| 1271 Avenue of the Americas | ||

| New York, New York 10020-1401 | ||

| Tel: +1.212.906.1200 Fax: +1.212.751.4864 | ||

| www.lw.com | ||

| |

FIRM / AFFILIATE OFFICES | |

| Beijing | Moscow | |

| Boston | Munich | |

| Brussels | New York | |

| Century City | Orange County | |

| Chicago | Paris | |

| Dubai | Riyadh | |

| July 22, 2021 | Düsseldorf | San Diego |

| Frankfurt | San Francisco | |

| Hamburg | Seoul | |

| Hong Kong | Shanghai | |

| Houston | Silicon Valley | |

| London | Singapore | |

| Los Angeles | Tokyo | |

| Madrid | Washington, D.C. | |

| Milan | ||

VIA EDGAR AND HAND DELIVERY

United States Securities and Exchange Commission

Division of Corporation Finance

100 F Street, N.E.

Washington, D.C. 20549-6010

| Attention: | Ernest Greene |

| Anne McConnell | |

| Thomas Jones | |

| Jay Ingram |

| Re: | IHS Towers Limited Amendment No. 2 to Draft Registration Statement on Form F-1 Confidentially submitted on June 4, 2021 CIK No. 0001725749 |

Ladies and Gentlemen:

On behalf of IHS Towers Limited (the "Company"), we are confidentially submitting a fourth Draft Registration Statement on Form F-1 ("Submission No. 4"). The Company previously submitted a Draft Registration Statement on Form F-1 on a confidential basis with the Securities and Exchange Commission (the "Commission") on January 27, 2020 (the "Draft Submission"), as amended by Amendment No. 1 to the Draft Submission on July 28, 2020 and Amendment No. 2 to the Draft Submission on June 4, 2021 ("Submission No. 3"). Submission No. 4 has been revised to reflect the Company’s responses to the comment letter to Submission No. 3 received on July 2, 2021 from the staff of the Commission (the "Staff").

For ease of review, we have set forth below each of the numbered comments of your letter in bold type followed by the Company’s responses thereto. Unless otherwise indicated, capitalized terms used herein have the meanings to be assigned to them in Submission No. 4, and all references to page numbers in such responses are to page numbers in Submission No. 4.

July 22, 2021

Page 2

Summary Consolidated Financial and Operating Data, page 17

| 1. | We note your responses to prior comments 2 and 3 and appreciate the additional information and disclosures you provided; however, please address the following: |

| · | We note the information you provided regarding the elimination of a provision for bad or doubtful debts related to a Key Customer’s restructuring from Adjusted EBITDA; however, it continues to appear to us that eliminating an impairment related to customer receivables from a non-IFRS performance measure is not appropriate. |

| · | We note the information you provided regarding the elimination of impairments of withholding tax receivables from Adjusted EBITDA. In order for us to better understand these adjustments, more fully explain to us when and how these receivables are recorded in your financial statements and tell us the basis for your accounting for them. Also, more fully explain to us the facts and circumstances that result in these receivables being impaired. Based on your current disclosures related to these receivables, it is not clear to us if they represent amounts previously recorded as revenues that are never realized or additional taxes. |

| · | We note the information you provided regarding Consolidated AFFO, AFFO, and ROIC; however, it remains unclear to us what these measures represent, why you believe they are useful to investors, and how you determined they are performance measures rather than liquidity measures. In this regard we note you appear to be include adjustments that present interest expense, interest income, and income taxes on a cash basis but continue to present other amounts on an accrual basis. We also note these measures appear to be more similar to adjusted free cash flow measures based on your elimination of non-discretionary capital expenditures. |

| · | We note you present the financial measures Adjusted EBITDA Margin, Net Leverage Ratio, and ROIC, which are all calculated using non-IFRS financial measures; however, you have not presented the most directly comparable IRFS measures with equal or greater prominence as required by Item 10(e)(1)(i)(A) of Regulation S-K. |

Response: The Company respectfully acknowledges the Staff’s comment and advises the Staff that:

| · | We note the information you provided regarding the elimination of a provision for bad or doubtful debts related to a Key Customer’s restructuring from Adjusted EBITDA; however, it continues to appear to us that eliminating an impairment related to customer receivables from a non-IFRS performance measure is not appropriate. |

The Company respectfully acknowledges the Staff’s comment with respect to the elimination of the impairment of receivables related to a Key Customer of $30.0 million and $38.3 million for the years ended December 31, 2018 and 2017, respectively. The Company believes that these were atypical collection issues, which were not indicative of its underlying business performance given their size and non-recurring nature, and notes that they are also excluded from the Company’s segment measures of performance. However, on reflection of the Staff’s comment, the Company has removed the adjustment for provision for bad or doubtful debts from its Adjusted EBITDA measure and made the necessary adjustments throughout Submission No. 4.

July 22, 2021

Page 3

| · | We note the information you provided regarding the elimination of impairments of withholding tax receivables from Adjusted EBITDA. In order for us to better understand these adjustments, more fully explain to us when and how these receivables are recorded in your financial statements and tell us the basis for your accounting for them. Also, more fully explain to us the facts and circumstances that result in these receivables being impaired. Based on your current disclosures related to these receivables, it is not clear to us if they represent amounts previously recorded as revenues that are never realized or additional taxes. |

The Company respectfully acknowledges the Staff’s comment and notes that withholding tax receivables arise primarily as a result of the Nigerian corporate income tax legislation. Withholding tax receivables represent amounts of taxes paid in advance to tax authorities on behalf of the Company by the Company’s customers. The recognition of withholding tax receivables and their subsequent impairment have no impact on, and are not recorded within, the revenue recognized by the Company.

The Company issues invoices to its customers at the transaction price agreed in its contracts with customers. The Company’s customers thereafter withhold 10% of a portion of the value billed to them, remit this amount to the tax authority on behalf of the Company and submit a certificate of such remittance to the Company. This remittance extinguishes the trade receivables from the customers related to such tax (the customers having now settled their obligation to the Company), and the Company recognizes withholding tax receivables due from the tax authority.

The withholding tax receivables represent cash tax credits that can be applied by the Company in full or partial settlement of its cash tax obligation in future years and are thus classified as financial assets in accordance with IFRS 9 Financial instruments. The recoverability of withholding tax receivables is assessed by reference to: a) the amount of cash tax liabilities that are expected to be due in future periods and that will be offset by withholding tax receivables; b) the amount of existing withholding tax receivables that can be applied against future cash tax liabilities; and c) the amount of withholding tax receivables that are expected to be generated through further customer billings in those future periods. The Company assesses the recoverability of withholding tax receivables based on future cash flow projections and an analysis of the utilization of withholding tax receivables balances against future income tax liabilities. Where the amount of withholding tax receivables exceeds the amount of forecast future tax liabilities, the Company recognizes an impairment of withholding tax receivables in the Consolidated Statement of Income and Other Comprehensive Income. This impairment charge is adjusted for in the reconciliation between the Loss for the period and Adjusted EBITDA.

The Company notes that revenue recognized under IFRS 15 Revenue from contracts with customers is not impacted by the existence of the withholding tax obligations. The contracts between the Company and its customers set out the transaction price payable by the customers and the performance obligations of the Company. The remittance of a portion of the contract price by the customers to the tax authorities is a mechanism by which the tax authority collects tax payable in advance and does not extinguish the customers’ obligations to deliver cash, either to the Company or to the tax authority (as a prepayment against the Company’s tax liabilities), in exchange for the settlement of amounts due to the Company under the terms of the revenue contracts.

July 22, 2021

Page 4

The Company therefore notes that the withholding tax receivables represent a prepayment of tax liabilities that may or may not be recoverable in future periods, and not an amount of revenue that is never realized. Accordingly, the Company believes that, although the withholding tax is not a direct tax that falls within the scope of IAS 12 - Income taxes, when such amounts of withholding tax are not expected to be recoverable against future tax liabilities and are therefore impaired, they are analogous to a minimum tax, which would be considered a form of income tax and consistent with tax related items added back to Adjusted EBITDA.

| · | We note the information you provided regarding Consolidated AFFO, AFFO, and ROIC; however, it remains unclear to us what these measures represent, why you believe they are useful to investors, and how you determined they are performance measures rather than liquidity measures. In this regard we note you appear to be include adjustments that present interest expense, interest income, and income taxes on a cash basis but continue to present other amounts on an accrual basis. We also note these measures appear to be more similar to adjusted free cash flow measures based on your elimination of non-discretionary capital expenditures. |

The Company respectfully acknowledges the Staff’s comment and notes that the Company uses Consolidated AFFO and AFFO as part of the Company’s annual operating plan presented to and approved by the Group Executive Committee and that, in this context, Consolidated AFFO and AFFO are used as performance measures. In particular, management uses these metrics to measure business performance across countries, across segments and to assess new business opportunities either through organic growth or through acquisition.

Furthermore, the Company notes that Consolidated AFFO and AFFO represent the Company’s ability to generate cash profits and reflect the requirement for recurring cash expenditure that is required to generate cash profits (including those of a capital nature) or that results from the generation of cash profits, such as resulting cash taxes. The AFFO measures differ from adjusted free cash flow measures as they do not include the cash impact of either working capital movements or discretionary capital expenditures. The exclusion of the working capital movements reduces volatility (for example, irregular customer payment patterns) and the exclusion of discretionary capital expenditures (which are non-recurring and underpin the Company’s growth plans) ensures that the measure focuses on the Company’s steady state business performance.

The Company further notes that the Company’s peers present Consolidated AFFO, AFFO and ROIC as performance measures, and as such, the Company believes its presentation of these measures is useful for investors to aid comparability between the performance of the Company and the performance of the Company’s peers. The Company believes that investors in the Company's industry would expect the Company to present these performance measures to allow for comparability and benchmarking. The Company believes that Consolidated AFFO, AFFO and ROIC are even more relevant given the decreased comparability of EBITDA following the introduction of IFRS 16 and ASC 842 which, given that many of the Company’s peers report under US GAAP, result in different accounting treatments under the two accounting frameworks.

The Company acknowledges that the Consolidated AFFO and AFFO measures are used by our peers, many of whom are REITs, as a performance measure. Given that the Company has a business model which is similar to its peers and may distribute returns to its shareholders in the future, the Company concluded that the Consolidated AFFO and AFFO measures are appropriate performance measures.

July 22, 2021

Page 5

The Company’s ROIC measure is a factor of the Company’s Consolidated AFFO measure (excluding the impacts of interest paid and received), and the Company concluded that ROIC is therefore also a performance measure, as it is a measure of the Company's ability to generate net cash profits from the Company’s asset base, the latter having been built up primarily through cash investments made by the Company. The Group Executive Committee and Board use ROIC when assessing the performance of historic invested capital against expected returns. The Company believes that ROIC is also a useful measure for investors to assess, in part, the success of inorganic investment.

The Company acknowledges the Staff’s query regarding items being added back to Consolidated AFFO and AFFO on a cash basis and on an accrual basis and respectfully notes that the adjustments between the Adjusted EBITDA measure and Consolidated AFFO measure are primarily adjustments reflecting cash movements and that these relate to items that require cash settlement. The exception is the “Amortization of prepaid site rent,” which represents a non-cash item not reflected in the reconciliation between the Adjusted EBITDA measure to the loss for the period. This is specifically related to the nature of some of the Company’s short-term leases that are often paid up to one year in advance, with the cost of those leases being amortized over the period of the lease. Given that the AFFO measure is a measure of cash performance, the non-cash amortization is removed from AFFO measure and replaced with “Lease payments made,” which reflects the cumulative cash paid in the period, in respect of those short-term leases and in respect of longer-term leases accounted for in accordance with IFRS 16.

| · | We note you present the financial measures Adjusted EBITDA Margin, Net Leverage Ratio, and ROIC, which are all calculated using non-IFRS financial measures; however, you have not presented the most directly comparable IRFS measures with equal or greater prominence as required by Item 10(e)(1)(i)(A) of Regulation S-K. |

The Company respectfully acknowledges the Staff’s comment and has revised page 19 of Submission No. 4.

Consolidated Financial Statements

31. Related Parties, page F-77

| 2. | We note your response to prior comment 7. Please tell us MTN Group's ownership interest in the company. |

Response: The Company respectfully acknowledges the Staff’s comment and advises the Staff that MTN Group's ownership interest in the Company was 28.96% as of March 31, 2021.

32. Business Combinations, page F-79

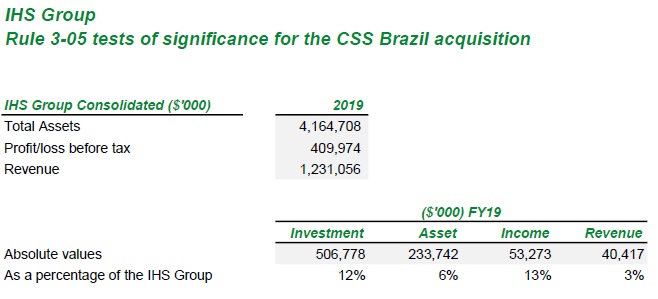

| 3. | We note your response to prior comment 1 indicates you provided the tests of significance you performed for the 2020 acquisition in Brazil as an appendix to your response letter; however, it does not appear an appendix was provided. Please advise. In addition, please revise note 34(c) to disclose the purchase price you paid for the disclosed transaction. |

Response: The Company respectfully acknowledges the Staff’s comment and has provided, as an appendix to this letter, the tests performed. The Company has revised note 34(c) to disclose the estimated purchase price the Company has agreed for the disclosed transaction.

July 22, 2021

Page 6

General

| 4. | We note your response to prior comment 8. The consent filed as exhibit 23.2 should be consistent with Rule 436. In this regard, it is inappropriate to include the second paragraph and items (1), (2) and (3) of exhibit 23.2. |

Response: The Company respectfully acknowledges the Staff’s comment and has included a revised exhibit 23.2.

* * *

Please do not hesitate to contact me by telephone at (212) 906-1281 with any questions or comments regarding this correspondence.

| Very truly yours, | |

| /s/ Marc D. Jaffe | |

| Marc D. Jaffe | |

| of LATHAM & WATKINS LLP |

| cc: | (via email) |

| Sam Darwish, IHS Towers Limited | |

| Adam Walker, IHS Towers Limited | |

| Ian D. Schuman, Esq., Latham & Watkins LLP | |

| Benjamin J. Cohen, Esq., Latham & Watkins LLP | |

| Roxane F. Reardon, Esq., Simpson Thacher & Bartlett LLP | |

| Jonathan R. Ozner, Esq., Simpson Thacher & Bartlett LLP |

July 22, 2021

Page 7

Appendix