.2

SKEENA RESOURCES LIMITED

Management Discussion and Analysis

For the year ended December 31, 2023

(Expressed in thousands of Canadian dollars within tables, unless otherwise noted)

The management’s discussion & analysis (“MD&A”) has been prepared by management and reviewed and approved by the Board of Directors of Skeena Resources Limited (“Skeena”, “us”, “our” or the “Company”) on March 28, 2024. The following discussion of performance, financial condition and future prospects should be read in conjunction with the audited consolidated financial statements and the related notes thereto for the years ended December 31, 2023 and December 31, 2022. The information provided herein supplements but does not form part of the consolidated financial statements. This discussion covers the three and twelve months ended December 31, 2023 and the subsequent period up to March 28, 2024, the date of issue of this MD&A. Monetary amounts in the following discussion are in Canadian dollars, unless otherwise noted.

Additional information, including the audited annual consolidated financial statements and more detail on specific mineral exploration properties discussed in this MD&A can be found on the Company’s System for Electronic Document Analysis and Retrieval (“SEDAR+”) profile at www.sedarplus.ca, the Company’s Electronic Data Gathering, Analysis, and Retrieval system (“EDGAR”) profile at www.sec.gov. Information on risks associated with investing in the Company’s securities is contained in the most recently filed Annual Information Form.

The technical information presented herein has been reviewed by Paul Geddes, P.Geo, the Company’s Senior Vice President of Exploration & Resource Development, and a qualified person as defined by National Instrument 43-101 – Standards of Disclosure for Mineral Projects (“NI 43-101”) (see “Responsibility for Technical Information” section below).

This MD&A contains forward looking information. |

| Management’s Discussion & Analysis | 2 |

SKEENA RESOURCES LIMITED

Management Discussion and Analysis

For the year ended December 31, 2023

(Expressed in thousands of Canadian dollars within tables, unless otherwise noted)

CONTENTS

| Management’s Discussion & Analysis | 3 |

SKEENA RESOURCES LIMITED

Management Discussion and Analysis

For the year ended December 31, 2023

(Expressed in thousands of Canadian dollars within tables, unless otherwise noted)

This MD&A contains certain forward-looking statements or forward-looking information within the meaning of applicable Canadian and US securities laws. All statements and information, other than statements of historical fact, included in or incorporated by reference into this MD&A are forward-looking statements and forward-looking information, including, without limitation, statements regarding activities, events or developments that we expect or anticipate may occur in the future. Such forward-looking statements and information can be identified by the use of forward-looking words such as “plans”, “expects” or “does not expect”, “is expected”, “budget” or “budgeted”, “scheduled”, “estimates”, “projects”, “intends”, “proposes”, “progressing towards”, “in search of”, “complete”, “anticipates” or “does not anticipate”, “believes”, “often”, “likely”, “may”, “will”, “should”, “intend”, “anticipate”, “proposed”, “potential”, or variations of such words and phrases or statements that certain actions, events, or results “may”, “can”, “could”, “would”, “might”, “will be taken”, “occur”, “continue”, or “be achieved” or similar words and expressions or the negative and grammatical variations thereof, or statements that certain events or conditions “may” or “will” happen, or by discussions of strategy. There can be no assurance that the plans, intentions or expectations upon which such forward-looking statements and information are based will occur or, even if they do occur, will result in the performance, events or results expected.

The forward-looking statements and forward-looking information reflect the current beliefs of the Company, and are based on currently available information. Accordingly, these statements are subject to known and unknown risks, uncertainties and other factors which could cause the actual results, performance or achievements of the Company to be materially different from those expressed in or implied by the forward-looking statements. The forward-looking information in this MD&A includes, without limitation, estimates, forecasts, plans, priorities, strategies and statements as to the Company’s current expectations and assumptions concerning, among other things, ability to access sufficient funds to carry on operations, financial and operational performance and prospects, ability to minimize negative environmental impacts of the Company’s operations, anticipated outcomes of lawsuits and other legal issues, particularly in relation to potential receipt or retention of regulatory approvals and any future appeals made by the Company in relation to the Albino Lake Storage Facility, permits and licenses, treatment under governmental regulatory regimes, stability of various governments including those who consider themselves self-governing, continuation of rights to explore and mine, collection of receivables, the success of exploration programs, the estimation of mineral resources, the ability to convert resources or mineral reserves, anticipated conclusions of economic assessments of projects, the suitability of our mineral projects to become open-pit mines, our ability to attract and retain skilled staff, expectations of market prices and costs, exploration, development and expansion plans and objectives, requirements for additional capital, the availability of financing, and the future development and costs and outcomes of the Company’s exploration projects. The foregoing list of assumptions is not exhaustive. Events or circumstances could cause actual results to vary materially.

| Management’s Discussion & Analysis | 4 |

SKEENA RESOURCES LIMITED

Management Discussion and Analysis

For the year ended December 31, 2023

(Expressed in thousands of Canadian dollars within tables, unless otherwise noted)

We caution readers of this MD&A not to place undue reliance on forward-looking statements and information contained herein, which are not a guarantee of performance, events or results and are subject to a number of risks, uncertainties and other factors that could cause actual performance, events or results to differ materially from those expressed or implied by such forward-looking statements and information. Such statements and information are based on numerous assumptions regarding, among other things, favourable equity markets, global financial condition, present and future business strategies and the environment in which the Company will operate in the future, including the price of commodities, anticipated costs, ability to achieve goals (including, without limitation, timing and amount of production), timing and availability of additional required financing on favourable terms, decision to implement (including the business strategy, timing and structure thereof), the ability to successfully complete proposed mergers and acquisitions and the expected results of such acquisitions on our operations, the ability to obtain or maintain permits, mineability and marketability, exchange and interest rate assumptions, including, without limitation, being approximately consistent with the assumptions in the FS (as defined herein) and upcoming DFS (as defined herein), the availability of certain consumables and services and the prices for power and other key supplies, including, without limitation, being approximately consistent with assumptions in the FS and upcoming DFS, labour and materials costs, including, without limitation, assumptions underlying Mineral Reserve (as defined herein) and Mineral Resource (as defined herein) estimates, assumptions made in the feasibility economic assessment estimates, including, but not limited to, geological interpretation, grades, metal price assumptions, metallurgical and mining recovery rates, geotechnical and hydrogeological assumptions, capital and operating cost estimates, and general marketing, political, business and economic conditions, as applicable, results of exploration activities, ability to develop infrastructure, assumptions made in the interpretation of drill results, geology, grade and continuity of mineral deposits, expectations regarding access and demand for equipment, skilled labour and services needed for exploration and development of mineral properties, and that activities will not be adversely disrupted or impeded by exploration, development, operating, regulatory, political, community, economic and/or environmental risks. Forward-looking statements are subject to known and unknown risks, uncertainties and other important factors. These factors include: the ability to obtain permits or approvals required to conduct planned exploration, development, construction and operation; the results of exploration and development; inaccurate geological and engineering assumptions; unanticipated future operational difficulties (including cost escalation, unavailability of materials and equipment, industrial disturbances or other job action and unanticipated events related to health, safety and environmental matters); social unrest; failure of counterparties to perform their contractual obligations; changes in priorities, plans, strategies and prospects; general economic, industry, business and market conditions; disruptions or changes in the credit or securities markets; changes in law, regulation, or application and interpretation of the same; the ability to implement business plans and strategies, and to pursue business opportunities; rulings by courts or arbitrators, proceedings and investigations; inflationary pressures; the ability of the Company to integrate acquired properties into its current business; and various other events, conditions or circumstances that could disrupt Skeena’s priorities, plans, strategies and prospects including those detailed from time to time in the Company’s reports and public filings with the Canadian and US securities administrators, filed on SEDAR+ and EDGAR.

This information speaks only as of the date of this MD&A. The Company undertakes no obligation to revise or update forward-looking information after the date of this document, nor to make revisions to reflect the occurrence of future unanticipated events, except as required under applicable securities laws or the policies of the Toronto Stock Exchange or the New York Stock Exchange.

| Management’s Discussion & Analysis | 5 |

SKEENA RESOURCES LIMITED

Management Discussion and Analysis

For the year ended December 31, 2023

(Expressed in thousands of Canadian dollars within tables, unless otherwise noted)

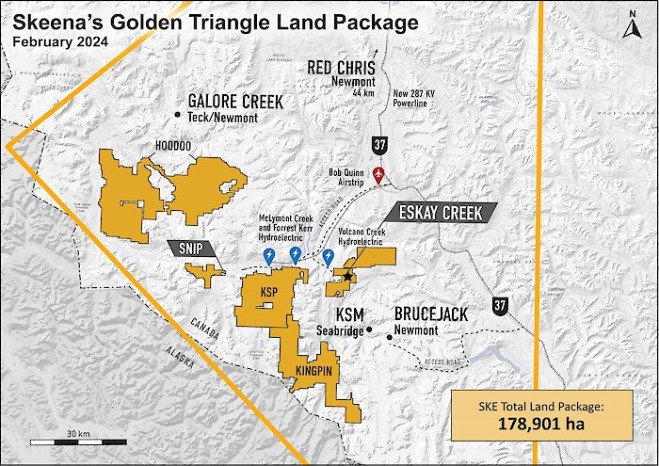

The principal business of Skeena is the exploration and development of mineral properties in the Golden Triangle region of northwest British Columbia, Canada. The Company owns or controls several exploration-stage properties in the region, including the past-producing Eskay Creek Revitalization Project (“Eskay Creek” or “Eskay Creek Project”), and the past-producing Snip gold mine (“Snip”).

The Company was awarded the 2023 A.O. Dufresne Exploration Achievement Award for exploration success and resource growth at Eskay Creek. The award was presented to Skeena during the Canadian Institute of Mining, Metallurgy and Petroleum Awards Gala on May 1, 2023.

In addition to Eskay Creek and Snip, the Company also owns several exploration stage mineral properties in the Golden Triangle and Liard Mining Division of British Columbia.

Figure 1: Property Locations – British Columbia’s Golden Triangle

The Company is a reporting issuer in all the provinces of Canada except Quebec, and trades on the Toronto Stock Exchange (“TSX”) and the New York Stock Exchange (“NYSE”), both under the symbol SKE, and on the Frankfurt Stock Exchange under the symbol RXF.

| Management’s Discussion & Analysis | 6 |

SKEENA RESOURCES LIMITED

Management Discussion and Analysis

For the year ended December 31, 2023

(Expressed in thousands of Canadian dollars within tables, unless otherwise noted)

See “The Company” section above for discussion of the exploration properties held by the Company. The Company considers the Eskay Creek Project to be its primary project.

Eskay Creek Project, British Columbia, Canada

Geological background

The Eskay Creek volcanogenic massive sulphide (“VMS”) and epigenetic deposits were emplaced in a submarine bimodal volcanic environment which are believed to be constrained within a contemporaneous fault-bounded basin. The volcanic sequence consists of footwall rhyolite units overlain by younger basalt units. The contact mudstone terrigenous sediments were deposited at a time of depositional quiescence during an otherwise active period of volcanism. This mudstone (“Contact Mudstone”) is spatially and temporally related to the main mineralizing event at Eskay Creek. The two are separated by the Contact Mudstone which hosts most of the historically exploited mineralization at Eskay Creek.

The Company’s drilling in 2020 has intercepted a compositionally similar mudstone unit (the Lower Mudstone) positioned approximately 100 metres (“m”) stratigraphically below the Contact Mudstone. The Lower Mudstone represents a similar period of volcanic quiescence during which clastic sedimentation dominated prior to the onset of bimodal volcanism that formed the Eskay Creek deposits. The presence of the Lower Mudstone demonstrates the stratigraphic cyclicity which is common to the group of VMS deposits worldwide, of which Eskay Creek is a member.

The bonanza precious metal Au-Ag grades and epigenetic suite of associated elements (Hg-Sb-As) occur predominantly within the Contact Mudstone but are not distributed uniformly throughout the unit. Rather, they are spatially associated with, and concentrated near interpreted hydrothermal vents fed from underlying syn-volcanic feeders. Company drilling campaigns, starting in 2019, have intercepted feeder-style, discordant mineralization in the footwall rhyolites.

Historically, the underlying rhyolite-hosted feeder style mineralization was minimally exploited due to its lower Au-Ag grades. It is noteworthy this rhyolite-hosted mineralization is not enriched in the Hg-Sb-As suite of elements and was often blended with mudstone-hosted zones to reduce smelter penalties for the on-site milled concentrates and direct shipping ore.

Mining history

The Eskay Creek property historically operated as a high-grade underground operation. Underground mining operations were conducted from 1995 to 2008. From 1995 to 1997, ore was direct-shipped after blending and primary crushing. From 1997 to closure in 2008, ore was milled on site to produce a shipping concentrate.

Eskay Creek’s historic production was 3.3 million ounces of gold and 162 million ounces of silver from 2.3 million tonnes (“Mt”) of ore. The property was regarded as having been the highest-grade gold operation in the world with an average grade of 45 grams per tonne (“g/t”) gold and over 2,000 g/t silver.

The historical production for Eskay Creek is summarized in Figure 2.

| Management’s Discussion & Analysis | 7 |

SKEENA RESOURCES LIMITED

Management Discussion and Analysis

For the year ended December 31, 2023

(Expressed in thousands of Canadian dollars within tables, unless otherwise noted)

Figure 2: Eskay Creek Historical Production

Skeena history at Eskay Creek

In August 2018, Skeena commenced an initial surface drill program at Eskay Creek. This first phase of exploratory and definition drilling was focused on the historically unmined portions of the 21A, 21C and 22 Zones of mineralization.

These near-surface targets are located proximal to the historical mine footprint and held potential for expansion of mineralization which may be suitable for open-pit mining. The goal of the 2019 Phase I program was to increase drill density in select areas of mineralization to increase confidence in the resource and allow for future mine planning, collect fresh material for preliminary metallurgical testing and expand exploration into areas that had not previously been drill tested to delineate additional resources. The results of this drill program were incorporated into the results of an initial resource estimate for the Eskay deposit.

The Phase I infill and expansion drilling program at Eskay Creek successfully upgraded the Inferred Resources (as defined in NI 43-101) hosted in the various zones. During this program, two additional drill holes (SK--19--063 and SK--19--067) were extended below the Inferred Resources to test the exploration potential of a secondary and lesser-known mineralized mudstone horizon, termed the Lower Mudstone.

On November 7, 2019, the Company published a Preliminary Economic Assessment (“PEA”) prepared by Ausenco Engineering Canada Inc. (“Ausenco”), supported by SRK Consulting (Canada) Inc. (“SRK”), and AGP Mining Consultants Inc. (“AGP”), for the Eskay Creek Project. On September 1, 2021, the Company advanced the PEA to a Prefeasibility Study for the Eskay Creek Project prepared by Ausenco, SRK, and AGP (the “PFS”).

On September 19, 2022, the Company published a Feasibility Study (“FS”) for the Eskay Creek Project, prepared by Ausenco (the “2022-FS”). A summary of the 2022-FS results was published in a news release on September 8, 2022.

On December 22, 2023, the Company published an Updated Feasibility Study for the Eskay Creek Project (the “2023-DFS” or “DFS”), prepared by Sedgman Canada Ltd. (“Sedgman”) and Global Resource Engineering (“GRE”).

| Management’s Discussion & Analysis | 8 |

SKEENA RESOURCES LIMITED

Management Discussion and Analysis

For the year ended December 31, 2023

(Expressed in thousands of Canadian dollars within tables, unless otherwise noted)

RECENT PROGRESS AT ESKAY CREEK AND SNIP

2023 Resource Update - Eskay Creek Project

On June 20, 2023, the Company announced an updated Mineral Resource Estimate (“MRE”) for Eskay Creek that incorporated an additional 278 drillholes totaling 67,885 metres, enhancements to the resource estimation methods, and updated metallurgical process recoveries. Overall, total pit constrained Measured and Indicated Resource grew to 5.6 million ounces (“Moz”) at 3.47 g/t gold equivalent (“AuEq”) including 4.1 Moz at 2.57 g/t Au and 102.5 Moz Ag at 63.63 g/t Ag, representing a growth of 8% compared to 2022 MRE. Measured Category AuEq Resources increased by 23% and now account for 73% of the total pit constrained MRE, up from 63% in the 2022 MRE.

Table 4: Eskay Creek consolidated pit constrained resources (0.7 g/t AuEq cut-off grade) and underground resources (3.2 g/t AuEq cut-off grade).

Category | Tonnes | AuEq (g/t) | Au (g/t) | Ag (g/t) | AuEq Ounces | Au Ounces | Ag Ounces |

Measured Pit | 27,881 | 4.60 | 3.34 | 88.91 | 4,126 | 2,997 | 79,701 |

Measured UG | 838 | 7.31 | 5.29 | 142.59 | 197 | 142 | 3,842 |

Total Measured | 28,719 | 4.68 | 3.40 | 90.48 | 4,323 | 3,139 | 83,543 |

Indicated Pit | 22,229 | 2.05 | 1.60 | 31.91 | 1,465 | 1,142 | 22,803 |

Indicated UG | 989 | 4.91 | 4.12 | 55.68 | 156 | 131 | 1,771 |

Total Indicated | 23,218 | 2.17 | 1.71 | 32.92 | 1,621 | 1,273 | 24,574 |

M+I Pit | 50,110 | 3.47 | 2.57 | 63.63 | 5,591 | 4,139 | 102,504 |

M+I UG | 1,827 | 6.01 | 4.66 | 95.54 | 353 | 273 | 5,613 |

Total M+I | 51,937 | 3.56 | 2.64 | 64.75 | 5,944 | 4,412 | 108,117 |

Inferred Pit | 643 | 1.92 | 1.46 | 32.33 | 40 | 30 | 668 |

Inferred UG | 272 | 4.57 | 4.21 | 23.37 | 40 | 37 | 222 |

Total Inferred | 915 | 2.71 | 2.28 | 30.26 | 80 | 67 | 890 |

All references to AuEq in the Eskay Creek MRE disclosure have factored metallurgical recoveries as per the calculation: AuEq = ((Au*1,700*0.84) + (Ag*23*0.88)) / (1,700*0.84), US$1,700/oz Au, US$23/oz Ag, 84% gold recovery and 88% silver recovery.

The 2023 MRE pit parameters used to determine Resources with reasonable prospects for eventual economic extraction are analogous to those used for the 2022 MRE apart from the updated metallurgical process recoveries of 84% gold and 88% silver which informed the 2022-FS. The differential in assumed process recoveries resulted in the shallowing of the Resource reporting pit in certain areas relative to the 2022 MRE. Conversely, the 2022 drilling programs in the 23 and 21A West Zones generated new resources which resulted in pit expansions.

2023 DFS – Eskay Creek Project

On December 22, 2023, the Company published the 2023-DFS prepared by Sedgman and GRE. The DFS highlights a base-case after-tax NPV of C$2.0B, representing an increase of 40% relative to the 2022-FS base-case after-tax net present value (“NPV”) of C$1.4B.

| Management’s Discussion & Analysis | 9 |

SKEENA RESOURCES LIMITED

Management Discussion and Analysis

For the year ended December 31, 2023

(Expressed in thousands of Canadian dollars within tables, unless otherwise noted)

The 2023-DFS incorporates several key enhancements and de-risking strategies relative to the 2022-FS including (1) increase in mineral reserve and mine life extension to 12-years, (2) remodelled ore body based on a more selective mining approach with smaller block size, (3) pre-production mining accelerated to create a larger stockpile at start-up, (4) metallurgical test work completed that supports a simplified flow sheet and results in a 43% reduction of mass pull with no material change to recovery, (5) lower concentrate tonnages at higher grades result in increased payables and decreased transport and smelter costs, (6) updated capital cost estimates to reflect a plan that is executable, technically proven, and significantly de-risked with an additional year of engineering and studies, and (7) on-site permanent camp brought forward in plan and relocated away from mine infrastructure to improve workforce attraction and retention, promote employee well-being, and to ensure sufficient available camp space during construction.

Table 3: Proven and Probable Mineral Reserves (Eskay Creek)

Category | Tonnes | AuEq (g/t) | Au (g/t) | Ag (g/t) | AuEq Ounces | Au Ounces | Ag Ounces |

Proven | 27.95 | 4.1 | 3.0 | 80.9 | 3.67 | 2.66 | 72.66 |

Probable | 11.89 | 2.3 | 1.8 | 40.1 | 0.89 | 0.68 | 15.31 |

Total Reserves | 39.84 | 3.6 | 2.6 | 68.7 | 4.56 | 3.34 | 87.97 |

2023 Site Works – Eskay Creek Project

During 2023, early works construction activities commenced on the Eskay Creek Project. These activities included:

| ● | Commencement of drill & blast excavation to prepare the site for future mine infrastructure and totaled approximately 230,000m3 of material moved |

| ● | Installation and successful commissioning of the on-site Assay Lab |

| ● | Continued geotechnical site investigation (“GSI”) programs to inform open-pit and infrastructure engineering and to support project permitting requirements |

2023 MRE - Snip

On September 5, 2023, Skeena released an updated MRE, for Snip which incorporates an additional 307 drillholes totaling 46,268 metres, enhancements to the geological interpretation, resource estimation methods, long hole mining method parameters, and updated metallurgical process recoveries. The majority of the new drilling was completed by Hochschild Mining Holdings Limited (“Hochschild”) under their option agreement before Skeena regained 100% ownership of Snip in April 2023.

2023 Snip MRE highlights:

| ● | Updated MRE of 823,000 ounces grading 9.35 g/t Au in the Indicated category and 114,000 ounces grading 7.10 g/t Au in the Inferred category |

| ● | An increase of 579,000 Au ounces in the Indicated Resource, representing a growth of 237% since the 2020 MRE |

| ● | 2021 and 2022 drilling programs heightened confidence of historical drilling data and improved certainty in continuity of the ore body |

| ● | Metallurgical recovery assumption increased to 96% from 90% based on scoping-level test work |

| Management’s Discussion & Analysis | 10 |

SKEENA RESOURCES LIMITED

Management Discussion and Analysis

For the year ended December 31, 2023

(Expressed in thousands of Canadian dollars within tables, unless otherwise noted)

2023 Regional Exploration Program

During 2023, the Company performed a grass roots reconnaissance exploration program on the KSP and Kingpin properties. These properties were acquired by Skeena on June 1, 2022 following the acquisition of QuestEx Gold & Copper Ltd. (“QuestEx”).

This acquisition added a total of 64,000 hectares of largely unexplored, highly prospective area to the Company’s already significant land package. The first pass of exploration on the KSP Property this year was completing property-scale stream sediment sampling to identify geochemical anomalies. Based on the results of these efforts and historical data, the team completed geological mapping, sampling, and prospecting with the objective of identifying the source, style and scale of mineralization present. Additional information is detailed in the Company’s news release dated October 5, 2023.

2023 Eskay Creek Exploration

Discovery of new mineralization in 2022 at Eskay Deeps by exploratory drillhole SK-22-1081 (3.79 g/t Au, 59.4 g/t Ag over 32.19 metres), prompted the 2023 Eskay Deeps Phase I exploration program. Completed in Q4 2023, the Phase I Deeps program was designed to test for additional high-grade Contact Mudstone mineralization in the down-dip extension of the Eskay Rift ~1,000 metres north of the current Eskay Creek Reserves. Targeting was supported by geological modelling and geophysical data, focusing on areas that were inadequately explored by previous operators. In total, 8 drillholes and 2 wedge branches were completed totalling 13,787 metres. To date, the Company has only tested an area of Contact Mudstone measuring 350 metres by 1,000 metres downdip of the main deposit with wide drill spacings in excess of 100 metres. Considerable exploration potential still exists in the Eskay Deeps as many prehistoric and modern day mineralized rift systems typically extend for tens of kilometres.

All 2023 drillholes intersected anomalous trace mineralization in the Contact Mudstone. Additionally, 120 metres below the Contact Mudstone and hosted by footwall rhyolite breccias, 2023 drillhole SK-23-1182 intersected 3.92 g/t Au, 5.2 g/t Ag over 5.38 metres. SK-23-1182 is 50 metres from the discovery drillhole SK-22-1081, indicating that the mineralized hydrothermal system was still active in this area. Feeder zones similar to this typically have a high-grade expression at the Contact Mudstone, which is yet to be encountered in this area.

By testing Eskay Deeps at widely spaced (>100 metre) hole spacings, a wealth of new information was collected from the 2023 program which has yielded a refined interpretation of the Eskay Creek Rift Model at depth. The Rift Model will be further analyzed once combined with Skeena’s proposed 2024 seismic survey.

A total of 13 surface drillholes were completed in 2023 with the aim of following up on drill intersections discovered during the 2022 exploratory programs in the vicinity of the 22 Zone. Drilling in this area yielded new occurrences of footwall gold-silver mineralization highlighted by SK-23-1203, which intersected 19.87 g/t Au, 59.1 g/t Ag over 2.95 metres including 64.80 g/t Au, 132.0 g/t Ag over 0.85 metres and a second high grade interval averaging 21.10 g/t Au, 15.4 g/t Ag over 1.50 metres. Additional mineralization was identified 200 metres north of the 22 Zone by SK-23-1200 grading 0.63 g/t Au, 86.1 g/t Ag over 14.50 metres and 1.37 g/t Au, 7.6 g/t Ag over 5.00 metres. These new intersections are not expected to materially affect the existing open-pit Resources and Reserves in the 22 Zone.

2024 Site Works – Eskay Creek Project

On-site project construction activities will continue in 2024 and include completion of the mine infrastructure pad, establishment of pilot roads to the technical sample open-pit and Tom Mackay Storage Facility, and possible commencement of technical sample pit mining.

| Management’s Discussion & Analysis | 11 |

SKEENA RESOURCES LIMITED

Management Discussion and Analysis

For the year ended December 31, 2023

(Expressed in thousands of Canadian dollars within tables, unless otherwise noted)

Engineering – Eskay Creek Project

Following completion of the DFS, basic engineering has been completed.

Pit Wall Steepening Investigation – Eskay Creek Project

Data collected during the 2023 GSI campaign will be analyzed and used to support an updated engineering recommendation with respect to pit-wall slope angles. This analysis is expected to yield recommended pit-wall angles that are generally steeper than those informing the 2023-DFS pit design. If successful, this change would result in a favourable outcome for overall project economics through reduction in waste tonnes mines and/or increase in reserves.

Metallurgical Optimization & Simplified Flowsheet at Eskay Creek

Following Eskay Creek’s 2022-FS, and in preparation for the 2023-DFS, Skeena continued metallurgical test work using representative samples of Eskay Creek material. The focus of this work has been to simplify the process flowsheet and improve the quality of the concentrate expected to be produced from the flotation plant. Metallurgical tests were conducted through 2023 in support of the DFS to optimize the flowsheet and to increase grades of payable metals in the concentrate.

As part of the DFS, metallurgical testing was conducted on composite samples that represented a range of 15-35% Mudstone with the balance as Rhyolite, matching the expected range to be produced by the mine.

Concentrate Comparison of 2022 FS vs. 2023 DFS

| Units | 2022 Feasibility Study | 2023 Definitive Feasibility Study |

Mass Yield to Concentrate (range) | % | 4.6 - 7.8% | 2.6 - 5.3% |

Mass Yield to Concentrate (average) | % | 6.8% | 3.9% |

Concentrate Production | Dmt | 2,018,000 | 1,574,000 |

Au Concentrate Grade (range) | g/t | 25 - 50 | 40 - 95 |

Au Concentrate Grade (Y1-5 average) | g/t | 48 | 82 |

Au Concentrate Grade (LOM average) | g/t | 37 | 55 |

Ag Concentrate Grade (range) | g/t | 674 - 1,629 | 1,020 - 2,970 |

Ag Concentrate Grade (Y1-5 average) | g/t | 1,313 | 2,466 |

Ag Concentrate Grade (LOM average) | g/t | 1,024 | 1,595 |

| ● | Concentrate production of 2,018,000 dmt in 2022-FS considered 29.9 Mt of mill feed over a 9-year life. Concentrate production of 1,574,000 dmt in 2023 DFS considers 39.8 Mt of mill feed over a 12-year life. |

An alternative flowsheet compared to the 2022-FS was tested with the purpose of simplifying the process flowsheet. The new testwork program evaluated a range of primary grinds and determined that 40 microns (“µm”) is optimal prior to rougher flotation. Following rougher flotation, regrinding rougher concentrate to approximately 10 µm was determined to provide the best flotation results.

The additional metallurgical testing has shown excellent results in producing a higher-grade gold and silver concentrate with lower concentrate volumes, compared to previous testing. Recoveries for gold were largely unchanged at 83%, slightly conservative based on test results, and silver recoveries increased from 88% to 91%, as compared to the 2022-FS .

| Management’s Discussion & Analysis | 12 |

SKEENA RESOURCES LIMITED

Management Discussion and Analysis

For the year ended December 31, 2023

(Expressed in thousands of Canadian dollars within tables, unless otherwise noted)

The outcome of producing a higher-grade concentrate led to a substantial cost reduction over life of mine (“LOM”) in both treatment charges and transportation costs in comparison to the 2022-FS . In addition to decreasing costs, the higher-grade concentrate also provides an opportunity for the base metals content to be payable, and some previous penalty elements are now neutral and do not incur penalties.

2024 Exploration Programs

2024 Seismic Survey

The Company is aiming to perform a surface based seismic survey in Summer 2024. It has been proven by previous operators that more conventional geophysical methods such as electromagnetics and induced polarization are unable to directly discern the Eskay Creek gold-silver mineralization. However, the Company is investigating the potential for a seismic survey to indirectly target mineralization by better defining the rift and Contact Mudstone at depth that is critical for hosting Eskay Creek style deposits. Additional Eskay Deeps drilling will be driven by the results of the seismic survey.

During H1 2024, Skeena will be finalizing a large airborne magnetics survey and data compilation for the new 74,633 hectare Hoodoo Project which was staked in October 2023. The Hoodoo property is situated approximately 65 kilometers northwest of Eskay Creek. Remarkably, this ground was unclaimed mineral tenure with virtually no historical exploration despite possessing very high prospectivity for alkalic porphyry deposits. Alkalic gold-copper porphyry deposits in the cordillera of British Columbia typically rank as the higher-grade end members such as Galore Creek and New Afton. These specific deposits are attractive exploration targets based on their atypically high gold tenor.

An accelerated exploration model will be employed in H2 2024 that judiciously ranks and ultimately culminates in drilling targets on the KSP and Hoodoo properties. The successes of the 2023 field program in discovering new gold-copper mineralization and increasing the geological understanding of the KSP and Hoodoo properties warrants augmented exploration in these areas. Overall, 14,000 metres has been budgeted for this regional program.

Maiden Engineering Study for Snip

Following the updated MRE for Snip, in 2024 Skeena will continue an engineering study on Snip to investigate Snip as a potential satellite operation, providing mineralized material to a centralized mill at Eskay Creek. The Company expects the additional clean (absent of deleterious elements), high-grade mineralization from Snip to further bolster the mine life at Eskay Creek.

ENVIRONMENTAL, SOCIAL AND CORPORATE GOVERNANCE UPDATE

Environmental

Skeena is committed to minimizing any negative environmental impacts from its operations and identifying opportunities to improve upon the environmental impacts of historical operations. As a high-grade ore body with a small operational footprint, Eskay Creek is expected to have much lower carbon emissions than comparable mines, and the proximity to hydroelectric power presents an opportunity to reduce this further.

One of Skeena’s core values is to respect and protect the land for future generations. Skeena’s employees, contractors and leadership live these values while conducting Skeena’s operations. A key example of this commitment to Skeena’s core values was the donation of the Spectrum property to create the nature conservancy further described below in the section “Relations with Indigenous Communities.”

| Management’s Discussion & Analysis | 13 |

SKEENA RESOURCES LIMITED

Management Discussion and Analysis

For the year ended December 31, 2023

(Expressed in thousands of Canadian dollars within tables, unless otherwise noted)

Permitting Considerations

Eskay Creek is an operating mine under the Mines Act, currently on care and maintenance. The site has been maintained in good standing and environmental monitoring has been ongoing during operations and since the site was closed in 2008. There is a substantial database of environmental information for the site and region spanning almost 30 years.

To accommodate the mine design contemplated for future development, an updated Environmental Assessment and mine permits will be required. Environmental and socio-economic baseline studies are ongoing to support the Environmental Assessment and permitting processes.

The Company is in the Environmental Assessment process. The Impact Assessment Agency of Canada (“IAAC”) issued a Substitution Decision for the Eskay Creek Project in November 2022, so Eskay Creek will undergo a single assessment under the BC process, with IAAC participation through the BC process. The Eskay Creek Project achieved a readiness determination from the BC government and the Tahltan Central Government (“TCG”) in November 2022, and the Process Order for the project was issued in April 2023. Eskay Creek is in the Application Development phase of the BC Environmental Assessment process.

In August of 2022, Skeena received an amended Mines Act Permit which provides flexibility for closure and exploration related activities on the Permitted Mine Area. The Company continues to advance on numerous operational authorizations that support ongoing and expanded activity at the project site.

On January 17, 2023, the Company announced that it concluded a joint workplan arrangement with the BC Government and the TCG. The Eskay Creek Process Charter outlines the manner in which the parties will collaborate on the authorizations that are needed for the Eskay Creek Project and includes an objective timeline for the project. The objective target for permitting and authorizations required for project construction to be in place is H1 2025 and is dependent on regulatory and Indigenous government processes and available resources.

Social Community Relations

The Company has been working in the Tahltan Territory since 2014 and has developed a strong working relationship with the Tahltan Nation (“Tahltan”), which has a long-standing relationship with Eskay Creek. Previous operators maintained agreements with the Tahltan which included provisions for training, employment, and contracting opportunities. Skeena also maintains formal agreements with the TCG which guide communications, permitting, capacity and environmental practices for projects in Tahltan Territory. Skeena is currently engaged in Impact Benefit Agreement negotiations with the TCG.

Skeena has established an agreement with the Gitanyow Hereditary Chiefs for participation in the Wilp Sustainability Assessment process. A portion of the traffic required to support the Eskay Creek Project will pass through Gitanyow Territory and the Wilp Sustainability Assessment process is their process to assess the potential impacts of that traffic. The agreement lays out the process that will be followed and provides for capacity funding to support Gitanyow’s assessment.

Skeena has also entered into an information sharing and confidentiality agreement with the Nisga’a Lisiims Government. The Eskay Creek Project will make use of port facilities that are within Nisga’a Treaty area and will require certain information from Nisga’a to assess the potential impacts of port use on Nisga’a Treaty rights. The agreement provides for the information sharing to occur.

| Management’s Discussion & Analysis | 14 |

SKEENA RESOURCES LIMITED

Management Discussion and Analysis

For the year ended December 31, 2023

(Expressed in thousands of Canadian dollars within tables, unless otherwise noted)

Relations with Indigenous Communities

Skeena has established a vision for the Company that includes committing to reconciliation with First Nations peoples through responsible and sustainable mining development, and to deliver value and prosperity to shareholders, employees, First Nation partners and surrounding communities.

One of Skeena’s core principles is to work closely with First Nations communities to achieve the responsible development of our projects, and to make a positive difference in the places we work. Skeena believes in building and sustaining mutually beneficial and supportive relationships with First Nations communities by creating a foundation of trust and respect, through open, honest and timely communication.

On April 8, 2021, Skeena announced that it had returned its mineral tenures on the Spectrum property, enabling the TCG, the Province of BC, Skeena, the Nature Conservancy of Canada and BC Parks Foundation to collaborate in the creation of a nature conservancy, the Tenh Dẕetle Conservancy.

Further to this announcement, the Company announced that it had entered into an investment agreement with the TCG, pursuant to which the TCG invested $5,000,000 into Skeena by purchasing 399,285 Tahltan Investment Rights (“Rights”) for approximately $12.52 per Right. Each Right will vest by converting into one Common Share of the Company upon the achievement of key company and permitting milestones, or over time, as set forth within the agreement, with all Rights vesting by the third anniversary of the agreement. The investment closed on April 16, 2021.

On July 19, 2021, two of the four milestones related to the previously announced Investment Rights Agreement with the TCG were met. As a result of achieving these milestones, 199,642 Rights were converted into 199,642 common shares of the Company. On January 17, 2023, TCG, the Government of BC, and Skeena signed a permitting Process Charter agreement for the Eskay Creek Project, triggering a third milestone achievement, resulting in the conversion of 119,785 Rights into 119,785 common shares of the Company. As at December 31, 2023, one milestone is yet to be achieved.

The Eskay Creek site is also subject to assertions of traditional use by Tsetsaut Skii km Lax Ha (“TSKLH”). Skeena has engaged with TSKLH for information sharing about the Eskay Creek Project and contracting and business opportunities related to our current activities.

Highway access to the Eskay Creek site and to tidewater ports for future shipping crosses through the Nass Wildlife Area, lands which are subject to the terms of the Nisga’a Final Agreement. Skeena has engaged with the Nisga’a Lisims Government directly and through the Environmental Assessment process to address Nisga’a concerns through the collaborative development of a Nisga’a process which meets requirements under paragraphs 8(e) and 8(f) of Chapter 10 in the Nisga’a Treaty and aligns with requirements in the Process Order. The highway access also passes through the Traditional Territory of the Gitanyow Hereditary Chiefs. Skeena has engaged with the Hereditary Chiefs Office to explain the project plans and request feedback.

Governance

In support of the culture and goals of the Company, and to better communicate them as the Company grows, Skeena has established formal mission, vision, and values statements and has implemented a suite of comprehensive board level policies. A set of complementary operational level policies were developed for staff and contractors and have been implemented to support the board level policies.

As part of the focus on ever-improving corporate governance, the Company has also engaged independent corporate governance consultants to further assist with improving Skeena’s policies and procedures as needed.

| Management’s Discussion & Analysis | 15 |

SKEENA RESOURCES LIMITED

Management Discussion and Analysis

For the year ended December 31, 2023

(Expressed in thousands of Canadian dollars within tables, unless otherwise noted)

Environmental, Social and Governance Report

On May 11, 2023, Skeena published its Environmental, Social and Governance (“ESG”) Report for 2022. The report provides Skeena shareholders and stakeholders with a comprehensive overview of the Company’s ESG practices, commitments and performance for the year.

Eskay Mining Corp. Transaction

On July 7, 2023, the Company acquired five mineral claims surrounding Eskay Creek from Eskay Mining Corp. for cash consideration of $4,000,000. The mineral claims are subject to a 2% net smelter return (“NSR”) royalty, of which 1% of the NSR royalty can be purchased at any time for $2,000,000.

Sale of Royalty

On December 18, 2023, the Company sold a 1% NSR royalty to Franco-Nevada Corporation (“Franco-Nevada”) for cash consideration of $56,000,000 and contingent cash consideration of $3,000,000 to $4,500,000 which is payable upon completion of certain milestones (the “December 2023 Contingent Consideration”). The December 2023 Contingent Consideration replaced the contingent cash consideration of $1,500,000 payable by Franco-Nevada in connection with the royalty sale to Franco-Nevada in December 2022.

Financing Transactions

Financing transactions for the year ended December 31, 2023 are covered in the Discussion of Operations sections below.

Other Capital Transactions

On January 28, 2024, the Company granted 822,093 stock options, 323,940 RSUs and 105,079 DSUs to various directors, officers, employees and consultants of the Company. The stock options and RSUs vest over a 36-month period, with one third of the stock options and RSUs vesting on each anniversary of the grant. The stock options have a term of 5 years, with each option allowing the holder to purchase one common share of the Company at a price of $5.71 per common share. In addition to the vesting period above, the stock options and RSUs granted to senior management will only vest upon the Company raising at least $65,000,000. The Board of Directors also approved to grant 199,912 RSUs to an officer of the Company, with the RSUs to be granted upon meeting certain regulatory conditions and to vest on December 10, 2024 upon the Company raising at least $65,000,000.

On January 28, 2024, the Company also granted 200,000 stock options to a consultant of the Company. The options have a term of 5 years and vest over a 24-month period, with one quarter of the stock options vesting every 6 months from the date of grant. Each option allows the holder to purchase one common share of the Company at a price of $5.71 per common share.

During the year ended December 31, 2023, the Company adopted the 2023 Omnibus Equity Incentive Plan (“Omnibus Plan”), which governs the terms of future equity incentive grants, including stock options, restricted share units (“RSUs”), performance share units (“PSUs”) and deferred share units (“DSUs”).

| Management’s Discussion & Analysis | 16 |

SKEENA RESOURCES LIMITED

Management Discussion and Analysis

For the year ended December 31, 2023

(Expressed in thousands of Canadian dollars within tables, unless otherwise noted)

During the year ended December 31, 2023, the Company granted the following:

Incentive Grant | Granted | Weighted Average Fair Value Per Unit |

Stock options | 485,151 | $3.33 |

Restricted share units | 607,750 | $8.15 |

Performance share units | 770,000 | $6.04 |

Deferred share units | 86,257 | $6.09 |

The stock options and RSUs granted during the year ended December 31, 2023 vest over a 36-month period, with one third vesting on each of the first, second and third anniversaries of the grant date. The stock options granted have a weighted average exercise price of $8.42 per common share and expire five years from the date of grant.

Performance-linked options and PSUs were granted for achieving certain results on the DFS and meeting certain ESG-linked minimum award threshold criteria (“Performance Criteria”). With the exception of 200,200 PSUs which vest on the first anniversary of the achievement of the Performance Criteria, the remainder of the performance-linked options and PSUs vest over a 36-month period, with one third of the performance-linked options and PSUs vesting on each of the first, second and third anniversaries of the Performance Criteria.

The following table sets forth selected annual information from the audited consolidated financial statements for the years ended December 31, 2023, 2022, and 2021:

Year ended | | 2023 | | | 2022 | | 2021 |

Loss | $ | (1) (108,980) | | $ | (2) (88,890) | $ | (3) (117,567) |

Basic & diluted loss per share | $ | (1.29) | | $ | (1.26) | $ | (1.97) |

Total assets | $ | 194,987 | | $ | 167,980 | $ | 154,962 |

Non-current financial liabilities | $ | 23,017 | | $ | 691 | $ | Nil |

Cash dividends paid | $ | Nil | | $ | Nil | $ | Nil |

| (1) | The Company’s total assets and non-current financial liabilities as at December 31, 2023 were impacted by the issuance of a convertible debenture to Franco-Nevada for cash proceeds of $25,000,000. Loss for the year ended December 31, 2023 includes $91,855,000 of exploration and evaluation expenditures, primarily on the Eskay property, $8,856,000 of share-based payments, and $5,078,000 of flow-through share premium recovery. |

| (2) | The Company’s financial results for the year ended December 31, 2022 were impacted by the purchase and sale of a royalty resulting in a gain of $9,463,000 reducing the loss for the year. Loss for the year ended December 31, 2022 includes $91,602,000 of exploration and evaluation expenditures, primarily on the Eskay property, $7,387,000 of share-based payments, and $13,326,000 of flow-through share premium recovery. |

| (3) | The Company’s financial results for the year ended December 31, 2021 were impacted by the increased exploration and evaluation activities on the Company’s Eskay and Snip properties. Loss for the year ended December 31, 2021 includes $107,452,000 of exploration and evaluation expenditures, primarily on the Eskay property, $10,950,000 of share-based payments, and $12,890,000 of flow-through share premium recovery. |

| Management’s Discussion & Analysis | 17 |

SKEENA RESOURCES LIMITED

Management Discussion and Analysis

For the year ended December 31, 2023

(Expressed in thousands of Canadian dollars within tables, unless otherwise noted)

The Company completed the year ended December 31, 2023 with cash and cash equivalents of $91,135,000. Being in the exploration stage, the Company does not have revenue from operations, and has historically relied primarily on equity funding for its continuing financial liquidity. The Company expects to continue to raise the necessary funds for operations and project construction through a combination of debt, equity and other metals-production-linked instruments at the appropriate time in order to pursue the development of the Eskay Creek Project.

Private placements and bought deal offerings

On December 27, 2023, the Company closed a non-brokered private placement offering, whereby gross proceeds of $10,734,000 were raised by the issuance of 892,461 flow-through shares at a price of $8.80 per flow-through share and 366,248 flow-through shares at a price of $7.865 per flow-through share. In relation to this financing, funds raised were spent in the following manner, as compared with the planned use of proceeds:

Planned Use of Proceeds | Amount | Actual Use of Proceeds to December 31, 2023 | Amount |

Exploration activities | $10,734 | Exploration activities | $nil |

On October 10, 2023, the Company closed a non-brokered private placement offering, whereby gross proceeds of $4,541,000 were raised by the issuance of 259,066 flow-through shares at a price of $8.44 per flow-through share and 249,409 flow-through shares at a price of $9.44 per flow-through share. In relation to this financing, funds raised were spent in the following manner, as compared with the planned use of proceeds:

Planned Use of Proceeds | Amount | Actual Use of Proceeds to December 31, 2023 | Amount |

Exploration activities | $4,541 | Exploration activities | $1,792 |

On May 24, 2023, the Company closed a bought deal offering, whereby gross proceeds of $73,537,000 were raised by the issuance of 10,005,000 common shares at a price of $7.35 per common share. In relation to this offering, net proceeds raised were spent in the following manner, as compared with the planned use of proceeds:

Planned Use of Proceeds | Amount | Actual Use of Proceeds to December 31, 2023 | Amount |

Infrastructure, capital and site preparation | $24,000 | Infrastructure, capital and site preparation | $24,000 |

Resource and feasibility updates | $5,000 | Resource and feasibility updates | $5,000 |

Environmental and engineering optimization | $7,000 | Environmental and engineering optimization | $7,000 |

Permitting and associated expenses | $8,000 | Permitting and associated expenses | $8,000 |

Exploration activities | $12,000 | Exploration activities | $12,000 |

General working capital | $13,601 | General working capital | $13,601 |

Total | $69,601 | Total | $69,601 |

On December 22, 2022, the Company closed a non-brokered private placement offering, whereby gross proceeds of $3,040,000 were raised by the issuance of 283,286 flow-through shares at a price of $10.73 per flow-through share. In relation to this financing, funds raised were spent in the following manner, as compared with the planned use of proceeds:

Planned Use of Proceeds | Amount | Actual Use of Proceeds to December 31, 2023 | Amount |

Exploration activities | $3,040 | Exploration activities | $3,040 |

| Management’s Discussion & Analysis | 18 |

SKEENA RESOURCES LIMITED

Management Discussion and Analysis

For the year ended December 31, 2023

(Expressed in thousands of Canadian dollars within tables, unless otherwise noted)

On December 16, 2022, the Company closed a non-brokered private placement offering, whereby gross proceeds of $10,000,000 were raised by the issuance of 1,000,000 flow-through shares at a price of $10.00 per flow-through share. In relation to this financing, funds raised were spent in the following manner, as compared with the planned use of proceeds:

Planned Use of Proceeds | Amount | Actual Use of Proceeds to December 31, 2023 | Amount |

Exploration activities | $10,000 | Exploration activities | $10,000 |

On November 16, 2022, the Company closed a non-brokered private placement offering, whereby gross proceeds of $5,000,000 were raised by the issuance of 250,784 flow-through shares at a price of $7.975 per flow-through share and 333,334 flow-through shares at a price of $9.00 per flow-through share. In relation to this financing, funds raised were spent in the following manner, as compared with the planned use of proceeds:

Planned Use of Proceeds | Amount | Actual Use of Proceeds to December 31, 2023 | Amount |

Exploration activities | $5,000 | Exploration activities | $5,000 |

Convertible debenture

On December 18, 2023, the Company issued an unsecured convertible debenture to Franco-Nevada for cash proceeds of $25,000,000 (the "Debenture"). The Debenture matures on the earlier of: (i) five years; or (ii) the completion of project financing of at least US$200,000,000 for the construction and development of the Eskay Creek project. The Debenture bears interest of 7% per annum, payable every calendar quarter. The Company has the option quarterly to elect to pay the interest in cash or accruing it to the principal amount of the Debenture and paying it upon the Debenture’s maturity. In December 2023, the Company elected to accrue the interest.

Franco-Nevada has the option (“conversion option”), at any time, to convert some or all of the outstanding principal amount of the Debenture into common shares at a conversion price of $7.70 per common share (the "conversion price"). After the third anniversary of the issuance of the Debenture, the Debenture may be redeemed in whole or in part from time to time at the Company's option (“redemption option”) at a price equal to the principal amount plus accrued and unpaid interest, provided that the volume weighted average trading price of the common shares on the TSX for the previous 20 consecutive trading day period is more than 135% of the conversion price.

Upon any occurrence of a change of control, Franco-Nevada has the option to require the Company to purchase the Debenture in cash by payment of: (i) 130% of the principal amount, plus any accrued or unpaid interest, if the change of control occurred on or prior to the third anniversary of the issuance of the Debenture; or (ii) 115% of the principal amount, plus any accrued and unpaid interest, if the change of control occurred at any time thereafter.

The Company must comply with certain covenants. As at December 31, 2023, the Company was in compliance with those covenants.

| Management’s Discussion & Analysis | 19 |

SKEENA RESOURCES LIMITED

Management Discussion and Analysis

For the year ended December 31, 2023

(Expressed in thousands of Canadian dollars within tables, unless otherwise noted)

Discussion of Exploration and Evaluation Expenses for the Years Ended December 31, 2023 and 2022

Year ended December 31, 2023 | | Eskay | | Snip | Other | | Total | ||||

Accretion | | $ | 207 | | $ | — | $ | — | | $ | 207 |

Assays and analysis/storage | |

| 1,667 | |

| 36 |

| 494 | |

| 2,197 |

Camp and safety | |

| 470 | |

| — |

| 7 | |

| 477 |

Claim renewals and permits | | | 1,013 | | | 82 | | 36 | | | 1,131 |

Community relations | |

| 60 | |

| — |

| 10 | |

| 70 |

Depreciation | | | 2,008 | | | — | | — | | | 2,008 |

Drilling | |

| 16,233 | |

| 11 |

| 93 | |

| 16,337 |

Electrical | | | 15 | | | — | | — | | | 15 |

Environmental studies | |

| 20,563 | |

| 358 |

| — | |

| 20,921 |

Equipment rental | |

| 1,370 | |

| 10 |

| 105 | |

| 1,485 |

Fieldwork, camp support | |

| 8,630 | |

| 101 |

| 1,408 | |

| 10,139 |

Fuel | | | 3,599 | | | 10 | | 147 | | | 3,756 |

Geology, geophysics, and geochemical | |

| 20,684 | |

| 236 |

| 292 | |

| 21,212 |

Helicopter | | | 3,222 | | | 69 | | 624 | | | 3,915 |

Metallurgy | | | 848 | | | 23 | | — | | | 871 |

Part XII.6 tax, net of METC | |

| (447) | |

| — |

| (81) | |

| (528) |

Share-based payments | |

| 3,131 | |

| — |

| — | |

| 3,131 |

Transportation and logistics | |

| 4,275 | |

| — |

| 236 | |

| 4,511 |

Total for the year | | $ | 87,548 | | $ | 936 | $ | 3,371 | | $ | 91,855 |

Year ended December 31, 2022 | | Eskay | | Snip | Other | | Total | ||||

Accretion | | $ | 63 | | $ | — | $ | — | | $ | 63 |

Assays and analysis/storage | |

| 3,728 | |

| 239 |

| 102 | |

| 4,069 |

Camp and safety | |

| 2,985 | |

| — |

| 1 | |

| 2,986 |

Claim renewals and permits | | | 900 | | | 57 | | — | | | 957 |

Community relations | |

| — | |

| — |

| 18 | |

| 18 |

Depreciation | | | 1,623 | | | — | | — | | | 1,623 |

Drilling | |

| 13,131 | |

| — |

| 1,681 | |

| 14,812 |

Electrical | | | 403 | | | — | | — | | | 403 |

Environmental studies | |

| 8,515 | |

| 54 |

| — | |

| 8,569 |

Equipment rental | |

| 3,272 | |

| 3 |

| 12 | |

| 3,287 |

Fieldwork, camp support | |

| 17,746 | |

| 104 |

| 135 | |

| 17,985 |

Fuel | | | 3,707 | | | — | | 284 | | | 3,991 |

Geology, geophysics, and geochemical | |

| 17,909 | |

| 18 |

| 273 | |

| 18,200 |

Helicopter | | | 4,441 | | | — | | 960 | | | 5,401 |

Metallurgy | | | 676 | | | — | | — | | | 676 |

Part XII.6 tax, net of METC | |

| 36 | |

| — |

| (250) | |

| (214) |

Share-based payments | |

| 3,584 | |

| — |

| — | |

| 3,584 |

Transportation and logistics | |

| 4,081 | |

| — |

| 1,111 | |

| 5,192 |

Total for the year | | $ | 86,800 | | $ | 475 | $ | 4,327 | | $ | 91,602 |

Exploration and evaluation expenses were slightly higher for the year ended December 31, 2023 as compared to the year ended December 31, 2022. Exploration and evaluation activity on the Eskay Creek property increased slightly primarily due to the completion of the DFS during the year ended December 31, 2023. The Company incurred increased amounts on environmental studies, drilling, and geology, which include salaries to complete the DFS. The increase in environmental studies costs was also due to supporting the advancement of permitting activities on Eskay Creek. The increased expenditures were partially offset by reduced costs in the following categories: fieldwork and camp support, camp and safety costs, assays and analysis, and helicopter costs.

| Management’s Discussion & Analysis | 20 |

SKEENA RESOURCES LIMITED

Management Discussion and Analysis

For the year ended December 31, 2023

(Expressed in thousands of Canadian dollars within tables, unless otherwise noted)

Overall exploration and evaluation activities on the Snip property for the year ended December 31, 2023 increased as compared to December 31, 2022 due to the termination of the Hochschild option agreement in April 2023.

The following tables report selected financial information of the Company for the past eight quarters.

Quarter ended | | 31-Dec-23 | | 30-Sep-23 | | 30-Jun-23 | | 31-Mar-23 | ||||||

Revenue (1) | $ | — | $ | — | $ | — | $ | — | ||||||

Loss for the quarter | $ | (32,956) | $ | (39,795) | $ | (19,486) | $ | (16,743) | ||||||

Loss per share | $ | (0.37) | $ | (0.45) | $ | (0.24) | $ | (0.22) | ||||||

Quarter ended | | 31-Dec-22 | | 30-Sep-22 | | 30-Jun-22 | | 31-Mar-22 | ||||||

Revenue (1) | $ | — | $ | — | $ | — | $ | — | ||||||

Loss for the quarter | $ | (16,409) | $ | (28,778) | $ | (24,687) | $ | (19,016) | ||||||

Loss per share | $ | (0.22) | $ | (0.41) | $ | (0.36) | $ | (0.29) | ||||||

| (1) | being an exploration stage company, there are no revenues from operations |

Loss and comprehensive loss for the fourth quarter ended December 31, 2023

Loss of $32,956,000 during the three months ended December 31, 2023 (“Q423”) were higher than the loss during the three months ended December 31, 2022 (“Q422”) of $16,409,000. The primary reason for the increase in loss in Q423 compared to Q422 is due to an increase in exploration and evaluation expenses to $27,956,000 (Q422 – $19,658,000). Exploration activity increased primarily due to expenses incurred on environmental studies, drilling, and geology. The increase in environmental studies costs was mainly incurred to support the advancement of permitting activities. Administrative compensation also increased to $2,069,000 (Q422 – $1,351,000) and in Q422, the Company recognized a gain of $9,463,000 relating to the purchase and sale of a royalty, with no such transaction in Q423. The aforementioned was partially offset by an increase in the flow-through share premium recovery to $1,258,000 (Q422 – $256,000) on higher flow-through eligible expenditures during Q423 as well as a decrease in communications costs to $282,000 (Q422 – $1,088,000) which is primarily attributable to the departure of the Senior VP, Corporate Development and a reduction in investor relation activities compared to Q422.

Loss and comprehensive loss for the year ended December 31, 2023

Loss of $108,980,000 during the year ended December 31, 2023 (“F2023”) was higher than the loss during the year ended December 31, 2022 (“F2022”) of $88,890,000. The primary reasons for the increase in loss is due to a decrease in flow-through share premium recovery to $5,078,000 (F2022 – $13,326,000) as a result of a reduction in flow-through eligible expenditures during F2023 compared to F2022. Share-based payments increased to $8,856,000 (F2022 – $7,387,000) which was primarily due to the amounts recognized on stock options and RSUs issued in previous years with vesting terms into F2023 and partially due to equity awards issued under the Company’s long term incentive plan during F2023. Administrative compensation also increased to $6,378,000 (F2022 – $4,805,000) as a result of an increase in the number of staff and individual compensation compared to prior year and in Q422, the Company recognized a gain of $9,463,000 relating to the purchase and sale of a royalty, with no such transaction in Q423. The Company also incurred a loss on marketable securities of $544,000 (F2022 – gain of $1,007,000) resulting from the decrease in the fair value of portfolio of securities held by the Company.

| Management’s Discussion & Analysis | 21 |

SKEENA RESOURCES LIMITED

Management Discussion and Analysis

For the year ended December 31, 2023

(Expressed in thousands of Canadian dollars within tables, unless otherwise noted)

The increase in loss between F2023 and F2022 was partially offset by an increase in interest income to $2,040,000 (F2022 – $361,000) due to higher average cash account balances in combination with higher interest rates on the Company’s savings accounts and GICs. Communication expenses decreased to $1,316,000 (F2022 – $2,800,000) due to the departure of the Senior VP, Corporate Development and reduction in investor relation activities, and insurance costs decreased to $1,721,000 (F2022 – $1,922,000) due to the reduction in the Company’s insurance policy premiums.

Cash flows for the year ended December 31, 2023

The Company’s operating activities consumed net cash of $90,598,000 during F2023 (F2022 – $93,381,000). The decrease in cash used in operating activities from F2022 to F2023 was primarily due to the timing of payments made for expenses which resulted in a higher accounts payable and accrued liabilities balance as well as higher amounts of BCMETC received in F2023.

During F2023, the Company’s investing activities generated net cash of $31,268,000 (F2022 – $11,401,000). More cash was generated in investing activities primarily due to the proceeds received of $56,000,000 from the sale of a 1% NSR royalty during F2023 compared to proceeds of $27,000,000 from the sale of a 0.5% NSR royalty. The aforementioned increase was partially offset by the construction of a modular analytical laboratory at Eskay Creek, construction of a newly leased office space in Vancouver, and amounts paid for earthworks for certain infrastructure at Eskay Creek.

Cash provided by financing activities of $109,863,000 increased during F2023 as compared to $82,269,000 during F2022. The increase is primarily attributed to the bought deal financing that closed in May 2023 for gross proceeds of $73,537,000 as compared to the bough deal financing the closed in September 2022 for gross proceeds of $34,500,000.

In addition, the Company received proceeds of $25,000,000 from the issuance of a convertible debenture to Franco-Nevada in December 2023. This was offset by a decrease in proceeds received from flow-through private placements to $15,275,000 in F2023 from $18,040,000 in F2022, decrease in proceeds received from warrant exercises to $65,000 in F2023 from $30,375,000 in F2022 and a decrease in proceeds received through option exercises to $1,034,000 in F2023 from $2,485,000 in F2022. Additionally, lease payments increased to $991,000 in F2023 as compared to $477,000 in F2022 due to increased office and equipment leases.

LIQUIDITY AND CAPITAL RESOURCES

The Company has previously relied primarily on share issuances in order to fund its exploration and evaluation activities and other business objectives. As at December 31, 2023, the Company has cash and cash equivalents of $91,135,000. Based on forecasted expenditures, this balance will be sufficient to fund the Company’s committed exploration and evaluation expenditures and general administrative costs for at least twelve months from the reporting date. However, if the Company continues its current level of exploration and evaluation activities planned for twelve months from the reporting date, the current cash balances will not be sufficient to fund these expenditures. The Company expects to continue to raise the necessary funds primarily through the issuance of shares and construction financing which is anticipated to be provided through a combination of debt, equity and other instruments at the appropriate time. In the longer term, the Company’s ability to continue as a going concern is dependent upon successful execution of its business plan (including bringing the Eskay Creek Project to profitable operations), raising additional capital or evaluating strategic alternatives for its mineral property interests. There can be no guarantees that future equity and construction financings will be available on acceptable terms or at all, in which case the Company may need to reduce or delay its longer-term exploration and evaluation plans.

| Management’s Discussion & Analysis | 22 |

SKEENA RESOURCES LIMITED

Management Discussion and Analysis

For the year ended December 31, 2023

(Expressed in thousands of Canadian dollars within tables, unless otherwise noted)

Critical accounting estimates are estimates and assumptions made by management that may result in a material adjustment to the carrying amounts of assets and liabilities and include the following:

| ● | Recoverable amount of exploration and evaluation interests |

The carrying value of exploration and evaluation assets and the likelihood of future economic recoverability of these carrying values is subject to significant management estimates. The application of the Company’s accounting policy for and determination of recoverability of capitalized assets is based on assumptions about future events or circumstances. New information may change estimates and assumptions made. If information becomes available indicating that recovery of expenditures are unlikely, the amounts capitalized are impaired and recognized as a loss in the period that the new information becomes available.

| ● | Valuation of exploration and evaluation assets acquired |

The cost of acquiring exploration and evaluation assets is capitalized and represents their fair value at the date of acquisition. The carrying values of properties acquired by Skeena resulting from the acquisition of QuestEx and sale of certain assets to Newmont Corporation are subject to estimates relating to: (i) fair value of non-cash portion of consideration paid to acquire QuestEx; (ii) fair value of other assets and liabilities of QuestEx at acquisition date; and (iii) estimated value of mineral resources within the properties, including their exploration potential. The carrying value of Eskay North mineral property, which was regarded as part of Eskay Creek property, and Red Chris properties are subject to estimates relating to the fair value of the non-cash consideration and discount rate used to determine the present value of future cash obligations.

| ● | Valuation of contingent consideration receivable |

The value of contingent consideration receivable from Franco-Nevada Corporation is subject to significant estimates relating to the probability of occurrence of certain contingent events.

| ● | Leases |

The incremental borrowing rates used to determine the fair values of the right-of-use assets and lease liabilities are highly subjective and could materially affect these fair value estimates.

| ● | Provision for closure and reclamation |

The process of determining a value for the closure and reclamation provision is subject to estimates and assumptions. Significant estimates include the amount and timing of closure and reclamation costs and the discount rate used.

| ● | Share-based payments |

The fair value of share-based payments is subject to the limitations of the Black-Scholes option pricing model that incorporates market data and involves uncertainty in estimates used by management in the assumptions. Because the Black-Scholes option pricing model requires the input of highly subjective assumptions, including the volatility of share prices and risk-free rates, changes in the subjective input assumptions can materially affect the fair value estimate.

| Management’s Discussion & Analysis | 23 |

SKEENA RESOURCES LIMITED

Management Discussion and Analysis

For the year ended December 31, 2023

(Expressed in thousands of Canadian dollars within tables, unless otherwise noted)

| ● | Valuation of the components of the convertible debenture |

The fair value of financial instruments that are not traded in active market are determined using valuation techniques. The convertible debenture contains multiple embedded derivatives. Management uses its judgment to select a method of valuation and makes estimates of specific model inputs that are based on conditions, including market, existing at the end of each reporting period. See Note 13 to the financial statements for further details on the methods and assumptions associated with the measurement of the convertible debenture. There is a high degree of estimation uncertainty associated with the inputs in the models used to value the components of the convertible debenture. Changes in assumptions or estimates used in determining the fair value of the financial instruments could impact the values attributed to the components of the convertible debenture in the statement of financial position. Such a change would also impact the fair value movements of the statement of loss and comprehensive loss for the period.

CHANGES IN ACCOUNTING POLICIES

New accounting policies adopted in 2023

The following amendments to existing standards have been adopted by the Company commencing January 1, 2023:

Amendments to IAS 1 and IFRS Practice Statement 2: Disclosure of Accounting Policies

The Company adopted Disclosure of Accounting Policies (Amendments to IAS 1 and IFRS Practice Statement 2) from January 1, 2023. The amendments require the disclosure of 'material', rather than 'significant', accounting policies. Although the amendments did not result in any changes to the accounting policies themselves, they impacted the accounting policy information disclosed in certain instances.

Amendments to IAS 1: Presentation of Financial Statements

In October 2022, the IASB issued amendments to IAS 1, Presentation of Financial Statements, titled Non-current liabilities with covenants. These amendments sought to improve the information that an entity provides when its right to defer settlement of a liability is subject to compliance with covenants within 12 months after reporting period. These amendments to IAS 1 override but incorporate the previous amendments, Classification of liabilities as current or non-current, issued in January 2020, which clarified that liabilities are classified as either current or non-current depending on the rights that exist at the end of the reporting period. Liabilities should be classified as non-current if a company has a substantive right to defer settlement for at least 12 months at the end of the reporting period.

The Company retrospectively adopted these amendments to IAS 1 from January 1, 2022. The adoption of these amendments to IAS 1 had no material impact on the 2022 financial statements. Had the Company not adopted the amendments to IAS 1 in 2023, under the previous IAS 1 guidance, the convertible debenture would have been classified as a current liability as at December 31, 2023 as Management expects that the convertible debenture will be repaid during 2024 upon completion of project financing for the construction and development of the Eskay Creek project (Note 13 to the financial statements). The amendments to IAS 1 eliminate the requirement to consider Management’s expectations of the timing and settlement of a liability when assessing the classification of a liability as current or non-current.

| Management’s Discussion & Analysis | 24 |

SKEENA RESOURCES LIMITED

Management Discussion and Analysis

For the year ended December 31, 2023

(Expressed in thousands of Canadian dollars within tables, unless otherwise noted)

New standards and interpretations not yet adopted in 2023

Amendments to IAS 7 and IFRS 7: Supplier Finance Arrangements

In May 2023, the IAS issued amendments to IAS 7, Statement of Cash flows, and IFRS 7, Financial Instruments Disclosures, to provide guidance on disclosures related to supplier finance arrangements that enable the users of financial statements to assess the effects of these arrangements on the entity’s liabilities and cash flows and on the entity’s exposure to liquidity risk.

The Company adopted these amendments to IAS 7 and IFRS 7 effective January 1, 2024. The Company has entered into certain equipment supplier finance arrangements in 2024. Management is currently evaluating the disclosure required under these amendments to IAS 7 and IFRS 7 for the Company’s condensed interim consolidated financial statements for the three months ended March 31, 2024.