| Disrupting a $3.5B neurotoxin market dominated by a single brand for >30 years CORPORATE PRESENTATION / MAY 2026 NYSEAMERICAN: AEON © 2 0 2 6 A E O N B I O P H A R M A |

| This presentation includes forward-looking statements. All statements other than statements of historical facts contained in this presentation, including statements concerning possible or assumed future actions, business strategies, events or results of operations, illustrative timelines and targets for financing and any statements that refer to projections, forecasts or other characterizations of future events or circumstances, including any underlying assumptions, are forward-looking statements. These statements may involve known and unknown risks, uncertainties and other important factors that may cause the actual results, performance or achievements of AEON Biopharma, Inc. (“AEON”) to be materially different from any future results, performance or achievements expressed or implied by the forward-looking statements. These statements may be preceded by, followed by or include the words “believes”, “estimates”, “expects”, “projects”, “forecasts”, “may”, “will”, “should”, “seeks”, “plans”, “scheduled”, “anticipates” or “intends” or similar expressions. The forward-looking statements in this presentation are only predictions. AEON has based these forward-looking statements largely on AEON’s current expectations and projections about future events and financial trends that AEON believes may affect its business, financial condition and results of operations. These forward-looking statements are based upon estimates and assumptions that, while considered reasonable by AEON and its management, are inherently uncertain. Factors that may cause actual results to differ materially from current expectations include, but are not limited to: (i) the outcome of any meetings with any regulatory authorities, including the FDA’s review of AEON’s biosimilar meetings and document submissions; (ii) the outcome of any legal proceedings that may be instituted against AEON or others; (iii) AEON’s future capital requirements; (iv) AEON’s ability to raise financing in the future; (v) AEON’s ability to continue to meet continued stock exchange listing standards; (vi) the ability of AEON to implement its strategic initiatives, including the continued development of ABP-450 and potential submission of a Biologics License Application as a BOTOX® biosimilar for therapeutic uses of ABP-450; (vii) the ability of AEON to satisfy regulatory requirements; (viii) the ability of AEON to defend its intellectual property or avoid infringement of existing intellectual property; (ix) the possibility that AEON may be adversely affected by other economic, business, regulatory, and/or competitive factors; (x) the FDA’s response to AEON’s proposed clinical program; and (xi) other risks and uncertainties set forth in the section entitled “Risk Factors” and “Cautionary Note Regarding Forward-Looking Statements” in AEON’s Annual Report on Form 10-K for the year ended December 31, 2025 and any current or periodic reports filed with the Securities and Exchange Commission (the "SEC"), which are available on the SEC’s website at www.sec.gov. Because forward-looking statements are inherently subject to risks and uncertainties, some of which cannot be predicted or quantified and some of which are beyond AEON’s control, you should not rely on these forward-looking statements as predictions of future events. The events and circumstances reflected in AEON’s forward-looking statements may not be achieved or occur, and actual results could differ materially from those projected in the forward-looking statements. Moreover, AEON operates in an evolving environment and a competitive industry. New risks and uncertainties may emerge from time to time, and it is not possible for management to predict all risks and uncertainties, nor can AEON assess the impact of all factors on AEON’s business or the extent to which any factor, or combination of factors, may cause actual results to differ materially from those contained in any forward-looking statements AEON may make in this presentation. As a result of these factors, although AEON believes that the expectations reflected in its forward-looking statements are reasonable, AEON cannot assure you that the forward-looking statements in this presentation will prove to be accurate. Except as required by applicable law, AEON does not plan to publicly update or revise any forward-looking statements contained herein, whether as a result of any new information, future events, changed circumstances, or otherwise. AEON qualifies all of its forward-looking statements by these cautionary statements. You should view this presentation completely and with the understanding that the actual future results, levels of activity, performance, events and circumstances of AEON may be materially different from what is expected. This presentation concerns anticipated products that are under clinical and analytical investigation, and which have not yet been approved for marketing by the FDA. These anticipated products are currently limited by federal law to investigational use, and no representation is made as to their safety or effectiveness for the purposes for which they are being investigated. Certain information contained in this presentation relates to or is based on studies, publications, surveys and other data obtained from third-party sources and AEON’s own internal estimates and research. AEON has not independently verified, and makes no representation as to the adequacy, fairness, accuracy or completeness of, any information obtained from third-party sources. In addition, all of the market data included in this presentation involves a number of assumptions and limitations, and there can be no guarantee as to the accuracy or reliability of such assumptions. Finally, AEON’s own internal estimates and research have not been verified by any independent source. AEON Biopharma and the AEON Biopharma logo are trademarks of AEON Biopharma, Inc. All other trademarks used herein are the property of their respective owners. Forward-Looking Statements © 2 0 2 6 A E O N B I O P H A R M A 2 |

| © 2 0 2 6 A E O N B I O P H A R M A Unlocking a $3.5B Market with the First True BOTOX® Substitute 3 Developing ABP-450 as the first clinically substitutable therapeutic alternative to BOTOX® → Licensed exclusive rights to commercialize all BOTOX® therapeutic indications in the U.S., Canada, EU, UK and select international territories → Advancing full-label Extrapolation Strategy under the FDA’s 351(k) biosimilar pathway for ABP-450 covering all BOTOX® therapeutic indications BOTOX® has remained the dominant player despite branded competition and expiration of key patents → Lack of full label for branded BOTOX® competitors serves as a significant hurdle for market adoption → A true biosimilar that could be substituted for BOTOX® has remained elusive given manufacturing complexity associated with toxins ABP-450 is a validated botulinum toxin platform with established clinical data and FDA inspected manufacturing facility → Manufactured by Daewoong Pharmaceuticals in compliance with cGMP o Identical product profile as Jeuveau®, approved and marketed for cosmetic indications by Evolus, Inc. → Composition and mechanism of action (MoA) supports similarity to BOTOX® o Same 900kDa size, 100% amino acid sequence identity, genetic & formulation parity, and highly similar potency supports clinical dose predictability Led by newly appointed seasoned management team with demonstrated experience in toxins and capital formation → Rob Bancroft (CEO) served as the former BOTOX® leader responsible for competitive strategy and long-range asset maximization → John Bencich (CFO) led Achieve Life Sciences (CEO & CFO) and Oncogenex Pharmaceuticals (CFO); brings growth and capital strategy experience Recent highlights and upcoming catalyst → January FDA Type 2a feedback provides a clear framework to complete remaining analytical work → Type 2b meeting planned for 2H26 to align on comparative clinical study requirements |

| © 2 0 2 6 A E O N B I O P H A R M A Advancing the First Clinically Substitutable BOTOX® Alternative 4 Despite >30 years of growth, no clinically substitutable alternative has threatened BOTOX® - until now Full-Label Parity Captures all 12 indications at approval → Competes for the entire therapeutic market from day one → Avoids the restricted labels that have constrained prior competitors Clinical Equivalence No change to physician workflow → Same dosing, preparation, and administration as BOTOX® → Prior competitors required changes → limited adoption Switching is Rewarded Aligned economics drive adoption → Improves physician margin per treatment → Payers incentivized to reinforce switching behavior W H A T D R I V E S A D O P T I O N A T S C A L E Adoption at scale + structurally limited follow-on competition → durable share |

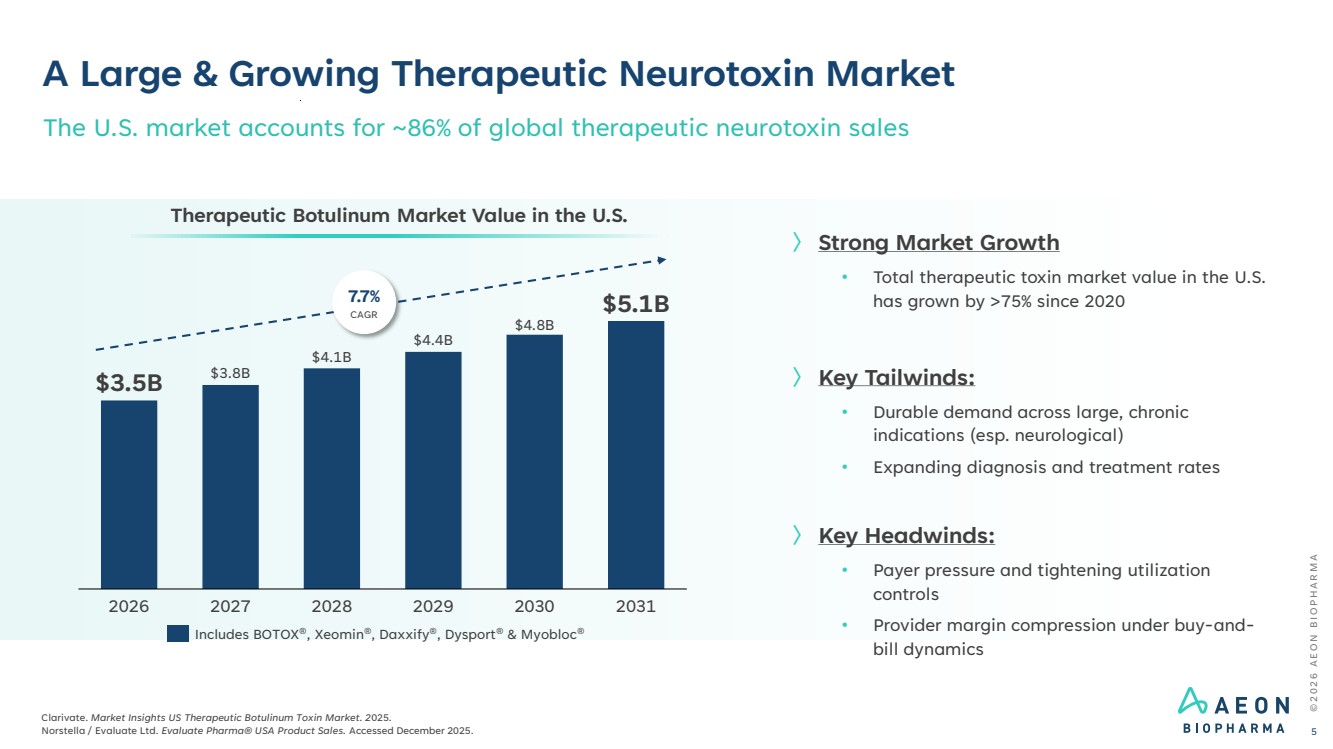

| © 2 0 2 6 A E O N B I O P H A R M A Clarivate. Market Insights US Therapeutic Botulinum Toxin Market. 2025. Norstella / Evaluate Ltd. Evaluate Pharma® USA Product Sales. Accessed December 2025. 5 The U.S. market accounts for ~86% of global therapeutic neurotoxin sales 2026 2027 2028 2029 2030 2031 $3.5B $3.8B $4.1B $4.4B $4.8B $5.1B Therapeutic Botulinum Market Value in the U.S. 7.7% CAGR Includes BOTOX®, Xeomin®, Daxxify®, Dysport® & Myobloc® 〉 Strong Market Growth • Total therapeutic toxin market value in the U.S. has grown by >75% since 2020 〉 Key Tailwinds: • Durable demand across large, chronic indications (esp. neurological) • Expanding diagnosis and treatment rates 〉 Key Headwinds: • Payer pressure and tightening utilization controls • Provider margin compression under buy-and-bill dynamics A Large & Growing Therapeutic Neurotoxin Market |

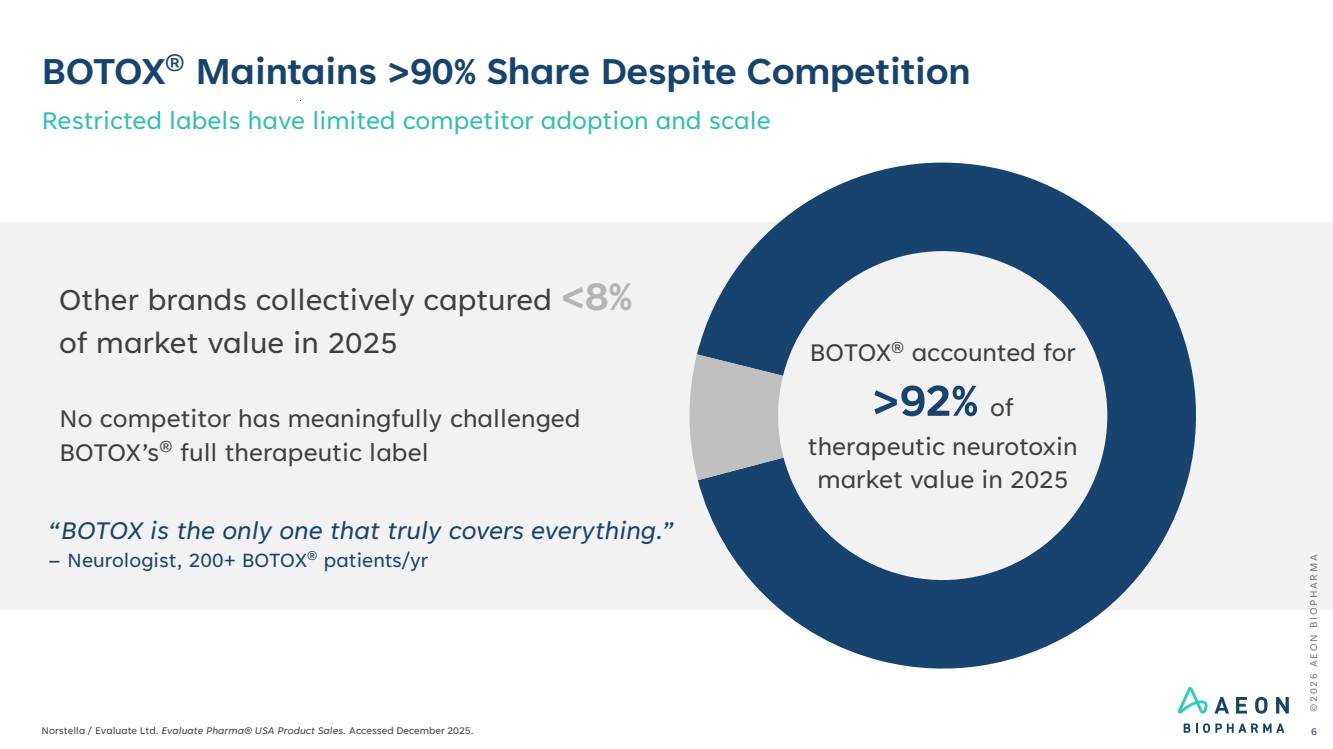

| BOTOX® Maintains >90% Share Despite Competition Restricted labels have limited competitor adoption and scale © 2 0 2 6 A E O N B I O P H A R M A Norstella / Evaluate Ltd. Evaluate Pharma® USA Product Sales. Accessed December 2025. 6 Other brands collectively captured <8% of market value in 2025 No competitor has meaningfully challenged BOTOX’s® full therapeutic label BOTOX® accounted for >92% of therapeutic neurotoxin market value in 2025 “BOTOX is the only one that truly covers everything.” – Neurologist, 200+ BOTOX® patients/yr |

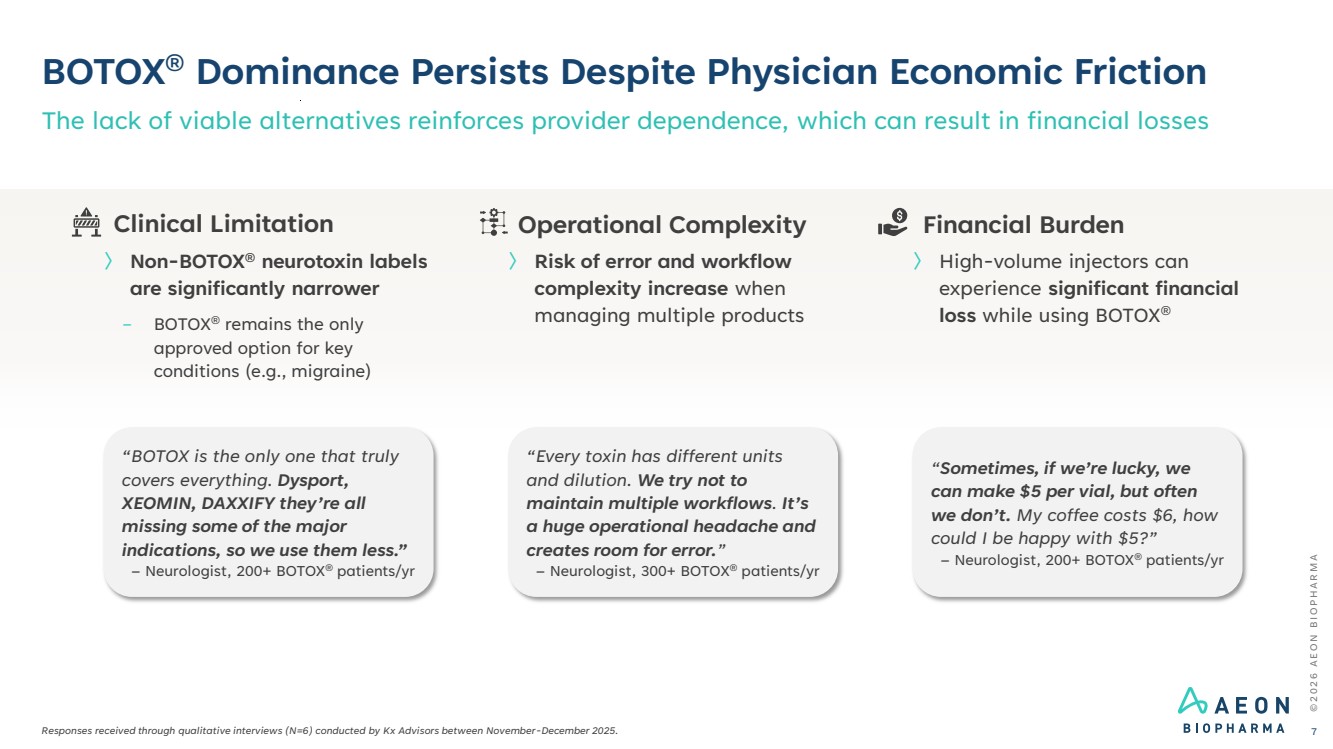

| © 2 0 2 6 A E O N B I O P H A R M A BOTOX® Dominance Persists Despite Physician Economic Friction Responses received through qualitative interviews (N=6) conducted by Kx Advisors between November-December 2025. The lack of viable alternatives reinforces provider dependence, which can result in financial losses 7 “Sometimes, if we’re lucky, we can make $5 per vial, but often we don’t. My coffee costs $6, how could I be happy with $5?” – Neurologist, 200+ BOTOX® patients/yr “Every toxin has different units and dilution. We try not to maintain multiple workflows. It’s a huge operational headache and creates room for error.” – Neurologist, 300+ BOTOX® patients/yr “BOTOX is the only one that truly covers everything. Dysport, XEOMIN, DAXXIFY they’re all missing some of the major indications, so we use them less.” – Neurologist, 200+ BOTOX® patients/yr Financial Burden 〉 High-volume injectors can experience significant financial loss while using BOTOX® Operational Complexity 〉 Risk of error and workflow complexity increase when managing multiple products Clinical Limitation 〉 Non-BOTOX® neurotoxin labels are significantly narrower − BOTOX® remains the only approved option for key conditions (e.g., migraine) |

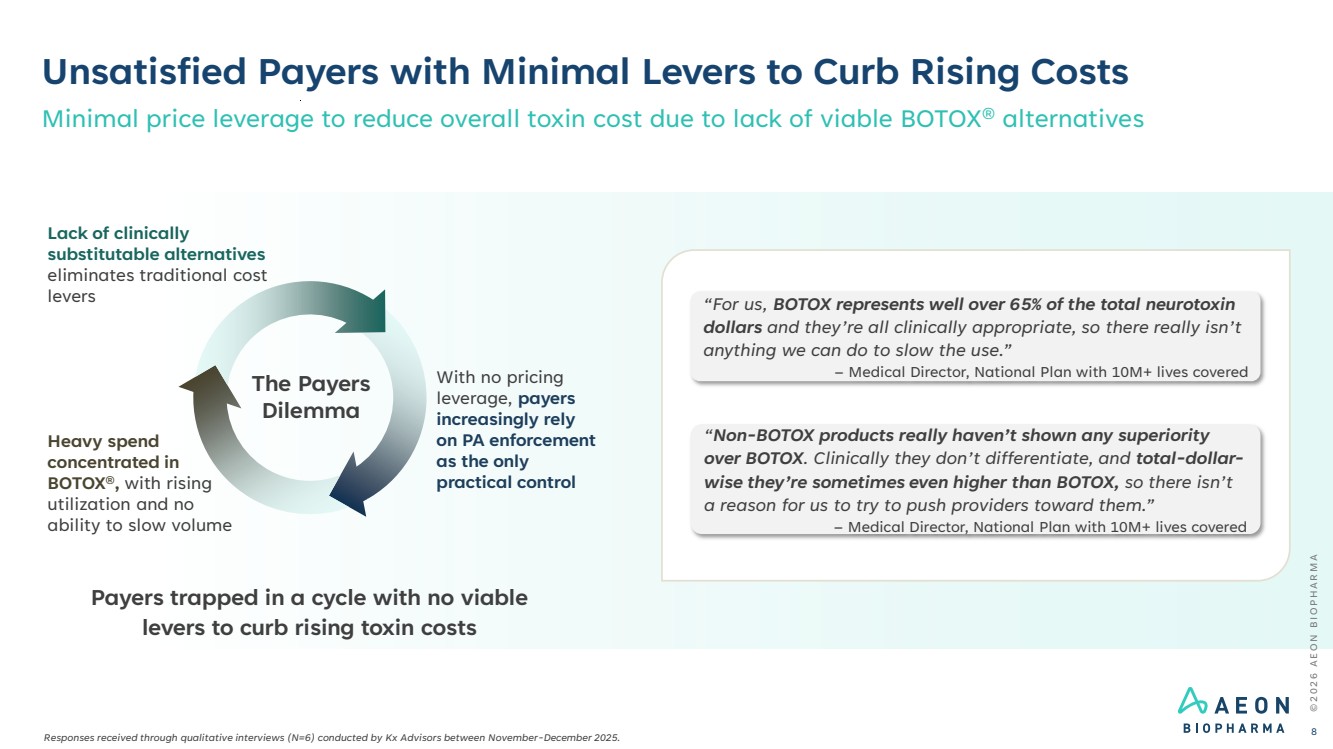

| Heavy spend concentrated in BOTOX®, with rising utilization and no ability to slow volume The Payers Dilemma Unsatisfied Payers with Minimal Levers to Curb Rising Costs © 2 0 2 6 A E O N B I O P H A R M A 8 Payers trapped in a cycle with no viable levers to curb rising toxin costs “For us, BOTOX represents well over 65% of the total neurotoxin dollars and they’re all clinically appropriate, so there really isn’t anything we can do to slow the use.” – Medical Director, National Plan with 10M+ lives covered “Non-BOTOX products really haven’t shown any superiority over BOTOX. Clinically they don’t differentiate, and total-dollar-wise they’re sometimes even higher than BOTOX, so there isn’t a reason for us to try to push providers toward them.” – Medical Director, National Plan with 10M+ lives covered Minimal price leverage to reduce overall toxin cost due to lack of viable BOTOX® alternatives Lack of clinically substitutable alternatives eliminates traditional cost levers With no pricing leverage, payers increasingly rely on PA enforcement as the only practical control Responses received through qualitative interviews (N=6) conducted by Kx Advisors between November-December 2025. |

| © 2 0 2 6 A E O N B I O P H A R M A 9 AEON is taking a different approach We are not trying to be different. We are trying to be the same. Equivalence to BOTOX® across every relevant dimension – same label, same dosing, same dilution, same outcomes, same coverage, same workflow. Differentiation forces competitors to fight three decades of cumulative BOTOX® investment, experience, and habit. Biosimilarity allows AEON to leverage it. |

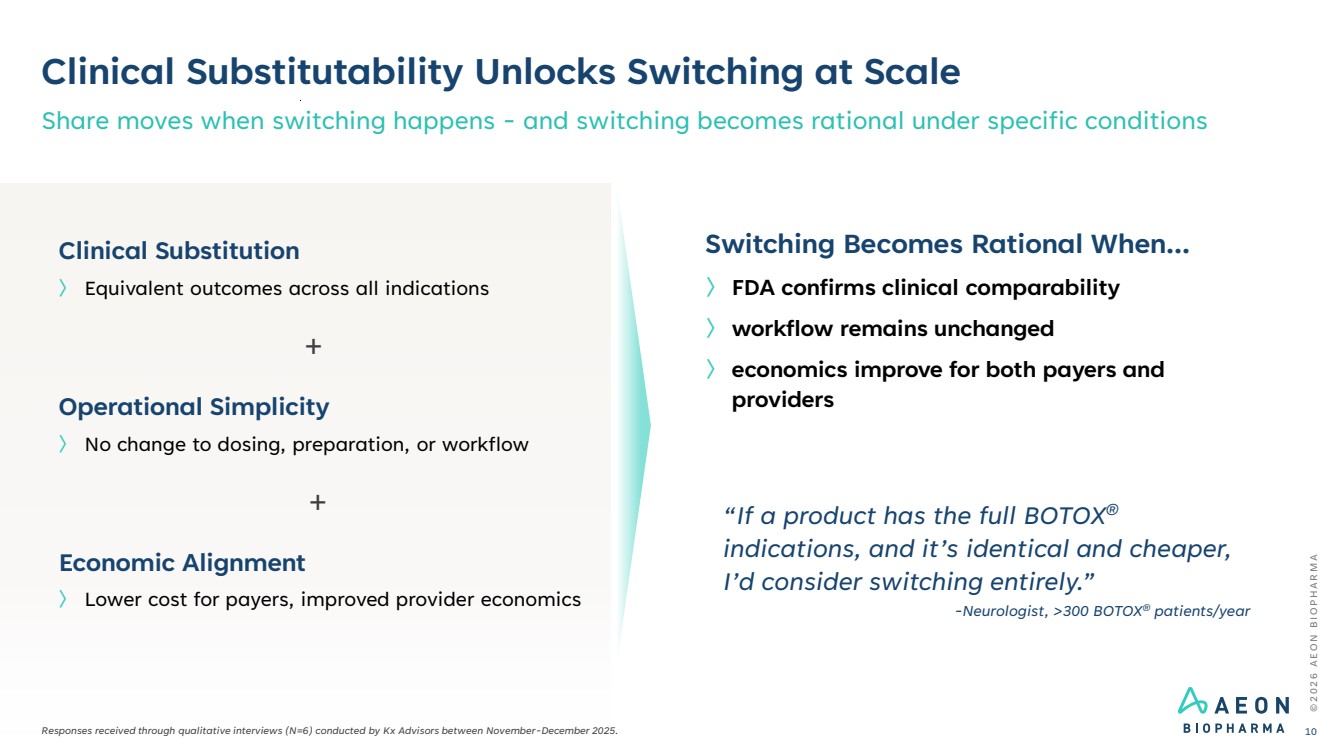

| Clinical Substitutability Unlocks Switching at Scale Share moves when switching happens - and switching becomes rational under specific conditions © 2 0 2 6 A E O N B I O P H A R M A 10 〉 Lower cost for payers, improved provider economics Economic Alignment 〉 No change to dosing, preparation, or workflow Operational Simplicity 〉 Equivalent outcomes across all indications Clinical Substitution Switching Becomes Rational When... 〉 FDA confirms clinical comparability 〉 workflow remains unchanged 〉 economics improve for both payers and providers + + “If a product has the full BOTOX® indications, and it’s identical and cheaper, I’d consider switching entirely.” -Neurologist, >300 BOTOX® patients/year Responses received through qualitative interviews (N=6) conducted by Kx Advisors between November-December 2025. |

| AbbVie Inc. 1989 Merz Pharma 2010 Ipsen Group 2009 Crown Laboratories 2023 Therapeutic Label (FDA Approved Indications) 1. Chronic migraine 2. Overactive bladder 3. Detrusor overactivity 4. Pediatric detrusor overactivity 5. Adult upper limb spasticity 6. Adult lower limb spasticity 7. Pediatric upper limb spasticity 8. Pediatric lower limb spasticity 9. Cervical dystonia 10. Axillary hyperhidrosis 11. Blepharospasm 12. Strabismus Full Label Parity (targeted) 1. Chronic migraine 2. Overactive bladder 3. Detrusor overactivity 4. Pediatric detrusor overactivity 5. Adult upper limb spasticity 6. Adult lower limb spasticity 7. Pediatric upper limb spasticity 8. Pediatric lower limb spasticity 9. Cervical dystonia 10. Axillary hyperhidrosis 11. Blepharospasm 12. Strabismus 1. Blepharospasm 2. Cervical dystonia 3. Adult upper limb spasticity 4. Chronic sialorrhea 1. Cervical dystonia 2. Upper limb spasticity (adults) 3. Lower limb spasticity (pediatric) 1. Cervical dystonia Full-Label Access Is the Gatekeeper to the Market Current competitors are restricted to a subset of indications - limiting adoption and scale Full-label access is required to compete at scale - and no competitor has it today © 2 0 2 6 A E O N B I O P H A R M A 11 *Clarivate. Market Insights US Therapeutic Botulinum Toxin Market. 2025. 91.9% share* 4.4% share* 3.1% share* <1% share* |

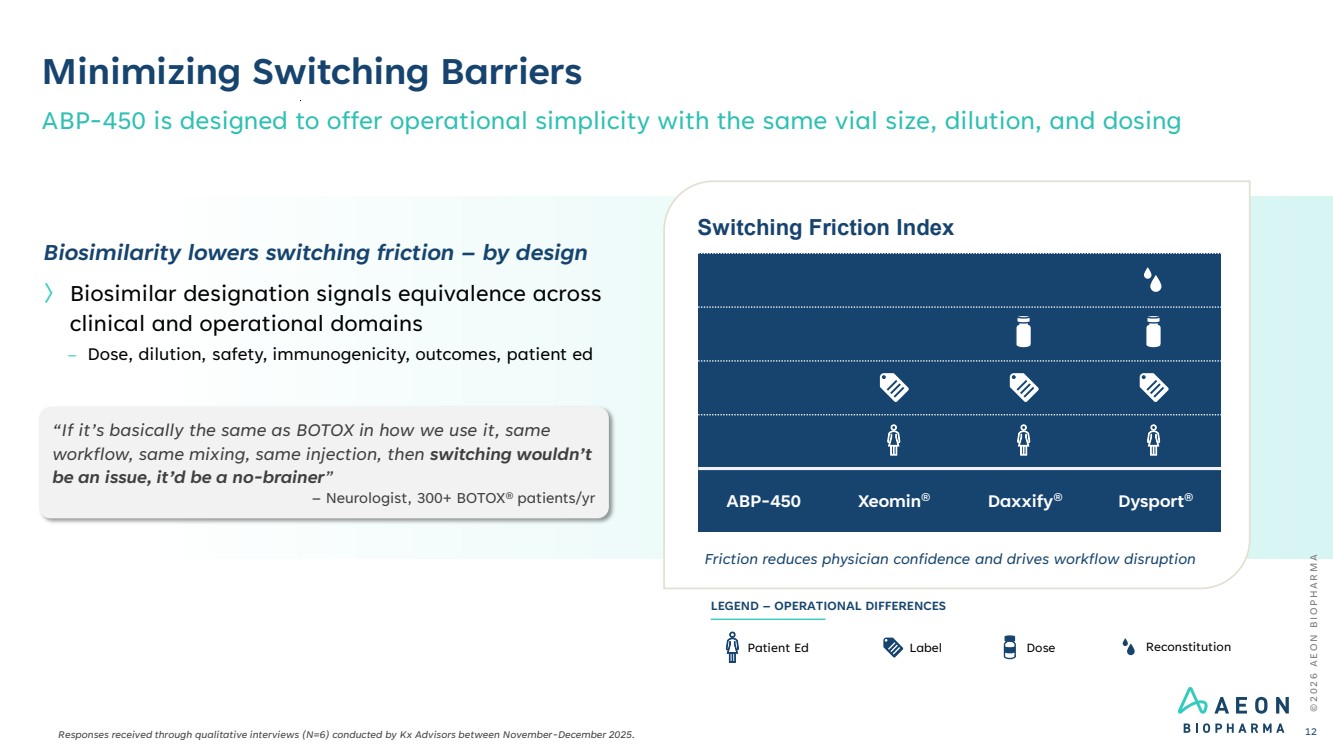

| © 2 0 2 6 A E O N B I O P H A R M A Minimizing Switching Barriers ABP-450 is designed to offer operational simplicity with the same vial size, dilution, and dosing 12 Switching Friction Index Friction reduces physician confidence and drives workflow disruption ABP-450 Xeomin® Daxxify® Dysport® Label Dose Reconstitution LEGEND – OPERATIONAL DIFFERENCES Patient Ed Biosimilarity lowers switching friction – by design 〉 Biosimilar designation signals equivalence across clinical and operational domains – Dose, dilution, safety, immunogenicity, outcomes, patient ed “If it’s basically the same as BOTOX in how we use it, same workflow, same mixing, same injection, then switching wouldn’t be an issue, it’d be a no-brainer” – Neurologist, 300+ BOTOX® patients/yr Responses received through qualitative interviews (N=6) conducted by Kx Advisors between November-December 2025. |

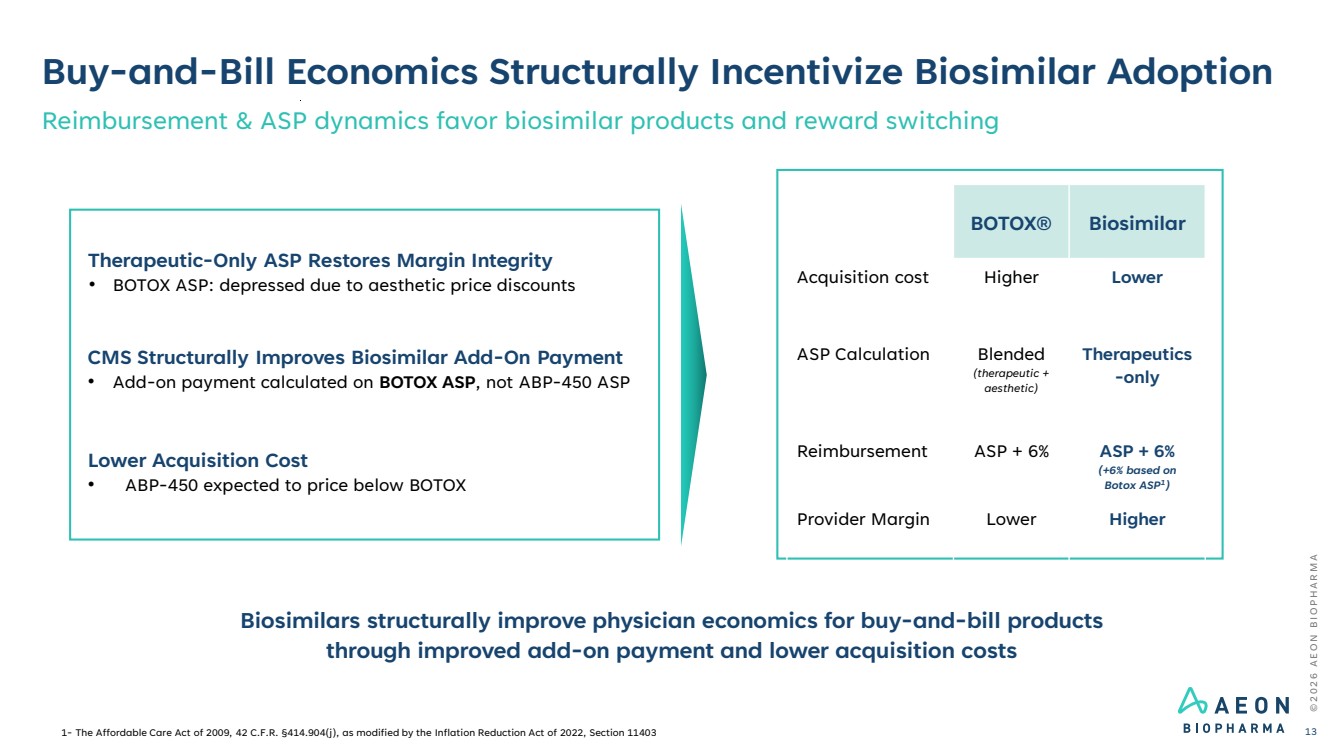

| Buy-and-Bill Economics Structurally Incentivize Biosimilar Adoption Reimbursement & ASP dynamics favor biosimilar products and reward switching © 2 0 2 6 A E O N B I O P H A R M A 13 Biosimilars structurally improve physician economics for buy-and-bill products through improved add-on payment and lower acquisition costs Therapeutic-Only ASP Restores Margin Integrity • BOTOX ASP: depressed due to aesthetic price discounts CMS Structurally Improves Biosimilar Add-On Payment • Add-on payment calculated on BOTOX ASP, not ABP-450 ASP Lower Acquisition Cost • ABP-450 expected to price below BOTOX BOTOX® Biosimilar Acquisition cost Higher Lower ASP Calculation Blended (therapeutic + aesthetic) Therapeutics -only Reimbursement ASP + 6% ASP + 6% (+6% based on Botox ASP1 ) Provider Margin Lower Higher 1- The Affordable Care Act of 2009, 42 C.F.R. §414.904(j), as modified by the Inflation Reduction Act of 2022, Section 11403 |

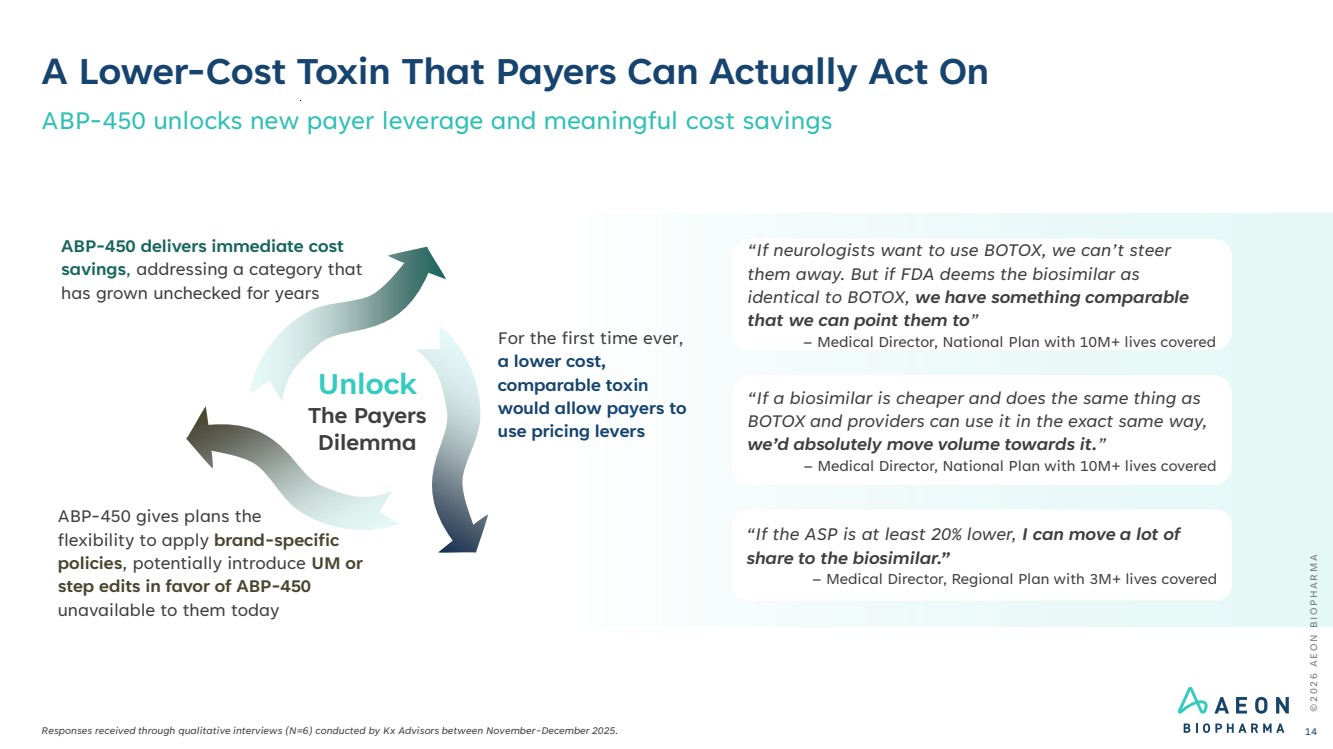

| © 2 0 2 6 A E O N B I O P H A R M A A Lower-Cost Toxin That Payers Can Actually Act On Responses received through qualitative interviews (N=6) conducted by Kx Advisors between November-December 2025. ABP-450 unlocks new payer leverage and meaningful cost savings 14 “If neurologists want to use BOTOX, we can’t steer them away. But if FDA deems the biosimilar as identical to BOTOX, we have something comparable that we can point them to” – Medical Director, National Plan with 10M+ lives covered “If a biosimilar is cheaper and does the same thing as BOTOX and providers can use it in the exact same way, we’d absolutely move volume towards it.” – Medical Director, National Plan with 10M+ lives covered “If the ASP is at least 20% lower, I can move a lot of share to the biosimilar.” – Medical Director, Regional Plan with 3M+ lives covered ABP-450 gives plans the flexibility to apply brand-specific policies, potentially introduce UM or step edits in favor of ABP-450 unavailable to them today For the first time ever, a lower cost, comparable toxin would allow payers to use pricing levers ABP-450 delivers immediate cost savings, addressing a category that has grown unchecked for years Unlock The Payers Dilemma |

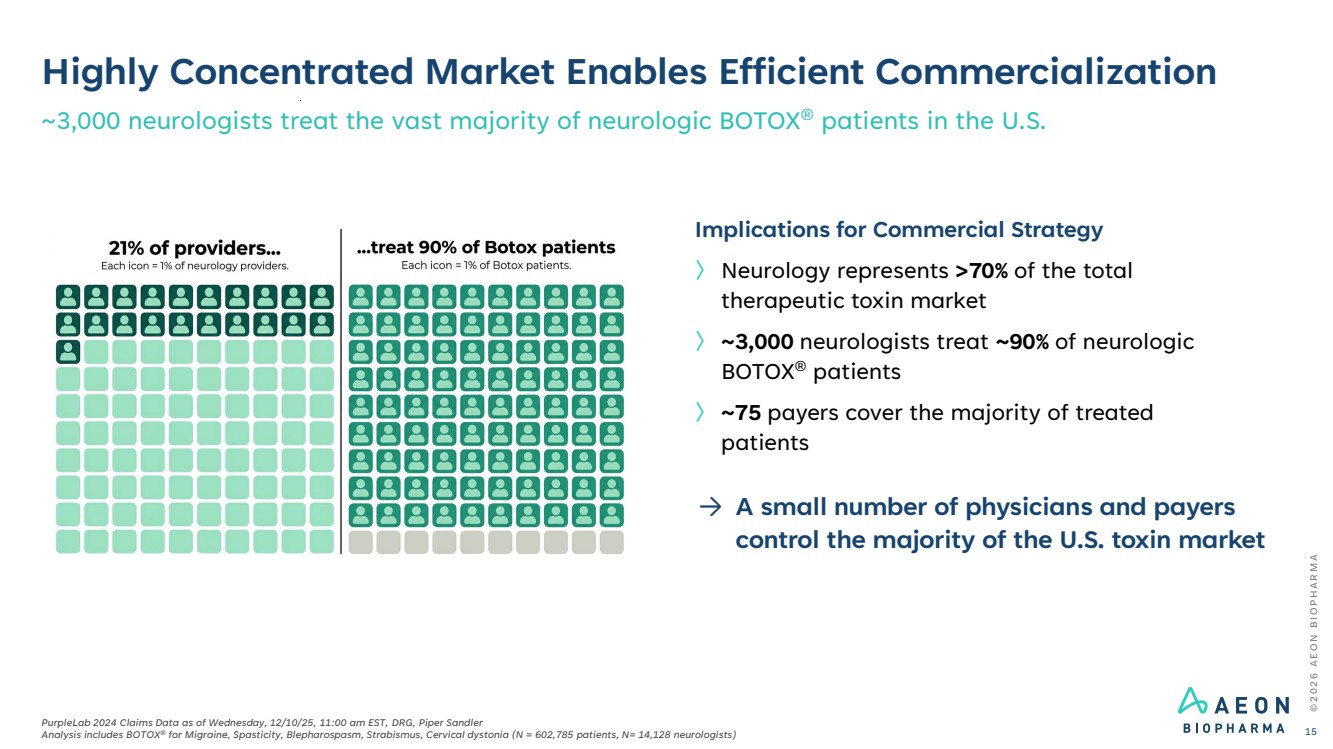

| Highly Concentrated Market Enables Efficient Commercialization ~3,000 neurologists treat the vast majority of neurologic BOTOX® patients in the U.S. © 2 0 2 6 A E O N B I O P H A R M A PurpleLab 2024 Claims Data as of Wednesday, 12/10/25, 11:00 am EST, DRG, Piper Sandler Analysis includes BOTOX® for Migraine, Spasticity, Blepharospasm, Strabismus, Cervical dystonia (N = 602,785 patients, N= 14,128 neurologists) 15 Implications for Commercial Strategy 〉 Neurology represents >70% of the total therapeutic toxin market 〉 ~3,000 neurologists treat ~90% of neurologic BOTOX® patients 〉 ~75 payers cover the majority of treated patients → A small number of physicians and payers control the majority of the U.S. toxin market |

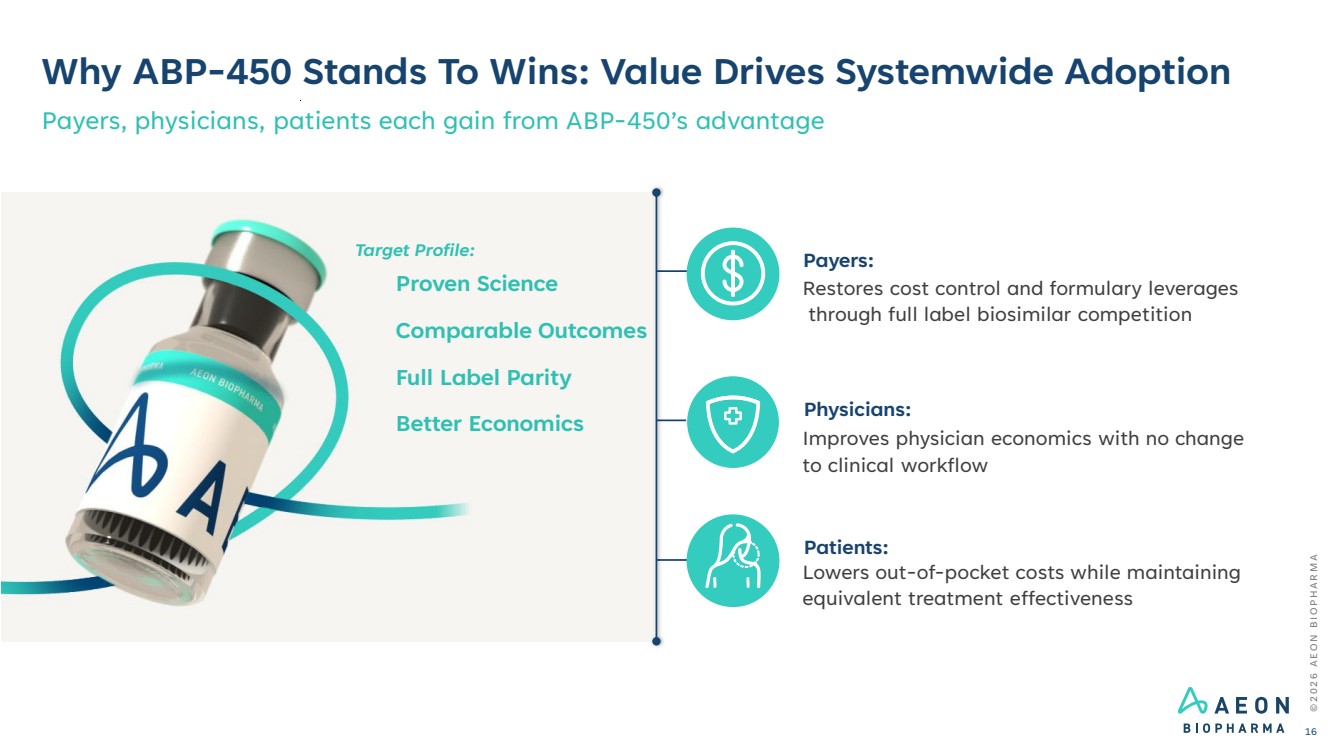

| Why ABP-450 Stands To Wins: Value Drives Systemwide Adoption Payers, physicians, patients each gain from ABP-450’s advantage Payers: Restores cost control and formulary leverages through full label biosimilar competition Physicians: Improves physician economics with no change to clinical workflow Patients: Lowers out-of-pocket costs while maintaining equivalent treatment effectiveness Proven Science Comparable Outcomes Full Label Parity Better Economics © 2 0 2 6 A E O N B I O P H A R M A 16 Target Profile: |

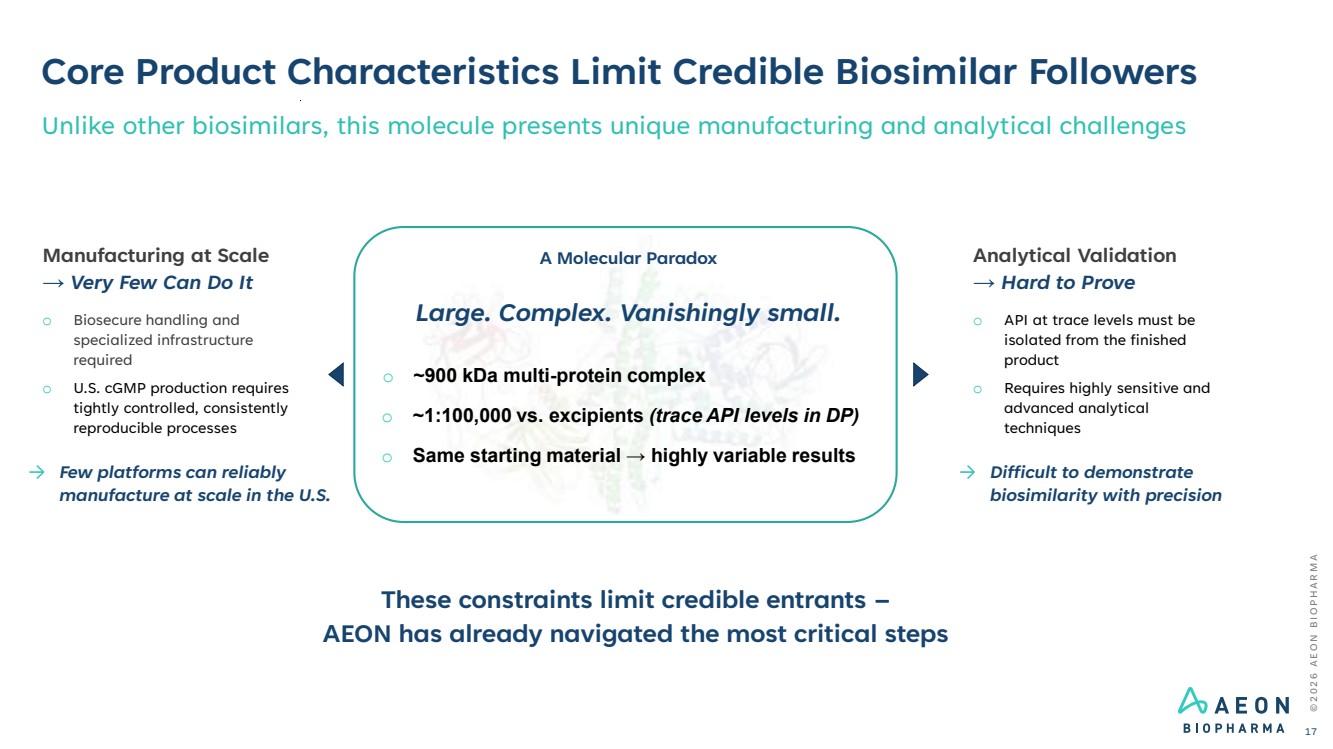

| © 2 0 2 6 A E O N B I O P H A R M A Core Product Characteristics Limit Credible Biosimilar Followers 17 Unlike other biosimilars, this molecule presents unique manufacturing and analytical challenges A Molecular Paradox Large. Complex. Vanishingly small. o ~900 kDa multi-protein complex o ~1:100,000 vs. excipients (trace API levels in DP) o Same starting material → highly variable results These constraints limit credible entrants – AEON has already navigated the most critical steps Manufacturing at Scale → Very Few Can Do It o Biosecure handling and specialized infrastructure required o U.S. cGMP production requires tightly controlled, consistently reproducible processes → Few platforms can reliably manufacture at scale in the U.S. Analytical Validation → Hard to Prove o API at trace levels must be isolated from the finished product o Requires highly sensitive and advanced analytical techniques → Difficult to demonstrate biosimilarity with precision |

| ABP-450 Biosimilar Development Program |

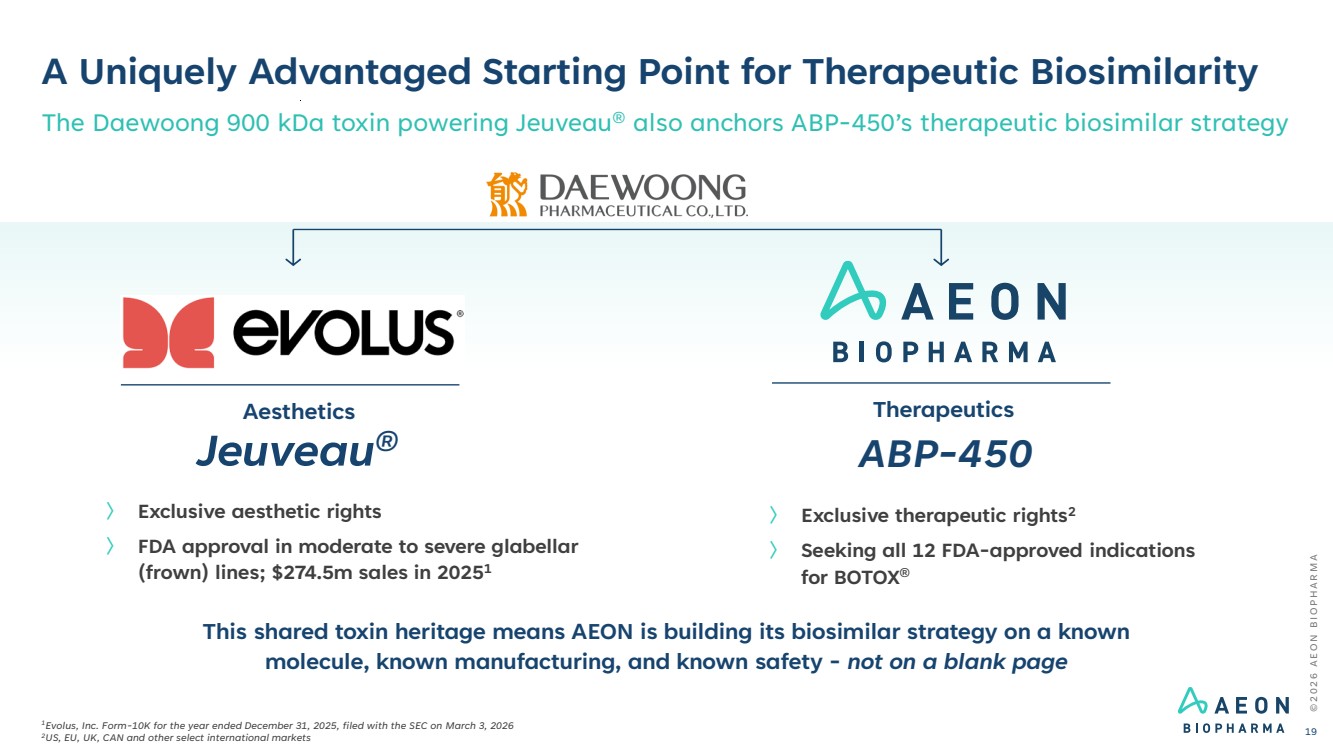

| A Uniquely Advantaged Starting Point for Therapeutic Biosimilarity 〉 Exclusive aesthetic rights 〉 FDA approval in moderate to severe glabellar (frown) lines; $274.5m sales in 20251 Jeuveau® ABP-450 Aesthetics Therapeutics 〉 Exclusive therapeutic rights2 〉 Seeking all 12 FDA-approved indications for BOTOX® © 2 0 2 6 A E O N B I O P H A R M A 19 The Daewoong 900 kDa toxin powering Jeuveau® also anchors ABP-450’s therapeutic biosimilar strategy This shared toxin heritage means AEON is building its biosimilar strategy on a known molecule, known manufacturing, and known safety - not on a blank page 1Evolus, Inc. Form-10K for the year ended December 31, 2025, filed with the SEC on March 3, 2026 2US, EU, UK, CAN and other select international markets |

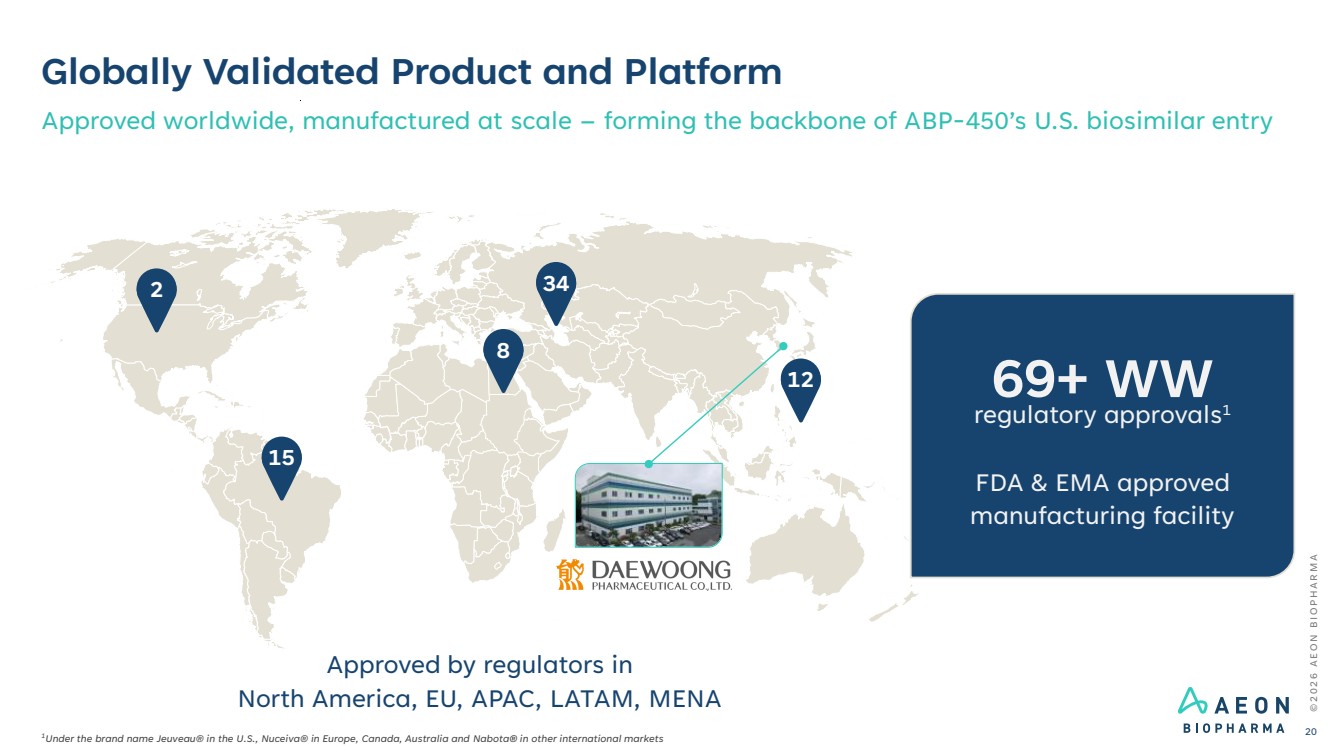

| Globally Validated Product and Platform Approved worldwide, manufactured at scale – forming the backbone of ABP-450’s U.S. biosimilar entry 2 15 8 34 12 Approved by regulators in North America, EU, APAC, LATAM, MENA © 2 0 2 6 A E O N B I O P H A R M A 20 1Under the brand name Jeuveau® in the U.S., Nuceiva® in Europe, Canada, Australia and Nabota® in other international markets regulatory approvals 69+ WW 1 FDA & EMA approved manufacturing facility |

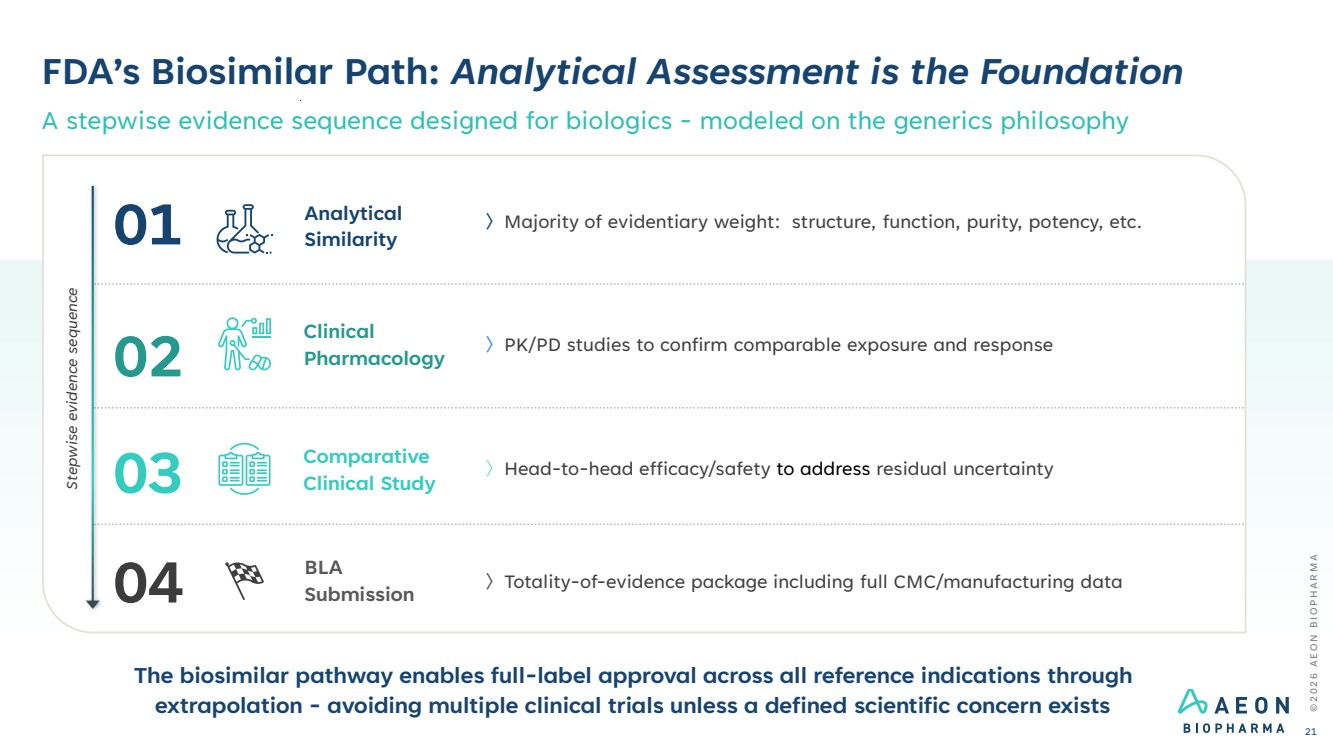

| FDA’s Biosimilar Path: Analytical Assessment is the Foundation A stepwise evidence sequence designed for biologics - modeled on the generics philosophy © 2 0 2 6 A E O N B I O P H A R M A 21 〉Majority of evidentiary weight: structure, function, purity, potency, etc. Analytical Similarity 〉PK/PD studies to confirm comparable exposure and response Clinical Pharmacology 〉Head-to-head efficacy/safety to address residual uncertainty Comparative Clinical Study 〉Totality-of-evidence package including full CMC/manufacturing data BLA Submission The biosimilar pathway enables full-label approval across all reference indications through extrapolation - avoiding multiple clinical trials unless a defined scientific concern exists Stepwise evidence sequence 01 02 03 04 |

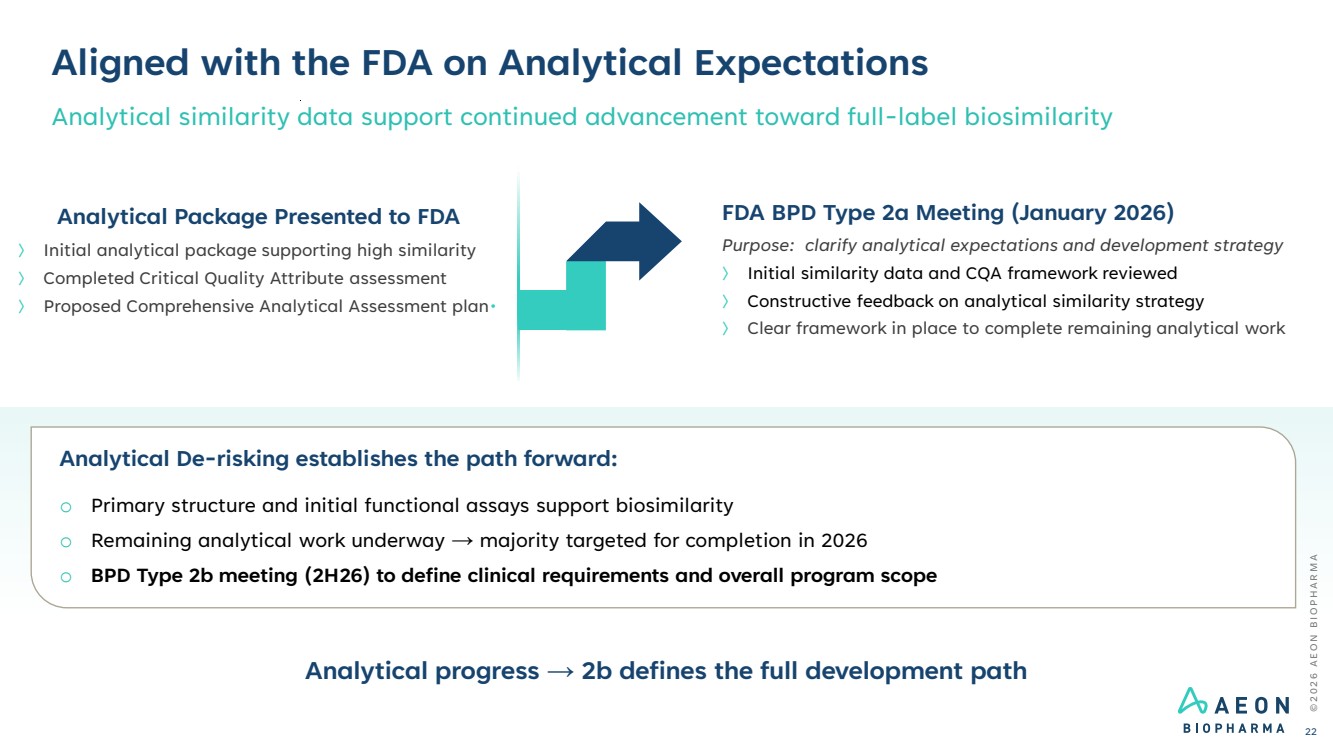

| FDA BPD Type 2a Meeting (January 2026) Purpose: clarify analytical expectations and development strategy 〉 Initial similarity data and CQA framework reviewed 〉 Constructive feedback on analytical similarity strategy 〉 Clear framework in place to complete remaining analytical work Analytical De-risking establishes the path forward: o Primary structure and initial functional assays support biosimilarity o Remaining analytical work underway → majority targeted for completion in 2026 o BPD Type 2b meeting (2H26) to define clinical requirements and overall program scope Aligned with the FDA on Analytical Expectations Analytical similarity data support continued advancement toward full-label biosimilarity © 2 0 2 6 A E O N B I O P H A R M A 22 Analytical Package Presented to FDA 〉 Initial analytical package supporting high similarity 〉 Completed Critical Quality Attribute assessment 〉 Proposed Comprehensive Analytical Assessment plan• Analytical progress → 2b defines the full development path |

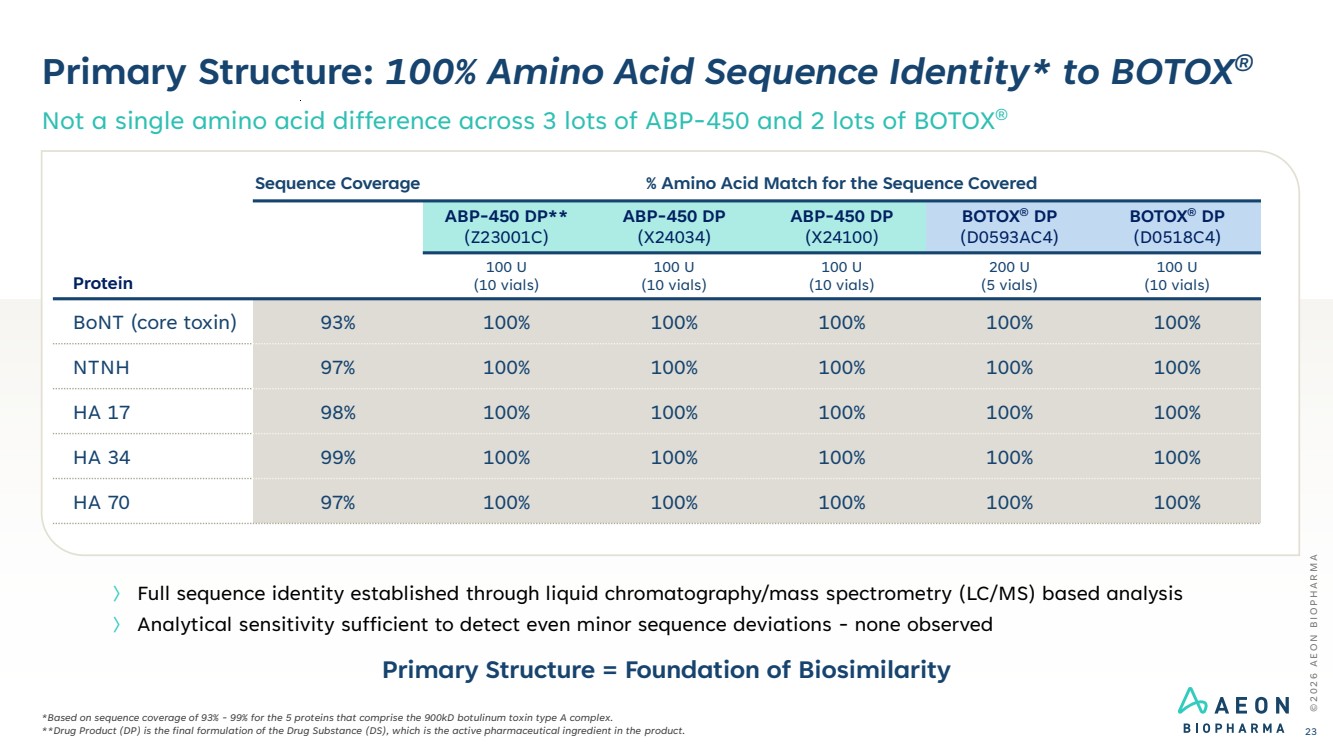

| Primary Structure: 100% Amino Acid Sequence Identity* to BOTOX® Not a single amino acid difference across 3 lots of ABP-450 and 2 lots of BOTOX® © 2 0 2 6 A E O N B I O P H A R M A 23 *Based on sequence coverage of 93% - 99% for the 5 proteins that comprise the 900kD botulinum toxin type A complex. **Drug Product (DP) is the final formulation of the Drug Substance (DS), which is the active pharmaceutical ingredient in the product. 〉 Full sequence identity established through liquid chromatography/mass spectrometry (LC/MS) based analysis 〉 Analytical sensitivity sufficient to detect even minor sequence deviations - none observed Protein Sequence Coverage % Amino Acid Match for the Sequence Covered ABP-450 DP** (Z23001C) ABP-450 DP (X24034) ABP-450 DP (X24100) BOTOX® DP (D0593AC4) BOTOX® DP (D0518C4) 100 U (10 vials) 100 U (10 vials) 100 U (10 vials) 200 U (5 vials) 100 U (10 vials) BoNT (core toxin) 93% 100% 100% 100% 100% 100% NTNH 97% 100% 100% 100% 100% 100% HA 17 98% 100% 100% 100% 100% 100% HA 34 99% 100% 100% 100% 100% 100% HA 70 97% 100% 100% 100% 100% 100% Primary Structure = Foundation of Biosimilarity |

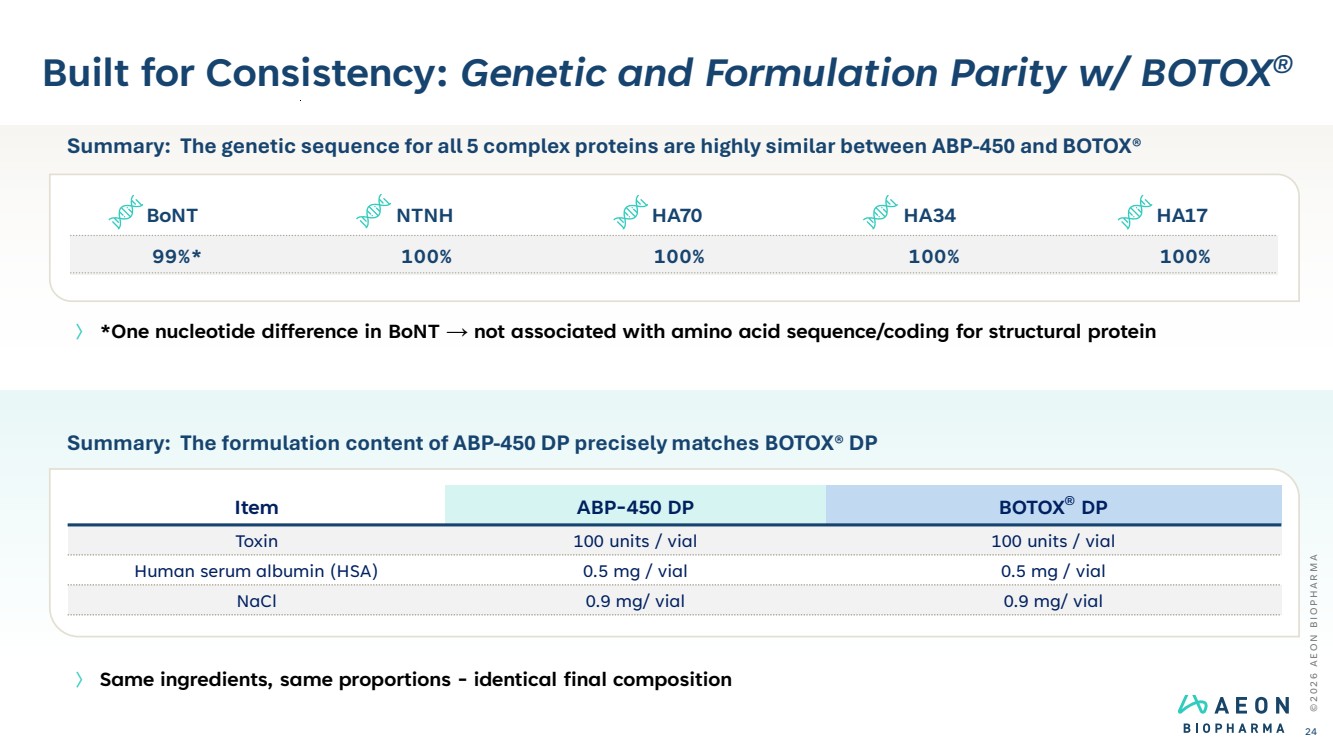

| Built for Consistency: Genetic and Formulation Parity w/ BOTOX® © 2 0 2 6 A E O N B I O P H A R M A 24 〉 *One nucleotide difference in BoNT → not associated with amino acid sequence/coding for structural protein 〉 Same ingredients, same proportions - identical final composition Summary: The formulation content of ABP-450 DP precisely matches BOTOX® DP Item ABP-450 DP BOTOX® DP Toxin 100 units / vial 100 units / vial Human serum albumin (HSA) 0.5 mg / vial 0.5 mg / vial NaCl 0.9 mg/ vial 0.9 mg/ vial Summary: The genetic sequence for all 5 complex proteins are highly similar between ABP-450 and BOTOX® BoNT NTNH HA70 HA34 HA17 99%* 100% 100% 100% 100% |

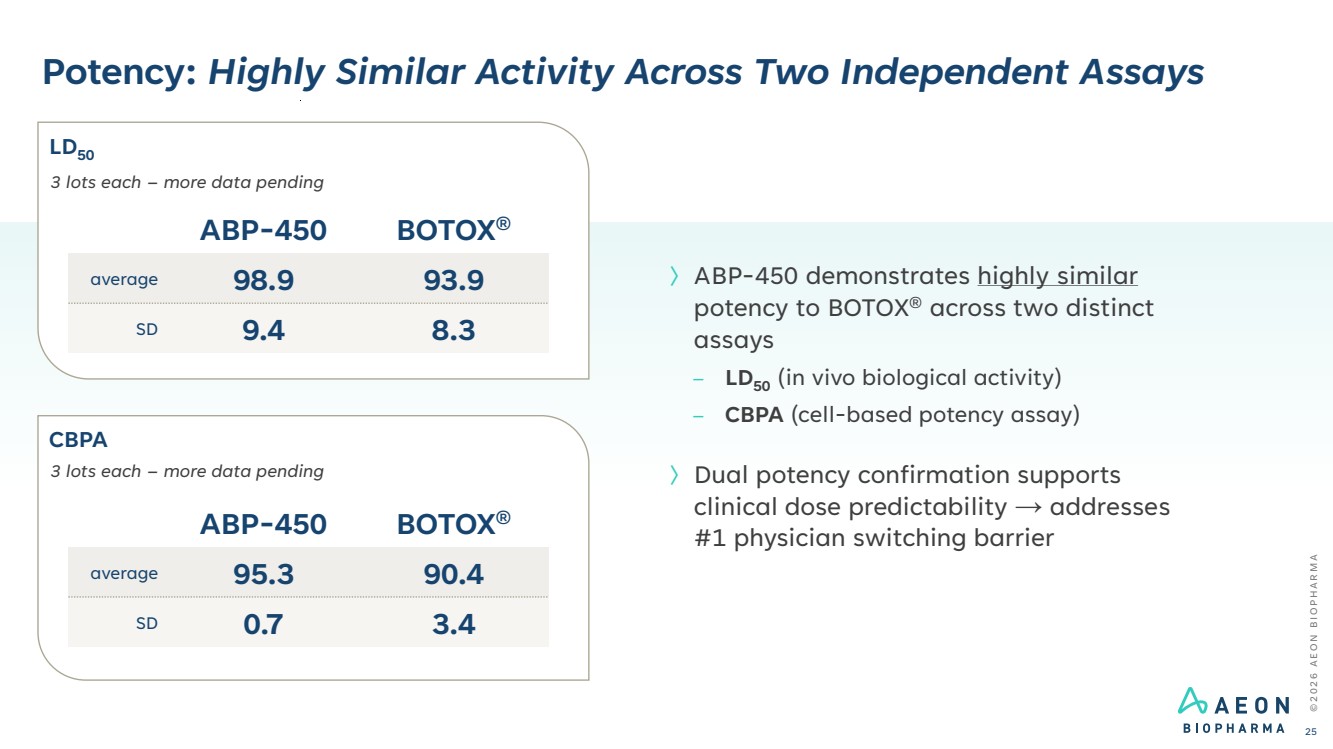

| Potency: Highly Similar Activity Across Two Independent Assays © 2 0 2 6 A E O N B I O P H A R M A 25 〉ABP-450 demonstrates highly similar potency to BOTOX® across two distinct assays – LD50 (in vivo biological activity) – CBPA (cell-based potency assay) 〉Dual potency confirmation supports clinical dose predictability → addresses #1 physician switching barrier ABP-450 BOTOX® average 98.9 93.9 SD 9.4 8.3 3 lots each – more data pending ABP-450 BOTOX® average 95.3 90.4 SD 0.7 3.4 3 lots each – more data pending LD50 CBPA |

| Corporate Profile |

| Proven Operators in Toxins, Biosimilars, and Capital Formation Collectively executed multiple equity, debt, and hybrid financings totaling more than $750 million 〉 20+ years in biotech and life sciences capital markets 〉 Over $500M in capital raised through a variety of equity, debt, and hybrid structures Alex Wilson Chief Legal & Strategy Officer; Corporate Secretary 〉 Former BOTOX® leader responsible for competitive strategy and long-range asset maximization 〉 Led multiple therapeutic and buy-and-bill biologic launches Rob Bancroft Chief Executive Officer 〉 20+ years in clinical development and regulatory strategy – responsible for multiple IND, NDA, and BLA submissions Chad Oh, MD Chief Medical Officer © 2 0 2 6 A E O N B I O P H A R M A 27 〉 25+ years of financial and leadership experience in the biotechnology and life sciences sectors John Bencich Chief Financial Officer |

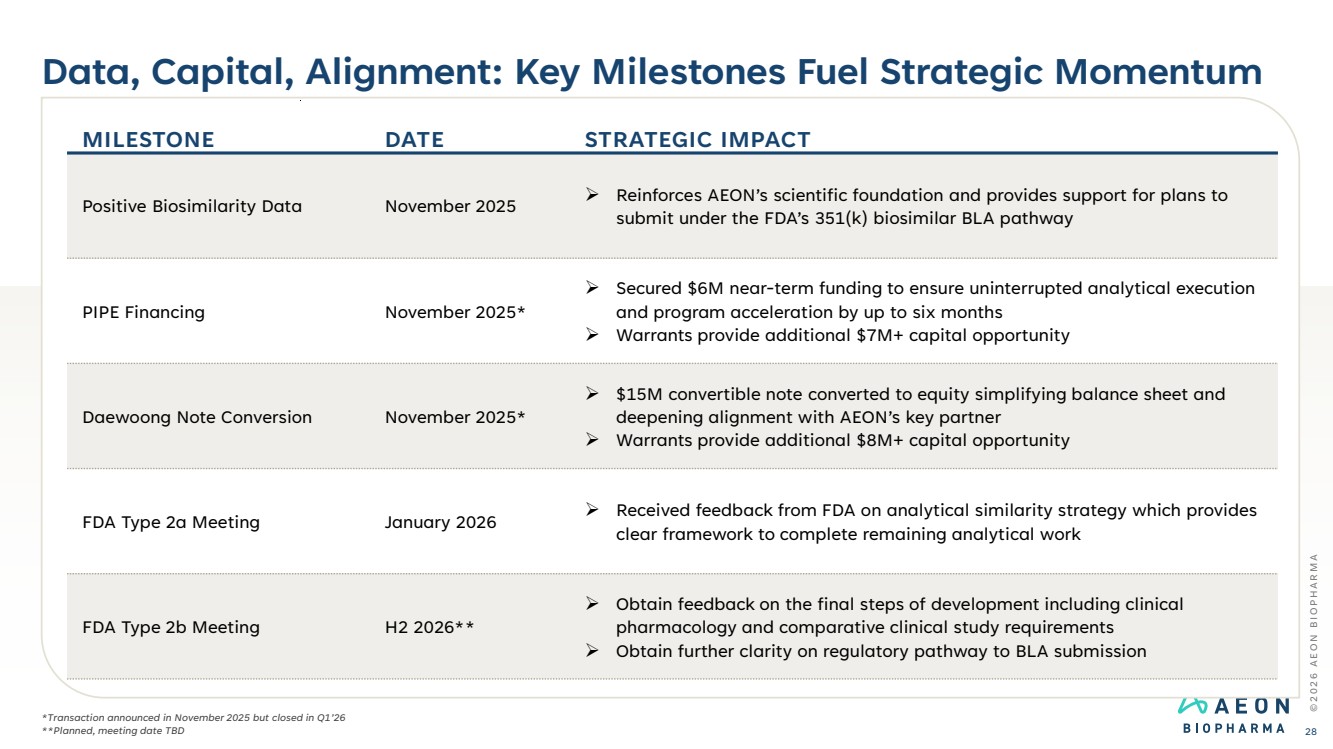

| Data, Capital, Alignment: Key Milestones Fuel Strategic Momentum © 2 0 2 6 A E O N B I O P H A R M A 28 MILESTONE DATE STRATEGIC IMPACT Positive Biosimilarity Data November 2025 ➢ Reinforces AEON’s scientific foundation and provides support for plans to submit under the FDA’s 351(k) biosimilar BLA pathway PIPE Financing November 2025* ➢ Secured $6M near-term funding to ensure uninterrupted analytical execution and program acceleration by up to six months ➢ Warrants provide additional $7M+ capital opportunity Daewoong Note Conversion November 2025* ➢ $15M convertible note converted to equity simplifying balance sheet and deepening alignment with AEON’s key partner ➢ Warrants provide additional $8M+ capital opportunity FDA Type 2a Meeting January 2026 ➢ Received feedback from FDA on analytical similarity strategy which provides clear framework to complete remaining analytical work FDA Type 2b Meeting H2 2026** ➢ Obtain feedback on the final steps of development including clinical pharmacology and comparative clinical study requirements ➢ Obtain further clarity on regulatory pathway to BLA submission *Transaction announced in November 2025 but closed in Q1’26 **Planned, meeting date TBD |

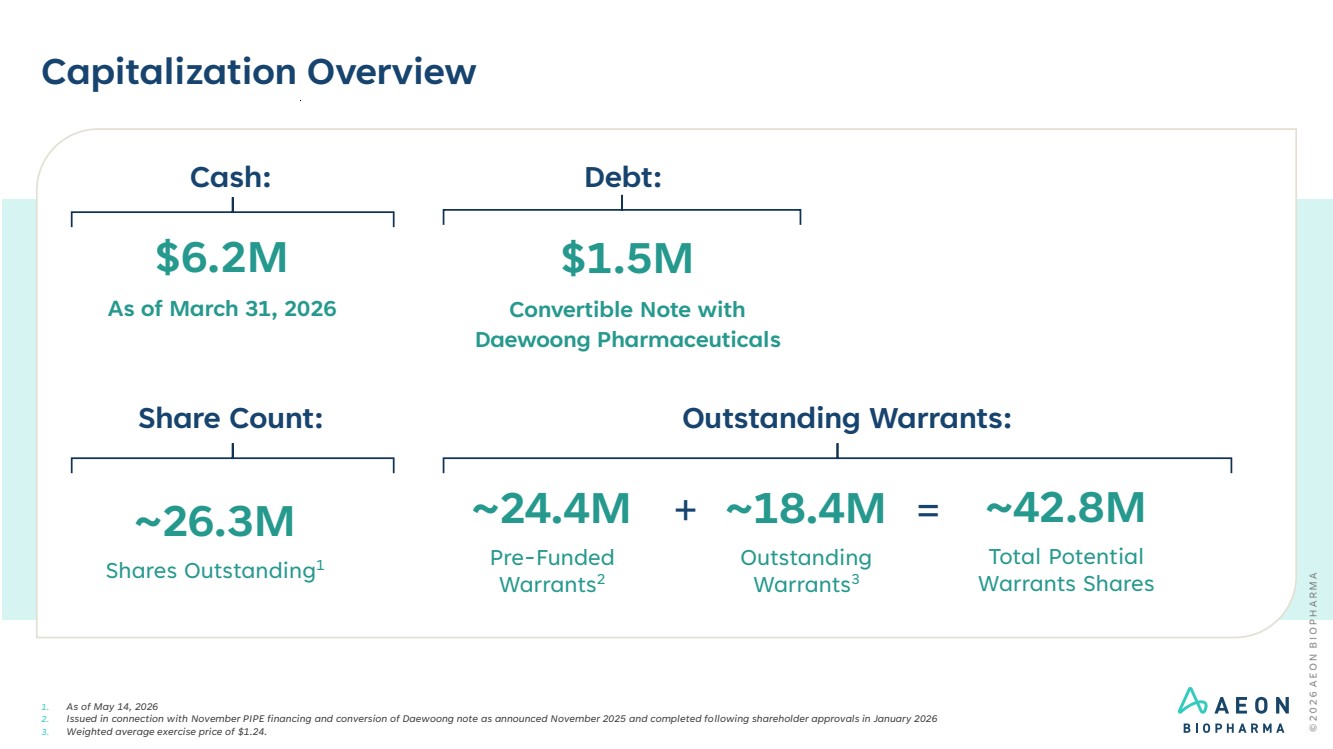

| Capitalization Overview 1. As of May 14, 2026 2. Issued in connection with November PIPE financing and conversion of Daewoong note as announced November 2025 and completed following shareholder approvals in January 2026 3. Weighted average exercise price of $1.24. Outstanding Warrants: ~26.3M Shares Outstanding1 ~18.4M Outstanding Warrants3 ~42.8M Total Potential Warrants Shares = Share Count: ~24.4M Pre-Funded Warrants2 + Debt: $6.2M As of March 31, 2026 Cash: $1.5M Convertible Note with Daewoong Pharmaceuticals |

| Strong analytical data flowing from a proven toxin platform Completed 2a meeting; advancing analytical similarity Positioned to drive broad market adoption Full-label biosimilarity uniquely unlocks the BOTOX® monopoly © 2 0 2 6 A E O N B I O P H A R M A 30 Positioned to Deliver the First True Clinical Substitute to BOTOX® Strong data, aligned partner, FDA engagement: ABP-450 on track to full-label biosimilarity A rare combination of scale, structural barriers, and clear de-risking path |

| Thank you NYSEAMERICAN: AEON © 2 0 2 6 A E O N B I O P H A R M A |