.3

.3

| P | Includes Accounting Policies |

| E | Includes Accounting Estimates and Judgments |

Management’s Responsibility

Management’s Responsibility for Financial Reporting

|

|

| |

| Chuck Magro President and Chief Executive Officer February 20, 2019 |

Pedro Farah Chief Financial Officer February 20, 2019 |

| NUTRIEN 2018 | 90 | ANNUAL REPORT |

FINANCIAL STATEMENTS AND NOTES

Report of Independent

Registered Public Accounting Firm – 2018

To the Shareholders and the Board of Directors of Nutrien Ltd.

| NUTRIEN 2018 | 91 | ANNUAL REPORT |

Report of Independent

Registered Public Accounting Firm – 2018

To the Shareholders and the Board of Directors of Nutrien Ltd.

| NUTRIEN 2018 | 92 | ANNUAL REPORT |

FINANCIAL STATEMENTS AND NOTES

Report of Independent

Registered Public Accounting Firm – 2017

To the Shareholders and the Board of Directors of Potash Corporation of Saskatchewan Inc.

| NUTRIEN 2018 | 93 | ANNUAL REPORT |

IN MILLIONS OF US DOLLARS EXCEPT AS OTHERWISE NOTED

Consolidated Financial Statements

Consolidated Statements of Earnings

| For the years ended December 31 | 2018 | 2017 | ||||||||||||

| (Note 33) | ||||||||||||||

| SALES |

Note 4 | $ | 19,636 | $ | 4,547 | |||||||||

| Freight, transportation and distribution |

Note 5 | (864 | ) | (537 | ) | |||||||||

| Cost of goods sold |

Note 5 | (13,380 | ) | (3,316 | ) | |||||||||

| GROSS MARGIN |

5,392 | 694 | ||||||||||||

| Selling expenses |

Note 5 | (2,337 | ) | (29 | ) | |||||||||

| General and administrative expenses |

Note 5 | (539 | ) | (185 | ) | |||||||||

| Provincial mining and other taxes |

Note 6 | (250 | ) | (146 | ) | |||||||||

| Impairment of property, plant and equipment |

Note 16 | (1,809 | ) | – | ||||||||||

| Other expenses |

Note 7 | (43 | ) | (125 | ) | |||||||||

| EARNINGS BEFORE FINANCE COSTS AND INCOME TAXES |

414 | 209 | ||||||||||||

| Finance costs |

Note 8 | (538 | ) | (238 | ) | |||||||||

| LOSS BEFORE INCOME TAXES |

(124 | ) | (29 | ) | ||||||||||

| Income tax recovery |

Note 9 | 93 | 183 | |||||||||||

| NET (LOSS) EARNINGS FROM CONTINUING OPERATIONS |

(31 | ) | 154 | |||||||||||

| Net earnings from discontinued operations |

Note 10 | 3,604 | 173 | |||||||||||

| NET EARNINGS |

$ | 3,573 | $ | 327 | ||||||||||

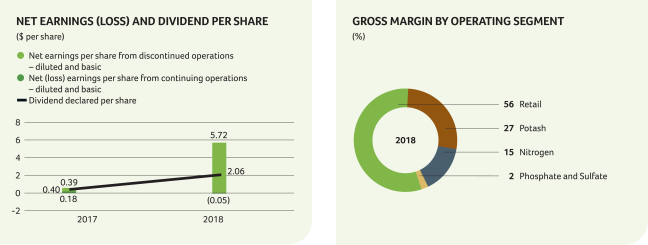

| NET (LOSS) EARNINGS PER SHARE FROM CONTINUING OPERATIONS |

Note 11 | |||||||||||||

| Basic |

$ | (0.05 | ) | $ | 0.18 | |||||||||

| Diluted |

$ | (0.05 | ) | $ | 0.18 | |||||||||

| NET EARNINGS PER SHARE FROM DISCONTINUED OPERATIONS |

Note 11 | |||||||||||||

| Basic |

$ | 5.77 | $ | 0.21 | ||||||||||

| Diluted |

$ | 5.77 | $ | 0.21 | ||||||||||

| NET EARNINGS PER SHARE FROM CONTINUING AND DISCONTINUED OPERATIONS |

Note 11 | |||||||||||||

| Basic |

$ | 5.72 | $ | 0.39 | ||||||||||

| Diluted |

$ | 5.72 | $ | 0.39 | ||||||||||

| Weighted average shares outstanding for basic earnings per share (“EPS”) |

Note 11 | 624,900,000 | 840,079,000 | |||||||||||

| Weighted average shares outstanding for diluted EPS |

Note 11 | 624,900,000 | 840,316,000 | |||||||||||

(See Notes to the Consolidated Financial Statements)

2018 HIGHLIGHTS

| • | Merger of Potash Corporation of Saskatchewan Inc. (“PotashCorp”) and Agrium Inc. (“Agrium”) occurred on January 1, 2018. As a result, the 2017 figures throughout are the financial results of PotashCorp only, the accounting acquirer. |

| NUTRIEN 2018 | 94 | ANNUAL REPORT |

FINANCIAL STATEMENTS AND NOTES

IN MILLIONS OF US DOLLARS EXCEPT AS OTHERWISE NOTED

Consolidated Statements of Comprehensive Income

| For the years ended December 31 (net of related income taxes) | 2018 | 2017 | ||||||||||||||

| (Note 33) | ||||||||||||||||

| NET EARNINGS |

$ | 3,573 | $ | 327 | ||||||||||||

| Other comprehensive (loss) income |

||||||||||||||||

| Items that will not be reclassified to net earnings: |

||||||||||||||||

| Net actuarial gain on defined benefit plans |

54 | 46 | ||||||||||||||

| Net fair value (loss) gain on investments 1 |

(99 | ) | 30 | |||||||||||||

| Items that have been or may be subsequently reclassified to net earnings: |

||||||||||||||||

| Loss on currency translation of foreign operations |

(249 | ) | – | |||||||||||||

| Other |

(8 | ) | 20 | |||||||||||||

| OTHER COMPREHENSIVE (LOSS) INCOME |

(302 | ) | 96 | |||||||||||||

| COMPREHENSIVE INCOME |

$ | 3,271 | $ | 423 | ||||||||||||

| 1 | As at December 31, 2018 and 2017, financial instruments measured at fair value through other comprehensive income (“FVTOCI”) are comprised of shares in Sinofert Holdings Limited (“Sinofert”) and other. The Company’s investment in Israel Chemicals Ltd. (“ICL”) was classified as held for sale at December 31, 2017 and the divestiture of all equity interests in ICL was completed on January 24, 2018. |

(See Notes to the Consolidated Financial Statements)

| NUTRIEN 2018 | 95 | ANNUAL REPORT |

IN MILLIONS OF US DOLLARS EXCEPT AS OTHERWISE NOTED

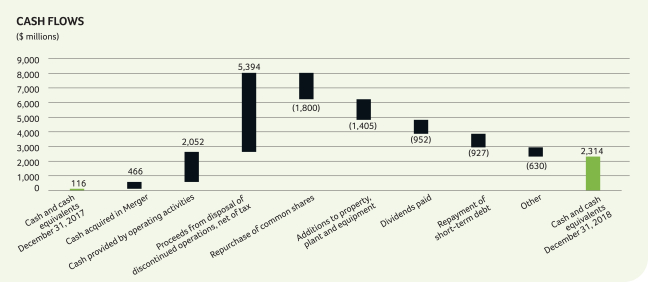

Consolidated Statements of Cash Flows

| For the years ended December 31 | 2018 | 2017 | ||||||||||||||||

| OPERATING ACTIVITIES |

||||||||||||||||||

| Net earnings |

$ | 3,573 | $ | 327 | ||||||||||||||

| Adjustments to reconcile net earnings to cash provided by operating activities |

Note 12 | (383 | ) | 826 | ||||||||||||||

| Changes in non-cash operating working capital |

Note 12 | (1,138 | ) | 72 | ||||||||||||||

| CASH PROVIDED BY OPERATING ACTIVITIES |

2,052 | 1,225 | ||||||||||||||||

| INVESTING ACTIVITIES |

||||||||||||||||||

| Cash acquired in Merger |

Note 3 | 466 | – | |||||||||||||||

| Business acquisitions, net of cash acquired |

Note 3 | (433 | ) | – | ||||||||||||||

| Additions to property, plant and equipment |

Note 16 | (1,405 | ) | (651 | ) | |||||||||||||

| Proceeds from disposal of discontinued operations, net of tax |

Note 10 | 5,394 | – | |||||||||||||||

| Purchase of investments |

(135 | ) | – | |||||||||||||||

| Other |

– | (1 | ) | |||||||||||||||

| CASH PROVIDED BY (USED IN) INVESTING ACTIVITIES |

3,887 | (652 | ) | |||||||||||||||

| FINANCING ACTIVITIES |

||||||||||||||||||

| Finance costs on long-term debt |

(21 | ) | (1 | ) | ||||||||||||||

| (Repayment of) proceeds from short-term debt |

Note 22 | (927 | ) | 341 | ||||||||||||||

| Repayment of long-term debt |

Note 23 | (12 | ) | (500 | ) | |||||||||||||

| Dividends paid |

Note 24 | (952 | ) | (330 | ) | |||||||||||||

| Repurchase of common shares |

Note 24 | (1,800 | ) | – | ||||||||||||||

| Issuance of common shares |

Note 24 | 7 | 1 | |||||||||||||||

| CASH USED IN FINANCING ACTIVITIES |

(3,705 | ) | (489 | ) | ||||||||||||||

| EFFECT OF EXCHANGE RATE CHANGES ON CASH AND CASH EQUIVALENTS |

(36 | ) | – | |||||||||||||||

| INCREASE IN CASH AND CASH EQUIVALENTS |

2,198 | 84 | ||||||||||||||||

| CASH AND CASH EQUIVALENTS, BEGINNING OF YEAR |

116 | 32 | ||||||||||||||||

| CASH AND CASH EQUIVALENTS, END OF YEAR |

$ | 2,314 | $ | 116 | ||||||||||||||

| Cash and cash equivalents comprised of: |

||||||||||||||||||

| Cash |

$ | 1,506 | $ | 14 | ||||||||||||||

| Short-term investments |

808 | 102 | ||||||||||||||||

| $ | 2,314 | $ | 116 | |||||||||||||||

(See Notes to the Consolidated Financial Statements)

2018 HIGHLIGHTS

The graph below represents the significant changes in Nutrien’s cash flows in 2018.

| NUTRIEN 2018 | 96 | ANNUAL REPORT |

FINANCIAL STATEMENTS AND NOTES

IN MILLIONS OF US DOLLARS EXCEPT AS OTHERWISE NOTED

Consolidated Statements of Changes

in Shareholders’ Equity

| Accumulated Other Comprehensive (Loss) Income (“AOCI”) | ||||||||||||||||||||||||||||||||||||

| Share Capital |

Contributed Surplus |

Net Fair Loss on |

Net Actuarial Gain on Defined Benefit Plans 3 |

Loss on Currency Translation of Foreign Operations |

Other | Total AOCI |

Retained Earnings |

Total Equity 4 |

||||||||||||||||||||||||||||

| (Note 33) | (Note 33) | |||||||||||||||||||||||||||||||||||

| BALANCE – DECEMBER 31, 2016 |

$ | 1,798 | $ | 222 | $ | 43 | $ | – | $ | (2 | ) | $ (66 | ) | $ | (25 | ) | $ | 6,204 | $ | 8,199 | ||||||||||||||||

| Net earnings |

– | – | – | – | – | – | – | 327 | 327 | |||||||||||||||||||||||||||

| Other comprehensive income |

– | – | 30 | 46 | – | 20 | 96 | – | 96 | |||||||||||||||||||||||||||

| Dividends declared |

– | – | – | – | – | – | – | (335 | ) | (335 | ) | |||||||||||||||||||||||||

| Effect of share-based compensation including issuance of common shares |

2 | 8 | – | – | – | – | – | – | 10 | |||||||||||||||||||||||||||

| Shares issued for dividend reinvestment plan |

6 | – | – | – | – | – | – | – | 6 | |||||||||||||||||||||||||||

| Transfer of net actuarial gain on defined benefit plans |

– | – | – | (46 | ) | – | – | (46 | ) | 46 | – | |||||||||||||||||||||||||

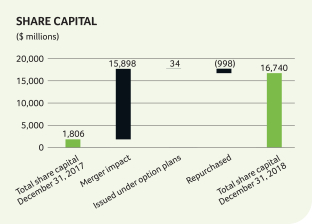

| BALANCE – DECEMBER 31, 2017 |

$ | 1,806 | $ | 230 | $ | 73 | $ | – | $ | (2 | ) | $ | (46 | ) | $ | 25 | $ | 6,242 | $ | 8,303 | ||||||||||||||||

| Merger impact (Notes 3 and 11) |

15,898 | 7 | – | – | – | – | – | (1 | ) | 15,904 | ||||||||||||||||||||||||||

| Net earnings |

– | – | – | – | – | – | – | 3,573 | 3,573 | |||||||||||||||||||||||||||

| Other comprehensive (loss) income |

– | – | (99 | ) | 54 | (249 | ) | (8 | ) | (302 | ) | – | (302 | ) | ||||||||||||||||||||||

| Shares repurchased (Note 24) |

(998 | ) | (23 | ) | – | – | – | – | – | (831 | ) | (1,852 | ) | |||||||||||||||||||||||

| Dividends declared |

– | – | – | – | – | – | – | (1,273 | ) | (1,273 | ) | |||||||||||||||||||||||||

| Effect of share-based compensation including issuance of common shares |

34 | 17 | – | – | – | – | – | – | 51 | |||||||||||||||||||||||||||

| Transfer of net actuarial gain on defined benefit plans |

– | – | – | (54 | ) | – | – | (54 | ) | 54 | – | |||||||||||||||||||||||||

| Transfer of net loss on sale of investment |

– | – | 19 | – | – | – | 19 | (19 | ) | – | ||||||||||||||||||||||||||

| Transfer of net loss on cash flow hedges |

– | – | – | – | – | 21 | 21 | – | 21 | |||||||||||||||||||||||||||

| BALANCE – DECEMBER 31, 2018 |

$ | 16,740 | $ | 231 | $ | (7 | ) | $ | – | $ (251 | ) | $ | (33 | ) | $ | (291 | ) | $ | 7,745 | $ | 24,425 | |||||||||||||||

| 1 | The Company adopted IFRS 9 “Financial Instruments” in 2018 and reclassified available-for-sale investments as financial instruments measured at FVTOCI. |

| 2 | The Company divested its equity interests in the investment in ICL on January 24, 2018. The loss on sale of ICL of $(19) was transferred to retained earnings in 2018. The cumulative net unrealized gain at December 31, 2017 was $4. |

| 3 | Any amounts incurred during a period were closed out to retained earnings at each period-end. Therefore, no balance exists at the beginning or end of period. |

| 4 | All equity transactions were attributable to common shareholders. |

(See Notes to the Consolidated Financial Statements)

| NUTRIEN 2018 | 97 | ANNUAL REPORT |

FINANCIAL STATEMENTS AND NOTES

IN MILLIONS OF US DOLLARS EXCEPT AS OTHERWISE NOTED

|

|

DESCRIPTION OF BUSINESS

|

Nutrien Ltd. is an integrated ag solutions provider and plays a critical role in helping growers around the globe increase food production in a sustainable manner. The Company’s Retail segment supplies key products and services directly to growers – including crop nutrients, crop protection and seed, as well as agronomic and application services. The Company produces the three essential nutrients – potash, nitrogen and phosphate – required to help farmers grow healthier, more abundant crops.

| NUTRIEN 2018 | 99 | ANNUAL REPORT |

IN MILLIONS OF US DOLLARS EXCEPT AS OTHERWISE NOTED

|

|

BASIS OF PRESENTATION

|

|

|

BUSINESS COMBINATIONS

|

The Company’s business combinations include the Merger between PotashCorp and Agrium and the acquisition of Retail businesses, including farm centers in North America and Australia, digital agriculture, proprietary products and agricultural services. Assets acquired and liabilities assumed are measured at fair value.

| Accounting Policies | Accounting Estimates and Judgments | |||

| • The acquisition method is followed.

• Consideration is measured at the aggregate of the fair values of assets transferred, liabilities incurred or assumed, and equity instruments issued in exchange for control of the acquiree at the acquisition date.

• The acquisition date is the date the Company obtains control over the acquiree.

• Identifiable assets acquired and liabilities assumed are generally measured at fair value.

• Acquisition-related costs are recognized in net earnings as incurred.

• The excess of total consideration for each acquisition plus non-controlling interest in the acquiree, over the fair value of the identifiable net assets acquired, is recorded as goodwill. |

• Purchase price allocation involves judgment in identifying assets acquired and liabilities assumed and estimation of their fair values.

• Judgment is required to determine which entity is the acquirer in a merger of equals. In identifying PotashCorp as the acquirer, the companies considered the voting rights of all equity instruments, the intended corporate governance structure of the combined company, the intended composition of senior management of the combined company and the size of each of the companies. In assessing the size of each of the companies, the companies evaluated various metrics. No single factor was the sole determinant in the overall conclusion that PotashCorp is the acquirer for accounting purposes; rather, all factors were considered in arriving at the conclusion. |

| NUTRIEN 2018 | 100 | ANNUAL REPORT |

FINANCIAL STATEMENTS AND NOTES

IN MILLIONS OF US DOLLARS EXCEPT AS OTHERWISE NOTED

NOTE 3 BUSINESS COMBINATIONS CONTINUED

| NUTRIEN 2018 | 101 | ANNUAL REPORT |

IN MILLIONS OF US DOLLARS EXCEPT AS OTHERWISE NOTED

NOTE 3 BUSINESS COMBINATIONS CONTINUED

| NUTRIEN 2018 | 102 | ANNUAL REPORT |

FINANCIAL STATEMENTS AND NOTES

IN MILLIONS OF US DOLLARS EXCEPT AS OTHERWISE NOTED

|

|

SEGMENT INFORMATION

|

The Company has four reportable operating segments: Retail, Potash, Nitrogen, and Phosphate and Sulfate. The Retail segment distributes crop nutrients, crop protection products, seed and merchandise, and provides services directly to growers through a network of farm centers in North and South America and Australia. The Potash, Nitrogen, and Phosphate and Sulfate segments are differentiated by the chemical nutrient contained in the products that each produces.

| Accounting Policies | Accounting Estimates and Judgments | |||

| Operating Segments Prior to the Merger, the Company identified the Chief Executive Officer as the Chief Operating Decision Maker (“CODM”) under IFRS and used gross margin to measure the segments’ profit or loss. The operating segments were limited to the following: Potash, Nitrogen and Phosphate. The changes in the structure of the Company’s internal organization as a result of the Merger caused the composition of the operating segments to change as well as who the Company identified to be the CODM.

Post-Merger, the Company identified the Executive Leadership Team (“ELT”), comprised of officers at the Executive Vice President level and above, as the CODM. The CODM uses net (loss) earnings before finance costs, income taxes, and depreciation and amortization (“EBITDA”) to measure performance and allocate resources to the operating segments. The CODM believes EBITDA to be an important measure as it excludes the effects of items that primarily reflect the impact of long-term investment and financing decisions, rather than the performance of the Company’s day-to-day operations.

In 2019, the Company’s CODM reassessed product groupings and decided to evaluate the performance of sulfate products as part of the Nitrogen segment, rather than the Phosphate and Sulfate segment; therefore, future comparative figures will be restated for the change in the composition of the segments, which will result in an increase in the Nitrogen segment and a decrease in the Phosphate and Sulfate segment. For the year ended December 31, 2018, this change will be approximately $121, $42, and $69 in sales, gross margin and EBITDA, respectively. |

Operating Segments Judgment is used in determining the composition of the reportable segments based on factors including risks and returns, internal organization, and internal reports reviewed by the CODM.

Certain expenses are allocated across segments based on an appropriate basis such as production capacities or historical trends. |

| Revenue The Company recognizes revenue when it transfers control over a good or service to a customer.

|

Revenue For product sales which contain volume rebates, revenue is recognized to the extent that it is highly probable that significant reversals will not occur using the most likely method and accumulated experience.

Returns and incentives are estimated based on historical and forecasted data, contractual terms and current conditions. Due to the nature of goods and services sold, any single estimate would have only a negligible impact on revenue recognition. | |||||||

| Retail | Potash, Nitrogen, and Phosphate and Sulfate | |||||||

| Transfer of control for the sale of goods | ||||||||

| At the point in time when the product is:

• purchased at the Company’s Retail farm center or

• delivered and accepted by customers at their premises |

At the point in time when the product is:

• loaded for shipping or

• delivered to the customer | |||||||

| Transfer of control for services | ||||||||

| When the promised service is rendered | When the promised service is rendered | |||||||

| Retail Sales revenue consists primarily of:

• Crop nutrients – sales of dry and liquid macronutrient products which include nitrogen, potash and phosphate, proprietary liquid micronutrient products and nutrient application services;

• Crop protection products – sales of various third-party supplier and proprietary products designed to maintain crop quality and manage plant diseases, weeds, and other pests; |

| NUTRIEN 2018 | 103 | ANNUAL REPORT |

IN MILLIONS OF US DOLLARS EXCEPT AS OTHERWISE NOTED

NOTE 4 SEGMENT INFORMATION CONTINUED

| Accounting Policies | Accounting Estimates and Judgments | |||

|

• Seed – various third-party supplier seed brands and proprietary seed product lines;

• Merchandise – sales of fencing, feed supplements, livestock-related animal health products, storage and irrigation equipment, and other products; and

• Services and other revenues – sales of product application, soil and leaf testing, crop scouting and precision agriculture services, financial services and livestock marketing.

Provisions for returns, trade discounts and rebates are deducted from sales revenue.

Potash, Nitrogen, and Phosphate and Sulfate

The Company manufactures and sells potash, nitrogen, and phosphate and sulfate products. While agriculture is the Company’s primary market, it also produces products for animal nutrition and industrial uses.

The Company’s sales revenue is recorded and measured based on the “freight on board” mine, plant, warehouse or terminal price specified in the contract (except for certain vessel sales or specific product sales that are shipped and recorded on a delivered basis), which reflects the consideration the Company expects to be entitled to in exchange for the goods or services, net of any variable consideration (e.g., any trade discounts or estimated volume rebates). Where volume rebates are provided for in customer contracts, the Company estimates revenue at the earlier of the most likely amount of consideration expected to be received or when the consideration becomes fixed. The Company’s customer contracts may provide certain product quality specification guarantees but do not generally provide for refunds or returns.

Sales prices are based on North American and International benchmark market prices which are variable and subject to global supply and demand, and competitive factors. |

| Potash | Nitrogen | Phosphate and Sulfate | ||||||||

| Products | • North American – primarily granular • Offshore (International) – primarily granular and standard |

• Ammonia, urea, urea ammonium nitrate, and industrial grade ammonium nitrate |

• Solid fertilizer, liquid fertilizer, industrial products and feed products |

|||||||

| Sales prices impacted by | • North American prices referenced at delivered prices (including transportation and distribution costs)

• International prices referenced at the mine site (excluding transportation and distribution costs) |

• Global energy costs and supply |

• Global ammonia and sulfur costs and supply |

|||||||

| Other The Company does not provide general warranties. Intersegment sales are made under terms that approximate market value. Transportation costs are generally recovered from the customer through sales pricing.

Seasonality in the Company’s business results from increased demand for products during planting season. Crop input sales are generally higher in spring and fall crop input application seasons. Crop nutrient inventories are normally accumulated leading up to each application season. The Company’s cash collections generally occur after the application season is complete while customer prepayments are concentrated in December and January. |

| NUTRIEN 2018 | 104 | ANNUAL REPORT |

FINANCIAL STATEMENTS AND NOTES

IN MILLIONS OF US DOLLARS EXCEPT AS OTHERWISE NOTED

NOTE 4 SEGMENT INFORMATION CONTINUED

Supporting Information

Financial information on each of these segments is summarized in the following tables:

| 2018 | Retail | Potash | Nitrogen | Phosphate and Sulfate |

Others | Eliminations | Consolidated | |||||||||||||||||||||

| Sales – third party |

$ | 12,620 | $ | 2,796 | $ | 2,651 | $ | 1,569 | $ | – | $ | – | $ | 19,636 | ||||||||||||||

| – intersegment |

50 | 220 | 566 | 328 | – | (1,164 | ) | – | ||||||||||||||||||||

| Sales – total |

12,670 | 3,016 | 3,217 | 1,897 | – | (1,164 | ) | 19,636 | ||||||||||||||||||||

| Freight, transportation and distribution |

– | (349 | ) | (358 | ) | (230 | ) | – | 73 | (864 | ) | |||||||||||||||||

| Net sales |

12,670 | 2,667 | 2,859 | 1,667 | – | (1,091 | ) | |||||||||||||||||||||

| Cost of goods sold |

(9,635 | ) | (1,183 | ) | (2,079 | ) | (1,539 | ) | – | 1,056 | (13,380 | ) | ||||||||||||||||

| Gross margin |

3,035 | 1,484 | 780 | 128 | – | (35 | ) | 5,392 | ||||||||||||||||||||

| Selling expenses |

(2,303 | ) | (14 | ) | (32 | ) | (10 | ) | 22 | – | (2,337 | ) | ||||||||||||||||

| General and administrative expenses |

(100 | ) | (10 | ) | (20 | ) | (9 | ) | (400 | ) | – | (539 | ) | |||||||||||||||

| Provincial mining and other taxes |

– | (244 | ) | (3 | ) | (1 | ) | (2 | ) | – | (250 | ) | ||||||||||||||||

| Impairment of property, plant and equipment (Note 16) |

– | (1,809 | ) | – | – | – | – | (1,809 | ) | |||||||||||||||||||

| Other income (expenses) |

75 | (14 | ) | 8 | (6 | ) | (106 | ) | – | (43 | ) | |||||||||||||||||

| Earnings (loss) before finance costs and income taxes |

707 | (607 | ) | 733 | 102 | (486 | ) | (35 | ) | 414 | ||||||||||||||||||

| Depreciation and amortization |

499 | 404 | 429 | 206 | 54 | – | 1,592 | |||||||||||||||||||||

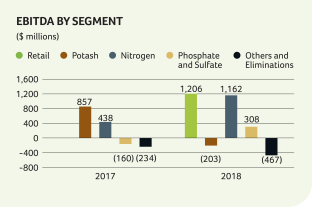

| EBITDA 1 |

$ | 1,206 | $ | (203 | ) | $ | 1,162 | $ | 308 | $ | (432 | ) | $ | (35 | ) | $ | 2,006 | |||||||||||

| Assets 2 |

$ | 17,964 | $ | 11,710 | $ | 10,009 | $ | 2,783 | $ | 3,678 | $ | (642 | ) | $ | 45,502 | |||||||||||||

| 1 | EBITDA is a non-IFRS measure calculated as net (loss) earnings from continuing operations before finance costs, income taxes, and depreciation and amortization. Nutrien uses EBITDA as a supplemental measure. Generally, this measure is a numerical measure of a company’s performance, that either excludes or includes amounts that are not normally excluded or included in the most directly comparable measure calculated and presented in accordance with IFRS. In evaluating this measure, investors should consider that the methodology applied in calculating this measure may differ among companies and analysts. The Company uses both IFRS and certain non-IFRS measures to assess performance. Management believes the non-IFRS measures provide useful supplemental information to investors in order that they may evaluate Nutrien’s financial performance using the same measures as management. Management believes that, as a result, the investor is afforded greater transparency in assessing the financial performance of the Company. This non-IFRS financial measure should not be considered as a substitute for, nor superior to, measures of financial performance prepared in accordance with IFRS. |

| 2 | Included in the Nitrogen and Retail segments are $428 and $208 relating to equity-accounted investees, respectively, as described in Note 21. |

| NUTRIEN 2018 | 105 | ANNUAL REPORT |

IN MILLIONS OF US DOLLARS EXCEPT AS OTHERWISE NOTED

NOTE 4 SEGMENT INFORMATION CONTINUED

| 2017 | Potash | Nitrogen | Phosphate and Sulfate |

Others | Eliminations | Consolidated | ||||||||||||||||||

| Sales – third party |

$ | 1,868 | $ | 1,395 | $ | 1,284 | $ | – | $ | – | $ | 4,547 | ||||||||||||

| – intersegment |

– | 74 | – | – | (74 | ) | – | |||||||||||||||||

| Sales – total |

1,868 | 1,469 | 1,284 | – | (74 | ) | 4,547 | |||||||||||||||||

| Freight, transportation and distribution |

(235 | ) | (129 | ) | (173 | ) | – | – | (537 | ) | ||||||||||||||

| Net sales |

1,633 | 1,340 | 1,111 | – | (74 | ) | ||||||||||||||||||

| Cost of goods sold 1 |

(829 | ) | (1,084 | ) | (1,477 | ) | – | 74 | (3,316 | ) | ||||||||||||||

| Gross margin |

804 | 256 | (366 | ) | – | – | 694 | |||||||||||||||||

| Selling expenses |

(7 | ) | (14 | ) | (6 | ) | (2 | ) | – | (29 | ) | |||||||||||||

| General and administrative expenses |

(7 | ) | (4 | ) | (4 | ) | (170 | ) | – | (185 | ) | |||||||||||||

| Provincial mining and other taxes |

(146 | ) | – | – | – | – | (146 | ) | ||||||||||||||||

| Other expenses |

(19 | ) | (3 | ) | (4 | ) | (99 | ) | – | (125 | ) | |||||||||||||

| Earnings (loss) before finance costs and |

625 | 235 | (380 | ) | (271 | ) | – | 209 | ||||||||||||||||

| Depreciation and amortization |

232 | 203 | 220 | 37 | – | 692 | ||||||||||||||||||

| EBITDA |

$ | 857 | $ | 438 | $ | (160 | ) | $ | (234 | ) | $ | – | $ | 901 | ||||||||||

| Assets 2 |

$ | 9,756 | $ | 2,577 | $ | 1,938 | $ | 2,727 | $ | – | $ | 16,998 | ||||||||||||

| 1 | Included in the Phosphate and Sulfate segment is $305 of impairment of property, plant and equipment as described in Note 16. |

| 2 | Included in the total assets relating to the Others segment is $1,858 relating to the investments held for sale as described in Note 10. |

Financial information by geographic area is summarized in the following tables:

| Country of Origin | ||||||||||||||||||||||||

| 2018 | United States | Canada | Australia | Trinidad | Other | Consolidated | ||||||||||||||||||

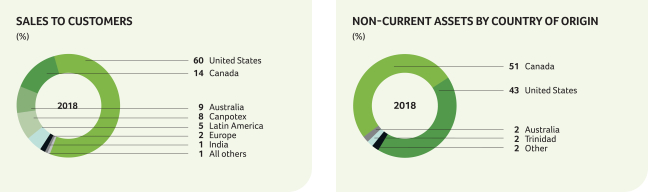

| Sales to customers outside the Company |

||||||||||||||||||||||||

| United States |

$ | 10,488 | $ | 1,249 | $ | – | $ | 153 | $ | 1 | $ | 11,891 | ||||||||||||

| Canada |

208 | 2,582 | – | – | – | 2,790 | ||||||||||||||||||

| Australia |

2 | – | 1,679 | – | – | 1,681 | ||||||||||||||||||

| Canpotex 1 |

– | 1,657 | – | – | – | 1,657 | ||||||||||||||||||

| Mexico |

70 | – | – | 15 | – | 85 | ||||||||||||||||||

| Trinidad |

9 | – | – | 181 | – | 190 | ||||||||||||||||||

| Argentina |

9 | – | – | – | 378 | 387 | ||||||||||||||||||

| Brazil |

38 | – | – | – | 74 | 112 | ||||||||||||||||||

| Colombia |

9 | – | – | 42 | – | 51 | ||||||||||||||||||

| Other Latin America |

20 | – | – | 59 | 92 | 171 | ||||||||||||||||||

| India |

151 | – | – | – | – | 151 | ||||||||||||||||||

| Europe |

11 | 58 | 67 | 93 | 83 | 312 | ||||||||||||||||||

| Other |

22 | – | 100 | 32 | 4 | 158 | ||||||||||||||||||

| $ | 11,037 | $ | 5,546 | $ | 1,846 | $ | 575 | $ | 632 | $ | 19,636 | |||||||||||||

| Non-current assets 2 |

$ | 14,501 | $ | 17,100 | $ | 607 | $ | 570 | $ | 621 | $ | 33,399 | ||||||||||||

| 1 | As described in Note 1, Canpotex executed offshore marketing, sales and distribution functions for certain of the Company’s products. Canpotex’s 2018 sales volumes were made to: Latin America 33%, China 18%, India 10%, Other Asian markets 31%, other markets 8% (Note 30). |

| 2 | Includes non-current assets other than financial instruments, deferred tax assets and post-employment benefit assets. |

| NUTRIEN 2018 | 106 | ANNUAL REPORT |

FINANCIAL STATEMENTS AND NOTES

IN MILLIONS OF US DOLLARS EXCEPT AS OTHERWISE NOTED

NOTE 4 SEGMENT INFORMATION CONTINUED

| Country of Origin | ||||||||||||||||||||

| 2017 | United States | Canada | Trinidad |

Other | Consolidated | |||||||||||||||

| Sales to customers outside the Company |

||||||||||||||||||||

| United States |

$ | 1,657 | $ | 784 | $ | 274 | $ | – | $ | 2,715 | ||||||||||

| Canada |

194 | 95 | – | – | 289 | |||||||||||||||

| Canpotex 1 |

– | 988 | – | – | 988 | |||||||||||||||

| Mexico |

76 | – | 9 | – | 85 | |||||||||||||||

| Trinidad |

– | – | 132 | – | 132 | |||||||||||||||

| Brazil |

26 | 1 | – | – | 27 | |||||||||||||||

| Colombia |

12 | – | 36 | – | 48 | |||||||||||||||

| Other Latin America |

26 | – | 42 | – | 68 | |||||||||||||||

| India |

97 | – | 7 | – | 104 | |||||||||||||||

| Other |

10 | – | 81 | – | 91 | |||||||||||||||

| $ | 2,098 | $ | 1,868 | $ | 581 | $ | – | $ | 4,547 | |||||||||||

| Non-current assets 2 |

$ | 3,259 | $ | 9,501 | $ | 554 | $ | 6 | $ | 13,320 | ||||||||||

| 1 | Canpotex’s 2017 sales volumes were made to: Latin America 30%, China 18%, India 12%, Other Asian markets 33%, other markets 7% (Note 30). |

| 2 | Includes non-current assets other than financial instruments, deferred tax assets and post-employment benefit assets. |

The Company disaggregated revenue from contracts with customers by product line or geographic location for each reportable segment to show how the nature, amount, timing and uncertainty of revenue and cash flows are affected by economic factors.

| NUTRIEN 2018 | 107 | ANNUAL REPORT |

IN MILLIONS OF US DOLLARS EXCEPT AS OTHERWISE NOTED

|

|

NATURE OF EXPENSES

|

Accounting Policies

Cost of goods sold represents the cost of purchasing products for resale and costs primarily incurred at, and charged to, producing facilities.

The primary components of selling and general and administrative expenses are compensation, other employee costs, depreciation and amortization, other operating leases, and fleet fuel, repairs and maintenance.

Supporting Information

Expenses by nature were comprised of:

| Cost of Goods Sold | Other | Total | ||||||||||||||||||||||||||||||||||||||

| 2018 | 2017 | 2018 | 2017 | 2018 | 2017 | |||||||||||||||||||||||||||||||||||

| (Note 33) | (Note 33) | (Note 33) | ||||||||||||||||||||||||||||||||||||||

| Purchased and produced raw materials and product for resale 1 |

$ | 11,145 | $ | 1,724 | $ | – | $ | – | $ | 11,145 | $ | 1,724 | ||||||||||||||||||||||||||||

| Depreciation and amortization |

1,038 | 655 | 554 | 37 | 1,592 | 692 | ||||||||||||||||||||||||||||||||||

| Employee costs 2 |

713 | 563 | 1,236 | 113 | 1,949 | 676 | ||||||||||||||||||||||||||||||||||

| Freight (direct and indirect) |

303 | – | 631 | 372 | 934 | 372 | ||||||||||||||||||||||||||||||||||

| Impairment of property, plant and equipment (Note 16) |

– | 305 | – | – | – | 305 | ||||||||||||||||||||||||||||||||||

| Offsite warehouse costs 3 |

– | – | 69 | 47 | 69 | 47 | ||||||||||||||||||||||||||||||||||

| Railcar and vessel costs 3 |

– | – | 131 | 102 | 131 | 102 | ||||||||||||||||||||||||||||||||||

| Merger and related costs |

– | – | 170 | 84 | 170 | 84 | ||||||||||||||||||||||||||||||||||

| Other operating leases |

38 | – | 110 | – | 148 | – | ||||||||||||||||||||||||||||||||||

| Fleet fuel, repairs and maintenance |

– | – | 183 | – | 183 | – | ||||||||||||||||||||||||||||||||||

| Other |

143 | 69 | 699 | 121 | 842 | 190 | ||||||||||||||||||||||||||||||||||

| Total |

$ | 13,380 | $ | 3,316 | $ | 3,783 | $ | 876 | $ | 17,163 | $ | 4,192 | ||||||||||||||||||||||||||||

| Expenses included in: |

||||||||||||||||||||||||||||||||||||||||

| Freight, transportation and distribution |

|

$ | 864 | $ | 537 | |||||||||||||||||||||||||||||||||||

| Cost of goods sold |

13,380 | 3,316 | ||||||||||||||||||||||||||||||||||||||

| Selling expenses |

2,337 | 29 | ||||||||||||||||||||||||||||||||||||||

| General and administrative expenses |

539 | 185 | ||||||||||||||||||||||||||||||||||||||

| Other expenses |

43 | 125 | ||||||||||||||||||||||||||||||||||||||

| 1 | Significant expenses include: contract services, supplies, energy, fuel, purchases of raw material (natural gas – feedstock, sulfur, ammonia and reagents) and product for resale (crop nutrients and protection products, and seed). |

| 2 | Includes employee benefits and share-based compensation. In 2018, employee costs also include a $157 gain on curtailment of defined benefit pension and other post-retirement benefit plans (“Defined Benefit Plans Curtailment Gain”) as described in Note 28. |

| 3 | Includes expenses relating to operating leases. |

| NUTRIEN 2018 | 108 | ANNUAL REPORT |

FINANCIAL STATEMENTS AND NOTES

IN MILLIONS OF US DOLLARS EXCEPT AS OTHERWISE NOTED

|

|

PROVINCIAL MINING AND OTHER TAXES

|

Under Saskatchewan provincial legislation, the Company is subject to resource taxes, including the potash production tax and the resource surcharge.

| 2018 | 2017 | |||||||

| (Note 33) | ||||||||

| Saskatchewan potash production tax |

$ 160 | $ 95 | ||||||

| Saskatchewan resource surcharge and other |

90 | 51 | ||||||

| $ 250 | $ 146 | |||||||

|

|

OTHER EXPENSES

|

| 2018 | 2017 | |||||||||||

| (Note 33) | ||||||||||||

| Merger and related costs |

$ (170) | $ (84) | ||||||||||

| Defined Benefit Plans Curtailment Gain (Note 28) |

157 | – | ||||||||||

| Foreign exchange gain (loss) |

10 | (21) | ||||||||||

| Other expenses |

(40) | (20) | ||||||||||

| $ (43) | $ (125) | |||||||||||

|

|

FINANCE COSTS

|

| 2018 | 2017 | |||||||||||

| Interest expense |

||||||||||||

| Short-term debt |

$ 129 | $ 9 | ||||||||||

| Long-term debt |

372 | 206 | ||||||||||

| Unwinding of discount on asset retirement obligations (Note 20) |

51 | 17 | ||||||||||

| Interest on net defined benefit pension and other post-retirement plan obligations (Note 28) |

15 | 19 | ||||||||||

| Borrowing costs capitalized to property, plant and equipment |

(12) | (11) | ||||||||||

| Interest income |

(17) | (2) | ||||||||||

| $ 538 | $ 238 | |||||||||||

Borrowing costs capitalized to property, plant and equipment in 2018 were calculated by applying an average capitalization rate of 4.4 percent (2017 – 4.4 percent) to expenditures on qualifying assets.

See Note 12 for interest paid.

| NUTRIEN 2018 | 109 | ANNUAL REPORT |

IN MILLIONS OF US DOLLARS EXCEPT AS OTHERWISE NOTED

|

|

INCOME TAXES

|

This note explains the Company’s income tax recovery and tax-related balances within the consolidated financial statements. The deferred tax section provides information on expected future tax payments.

| Accounting Policies | Accounting Estimates and Judgments | |||||

| The Company operates in a specialized industry and in several tax jurisdictions. As a result, its income is subject to various rates of taxation. Taxation on items recognized in the consolidated statements of earnings, other comprehensive income (“OCI”) or contributed surplus is recognized in the same location as those items.

Taxation on (loss) earnings is comprised of current and deferred income tax.

|

Estimates and judgments to determine the Company’s taxes are impacted by:

• the breadth of the Company’s operations; and

• global complexity of tax regulations.

The final taxes paid, and potential adjustments to tax assets and liabilities, are dependent upon many factors including:

• negotiations with taxation authorities in various jurisdictions;

• outcomes of tax litigation; and

• resolution of disputes arising from federal, provincial, state and local tax audits.

Estimates and judgments are used to recognize the amount of deferred tax assets, which:

• includes the probability that future taxable profit will be available to use deductible temporary differences, and could be reduced if projected earnings are not achieved or increased if earnings previously not projected become probable. | |||||

| Current income tax is: |

Deferred income tax is: | |||||

|

• the expected tax payable on the taxable earnings for the year;

• calculated using rates enacted or substantively enacted at the dates of the consolidated balance sheets in the countries where the Company’s subsidiaries, held for sale investees and equity-accounted investees operate and generate taxable earnings; and

• inclusive of any adjustment to income tax payable or recoverable in respect of previous years. |

• recognized using the liability method;

• based on temporary differences between financial statements’ carrying amounts of assets and liabilities and their respective income tax bases; and

• determined using tax rates that have been enacted or substantively enacted by the dates of the consolidated balance sheets and are expected to apply when the related deferred income tax asset is realized or the deferred income tax liability is settled. |

|||||

|

Uncertain income tax positions are accounted for using the standards applicable to current income tax liabilities and assets, i.e., both liabilities and assets are recorded when probable and measured at the amount expected to be paid to (recovered from) the taxation authorities using the Company’s best estimate of the amount.

Deferred income tax is not accounted for:

• with respect to investments in subsidiaries and equity-accounted investees where the Company is able to control the reversal of the temporary difference and that difference is not expected to reverse in the foreseeable future; and

• if arising from initial recognition of an asset or liability in a transaction, other than a business combination, that at the time of the transaction affects neither accounting nor taxable profit or loss.

The realized and unrealized excess tax benefits from share-based payment arrangements are recognized in contributed surplus as current and deferred tax, respectively.

Deferred income tax assets are reviewed at each balance sheet date and amended to the extent that it is no longer probable that the related tax benefit will be realized.

Income tax assets and liabilities are offset when:

|

||||||

| For current income taxes, the Company has: | For deferred income taxes: | |||||

|

• a legally enforceable right to offset the recognized amounts 1 ; and

• the intention to settle on a net basis or realize the asset and settle the liability simultaneously. |

• the Company has a legally enforceable right to set off current tax assets against current tax liabilities; and

• they relate to income taxes levied by the same taxation authority on either: 1) the same taxable entity; or 2) different taxable entities intending to settle current tax liabilities and assets on a net basis, or realize assets and settle liabilities simultaneously in each future period. 2 |

|||||

|

1 For income taxes levied by the same taxation authority and the authority permits the Company to make or receive a single net payment or receipt. 2 In which significant amounts of deferred tax liabilities or assets expected are to be settled or recovered. |

||||||

| NUTRIEN 2018 | 110 | ANNUAL REPORT |

FINANCIAL STATEMENTS AND NOTES

IN MILLIONS OF US DOLLARS EXCEPT AS OTHERWISE NOTED

NOTE 9 INCOME TAXES CONTINUED

Supporting Information

Income Tax Balances

Income tax balances within the consolidated balance sheets as at December 31 were comprised of the following:

| Income Tax Assets (Liabilities) | Balance Sheet Location | 2018 | 2017 | |||||||||||||||

| Current income tax assets |

||||||||||||||||||

| Current |

Receivables (Note 14) | $ | 248 | $ | 24 | |||||||||||||

| Long-term |

Other assets (Note 18) | 36 | 64 | |||||||||||||||

| Deferred income tax assets |

Other assets (Note 18) | 216 | 18 | |||||||||||||||

| Total income tax assets |

$ | 500 | $ | 106 | ||||||||||||||

| Current income tax liabilities |

||||||||||||||||||

| Current |

Payables and accrued charges (Note 19) | $ | (47 | ) | $ | (16 | ) | |||||||||||

| Non-current |

Other non-current liabilities | (64 | ) | (43 | ) | |||||||||||||

| Deferred income tax liabilities |

Deferred income tax liabilities | (2,907 | ) | (2,205 | ) | |||||||||||||

| Total income tax liabilities |

$ | (3,018 | ) | $ | (2,264 | ) | ||||||||||||

| NUTRIEN 2018 | 111 | ANNUAL REPORT |

IN MILLIONS OF US DOLLARS EXCEPT AS OTHERWISE NOTED

NOTE 9 INCOME TAXES CONTINUED

Deferred Income Taxes

In respect of each type of temporary difference, unused tax loss and unused tax credit, the amounts of deferred tax assets and liabilities recognized in the consolidated balance sheets as at December 31 and the amount of the deferred tax recovery (expense) recognized in net (loss) earnings from continuing operations were:

| Deferred Income Tax Assets (Liabilities) |

Deferred Income Tax Recovery (Expense) Recognized in Net Earnings |

|||||||||||||||||||||||

| 2018 | 2017 | 2018 | 2017 | |||||||||||||||||||||

| Deferred income tax assets |

||||||||||||||||||||||||

| Asset retirement obligations and accrued environmental costs |

$ 412 | $ 120 | $ | (11 | ) | $ | (56 | ) | ||||||||||||||||

| Tax loss and other carryforwards |

261 | 13 | 198 | (105 | ) | |||||||||||||||||||

| Pension and other post-retirement benefit liabilities |

130 | 124 | (44 | ) | (22 | ) | ||||||||||||||||||

| Long-term debt |

110 | – | (10 | ) | – | |||||||||||||||||||

| Receivables |

58 | – | 3 | – | ||||||||||||||||||||

| Inventories |

54 | 4 | 13 | (2 | ) | |||||||||||||||||||

| Derivatives |

17 | 13 | (15 | ) | – | |||||||||||||||||||

| Other assets |

57 | 11 | (18 | ) | (11 | ) | ||||||||||||||||||

| Deferred income tax liabilities |

||||||||||||||||||||||||

| Property, plant and equipment |

(3,218 | ) | (2,441 | ) | 132 | 472 | ||||||||||||||||||

| Goodwill and other intangible assets |

(546 | ) | (17 | ) | 31 | – | ||||||||||||||||||

| Other liabilities |

(26 | ) | (14 | ) | (6 | ) | (3 | ) | ||||||||||||||||

| $ (2,691 | ) | $ (2,187 | ) | $ | 273 | $ | 273 | |||||||||||||||||

| NUTRIEN 2018 | 112 | ANNUAL REPORT |

FINANCIAL STATEMENTS AND NOTES

IN MILLIONS OF US DOLLARS EXCEPT AS OTHERWISE NOTED

|

|

DISCONTINUED OPERATIONS

|

Held for Sale and Discontinued Operations

| Accounting Policies | Accounting Estimates and Judgments | |||

| The Company classifies assets and liabilities as held for sale if it is highly probable that the carrying value will be recovered through a sale transaction within one year rather than through continuing use.

Discontinued operations represent a component of the Company’s business that either has been disposed of, or is classified as held for sale, and represents a separate major line of business or geographic area of operations or is a part of a single coordinated plan to dispose of a separate major line of business or geographical area of operations.

The Company’s significant policies include:

• cessation of equity accounting for associates and joint ventures at the date the investments were classified as held for sale;

• measurement of assets at the lower of carrying amount and fair value less costs to sell, with the exception of financial assets measured at FVTOCI;

• unrealized gains and losses on remeasurement of investments measured at FVTOCI are recorded, net of related income taxes, to OCI;

• dividends received are recorded on the consolidated statements of earnings; and

• the comparative statements of earnings and OCI are restated as if the operation had been discontinued from the start of the comparative year. |

Expected cost to sell the investments requires estimation, which is based on several factors such as historical trends of similar types of investments sold, the percentage of investments held relative to the total shares in circulation and the type of the investment.

Judgment involves determining:

• whether the highly probable standard is met and the date when equity accounting ceases; and

• if the business component for sale or disposal meets the criteria of a discontinued operation. |

The Company’s investments in SQM, ICL and APC were classified as held for sale and as discontinued operations in December 2017, due to regulatory requirements to dispose of these investments in connection with the Merger.

As of December 31, 2018, the Company completed all required divestitures and retained no residual interests as outlined below:

| For the year ended December 31, 2018 | Proceeds 1 | Gain (Loss) on Sale |

Gain (Loss) on Taxes |

AOCI | Net Earnings and Retained Earnings |

|||||||||||||||

| Shares in SQM |

$ | 5,126 | $ | 4,278 | $ | 3,366 | $ | – | $ | 3,366 | ||||||||||

| Shares in ICL |

685 | (19 | ) | (19 | ) | (19 | ) | – | ||||||||||||

| Shares in APC |

501 | 121 | 126 | – | 126 | |||||||||||||||

| Conda Phosphate operations |

98 | – | – | – | – | |||||||||||||||

| Total Sale |

$ | 6,410 | $ | 4,380 | $ | 3,473 | $ | (19 | ) | $ | 3,492 | |||||||||

| 1 | Proceeds are net of commissions. |

| NUTRIEN 2018 | 113 | ANNUAL REPORT |

IN MILLIONS OF US DOLLARS EXCEPT AS OTHERWISE NOTED

NOTE 10 DISCONTINUED OPERATIONS CONTINUED

Supporting Information

Cash flows from discontinued operations for the year ended December 31 were as follows:

| 2018 | 2017 | |||||||||||||||

| Cash provided by operating activities |

||||||||||||||||

| Dividends from discontinued operations |

$ | 156 | $ | 176 | ||||||||||||

| Income tax related to the disposal of discontinued operations |

(26 | ) | – | |||||||||||||

| Dividends from discontinued operations, net of tax |

$ | 130 | $ | 176 | ||||||||||||

| Cash provided by investing activities |

||||||||||||||||

| Proceeds from disposal of discontinued operations 1 |

$ | 6,371 | $ | – | ||||||||||||

| Income tax related to the disposal of discontinued operations |

(977 | ) | – | |||||||||||||

| Proceeds from disposal of discontinued operations, net of tax |

$ | 5,394 | $ | – | ||||||||||||

| 1 | Excludes a receivable of $39 to be collected in 2019. |

|

|

NET EARNINGS PER SHARE

|

Basic net earnings per share provides a measure of the interests of each ordinary common share in the Company’s performance over the year. Diluted net earnings per share adjusts basic net earnings per share for the effects of all dilutive potential common shares.

| 2018 1 | 2017 | |||||||||||||||

| WEIGHTED AVERAGE NUMBER OF COMMON SHARES |

624,900,000 | 840,079,000 | ||||||||||||||

| Dilutive effect of stock options 2 |

– | 3 | 199,000 | |||||||||||||

| Dilutive effect of share-settled performance share units (“PSUs”) 4 |

– | 3 | 38,000 | |||||||||||||

| Weighted average number of diluted common shares |

624,900,000 | 840,316,000 | ||||||||||||||

| 1 | The number of shares, stock options and share-settled PSUs reflect the Merger. Refer to Note 3 for details. |

| 2 | Diluted effect of stock options assumes exercise of all stock options with exercise prices at or below the average market price for the year would increase the denominator, and the denominator would be decreased by the number of shares that the Company could have repurchased if it had assumed proceeds from the exercise of stock options to repurchase them on the open market at the average share price for the year. |

| 3 | The diluted weighted average share calculations excluded an additional 658,000 stock options and 137,000 equity-settled PSUs due to their anti-dilutive effect. |

| 4 | Diluted effect of PSUs assumes the denominator would be increased by the total of the additional share-settled PSUs that could be issued if vesting criteria are achieved. |

| NUTRIEN 2018 | 114 | ANNUAL REPORT |

FINANCIAL STATEMENTS AND NOTES

IN MILLIONS OF US DOLLARS EXCEPT AS OTHERWISE NOTED

NOTE 11 NET EARNINGS PER SHARE CONTINUED

Options excluded from the calculation of diluted net earnings per share due to the option exercise prices being greater than the average market price of common shares were as follows:

| 2018 | 2017 | |||||||||||||||

| Number of options excluded |

5,721,656 | 12,304,351 | ||||||||||||||

| Performance option plan years fully excluded |

2009-2015 | 2008-2015, 2017 | ||||||||||||||

| Stock option plan years fully excluded |

2015, 2018 | – | ||||||||||||||

|

|

CONSOLIDATED STATEMENTS OF CASH FLOWS

|

Accounting Policy

Highly liquid investments with a maturity of three months or less from the date of purchase are considered to be cash equivalents.

Supporting Information

| For the years ended December 31 | 2018 | 2017 | ||||||||||||

| (Note 33 | ) | |||||||||||||

| RECONCILIATION OF CASH PROVIDED BY OPERATING ACTIVITIES |

||||||||||||||

| Net earnings |

$ | 3,573 | $ | 327 | ||||||||||

| Adjustments to reconcile net earnings to cash provided by operating activities |

||||||||||||||

| Gain on sale of investments in SQM and APC |

(4,399 | ) | – | |||||||||||

| Income tax related to the sale of the investment in SQM |

977 | – | ||||||||||||

| Depreciation and amortization |

1,592 | 692 | ||||||||||||

| Impairment of property, plant and equipment (Note 16) |

1,809 | 305 | ||||||||||||

| Share-based compensation (Note 29) |

116 | 11 | ||||||||||||

| Recovery of deferred income tax |

(290 | ) | (273 | ) | ||||||||||

| Other long-term liabilities and miscellaneous |

(188 | ) | 91 | |||||||||||

| Subtotal of adjustments

|

|

(383

|

)

|

|

826

|

| ||||||||

| CHANGES IN NON-CASH OPERATING WORKING CAPITAL |

||||||||||||||

| Receivables |

(153 | ) | 47 | |||||||||||

| Inventories |

(887 | ) | (10 | ) | ||||||||||

| Prepaid expenses and other current assets |

561 | (13 | ) | |||||||||||

| Payables and accrued charges |

(659 | ) | 48 | |||||||||||

| Subtotal of changes in non-cash operating working capital |

(1,138 | ) | 72 | |||||||||||

| CASH PROVIDED BY OPERATING ACTIVITIES

|

$

|

2,052

|

|

$

|

1,225

|

| ||||||||

| SUPPLEMENTAL CASH FLOWS DISCLOSURES |

||||||||||||||

| Interest paid |

$ | 507 | $ | 198 | ||||||||||

| Income taxes paid |

$ | 1,155 | $ | 83 | ||||||||||

| NUTRIEN 2018 | 115 | ANNUAL REPORT |

IN MILLIONS OF US DOLLARS EXCEPT AS OTHERWISE NOTED

NOTE 12 CONSOLIDATED STATEMENTS OF CASH FLOWS CONTINUED

The following is a summary of changes in liabilities arising from financing activities:

|

Short-Term Debt and Current Portion of Long-Term Debt 1 |

Long-Term Debt | Total | ||||||||||

| Balance – December 31, 2017 |

$ | 730 | $ | 3,711 | $ | 4,441 | ||||||

| Debt acquired in Merger (Note 3) |

878 | 4,930 | 5,808 | |||||||||

| Cash flows 1 |

(927 | ) | (12 | ) | (939 | ) | ||||||

| Reclassifications |

1,023 | (1,023 | ) | – | ||||||||

| Foreign currency translation and other non-cash changes |

(72 | ) | (15 | ) | (87 | ) | ||||||

| Balance – December 31, 2018 |

$ | 1,632 | $ | 7,591 | $ | 9,223 | ||||||

| Balance – December 31, 2016 |

$ | 884 | $ | 3,707 | $ | 4,591 | ||||||

| Cash flows 1 |

(159 | ) | (1 | ) | (160 | ) | ||||||

| Non-cash changes |

5 | 5 | 10 | |||||||||

| Balance – December 31, 2017 |

$ | 730 | $ | 3,711 | $ | 4,441 | ||||||

| 1 | Cash inflows and cash outflows arising from short-term debt transactions are presented on a net basis. |

|

|

FINANCIAL INSTRUMENTS AND RELATED RISK MANAGEMENT

|

Outlined below are the Company’s financial instruments, related risk management objectives, policies and exposure, sensitivity and monitoring strategies to financial risks.

| Accounting Policies | Accounting Estimates and Judgments | |||

| Financial instruments are classified and measured as follows: |

Judgment is required to determine whether the right to offset is legally enforceable. | |||

| Fair Value Through Profit or Loss (“FVTPL”) |

FVTOCI | Financial Assets and Liabilities at Amortized Cost 1 |

For derivatives or embedded derivatives, the most significant area of judgment is whether the contract can be settled net. This is one of the criteria used to determine whether a contract for a nonfinancial asset is considered a derivative and accounted for as such. Judgment is also applied in determining whether an embedded derivative is closely related to the host contract, in which case bifurcation and separate accounting are not necessary. | |||||

| Instrument type |

Cash and cash equivalents and derivatives | Equity investments not held for trading | Receivables, short-term debt, payables and accrued charges, long-term debt, other long-term debt instruments | |||||

| Measurement | Fair value | Fair value | Amortized cost | |||||

| Fair value gains and losses | Profit or loss | OCI 2 | – | |||||

| Interest and dividends | Profit or loss | Profit or loss | Profit or loss: effective interest rate | |||||

| Impairment of assets | – | – | Profit or loss | |||||

| Foreign exchange | Profit or loss | OCI | Profit or loss | |||||

| Transaction costs | Profit or loss | OCI | Included in cost of instrument | |||||

| 1 Amortized cost is applied if the objective of the business model for the instrument or group of instruments is to hold the asset to collect the contractual cash flows and the contractual terms give rise on specified dates to cash flows that are solely payments of principal and interest. 2 For equity investments not held for trading, the Company may make an irrevocable election at initial recognition to recognize changes in fair value through OCI rather than profit or loss. The Company made this election for its investments in ICL, Sinofert and certain equity investments as the investments are held for strategic purposes. |

||||||||

| NUTRIEN 2018 | 116 | ANNUAL REPORT |

FINANCIAL STATEMENTS AND NOTES

IN MILLIONS OF US DOLLARS EXCEPT AS OTHERWISE NOTED

NOTE 13 FINANCIAL INSTRUMENTS AND RELATED RISK MANAGEMENT CONTINUED

| Accounting Policies | Accounting Estimates and Judgments | |||

| Financial instruments are recognized at trade date when the Company commits to purchase or sell the asset. Financial assets are derecognized when the rights to receive cash flows from the investments have expired or the Company has transferred them, and all the risks and rewards of ownership have been substantially transferred.

Derivatives are used to lock in commodity prices and exchange rates. For designated and qualified cash flow hedges:

• the effective portion of the change in the fair value of the derivative is accumulated in OCI;

• when the hedged forecast transaction occurs, the related gain or loss is removed from AOCI and included in the cost of inventory;

• the hedging gain or loss included in the cost of inventory is recognized in earnings when the product containing the hedged item is sold or becomes impaired; and

• the ineffective portions of hedges are recorded in net earnings in the current period.

The Company also assesses whether the natural gas derivatives used in hedging transactions are expected to be or were highly effective, both at the hedge’s inception and on an ongoing basis, in offsetting changes in fair values of hedged items. Hedge effectiveness related to the Company’s New York Mercantile Exchange (“NYMEX”) natural gas hedges is assessed on a prospective and retrospective basis using regression analyses. The Company’s Alberta Energy Company (“AECO”) natural gas hedges are assessed using a qualitative assessment. Potential sources of ineffectiveness are changes in timing of forecast transactions, changes in volume delivered or changes in credit risk of the Company or the counterparty.

Financial assets and financial liabilities are offset and the net amount is presented in the consolidated balance sheets when the Company:

• currently has a legally enforceable right to offset the recognized amounts; and

• intends either to settle on a net basis, or to realize the assets and settle the liabilities simultaneously.

See Note 32 for discussion related to the policies, estimates and judgments for fair value measurements. |

Credit risk is managed through policies applicable to the following assets:

| Acceptable Minimum Counterparty Credit Ratings |

Exposure Thresholds by Counterparty |

Daily Counterparty Settlement Based on Prescribed Credit Thresholds |

Counterparties to Contracts are Investment-Grade Quality |

|||||||||||||

| Cash and Cash Equivalents |

X | X | ||||||||||||||

| Natural Gas Derivatives |

X | X | X | |||||||||||||

| Foreign Currency Derivatives |

X | |||||||||||||||

| NUTRIEN 2018 | 117 | ANNUAL REPORT |

IN MILLIONS OF US DOLLARS EXCEPT AS OTHERWISE NOTED

NOTE 13 FINANCIAL INSTRUMENTS AND RELATED RISK MANAGEMENT CONTINUED

The following maturity analysis of the Company’s financial liabilities and gross settled derivative contracts (for which the cash flows are settled simultaneously) is based on the expected undiscounted contractual cash flows from the date of the consolidated balance sheets to the contractual maturity date.

| 2018 | Carrying Amount of Liability as at December 31 |

Contractual Cash Flows |

Within 1 Year |

1 to 3 Years | 3 to 5 Years | Over 5 Years | ||||||||||||||||||||||||||||||||||||||||||

| Short-term debt 1 |

$ | 629 | $ | 629 | $ | 629 | $ | – | $ | – | $ | – | ||||||||||||||||||||||||||||||||||||

| Payables and accrued charges 2 |

4,695 | 4,695 | 4,695 | – | – | – | ||||||||||||||||||||||||||||||||||||||||||

| Current portion of long-term debt and Long-term debt1 |

8,594 | 12,818 | 1,362 | 1,121 | 1,583 | 8,752 | ||||||||||||||||||||||||||||||||||||||||||

| Derivatives |

71 | 72 | 44 | 19 | 9 | – | ||||||||||||||||||||||||||||||||||||||||||

| $ | 13,989 | $ | 18,214 | $ | 6,730 | $ | 1,140 | $ | 1,592 | $ | 8,752 | |||||||||||||||||||||||||||||||||||||

| 1 | Contractual cash flows include contractual interest payments related to debt obligations. Interest rates on variable rate debt are based on prevailing rates as at December 31, 2018. Disclosures regarding offsetting of certain debt obligations are provided below. |

| 2 | Excludes non-financial liabilities and includes trade payables of approximately $500 paid in January 2019 through an arrangement whereby a supplier sold the right to receive payment to a financial institution. |

| NUTRIEN 2018 | 118 | ANNUAL REPORT |

FINANCIAL STATEMENTS AND NOTES

IN MILLIONS OF US DOLLARS EXCEPT AS OTHERWISE NOTED

NOTE 13 FINANCIAL INSTRUMENTS AND RELATED RISK MANAGEMENT CONTINUED

Market Risk

Market risks, where financial instrument fair values can fluctuate due to changes in market prices, include foreign exchange risk, interest rate risk and price risk (related to commodity and equity securities).

Foreign Exchange Risk

To manage foreign exchange risk (primarily related to Canadian operating and capital expenditures, certain subsidiaries denominated in currencies other than the functional currency of an operation, taxes and dividends), the Company may enter into foreign currency derivatives. Treasury risk management policies allow such exposures to be hedged within certain prescribed limits for both forecast operating and capital expenditures. The risk management policy is to manage the earnings impact that could occur from a reasonably possible strengthening or weakening of the US dollar. The foreign currency derivatives are not currently designated as hedging instruments for accounting purposes. The Company had no material exposure to foreign exchange risk that could affect the Company’s net earnings as at December 31, 2018 and 2017.

Interest Rate Risk

Fair Value

Estimated fair values for financial instruments are designed to approximate amounts for which the instruments could be exchanged in a current arm’s-length transaction between knowledgeable, willing parties. The valuation policies and procedures for financial reporting purposes are determined by the Company’s finance department.

Financial instruments included in the consolidated balance sheets are measured either at fair value or amortized cost. The tables below explain the valuation methods used to determine the fair value of each financial instrument and its associated level in the fair value hierarchy.

| Financial Instruments Measured at Fair Value | Fair Value Method | |

| Cash and cash equivalents | Carrying amount (approximation to fair value assumed due to short-term nature) | |

| Equity securities | Closing bid price of the common shares as at the balance sheet date | |

| Debt securities | Closing bid price of the debt (Level 2) as at the balance sheet date | |

| Foreign currency derivatives not traded in an active market | Quoted forward exchange rates (Level 2) as at the balance sheet date | |

| NUTRIEN 2018 | 119 | ANNUAL REPORT |

IN MILLIONS OF US DOLLARS EXCEPT AS OTHERWISE NOTED

NOTE 13 FINANCIAL INSTRUMENTS AND RELATED RISK MANAGEMENT CONTINUED

| Financial Instruments Measured at Fair Value | Fair Value Method | |

| Foreign exchange forward contracts, swaps and options and natural gas swaps not traded in an active market | A discounted cash flow model 1

Market comparison 2 | |

| 1 | Inputs included contractual cash flows based on prices for natural gas futures contracts, fixed prices and notional volumes specified by the swap contracts, the time value of money, liquidity risk, the Company’s own credit risk (related to instruments in a liability position) and counterparty credit risk (related to instruments in an asset position). Futures contract prices used as inputs in the model were supported by prices quoted in an active market and therefore categorized in Level 2. |

| 2 | Inputs include current market and contractual prices, forward pricing curves, quoted forward prices, basis differentials, volatility factors and interest rates and therefore categorized in Level 2. |

| Financial Instruments Measured at Amortized Cost | Fair Value Method | |

| Receivables, short-term debt and payables and accrued charges | Carrying amount (approximation to fair value assumed due to short-term nature) | |

| Long-term debt | Quoted market prices (Level 1 or 2 depending on the market liquidity of the debt) | |

| Other long-term debt instruments | Carrying amount | |

The following table presents the Company’s fair value hierarchy for financial assets and financial liabilities carried at fair value on a recurring basis or measured at amortized costs:

| Fair Value Measurements at Reporting Dates Using: |

||||||||||||

| 2018 | Carrying Amount of Asset (Liability) as at December 31 |

Quoted Prices in for Identical Assets |

Significant Other Inputs (Level 2) 1 |

|||||||||

| Financial instruments measured at fair value on a recurring basis |

||||||||||||

| Derivative instrument assets |

$ | 5 | $ | – | $ | 5 | ||||||

| Other current financial assets – marketable securities 2 |

97 | 12 | 85 | |||||||||

| Investments at FVTOCI 3 |

186 | 186 | – | |||||||||

| Derivative instrument liabilities |

(71 | ) | – | (71 | ) | |||||||

| Financial instruments measured at amortized cost |

||||||||||||

| Cash and cash equivalents |

$ | 2,314 | $ | – | $ | 2,314 | ||||||

| Current portion of long-term debt |

||||||||||||

| Senior notes and debentures 4 |

(995 | ) | – | (1,009 | ) | |||||||

| Fixed and floating rate debt |

(8 | ) | – | (8 | ) | |||||||

| Long-term debt |

||||||||||||

| Senior notes and debentures 4 |

(7,569 | ) | (1,004 | ) | (6,177 | ) | ||||||

| Fixed and floating rate debt |

(22 | ) | – | (22 | ) | |||||||

|

2017 |

||||||||||||

| Derivative instrument assets |

||||||||||||

| Natural gas derivatives |

$ | 9 | $ | – | $ | 9 | ||||||

| Investments at FVTOCI 3 |

970 | 970 | – | |||||||||

| Derivative instrument liabilities |

||||||||||||

| Natural gas derivatives |

(64 | ) | – | (64 | ) | |||||||

| Long-term debt |

||||||||||||

| Senior notes 4 |

(3,707 | ) | (490 | ) | (3,555 | ) | ||||||

| 1 | During the period ended December 31, 2018, there were no transfers between Level 1 and Level 2 for financial instruments measured at fair value. The Company’s policy is to recognize transfers at the end of the reporting period. |

| 2 | Marketable securities consist of equity and fixed income securities. The Company determines the fair value of equity securities based on the bid price of identical instruments in active markets. The Company values fixed income securities using quoted prices of instruments with similar terms and credit risk. |

| 3 | Investments at FVTOCI are comprised of shares in Sinofert and other (Note 21) (2017 – ICL, Sinofert and other). The Company’s investment in ICL was sold during 2018 (Note 10). |

| 4 | Carrying amount of liability includes net unamortized debt issue costs. |

| NUTRIEN 2018 | 120 | ANNUAL REPORT |

FINANCIAL STATEMENTS AND NOTES

IN MILLIONS OF US DOLLARS EXCEPT AS OTHERWISE NOTED

NOTE 13 FINANCIAL INSTRUMENTS AND RELATED RISK MANAGEMENT CONTINUED

| 2018 | 2017 | |||||||||||||||||||||||||||||||||||||||||||

| Financial assets (liabilities) | Gross | Offset | Net Presented |

Gross | Offset | Net Presented |

||||||||||||||||||||||||||||||||||||||

| Derivative instrument assets |

||||||||||||||||||||||||||||||||||||||||||||

| Natural gas derivatives 1 |

$ | 31 | $ | (27 | ) | $ | 4 | $ | 11 | $ | (2 | ) | $ | 9 | ||||||||||||||||||||||||||||||

| Derivative instrument liabilities |

||||||||||||||||||||||||||||||||||||||||||||

| Natural gas derivatives 2 |

(92 | ) | 26 | (66 | ) | (74 | ) | 10 | (64 | ) | ||||||||||||||||||||||||||||||||||

| Other long-term debt instruments 3 |

(150 | ) | 150 | – | (150 | ) | 150 | – | ||||||||||||||||||||||||||||||||||||

| $ | (211 | ) | $ | 149 | $ | (62 | ) | $ | (213 | ) | $ | 158 | $ | (55 | ) | |||||||||||||||||||||||||||||

| 1 | Cash margin deposits of $NIL (2017 – $(1)) were held related to legally enforceable master netting arrangements. |

| 2 | Cash margin deposits of $18 (2017 – $38) were placed with counterparties related to legally enforceable master netting arrangements. |

| 3 | Back-to-back loan arrangements that are not subject to any financial test covenants but are subject to certain customary covenants and events of default, including, for other long-term debt, an event of default for non-payment or other debt in excess of $25. Non-compliance with such covenants could result in accelerated payment of the related debt. The Company was in compliance with these covenants as at December 31, 2018. |

Natural gas derivatives outstanding:

| 2018 | 2017 | |||||||||||||||||||||||||||||||||||||||

| Notional 1 | Maturities | Average Price 2 |

Fair Value of Assets (Liabilities) |

Notional 1 | Maturities | Average Contract Price 2 |

Fair Value of Assets (Liabilities) |

|||||||||||||||||||||||||||||||||

| Natural gas |

||||||||||||||||||||||||||||||||||||||||

| NYMEX swaps |

22 | 2019 – 2022 | $ | 4.26 | $ | (35 | ) | 27 | 2018 – 2022 | $ | 4.89 | $ | (54 | ) | ||||||||||||||||||||||||||

| AECO swaps 3 |

26 | 2019 | $ | 1.92 | $ | (25 | ) | – | – | – | $ | – | ||||||||||||||||||||||||||||

| 1 | In millions of British thermal units (“MMBtu”). |

| 2 | US dollars per MMBtu. |

| 3 | AECO swaps are only included in 2018 as a result of the Merger as described in Note 3. |

|

|

RECEIVABLES

|

Trade accounts receivable mainly consist of amounts owed to Nutrien by its customers, the largest individual customer being the related party, Canpotex.

| Accounting Policies | Accounting Estimates and Judgments | |||

| Trade accounts receivable are recognized initially at fair value and subsequently measured at amortized cost less provision for impairment of trade accounts receivable. When a trade account receivable is uncollectible, it is written off against the provision. Subsequent recoveries of amounts previously written off are credited to the consolidated statements of earnings.

Vendors may offer various incentives to purchase products for resale. Vendor rebates and prepay discounts are accounted for as a reduction of the prices of the suppliers’ products. Rebates based on the amount of materials purchased reduce cost of goods sold as inventory is sold. Rebates are offset based on sales volumes to cost of goods sold if the rebate has been earned based on sales volumes of products.

Rebates that are probable and can be reasonably estimated are accrued. Rebates that are not probable or estimable are accrued when certain milestones are achieved. Rebates not covered by binding agreements or published vendor programs are accrued when conclusive documentation of right of receipt is obtained. |

Determining when amounts are deemed uncollectible requires judgment.

Estimation of rebates can be complex in nature as vendor arrangements are diverse. The amount of the accrual is determined by analyzing and reviewing historical trends to apply negotiated rates to estimated and actual purchase volumes. Estimated amounts accrued throughout the year could also be impacted if actual purchase volumes differ from projected volumes. |

| NUTRIEN 2018 | 121 | ANNUAL REPORT |

IN MILLIONS OF US DOLLARS EXCEPT AS OTHERWISE NOTED

NOTE 14 RECEIVABLES CONTINUED

Supporting Information

| December 31, 2018 | December 31, 2017 | |||||||||||||||

| Trade accounts – third parties |

$ | 2,628 | $ | 314 | ||||||||||||

| – Canpotex (Note 30) |

208 | 82 | ||||||||||||||

| Less provisions for impairment of trade accounts receivable |

(90 | ) | (6 | ) | ||||||||||||

| 2,746 | 390 | |||||||||||||||

| Rebates |

169 | – | ||||||||||||||

| Income taxes (Note 9) |

248 | 24 | ||||||||||||||

| Other non-trade accounts |

179 | 75 | ||||||||||||||

| $ | 3,342 | $ | 489 | |||||||||||||

|

|

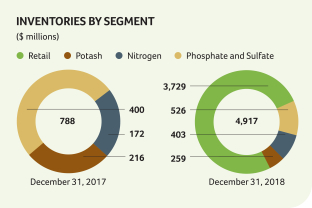

INVENTORIES

|

Inventories consist of Retail inventory (crop nutrients, crop protection products, seed and merchandise products) and products from the Potash, Nitrogen, and Phosphate and Sulfate segments in varying stages of the production process.

| Accounting Policies | Accounting Estimates and Judgments | |||||

| Inventories are valued monthly at the lower of cost and net realizable value. Costs are allocated to inventory using the weighted average cost method and include: direct acquisition costs, direct costs related to units of production and a systematic allocation of fixed and variable production overhead, as applicable.

Net realizable value is based on: |

Judgment is used to allocate production overhead to inventories and to determine net realizable value, including the appropriate measure and inputs of a combination of interrelated demand and supply variables. | |||||

| For products purchased for resale, finished products, intermediate products and raw materials |

For materials and supplies |

|||||

| • selling price of the finished product (in ordinary course of business);

• less the estimated costs of completion; and

• less the estimated costs to make the sale. |

• replacement cost. |

|||||

| A writedown is recognized if carrying amount exceeds net realizable value and may be reversed if the circumstances which caused it no longer exist. |

||||||

| NUTRIEN 2018 | 122 | ANNUAL REPORT |

FINANCIAL STATEMENTS AND NOTES

IN MILLIONS OF US DOLLARS EXCEPT AS OTHERWISE NOTED

|

|

PROPERTY, PLANT AND EQUIPMENT

|

The majority of the Company’s tangible assets are the buildings, machinery and equipment used to produce or distribute its products and render its services. These assets are depreciated over their estimated useful lives.

| Accounting Policies | Accounting Estimates and Judgments | |||||||||||

| Property, plant and equipment (which include certain mine development costs, pre-stripping costs and assets under construction) are carried at cost less accumulated depreciation and any recognized impairment loss.

Cost includes all expenditures directly attributable to bringing the asset to the location and installing it in working condition for its intended use, including:

• additions to, and betterments and renewals of, existing assets;

• borrowing costs incurred during construction using a capitalization rate based on the weighted average interest rate of the Company’s outstanding debt; and

• a reduction for income derived from the asset during construction.

Each component of an item of property, plant and equipment with a cost that is significant in relation to the item’s total cost is depreciated separately. When the cost of replacing part of an item of property, plant and equipment is capitalized, the carrying amount of the replaced part is derecognized. The cost of major inspections and overhauls is capitalized and depreciated over the period until the next major inspection or overhaul. Maintenance and repair expenditures that do not improve or extend productive life are expensed in the period incurred.

Environmental costs related to current operations are also capitalized if:

• property life is extended;

• capacity is increased;

• contamination from future operations is mitigated or prevented; or

• related to legal or constructive asset retirement obligations.

|

Judgment involves determining:

• costs, including income or expenses derived from an asset under construction, that are eligible for capitalization;

• timing to cease cost capitalization, generally when the asset is capable of operating in the manner intended by management, but also considering the circumstances and the industry in which the asset is to be operated, normally predetermined by management with reference to such factors as productive capacity;

• the appropriate level of componentization (for individual components for which different depreciation methods or rates are appropriate);

• repairs and maintenance that qualify as major inspections and overhauls; and