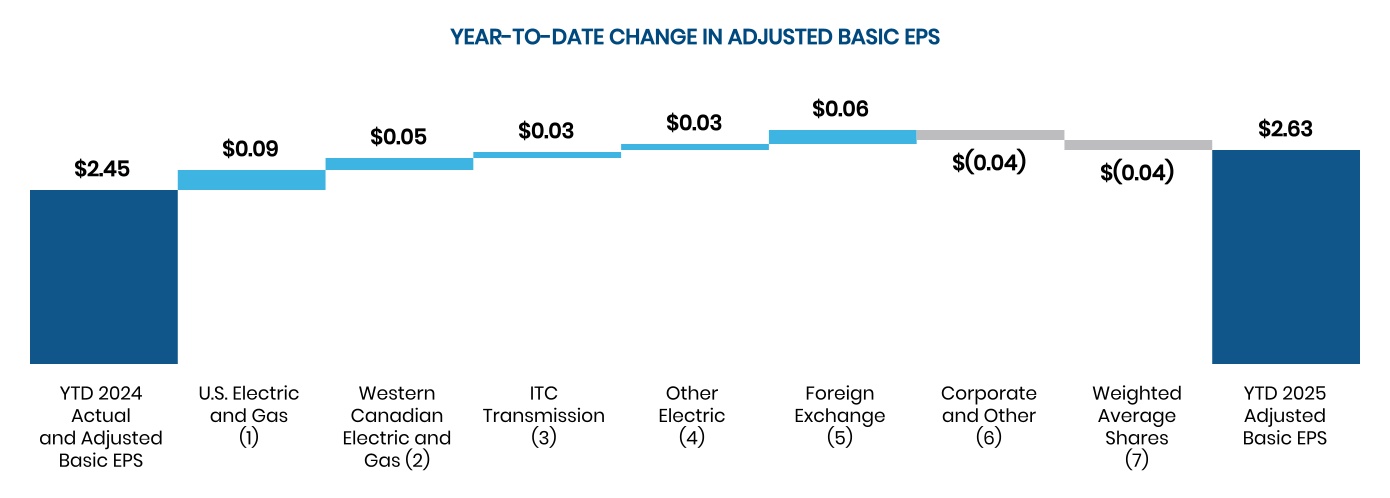

For the quarter and year-to-date periods: (i) Adjusted Common Equity Earnings increased by $21 million and $114 million, respectively, as discussed above; and (ii) Adjusted Basic EPS increased by $0.02 and $0.18, respectively. Refer to "Non-U.S. GAAP Financial Measures" on page 9 for a reconciliation of these measures. The changes in Adjusted Basic EPS for the quarter and year-to-date periods are illustrated in the following charts.

| | | | | | | | | | | |

2 | FORTIS INC. | SEPTEMBER 30, 2025 QUARTER REPORT | |

| | | | | | | | |

| Interim Management Discussion and Analysis | |

(1) Includes UNS Energy and Central Hudson. Reflects higher earnings at Central Hudson due to Rate Base growth and a change in a regulatory deferral for uncollectible accounts as approved in the order on the 2025 general rate application, partially offset by higher costs associated with a contribution to a customer benefit fund. Also reflects higher earnings at UNS Energy due to an increase in transmission revenue and higher AFUDC associated with ongoing Major Capital Projects, partially offset by higher costs associated with Rate Base growth not yet reflected in customer rates

(2) Reflects Rate Base growth, partially offset by an increase in non-recoverable stock-based compensation costs and higher holding company finance costs

(3) Includes FortisBC Energy, FortisAlberta and FortisBC Electric. Reflects Rate Base growth, including earnings associated with FortisBC Energy's investment in the Eagle Mountain Pipeline project, partially offset by the expiration of the PBR efficiency carry over mechanism at the end of 2024, and a lower allowed ROE effective January 1, 2025 at FortisAlberta

(4) Reflects the change in the average U.S. dollar-to-Canadian dollar exchange rate

(5) Reflects higher holding company costs, unrealized losses on foreign exchange contracts, and lower unrealized gains on total return swaps

(6) Weighted average shares of 504.5 million in 2025 compared to 496.2 million in 2024

(1) Includes UNS Energy and Central Hudson. Reflects higher earnings at Central Hudson due to Rate Base growth, the rebasing of costs and a higher allowed ROE effective July 1, 2024, the timing of operating costs, and a change in a regulatory deferral for uncollectible accounts as approved in the order on the 2025 general rate application. Also reflects lower earnings at UNS Energy due to lower margin on wholesale sales and higher costs associated with Rate Base growth not yet reflected in customer rates, partially offset by higher transmission revenue and AFUDC

(2) Includes FortisBC Energy, FortisAlberta and FortisBC Electric. Reflects higher earnings at FortisBC due to Rate Base growth, including earnings associated with FortisBC Energy's investment in the Eagle Mountain Pipeline project. Also reflects lower earnings at FortisAlberta primarily due to the timing of operating costs, the expiration of the PBR efficiency carry-over mechanism at the end of 2024, and a lower allowed ROE effective January 1, 2025

(3) Reflects Rate Base growth, partially offset by an increase in non-recoverable stock-based compensation costs and higher holding company finance costs

(4) Primarily reflects higher electricity sales, Rate Base growth, as well as the timing of earnings at Newfoundland Power, partially offset by the September 2025 disposition of FortisTCI

(5) Reflects the change in the average U.S. dollar-to-Canadian dollar exchange rate and the revaluation of U.S. dollar denominated liabilities

(6) Reflects higher holding company finance costs, the timing of income tax recoveries and higher stock-based compensation costs, partially offset by unrealized gains on foreign exchange contracts and total return swaps

(7) Weighted average shares of 502.5 million in 2025 compared to 493.9 million in 2024

| | | | | | | | | | | |

3 | FORTIS INC. | SEPTEMBER 30, 2025 QUARTER REPORT | |

| | | | | | | | |

| Interim Management Discussion and Analysis | |

Dividends and TSR

Fortis paid a dividend of $0.615 per common share in the third quarter of 2025, up from $0.590 paid in the third quarter of 2024.

On November 3, 2025, Fortis declared a fourth quarter common share dividend of $0.64, up 4.1% from its third quarter 2025 common share dividend. Fortis has increased its common share dividends for 52 consecutive years and is targeting annual dividend growth of approximately 4-6% through 2030. See "Outlook" on page 21.

Growth in dividends and the market price of the Corporation's common shares have yielded the following TSRs.

| | | | | | | | | | | | | | | | | | | | | | | |

TSR (1) (%) | 1-Year | | 5-Year | | 10-Year | | 20-Year |

| Fortis | 19.3 | | | 9.5 | | | 10.5 | | | 9.5 | |

(1)Annualized TSR per Bloomberg as at September 30, 2025

Operating Cash Flow

The $311 million decrease in Operating Cash Flow for the quarter was due to amounts collected at FortisBC Energy in the third quarter of 2024 associated with: (i) deposits, net of construction costs incurred, related to the Eagle Mountain Pipeline project; and (ii) an income tax refund. In addition, the timing of payments at FortisBC Energy and transmission charges at FortisAlberta, and higher interest payments, also contributed to the decrease. The decrease was partially offset by higher cash earnings, reflecting Rate Base growth and the implementation of customer rate changes at Central Hudson in July 2024 and 2025.

The $124 million increase in Operating Cash Flow for the year-to-date period was due to: (i) higher cash earnings, as discussed above; (ii) the timing of flow-through costs at FortisBC Energy, largely reflecting changes in commodity and midstream costs; (iii) higher deposits received, net of construction costs incurred, for the Eagle Mountain Pipeline project; and (iv) the higher U.S. dollar-to-Canadian dollar exchange rate. The increase was partially offset by the timing of flow-through costs at UNS Energy largely associated with higher PPFAC collections in 2024, the receipt of a tax refund at FortisBC Energy in 2024, as well as higher interest payments.

Capital Expenditures

Capital Expenditures for 2025 are expected to be $5.6 billion, up from $5.2 billion disclosed in the 2024 Annual MD&A. The increase is largely due to the acceleration of investments at ITC related to tranche 1 LRTP projects and the Big Cedar Load Expansion project, as well as a higher forecast U.S. dollar-to-Canadian dollar exchange rate. The Corporation is now using an assumed foreign exchange rate of 1.38 for 2025, as compared to 1.30 assumed previously.

Year-to-date Capital Expenditures of $4.2 billion represent 75% of the annual forecast, and are $0.6 billion higher than the same period in 2024, largely related to energy storage and transmission investments at UNS Energy, as well as transmission projects at ITC.

Capital Expenditures is a Non-U.S. GAAP Financial Measure. Refer to "Non-U.S. GAAP Financial Measures" on page 9 and in the "Glossary" on page 23.

New Five-Year Capital Plan

The Corporation's new 2026-2030 Capital Plan totals $28.8 billion, $2.8 billion higher than the previous five-year plan. The increase is primarily driven by higher FERC regulated transmission investments associated with new interconnections, the MISO LRTP and baseline reliability projects at ITC. It also includes incremental capital at UNS Energy, reflecting an increase in transmission and distribution investments to serve load growth, increase reliability, and provide a path for connecting future generation resources. Planned generation investments in Arizona have also been updated to reflect the recently announced Springerville Natural Gas Conversion project. Customer growth and reliability investments across our utilities, as well as a higher assumed U.S. dollar-to-Canadian dollar exchange rate also contributed to the increase in the five-year plan. See "Capital Plan" on page 16 for additional information.

Subsequent Event

On October 31, 2025, Fortis sold its 100% ownership in Fortis Belize and its 33% ownership in Belize Electricity to the Government of Belize. A loss on sale of approximately $60 million is expected to be recorded in the fourth quarter of 2025, approximately half of which reflects income taxes. Proceeds from the sale will be used to further strengthen the balance sheet and provide funding flexibility in support of our regulated utility growth strategy.

| | | | | | | | | | | |

4 | FORTIS INC. | SEPTEMBER 30, 2025 QUARTER REPORT | |

| | | | | | | | |

| Interim Management Discussion and Analysis | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| BUSINESS UNIT PERFORMANCE | | | | | | | | | | | | |

| Common Equity Earnings | Quarter | | Year-to-Date |

| Periods ended September 30 | | | | | Variance | | | | | | Variance |

| ($ millions) | 2025 | | | 2024 | | | FX (1) | | Other | | 2025 | | | 2024 | | | FX (1) | | Other |

| Regulated Utilities | | | | | | | | | | | | | | | |

| ITC | 149 | | | 138 | | | 2 | | | 9 | | | 442 | | | 415 | | | 12 | | | 15 | |

| UNS Energy | 209 | | | 204 | | | 2 | | | 3 | | | 394 | | | 396 | | | 8 | | | (10) | |

| Central Hudson | 31 | | | 20 | | | 1 | | | 10 | | | 121 | | | 62 | | | 3 | | | 56 | |

| FortisBC Energy | — | | | (4) | | | — | | | 4 | | | 202 | | | 173 | | | — | | | 29 | |

| FortisAlberta | 54 | | | 54 | | | — | | | — | | | 132 | | | 139 | | | — | | | (7) | |

| FortisBC Electric | 15 | | | 14 | | | — | | | 1 | | | 57 | | | 54 | | | — | | | 3 | |

Other Electric (2) | 41 | | | 39 | | | — | | | 2 | | | 129 | | | 111 | | | 1 | | | 17 | |

| 499 | | | 465 | | | 5 | | | 29 | | | 1,477 | | | 1,350 | | | 24 | | | 103 | |

| Non-Regulated | | | | | | | | | | | | | | | |

Corporate and Other (3) | (90) | | | (45) | | | — | | | (45) | | | (185) | | | (140) | | | 4 | | | (49) | |

| Common Equity Earnings | 409 | | | 420 | | | 5 | | | (16) | | | 1,292 | | | 1,210 | | | 28 | | | 54 | |

(1) The reporting currency for each of ITC, UNS Energy, Central Hudson, Caribbean Utilities, FortisTCI and Fortis Belize is the U.S. dollar. The reporting currency of Belize Electricity is the Belizean dollar, which is pegged to the U.S. dollar at BZ$2.00=US$1.00. Certain corporate and non-regulated holding company transactions, included in the Corporate and Other segment, are denominated in U.S. dollars

(2) Consists of the utility operations in eastern Canada and the Caribbean: Newfoundland Power; Maritime Electric; FortisOntario; Wataynikaneyap Power; Caribbean Utilities; and Belize Electricity (see "Subsequent Event" on page 4). Also includes FortisTCI up to the September 2, 2025 date of disposition

(3) Consists of non-regulated holding company expenses, as well as long-term contracted generation assets in Belize (see "Subsequent Event" on page 4)

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| ITC | Quarter | | Year-to-Date |

| Periods ended September 30 | | | | | Variance | | | | | | Variance |

| ($ millions) | 2025 | | | 2024 | | | FX | | Other | | 2025 | | | 2024 | | | FX | | Other |

Revenue (1) | 625 | | | 556 | | | 5 | | | 64 | | | 1,870 | | | 1,662 | | | 46 | | | 162 | |

Earnings (1) | 149 | | | 138 | | | 2 | | | 9 | | | 442 | | | 415 | | | 12 | | | 15 | |

(1)Revenue represents 100% of ITC. Earnings represent the Corporation's 80.1% controlling ownership interest in ITC and reflect consolidated purchase price accounting adjustments

Revenue

The increase in revenue, net of foreign exchange, for the quarter and year-to-date periods was due primarily to Rate Base growth and higher flow-through costs in customer rates.

Earnings

The increase in earnings, net of foreign exchange, for the quarter and year-to-date periods was due to Rate Base growth, partially offset by an increase in non-recoverable stock-based compensation costs and higher holding company finance costs.

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| UNS Energy | Quarter | | Year-to-Date |

| Periods ended September 30 | | | | | Variance | | | | | | Variance |

| ($ millions, except as indicated) | 2025 | | | 2024 | | | FX | | Other | | 2025 | | | 2024 | | | FX | | Other |

Retail electricity sales (GWh) | 3,654 | | | 3,631 | | | — | | | 23 | | | 8,456 | | | 8,522 | | | — | | | (66) | |

Wholesale electricity sales (GWh) (1) | 1,328 | | | 1,325 | | | — | | | 3 | | | 3,513 | | | 4,515 | | | — | | | (1,002) | |

Gas sales (PJ) | 2 | | | 2 | | | — | | | — | | | 12 | | | 12 | | | — | | | — | |

| Revenue | 893 | | | 883 | | | 8 | | | 2 | | | 2,267 | | | 2,348 | | | 61 | | | (142) | |

| Earnings | 209 | | | 204 | | | 2 | | | 3 | | | 394 | | | 396 | | | 8 | | | (10) | |

(1) Primarily short-term wholesale sales

| | | | | | | | | | | |

5 | FORTIS INC. | SEPTEMBER 30, 2025 QUARTER REPORT | |

| | | | | | | | |

| Interim Management Discussion and Analysis | |

Sales

The increase in retail electricity sales for the quarter was due primarily to higher average use by industrial customers. The decrease in retail electricity sales year to date was due primarily to lower average use associated with milder temperatures in comparison to the prior year.

Wholesale electricity sales for the quarter were relatively consistent with the same period in 2024. The decrease in wholesale electricity sales year to date was driven by lower short-term wholesale sales reflecting unfavourable market conditions as well as outages at certain of the company's generation facilities, resulting in lower generation levels. Revenue from short-term wholesale sales, which relate to contracts that are less than one-year in duration, is primarily credited to customers through the PPFAC mechanism and, therefore, does not materially impact earnings.

Gas sales for the quarter and year-to-date periods were consistent with the same periods in 2024.

Revenue

Revenue for the quarter, excluding foreign exchange, was comparable with the third quarter of 2024. An increase in retail revenue, largely reflecting higher transmission revenue and retail electricity sales, was largely offset by the recovery of overall lower fuel and non-fuel costs through the normal operation of regulatory mechanisms.

The decrease in revenue, net of foreign exchange, year to date was due primarily to: (i) the recovery of overall lower fuel and non-fuel costs through the normal operation of regulatory mechanisms; (ii) lower wholesale electricity sales, discussed above; and (iii) lower pricing on wholesale sales in the first quarter of 2025. The decrease was partially offset by higher transmission revenue.

Earnings

The increase in earnings, net of foreign exchange, for the quarter was primarily due to: (i) an increase in retail margin, including the impact of higher transmission revenue and retail electricity sales; and (ii) an increase in AFUDC associated with ongoing Major Capital Projects, partially offset by higher costs associated with Rate Base growth not yet reflected in customer rates.

The decrease in earnings, net of foreign exchange, year to date was primarily due to lower margin on wholesale sales, reflecting less favourable market conditions, and higher costs associated with Rate Base growth not yet reflected in customer rates. The decrease was partially offset by higher transmission revenue and AFUDC.

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Central Hudson | Quarter | | Year-to-Date |

| Periods ended September 30 | | | | | Variance | | | | | | Variance |

| ($ millions, except as indicated) | 2025 | | | 2024 | | | FX | | Other | | 2025 | | | 2024 | | | FX | | Other |

Electricity sales (GWh) | 1,356 | | | 1,402 | | | — | | | (46) | | | 3,874 | | | 3,873 | | | — | | | 1 | |

Gas sales (PJ) | 8 | | | 6 | | | — | | | 2 | | | 21 | | | 19 | | | — | | | 2 | |

| Revenue | 388 | | | 338 | | | 4 | | | 46 | | | 1,208 | | | 1,016 | | | 32 | | | 160 | |

| Earnings | 31 | | | 20 | | | 1 | | | 10 | | | 121 | | | 62 | | | 3 | | | 56 | |

Sales

The decrease in electricity sales for the quarter was due to lower average consumption by residential, industrial and commercial customers.

Electricity sales for the year-to-date period were consistent with the same period in 2024.

The increase in gas sales for the quarter and year-to-date periods was due to higher average consumption by industrial customers.

Changes in electricity and gas sales at Central Hudson are subject to regulatory revenue decoupling mechanisms and, therefore, do not materially impact earnings.

Revenue

The increase in revenue, net of foreign exchange, for the quarter was due primarily to: (i) the flow-through of higher energy supply costs driven by commodity prices; (ii) Rate Base growth; and (iii) higher customer delivery rates, as approved by the PSC effective July 1, 2025 in relation to Central Hudson's 2025 general rate application.

The increase in revenue, net of foreign exchange, year to date was due to the flow-through of higher energy supply costs, Rate Base growth, and higher customer delivery rates effective July 1, 2024 and 2025 as approved by the PSC.

| | | | | | | | | | | |

6 | FORTIS INC. | SEPTEMBER 30, 2025 QUARTER REPORT | |

| | | | | | | | |

| Interim Management Discussion and Analysis | |

Earnings

The increase in earnings, net of foreign exchange, for the quarter was due primarily to: (i) a change in the timing of recognition of a regulatory deferral for uncollectible accounts, as approved in the order on the 2025 general rate application; and (ii) Rate Base growth, partially offset by a contribution to a customer benefit fund, which was accepted by the PSC in August 2025 in connection with a joint settlement agreement (see "Regulatory Matters" on page 10).

The increase in earnings, net of foreign exchange, year to date was due primarily to: (i) Rate Base growth; (ii) the rebasing of customer rates effective July 1, 2024, which reflected a higher allowed ROE and improved recovery of costs; (iii) the timing of operating costs; and (iv) a change in a regulatory deferral for uncollectible accounts, as discussed above. This increase was partially offset by the net impact of contributions made to a customer benefit fund in both 2024 and 2025.

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| FortisBC Energy | | | | | | | |

| Periods ended September 30 | Quarter | | Year-to-Date |

| ($ millions, except as indicated) | 2025 | | | 2024 | | | Variance | | 2025 | | | 2024 | | | Variance |

Gas sales (PJ) | 29 | | | 32 | | | (3) | | | 152 | | | 153 | | | (1) | |

| Revenue | 281 | | | 246 | | | 35 | | | 1,298 | | | 1,143 | | | 155 | |

| Earnings | — | | | (4) | | | 4 | | | 202 | | | 173 | | | 29 | |

Sales

The decrease in gas sales for the quarter and year-to-date periods was due to lower average consumption by transportation and residential customers, partially offset by higher average consumption by industrial customers. Lower average consumption by residential customers was primarily due to milder weather in the third quarter of 2025.

Revenue

The increase in revenue for the quarter and year-to-date periods was due primarily to: (i) the normal operation of regulatory mechanisms; (ii) Rate Base growth; and (iii) a higher cost of natural gas recovered from customers.

Earnings

The increase in earnings for the quarter and year-to-date periods was due primarily to Rate Base growth, including higher AFUDC associated with the timing of FortisBC Energy's investment in the Eagle Mountain Pipeline project.

FortisBC Energy earns approximately the same margin regardless of whether a customer contracts for the purchase and delivery of natural gas or only for delivery. Due to regulatory deferral mechanisms, changes in consumption levels and commodity costs do not materially impact earnings.

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| FortisAlberta | | | |

| Periods ended September 30 | Quarter | | Year-to-Date |

| ($ millions, except as indicated) | 2025 | | | 2024 | | | Variance | | 2025 | | | 2024 | | | Variance |

Electricity deliveries (GWh) | 4,257 | | | 4,388 | | | (131) | | | 13,054 | | | 12,896 | | | 158 | |

| Revenue | 213 | | | 209 | | | 4 | | | 621 | | | 610 | | | 11 | |

| Earnings | 54 | | | 54 | | | — | | | 132 | | | 139 | | | (7) | |

Deliveries

The decrease in electricity deliveries for the quarter was due primarily to lower average consumption by commercial and industrial customers. This decrease was partially offset by higher sales to residential customers due to customer additions.

On a year-to-date basis, the increase in electricity deliveries was primarily due to higher average consumption by industrial customers, largely reflecting higher activity in the energy sector. Customer additions, as well as higher average consumption by residential customers due to warmer weather in the second quarter of 2025, also contributed to the increase.

As approximately 85% of FortisAlberta's revenue is derived from fixed or largely fixed billing determinants, changes in quantities of energy delivered are not entirely correlated with changes in revenue. Revenue is a function of numerous variables, many of which are independent of actual energy deliveries. Significant variations in weather conditions, however, can impact revenue and earnings.

| | | | | | | | | | | |

7 | FORTIS INC. | SEPTEMBER 30, 2025 QUARTER REPORT | |

| | | | | | | | |

| Interim Management Discussion and Analysis | |

Revenue

The increase in revenue for the quarter and year-to-date periods was due to Rate Base growth and customer additions, partially offset by: (i) the expiration of the PBR efficiency carry-over mechanism, as this regulatory incentive was only available through 2024; (ii) favourable non-recurring true-ups recorded in 2024 associated with the finalization of prior period Rate Base balances; and (iii) a reduction in the allowed ROE from 9.28% to 8.97% effective January 1, 2025 due to the automatic adjustment mechanism.

Earnings

Earnings for the quarter were consistent with the same period in 2024. An increase in earnings associated with Rate Base growth and customer additions was offset by the expiration of the PBR efficiency carry-over mechanism, the non-recurring true-ups recorded in 2024 and the lower allowed ROE, as discussed above.

The decrease in earnings year to date was due to the items discussed above for the quarter, as well as the timing of operating costs.

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| FortisBC Electric | | | |

| Periods ended September 30 | Quarter | | Year-to-Date |

| ($ millions, except as indicated) | 2025 | | | 2024 | | | Variance | | 2025 | | | 2024 | | | Variance |

Electricity sales (GWh) | 887 | | | 864 | | | 23 | | | 2,705 | | | 2,597 | | | 108 | |

| Revenue | 133 | | | 130 | | | 3 | | | 412 | | | 396 | | | 16 | |

| Earnings | 15 | | | 14 | | | 1 | | | 57 | | | 54 | | | 3 | |

Sales

The increase in electricity sales for the quarter and year-to-date periods was due primarily to higher average consumption by industrial and commercial customers. The increase was partially offset by lower average consumption by residential customers in the third quarter of 2025 due to milder weather.

Revenue

The increase in revenue for the quarter was due primarily to the normal operation of regulatory mechanisms, higher electricity sales and Rate Base growth.

The increase in revenue year to date was due primarily to higher energy supply costs recovered from customers, higher electricity sales and Rate Base growth. The increase was partially offset by the normal operation of regulatory mechanisms.

Earnings

The increase in earnings for the quarter and year-to-date periods was due primarily to Rate Base growth.

Due to regulatory deferral mechanisms, changes in consumption levels do not materially impact earnings.

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Other Electric | Quarter | | Year-to-Date |

| Periods ended September 30 | | | | | Variance | | | | | | Variance |

| ($ millions, except as indicated) | 2025 | | | 2024 | | | FX | | Other | | 2025 | | | 2024 | | | FX | | Other |

Electricity sales (GWh) | 1,899 | | | 1,924 | | | — | | | (25) | | | 7,403 | | | 7,346 | | | — | | | 57 | |

| Revenue | 393 | | | 399 | | | 1 | | | (7) | | | 1,386 | | | 1,359 | | | 10 | | | 17 | |

| Earnings | 41 | | | 39 | | | — | | | 2 | | | 129 | | | 111 | | | 1 | | | 17 | |

Sales

The decrease in electricity sales for the quarter was primarily due to the September 2, 2025 disposition of FortisTCI.

The increase in electricity sales year to date was due to higher average consumption by residential and commercial customers, as well as customer additions. Higher average consumption for residential customers was largely due to the conversion of home heating systems from oil to electric in Eastern Canada. The increase was partially offset by the disposition of FortisTCI.

| | | | | | | | | | | |

8 | FORTIS INC. | SEPTEMBER 30, 2025 QUARTER REPORT | |

| | | | | | | | |

| Interim Management Discussion and Analysis | |

Revenue

The decrease in revenue, net of foreign exchange, for the quarter was due primarily to the flow-through of lower energy supply costs recovered from customers and the disposition of FortisTCI. The decrease was partially offset by the July 1, 2025 electricity rate increase at Newfoundland Power, as well as Rate Base growth.

The increase in revenue, net of foreign exchange, year to date was due primarily to higher electricity sales and Rate Base growth. The July 1, 2025 electricity rate increase and the operation of regulatory deferral mechanisms at Newfoundland Power also contributed to the increase in revenue. The increase was partially offset by the flow-through of lower energy supply costs recovered from customers and the disposition of FortisTCI.

Earnings

The increase in earnings for the quarter was primarily due to Rate Base growth, partially offset by the disposition of FortisTCI.

The increase in earnings, net of foreign exchange, year to date was due to higher electricity sales and Rate Base growth, as well as the timing of earnings at Newfoundland Power, reflecting the timing of approval of regulatory applications and the related cost recovery mechanisms. The increase was partially offset by the disposition of FortisTCI.

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Corporate and Other | Quarter | | Year-to-Date |

| Periods ended September 30 | | | | | Variance | | | | | | Variance |

| ($ millions, except as indicated) | 2025 | | | 2024 | | | FX | | Other | | 2025 | | | 2024 | | | FX | | Other |

Electricity sales (GWh) | 67 | | | 59 | | | — | | | 8 | | | 154 | | | 135 | | | — | | | 19 | |

| Revenue | 12 | | | 10 | | | — | | | 2 | | | 29 | | | 25 | | | 1 | | | 3 | |

| Net loss | (90) | | | (45) | | | — | | | (45) | | | (185) | | | (140) | | | 4 | | | (49) | |

Sales and Revenue

The increase in electricity sales and revenue for the quarter and year-to-date periods reflected higher hydroelectric production in Belize associated with rainfall levels.

Net Loss

The increase in net loss for the quarter was due primarily to income taxes and closing costs totalling $32 million associated with the disposition of FortisTCI in September 2025. Higher holding company finance costs, unrealized losses on foreign exchange contracts, and lower unrealized gains on total return swaps also contributed to the increase in net loss.

The increase in net loss, excluding foreign exchange, year to date was primarily due to the disposition of FortisTCI, as discussed above. Higher holding company finance costs, the timing of income tax recoveries and an increase in stock-based compensation costs also contributed to the increase in net loss, partially offset by unrealized gains on foreign exchange contracts and total return swaps.

The favourable foreign exchange impact for the year-to-date period was due to the change in the U.S. dollar-to-Canadian dollar exchange rate since December 31, 2024, and the related revaluation of U.S. dollar denominated liabilities, partially offset by the increase in the average exchange rate in 2025.

NON-U.S. GAAP FINANCIAL MEASURES

Adjusted Common Equity Earnings, Adjusted Basic EPS and Capital Expenditures are Non-U.S. GAAP Financial Measures and may not be comparable to similar measures used by other entities. They are presented because management and external stakeholders use them in evaluating the Corporation's financial performance.

Net earnings attributable to common equity shareholders (i.e. Common Equity Earnings) and basic EPS are the most directly comparable U.S. GAAP measures to Adjusted Common Equity Earnings and Adjusted Basic EPS, respectively. These adjusted measures reflect the removal of items that management excludes in its key decision-making processes and evaluation of operating results.

Capital Expenditures include additions to property, plant and equipment and additions to intangible assets, as shown on the condensed consolidated interim statements of cash flows, less CIACs received by FortisBC Energy associated with the Eagle Mountain Pipeline project. The CIACs received for this Major Capital Project are significant and presentation of Capital Expenditures net of CIACs better aligns with the Rate Base growth associated with this project. Capital Expenditures for 2024 also included Fortis' 39% share of capital spending for the Wataynikaneyap Transmission Power project, consistent with Fortis' evaluation of operating results and its role as project manager during the construction of the project.

| | | | | | | | | | | |

9 | FORTIS INC. | SEPTEMBER 30, 2025 QUARTER REPORT | |

| | | | | | | | |

| Interim Management Discussion and Analysis | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Non-U.S. GAAP Reconciliation | | | |

| Periods ended September 30 | Quarter | | Year-to-Date |

| ($ millions, except as indicated) | 2025 | | | 2024 | | | Variance | | 2025 | | | 2024 | | | Variance |

| Adjusted Common Equity Earnings and Adjusted Basic EPS | | | | | | | | | | | |

| Common Equity Earnings | 409 | | | 420 | | | (11) | | | 1,292 | | | 1,210 | | | 82 | |

| Adjusting item: | | | | | | | | | | | |

Disposition of FortisTCI (1) | 32 | | | — | | | 32 | | | 32 | | | — | | | 32 | |

| | | | | | | | | | | |

| Adjusted Common Equity Earnings | 441 | | | 420 | | | 21 | | | 1,324 | | | 1,210 | | | 114 | |

Adjusted Basic EPS ($) | 0.87 | | | 0.85 | | | 0.02 | | | 2.63 | | | 2.45 | | | 0.18 | |

| | | | | | | | | | | |

| Capital Expenditures | | | | | | | | | | | |

| Additions to property, plant and equipment | 1,362 | | | 1,248 | | | 114 | | | 4,324 | | | 3,383 | | | 941 | |

| Additions to intangible assets | 91 | | | 52 | | | 39 | | | 216 | | | 142 | | | 74 | |

| Adjusting items: | | | | | | | | | | | |

Eagle Mountain Pipeline Project (2) | (137) | | | — | | | (137) | | | (369) | | | — | | | (369) | |

Wataynikaneyap Transmission Power Project (3) | — | | | — | | | — | | | — | | | 29 | | | (29) | |

| Capital Expenditures | 1,316 | | | 1,300 | | | 16 | | | 4,171 | | | 3,554 | | | 617 | |

(1) Reflects income taxes and closing costs associated with the disposition of FortisTCI, included in the Corporate and Other segment

(2) Represents CIACs received for the Eagle Mountain Pipeline project, included in the FortisBC Energy segment

(3) Represents Fortis' 39% share of capital spending during the construction of the Wataynikaneyap Transmission Power project, included in the Other Electric segment. Construction was completed in the second quarter of 2024

REGULATORY MATTERS

ITC

MISO Base ROE: In October 2024, FERC issued an order that revised the base ROE for transmission owners operating in the MISO region, including ITC, from 10.02% to 9.98%, with a maximum ROE inclusive of incentives not to exceed 12.58%. The order also directed the payment of certain refunds, with interest, by December 2025, for the 15-month period from November 2013 through February 2015, and prospectively from September 2016. Certain MISO transmission owners, including ITC, filed a request for rehearing with FERC in November 2024, and filed an appeal of the order with the D.C. Circuit Court in January 2025, with particular focus on the refund period and related interest. In March 2025, FERC issued an order addressing the request for rehearing but made no changes to the October 2024 order. The MISO transmission owners continue to pursue an appeal at the D.C. Circuit Court in relation to FERC's October 2024 and March 2025 orders. The timing and outcome of this appeal are unknown. In addition, MISO and the MISO transmission owners are awaiting a response from FERC with respect to a request filed in September 2025 to extend the period to pay refunds from December 2025 to June 30, 2026.

Transmission Incentives: In 2021, FERC issued a supplemental NOPR on transmission incentives modifying the proposal in the initial NOPR released by FERC in 2020. The supplemental NOPR proposes to eliminate the 50-basis point RTO ROE incentive adder for RTO members that have been members for longer than three years. Although the timing and outcome of this proceeding are unknown, every 10-basis point change in ROE at ITC impacts Fortis' annual EPS by approximately $0.01.

UNS Energy

TEP General Rate Application: In June 2025, TEP filed a general rate application with the ACC requesting new rates effective September 1, 2026 using a December 31, 2024 test year, with post-test year adjustments through June 30, 2025. The application includes a proposal to phase-out or eliminate certain adjustor mechanisms, and requests an annual formulaic rate adjustment mechanism consistent with the ACC's approval of a formula rate policy statement in 2024.

UNS Gas General Rate Application: In November 2024, UNS Gas filed a general rate application with the ACC requesting an increase in gas delivery rates effective February 1, 2026. In January 2025, UNS Gas filed supplemental material proposing an annual formulaic rate adjustment mechanism. The outcome of this proceeding is unknown.

Central Hudson

2025 General Rate Application: In August 2025, the PSC approved a three-year rate plan for Central Hudson with retroactive application to July 1 2025, including the continuation of a 9.5% allowed ROE and a 48% common equity component of capital structure. The three-year rate plan also includes the use of existing regulatory balances and other measures to reduce customer bill impacts, as well as initiatives to support New York States's energy conservation emission reduction goals.

| | | | | | | | | | | |

10 | FORTIS INC. | SEPTEMBER 30, 2025 QUARTER REPORT | |

| | | | | | | | |

| Interim Management Discussion and Analysis | |

Enforcement Proceeding: In August 2025, the PSC issued an order which accepted a joint settlement agreement and concluded the enforcement proceeding in connection with a gas-related explosion that occurred in November 2023. As part of the order, Central Hudson agreed to make a contribution to a customer benefit fund which was recorded in the third quarter of 2025.

FortisBC

2025-2027 Rate Framework: In March 2025, the BCUC issued a decision on FortisBC's application with respect to the rate framework for 2025 through 2027. The rate framework builds upon the previous multi-year rate plan and includes, amongst other items, updates to depreciation and capitalized overhead rates, a revised level of operation and maintenance expense per customer indexed for inflation less a fixed productivity adjustment factor, a similar approach to growth capital, a forecast approach to sustaining and other capital, continued collection of an innovation fund recognizing the need to accelerate investment in clean energy innovation, and the continued sharing with customers of variances from the allowed ROE. The rate framework also includes the continuation of deferral mechanisms included in the previous multi-year rate plan.

FortisAlberta

GCOC Decision: FortisAlberta filed an appeal with respect to the AUC's decision on the 2024 GCOC proceeding based on FortisAlberta's business and regulatory risks associated with REAs located in its service area. In March 2025, the Court of Appeal dismissed the appeal.

Third PBR Term Decision: In 2023, the AUC issued a decision establishing the parameters for the third PBR term for the period of 2024 through 2028. FortisAlberta sought permission to appeal the decision to the Court of Appeal on the basis that the AUC erred in its decision to determine capital funding using 2018-2022 historical capital investments without consideration for funding of new capital programs included in the company's 2023 cost of service revenue requirement as approved by the AUC. In March 2025, the Court of Appeal granted FortisAlberta permission to appeal, which is expected to be heard in the first quarter of 2026.

FINANCIAL POSITION

| | | | | | | | | | | |

Significant Changes between September 30, 2025 and December 31, 2024 |

| | | |

| Balance Sheet Account | Increase (Decrease) | |

| ($ millions) | FX | Other | Explanation |

| Cash and cash equivalents | (5) | | 174 | | Primarily due to the issuance of subordinated notes at the Corporation in September 2025. Fortis plans to utilize the net proceeds from this issuance by the end of the year. Balances on hand have been largely invested in interest-bearing accounts. |

| Accounts receivable and other current assets | (37) | | (227) | | Primarily due to seasonality of revenues, particularly in Canada and New York. |

| | | |

| | | |

| | | |

| Other assets | (42) | | 183 | | Reflects an increase in long-term payment arrangements with customers at Central Hudson as a result of collection efforts, as well as an equity contribution to Wataynikaneyap Power. |

| Regulatory assets (current and long-term) | (44) | | 262 | | Due to changes associated with various regulatory mechanisms, including an increase in deferred income taxes and deferred energy management costs, partially offset by lower unrealized losses on natural gas derivatives at FortisBC Energy. |

| Property, plant and equipment, net | (1,066) | | 2,172 | | Due to capital expenditures, partially offset by depreciation expense and CIACs, as well as the September 2025 disposition of FortisTCI. |

| | | |

| | | |

| Short-term borrowings | (3) | | 199 | | Reflects the issuance of commercial paper at ITC to finance working capital requirements. |

| Accounts payable and other current liabilities | (52) | | (308) | | Primarily due to timing of the declaration of common share dividends. |

| | | |

| Regulatory liabilities (current and long-term) | (91) | | 195 | | Due to changes associated with various regulatory mechanisms including an increase in future removal costs, deferred income taxes, and rate stabilization accounts. |

| Deferred income taxes | (107) | | 242 | | Due to higher temporary differences associated with ongoing capital investments. |

| | | | | | | | | | | |

11 | FORTIS INC. | SEPTEMBER 30, 2025 QUARTER REPORT | |

| | | | | | | | |

| Interim Management Discussion and Analysis | |

| | | | | | | | | | | |

Significant Changes between September 30, 2025 and December 31, 2024 |

| | | |

| Balance Sheet Account | Increase (Decrease) | |

| ($ millions) | FX | Other | Explanation |

| Long-term debt (including current portion) | (693) | | 1,255 | | Reflects debt issuances, partially offset by debt and credit facility repayments, in support of the Corporation's Capital Plan. |

| | | |

| Shareholders' equity | (647) | | 1,040 | | Due primarily to: (i) Common Equity Earnings for the nine months ended September 30, 2025, less dividends declared on common shares; and (ii) the issuance of common shares, largely under the DRIP. |

| | | |

LIQUIDITY AND CAPITAL RESOURCES

Cash Flow Requirements

At the subsidiary level, it is expected that operating expenses and interest costs will be paid from Operating Cash Flow, with varying levels of residual cash flow available for capital expenditures and/or dividend payments to Fortis. Remaining capital expenditures are expected to be financed primarily from borrowings under credit facilities, long-term debt offerings and equity injections from Fortis. Borrowings under credit facilities may be required periodically to support seasonal working capital requirements.

Cash required of Fortis to support subsidiary growth is generally derived from borrowings under the Corporation's credit facilities, the operation of the DRIP, as well as issuances of long-term debt, preference equity, and common shares including any issued through the ATM Program. The subsidiaries pay dividends to Fortis and receive equity injections from Fortis when required. Both Fortis and its subsidiaries initially borrow through their credit facilities and periodically replace these borrowings with long-term financing. Financing needs also arise to refinance maturing debt.

Credit facilities are syndicated primarily with large banks in Canada and the U.S., with no one bank holding more than approximately 20% of the Corporation's total revolving credit facilities. Approximately $5.4 billion of the total credit facilities are committed with maturities ranging from 2027 through 2030. Available credit facilities are summarized in the following table.

| | | | | | | | | | | | | | | | | | | | | | | |

| Credit Facilities | | | | | |

| As at | Regulated

Utilities | | Corporate

and Other | | September 30,

2025 | | December 31,

2024 |

| ($ millions) | | | |

Total credit facilities (1) | 4,230 | | | 1,581 | | | 5,811 | | | 6,342 | |

| Credit facilities utilized: | | | | | | | |

| Short-term borrowings | (294) | | | — | | | (294) | | | (98) | |

| Long-term debt (including current portion) | (1,478) | | | — | | | (1,478) | | | (2,216) | |

| Letters of credit outstanding | (94) | | | (22) | | | (116) | | | (102) | |

| Credit facilities unutilized | 2,364 | | | 1,559 | | | 3,923 | | | 3,926 | |

(1) See Note 14 in the 2024 Annual Financial Statements for a description of the credit facilities as at December 31, 2024

In April 2025, FortisAlberta increased its operating credit facility from $250 million to $300 million and extended the maturity to April 2030.

In May 2025, the Corporation amended its $1.3 billion revolving term committed credit facility to extend the maturity to July 2030.

In September 2025, FortisUS Inc., a holding company subsidiary of Fortis, extended the maturity on its unsecured US$150 million revolving term credit facility to October 2027. Also in September 2025, the Corporation fully repaid its unsecured US$250 million non-revolving term credit facility.

The Corporation's ability to service debt and pay dividends is dependent on the financial results of, and the related cash payments from, its subsidiaries. Certain regulated subsidiaries are subject to restrictions that limit their ability to distribute cash to Fortis, including restrictions by certain regulators limiting annual dividends and restrictions by certain lenders limiting debt to total capitalization. There are also practical limitations on using the net assets of the regulated subsidiaries to pay dividends, based on management's intent to maintain the subsidiaries' regulator-approved capital structures. Fortis does not expect that maintaining these capital structures will impact its ability to pay dividends in the foreseeable future.

As at September 30, 2025, consolidated fixed-term debt maturities/repayments are expected to average $1.7 billion annually over the next five years, with a maximum of $2.4 billion due in any one year. Approximately 74% of the Corporation's consolidated long-term debt, excluding credit facility borrowings, had maturities beyond five years.

| | | | | | | | | | | |

12 | FORTIS INC. | SEPTEMBER 30, 2025 QUARTER REPORT | |

| | | | | | | | |

| Interim Management Discussion and Analysis | |

In December 2024, Fortis filed a short-form base shelf prospectus with a 25-month life under which it may issue common or preference shares, subscription receipts, or debt securities in an aggregate principal amount of up to $2.0 billion. Fortis re-established the ATM Program pursuant to the short-form base shelf prospectus, which allows the Corporation to issue up to $500 million of common shares from treasury to the public from time to time, at the Corporation's discretion, effective until January 10, 2027. As at September 30, 2025, $500 million remained available under the ATM Program and $1.5 billion remained available under the short-form base shelf prospectus.

Fortis is well positioned with strong liquidity. The combination of available credit facilities and manageable annual debt maturities/repayments provides flexibility in the timing of access to capital markets. Given current credit ratings and capital structures, the Corporation and its subsidiaries currently expect to continue to have access to long-term capital.

Fortis and its subsidiaries were in compliance with debt covenants as at September 30, 2025 and are expected to remain compliant.

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Cash Flow Summary | | | | | | | | | | | |

| Summary of Cash Flows | | | |

| Periods ended September 30 | Quarter | | Year-to-Date |

| ($ millions) | 2025 | | | 2024 | | | Variance | | 2025 | | | 2024 | | | Variance |

| Cash and cash equivalents, beginning of period | 221 | | | 561 | | | (340) | | | 220 | | | 625 | | | (405) | |

| Cash from (used in): | | | | | | | | | | | |

| Operating activities | 1,027 | | | 1,338 | | | (311) | | | 3,044 | | | 2,920 | | | 124 | |

| Investing activities | (1,081) | | | (1,313) | | | 232 | | | (4,016) | | | (3,599) | | | (417) | |

| Financing activities | 220 | | | 316 | | | (96) | | | 1,156 | | | 939 | | | 217 | |

| Effect of exchange rate changes on cash and cash equivalents | 2 | | | (6) | | | 8 | | | (15) | | | 11 | | | (26) | |

| | | | | | | | | | | |

| Cash and cash equivalents, end of period | 389 | | | 896 | | | (507) | | | 389 | | | 896 | | | (507) | |

Operating Activities

See "Performance at a Glance - Operating Cash Flow" on page 4.

Investing Activities

Cash used in investing activities for the third quarter of 2025 was $232 million lower than the same period in 2024 due to proceeds received on the disposition of FortisTCI in September 2025 partially offset by higher demand side expenditures at FortisBC Energy. An increase in Capital Expenditures in the third quarter of 2025 was offset by higher CIACs largely associated with the Eagle Mountain Pipeline project.

On a year-to-date basis, cash used in investing activities increased by $417 million as compared to the same period in 2024. The increase was due to: (i) higher Capital Expenditures, net of CIACs, (ii) higher demand side management expenditures at FortisBC Energy; (iii) an equity contribution to Wataynikaneyap Power; and (iv) the higher U.S. dollar-to-Canadian dollar exchange rate. The increase was partially offset by proceeds received on the disposition of FortisTCI.

Financing Activities

Cash flows related to financing activities will fluctuate largely as a result of changes in the subsidiaries' capital expenditures and the amount of Operating Cash Flow available to fund those capital expenditures, which together impact the amount of funding required from debt and common equity issuances. See "Cash Flow Requirements" on page 12.

Cash provided by financing activities for the third quarter of 2025 decreased by $96 million as compared to the third quarter of 2024. The reduction was due to an increase in the net repayment of credit facilities, largely associated with proceeds received on the disposition of FortisTCI.

On a year-to-date basis, cash provided by financing activities increased by $217 million as compared to the same period in 2024 due to a net increase in borrowings in support of the Corporation's annual Capital Plan.

| | | | | | | | | | | |

13 | FORTIS INC. | SEPTEMBER 30, 2025 QUARTER REPORT | |

| | | | | | | | |

| Interim Management Discussion and Analysis | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Debt Financing | | | | | | | | | |

| Significant Long-Term Debt Issuances | | | | | | | | | |

| Year-to-date September 30, 2025 | Month | | Interest | | | | | | Use of Proceeds |

($ millions, except as noted) | Issued | | Rate (%) | | Maturity | | Amount | |

| | | | | | | | | |

| | | | | | | | | |

| | | | | | | | | |

| | | | | | | | | |

| | | | | | | | | |

| UNS Energy | | | | | | | | | |

| Unsecured senior notes | February | | 5.90 | | | 2055 | | US $300 | | | (1) (2) (3) |

| | | | | | | | | |

| Central Hudson | | | | | | | | | |

| Senior notes | April | | 5.61 | | | 2035 | | US $20 | | | (1) (3) |

| Senior notes | April | | 5.81 | | | 2040 | | US $30 | | | (1) (3) |

| Senior notes | April | | 6.01 | | | 2045 | | US $20 | | | (1) (3) |

| | | | | | | | | |

| | | | | | | | | |

| FortisAlberta | | | | | | | | | |

| Unsecured senior debentures | July | | 4.76 | | | 2055 | | 200 | | | (1) (2) (3) |

| Newfoundland Power | | | | | | | | | |

| First mortgage bonds | August | | 4.91 | | | 2055 | | 120 | | | (1) (2) (3) |

| | | | | | | | | |

| Maritime Electric | | | | | | | | | |

| First mortgage bonds | July | | 4.94 | | | 2055 | | 120 | | | (1) (2) |

| Fortis | | | | | | | | | |

| Unsecured senior notes | March | | 4.09 | | | 2032 | | 600 | | | (1) (3) |

Subordinated notes (4) | September | | 5.10 | | | 2055 | | 750 | | | (1) (3) |

(1) Repay credit facility borrowings

(2) Fund capital expenditures

(3) General corporate purposes

(4) Issuance reflects fixed-to-fixed rate hybrid subordinated notes. The interest rate will be reset on December 4, 2030, and every 5-years thereafter, equal to the 5-year Government of Canada bond yield plus 2.09% provided that the interest rate reset will not be below the initial interest rate of 5.10%. The subordinated notes receive partial equity treatment from credit rating agencies

In October 2025, UNS Energy issued US$50 million of 10-year, 5.38% unsecured senior notes. Proceeds will be used to repay credit facility borrowings and for general corporate purposes.

In October 2025, FortisBC Energy issued $200 million of 5-year, 3.38% unsecured debentures. Proceeds will be used to repay credit facility borrowings.

In October 2025, Central Hudson priced US$80 million of senior notes with funding expected in November 2025. The related issuances will consist of US$15 million of 10-year, 5.25% notes and US$65 million of 20-year, 5.90% notes. Proceeds are expected to be used for general corporate purposes.

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Common Equity Financing | | | | | | | | | | | |

| Common Equity Issuances and Dividends Paid |

| Periods ended September 30 | Quarter | | Year-to-Date |

| ($ millions, except as indicated) | 2025 | | | 2024 | | | Variance | | 2025 | | | 2024 | | | Variance |

| Common shares issued: | | | | | | | | | | | |

Cash (1) | 11 | | | 13 | | | (2) | | | 45 | | | 34 | | | 11 | |

Non-cash (2) | 112 | | | 107 | | | 5 | | | 346 | | | 324 | | | 22 | |

| Total common shares issued | 123 | | | 120 | | | 3 | | | 391 | | | 358 | | | 33 | |

Number of common shares issued (# millions) | 1.8 | | | 2.1 | | | (0.3) | | | 6.1 | | | 6.7 | | | (0.6) | |

| Common share dividends paid: | | | | | | | | | | | |

| Cash | (198) | | | (186) | | | (12) | | | (581) | | | (549) | | | (32) | |

Non-cash (3) | (112) | | | (106) | | | (6) | | | (345) | | | (324) | | | (21) | |

| Total common share dividends paid | (310) | | | (292) | | | (18) | | | (926) | | | (873) | | | (53) | |

Dividends paid per common share ($) | 0.615 | | | 0.590 | | | 0.025 | | | 1.845 | | 1.770 | | | 0.075 | |

(1) Includes common shares issued under stock option and employee share purchase plans

(2) Common shares issued under the DRIP and stock option plan

(3) Common share dividends reinvested under the DRIP

| | | | | | | | | | | |

14 | FORTIS INC. | SEPTEMBER 30, 2025 QUARTER REPORT | |

| | | | | | | | |

| Interim Management Discussion and Analysis | |

On February 13, 2025 and July 31, 2025 Fortis declared a dividend of $0.615 per common share which was paid on June 1, 2025, and September 1, 2025, respectively. On November 3, 2025, Fortis declared a dividend of $0.64 per common share payable on December 1, 2025. The payment of dividends is at the discretion of the Board and depends on the Corporation's financial condition and other factors.

On June 1, 2025, the annual fixed dividend per share for the First Preference Shares, Series H reset from $0.4588 to $1.0458 for the five-year period up to but excluding June 1, 2030. Also on June 1, 2025, 11,298 First Preference Shares, Series H were converted on a one-for-one basis into First Preference Shares, Series I and 248,830 First Preference Shares, Series I were converted on a one-for-one basis into First Preference Shares, Series H.

Contractual Obligations

There were no material changes to the contractual obligations disclosed in the 2024 Annual MD&A, other than issuances of long-term debt and credit facility utilization (see "Cash Flow Summary" on page 13), and new agreements at UNS Electric and TEP as detailed below.

UNS Electric entered into a US$233 million Engineering, Procurement, and Construction Agreement for the development of four gas engine turbines at the Black Mountain Generating Station, which are expected to be placed in service in 2028.

TEP entered into an energy supply agreement to serve a customer expected to be located in TEP's service territory. The agreement, requiring potential power demand of approximately 300 MW, is subject to approval by the ACC and other contractual contingencies. The initial phase is expected to be operational as early as 2027, with a ramp schedule through 2029. TEP currently expects to serve this customer from its existing and planned capacity, including solar and battery storage projects currently in development.

TEP and UNS Electric entered into long-term gas transportation precedent agreements to secure reliable access to natural gas. The agreements support the development of a new pipeline, expected to be in service in 2029, which will be owned and operated by a third-party. The purchase commitments, expected to begin in 2029, are estimated to total US$1.9 billion over the 25-year service period, and are conditional on the construction and commercial operation of the new pipeline.

Off-Balance Sheet Arrangements

There were no material changes to off-balance sheet arrangements from those disclosed in the 2024 Annual MD&A.

Capital Structure and Credit Ratings

Fortis requires ongoing access to capital and, therefore, targets a consolidated long-term capital structure that will enable it to maintain investment-grade credit ratings. The regulated utilities maintain their own capital structures in line with those reflected in customer rates.

| | | | | | | | | | | | | | | | | | | | | | | |

| Consolidated Capital Structure | September 30, 2025 | | December 31, 2024 |

| As at | ($ millions) | | (%) | | ($ millions) | | (%) |

Debt (1) | 34,030 | | | 56.4 | | | 33,435 | | | 56.4 | |

| Preference shares | 1,623 | | | 2.7 | | | 1,623 | | | 2.7 | |

Common shareholders' equity and non-controlling interests (2) | 24,630 | | | 40.9 | | | 24,230 | | | 40.9 | |

| 60,283 | | | 100.0 | | | 59,288 | | | 100.0 | |

(1) Includes long-term debt and finance leases, including current portion, and short-term borrowings, net of cash

(2) Includes shareholders' equity, excluding preference shares, and non-controlling interests. Non-controlling interests represented 3.4% as at September 30, 2025 (December 31, 2024 - 3.4%)

Outstanding Share Data

As at November 3, 2025, the Corporation had issued and outstanding 505.4 million common shares and the following first preference shares: 5.0 million Series F; 9.2 million Series G; 7.9 million Series H; 2.1 million Series I; 8.0 million Series J; 10.0 million Series K; and 24.0 million Series M.

The common shares of the Corporation have voting rights. The Corporation's first preference shares do not have voting rights unless and until Fortis fails to pay eight quarterly dividends, whether or not consecutive or declared.

If all outstanding stock options were converted as at November 3, 2025, an additional 1.1 million common shares would be issued and outstanding.

| | | | | | | | | | | |

15 | FORTIS INC. | SEPTEMBER 30, 2025 QUARTER REPORT | |

| | | | | | | | |

| Interim Management Discussion and Analysis | |

Credit Ratings

The Corporation's credit ratings shown below reflect its low business risk profile, diversity of operations, the stand-alone nature and financial separation of each regulated subsidiary, and the level of holding company debt.

| | | | | | | | | | | | | | | | | |

| As at September 30, 2025 | Rating | | Type | | Outlook |

| S&P | A- | | Issuer | | Negative |

| BBB+ | | Unsecured debt | | |

| Fitch | BBB+ | | Issuer | | Stable |

| BBB+ | | Unsecured debt | | |

| Morningstar DBRS | A (low) | | Issuer | | Stable |

| A (low) | | Unsecured debt | | Stable |

| Moody's | Baa3 | | Issuer | | Stable |

| Baa3 | | Unsecured debt | | |

| | | | | |

| | | | | |

In March 2025, Moody's confirmed the Corporation's Baa3 issuer and senior unsecured debt credit ratings and stable outlook.

In May 2025, Fitch assigned first time issuer and senior unsecured debt ratings of BBB+ to the Corporation with a stable outlook.

In May 2025, Morningstar DBRS confirmed the Corporation's A (low) issuer and senior unsecured debt credit ratings and stable outlook.

Capital Plan

Capital Expenditures for 2025 are expected to be $5.6 billion, up from $5.2 billion disclosed in the 2024 Annual MD&A. The increase is largely due to the acceleration of investments at ITC related to tranche 1 LRTP projects and the Big Cedar Load Expansion project, as well as a higher forecast U.S. dollar-to-Canadian dollar exchange rate. The Corporation is now assuming a forecast foreign exchange rate of 1.38 for 2025, as compared to 1.30 assumed previously.

Year-to-date Capital Expenditures of $4.2 billion are consistent with expectations and represent 75% of the annual forecast.

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Capital Expenditures (1) | | | | | | | | | | |

| Year-to-date September 30, 2025 | Regulated Utilities | | | | | | |

| | | | UNS Energy | | Central Hudson | | FortisBC Energy | | Fortis Alberta | | FortisBC Electric | | Other Electric | | Total Regulated Utilities | | Non-Regulated Corporate and Other | | |

| ($ millions, except as indicated) | | ITC | | | | | | | | | | Total (1) |

| Total | | 1,363 | | | 1,128 | | | 330 | | | 423 | | | 424 | | | 127 | | | 373 | | | 4,168 | | | 3 | | | 4,171 | |

(1) See "Non-U.S. GAAP Financial Measures" on page 9

New Five-Year Capital Plan

The Corporation's five-year 2026-2030 Capital Plan is targeted at $28.8 billion.

| | | | | | | | | | | | | | | | | | | | |

| ($ billions) | 2026 | 2027 | 2028 | 2029 | 2030 | Total (1) |

| Five-Year Capital Plan | 5.6 | 5.9 | 5.6 | 6.2 | 5.5 | 28.8 |

(1) Reflects an assumed U.S. dollar-to-Canadian dollar exchange rate of 1.35. On average, a five-cent increase or decrease in the U.S. dollar relative to the Canadian dollar would increase or decrease the new Capital Plan by approximately $0.7 billion over the five-year planning period

The 2026-2030 Capital Plan is $2.8 billion higher than the previous five-year plan. The increase is primarily driven by higher FERC regulated transmission investments associated with new interconnections, the MISO LRTP and baseline reliability projects at ITC. It also includes incremental capital at UNS Energy, reflecting an increase in transmission and distribution investments to serve load growth, increase reliability, and provide a path for connecting future generation resources. Planned generation investments in Arizona have also been updated to reflect the recently announced Springerville Natural Gas Conversion project. Customer growth and reliability investments across our utilities also contributed to the increase, and the higher assumed U.S. dollar-to-Canadian dollar exchange rate of 1.35 resulted in approximately $0.6 billion of additional capital as compared to the previous plan.

Investments in the 2026-2030 Capital Plan are categorized as: (i) 46% transmission; (ii) 31% distribution; (iii) 7% generation; (iv) 5% renewable gas and LNG; and (v) 11% other, largely related to information technology and facility investments. The five-year Capital Plan is low risk and highly executable, with only 21% relating to Major Capital Projects. Geographically, 63% of planned expenditures are expected in the U.S., including 34% at ITC, with 35% in Canada and the remaining 2% in the Caribbean.

| | | | | | | | | | | |

16 | FORTIS INC. | SEPTEMBER 30, 2025 QUARTER REPORT | |

| | | | | | | | |

| Interim Management Discussion and Analysis | |

The Capital Plan is expected to be funded primarily by cash from operations and regulated utility debt. Common equity is expected to be provided by the Corporation's DRIP, assuming current participation levels. The Corporation's $500 million ATM Program has not been utilized to date and remains available for funding flexibility as required.

Planned capital expenditures are based on detailed forecasts of energy demand as well as labour and material costs, including inflation, supply chain availability, general economic conditions, foreign exchange rates and other factors. These factors, including new or revised tariffs, could change and cause actual expenditures to differ from forecast. In particular, the Corporation continues to monitor government policy on foreign trade, including the imposition of tariffs and the potential impacts on the supply chain, commodity prices, the cost of energy and general economic conditions. While it is not possible to predict the impact on the supply chain, business operations or the five-year Capital Plan, the Corporation does not currently expect a material financial impact in 2025.

| | | | | | | | | | | | | | | | | | | | |

Major Capital Projects | | | | | | | |

| Forecast | | | | | Plan | | Expected |

| ($ millions) | 2025 | | | | | | 2026-2030 | | Completion |

ITC | | | | | | | | |

| MISO LRTP Tranche 1 | 208 | | | | | | 1,776 | | | 2030 | |

| MISO LRTP Tranche 2.1 | 1 | | | | | | 536 | | | Post-2030 |

| Big Cedar Load Expansion | 90 | | | | | | 472 | | | 2028 | |

UNS Energy | | | | | | | | |

| TEP Transmission Project | — | | | | | | 608 | | | 2029 | |

| Springerville Natural Gas Conversion | — | | | | | | 238 | | | 2030 | |

| Black Mountain Gas Generation | 30 | | | | | | 366 | | | 2028 | |

| Vail-to-Tortolita Transmission Project | 131 | | | | | | 158 | | | 2027 | |

| Roadrunner Reserve Battery Storage Project | 319 | | | | | | 8 | | | 2026 | |

| FortisBC Energy | | | | | | | | |

| Tilbury LNG Storage Expansion | 4 | | | | | | 628 | | | Post-2030 |

| AMI Project | 159 | | | | | | 547 | | | 2028 | |

| Tilbury 1B Project | 20 | | | | | | 334 | | | 2030 | |

Eagle Mountain Pipeline Project (1) | 8 | | | | | | 280 | | | 2027 |

| Total | 970 | | | | | | 5,951 | | | |

(1)Net of customer contributions

MISO LRTP - Tranches 1 and 2.1

Six projects included in first tranche of the MISO LRTP portfolio run through ITC's MISO operating companies' service territories. ITC estimates a majority of its investment associated with these projects is reflected in the 2026-2030 Capital Plan.

ITC has reflected investments of approximately $0.5 billion (US$0.4 billion) in the Corporation's 2026-2030 Capital Plan associated with MISO LRTP tranche 2.1 projects located in Michigan and Minnesota where ROFRs are in effect and for projects requiring system upgrades in Iowa which are not subject to a competitive bidding process. Significant additional investment opportunities remain for tranche 2.1 (see "Additional Investment Opportunities" on page 18).

In July 2025, certain state regulatory commissions in the MISO region filed a complaint at FERC challenging the manner in which MISO developed the tranche 2.1 portfolio. The timing and outcome of this filing, and any potential impact on the Capital Plan, are unknown.

Big Cedar Load Expansion

The project consists of two phases and includes transmission upgrades to serve up to 1,600 MW of new data center load at the Big Cedar Industrial Center. The first phase of the project requires transmission upgrades to support 800 MW of new load with a targeted in-service date of 2027, and phase two requires an additional 800 MW with an expected in-service date of 2028.

TEP Transmission Project

Reflects a transmission project with expected completion in 2029 to serve load demand growth, increase reliability, and provide a path for connecting future generation investments.

Springerville Natural Gas Conversion

The project reflects the conversion of 793 MW of coal-fired generation at TEP's existing Springerville Generating Station to natural gas-fired generation with similar capacity by 2030. The conversion supports customer affordability, local communities, and reliability, and satisfies the need for replacement capacity included in TEP's 2023 IRP.

| | | | | | | | | | | |

17 | FORTIS INC. | SEPTEMBER 30, 2025 QUARTER REPORT | |

| | | | | | | | |

| Interim Management Discussion and Analysis | |

Black Mountain Gas Generation

Reflects the expansion of the existing Black Mountain Generation Station owned and operated by UNS Electric to support rising capacity demands in the service territory. The expansion will include four gas turbines, each with a nominal capacity of 48 MW, a 230 kV substation, and a 230 kV interconnection substation. The project is scheduled for completion in 2028.

Vail-to-Tortolita Transmission Project

Includes investment in one circuit of a new double circuit 230 kV transmission line to tie infrastructure into the TEP system, improving service and reliability to customers. The project is scheduled for completion in 2027.

Roadrunner Reserve Battery Storage Project

Reflects the second 200 MW Roadrunner Reserve battery project at TEP, following the completion of the first Roadrunner Reserve project in July 2025. The project consists of a battery energy storage system that will facilitate the integration of renewable energy into the electric grid. The system is capable of storing 800 MW hours of energy, enough to serve approximately 42,000 homes for four hours when deployed at full capacity. TEP will own and operate the system. The project is scheduled for completion in 2026.

Tilbury LNG Storage Expansion Project

In October 2025, the CPCN application for this project was approved by the BCUC. Consistent with the expansion options outlined in the CPCN, the approval will allow FortisBC Energy to replace the original LNG storage tank at the Tilbury site with a new, expanded LNG storage tank, as well as increased regasification capacity, to ensure FortisBC Energy can continue to provide reliable and resilient energy services. The project remains subject to an environmental assessment process.

AMI Project

The project includes replacement of residential, commercial and industrial meters with advanced gas meters to support the safety, resiliency, and efficient operation of FortisBC Energy's gas distribution system. The project will enable remote meter reading and remote shutoff of gas. The CPCN application was approved by the BCUC in 2023. The installation of the advanced meters commenced in 2025 and is expected to be substantially complete in 2028.

Tilbury 1B Project

Construction of additional liquefaction and dispensing, including on-shore piping, in support of marine bunkering and to further optimize the Tilbury Phase 1A Expansion Project. This FortisBC Energy project has received an Order in Council from the Government of British Columbia. An initial project scope has been filed with regulators to support the federal impact assessment and provincial environmental assessment required to further expand the Tilbury site.

Eagle Mountain Pipeline Project

The project consists of a 50-km pipeline expansion to a small-scale LNG facility owned by Woodfibre LNG near Squamish, British Columbia. FortisBC Energy commenced construction of the project in 2023 which is scheduled for completion in 2027.

Additional Investment Opportunities

ITC

The MISO board has approved tranche 2.1 LRTP projects with estimated transmission costs of approximately US$22 billion. ITC estimates a total range of US$3.7 billion to US$4.2 billion in capital expenditures for the MISO tranche 2.1 projects located in Michigan and Minnesota where ROFRs are in effect and for projects requiring system upgrades in Iowa which are not subject to a competitive bidding process. The majority of the tranche 2.1 investments are expected beyond 2030.

Any additional tranche 2.1 projects awarded to ITC as part of a competitive bidding process would be incremental to the estimated range of tranche 2.1 investments discussed above. ITC is evaluating projects within the portfolio and preparing to bid as deemed appropriate.

UNS Energy

In addition to the energy supply agreement signed in July 2025 (see "Contractual Obligations" on page 15), further negotiations are ongoing with the customer for additional capacity to support a full build at the initial site for a total of 600 MW. The customer has also indicated that additional capacity may be required for 500 MW to 700 MW at a second site. Should discussions progress and an agreement be negotiated, additional generation and transmission investments would be required for these subsequent phases.