0001840776FALSEFY202512/31P3YP1Yhttp://fasb.org/us-gaap/2025#OtherAssetshttp://fasb.org/us-gaap/2025#OtherAssetshttp://fasb.org/us-gaap/2025#OtherLiabilitiesNoncurrentP2Y142iso4217:USDxbrli:sharesiso4217:USDxbrli:sharesxbrli:purehgty:segmentshgty:borrowerhgty:claimhgty:letter_of_credithgty:consecutiveTradingDayhgty:vote00018407762025-01-012025-12-3100018407762025-06-300001840776us-gaap:CommonClassAMember2026-02-200001840776hgty:CommonClassVMember2026-02-200001840776hgty:CommissionRevenueAndFeeRevenueMember2025-01-012025-12-310001840776hgty:CommissionRevenueAndFeeRevenueMember2024-01-012024-12-310001840776hgty:CommissionRevenueAndFeeRevenueMember2023-01-012023-12-3100018407762024-01-012024-12-3100018407762023-01-012023-12-310001840776hgty:MembershipAndOtherRevenueMember2025-01-012025-12-310001840776hgty:MembershipAndOtherRevenueMember2024-01-012024-12-310001840776hgty:MembershipAndOtherRevenueMember2023-01-012023-12-310001840776us-gaap:CommonClassAMember2025-01-012025-12-310001840776us-gaap:CommonClassAMember2024-01-012024-12-310001840776us-gaap:CommonClassAMember2023-01-012023-12-3100018407762025-12-3100018407762024-12-310001840776us-gaap:CommonClassAMember2024-12-310001840776us-gaap:CommonClassAMember2025-12-310001840776hgty:CommonClassVMember2025-12-310001840776hgty:CommonClassVMember2024-12-310001840776us-gaap:SeriesAPreferredStockMemberus-gaap:PreferredStockMember2024-12-310001840776us-gaap:CommonClassAMemberus-gaap:CommonStockMember2024-12-310001840776hgty:CommonClassVMemberus-gaap:CommonStockMember2024-12-310001840776us-gaap:AdditionalPaidInCapitalMember2024-12-310001840776us-gaap:RetainedEarningsMember2024-12-310001840776us-gaap:AccumulatedOtherComprehensiveIncomeMember2024-12-310001840776us-gaap:ParentMember2024-12-310001840776us-gaap:NoncontrollingInterestMember2024-12-310001840776us-gaap:RetainedEarningsMember2025-01-012025-12-310001840776us-gaap:ParentMember2025-01-012025-12-310001840776us-gaap:NoncontrollingInterestMember2025-01-012025-12-310001840776us-gaap:SeriesAPreferredStockMemberus-gaap:PreferredStockMember2025-01-012025-12-310001840776us-gaap:AdditionalPaidInCapitalMember2025-01-012025-12-310001840776us-gaap:AccumulatedOtherComprehensiveIncomeMember2025-01-012025-12-310001840776us-gaap:CommonClassAMemberus-gaap:CommonStockMember2025-01-012025-12-310001840776hgty:CommonClassVMemberus-gaap:CommonStockMember2025-01-012025-12-310001840776us-gaap:SeriesAPreferredStockMemberus-gaap:PreferredStockMember2025-12-310001840776us-gaap:CommonClassAMemberus-gaap:CommonStockMember2025-12-310001840776hgty:CommonClassVMemberus-gaap:CommonStockMember2025-12-310001840776us-gaap:AdditionalPaidInCapitalMember2025-12-310001840776us-gaap:RetainedEarningsMember2025-12-310001840776us-gaap:AccumulatedOtherComprehensiveIncomeMember2025-12-310001840776us-gaap:ParentMember2025-12-310001840776us-gaap:NoncontrollingInterestMember2025-12-310001840776us-gaap:SeriesAPreferredStockMemberus-gaap:PreferredStockMember2023-12-310001840776us-gaap:CommonClassAMemberus-gaap:CommonStockMember2023-12-310001840776hgty:CommonClassVMemberus-gaap:CommonStockMember2023-12-310001840776us-gaap:AdditionalPaidInCapitalMember2023-12-310001840776us-gaap:RetainedEarningsMember2023-12-310001840776us-gaap:AccumulatedOtherComprehensiveIncomeMember2023-12-310001840776us-gaap:ParentMember2023-12-310001840776us-gaap:NoncontrollingInterestMember2023-12-3100018407762023-12-310001840776us-gaap:RetainedEarningsMember2024-01-012024-12-310001840776us-gaap:ParentMember2024-01-012024-12-310001840776us-gaap:NoncontrollingInterestMember2024-01-012024-12-310001840776us-gaap:SeriesAPreferredStockMemberus-gaap:PreferredStockMember2024-01-012024-12-310001840776us-gaap:AdditionalPaidInCapitalMember2024-01-012024-12-310001840776us-gaap:AccumulatedOtherComprehensiveIncomeMember2024-01-012024-12-310001840776us-gaap:CommonClassAMemberus-gaap:CommonStockMember2024-01-012024-12-310001840776us-gaap:SeriesAPreferredStockMemberus-gaap:PreferredStockMember2022-12-310001840776us-gaap:CommonClassAMemberus-gaap:CommonStockMember2022-12-310001840776hgty:CommonClassVMemberus-gaap:CommonStockMember2022-12-310001840776us-gaap:AdditionalPaidInCapitalMember2022-12-310001840776us-gaap:RetainedEarningsMember2022-12-310001840776us-gaap:AccumulatedOtherComprehensiveIncomeMember2022-12-310001840776us-gaap:ParentMember2022-12-310001840776us-gaap:NoncontrollingInterestMember2022-12-3100018407762022-12-310001840776us-gaap:RetainedEarningsMember2023-01-012023-12-310001840776us-gaap:ParentMember2023-01-012023-12-310001840776us-gaap:NoncontrollingInterestMember2023-01-012023-12-310001840776us-gaap:SeriesAPreferredStockMemberus-gaap:PreferredStockMember2023-01-012023-12-310001840776us-gaap:AdditionalPaidInCapitalMember2023-01-012023-12-310001840776us-gaap:AccumulatedOtherComprehensiveIncomeMember2023-01-012023-12-310001840776us-gaap:CommonClassAMemberus-gaap:CommonStockMember2023-01-012023-12-310001840776hgty:HagertyReinsuranceLimitedMembersrt:MinimumMember2025-01-012025-12-310001840776hgty:HagertyReinsuranceLimitedMembersrt:MaximumMember2025-01-012025-12-310001840776hgty:HagertyReinsuranceLimitedMember2025-01-012025-12-310001840776srt:RevisionOfPriorPeriodReclassificationAdjustmentMember2024-01-012024-12-310001840776srt:RevisionOfPriorPeriodReclassificationAdjustmentMember2023-01-012023-12-310001840776hgty:TheHagertyGroupLLCMember2025-01-012025-12-310001840776hgty:TheHagertyGroupLLCMember2024-01-012024-12-310001840776srt:MinimumMemberus-gaap:ComputerEquipmentMember2025-12-310001840776srt:MaximumMemberus-gaap:AutomobilesMember2025-12-310001840776us-gaap:BuildingAndBuildingImprovementsMember2025-12-310001840776srt:MinimumMember2025-12-310001840776srt:MaximumMember2025-12-310001840776hgty:SpeedDigitalAndBroadArrowMember2025-12-310001840776us-gaap:CustomerConcentrationRiskMemberhgty:TheHagertyGroupLLCMemberus-gaap:SalesRevenueNetMember2025-01-012025-12-310001840776us-gaap:ShortTermContractWithCustomerMember2025-01-012025-12-310001840776hgty:LaborAndRelatedExpenseMemberMember2025-01-012025-12-310001840776hgty:LaborAndRelatedExpenseMemberMember2024-01-012024-12-310001840776hgty:LaborAndRelatedExpenseMemberMember2023-01-012023-12-310001840776us-gaap:VariableInterestEntityPrimaryBeneficiaryMember2025-12-310001840776us-gaap:VariableInterestEntityPrimaryBeneficiaryMember2024-12-310001840776us-gaap:OperatingSegmentsMemberhgty:CommissionRevenueAndFeeRevenueMemberhgty:InsuranceSegmentMember2025-01-012025-12-310001840776us-gaap:OperatingSegmentsMemberhgty:CommissionRevenueAndFeeRevenueMemberhgty:MarketplaceSegmentMember2025-01-012025-12-310001840776us-gaap:OperatingSegmentsMemberhgty:InsuranceSegmentMember2025-01-012025-12-310001840776us-gaap:OperatingSegmentsMemberhgty:MarketplaceSegmentMember2025-01-012025-12-310001840776us-gaap:OperatingSegmentsMemberhgty:MembershipAndOtherRevenueMemberhgty:InsuranceSegmentMember2025-01-012025-12-310001840776us-gaap:OperatingSegmentsMemberhgty:MembershipAndOtherRevenueMemberhgty:MarketplaceSegmentMember2025-01-012025-12-310001840776us-gaap:CorporateNonSegmentMember2025-01-012025-12-310001840776us-gaap:OperatingSegmentsMemberhgty:CommissionRevenueAndFeeRevenueMemberhgty:InsuranceSegmentMember2024-01-012024-12-310001840776us-gaap:OperatingSegmentsMemberhgty:CommissionRevenueAndFeeRevenueMemberhgty:MarketplaceSegmentMember2024-01-012024-12-310001840776us-gaap:OperatingSegmentsMemberhgty:InsuranceSegmentMember2024-01-012024-12-310001840776us-gaap:OperatingSegmentsMemberhgty:MarketplaceSegmentMember2024-01-012024-12-310001840776us-gaap:OperatingSegmentsMemberhgty:MembershipAndOtherRevenueMemberhgty:InsuranceSegmentMember2024-01-012024-12-310001840776us-gaap:OperatingSegmentsMemberhgty:MembershipAndOtherRevenueMemberhgty:MarketplaceSegmentMember2024-01-012024-12-310001840776us-gaap:CorporateNonSegmentMember2024-01-012024-12-310001840776us-gaap:OperatingSegmentsMemberhgty:CommissionRevenueAndFeeRevenueMemberhgty:InsuranceSegmentMember2023-01-012023-12-310001840776us-gaap:OperatingSegmentsMemberhgty:CommissionRevenueAndFeeRevenueMemberhgty:MarketplaceSegmentMember2023-01-012023-12-310001840776us-gaap:OperatingSegmentsMemberhgty:InsuranceSegmentMember2023-01-012023-12-310001840776us-gaap:OperatingSegmentsMemberhgty:MarketplaceSegmentMember2023-01-012023-12-310001840776us-gaap:OperatingSegmentsMemberhgty:MembershipAndOtherRevenueMemberhgty:InsuranceSegmentMember2023-01-012023-12-310001840776us-gaap:OperatingSegmentsMemberhgty:MembershipAndOtherRevenueMemberhgty:MarketplaceSegmentMember2023-01-012023-12-310001840776us-gaap:CorporateNonSegmentMember2023-01-012023-12-310001840776country:UShgty:InsuranceSegmentMember2025-01-012025-12-310001840776country:UShgty:MarketplaceSegmentMember2025-01-012025-12-310001840776country:US2025-01-012025-12-310001840776us-gaap:NonUsMemberhgty:InsuranceSegmentMember2025-01-012025-12-310001840776us-gaap:NonUsMemberhgty:MarketplaceSegmentMember2025-01-012025-12-310001840776us-gaap:NonUsMember2025-01-012025-12-310001840776hgty:InsuranceSegmentMember2025-01-012025-12-310001840776hgty:MarketplaceSegmentMember2025-01-012025-12-310001840776country:UShgty:InsuranceSegmentMember2024-01-012024-12-310001840776country:UShgty:MarketplaceSegmentMember2024-01-012024-12-310001840776country:US2024-01-012024-12-310001840776us-gaap:NonUsMemberhgty:InsuranceSegmentMember2024-01-012024-12-310001840776us-gaap:NonUsMemberhgty:MarketplaceSegmentMember2024-01-012024-12-310001840776us-gaap:NonUsMember2024-01-012024-12-310001840776hgty:InsuranceSegmentMember2024-01-012024-12-310001840776hgty:MarketplaceSegmentMember2024-01-012024-12-310001840776country:UShgty:InsuranceSegmentMember2023-01-012023-12-310001840776country:UShgty:MarketplaceSegmentMember2023-01-012023-12-310001840776country:US2023-01-012023-12-310001840776us-gaap:NonUsMemberhgty:InsuranceSegmentMember2023-01-012023-12-310001840776us-gaap:NonUsMemberhgty:MarketplaceSegmentMember2023-01-012023-12-310001840776us-gaap:NonUsMember2023-01-012023-12-310001840776hgty:InsuranceSegmentMember2023-01-012023-12-310001840776hgty:MarketplaceSegmentMember2023-01-012023-12-310001840776hgty:CommissionAndFeeRevenueMemberus-gaap:SalesChannelThroughIntermediaryMember2025-01-012025-12-310001840776hgty:CommissionAndFeeRevenueMemberus-gaap:SalesChannelDirectlyToConsumerMember2025-01-012025-12-310001840776hgty:CommissionAndFeeRevenueMember2025-01-012025-12-310001840776hgty:ContingentCommissionMemberus-gaap:SalesChannelThroughIntermediaryMember2025-01-012025-12-310001840776hgty:ContingentCommissionMemberus-gaap:SalesChannelDirectlyToConsumerMember2025-01-012025-12-310001840776hgty:ContingentCommissionMember2025-01-012025-12-310001840776hgty:CommissionRevenueAndFeeRevenueMemberus-gaap:SalesChannelThroughIntermediaryMember2025-01-012025-12-310001840776hgty:CommissionRevenueAndFeeRevenueMemberus-gaap:SalesChannelDirectlyToConsumerMember2025-01-012025-12-310001840776hgty:CommissionAndFeeRevenueMemberus-gaap:SalesChannelThroughIntermediaryMember2024-01-012024-12-310001840776hgty:CommissionAndFeeRevenueMemberus-gaap:SalesChannelDirectlyToConsumerMember2024-01-012024-12-310001840776hgty:CommissionAndFeeRevenueMember2024-01-012024-12-310001840776hgty:ContingentCommissionMemberus-gaap:SalesChannelThroughIntermediaryMember2024-01-012024-12-310001840776hgty:ContingentCommissionMemberus-gaap:SalesChannelDirectlyToConsumerMember2024-01-012024-12-310001840776hgty:ContingentCommissionMember2024-01-012024-12-310001840776hgty:CommissionRevenueAndFeeRevenueMemberus-gaap:SalesChannelThroughIntermediaryMember2024-01-012024-12-310001840776hgty:CommissionRevenueAndFeeRevenueMemberus-gaap:SalesChannelDirectlyToConsumerMember2024-01-012024-12-310001840776hgty:CommissionAndFeeRevenueMemberus-gaap:SalesChannelThroughIntermediaryMember2023-01-012023-12-310001840776hgty:CommissionAndFeeRevenueMemberus-gaap:SalesChannelDirectlyToConsumerMember2023-01-012023-12-310001840776hgty:CommissionAndFeeRevenueMember2023-01-012023-12-310001840776hgty:ContingentCommissionMemberus-gaap:SalesChannelThroughIntermediaryMember2023-01-012023-12-310001840776hgty:ContingentCommissionMemberus-gaap:SalesChannelDirectlyToConsumerMember2023-01-012023-12-310001840776hgty:ContingentCommissionMember2023-01-012023-12-310001840776hgty:CommissionRevenueAndFeeRevenueMemberus-gaap:SalesChannelThroughIntermediaryMember2023-01-012023-12-310001840776hgty:CommissionRevenueAndFeeRevenueMemberus-gaap:SalesChannelDirectlyToConsumerMember2023-01-012023-12-310001840776us-gaap:CorporateDebtSecuritiesMember2025-12-310001840776us-gaap:USTreasurySecuritiesMember2025-12-310001840776us-gaap:USStatesAndPoliticalSubdivisionsMember2025-12-310001840776us-gaap:ForeignGovernmentDebtSecuritiesMember2025-12-310001840776us-gaap:AssetBackedSecuritiesMember2025-12-310001840776us-gaap:MortgageBackedSecuritiesMember2025-12-310001840776us-gaap:CorporateDebtSecuritiesMember2024-12-310001840776us-gaap:USTreasurySecuritiesMember2024-12-310001840776us-gaap:USStatesAndPoliticalSubdivisionsMember2024-12-310001840776us-gaap:ForeignGovernmentDebtSecuritiesMember2024-12-310001840776us-gaap:AssetBackedSecuritiesMember2024-12-310001840776us-gaap:MortgageBackedSecuritiesMember2024-12-310001840776hgty:StatesAndMunicipalitiesMember2025-12-310001840776us-gaap:CashAndCashEquivalentsMember2025-01-012025-12-310001840776us-gaap:CashAndCashEquivalentsMember2024-01-012024-12-310001840776us-gaap:CashAndCashEquivalentsMember2023-01-012023-12-310001840776us-gaap:FixedMaturitiesMember2025-01-012025-12-310001840776us-gaap:FixedMaturitiesMember2024-01-012024-12-310001840776us-gaap:FixedMaturitiesMember2023-01-012023-12-310001840776us-gaap:FixedMaturitiesMember2025-01-012025-12-310001840776us-gaap:FixedMaturitiesMember2024-01-012024-12-310001840776us-gaap:InterestRateSwapMember2020-12-310001840776us-gaap:InterestRateSwapMember2024-06-300001840776us-gaap:CommonClassAMember2024-07-3100018407762024-07-3100018407762024-07-012024-09-300001840776us-gaap:CommonClassAMember2024-07-012024-09-300001840776hgty:PrivatePlacementWarrantsMemberhgty:WarrantLiabilitiesMember2023-12-310001840776hgty:UnderwriterWarrantsMemberhgty:WarrantLiabilitiesMember2023-12-310001840776hgty:OTMWarrantsMemberhgty:WarrantLiabilitiesMember2023-12-310001840776hgty:PIPEWarrantsMemberhgty:WarrantLiabilitiesMember2023-12-310001840776hgty:WarrantLiabilitiesMember2023-12-310001840776hgty:PrivatePlacementWarrantsMemberhgty:WarrantLiabilitiesMember2024-01-012024-12-310001840776hgty:UnderwriterWarrantsMemberhgty:WarrantLiabilitiesMember2024-01-012024-12-310001840776hgty:OTMWarrantsMemberhgty:WarrantLiabilitiesMember2024-01-012024-12-310001840776hgty:PIPEWarrantsMemberhgty:WarrantLiabilitiesMember2024-01-012024-12-310001840776hgty:WarrantLiabilitiesMember2024-01-012024-12-310001840776hgty:PrivatePlacementWarrantsMemberhgty:WarrantLiabilitiesMember2024-12-310001840776hgty:UnderwriterWarrantsMemberhgty:WarrantLiabilitiesMember2024-12-310001840776hgty:OTMWarrantsMemberhgty:WarrantLiabilitiesMember2024-12-310001840776hgty:PIPEWarrantsMemberhgty:WarrantLiabilitiesMember2024-12-310001840776hgty:WarrantLiabilitiesMember2024-12-310001840776us-gaap:CorporateDebtSecuritiesMemberus-gaap:FairValueMeasurementsRecurringMember2025-12-310001840776us-gaap:CorporateDebtSecuritiesMemberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel1Member2025-12-310001840776us-gaap:CorporateDebtSecuritiesMemberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel2Member2025-12-310001840776us-gaap:CorporateDebtSecuritiesMemberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel3Member2025-12-310001840776us-gaap:USTreasurySecuritiesMemberus-gaap:FairValueMeasurementsRecurringMember2025-12-310001840776us-gaap:USTreasurySecuritiesMemberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel1Member2025-12-310001840776us-gaap:USTreasurySecuritiesMemberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel2Member2025-12-310001840776us-gaap:USTreasurySecuritiesMemberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel3Member2025-12-310001840776us-gaap:USStatesAndPoliticalSubdivisionsMemberus-gaap:FairValueMeasurementsRecurringMember2025-12-310001840776us-gaap:USStatesAndPoliticalSubdivisionsMemberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel1Member2025-12-310001840776us-gaap:USStatesAndPoliticalSubdivisionsMemberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel2Member2025-12-310001840776us-gaap:USStatesAndPoliticalSubdivisionsMemberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel3Member2025-12-310001840776us-gaap:ForeignGovernmentDebtSecuritiesMemberus-gaap:FairValueMeasurementsRecurringMember2025-12-310001840776us-gaap:ForeignGovernmentDebtSecuritiesMemberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel1Member2025-12-310001840776us-gaap:ForeignGovernmentDebtSecuritiesMemberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel2Member2025-12-310001840776us-gaap:ForeignGovernmentDebtSecuritiesMemberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel3Member2025-12-310001840776us-gaap:AssetBackedSecuritiesMemberus-gaap:FairValueMeasurementsRecurringMember2025-12-310001840776us-gaap:AssetBackedSecuritiesMemberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel1Member2025-12-310001840776us-gaap:AssetBackedSecuritiesMemberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel2Member2025-12-310001840776us-gaap:AssetBackedSecuritiesMemberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel3Member2025-12-310001840776us-gaap:MortgageBackedSecuritiesMemberus-gaap:FairValueMeasurementsRecurringMember2025-12-310001840776us-gaap:MortgageBackedSecuritiesMemberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel1Member2025-12-310001840776us-gaap:MortgageBackedSecuritiesMemberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel2Member2025-12-310001840776us-gaap:MortgageBackedSecuritiesMemberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel3Member2025-12-310001840776us-gaap:CommonStockMemberus-gaap:FairValueMeasurementsRecurringMember2025-12-310001840776us-gaap:CommonStockMemberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel1Member2025-12-310001840776us-gaap:CommonStockMemberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel2Member2025-12-310001840776us-gaap:CommonStockMemberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel3Member2025-12-310001840776us-gaap:FairValueMeasurementsRecurringMember2025-12-310001840776us-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel1Member2025-12-310001840776us-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel2Member2025-12-310001840776us-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel3Member2025-12-310001840776us-gaap:CorporateDebtSecuritiesMemberus-gaap:FairValueMeasurementsRecurringMember2024-12-310001840776us-gaap:CorporateDebtSecuritiesMemberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel1Member2024-12-310001840776us-gaap:CorporateDebtSecuritiesMemberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel2Member2024-12-310001840776us-gaap:CorporateDebtSecuritiesMemberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel3Member2024-12-310001840776us-gaap:USTreasurySecuritiesMemberus-gaap:FairValueMeasurementsRecurringMember2024-12-310001840776us-gaap:USTreasurySecuritiesMemberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel1Member2024-12-310001840776us-gaap:USTreasurySecuritiesMemberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel2Member2024-12-310001840776us-gaap:USTreasurySecuritiesMemberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel3Member2024-12-310001840776us-gaap:USStatesAndPoliticalSubdivisionsMemberus-gaap:FairValueMeasurementsRecurringMember2024-12-310001840776us-gaap:USStatesAndPoliticalSubdivisionsMemberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel1Member2024-12-310001840776us-gaap:USStatesAndPoliticalSubdivisionsMemberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel2Member2024-12-310001840776us-gaap:USStatesAndPoliticalSubdivisionsMemberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel3Member2024-12-310001840776us-gaap:ForeignGovernmentDebtSecuritiesMemberus-gaap:FairValueMeasurementsRecurringMember2024-12-310001840776us-gaap:ForeignGovernmentDebtSecuritiesMemberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel1Member2024-12-310001840776us-gaap:ForeignGovernmentDebtSecuritiesMemberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel2Member2024-12-310001840776us-gaap:ForeignGovernmentDebtSecuritiesMemberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel3Member2024-12-310001840776us-gaap:AssetBackedSecuritiesMemberus-gaap:FairValueMeasurementsRecurringMember2024-12-310001840776us-gaap:AssetBackedSecuritiesMemberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel1Member2024-12-310001840776us-gaap:AssetBackedSecuritiesMemberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel2Member2024-12-310001840776us-gaap:AssetBackedSecuritiesMemberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel3Member2024-12-310001840776us-gaap:MortgageBackedSecuritiesMemberus-gaap:FairValueMeasurementsRecurringMember2024-12-310001840776us-gaap:MortgageBackedSecuritiesMemberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel1Member2024-12-310001840776us-gaap:MortgageBackedSecuritiesMemberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel2Member2024-12-310001840776us-gaap:MortgageBackedSecuritiesMemberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel3Member2024-12-310001840776us-gaap:CommonStockMemberus-gaap:FairValueMeasurementsRecurringMember2024-12-310001840776us-gaap:CommonStockMemberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel1Member2024-12-310001840776us-gaap:CommonStockMemberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel2Member2024-12-310001840776us-gaap:CommonStockMemberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel3Member2024-12-310001840776us-gaap:FairValueMeasurementsRecurringMember2024-12-310001840776us-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel1Member2024-12-310001840776us-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel2Member2024-12-310001840776us-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel3Member2024-12-310001840776hgty:BroadArrowGroupIncMember2025-01-012025-12-310001840776hgty:BroadArrowGroupIncMember2025-12-310001840776hgty:BroadArrowGroupIncMember2024-12-310001840776us-gaap:LoansReceivableMember2025-12-310001840776hgty:ConsignorAdvancesReceivableMember2025-12-310001840776us-gaap:CustomerConcentrationRiskMemberus-gaap:FinanceReceivablesMember2025-12-310001840776hgty:OneBorrowMemberus-gaap:CustomerConcentrationRiskMemberus-gaap:FinanceReceivablesMember2025-01-012025-12-310001840776us-gaap:CustomerConcentrationRiskMemberus-gaap:FinanceReceivablesMember2025-01-012025-12-310001840776hgty:ConsolidatedNationalInsuranceCompanyCNICMember2024-09-012024-09-010001840776hgty:MemberHubsHoldingLLCMember2024-09-300001840776hgty:MemberHubsHoldingLLCMemberhgty:HagertyVenturesLLCMember2024-07-012024-09-300001840776hgty:MemberHubsHoldingLLCMember2023-07-012023-09-300001840776hgty:MemberHubsHoldingLLCMember2023-09-290001840776hgty:HagertyDriveShareLLCMember2023-07-012023-09-300001840776hgty:HagertyDriveShareLLCMember2024-04-012024-06-300001840776hgty:ReductionInForceMember2023-01-012023-12-310001840776srt:WeightedAverageMemberus-gaap:ComputerSoftwareIntangibleAssetMember2025-12-310001840776us-gaap:ComputerSoftwareIntangibleAssetMember2025-12-310001840776srt:WeightedAverageMemberus-gaap:CustomerContractsMember2025-12-310001840776us-gaap:CustomerContractsMember2025-12-310001840776srt:WeightedAverageMemberus-gaap:TrademarksAndTradeNamesMember2025-12-310001840776us-gaap:TrademarksAndTradeNamesMember2025-12-310001840776us-gaap:LicensingAgreementsMember2025-12-310001840776srt:WeightedAverageMemberus-gaap:CustomerRelatedIntangibleAssetsMember2025-12-310001840776us-gaap:CustomerRelatedIntangibleAssetsMember2025-12-310001840776srt:WeightedAverageMemberus-gaap:OtherIntangibleAssetsMember2025-12-310001840776us-gaap:OtherIntangibleAssetsMember2025-12-310001840776srt:WeightedAverageMemberus-gaap:ComputerSoftwareIntangibleAssetMember2024-12-310001840776us-gaap:ComputerSoftwareIntangibleAssetMember2024-12-310001840776srt:WeightedAverageMemberus-gaap:CustomerContractsMember2024-12-310001840776us-gaap:CustomerContractsMember2024-12-310001840776srt:WeightedAverageMemberus-gaap:TrademarksAndTradeNamesMember2024-12-310001840776us-gaap:TrademarksAndTradeNamesMember2024-12-310001840776us-gaap:LicensingAgreementsMember2024-12-310001840776srt:WeightedAverageMemberus-gaap:CustomerRelatedIntangibleAssetsMember2024-12-310001840776us-gaap:CustomerRelatedIntangibleAssetsMember2024-12-310001840776srt:WeightedAverageMemberus-gaap:OtherIntangibleAssetsMember2024-12-310001840776us-gaap:OtherIntangibleAssetsMember2024-12-310001840776hgty:HurricaneHeleneMember2025-01-012025-12-310001840776hgty:HurricaneHeleneMember2024-01-012024-12-310001840776hgty:HurricaneMiltonMember2025-01-012025-12-310001840776hgty:HurricaneMiltonMember2024-01-012024-12-310001840776hgty:AutoInsurancePolicyMember2025-12-310001840776hgty:AutoInsurancePolicyMember2024-12-310001840776hgty:MarineInsurancePolicyMember2025-12-310001840776hgty:MarineInsurancePolicyMember2024-12-310001840776hgty:AutoInsurancePolicyMemberus-gaap:ShortDurationInsuranceContractAccidentYear2020Member2021-12-310001840776hgty:AutoInsurancePolicyMemberus-gaap:ShortDurationInsuranceContractAccidentYear2020Member2022-12-310001840776hgty:AutoInsurancePolicyMemberus-gaap:ShortDurationInsuranceContractAccidentYear2020Member2023-12-310001840776hgty:AutoInsurancePolicyMemberus-gaap:ShortDurationInsuranceContractAccidentYear2020Member2024-12-310001840776hgty:AutoInsurancePolicyMemberus-gaap:ShortDurationInsuranceContractAccidentYear2020Member2025-12-310001840776hgty:AutoInsurancePolicyMemberus-gaap:ShortDurationInsuranceContractAccidentYear2021Member2022-12-310001840776hgty:AutoInsurancePolicyMemberus-gaap:ShortDurationInsuranceContractAccidentYear2021Member2023-12-310001840776hgty:AutoInsurancePolicyMemberus-gaap:ShortDurationInsuranceContractAccidentYear2021Member2024-12-310001840776hgty:AutoInsurancePolicyMemberus-gaap:ShortDurationInsuranceContractAccidentYear2021Member2025-12-310001840776hgty:AutoInsurancePolicyMemberus-gaap:ShortDurationInsuranceContractAccidentYear2022Member2023-12-310001840776hgty:AutoInsurancePolicyMemberus-gaap:ShortDurationInsuranceContractAccidentYear2022Member2024-12-310001840776hgty:AutoInsurancePolicyMemberus-gaap:ShortDurationInsuranceContractAccidentYear2022Member2025-12-310001840776hgty:AutoInsurancePolicyMemberus-gaap:ShortDurationInsuranceContractAccidentYear2023Member2024-12-310001840776hgty:AutoInsurancePolicyMemberus-gaap:ShortDurationInsuranceContractAccidentYear2023Member2025-12-310001840776hgty:AutoInsurancePolicyMemberus-gaap:ShortDurationInsuranceContractAccidentYear2024Member2024-12-310001840776hgty:AutoInsurancePolicyMemberus-gaap:ShortDurationInsuranceContractAccidentYear2024Member2025-12-310001840776hgty:VariousReinsurersMember2025-01-012025-12-310001840776us-gaap:HurricaneMember2025-12-310001840776Catastrophe Reinsurance Layer One2025-01-012025-12-310001840776Catastrophe Reinsurance Layer One2025-01-012025-01-310001840776Catastrophe Reinsurance Layer Two2025-01-012025-01-310001840776Catastrophe Reinsurance Layer Two2025-01-012025-12-310001840776hgty:VariousReinsurersMemberCatastrophe Program - High Net Worth2025-01-012025-12-310001840776hgty:EvanstonInsuranceCompanyMemberCatastrophe Program - High Net Worth2025-01-012025-12-310001840776hgty:HagertyReinsuranceLtdMember2025-12-310001840776hgty:HagertyReinsuranceLtdMember2024-12-310001840776hgty:StateFarmTermLoanFacilityMemberhgty:HagertyReinsuranceLtdMemberus-gaap:LineOfCreditMember2025-12-310001840776hgty:HagertyReinsuranceLtdMember2025-01-012025-12-310001840776hgty:HagertyReinsuranceLtdMember2024-01-012024-12-310001840776hgty:HagertyReinsuranceLtdMember2023-01-012023-12-310001840776hgty:DriversEdgeInsuranceLtdMember2025-12-310001840776hgty:DriversEdgeInsuranceLtdMember2024-12-310001840776hgty:DriversEdgeInsuranceLtdMember2025-01-012025-12-310001840776hgty:DriversEdgeInsuranceLtdMember2024-01-012024-12-310001840776us-gaap:RevolvingCreditFacilityMemberhgty:A2025JPMCreditFacilityMemberus-gaap:LineOfCreditMember2025-12-310001840776us-gaap:RevolvingCreditFacilityMemberhgty:A2025JPMCreditFacilityMemberus-gaap:LineOfCreditMember2024-12-310001840776us-gaap:RevolvingCreditFacilityMemberhgty:JPMCreditFacilityMemberus-gaap:LineOfCreditMember2025-12-310001840776us-gaap:RevolvingCreditFacilityMemberhgty:JPMCreditFacilityMemberus-gaap:LineOfCreditMember2024-12-310001840776us-gaap:RevolvingCreditFacilityMemberhgty:BACCreditFacilityMemberus-gaap:LineOfCreditMember2025-12-310001840776us-gaap:RevolvingCreditFacilityMemberhgty:BACCreditFacilityMemberus-gaap:LineOfCreditMember2024-12-310001840776hgty:StateFarmTermLoanFacilityMemberus-gaap:LineOfCreditMember2025-12-310001840776hgty:StateFarmTermLoanFacilityMemberus-gaap:LineOfCreditMember2024-12-310001840776us-gaap:NotesPayableOtherPayablesMember2025-12-310001840776us-gaap:NotesPayableOtherPayablesMember2024-12-310001840776us-gaap:LetterOfCreditMemberhgty:A2025JPMCreditFacilityMemberus-gaap:LineOfCreditMember2025-12-310001840776us-gaap:RevolvingCreditFacilityMemberhgty:A2025JPMCreditFacilityMemberus-gaap:ForeignLineOfCreditMember2025-12-310001840776us-gaap:LetterOfCreditMemberhgty:A2025JPMCreditFacilityMemberus-gaap:ForeignLineOfCreditMember2025-12-310001840776hgty:A2025JPMCreditFacilityMember2025-12-310001840776hgty:A2025JPMCreditFacilityMemberus-gaap:LineOfCreditMember2025-01-012025-12-310001840776us-gaap:RevolvingCreditFacilityMemberhgty:BACCreditFacilityMemberus-gaap:LineOfCreditMember2025-11-030001840776us-gaap:RevolvingCreditFacilityMemberhgty:BACCreditFacilityMemberus-gaap:LineOfCreditMember2025-11-040001840776us-gaap:RevolvingCreditFacilityMemberhgty:BACCreditFacilityMemberus-gaap:LineOfCreditMember2025-01-012025-12-310001840776hgty:StateFarmTermLoanFacilityMemberhgty:HagertyReinsuranceLtdMemberus-gaap:LineOfCreditMember2023-09-300001840776hgty:StateFarmTermLoanFacilityMemberus-gaap:LineOfCreditMember2023-09-300001840776country:GBus-gaap:NotesPayableOtherPayablesMember2024-12-310001840776us-gaap:SeriesAPreferredStockMember2023-06-012023-06-300001840776us-gaap:SeriesAPreferredStockMember2023-06-300001840776hgty:HagertyIncMember2023-12-310001840776us-gaap:SeriesAPreferredStockMember2025-12-310001840776us-gaap:SeriesAPreferredStockMember2025-01-012025-12-310001840776us-gaap:SeriesAPreferredStockMember2024-06-012024-06-300001840776us-gaap:SeriesAPreferredStockMember2025-06-012025-06-300001840776us-gaap:DebtInstrumentRedemptionPeriodOneMemberus-gaap:CommonClassAMember2025-01-012025-12-310001840776us-gaap:DebtInstrumentRedemptionPeriodTwoMemberus-gaap:CommonClassAMember2025-01-012025-12-310001840776us-gaap:SeriesAPreferredStockMemberus-gaap:DebtInstrumentRedemptionPeriodOneMemberhgty:ChangeOfControlMember2025-01-012025-12-310001840776us-gaap:SeriesAPreferredStockMemberus-gaap:DebtInstrumentRedemptionPeriodTwoMemberhgty:ChangeOfControlMember2025-01-012025-12-310001840776us-gaap:SeriesAPreferredStockMemberus-gaap:DebtInstrumentRedemptionPeriodThreeMemberhgty:ChangeOfControlMember2025-01-012025-12-310001840776hgty:FundamentalTransactionMemberus-gaap:SeriesAPreferredStockMember2025-12-310001840776us-gaap:SeriesAPreferredStockMemberus-gaap:DebtInstrumentRedemptionPeriodOneMemberhgty:FundamentalTransactionMember2025-01-012025-12-310001840776us-gaap:SeriesAPreferredStockMemberus-gaap:DebtInstrumentRedemptionPeriodTwoMemberhgty:FundamentalTransactionMember2025-01-012025-12-310001840776us-gaap:SeriesAPreferredStockMemberus-gaap:DebtInstrumentRedemptionPeriodFourMemberhgty:FundamentalTransactionMember2025-01-012025-12-310001840776us-gaap:SeriesAPreferredStockMemberus-gaap:DebtInstrumentRedemptionPeriodFiveMemberhgty:FundamentalTransactionMember2025-01-012025-12-310001840776us-gaap:SeriesAPreferredStockMemberhgty:DebtInstrumentRedemptionPeriodSixMemberhgty:FundamentalTransactionMember2025-01-012025-12-310001840776us-gaap:SeriesAPreferredStockMemberhgty:DebtInstrumentRedemptionPeriodSevenMemberhgty:FundamentalTransactionMember2025-01-012025-12-310001840776us-gaap:SeriesAPreferredStockMemberhgty:DebtInstrumentRedemptionPeriodEightMemberhgty:FundamentalTransactionMember2025-01-012025-12-310001840776us-gaap:SeriesAPreferredStockMemberus-gaap:DebtInstrumentRedemptionPeriodFourMemberhgty:OptionalTermRedemptionMember2025-01-012025-12-310001840776us-gaap:SeriesAPreferredStockMemberus-gaap:DebtInstrumentRedemptionPeriodFiveMemberhgty:OptionalTermRedemptionMember2025-01-012025-12-310001840776us-gaap:SeriesAPreferredStockMemberhgty:DebtInstrumentRedemptionPeriodSixMemberhgty:OptionalTermRedemptionMember2025-01-012025-12-310001840776us-gaap:SeriesAPreferredStockMemberhgty:DebtInstrumentRedemptionPeriodSevenMemberhgty:OptionalTermRedemptionMember2025-01-012025-12-310001840776us-gaap:SeriesAPreferredStockMemberhgty:DebtInstrumentRedemptionPeriodThirteenMemberhgty:OptionalTermRedemptionMember2025-01-012025-12-310001840776us-gaap:SeriesAPreferredStockMemberhgty:DebtInstrumentRedemptionPeriodFourteenMemberhgty:OptionalTermRedemptionMember2025-01-012025-12-310001840776hgty:CommonClassVMember2025-01-012025-12-310001840776us-gaap:ConvertiblePreferredStockMember2025-12-310001840776us-gaap:SeriesAPreferredStockMember2024-12-310001840776hgty:TheHagertyGroupLLCMemberus-gaap:CommonClassAMember2024-12-310001840776hgty:TheHagertyGroupLLCMemberus-gaap:CommonClassAMember2023-12-310001840776hgty:TheHagertyGroupLLCMemberus-gaap:CommonClassAMember2025-01-012025-12-310001840776hgty:TheHagertyGroupLLCMemberus-gaap:CommonClassAMember2024-01-012024-12-310001840776hgty:TheHagertyGroupLLCMemberus-gaap:CommonClassAMember2025-12-310001840776hgty:TheHagertyGroupLLCMember2024-12-310001840776hgty:TheHagertyGroupLLCMember2023-12-310001840776hgty:TheHagertyGroupLLCMember2025-12-310001840776hgty:OtherUnitHoldersMember2024-12-310001840776hgty:OtherUnitHoldersMember2023-12-310001840776hgty:OtherUnitHoldersMemberus-gaap:CommonClassAMember2025-01-012025-12-310001840776hgty:OtherUnitHoldersMemberus-gaap:CommonClassAMember2024-01-012024-12-310001840776hgty:OtherUnitHoldersMember2025-12-310001840776hgty:A2021StockIncentivePlanMemberus-gaap:CommonClassAMember2025-01-012025-12-310001840776hgty:A2021StockIncentivePlanMemberus-gaap:CommonClassAMember2024-01-012024-12-310001840776hgty:A2021EmployeeStockPurchasePlanMemberus-gaap:CommonClassAMember2025-01-012025-12-310001840776hgty:A2021EmployeeStockPurchasePlanMemberus-gaap:CommonClassAMember2024-01-012024-12-310001840776hgty:CommonClassVMember2025-07-012025-09-300001840776us-gaap:CommonClassAMember2025-07-012025-09-300001840776hgty:CommonClassVMember2024-01-012024-12-310001840776hgty:THGUnitExchangeMember2025-01-012025-12-310001840776hgty:THGLLCMember2024-06-012024-06-300001840776hgty:THGLLCMember2025-06-012025-06-300001840776hgty:THGLLCMember2025-01-012025-12-310001840776hgty:THGLLCMember2024-01-012024-12-310001840776hgty:HagertyIncMemberhgty:THGLLCMember2025-01-012025-12-310001840776hgty:HagertyIncMemberhgty:THGLLCMember2024-01-012024-12-310001840776hgty:A2021StockIncentivePlanMemberus-gaap:CommonClassAMember2021-12-310001840776hgty:A2021StockIncentivePlanMember2025-12-310001840776us-gaap:RestrictedStockUnitsRSUMember2025-01-012025-12-310001840776us-gaap:RestrictedStockUnitsRSUMember2024-01-012024-12-310001840776us-gaap:RestrictedStockUnitsRSUMember2023-01-012023-12-310001840776us-gaap:PerformanceSharesMember2025-01-012025-12-310001840776us-gaap:PerformanceSharesMember2024-01-012024-12-310001840776us-gaap:PerformanceSharesMember2023-01-012023-12-310001840776hgty:EmployeeStockPurchasePlanMember2025-01-012025-12-310001840776hgty:EmployeeStockPurchasePlanMember2024-01-012024-12-310001840776hgty:EmployeeStockPurchasePlanMember2023-01-012023-12-310001840776srt:MinimumMemberus-gaap:EmployeeStockOptionMember2025-01-012025-12-310001840776srt:MaximumMemberus-gaap:EmployeeStockOptionMember2025-01-012025-12-310001840776us-gaap:RestrictedStockUnitsRSUMember2024-12-310001840776us-gaap:RestrictedStockUnitsRSUMember2025-12-310001840776us-gaap:RestrictedStockUnitsRSUMemberus-gaap:CommonClassAMember2025-01-012025-12-310001840776hgty:MarketConditionPerformanceSharesMember2022-04-012022-04-300001840776hgty:MarketConditionPerformanceSharesMemberus-gaap:ShareBasedCompensationAwardTrancheOneMember2022-04-012022-04-300001840776hgty:MarketConditionPerformanceSharesMemberus-gaap:ShareBasedCompensationAwardTrancheOneMember2022-04-300001840776hgty:MarketConditionPerformanceSharesMemberus-gaap:ShareBasedCompensationAwardTrancheTwoMember2022-04-012022-04-300001840776hgty:MarketConditionPerformanceSharesMemberus-gaap:ShareBasedCompensationAwardTrancheTwoMember2022-04-300001840776hgty:MarketConditionPerformanceSharesMemberus-gaap:ShareBasedCompensationAwardTrancheThreeMember2022-04-012022-04-300001840776hgty:MarketConditionPerformanceSharesMemberus-gaap:ShareBasedCompensationAwardTrancheThreeMember2022-04-300001840776srt:MinimumMemberhgty:MarketConditionPerformanceSharesMember2022-04-012022-04-300001840776srt:MaximumMemberhgty:MarketConditionPerformanceSharesMember2022-04-012022-04-300001840776hgty:MarketConditionPerformanceSharesMember2025-01-012025-12-310001840776hgty:MarketConditionPerformanceSharesMember2025-12-310001840776hgty:PerformanceConditionPerformanceSharesMembersrt:MinimumMemberhgty:A2024PerformanceRestrictedStockUnitAgreementMember2024-03-310001840776hgty:PerformanceConditionPerformanceSharesMembersrt:MaximumMemberhgty:A2024PerformanceRestrictedStockUnitAgreementMember2024-03-310001840776hgty:PerformanceConditionPerformanceSharesMember2024-12-310001840776hgty:PerformanceConditionPerformanceSharesMember2025-01-012025-12-310001840776hgty:PerformanceConditionPerformanceSharesMember2025-12-310001840776hgty:A2024PerformanceRestrictedStockUnitAgreementMemberus-gaap:CommonClassAMember2025-01-012025-12-310001840776hgty:PerformanceConditionPerformanceSharesMember2024-01-012024-12-310001840776us-gaap:CommonClassAMemberhgty:EmployeeStockPurchasePlanMember2025-01-012025-12-310001840776us-gaap:CommonClassAMemberhgty:EmployeeStockPurchasePlanMember2025-12-310001840776hgty:HagertyGroupUnitsMember2025-01-012025-12-310001840776hgty:HagertyGroupUnitsMember2024-01-012024-12-310001840776hgty:HagertyGroupUnitsMember2023-01-012023-12-310001840776us-gaap:SeriesAPreferredStockMember2025-01-012025-12-310001840776us-gaap:SeriesAPreferredStockMember2024-01-012024-12-310001840776us-gaap:SeriesAPreferredStockMember2023-01-012023-12-310001840776us-gaap:StockCompensationPlanMember2025-01-012025-12-310001840776us-gaap:StockCompensationPlanMember2024-01-012024-12-310001840776us-gaap:StockCompensationPlanMember2023-01-012023-12-310001840776us-gaap:WarrantMember2025-01-012025-12-310001840776us-gaap:WarrantMember2024-01-012024-12-310001840776us-gaap:WarrantMember2023-01-012023-12-310001840776country:BM2025-01-012025-12-310001840776country:CA2025-01-012025-12-310001840776country:GB2025-01-012025-12-310001840776us-gaap:ForeignTaxJurisdictionOtherMember2025-01-012025-12-310001840776hgty:THGUnitExchangeMember2025-12-310001840776hgty:THGUnitExchangeMember2024-12-310001840776us-gaap:DomesticCountryMember2025-12-310001840776us-gaap:StateAndLocalJurisdictionMember2025-12-310001840776us-gaap:StateAndLocalJurisdictionMemberhgty:IndefiniteMember2025-12-310001840776us-gaap:StateAndLocalJurisdictionMemberhgty:TaxYear2026Through2045Member2025-12-310001840776us-gaap:ForeignCountryMember2025-12-310001840776us-gaap:ForeignCountryMemberhgty:IndefiniteMember2025-12-310001840776us-gaap:ForeignCountryMemberhgty:TaxYear2036Through2044Member2025-12-310001840776us-gaap:DomesticCountryMemberhgty:TaxYear2044Through2045Memberus-gaap:ResearchMember2025-12-3100018407762025-07-012025-09-300001840776hgty:THGUnitExchangeMember2025-07-012025-09-300001840776hgty:THGUnitExchangeMember2024-01-012024-12-3100018407762024-10-012024-12-310001840776hgty:HagertyIncMemberus-gaap:CommonClassAMembersrt:AffiliatedEntityMemberhgty:MarkelMember2025-12-310001840776hgty:HagertyIncMemberus-gaap:CommonClassAMembersrt:AffiliatedEntityMemberhgty:StateFarmMember2025-12-310001840776hgty:HagertyIncMemberhgty:CommonClassVMembersrt:AffiliatedEntityMemberhgty:MarkelMember2025-12-310001840776hgty:HagertyIncMemberhgty:CommonClassVMembersrt:AffiliatedEntityMemberhgty:StateFarmMember2025-12-310001840776hgty:HagertyIncMemberus-gaap:SeriesAPreferredStockMembersrt:AffiliatedEntityMemberhgty:MarkelMember2025-12-310001840776hgty:HagertyIncMemberus-gaap:SeriesAPreferredStockMembersrt:AffiliatedEntityMemberhgty:StateFarmMember2025-12-310001840776hgty:HagertyIncMembersrt:AffiliatedEntityMemberhgty:MarkelMemberhgty:HagertyGroupUnitsMember2025-12-310001840776hgty:HagertyIncMembersrt:AffiliatedEntityMemberhgty:StateFarmMemberhgty:HagertyGroupUnitsMember2025-12-310001840776hgty:HagertyIncMembersrt:AffiliatedEntityMemberhgty:MarkelMemberus-gaap:ParentMember2025-12-310001840776hgty:HagertyIncMembersrt:AffiliatedEntityMemberhgty:StateFarmMemberus-gaap:ParentMember2025-12-310001840776hgty:HagertyIncMembersrt:AffiliatedEntityMemberhgty:MarkelMember2025-12-310001840776hgty:HagertyIncMembersrt:AffiliatedEntityMemberhgty:StateFarmMember2025-12-310001840776srt:AffiliatedEntityMemberhgty:MarkelMemberhgty:AllianceAgreementMember2025-01-012025-12-310001840776srt:AffiliatedEntityMemberhgty:MarkelMemberhgty:AllianceAgreementMember2024-01-012024-12-310001840776srt:AffiliatedEntityMemberhgty:MarkelMemberhgty:AllianceAgreementMember2023-01-012023-12-310001840776srt:AffiliatedEntityMemberhgty:MarkelMemberhgty:RelatedPartyConcentrationRiskMemberus-gaap:RevenueFromContractWithCustomerMemberhgty:AllianceAgreementMember2025-01-012025-12-310001840776srt:AffiliatedEntityMemberhgty:MarkelMemberhgty:RelatedPartyConcentrationRiskMemberus-gaap:RevenueFromContractWithCustomerMemberhgty:AllianceAgreementMember2024-01-012024-12-310001840776srt:AffiliatedEntityMemberhgty:MarkelMemberhgty:RelatedPartyConcentrationRiskMemberus-gaap:RevenueFromContractWithCustomerMemberhgty:AllianceAgreementMember2023-01-012023-12-310001840776srt:AffiliatedEntityMemberhgty:MarkelMemberhgty:AllianceAgreementMember2025-12-310001840776srt:AffiliatedEntityMemberhgty:MarkelMemberhgty:AllianceAgreementMember2024-12-310001840776srt:AffiliatedEntityMemberhgty:MarkelMemberhgty:RelatedPartyConcentrationRiskMemberhgty:DueToRelatedPartiesMemberhgty:AllianceAgreementMember2025-01-012025-12-310001840776srt:AffiliatedEntityMemberhgty:MarkelMemberhgty:RelatedPartyConcentrationRiskMemberhgty:DueToRelatedPartiesMemberhgty:AllianceAgreementMember2024-01-012024-12-310001840776hgty:ReinsuranceAgreementMembersrt:AffiliatedEntityMember2025-01-012025-12-310001840776hgty:ReinsuranceAgreementMembersrt:AffiliatedEntityMember2023-01-012023-01-010001840776srt:AffiliatedEntityMemberhgty:MarkelMemberhgty:ReinsuranceAgreementMember2025-01-012025-12-310001840776srt:AffiliatedEntityMemberhgty:MarkelMemberhgty:ReinsuranceAgreementMember2024-01-012024-12-310001840776srt:AffiliatedEntityMemberhgty:MarkelMemberhgty:ReinsuranceAgreementMember2023-01-012023-12-310001840776srt:AffiliatedEntityMemberhgty:MarkelMemberhgty:ReinsuranceAgreementMember2025-12-310001840776srt:AffiliatedEntityMemberhgty:MarkelMemberhgty:ReinsuranceAgreementMember2024-12-310001840776srt:AffiliatedEntityMemberhgty:EvanstonMemberhgty:ReinsuranceAgreementMember2025-12-310001840776srt:AffiliatedEntityMemberhgty:EvanstonMemberhgty:ReinsuranceAgreementMember2024-12-310001840776srt:AffiliatedEntityMemberhgty:StateFarmMemberhgty:AllianceAgreementMember2025-01-012025-12-310001840776srt:AffiliatedEntityMemberhgty:StateFarmMemberhgty:AllianceAgreementMember2025-12-310001840776srt:AffiliatedEntityMemberhgty:StateFarmMemberhgty:ReinsuranceAgreementMember2025-01-012025-12-310001840776srt:AffiliatedEntityMemberhgty:StateFarmMemberhgty:ReinsuranceAgreementMember2024-01-012024-12-310001840776srt:AffiliatedEntityMemberhgty:StateFarmMemberhgty:ReinsuranceAgreementMember2023-01-012023-12-310001840776srt:AffiliatedEntityMemberhgty:StateFarmMemberhgty:ReinsuranceAgreementMember2025-12-310001840776srt:AffiliatedEntityMemberhgty:StateFarmMemberhgty:ReinsuranceAgreementMember2024-12-310001840776hgty:NewYorkDepartmentOfFinancialServicesMember2025-10-012025-10-310001840776hgty:NewYorkAttorneyGeneralMember2025-10-012025-10-310001840776srt:ParentCompanyMember2025-01-012025-12-310001840776srt:ParentCompanyMember2024-01-012024-12-310001840776srt:ParentCompanyMember2023-01-012023-12-310001840776srt:ParentCompanyMember2025-12-310001840776srt:ParentCompanyMember2024-12-310001840776us-gaap:CommonClassAMembersrt:ParentCompanyMember2025-12-310001840776us-gaap:CommonClassAMembersrt:ParentCompanyMember2024-12-310001840776hgty:CommonClassVMembersrt:ParentCompanyMember2025-12-310001840776hgty:CommonClassVMembersrt:ParentCompanyMember2024-12-310001840776srt:ParentCompanyMember2023-12-310001840776srt:ParentCompanyMember2022-12-310001840776stpr:CAsrt:ParentCompanyMember2025-01-012025-12-310001840776stpr:GAsrt:ParentCompanyMember2025-01-012025-12-310001840776stpr:NYsrt:ParentCompanyMember2025-01-012025-12-310001840776us-gaap:ValuationAllowanceOfDeferredTaxAssetsMember2024-12-310001840776us-gaap:ValuationAllowanceOfDeferredTaxAssetsMember2025-01-012025-12-310001840776us-gaap:ValuationAllowanceOfDeferredTaxAssetsMember2025-12-310001840776us-gaap:ValuationAllowanceOfDeferredTaxAssetsMember2023-12-310001840776us-gaap:ValuationAllowanceOfDeferredTaxAssetsMember2024-01-012024-12-310001840776us-gaap:ValuationAllowanceOfDeferredTaxAssetsMember2022-12-310001840776us-gaap:ValuationAllowanceOfDeferredTaxAssetsMember2023-01-012023-12-310001840776hgty:LaurieHarrisMember2025-10-012025-12-310001840776hgty:LaurieHarrisMember2025-12-3100018407762025-10-012025-12-31

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 2025

OR

☐

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from ________ to _______

Commission file number: 001-40244

HAGERTY, INC.

(Exact name of registrant as specified in its charter)

Delaware

86-1213144

(State of incorporation)

(I.R.S. Employer Identification No.)

121 Drivers Edge, Traverse City, Michigan

49684

(Address of principal executive offices)

(Zip code)

(800)922-4050

Registrant's telephone number, including area code

Securities registered pursuant to Section 12(b) of the Act:

Title of each class

Trading Symbols

Name of each exchange on which registered

Class A common stock, par value $0.0001 per share

HGTY

The New York Stock Exchange

Securities registered pursuant to section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐ No☒

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☐No☒

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports); and (2) has been subject to such filing requirements for the past 90 days. Yes☒ No ☐

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes☒ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company, or an emerging growth company. See the definitions of "large accelerated filer," "accelerated filer," "smaller reporting company," and "emerging growth company" in Rule 12b-2 of the Exchange Act.

Large accelerated filer

☐

Accelerated filer

☒

Non-accelerated filer

☐

Smaller reporting company

☐

Emerging growth company

☐

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant has filed a report on and attestation to its management's assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☒

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. ☐

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant's executive officers during the relevant recovery period pursuant to §240.10D-1(b) ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ☐ No ☒

The aggregate market value of voting stock held by non-affiliates of the Registrant on June 30, 2025, based on the closing price of $10.11 for shares of the Registrant’s Class A Common Stock as reported by the New York Stock Exchange, was approximately $309.9 million. Shares of common stock beneficially owned by each executive officer, director, and holders of more than 10% of our common stock have been excluded in that such persons may be deemed to be affiliates. This determination of affiliate status is not necessarily a conclusive determination for other purposes.

The registrant had 101,066,533 shares of Class A Common Stock outstanding and 241,552,156 shares of Class V Common Stock outstanding as of February 20, 2026.

Documents incorporated by reference:

Portions of the registrant's definitive Proxy Statement for its 2026 Annual Meeting of Stockholders, which will be filed with the Securities and Exchange Commission within 120 days of December 31, 2025, are incorporated by reference into Part III, Items 10-14 of this Annual Report on Form 10-K.

Our Annual Reports on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K, as well as any amendments to those reports, are available free of charge through our website at investor.hagerty.com after we file them with, or furnish them to, the Securities and Exchange Commission ("SEC"). We use our investor relations website, investor.hagerty.com, as a means of disclosing information which may be of interest or material to our investors and for complying with disclosure obligations under Regulation FD. Accordingly, investors should monitor our investor relations website, in addition to following our press releases, SEC filings, public conference calls, webcasts, and social media channels. Information contained on or accessible through our website or social media channels is not a part of, and is not incorporated by reference into, this Annual Report on Form 10-K (this "Annual Report") or any other report or document we file with the SEC. Any reference to our website in this Annual Report is intended to be an inactive textual reference only.

Unless the context indicates otherwise, the terms "we," "our," "us," "Hagerty," and the "Company" refer to Hagerty, Inc. and its consolidated subsidiaries, including The Hagerty Group, LLC ("THG").

This Annual Report, as well as other oral or written information we provide, contain statements that constitute "forward-looking statements" within the meaning of the federal securities laws. All statements we provide, other than statements of historical fact, are forward-looking statements, including those regarding our future operating results and financial position, our business strategy and plans, products, services, and technology implementations, market conditions, growth and trends, expansion plans and opportunities, and our objectives for future operations. The words "anticipate," "believe," "envision," "estimate," "expect," "intend," "may," "plan," "predict," "project," "target," "potential," "will," "would," "could," "should," "continue," "ongoing," "contemplate," and similar expressions, and the negative of these expressions, are intended to identify forward-looking statements.

We have based these forward-looking statements largely on our current expectations about future events, which may not materialize. Actual results could differ materially and adversely from those anticipated or implied in our forward-looking statements. Some of the factors that could cause actual results to differ from our expectations include the risks and uncertainties described in Item 1A of Part I — Risk Factors of this Annual Report, which highlight, among other risks, our ability to:

•compete effectively within our industry and attract and retain our insurance policyholders and paid Hagerty Drivers Club subscribers (collectively, "Members");

•maintain key strategic relationships with our insurance distribution and underwriting carrier partners;

•prevent, monitor, and detect fraudulent activity;

•manage risks associated with disruptions, interruptions, outages or other issues with our technology platforms or our use of third-party services;

•accelerate the adoption of our membership and marketplace products and services, as well as any new insurance programs and products we offer;

•successfully implement the fronting arrangement consummated with Markel Group Inc. (together with its subsidiaries, "Markel") and realize the anticipated benefits while also managing the increased exposure to underwriting volatility, catastrophes, reinsurance counterparty risk, and legal, compliance, and regulatory risks resulting from the shift to our wholly owned subsidiary, Hagerty Reinsurance Limited ("Hagerty Re"), assuming 100% of the risk for policies written through this arrangement;

•underwrite and price new products, including Enthusiast+, consistent with expected loss ratios and risk tolerances;

•execute Broad Arrow Group, Inc.'s ("Broad Arrow") private sale, auction, and financing strategies;

•manage the cyclical nature of the insurance business and broader macroeconomic conditions, including inflation, interest rates, and potential recessionary pressures;

•achieve our investment objectives and avoid losses in our investment portfolio;

•address unexpected increases in the frequency or severity of claims, including catastrophe losses; and

•comply with the numerous laws and regulations applicable to our business, including without limitation state, federal, and foreign laws relating to insurance and rate increases, privacy and cybersecurity, marketing and advertising, digital services, accounting matters, tax, anti-money laundering, and economic sanctions.

You should not rely on forward-looking statements as predictions of future events. We operate in a very competitive and rapidly changing environment and new risks emerge from time to time. The forward-looking statements in this Annual Report represent our views as of the date hereof. We undertake no obligation to update any of these forward-looking statements for any reason after the date of this Annual Report.

We are a market leader in providing insurance for collector cars and enthusiast vehicles, helping the automotive enthusiast community protect and enjoy their special cars for more than 40 years. Our insurance products are complemented by our membership product, Hagerty Drivers Club ("HDC"), our renowned car events, and our media and entertainment platforms. We also operate a trusted marketplace where collectors and enthusiasts can buy and sell a wide range of vehicles, from entry level enthusiast vehicles to high value collector cars. Together, our integrated automotive ecosystem fosters a vibrant community where enthusiasts connect, share their passion, and access resources that enhance their ownership experience. Our vision is to be the world's most trusted and preferred brand for automotive enthusiasts to insure, buy, sell, and enjoy their special cars.

Beginning with this Annual Report, we present our Consolidated Financial Statements in accordance with Article 7 of Regulation S-X, reflecting the continued expansion of our insurance operations, including expanded risk assumption under the Markel Fronting Arrangement and the introduction of Enthusiast+, as discussed under "Markel Alliance" and "Drivers Edge Insurance Company"below. In addition, we now operate our business and report our financial performance using two segments: Insurance and Marketplace. Our segments provide management with a comprehensive financial view of our key businesses, as well as a framework for timely and rational allocation of resources.

Refer to "Transition to Article 7 Reporting Framework" in Item 7 of Part II of this Annual Report and Note 2 — Summary of Significant Accounting Policies in Item 8 of Part II of this Annual Report for additional information on the transition to Article 7 reporting.

Refer to Note 4 — Segment Reporting and Disaggregated Revenue in Item 8 of Part II of this Annual Report for additional information regarding segment reporting.

The first Hagerty company was founded in 1984. Hagerty, Inc., a Delaware corporation, was formed in 2020 and became a public company traded on the New York Stock Exchange ("NYSE") in 2021 under the ticker symbol HGTY.

Business Model and Competitive Strengths

The Hagerty brand has been carefully curated over the last four decades by providing Members with excellent customer service through our passionate team of automotive experts. We have become known as an automotive enthusiast brand built by drivers, for drivers. We believe that consumers who feel a part of an enthusiast community or club are more engaged and have higher renewal rates than those who simply purchase a good or service. With an insurance policy retention rate of nearly 90% and an average policy life of nine years, we have demonstrated a strong recurring revenue model that benefits from a combination of high insurance policy retention, new Member growth, and increases in premiums driven, in part, by the increasing values of insured vehicles over the long term.

Our connection to the automotive enthusiast community is complemented by HDC, our renowned car events, and our media and entertainment platforms, which generate positive ongoing engagement with current Members, as well as interest in our brand, products, and services from prospective members. The enthusiast community also benefits from the synergies of our trusted marketplace where we leverage our brand, relationships, and expertise to provide collectors and enthusiasts a seamless way to buy and sell a wide range of vehicles, from entry level enthusiast vehicles to high value collector cars.

Typical insurance businesses engage with their customers only a few times a year, but our diverse offerings result in numerous touchpoints with Members throughout the year. In addition, our media content features the work of talented automotive content creators, journalists, and storytellers who bring the automotive world to life in exciting and unexpected ways across a variety of digital, print, and video media formats. Our media team covers entertainment, news, market information, and vehicle valuation trends, all of which help generate an engaged audience that drives retention and attracts new Members. We believe our leading Net Promoter Score ("NPS")1 and strong retention rates reflect the effectiveness of our enthusiast ecosystem and that our business model is a significant advantage over competitors who, without strong affinity or engagement, are left to compete solely on price.

1NPS is a barometer of brand loyalty and engagement, supporting Member growth and policy retention. NPS is measured twice annually through a web-based survey sent by email invitation to a random sample of existing Members, which currently excludes customers in our Marketplace segment, and is reported annually using an average of the two surveys.

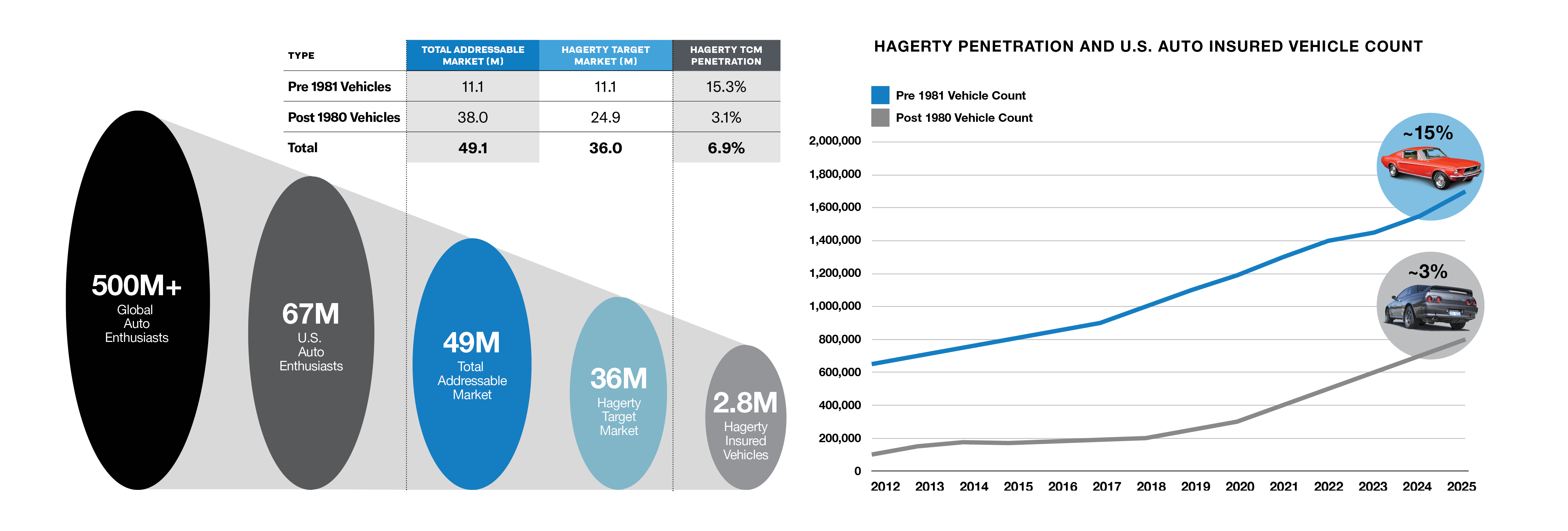

We have established ourselves as one of the leading providers of collector car and enthusiast vehicle insurance with an overall market share of approximately 7% within the United States ("U.S.") collector car and enthusiast vehicle market of 36 million vehicles. This includes an estimated market share of approximately 15% for pre-1981 classic vehicles in the U.S. and an estimated U.S. market share for post-1980 collectible vehicles of 3%. On this basis, we estimate that our U.S. target market of collector cars and enthusiast vehicles represents approximately $15 billion of annual written premium based on our average vehicle premium of $423 per year. Over the last decade, we have increased our written premium by a compound annual growth rate of 14%, powered primarily by strong growth in the number of our insurance policies in force.

We believe that our strong brand and value proposition position us well to capture a larger share of this growing market over the coming decade, including through our recent acquisition of Drivers Edge Insurance Company ("Drivers Edge"). For more information regarding Drivers Edge, refer to "Insurance and Reinsurance — Drivers Edge Insurance Company" below.

In order to fully capitalize on this opportunity, we perform a data-driven Member and vehicle analysis to understand vehicle ownership data, demographic data, vehicle usage, and values. Based upon this analysis, we are able to identify key vehicle markets, explore additional opportunities within these markets, and overlay demographic and usage data to enrich our approach and leverage the information to better serve the automotive enthusiast community.

Insurance Segment

We operate as a Managing General Agent ("MGA") by underwriting, selling, and servicing collector car and enthusiast vehicle insurance policies on behalf of our insurance carrier partners. Due to our consistent track record of delivering strong underwriting results, we then reinsure a significant portion of the risks written by our MGA subsidiaries through Hagerty Re. Hagerty Re reinsures risks predominantly from policies issued by Essentia Insurance Company ("Essentia"), a wholly owned subsidiary of Markel. Hagerty Re's quota share percentage for the risks that is assumes from Essentia has ranged from 25% at the program's inception to 80% as of December 31, 2025, and increased to 100% in 2026 as discussed under "Markel Alliance" below.

Our insurance offerings are centered around our "Guaranteed Value" insurance policy, which differentiates our coverage from the standard auto insurance market by insuring covered vehicles at their agreed upon value, rather than their depreciated value. We work closely with our Members to determine the right amount of coverage for their vehicle, utilizing Hagerty Valuation Tools, which has been built over decades of collecting vehicle sales information, to accurately assess the risk associated with insuring collector cars and enthusiast vehicles.

For over 40 years, we have consistently grown our insurance business and, as of December 31, 2025, 2.8 million collector cars and enthusiast vehicles were covered by our insurance policies. We have built a strong reputation for providing excellent customer service through our passionate team of member service center professionals, resulting in an NPS of approximately 81 in recent years, an insurance policy retention rate approaching 90%, and a typical policy life of approximately nine years.

For the years ended December 31, 2025, 2024, and 2023, Insurance segment revenue represented 92%, 96% and 97%, respectively, of our total revenue.

Operating as an MGA allows us to offer our insurance products through an omnichannel distribution model, enabling us to sell our insurance wherever our policyholders need us. This omnichannel approach allows us to offer our insurance products across two channels: (i) directly to consumers; and (ii) through our agent channel, which includes a vast network of independent agents and brokers, as well as strategic distribution partnerships with large traditional auto insurers. We believe that this distribution model creates a win-win situation that allows us to capture more of the collector car and enthusiast vehicle insurance market. In connection with the servicing of insurance policies, we also handle claims on behalf of our insurance carrier partners to ensure that our Members receive a high level of service focused on the unique requirements of repairing vintage and rare vehicles.

When operating as an MGA, we earn commission and fee revenue primarily from the underwriting, sale, and servicing of collector car and enthusiast vehicle insurance policies written on behalf of insurance carriers. For the years ended December 31, 2025, 2024, and 2023, commission and fee revenue earned by our MGA subsidiaries represented 33%, 34%, and 36%, respectively, of our total revenue.

Direct Sales Channel

Our direct sales channel is serviced by our employee agents who sell policies in the U.S., Canada, and the United Kingdom ("U.K."). For the year ended December 31, 2025, approximately 44% of our total auto written premium was generated through direct sales.

Agent Channel

We market our insurance products through our insurance distribution partnerships, which include 9 of the top 10 largest auto insurers, as ranked by the National Association of Insurance Commissioners based upon 2024 direct premiums written. Under these arrangements, we generally make our specialty insurance products and related services available to the insurers' agents, who then refer or present Hagerty to their customers. Our track record of expertise and growth creates opportunities for cultivating strong, mutually beneficial distribution partnerships that allow us to continue to meaningfully grow our share of the collector car and enthusiast vehicle market in the U.S.

Most insurance companies offer and compete for multi-line insurance: auto, homeowners, umbrella, watercraft, aircraft, and other exclusive collectibles. Our focus on collector car and enthusiast vehicle products reduces competitive threats for partners and raises their confidence in transacting with us. Furthermore, we focus on developing capabilities that serve the interests of the automotive enthusiast market. This depth and discipline of focus has enabled us to maintain a "neutral" and non-threatening partner of choice position with the highest quality automobile insurance companies in the market as we help them reduce the risk of losing a customer and the total value of the bundled insurance and membership offerings.

Our approach to distribution partnerships enables complementary growth. Our business model is attractive to our partners because we offer a full-service solution for their customers and their special cars. Our focus on the collector car and enthusiast vehicle space allows our distribution partners to focus on other parts of their business portfolios and because our financial interests are aligned, both parties benefit from the relationship. We do well when our partners win and grow, and we take great care to build partnerships with companies who share our focus on excellent customer service. As a result of these partnerships, both brands benefit symbiotically through longer-lasting and more intimate customer relationships.

We also have relationships with over 54,000 independent agents and brokers, representing all top 10 brokers in the U.S. by revenue. Our high-engagement and experiential approach to the market is often co-branded by independent agents and brokers to deliver automotive enthusiasts an experience the agent or broker could not deliver themselves.

For the year ended December 31, 2025, approximately 56% of our total U.S. auto written premium was generated through our agent channel.

Insurance and Reinsurance

Hagerty Re

Hagerty Re's primary function is to reinsure a significant portion of the risk underwritten by our MGA subsidiaries, allowing us to retain and manage risk on our balance sheet, efficiently deploy capital, and participate directly in the underwriting profit generated by our MGA operations.

Hagerty Re reinsures risks predominantly from policies issued by Essentia. Hagerty Re's quota share percentage for the risks that it assumes from Essentia has ranged from 25% at the program's inception to 80% as of December 31, 2025, and increased to 100% in 2026 as discussed under "Markel Alliance" below.

Our risk management philosophy is rooted in actuarial discipline and a deliberate approach to underwriting. Through our MGA subsidiaries, we leverage proprietary data analytics, rigorous pricing models, and ongoing reserve analysis to ensure prudent risk selection and loss reserving. Over the last three years, Hagerty Re has achieved an average loss ratio of 42%, which is significantly better than the overall auto insurance industry average of approximately 74%, excluding loss adjustment expenses. This performance underscores our ability to deliver consistent, profitable underwriting results and highlights the effectiveness of our risk management framework.

Hagerty Re purchases catastrophe reinsurance to manage risk exposure and protect its capital from large catastrophic events, and facultative reinsurance to cede a portion of the physical damage exposure related to certain high value vehicles. In addition, Hagerty Re cedes 100% of its physical damage exposure on U.S. policies written or renewed with total insured values ("TIV") equal to or greater than $5.0 million ("High-Net-Worth Accounts") via quota share agreements with various reinsurers. These High-Net-Worth Accounts are assumed 100% from Essentia. Certain reinsurers involved in these quota share agreements are related parties. Refer to Note 16 — Reinsurance and Note 24 — Related-Party Transactions in Item 8 of Part II of this Annual Report for additional information.

Hagerty Re is a registered Class 3A reinsurer under the Bermuda Insurance Act of 1978 and is subject to comprehensive regulatory oversight by the Bermuda Monetary Authority ("BMA"). Under its license, Hagerty Re is only permitted to accept business underwritten by our MGA subsidiaries on behalf of our insurance carrier partners. The BMA requires Hagerty Re to maintain minimum capital and surplus levels, comply with solvency and liquidity ratios, adhere to restrictions on dividends and investment activities, and satisfy reporting obligations. In addition, Hagerty Re's reinsurance arrangements are structured to ensure that all counterparties meet stringent credit quality standards, further reinforcing the financial strength and stability of our insurance platform.

For the years ended December 31, 2025, 2024, and 2023, Hagerty Re earned premium represented 50%, 52%, and 52%, respectively, of our total revenue.

Drivers Edge Insurance Company

In September 2024, we acquired all the issued and outstanding capital stock of Consolidated National Insurance Company ("CNIC"), which was a shell insurance company holding certain state licenses. CNIC was subsequently renamed Drivers Edge Insurance Company. In the third quarter of 2025, Drivers Edge launched Enthusiast+ in Colorado, which is a new insurance product tailored for modern enthusiast vehicles that are typically driven more frequently and stored more flexibly than traditional collector cars. This product evolved from our growing exposure to modern enthusiast vehicles and is designed to broaden our addressable market by offering coverage to a wider range of vehicles and customer profiles. The entirety of the risk underwritten by our U.S. MGA subsidiary on behalf of Drivers Edge is ceded to Hagerty Re.

We expect Enthusiast+ policies to command higher premiums and, given the distinct risk characteristics of the targeted vehicles and customer segments, have higher loss ratios relative to our traditional insurance offerings. Enthusiast+ features differentiated pricing and advanced coverage options, representing a strategic evolution in our risk profile and business model.

We plan to implement a phased, nationwide rollout of Enthusiast+ over the next four years. We believe that Enthusiast+ will generate attractive returns for us, widen our funnel of insurable vehicles, and contribute to the long-term growth and diversification of our insurance portfolio.

HDC, Events and Media

Our Insurance segment also offers HDC memberships, which are bundled with our insurance policies and provide Members with access to an array of products and services, including emergency roadside assistance, Hagerty Drivers Club Magazine, special access to automotive enthusiast events, our proprietary vehicle valuation tool, and special vehicle-related discounts. Lastly, our Insurance segment includes related ancillary activities such as our events and media and entertainment platforms, which support brand awareness and sales of our insurance policies through their distribution and high rates of pass-along circulation.

We are party to an alliance agreement (the "Markel Alliance Agreement") and associated agency and claims services agreements with Markel, which govern our long-standing business relationship related to marketing, underwriting, and administration of personal automobile insurance for collector cars and enthusiast vehicles in the U.S. Under this arrangement, our U.S. MGA subsidiary is licensed and authorized to develop insurance products, underwrite, bill, and perform claims services for policies written through Essentia. Essentia is exclusive to our U.S. MGA subsidiary and only writes insurance policies we produce. State laws govern many of the activities under this relationship and our MGA subsidiary must maintain the appropriate licensing as a producer and, where required, as an MGA, plus additional requirements in some states for claims adjusting. In 2025 and 2024, our U.S. MGA subsidiary earned a base commission rate of approximately 37%, as well as an additional contingent underwriting commission ("CUC") that scaled annually from -5% to a maximum of +5% of written premium.

On December 31, 2025, we entered into new contractual arrangements and amended the terms of our existing contractual arrangements with Markel and its affiliates. These coordinated transactions with Markel formed an arrangement that became effective January 1, 2026 (the "Markel Fronting Arrangement"). Under the Markel Fronting Arrangement: (i) we continue to issue policies through Essentia, with our underwriting authority (including pricing decisions, rate filing, insurance rating, and risk selections) and claims authority expanded to the maximum levels permitted by applicable law; (ii) we have assumed increased administrative responsibilities for the policies issued through Essentia; (iii) Hagerty Re controls 100% of the premium and assumes 100% of the risk for policies issued through Essentia; and (iv) Hagerty Re pays an initial fronting fee, representing 2% of written premium, to Markel for administrative support, which incrementally decreases based on the level of written premium in each calendar year. We expect these changes to result in increased profitability and additional control, allowing for enhanced operational efficiencies.

As a result of these changes, beginning in the first quarter of 2026, our accounting for the Essentia book of business will significantly change, impacting the recognition of commission revenue earned by our U.S. MGA subsidiary and ceding commission expense incurred by Hagerty Re. Refer to the section entitled "Recent Developments" within Item 7 of Part II of this Annual Report for additional information.

For the years ended December 31, 2025, 2024, and 2023, commission revenue associated with the Markel Alliance Agreement was $436.8 million, $388.0 million, and $340.5 million, respectively, representing 91%, 93%, and 95%, respectively, of total commission revenue.

Markel is a related party to the Company. Refer to Note 24 — Related-Party Transactions in Item 8 of Part II of this Annual Report for additional information.

Aviva Canada Alliance

Aviva Canada Inc. ("Aviva") serves as the carrier for the specialty collector vehicle insurance policies sold by our Canadian MGA subsidiary ("Hagerty Canada"). The relationship with Aviva in Canada is exclusive with respect to specialty, enthusiast, classic, and collector vehicle insurance, with the exception of the Quebec province, where a third-party insurance agency carries the appropriate licenses and authority to submit business to Aviva. Aviva and Hagerty Re also have a quota share reinsurance agreement under which Hagerty Re reinsures 50% of the risk written by Hagerty Canada on behalf of Aviva. Canadian provincial laws govern many of the activities under this relationship and Hagerty Canada must maintain the appropriate licensing. The terms of our agreements with Aviva expire in 2030 and include a 5-year extension if certain thresholds are met.

State Farm Alliance

We have a 10-year master alliance agreement and associated managing general underwriter agreement with State Farm Mutual Automobile Insurance Company ("State Farm") (the "State Farm Master Alliance Agreement") under which State Farm Classic+ policies are offered to State Farm's customers through State Farm agents. This program began offering State Farm Classic+ policies in September 2023. As of December 31, 2025, State Farm Classic+ policies were being offered in 27 states, with conversions of their existing book of business occurring in seven of these states and plans to offer such policies in additional states in 2026 and 2027. Hagerty Re does not have a quota share reinsurance agreement with State Farm and as such, we do not reinsure any of the risk written under the State Farm Classic+ policies. Under the State Farm Master Alliance Agreement, State Farm paid Hagerty an advanced commission of $20.0 million in 2020, which is being recognized as "Commission and fee revenue" over the remaining life of the arrangement. In addition, we are paid a commission for underwriting, binding coverage, and issuing State Farm Classic+ policies and can offer HDC memberships to State Farm Classic+ customers, providing us an additional revenue opportunity.