Q1 2026PRESENTATION May 21, 2026

Disclaimer Forward-Looking Statements These presentational materials and related

discussions include forward-looking statements made under the "safe harbor" provisions of the U.S. Private Securities Litigation Reform Act of 1995. Forward looking statements do not reflect historical facts and may be identified by words such

as "anticipate", "believe", "continue", "estimate", "expect", "intends", "may", "should", "will", "likely", "aim", "plan", "guidance", the negative of such terms, and similar expressions and include statements regarding industry trends and

market outlook, expectations about Adjusted EBITDA in Q2, an expected rebound in the second half of 2026, expectations about the start date of the Odin contract, supply/demand expectations, statements about the state of the jack-up rig and oil

industry, including our confidence in our prospects for 2027 and 2028, our expectations about increased activity and dayrates, including associated oil price developments and associated timing, and our expectations about the impact of the

Middle East conflict, Dayrate Equivalent Backlog, contractual commitments, tender activity and expected contracting, customer activity and contracting opportunities, market conditions, statements about the global jack-up fleet, including the

number of rigs contracted and available and expected trends in the global fleet, including expected new deliveries and the number of rigs under construction and expectations as to when such rigs will join the global fleet, statements about the

Five-Rig Acquisition and the Fontis Acquisition (both as defined in our Q1 2026 earnings release dated May 20, 2026), including the expected timing of the completion of such acquisition, and statements made under “Market” and "Risk and

uncertainties" in our Q1 2026 earnings release dated May 20, 2026, and other non-historical statements. These forward-looking statements are based upon current expectations and various assumptions, which are, by their nature, uncertain and are

subject to significant known and unknown risks, contingencies and other important factors which are difficult or impossible to predict and are beyond our control. Such risks, uncertainties, contingencies and other factors could cause our actual

financial results, level of activity, performance, financial position, liquidity or achievements to differ materially from those expressed or implied by these forward-looking statements, including risks relating to our industry and industry

conditions, business, the risk that our actual results of operations in current or future periods differ materially from expected trends in results discussed herein, the timing of payments to us and the risk of delays in payments or receivables

to our JVs and payments from our JVs to us, the risk that our customers do not comply with their contractual obligations, including the risk that we may not be able to recover amounts due from our customers or that customers may not be able to

continue to comply with contracts with us, the risk of customers becoming subject to sanctions, risks relating to geopolitical events and inflation, risks relating to global economic uncertainty and energy commodity prices, risks relating to

contracting, including our ability to convert commitments, LOIs and LOAs into contracts, the risk of contract suspension or termination, the risk that options will not be exercised, the risk that backlog will not materialize as expected, risks

relating to the operations of our rigs, risks relating to dayrates and duration of contracts and the terms of contracts and the risk that we may not enter into contracts or that contracts are not performed as expected, risks relating to

contracting our most recently delivered and acquired rigs and other available rigs including the five rigs acquired in the Five-Rig Acquisition and the five rigs to be acquired in respect of the Fontis Acquisition, and other risks related to

such acquisitions, risks relating to market trends, including tender activity, risks relating to customer demand and contracting activity and suspension or termination of operations, including as a result of customers becoming subject to

sanctions, risks relating to our liquidity and cash flows, risks relating to our indebtedness including risks relating to our ability to repay or refinance our debt at maturity, including our secured notes maturing in 2028 and 2030, our

Convertible Bonds due 2028 and due 2033, our seller’s credit with Noble Corporation due 2032 and debt under our revolving credit facilities and risks relating to our other payment obligations on these debt instruments including interest,

amortization and cash sweeps, risks relating to our ability to comply with covenants under our revolving credit facilities and other debt instruments and obtain any necessary waivers and the risk of cross defaults, risks relating to our ability

to pay cash distributions and repurchase shares including the risk that we may not have available liquidity or distributable reserves or the ability under our debt instruments to pay such cash distributions or repurchase shares and the risk

that we may not complete our share repurchase program in full, and risks relating to the amount and timing of any cash distributions we declare, risks relating to future financings including the risk that future financings may not be completed

when required and risks relating to the terms of any refinancing, including risks related to dilution from any future offering of shares or convertible bonds, risks related to climate change, including climate-change or greenhouse gas related

legislation or regulations and the impact on our business from physical climate-change related to changes in weather patterns, and the potential impact of new regulations relating to climate change and the potential impact on the demand for oil

and gas, risks relating to military actions and their impact on our business and industry, and other risks factors set forth under “Risk Factors” in our most recent annual report on Form 20-F and other filings with and submissions to the U.S.

Securities and Exchange Commission. These forward-looking statements are made only as of the date of this document. We undertake no (and expressly disclaim any) obligation to update any forward-looking statements after the date of this report

or to conform such statements to actual results or revised expectations, except as required by law. Non-GAAP Financial Measures The Company uses certain financial information calculated on a basis other than in accordance with accounting

principles generally accepted in the United States (US GAAP) including Adjusted EBITDA. Adjusted EBITDA as presented above represents our periodic net income/(loss) adjusted for: depreciation of non-current assets, (loss)/income) from equity

method investments, total financial expense net and income tax expense. Adjusted EBITDA is presented here because the Company believes that the measure provides useful information regarding the Company’s operational performance. For a

reconciliation of Adjusted EBITDA to Net income/(loss), please see the last page of this report. The Company provides guidance on expected Adjusted EBITDA, which is a non-GAAP financial measure. Management evaluates the Company's financial

performance in part based on the basis of actual and expected Adjusted EBITDA, which management believes enhances investors' understanding of the Company's overall financial performance by providing them with an additional meaningful relevant

comparison of current and anticipated future results across periods. Due to the forward-looking nature of Adjusted EBITDA, management cannot reliably predict certain of the necessary components of the most directly comparable forward-looking

GAAP measure. Accordingly, the Company is unable to present a quantitative reconciliation of such forward looking non-GAAP financial measure to the most directly comparable forward-looking GAAP financial measure without unreasonable effort. The

Company disclaims any current intention to update such guidance, except as required by law

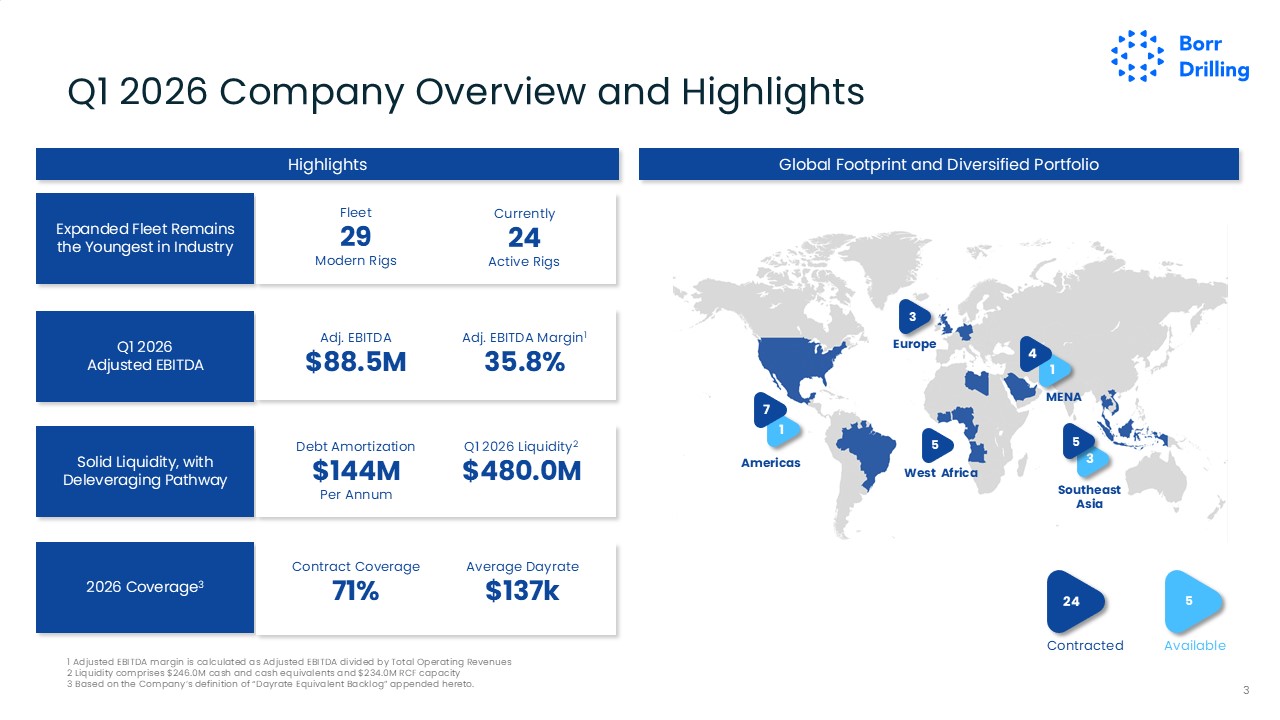

1 Q1 2026 Company Overview and Highlights 1 Adjusted EBITDA margin is calculated

as Adjusted EBITDA divided by Total Operating Revenues 2 Liquidity comprises $246.0M cash and cash equivalents and $234.0M RCF capacity 3 Based on the Company’s definition of “Dayrate Equivalent Backlog” appended hereto. 3 Global Footprint

and Diversified Portfolio Q1 2026 Adjusted EBITDA Adj. EBITDA $88.5M Adj. EBITDA Margin1 35.8% 2026 Coverage3 Contract Coverage71% Average Dayrate $137k Solid Liquidity, with Deleveraging Pathway Q1 2026 Liquidity2 $480.0M Debt

Amortization $144M Per Annum Expanded Fleet Remains the Youngest in Industry Currently 24 Active Rigs Fleet 29 Modern Rigs Highlights Contracted 24 Available 5 3 Americas 2 1 5 Southeast Asia MENA 4 West

Africa 5 1 3 Europe 1 7

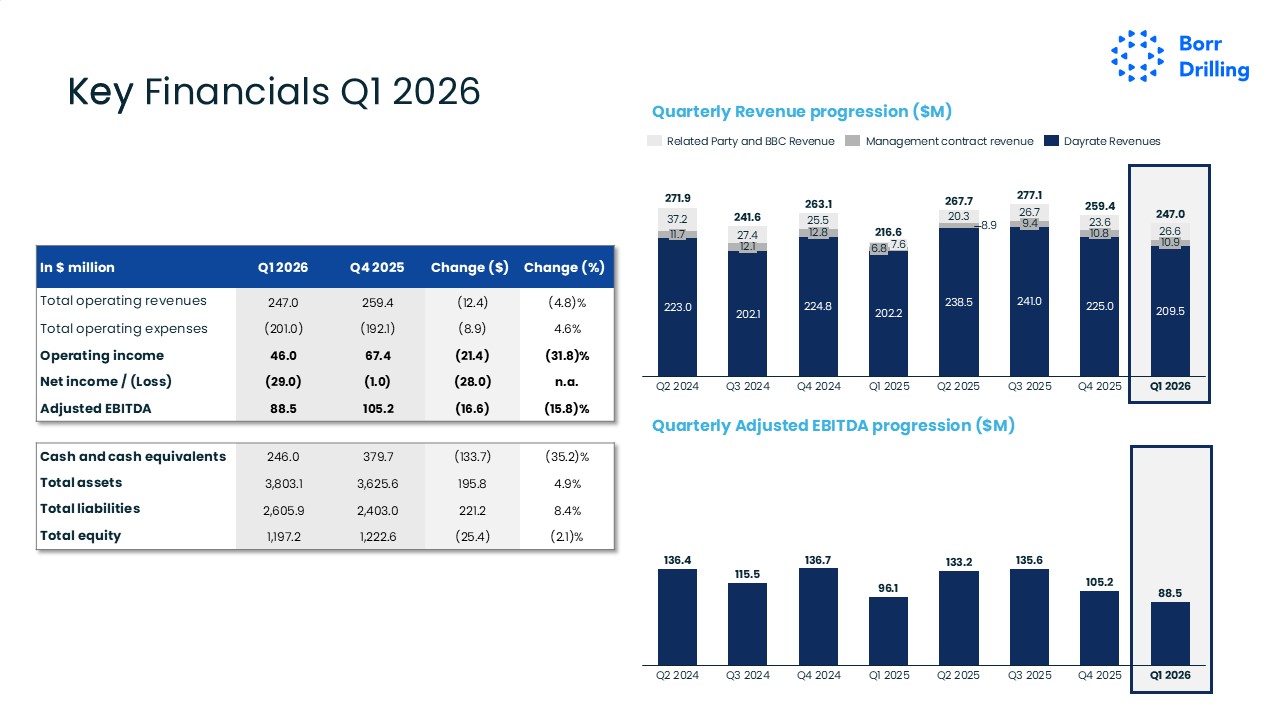

In $ million Q1 2026 Q4 2025 Change ($) Change (%) Total operating

revenues 247.0 259.4 (12.4) (4.8)% Total operating expenses (201.0) (192.1) (8.9) 4.6% Operating income 46.0 67.4 (21.4) (31.8)% Net income / (Loss) (29.0) (1.0) (28.0) n.a. Adjusted

EBITDA 88.5 105.2 (16.6) (15.8)% Cash and cash equivalents 246.0 379.7 (133.7) (35.2)% Total assets 3,803.1 3,625.6 195.8 4.9% Total liabilities 2,605.9 2,403.0 221.2 8.4% Total

equity 1,197.2 1,222.6 (25.4) (2.1)% Quarterly Revenue progression ($M) Quarterly Adjusted EBITDA progression ($M) Key Financials Q1 2026 Key 11.7 Q2 2024 12.1 Q3 2024 12.8 Q4 2024 7.6 6.8 Q1 2025 Q2 2025 9.4 Q3

2025 10.8 Q4 2025 10.9 Q1 2026 271.9 241.6 263.1 216.6 267.7 277.1 259.4 247.0 Related Party and BBC Revenue Management contract revenue Dayrate Revenues Q2 2024 Q3 2024 Q4 2024 Q1 2025 Q2 2025 Q3 2025 Q4 2025 Q1

2026 88.5

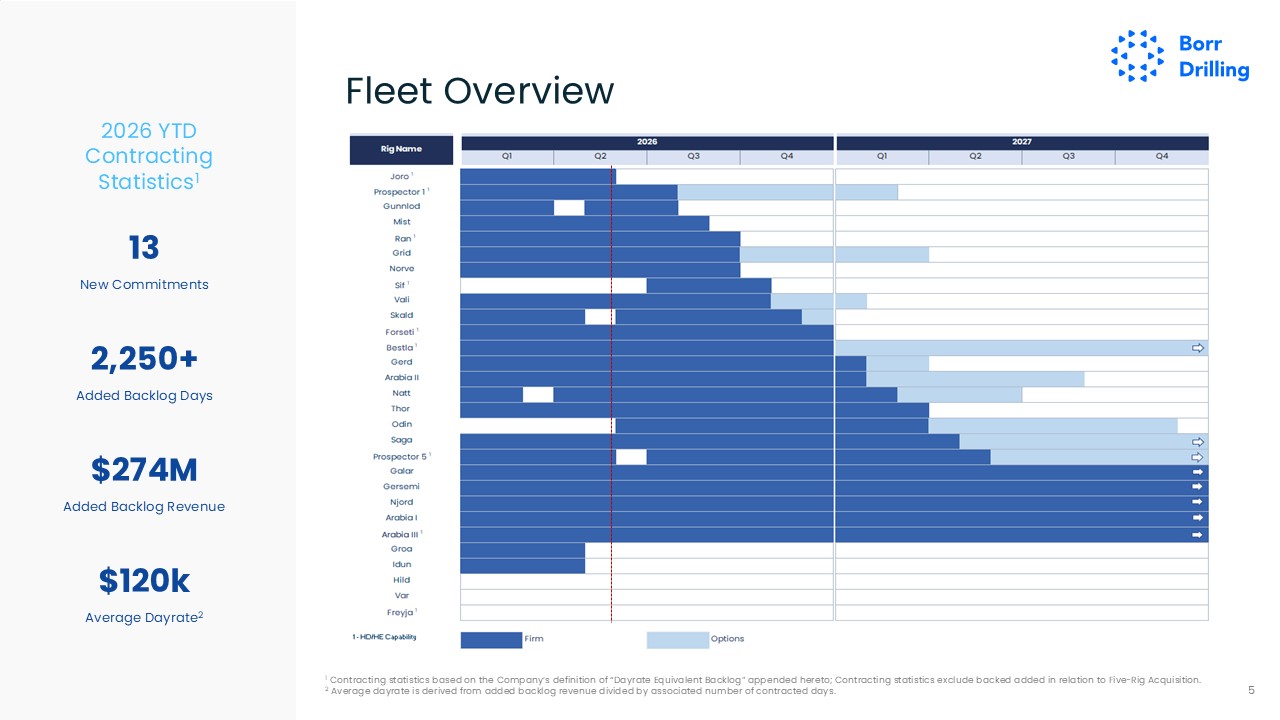

1 Contracting statistics based on the Company’s definition of “Dayrate Equivalent

Backlog” appended hereto; Contracting statistics exclude backed added in relation to Five-Rig Acquisition. 2 Average dayrate is derived from added backlog revenue divided by associated number of contracted days. 5 Fleet Overview 13 New

Commitments $274M Added Backlog Revenue $120k Average Dayrate2 2,250+ Added Backlog Days 2026 YTD Contracting Statistics1

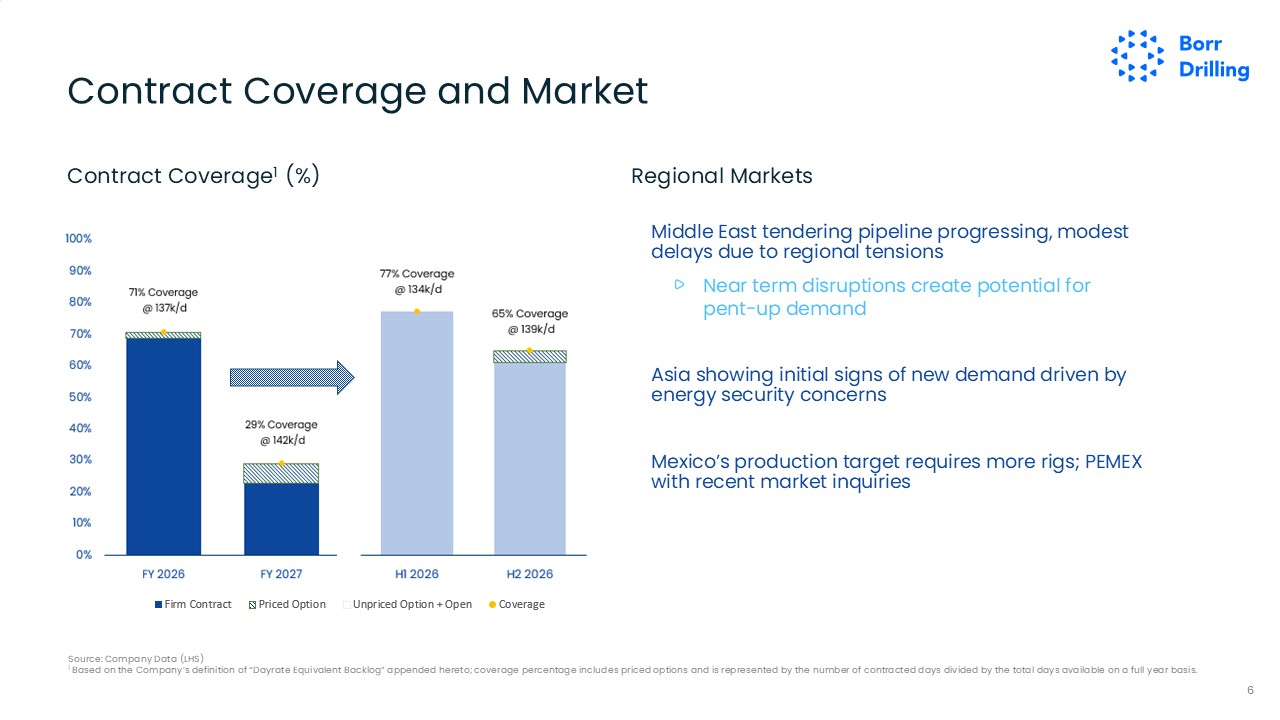

Contract Coverage and Market Source: Company Data (LHS) 1 Based on the

Company’s definition of “Dayrate Equivalent Backlog” appended hereto; coverage percentage includes priced options and is represented by the number of contracted days divided by the total days available on a full year basis. 6 Middle East

tendering pipeline progressing, modest delays due to regional tensions Asia showing initial signs of new demand driven by energy security concerns Mexico’s production target requires more rigs; PEMEX with recent market inquiries Contract

Coverage1 (%) Near term disruptions create potential for pent-up demand Regional Markets

7 In Conclusion Macro events continue to strengthen the fundamental outlook for

shallow water market 1 Driving shareholder value via opportunistic asset acquisitions and continuing to enhance capital structure 3 1 Focused on near-term coverage; Fleet availability in 2027-2028 is a strategic asset 2

Appendix

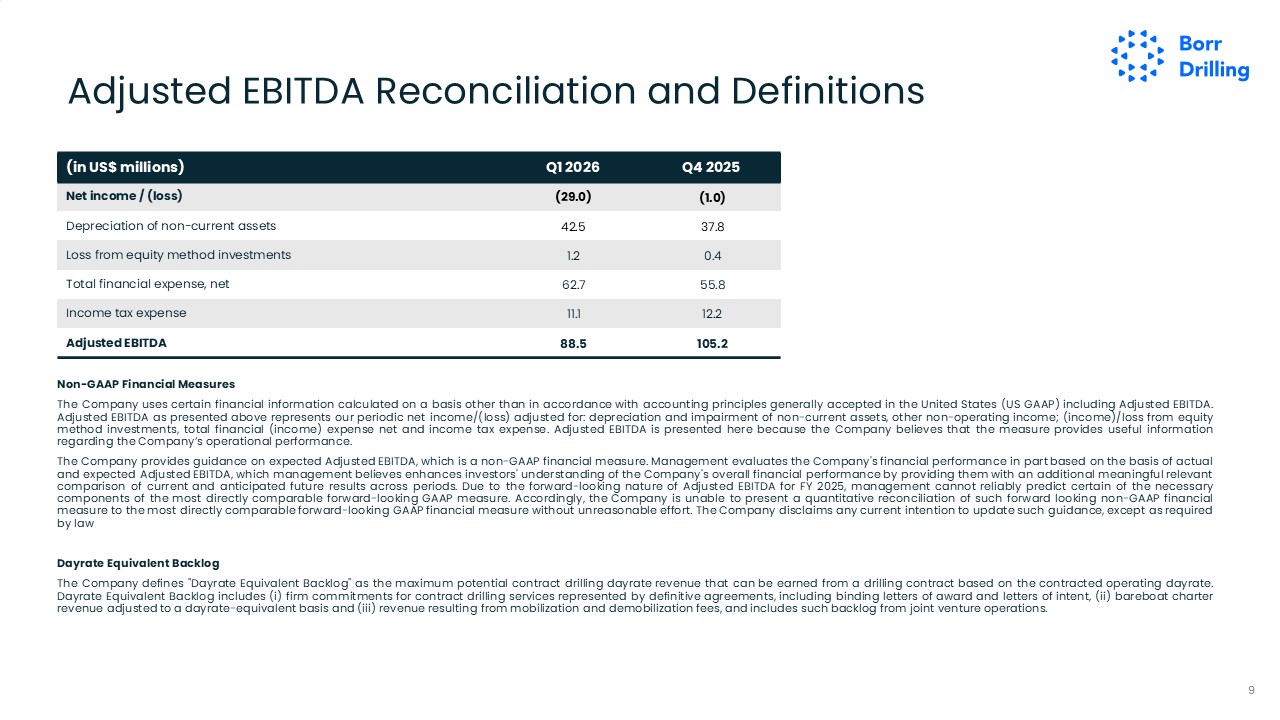

9 (in US$ millions) Q1 2026 Q4 2025 Net income /

(loss) (29.0) (1.0) Depreciation of non-current assets 42.5 37.8 Loss from equity method investments 1.2 0.4 Total financial expense, net 62.7 55.8 Income tax expense 11.1 12.2 Adjusted EBITDA 88.5 105.2 Non-GAAP Financial

Measures The Company uses certain financial information calculated on a basis other than in accordance with accounting principles generally accepted in the United States (US GAAP) including Adjusted EBITDA. Adjusted EBITDA as presented above

represents our periodic net income/(loss) adjusted for: depreciation and impairment of non-current assets, other non-operating income; (income)/loss from equity method investments, total financial (income) expense net and income tax expense.

Adjusted EBITDA is presented here because the Company believes that the measure provides useful information regarding the Company’s operational performance. The Company provides guidance on expected Adjusted EBITDA, which is a non-GAAP

financial measure. Management evaluates the Company's financial performance in part based on the basis of actual and expected Adjusted EBITDA, which management believes enhances investors' understanding of the Company's overall financial

performance by providing them with an additional meaningful relevant comparison of current and anticipated future results across periods. Due to the forward-looking nature of Adjusted EBITDA for FY 2025, management cannot reliably predict

certain of the necessary components of the most directly comparable forward-looking GAAP measure. Accordingly, the Company is unable to present a quantitative reconciliation of such forward looking non-GAAP financial measure to the most

directly comparable forward-looking GAAP financial measure without unreasonable effort. The Company disclaims any current intention to update such guidance, except as required by law Dayrate Equivalent Backlog The Company defines "Dayrate

Equivalent Backlog" as the maximum potential contract drilling dayrate revenue that can be earned from a drilling contract based on the contracted operating dayrate. Dayrate Equivalent Backlog includes (i) firm commitments for contract drilling

services represented by definitive agreements, including binding letters of award and letters of intent, (ii) bareboat charter revenue adjusted to a dayrate-equivalent basis and (iii) revenue resulting from mobilization and demobilization fees,

and includes such backlog from joint venture operations. Adjusted EBITDA Reconciliation and Definitions

10