Please wait

Super Group (SGHC) Ltd

Bordeaux Court, Les Echelons

St. Peter Port, Guernsey, GY11AR

August 05,2025

VIA EDGAR

United States Securities and Exchange Commission

Division of Corporation Finance

Office of Trade & Services

100F Street NE

Washington, D.C. 20549

Attention: Robert Shapiro/Doug Jones

RE: Super Group (SGHC) Limited

Form 20-F for the Fiscal Year Ended December 31, 2024

File No. 001-41253

Dear Mr. Shapiro and Mr. Jones:

Set forth below are the responses of Super Group (SGHC) Limited (the “Company,” “we,” “us”, “management” or “our”) to comments received from the staff of the Division of Corporation Finance (the “Staff”) of the Securities and Exchange Commission (the “Commission”) by letter, dated July 9, 2025 related to the above referenced Form 20-F (the “Form 20-F”).

To facilitate the Staff’s review, we have repeated each of the Staff’s comments below, followed by the Company’s responses thereto.

Form 20-F for Fiscal Year Ended December 31, 2024

Item 5.A. Operating Results

Results of Operations

Year Ended December 31, 2024, compared to the Year Ended December 31, 2023, Revenue, page 80

1.Please quantify all factors cited for the variances in each revenue category, particularly in regard to changes in the volume or amount of products/offerings provided or to the introduction of new products/offerings cited in your analysis. Refer to the introductory paragraph of Item 5 and Item 5.A.1 of Form 20-F. Additionally, explain what "margins" you cite refers to and how changes therein affect your revenue.

Response:

The Company acknowledges the Staff’s comment and advises that it will quantify the underlying components of revenue changes in all future filings that include Item 5 Operating and Financial Review and Prospects, starting with the Form 20-F for the year to 31 December 2025.

By way of illustration, the company presents below its revenue discussion as included in the Form 20-F for the year ended December 31, 2024, with additional quantification shown as marked. Further explanatory narrative is also provided in response to the Staff’s comment but not as a proposed amendment to the Form 20-F disclosure for the year to 31 December 2024.

Extract of page 80 and page 81 of the Super Group Annual Reporting on Form 20-F for the year ended December 31, 2024, with proposed amendments as marked

Our total revenue was €1.70 billion for the year ended December 31, 2024, an increase of €260.7 million or 18.2% (Constant Currency: 20.6%) compared to €1.44 billion for the year ended December 31, 2023, mainly due to strong performances in the Africa & Middle East and European markets (an increase of €240.2 million or 57.9% and €52.1 million or 23.1% respectively), especially with the continued launch of new casino content as well as improved sports margins, especially on soccer, and thus increased sports betting revenue. Despite the strong performance, overall growth was offset by the impact of currency fluctuations across various jurisdictions in which we operate.

Further explanatory narrative in response to the Staff’s question

To quantity the factors cited for the impact on revenue due to the changes related to new casino content i.e products and offerings, it’s important to note that new casino content is the offerings relating to game play and content on the websites that are used by our customers. The Company respectfully advises that in order to be able to provide information on changes in the volume or amount of products/offerings or the introduction of new products/offerings, we have in places referenced below to an operational metric that is used by the company to monitor and understand growth in the drivers of net gaming revenue, being Gross Gaming Revenue (“GGR”). GGR is a component of net gaming revenue and represents the sum of total wagers less payouts on both online casino and sports betting products and games, before deduction of: bonuses; comps; incentives; contribution to casino game suppliers in order to fund progressive jackpot network games; and value-added tax. Whilst net gaming revenue can be ascertained at an overall product level (being online casino or sports betting) and at a segment level, bonuses are not recorded on a sub-product or game-specific basis, meaning that net gaming revenue is not able to be determined at that lower level. As a result, in order to review revenue performance drivers at that lower level, the company uses GGR.

New casino content and offerings, within the casino product, increased the group GGR by €241.5 million or 58.8% to €652.0 million for the year ended December 31, 2024, compared to €410.5 million for the year ended December 31, 2023. Introduction of new casino content and offerings to the Africa & Middle East segmental regions, had the most favourable impact on GGR within these geographical segments, where GGR derived from new casino content resulted in an increase in total GGR of €174.5 million or 74.9% to €407.6 million for the year ended December 31, 2024, compared to total GGR of €233.1 million for the year ended December 31, 2023.

With respect to the sport product offering the group total revenue increased by €39.1 million or 13.2% for the year ended December 31, 2024 to €336.0 million compared to €297.0 million for the year ended December 31, 2023 due to improved sports margins which increased to 12.8% for the year ending December 31, 2024, representing an increase of 29.5 basis point year on year from 9.8% for the year ending December 31, 2023, especially on soccer, and thus increased sports betting revenue. Despite the strong performance, overall growth was offset by the impact of currency fluctuations across various jurisdictions in which we operate which negatively affected revenue by 2.4%.

The Company respectfully advises the Staff that sports margin represents the difference between customer wagers placed and customer winnings. Variances arise as a result of changes in volume; the mix of wagers between different sports; the type of bets placed and the results of both sports events and certain incidents occurring during those events. An increase in sports margin due to these factors would result in an increase in net gaming revenue, while a reduction in sports margin would result in a decrease in net gaming revenue.

Another factor contributing to increases in the Company’s total revenue is the volumes of customers in the product at any point in time.

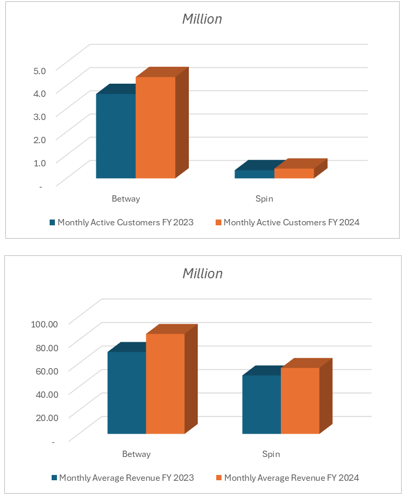

The charts below illustrate the monthly active customers, and revenue, for Betway and Spin respectively.

Monthly active customers increased by 0.8 million or 20.0% to 4.79 million for the year ending December 31,2024 compared to 3.99 million for the year ending December 31,2023.

Extract of page 80 and page 81 of the Super Group Annual Reporting on Form 20-F for the year ended December 31, 2024, with proposed amendments as marked (continued)

Betway

Revenue for the Betway segment increased by €184.6 million or 22.0% to €1,022.6 million for the year ended December 31, 2024, compared to €838.0 million for the year ended December 31, 2023.

Brand licensing revenue decreased by €15.5 million or 45.4% to €18.6 million for the year ended December 31, 2024, compared with €34.1 million for the year ended December 31, 2023. Brand license fees are generated for the use of the Betway brand, which decreased during 2024 mainly due to renegotiations of the brand license fee agreements because of pressure on the licensed partner’s revenue.

Sports betting gaming revenue for the Betway segment increased by €39.1 million or 13.2% to €336.0 million for the year ended December 31, 2024, compared to €296.9 million for the year ended December 31, 2023. The growth in 2024 was largely due to increasingly positive sports margins which increased to 12.8% for the year ending December 31, 2024, representing an increase of 29.5 basis point year on year from 9.8% for the year ending December 31, 2023, especially in European soccer, as well as increased betting fixtures in the UEFA Champions League in the second half of 2024 (144 league stage fixtures compared with 96 group stage fixtures in the second half of 2023), versus unprecedented unfavorable sports betting margins in the latter part of 2023. Additionally, 2023 comparative sports betting revenue

included €52.0 million from the Indian market, which the Group exited at the end of the third quarter of 2023 due to the introduction of an unsustainable goods and services tax ("GST") regime in India. Online casino gaming revenue for the Betway segment increased by €180.1 million or 37.4% to €662.1 million for the year ended December 31, 2024, compared to €482.0 million for the year ended December 31, 2023. Betway saw a decline in its online casino gaming revenue from its Asia-Pacific market for the year ended December 31, 2024, of €30.8 million due to the closure of the Indian market in September 2023 due to the passing of new GST regulation that would have made the market unprofitable. This impact was offset by positive performance in the Africa & Middle East and European segments (an increase of €179.6 million or 56.9% and €43.1 million or 48.5% respectively), both far exceeding forecasted performance due to an improved focus on casino offerings in Betway along with the launching of new platform providers and gaming content offered to customers. Such increase in revenue was driven primarily by growth in GGR as a result of new offerings in Africa & Middle East which contributed €170.9 million and 73.5% year on year, and new offerings in Europe which contributed €39.2 million and 132.5% year on year in Europe respectively.

Average monthly active customers for Betway increased by 0.73 million or 20%, to 4.4 million for the year ended December 31, 2024, from 3.6 million for the year ended December 31,2023.

Spin

Revenue for the Spin segment increased by €76.1 million or 12.7% to €674.2 million for the year ended December 31, 2024, compared with €598.1 million for the year ended December 31, 2023.

Online casino gaming revenue for the Spin segment increased by €76.2 million or 12.8% to €673.4 million for the year ended December 31, 2024, compared to €597.1 million for the year ended December 31, 2023. Spin saw a growth in its online casino gaming revenue from its North American market for the year ended December 31, 2024 of €60.9 million, mainly due to the enhanced customer acquisition and retention strategies, after the migration to the Ontario regulatory platform during 2022, the effects of which were still felt in the 2023 comparatives. Monthly active customers in the North American market for Spin increased by 20,359 or 14.7%, to 158,417 for the year ended December 31, 2024, from 138,058 for the year ended December 31, 2023. Citing this as a major contributor for the total revenue increase of €62.4 million or 15.8% in this market from €396.9 million at year ending December 31,2023 to €458.5 million as at December 31, 2024. Spin also saw further positive growth in New Zealand due to an investment in local marketing during 2023 and additional casino game offerings introduced to the market with monthly active customers in the Asia & Pacific market for Spin increasing by 11,721 or 12.8%, to 103,489 for the year ended December 31, 2024, from 91,768 for the year ended December 31, 2023.

Notes to Consolidated Financial Statements

Note 2. Accounting policies, page F-9

2.Please explain to us why you do not present accounting policies for net gaming revenue, gaming incentives including bonuses, comps and payments to game suppliers, and affiliate(s) marketing. In regards to affiliates marketing and payments to game suppliers, explain to us what each represents and your basis of recognition, how amounts for each are incurred, the basis for these amounts, how they are paid, and where initial amounts incurred are reported in the statement of cash flows.

Response:

The Company acknowledges the Staff’s comments and respectfully advises the Staff as follows:

Accounting policies

Revenue

Our accounting policy for revenue is included in Note 2.4 “Revenue Recognition” on page F-11 of the Form 20-F. Revenue is comprised of online casino and sports betting revenue and brand licensing revenue. Net gaming revenue is recognized in relation to online casino and sports betting in accordance with IFRS 9 Financial instruments. Brand licensing revenue, which is not material, is recognized in accordance with IFRS 15 Revenue from contracts with customers.

The Company also advises the Staff that there are two distinct categories of payments made to casino game suppliers, as follows:

•Payments to casino game suppliers to fund progressive jackpot network games relates to a third-party jackpot game that players can enter through one of the company’s gaming platforms. Players wager an amount to enter and any jackpot amounts would be paid out by the third-party operator. The company is only required to contribute a fixed percentage of the wagers to the third-party operator. These payments are deducted in arriving at net gaming revenue, as clarified in the proposed amendment to the revenue recognition policy below. They are reported in the statement of cash flows as a cash flow from operating activities.

•Payments to casino game suppliers which relate to royalties paid to third-party gaming service providers for supplying games, software platforms or gaming content which is used on the Group’s websites. These are treated as an expense and the basis of recognition is set out further below. They are reported in the statement of cash flows as a cash flow from operating activities.

In our future filings, starting with the Form 20-F for the year ended31 December 2025, we will include an explanation of net gaming revenue in our Revenue Recognition accounting policy as set out below, in order to better link our discussion of net gaming revenue to our Revenue Recognition accounting policies.

Extract of page F-11 of Form 20-F - Revenue recognition policy

Online casino and sports betting

Net revenue represents the consolidated value of all transactions realised and unrealised as at the period end attributable to wins and losses on the online casino and sports betting. Revenues generated from online casino games and sports betting are classified as derivative financial instruments accounted for in accordance with IFRS 9 ‘Financial Instruments’. These derivatives financial instruments are initially recognized at fair value, representing the amount staked by the customer adjusted for any customer incentives. They are subsequently remeasured when the outcome and the transaction price is known and the amount payable is confirmed, at which point the movement is recorded as a gain or loss on the financial instrument in the Consolidated Statements of Profit or Loss and Other Comprehensive Income in the revenue line item. As such gains and losses arise from similar transactions, they are offset within revenue.

The Group recognizes revenue transactions at the fair value of the consideration received or receivable at the point the transactions are settled. Any open positions (i.e. for unused bonuses, comps, incentives or open bets) at year end are fair valued with the resulting gain or loss recorded in the Consolidated Statements of Profit or Loss and Other Comprehensive

Income. Customer liabilities related to these timing differences are accounted for as derivative financial instruments, further discussed in note 20 and 26.

Sports betting and online casino revenue represents the net house win adjusted for the fair market value of gains and losses on open betting positions and certain customer incentives.

The net house win (which represents realized net gaming revenue) consists of the following components:

•Total wagers less payouts for online casino and sport betting positions that have settled in the year

•Less, bonuses, comps (complementary) and incentives that are realized in the year

•Less, payments to casino game suppliers to fund progressive jackpot network games for the associated wagers placed in the year (on an accruals basis)

•Less value added tax, and goods and services tax incurred in the year in relation to the above transactions

Payments to game suppliers to fund progressive jackpots represent a financial liability for the company to contribute a fixed amount of the wagers received from players to the third-party jackpot pool for wagers placed during the year. These are recognized as financial liabilities measured at amortized cost and the amounts accrued are offset within revenue against the associated wager transaction. Any jackpot winnings are a financial liability of the third-party jackpot operator.

Direct and Marketing Expenses

Gaming supplier and affiliate marketing expenses are disclosed under note 6. Gaming supplier expenses, which are distinct from payments to game suppliers to fund progressive jackpots mentioned above, are referred to as royalties whilst affiliate marketing are grouped under marketing expenses. Our next 20-F filing for the year ended 31 December 2025 will include an accounting policy note for Direct and Marketing Expenses and will read as follows:

Direct and Marketing expenses

Direct expenses comprise costs incurred directly in relation to the company’s gaming operations and associated activities. These costs include Gaming tax, license costs and other tax, Processing & Fraud Costs, Royalties, Staff related expenses, Other operational costs, and Foreign exchange losses (excluding foreign exchange on processing), and the costs are expensed as incurred. Royalty costs are calculated monthly and expensed accordingly in the statement of profit or loss.

Marketing Expenses are the costs associated with Affiliates Marketing, Brand Spend, Other Marketing Taxes, Marketing Usage and Marketing Operational costs. Affiliate marketing expenses include commission paid to the affiliates and include both costs per acquisition and revenue-share agreements. Costs associated with marketing are expensed as incurred. Affiliate marketing cost is calculated monthly and expensed in the statement of profit or loss.

For the years reported in the Form 20-F, the company respectfully advises the Staff of the process involving the activities for affiliates marketing and payment to game suppliers as follows.

Affiliate Marketing

Affiliate Marketing relates to affiliates (or partners) for driving traffic, leads, or customers to the Groups platform, typically through marketing efforts such as referrals, links, or advertisements. The costs are measured as a percentage of chargeable revenue ((net gaming revenue less other deduction as agreed with the supplier) from customers and are recognized monthly in the consolidated statement of profit or loss. The amounts are reported under cash flows from operating activities in the statement of cash flows and are paid to the suppliers in accordance with the agreed payment terms.

Game Suppliers

Game suppliers relates to royalties paid to third-party gaming service providers for supplying games, software platforms or gaming content which is used on the Group’s websites. The costs are measured as a percentage of chargeable revenue (net gaming revenue less other deductions as agreed with the supplier) from customers and are recognized monthly in the consolidated statement of profit or loss. The amounts are reported under cash flows from operating activities in the statement of cash flows and are paid to the suppliers in accordance with the agreed payment terms.

Note 11.1 Exit from U.S. sportsbook market, page F-43

3.Please explain to us your consideration of presenting and disclosing the exit from the U.S. sportsbook market as discontinued operations in your financial statements for the years ended December 31, 2024 and 2023. Refer to the guidance in IFRS 5 and specifically the presentation and disclosure requirements of paragraphs 30 through 34.

Response:

The Company acknowledges the Staff’s comments and respectfully advised the Staff as follows:

During July 2024, the group implemented a restructuring plan to exit the U.S. sportsbook market (“U.S. sportsbook”). Management has assessed the exit in accordance with the criteria set out in IFRS 5.31 and IFRS 5.32 – Non-Current Assets Held for sale and Discontinued Operation. We considered the following in our assessment:

IFRS 5, para 31 states that “a component of an entity comprises operations and cash flows that can be clearly

distinguished, operationally and for financial reporting purposes, from the rest of the entity. In other words, a component of an entity will have been a cash-generating unit or a group of cash-generating units while being held for use”. Our U.S. Operations consisted of Online Casino (iGaming) and Sportsbooks and while we were able to measure the revenue contributions and assets associated with the Sportsbook operations separately from iGaming, we could not measure the direct expenditures associated with the Sportsbook at June 30, 2024, and therefore cannot distinguish the cash flows and losses associated with the Sportsbook operations at this date. Thus, we did not consider U.S. sportsbook to be a cash-generating unit or a group of cash-generating units, therefore not a component.

Nonetheless, we additionally considered the requirements IFRS 5.32 (a-c), and our analysis is as follows:

1)The U.S. sportsbook operation did not represent a major line of business or geographical area of operations as the revenue derived from the U.S. sportsbook constituted 1.3% of total group sportsbook revenue at June 30, 2024, and is therefore not a substantial revenue contribution to the group. At December 31, 2024, and December 31, 2023, the U.S. Sportsbook contributed 0.5% and 0.6% respectively to total group sportsbook revenue. Furthermore, it does not represent the only operations in the U.S. due the group having iGaming activity in the market as noted above. The Sportsbook assets were impaired by December 31, 2024;

2)The U.S. sportsbook operations was not part of a single coordinated plan to dispose of a major line of business or geographical area given the low revenue contribution from the U.S sportsbook; and

3)The Company’s intention in acquiring the U.S. sportsbook was not with a view to resale. The U.S. Sportsbook was acquired on January 1, 2023, the considered acquisition date as disclosed on page F-29, with the intention to grow the business within the U.S.

Management have also considered the disclosure guidance under IFRS 5.33 (a-d) and have determined that the disclosure guidance is not relevant to the U.S. sportsbook exit, as we have determined that this did not meet the definition of discontinued operations under paragraph 32 of IFRS 5, and therefore has not been classified as a discontinued operation.

Please direct any questions that you have with respect to the foregoing or if any additional supplemental information is required by the Staff, please contact the undersigned at +27 (82) 415 1670.

Sincerely,

Super Group (SGHC) Limited

/s/Alinda van Wyk

Chief Financial Officer