Please wait

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

|

|

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) |

OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2018

Commission file number 001-38414

SPIRIT MTA REIT

(Exact name of registrant as specified in its charter)

|

| | | | |

Maryland | | | | 82-6712510 |

(State or other jurisdiction of incorporation or organization) | | | | (I.R.S. Employer Identification Number) |

| | | | |

2727 North Harwood Street, Suite 300, Dallas, Texas 75201 | | | | (972) 476-1409 |

(Address of principal executive offices; zip code) | | | | (Registrant’s telephone number, including area code) |

Securities registered pursuant to Section 12(b) of the Act:

|

| | | |

Title of each class: | | | Name of exchange on which registered: |

Common Shares of Beneficial Interest, par value $0.01 per share | | | New York Stock Exchange |

Securities registered pursuant to Section 12(g) of the Act: None.

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes o No x

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes o No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No o

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes x No o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§ 229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. x

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and "emerging growth company" in Rule 12b-2 of the Exchange Act.

|

| | | | | | | |

Large accelerated filer | o | Accelerated filer | o | Non-accelerated filer | x | Smaller reporting company | o |

Emerging growth company | x | | | | | | |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. o

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes o No x

As of June 29, 2018 (the last business day of the registrant’s most recently completed second fiscal quarter), the aggregate market value of Spirit MTA REIT's common shares, $0.01 par value, held by non-affiliates of the Registrant, was $441.4 million based on the last reported sale price of $10.30 per share on the New York Stock Exchange on June 29, 2018.

The number of outstanding shares of Spirit MTA REIT's common shares, $0.01 par value, as of March 19, 2019, was 43,085,751 shares.

Documents Incorporated by Reference

Certain specific portions of the definitive Proxy Statement for Spirit MTA REIT's 2019 Annual Meeting of Shareholders to be filed pursuant to Regulation 14A are incorporated by reference into Part III, Items 10, 11, 12, 13 and 14 of this Annual Report on Form 10-K. Only those portions of the Proxy Statement which are specifically incorporated by reference herein shall constitute a part of this Annual Report on Form 10-K.

EXPLANATORY NOTE

This annual report of Spirit MTA REIT includes the financial information of the Company as of December 31, 2018 and December 31, 2017 and for the years ended December 31, 2018, 2017 and 2016.

On May 31, 2018, the distribution date, Spirit Realty Capital, Inc. completed the previously announced Spin-Off of the assets that collateralize Master Trust 2014, all of its properties leased to Shopko, and certain other assets into an independent, publicly traded REIT, Spirit MTA REIT. The Spin-Off was effected by means of a pro rata distribution of one SMTA common share for every ten shares of Spirit common stock held by each of Spirit's stockholders as of May 18, 2018, the record date.

The accompanying financial statements include the consolidated accounts of the Company and its wholly-owned subsidiaries for the period subsequent to the Spin-Off on May 31, 2018. The pre-spin financial statements were prepared on a carve-out basis and reflect the combined net assets and operations of the predecessor legal entities for periods prior to the Spin-Off which formed the Company at the time of the Spin-Off. Accordingly, the results of operations for the years ended December 31, 2018, 2017 and 2016 reflect the aggregate operations and changes in cash flows and equity on a combined basis for all periods prior to May 31, 2018 and on a consolidated basis for all periods subsequent to May 31, 2018. The discussion of our results of operations, cash flows and financial condition set forth in this report is not necessarily indicative of the future results of operations, cash flows or financial condition as an independent, publicly traded company.

GLOSSARY

|

| |

2017 Tax Legislation | Tax Cuts and Jobs Act |

2018 Incentive Award Plan | Spirit MTA REIT and Spirit MTA REIT, L.P. 2018 Incentive Award Plan |

ACM | Asbestos-containing materials |

ADA | Americans with Disabilities Act |

Adjusted Debt | Adjusted Debt is a non-GAAP financial measure. See definition in Item 6. Selected Financial Data. |

Adjusted EBITDAre | Adjusted EBITDAre is a non-GAAP financial measure. See definition in Item 6. Selected Financial Data. |

AFFO | Adjusted Funds From Operations is a non-GAAP financial measure. See definition in Item 6. Selected Financial Data. |

ASC | Accounting Standards Codification |

Asset Management Agreement | Asset Management Agreement between Spirit Realty, L.P. and Spirit MTA REIT dated May 31, 2018 |

ASU | Accounting Standards Update |

CMBS | Commercial mortgage-backed securities |

Code | Internal Revenue Code of 1986, as amended |

Collateral Pool | Pool of collateral assets that are pledged to the indenture trustee for the benefit of the noteholders and secure obligations of issuers under Master Trust 2014 |

Contractual Rent | Monthly contractual cash rent, excluding percentage rents, from properties owned fee-simple or ground leased, recognized during the final month of the reporting period, adjusted to exclude amounts received from properties sold during that period and adjusted to include a full month of contractual rent for properties acquired during that period. We use Contractual Rent when calculating certain metrics that are useful to evaluate portfolio credit, asset type, industry, and geographic diversity and to manage risk. |

CPI | Consumer Price Index |

EBITDA | Earnings Before Interest, Taxes, Depreciation and Amortization |

EBITDAR | EBITDAR is a non-GAAP financial measure defined as Earnings Before Interest, Taxes, Depreciation, Amortization and Rent |

EBITDAre | EBITDAre is a non-GAAP financial measure and is computed in accordance with standards established by NAREIT. See definition in Item 6. Selected Financial Data. |

EDF | Expected Default Frequency |

Exchange Act | Securities Exchange Act of 1934, as amended |

FASB | Financial Accounting Standards Board |

FFO | Funds From Operations. See definition in Item 6. Selected Financial Data. |

GAAP | Generally Accepted Accounting Principles in the United States |

LIBOR | London Interbank Offered Rate |

Liquidity Reserve | Cash held on deposit until there is a cashflow shortfall as defined in the Master Trust 2014 agreements or a liquidation of Master Trust 2014 occurs |

Manager | Spirit Realty, L.P., a wholly-owned subsidiary of Spirit |

Master Trust 2014 | The asset-backed securitization trust established in 2005, and amended and restated in 2014, which issues non-recourse net-lease mortgage notes collateralized by commercial real estate, net-leases and mortgage loans from time to time. Indirect special purpose entity subsidiaries of the Company are the borrowers. |

MGCL | Maryland General Corporation Law |

|

| |

NAREIT | National Association of Real Estate Investment Trusts |

NYSE | New York Stock Exchange |

Occupancy | The number of economically yielding owned properties divided by total owned properties |

Other Properties | One of two reportable segments consisting of all properties not included in the Master Trust 2014 Collateral Pool |

Properties | Owned properties and mortgage loans receivable secured by properties |

Property Management and Servicing Agreement | Second amended and restated agreement governing the management services and special services provided to Master Trust 2014 by Spirit Realty, L.P., dated as of May 20, 2014, as amended, supplemented, amended and restated or otherwise modified |

Real Estate Investment Value | The gross acquisition cost, including capitalized transaction costs, plus improvements and less impairments, if any |

REIT | Real Estate Investment Trust |

Release Account | Proceeds from the sale of assets securing Master Trust 2014 held in a restricted account until a qualifying substitution is made or the funds are applied as prepayment of principal |

Separation and Distribution Agreement | Separation and Distribution Agreement between Spirit Realty Capital, Inc. and Spirit MTA REIT dated May 21, 2018 |

SEC | Securities and Exchange Commission |

Shopko | Shopko Stores Inc. and its affiliates and subsidiaries, including Specialty Retail Shops Holding Corp. |

Shopko B-1 Term Loan | The secured loan made to Shopko in the initial principal amount of $35.0 million |

Shopko CMBS Loan Agreements | The combination of the non-recourse mortgage loan agreement, establishing an aggregate loan amount of $125.0 million, and the mezzanine loan agreement, establishing an aggregate loan amount of $40.0 million |

Shopko Lenders | An institutional lender and certain other lenders from time to time party to the Shopko CMBS Loan Agreements |

SMTA | Spirit MTA REIT |

Spin-Off | Creation of an independent, publicly traded REIT, SMTA, through the a pro rata distribution of one SMTA common share for every ten shares of Spirit common stock held by each of Spirit's stockholders as of May 18, 2018, the record date |

Spirit | Spirit Realty Capital, Inc. |

SubREIT | Spirit MTA SubREIT, Inc., a wholly-owned subsidiary of SMTA |

TRS | Taxable REIT Subsidiary, a corporation, other than a REIT, in which a REIT directly or indirectly holds stock or shares, and that has made a joint election with such REIT to be treated as a taxable REIT subsidiary |

U.S. | United States of America |

Vacant | Owned properties that are not economically yielding |

VFN | Variable funding notes |

Unless otherwise indicated or unless the context requires otherwise, all references to the "Company," "Spirit MTA REIT," “SMTA,” "we," "us" or "our" refer to Spirit MTA REIT and its wholly-owned subsidiaries.

INDEX

|

| | |

PART I | | |

Item 1. | Business | |

Item 1A. | Risk Factors | |

Item 1B. | Unresolved Staff Comments | |

Item 2. | Properties | |

Item 3. | Legal Proceedings | |

Item 4. | Mine Safety Disclosure | |

PART II | | |

Item 5. | Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities | |

Item 6. | Selected Financial Data | |

Item 7. | Management’s Discussion and Analysis of Financial Condition and Results of Operations | |

Item 7A. | Quantitative and Qualitative Disclosures About Market Risk | |

Item 8. | Financial Statements and Supplementary Data | |

PART III | | |

Item 9. | Changes in and Disagreements with Accountants on Accounting and Financial Disclosure | |

Item 9A. | Controls and Procedures | |

Item 9B. | Other Information | |

Item 10. | Trustees, Executive Officers and Corporate Governance | |

Item 11. | Executive Compensation | |

Item 12. | Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters | |

Item 13. | Certain Relationships and Related Transactions, and Trustee Independence | |

Item 14. | Principal Accountant Fees and Services | |

PART IV | | |

Item 15. | Exhibits, Financial Statement Schedules | |

SIGNATURES | | |

PART I

SPECIAL NOTE REGARDING FORWARD-LOOKING STATEMENTS

This Annual Report on Form 10-K contains forward-looking statements within the meaning of Section 27A of the Securities Act of 1933 (the “Securities Act”) and Section 21E of the Securities Exchange Act of 1934 (the “Exchange Act”). When used in this Annual Report on Form 10-K, the words “estimate,” “anticipate,” “expect,” “believe,” “intend,” “may,” “will,” “should,” “seek,” “approximately” or “plan,” or the negative of these words or similar words or phrases that are predictions of or indicate future events or trends and which do not relate solely to historical matters are intended to identify forward-looking statements. You can also identify forward-looking statements by discussions of strategy, plans or intentions of management.

Forward-looking statements involve numerous risks and uncertainties and you should not rely on them as predictions of future events. Forward-looking statements depend on assumptions, data or methods which may be incorrect or imprecise and we may not be able to realize them. We do not guarantee that the transactions and events described will happen as described (or that they will happen at all).

The following risks and uncertainties, among others, could cause actual results and future events to differ materially from those set forth or contemplated in the forward-looking statements:

| |

• | our success in pursuing and executing on strategic alternatives to maximize shareholder value; |

| |

• | industry and economic conditions; |

| |

• | the financial performance of our retail tenants and the demand for retail space, particularly with respect to challenges being experienced by general merchandise retailers; |

| |

• | the impact of any financial, accounting, legal or regulatory issues, bankruptcy or litigation that may affect us or our major tenants, in particular the bankruptcy petition of Shopko; |

| |

• | the nature and extent of future competition; |

| |

• | increases in our costs of borrowing as a result of changes in interest rates and other factors; |

| |

• | our ability to pay down, refinance, restructure and/or extend our indebtedness as it becomes due; |

| |

• | our ability and willingness to renew our leases upon expiration and to reposition our properties on the same or better terms upon expiration in the event such properties are not renewed by tenants or we exercise our rights to replace existing tenants upon default; |

| |

• | our ability to manage our operations; |

| |

• | our ability and willingness to maintain our qualification as a REIT; |

| |

• | our relationship with our Manager and its ability to retain qualified personnel; |

| |

• | potential conflicts of interest with our Manager or Spirit; |

| |

• | our ability to achieve the intended benefits from our Spin-Off from Spirit; and |

| |

• | other risks inherent in the real estate business, including tenant defaults, potential liability relating to environmental matters, illiquidity of real estate investments and potential damages from natural disasters. |

You are cautioned not to place undue reliance on forward-looking statements, which speak only as of the date of this Annual Report on Form 10-K. While forward-looking statements reflect our good faith beliefs, they are not guarantees of future performance. We disclaim any obligation to publicly update or revise any forward-looking statement to reflect changes in underlying assumptions or factors, new information, data or methods, future events or other changes, except as required by law.

Available Information

The Company's principal executive offices are located at 2727 North Harwood Street, Suite 300, Dallas, Texas 75201. Our telephone number at that location is 972-476-1409. We maintain a website at www.spiritmastertrust.com. On the Investor Relations page of our website, we post the following filings as soon as reasonably practicable after they are electronically filed with or furnished to the SEC: our Annual Report on Form 10-K, our Quarterly Reports on Form 10-Q, our Current Reports on Form 8-K, and the Section 16 filings of our directors and officers, as well as any amendments to those reports filed or furnished pursuant to Section 13(a) or 15(d) of the Exchange Act. All such filings on our Investor Relations page of our website are available to be viewed free of charge. Also available on our website, free of charge, are our corporate governance guidelines, the charters of the related party transaction, nominating and corporate

governance, audit and compensation committees of our Board of Trustees and our code of business conduct and ethics (which applies to all directors and our principal executive officer).

Information contained on or hyperlinked from our website is not incorporated by reference into and should not be considered part of this Annual Report on Form 10-K or our other filings with the SEC. Our common shares are listed on the NYSE under the symbol “SMTA.”

Item 1. Business

THE COMPANY

We operate as an externally managed REIT formed in Maryland that invests in and manages a portfolio of single-tenant, operationally essential real estate throughout the U.S. that is generally leased on a long-term, triple-net basis to tenants operating within retail, office, and industrial property types.

We began operations through predecessor legal entities which were wholly-owned subsidiaries of Spirit. On May 31, 2018, Spirit completed the Spin-Off that resulted in our establishment as an independent, publicly traded company. The Spin-Off was effected by means of a pro rata distribution of SMTA common shares to Spirit shareholders of record as of the close of business on the record date of May 18, 2018. In conjunction with the Spin-Off, we and our Manager, a wholly-owned subsidiary of Spirit, entered into an Asset Management Agreement under which our Manager provides external management of SMTA for a flat rate of $20 million per annum. As of December 31, 2018, we had no employees.

Our portfolio currently includes (i) Master Trust 2014, an asset-backed securitization trust which issues non-recourse asset-backed securities collateralized by commercial real estate, net-leases and mortgage loans, (ii) a portfolio of properties leased to Shopko encumbered with CMBS debt under the Shopko CMBS Loan Agreements, subject to the Shopko bankruptcy filing and subsequent foreclosure on the CMBS debt as discussed elsewhere in this Annual Report, (iii) a single distribution center property leased to a sporting goods tenant encumbered with CMBS debt, and (iv) a portfolio of 14 unencumbered properties. As of December 31, 2018, our gross investment in real estate and loans totaled approximately $2.56 billion, representing investments in 876 owned properties (788 excluding properties leased to Shopko) and eight properties securing our mortgage loans. See Item 2. "Properties" for further information on our properties and tenants.

RECENT DEVELOPMENTS

Shopko Bankruptcy Filing

On January 16, 2019, Shopko, our largest tenant, filed a petition for relief under chapter 11 of title 11 of the United States Code (the “Bankruptcy Code”). As of December 31, 2018, we received $42.1 million in annualized Contractual Rent from Shopko, which represented 17.9% of our total annualized Contractual Rent. As a consequence of the bankruptcy filing and the subsequent foreclosure by the Shopko Lenders on the majority of our Shopko assets, we do not expect to receive any additional cash flow going forward from any of the assets leased to Shopko, nor bear further meaningful expenses related to those assets. On March 18, 2019, Shopko announced that it would seek to liquidate its operations.

We also hold a secured loan previously made to Shopko with principal outstanding of $34.4 million as of December 31, 2018 (the "Shopko B-1 Term Loan"). While the outcome of the Shopko bankruptcy filing is uncertain and there can be no assurances that we will recover any amounts due to us under the Shopko B-1 Term Loan, we intend to pursue all of our rights and remedies in connection with the bankruptcy proceedings, with the goal of maximizing the receipt of amounts due to us under the Shopko B-1 Term loan.

Strategy Update

On January 16, 2019, in connection with Shopko filing for relief under Chapter 11 of the Bankruptcy Code, we announced that our Board of Trustees had elected to accelerate our strategic plan by initiating a process to explore strategic alternatives focused on maximizing shareholder value. Strategic alternatives to be considered may include, but are not limited to, a sale of the Company or the Master Trust 2014, a merger, the sale of the single distribution center property and other non-core assets, and the maximizing of recoveries in connection with the Shopko bankruptcy. We have not set a timetable for completion of the execution of any portion of this strategic plan, and there can be no assurance that the exploration of strategic alternatives will result in any transaction or other alternative.

Recent Financings

Shopko CMBS

On November 1, 2018, four indirectly wholly-owned, property-owning subsidiaries of the Company entered into a non-recourse mortgage loan agreement with an institutional lender and certain other lenders from time to time party thereto (the "Shopko Lenders"), in an aggregate amount of $165.0 million. The Company received net proceeds from this loan agreement of approximately $141.9 million after the payment of fees, expenses and required reserves. The loan was secured by a pledge of the equity in the four subsidiaries, which collectively hold 85 assets (83 owned properties and two seller-financed notes on properties) that are leased to Shopko. On November 27, 2018, SMTA, through the indirectly wholly-owned subsidiary that owns the four property-owning subsidiaries, entered into a non-recourse mezzanine loan agreement with the Shopko Lenders, pursuant to which $40.0 million of the original $165.0 million was carved out, resulting in no additional proceeds to SMTA (such mezzanine loan agreement, together with the original loan agreement, the “Shopko CMBS Loan Agreements”). The mezzanine loan was secured by an equity pledge of the indirect wholly-owned subsidiary that owns the four property-owning subsidiaries.

In connection with the Shopko CMBS Loan Agreements, SMTA entered into a customary non-recourse loan guaranty agreement, in favor of the Shopko Lenders, pursuant to which SMTA guaranteed the payment and performance of the liabilities of the property-owning subsidiaries under the non-recourse loan agreements for damages resulting from certain breaches or actions, including, but not limited to, fraud or intentional misrepresentation by the borrowers, and for the repayment in full of the debt in the event of certain actions, including, without limitation, certain bankruptcy events and prohibited transactions.

On January 16, 2019, our indirect wholly-owned subsidiaries as borrowers under the Shopko CMBS Loan Agreements defaulted on the loans when those entities ceased to make interest payments as a result of Shopko ceasing to pay its rent obligations following its bankruptcy filing. The full principal amount of $157.4 million outstanding under the Shopko CMBS Loan Agreements immediately became due and payable, and interest is accruing at the default rate of LIBOR plus 12.5% on the original loan portion and LIBOR plus 18.0% on the mezzanine loan portion. On March 1, 2019, the Shopko Lenders foreclosed on the equity of the entity that owns the four property-owning subsidiaries.

Variable Funding Notes

On November 1, 2018 (the “VFN Closing Date”), the Company completed the issuance of net-lease mortgage notes Series 2018-1, Class A (the “Variable Funding Notes” or "VFN"), which allow for the funding of up to $50.0 million of Variable Funding Notes within Master Trust 2014. Master Trust 2014 is comprised of five issuers, each an indirectly wholly-owned, bankruptcy remote subsidiary of the Company. The VFN has been rated “A+” by Standard & Poor’s Rating Services. The VFN was sold in reliance on certain exemptions from registration under the Securities Act. The VFN may only be acquired by qualified institutional buyers in reliance on Rule 144A under the Securities Act or pursuant to another exemption under the Securities Act. Prior to the VFN Closing Date, Master Trust 2014 had existing notes that are secured by the same collateral as the VFN, which had approximately $1.95 billion in aggregate outstanding principal as of the VFN Closing Date.

For further discussion of the Non-Recourse Loan, Mezzanine Loan and Variable Funding Notes, see Item 7. “Management’s Discussion and Analysis of Financial Condition and Results of Operations - Liquidity and Capital Resources.”

Real Estate Portfolio Activities

Concentration

During the year ended December 31, 2018, no tenant, excluding Shopko, exceeded 7.0% of our Contractual Rent and no one single property contributed more than 7.0% of our Contractual Rent. See Item 2. “Properties" for further information on our ten largest tenants and the composition of our tenant base.

Acquisitions and Dispositions

During the year ended December 31, 2018, we purchased nine properties, representing an aggregate gross investment of $112.6 million, and invested $2.6 million in revenue producing capital expenditures on existing properties. During the same period, we sold 47 properties for $91.0 million in gross sales proceeds. See Note 3 to our consolidated financial statements included in this Annual Report on Form 10-K for additional discussion of our investments.

Declaration of Quarterly and Special Dividend

On December 5, 2019, we announced that our Board of Trustees declared a quarterly cash dividend of $0.33 per common share for the fourth quarter of 2018. In addition, the Board of Trustees declared a special cash dividend of $1.00 per common share. Both dividends were paid on January 15, 2019 to shareholders of record as of December 31, 2018.

On March 5, 2019, the Board of Trustees declared a special cash dividend of $0.33 per common share for the first quarter ended March 31, 2019. The dividend will be paid on April 15, 2019 to holders of record as of March 29, 2019.

LEASING

We typically enter into master leases, leases with contractual rent escalators and leases that require ongoing tenant financial reporting. Most of our leases contain rent escalators, or provisions that periodically increase the base rent payable by the tenant under the lease. Although 34.7% of our rent escalators increase rent at a fixed amount on fixed dates, as of December 31, 2018, approximately 59.6% (41.5% excluding Shopko) (excluding leases on multi-tenant properties) of our rent escalators increase rent by a multiple of any increases in the CPI or the lesser of (a) a multiple of any increase in the CPI over a specified period or (b) a fixed percentage.

Many of our tenants are required to provide financial information, which includes balance sheet, income statement and cash flow statement data, on a quarterly and/or annual basis, and, as of December 31, 2018, approximately 76.2% (58.3% excluding Shopko) of our lease investment portfolio requires the tenant to provide property-level performance information, which includes income statement data on a quarterly and/or annual basis. To assist in our determination of a tenant’s credit quality, we license a product from Moody’s Analytics that provides an EDF and a “shadow rating,” and we evaluate a lease’s property-level rent coverage ratio. An EDF is only an estimate of default probability based, in part, on assumptions incorporated into the product. A shadow rating does not constitute a published credit rating and lacks the extensive company participation that is typically involved when a rating agency publishes a rating; accordingly, a shadow rating may not be as indicative of creditworthiness as a rating published by Moody’s, S&P, or another nationally recognized statistical rating organization. Our calculations of EDFs, shadow ratings and rent coverage ratios are based on financial information provided to us by our tenants and prospective tenants without independent verification on our part, and we must assume the appropriateness of estimates and judgments that were made by the party preparing the financial information. See Item 2. “Properties."

OUR MANAGER

We and our Manager are parties to the Asset Management Agreement, pursuant to which our Manager provides a management team that is responsible for implementing our business strategy and performing certain services for us, subject to oversight by our Board of Trustees. We do not have any employees. Our officers and the other individuals who execute our business strategy are employees of our Manager or its affiliates. Our Manager’s duties, subject to the supervision of our Board of Trustees, include: (1) performing all of our day-to-day functions, (2) sourcing, analyzing and executing on investments and dispositions, (3) determining investment criteria, (4) performing liability management duties, including financing and hedging, and (5) performing financial and accounting management. For its services, our Manager is entitled to an annual management fee and incentive compensation, as well as a termination fee and a promoted interest under certain circumstances. This description of our Asset Management Agreement is qualified in its entirety by the text of the Asset Management Agreement, which has been included as an exhibit to this Annual Report.

COMPETITION

As a landlord, we compete in the multi-billion dollar commercial real estate market with numerous developers and owners of properties, many of which own properties similar to ours in the same markets in which our properties are located. In operating and managing our portfolio, we compete for tenants based on a number of factors, including location, rental rates and flexibility. Some of our competitors have greater economies of scale, have lower cost of capital, have access to more resources and have greater name recognition than we do. If our competitors offer space at rental rates below current market rates or below the rental rates we currently charge our tenants, we may lose our tenants or prospective tenants and we may be pressured to reduce our rental rates or to offer substantial rent abatements, tenant improvement allowances, early termination rights or below-market renewal options in order to retain tenants when our leases expire.

REGULATION

General

Our properties are subject to various covenants, laws, ordinances and regulations, including regulations relating to common areas and fire and safety requirements. We believe that each of our properties has the necessary permits and approvals.

Americans With Disabilities Act

Pursuant to the ADA, our properties are required to meet federal requirements related to access and use by persons with disabilities. Compliance with the ADA, as well as a number of additional federal, state and local laws and regulations, may require modifications to properties we currently own and any properties we purchase, or may restrict renovations of those properties. Noncompliance with these laws or regulations could result in the imposition of fines or an award of damages to private litigants, as well as the incurrence of the costs of making modifications to attain compliance, and future legislation could impose additional financial obligations or restrictions on our properties. Although our tenants are generally responsible for all maintenance and repair costs pursuant to triple-net leases, including compliance with the ADA and other similar laws or regulations, we could be held liable as the owner of the property for a failure of one of our tenants to comply with such laws or regulations.

Environmental Matters

Federal, state and local environmental laws and regulations regulate, and impose liability for, releases of hazardous or toxic substances into the environment. Under various of these laws and regulations, a current or previous owner, operator or tenant of real estate may be required to investigate and clean up hazardous or toxic substances, hazardous wastes or petroleum product releases or threats of releases at the property, and may be held liable to a government entity or to third parties for property damage and for investigation, clean-up and monitoring costs incurred by those parties in connection with actual or threatened contamination. These laws typically impose clean-up responsibility and liability without regard to fault, or whether or not the owner, operator or tenant knew of or caused the presence of the contamination. The liability under these laws may be joint and several for the full amount of the investigation, clean-up and monitoring costs incurred or to be incurred or actions to be undertaken, although a party held jointly and severally liable may seek contributions from other identified, solvent, responsible parties for their fair share toward these costs. These costs may be substantial, and can exceed the value of the property. The presence of contamination, or the failure to properly remediate contamination, on a property may adversely affect the ability of the owner, operator or tenant to sell or rent that property or to borrow using the property as collateral and may adversely impact our investment in that property.

Some of our properties contain, have contained, or are adjacent to or near other properties that have contained or currently contain storage tanks for the storage of petroleum products or other hazardous or toxic substances. Similarly, some of our properties are or were used for commercial or industrial purposes that involve or involved the use of petroleum products or other hazardous or toxic substances, or are adjacent to or near properties that have been or are used for similar commercial or industrial purposes. These operations create a potential for the release of petroleum products or other hazardous or toxic substances, and we could potentially be required to pay to clean up any contamination. In addition, strict environmental laws regulate a variety of activities that can occur on a property, including the storage of petroleum products or other hazardous or toxic substances, air emissions and water discharges. Such laws may impose fines or penalties for violations. As a result of the foregoing, we could be materially and adversely affected.

Environmental laws also govern the presence, maintenance and removal of ACM. Federal regulations require building owners and those exercising control over a building’s management to identify and warn, through signs and labels, of potential hazards posed by workplace exposure to installed ACM in their building. The regulations also have employee training, record keeping and due diligence requirements pertaining to ACM. Significant fines can be assessed for violation of these regulations. As a result of these regulations, building owners and those exercising control over a building’s management may be subject to an increased risk of personal injury lawsuits by workers and others exposed to ACM. The regulations may affect the value of a building containing ACM in which we have invested. Federal, state and local laws and regulations also govern the removal, encapsulation, disturbance, handling and/or disposal of ACM when those materials are in poor condition or in the event of construction, remodeling, renovation or demolition of a building. These laws may impose liability for improper handling or a release into the environment of ACM and may provide for fines to owners or operators of real properties. In addition, owners or operators of real properties can be exposed to third-party liability for personal injury or improper work exposure associated with ACM.

When excessive moisture accumulates in buildings or on building materials, mold growth may occur, particularly if the moisture problem remains undiscovered or is not addressed over a period of time. Some molds may produce airborne toxins or irritants. Indoor air quality issues can also stem from inadequate ventilation, chemical contamination from indoor or outdoor sources, and other biological contaminants such as pollen, viruses and bacteria. Indoor exposure to airborne toxins or irritants above certain levels can be alleged to cause a variety of adverse health effects and symptoms, including allergic or other reactions. As a result, the presence of significant mold or other airborne contaminants at any of our properties could require us to undertake a costly remediation program to contain or remove the mold or other airborne contaminants from the affected property or increase indoor ventilation. In addition, the presence of significant mold or other airborne contaminants could expose us to liability from our tenants, employees of our tenants or others if property damage or personal injury occurs. We are not presently aware of any material adverse indoor air quality issues at our properties that have not been previously addressed or remediated by us.

Before completing any property acquisition, we obtain environmental assessments in order to identify potential environmental concerns at the property. These assessments are carried out in accordance with the Standard Practice for Environmental Site Assessments (ASTM Practice E 1527-13) as set by ASTM International, formerly known as the American Society for Testing and Materials, and generally include a physical site inspection, a review of relevant federal, state and local environmental and health agency database records, one or more interviews with appropriate site-related personnel, review of the property’s chain of title and review of historical aerial photographs and other information on past uses of the property. These assessments are limited in scope; however, if recommended in the initial assessments, we may undertake additional assessments such as soil and/or groundwater sampling or other limited subsurface investigations and ACM or mold surveys to test for substances of concern. A prior owner or operator of a property or historic operations at our properties may have created a material environmental condition that is not known to us or the independent consultants preparing the site assessments. Material environmental conditions may have arisen after the review was completed or may arise in the future, and future laws, ordinances or regulations may impose material additional environmental liability. If environmental concerns are not satisfactorily resolved in any initial or additional assessments, we may obtain environment insurance policies to insure against potential environmental risk or loss depending on the type of property, the availability and cost of the insurance and various other factors we deem relevant (e.g., an environmental occurrence affects one of our properties where our lessee may not have the financial capability to honor its indemnification obligations to us).

Generally, our leases provide that the lessee will indemnify us for any loss or expense we incur as a result of the presence, use or release of hazardous materials on our property. However, our ultimate liability for environmental conditions may exceed the policy limits on any environmental insurance policies we obtain, if any. If we are unable to enforce the indemnification obligations of our lessees or if the amount of environmental insurance we carry is inadequate, our results of operations would be adversely affected.

INSURANCE

Our tenants are generally required to maintain liability and property insurance coverage for the properties they lease from us pursuant to triple-net leases. Under such leases, our tenants are generally required to name us (and any of our lenders that have a mortgage on the property leased by the tenant) as additional insureds on their liability policies and additional insured and/or loss payee (or mortgagee, in the case of our lenders) on their property policies. Tenants are required to maintain casualty coverage and most carry limits at 100% of replacement cost. Depending on the location of the property, losses of a catastrophic nature, such as those caused by earthquakes and floods, may be covered by insurance policies that are held by our tenant with limitations such as large deductibles or co-payments that a tenant may not be able to meet. In addition, losses of a catastrophic nature, such as those caused by wind/hail, hurricanes, terrorism or acts of war, may be uninsurable or not economically insurable. In the event there is damage to our properties that is not covered by insurance and such properties are subject to recourse indebtedness, we will continue to be liable for the indebtedness, even if these properties are irreparably damaged. See Item 1A. “Risk Factors - Risks Related to Our Business and Properties - Insurance on our properties may not adequately cover all losses, which could materially and adversely affect us.”

In addition to being generally named as additional insureds on our tenants’ liability policies, we separately maintain commercial general liability coverage with limits of $1.0 million for each occurrence and $2.0 million general aggregate. We also maintain primary property coverage on (i) all unleased properties, (ii) all properties for which such coverage is not required to be carried by a tenant and (iii) all properties for which we obtain such coverage but the costs of which are reimbursed by tenants. In addition, we maintain excess property coverage on all remaining properties and other property coverage as may be required by our lenders.

Item 1A. Risk Factors

You should consider carefully the risks and uncertainties described below, together with all of the other information in this Annual Report on Form 10-K, which could materially affect our business, financial condition, results of operations and prospects. The risks described below are not the only risks facing us. Risks and uncertainties not currently known to us or that we currently deem to be immaterial also may materially affect our business, financial condition, results of operations and prospects.

RISKS RELATED TO OUR BUSINESS AND PROPERTIES

We are exploring and evaluating strategic alternatives and there can be no assurance that we will be successful in identifying or completing any strategic alternative or that any such strategic alternative will yield additional value for our shareholders.

On January 16, 2019, our Board of Trustees announced the intention to explore strategic alternatives focused on maximizing shareholder value. Strategic alternatives being considered by the Board of Trustees may include, but are not limited to, a sale of SMTA or the Master Trust 2014, a merger or other potential alternatives transactions. There can be no assurance that the exploration of strategic alternatives will result in the identification or consummation of any transaction or transactions or that any resulting plans or transactions will yield additional value for shareholders. In addition, we may incur substantial expenses associated with identifying and evaluating potential strategic alternatives. The process of exploring strategic alternatives may be time consuming and disruptive. Any potential transaction would be dependent upon a number of factors that may be beyond our control, including, among other factors, market conditions, industry trends, regulatory limitations and the interest of third parties in our business.

The bankruptcy or insolvency of Shopko is likely to result in the termination of Shopko leases and material losses to us.

On January 16, 2019, Shopko filed a petition for relief under chapter 11 of the Bankruptcy Code, and subsequently announced on March 18, 2019 that it intends to liquidate its operations. Rental revenues generated from Shopko represented 17.9% of our Contractual Rent at December 31, 2018. As a consequence of the Shopko bankruptcy filing, we do not expect to receive any additional cash flow going forward from any of the assets leased to Shopko. The loss of Shopko as a tenant will reduce our contractual rent in future periods, which is likely to have a material adverse effect on our business, financial condition and results of operations.

We also made the Shopko B-1 Term Loan to Shopko, with principal outstanding of $34.4 million as of December 31, 2018. This secured loan has been accelerated due to the Shopko bankruptcy filing. The outcome of the Shopko bankruptcy is uncertain and there can be no assurances that there will be any recovery with respect to the Shopko B-1 Term Loan.

The bankruptcy or insolvency of any of our other tenants could result in the termination of such tenant’s lease and incremental material losses to us, in addition to those from the Shopko leases.

The occurrence of a bankruptcy or insolvency of any of our other tenants could diminish the income we receive from that tenant’s lease or leases. In particular, the retail industry is facing reductions in sales revenues and increased bankruptcies throughout the United States, and revenues generated from retail tenants other than Shopko represented 29.4% of our Contractual Rent at December 31, 2018. If a tenant becomes bankrupt or insolvent, federal law may prohibit us from evicting such tenant based solely upon such bankruptcy or insolvency. In addition, a bankrupt or insolvent tenant may be authorized to reject and terminate its lease or leases with us. Any claims against such bankrupt tenant for unpaid future rent would be subject to statutory limitations that would likely result in our receipt of rental revenues that are substantially less than the contractually specified rent we are owed under the lease or leases. In addition, any claim we have for unpaid past rent, if any, may not be paid in full. We may also be unable to re-lease a terminated or rejected space or to re-lease it on comparable or more favorable terms. Moreover, tenants who are considering filing for bankruptcy protection may request that we agree to amendments of their master leases to remove certain of the properties they lease from us under such master leases. We cannot guarantee that we will be able to sell or re-lease such properties or that lease termination fees, if any, received in exchange for such releases will be sufficient to make up for the rental revenues lost as a result of such lease amendments. As a result, future tenant bankruptcies may materially and adversely affect us.

Risks related to commercial real estate ownership could reduce the value of our properties.

Our core business is the ownership of real estate that is leased to retail, service and distribution companies on a triple-net basis. Accordingly, our performance is subject to risks inherent to the ownership of commercial real estate, including:

| |

• | inability to collect rent from tenants due to financial hardship, including bankruptcy; |

| |

• | changes in local real estate markets resulting in the lack of availability or demand for single-tenant retail space; |

| |

• | changes in consumer trends and preferences that reduce the demand for products/services of our tenants; |

| |

• | inability to lease or sell properties upon expiration or termination of existing leases; |

| |

• | environmental risks related to the presence of hazardous or toxic substances or materials on our properties; |

| |

• | subjectivity of real estate valuations and changes in such valuations over time; |

| |

• | illiquid nature of real estate compared to most other financial assets; |

| |

• | changes in laws and regulations, including those governing real estate usage and zoning; |

| |

• | changes in interest rates and the availability of financing; and |

| |

• | changes in the general economic and business climate. |

The occurrence of any of the risks described above may cause the value of our real estate to decline, which could materially and adversely affect our business, financial condition and results of operations.

Credit and capital market conditions may adversely affect our access to and/or the cost of capital.

Periods of volatility in the credit and capital markets negatively affect the amounts, sources and cost of capital available to us. We primarily use external financing to refinance indebtedness as it matures. If sufficient sources of external financing are not available to us on cost effective terms, we could be forced to limit our business activities and repayment of debt, such as selling assets. To the extent that we access capital at a higher cost (reflected in higher interest rates for debt financing or lower share price for equity financing), our earnings per share and cash flow could be adversely affected.

Our tenants may fail to successfully operate their businesses, which could adversely affect us.

The success of our investments is dependent on the financial stability of our tenants’ financial condition and leasing practices. Adverse economic conditions such as high unemployment levels, interest rates, tax rates and fuel and energy costs may have an impact on the results of operations and financial condition of our tenants and result in a decline in rent or an increased incidence of default under existing leases. Such adverse economic conditions may also reduce overall demand for rental space, which could adversely affect our ability to maintain our current tenants and attract new tenants.

At any given time, our tenants may experience a downturn in their business that may weaken the operating results and financial condition of individual properties or of their business as whole. As a result, a tenant may delay lease commencement, decline to extend a lease upon its expiration, fail to make rental payments when due, become insolvent or declare bankruptcy, as in the case of Shopko's recent bankruptcy filing. We depend on our tenants to operate the properties we own in a manner which generates revenues sufficient to allow them to meet their obligations to us, including their obligations to pay rent, maintain certain insurance coverage and pay real estate taxes and maintain the properties in a manner so as not to jeopardize their operating licenses or regulatory status. The ability of our tenants to fulfill their obligations under our leases may depend, in part, upon the overall profitability of their operations. Cash flow generated by certain tenant businesses may not be sufficient for a tenant to meet its obligations to us. Although our occupied properties are generally operationally essential to our tenants, meaning the property is essential to the tenant’s generation of sales and profits, this does not guarantee that a tenant’s operations at a particular property will be successful or that the tenant will be able to meet all of its obligations to us. Our tenants’ failure to successfully operate their businesses could materially and adversely affect us.

Single-tenant leases involve particular and significant risks related to tenant default.

Many properties in our portfolio are single-tenant triple-net leased properties throughout the U.S. The financial failure of, or default in payment by, a single tenant under its lease is likely to cause a significant reduction in, or elimination of, our rental revenue from that property and a reduction in the value of the property. We may also experience difficulty or a significant delay in re-leasing or selling such property. This risk is magnified in situations where we lease multiple properties to a single tenant under a master lease. The failure or default of a tenant under a master lease could reduce or eliminate rental revenue from multiple properties and reduce the value of such properties. Although the master

lease structure may be beneficial to us because it restricts the ability of tenants to individually remove underperforming properties from the portfolio of properties leased from us, there is no guarantee that a tenant will not default in its obligations to us or decline to renew its master lease upon expiration. The default of a tenant that leases multiple properties from us, as in the case of Shopko's recent bankruptcy filing, could materially and adversely affect us.

A substantial portion of our properties are leased to unrated tenants and the tools we use to measure the credit quality of such tenants may not be accurate.

A substantial portion of our properties are leased to unrated tenants whom we determine, through our internal underwriting and credit analysis, to be creditworthy. Many of our tenants are required to provide financial information, which includes balance sheet, income statement and cash flow statement data, on a quarterly and/or annual basis, and, as of December 31, 2018, approximately 76.2% (58.3% excluding Shopko) of our Contractual Rent was generated pursuant to leases that require the tenant to provide property-level performance information, which includes income statement data on a quarterly and/or annual basis. To assist in our determination of a tenant’s credit quality, we license a product from Moody’s Analytics that provides an EDF and a “shadow rating,” and we evaluate a lease’s property-level rent coverage ratio. An EDF is only an estimate of default probability based, in part, on assumptions incorporated into the product. A shadow rating does not constitute a published credit rating and lacks the extensive company participation that is typically involved when a rating agency publishes a rating; accordingly, a shadow rating may not be as indicative of creditworthiness as a rating published by Moody’s, S&P, or another nationally recognized statistical rating organization. Our calculations of EDFs, shadow ratings and rent coverage ratios are based on financial information provided to us by our tenants and prospective tenants without independent verification on our part, and we must assume the appropriateness of estimates and judgments that were made by the party preparing the financial information. If our measurement of credit quality proves to be inaccurate, we may be subject to defaults, and investors may view our cash flows as less stable.

Decrease in demand for retail and restaurant space may materially and adversely affect us.

As of December 31, 2018, leases representing approximately 47.3% (29.4% excluding Shopko) and 19.6% of our Contractual Rent were with tenants in the retail and restaurant industries, respectively, and we may enter into leases with additional retail and restaurant tenants in the future. Accordingly, a decrease in the demand for retail and/or restaurant spaces adversely impacts us. The market for retail and restaurant space has previously been, and could continue to be, adversely affected by the following factors: weakness in the national, regional and local economies; the adverse financial condition of some large retail and restaurant companies; the ongoing consolidation in the retail and restaurant industries; the excess amount of retail and restaurant space in a number of markets; and, in the case of the retail industry, increasing consumer purchases over the Internet. To the extent that these conditions continue, they are likely to negatively affect market rents for retail and restaurant space, which could materially and adversely affect our business, financial condition and results of operations.

High geographic concentration of our properties could magnify the effects of adverse economic or regulatory developments in such geographic areas on our operations and financial condition.

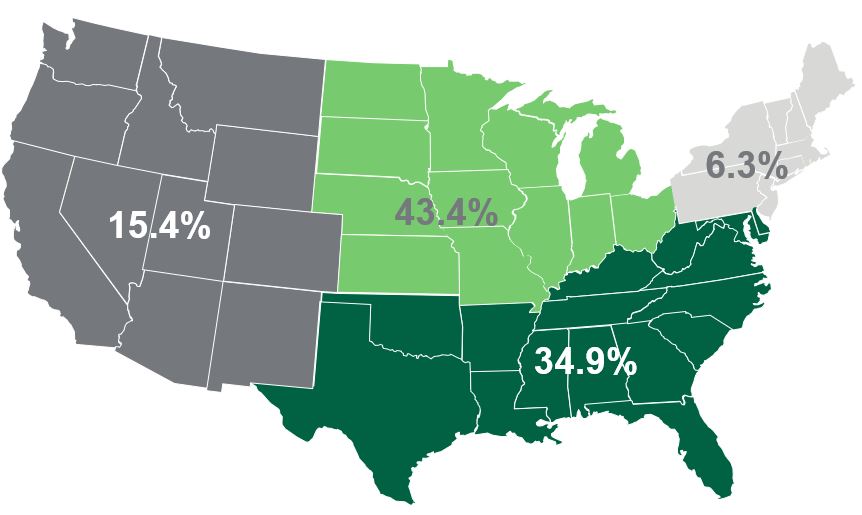

As of December 31, 2018, 11.7% of our portfolio (as a percentage of Contractual Rent) was located in Texas, representing the highest concentration of our assets. Geographic concentration exposes us to greater economic or regulatory risks than if we owned a more geographically diverse portfolio. We are susceptible to adverse developments in the economic or regulatory environments of the geographic areas in which we concentrate (or in which we may develop a substantial concentration of assets in the future), such as business layoffs or downsizing, industry slowdowns, relocations of businesses, increases in real estate and other taxes or costs of complying with governmental regulations.

We may be unable to renew leases, lease vacant space or re-lease space as leases expire on favorable terms or at all.

Our results of operations depend on our ability to strategically lease space in our properties (by renewing or re-leasing expiring leases and leasing vacant space), optimize our tenant mix or lease properties on more economically favorable terms. As of December 31, 2018, leases representing approximately 4.7% of our Contractual Revenue will expire during 2020. As of December 31, 2018, 25 of our properties, representing approximately 2.9% of our total number of owned properties, were Vacant. Current tenants may decline, or may not have the financial resources available, to renew current leases and we cannot guarantee that leases that are renewed will have terms that are as economically favorable to us as the expiring lease terms. If tenants do not renew the leases as they expire, we will have to find new tenants to lease our properties and there is no guarantee that we will be able to find new tenants or that our properties will be re-leased at rental rates equal to or above the current average rental rates or that substantial rent abatements, tenant improvement allowances, early termination rights, below-market renewal options or other lease incentive

payments will not be offered to attract new tenants. We may experience significant costs in connection with renewing, leasing or re-leasing a significant number of our properties, which could materially and adversely affect our results of operations.

Our ability to realize future rent increases will vary depending on changes in the CPI.

Most of our leases contain rent escalators, or provisions that periodically increase the base rent payable by the tenant under the lease. Although 34.7% of our rent escalators increase rent at a fixed amount on fixed dates, as of December 31, 2018, approximately 59.6% (41.5% excluding Shopko) (excluding leases on multi-tenant properties) of our rent escalators increase rent by a multiple of any increases in the CPI or the lesser of (a) a multiple of any increase in the CPI over a specified period or (b) a fixed percentage. If the product of any increase in the CPI multiplied by the applicable factor is less than the fixed percentage, the increased rent we are entitled to receive will be less than what we otherwise would have been entitled to receive if the rent escalator was based solely on a fixed percentage. Therefore, during periods of low inflation or deflation, small increases or decreases in the CPI will subject us to the risk of receiving lower rental revenue than we otherwise would have been entitled to receive if our rent escalators were based solely on fixed percentages or amounts. Conversely, if the product of any increase in the CPI multiplied by the applicable factor is more than the fixed percentage, the increased rent we are entitled to receive will be less than what we otherwise would have been entitled to receive if the rent escalator was based solely on an increase in CPI. Therefore, periods of high inflation will subject us to the risk of receiving lower rental revenue than we otherwise would have been entitled to receive if our rent escalators were based solely on CPI increases.

Property vacancies could result in significant capital expenditures and illiquidity.

The loss of a tenant, either through lease expiration or tenant bankruptcy or insolvency, may require us to spend significant amounts of capital to renovate the property before it is suitable for a new tenant. Many of the leases we enter into or acquire are for properties that are specially suited to the particular business of our tenants. Because these properties have been designed or physically modified for a particular tenant, if the current lease is terminated or not renewed, we may be required to renovate the property at substantial costs, decrease the rent we charge or provide other concessions in order to lease the property to another tenant. In the event we are required to sell these or other properties, we may have difficulty selling it then due to the special purpose for which the property may have been designed or modified. This potential illiquidity may limit our ability to quickly modify our portfolio in response to changes in economic or other conditions, including tenant demand. These limitations could have a material adverse effect on our business, financial condition and results of operations.

Operational risks may disrupt our businesses or result in losses.

We are completely dependent on our Manager’s financial, accounting, communications and other data processing systems. Such systems may fail to operate properly or become disabled as a result of tampering or a breach of the network security systems or otherwise. In addition, such systems are from time to time subject to cyberattacks. Breaches of our Manager’s network security systems could involve attacks that are intended to obtain unauthorized access to our proprietary information or personal identifying information of our shareholders, destroy data or disable, degrade or sabotage our systems, often through the introduction of computer viruses, cyberattacks and other means, and could originate from a wide variety of sources, including unknown third parties. There can be no assurance that measures to provide adequate protection to the integrity of our systems will be successful. If such systems are compromised, do not operate properly or are disabled, we could suffer financial loss, a disruption of our businesses, liability to investors, regulatory intervention or reputational damage. Finally, our Manager relies on third-party service providers for certain aspects of our business, including for certain information systems, technology and administration. Any interruption or deterioration in the performance of these third parties or failures of their information systems and technology could impair the quality of our operations and could affect our reputation and hence adversely affect our business.

Illiquidity of real estate investments could significantly impede our ability to pursue our ongoing business strategy to sell certain of our assets or respond to adverse changes in the performance of our properties and harm our financial condition.

The real estate investments we have made are relatively difficult to sell quickly. As a result, our ability to promptly sell one or more properties in our portfolio in response to changing economic, financial or investment conditions is limited. Return of capital and realization of gains, if any, from an investment generally will occur upon disposition or refinancing of the underlying property. We may be unable to realize our investment objective by sale, other disposition or refinancing at attractive prices within any given period of time or may otherwise be unable to complete any exit strategy. In particular, these risks could arise from weakness in or even the lack of an established market for a property, changes in the

financial condition or prospects of prospective purchasers, changes in national or international economic conditions and changes in laws, regulations or fiscal policies of the jurisdiction in which a property is located.

In addition, the Code imposes restrictions on a REIT’s ability to dispose of properties that are not applicable to other types of real estate companies. In particular, the tax laws applicable to REITs effectively require that we hold our properties for investment, rather than primarily for sale in the ordinary course of business, which may cause us to forego or defer sales of properties that otherwise would be in our best interest. Therefore, we may not be able to vary our portfolio in response to economic or other conditions promptly or on favorable terms, which may materially and adversely affect our business and results of operations.

We face significant competition for tenants, which may decrease or prevent increases of the occupancy and rental rates of our properties.

We compete with numerous developers, owners and operators of properties, many of which own properties similar to ours in the same markets in which our properties are located. In operating and managing our portfolio, we compete for tenants based on a number of factors, including location, rental rates and flexibility. Some of our competitors have greater economies of scale, have lower cost of capital, have access to more resources and have greater name recognition than we do. If our competitors offer space at rental rates below current market rates or below the rental rates we currently charge our tenants, we may lose existing or potential tenants and we may be pressured to reduce our rental rates or to offer more substantial rent abatements, tenant improvements, early termination rights, below-market renewal options or other lease incentive payments in order to retain tenants when our leases expire. Competition for tenants could decrease or prevent increases of the occupancy and rental rates of our properties, which could materially and adversely affect us.

The loss of a borrower or the failure of a borrower to make loan payments on a timely basis will reduce our revenues, which could lead to losses on our investments and reduced returns to our shareholders.

We have originated or acquired long-term, commercial mortgage and other loans. The success of our loan investments is dependent on the financial stability of our borrowers. The success of our borrowers is dependent on each of their individual businesses and their industries, which could be affected by economic conditions in general, changes in consumer trends and preferences and other factors over which neither they nor we have control. For example, in connection with Shopko’s bankruptcy filing, Shopko has filed pleadings asserting that any recovery under the Shopko B-1 Term Loan will be limited and may be impaired in full. We have therefore established a loss reserve in the amount of approximately $33.8 million, representing the remaining amount of the Shopko B-1 Term Loan as of the date hereof. A default on loans owed to us, including the loan made to Shopko, could prevent us from earning interest or receiving a return of the principal of our loan and, as a result, would materially and adversely affect us. In the event of a default, we may also experience delays in enforcing our rights as lender and may incur substantial costs in collecting the amounts owed to us and in liquidating any collateral.

Foreclosure and other similar proceedings used to enforce payment of real estate loans are generally subject to principles of equity, which are designed to relieve the indebted party from the legal effect of that party’s default. Foreclosure and other similar laws may limit our right to obtain a deficiency judgment against the defaulting party after a foreclosure or sale. The application of any of these principles may lead to a loss or delay in the payment on loans we hold, which in turn could reduce the amounts we have available to make distributions. Further, in the event we have to foreclose on a property, the amount we receive from the foreclosure sale of the property may be inadequate to fully pay the amounts owed to us by the borrower and our costs incurred to foreclose, repossess and sell the property which could materially and adversely affect us.

Our investments in mortgage loans may be affected by unfavorable real estate market conditions, including interest rate fluctuations, which could decrease the value of those loans.

Our investments in mortgage loans are subject to risk of default by the borrowers and to interest rate risks. To the extent we incur delays in liquidating defaulted mortgage loans, we may not be able to obtain all amounts due to us under such loans. Further, we will not know whether the values of the properties securing the mortgage loans will remain at the levels existing on the dates of origination of those mortgage loans or the dates of our investment in the loans. If the values of the underlying properties decline, the value of the collateral securing our mortgage loans will also decline and if we were to foreclose on any of the properties securing the mortgage loans, we may not be able to sell or lease them for an amount equal to the unpaid amounts due to us under the mortgage loans. As such, defaults on mortgage loans in which we invest may materially and adversely affect our investment strategy.

Inflation may materially and adversely affect us and our tenants.

Increased inflation could have a negative impact on variable-rate debt we currently have or that we may incur in the future. Our leases typically contain provisions designed to mitigate the adverse impact of inflation on our results of operations. Because tenants are typically required to pay all property operating expenses, increases in property-level expenses at our leased properties generally do not affect us. However, increased operating expenses at vacant properties and the limited number of properties that are not subject to full triple-net leases could cause us to incur additional operating expenses, which could increase our exposure to inflation. Additionally, the increases in rent provided by many of our leases may not keep up with the rate of inflation. Increased costs may also have an adverse impact on our tenants if increases in their operating expenses exceed increases in revenue, which may adversely affect the tenants’ ability to pay rent owed to us.

If we fail to maintain effective internal controls over financial reporting, we may not be able to accurately and timely report our financial results.

Section 404(a) of Sarbanes-Oxley Act of 2002 ("SOX") requires that, beginning with our annual report for the fiscal year ending December 31, 2020, our management is required to assess and report annually on the effectiveness of our internal controls over financial reporting and identify any material weaknesses in internal controls over financial reporting. However, for so long as we are an “emerging growth company”, our independent registered public accounting firm will not be required to issue an annual report that addresses the effectiveness of our internal controls over financial reporting.

Effective internal controls over financial reporting are necessary for us to provide reliable financial reports, effectively prevent fraud and operate successfully as a public company. If we cannot provide reliable financial reports or prevent fraud, our reputation and operating results would be harmed. We are required to perform system and process evaluation and testing of our internal control over financial reporting to allow management to report on, and our independent registered public accounting firm to attest to, the effectiveness of our internal control over financial reporting, as required by Section 404 of the Sarbanes-Oxley Act of SOX.

Any failure to maintain effective internal controls or timely effect any necessary improvement of our internal control over financial reporting controls could harm operating results or cause us to fail to meet our reporting obligations, which could affect the listing of our common shares on the NYSE. Ineffective internal control over financial reporting could also cause investors to lose confidence in our reported financial information, which would likely have a negative effect on the trading price of our common shares.

The requirements of being a public company may strain our resources.

We are subject to the reporting requirements of the Exchange Act, SOX, the listing requirements of the NYSE, and other applicable securities rules and regulations. Compliance with these rules and regulations requires substantial legal and financial compliance costs, makes some activities more difficult, time-consuming, or costly, and places increased demand on our systems and resources. The Exchange Act requires, among other things, that we file annual and current reports with respect to our business and operating results. SOX requires, among other things, that we maintain effective disclosure controls and procedures and internal control over financial reporting. In order to maintain disclosure controls and procedures and internal control over financial reporting that meet this standard, significant resources and oversight are required.

In addition, changing laws, regulations, and standards relating to corporate governance and public disclosure are creating uncertainty for public companies, increasing legal and financial compliance costs and making some activities more time consuming. These laws, regulations, and standards are subject to varying interpretations, in many cases due to their lack of specificity, and, as a result, their application in practice may evolve over time as new guidance is provided by regulatory and governing bodies. This could result in continuing uncertainty regarding compliance matters and higher costs necessitated by ongoing revisions to disclosure and governance practices. We intend to continue to invest resources to complying with evolving laws, regulations, and standards, and this investment may result in increased general and administrative expenses. If our efforts to comply with new laws, regulations, and standards differ from the activities intended by regulatory or governing bodies due to ambiguities related to practice, regulatory authorities may initiate legal proceedings against us and our business may be harmed.

We depend on external sources of capital that are outside of our control and may not be available to us on commercially reasonable terms or at all.

In order to maintain our qualification as a REIT, we are required under the Code to distribute annually at least 90% of our REIT taxable income, determined without regard to the dividends paid deduction and excluding any net capital gain. In addition, we will be subject to income tax at regular corporate rates to the extent that we distribute less than 100% of our REIT taxable income, determined without regard to the dividends paid deduction and including any net capital gain. Because of these distribution requirements, we may not be able to fund future capital needs from operating cash flow. Consequently, we may rely on third-party sources to fund our capital needs. We may not be able to obtain the financing on favorable terms or at all. Any additional debt we incur will increase our leverage and likelihood of default. Our access to third-party sources of capital depends, in part, on:

| |

• | general market conditions; |

| |

• | our current debt levels; |

| |

• | our current and expected future earnings; |

| |

• | our cash flow and cash distributions; and |

| |

• | the market price of our common shares. |

If we cannot obtain capital from third-party sources, we may not be able to meet the capital and operating needs of our existing properties, satisfy our debt service obligations or make the cash distributions to our shareholders necessary to maintain our qualification as a REIT.

Historically, we have raised a significant amount of capital through debt issuances of our Master Trust 2014. We have generally used the proceeds from this program to repay other debt and fund real estate acquisitions. As of December 31, 2018, we had issued notes under our Master Trust 2014 in seven different series over five separate issuances with $1.94 billion aggregate principal amount outstanding. Additionally, under our Master Trust 2014, we had availability of $41.1 million borrowing capacity under our variable funding note as of December 31, 2018 ($45.8 million as of March 19, 2019). The Master Trust 2014 notes have a weighted average maturity of 4.4 years as of December 31, 2018. Our obligations under this program are generally secured by liens on certain of our properties. Subject to certain conditions, we may substitute real estate collateral within our securitization trust from time to time. Moreover, we view our ability to substitute collateral under our Master Trust 2014 favorably, and no assurance can be given that financing facilities offering similar flexibility will be available to us in the future.

Dispositions of real estate assets could change the holding period assumption in our valuation analyses, which could result in material impairment losses and adversely affect our financial results.