.2

| 2025 | ||

| MANAGEMENT’S | ||

| DISCUSSION AND | ||

| ANALYSIS | ||

.2

| 2025 | ||

| MANAGEMENT’S | ||

| DISCUSSION AND | ||

| ANALYSIS | ||

|

|

Overview | MD&A | Five-year highlights | Financial statements and notes | ||||||||||

|

|

Management’s discussion and analysis

MANAGEMENT’S DISCUSSION AND ANALYSIS

The following management’s discussion and analysis (“MD&A”) is the responsibility of management and is dated as of February 19, 2026.

The Board of Directors (“Board”) of Nutrien carries out its responsibility for review of this disclosure principally through its Audit Committee, comprised exclusively of independent directors. The Audit Committee reviews and, prior to its publication, recommends approval of this disclosure to the Board. The Board has approved this disclosure. The term “Nutrien” refers to Nutrien Ltd. and the terms “we”, “us”, “our”, “Nutrien” and “the Company” refer to Nutrien and, as applicable, Nutrien and its direct and indirect subsidiaries on a consolidated basis. This MD&A should be read together with the Company’s audited consolidated financial statements for the year ended December 31, 2025 (“consolidated financial statements”).

The generally accepted accounting principles (“GAAP”) we use are International Financial Reporting Standards (“IFRS”) as issued by the International Accounting Standards Board, unless otherwise stated.

This MD&A contains certain non-GAAP financial measures and ratios, which do not have a standard meaning under IFRS and, therefore, may not be comparable to similar measures presented by other issuers. Such non-GAAP financial measures and ratios include:

| • |

Adjusted EBITDA |

| • |

Adjusted net earnings and adjusted net earnings per share |

| • |

Effective tax rate on adjusted net earnings guidance |

| • |

Free cash flow |

| • |

Gross margin excluding depreciation and amortization per tonne – manufactured product |

| • |

Potash controllable cash cost of product manufactured per tonne |

| • |

Ammonia controllable cash cost of product manufactured per tonne |

| • |

Retail average working capital to sales and Retail average working capital to sales excluding Nutrien Financial |

| • |

Nutrien Financial adjusted net interest margin |

| • |

Retail cash operating coverage ratio |

| • |

Return on invested capital (“ROIC”) |

| • |

Adjusted net debt |

For definitions, further information and reconciliations of these measures to the most directly comparable measures under IFRS, see the “Non-GAAP financial measures” and “Other financial measures” sections.

This MD&A also contains forward-looking information and forward-looking statements. See the “Forward-Looking Statements” section.

All references to per share amounts pertain to diluted net earnings per share. Financial data in this MD&A is stated in millions of US dollars, which is the functional currency of Nutrien and the majority of its subsidiaries, unless otherwise noted. Information that is not meaningful is indicated by n/m. Information that is not applicable is indicated by n/a. See the “Other financial measures” and “Terms and Definitions” sections for certain definitions, abbreviations, measures and terms used in this MD&A.

Additional information relating to Nutrien (which, except as otherwise noted, is not incorporated by reference herein), including our Annual Information Form for the year ended December 31, 2025, can be found on SEDAR+ at sedarplus.ca and on EDGAR at sec.gov. The Company is a foreign private issuer under the rules and regulations of the US Securities and Exchange Commission (the “SEC”).

The information contained on or accessible from our website or any other website is not incorporated by reference into this MD&A or any other report or document we file with or furnish to applicable Canadian or US securities regulatory authorities.

| 6 Nutrien Annual Report 2025 | ||||

45

| Overview |

MD&A | Five-year highlights | Financial statements and notes |

| ||||||||||

|

|

Our approach to annual reporting

| 8 OUR COMPANY |

16 MARKET |

|||||||||||

| Outlines who we are as a company, where we operate, and our competitive advantages. Describes our strategy, how we delivered in 2025 and our focus going forward.

15 2026 Focus |

Describes factors and trends that influence the environment we operate in.

18 Market overview and fundamentals

|

|||||||||||

| 22 GOVERNANCE |

30 OUR OUTLOOK AND RESULTS |

|||||||||||

| Explains our core corporate governance principles and risk management process and outlines the key enterprise risks that may impact our performance and future operations.

23 Board and executive leadership

For more information on our corporate governance practices, see

For a more detailed discussion of our key enterprise risks and other risks that may have a material effect on us, refer to our 2025 Annual Information Form. |

Provides a review of our operating segments, including market outlook, 2026 guidance and highlights of our overall financial performance.

33 2026 Guidance and sensitivities

34 Operating segments and results

44 Financial results and capital management

56 Appendices |

|||||||||||

Nutrien Annual Report 2025 7

| Overview | MD&A | Five-year highlights | Financial statements and notes |

| ||||||||||

|

|

Our Company profile and

strategy

Nutrien is a leading global provider of crop inputs and services. We operate a world-class network of production, distribution and ag retail facilities that positions us to efficiently serve farmers. Our vision is to be the leading global agricultural solutions provider, delivering superior shareholder value through safe and sustainable operations. To achieve this vision, our strategy is anchored in three priorities: simplify and focus, operational excellence and a disciplined and intentional approach to capital allocation. This strategy is designed to create low-risk, structural free cash flow growth by leveraging our core competencies and to deliver reliable, growing cash returns to shareholders.

Nutrien Annual Report 2025 9

|

Overview | MD&A | Five-year highlights | Financial statements and notes |

| Global profile

Our upstream fertilizer manufacturing assets are primarily located in North America, with access to high-quality resources, lower-cost inputs and an extensive midstream distribution network to efficiently supply our customers. Our downstream Retail business serves farmers in key agricultural markets in North America, Australia and South America.

SCALE AND ADVANTAGED POSITION ACROSS THE AG VALUE CHAIN |

| #1 | #1 | #2 | ||||

| Global ag retailer | Global potash producer | North American nitrogen producer |

||||

| UNIQUE AND DIVERSE RELATIONSHIP WITH THE FARMER | ||||||

| >50 | >4,200 | >600,000 | ||||

| countries served by our products and services |

crop consultants | customer accounts | ||||

|

PROVEN FINANCIAL STRENGTH AND STABILITY

| ||||||

| World-class assets | High-quality earnings | Strong balance sheet and | ||||

| and market access | through the cycle | track record of returns | ||||

| 10 Nutrien Annual Report 2025 | ||||||

| Overview | MD&A | Five-year highlights | Financial statements and notes |

|

|

Global profile

| >1,800 |

6 | 12 | 6 | |||||

| Retail locations |

Potash mines | Nitrogen facilities | Phosphate facilities |

| Retail | Potash | Nitrogen | Phosphate | Proprietary products |

Australia

Nutrien Annual Report 2025 11

|

|

Overview | MD&A | Five-year highlights | Financial statements and notes | ||||||||||

|

|

Nutrien’s advantage

Our leading position across the ag value chain offers key competitive advantages and differentiation from our competitors. We focus on driving efficiencies across our network, enhancing our relationships with farmers, and strengthening our financial position and resilience.

|

|

|

|||

| SCALE AND ADVANTAGED POSITION ACROSS THE AG VALUE CHAIN

Our global reach provides competitive advantages to support higher upstream sales of manufactured fertilizer and proprietary products, drive supply chain efficiencies, optimize transportation and logistics and efficiently supply our customers. | ||||

|

|

UNIQUE AND DIVERSE RELATIONSHIP WITH THE FARMER

The farmer is at the heart of everything we do and our connection with our customers is unlike any other. Together we are working to improve on-farm productivity and foster innovation to address the demands of a growing global population. | |||

|

|

PROVEN FINANCIAL STRENGTH AND STABILITY

Our business is diversified, which enhances our earnings profile. Our downstream Retail business provides greater stability to our earnings base and counter-cyclical cash flow, while our low-cost upstream fertilizer production assets are positioned to generate significant cash flow, providing the ability to invest in our business and consistently return cash to our shareholders. |

| 12 Nutrien Annual Report 2025 | ||||

| Overview | MD&A | Five-year highlights | Financial statements and notes |

| ||||||||||

|

|

Nutrien’s strategy

Our strategy is centered on three priorities that span our upstream, midstream and downstream businesses.

|

|

||||

| SIMPLIFY AND FOCUS

Simplify our approach to focus on business activities that are core to our long-term vision and explore opportunities to exit non-core activities.

| ||||

|

|

OPERATIONAL EXCELLENCE

Enhance safety, increase operational efficiency and asset utilization, maximize cost savings and improve the quality of earnings. | |||

|

|

DISCIPLINED AND INTENTIONAL CAPITAL ALLOCATION

Optimize the sources and uses of our cash and prioritize sustaining safe and reliable operations, maintaining a strong and flexible balance sheet, strategically investing in our business and increasing cash returns to shareholders. |

| Nutrien Annual Report 2025 13 | ||||

|

|

Overview | MD&A | Five-year highlights | Financial statements and notes | ||||||||||

|

|

2025 Delivery

We delivered significant progress on our strategic priorities and 2026 performance targets.

| SIMPLIFY AND FOCUS

~$900M of total gross proceeds from asset divestitures since the fourth quarter of 2024

~$200M annual cost savings target surpassed through centralization of functions and retail optimizations

Controlled shutdown of Trinidad facility and ceased production at New Madrid upgrade facility

Initiated strategic review of Phosphate business |

OPERATIONAL EXCELLENCE

49% potash ore tonnes mined using automation – more than double 2023 level

92% ammonia operating rate1 – achieved through reliability improvements

Achieved Brazil margin-improvement plan despite challenging market conditions

87% Phosphate P2O5 operating rate for second half of 2025 – improving reliability and cost stewardship |

DISCIPLINED AND INTENTIONAL CAPITAL ALLOCATION

$1.6B in cash returns to shareholders – increase facilitated by ratable buyback program

$2.0B in capital expenditures, driven by risk-orientated approach to capital optimization, continuous improvement initiatives and a focus on leveraging existing assets to deliver organic growth

1.8x adjusted net debt to adjusted EBITDA2 – strengthening our balance sheet |

| 1 | Operating rate represents production volumes divided by production capacity (excluding Joffre and Trinidad facilities). |

| 2 | This is a capital management measure that includes non-GAAP components. See the “Non-GAAP financial measures” and “Other financial measures” sections. |

| 14 Nutrien Annual Report 2025 | ||||

| Overview | MD&A | Five-year highlights | Financial statements and notes |

| ||||||||||

|

|

2026 Focus

We are determined to build on our momentum and deliver stronger performance.

In 2026, we will continue driving the priorities that support structural free cash flow growth:

| • | With streamlined leadership and disciplined organization, we are lowering costs, increasing production through reliability and debottlenecks and enhancing margins by optimizing our midstream and retail network. |

| • | We are improving the resilience and efficiency of our portfolio, all while identifying additional opportunities to increase profitability. |

Enhance safety performance

| • | Safety is a core value – reinforce standards, strengthen accountability and continue building required capabilities to improve safety performance across our operations. |

Grow free cash flow

| • | Deliver upstream fertilizer sales volume growth from our low-cost North American asset base and increase Retail adjusted EBITDA through targeted growth initiatives. |

| • | Strengthen our midstream capabilities, including evaluation of west coast port facility. |

| • | Assess further growth pathways that leverage asset quality and inter-asset synergies to improve margins and reduce costs. |

Reliably increase cash returns to shareholders

| • | Maintain ratable share repurchases that align with free cash flow per share growth and reliable dividend per share increase. |

| • | Continue positioning the balance sheet as a strategic asset. |

Optimize portfolio

| • | Strengthen our world-class asset base, which is a competitive differentiator. |

| • | Complete the strategic review of alternatives for our Phosphate business, assess options for our Trinidad operations and evaluate each component of our Brazilian business to determine the optimal way to participate in the long-term growth in this market. |

| • | Progress optimizing capital on our highest-quality assets and resilient earnings streams. |

| GROWING FREE CASH FLOW INTO 2026 |

| Upstream manufactured sales volumes guidance

(million tonnes) |

Downstream adjusted EBITDA guidance

($ billions)

| |

|

|

1 Guidance provided in our news release dated February 18, 2026.

2 See the “Forward-looking statements” section.

3 Guidance assumes no production from Trinidad and New Madrid facilities in 2026.

| Nutrien Annual Report 2025 15 | ||||

|

|

Overview | MD&A | Five-year highlights | Financial statements and notes | ||||||||||

|

|

Market environment

ENVIRONMENT

We operate in a rapidly changing world and must anticipate and adapt to our market environment. We seek to understand global markets and broader trends that influence and shape our operational landscape. This understanding helps us to seize new opportunities as they emerge and better identify the risks that could impact our ability to deliver on our strategy.

16 Nutrien Annual Report 2025

| Overview | MD&A | Five-year highlights | Financial statements and notes |

| ||||||||||

|

|

Market environment

Nutrien Annual Report 2025 17

|

|

Overview | MD&A | Five-year highlights | Financial statements and notes | ||||||||||

|

|

Market overview and fundamentals

MARKET OVERVIEW AND FUNDAMENTALS

| Rising global food demand

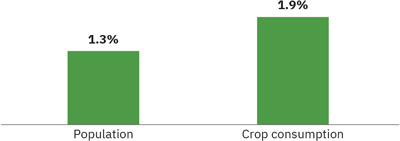

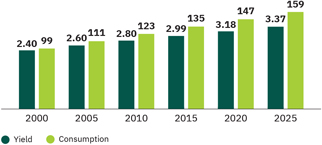

From 2000 to 2025, global food consumption growth outpaced population growth. This increase was driven largely by higher per-capita consumption of animal products, fruits, and oils, particularly in emerging economies where rising incomes and urbanization reshape diets. Looking ahead, as global population continues to rise, arable land per capita is expected to decline. These dynamics underscore the mounting challenge of food security, creating long-term opportunities for farmers and input providers to meet escalating demand amid geopolitical volatility that continues to influence trade flows and commodity pricing. |

Growth in global population vs. crop consumption1,2 (2000–2025 CAGR)

| |

| Driving the need for farming improvements

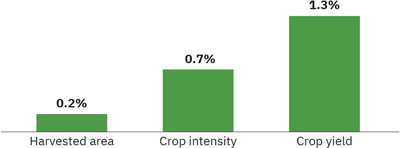

To meet rising consumption, farming practices that include crop inputs, technology and agronomy have evolved significantly, enabling farmers to produce more from finite land. Crop yield, measured as output per unit of land, has been a major contributor to aggregate production growth. Crop intensity, measured as higher rotation of crops each year, has also contributed. Lastly, increases in cropping area have played an important role in meeting historical food consumption growth; however, availability of arable land will limit future growth. This trend underscores the importance of productivity gains as crucial to meet the needs of a growing population. |

Crop growth drivers (2000–2025 CAGR)

| |

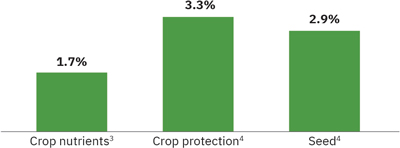

| Supported by critical role of crop inputs for growers

Modern agriculture relies on a tightly integrated set of inputs that include balanced crop nutrition, crop protection, improved seed genetics and agronomy advancements. Collectively, these advancements support yield across seasons by enhancing plant resilience against pests, weeds and environmental stress.

Potash, nitrogen and phosphate are essential to crop production and a cornerstone of agricultural output. Each nutrient plays a distinct role: potash supports water uptake and efficiency of other nutrients, nitrogen improves crop yield and quality and phosphate aids root development. |

Growth in key crop inputs (2000–2024 CAGR)

| |

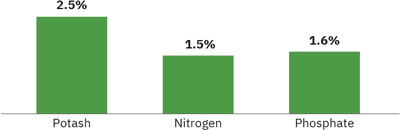

| Together, they enable farmers to improve crop intensity and achieve higher yields. Looking ahead, fertilizer demand is expected to grow steadily – as global food, feed and fuel demand grows, the need for crop inputs and agronomic services remains a key growth engine for the agricultural supply chain.

1 Global data excludes China. 2 Crop consumption data includes grains, oilseeds, pulses, roots and tubers. 3 Based on annual figures represented on a tonnes basis. 4 Reported data is calculated on the basis of size of global market in $ billions. |

Growth in crop nutrients (2000–2024 CAGR)

Source: Nutrien estimates based on CRU, IFA, IHS, FAO STAT, S&P, USDA | |

| 18 Nutrien Annual Report 2025 | ||||

| Overview | MD&A | Five-year highlights | Financial statements and notes |

| ||||||||||

|

|

Market overview and fundamentals

| Agriculture and retail markets | ||

| $127B

2025 crop input sales1 |

| |

| Crop nutrients | ||

| ~74.5Mmt

2025 global potash (KCl) demand |

| |

| ~167Mmt

2025 global nitrogen (N) demand |

| |

| ~52Mmt

2025 global phosphate (P2O5) demand |

| |

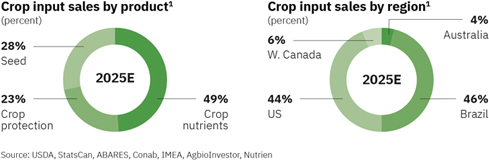

| 1 | Represents total market sales of seed, fertilizer and crop protection products in the US, Canada, Australia and Brazil. |

| Nutrien Annual Report 2025 19 | ||||

|

|

Overview | MD&A | Five-year highlights | Financial statements and notes | ||||||||||

|

|

Market overview and fundamentals

The agriculture retail industry is highly fragmented in most of the major markets in which we operate, and is primarily composed of small and medium-sized competitors. Scale, reliability of supply and the ability to provide innovative products and solutions, including digital offerings, are increasingly important to farmers.

In North America, the primary crops grown include corn, soybeans, wheat, canola and cotton. It is a more mature market, with farmers who are leveraging advanced agriculture tools and are willing and able to invest in high-value products and services. In Australia, our customers require a full suite of crop production inputs and solutions for livestock, water and irrigation services given the more mixed nature of farm operations. Brazil is one of the world’s largest and fastest-growing agriculture markets. It is currently the largest soybean producer and the third largest producer of corn and cotton globally.

Our Proprietary products differentiate our crop input offerings and deliver stronger agronomic outcomes, while contributing to an improved margin profile. We also provide flexible financing solutions aligned with growers’ seasonal cash-flow needs, helping them obtain essential crop inputs and supporting our product and service sales.

Agricultural and retail markets are influenced by short and long-term factors ranging from acreage and crop yield, to crop prices and grower cash margins, to government incentives and trade-flows. Global grains ending stocks-to-use ratio is a key indicator to understand supply tightness and explains price trends for key crops.

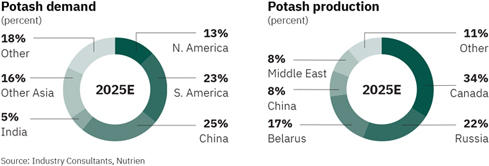

Potash strengthens root systems, supporting water uptake and drought and disease tolerance, and increases the efficiency of other nutrients. Potash demand growth is driven by increasing nutrient requirements of higher-yielding crops and improving soil fertility practices, particularly in emerging markets where potash has been historically under-applied and crop yields lag.

High-quality potash reserves in significant quantities are limited to a small number of countries. Canada has the largest known global potash capacity, accounting for approximately 40 percent of the total. Another 35 percent of the world’s potash production capacity is held by Russia and Belarus, making them the next major exporting countries after Canada.

Building new production capacity requires significant capital and time to bring online. The expected cost for a greenfield project, including infrastructure, is over $2,300 per tonne and requires a minimum of 10 years.1 Brownfield projects have a significant per-tonne capital cost advantage over greenfield projects.

Most major potash-consuming countries in Asia and Latin America have limited production capability and rely on imports to meet their needs. Trade typically accounts for approximately three-quarters of demand for potash, resulting in a globally diversified marketplace.

Inflation in operating and logistics costs has increased the short run marginal cost of potash supply and higher capital costs have also impacted the long-run marginal cost.

| Yield vs. nutrient consumption2

(tonnes/hectare, million tonnes) |

Global potash demand

(million tonnes KCl) | |||

|

| |||

| Source: USDA, IFA, CRU, Nutrien | Source: IFA, Argus, CRU, SPGCI, Nutrien | |||

| 1 | KCl conventional potash mine of 3 million tonnes in Saskatchewan, Canada. Cost includes rail, utility systems, port facilities and, if applicable, cost of deposit. |

| 2 | Global data excludes China. |

| 20 Nutrien Annual Report 2025 | ||||

| Overview | MD&A | Five-year highlights | Financial statements and notes |

| ||||||||||

|

|

Market overview and fundamentals

Nitrogen

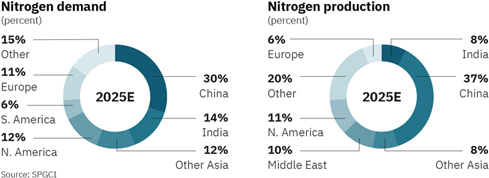

Nitrogen is an essential crop nutrient and is a fundamental building block of plant proteins that improves both crop yield and quality. The necessity of nitrogen for crop yield supports a strong and growing demand for nitrogen fertilizers. Additionally, nitrogen is used as an input in many industrial processes, both as a chemical feedstock and as an inert process gas.

Production of nitrogen products is the most geographically diverse of the three primary crop nutrients due to the widespread availability of hydrogen sources. Access to reliable and competitively priced energy feedstock supply, commonly natural gas, is an important driver of profitability. Geopolitical events continue to create additional volatility in certain global energy markets. North American nitrogen producers currently have an advantaged cost position due to the relatively low price of natural gas compared to competitors in Europe and Asia.

The US is the third largest nitrogen-producing country and remains one of the largest importers of nitrogen products. China and India are the largest consumers of nitrogen fertilizer, accounting for approximately 45 percent of the world’s consumption.

Phosphate

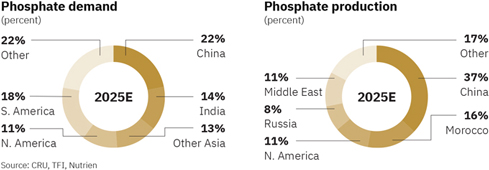

Phosphorus is essential to all living things and is key to energy reactions in plants, particularly photosynthesis, and is vital to plant growth. Additionally, phosphate is used as an input in animal feed, food ingredients and industrial processes.

Phosphate rock is found in significant quantity and quality in only a handful of geographic locations, with only 11 major phosphate-producing countries. Due to the concentration of deposits, the majority of recent capacity additions have come from existing producers in North Africa, the Middle East and China.

China is the world’s largest producer of phosphate, and its trade policy has a major impact on the global market. To illustrate, in 2025, Chinese DAP/MAP exports were down approximately 40 percent, compared to normal historical levels as a result of export restrictions that prioritized domestic use.

India and Brazil are the largest importers of phosphate fertilizers, with limited domestic production. In more mature markets like North America, we have seen continued demand growth for phosphate fertilizers that incorporate secondary nutrients and micronutrients like Nutrien’s MAP+MST product.

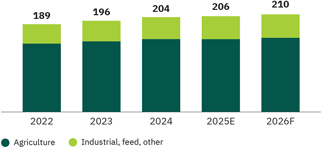

| Global ammonia demand

(million tonnes NH3) |

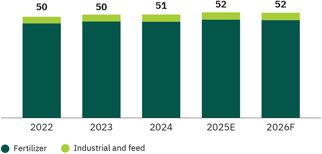

Global P2 O5 demand

(million tonnes P2O5) | |||

|

| |||

| Source: SPGCI, CRU, Argus, Nutrien | Source: CRU, TFI, Industry Consultants, Nutrien | |||

| Nutrien Annual Report 2025 21 | ||||

|

|

Overview | MD&A | Five-year highlights | Financial statements and notes | ||||||||||

|

|

Governance and key enterprise risks

GOVERNANCE AND

KEY ENTERPRISE RISKS

We embed strong corporate governance systems and principles across our business to ensure the interests of shareholders and other stakeholders remain central to our decision making. Our governance supports value preservation and long-term value creation by ensuring that our key enterprise risks and opportunities are appropriately identified and addressed. Nutrien’s corporate governance structure includes policies and processes that clearly define the respective roles of the Board and the Executive Leadership Team (“ELT”). Our Board provides oversight of corporate strategy execution and risk management.

22 Nutrien Annual Report 2025

| Overview |

MD&A | Five-year highlights | Financial statements and notes |

| ||||||||||

|

|

Governance and key enterprise risks

BOARD OF DIRECTORS

|

|

|

|

|

| |||||

| Russell Girling |

Ken Seitz |

Christopher Burley |

Maura Clark |

Michael Hennigan |

Miranda Hubbs | |||||

| Chair |

President and Chief |

Director |

Director |

Director |

Director | |||||

| Executive Officer |

||||||||||

|

|

|

|

|

| |||||

| Raj Kushwaha |

Julie Lagacy |

Consuelo Madere |

Keith Martell |

Aaron Regent |

Nelson L.C. Silva | |||||

| Director |

Director |

Director |

Director |

Director |

Director | |||||

EXECUTIVE LEADERSHIP TEAM

|

|

|

|

|

| |||||

| Ken Seitz |

Noralee Bradley |

Andrew Kelemen |

Chris Reynolds |

Mark Thompson |

Sarah Walters | |||||

| President and Chief |

Executive Vice |

Executive Vice |

Executive Vice |

Executive Vice |

Executive Vice | |||||

| Executive Officer |

President, External |

President, Corporate |

President, Global Sales |

President and Chief |

President, IT and | |||||

| Affairs, Chief Legal |

Development and |

Financial Officer |

Chief People Officer | |||||||

| Officer and Corporate |

Chief Strategy Officer |

|||||||||

| Secretary |

||||||||||

Nutrien Annual Report 2025 23

|

|

Overview | MD&A | Five-year highlights | Financial statements and notes | ||||||||||

|

|

Risk governance

Risk management is an integral part of doing business and our Board is responsible for overseeing the execution and alignment of Nutrien’s corporate strategy and risk management processes.

Nutrien’s ELT has the responsibility of ensuring the Company’s principal risks are being appropriately identified, assessed and addressed. Management keeps the Board and each of the Board committees regularly apprised of risks and developments relevant to their mandates.

Responsibility and accountability for risk management are embedded in all levels of our organization, and we strive to integrate risk management into key decision-making processes and strategies. By proactively assessing risk across our organization, we aim to effectively manage the risks that could have an impact on our ability to achieve our strategic objectives and deliver long-term value.

Role of the Board committees

While the Board as a whole oversees our strategy and risk management processes, each Board committee has oversight over business topics and certain risk areas relevant to their committee mandate. More information can be found in Nutrien’s Board and Board committee charters on our website at nutrien.com.

| Board/Board Committee

|

Oversight includes the following business topics or risk areas

| |||

| Board of Directors |

Corporate strategy |

Risk management | ||

| Oversight of safety, health, environmental and security matters |

Human resources and compensation | |||

| Corporate governance and compliance | ||||

| Safety Committee |

Health and safety risks |

Environmental risks | ||

| Crisis and emergency response management |

Process safety and operational integrity | |||

| Incident reporting and response |

Regulatory and compliance risk | |||

| Safety culture and performance | ||||

| Audit Committee |

Accounting and financial reporting |

Whistleblower, ethics and compliance | ||

| Internal controls and disclosure controls |

Financial risk management | |||

| Internal audit |

External audit | |||

| Corporate Governance & |

Corporate governance |

Board evaluations | ||

| Nominating Committee |

Board composition |

Activities that maintain or enhance the ability to create value over the long term (including oversight of climate-related risks) | ||

| Director compensation | ||||

| Director orientation and continuing education | ||||

| Stakeholder and Indigenous relations |

Cybersecurity, artificial intelligence (“AI”) and | |||

| data governance | ||||

| Related-party transactions | ||||

| Human Resources & |

Executive compensation |

Human capital management, including the Company’s Indigenous Strategy as it relates to Indigenous employment and human resources | ||

| Compensation Committee |

Incentive plan design and performance metrics | |||

| Succession planning | ||||

| Talent management and leadership |

Learning and development | |||

| development |

||||

| 24 Nutrien Annual Report 2025 | ||||

| Overview | MD&A | Five-year highlights | Financial statements and notes |

| ||||||||||

|

|

Risk management process

Risk management is embedded in our strategy and business processes to support informed decision making and responsible stewardship of resources. Our centralized Enterprise Risk Management program is guided by a global risk management framework. The framework promotes consistent and integrated application of risk management principles and practices across our organization.

Nutrien’s operating segments and corporate functions use our global risk management framework to identify, assess and develop mitigation actions for risks that may affect their strategy, operations or future performance. Annually, we conduct a top-down enterprise risk assessment alongside a bottom-up risk assessment, resulting in a consolidated view of our risk profile.

Management evaluates risk holistically to understand Nutrien’s overall risk landscape and the interconnections among risks. A comprehensive view of enterprise risks is evaluated by our ELT and senior leaders, and our key enterprise risks are presented to the Board at least annually.

| Nutrien Annual Report 2025 25 | ||||

|

|

Overview | MD&A | Five-year highlights | Financial statements and notes | ||||||||||

|

|

Key enterprise risks

We characterize a key enterprise risk as an individual risk, or combination of risks, that could materially affect our ability to achieve our strategic objectives, deliver shareholder value or maintain operational and financial stability. Our key enterprise risks presented below represent our most significant exposures; however, we continue to be exposed to other important general business, financial and operational risks.

| 1 | COMPETITION AND MACROECONOMIC CONDITIONS |

| Description

Changes in global macroeconomic conditions and market dynamics – including tariffs, trade or export restrictions, market volatility, geopolitical events, increased price competition or new competitors or major shifts in agriculture production or consumption – could lead to a sustained environment of reduced demand for our products, create lower or more volatile commodity prices or increase costs and thereby negatively affect our short- and long-term profitability. |

Risk management approach

We operate across the ag value chain with a favorable cost structure and a diversified portfolio of products and services that help minimize the impact of changing market conditions. Additionally, we maintain a strong and flexible balance sheet and pursue a clearly identified strategy that aims to enhance key advantages of our core business and drive operational excellence.

See page 18 of this report for more information on our market environment. |

| 2 | CHANGING REGULATIONS |

| Description

Changes in laws, regulations or government policies – including those relating to the environment, climate change, data privacy, health and safety, taxes and royalties, or from pressure on lawmakers and regulators to address concerns related to fertilizer and food prices – can affect how we operate. New requirements may limit our ability to produce or sell certain products, reduce our efficiency, increase costs for materials, energy, transportation or compliance or require upgrades to our facilities. These and other factors could impact our strategy, operations, financial results or reputation. |

Risk management approach

We maintain regular engagement with governments, regulators and key industry associations through our Government & External Affairs Team. This helps us to stay informed about policy and regulatory developments, anticipate their impacts and work with industry partners to support outcomes that enable our long-term success. We also use cross-functional compliance programs and internal reviews to assess potential impacts and ensure our operations and products meet evolving requirements. |

| 26 Nutrien Annual Report 2025 | ||||

| Overview | MD&A | Five-year highlights | Financial statements and notes |

| ||||||||||

|

|

Key enterprise risks

| 3 | POLITICAL, ECONOMIC AND SOCIAL INSTABILITY |

| Description

Nutrien operates a global business with significant operations in Canada and the US and additional operations in Australia, South America, Trinidad and parts of Europe. Operating internationally exposes us to political, economic and social instability that can affect how we do business.

These risks include, but are not limited to, restrictions on moving money out of certain countries, inflation or government actions aimed at controlling inflation, currency exchange rate fluctuations between the US dollar and foreign currencies, labor disruptions, competitive restrictions and changes to or loss of important agreements or permits. We may also be affected by tariffs, sanctions, embargoes, trade barriers, exchange controls,forced divestitures or broad geopolitical events such as military conflict. Shifts in political or regulatory environments can disrupt our operations or ability to do business, affect the value of our assets and impact our financial performance. |

Risk management approach

Our Government & External Affairs Team engages regularly with governments, regulators, industry associations and other stakeholders in the regions where we operate or plan to operate. We factor political and country-specific risks into our capital investment and project decisions and limit our exposure in jurisdictions where we believe the risk is too high. We also monitor global political and regulatory developments and trends to understand potential impacts on our business. |

| 4 | AGRICULTURAL CHANGES AND TRENDS |

| Description

The agricultural landscape is impacted by factors such as ongoing farm and industry consolidation, shifts in farmer demographics, new technologies, evolving sustainability practices, changing government programs and policies, trade disputes and trade tariffs, climate impacts and broader social trends. Many of these factors vary by region and can affect long-term demand for our products and services and as a result may adversely affect our strategy and our financial performance. |

Risk management approach

Our downstream Retail network gives us direct insight into what farmers need, allowing us to anticipate emerging trends early and respond quickly. We focus on delivering solutions that help farmers manage challenges, including offering financing solutions through Nutrien Financial, expanding our portfolio of proprietary products and investing in digital tools, agronomic expertise and technologies that improve productivity and on-farm decision making. |

| Nutrien Annual Report 2025 27 | ||||

|

|

Overview | MD&A | Five-year highlights | Financial statements and notes | ||||||||||

|

|

Key enterprise risks

| 5 | SUPPLY CHAIN DISRUPTION |

| Description

Our ability to produce and deliver products depends on reliable inbound and outbound supply chains. Disruptions can affect our access to key materials or limit our ability, as well as the ability of third parties we depend on, to transport products to customers on time. Geopolitical conflicts, regulatory changes, sanctions, tariffs, labor disputes, pandemics and extreme weather events can create supply chain challenges and delays and/or limit our future ability to sell or distribute our products when needed. These challenges can negatively affect our business and financial performance. |

Risk management approach

Our scale and advantaged position across the ag value chain provides us the flexibility to optimize our operations and distribution network in response to supply chain disruptions. We have an extensive and diverse transportation and storage network that helps us navigate logistical challenges. We also maintain a diverse supplier base that we regularly review to ensure we have reliable access to critical feedstocks and materials for our operations. |

| 6 | CYBERSECURITY THREATS |

| Description

Nutrien relies on information technology, operational control systems and third-party or cloud-based platforms to run our business. As our dependence on these systems grows, so does our exposure to increasingly sophisticated cyber threats, including those driven by AI. Cybersecurity risks can include attacks on information technology and infrastructure by hackers, ransomware, viruses, unauthorized access to confidential or personal information, disruptions to computer control systems and broader business or supply chain interruptions. A cyber incident could lead to operational downtime, higher security or insurance costs, reputational harm, legal or third-party claims and other impacts that could negatively affect our business and financial performance. |

Risk management approach

Our Global Information Management and Cyber Security Team, supported by third-party specialists, oversees our network security and helps coordinate incident response when needed. We promote strong cybersecurity awareness across the Company through our cybersecurity policies, controls and best practices. All new information technology systems undergo threat and risk assessments, and our incident response processes are reinforced by external support. We also run regular phishing simulations and targeted cybersecurity and incident response training to help reduce vulnerabilities. |

| 7 | SAFETY, HEALTH AND ENVIRONMENT |

| Description

Our operations involve safety, health and environmental risks inherent in mining, manufacturing and the transportation, storage and distribution of our products. These risks can lead to injuries or fatalities and may affect air quality, biodiversity, water resources or local ecosystems near our sites. Any such incident could disrupt our operations and have a negative impact on our financial performance and reputation. |

Risk management approach

We follow regulatory, industry and internal safety, health and environmental standards, supported by strong governance and oversight. We have structured systems to prevent and respond to incidents, and we conduct regular security and vulnerability assessments. Across our operations, we maintain crisis communication and emergency response programs, along with environmental monitoring and controls, including independent reviews of key containment structures. |

| 28 Nutrien Annual Report 2025 | ||||

| Overview | MD&A | Five-year highlights | Financial statements and notes |

| ||||||||||

|

|

Key enterprise risks

| 8 | TALENT AND ORGANIZATIONAL CULTURE |

| Description

Our ability to attract, develop and retain skilled employees, as well as maintain the programs, structure and culture that support them, is essential to our growth and performance. Increasing competition for talent, particularly in certain regions or for specialized roles, can create challenges in hiring or retaining employees and increase costs and reduce productivity. Our investment in training also makes our employees valuable to competitors. If we are unable to sustain an engaging workplace or retain the talent needed to support our operations and future growth, our operations and financial performance could be negatively affected. |

Risk management approach

Our Talent Attraction and Sourcing Team works to build a diverse, skilled workforce, while our development programs support employee growth and engagement. We use a structured succession process to identify critical roles and strengthen our internal and external talent pipelines. Our compensation and incentive programs are competitive, performance-based and aligned with our purpose-driven culture. |

| 9 | CAPITAL REDEPLOYMENT |

| Description

We may be unable to deploy capital to efficiently achieve sustained growth, effectively execute on opportunities or meet stakeholder expectations. This risk may arise from market conditions, limited investment opportunities or other factors. Additionally, deploying capital in a manner that is inconsistent with our strategic priorities could negatively impact our returns, operations, reputation, access to or cost of capital or result in potential asset impairments. |

Risk management approach

Our capital allocation is guided by a disciplined framework and supported by Nutrien’s diversified earnings base. We focus on sustaining safe and reliable operations, preserving balance sheet strength and flexibility, deploying capital to strategic investments and providing meaningful returns to our shareholders. Additionally, our centralized Enterprise Capital Team helps to ensure consistent project evaluation and an enterprise-wide view of capital project decisions. |

| 10 | STAKEHOLDER SUPPORT |

| Description

Nutrien’s reputation and stakeholder relationships are critical to our ability to operate and execute our strategy and can be affected by actual or perceived actions across our business and supply chain. Any erosion of trust could impair our ability to execute on our business plans. It could also negatively impact our ability to produce or sell our products, lead to reputational and financial losses or negatively impact our access to or cost of capital or trigger shareholder action. |

Risk management approach

Our Investor Relations and Government & External Affairs teams regularly engage with key stakeholders to identify their concerns and convey the long-term value proposition of our business. We are active in industry associations, implement our community relations and investment initiatives across our operations and have a focused Indigenous Relations engagement strategy. Our overarching strategy is designed to address and support the areas most important to our stakeholders. |

| Nutrien Annual Report 2025 29 | ||||

|

|

Overview | MD&A | Five-year highlights | Financial statements and notes | ||||||||||

|

|

Our outlook and results

RESULTS

Nutrien has four reportable operating segments: Retail, Potash, Nitrogen and Phosphate. The downstream Retail segment distributes crop nutrients, crop protection products, seed and merchandise and provides services, including financing, directly to farmers through a network of retail locations in North America, Australia and South America. The upstream Potash, Nitrogen and Phosphate segments are differentiated by the chemical nutrient contained in the products that each produces.

30 Nutrien Annual Report 2025

| Overview |

MD&A | Five-year highlights | Financial statements and notes |

| ||||||||||

|

|

Our outlook and results

Adjusted EBITDA is the primary profit measure used to evaluate the segments’ performance as it excludes the impact of non-cash impairments and impairment reversals and other costs that are centrally managed by our corporate function. Refer to Note 3 to the consolidated financial statements for details.

Net sales (sales less freight, transportation and distribution expenses) is the primary measure used in planning and forecasting in the Potash, Nitrogen and Phosphate operating segments.

Nutrien Annual Report 2025 31

|

|

Overview | MD&A | Five-year highlights | Financial statements and notes | ||||||||||

|

|

Market outlook

Agriculture and retail markets

| • | Higher global grain and oilseed production in 2025 increased stocks-to-use ratios towards historical average levels and led to significant nutrient removal from the soil. Strong demand for food, feed and biofuel uses is expected to drive continued need for higher global crop production and related crop inputs. |

| • | We expect total US crop acres in 2026 to be consistent with 2025 levels and project corn plantings of 94 to 96 million acres and soybean plantings of 84 to 86 million acres. This acreage outlook, combined with a compressed fertilizer application season in the fall of 2025, is expected to support increased crop input demand in the first half of 2026. |

| • | In Brazil, soybean production is expected to set another record in 2026, with harvest currently underway, and we anticipate a 3 to 5 percent increase in safrinha corn plantings. Growth in planted area is expected to support crop input demand; however, weaker affordability is expected to result in just-in-time purchases and a continued shift to lower analysis nitrogen and phosphate products. |

| • | In Australia, improved weather compared to the first half of 2025 is expected to support crop input demand and strong livestock prices to support sales of Retail products and services. |

Crop nutrient markets

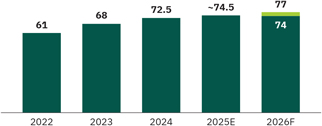

| • | Global potash shipments increased to approximately 74.5 million tonnes in 2025, primarily driven by strong demand in Southeast Asia. We expect a fourth consecutive year of growth in 2026, with total global potash shipments ranging between 74 and 77 million tonnes. Demand is supported by the need to replenish soil nutrients following a record crop, favorable relative affordability and low inventory levels in key markets such as China and Brazil. We anticipate relatively tight fundamentals throughout 2026, as trend line demand growth is testing existing global operating and supply chain capabilities. |

| • | Global nitrogen demand is expected to grow in line with historical rates, driven by increasing use in agricultural growth markets such as Asia and Latin America. Global ammonia markets remain tight due to project delays and plant outages. Global urea markets have strengthened in the first quarter of 2026 due to strong seasonal demand from India, North America and Brazil and geopolitical uncertainties impacting supply. |

| • | Global phosphate markets eased in the fourth quarter of 2025 due to lower demand related to weaker affordability relative to potash and nitrogen. Phosphate markets have strengthened in the first quarter of 2026 due to Chinese export restrictions and elevated input costs. |

| 32 Nutrien Annual Report 2025 | ||||

| Overview | MD&A | Five-year highlights | Financial statements and notes |

| ||||||||||

|

|

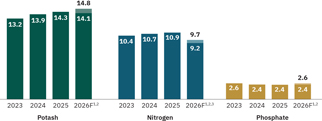

2026 Guidance and sensitivities

|

|

2026 Guidance ranges1,2 as of

February 18, 2026

|

|

||||||||||

| ($ billions, except as otherwise noted)

|

|

Low

|

|

|

High

|

|

|

2025 Actual

|

| |||

|

Retail adjusted EBITDA |

|

1.75 |

|

|

1.95 |

|

|

1.74 |

| |||

| Potash sales volumes (million tonnes)3 |

14.1 | 14.8 | 14.25 | |||||||||

| Nitrogen sales volumes (million tonnes)3 |

9.2 | 9.7 | 10.89 | |||||||||

| Phosphate sales volumes (million tonnes)3 |

2.4 | 2.6 | 2.36 | |||||||||

| Depreciation and amortization |

2.4 | 2.5 | 2.4 | |||||||||

| Finance costs |

0.65 | 0.75 | 0.7 | |||||||||

| Effective tax rate on adjusted net earnings (%)4 |

24.0 | 26.0 | 24.9 | |||||||||

| Capital expenditures5 |

2.0 | 2.1 | 2.0 | |||||||||

| 1 | Guidance provided in our news release dated February 18, 2026. |

| 2 | See the “Forward-looking statements” section. |

| 3 | Manufactured product only. |

| 4 | This is a non-GAAP financial measure. See the “Non-GAAP financial measures” section. |

| 5 | Comprised of sustaining capital expenditures, investing capital expenditures and mine development and pre-stripping capital expenditures, which are supplementary financial measures. See the “Other financial measures” section. |

2026 SENSITIVITIES

|

|

Effect on1

|

| ||||||

| ($ millions, except EPS amounts)

|

|

Adjusted EBITDA

|

|

|

Adjusted EPS

|

4

| ||

| $25 per tonne change in potash net selling prices |

± 280 | ± 0.45 | ||||||

| $25 per tonne change in ammonia net selling prices2 |

± 35 | ± 0.05 | ||||||

| $25 per tonne change in urea and ESN® net selling prices |

± 65 | ± 0.10 | ||||||

| $25 per tonne change in solutions, nitrates and sulfates net selling prices |

± 135 | ± 0.20 | ||||||

| $1 per MMBtu change in NYMEX natural gas price3 |

± 180 | ± 0.30 | ||||||

| 1 | See the “Forward-looking statements” section. |

| 2 | Excludes Trinidad. |

| 3 | Nitrogen related impact. |

| 4 | Based on shares outstanding as at December 31, 2025. |

| Nutrien Annual Report 2025 33 | ||||

|

|

Overview | MD&A | Five-year highlights | Financial statements and notes | ||||||||||

|

|

Results

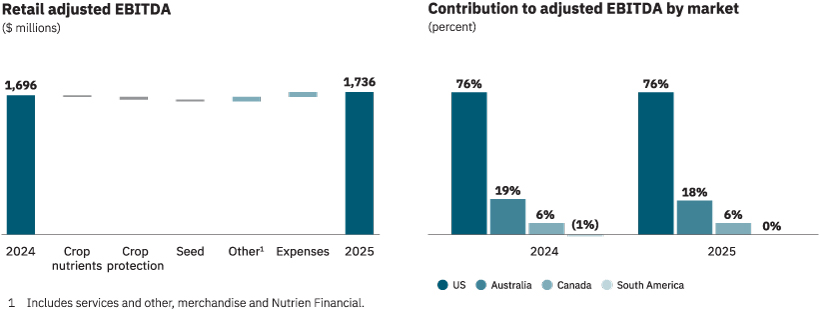

2025 RETAIL OPERATING SEGMENT AND RESULTS

Our Retail network of over 1,800 locations provides the reach and flexibility to reliably serve our grower customers. We offer a comprehensive portfolio of value-added products, including crop nutrients, crop protection products, seed and merchandise, and provide services, including financing. Over 4,200 crop consultants support our customers with crop planning, seed selection, soil sampling, variable-rate fertilizer application and crop monitoring.

We own and operate eight formulation facilities focused on manufacturing proprietary crop nutrient and crop protection products. As a leading provider of crop nutritionals, including biostimulants, our portfolio includes approximately 1,700 innovative proprietary crop nutrient, crop protection and seed products. Our proprietary offering generates higher margins for Nutrien and enhances crop production efficiency and profitability for farmers.

Retail adjusted EBITDA increased to $1.74 billion in 2025 due to lower operating expenses from our cost savings initiatives, stronger proprietary products gross margin and disciplined execution of our Brazil margin-improvement plan. We continue to simplify our business and deliver earnings growth through proven organic initiatives.

| ($ millions, except as otherwise noted) | 2025 | 2024 | % Change | |||||||||

| Sales |

17,620 | 17,832 | (1 | ) | ||||||||

| Cost of goods sold |

13,017 | 13,211 | (1 | ) | ||||||||

| Gross margin |

4,603 | 4,621 | – | |||||||||

| Adjusted EBITDA1 |

1,736 | 1,696 | 2 | |||||||||

| 1 | See Note 3 to the consolidated financial statements. |

| Sales | Gross margin | |||||||||||||||

| ($ millions) | 2025 | 2024 | 2025 | 2024 | ||||||||||||

| Crop nutrients |

7,285 | 7,211 | 1,424 | 1,444 | ||||||||||||

| Crop protection products |

6,105 | 6,313 | 1,590 | 1,622 | ||||||||||||

| Seed |

2,128 | 2,235 | 408 | 431 | ||||||||||||

| Services and other |

944 | 918 | 750 | 716 | ||||||||||||

| Merchandise |

875 | 897 | 148 | 150 | ||||||||||||

| Nutrien Financial |

376 | 361 | 376 | 361 | ||||||||||||

| Nutrien Financial elimination1 |

(93 | ) | (103 | ) | (93 | ) | (103 | ) | ||||||||

| Total |

17,620 | 17,832 | 4,603 | 4,621 | ||||||||||||

| 1 | Represents elimination of the interest and service fees charged by Nutrien Financial to Retail branches. |

Supplemental data

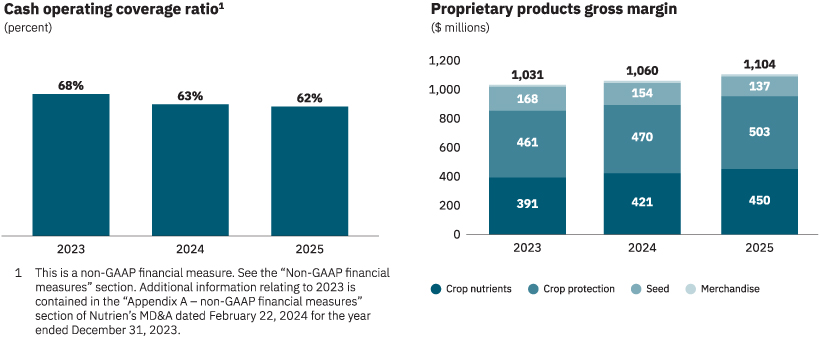

| Gross margin | % of product line1 | |||||||||||||||

| ($ millions, except as otherwise noted) | 2025 | 2024 | 2025 | 2024 | ||||||||||||

| Proprietary products |

||||||||||||||||

| Crop nutrients |

450 | 421 | 32 | 29 | ||||||||||||

| Crop protection products |

503 | 470 | 32 | 29 | ||||||||||||

| Seed |

137 | 154 | 34 | 36 | ||||||||||||

| Merchandise |

14 | 15 | 9 | 10 | ||||||||||||

| Total |

1,104 | 1,060 | 24 | 23 | ||||||||||||

| 1 | Represents percentage of proprietary product margins over total product line gross margin. |

34 Nutrien Annual Report 2025

| Overview | MD&A | Five-year highlights | Financial statements and notes |

| ||||||||||

|

|

Results

| Sales volumes (tonnes – thousands) |

Gross margin / tonne (dollars) |

|||||||||||||||

|

|

2025 | 2024 | 2025 | 2024 | ||||||||||||

| Crop nutrients |

||||||||||||||||

| North America |

8,502 | 8,547 | 143 | 142 | ||||||||||||

| International |

3,358 | 3,715 | 61 | 62 | ||||||||||||

| Total |

11,860 | 12,262 | 120 | 118 | ||||||||||||

|

|

2025 versus 2024 | |

| Crop nutrients |

Sales increased due to higher selling prices, and gross margin was impacted by product mix shifts in North America and reduced demand in the fourth quarter. International crop nutrient sales volumes were lower mainly due to strategic actions in South America. | |

| Crop protection products |

Sales and gross margin were lower due to product mix shifts in North America and dry conditions in Australia, partially offset by higher proprietary products gross margin. | |

| Seed |

Sales and gross margin were lower due to weather related impacts in the Southern US leading to fewer planted acres, which impacted proprietary products gross margin. | |

Nutrien Annual Report 2025 35

|

|

Overview | MD&A | Five-year highlights | Financial statements and notes | ||||||||||

|

|

Results

Selected financial performance measures

| (percentages) | 2025 | 2024 | ||||||

| Retail adjusted EBITDA margin1 |

9.9 | 9.5 | ||||||

| Cash operating coverage ratio2 |

62 | 63 | ||||||

| Average working capital to sales2 |

22 | 20 | ||||||

| Average working capital to sales excluding Nutrien Financial2 |

1 | – | ||||||

| Nutrien Financial adjusted net interest margin2 |

5.4 | 5.3 | ||||||

| 1 | This is a supplementary financial measure. See the “Other financial measures” section. |

| 2 | This is a non-GAAP financial measure. See the “Non-GAAP financial measures” section. |

Nutrien Financial

We offer flexible financing solutions to our customers in support of Nutrien’s agricultural product and service sales. Qualifying Retail customers in the US and Australia are offered extended payment terms, typically up to one year, to facilitate the alignment of farmer crop cycles with cash flows. Nutrien Financial revenues are primarily earned through interest from farmers.

We hold a significant portion of receivables from customers that have historically experienced a low-default rate. We manage our credit portfolio based on a combination of review of customer credit metrics, past experience with the customer and exposure to any single customer. Nutrien Financial, which is our wholly owned finance captive, monitors and services the portfolio of our high-quality receivables from customers that have the lowest risk of default among Retail’s receivables from customers. We monitor the results of this portfolio of receivables separately because we calculate the cost of capital attributable to the high-quality receivables from customers differently from our other receivables. Specifically, we assume a debt-to-equity ratio of 9:1 in funding Nutrien Financial receivables, based on the underlying credit quality of the assets.

Nutrien Financial relies on corporate capital for funding. For 2025, we estimated the deemed interest expense using an average borrowing rate of 5.0 percent (2024 — 5.6 percent) applied to the notional debt required to fund the portfolio of receivables from customers monitored and serviced by Nutrien Financial. The balance of our Retail receivables (outside of Nutrien Financial) is subject to marginally higher credit risk.

| As at December 31 | ||||||||||||||||||||||||||||||||

| ($ millions) | Current | |

<31 Days past due |

|

|

31–90 Days past due |

|

|

>90 Days past due |

|

|

Gross receivables |

|

Allowance1 | |

2025 Net receivables |

|

|

2024 Net receivables |

| ||||||||||||

| North America |

1,831 | 260 | 110 | 181 | 2,382 | (50 | ) | 2,332 | 2,178 | |||||||||||||||||||||||

| International |

647 | 82 | 21 | 31 | 781 | (7 | ) | 774 | 699 | |||||||||||||||||||||||

| Nutrien Financial receivables |

2,478 | 342 | 131 | 212 | 3,163 | (57 | ) | 3,106 | 2,877 | |||||||||||||||||||||||

| 1 | Bad debt expense on the above receivables for 2025 was $46 million (2024 – $55 million) in the Retail segment. |

36 Nutrien Annual Report 2025

| Overview | MD&A | Five-year highlights | Financial statements and notes |

| ||||||||||

|

|

Results

2025 POTASH OPERATING SEGMENT AND RESULTS

We operate six low-cost potash mines in Saskatchewan, located within a world-class potash deposit and in a stable geopolitical environment, which helps minimize supply risk for our customers. We produce multiple grades of potash and our flexible network provides the operational flexibility to optimize value.

Our extensive North American transportation and distribution network includes approximately 5,600 owned or leased railcars serviced by multiple railway providers. Through Canpotex – our joint venture potash export, sales and marketing company – we have access to four primary North American marine terminals and other facilities as needed to export potash to customers in over 40 countries around the world.

Potash adjusted EBITDA increased to $2.25 billion in 2025 due to higher net selling prices and record sales volumes, supported by strong potash affordability and underlying consumption growth in key offshore markets, and partially offset by higher provincial mining taxes. We delivered a potash controllable cash cost of product manufactured2 per tonne of $58. We mined 49 percent of our potash ore tonnes using automation, further strengthening our low-cost advantage.

| ($ millions, except as otherwise noted) | 2025 | 2024 | % Change | |||||||||

| Net sales |

3,593 | 2,989 | 20 | |||||||||

| Cost of goods sold |

1,581 | 1,448 | 9 | |||||||||

| Gross margin |

2,012 | 1,541 | 31 | |||||||||

| Adjusted EBITDA1 |

2,254 | 1,848 | 22 | |||||||||

|

Manufactured product

|

||||||||||||

| ($ per tonne, except as otherwise noted) |

|

2025 | 2024 | |||||||||

| Sales volumes (tonnes – thousands) |

||||||||||||

| North America |

4,638 | 4,672 | ||||||||||

| Offshore |

|

|

|

9,615 | 9,214 | |||||||

| Total sales volumes |

|

|

|

14,253 | 13,886 | |||||||

| Net selling price |

||||||||||||

| North America |

286 | 285 | ||||||||||

| Offshore |

|

|

|

235 | 180 | |||||||

| Average net selling price |

252 | 215 | ||||||||||

| Cost of goods sold |

|

|

|

111 | 104 | |||||||

| Gross margin |

141 | 111 | ||||||||||

| Depreciation and amortization |

|

|

|

46 | 44 | |||||||

| Gross margin excluding depreciation and amortization2 |

|

|

|

187 | 155 | |||||||

| 1 | See Note 3 to the consolidated financial statements. |

| 2 | This is a non-GAAP financial measure. See the “Non-GAAP financial measures” section. |

Nutrien Annual Report 2025 37

|

|

Overview | MD&A | Five-year highlights | Financial statements and notes | ||||||||||

|

|

Results

Supplemental data

|

|

|

2025 | 2024 | |||||||||

| Potash controllable cash cost of product manufactured per tonne1 |

|

|

|

58 | 54 | |||||||

| Canpotex sales by market (percentage of sales volumes)2 |

||||||||||||

| Latin America |

39 | 40 | ||||||||||

| Other Asian markets3 |

29 | 28 | ||||||||||

| China |

11 | 13 | ||||||||||

| India |

6 | 7 | ||||||||||

| Other markets |

|

|

|

15 | 12 | |||||||

| Total |

|

|

|

100 | 100 | |||||||

| 1 | This is a non-GAAP financial measure. See the “Non-GAAP financial measures” section. |

| 2 | See Note 26 to the consolidated financial statements. |

| 3 | All Asian markets except China and India. |

|

|

2025 versus 2024 | |

| Sales volumes |

Higher offshore sales volumes were supported by strong potash affordability and underlying consumption growth in key offshore markets. North America sales volumes were consistent with the prior year. | |

| Net selling price per tonne |

Increased due to higher global benchmark prices. | |

| Cost of goods sold per tonne |

Increased primarily due to higher royalties, maintenance costs and depreciation. | |

Potash production

| Operational capability2 | Production | |||||||||||||||||||||||||||||||||||||||||

| (million tonnes KCl) |

|

|

|

|

|

Nameplate capacity1 | 20263 | 2025 |

|

2025 | 2024 | |||||||||||||||||||||||||||||||

| Rocanville |

6.5 | 4.5 | 5.0 | 4.64 | 5.02 | |||||||||||||||||||||||||||||||||||||

| Allan |

4.0 | 3.1 | 2.7 | 2.51 | 2.40 | |||||||||||||||||||||||||||||||||||||

| Lanigan |

3.8 | 3.5 | 3.2 | 3.43 | 3.40 | |||||||||||||||||||||||||||||||||||||

| Vanscoy |

3.0 | 1.1 | 1.1 | 1.08 | 1.03 | |||||||||||||||||||||||||||||||||||||

| Cory |

3.0 | 2.2 | 2.1 | 2.09 | 2.11 | |||||||||||||||||||||||||||||||||||||

| Patience Lake |

0.3 | 0.3 | 0.3 | 0.22 | 0.25 | |||||||||||||||||||||||||||||||||||||

| Total |

20.6 | 14.7 | 14.4 | 13.97 | 14.21 | |||||||||||||||||||||||||||||||||||||

| 1 | Represents estimates of capacity as at December 31, 2025. Estimates based on capacity as per design specifications or Canpotex entitlements once determined. In the case of Patience Lake, estimate reflects current operational capability. Estimates for all other mine facilities do not necessarily represent operational capability. |

| 2 | Estimated annual achievable production based on expected staffing and operational readiness (estimated at the beginning of the year, and may vary during the year, and year to year, including between our mine facilities). Estimate does not include inventory-related shutdowns and unplanned downtime. |

| 3 | See the “Forward-Looking Statements” section. |

38 Nutrien Annual Report 2025

| Overview | MD&A | Five-year highlights | Financial statements and notes |

| ||||||||||

|

|

Results

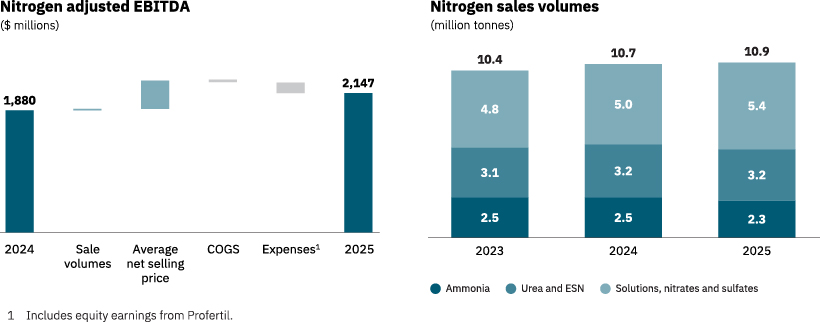

2025 NITROGEN OPERATING SEGMENT AND RESULTS

We produce and upgrade nitrogen at 11 strategically located facilities in Canada and the US, in addition to our facility in Trinidad. Our North American operations, which account for approximately 85 percent of our nitrogen sales volumes, have access to some of the lowest-cost natural gas in the world and are well positioned to serve agriculture and industrial markets.

We produce a diverse portfolio of nitrogen products and have flexibility to optimize product mix in changing market conditions. Our transportation and distribution network leverages truck, rail, pipeline, barge and marine vessels. We utilize established CCUS infrastructure in Alberta and Louisiana to reduce GHG emissions. Over the last five years, we captured and sold an annual average of 1 million tonnes of CO2, with approximately 40 percent permanently sequestered via enhanced oil recovery.

Nitrogen adjusted EBITDA increased to $2.15 billion in 2025 due to higher net selling prices, partially offset by lower equity earnings from Profertil. Adjusted EBITDA for the full year of 2024 benefitted from insurance recoveries. Total ammonia production increased in 2025, supported by a four-percentage-point improvement in ammonia operating rate (excludes Trinidad and Joffre) as we advanced reliability initiatives across our North American plants and completed low-cost debottlenecks at Redwater and Geismar. In the fourth quarter of 2025, we completed a controlled shutdown of our Trinidad Nitrogen facility due to uncertainty with respect to port access and a lack of reliable and economic gas supply that has reduced the free cash flow contribution of the Trinidad Nitrogen operations over an extended period of time.

| ($ millions, except as otherwise noted) | 2025 | 2024 | ¹ | % Change | ||||||||

| Net sales |

4,187 | 3,576 | 17 | |||||||||

| Cost of goods sold |

2,580 | 2,374 | 9 | |||||||||

| Gross margin |

1,607 | 1,202 | 34 | |||||||||

| Adjusted EBITDA2 |

2,147 | 1,880 | 14 | |||||||||

|

1 Comparative figures have been reclassified for our Purchase for Resale business from Nitrogen to the Corporate and Others segment. See Note 3 to the consolidated financial statements. 2 See Note 3 to the consolidated financial statements. |

| |||||||||||

|

Manufactured product

|

||||||||||||

| ($ per tonne, except as otherwise noted) |

|

2025 | 2024 | |||||||||

| Sales volumes (tonnes – thousands) |

||||||||||||

| Ammonia |

2,420 | 2,483 | ||||||||||

| Urea and ESN® |

3,099 | 3,188 | ||||||||||

| Solutions, nitrates and sulfates |

|

|

|

5,369 | 5,023 | |||||||

| Total sales volumes |

|

|

|

10,888 | 10,694 | |||||||

| Net selling price |

||||||||||||

| Ammonia |

422 | 410 | ||||||||||

| Urea and ESN® |

490 | 421 | ||||||||||

| Solutions, nitrates and sulfates |

|

|

|

268 | 221 | |||||||

| Average net selling price |

365 | 324 | ||||||||||

| Cost of goods sold |

|

|

|

219 | 213 | |||||||

| Gross margin |

146 | 111 | ||||||||||

| Depreciation and amortization |

|

|

|

57 | 55 | |||||||

| Gross margin excluding depreciation and amortization1 |

|

|

|

203 | 166 | |||||||

|

1 This is a non-GAAP financial measure. See the “Non-GAAP financial measures” section. |

||||||||||||

Supplemental data

|

|

|

2025 | 2024 | |||||||

| Ammonia controllable cash cost of product manufactured per tonne1 |

58 | 61 | ||||||||

| Sales volumes (tonnes – thousands) |

||||||||||

| Fertilizer |

6,425 | 6,259 | ||||||||

| Industrial and feed |

4,463 | 4,435 | ||||||||

| Ammonia operating rate2 (%) |

92 | 88 | ||||||||

| Natural gas costs ($ per MMBtu) |

||||||||||

| Overall natural gas cost excluding realized derivative impact |

3.53 | 3.15 | ||||||||

| Realized derivative impact |

|

– | 0.09 | |||||||

| Overall natural gas cost |

|

3.53 | 3.24 | |||||||

|

1 This is a non-GAAP financial measure. See the “Non-GAAP financial measures” section. 2 Excludes Trinidad and Joffre. |

| |||||||||

Nutrien Annual Report 2025 39

|

|

Overview | MD&A | Five-year highlights | Financial statements and notes | ||||||||||

|

|

Results

|

|

2025 versus 2024 | |

| Sales volumes |

Increased due to higher production from reliability improvements and low-cost debottlenecks that increased the availability of upgraded products. | |

| Net selling price per tonne |

Higher for all major nitrogen products due to stronger benchmark prices. | |

| Cost of goods sold per tonne |

Increased due to higher natural gas costs, mainly driven by Henry Hub benchmark. | |

Nitrogen production

| Ammonia1 | Urea2 | |||||||||||||||||||||||

| (million tonnes, except as otherwise noted) | |

Annual capacity3 |

|

Production | |

Annual capacity3 |

|

Production | ||||||||||||||||

| 2025 | 2024 | 2025 | 2024 | |||||||||||||||||||||

| Trinidad4 |

2.2 | 1.18 | 1.27 | 0.7 | 0.54 | 0.47 | ||||||||||||||||||

| Redwater |

1.0 | 0.73 | 0.86 | 0.7 | 0.53 | 0.70 | ||||||||||||||||||

| Augusta |

0.8 | 0.74 | 0.68 | 0.6 | 0.58 | 0.52 | ||||||||||||||||||

| Lima |

0.7 | 0.76 | 0.59 | 0.5 | 0.53 | 0.46 | ||||||||||||||||||

| Geismar |

0.6 | 0.61 | 0.58 | 0.4 | 0.43 | 0.38 | ||||||||||||||||||

| Carseland |

0.5 | 0.53 | 0.46 | 0.7 | 0.73 | 0.65 | ||||||||||||||||||

| Fort Saskatchewan |

0.5 | 0.47 | 0.44 | 0.4 | 0.42 | 0.40 | ||||||||||||||||||

| Borger |

0.5 | 0.29 | 0.35 | 0.6 | 0.38 | 0.42 | ||||||||||||||||||

| Joffre |

0.5 | 0.39 | 0.38 | – | – | – | ||||||||||||||||||

| Total |

7.3 | 5.71 | 5.61 | 4.6 | 4.14 | 4.00 | ||||||||||||||||||

| Adjusted total5 |

|

|

|

4.13 | 3.96 |

|

|

|

|

|

|

|

|

| ||||||||||

| 1 | All figures are shown on a gross production basis. |

| 2 | Reflects capacity and production of urea liquor prior to final product upgrade. Urea liquor is used in the production of solid urea, UAN and DEF. |

| 3 | Annual capacity estimates include allowances for normal operating plant conditions. |

| 4 | In 2024 and 2025, Trinidad production was restricted due to natural gas curtailments. On October 23, 2025, we completed a controlled shutdown of our Trinidad facility due to uncertainty with respect to port access and a lack of reliable and economic gas supply. |

| 5 | Excludes Trinidad and Joffre. |

40 Nutrien Annual Report 2025

| Overview | MD&A | Five-year highlights | Financial statements and notes |

| ||||||||||

|

|

Results

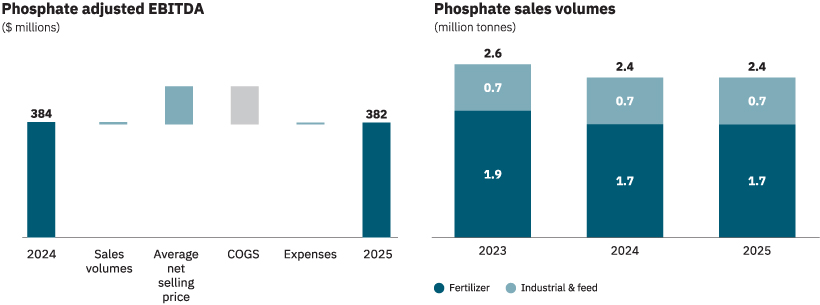

2025 PHOSPHATE OPERATING SEGMENT AND RESULTS

Nutrien has two large integrated phosphate production facilities and four regional product upgrade sites in the US. Our high-quality phosphate rock enables production of a diverse mix of phosphate products, including solid and liquid fertilizers, feed and industrial acids. We are the largest producer of purified phosphoric acid in North America and sell the majority of our product in this market, benefiting from our extensive distribution network and customer relationships.

Phosphate adjusted EBITDA slightly decreased to $382 million in 2025 due to higher sulfur input costs and lower sales volumes, partially offset by higher net selling prices. In the third quarter of 2025, we initiated a review of strategic alternatives for our Phosphate business, which could include reconfiguring operations, strategic partnerships or a potential sale, and we intend to solidify the optimal path in 2026.

| ($ millions, except as otherwise noted) | 2025 | 2024 | % Change | |||||||||

| Net sales |

1,734 | 1,657 | 5 | |||||||||

| Cost of goods sold |

1,590 | 1,510 | 5 | |||||||||

| Gross margin |

144 | 147 | (2 | ) | ||||||||

| Adjusted EBITDA1 |

382 | 384 | (1 | ) | ||||||||

| 1 | See Note 3 to the consolidated financial statements. |

Manufactured product

| ($ per tonne, except as otherwise noted) | 2025 | 2024 | ||||||

| Sales volumes (tonnes – thousands) |

||||||||

| Fertilizer |

1,646 | 1,751 | ||||||

| Industrial and feed |

717 | 683 | ||||||

| Total sales volumes |

2,363 | 2,434 | ||||||

| Net selling price |

||||||||

| Fertilizer |

677 | 612 | ||||||

| Industrial and feed |

835 | 822 | ||||||

| Average net selling price |

725 | 671 | ||||||

| Cost of goods sold |

657 | 603 | ||||||

| Gross margin |

68 | 68 | ||||||

| Depreciation and amortization |

121 | 119 | ||||||

| Gross margin excluding depreciation and amortization1 |

189 | 187 | ||||||

| 1 | This is a non-GAAP financial measure. See the “Non-GAAP financial measures” section. |

|

|

2025 versus 2024 | |

| Sales volumes |

Lower due to lower production volumes in the first quarter of 2025. | |

| Net selling price |

Increased due to the strength of fertilizer benchmark prices. | |

| Cost of goods sold per tonne |

Increased primarily due to higher sulfur input costs. | |

Nutrien Annual Report 2025 41

|

|

Overview | MD&A | Five-year highlights | Financial statements and notes | ||||||||||

|

|

Results

Phosphate production

| Phosphate rock | Phosphoric acid (P2O5) | Liquid products | Solid fertilizer products | |||||||||||||||||||||||||||||||||||||||||||||

| (million tonnes, except as otherwise noted) |

Annual capacity |

Production | Annual capacity |

Production | Annual capacity |

Production | Annual capacity |

Production | ||||||||||||||||||||||||||||||||||||||||

| 2025 | 2024 | 2025 | 2024 | 2025 | 2024 | 2025 | 2024 | |||||||||||||||||||||||||||||||||||||||||

| Aurora |

5.4 | 4.66 | 3.99 | 1.2 | 1.00 | 0.97 | 2.7 | 1 | 2.10 | 2.05 | 0.9 | 0.72 | 0.76 | |||||||||||||||||||||||||||||||||||

| White Springs |

2.0 | 1.39 | 1.19 | 0.5 | 0.36 | 0.36 | 0.7 | 2 | 0.31 | 0.29 | 0.8 | 0.29 | 0.31 | |||||||||||||||||||||||||||||||||||

| Total |

7.4 | 6.05 | 5.18 | 1.7 | 1.36 | 1.33 | 3.4 | 2.41 | 2.34 | 1.7 | 1.01 | 1.07 | ||||||||||||||||||||||||||||||||||||

| P2O5 operating rate (%) |

|

|

|

|

|

|

|

|

|

|

|

|

80 | 78 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| ||||||||||||||||

| 1 | A substantial portion is consumed internally in the production of downstream products. The balance is exported to phosphate fertilizer producers or sold domestically to dealers who custom-mix liquid fertilizer. Capacity is composed of 2.0 million tonnes MGA and 0.7 million tonnes SPA. |

| 2 | Represents annual SPA capacity. A substantial portion is consumed internally in the production of downstream products. The balance is exported to phosphate fertilizer producers or sold domestically to dealers who custom-mix liquid fertilizer. |

In addition to the production above, annual capacity for phosphate feed and purified acid was 0.7 and 0.3 million tonnes, respectively. Production in 2025 was 0.34 and 0.19 million tonnes, respectively, and 2024 production was 0.31 and 0.17 million tonnes, respectively.

42 Nutrien Annual Report 2025