Exhibit (c)(ii) PRIVILEGED & CONFIDENTIAL PRELIMINARY DRAFT SUBJECT TO DUE DILIGENCE & SUBSTANTIAL REVISION Project Elegant Discussion Materials December 23, 2025 Content must not go below this line

PRIVILEGED & CONFIDENTIAL PRELIMINARY DRAFT SUBJECT TO DUE DILIGENCE & SUBSTANTIAL REVISION Executive Summary • At the request of the Special Committee, Elegant’s CEO and CFO presented the Company’s latest business plan and financial th forecast (the “Management LRP”) to the Special Committee on Decembe, r 21 08 25 o The Board of Directors held a strategy session in October of 2025 as a part of their Q3 board meeting, during which Management presented on both quarterly earnings and the business’ -fo rw goard strategy. This session included a high-level discussion of the business plan, which Management has continued to refine over the past several months to incorporate input from newly onboarded executives, including the recently hired COO and CDO o From a financial perspective, the Management LRP in light of the turnaround plan is largely consistent with the forecast presented at the prior Board of Directors meeting in October (see page 10 for a detailed summary of differences) • The Management LRP assumes Management successfully implements a turnaround in 2026 after the business has faced significant pressure over the past few years o After conducting research to assess areas of focus for operational improvements, Management has identified several key initiatives to address operational gaps and achieve topline growth potential, which were discussed at length with the Special th Committee during the December 18 meeting • Identified strategic initiatives include improving waxer training, optimizing scheduling, enhancing guest onboarding, investing in CRM infrastructure and providing ramping / mature center closure mitigation support o Management indicates that implementation of the strategic initiatives will be challenging • To assist the Special Committee in its review of the Management LRP, we have included benchmarking of several key data points in the Management LRP against equity research estimates for Elegant and a group of selected publicly traded companies • Moelis is continuing to conduct due diligence on Elegant, the Management LRP and the Company’s tax receivable agreement, including submitting follow-up diligence requests and scheduling calls with Management and KPMG Content must not go below this line Confidential | 1

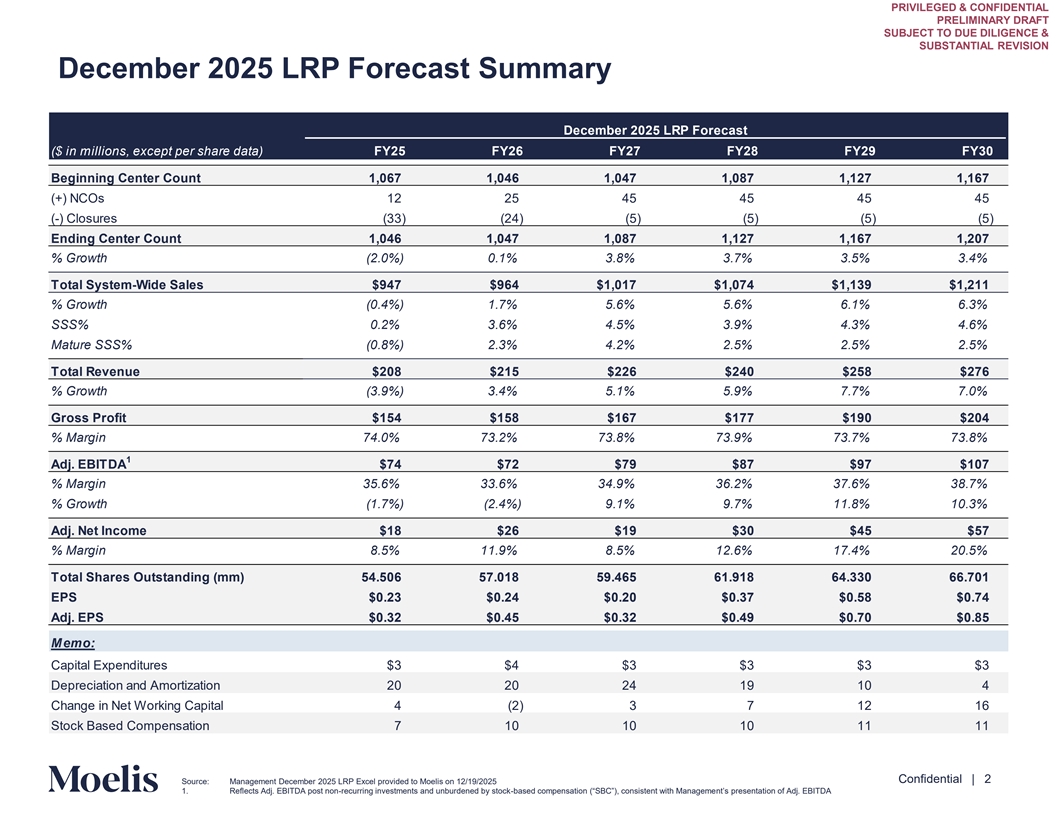

PRIVILEGED & CONFIDENTIAL PRELIMINARY DRAFT SUBJECT TO DUE DILIGENCE & SUBSTANTIAL REVISION December 2025 LRP Forecast Summary December 2025 LRP Forecast ($ in millions, except per share data) FY25 FY26 FY27 FY28 FY29 FY30 Beginning Center Count 1,067 1,046 1,047 1,087 1,127 1,167 (+) NCOs 12 25 45 45 45 45 (-) Closures (33) (24) (5) (5) (5) (5) Ending Center Count 1,046 1,047 1,087 1,127 1,167 1,207 % Growth (2.0%) 0.1% 3.8% 3.7% 3.5% 3.4% Total System-Wide Sales $947 $964 $1,017 $1,074 $1,139 $1,211 % Growth (0.4%) 1.7% 5.6% 5.6% 6.1% 6.3% SSS% 0.2% 3.6% 4.5% 3.9% 4.3% 4.6% Mature SSS% (0.8%) 2.3% 4.2% 2.5% 2.5% 2.5% Total Revenue $208 $215 $226 $240 $258 $276 % Growth (3.9%) 3.4% 5.1% 5.9% 7.7% 7.0% Gross Profit $154 $158 $167 $177 $190 $204 % Margin 74.0% 73.2% 73.8% 73.9% 73.7% 73.8% 1 Adj. EBITDA $74 $72 $79 $87 $97 $107 % Margin 35.6% 33.6% 34.9% 36.2% 37.6% 38.7% % Growth (1.7%) (2.4%) 9.1% 9.7% 11.8% 10.3% Adj. Net Income $18 $26 $19 $30 $45 $57 % Margin 8.5% 11.9% 8.5% 12.6% 17.4% 20.5% Total Shares Outstanding (mm) 54.506 57.018 59.465 61.918 64.330 66.701 EPS $0.23 $0.24 $0.20 $0.37 $0.58 $0.74 Adj. EPS $0.32 $0.45 $0.32 $0.49 $0.70 $0.85 Memo: Capital Expenditures $3 $4 $3 $3 $3 $3 Depreciation and Amortization 20 20 24 19 10 4 Change in Net Working Capital 4 (2) 3 7 12 16 Stock Based Compensation 7 10 10 10 11 11 Content must not go below this line Confidential | 2 Source: Management December 2025 LRP Excel provided to Moelis on 12/19/2025 1. Reflects Adj. EBITDA post non-recurring investments and unburdened by stock-based compensation (“SBC”), consistent with Managem nt’s e presentation of Adj. EBITDA

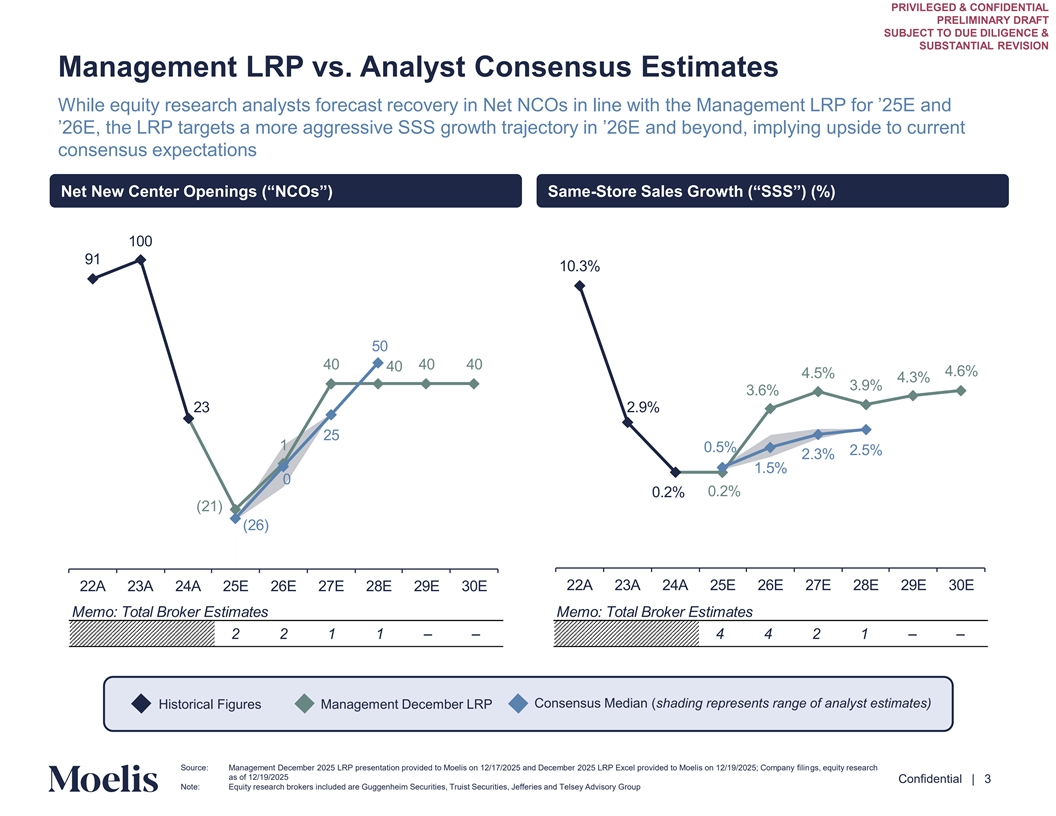

PRIVILEGED & CONFIDENTIAL PRELIMINARY DRAFT SUBJECT TO DUE DILIGENCE & SUBSTANTIAL REVISION Management LRP vs. Analyst Consensus Estimates While equity research analysts forecast recovery in Net NCOs in line with the Management LRP for ’ E and ’ E, the LRP targets a more aggressive SSS growth trajectory in ’ E and beyond, implying upside to current consensus expectations Net New Center Openings (“NCOs”) Same-Store Sales Growth (“SSS”) (%) 1 1 1 . . . . . . . 1 . . . 1. . . ( 1) ( ) A A A E E E 8E E E A A A E E E 8E E E Memo: Total Broker Estimates Memo: Total Broker Estimates 2 2 1 1–– 4 4 2 1–– Consensus Median (shading represents range of analyst estimates) Historical Figures Management December LRP Content must not Source: Management December 2025 LRP presentation provided to Moelis on 12/17/2025 and December 2025 LRP Excel provided to Moelis on 12/19/2025; Company filings, equity research go below this line as of 12/19/2025 Confidential | 3 Note: Equity research brokers included are Guggenheim Securities, Truist Securities, Jefferies and Telsey Advisory Group

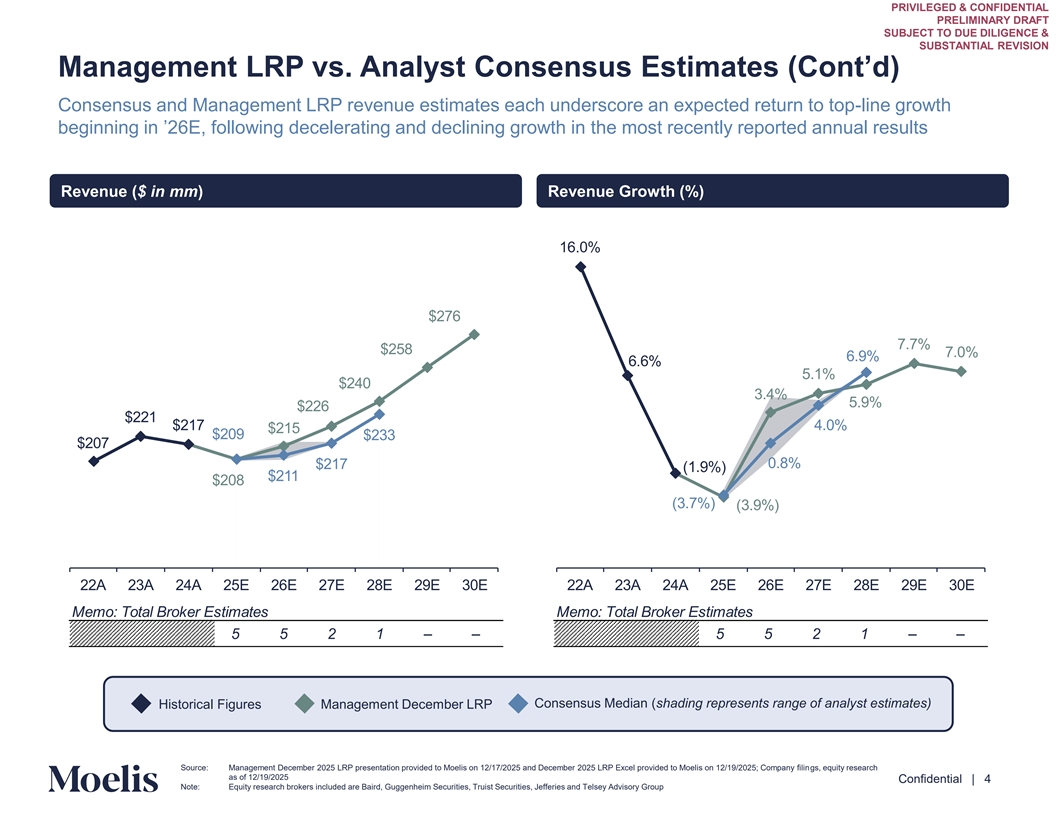

PRIVILEGED & CONFIDENTIAL PRELIMINARY DRAFT SUBJECT TO DUE DILIGENCE & SUBSTANTIAL REVISION Management LRP vs. Analyst Consensus Estimates (Cont’d) Consensus and Management LRP revenue estimates each underscore an expected return to top-line growth beginning in ’ E, following decelerating and declining growth in the most recently reported annual results Revenue ($ in mm) Revenue Growth (%) 1 . . 8 . . . .1 . . 1 1 . 1 .8 1 (1. ) 11 8 ( . ) ( . ) A A A E E E 8E E E A A A E E E 8E E E Memo: Total Broker Estimates Memo: Total Broker Estimates 5 5 2 1–– 5 5 2 1–– Consensus Median (shading represents range of analyst estimates) Historical Figures Management December LRP Content must not Source: Management December 2025 LRP presentation provided to Moelis on 12/17/2025 and December 2025 LRP Excel provided to Moelis on 12/19/2025; Company filings, equity research go below this line as of 12/19/2025 Confidential | 4 Note: Equity research brokers included are Baird, Guggenheim Securities, Truist Securities, Jefferies and Telsey Advisory Group

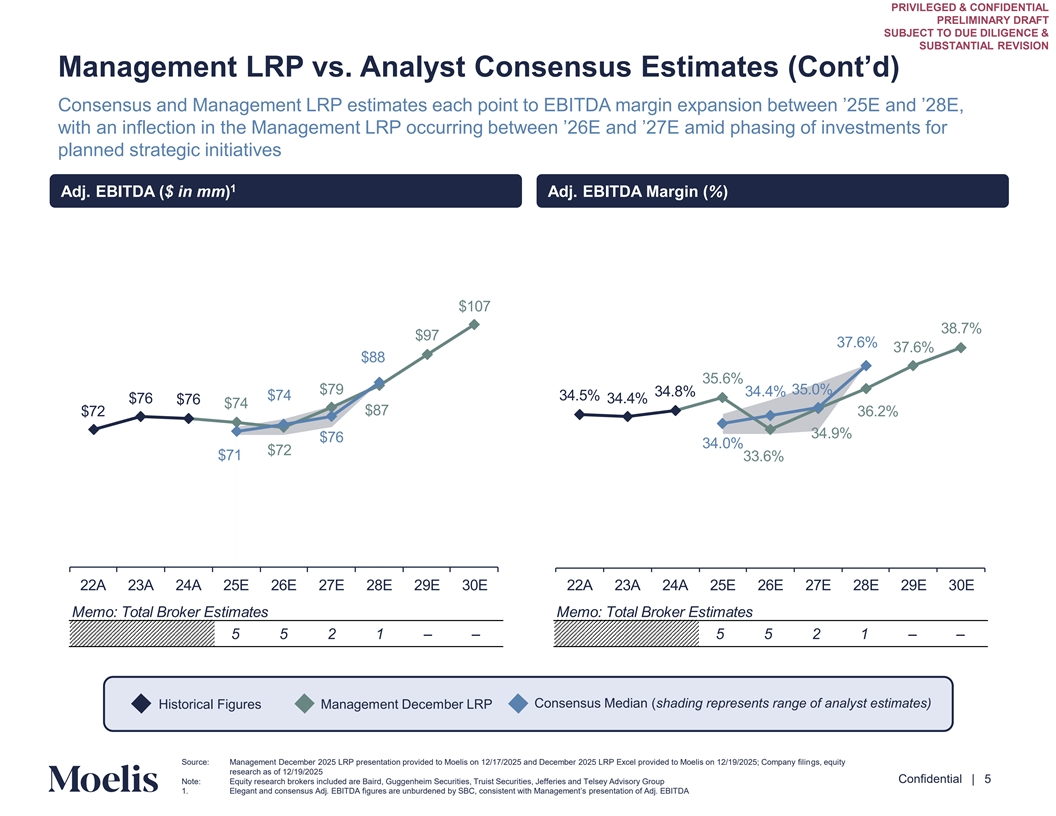

PRIVILEGED & CONFIDENTIAL PRELIMINARY DRAFT SUBJECT TO DUE DILIGENCE & SUBSTANTIAL REVISION Management LRP vs. Analyst Consensus Estimates (Cont’d) Consensus and Management LRP estimates each point to EBITDA margin expansion between ’ E and ’ 8E, with an inflection in the Management LRP occurring between ’ E and ’ E amid phasing of investments for planned strategic initiatives 1 Adj. EBITDA ($ in mm) Adj. EBITDA Margin (%) 1 8. . . 88 . . .8 . . . 8 . . . 1 . A A A E E E 8E E E A A A E E E 8E E E Memo: Total Broker Estimates Memo: Total Broker Estimates 5 5 2 1–– 5 5 2 1–– Consensus Median (shading represents range of analyst estimates) Historical Figures Management December LRP Content must not Source: Management December 2025 LRP presentation provided to Moelis on 12/17/2025 and December 2025 LRP Excel provided to Moelis on 12/19/2025; Company filings, equity go below this line research as of 12/19/2025 Confidential | 5 Note: Equity research brokers included are Baird, Guggenheim Securities, Truist Securities, Jefferies and Telsey Advisory Group 1. Elegant and consensus Adj. EBITDA figures are unburdened by SBC, consistent with Management’s presentation of Adj. EBITDA

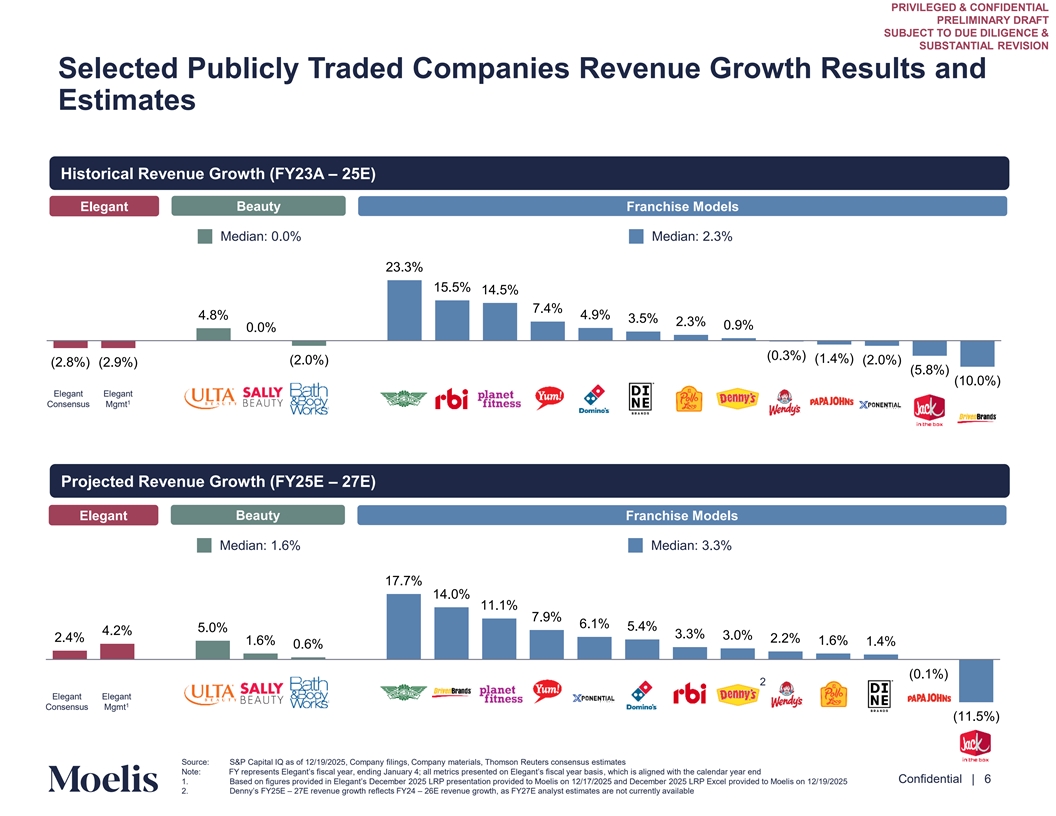

PRIVILEGED & CONFIDENTIAL PRELIMINARY DRAFT SUBJECT TO DUE DILIGENCE & SUBSTANTIAL REVISION Selected Publicly Traded Companies Revenue Growth Results and Estimates Historical Revenue Growth (FY23A – 25E) Beauty Elegant Franchise Models Median: 0.0% Median: 2.3% 23.3% 15.5% 14.5% 7.4% 4.8% 4.9% 3.5% 2.3% 0.9% 0.0% (0.3%) (1.4%) (2.0%) (2.0%) (2.8%) (2.9%) (5.8%) (10.0%) Elegant Elegant 1 Consensus Mgmt Net Le Projected veraRev ge enue Growth (FY25E – 27E) Elegant Beauty Franchise Models Median: 1.6% Median: 3.3% 17.7% 14.0% 11.1% 7.9% 6.1% 5.4% 5.0% 4.2% 3.3% 3.0% 2.4% 2.2% 1.6% 1.6% 1.4% 0.6% (0.1%) 2 Elegant Elegant 1 Consensus Mgmt (11.5%) Content must not Source: S&P Capital IQ as of 12/19/2025, Company filings, Company materials, Thomson Reuters consensus estimates go below this line Note: FY represents Elegant’s fiscal year, ending January ; all metrics presented on Elegant’s f , isca which l ye is aar b liga nsi eds with the calendar year end Confidential | 6 1. Based on figures provided in EleganDece t’s mber 2025 LRP presentation provided to Moelis on 12/17/2025 and December 2025 LRP Excel provided to Moelis on 12/19/2025 2. Denny’s FY E– 27E revenue growth reflects FY24 – 26E revenue growth, as FY27E analyst estimates are not currently available

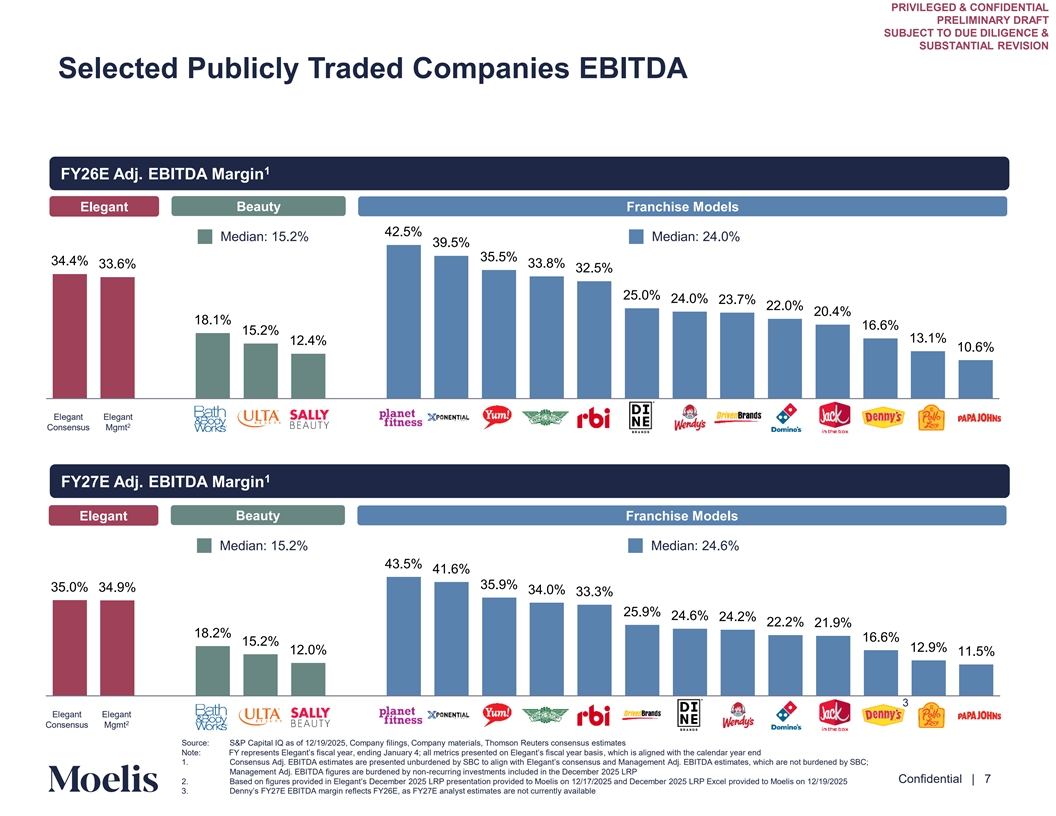

PRIVILEGED & CONFIDENTIAL PRELIMINARY DRAFT SUBJECT TO DUE DILIGENCE & SUBSTANTIAL REVISION Selected Publicly Traded Companies EBITDA 1 FY26E Adj. EBITDA Margin Elegant Beauty Franchise Models 42.5% Median: 15.2% Median: 24.0% 39.5% 35.5% 34.4% 33.6% 33.8% 32.5% 25.0% 24.0% 23.7% 22.0% 20.4% 18.1% 16.6% 15.2% 13.1% 12.4% 10.6% Elegant Elegant 2 Consensus Mgmt 1 Net Le FY27E v A edj ra. ge EBITDA Margin Beauty Elegant Franchise Models Median: 15.2% Median: 24.6% 43.5% 41.6% 35.9% 35.0% 34.9% 34.0% 33.3% 25.9% 24.6% 24.2% 22.2% 21.9% 18.2% 16.6% 15.2% 12.9% 12.0% 11.5% 3 Elegant Elegant 2 Consensus Mgmt Source: S&P Capital IQ as of 12/19/2025, Company filings, Company materials, Thomson Reuters consensus estimates Content must not Note: FY represents Elegant’s fiscal year, ending January ; all metrics presented on Elegant’s f , isca which l ye is aar b liga nsi eds with the calendar year end 1. Consensus Adj. EBITDA estimates are presented unburdened by SBC to align with Elegant’s consensus and Management Adj. EBITDA estimates, which are not burdened by SBC; go below this line Management Adj. EBITDA figures are burdened by non-recurring investments included in the December 2025 LRP Confidential | 7 2. Based on figures provided in EleganDece t’s mber 2025 LRP presentation provided to Moelis on 12/17/2025 and December 2025 LRP Excel provided to Moelis on 12/19/2025 3. Denny’s FY E EBITDA margin reflects FY E, as FY E analyst estimates are not currently available

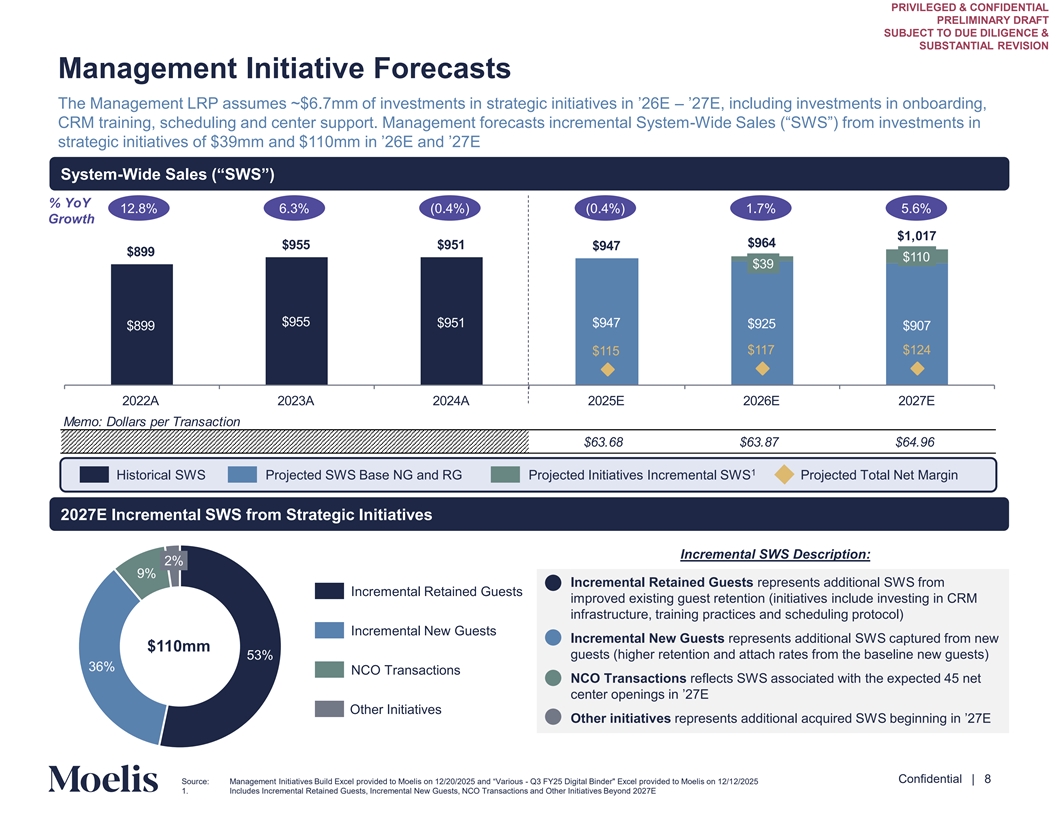

PRIVILEGED & CONFIDENTIAL PRELIMINARY DRAFT SUBJECT TO DUE DILIGENCE & SUBSTANTIAL REVISION Management Initiative Forecasts The Management LRP assumes ~ . mm of investments in strategic initiatives in – ’ ’ E E , including investments in onboarding, CRM training, scheduling and center support. Management forecasts incremental System-Wide Sales (“SWS”) from investments in strategic initiatives of mm and 11 mm in ’ E and ’ E System-Wide Sales (“SWS”) % YoY 12.8% 6.3% (0.4%) (0.4%) 1.7% 5.6% Growth 11 1 8 11 1 11 A A A E E E Memo: Dollars per Transaction $63.68 $63.87 $64.96 1 Historical SWS Projected SWS Base NG and RG Projected Initiatives Incremental SWS Projected Total Net Margin 2027E Incremental SWS from Strategic Initiatives Incremental SWS Description: 2% 9% • Incremental Retained Guests represents additional SWS from Incremental Retained Guests improved existing guest retention (initiatives include investing in CRM infrastructure, training practices and scheduling protocol) Incremental New Guests • Incremental New Guests represents additional SWS captured from new $110mm guests (higher retention and attach rates from the baseline new guests) 53% 36% NCO Transactions • NCO Transactions reflects SWS associated with the expected 45 net center openings in ’ E Other Initiatives • Other initiatives represents additional acquired SWS beginning in ’ E Content must not go below this line Confidential | 8 Source: Management Initiatives Build Excel provided to Moelis on 1 / / and “Var -i o Q3 us FY25 Digital Binder Excel provided to Moelis on 12/12/2025 1. Includes Incremental Retained Guests, Incremental New Guests, NCO Transactions and Other Initiatives Beyond 2027E

Appendix Content must not go below this line Confidential | 9

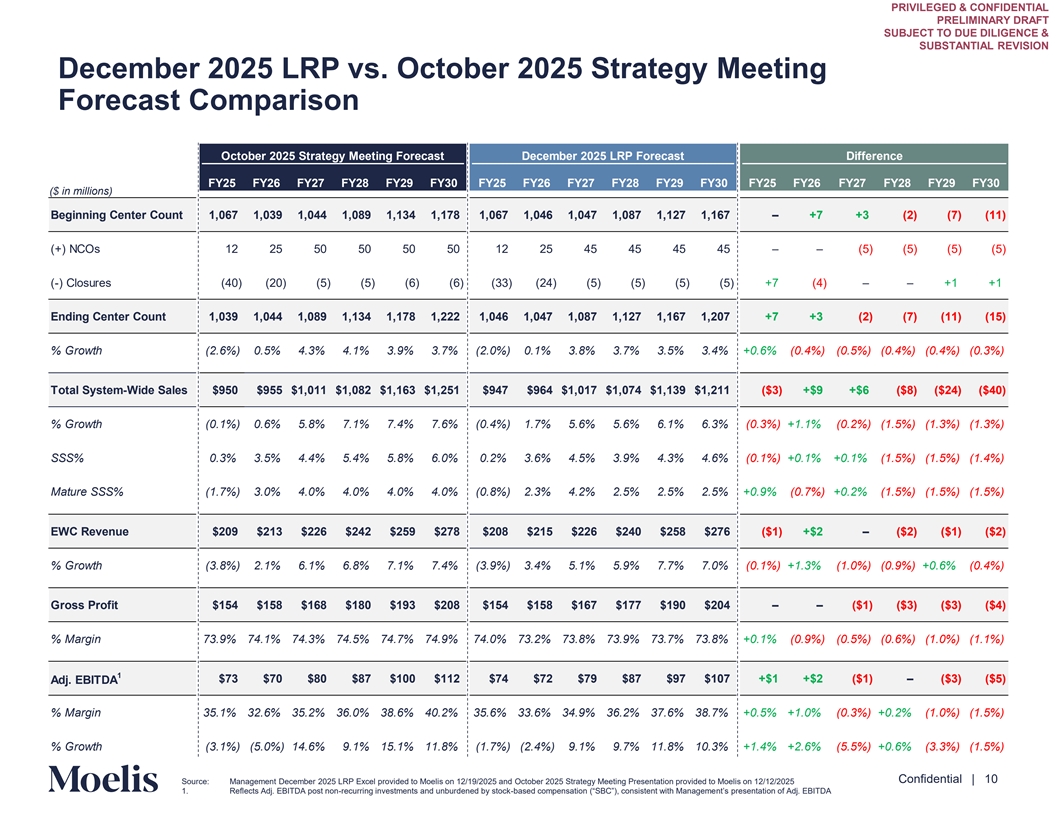

PRIVILEGED & CONFIDENTIAL PRELIMINARY DRAFT SUBJECT TO DUE DILIGENCE & SUBSTANTIAL REVISION December 2025 LRP vs. October 2025 Strategy Meeting Forecast Comparison October 2025 Strategy Meeting Forecast December 2025 LRP Forecast Difference December 2025 LRP Forecast (Presentation) FY25 FY26 FY27 FY28 FY29 FY30 FY25 FY26 FY27 FY28 FY29 FY30 FY25 FY26 FY27 FY28 FY29 FY30 ($ in millions) Beginning Center Count 1,067 1,039 1,044 1,089 1,134 1,178 1,067 1,046 1,047 1,087 1,127 1,167 – +7 +3 (2) (7) (11) (+) NCOs 12 25 50 50 50 50 12 25 45 45 45 45 – – (5) (5) (5) (5) (-) Closures (40) (20) (5) (5) (6) (6) (33) (24) (5) (5) (5) (5) +7 (4) – – +1 +1 Ending Center Count 1,039 1,044 1,089 1,134 1,178 1,222 1,046 1,047 1,087 1,127 1,167 1,207 +7 +3 (2) (7) (11) (15) % Growth (2.6%) 0.5% 4.3% 4.1% 3.9% 3.7% (2.0%) 0.1% 3.8% 3.7% 3.5% 3.4% +0.6% (0.4%) (0.5%) (0.4%) (0.4%) (0.3%) Total System-Wide Sales $950 $955 $1,011 $1,082 $1,163 $1,251 $947 $964 $1,017 $1,074 $1,139 $1,211 ($3) +$9 +$6 ($8) ($24) ($40) % Growth (0.1%) 0.6% 5.8% 7.1% 7.4% 7.6% (0.4%) 1.7% 5.6% 5.6% 6.1% 6.3% (0.3%) +1.1% (0.2%) (1.5%) (1.3%) (1.3%) SSS% 0.3% 3.5% 4.4% 5.4% 5.8% 6.0% 0.2% 3.6% 4.5% 3.9% 4.3% 4.6% (0.1%) +0.1% +0.1% (1.5%) (1.5%) (1.4%) Mature SSS% (1.7%) 3.0% 4.0% 4.0% 4.0% 4.0% (0.8%) 2.3% 4.2% 2.5% 2.5% 2.5% +0.9% (0.7%) +0.2% (1.5%) (1.5%) (1.5%) EWC Revenue $209 $213 $226 $242 $259 $278 $208 $215 $226 $240 $258 $276 ($1) +$2 – ($2) ($1) ($2) % Growth (3.8%) 2.1% 6.1% 6.8% 7.1% 7.4% (3.9%) 3.4% 5.1% 5.9% 7.7% 7.0% (0.1%) +1.3% (1.0%) (0.9%) +0.6% (0.4%) Gross Profit $154 $158 $168 $180 $193 $208 $154 $158 $167 $177 $190 $204 – – ($1) ($3) ($3) ($4) % Margin 73.9% 74.1% 74.3% 74.5% 74.7% 74.9% 74.0% 73.2% 73.8% 73.9% 73.7% 73.8% +0.1% (0.9%) (0.5%) (0.6%) (1.0%) (1.1%) 1 $73 $70 $80 $87 $100 $112 $74 $72 $79 $87 $97 $107 +$1 +$2 ($1) – ($3) ($5) Adj. EBITDA % Margin 35.1% 32.6% 35.2% 36.0% 38.6% 40.2% 35.6% 33.6% 34.9% 36.2% 37.6% 38.7% +0.5% +1.0% (0.3%) +0.2% (1.0%) (1.5%) % Growth (3.1%) (5.0%) 14.6% 9.1% 15.1% 11.8% (1.7%) (2.4%) 9.1% 9.7% 11.8% 10.3% +1.4% +2.6% (5.5%) +0.6% (3.3%) (1.5%) Content must not go below this line Confidential | 10 Source: Management December 2025 LRP Excel provided to Moelis on 12/19/2025 and October 2025 Strategy Meeting Presentation provided to Moelis on 12/12/2025 1. Reflects Adj. EBITDA post non-recurring investments and unburdened by stock-based compensation (“SBC”), consistent with Managem nt’s e presentation of Adj. EBITDA

PRIVILEGED & CONFIDENTIAL PRELIMINARY DRAFT SUBJECT TO DUE DILIGENCE & SUBSTANTIAL REVISION Disclaimer This presentation has been prepared by Moelis & Company LLC (“Moelis”) solely for the information and assistance of al tC he omm Spe ittci ee of the Board of Directors of the company codenamed “Elegant” (the “Company”) in considering the matters referred to in t erihe als. se Thi ms at presentation is confidential and may not be disclosed (in whole or in part) or utilized for other purposes without the express prior written consent of Moelis. This presentation has been prepared based on information provided by the Company and/or from third party sources. Moelis assumed such information is complete and accurate in all material respects. Moelis has not independently verified such information (or assumed responsibility for the independent verification of such information). To the extent this presentation includes projections, forecasts or other forward-looking statements, Moelis has assumed that such information was reasonably prepared based on the best currently available estimates and judgments of the Company and/or other parties as to the future performance of the Company and/or such other parties. Moelis expresses no views as to the reasonableness of any such projections, forecasts or other forward-looking statements or the assumptions on which they are based. Moelis has not made any independent evaluation or appraisal of any of the assets or liabilities (contingent, derivative, off-balance-sheet, or otherwise) of the Company or any other party. Moelis’ participation in any due diligence review is solely for purposes of supdv poir ce ting an id ts anaalysis. This presentation is based on economic, monetary, market and other conditions as in effect on, and the information made available to us as of, the date hereof, and Moelis assumes no obligation to update this presentation or correct any information herein. No company or transaction used in this presentation is identical to the Company or any potential transaction. The analyses set forth in this presentation do not purport to be appraisals and such analyses do not reflect Moelis’ views of the prices at which businesses or securities actually d. may Beca beuse sol the analyses described in these materials (including the information used in such analyses) are inherently subject to uncertainty, Moelis does not assume responsibility if future results are materially different from those forecast. This presentation was designed for use by certain persons familiar with the business of the Company. This presentation is not intended to provide the sole basis for any decision on any transaction or strategic alternative and is not a recommendation with respect to any transaction or strategic alternative. This presentation does not address the Special Committee’s underlying business decision to ex repl comm ore or end any transaction or strategic alternative or the relative merits of any transaction or strategic alternative as compared to any alternative business strategies or transactions that might be available to the Company. Nothing contained in this presentation should be construed as legal, regulatory, tax or accounting advice. Moelis and its affiliates are engaged globally in a wide range of investment banking and other activities for their own account and otherwise. Moelis and its affiliates may have advised, may seek to advise and may in the future advise in companies referred to in this presentation. Personnel of Moelis or such affiliates may make statements or provide advice that is contrary to information included in this presentation. The proprietary interests of Moelis or its affiliates may conflict with your interests. In addition, Moelis and its affiliates and their personnel may from time to time have positions in or effect transactions in securities referred to in this material (or derivatives of such securities), or serve as a director of companies referred to in this presentation. Content must not go below this line Confidential | 11