Exhibit 99 (a)(5)(G)

Strictly Confidential. Not for Distribution. Project Feather Preliminary Discussion Materials for the

Special Committee December 18, 2025

01 02 03 04 05 EXECUTIVE SUMMARY 3 SELECTED COMPANY OBSERVATIONS 5 ILLUSTRATIVE PRELIMINARY

FINANCIAL CONSIDERATIONS 12 SELECTED CONSIDERATIONS RELATED TO CANARY PROPOSAL 25 APPENDICES Selected Historical & Projected Financial Data 35 36 Illustrative Premiums Paid Observations Financial Projections

Comparisons 38 41 06 DISCLAIMER 45

01 CONFIDENTIAL – PRELIMINARY – SUBJECT TO FURTHER REVIEW 01 EXECUTIVE SUMMARY

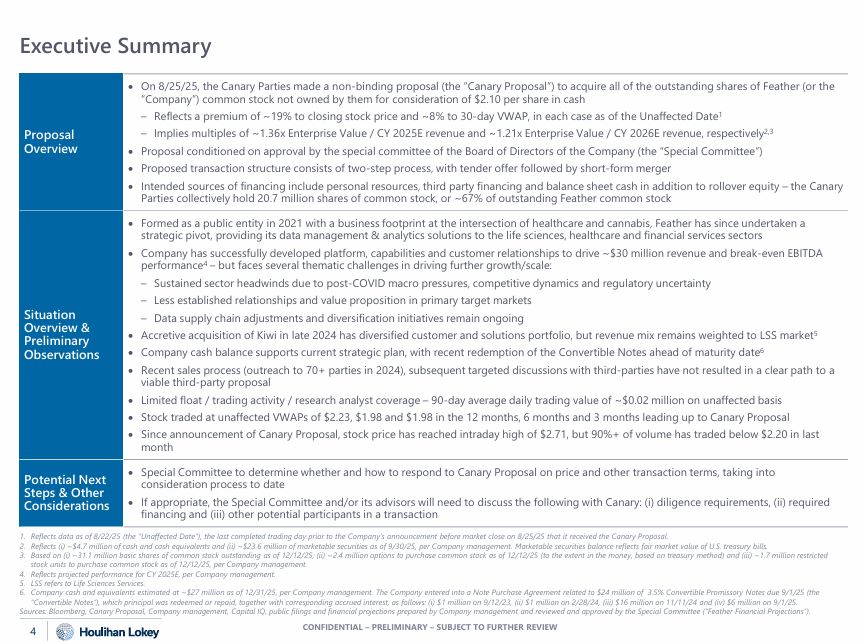

Executive Summary CONFIDENTIAL – PRELIMINARY – SUBJECT TO FURTHER REVIEW 4 Proposal Overview On 8/25/25,

the Canary Parties made a non-binding proposal (the “Canary Proposal”) to acquire all of the outstanding shares of Feather (or the “Company”) common stock not owned by them for consideration of $2.10 per share in cash Reflects a premium of

~19% to closing stock price and ~8% to 30-day VWAP, in each case as of the Unaffected Date1 Implies multiples of ~1.36x Enterprise Value / CY 2025E revenue and ~1.21x Enterprise Value / CY 2026E revenue, respectively2,3 Proposal conditioned

on approval by the special committee of the Board of Directors of the Company (the “Special Committee”) Proposed transaction structure consists of two-step process, with tender offer followed by short-form merger Intended sources of

financing include personal resources, third party financing and balance sheet cash in addition to rollover equity – the Canary Parties collectively hold 20.7 million shares of common stock, or ~67% of outstanding Feather common

stock Situation Overview & Preliminary Observations Formed as a public entity in 2021 with a business footprint at the intersection of healthcare and cannabis, Feather has since undertaken a strategic pivot, providing its data

management & analytics solutions to the life sciences, healthcare and financial services sectors Company has successfully developed platform, capabilities and customer relationships to drive ~$30 million revenue and break-even EBITDA

performance4 – but faces several thematic challenges in driving further growth/scale: Sustained sector headwinds due to post-COVID macro pressures, competitive dynamics and regulatory uncertainty Less established relationships and value

proposition in primary target markets Data supply chain adjustments and diversification initiatives remain ongoing Accretive acquisition of Kiwi in late 2024 has diversified customer and solutions portfolio, but revenue mix remains weighted

to LSS market5 Company cash balance supports current strategic plan, with recent redemption of the Convertible Notes ahead of maturity date6 Recent sales process (outreach to 70+ parties in 2024), subsequent targeted discussions with

third-parties have not resulted in a clear path to a viable third-party proposal Limited float / trading activity / research analyst coverage – 90-day average daily trading value of ~$0.02 million on unaffected basis Stock traded at

unaffected VWAPs of $2.23, $1.98 and $1.98 in the 12 months, 6 months and 3 months leading up to Canary Proposal Since announcement of Canary Proposal, stock price has reached intraday high of $2.71, but 90%+ of volume has traded below $2.20

in last month Potential Next Steps & Other Considerations Special Committee to determine whether and how to respond to Canary Proposal on price and other transaction terms, taking into consideration process to date If appropriate, the

Special Committee and/or its advisors will need to discuss the following with Canary: (i) diligence requirements, (ii) required financing and (iii) other potential participants in a transaction Reflects data as of 8/22/25 (the “Unaffected

Date”), the last completed trading day prior to the Company’s announcement before market close on 8/25/25 that it received the Canary Proposal. Reflects (i) ~$4.7 million of cash and cash equivalents and (ii) ~$23.6 million of marketable

securities as of 9/30/25, per Company management. Marketable securities balance reflects fair market value of U.S. treasury bills. Based on (i) ~31.1 million basic shares of common stock outstanding as of 12/12/25, (ii) ~2.4 million options

to purchase common stock as of 12/12/25 (to the extent in the money, based on treasury method) and (iii) ~1.7 million restricted stock units to purchase common stock as of 12/12/25, per Company management. Reflects projected performance for

CY 2025E, per Company management. LSS refers to Life Sciences Services. Company cash and equivalents estimated at ~$27 million as of 12/31/25, per Company management. The Company entered into a Note Purchase Agreement related to $24 million

of 3.5% Convertible Promissory Notes due 9/1/25 (the “Convertible Notes“), which principal was redeemed or repaid, together with corresponding accrued interest, as follows: (i) $1 million on 9/12/23, (ii) $1 million on 2/28/24, (iii) $16

million on 11/11/24 and (iv) $6 million on 9/1/25. Sources: Bloomberg, Canary Proposal, Company management, Capital IQ, public filings and financial projections prepared by Company management and reviewed and approved by the Special

Committee ("Feather Financial Projections").

02 CONFIDENTIAL – PRELIMINARY – SUBJECT TO FURTHER REVIEW 02 SELECTED COMPANY OBSERVATIONS

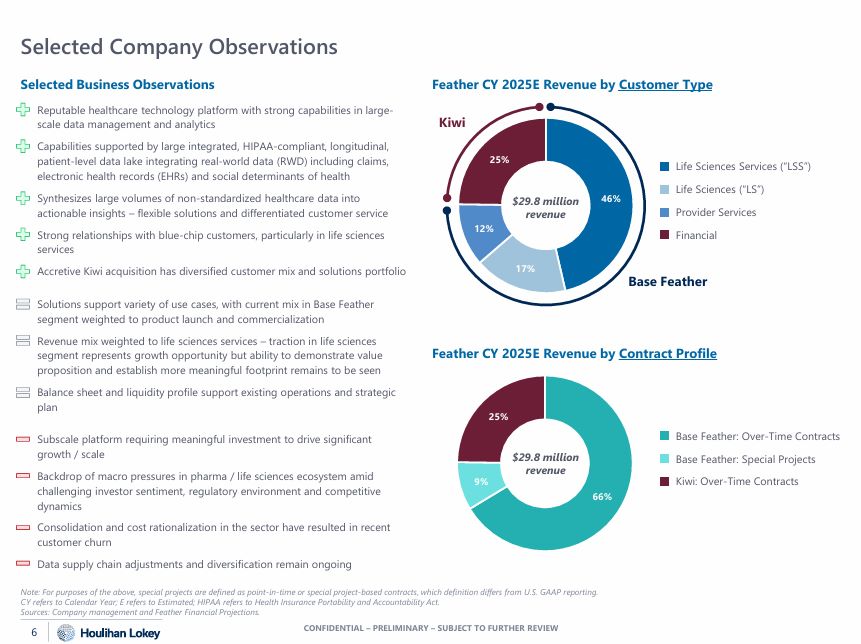

66% 9% 25% Selected Company Observations Note: For purposes of the above, special projects are defined

as point-in-time or special project-based contracts, which definition differs from U.S. GAAP reporting. CY refers to Calendar Year; E refers to Estimated; HIPAA refers to Health Insurance Portability and Accountability Act. Sources: Company

management and Feather Financial Projections. Feather CY 2025E Revenue by Customer Type Feather CY 2025E Revenue by Contract Profile $29.8 million revenue Kiwi Base Feather Life Sciences (“LS”) Provider Services Financial Life

Sciences Services (“LSS”) Base Feather: Over-Time Contracts Base Feather: Special Projects Kiwi: Over-Time Contracts $29.8 million revenue Selected Business Observations Reputable healthcare technology platform with strong capabilities

in large-scale data management and analytics Capabilities supported by large integrated, HIPAA-compliant, longitudinal, patient-level data lake integrating real-world data (RWD) including claims, electronic health records (EHRs) and social

determinants of health Synthesizes large volumes of non-standardized healthcare data into actionable insights – flexible solutions and differentiated customer service Strong relationships with blue-chip customers, particularly in life

sciences services Accretive Kiwi acquisition has diversified customer mix and solutions portfolio 46% 17% 12% 25% Solutions support variety of use cases, with current mix in Base Feather segment weighted to product launch and

commercialization Revenue mix weighted to life sciences services – traction in life sciences segment represents growth opportunity but ability to demonstrate value proposition and establish more meaningful footprint remains to be

seen Balance sheet and liquidity profile support existing operations and strategic plan Subscale platform requiring meaningful investment to drive significant growth / scale Backdrop of macro pressures in pharma / life sciences ecosystem

amid challenging investor sentiment, regulatory environment and competitive dynamics Consolidation and cost rationalization in the sector have resulted in recent customer churn Data supply chain adjustments and diversification remain

ongoing CONFIDENTIAL – PRELIMINARY – SUBJECT TO FURTHER REVIEW 6

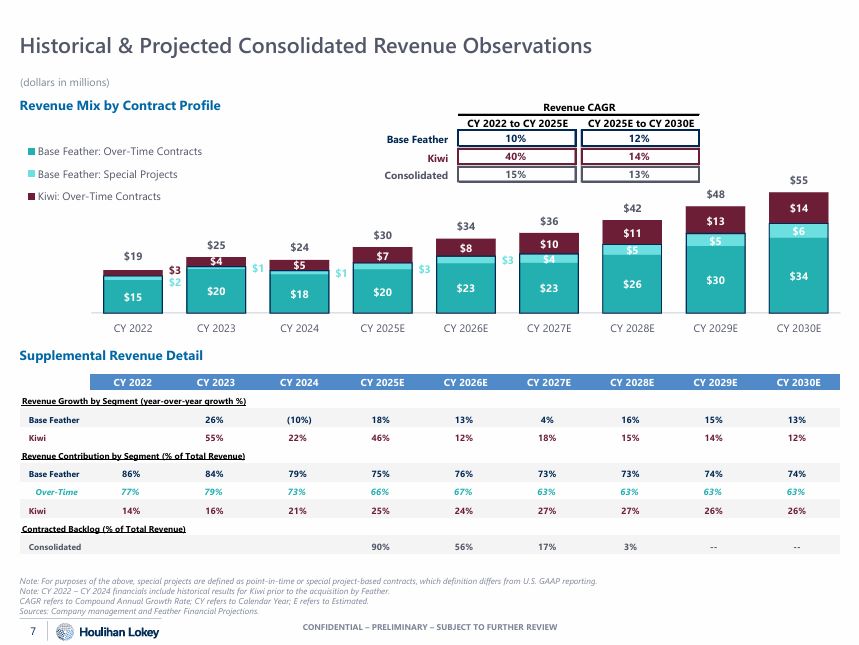

$15 $20 $18 $20 $23 $23 $26 $30 $34 $1 $1 $3 $3 $5 $6 $3 $2 $4 $5 $7 $8 $10 $4 $11 $5 $13 $14 $19 $25 $24 $30 $34 $36 $42 $48 $55 CY

2022 CY 2023 Supplemental Revenue Detail CY 2024 CY 2025E CY 2026E CY 2027E CY 2028E CY 2029E CY 2030E Base Feather: Over-Time Contracts Base Feather: Special Projects Kiwi: Over-Time Contracts Historical & Projected

Consolidated Revenue Observations Note: For purposes of the above, special projects are defined as point-in-time or special project-based contracts, which definition differs from U.S. GAAP reporting. Note: CY 2022 – CY 2024 financials

include historical results for Kiwi prior to the acquisition by Feather. (dollars in millions) Revenue Mix by Contract Profile Revenue CAGR CY 2022 to CY 2025E CY 2025E to CY 2030E CAGR refers to Compound Annual Growth Rate; CY refers to

Calendar Year; E refers to Estimated. Sources: Company management and Feather Financial Projections. CONFIDENTIAL – PRELIMINARY – SUBJECT TO FURTHER REVIEW 7 Base Feather Kiwi Consolidated 10% 12% 40% 14% 15% 13% Base

Feather 26% (10%) 18% 13% 4% 16% 15% 13% Kiwi 55% 22% 46% 12% 18% 15% 14% 12% Revenue Contribution by Segment (% of Total Revenue) Base Feather 86% 84% 79% 75% 76% 73% 73% 74% 74% Over-Time 77%

79% 73% 66% 67% 63% 63% 63% 63% Kiwi 14% 16% 21% 25% 24% 27% 27% 26% 26% Contracted Backlog (% of Total Revenue) Consolidated 90% 56% 17% 3% -- -- CY 2022 CY 2023 CY 2024 CY 2025E CY 2026E CY 2027E CY 2028E CY 2029E CY

2030E Revenue Growth by Segment (year-over-year growth %)

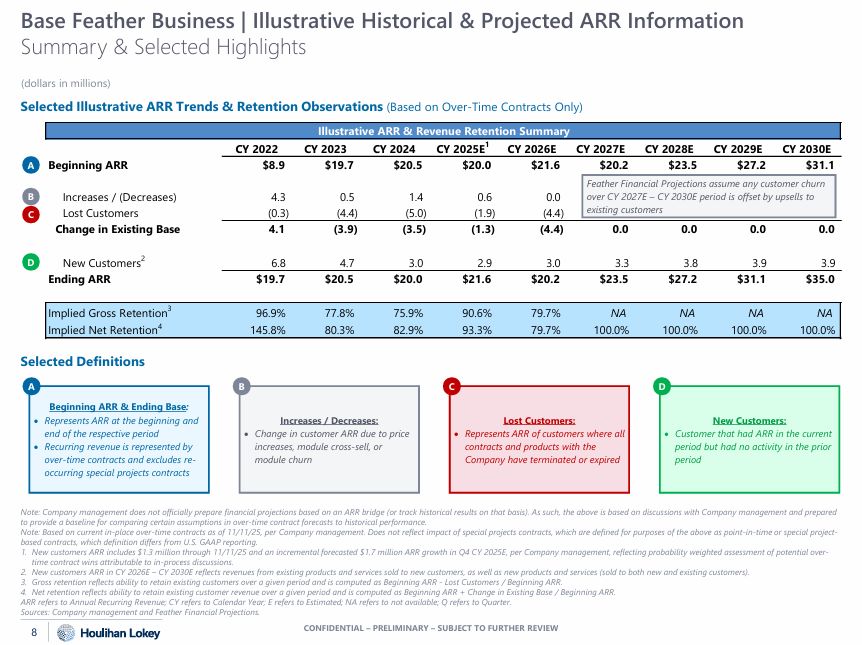

Base Feather Business | Illustrative Historical & Projected ARR Information Summary & Selected

Highlights Note: Company management does not officially prepare financial projections based on an ARR bridge (or track historical results on that basis). As such, the above is based on discussions with Company management and prepared to

provide a baseline for comparing certain assumptions in over-time contract forecasts to historical performance. Note: Based on current in-place over-time contracts as of 11/11/25, per Company management. Does not reflect impact of special

projects contracts, which are defined for purposes of the above as point-in-time or special project-based contracts, which definition differs from U.S. GAAP reporting. New customers ARR includes $1.3 million through 11/11/25 and an

incremental forecasted $1.7 million ARR growth in Q4 CY 2025E, per Company management, reflecting probability weighted assessment of potential over- time contract wins attributable to in-process discussions. New customers ARR in CY 2026E –

CY 2030E reflects revenues from existing products and services sold to new customers, as well as new products and services (sold to both new and existing customers). Gross retention reflects ability to retain existing customers over a given

period and is computed as Beginning ARR - Lost Customers / Beginning ARR. Net retention reflects ability to retain existing customer revenue over a given period and is computed as Beginning ARR + Change in Existing Base / Beginning

ARR. Beginning ARR & Ending Base: Represents ARR at the beginning and end of the respective period Recurring revenue is represented by over-time contracts and excludes re- occurring special projects contracts Selected

Definitions A Increases / Decreases: Change in customer ARR due to price increases, module cross-sell, or module churn B Lost Customers: Represents ARR of customers where all contracts and products with the Company have terminated or

expired C New Customers: Customer that had ARR in the current period but had no activity in the prior period D (dollars in millions) Selected Illustrative ARR Trends & Retention Observations (Based on Over-Time Contracts

Only) Illustrative ARR & Revenue Retention Summary CY 2022 CY 2023 CY 2024 CY 2025E1 CY 2026E CY 2027E CY 2028E CY 2029E CY 2030E A Beginning ARR $8.9 $19.7 $20.5 $20.0 $21.6 $20.2 $23.5 $27.2 $31.1 Feather Financial

Projections assume any customer churn B Increases / (Decreases) 4.3 0.5 1.4 0.6 0.0 over CY 2027E – CY 2030E period is offset by upsells to C Lost Customers (0.3) (4.4) (5.0) (1.9) (4.4) existing customers Change in Existing

Base 4.1 (3.9) (3.5) (1.3) (4.4) 0.0 0.0 0.0 0.0 D New Customers2 6.8 4.7 3.0 2.9 3.0 3.3 3.8 3.9 3.9 Ending ARR $19.7 $20.5 $20.0 $21.6 $20.2 $23.5 $27.2 $31.1 $35.0 Implied Gross

Retention3 96.9% 77.8% 75.9% 90.6% 79.7% NA NA NA NA Implied Net Retention4 145.8% 80.3% 82.9% 93.3% 79.7% 100.0% 100.0% 100.0% 100.0% ARR refers to Annual Recurring Revenue; CY refers to Calendar Year; E refers to

Estimated; NA refers to not available; Q refers to Quarter. Sources: Company management and Feather Financial Projections. CONFIDENTIAL – PRELIMINARY – SUBJECT TO FURTHER REVIEW 8

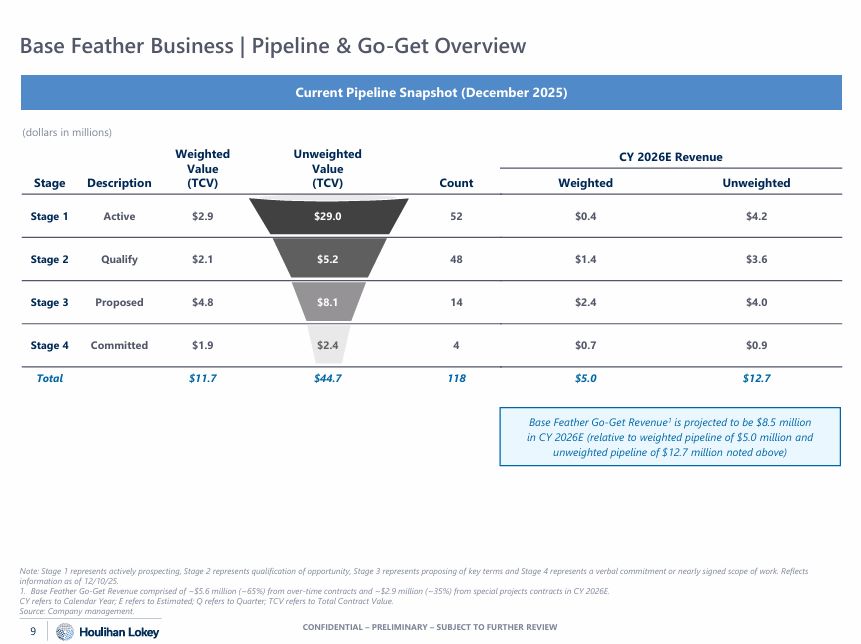

Weighted Unweighted CY 2026E Revenue Stage Description (TCV) (TCV) Count Weighted Unweighted Stage

1 Active $2.9 $29.0 52 $0.4 $4.2 Stage 2 Qualify $2.1 $5.2 48 $1.4 $3.6 Stage 3 Proposed $4.8 $8.1 14 $2.4 $4.0 Stage 4 Committed $1.9 $2.4 4 $0.7 $0.9 Total $11.7 $44.7 118 $5.0 $12.7 Source: Company

management. 9 CONFIDENTIAL – PRELIMINARY – SUBJECT TO FURTHER REVIEW Base Feather Business | Pipeline & Go-Get Overview (dollars in millions) Note: Stage 1 represents actively prospecting, Stage 2 represents qualification of

opportunity, Stage 3 represents proposing of key terms and Stage 4 represents a verbal commitment or nearly signed scope of work. Reflects information as of 12/10/25. 1. Base Feather Go-Get Revenue comprised of ~$5.6 million (~65%) from

over-time contracts and ~$2.9 million (~35%) from special projects contracts in CY 2026E. CY refers to Calendar Year; E refers to Estimated; Q refers to Quarter; TCV refers to Total Contract Value. Current Pipeline Snapshot (December

2025) Base Feather Go-Get Revenue1 is projected to be $8.5 million in CY 2026E (relative to weighted pipeline of $5.0 million and unweighted pipeline of $12.7 million noted above)

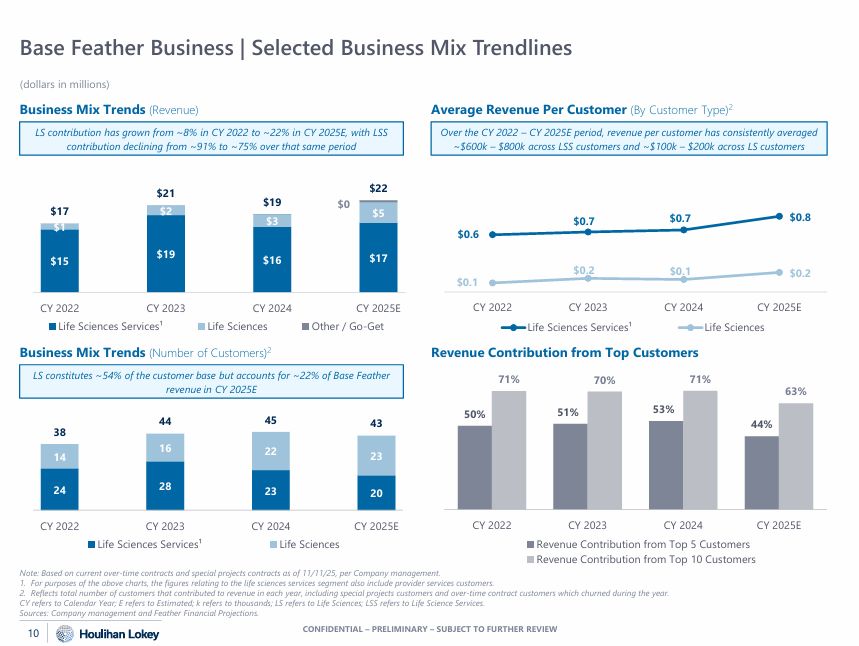

24 28 23 20 14 16 22 23 38 44 45 43 CY 2022 CY 2023 Life Sciences Services¹ CY 2025E CY

2024 Life Sciences LS contribution has grown from ~8% in CY 2022 to ~22% in CY 2025E, with LSS contribution declining from ~91% to ~75% over that same period Base Feather Business | Selected Business Mix Trendlines (dollars in

millions) Business Mix Trends (Revenue) Average Revenue Per Customer (By Customer Type)2 Note: Based on current over-time contracts and special projects contracts as of 11/11/25, per Company management. For purposes of the above charts,

the figures relating to the life sciences services segment also include provider services customers. Reflects total number of customers that contributed to revenue in each year, including special projects customers and over-time contract

customers which churned during the year. CY refers to Calendar Year; E refers to Estimated; k refers to thousands; LS refers to Life Sciences; LSS refers to Life Science Services. Sources: Company management and Feather Financial

Projections. LS constitutes ~54% of the customer base but accounts for ~22% of Base Feather revenue in CY 2025E Business Mix Trends (Number of Customers)2 Revenue Contribution from Top Customers 71% 70% 71% Over the CY 2022 – CY 2025E

period, revenue per customer has consistently averaged ~$600k – $800k across LSS customers and ~$100k – $200k across LS customers 50% 51% 53% 44% 63% CY 2022 CY 2025E CY 2023 CY 2024 Revenue Contribution from Top 5 Customers Revenue

Contribution from Top 10 Customers $15 $19 $16 $17 $2 $3 $5 $17 $1 $0 $21 $19 $22 CY 2024 Life Sciences CY 2025E Other / Go-Get CY 2022 CY 2023 Life Sciences Services¹ $0.6 $0.7 $0.7 $0.8 $0.1 $0.2 $0.1 $0.2 CY

2022 CY 2023 Life Sciences Services¹ CY 2024 CY 2025E Life Sciences CONFIDENTIAL – PRELIMINARY – SUBJECT TO FURTHER REVIEW 10

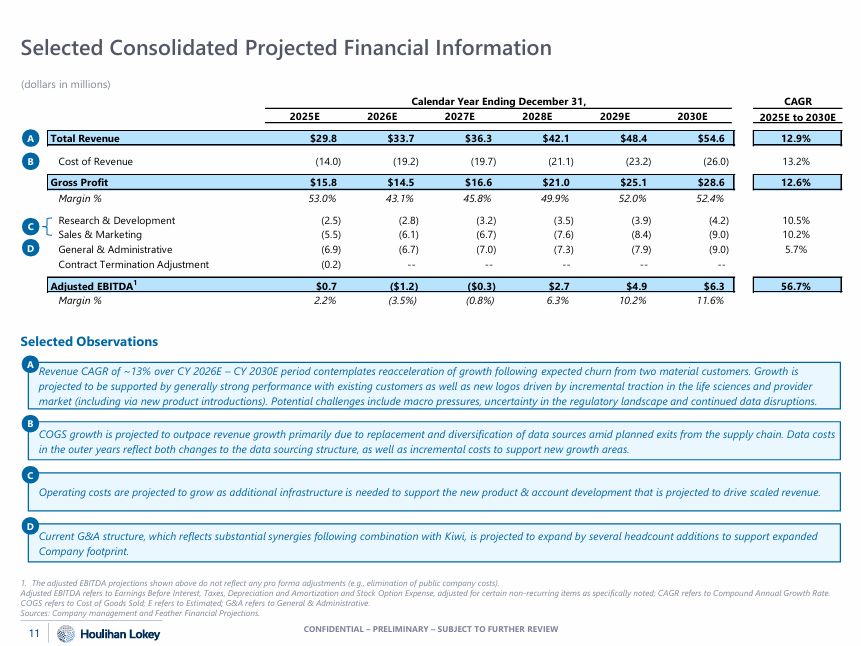

Selected Consolidated Projected Financial Information (dollars in millions) Calendar Year Ending December

31, C D Selected Observations A Revenue CAGR of ~13% over CY 2026E – CY 2030E period contemplates reacceleration of growth following expected churn from two material customers. Growth is projected to be supported by generally strong

performance with existing customers as well as new logos driven by incremental traction in the life sciences and provider market (including via new product introductions). Potential challenges include macro pressures, uncertainty in the

regulatory landscape and continued data disruptions. B COGS growth is projected to outpace revenue growth primarily due to replacement and diversification of data sources amid planned exits from the supply chain. Data costs in the outer

years reflect both changes to the data sourcing structure, as well as incremental costs to support new growth areas. C Operating costs are projected to grow as additional infrastructure is needed to support the new product & account

development that is projected to drive scaled revenue. D Current G&A structure, which reflects substantial synergies following combination with Kiwi, is projected to expand by several headcount additions to support expanded Company

footprint. 1. The adjusted EBITDA projections shown above do not reflect any pro forma adjustments (e.g., elimination of public company costs). Adjusted EBITDA refers to Earnings Before Interest, Taxes, Depreciation and Amortization and

Stock Option Expense, adjusted for certain non-recurring items as specifically noted; CAGR refers to Compound Annual Growth Rate. COGS refers to Cost of Goods Sold; E refers to Estimated; G&A refers to General &

Administrative. Sources: Company management and Feather Financial Projections. 2025E 2026E 2027E 2028E 2029E 2030E 2025E to 2030E A Total Revenue $29.8 $33.7 $36.3 $42.1 $48.4 $54.6 12.9% B Cost of

Revenue (14.0) (19.2) (19.7) (21.1) (23.2) (26.0) 13.2% Gross Profit $15.8 $14.5 $16.6 $21.0 $25.1 $28.6 12.6% Margin % 53.0% 43.1% 45.8% 49.9% 52.0% 52.4% Research &

Development (2.5) (2.8) (3.2) (3.5) (3.9) (4.2) 10.5% Sales & Marketing (5.5) (6.1) (6.7) (7.6) (8.4) (9.0) 10.2% General & Administrative (6.9) (6.7) (7.0) (7.3) (7.9) (9.0) 5.7% Contract Termination

Adjustment (0.2) -- -- -- -- -- Adjusted EBITDA1 $0.7 ($1.2) ($0.3) $2.7 $4.9 $6.3 56.7% Margin % 2.2% (3.5%) (0.8%) 6.3% 10.2% 11.6% CAGR CONFIDENTIAL – PRELIMINARY – SUBJECT TO FURTHER REVIEW 11

03 03 ILLUSTRATIVE PRELIMINARY FINANCIAL CONSIDERATIONS CONFIDENTIAL – PRELIMINARY – SUBJECT TO FURTHER

REVIEW

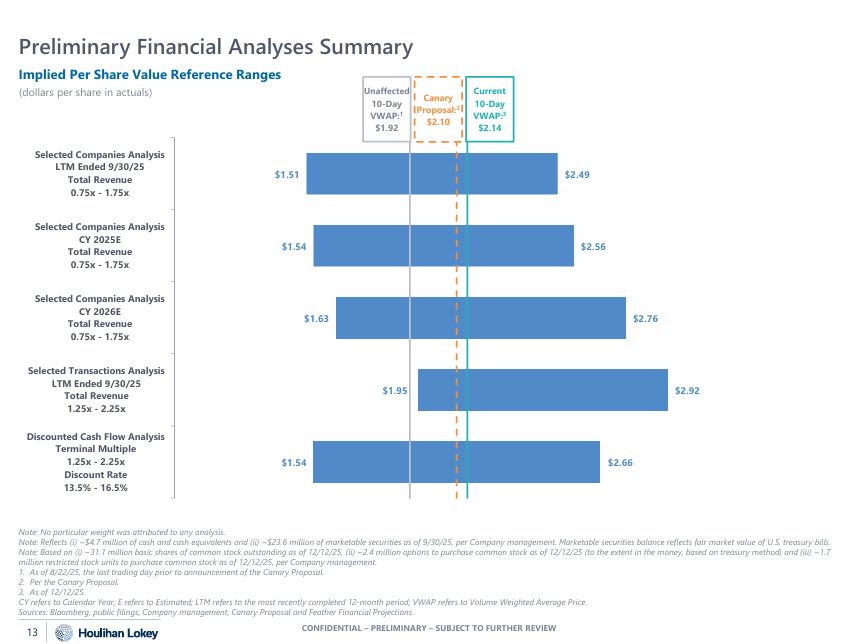

Implied Per Share Value Reference Ranges (dollars per share in

actuals) $1.54 $1.95 $1.63 $1.54 $1.51 $2.66 $2.92 $2.76 $2.56 $2.49 Discounted Cash Flow Analysis Terminal Multiple 1.25x - 2.25x Discount Rate 13.5% - 16.5% Selected Transactions Analysis LTM Ended 9/30/25 Total

Revenue 1.25x - 2.25x Selected Companies Analysis CY 2026E Total Revenue 0.75x - 1.75x Selected Companies Analysis CY 2025E Total Revenue 0.75x - 1.75x Selected Companies Analysis LTM Ended 9/30/25 Total Revenue 0.75x -

1.75x Preliminary Financial Analyses Summary Note: No particular weight was attributed to any analysis. Note: Reflects (i) ~$4.7 million of cash and cash equivalents and (ii) ~$23.6 million of marketable securities as of 9/30/25, per

Company management. Marketable securities balance reflects fair market value of U.S. treasury bills. Note: Based on (i) ~31.1 million basic shares of common stock outstanding as of 12/12/25, (ii) ~2.4 million options to purchase common stock

as of 12/12/25 (to the extent in the money, based on treasury method) and (iii) ~1.7 million restricted stock units to purchase common stock as of 12/12/25, per Company management. As of 8/22/25, the last trading day prior to announcement of

the Canary Proposal. Per the Canary Proposal. As of 12/12/25. CY refers to Calendar Year; E refers to Estimated; LTM refers to the most recently completed 12-month period; VWAP refers to Volume Weighted Average Price. Sources: Bloomberg,

public filings, Company management, Canary Proposal and Feather Financial Projections. Unaffected 10-Day VWAP:1 $1.92 2 Canary Proposal: $2.10 Current 10-Day VWAP:3 $2.14 CONFIDENTIAL – PRELIMINARY – SUBJECT TO FURTHER REVIEW 13

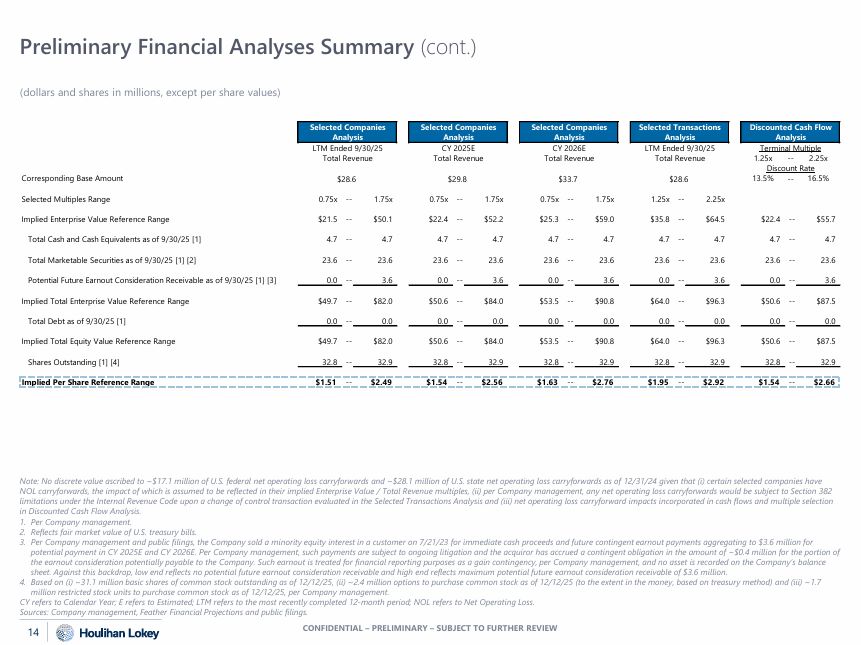

Preliminary Financial Analyses Summary (cont.) Sources: Company management, Feather Financial Projections

and public filings. CONFIDENTIAL – PRELIMINARY – SUBJECT TO FURTHER REVIEW 14 (dollars and shares in millions, except per share values) Selected Companies Analysis Selected Companies Analysis Selected Companies Analysis Selected

Transactions Analysis Discounted Cash Flow Analysis Corresponding Base Amount LTM Ended 9/30/25 Total Revenue $28.6 CY 2025E Total Revenue $29.8 CY 2026E Total Revenue $33.7 LTM Ended 9/30/25 Total Revenue $28.6 Terminal

Multiple 1.25x -- 2.25x Discount Rate 13.5% -- 16.5% Selected Multiples Range 0.75x -- 1.75x 0.75x -- 1.75x 0.75x -- 1.75x 1.25x -- 2.25x Implied Enterprise Value Reference

Range $21.5 -- $50.1 $22.4 -- $52.2 $25.3 -- $59.0 $35.8 -- $64.5 $22.4 -- $55.7 Total Cash and Cash Equivalents as of 9/30/25 [1] 4.7 -- 4.7 4.7 -- 4.7 4.7 -- 4.7 4.7 -- 4.7 4.7 -- 4.7 Total Marketable

Securities as of 9/30/25 [1] [2] 23.6 -- 23.6 23.6 -- 23.6 23.6 -- 23.6 23.6 -- 23.6 23.6 -- 23.6 Potential Future Earnout Consideration Receivable as of 9/30/25 [1] [3] 0.0 -- 3.6 0.0 -- 3.6 0.0 -- 3.6 0.0 -- 3.6

0.0 -- 3.6 Implied Total Enterprise Value Reference Range $49.7 -- $82.0 $50.6 -- $84.0 $53.5 -- $90.8 $64.0 -- $96.3 $50.6 -- $87.5 Total Debt as of 9/30/25 [1] 0.0 -- 0.0 0.0 -- 0.0 0.0 -- 0.0 0.0 -- 0.0 0.0 --

0.0 Implied Total Equity Value Reference Range $49.7 -- $82.0 $50.6 -- $84.0 $53.5 -- $90.8 $64.0 -- $96.3 $50.6 -- $87.5 Shares Outstanding [1] [4] 32.8 -- 32.9 32.8 -- 32.9 32.8 -- 32.9 32.8 -- 32.9 32.8 -- 32.9

Implied Per Share Reference Range $1.51 -- $2.49 $1.54 -- $2.56 $1.63 -- $2.76 $1.95 -- $2.92 $1.54 -- $2.66 Note: No discrete value ascribed to ~$17.1 million of U.S. federal net operating loss carryforwards and ~$28.1 million

of U.S. state net operating loss carryforwards as of 12/31/24 given that (i) certain selected companies have NOL carryforwards, the impact of which is assumed to be reflected in their implied Enterprise Value / Total Revenue multiples, (ii)

per Company management, any net operating loss carryforwards would be subject to Section 382 limitations under the Internal Revenue Code upon a change of control transaction evaluated in the Selected Transactions Analysis and (iii) net

operating loss carryforward impacts incorporated in cash flows and multiple selection in Discounted Cash Flow Analysis. Per Company management. Reflects fair market value of U.S. treasury bills. Per Company management and public filings,

the Company sold a minority equity interest in a customer on 7/21/23 for immediate cash proceeds and future contingent earnout payments aggregating to $3.6 million for potential payment in CY 2025E and CY 2026E. Per Company management, such

payments are subject to ongoing litigation and the acquiror has accrued a contingent obligation in the amount of ~$0.4 million for the portion of the earnout consideration potentially payable to the Company. Such earnout is treated for

financial reporting purposes as a gain contingency, per Company management, and no asset is recorded on the Company’s balance sheet. Against this backdrop, low end reflects no potential future earnout consideration receivable and high end

reflects maximum potential future earnout consideration receivable of $3.6 million. Based on (i) ~31.1 million basic shares of common stock outstanding as of 12/12/25, (ii) ~2.4 million options to purchase common stock as of 12/12/25 (to the

extent in the money, based on treasury method) and (iii) ~1.7 million restricted stock units to purchase common stock as of 12/12/25, per Company management. CY refers to Calendar Year; E refers to Estimated; LTM refers to the most recently

completed 12-month period; NOL refers to Net Operating Loss.

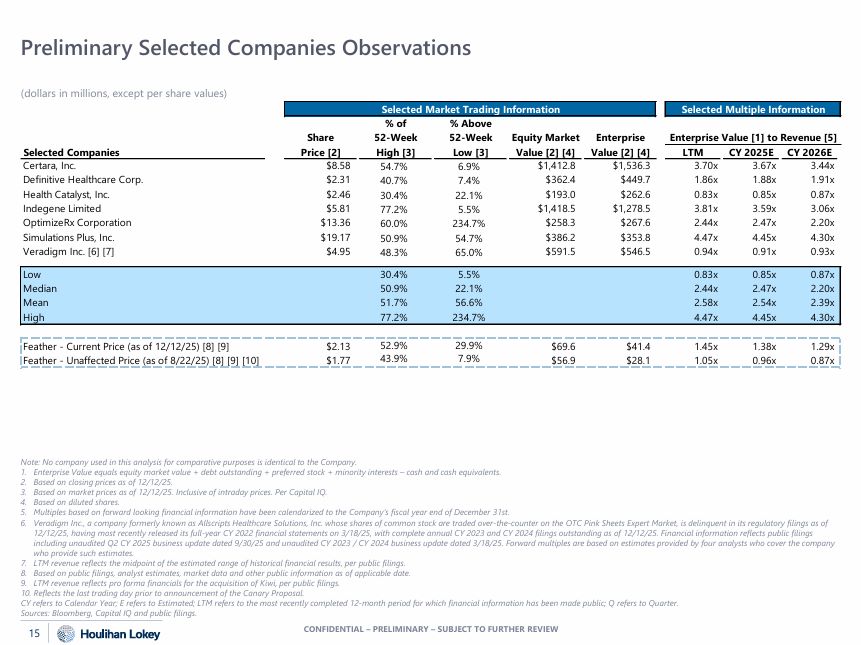

Preliminary Selected Companies Observations (dollars in millions, except per share values) Note: No

company used in this analysis for comparative purposes is identical to the Company. Enterprise Value equals equity market value + debt outstanding + preferred stock + minority interests – cash and cash equivalents. Based on closing prices

as of 12/12/25. Based on market prices as of 12/12/25. Inclusive of intraday prices. Per Capital IQ. Based on diluted shares. Multiples based on forward looking financial information have been calendarized to the Company’s fiscal year end

of December 31st. Veradigm Inc., a company formerly known as Allscripts Healthcare Solutions, Inc. whose shares of common stock are traded over-the-counter on the OTC Pink Sheets Expert Market, is delinquent in its regulatory filings as of

12/12/25, having most recently released its full-year CY 2022 financial statements on 3/18/25, with complete annual CY 2023 and CY 2024 filings outstanding as of 12/12/25. Financial information reflects public filings including unaudited Q2

CY 2025 business update dated 9/30/25 and unaudited CY 2023 / CY 2024 business update dated 3/18/25. Forward multiples are based on estimates provided by four analysts who cover the company who provide such estimates. LTM revenue reflects

the midpoint of the estimated range of historical financial results, per public filings. Based on public filings, analyst estimates, market data and other public information as of applicable date. LTM revenue reflects pro forma financials

for the acquisition of Kiwi, per public filings. Reflects the last trading day prior to announcement of the Canary Proposal. CY refers to Calendar Year; E refers to Estimated; LTM refers to the most recently completed 12-month period for

which financial information has been made public; Q refers to Quarter. Selected Market Trading Information Selected Multiple Information Share % of 52-Week % Above 52-Week Equity Market Enterprise Enterprise Value [1] to Revenue

[5] Selected Companies Price [2] High [3] Low [3] Value [2] [4] Value [2] [4] LTM CY 2025E CY 2026E Certara, Inc. $8.58 54.7% 6.9% $1,412.8 $1,536.3 3.70x 3.67x 3.44x Definitive Healthcare

Corp. $2.31 40.7% 7.4% $362.4 $449.7 1.86x 1.88x 1.91x Health Catalyst, Inc. $2.46 30.4% 22.1% $193.0 $262.6 0.83x 0.85x 0.87x Indegene Limited $5.81 77.2% 5.5% $1,418.5 $1,278.5 3.81x 3.59x 3.06x OptimizeRx

Corporation $13.36 60.0% 234.7% $258.3 $267.6 2.44x 2.47x 2.20x Simulations Plus, Inc. $19.17 50.9% 54.7% $386.2 $353.8 4.47x 4.45x 4.30x Veradigm Inc. [6]

[7] $4.95 48.3% 65.0% $591.5 $546.5 0.94x 0.91x 0.93x Low 30.4% 5.5% 0.83x 0.85x 0.87x Median 50.9% 22.1% 2.44x 2.47x 2.20x Mean 51.7% 56.6% 2.58x 2.54x 2.39x High 77.2% 234.7% 4.47x 4.45x 4.30x Feather -

Current Price (as of 12/12/25) [8] [9] $2.13 52.9% 29.9% $69.6 $41.4 1.45x 1.38x 1.29x Feather - Unaffected Price (as of 8/22/25) [8] [9] [10] $1.77 43.9% 7.9% $56.9 $28.1 1.05x 0.96x 0.87x Sources: Bloomberg, Capital IQ and

public filings. 15 CONFIDENTIAL – PRELIMINARY – SUBJECT TO FURTHER REVIEW

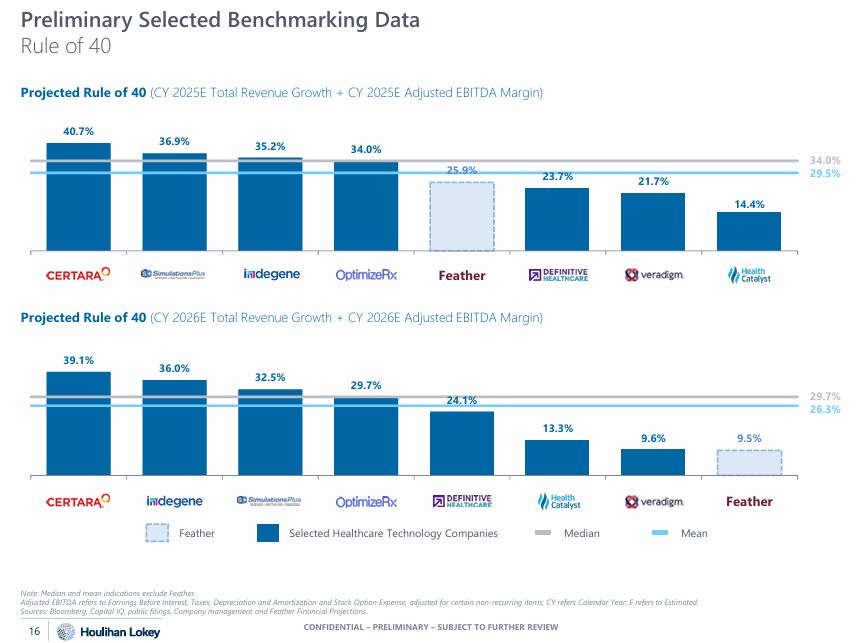

39.1% 36.0% 32.5% 29.7% 24.1% 13.3% 9.6% 9.5% Certara Indegene Simulations Plus OptimizeRx

Definitive Health Catalyst Veradigm Feather 36.9% 35.2% 34.0% 25.9% 23.7% 21.7% 14.4% Projected Rule of 40 (CY 2025E Total Revenue Growth + CY 2025E Adjusted EBITDA Margin) 40.7% Certara Simulations Plus Indegene OptimizeRx Feather

Definitive Veradigm Health Catalyst Preliminary Selected Benchmarking Data Rule of 40 34.0% 29.5% 29.7% 26.3% Note: Median and mean indications exclude Feather. Feather Projected Rule of 40 (CY 2026E Total Revenue Growth + CY 2026E

Adjusted EBITDA Margin) Feather Selected Healthcare Technology Companies Median Feather Mean Adjusted EBITDA refers to Earnings Before Interest, Taxes, Depreciation and Amortization and Stock Option Expense, adjusted for certain

non-recurring items; CY refers Calendar Year; E refers to Estimated. Sources: Bloomberg, Capital IQ, public filings, Company management and Feather Financial Projections. CONFIDENTIAL – PRELIMINARY – SUBJECT TO FURTHER REVIEW 16

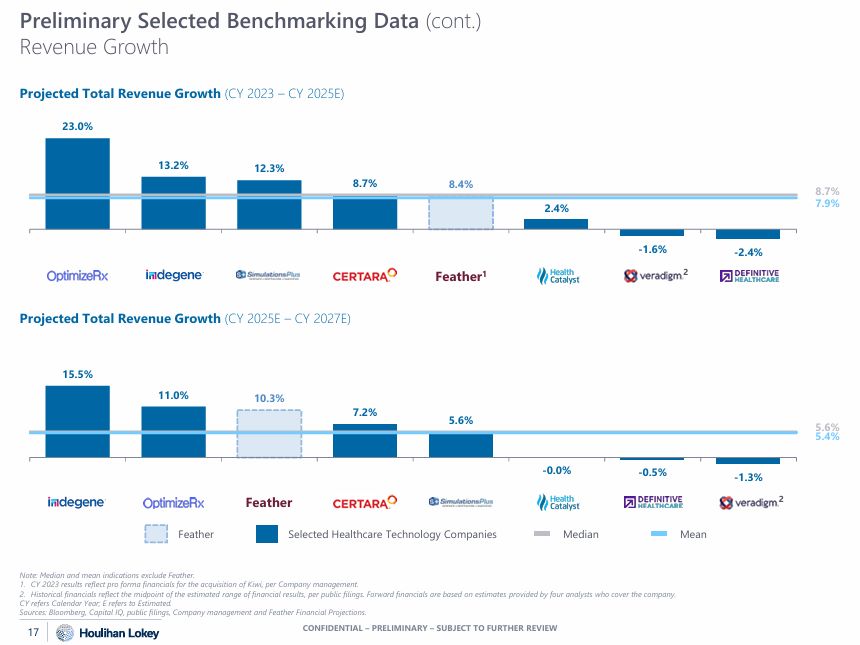

15.5% 11.0% 10.3% 7.2% 5.6% -0.0% -0.5% -1.3% Indegene OptimizeRx Feather Certara Simulations Plus

Health Catalyst Definitive Veradigm Projected Total Revenue Growth (CY 2023 – CY 2025E) 23.0% 13.2% 12.3% 8.7% 8.4% 2.4% -1.6% -2.4% OptimizeRx Indegene Simulations Plus Certara Feather Health Catalyst Veradigm Definitive Projected

Total Revenue Growth (CY 2025E – CY 2027E) Preliminary Selected Benchmarking Data (cont.) Revenue Growth 8.7% 7.9% 5.6% 5.4% Note: Median and mean indications exclude Feather. 1. CY 2023 results reflect pro forma financials for the

acquisition of Kiwi, per Company management. Feather1 2 Feather 2 Selected Healthcare Technology Companies Median Feather 2. Historical financials reflect the midpoint of the estimated range of financial results, per public filings.

Forward financials are based on estimates provided by four analysts who cover the company. CY refers Calendar Year; E refers to Estimated. Sources: Bloomberg, Capital IQ, public filings, Company management and Feather Financial

Projections. CONFIDENTIAL – PRELIMINARY – SUBJECT TO FURTHER REVIEW 17 Mean

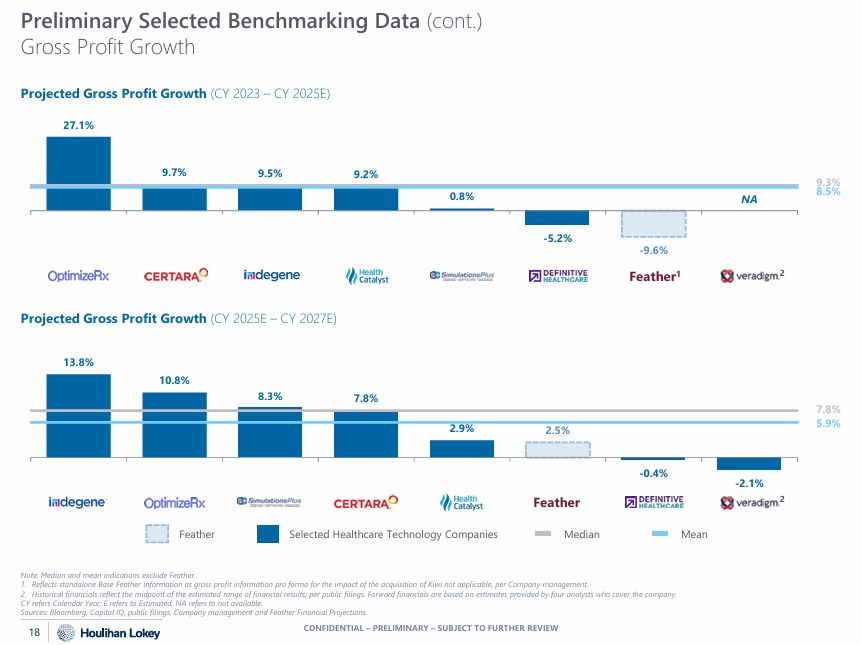

8.3% 7.8% 2.9% 2.5% -0.4% Projected Gross Profit Growth (CY 2025E – CY

2027E) 13.8% 10.8% -2.1% Indegene Limited OptimizeRx Simulations Plus, Certara, Inc. Health Catalyst, Inc. Feather Definitive Veradigm Inc. [2] Corporation Inc. Healthcare Corp. Projected Gross Profit Growth (CY 2023 – CY

2025E) 27.1% 9.7% 9.5% 9.2% -5.2% 0.8% NA -9.6% OptimizeRx Certara, Inc. Indegene Limited Health Catalyst, Inc. Simulations Plus, Definitive Feather Veradigm Inc. [2] Corporation Inc. Healthcare Corp. Preliminary Selected

Benchmarking Data (cont.) Gross Profit Growth 9.3% 8.5% 7.8% 5.9% Note: Median and mean indications exclude Feather. 1. Reflects standalone Base Feather information as gross profit information pro forma for the impact of the acquisition

of Kiwi not applicable, per Company management. Feather1 Feather 2 2 Selected Healthcare Technology Companies Median Feather Mean 2. Historical financials reflect the midpoint of the estimated range of financial results, per public

filings. Forward financials are based on estimates provided by four analysts who cover the company. CY refers Calendar Year; E refers to Estimated; NA refers to not available. Sources: Bloomberg, Capital IQ, public filings, Company

management and Feather Financial Projections. CONFIDENTIAL – PRELIMINARY – SUBJECT TO FURTHER REVIEW 18

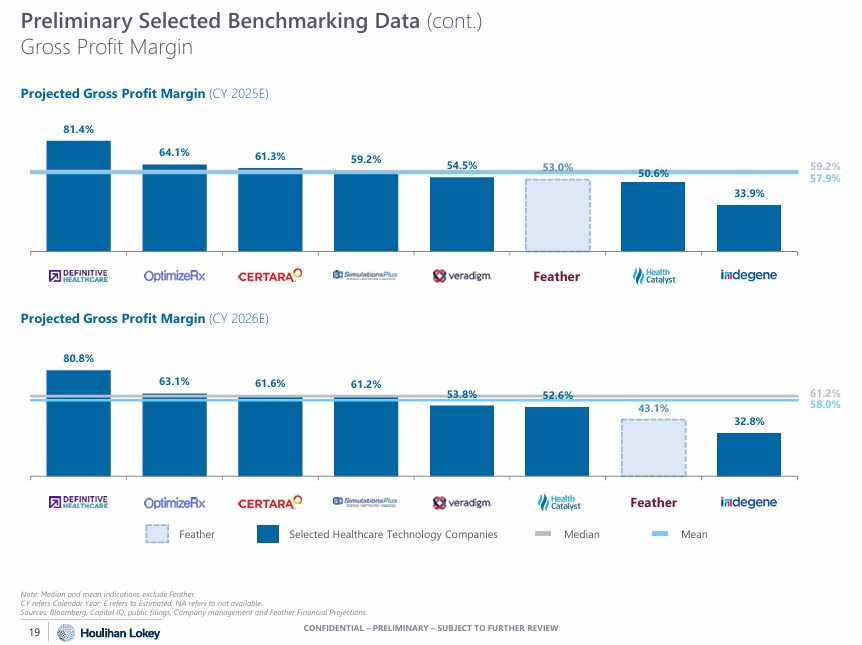

Projected Gross Profit Margin (CY 2026E) 80.8% 63.1% 61.6% 61.2% 53.8% 52.6% 43.1% 32.8% Definitive

OptimizeRx Certara Simulations Plus Veradigm Health Catalyst Feather Indegene Projected Gross Profit Margin (CY 2025E) 81.4% 64.1% 61.3% 59.2% 54.5% 53.0% 50.6% 33.9% Definitive OptimizeRx Certara Simulations Plus Veradigm Feather

Health Catalyst Indegene Preliminary Selected Benchmarking Data (cont.) Gross Profit Margin 59.2% 57.9% 61.2% 58.0% Feather Selected Healthcare Technology Companies Median Feather Mean Feather Note: Median and mean indications

exclude Feather. CY refers Calendar Year; E refers to Estimated; NA refers to not available. Sources: Bloomberg, Capital IQ, public filings, Company management and Feather Financial Projections. CONFIDENTIAL – PRELIMINARY – SUBJECT TO

FURTHER REVIEW 19

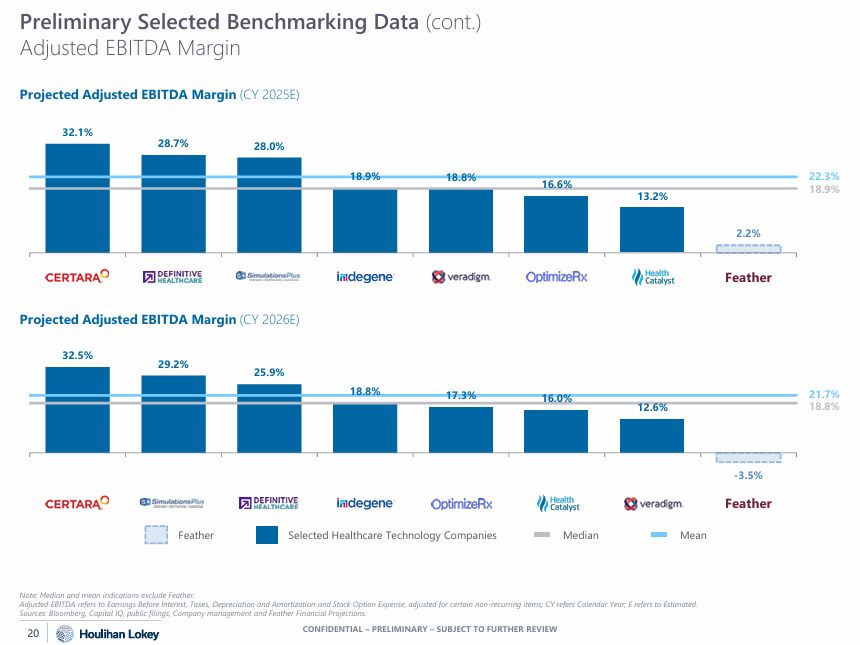

32.5% 29.2% 25.9% 18.8% 17.3% 16.0% 12.6% Certara Simulations Plus Definitive Indegene OptimizeRx

Health Catalyst Veradigm Feather 28.7% 28.0% 18.9% 18.8% 16.6% 13.2% Certara Definitive Simulations Plus Indegene Veradigm OptimizeRx Health Catalyst Feather Projected Adjusted EBITDA Margin (CY 2025E) 32.1% Preliminary Selected

Benchmarking Data (cont.) Adjusted EBITDA Margin Projected Adjusted EBITDA Margin (CY 2026E) 22.3% 18.9% 21.7% 18.8% 2.2% Feather -3.5% Feather Selected Healthcare Technology Companies Median Feather Mean Note: Median and mean

indications exclude Feather. Adjusted EBITDA refers to Earnings Before Interest, Taxes, Depreciation and Amortization and Stock Option Expense, adjusted for certain non-recurring items; CY refers Calendar Year; E refers to Estimated.

Sources: Bloomberg, Capital IQ, public filings, Company management and Feather Financial Projections. CONFIDENTIAL – PRELIMINARY – SUBJECT TO FURTHER REVIEW 20

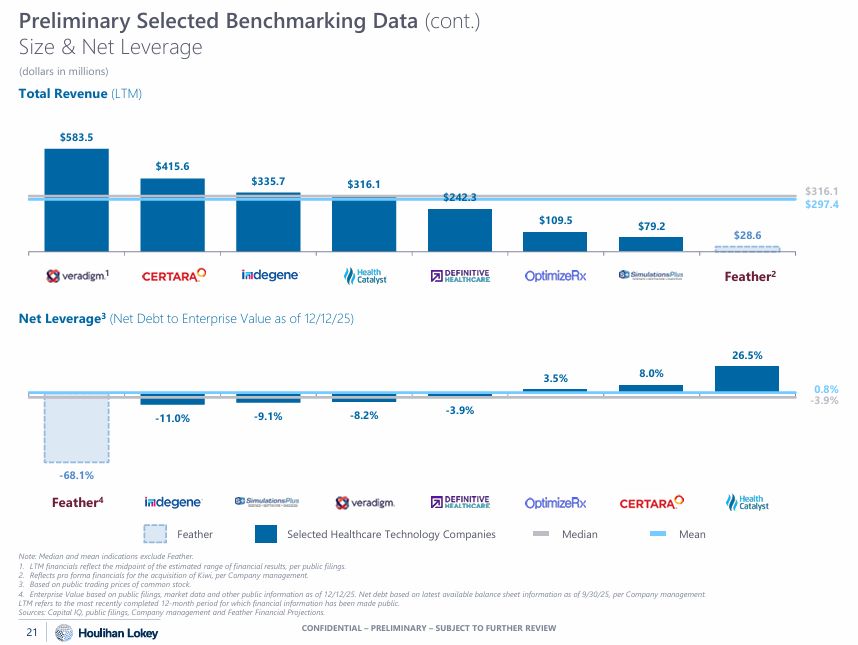

-11.0% -9.1% -8.2% -3.9% 3.5% 8.0% 26.5% Feather Indegene Simulations Plus Veradigm Definitive

OptimizeRx Certara Health Catalyst $335.7 $316.1 $242.3 $109.5 $79.2 $28.6 Veradigm Inc. Certara Indegene Health Catalyst Definitive OptimizeRx Simulations Plus Feather Preliminary Selected Benchmarking Data (cont.) Size & Net

Leverage (dollars in millions) Total Revenue (LTM) $583.5 $415.6 Net Leverage3 (Net Debt to Enterprise Value as of 12/12/25) $316.1 $297.4 0.8% -3.9% 1 -68.1% Feather4 Feather Selected Healthcare Technology Companies Median

Mean Note: Median and mean indications exclude Feather. LTM financials reflect the midpoint of the estimated range of financial results, per public filings. Reflects pro forma financials for the acquisition of Kiwi, per Company

management. Based on public trading prices of common stock. Enterprise Value based on public filings, market data and other public information as of 12/12/25. Net debt based on latest available balance sheet information as of 9/30/25, per

Company management. LTM refers to the most recently completed 12-month period for which financial information has been made public. Feather2 Sources: Capital IQ, public filings, Company management and Feather Financial

Projections. CONFIDENTIAL – PRELIMINARY – SUBJECT TO FURTHER REVIEW 21

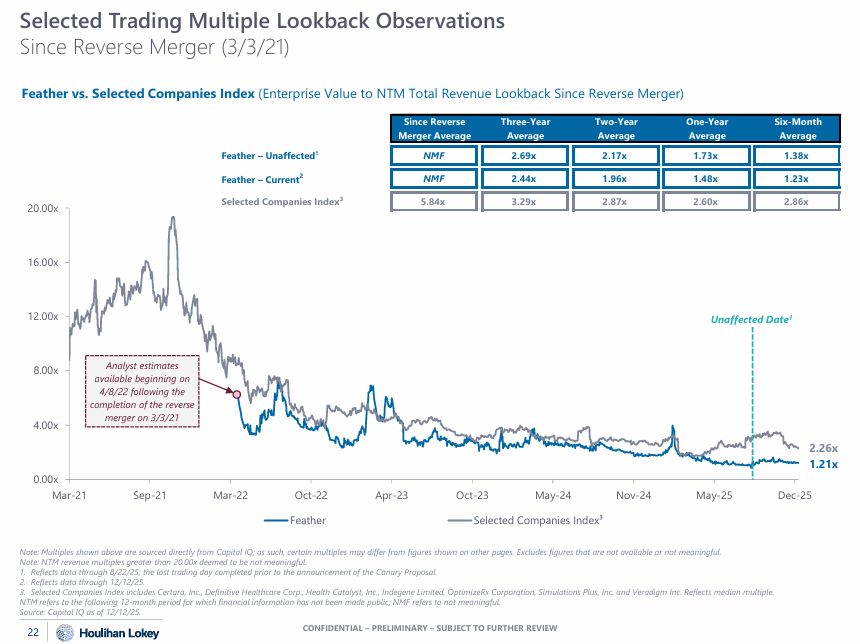

0.00x 4.00x 8.00x 12.00x 16.00x 20.00x Mar-21 Sep-21 Mar-22 Oct-22 Feather Apr-23 Nov-24 May-25 Dec-25 Oct-23

May-24 Selected Companies Index³ Source: Capital IQ as of 12/12/25. 22 CONFIDENTIAL – PRELIMINARY – SUBJECT TO FURTHER REVIEW Note: Multiples shown above are sourced directly from Capital IQ; as such, certain multiples may differ from

figures shown on other pages. Excludes figures that are not available or not meaningful. Note: NTM revenue multiples greater than 20.00x deemed to be not meaningful. Reflects data through 8/22/25, the last trading day completed prior to the

announcement of the Canary Proposal. Reflects data through 12/12/25. Selected Companies Index includes Certara, Inc., Definitive Healthcare Corp., Health Catalyst, Inc., Indegene Limited, OptimizeRx Corporation, Simulations Plus, Inc. and

Veradigm Inc. Reflects median multiple. NTM refers to the following 12-month period for which financial information has not been made public; NMF refers to not meaningful. Selected Trading Multiple Lookback Observations Since Reverse Merger

(3/3/21) 2.26x 1.21x Feather vs. Selected Companies Index (Enterprise Value to NTM Total Revenue Lookback Since Reverse Merger) Analyst estimates available beginning on 4/8/22 following the completion of the reverse merger on

3/3/21 Unaffected Date1 Feather – Unaffected1 Feather – Current2 Selected Companies Index³ Since Reverse Merger

Average Three-Year Average Two-Year Average One-Year Average Six-Month Average NMF 2.69x 2.17x 1.73x 1.38x NMF 2.44x 1.96x 1.48x 1.23x 5.84x 3.29x 2.87x 2.60x 2.86x

Transaction Value / CONFIDENTIAL – PRELIMINARY – SUBJECT TO FURTHER REVIEW 23 LTM Adjusted NFY

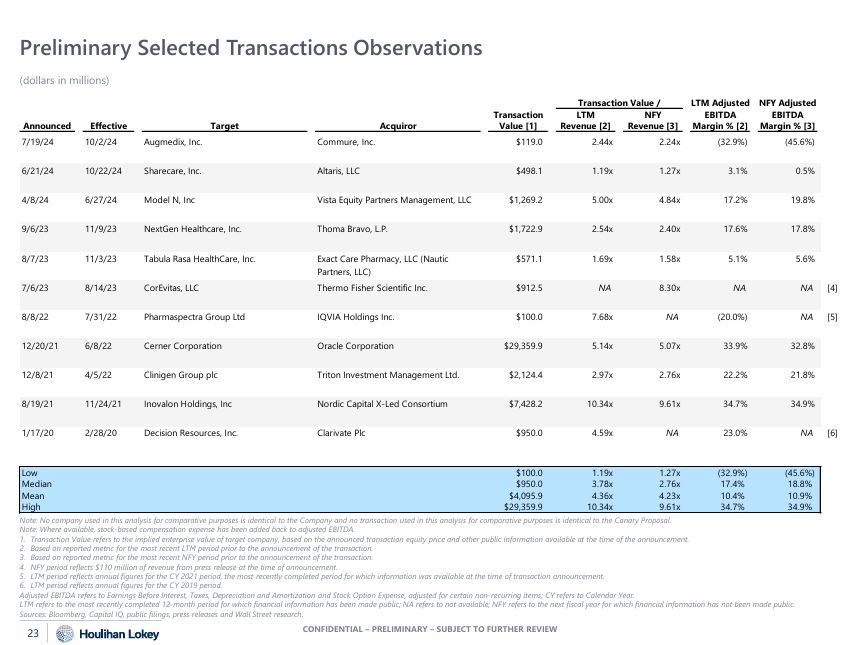

Adjusted Announced Effective Target Acquiror Transaction Value [1] LTM Revenue [2] NFY Revenue [3] EBITDA Margin % [2] EBITDA Margin % [3] 7/19/24 10/2/24 Augmedix, Inc. Commure,

Inc. $119.0 2.44x 2.24x (32.9%) (45.6%) 6/21/24 10/22/24 Sharecare, Inc. Altaris, LLC $498.1 1.19x 1.27x 3.1% 0.5% 4/8/24 6/27/24 Model N, Inc Vista Equity Partners Management,

LLC $1,269.2 5.00x 4.84x 17.2% 19.8% 9/6/23 11/9/23 NextGen Healthcare, Inc. Thoma Bravo, L.P. $1,722.9 2.54x 2.40x 17.6% 17.8% 8/7/23 11/3/23 Tabula Rasa HealthCare, Inc. Exact Care Pharmacy, LLC

(Nautic $571.1 1.69x 1.58x 5.1% 5.6% Partners, LLC) 7/6/23 8/14/23 CorEvitas, LLC Thermo Fisher Scientific Inc. $912.5 NA 8.30x NA NA [4] 8/8/22 7/31/22 Pharmaspectra Group Ltd IQVIA Holdings

Inc. $100.0 7.68x NA (20.0%) NA [5] 12/20/21 6/8/22 Cerner Corporation Oracle Corporation $29,359.9 5.14x 5.07x 33.9% 32.8% 12/8/21 4/5/22 Clinigen Group plc Triton Investment Management

Ltd. $2,124.4 2.97x 2.76x 22.2% 21.8% 8/19/21 11/24/21 Inovalon Holdings, Inc Nordic Capital X-Led Consortium $7,428.2 10.34x 9.61x 34.7% 34.9% 1/17/20 2/28/20 Decision Resources, Inc. Clarivate

Plc $950.0 4.59x NA 23.0% NA [6] Low $100.0 1.19x 1.27x (32.9%) (45.6%) Median $950.0 3.78x 2.76x 17.4% 18.8% Mean $4,095.9 4.36x 4.23x 10.4% 10.9% High $29,359.9 10.34x 9.61x 34.7% 34.9% Preliminary Selected

Transactions Observations (dollars in millions) Note: No company used in this analysis for comparative purposes is identical to the Company and no transaction used in this analysis for comparative purposes is identical to the Canary

Proposal. Note: Where available, stock-based compensation expense has been added back to adjusted EBITDA. Transaction Value refers to the implied enterprise value of target company, based on the announced transaction equity price and other

public information available at the time of the announcement. Based on reported metric for the most recent LTM period prior to the announcement of the transaction. Based on reported metric for the most recent NFY period prior to the

announcement of the transaction. NFY period reflects $110 million of revenue from press release at the time of announcement. LTM period reflects annual figures for the CY 2021 period, the most recently completed period for which information

was available at the time of transaction announcement. LTM period reflects annual figures for the CY 2019 period. Adjusted EBITDA refers to Earnings Before Interest, Taxes, Depreciation and Amortization and Stock Option Expense, adjusted

for certain non-recurring items; CY refers to Calendar Year. LTM refers to the most recently completed 12-month period for which financial information has been made public; NA refers to not available; NFY refers to the next fiscal year for

which financial information has not been made public. Sources: Bloomberg, Capital IQ, public filings, press releases and Wall Street research.

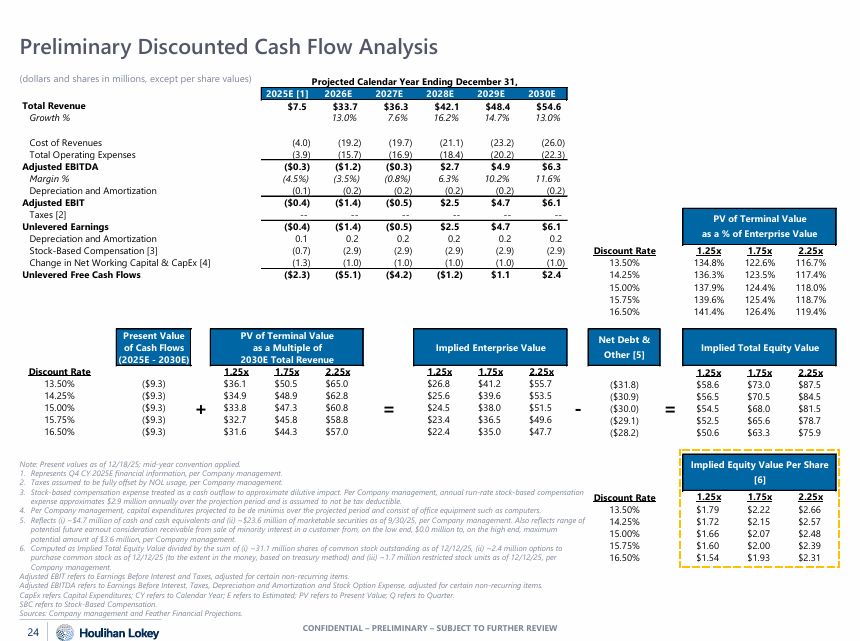

Present Value of Cash Flows (2025E - 2030E) Projected Calendar Year Ending December 31, Implied

Enterprise Value Implied Total Equity Value PV of Terminal Value as a Multiple of 2030E Total Revenue Discount Rate 1.25x 1.75x 2.25x 1.25x 1.75x 2.25x 1.25x 1.75x

2.25x 13.50% ($9.3) $36.1 $50.5 $65.0 $26.8 $41.2 $55.7 ($31.8) $58.6 $73.0 $87.5 14.25% ($9.3) $34.9 $48.9 $62.8 $25.6 $39.6 $53.5 ($30.9) $56.5 $70.5 $84.5 15.00% ($9.3) $33.8 $47.3 $60.8 $24.5 $38.0 $51.5 ($30.0) $54.5 $68.0 $81.5 15.75% ($9.3) $32.7 $45.8 $58.8 $23.4 $36.5 $49.6 ($29.1) $52.5 $65.6 $78.7 16.50% ($9.3) $31.6 $44.3 $57.0 $22.4 $35.0 $47.7 ($28.2) $50.6 $63.3 $75.9 Discount

Rate Implied Equity Value Per Share [6] 1.25x 1.75x 2.25x Net Debt & Other [5] 2025E [1] 2026E 2027E 2028E 2029E 2030E Total Revenue $7.5 $33.7 $36.3 $42.1 $48.4 $54.6 Growth % 13.0% 7.6% 16.2% 14.7% 13.0% Cost of

Revenues (4.0) (19.2) (19.7) (21.1) (23.2) (26.0) Total Operating Expenses (3.9) (15.7) (16.9) (18.4) (20.2) (22.3) Adjusted EBITDA ($0.3) ($1.2) ($0.3) $2.7 $4.9 $6.3 Margin

% (4.5%) (3.5%) (0.8%) 6.3% 10.2% 11.6% Depreciation and Amortization (0.1) (0.2) (0.2) (0.2) (0.2) (0.2) Adjusted EBIT ($0.4) ($1.4) ($0.5) $2.5 $4.7 $6.1 Taxes [2] -- -- -- -- -- -- Unlevered

Earnings ($0.4) ($1.4) ($0.5) $2.5 $4.7 $6.1 Depreciation and Amortization 0.1 0.2 0.2 0.2 0.2 0.2 Stock-Based Compensation [3] (0.7) (2.9) (2.9) (2.9) (2.9) (2.9) Discount Rate 1.25x 1.75x 2.25x Change in Net Working

Capital & CapEx [4] (1.3) (1.0) (1.0) (1.0) (1.0) (1.0) 13.50% 134.8% 122.6% 116.7% Unlevered Free Cash

Flows ($2.3) ($5.1) ($4.2) ($1.2) $1.1 $2.4 14.25% 136.3% 123.5% 117.4% 15.00% 137.9% 124.4% 118.0% 15.75% 139.6% 125.4% 118.7% 16.50% 141.4% 126.4% 119.4% PV of Terminal Value as a % of Enterprise Value Preliminary

Discounted Cash Flow Analysis CONFIDENTIAL – PRELIMINARY – SUBJECT TO FURTHER REVIEW 24 Note: Present values as of 12/18/25; mid-year convention applied. Represents Q4 CY 2025E financial information, per Company management. Taxes assumed

to be fully offset by NOL usage, per Company management. Stock-based compensation expense treated as a cash outflow to approximate dilutive impact. Per Company management, annual run-rate stock-based compensation expense approximates $2.9

million annually over the projection period and is assumed to not be tax deductible. 4. Per Company management, capital expenditures projected to be de minimis over the projected period and consist of office equipment such as

computers. 13.50% $1.79 $2.22 $2.66 5. Reflects (i) ~$4.7 million of cash and cash equivalents and (ii) ~$23.6 million of marketable securities as of 9/30/25, per Company management. Also reflects range

of 14.25% $1.72 $2.15 $2.57 potential future earnout consideration receivable from sale of minority interest in a customer from, on the low end, $0.0 million to, on the high end, maximum potential amount of $3.6 million, per Company

management. 6. Computed as Implied Total Equity Value divided by the sum of (i) ~31.1 million shares of common stock outstanding as of 12/12/25, (ii) ~2.4 million options to 15.00% 15.75% $1.66 $1.60 $2.07 $2.00 $2.48 $2.39 purchase

common stock as of 12/12/25 (to the extent in the money, based on treasury method) and (iii) ~1.7 million restricted stock units as of 12/12/25, per Company management. 16.50% $1.54 $1.93 $2.31 Adjusted EBIT refers to Earnings Before

Interest and Taxes, adjusted for certain non-recurring items. Adjusted EBITDA refers to Earnings Before Interest, Taxes, Depreciation and Amortization and Stock Option Expense, adjusted for certain non-recurring items. CapEx refers Capital

Expenditures; CY refers to Calendar Year; E refers to Estimated; PV refers to Present Value; Q refers to Quarter. SBC refers to Stock-Based Compensation. Sources: Company management and Feather Financial Projections. (dollars and shares in

millions, except per share values)

04 04 SELECTED CONSIDERATIONS RELATED TO CANARY PROPOSAL CONFIDENTIAL – PRELIMINARY – SUBJECT TO FURTHER

REVIEW

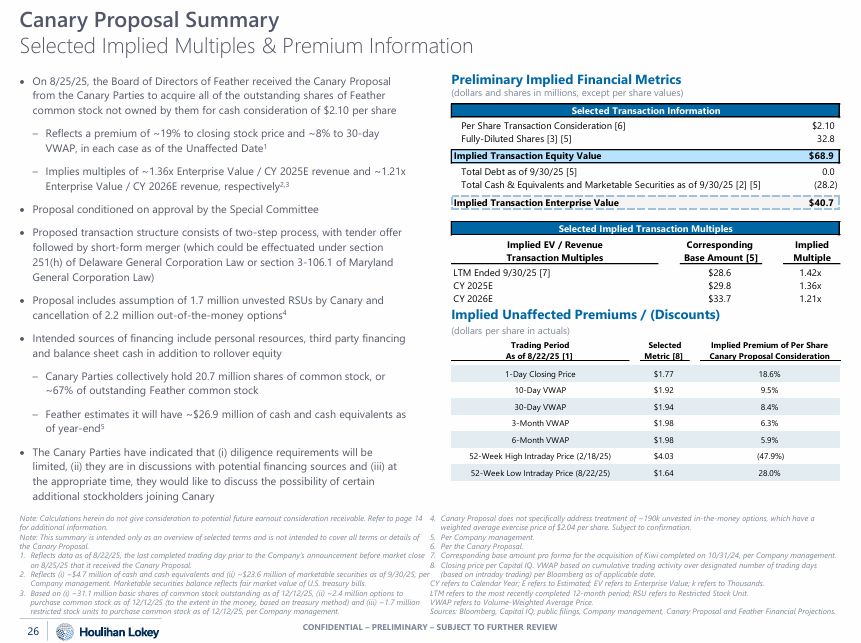

Canary Proposal Summary Selected Implied Multiples & Premium Information Note: Calculations herein do

not give consideration to potential future earnout consideration receivable. Refer to page 14 4. Canary Proposal does not specifically address treatment of ~190k unvested in-the-money options, which have a for additional information. weighted

average exercise price of $2.04 per share. Subject to confirmation. Note: This summary is intended only as an overview of selected terms and is not intended to cover all terms or details of 5. Per Company management. the Canary Proposal. 6.

Per the Canary Proposal. Reflects data as of 8/22/25, the last completed trading day prior to the Company’s announcement before market close 7. Corresponding base amount pro forma for the acquisition of Kiwi completed on 10/31/24, per

Company management. on 8/25/25 that it received the Canary Proposal. 8. Closing price per Capital IQ. VWAP based on cumulative trading activity over designated number of trading days Reflects (i) ~$4.7 million of cash and cash equivalents

and (ii) ~$23.6 million of marketable securities as of 9/30/25, per (based on intraday trading) per Bloomberg as of applicable date. Company management. Marketable securities balance reflects fair market value of U.S. treasury bills. CY

refers to Calendar Year; E refers to Estimated; EV refers to Enterprise Value; k refers to Thousands. Based on (i) ~31.1 million basic shares of common stock outstanding as of 12/12/25, (ii) ~2.4 million options to LTM refers to the most

recently completed 12-month period; RSU refers to Restricted Stock Unit. purchase common stock as of 12/12/25 (to the extent in the money, based on treasury method) and (iii) ~1.7 million VWAP refers to Volume-Weighted Average

Price. restricted stock units to purchase common stock as of 12/12/25, per Company management. Sources: Bloomberg, Capital IQ, public filings, Company management, Canary Proposal and Feather Financial Projections. Preliminary Implied

Financial Metrics (dollars and shares in millions, except per share values) On 8/25/25, the Board of Directors of Feather received the Canary Proposal from the Canary Parties to acquire all of the outstanding shares of Feather common stock

not owned by them for cash consideration of $2.10 per share Reflects a premium of ~19% to closing stock price and ~8% to 30-day VWAP, in each case as of the Unaffected Date1 Implies multiples of ~1.36x Enterprise Value / CY 2025E revenue

and ~1.21x Enterprise Value / CY 2026E revenue, respectively2,3 Proposal conditioned on approval by the Special Committee Proposed transaction structure consists of two-step process, with tender offer followed by short-form merger (which

could be effectuated under section 251(h) of Delaware General Corporation Law or section 3-106.1 of Maryland General Corporation Law) Proposal includes assumption of 1.7 million unvested RSUs by Canary and cancellation of 2.2 million

out-of-the-money options4 Intended sources of financing include personal resources, third party financing and balance sheet cash in addition to rollover equity Canary Parties collectively hold 20.7 million shares of common stock, or ~67%

of outstanding Feather common stock Feather estimates it will have ~$26.9 million of cash and cash equivalents as of year-end5 The Canary Parties have indicated that (i) diligence requirements will be limited, (ii) they are in discussions

with potential financing sources and (iii) at the appropriate time, they would like to discuss the possibility of certain additional stockholders joining Canary Implied Unaffected Premiums / (Discounts) (dollars per share in

actuals) Trading Period Selected Implied Premium of Per Share As of 8/22/25 [1] Metric [8] Canary Proposal Consideration 1-Day Closing Price $1.77 18.6% 10-Day VWAP $1.92 9.5% 30-Day VWAP $1.94 8.4% 3-Month

VWAP $1.98 6.3% 6-Month VWAP $1.98 5.9% 52-Week High Intraday Price (2/18/25) $4.03 (47.9%) 52-Week Low Intraday Price (8/22/25) $1.64 28.0% Selected Transaction Information Per Share Transaction Consideration [6] Fully-Diluted

Shares [3] [5] $2.10 32.8 Implied Transaction Equity Value $68.9 Total Debt as of 9/30/25 [5] Total Cash & Equivalents and Marketable Securities as of 9/30/25 [2] [5] 0.0 (28.2) Implied Transaction Enterprise Value $40.7 Selected

Implied Transaction Multiples Implied EV / Revenue Transaction Multiples LTM Ended 9/30/25 [7] CY 2025E CY 2026E Corresponding Base Amount [5] $28.6 $29.8 $33.7 Implied Multiple 1.42x 1.36x 1.21x CONFIDENTIAL –

PRELIMINARY – SUBJECT TO FURTHER REVIEW 26

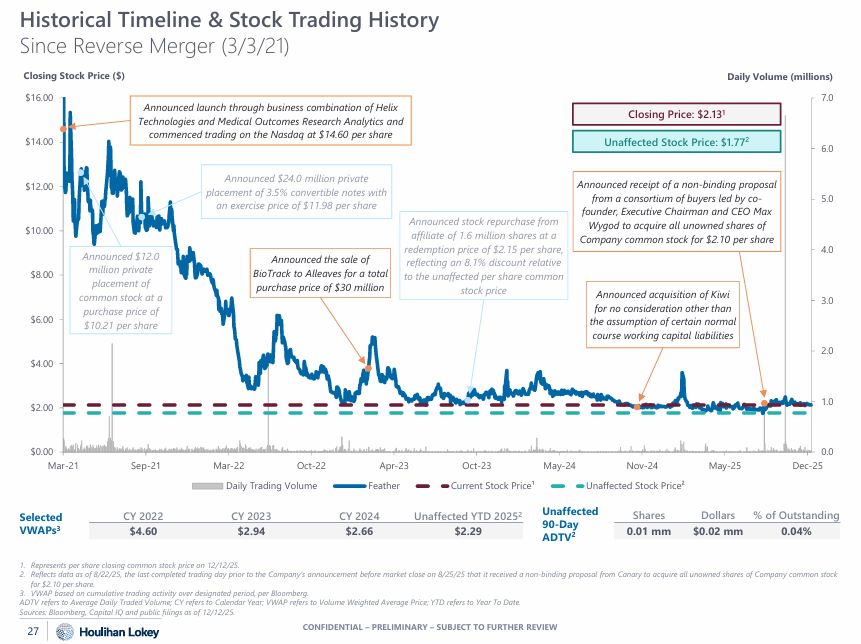

0.0 1.0 2.0 3.0 4.0 5.0 6.0 7.0 $0.00 $2.00 $4.00 $6.00 $8.00 $10.00 $12.00 $14.00 $16.00 Mar-21 Sep-21 Apr-23 Feather Oct-23 Current

Stock Price¹ May-24 Nov-24 Unaffected Stock Price² May-25 Dec-25 Mar-22 Oct-22 Daily Trading Volume Closing Stock Price ($) Daily Volume (millions) Historical Timeline & Stock Trading History Since Reverse Merger

(3/3/21) Represents per share closing common stock price on 12/12/25. Reflects data as of 8/22/25, the last completed trading day prior to the Company’s announcement before market close on 8/25/25 that it received a non-binding proposal

from Canary to acquire all unowned shares of Company common stock for $2.10 per share. VWAP based on cumulative trading activity over designated period, per Bloomberg. ADTV refers to Average Daily Traded Volume; CY refers to Calendar Year;

VWAP refers to Volume Weighted Average Price; YTD refers to Year To Date. Closing Price: $2.131 Announced receipt of a non-binding proposal from a consortium of buyers led by co-founder, Executive Chairman and CEO Max Wygod to acquire all

unowned shares of Company common stock for $2.10 per share Unaffected Stock Price: $1.772 Announced launch through business combination of Helix Technologies and Medical Outcomes Research Analytics and commenced trading on the Nasdaq at

$14.60 per share Announced the sale of BioTrack to Alleaves for a total purchase price of $30 million Announced stock repurchase from affiliate of 1.6 million shares at a redemption price of $2.15 per share, reflecting an 8.1% discount

relative to the unaffected per share common stock price Unaffected 90-Day ADTV2 Shares Dollars % of Outstanding 0.01 mm $0.02 mm 0.04% Selected VWAPs3 Announced $12.0 million private placement of common stock at a purchase price

of $10.21 per share Announced $24.0 million private placement of 3.5% convertible notes with an exercise price of $11.98 per share Announced acquisition of Kiwi for no consideration other than the assumption of certain normal course

working capital liabilities CY 2022 CY 2023 CY 2024 Unaffected YTD 20252 $4.60 $2.94 $2.66 $2.29 Sources: Bloomberg, Capital IQ and public filings as of 12/12/25. 27 CONFIDENTIAL – PRELIMINARY – SUBJECT TO FURTHER REVIEW

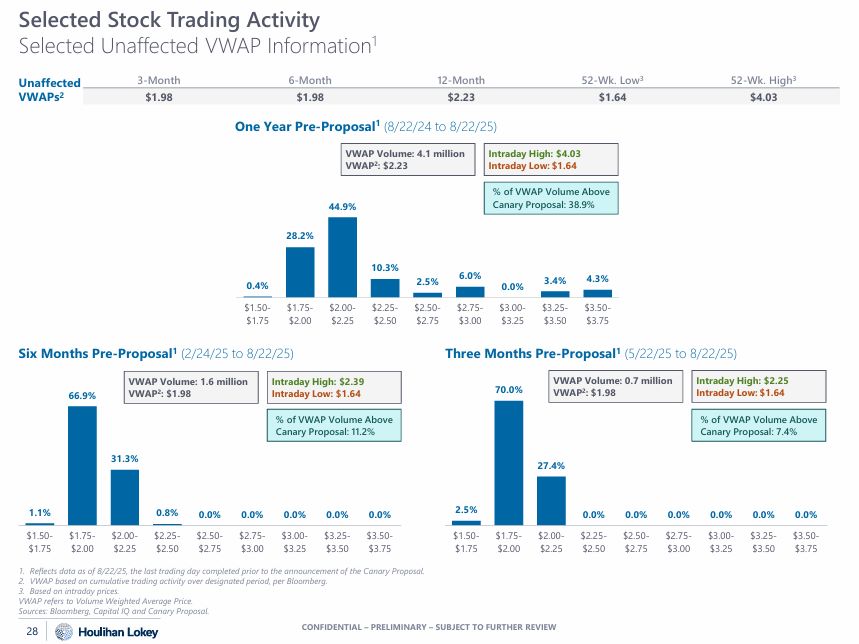

70.0% 27.4% 28.2% 44.9% 10.3% 6.0% 3.4% 4.3% 0.4% 2.5% 0.0% $1.50- $1.75- $2.00- $2.25- $2.50- $2.75- $3.00- $3.25- $3.50- $1.75 $2.00 $2.25 $2.50 $2.75 $3.00 $3.25 $3.50 $3.75 Reflects

data as of 8/22/25, the last trading day completed prior to the announcement of the Canary Proposal. VWAP based on cumulative trading activity over designated period, per Bloomberg. Based on intraday prices. VWAP refers to Volume Weighted

Average Price. Intraday High: $4.03 Intraday Low: $1.64 Selected Stock Trading Activity Selected Unaffected VWAP Information1 One Year Pre-Proposal1 (8/22/24 to 8/22/25) VWAP Volume: 4.1 million VWAP2: $2.23 66.9% Sources: Bloomberg,

Capital IQ and Canary Proposal. 28 CONFIDENTIAL – PRELIMINARY – SUBJECT TO FURTHER

REVIEW 31.3% 1.1% 0.8% 0.0% 0.0% 0.0% 0.0% 0.0% 2.5% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% $1.50- $1.75- $2.00- $2.25- $2.50- $2.75- $3.00- $3.25- $3.50- $1.50- $1.75- $2.00- $2.25- $2.50- $2.75- $3.00- $3.25- $3.50- $1.75 $2.00 $2.25 $2.50 $2.75 $3.00 $3.25 $3.50 $3.75 $1.75 $2.00 $2.25 $2.50 $2.75 $3.00 $3.25 $3.50 $3.75 Six

Months Pre-Proposal1 (2/24/25 to 8/22/25) Intraday High: $2.39 Intraday Low: $1.64 VWAP Volume: 1.6 million VWAP2: $1.98 Three Months Pre-Proposal1 (5/22/25 to 8/22/25) VWAP Volume: 0.7 million VWAP2: $1.98 Intraday High: $2.25 Intraday

Low: $1.64 Unaffected VWAPs2 3-Month 6-Month 12-Month 52-Wk. Low3 52-Wk. High3 $1.98 $1.98 $2.23 $1.64 $4.03 % of VWAP Volume Above Canary Proposal: 38.9% % of VWAP Volume Above Canary Proposal: 7.4% % of VWAP Volume Above

Canary Proposal: 11.2%

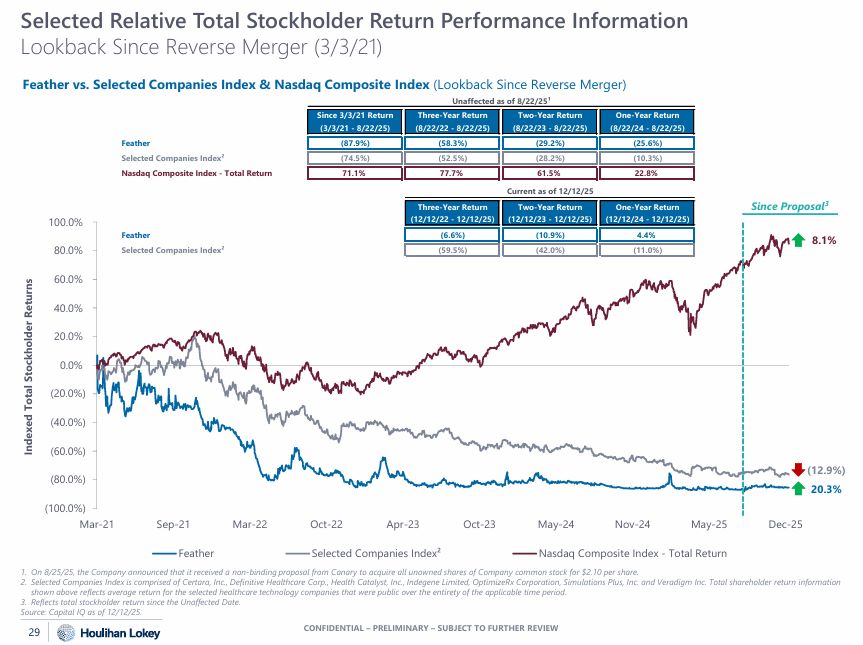

(100.0%) (80.0%) 60.0% 40.0% 20.0% 0.0% (20.0%) (40.0%) (60.0%) 80.0% 100.0% Mar-21 Sep-21 Mar-22 Oct-23 May-24

Nov-24 May-25 Nasdaq Composite Index - Total Return Dec-25 Feather Oct-22 Apr-23 Selected Companies Index² On 8/25/25, the Company announced that it received a non-binding proposal from Canary to acquire all unowned shares of Company

common stock for $2.10 per share. Selected Companies Index is comprised of Certara, Inc., Definitive Healthcare Corp., Health Catalyst, Inc., Indegene Limited, OptimizeRx Corporation, Simulations Plus, Inc. and Veradigm Inc. Total

shareholder return information shown above reflects average return for the selected healthcare technology companies that were public over the entirety of the applicable time period. Reflects total stockholder return since the Unaffected

Date. Selected Relative Total Stockholder Return Performance Information Lookback Since Reverse Merger (3/3/21) Indexed Total Stockholder Returns Feather vs. Selected Companies Index & Nasdaq Composite Index (Lookback Since Reverse

Merger) Unaffected as of 8/22/25¹ 8.1% (12.9%) 20.3% Since Proposal3 Since 3/3/21 Return (3/3/21 - 8/22/25) Three-Year Return (8/22/22 - 8/22/25) Two-Year Return (8/22/23 - 8/22/25) One-Year Return (8/22/24 -

8/22/25) (87.9%) (58.3%) (29.2%) (25.6%) (74.5%) (52.5%) (28.2%) (10.3%) 71.1% 77.7% 61.5% 22.8% Feather Selected Companies Index² Nasdaq Composite Index - Total Return Current as of 12/12/25 Feather Selected Companies

Index² Three-Year Return (12/12/22 - 12/12/25) Two-Year Return (12/12/23 - 12/12/25) One-Year Return (12/12/24 - 12/12/25) (6.6%) (10.9%) 4.4% (59.5%) (42.0%) (11.0%) Source: Capital IQ as of 12/12/25. 29 CONFIDENTIAL –

PRELIMINARY – SUBJECT TO FURTHER REVIEW

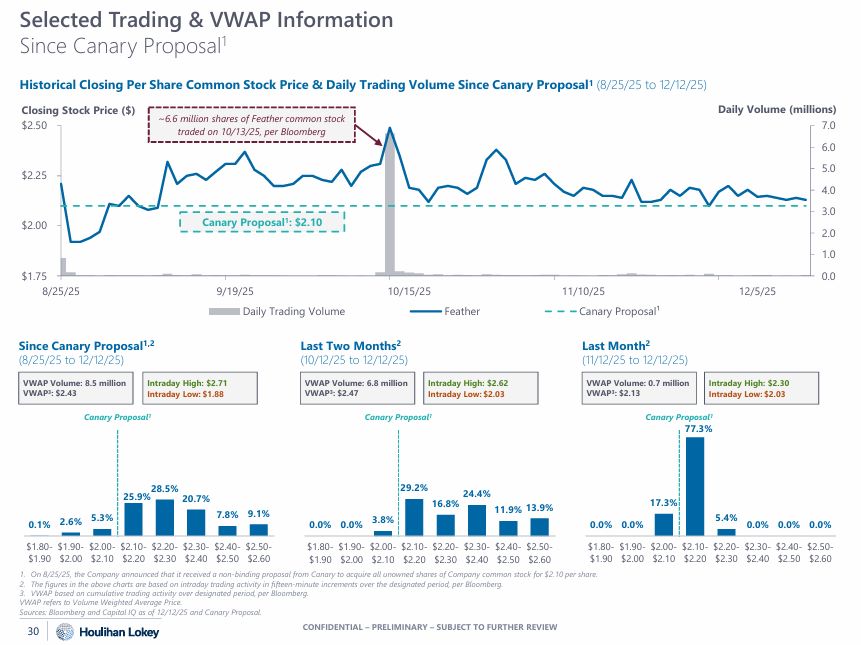

Canary Proposal1:

$2.10 7.0 6.0 5.0 4.0 3.0 2.0 1.0 0.0 $1.75 $2.00 $2.25 $2.50 8/25/25 9/19/25 10/15/25 11/10/25 12/5/25 Daily Trading Volume Feather Canary Proposal¹ Closing Stock Price ($) Daily Volume

(millions) 0.1% 2.6% 5.3% 25.9% 28.5% 20.7% 7.8% 9.1% $1.80- $1.90- $2.00- $2.10- $2.20- $2.30- $2.40- $2.50- $1.90 $2.00 $2.10 $2.20 $2.30 $2.40 $2.50 $2.60 0.0% 0.0% 3.8% 29.2% 16.8% 24.4% 11.9% 13.9% $1.80- $1.90- $2.00-

$2.10- $2.20- $2.30- $2.40- $2.50- $1.90 $2.00 $2.10 $2.20 $2.30 $2.40 $2.50 $2.60 17.3% 77.3% 5.4% 0.0% 0.0% 0.0% 0.0% 0.0% $1.80- $1.90- $2.00- $2.10- $2.20- $2.30- $2.40- $2.50- $1.90 $2.00 $2.10 $2.20 $2.30 $2.40 $2.50 $2.60 On

8/25/25, the Company announced that it received a non-binding proposal from Canary to acquire all unowned shares of Company common stock for $2.10 per share. The figures in the above charts are based on intraday trading activity in

fifteen-minute increments over the designated period, per Bloomberg. VWAP based on cumulative trading activity over designated period, per Bloomberg. VWAP refers to Volume Weighted Average Price. Selected Trading & VWAP

Information Since Canary Proposal1 Since Canary Proposal1,2 (8/25/25 to 12/12/25) Historical Closing Per Share Common Stock Price & Daily Trading Volume Since Canary Proposal1 (8/25/25 to 12/12/25) Last Two Months2 (10/12/25 to

12/12/25) Last Month2 (11/12/25 to 12/12/25) ~6.6 million shares of Feather common stock traded on 10/13/25, per Bloomberg VWAP Volume: 8.5 million VWAP3: $2.43 Intraday High: $2.71 Intraday Low: $1.88 VWAP Volume: 6.8 million VWAP3:

$2.47 Intraday High: $2.62 Intraday Low: $2.03 VWAP Volume: 0.7 million VWAP3: $2.13 Intraday High: $2.30 Intraday Low: $2.03 Canary Proposal1 Sources: Bloomberg and Capital IQ as of 12/12/25 and Canary Proposal. 30 CONFIDENTIAL –

PRELIMINARY – SUBJECT TO FURTHER REVIEW Canary Proposal1 Canary Proposal1

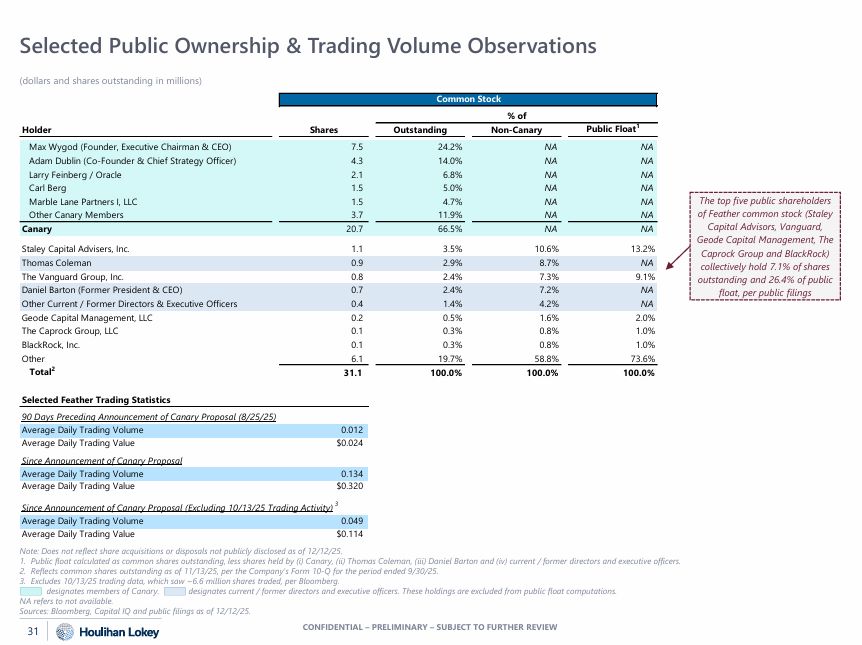

Selected Public Ownership & Trading Volume Observations (dollars and shares outstanding in

millions) The top five public shareholders of Feather common stock (Staley Capital Advisors, Vanguard, Geode Capital Management, The Caprock Group and BlackRock) collectively hold 7.1% of shares outstanding and 26.4% of public float, per

public filings Max Wygod (Founder, Executive Chairman & CEO) 7.5 24.2% NA NA Adam Dublin (Co-Founder & Chief Strategy Officer) 4.3 14.0% NA NA Larry Feinberg / Oracle 2.1 6.8% NA NA Carl Berg 1.5 5.0% NA NA Marble

Lane Partners I, LLC 1.5 4.7% NA NA Other Canary Members 3.7 11.9% NA NA Canary 20.7 66.5% NA NA Staley Capital Advisers, Inc. 1.1 3.5% 10.6% 13.2% Thomas Coleman 0.9 2.9% 8.7% NA The Vanguard Group,

Inc. 0.8 2.4% 7.3% 9.1% Daniel Barton (Former President & CEO) 0.7 2.4% 7.2% NA Other Current / Former Directors & Executive Officers 0.4 1.4% 4.2% NA Geode Capital Management, LLC 0.2 0.5% 1.6% 2.0% The Caprock

Group, LLC 0.1 0.3% 0.8% 1.0% BlackRock, Inc. 0.1 0.3% 0.8% 1.0% Other 6.1 19.7% 58.8% 73.6% Total2 31.1 100.0% 100.0% 100.0% Common Stock Holder Shares Outstanding % of Non-Canary Public Float1 Selected Feather

Trading Statistics 90 Days Preceding Announcement of Canary Proposal (8/25/25) Average Daily Trading Volume 0.012 Average Daily Trading Value $0.024 Since Announcement of Canary Proposal Average Daily Trading Volume 0.134 Average Daily

Trading Value $0.320 Since Announcement of Canary Proposal (Excluding 10/13/25 Trading Activity) 3 Average Daily Trading Volume 0.049 Average Daily Trading Value $0.114 Note: Does not reflect share acquisitions or disposals not publicly

disclosed as of 12/12/25. Public float calculated as common shares outstanding, less shares held by (i) Canary, (ii) Thomas Coleman, (iii) Daniel Barton and (iv) current / former directors and executive officers. Reflects common shares

outstanding as of 11/13/25, per the Company's Form 10-Q for the period ended 9/30/25. Excludes 10/13/25 trading data, which saw ~6.6 million shares traded, per Bloomberg. designates members of Canary. designates current / former directors

and executive officers. These holdings are excluded from public float computations. NA refers to not available. Sources: Bloomberg, Capital IQ and public filings as of 12/12/25. 31 CONFIDENTIAL – PRELIMINARY – SUBJECT TO FURTHER REVIEW

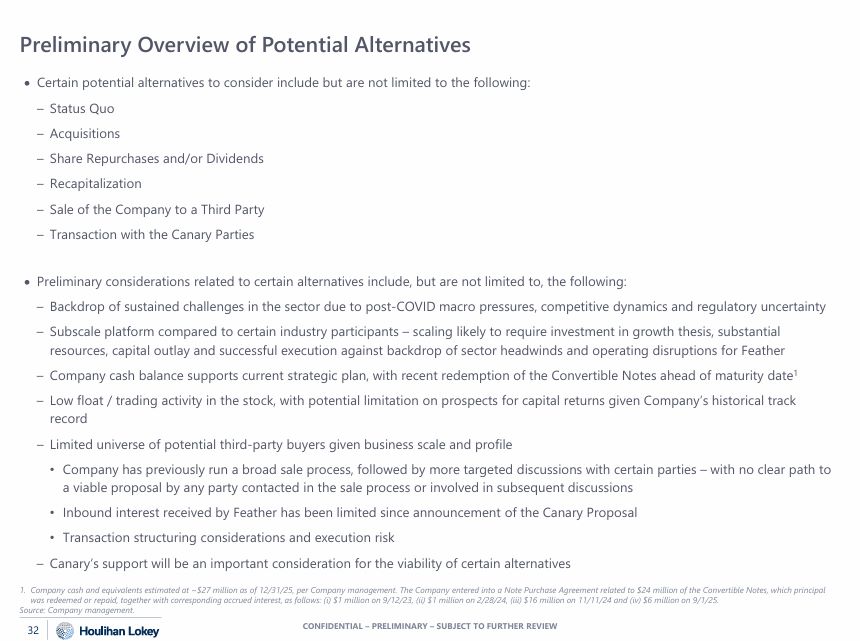

Preliminary Overview of Potential Alternatives Source: Company management. 32 CONFIDENTIAL – PRELIMINARY

– SUBJECT TO FURTHER REVIEW Certain potential alternatives to consider include but are not limited to the following: Status Quo Acquisitions Share Repurchases and/or Dividends Recapitalization Sale of the Company to a Third

Party Transaction with the Canary Parties Preliminary considerations related to certain alternatives include, but are not limited to, the following: Backdrop of sustained challenges in the sector due to post-COVID macro pressures,

competitive dynamics and regulatory uncertainty Subscale platform compared to certain industry participants – scaling likely to require investment in growth thesis, substantial resources, capital outlay and successful execution against

backdrop of sector headwinds and operating disruptions for Feather Company cash balance supports current strategic plan, with recent redemption of the Convertible Notes ahead of maturity date1 Low float / trading activity in the stock, with

potential limitation on prospects for capital returns given Company’s historical track record Limited universe of potential third-party buyers given business scale and profile Company has previously run a broad sale process, followed by

more targeted discussions with certain parties – with no clear path to a viable proposal by any party contacted in the sale process or involved in subsequent discussions Inbound interest received by Feather has been limited since

announcement of the Canary Proposal Transaction structuring considerations and execution risk Canary’s support will be an important consideration for the viability of certain alternatives 1. Company cash and equivalents estimated at ~$27

million as of 12/31/25, per Company management. The Company entered into a Note Purchase Agreement related to $24 million of the Convertible Notes, which principal was redeemed or repaid, together with corresponding accrued interest, as

follows: (i) $1 million on 9/12/23, (ii) $1 million on 2/28/24, (iii) $16 million on 11/11/24 and (iv) $6 million on 9/1/25.

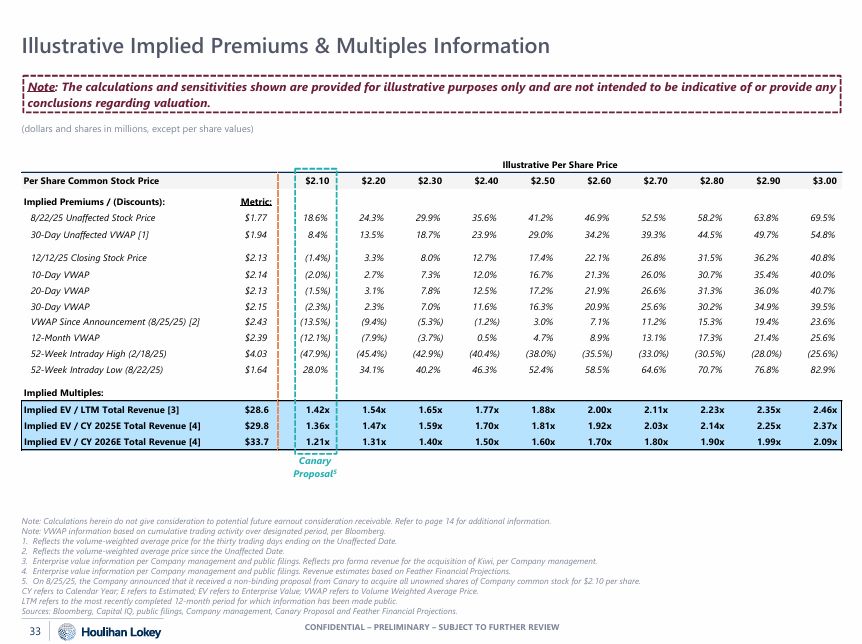

Per Share Common Stock Price $2.10 $2.20 $2.30 $2.40 $2.50 $2.60 $2.70 $2.80 $2.90 $3.00 Implied

Premiums / (Discounts): Metric: 8/22/25 Unaffected Stock Price $1.77 18.6% 24.3% 29.9% 35.6% 41.2% 46.9% 52.5% 58.2% 63.8% 69.5% 30-Day Unaffected VWAP

[1] $1.94 8.4% 13.5% 18.7% 23.9% 29.0% 34.2% 39.3% 44.5% 49.7% 54.8% 12/12/25 Closing Stock Price $2.13 (1.4%) 3.3% 8.0% 12.7% 17.4% 22.1% 26.8% 31.5% 36.2% 40.8% 10-Day

VWAP $2.14 (2.0%) 2.7% 7.3% 12.0% 16.7% 21.3% 26.0% 30.7% 35.4% 40.0% 20-Day VWAP $2.13 (1.5%) 3.1% 7.8% 12.5% 17.2% 21.9% 26.6% 31.3% 36.0% 40.7% 30-Day

VWAP $2.15 (2.3%) 2.3% 7.0% 11.6% 16.3% 20.9% 25.6% 30.2% 34.9% 39.5% VWAP Since Announcement (8/25/25) [2] $2.43 (13.5%) (9.4%) (5.3%) (1.2%) 3.0% 7.1% 11.2% 15.3% 19.4% 23.6% 12-Month

VWAP $2.39 (12.1%) (7.9%) (3.7%) 0.5% 4.7% 8.9% 13.1% 17.3% 21.4% 25.6% 52-Week Intraday High (2/18/25) $4.03 (47.9%) (45.4%) (42.9%) (40.4%) (38.0%) (35.5%) (33.0%) (30.5%) (28.0%) (25.6%) 52-Week Intraday Low

(8/22/25) $1.64 28.0% 34.1% 40.2% 46.3% 52.4% 58.5% 64.6% 70.7% 76.8% 82.9% Implied Multiples: Implied EV / LTM Total Revenue [3] $28.6 1.42x 1.54x 1.65x 1.77x 1.88x 2.00x 2.11x 2.23x 2.35x 2.46x Implied EV / CY 2025E

Total Revenue [4] $29.8 1.36x 1.47x 1.59x 1.70x 1.81x 1.92x 2.03x 2.14x 2.25x 2.37x Implied EV / CY 2026E Total Revenue [4] $33.7 1.21x 1.31x 1.40x 1.50x 1.60x 1.70x 1.80x 1.90x 1.99x 2.09x CONFIDENTIAL – PRELIMINARY –

SUBJECT TO FURTHER REVIEW 33 Illustrative Per Share Price Illustrative Implied Premiums & Multiples Information (dollars and shares in millions, except per share values) Note: The calculations and sensitivities shown are provided for

illustrative purposes only and are not intended to be indicative of or provide any conclusions regarding valuation. Note: Calculations herein do not give consideration to potential future earnout consideration receivable. Refer to page 14

for additional information. Note: VWAP information based on cumulative trading activity over designated period, per Bloomberg. Reflects the volume-weighted average price for the thirty trading days ending on the Unaffected Date. Reflects

the volume-weighted average price since the Unaffected Date. Enterprise value information per Company management and public filings. Reflects pro forma revenue for the acquisition of Kiwi, per Company management. Enterprise value

information per Company management and public filings. Revenue estimates based on Feather Financial Projections. On 8/25/25, the Company announced that it received a non-binding proposal from Canary to acquire all unowned shares of Company

common stock for $2.10 per share. CY refers to Calendar Year; E refers to Estimated; EV refers to Enterprise Value; VWAP refers to Volume Weighted Average Price. LTM refers to the most recently completed 12-month period for which information

has been made public. Sources: Bloomberg, Capital IQ, public filings, Company management, Canary Proposal and Feather Financial Projections. Canary Proposal5

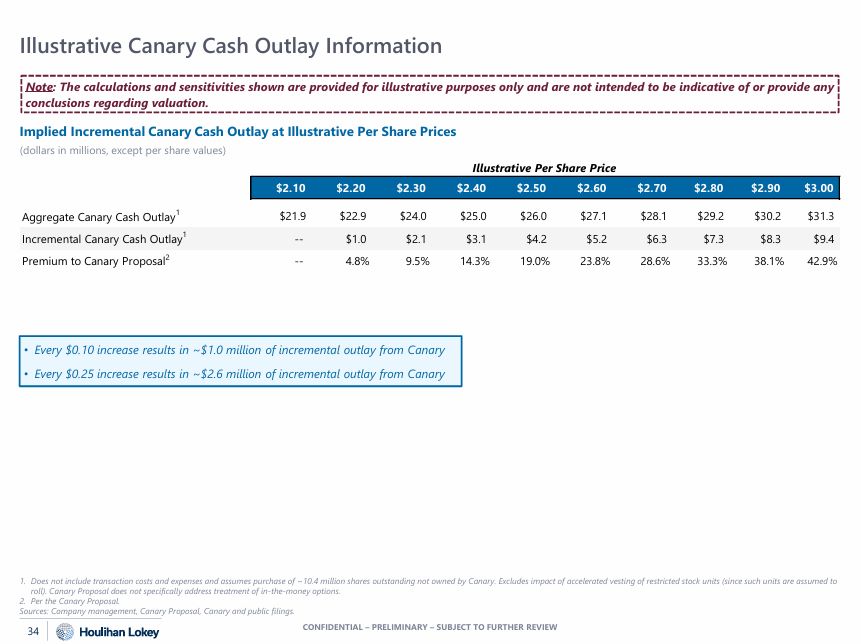

Illustrative Canary Cash Outlay Information CONFIDENTIAL – PRELIMINARY – SUBJECT TO FURTHER

REVIEW 34 Does not include transaction costs and expenses and assumes purchase of ~10.4 million shares outstanding not owned by Canary. Excludes impact of accelerated vesting of restricted stock units (since such units are assumed to roll).

Canary Proposal does not specifically address treatment of in-the-money options. Per the Canary Proposal. Sources: Company management, Canary Proposal, Canary and public filings. Implied Incremental Canary Cash Outlay at Illustrative Per

Share Prices (dollars in millions, except per share values) Illustrative Per Share Price Every $0.10 increase results in ~$1.0 million of incremental outlay from Canary Every $0.25 increase results in ~$2.6 million of incremental outlay

from Canary Note: The calculations and sensitivities shown are provided for illustrative purposes only and are not intended to be indicative of or provide any conclusions regarding

valuation. $2.10 $2.20 $2.30 $2.40 $2.50 $2.60 $2.70 $2.80 $2.90 $3.00 Aggregate Canary Cash Outlay1 $21.9 $22.9 $24.0 $25.0 $26.0 $27.1 $28.1 $29.2 $30.2 $31.3 Incremental Canary Cash

Outlay1 -- $1.0 $2.1 $3.1 $4.2 $5.2 $6.3 $7.3 $8.3 $9.4 Premium to Canary Proposal2 -- 4.8% 9.5% 14.3% 19.0% 23.8% 28.6% 33.3% 38.1% 42.9%

06 CONFIDENTIAL – PRELIMINARY – SUBJECT TO FURTHER REVIEW 05 APPENDICES

06 05 APPENDICES Selected Historical & Projected Financial Data CONFIDENTIAL – PRELIMINARY – SUBJECT

TO FURTHER REVIEW

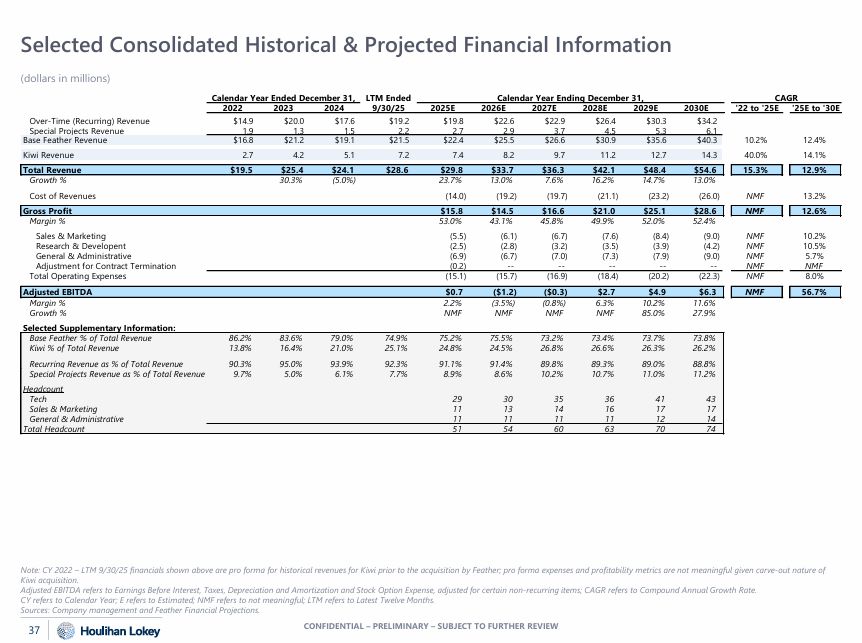

(dollars in millions) Calendar Year Ended December 31, LTM Ended Calendar Year Ending December 31, CAGR

2022 2023 2024 9/30/25 2025E 2026E 2027E 2028E 2029E 2030E '22 to '25E '25E to '30E CONFIDENTIAL – PRELIMINARY – SUBJECT TO FURTHER REVIEW 37 Note: CY 2022 – LTM 9/30/25 financials shown above are pro forma for historical revenues for Kiwi

prior to the acquisition by Feather; pro forma expenses and profitability metrics are not meaningful given carve-out nature of Kiwi acquisition. Adjusted EBITDA refers to Earnings Before Interest, Taxes, Depreciation and Amortization and

Stock Option Expense, adjusted for certain non-recurring items; CAGR refers to Compound Annual Growth Rate. CY refers to Calendar Year; E refers to Estimated; NMF refers to not meaningful; LTM refers to Latest Twelve Months. Sources: Company

management and Feather Financial Projections. Selected Consolidated Historical & Projected Financial Information Over-Time (Recurring) Revenue $14.9 $20.0 $17.6 $19.2 $19.8 $22.6 $22.9 $26.4 $30.3 $34.2 Special Projects

Revenue 1.9 1.3 1.5 2.2 2.7 2.9 3.7 4.5 5.3 6.1 Base Feather Revenue $16.8 $21.2 $19.1 $21.5 $22.4 $25.5 $26.6 $30.9 $35.6 $40.3 10.2% 12.4% Kiwi

Revenue 2.7 4.2 5.1 7.2 7.4 8.2 9.7 11.2 12.7 14.3 40.0% 14.1% Total Revenue $19.5 $25.4 $24.1 $28.6 $29.8 $33.7 $36.3 $42.1 $48.4 $54.6 15.3% 12.9% Growth

% 30.3% (5.0%) 23.7% 13.0% 7.6% 16.2% 14.7% 13.0% Cost of Revenues (14.0) (19.2) (19.7) (21.1) (23.2) (26.0) NMF 13.2% Gross Profit $15.8 $14.5 $16.6 $21.0 $25.1 $28.6 NMF 12.6% Margin

% 53.0% 43.1% 45.8% 49.9% 52.0% 52.4% Sales & Marketing (5.5) (6.1) (6.7) (7.6) (8.4) (9.0) NMF 10.2% Research & Developent (2.5) (2.8) (3.2) (3.5) (3.9) (4.2) NMF 10.5% General &

Administrative (6.9) (6.7) (7.0) (7.3) (7.9) (9.0) NMF 5.7% Adjustment for Contract Termination (0.2) -- -- -- -- -- NMF NMF Total Operating Expenses (15.1) (15.7) (16.9) (18.4) (20.2) (22.3) NMF 8.0% Adjusted

EBITDA $0.7 ($1.2) ($0.3) $2.7 $4.9 $6.3 NMF 56.7% Margin % 2.2% (3.5%) (0.8%) 6.3% 10.2% 11.6% Growth % NMF NMF NMF NMF 85.0% 27.9% Selected Supplementary Information: Base Feather % of Total

Revenue 86.2% 83.6% 79.0% 74.9% 75.2% 75.5% 73.2% 73.4% 73.7% 73.8% Kiwi % of Total Revenue 13.8% 16.4% 21.0% 25.1% 24.8% 24.5% 26.8% 26.6% 26.3% 26.2% Recurring Revenue as % of Total

Revenue 90.3% 95.0% 93.9% 92.3% 91.1% 91.4% 89.8% 89.3% 89.0% 88.8% Special Projects Revenue as % of Total Revenue 9.7% 5.0% 6.1% 7.7% 8.9% 8.6% 10.2% 10.7% 11.0% 11.2% Headcount Tech 29 30 35 36 41 43 Sales

& Marketing 11 13 14 16 17 17 General & Administrative 11 11 11 11 12 14 Total Headcount 51 54 60 63 70 74

06 05 APPENDICES Illustrative Premiums Paid Observations CONFIDENTIAL – PRELIMINARY – SUBJECT TO FURTHER

REVIEW

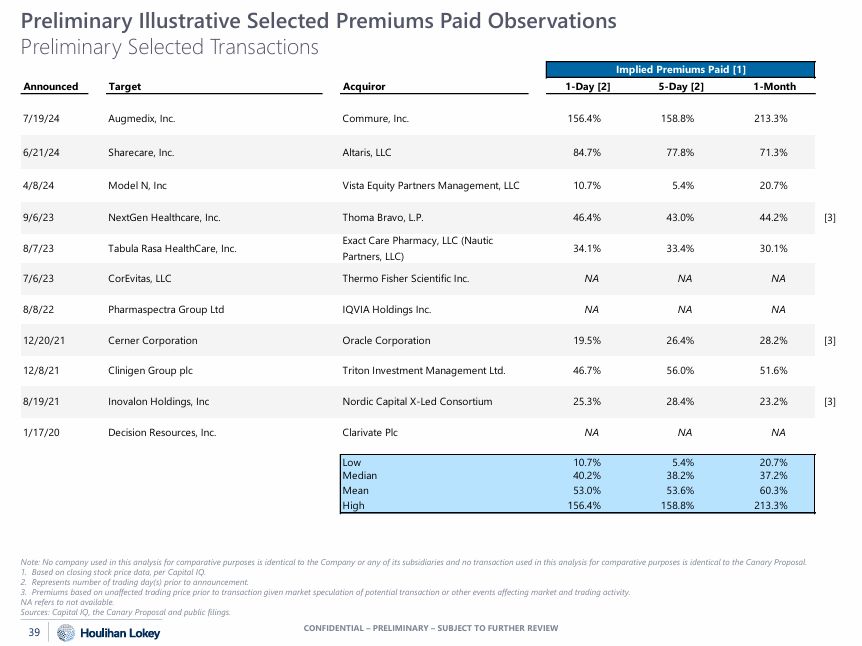

Preliminary Illustrative Selected Premiums Paid Observations Preliminary Selected Transactions Note: No

company used in this analysis for comparative purposes is identical to the Company or any of its subsidiaries and no transaction used in this analysis for comparative purposes is identical to the Canary Proposal. Based on closing stock price

data, per Capital IQ. Represents number of trading day(s) prior to announcement. Premiums based on unaffected trading price prior to transaction given market speculation of potential transaction or other events affecting market and trading

activity. NA refers to not available. Sources: Capital IQ, the Canary Proposal and public filings. Implied Premiums Paid [1] Announced Target Acquiror 1-Day [2] 5-Day [2] 1-Month 7/19/24 Augmedix, Inc. Commure,

Inc. 156.4% 158.8% 213.3% 6/21/24 Sharecare, Inc. Altaris, LLC 84.7% 77.8% 71.3% 4/8/24 Model N, Inc Vista Equity Partners Management, LLC 10.7% 5.4% 20.7% 9/6/23 NextGen Healthcare, Inc. Thoma Bravo,

L.P. 46.4% 43.0% 44.2% [3] 8/7/23 Tabula Rasa HealthCare, Inc. Exact Care Pharmacy, LLC (Nautic 34.1% 33.4% 30.1% Partners, LLC) 7/6/23 CorEvitas, LLC Thermo Fisher Scientific Inc. NA NA NA 8/8/22 Pharmaspectra Group

Ltd IQVIA Holdings Inc. NA NA NA 12/20/21 Cerner Corporation Oracle Corporation 19.5% 26.4% 28.2% [3] 12/8/21 Clinigen Group plc Triton Investment Management Ltd. 46.7% 56.0% 51.6% 8/19/21 Inovalon Holdings, Inc Nordic

Capital X-Led Consortium 25.3% 28.4% 23.2% [3] 1/17/20 Decision Resources, Inc. Clarivate Plc NA NA NA Low 10.7% 5.4% 20.7% Median 40.2% 38.2% 37.2% Mean 53.0% 53.6% 60.3% High 156.4% 158.8% 213.3% CONFIDENTIAL –

PRELIMINARY – SUBJECT TO FURTHER REVIEW 39

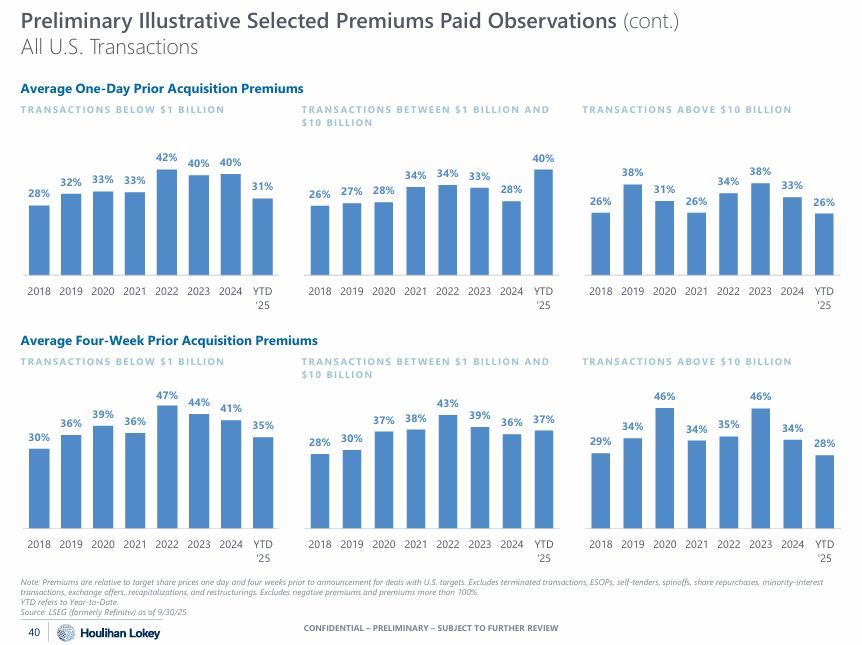

29% 34% 46% 34% 35% 46% 34% 28% 2018 2019 2020 2021 2022 2023 2024 YTD '25 Preliminary

Illustrative Selected Premiums Paid Observations (cont.) All U.S. Transactions Average One-Day Prior Acquisition Premiums Average Four-Week Prior Acquisition Premiums T R A N S A C T IO N S B E LO W $ 1 B ILLIO N T R A NS A C T I O NS BE

T W E E N $ 1 BI L L I O N A ND T R A N S A C T IO N S A B O V E $ 1 0 B ILLIO N $ 1 0 B ILLIO N T R A N S A C T IO N S B E LO W $ 1 B ILLIO N T R A NS A C T I O NS BE T W E E N $ 1 BI L L I O N A ND $ 1 0 B ILLIO N T R A N S A C T IO N

S A B O V E $ 1 0 B ILLIO N 26% 38% 31% 26% 34% 38% 33% 26% 2018 2019 2020 2021 2022 2023 2024 YTD '25 26% 27% 28% 34% 34% 33% 28% 40% 2018 2019 2020 2021 2022 2023 2024

YTD '25 28% 30% 37% 38% 43% 39% 36% 37% 2018 2019 2020 2021 2022 2023 2024 YTD '25 28% 32% 33% 33% 42% 40% 40% 31% 2018 2019 2020 2021 2022 2023 2024 YTD '25 30% CONFIDENTIAL – PRELIMINARY – SUBJECT TO FURTHER

REVIEW 40 36% 39% 36% 47% 44% 41% 35% 2018 2019 2020 2021 2022 2023 2024 YTD '25 Note: Premiums are relative to target share prices one day and four weeks prior to announcement for deals with U.S. targets. Excludes terminated

transactions, ESOPs, self-tenders, spinoffs, share repurchases, minority-interest transactions, exchange offers, recapitalizations, and restructurings. Excludes negative premiums and premiums more than 100%. YTD refers to

Year-to-Date. Source: LSEG (formerly Refinitiv) as of 9/30/25.

06 05 APPENDICES Financial Projections Comparisons CONFIDENTIAL – PRELIMINARY – SUBJECT TO FURTHER

REVIEW

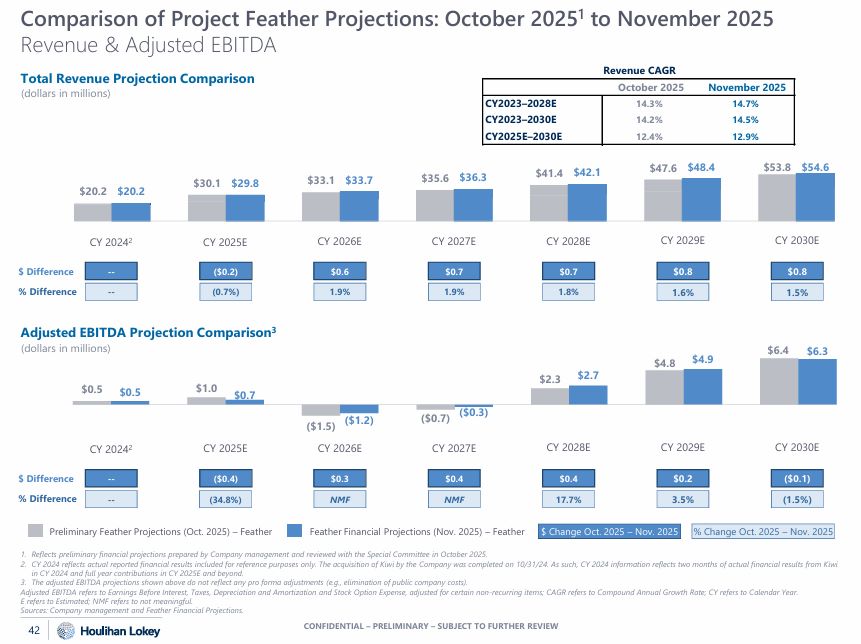

$33.1 $35.6 $41.4 $47.6 $53.8 $20.2 $20.2 $30.1 $29.8 $33.7 $36.3 $42.1 $48.4 $54.6 Comparison

of Project Feather Projections: October 20251 to November 2025 Revenue & Adjusted EBITDA Total Revenue Projection Comparison (dollars in millions) Reflects preliminary financial projections prepared by Company management and reviewed

with the Special Committee in October 2025. CY 2024 reflects actual reported financial results included for reference purposes only. The acquisition of Kiwi by the Company was completed on 10/31/24. As such, CY 2024 information reflects two

months of actual financial results from Kiwi in CY 2024 and full year contributions in CY 2025E and beyond. The adjusted EBITDA projections shown above do not reflect any pro forma adjustments (e.g., elimination of public company

costs). Adjusted EBITDA refers to Earnings Before Interest, Taxes, Depreciation and Amortization and Stock Option Expense, adjusted for certain non-recurring items; CAGR refers to Compound Annual Growth Rate; CY refers to Calendar Year. E

refers to Estimated; NMF refers to not meaningful. Sources: Company management and Feather Financial Projections. CY 20242 CY 2025E CY 2026E CY 2027E CY 2028E CY 2029E CY 2030E $

Difference -- ($0.2) $0.6 $0.7 $0.7 $0.8 $0.8 % Difference -- (0.7%) 1.9% 1.9% 1.8% 1.6% 1.5% Preliminary Feather Projections (Oct. 2025) – Feather Feather Financial Projections (Nov. 2025) – Feather % Change Oct. 2025 – Nov.

2025 $ Change Oct. 2025 – Nov. 2025 Adjusted EBITDA Projection Comparison3 (dollars in millions) $0.5 CONFIDENTIAL – PRELIMINARY – SUBJECT TO FURTHER REVIEW 42 $1.0 ($1.5) ($0.7) $2.3 $4.8 $6.4 $0.5 $0.7

($1.2) ($0.3) $2.7 $4.9 $6.3 CY 20242 CY 2025E CY 2026E CY 2027E CY 2028E CY 2029E CY 2030E $ Difference -- ($0.4) $0.3 $0.4 $0.4 $0.2 ($0.1) % Difference -- (34.8%) NMF NMF 17.7% 3.5% (1.5%) Revenue

CAGR October 2025 November 2025 CY2023–2028E 14.3% 14.7% CY2023–2030E 14.2% 14.5% CY2025E–2030E 12.4% 12.9%

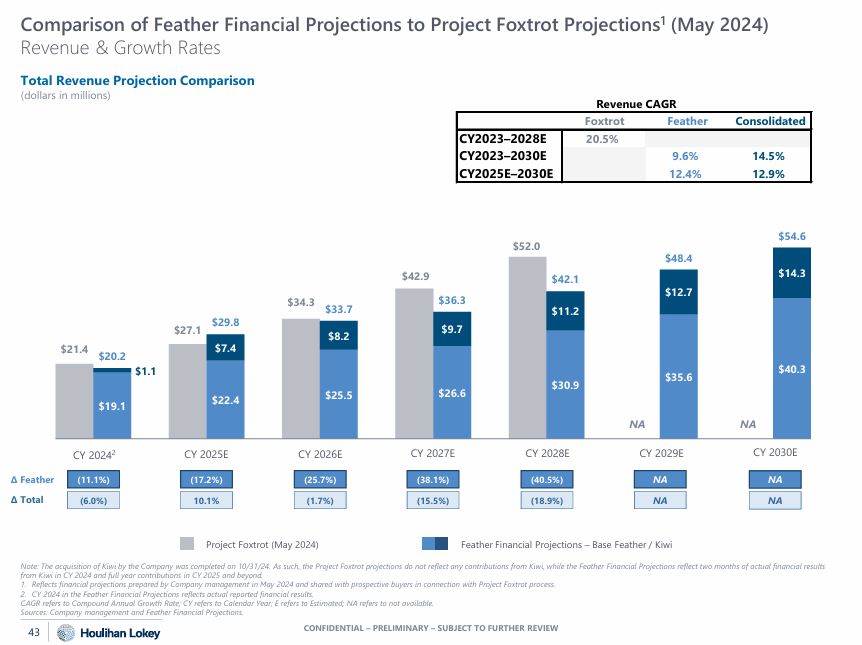

$21.4 $27.1 $34.3 $42.9 $52.0 NA NA $19.1 $22.4 $25.5 $26.6 $30.9 $35.6 $40.3 $1.1 $7.4 $8.2 $9.7 $11.2 $12.7 $14.3 $20.2 $29.8 $33.7 $36.3 $42.1 $48.4 $54.6 Project

Foxtrot (May 2024) Feather Financial Projections – Base Feather / Kiwi Note: The acquisition of Kiwi by the Company was completed on 10/31/24. As such, the Project Foxtrot projections do not reflect any contributions from Kiwi, while the

Feather Financial Projections reflect two months of actual financial results from Kiwi in CY 2024 and full year contributions in CY 2025 and beyond. Reflects financial projections prepared by Company management in May 2024 and shared with

prospective buyers in connection with Project Foxtrot process. CY 2024 in the Feather Financial Projections reflects actual reported financial results. CAGR refers to Compound Annual Growth Rate; CY refers to Calendar Year; E refers to

Estimated; NA refers to not available. Sources: Company management and Feather Financial Projections. CONFIDENTIAL – PRELIMINARY – SUBJECT TO FURTHER REVIEW 43 CY 20242 CY 2025E CY 2026E CY 2027E CY 2028E CY 2029E CY 2030E ∆

Feather (11.1%) (17.2%) (25.7%) (38.1%) (40.5%) NA NA ∆ Total (6.0%) 10.1% (1.7%) (15.5%) (18.9%) NA NA Total Revenue Projection Comparison (dollars in

millions) Foxtrot Feather Consolidated CY2023–2028E 20.5% CY2023–2030E 9.6% 14.5% CY2025E–2030E 12.4% 12.9% Revenue CAGR Comparison of Feather Financial Projections to Project Foxtrot Projections1 (May 2024) Revenue & Growth

Rates

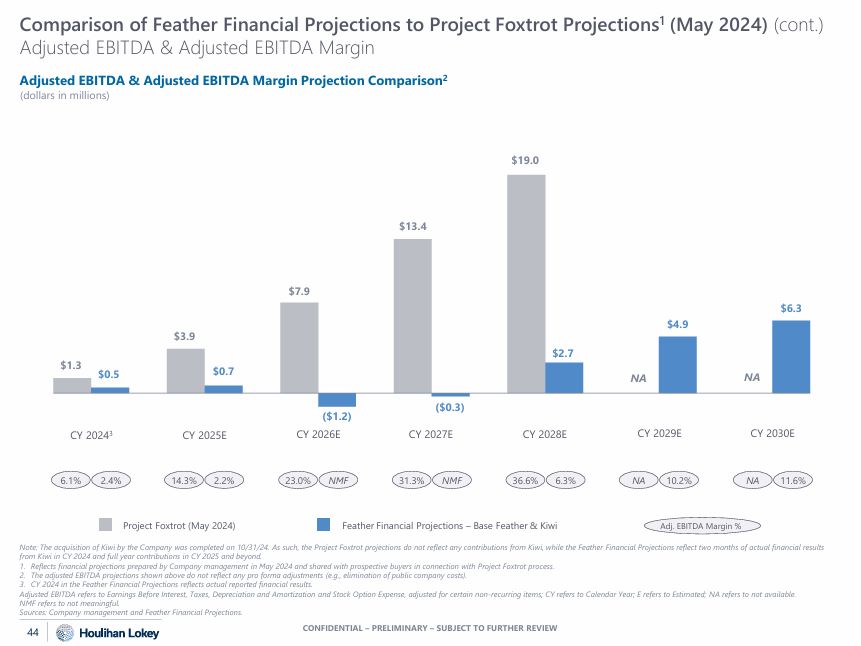

$1.3 $3.9 $7.9 $13.4 $19.0 NA NA $0.5 $0.7 ($0.3) $2.7 $4.9 $6.3 ($1.2) CY 2026E Note: The

acquisition of Kiwi by the Company was completed on 10/31/24. As such, the Project Foxtrot projections do not reflect any contributions from Kiwi, while the Feather Financial Projections reflect two months of actual financial results from

Kiwi in CY 2024 and full year contributions in CY 2025 and beyond. Reflects financial projections prepared by Company management in May 2024 and shared with prospective buyers in connection with Project Foxtrot process. The adjusted EBITDA

projections shown above do not reflect any pro forma adjustments (e.g., elimination of public company costs). CY 2024 in the Feather Financial Projections reflects actual reported financial results. Adjusted EBITDA refers to Earnings Before

Interest, Taxes, Depreciation and Amortization and Stock Option Expense, adjusted for certain non-recurring items; CY refers to Calendar Year; E refers to Estimated; NA refers to not available. NMF refers to not meaningful. Sources: Company

management and Feather Financial Projections. Adjusted EBITDA & Adjusted EBITDA Margin Projection Comparison2 (dollars in millions) Project Foxtrot (May 2024) Feather Financial Projections – Base Feather & Kiwi Adj. EBITDA Margin

% 2.4% 6.1% 23.0% NMF 31.3% NMF 6.3% 36.6% 2.2% 14.3% NA 10.2% NA 11.6% CONFIDENTIAL – PRELIMINARY – SUBJECT TO FURTHER REVIEW 44 CY 20243 CY 2025E CY 2027E CY 2028E CY 2029E CY 2030E Comparison of Feather Financial

Projections to Project Foxtrot Projections1 (May 2024) (cont.) Adjusted EBITDA & Adjusted EBITDA Margin

06 CONFIDENTIAL – PRELIMINARY – SUBJECT TO FURTHER REVIEW 06 DISCLAIMER

This presentation, and any supplemental information (written or oral) or other documents provided in

connection therewith (collectively, the “materials”), are provided solely for the information of the Special Committee (the “Committee” or the “Special Committee”) of the Board of Directors (the “Board”) of Feather (the “Company”) by Houlihan

Lokey in connection with the Committee’s consideration of a potential transaction (the “Transaction”) involving the Company. This presentation is incomplete without reference to, and should be considered in conjunction with, any supplemental

information provided by and discussions with Houlihan Lokey in connection therewith. Any defined terms used herein shall have the meanings set forth herein, even if such defined terms have been given different meanings elsewhere in the

materials. Houlihan Lokey makes no representation to any party that the information and analysis contained in the materials supports any particular determination regarding the Transaction. The materials are for discussion purposes only.

Houlihan Lokey expressly disclaims any and all liability, whether direct or indirect, in contract or tort or otherwise, to any person in connection with the materials. The materials were prepared for specific persons familiar with the

business and affairs of the Company for use in a specific context and were not prepared with a view to public disclosure or to conform with any disclosure standards under any state, federal or international securities laws or other laws,

rules or regulations, and none of the Committee, the Company or Houlihan Lokey takes any responsibility for the use of the materials by persons other than the Committee. The materials are provided on a confidential basis solely for the

information of the Committee and may not be disclosed, summarized, reproduced, disseminated or quoted or otherwise referred to, in whole or in part, without Houlihan Lokey’s express prior written consent. Notwithstanding any other provision

herein, the Company (and each employee, representative or other agent of the Company) may disclose to any and all persons without limitation of any kind, the tax treatment and tax structure of any transaction and all materials of any kind

(including opinions or other tax analyses, if any) that are provided to the Company relating to such tax treatment and structure. However, any information relating to the tax treatment and tax structure shall remain confidential (and the

foregoing sentence shall not apply) to the extent necessary to enable any person to comply with securities laws. For this purpose, the tax treatment of a transaction is the purported or claimed U.S. income or franchise tax treatment of the

transaction and the tax structure of a transaction is any fact that may be relevant to understanding the purported or claimed U.S. income or franchise tax treatment of the transaction. If the Company plans to disclose information pursuant to

the first sentence of this paragraph, the Company shall inform those to whom it discloses any such information that they may not rely upon such information for any purpose without Houlihan Lokey’s prior written consent. Houlihan Lokey is not

an expert on, and nothing contained in the materials should be construed as advice with regard to, legal, accounting, regulatory, insurance, tax or other specialist matters. Houlihan Lokey’s role in reviewing any information was limited

solely to performing such a review as it deemed necessary to support its own advice and analysis and was not on behalf of the Committee. The materials necessarily are based on financial, economic, market and other conditions as in effect on,

and the information available to Houlihan Lokey as of, the date of the materials. Although subsequent developments may affect the contents of the materials, Houlihan Lokey has not undertaken, and is under no obligation, to update, revise or

reaffirm the materials. The materials are not intended to provide the sole basis for evaluation of the Transaction and do not purport to contain all information that may be required. The materials do not address the underlying business