.2

M AY 2 0 2 6 Mentari Therapeutics Overview

2 Disclaimers The information contained in this presentation has been prepared by Mentari Therapeutics, Inc. and its affiliates ("we," "us," "our" or the "Company") and contains information pertaining to the business and operations of the Company. The information contained in this presentation: (a) is provided as at the date hereof, is subject to change without notice, and is based on publicly available information, internally developed data and third party information from other sources; (b) does not purport to contain all the information that may be necessary or desirable to fully and accurately evaluate an investment in the Company; (c) is not to be considered as a recommendation by the Company that any person make an investment in the Company; (d) is for information purposes only and shall not constitute an offer to buy, sell, issue or subscribe for, or the solicitation of an offer to buy, sell or issue, or subscribe for any securities of the Company in any jurisdiction in which such offer, solicitation or sale would be unlawful. Where any opinion or belief is expressed in this presentation, it is based on certain assumptions and limitations and is an expression of present opinion or belief only. This presentation should not be construed as legal, financial or tax advice to any individual, as each individual's circumstances are different. This document is for informational purposes only and should not be considered a solicitation or recommendation to purchase, sell or hold a security. This presentation is for informational purposes only and only a summary of certain information related to the Company. The information contained herein does not constitute investment, legal, accounting, regulatory, taxation or other advice, and the information does not take into account your investment objectives or legal, accounting, regulatory, taxation or financial situation or particular needs. Statements in this presentation are made as of the date hereof unless stated otherwise herein, and neither the delivery of this presentation at any time, nor any sale of securities, shall under any circumstances create an implication that the information contained herein is correct as of any time subsequent to such date. The Company is under no obligation to update or keep current the information contained in this document. No representation or warranty, express or implied, is made as to, and no reliance should be placed on, the fairness, accuracy, completeness or correctness of the information or opinions contained herein, and any reliance you place on them will be at your sole risk. The Company, its affiliates and advisors do not accept any liability whatsoever for any loss howsoever arising, directly or indirectly, from the use of this document or its contents. No offer or solicitation This presentation shall not constitute an offer to sell or the solicitation of an offer to buy any securities, nor shall there be any sale of securities in any jurisdiction in which such offer, solicitation or sale would be unlawful prior to registration or qualification under the securities laws of any such jurisdiction. No offering of securities shall be made except by means of a prospectus meeting the requirements of Section 10 of the U.S. Securities Act of 1933, as amended. Additional information and where to find it In connection with the proposed Transaction, InMed Pharmaceuticals Inc. ("InMed") intends to file with the U.S. Securities and Exchange Commission (the "SEC") a registration statement on Form S-4 that will include a proxy statement of InMed and a prospectus of InMed relating to the shares of InMed common stock to be issued in connection with the proposed Transaction. After the registration statement has been declared effective by the SEC, a definitive proxy statement/prospectus will be mailed to stockholders of InMed. INVESTORS AND SECURITY HOLDERS ARE URGED TO READ THE REGISTRATION STATEMENT ON FORM S-4 AND THE RELATED PROXY STATEMENT/PROSPECTUS, AS WELL AS ANY AMENDMENTS OR SUPPLEMENTS TO THOSE DOCUMENTS AND ANY OTHER RELEVANT DOCUMENTS THAT ARE FILED OR TO BE FILED WITH THE SEC, CAREFULLY AND IN THEIR ENTIRETY BECAUSE THEY WILL CONTAIN IMPORTANT INFORMATION ABOUT INMED, MENTARI, THE PROPOSED TRANSACTION AND RELATED MATTERS. Investors and security holders may obtain free copies of the registration statement and proxy statement/prospectus (when available) and other documents filed with the SEC by InMed through the SEC's website at www.sec.gov or by directing a request to InMed at InMed's principal offices. Forward-looking statements and other information Certain statements contained in this presentation that are not descriptions of historical facts are "forward-looking statements." When we use words such as "potentially," "could," "will," "projected," "possible," "expect," "illustrative," "estimated" or similar expressions that do not relate solely to historical matters, we are making forward-looking statements. Forward-looking statements are not guarantees of future performance and involve risks and uncertainties that may cause our actual results to differ materially from our expectations discussed in the forward-looking statements. This may be a result of various factors, including, but not limited to: our management team's expectations, hopes, beliefs, intentions or strategies regarding the future including, without limitation, statements regarding: the proposed business combination between InMed Pharmaceuticals Inc. ("InMed") and the Company (the "Transaction"), including the expected timing, completion and effects of the Transaction; the anticipated benefits of the Transaction, including the combined company's estimated pro forma capitalization, ownership structure and cash position; the concurrent private placement and expected use of proceeds; expectations regarding or plans for discovery, preclinical studies, clinical trials and research and development programs and therapies, including timing of regulatory filings and preclinical and clinical trials for MT-001, MT-002, MT-003 and other pipeline candidates; the potential clinical benefit and safety of product candidates targeting PACAP, CGRP and other migraine-related pathways, including as compared to third-party products and product candidates in development; expectations regarding the time period over which our capital resources will be sufficient to fund our anticipated operations; and statements regarding the market, competition, and potential opportunities for migraine prevention and treatment therapies. All forward-looking statements, expressed or implied, included in this presentation are expressly qualified in their entirety by this cautionary statement. You are cautioned not to place undue reliance on any forward-looking statements. Except as otherwise required by applicable law, we disclaim any duty to update any forward-looking statements, all of which are expressly qualified by this cautionary statement, to reflect events or circumstances after the date of this presentation. This presentation concerns drug candidates that are under preclinical investigation, and which have not yet been approved by the U.S. Food and Drug Administration. These are currently limited by federal law to investigational use, and no representation is made as to their safety or effectiveness for the purposes for which they are being investigated. Market and Industry Data Certain information contained in this presentation and statements made orally during this presentation relate to or are based on studies, publications and other data obtained from third-party sources as well as our own internal estimates and research. While we believe these third-party sources to be reliable as of the date of this presentation, we have not independently verified, and make no representation as to the adequacy, fairness, accuracy or completeness of, any information obtained from third party sources. Forecasts and other forward-looking information obtained from these sources are subject to the same qualifications and uncertainties as the other forward-looking statements in this presentation. Statements as to our market and competitive position data are based on market data currently available to us, as well as management's internal analyses and assumptions regarding the Company, which involve certain assumptions and estimates. These internal analyses have not been verified by any independent sources and there can be no assurance that the assumptions or estimates are accurate. While we are not aware of any misstatements regarding our industry data presented herein, our estimates involve risks and uncertainties and are subject to change based on various factors. As a result, we cannot guarantee the accuracy or completeness of such information contained in this presentation.

3 Transaction summary Transaction: Transaction between InMed Pharmaceuticals Inc. (InMed), including its wholly owned subsidiaries, and Mentari Therapeutics, Inc. (Mentari) Transaction Structure: InMed to acquire 100% of Mentari equity interests in a reverse triangular merger of a wholly owned subsidiary of InMed with and into Mentari, with Mentari surviving the merger as a wholly owned subsidiary of InMed. Transaction intended to be structured as a tax-free event. Post-Closing Ownership: InMed holders expected to own ~1.51% ($6.4M valuation); Mentari holders expected to own ~29.66% ($125.0M valuation); Concurrent Investment ~68.82% ($290.0M). Total value: $421.4M. Concurrent Financing: $290.0 million concurrent private placement into Mentari (or alternatively into InMed, if necessary) effected immediately prior to the Closing. Management and Board: Mentari's senior management team will operate the combined company. Post-Closing board to consist of a number of directors to be determined by Mentari (in its sole discretion), subject to Nasdaq independence requirements. Certain Closing Conditions: Customary conditions including absence of MAE; stockholder approval of each party; S-4/Proxy deemed effective by the SEC; Nasdaq new listing application with respect to post-Closing company; and any other required regulatory approvals. InMed Legacy Assets: InMed stockholders of record as of immediately prior to Closing would receive in aggregate 90% of any net proceeds received by Mentari from the sale of InMed Legacy Assets. At Closing, it is expected that InMed will distribute legacy cash assets, if any, to pre-merger InMed stockholders. Lock-Up Agreements: Continuing executive officers and members of the board of directors of Mentari and InMed will agree to a 180-day lock-up post- Closing. SEC Filings: Parties to file Form S-4 with InMed to hold a stockholder meeting promptly following effectiveness of the Form S-4. Primary Use of Proceeds: The proceeds from the private placement are expected to be primarily used to advance the Mentari pipeline and deliver the following anticipated milestones: Phase 1 healthy volunteer data and Phase 2a proof-of-concept data in migraine patients for MT-001 and Phase 1 healthy volunteer data for MT-002. Proceeds are expected to provide cash runway through 2028.

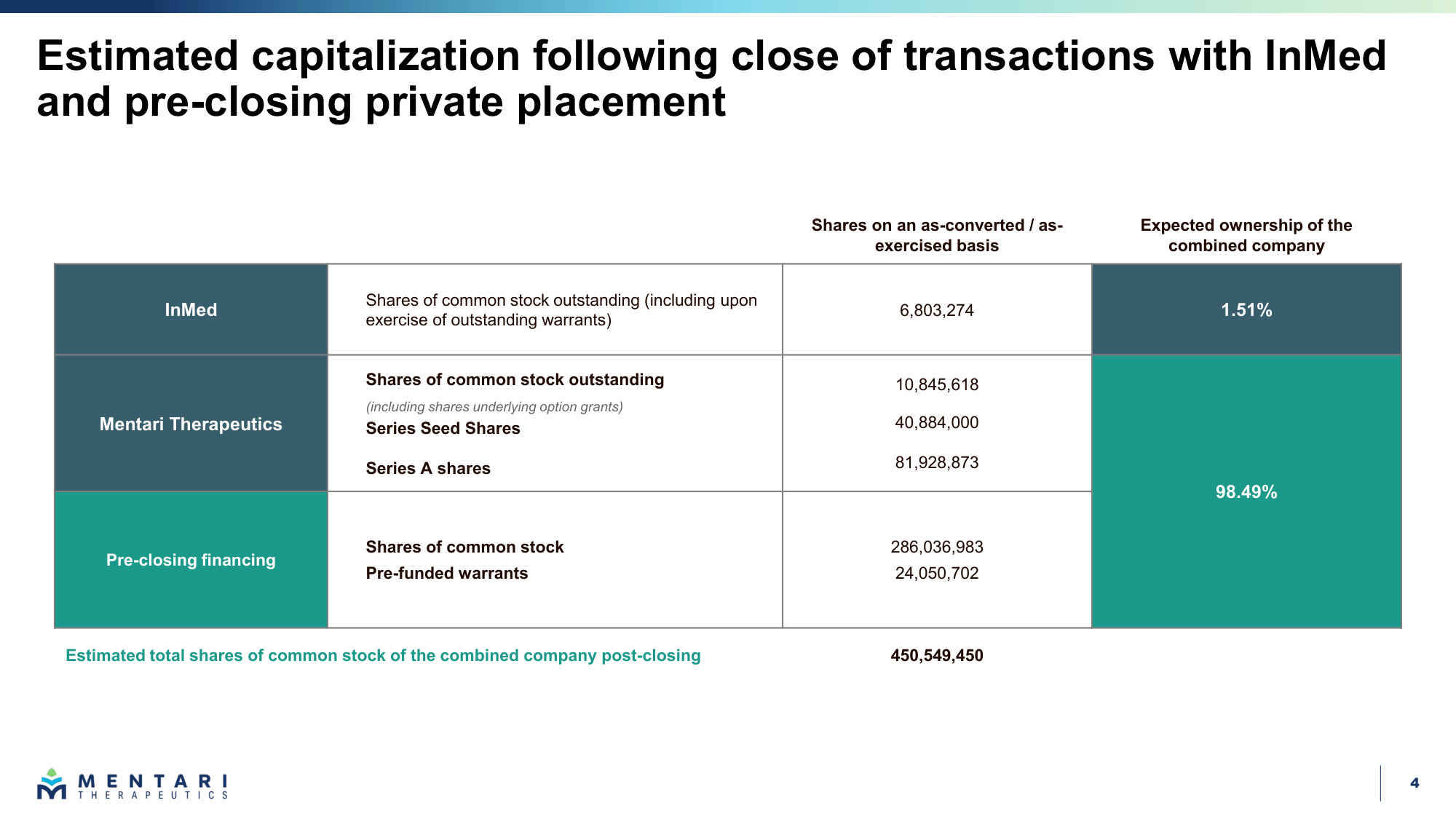

4 Estimated capitalization following close of transactions with InMed and pre-closing private placement Shares on an as-converted / as- exercised basis Expected ownership of the combined company InMed Shares of common stock outstanding (including upon exercise of outstanding warrants) 6,803,274 1.51% Mentari Therapeutics Shares of common stock outstanding (including shares underlying option grants) Series Seed Shares Series A shares 10,845,618 40,884,000 81,928,873 98.49% Pre-closing financing Shares of common stock Pre-funded warrants 286,036,983 24,050,702 Estimated total shares of common stock of the combined company post-closing 450,549,450

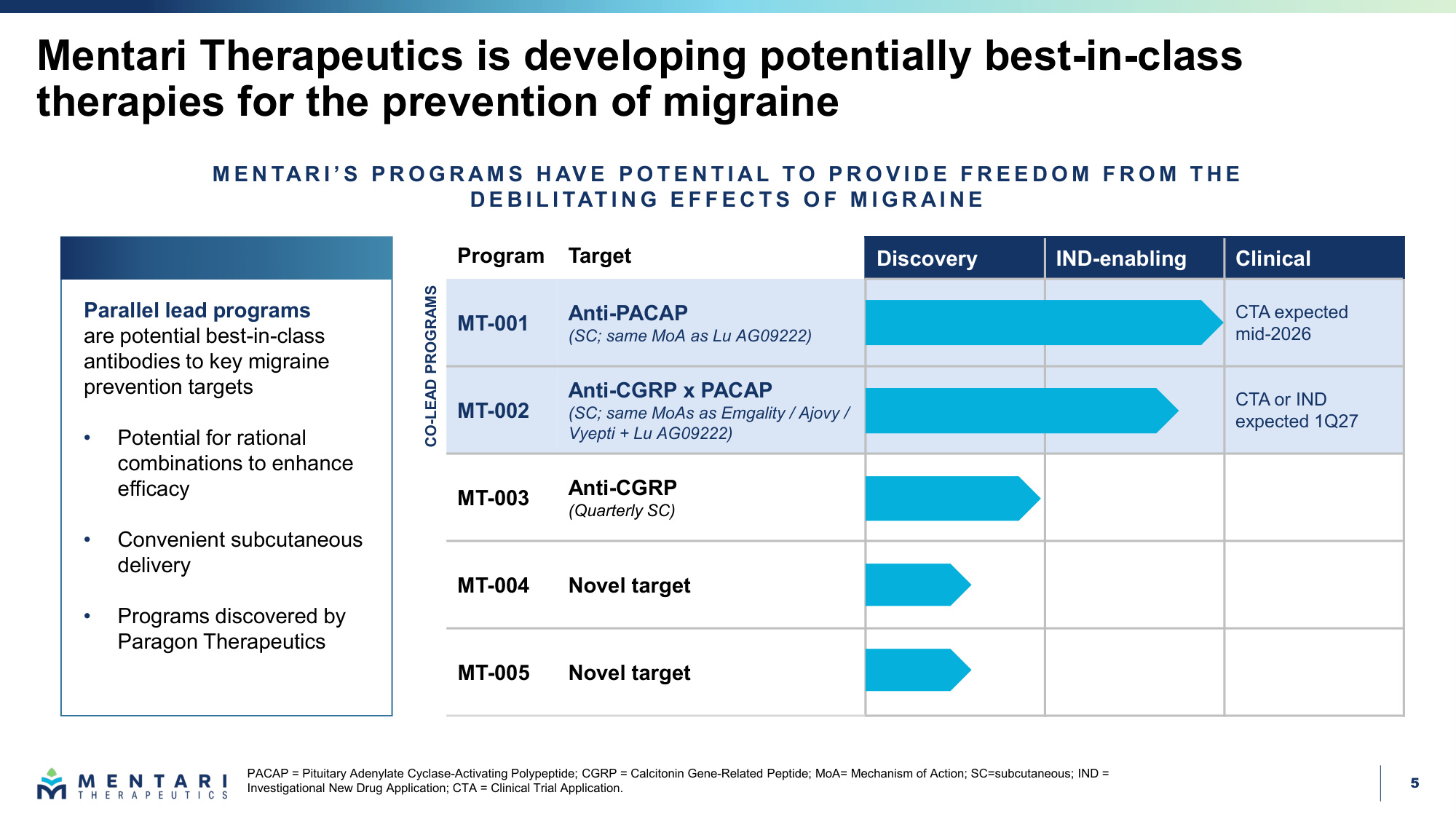

5 Mentari Therapeutics is developing potentially best-in-class therapies for the prevention of migraine PACAP = Pituitary Adenylate Cyclase-Activating Polypeptide; CGRP = Calcitonin Gene-Related Peptide; MoA= Mechanism of Action; SC=subcutaneous; IND = Investigational New Drug Application; CTA = Clinical Trial Application. Program Target Discovery IND-enabling Clinical MT-001 Anti-PACAP (SC; same MoA as Lu AG09222) CTA expected mid-2026 MT-002 Anti-CGRP x PACAP (SC; same MoAs as Emgality / Ajovy / Vyepti + Lu AG09222) CTA or IND expected 1Q27 MT-003 Anti-CGRP (Quarterly SC) MT-004 Novel target MT-005 Novel target CO-LEAD PROGRAMS M E N TAR I ' S P R O G R AM S H AV E P O T E N T I AL T O P R O V I D E F R E E D O M F R O M T H E D E B I L I TAT I N G E F F E C T S O F M I G R AI N E Parallel lead programs are potential best-in-class antibodies to key migraine prevention targets • Potential for rational combinations to enhance efficacy • Convenient subcutaneous delivery • Programs discovered by Paragon Therapeutics

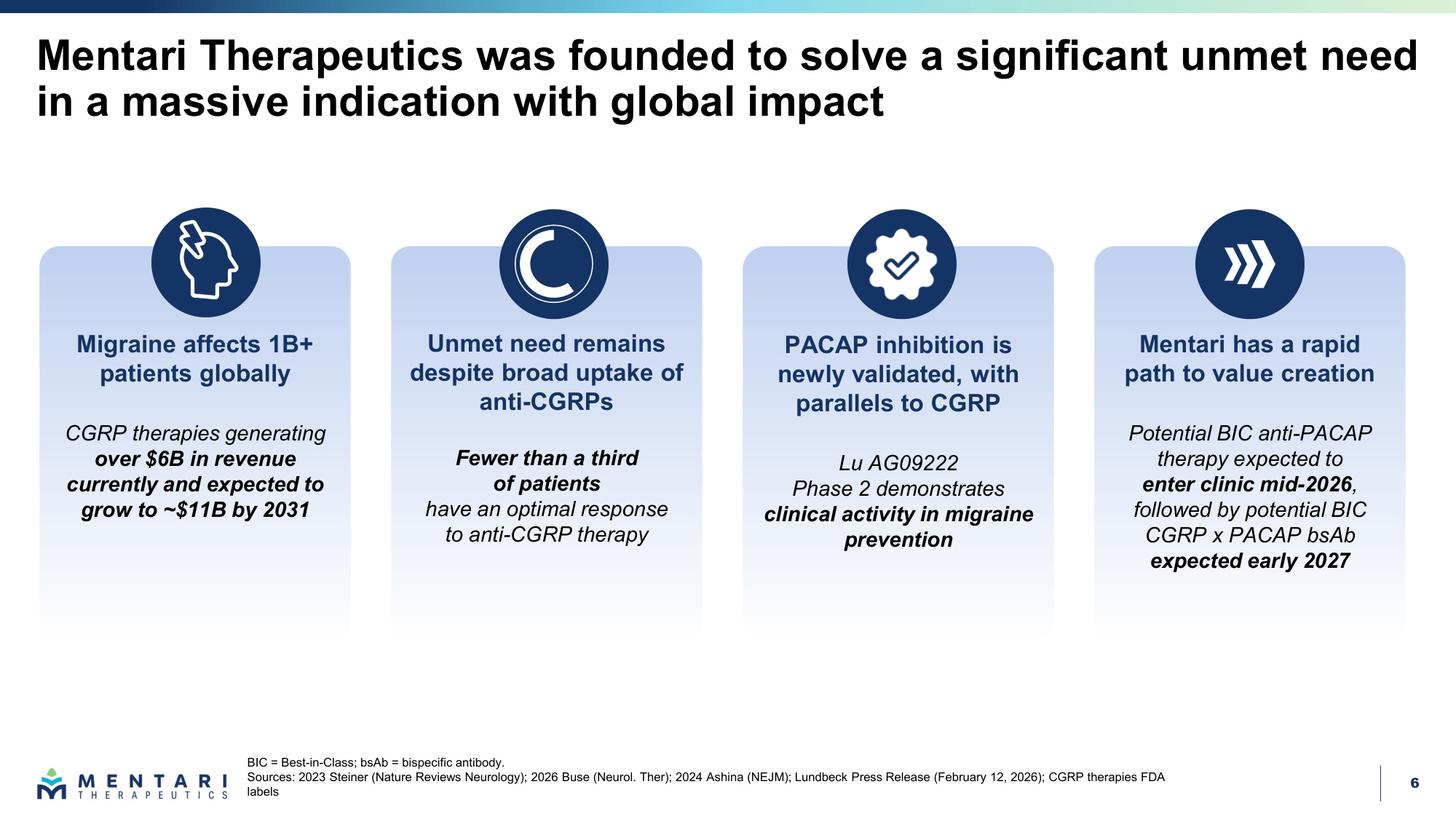

6 Mentari has a rapid path to value creation Potential BIC anti-PACAP therapy expected to enter clinic mid-2026, followed by potential BIC CGRP x PACAP bsAb expected early 2027 Migraine affects 1B+ patients globally CGRP therapies generating over $6B in revenue currently and expected to grow to ~$11B by 2031 Unmet need remains despite broad uptake of anti-CGRPs Fewer than a third of patients have an optimal response to anti-CGRP therapy PACAP inhibition is newly validated, with parallels to CGRP Lu AG09222 Phase 2 demonstrates clinical activity in migraine prevention Mentari Therapeutics was founded to solve a significant unmet need in a massive indication with global impact BIC = Best-in-Class; bsAb = bispecific antibody. Sources: 2023 Steiner (Nature Reviews Neurology); 2026 Buse (Neurol. Ther); 2024 Ashina (NEJM); Lundbeck Press Release (February 12, 2026); CGRP therapies FDA labels

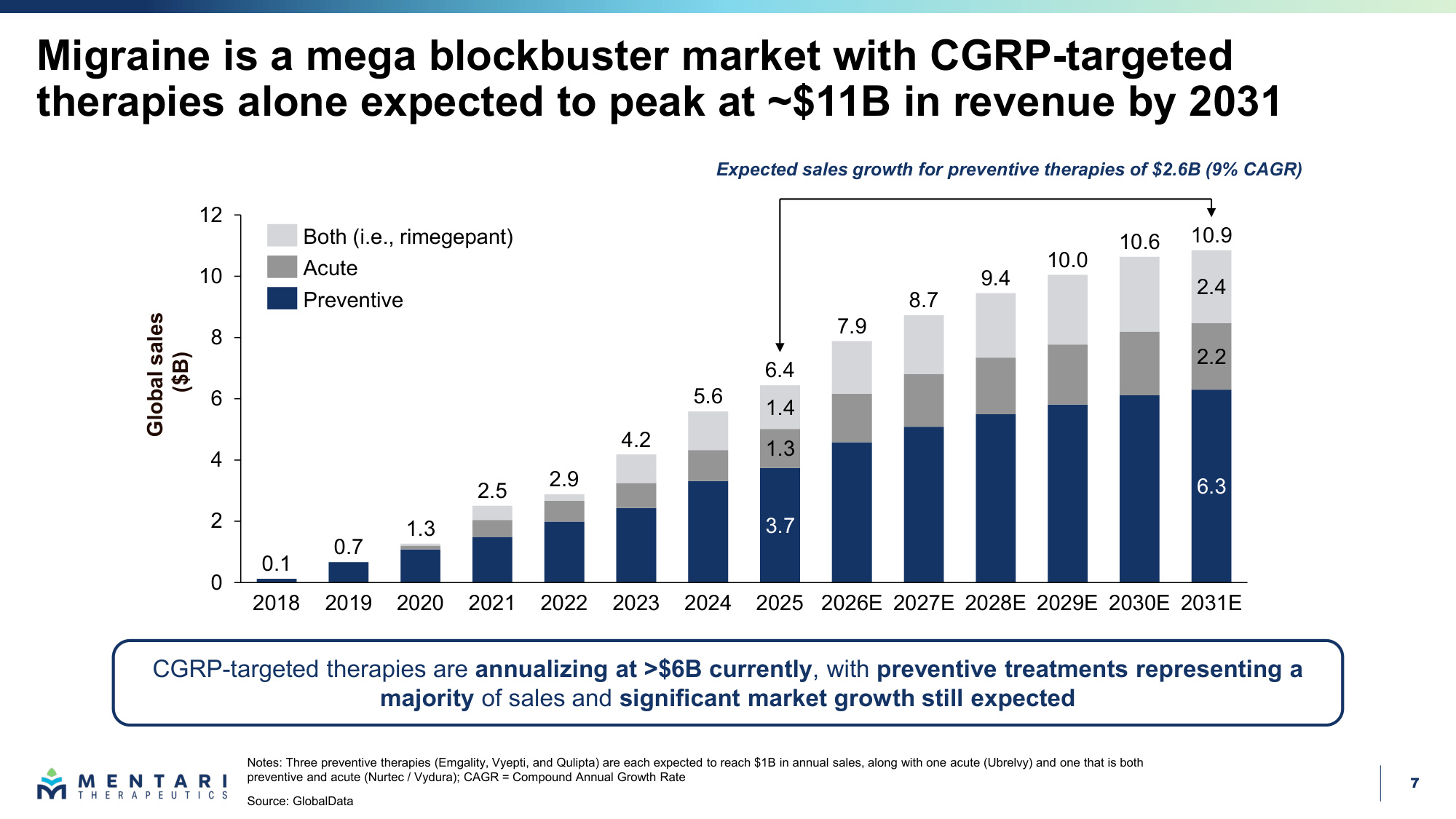

7 Migraine is a mega blockbuster market with CGRP-targeted therapies alone expected to peak at ~$11B in revenue by 2031 3.7 6.3 1.3 2.2 1.4 2.4 0 2 4 6 8 10 12 2022 2023 2024 2025 2026E 2027E 2028E 2029E 2030E 2031E 2021 2020 2019 0.1 0.7 1.3 2.5 2.9 4.2 5.6 6.4 7.9 8.7 9.4 10.0 10.6 10.9 2018 Expected sales growth for preventive therapies of $2.6B (9% CAGR) Notes: Three preventive therapies (Emgality, Vyepti, and Qulipta) are each expected to reach $1B in annual sales, along with one acute (Ubrelvy) and one that is both preventive and acute (Nurtec / Vydura); CAGR = Compound Annual Growth Rate Source: GlobalData Both (i.e., rimegepant) Acute Preventive CGRP-targeted therapies are annualizing at >$6B currently, with preventive treatments representing a majority of sales and significant market growth still expected Global sales ($B)

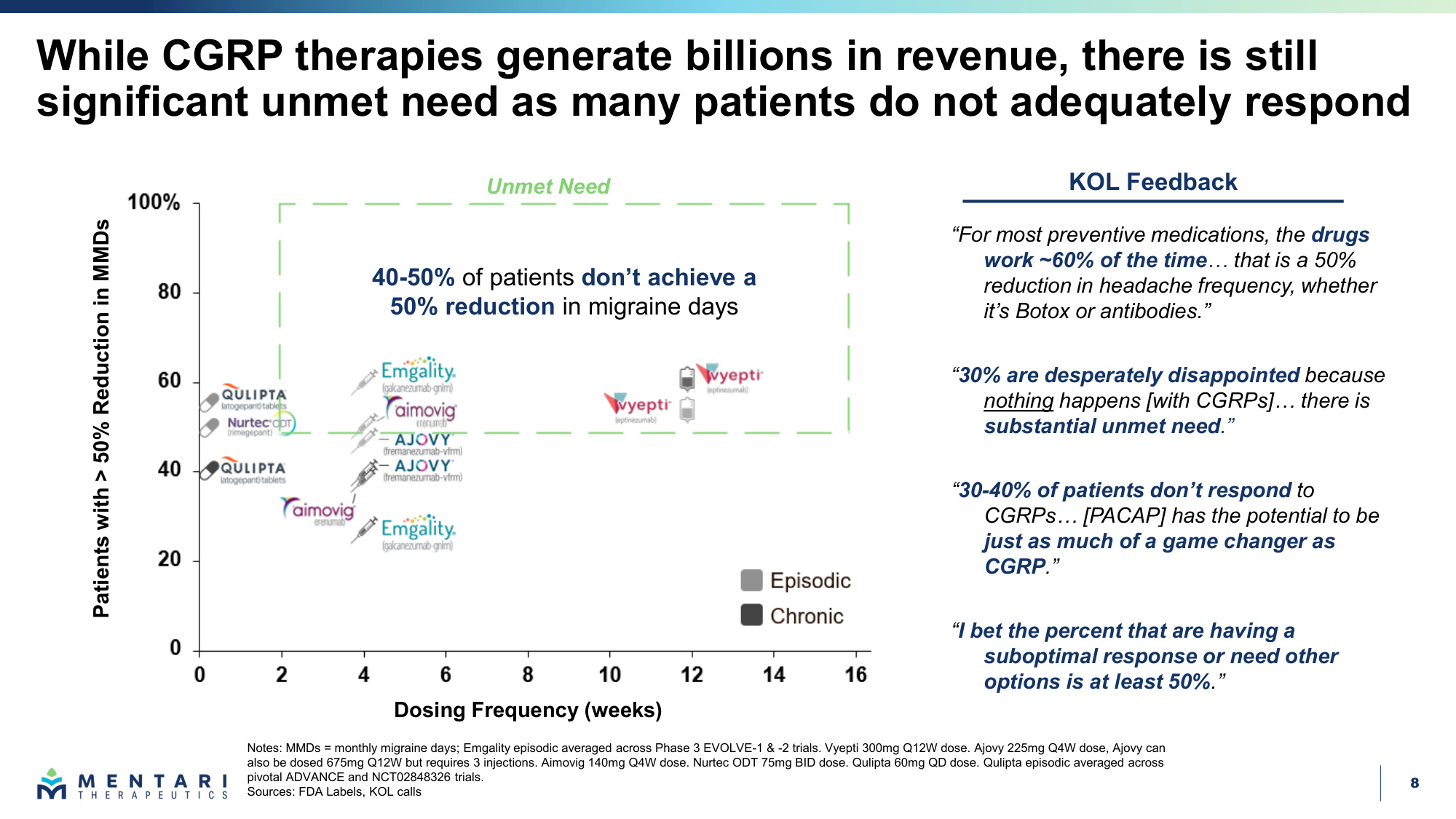

8 While CGRP therapies generate billions in revenue, there is still significant unmet need as many patients do not adequately respond Notes: MMDs = monthly migraine days; Emgality episodic averaged across Phase 3 EVOLVE-1 & -2 trials. Vyepti 300mg Q12W dose. Ajovy 225mg Q4W dose, Ajovy can also be dosed 675mg Q12W but requires 3 injections. Aimovig 140mg Q4W dose. Nurtec ODT 75mg BID dose. Qulipta 60mg QD dose. Qulipta episodic averaged across pivotal ADVANCE and NCT02848326 trials. Sources: FDA Labels, KOL calls "30% are desperately disappointed because nothing happens [with CGRPs]... there is substantial unmet need." "30-40% of patients don't respond to CGRPs... [PACAP] has the potential to be just as much of a game changer as CGRP." "For most preventive medications, the drugs work ~60% of the time... that is a 50% reduction in headache frequency, whether it's Botox or antibodies." KOL Feedback "I bet the percent that are having a suboptimal response or need other options is at least 50%." 40-50% of patients don't achieve a 50% reduction in migraine days Unmet Need Patients with > 50% Reduction in MMDs Dosing Frequency (weeks)

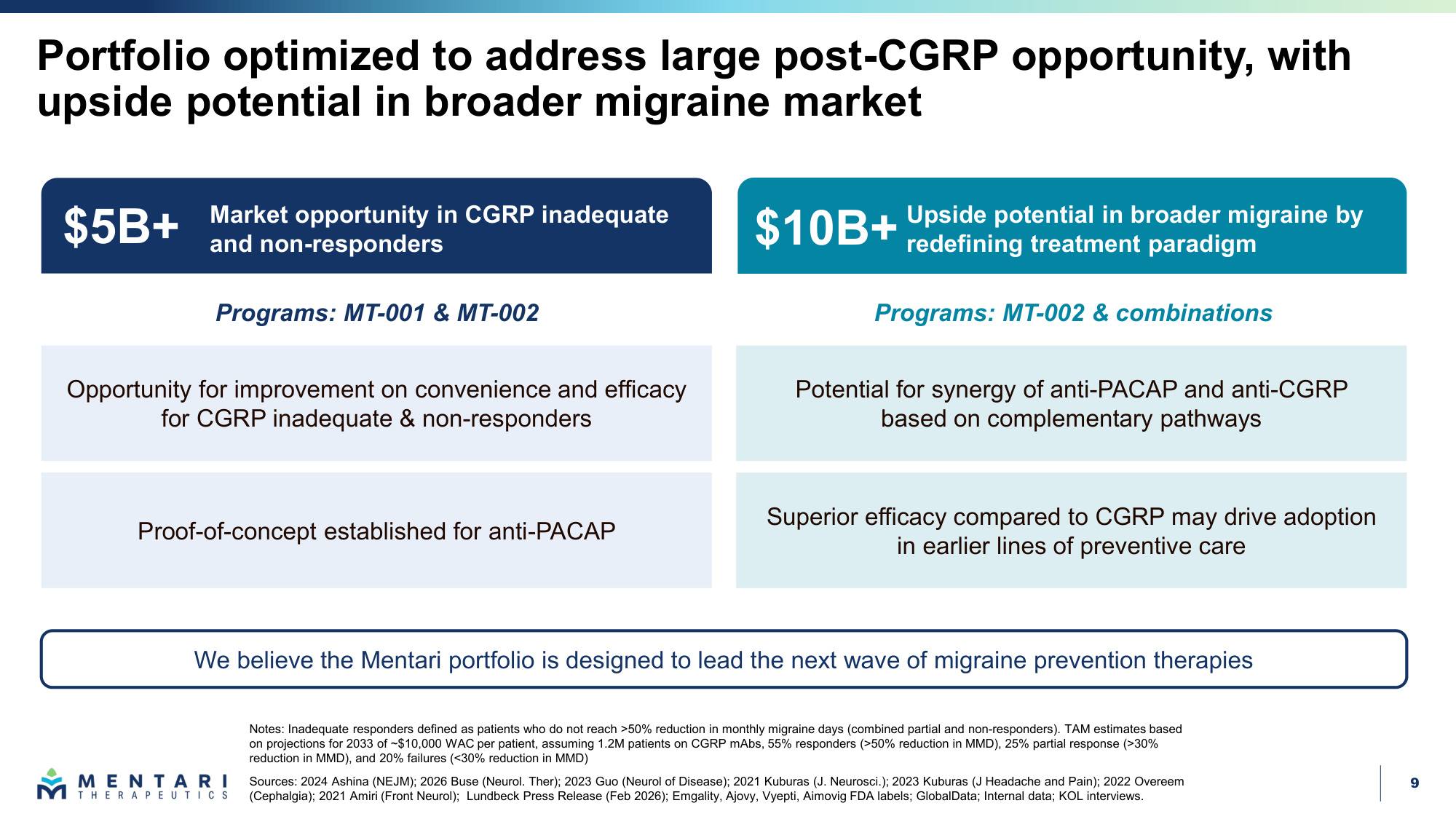

9 Portfolio optimized to address large post-CGRP opportunity, with upside potential in broader migraine market Notes: Inadequate responders defined as patients who do not reach >50% reduction in monthly migraine days (combined partial and non-responders). TAM estimates based on projections for 2033 of ~$10,000 WAC per patient, assuming 1.2M patients on CGRP mAbs, 55% responders (>50% reduction in MMD), 25% partial response (>30% reduction in MMD), and 20% failures (<30% reduction in MMD) Sources: 2024 Ashina (NEJM); 2026 Buse (Neurol. Ther); 2023 Guo (Neurol of Disease); 2021 Kuburas (J. Neurosci.); 2023 Kuburas (J Headache and Pain); 2022 Overeem (Cephalgia); 2021 Amiri (Front Neurol); Lundbeck Press Release (Feb 2026); Emgality, Ajovy, Vyepti, Aimovig FDA labels; GlobalData; Internal data; KOL interviews. We believe the Mentari portfolio is designed to lead the next wave of migraine prevention therapies Programs: MT-001 & MT-002 Market opportunity in CGRP inadequate and non-responders Upside potential in broader migraine by redefining treatment paradigm $5B+ $10B+ Opportunity for improvement on convenience and efficacy for CGRP inadequate & non-responders Proof-of-concept established for anti-PACAP Potential for synergy of anti-PACAP and anti-CGRP based on complementary pathways Superior efficacy compared to CGRP may drive adoption in earlier lines of preventive care Programs: MT-002 & combinations

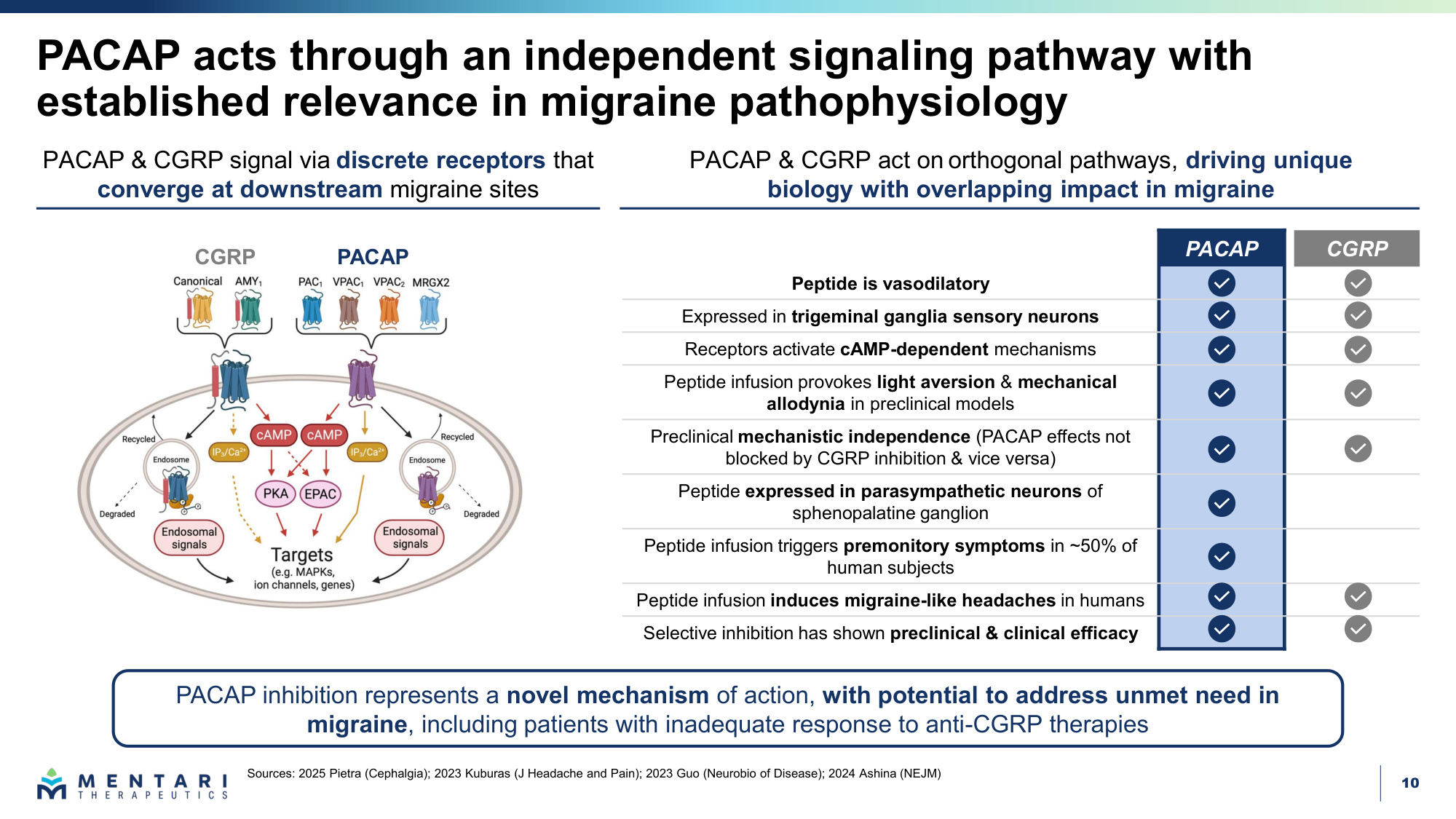

10 PACAP acts through an independent signaling pathway with established relevance in migraine pathophysiology Sources: 2025 Pietra (Cephalgia); 2023 Kuburas (J Headache and Pain); 2023 Guo (Neurobio of Disease); 2024 Ashina (NEJM) PACAP & CGRP signal via discrete receptors that converge at downstream migraine sites PACAP CGRP Peptide is vasodilatory Expressed in trigeminal ganglia sensory neurons Receptors activate cAMP-dependent mechanisms Peptide infusion provokes light aversion & mechanical allodynia in preclinical models Preclinical mechanistic independence (PACAP effects not blocked by CGRP inhibition & vice versa) Peptide expressed in parasympathetic neurons of sphenopalatine ganglion Peptide infusion triggers premonitory symptoms in ~50% of human subjects Peptide infusion induces migraine-like headaches in humans Selective inhibition has shown preclinical & clinical efficacy PACAP & CGRP act on orthogonal pathways, driving unique biology with overlapping impact in migraine PACAP CGRP PACAP inhibition represents a novel mechanism of action, with potential to address unmet need in migraine, including patients with inadequate response to anti-CGRP therapies

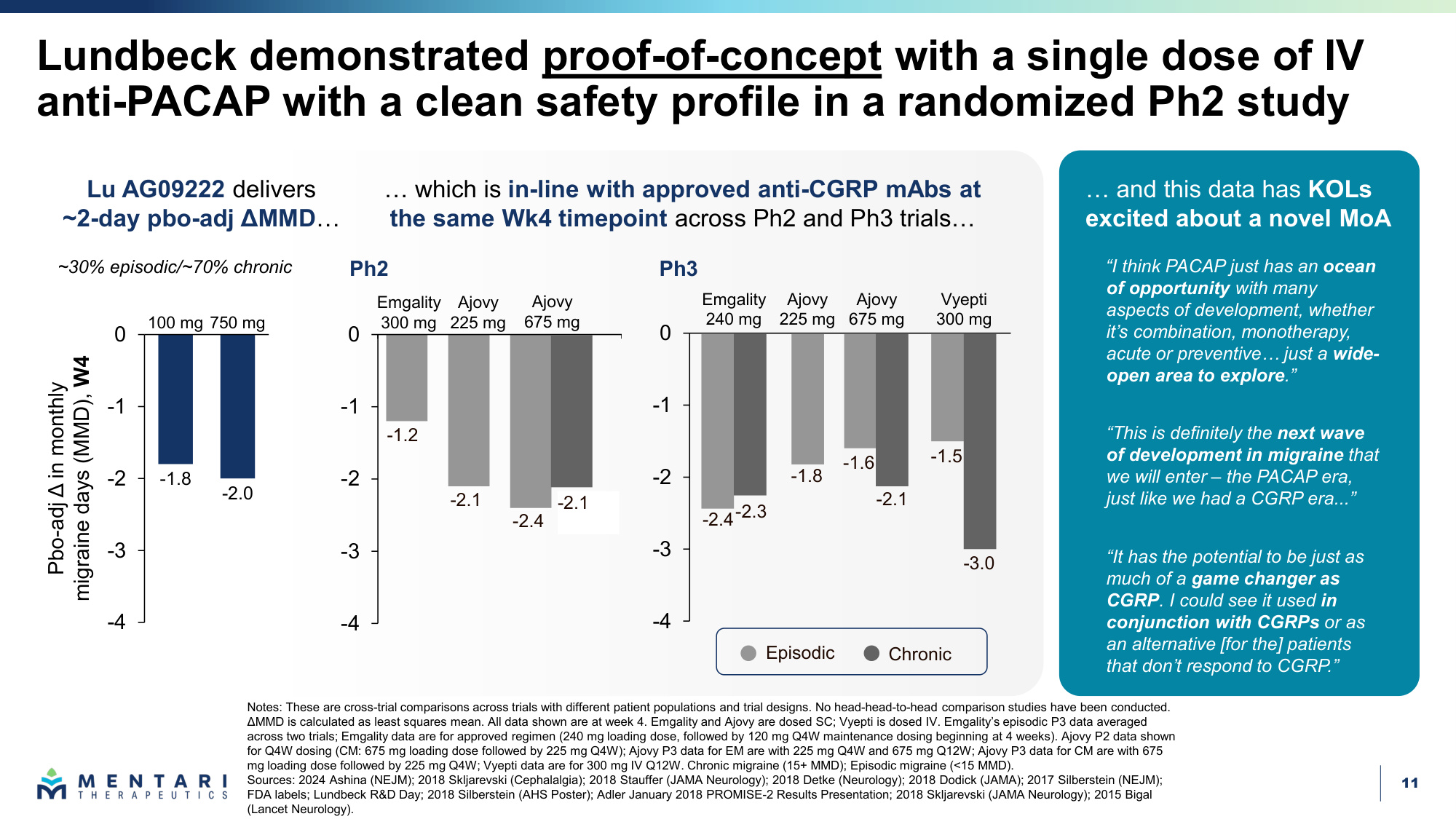

11 -4 -3 -2 -1 0 Lundbeck demonstrated proof-of-concept with a single dose of IV anti-PACAP with a clean safety profile in a randomized Ph2 study Notes: These are cross-trial comparisons across trials with different patient populations and trial designs. No head-head-to-head comparison studies have been conducted. ΔMMD is calculated as least squares mean. All data shown are at week 4. Emgality and Ajovy are dosed SC; Vyepti is dosed IV. Emgality's episodic P3 data averaged across two trials; Emgality data are for approved regimen (240 mg loading dose, followed by 120 mg Q4W maintenance dosing beginning at 4 weeks). Ajovy P2 data shown for Q4W dosing (CM: 675 mg loading dose followed by 225 mg Q4W); Ajovy P3 data for EM are with 225 mg Q4W and 675 mg Q12W; Ajovy P3 data for CM are with 675 mg loading dose followed by 225 mg Q4W; Vyepti data are for 300 mg IV Q12W. Chronic migraine (15+ MMD); Episodic migraine (<15 MMD). Sources: 2024 Ashina (NEJM); 2018 Skljarevski (Cephalalgia); 2018 Stauffer (JAMA Neurology); 2018 Detke (Neurology); 2018 Dodick (JAMA); 2017 Silberstein (NEJM); FDA labels; Lundbeck R&D Day; 2018 Silberstein (AHS Poster); Adler January 2018 PROMISE-2 Results Presentation; 2018 Skljarevski (JAMA Neurology); 2015 Bigal (Lancet Neurology). Ajovy 675 mg Vyepti 300 mg Emgality 240 mg Ajovy 225 mg -2.4-2.3 -1.8 -2.1 -1.5 -3.0 -1.6 -1.8 -2.0 -4 -3 -2 -1 0 Pbo-adj Δ in monthly migraine days (MMD), W4 750 mg 100 mg Emgality 300 mg Ajovy 225 mg Ajovy 675 mg ~30% episodic/~70% chronic -1.2 -2.1 -2.4 -2.1 Ph2 Ph3 Lu AG09222 delivers ~2-day pbo-adj ΔMMD... ... which is in-line with approved anti-CGRP mAbs at the same Wk4 timepoint across Ph2 and Ph3 trials... "This is definitely the next wave of development in migraine that we will enter – the PACAP era, just like we had a CGRP era..." "I think PACAP just has an ocean of opportunity with many aspects of development, whether it's combination, monotherapy, acute or preventive... just a wide- open area to explore." "It has the potential to be just as much of a game changer as CGRP. I could see it used in conjunction with CGRPs or as an alternative [for the] patients that don't respond to CGRP." ... and this data has KOLs excited about a novel MoA Episodic Chronic -4 -3 -2 -1 0 -2.1

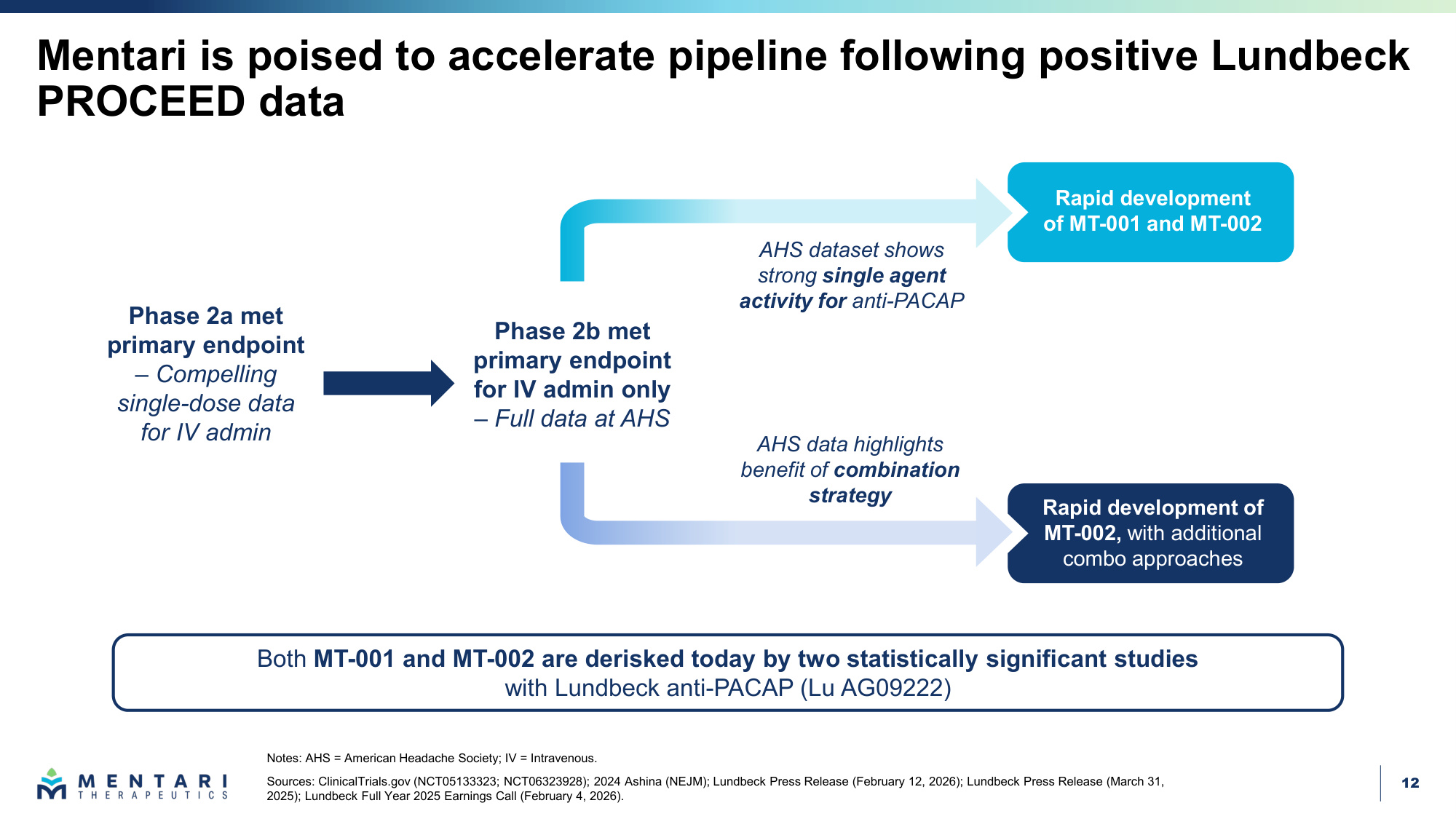

12 Mentari is poised to accelerate pipeline following positive Lundbeck PROCEED data Phase 2b met primary endpoint for IV admin only – Full data at AHS Rapid development of MT-001 and MT-002 AHS data highlights benefit of combination strategy AHS dataset shows strong single agent activity for anti-PACAP Rapid development of MT-002, with additional combo approaches Phase 2a met primary endpoint – Compelling single-dose data for IV admin Notes: AHS = American Headache Society; IV = Intravenous. Sources: ClinicalTrials.gov (NCT05133323; NCT06323928); 2024 Ashina (NEJM); Lundbeck Press Release (February 12, 2026); Lundbeck Press Release (March 31, 2025); Lundbeck Full Year 2025 Earnings Call (February 4, 2026). Both MT-001 and MT-002 are derisked today by two statistically significant studies with Lundbeck anti-PACAP (Lu AG09222)

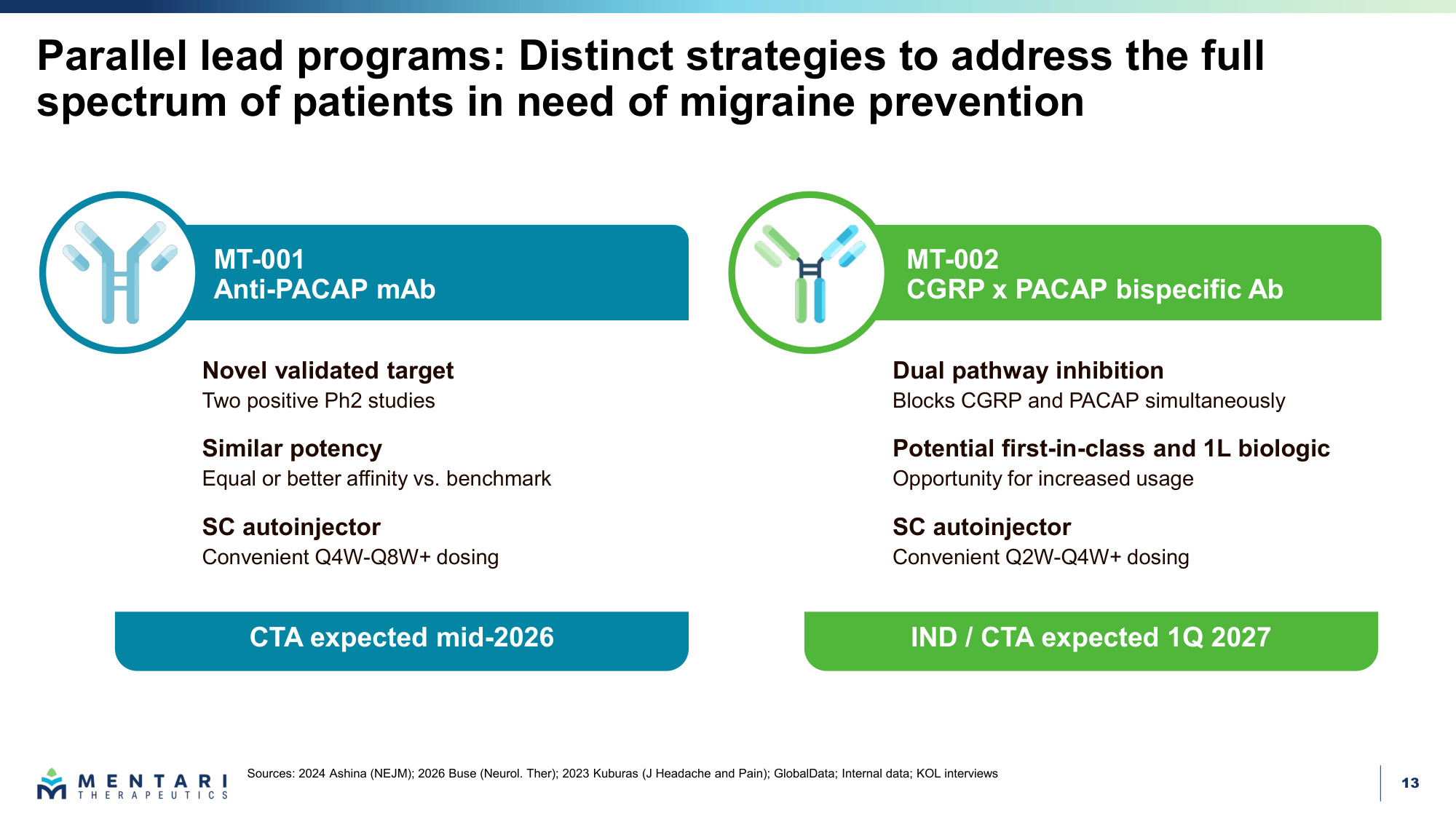

13 MT-002 CGRP x PACAP bispecific Ab MT-001 Anti-PACAP mAb Parallel lead programs: Distinct strategies to address the full spectrum of patients in need of migraine prevention Sources: 2024 Ashina (NEJM); 2026 Buse (Neurol. Ther); 2023 Kuburas (J Headache and Pain); GlobalData; Internal data; KOL interviews Dual pathway inhibition Blocks CGRP and PACAP simultaneously Potential first-in-class and 1L biologic Opportunity for increased usage SC autoinjector Convenient Q2W-Q4W+ dosing Novel validated target Two positive Ph2 studies Similar potency Equal or better affinity vs. benchmark SC autoinjector Convenient Q4W-Q8W+ dosing IND / CTA expected 1Q 2027 CTA expected mid-2026

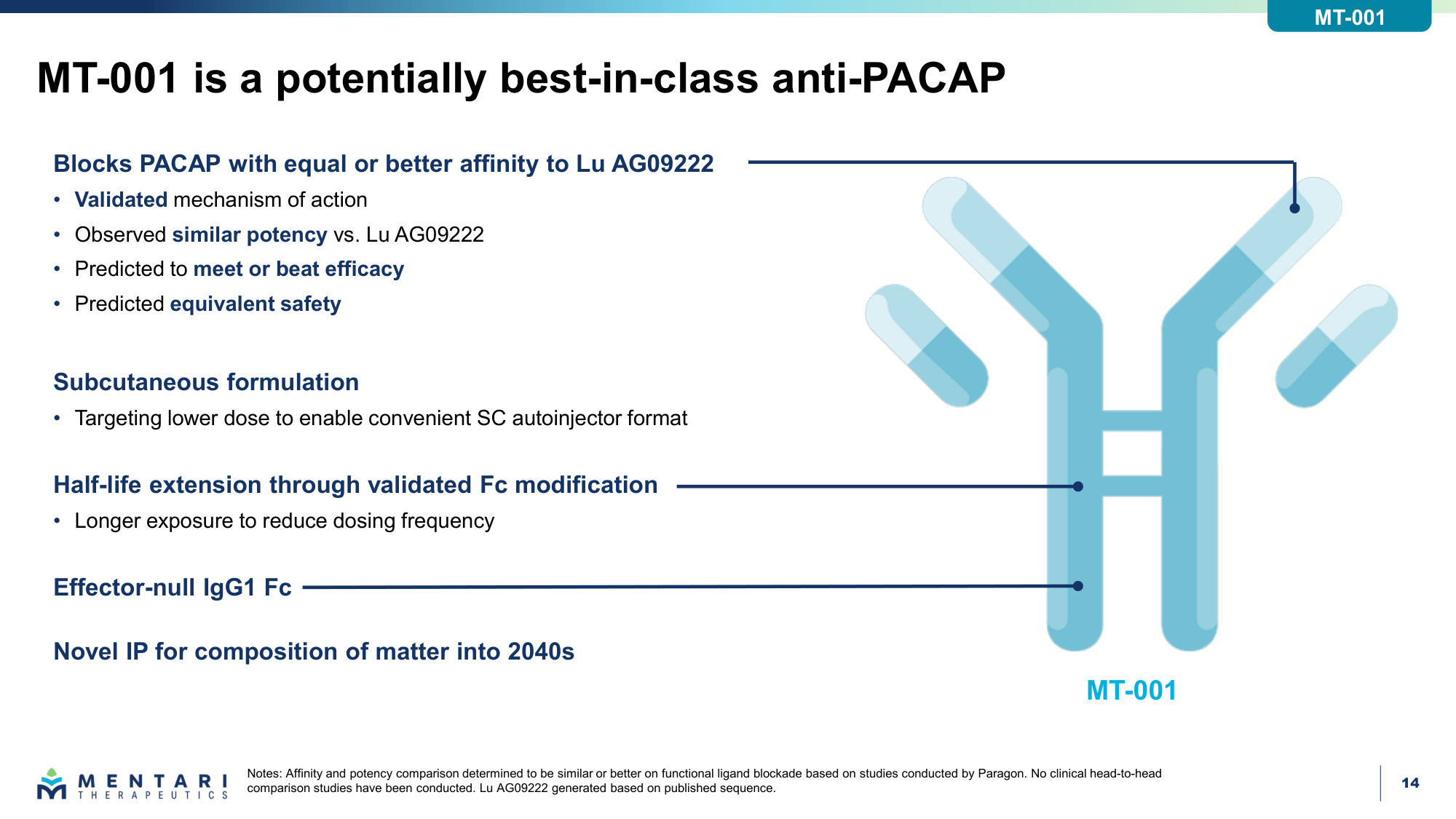

14 MT-001 is a potentially best-in-class anti-PACAP Notes: Affinity and potency comparison determined to be similar or better on functional ligand blockade based on studies conducted by Paragon. No clinical head-to-head comparison studies have been conducted. Lu AG09222 generated based on published sequence. Blocks PACAP with equal or better affinity to Lu AG09222 • Validated mechanism of action • Observed similar potency vs. Lu AG09222 • Predicted to meet or beat efficacy • Predicted equivalent safety Novel IP for composition of matter into 2040s Effector-null IgG1 Fc Half-life extension through validated Fc modification • Longer exposure to reduce dosing frequency MT-001 Subcutaneous formulation • Targeting lower dose to enable convenient SC autoinjector format MT-001

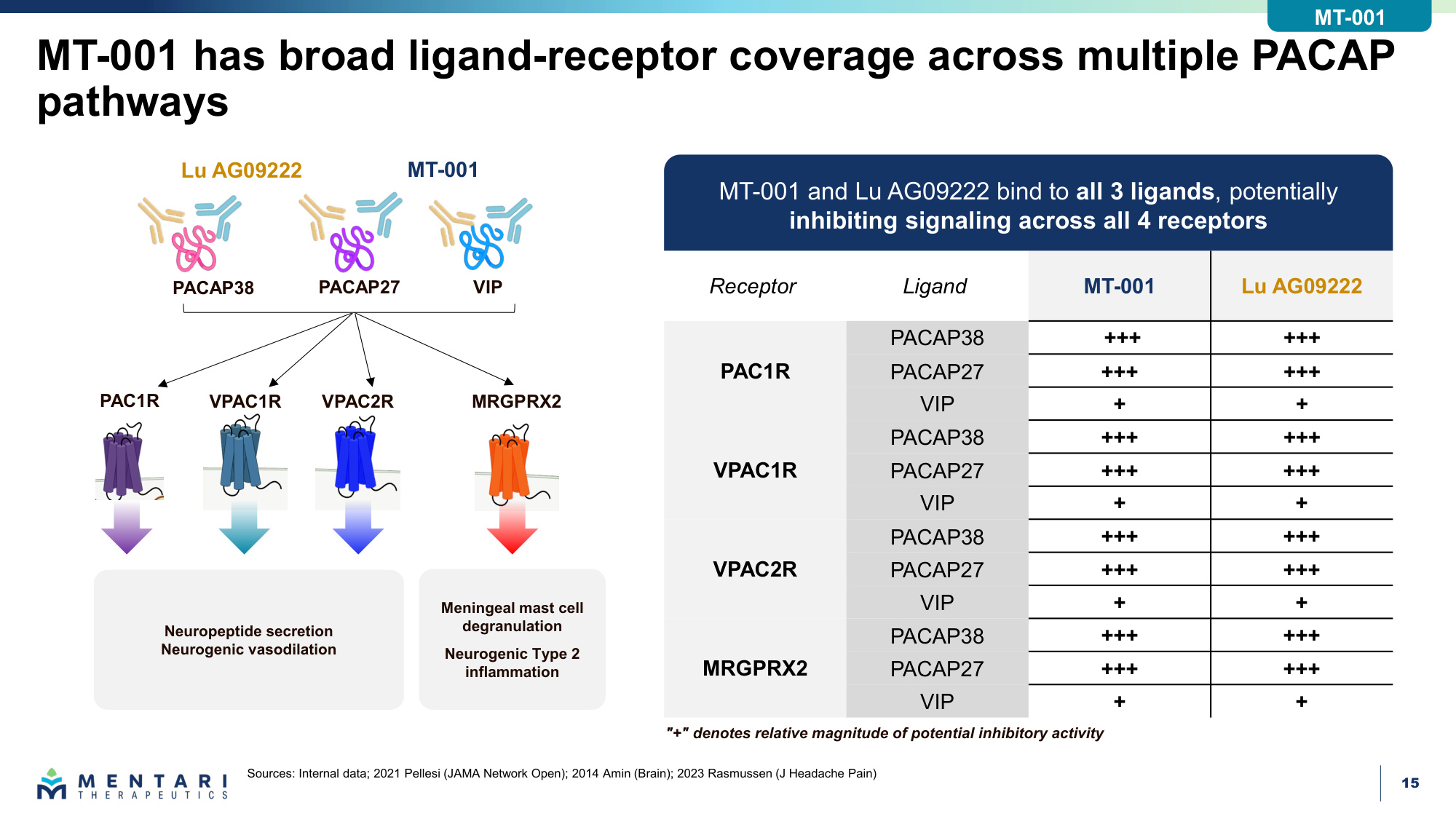

15 MT-001 has broad ligand-receptor coverage across multiple PACAP pathways Sources: Internal data; 2021 Pellesi (JAMA Network Open); 2014 Amin (Brain); 2023 Rasmussen (J Headache Pain) "+" denotes relative magnitude of potential inhibitory activity Meningeal mast cell degranulation Neurogenic Type 2 inflammation Neuropeptide secretion Neurogenic vasodilation PACAP38 PACAP27 VIP Lu AG09222 MT-001 Receptor Ligand MT-001 Lu AG09222 PAC1R PACAP38 +++ +++ PACAP27 +++ +++ VIP + + VPAC1R PACAP38 +++ +++ PACAP27 +++ +++ VIP + + VPAC2R PACAP38 +++ +++ PACAP27 +++ +++ VIP + + MRGPRX2 PACAP38 +++ +++ PACAP27 +++ +++ VIP + + MT-001 and Lu AG09222 bind to all 3 ligands, potentially inhibiting signaling across all 4 receptors PAC1R VPAC1R VPAC2R MRGPRX2 MT-001

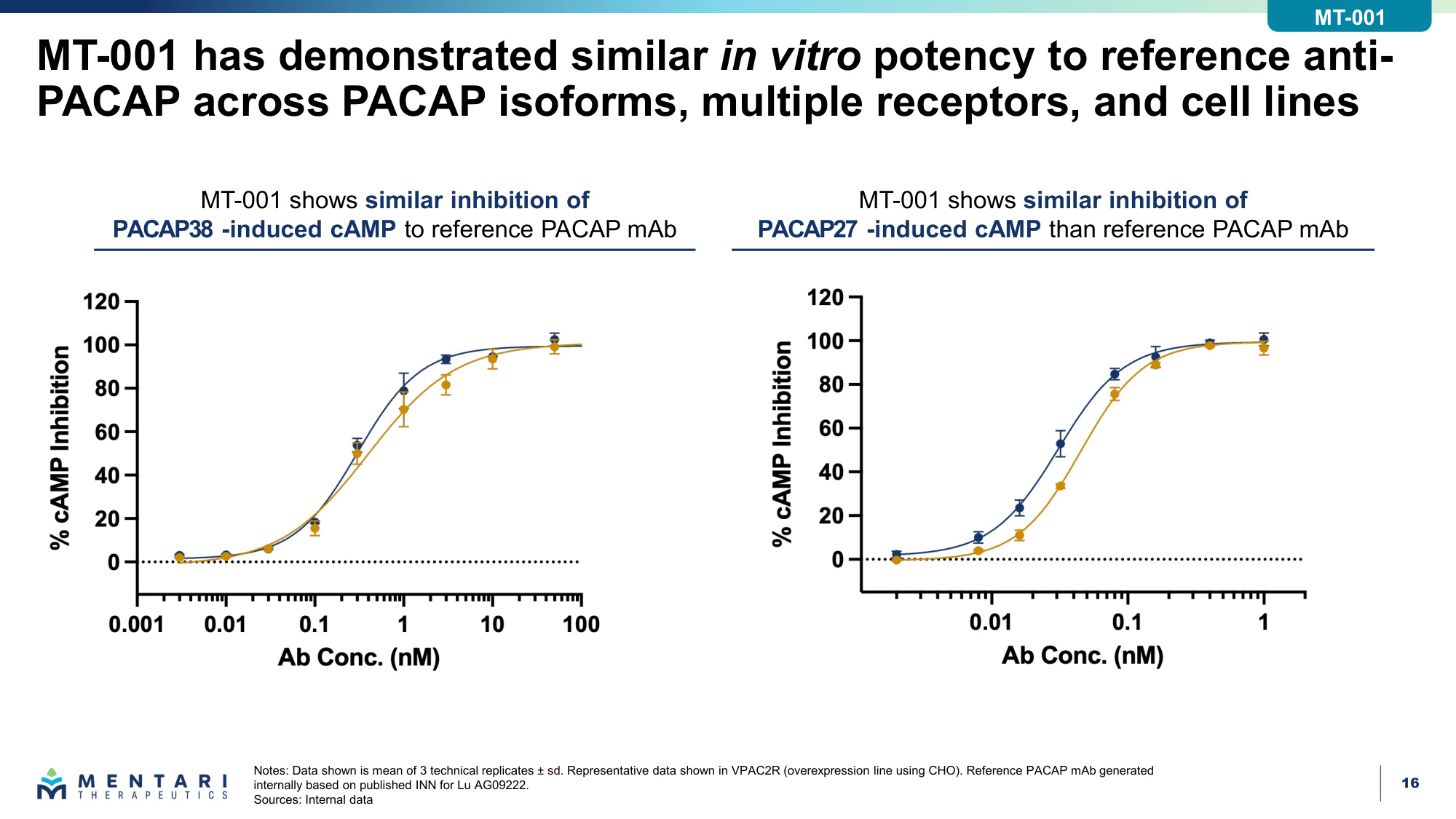

16 MT-001 has demonstrated similar in vitro potency to reference anti- PACAP across PACAP isoforms, multiple receptors, and cell lines Notes: Data shown is mean of 3 technical replicates ± sd. Representative data shown in VPAC2R (overexpression line using CHO). Reference PACAP mAb generated internally based on published INN for Lu AG09222. Sources: Internal data MT-001 shows similar inhibition of PACAP38 -induced cAMP to reference PACAP mAb MT-001 shows similar inhibition of PACAP27 -induced cAMP than reference PACAP mAb MT-001

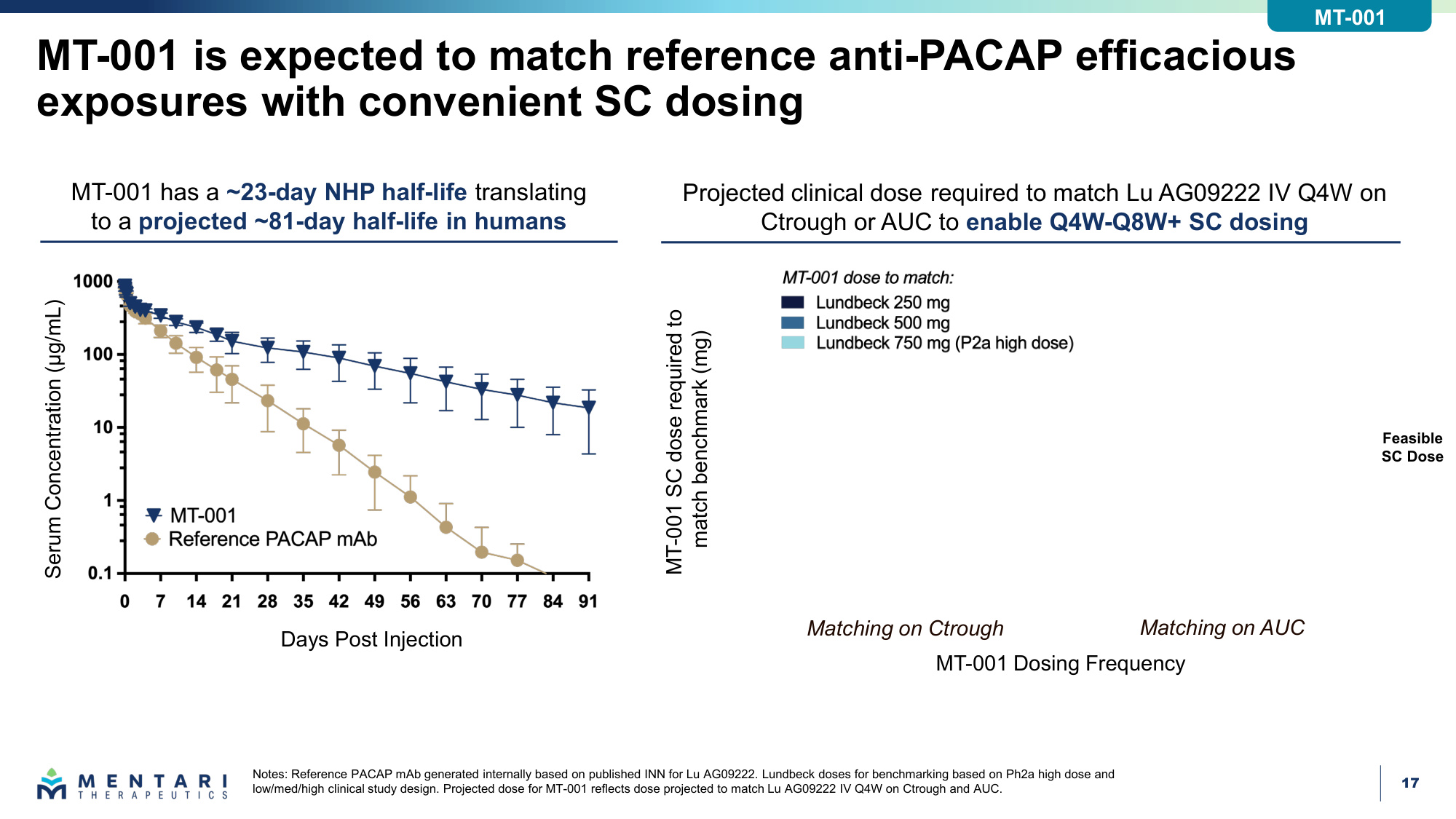

17 MT-001 is expected to match reference anti-PACAP efficacious exposures with convenient SC dosing Notes: Reference PACAP mAb generated internally based on published INN for Lu AG09222. Lundbeck doses for benchmarking based on Ph2a high dose and low/med/high clinical study design. Projected dose for MT-001 reflects dose projected to match Lu AG09222 IV Q4W on Ctrough and AUC. MT-001 has a ~23-day NHP half-life translating to a projected ~81-day half-life in humans Serum Concentration (μg/mL) Days Post Injection MT-001 Dosing Frequency MT-001 SC dose required to match benchmark (mg) Projected clinical dose required to match Lu AG09222 IV Q4W on Ctrough or AUC to enable Q4W-Q8W+ SC dosing Feasible SC Dose Matching on Ctrough Matching on AUC MT-001

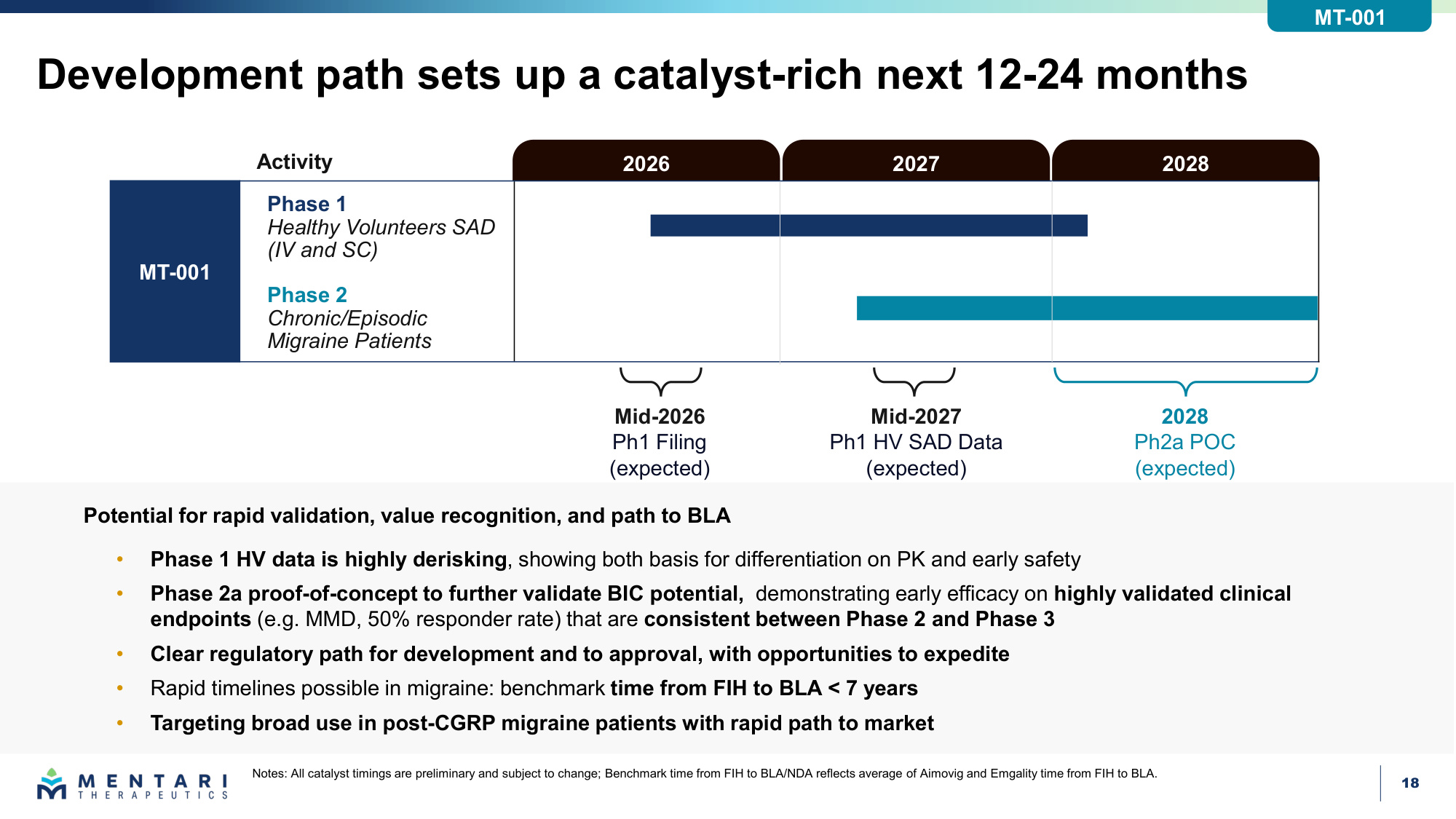

18 Development path sets up a catalyst-rich next 12-24 months Notes: All catalyst timings are preliminary and subject to change; Benchmark time from FIH to BLA/NDA reflects average of Aimovig and Emgality time from FIH to BLA. Activity Phase 2 Chronic/Episodic Migraine Patients Phase 1 Healthy Volunteers SAD (IV and SC) MT-001 Potential for rapid validation, value recognition, and path to BLA • Phase 1 HV data is highly derisking, showing both basis for differentiation on PK and early safety • Phase 2a proof-of-concept to further validate BIC potential, demonstrating early efficacy on highly validated clinical endpoints (e.g. MMD, 50% responder rate) that are consistent between Phase 2 and Phase 3 • Clear regulatory path for development and to approval, with opportunities to expedite • Rapid timelines possible in migraine: benchmark time from FIH to BLA < 7 years • Targeting broad use in post-CGRP migraine patients with rapid path to market Mid-2026 Ph1 Filing (expected) 2028 Ph2a POC (expected) Mid-2027 Ph1 HV SAD Data (expected) 2028 2027 2026 MT-001

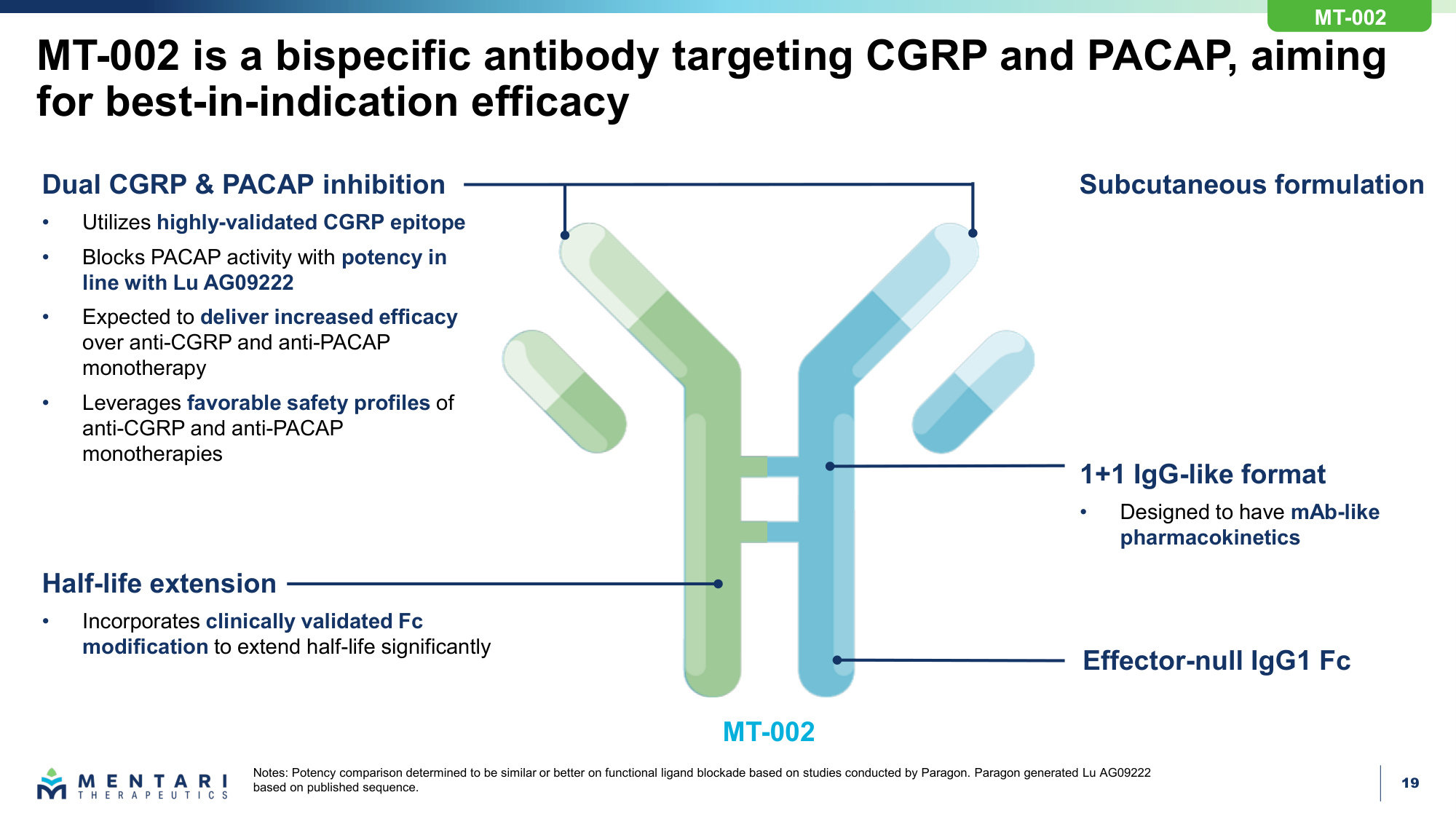

19 MT-002 is a bispecific antibody targeting CGRP and PACAP, aiming for best-in-indication efficacy Notes: Potency comparison determined to be similar or better on functional ligand blockade based on studies conducted by Paragon. Paragon generated Lu AG09222 based on published sequence. Dual CGRP & PACAP inhibition • Utilizes highly-validated CGRP epitope • Blocks PACAP activity with potency in line with Lu AG09222 • Expected to deliver increased efficacy over anti-CGRP and anti-PACAP monotherapy • Leverages favorable safety profiles of anti-CGRP and anti-PACAP monotherapies Half-life extension • Incorporates clinically validated Fc modification to extend half-life significantly 1+1 IgG-like format • Designed to have mAb-like pharmacokinetics Subcutaneous formulation Effector-null IgG1 Fc MT-002 MT-002

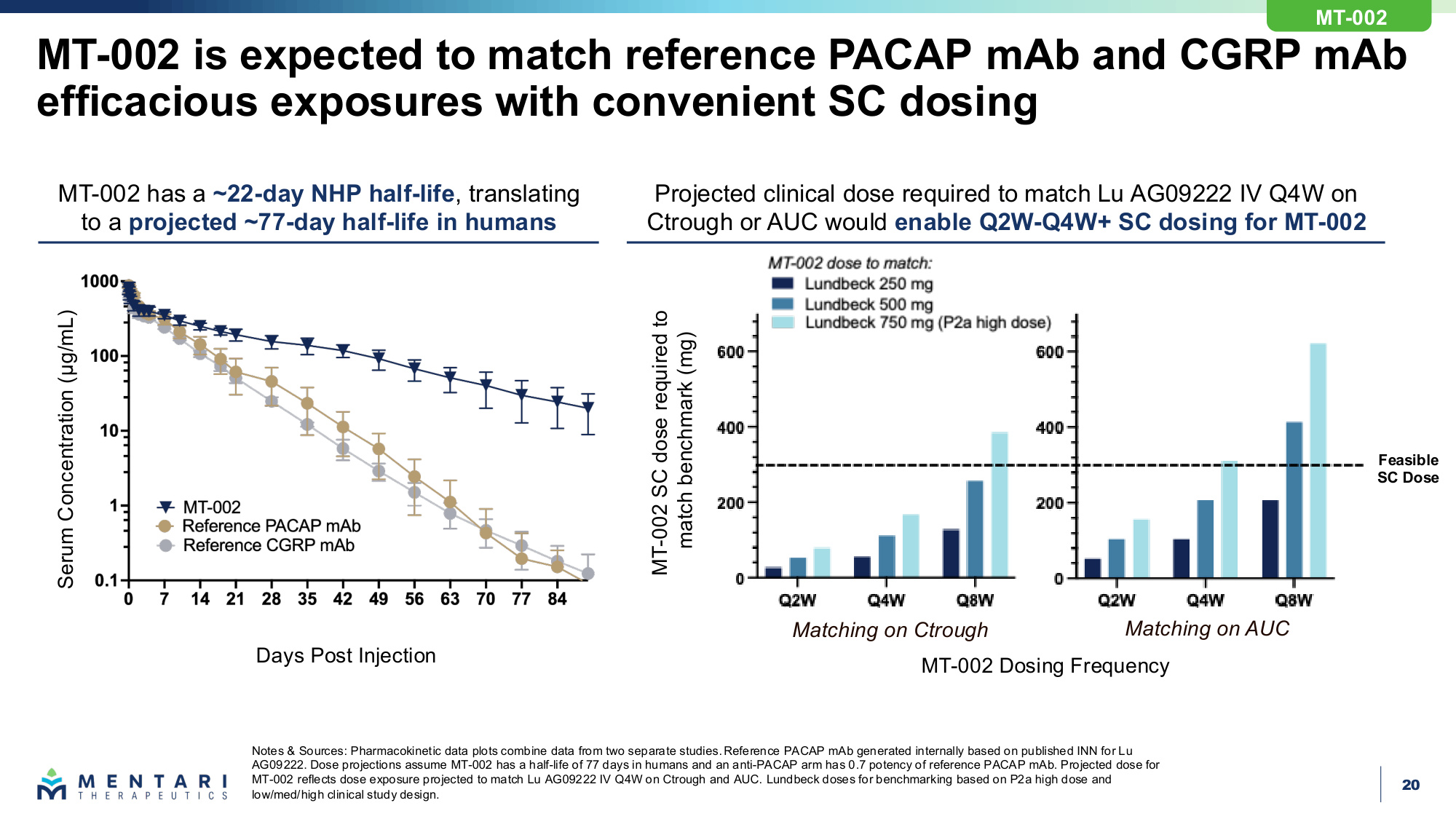

20 MT-002 is expected to match reference PACAP mAb and CGRP mAb efficacious exposures with convenient SC dosing Notes & Sources: Pharmacokinetic data plots combine data from two separate studies. Reference PACAP mAb generated internally based on published INN for Lu AG09222. Dose projections assume MT-002 has a half-life of 77 days in humans and an anti-PACAP arm has 0.7 potency of reference PACAP mAb. Projected dose for MT-002 reflects dose exposure projected to match Lu AG09222 IV Q4W on Ctrough and AUC. Lundbeck doses for benchmarking based on P2a high dose and low/med/high clinical study design. MT-002 has a ~22-day NHP half-life, translating to a projected ~77-day half-life in humans Serum Concentration (μg/mL) Days Post Injection MT-002 Dosing Frequency MT-002 SC dose required to match benchmark (mg) Projected clinical dose required to match Lu AG09222 IV Q4W on Ctrough or AUC would enable Q2W-Q4W+ SC dosing for MT-002 Matching on Ctrough Matching on AUC MT-002 Feasible SC Dose

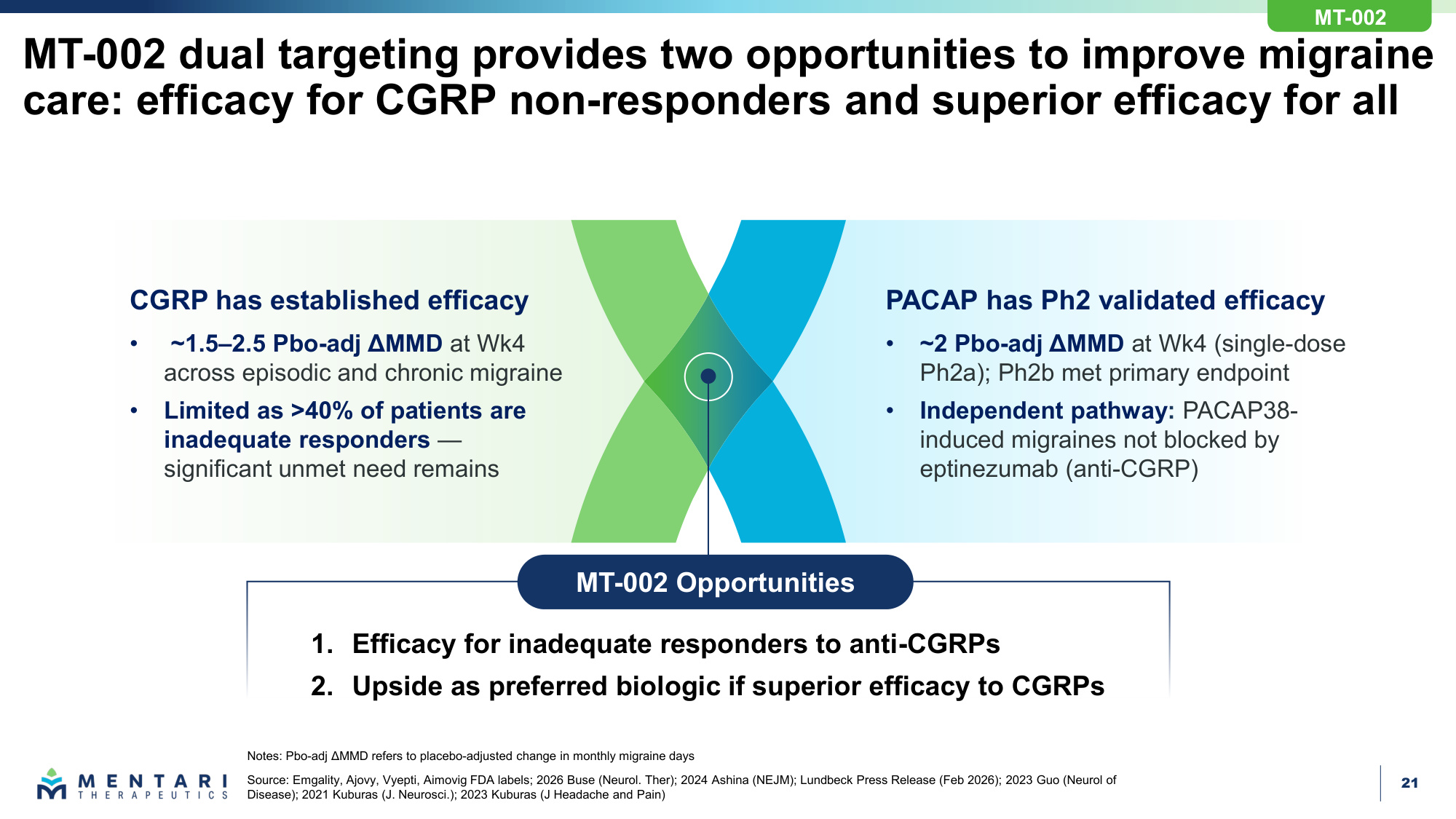

21 Notes: Pbo-adj ΔMMD refers to placebo-adjusted change in monthly migraine days Source: Emgality, Ajovy, Vyepti, Aimovig FDA labels; 2026 Buse (Neurol. Ther); 2024 Ashina (NEJM); Lundbeck Press Release (Feb 2026); 2023 Guo (Neurol of Disease); 2021 Kuburas (J. Neurosci.); 2023 Kuburas (J Headache and Pain) PACAP has Ph2 validated efficacy • ~2 Pbo-adj ΔMMD at Wk4 (single-dose Ph2a); Ph2b met primary endpoint • Independent pathway: PACAP38- induced migraines not blocked by eptinezumab (anti-CGRP) CGRP has established efficacy • ~1.5–2.5 Pbo-adj ΔMMD at Wk4 across episodic and chronic migraine • Limited as >40% of patients are inadequate responders — significant unmet need remains 1. Efficacy for inadequate responders to anti-CGRPs 2. Upside as preferred biologic if superior efficacy to CGRPs MT-002 Opportunities MT-002 dual targeting provides two opportunities to improve migraine care: efficacy for CGRP non-responders and superior efficacy for all MT-002

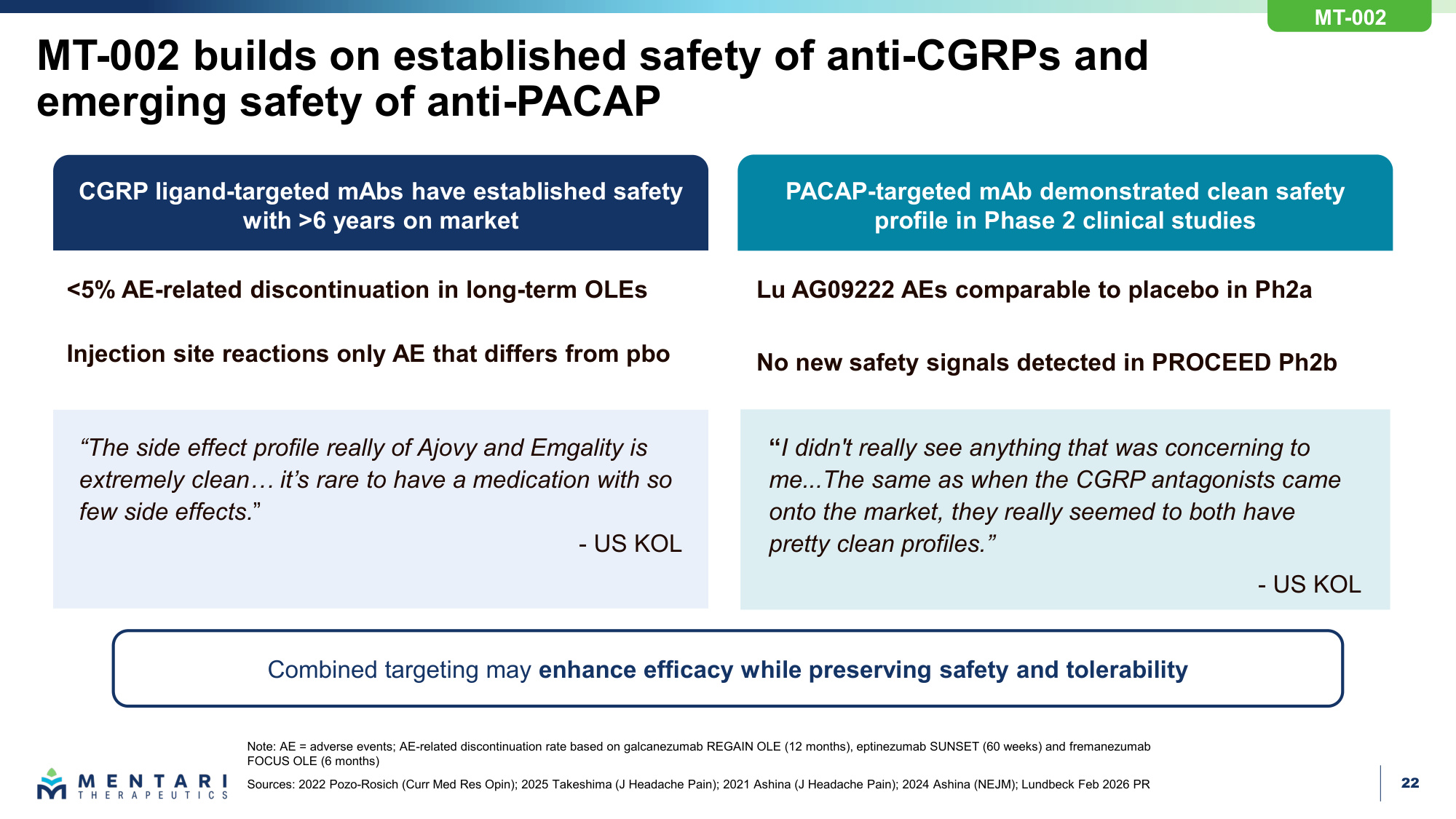

22 MT-002 builds on established safety of anti-CGRPs and emerging safety of anti-PACAP Note: AE = adverse events; AE-related discontinuation rate based on galcanezumab REGAIN OLE (12 months), eptinezumab SUNSET (60 weeks) and fremanezumab FOCUS OLE (6 months) Sources: 2022 Pozo-Rosich (Curr Med Res Opin); 2025 Takeshima (J Headache Pain); 2021 Ashina (J Headache Pain); 2024 Ashina (NEJM); Lundbeck Feb 2026 PR CGRP ligand-targeted mAbs have established safety with >6 years on market PACAP-targeted mAb demonstrated clean safety profile in Phase 2 clinical studies <5% AE-related discontinuation in long-term OLEs Injection site reactions only AE that differs from pbo Lu AG09222 AEs comparable to placebo in Ph2a No new safety signals detected in PROCEED Ph2b Combined targeting may enhance efficacy while preserving safety and tolerability "The side effect profile really of Ajovy and Emgality is extremely clean... it's rare to have a medication with so few side effects." - US KOL "I didn't really see anything that was concerning to me...The same as when the CGRP antagonists came onto the market, they really seemed to both have pretty clean profiles." - US KOL MT-002

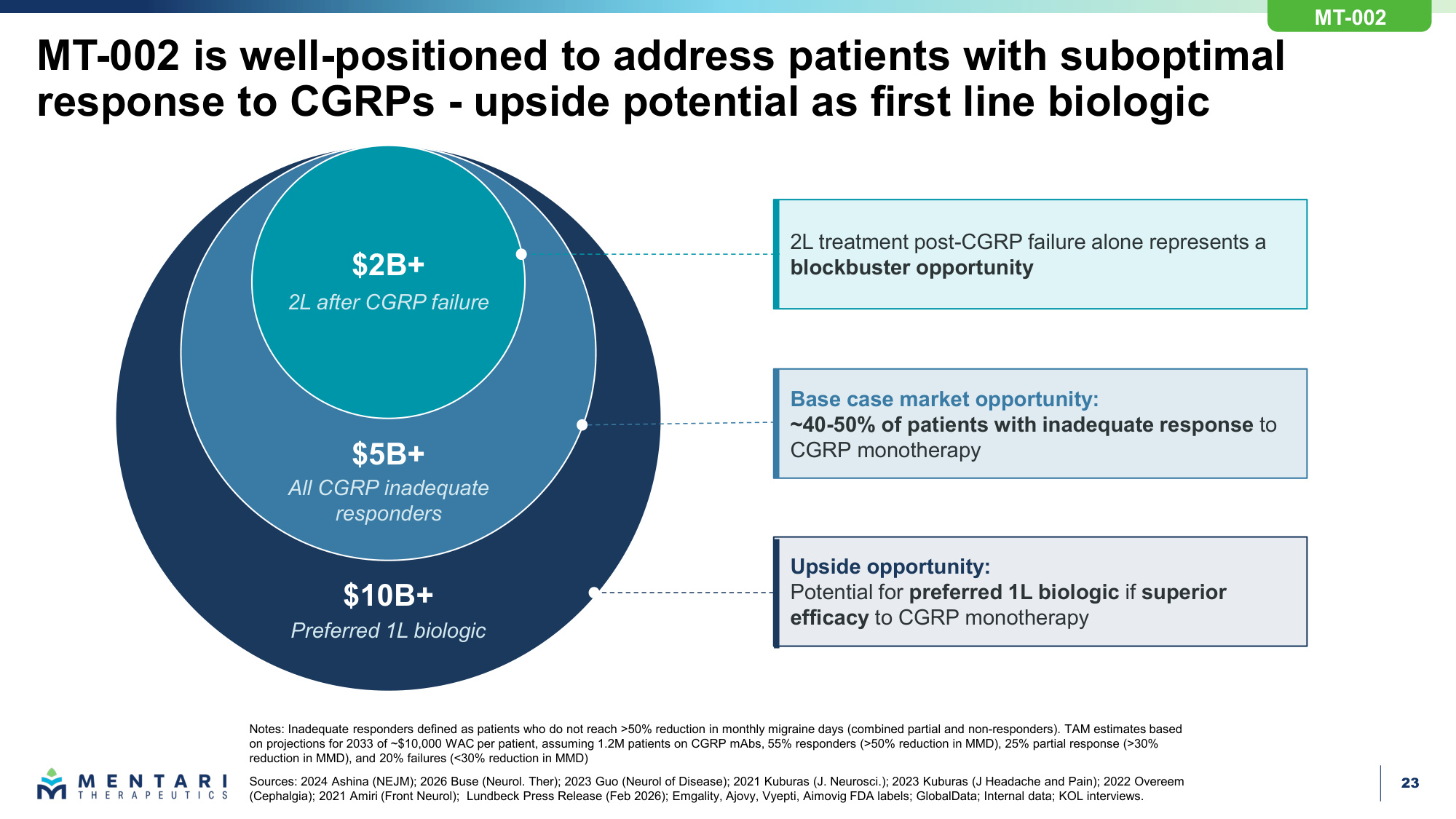

23 $2B+ 2L after CGRP failure $5B+ All CGRP inadequate responders $10B+ Preferred 1L biologic 2L treatment post-CGRP failure alone represents a blockbuster opportunity Base case market opportunity: ~40-50% of patients with inadequate response to CGRP monotherapy Upside opportunity: Potential for preferred 1L biologic if superior efficacy to CGRP monotherapy MT-002 is well-positioned to address patients with suboptimal response to CGRPs - upside potential as first line biologic MT-002 Notes: Inadequate responders defined as patients who do not reach >50% reduction in monthly migraine days (combined partial and non-responders). TAM estimates based on projections for 2033 of ~$10,000 WAC per patient, assuming 1.2M patients on CGRP mAbs, 55% responders (>50% reduction in MMD), 25% partial response (>30% reduction in MMD), and 20% failures (<30% reduction in MMD) Sources: 2024 Ashina (NEJM); 2026 Buse (Neurol. Ther); 2023 Guo (Neurol of Disease); 2021 Kuburas (J. Neurosci.); 2023 Kuburas (J Headache and Pain); 2022 Overeem (Cephalgia); 2021 Amiri (Front Neurol); Lundbeck Press Release (Feb 2026); Emgality, Ajovy, Vyepti, Aimovig FDA labels; GlobalData; Internal data; KOL interviews.

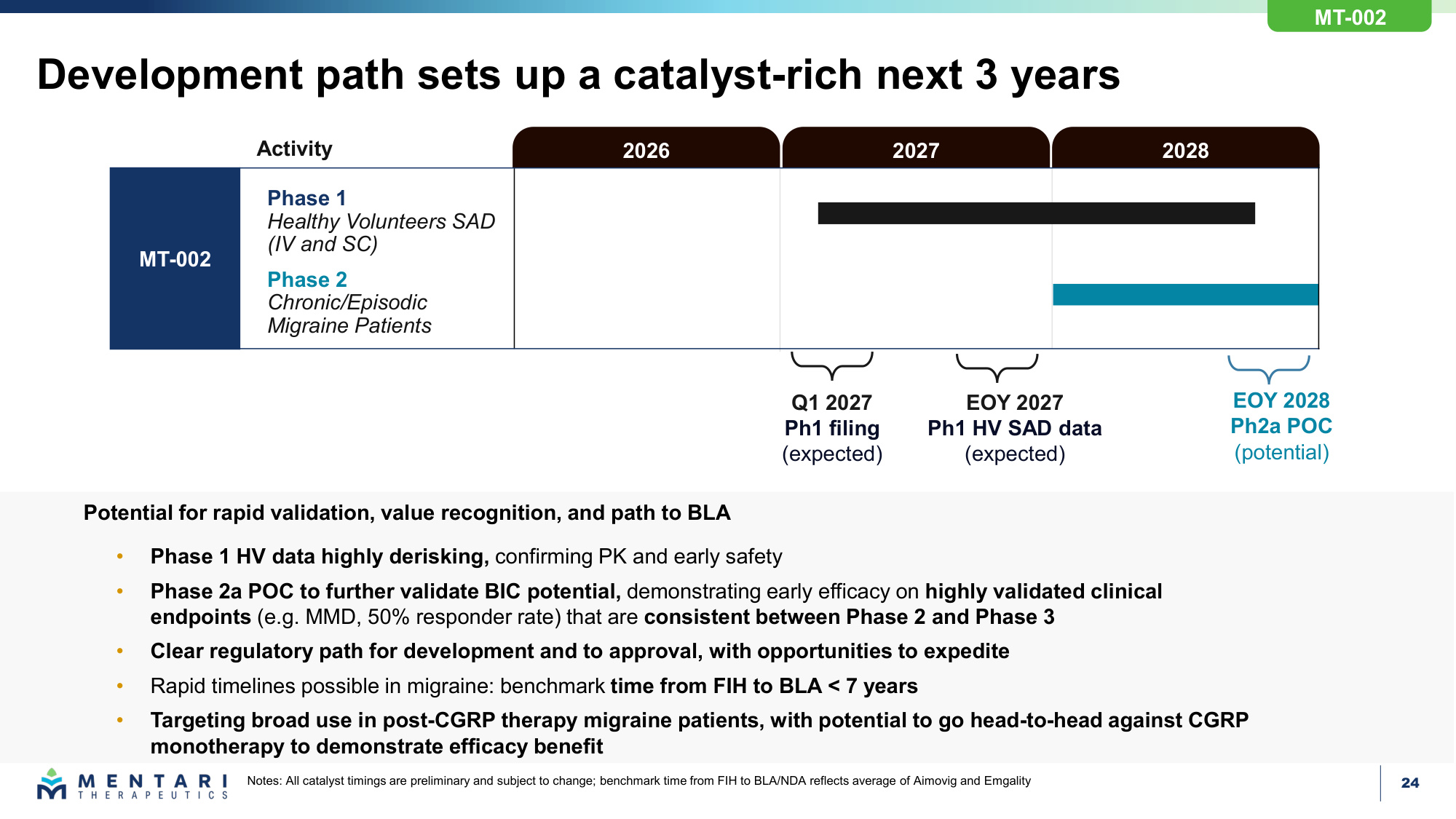

24 Development path sets up a catalyst-rich next 3 years Notes: All catalyst timings are preliminary and subject to change; benchmark time from FIH to BLA/NDA reflects average of Aimovig and Emgality Potential for rapid validation, value recognition, and path to BLA • Phase 1 HV data highly derisking, confirming PK and early safety • Phase 2a POC to further validate BIC potential, demonstrating early efficacy on highly validated clinical endpoints (e.g. MMD, 50% responder rate) that are consistent between Phase 2 and Phase 3 • Clear regulatory path for development and to approval, with opportunities to expedite • Rapid timelines possible in migraine: benchmark time from FIH to BLA < 7 years • Targeting broad use in post-CGRP therapy migraine patients, with potential to go head-to-head against CGRP monotherapy to demonstrate efficacy benefit Activity Phase 2 Chronic/Episodic Migraine Patients Phase 1 Healthy Volunteers SAD (IV and SC) MT-002 2028 2027 2026 Q1 2027 Ph1 filing (expected) EOY 2027 Ph1 HV SAD data (expected) EOY 2028 Ph2a POC (potential) MT-002

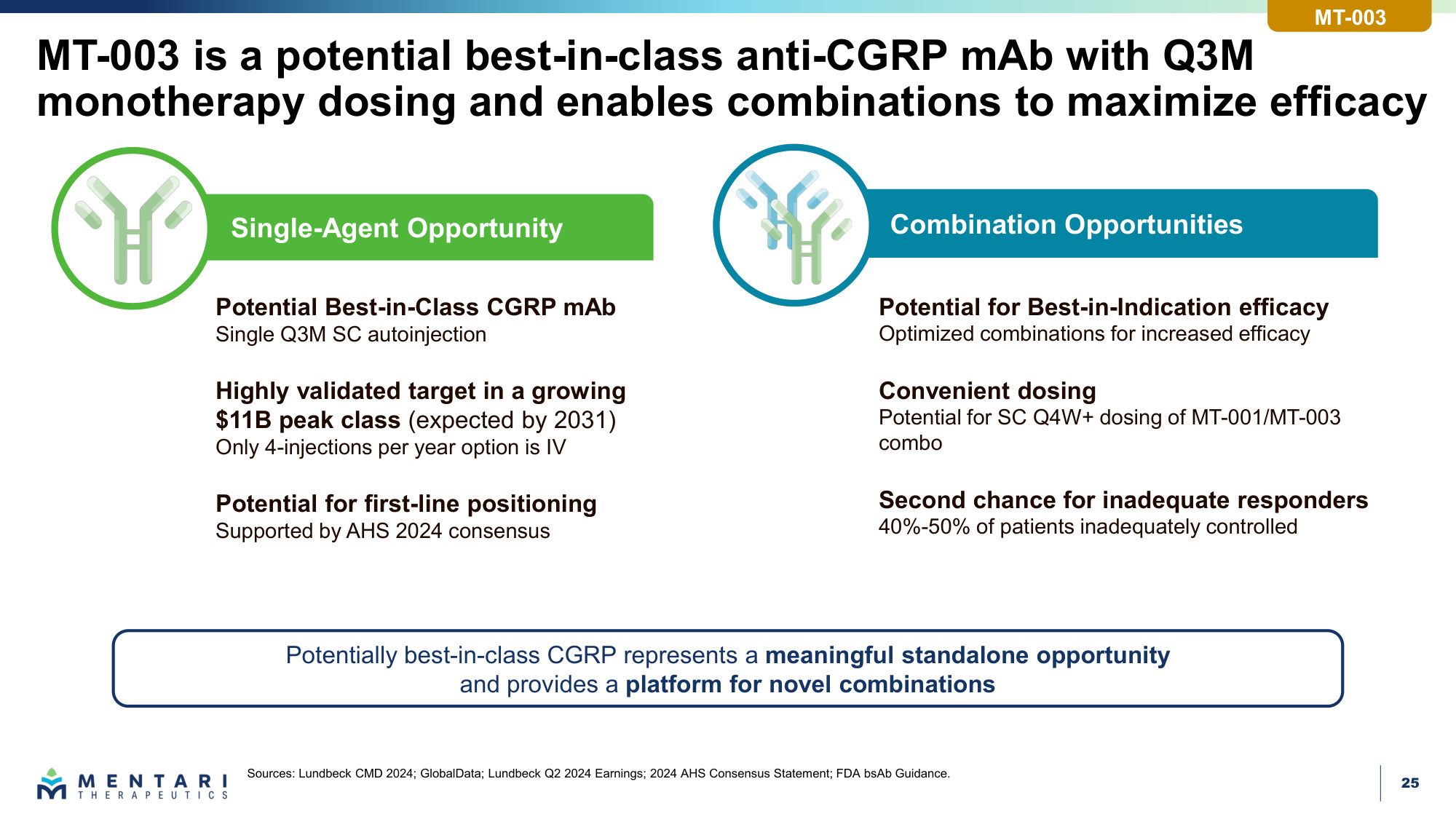

25 Combination Opportunities Single-Agent Opportunity MT-003 is a potential best-in-class anti-CGRP mAb with Q3M monotherapy dosing and enables combinations to maximize efficacy Potential Best-in-Class CGRP mAb Single Q3M SC autoinjection Highly validated target in a growing $11B peak class (expected by 2031) Only 4-injections per year option is IV Potential for first-line positioning Supported by AHS 2024 consensus Potential for Best-in-Indication efficacy Optimized combinations for increased efficacy Convenient dosing Potential for SC Q4W+ dosing of MT-001/MT-003 combo Second chance for inadequate responders 40%-50% of patients inadequately controlled Sources: Lundbeck CMD 2024; GlobalData; Lundbeck Q2 2024 Earnings; 2024 AHS Consensus Statement; FDA bsAb Guidance. Potentially best-in-class CGRP represents a meaningful standalone opportunity and provides a platform for novel combinations MT-003

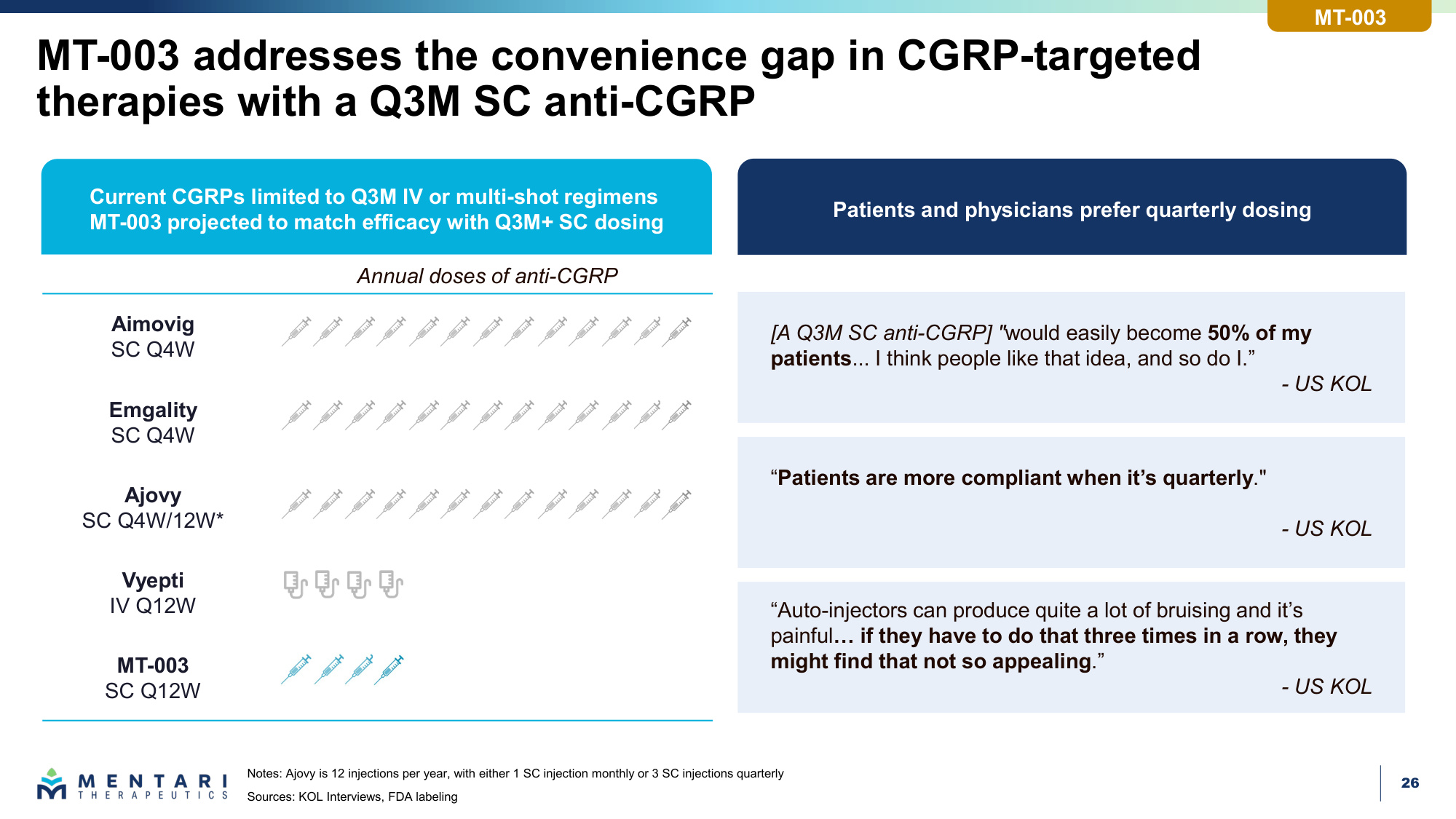

26 "Patients are more compliant when it's quarterly." - US KOL MT-003 addresses the convenience gap in CGRP-targeted therapies with a Q3M SC anti-CGRP Notes: Ajovy is 12 injections per year, with either 1 SC injection monthly or 3 SC injections quarterly Sources: KOL Interviews, FDA labeling [A Q3M SC anti-CGRP] "would easily become 50% of my patients... I think people like that idea, and so do I." - US KOL Annual doses of anti-CGRP Current CGRPs limited to Q3M IV or multi-shot regimens MT-003 projected to match efficacy with Q3M+ SC dosing "Auto-injectors can produce quite a lot of bruising and it's painful... if they have to do that three times in a row, they might find that not so appealing." - US KOL Patients and physicians prefer quarterly dosing Aimovig SC Q4W Emgality SC Q4W Ajovy SC Q4W/12W* Vyepti IV Q12W MT-003 SC Q12W MT-003

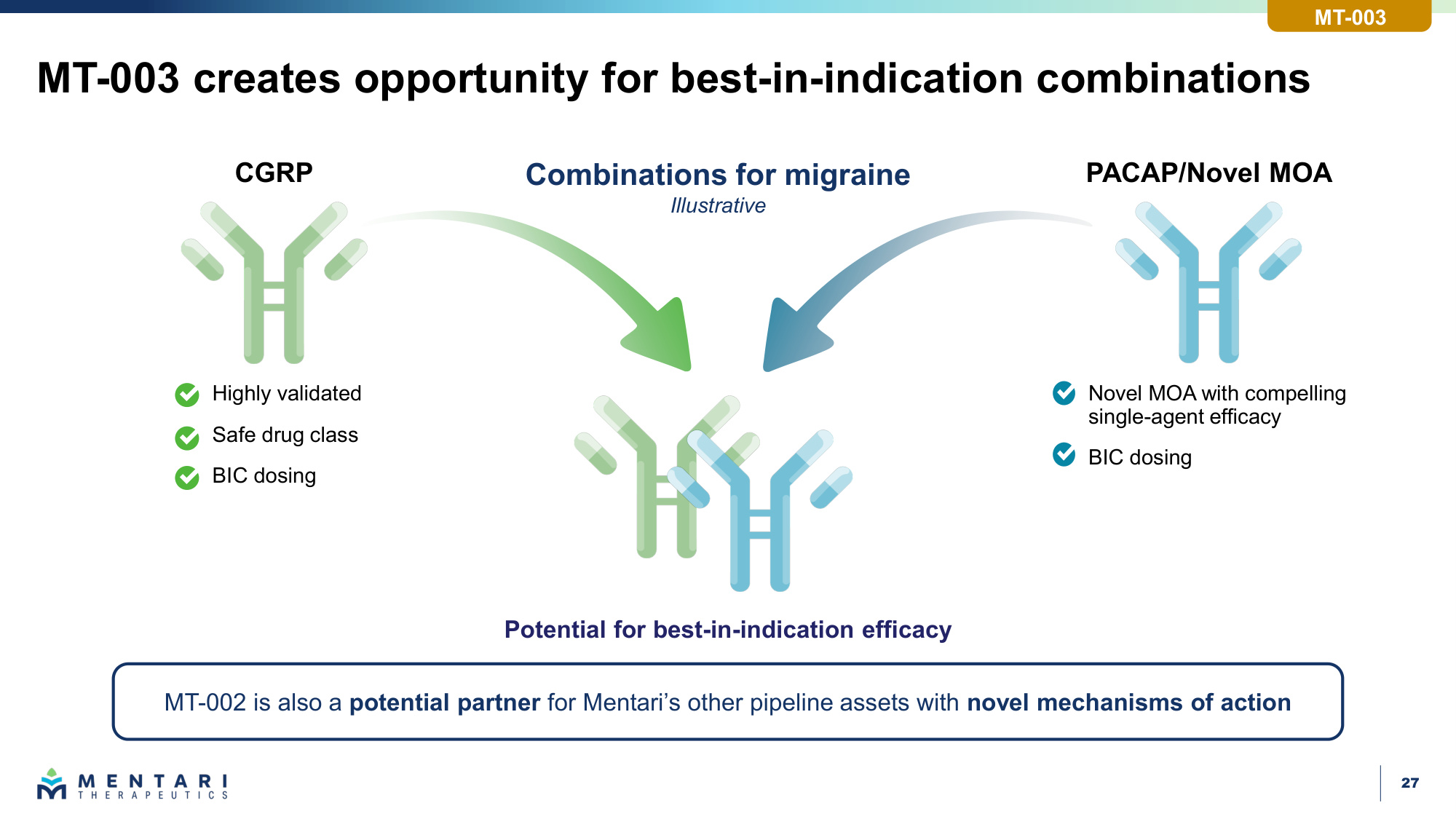

27 MT-003 creates opportunity for best-in-indication combinations Highly validated Safe drug class BIC dosing CGRP Novel MOA with compelling single-agent efficacy BIC dosing PACAP/Novel MOA Potential for best-in-indication efficacy Combinations for migraine Illustrative MT-002 is also a potential partner for Mentari's other pipeline assets with novel mechanisms of action MT-003

28 MT-004 and MT-005 are potentially best-in-class antibodies against novel targets, enabling additional combo approaches in migraine MT-005 1Q27 DC Selection Additional Pipeline Opportunities Differentiated targets in headache disorders: Targets are distinct from CGRP and have preclinical validation Improved design: MT-004 and MT-005 are engineered to be best-in-class Enabling potential best-in-indication combinations Upcoming expected catalysts: MT-004 1Q27 DC Selection

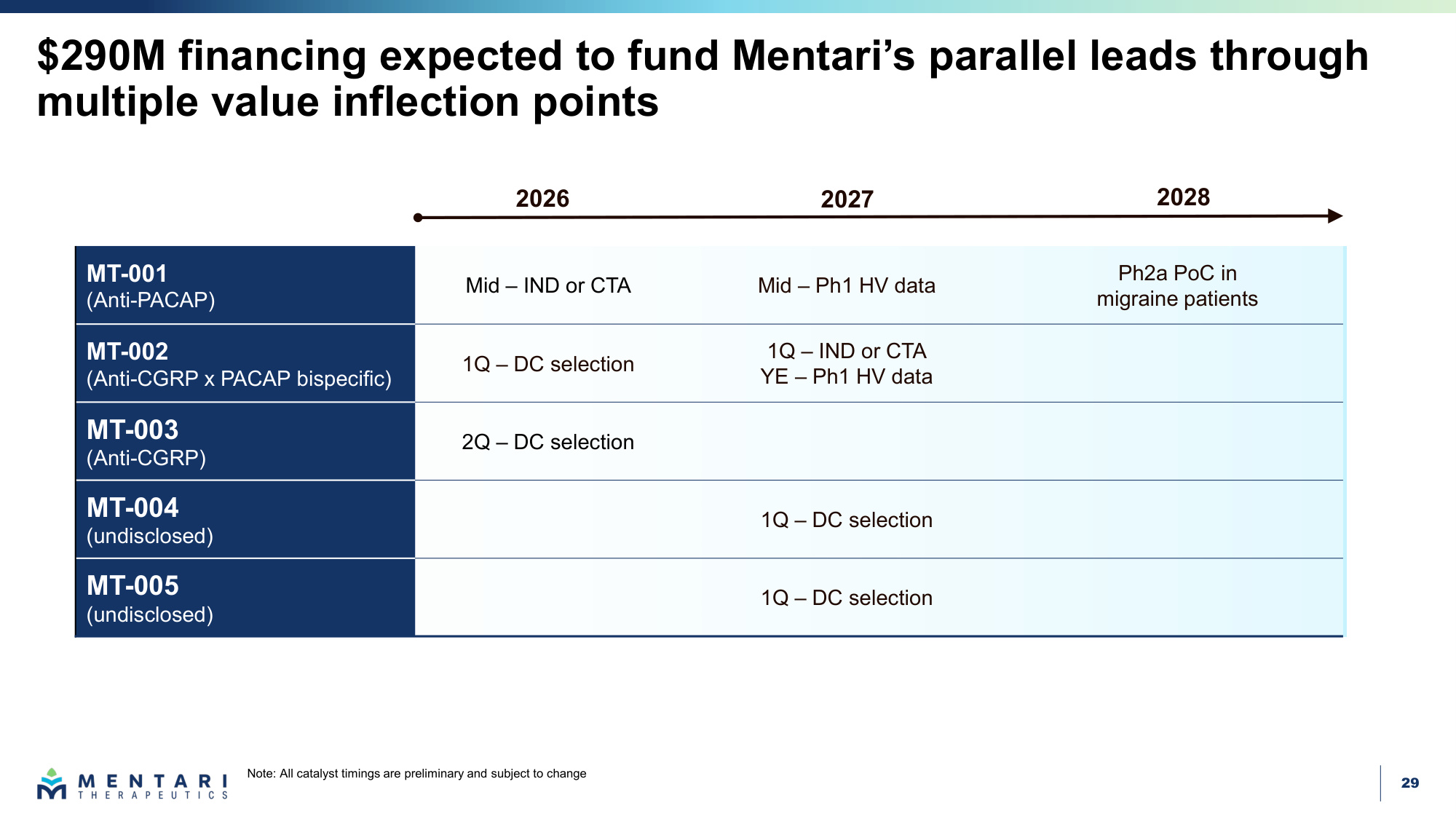

29 MT-001 (Anti-PACAP) Mid – IND or CTA Mid – Ph1 HV data Ph2a PoC in migraine patients MT-002 (Anti-CGRP x PACAP bispecific) 1Q – DC selection 1Q – IND or CTA YE – Ph1 HV data MT-003 (Anti-CGRP) 2Q – DC selection MT-004 (undisclosed) 1Q – DC selection MT-005 (undisclosed) 1Q – DC selection $290M financing expected to fund Mentari's parallel leads through multiple value inflection points 2028 2027 2026 Note: All catalyst timings are preliminary and subject to change

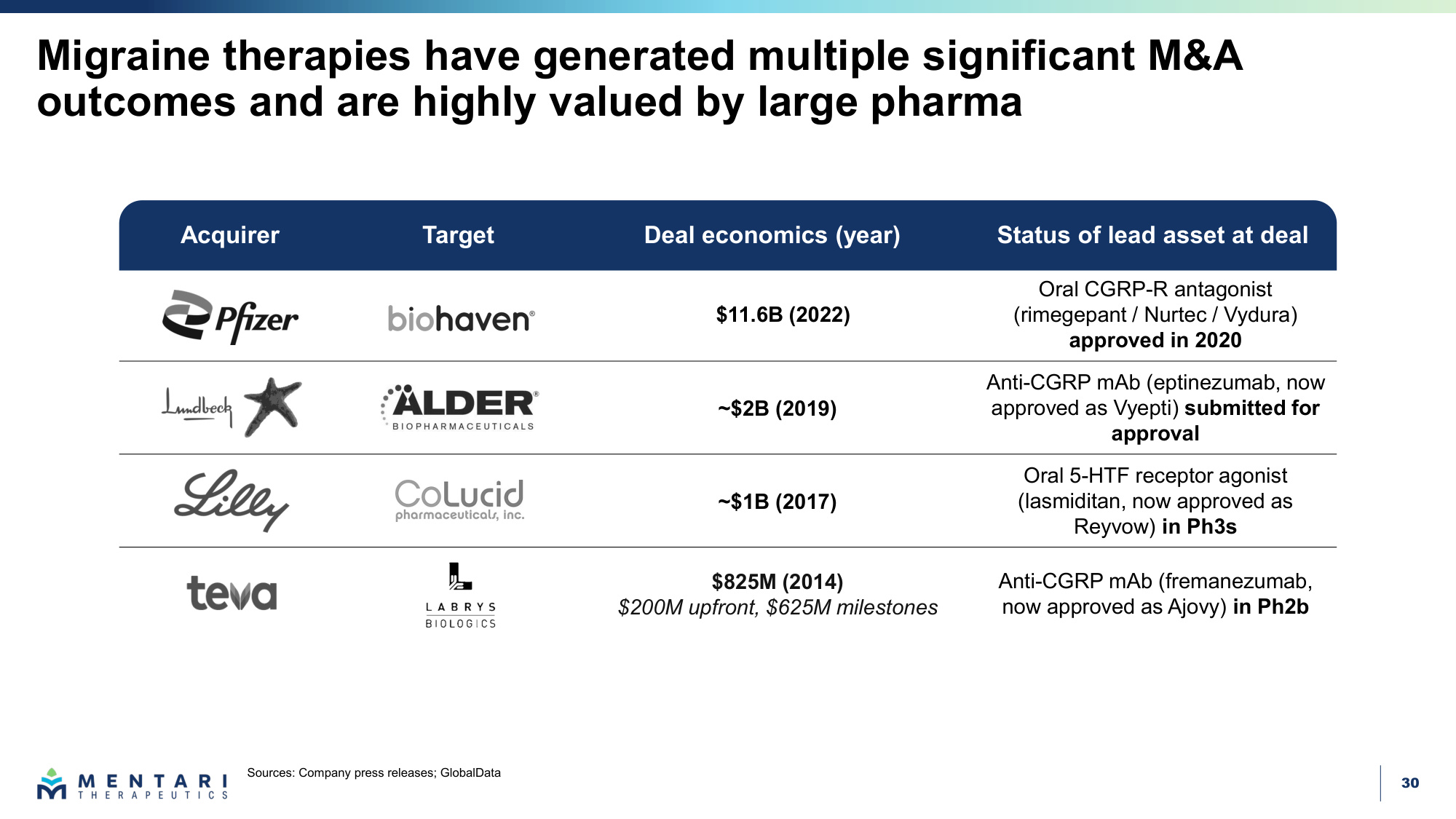

30 Migraine therapies have generated multiple significant M&A outcomes and are highly valued by large pharma Sources: Company press releases; GlobalData Acquirer Target Deal economics (year) Status of lead asset at deal $11.6B (2022) Oral CGRP-R antagonist (rimegepant / Nurtec / Vydura) approved in 2020 ~$2B (2019) Anti-CGRP mAb (eptinezumab, now approved as Vyepti) submitted for approval ~$1B (2017) Oral 5-HTF receptor agonist (lasmiditan, now approved as Reyvow) in Ph3s $825M (2014) $200M upfront, $625M milestones Anti-CGRP mAb (fremanezumab, now approved as Ajovy) in Ph2b

31 Mentari programs were developed by team with deep expertise in antibody engineering and drug development Julianne Bruno Chairperson, Board of Directors Michelle Pernice Board of Directors Neta Batscha SVP, Strategy & Operations Mike Meehl SVP, Biologics Research Hussam Shaheen CSO Jason Oh SVP, Biology Shawn Russell SVP, CMC Damon Banks SVP, Legal Affairs Keri Lantz CFO Mary Beth DeLena CLO Ghassan Fayad SVP, Translational Sciences Cyrus Stacey SVP, Quality Laura Sandler Board of Directors

Thank you