The information in this preliminary proxy statement/prospectus is not complete and may be changed. Cyclerion Therapeutics, Inc. may not sell the securities described in this preliminary proxy statement/prospectus until the registration statement filed with the Securities and Exchange Commission is effective. This preliminary proxy statement/prospectus is not an offer to sell and it is not soliciting an offer to buy these securities in any jurisdiction where the offer or sale is not permitted.

PRELIMINARY PROXY STATEMENT/PROSPECTUS

SUBJECT TO COMPLETION, DATED APRIL 17, 2026

|

|

PROPOSED MERGER

YOUR VOTE IS VERY IMPORTANT

To the Shareholders of Cyclerion Therapeutics, Inc. and Korsana Biosciences, Inc.,

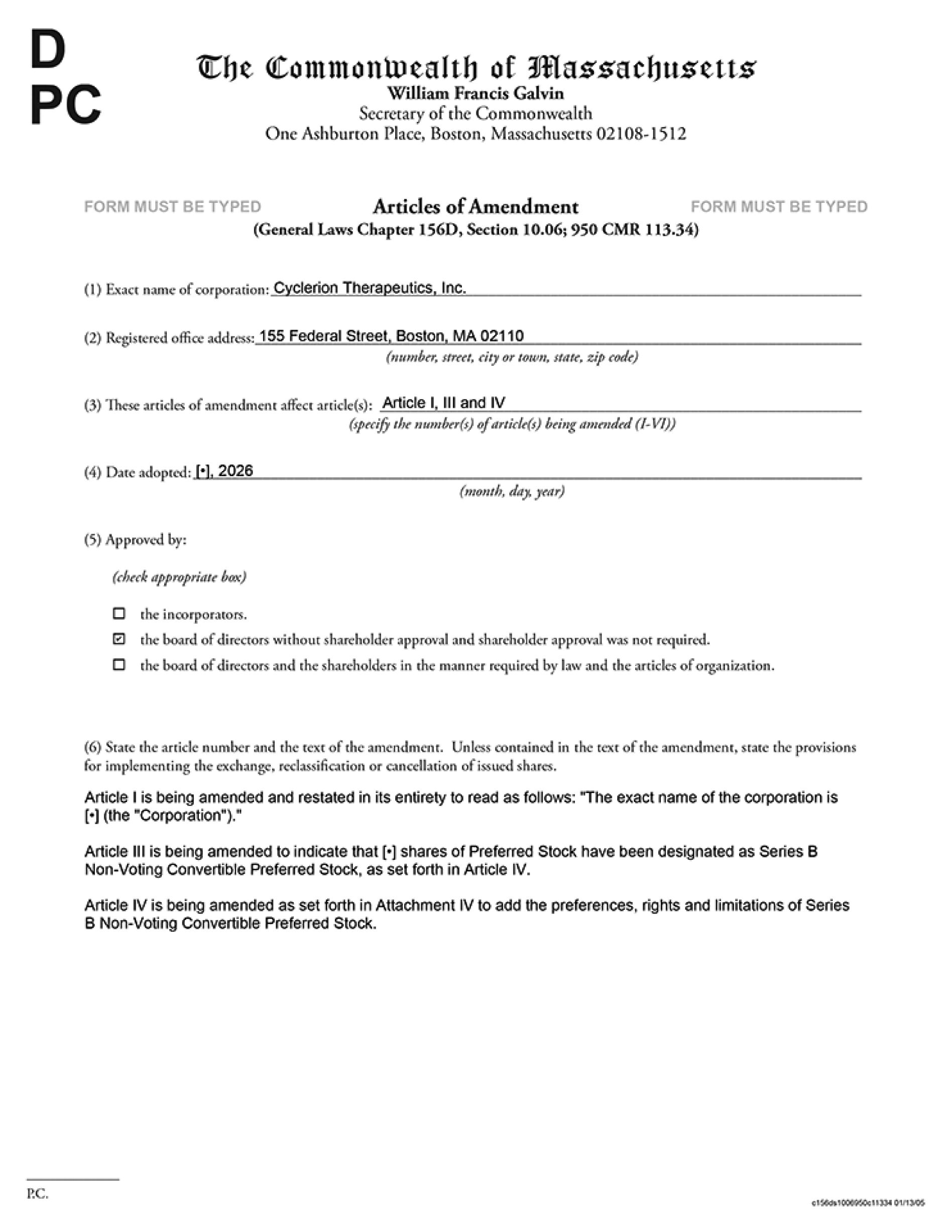

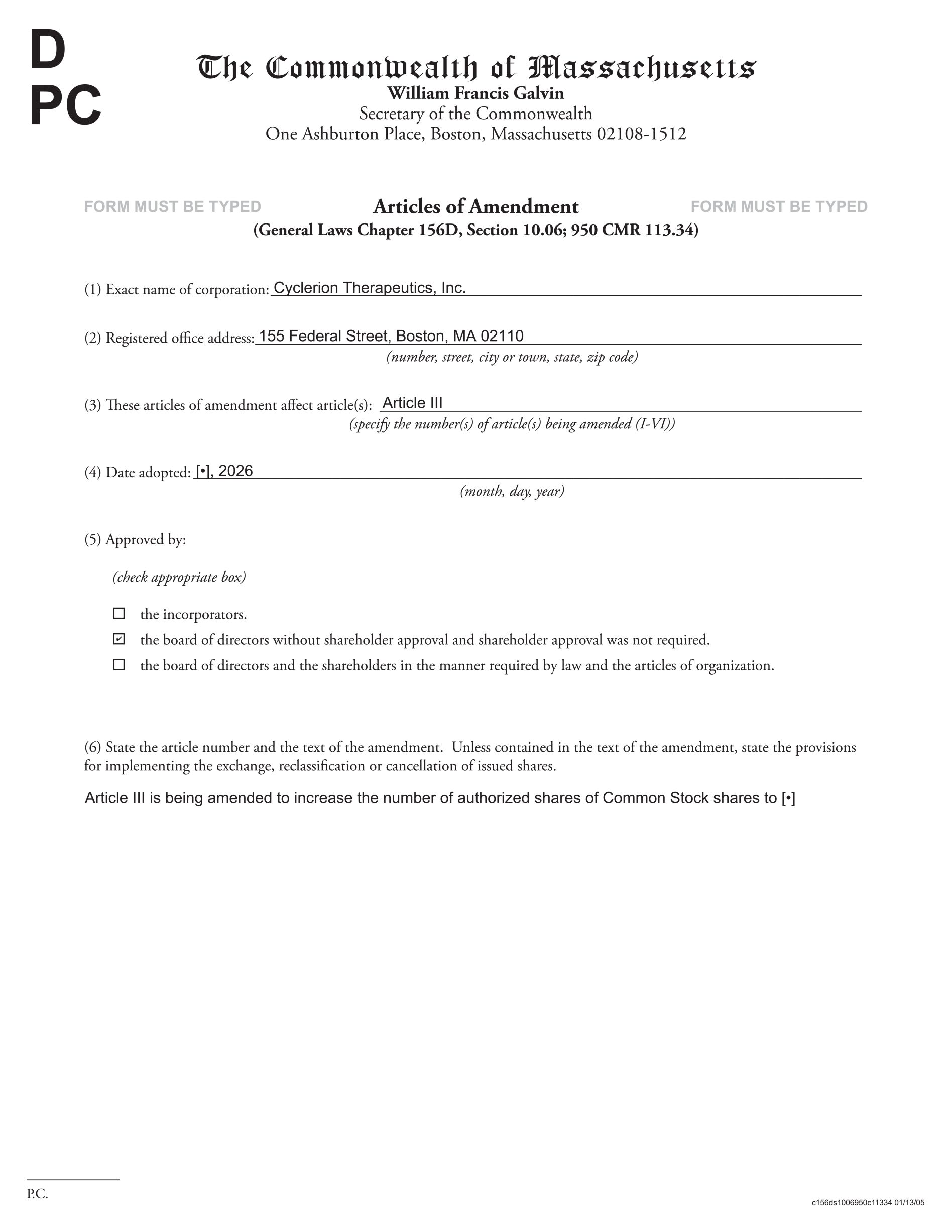

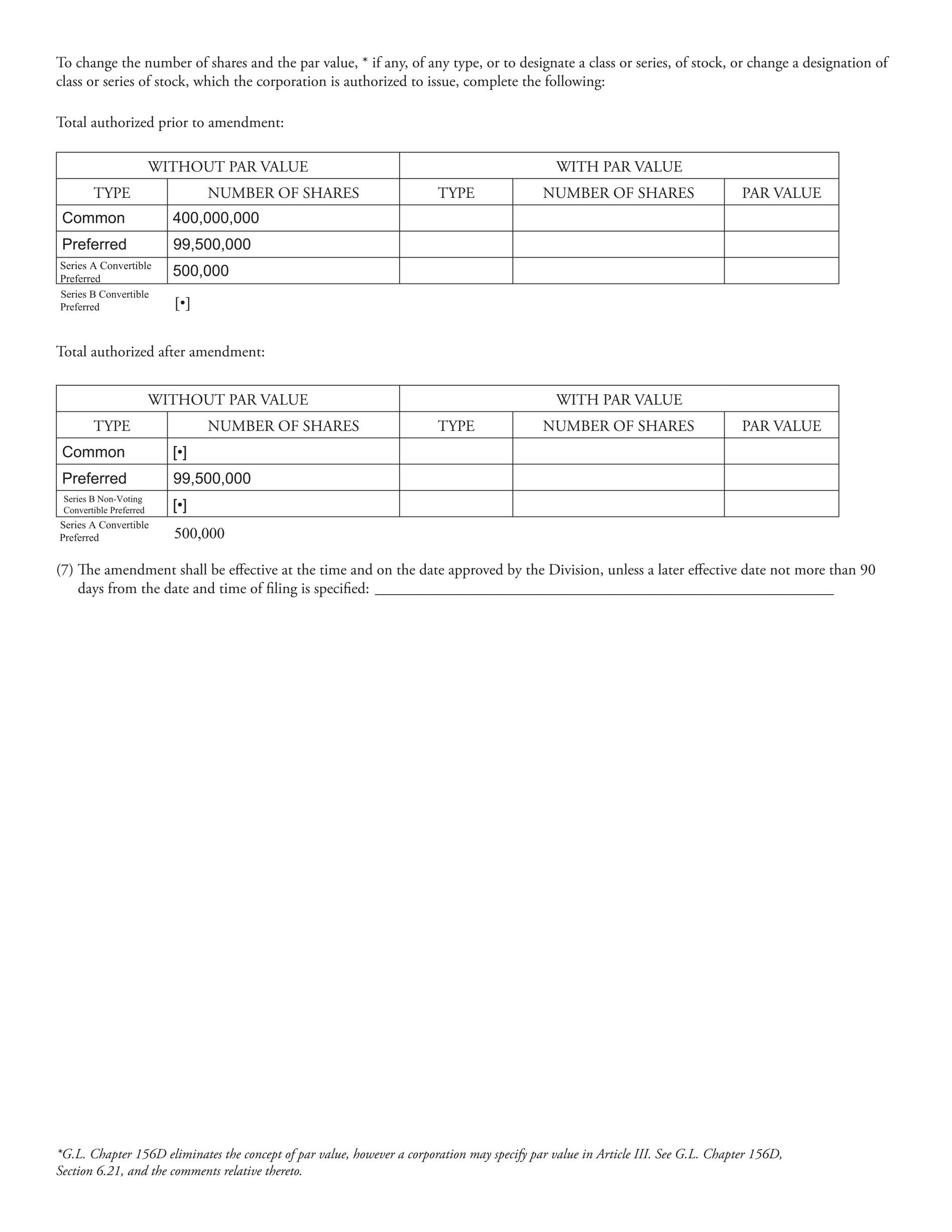

Cyclerion Therapeutics, Inc., a Massachusetts corporation (“Cyclerion”), and Korsana Biosciences, Inc., a Delaware corporation (“Korsana”), entered into an Agreement and Plan of Merger and Reorganization on April 1, 2026, which agreement was subsequently amended on April 17, 2026 (as amended, the “Merger Agreement”), pursuant to which, among other matters, and subject to the satisfaction or waiver of the conditions set forth in the Merger Agreement, Cariboos Merger Sub Corp., a Delaware corporation (“First Merger Sub”), will merge with and into Korsana, with Korsana continuing as a wholly owned subsidiary of Cyclerion and the surviving corporation of the merger (the “First Merger”), and Korsana will merge with and into Cariboos Merger Sub II, LLC, a Delaware limited liability company (“Second Merger Sub” and together with First Merger Sub, “Merger Subs”), with Second Merger Sub being the surviving entity of the merger (the “Second Merger” and, together with the First Merger, the “Merger”). After the completion of the Merger, Second Merger Sub will change its corporate name to “Korsana Biosciences Operating Company, LLC” and Cyclerion will change its name to “Korsana Biosciences, Inc.” The term “Combined Company” when used in the accompanying proxy statement/prospectus refers to the post-Merger corporate structure including Korsana Biosciences, Inc. (f/k/a Cyclerion Therapeutics, Inc.) as the parent entity and Korsana Biosciences Operating Company, LLC as its wholly-owned subsidiary.

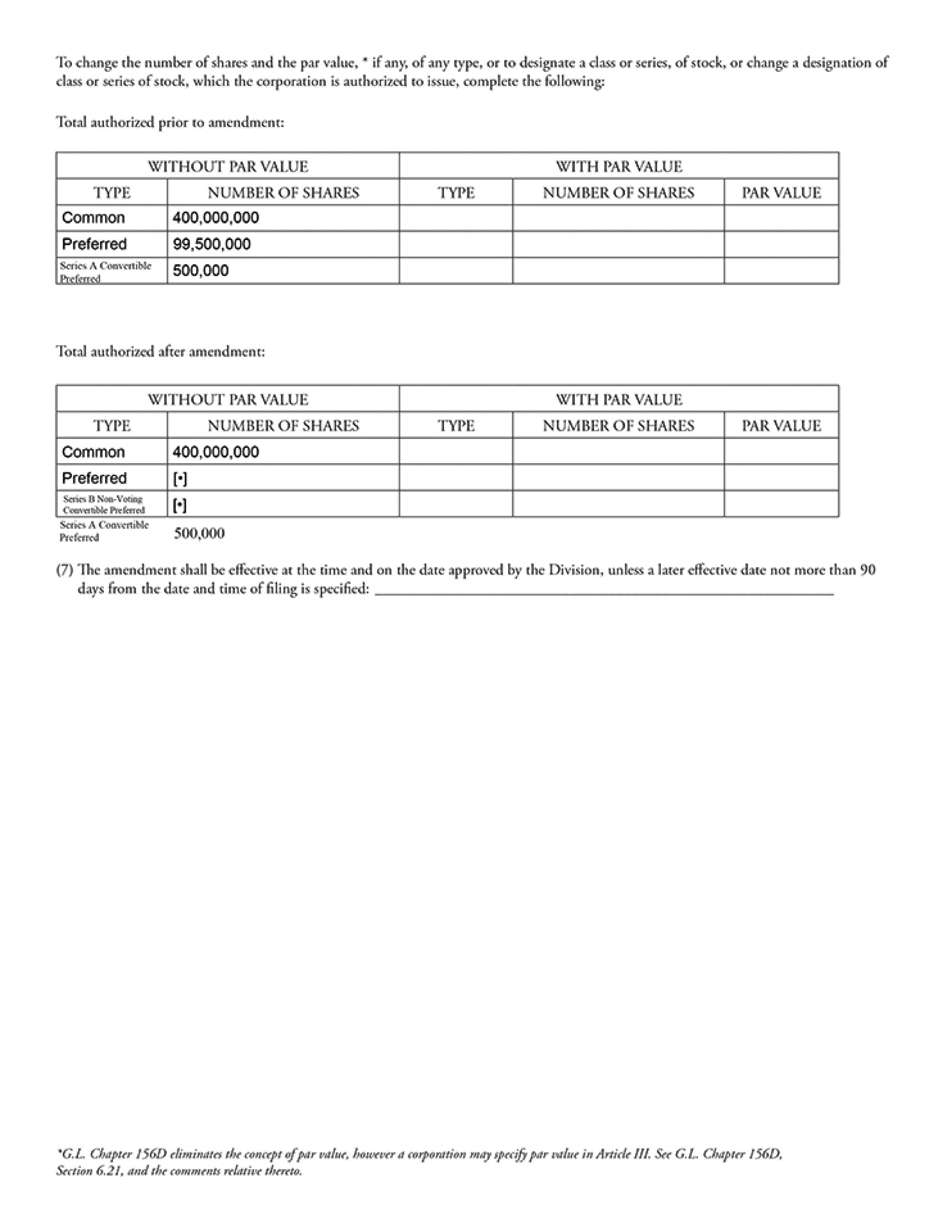

At the closing of the First Merger (the “First Effective Time”, and the date on which the closing of the Merger occurs, the “Closing Date”), upon the terms and subject to the conditions set forth in the Merger Agreement: (i) each then-outstanding share of Korsana common stock, $0.0001 par value per share, of Korsana (the “Korsana Common Stock”) and Korsana Series A Preferred Stock, $0.0001 par value per share (“Korsana Series A Preferred Stock”) (including shares of Korsana Common Stock issued in the Korsana Pre-Closing Financing described below), excluding any shares to be cancelled pursuant to the Merger Agreement and excluding dissenting shares, will be automatically converted solely into the right to receive a number of shares of Cyclerion common stock, no par value per share (the “Cyclerion Common Stock”), equal to the exchange ratio as described in more detail in the section titled “The Merger Agreement — Exchange Ratio” beginning on page 167 of the accompanying proxy statement/prospectus (the “Exchange Ratio”); provided, that in the event the aggregate number of shares of Cyclerion Common Stock issuable to a holder of Korsana capital stock (when aggregated with all of the shares of the Cyclerion Common Stock outstanding then beneficially owned by such person and its affiliates (as calculated pursuant to Section 13(d) of the Securities Exchange Act of 1934, as amended, and Rule 13d-3 promulgated thereunder) immediately after giving effect to the issuance of the merger consideration) would result in the issuance of shares of Cyclerion Common Stock to a holder in excess of a specified percentage (initially set at a percentage up to 9.99%) of the total outstanding shares of Cyclerion Common Stock (such specified percentage, a “Beneficial Ownership Limitation”), then Cyclerion will issue to any such holder (x) shares of Cyclerion Common Stock up to such holder’s Beneficial Ownership Limitation and (y) in lieu of any shares in excess of such holder’s Beneficial Ownership Limitation, pre-funded warrants (“Cyclerion Pre-Funded Warrants”) to purchase a number of shares of Cyclerion Common Stock upon exercise of such Cyclerion Pre-Funded Warrants equal to such excess shares; (ii) each then-outstanding share of Korsana Series Seed Preferred Stock, $0.0001 par value per share (“Korsana Series Seed Preferred Stock” and, together with the Korsana Series A Preferred Stock, the “Korsana Preferred Stock”), excluding any shares of Korsana Series Seed Preferred Stock to be cancelled pursuant to the Merger Agreement and any dissenting shares, will be converted into the right to receive a number of shares of Cyclerion Series B non-voting convertible preferred stock, no par value per share (“Cyclerion Series B Preferred Stock”), equal to the Exchange Ratio divided by 1,000; (iii) each then-outstanding option (a “Korsana Option”) to purchase shares of Korsana Common Stock will be converted into and become an option to purchase shares of Cyclerion Common Stock on the existing terms and conditions (including with respect to vesting and accelerated vesting),