.3

MANAGEMENT’S DISCUSSION AND ANALYSIS

Year ended December 31, 2025

Background

This Management’s Discussion and Analysis (“MD&A”) has been prepared based on information available to DeFi Technologies Inc. (“we”, “our”, “us”, “DeFi” or the “Company”) containing information through April 2, 2026, unless otherwise noted.

The MD&A provides a detailed analysis of the Company’s operations and compares its financial results for the year ended December 31, 2025 and 2024. The December 31, 2025 annual consolidated financial statements and related notes of DeFi have been prepared in accordance with IFRS Accounting Standards as issued by the International Accounting Standards Board (“IFRS”). Please refer to the notes of the December 31, 2025 annual audited consolidated financial statements for disclosure of the Company’s significant accounting policies. Commencing with the Company’s June 30, 2025 quarter-end, the Company’s presentation currency is the U.S. dollar. Unless otherwise noted, all references to currency in this MD&A refer to U.S. dollars.

Additional information, including our Annual Information Form, have been filed electronically through “SEDAR+ and is available online under the Company’s SEDAR profile at www.sedarplus.ca.

Cautionary Statement Regarding Forward Looking Information

This MD&A contains “forward-looking information” within the meaning of that term under Canadian securities laws. This information relates to future events or future performance and reflects the Company’s expectations and assumptions regarding such future events and performance. Forward-looking information can be identified by the use of words such as, but not limited to, “plans”, “expects”, “project”, “predict”, “potential”, “is expected”, “budget”, “scheduled”, “estimates”, “forecasts”, “intends”, “anticipates”, or “believes” or variations (including negative variations) of such words and phrases, or statements that certain actions, events or results “may”, “could”, “would”, “might” or “will” be taken, occur or be achieved.

In particular, all statements, other than statements of historical facts, included in this MD&A that address activities, events or developments that management of the Company expects or anticipates will or may occur in the future contain forward-looking information, including but not limited to, statements with respect to:

| ● | financial, operational and other projections and outlooks as well as statements or information concerning future operation plans, objectives, performance, revenues, growth, acquisition strategies, profits or operating expenses of the Company and its subsidiaries; |

| ● | details and expectations regarding the Company’s investments in the decentralized finance (“DeFi”) industry and the Company’s Equity Investments in Digital Assets (as defined herein); |

| ● | expectations regarding revenue growth due to changes in the Company’s business strategy; |

| ● | expansion and growth of the Company’s Asset Management, Ventures and Infrastructure business lines; |

| ● | development of ETPs and partnerships and joint ventures with other companies; |

| ● | growth of assets under management (“AUM”); |

| ● | listing of ETPs; |

| ● | identifying and capitalizing on low-risk arbitrage opportunities within the digital asset market; |

| ● | digital asset staking, lending or trading transactions; |

| ● | the Company becoming more active in the stablecoin market in the future; |

| ● | the continued listing of the Company’s common shares on Nasdaq; |

| ● | DeFi Advisory and the development of digital asset treasury companies; |

| ● | anticipated lending and staking income and management fees charged on ETPs; |

| ● | hedging activities; |

| ● | the Company receiving the outstanding balance of BTC owed to it by Genesis; |

| ● | investment performance of ETPs, DeFi protocols and digital assets underlying ETPs and portfolio companies that the Company has invested in; |

| ● | additional locations and distribution channels coming online in 2026, and the Company being able to expand presence across Europe and Latin America, and bringing new regions, such as Africa and the Middle East, into the platform; |

| ● | the Company’s global expansion positioning the Company for long-term growth, leveraging strategic partnerships, market-first advantages, and increasing investor demand to strengthen its market leadership; |

| ● | future development of laws and regulations governing the DeFi industry, in particular in the United States; |

| ● | requirements for additional capital and future financing options; |

| ● | publishing and marketing plans; |

| ● | the availability of attractive investments that align with the Company’s investment strategy; |

| ● | future outbreaks of infectious diseases; |

| ● | the impact of climate change; |

| ● | the Company’s ability to maintain compliance with the minimum required closing bid price for continued listing on the Nasdaq Capital Market; and |

| ● | other expectations of the Company. |

2

Forward-looking information and statements above involve various risks and uncertainties. There can be no assurance that such statements will prove to be accurate, as actual results and future events could differ materially from those anticipated in such information. Important factors that could cause actual results to differ materially from the Company’s expectations are described in the Company’s documents filed from time to time with the applicable regulatory authorities and such factors include, but are not limited to, risks related to the staking and lending of cryptocurrencies, DeFi protocol tokens, or other digital assets; risks relating to momentum pricing and volatility of cryptocurrencies, DeFi protocol tokens, and other digital assets; cybersecurity threats, security breaches and hacks; the relative novelty of cryptocurrency exchanges and other trading venues; regulatory risks; hedging risk; the U.S. classification of crypto assets and the Investment Company Act of 1940; the issuance of crypto ETPs in the EU and non-EU countries; risk related the Company’s Ventures portfolio exposure; risks associated with the lending and staking of digital assets, risks related to the Company’s internal arbitrage and trading business, risks associated with banks cutting off services to businesses that provide cryptocurrency related services; the impact of geopolitical events; the further development and acceptance of digital and DeFi networks; trade errors; dependence on investment manager, discretion as to distributions and timing of withdrawals, discretion as to form of payment, risks and uncertainties associated with custodians of digital assets; conditions on equity investments in digital assets; development and acceptance of the digital asset network, digital asset audit risk, risk of total loss of equity investment in digital assets, risk of loss, theft or destruction of cryptocurrencies; risks associated with the irrevocability of transactions; risks associated with the potential failure to maintain the cryptocurrency networks; risks associated with the potential manipulation of blockchain; risks that miners may cease operations; risks related to insurance; risks related to the concentration of investments; risks related to competition; risk related to investments in private issuers and illiquid securities; risks related to cash flow, revenue and liquidity; risk management, risks related to the Company’s dependence on management personnel; risks related to macro-economic conditions; risks related to the availability or opportunities and competition for investments; risks related the share prices of investments; risks related to additional financing requirements; risks related to the return on investments; failure to develop and execute successful investment or trading strategies, risks related to the management of the Company’s growth; social, political, environmental, and economic risks in the countries in which the Company’s investment interests are located; risks related to hostilities, geo-political events and wars, risks related to the due diligence process undertaken by the Company in connection with investment opportunities; risks related to exchange-rate fluctuations; risks related to non-controlling interests; risks related to changes in legislation and regulations; risks related to the fact the Company is likely a passive foreign investment company for U.S. federal income tax purposes; risks associated with the Company’s limited operating history and no history of operating revenue and cash flow; risks associated with the Company having limited cash flow and funds in reserve which may not be sufficient to fund its ongoing activities at all times; risks associated with material weakness in the Company’s financial statements, risk related to the restatement of the Company’s historical financial statements, lack of comprehensive accounting guidance for digital assets under IFRS accounting standards; risks associated with conflicts of interest; litigation risk, risks associated with the volatility of the Company’s common shares market price and the Company’s ability to maintain compliance with the minimum required closing bid price for continued listing on the Nasdaq Capital Market, risks associated with share imbalances, risks associated the future dilution of shareholders’ interest in the Company; and risks associated with the Company’s history of never paying dividends; and other risks described herein including under the heading “Risks and Uncertainties”.

When relying on forward-looking information to make decisions, readers should ensure that the preceding information, the risks and uncertainties described in “Risks and Uncertainties” and the other contents of this MD&A are all carefully considered. The forward-looking information contained herein is current as of the date of this MD&A, and, except as may be required by applicable law, the Company disclaims any obligation or undertaking to publicly release any updates or revisions to any forward-looking information contained herein to reflect any change in expectations, estimates and projections with regard thereto or any changes in events, conditions or circumstances on which any information is based. Readers should not place undue importance on such forward-looking information and should not rely upon this information as of any other date. In addition to the disclosure contained herein, for more information concerning the Company’s various risks and uncertainties, please refer to the Company’s public filings available under its profile on SEDAR+ at www.sedarplus.ca and at www.cboe.ca.

With regard to all information included herein relating to companies in the Company’s Venture portfolio, the Company has relied on information provided by the investee companies and on publicly available information disclosed by the respective companies.

3

Overview of the Company

The Company is a publicly listed issuer on the CBOE Canada stock exchange trading under the symbol “DEFI” and the Nasdaq stock market in the United States under the symbol “DEFT”. The Company is a financial technology company that pioneers the convergence of traditional capital markets with the world of decentralized finance. The Company’s mission is to expand investor access to industry-leading decentralized technologies which it believes lie at the heart of the future of finance. On behalf of its shareholders and investors, it identifies opportunities and areas of innovation and builds and invests in new technologies and ventures in order to provide trusted, diversified exposure across the decentralized finance ecosystem. The Company does so through six distinct business lines: Asset Management, DeFi Alpha, Stillman Digital, DeFi Ventures, Reflexivity Research LLC and DeFi Advisory.

The Company’s condensed consolidated interim financial statements have been prepared in accordance with IFRS applicable to a going concern. Accordingly, they do not give effect to adjustments that would be necessary should the Company be unable to continue as a going concern and therefore be required to realize its assets and liquidate its liabilities and commitments in other than the normal course of business and at amounts different from those in the accompanying condensed consolidated interim financial statements.

Investment Pillars

DeFi operated through six core pillars during 2025:

Asset Management

The Company through its wholly-owned subsidiary Valour Inc. (“Valour”), and Valour Digital Securities Limited (“VDSL” and together with Valour Cayman, “Valour”) is developing Exchange Traded Products (“ETPs”) that synthetically track the value of a single DeFi protocol or a basket of protocols. ETPs simplify the ability for retail and institutional investors to gain exposure to DeFi protocols or basket of protocols as it removes the need to manage a self-custodial wallet, two-factor authentication, various logins, and other intricacies that are linked to managing a decentralized finance protocol portfolio.

The Company does not simply list ETP products and collect a management fee. The Company has monetized the entire issuance stack end to end:

| ● | Market making and liquidity provisioning |

| ● | Staking and yield generation on underlying assets |

DeFi Alpha

DeFi Alpha is a specialized trading desk within DeFi Technologies focused on opportunistic trading and arbitrage across the digital asset ecosystem. The desk seeks to generate returns by identifying attractive market dislocations and pricing inefficiencies, with opportunities sourced through deep market experience and strong counterparty relationships.

Its activities span both centralized and decentralized markets, with a focus on disciplined execution, prudent risk management, and capitalizing on opportunities as they arise.

4

Stillman Digital

Stillman Digital is a digital asset trading firm that provides OTC trading, liquidity solutions, and market-making services to institutional counterparties across global cryptocurrency markets.

DeFi Ventures

The Company, whether by itself or through its subsidiaries, invests in various companies and leading protocols across the decentralized finance ecosystem to build a diversified portfolio of decentralized finance assets.

Reflexivity Research LLC

Research Reflexivity LLC specializes in producing cutting-edge research reports for the cryptocurrency industry. Reflexivity has also focused on creating a large third-party distribution channel for its research, which has been accomplished by partnering with platforms such as CoinMarketCap, Beluga Inc, and others.

DeFi Advisory

DeFi Advisory positions the Company to further capitalize on the proliferation of public digital asset treasury companies being formed across global markets. With proven in-house infrastructure in ETPs, trading, custody, and research, DeFi Technologies is uniquely equipped to support these companies in navigating go-public transactions, producing research, managing digital asset portfolios, and executing institutional-grade trades, all under one roof.

Given the revenues generated during 2025 (with challenging growth prospects) by DeFi Advisory ($287,558) and Reflexivity Research ($533,000), the Company will discontinue separately reporting on these investment pillars commencing in Q1 2026. The minor revenues generated by these activities going forward will be included in an “other revenue” line as part of the main asset management business.

5

Highlights For The Year ended December 31, 2025:

Readers should refer to the Company’s Quarterly MD&A’s for a summary of all developments during 2025. The list below represents the most significant items during 2025.

New Product Launches

By December 31, 2025, Valour reached 102 listed ETPs and built a more diversified regulated digital asset shelf globally.

The Company’s growth to more than 100 listed ETPs is not just a product milestone. It reflects a simple strategic goal: to give investors optionality and the choice to allocate to the world’s top digital assets in a regulated, exchange-traded format, using the same brokerage and custody rails they already trust.

These are not only spot Bitcoin and Ether products. Our lineup spans many of the most important networks and themes shaping digital assets, giving investors exposure across the sector without wallets, private keys, and unregulated venues. The Company now offers the most diverse regulated digital asset ETP lineups globally, and that breadth is a durable competitive advantage.

Investors can review the full list of the Company’s ETP products on its website at www.valour.com.

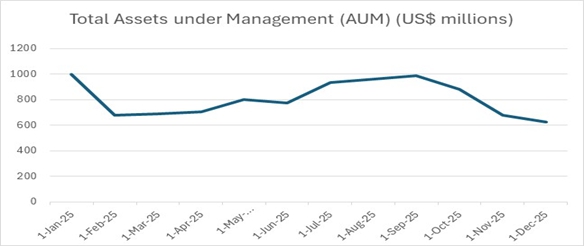

Valour’s Top ETPs by AUM

Valour’s AUM on December 31, 2025 was $622.3 million. Average AUM for 2025 increased to $809.9 million from $645.3 million 2024. Valour monetizes its AUM primarily through trading, staking, management fees, and trade-flow arbitrage. In addition to management fees, Valour retains staking yields as revenue, capturing value directly from the digital assets held in its ETPs. This vertically integrated model enables recurring, protocol-driven revenue as AUM grows. As of December 31, 2025, Valour’s ETPs with the highest AUM were:

| ● | VALOUR BTC: $226,518,547 |

| ● | VALOUR SOL: $176,086,342 |

| ● | VALOUR ETH: $61,907,800 |

| ● | VALOUR XRP: $38,395,788 |

| ● | VALOUR SUI: $25,850,564 |

| ● | VALOUR ADA: $24,221,997 |

6

A chart showing the development of the Company’s AUM is below:

Valour’s Global Expansion and Strategic Market Development

In 2025, we grew globally with meaningful progress across key markets and listings. We advanced our footprint through:

| ● | London Stock Exchange |

| ● | SIX Swiss Exchange |

| ● | B3 – Brazil Stock Exchange, including listings that established a strategic beachhead in LATAM |

Brazil matters because it is not just another listing. It is proof that we can bring our platform into new regulatory environments, connect to local market infrastructure, and build distribution pathways beyond our historical base.

Looking forward, the Company expects additional locations and distribution channels to come online in 2026, with particular focus on expanding our presence across Europe and Latin America, and bringing new regions into the platform such as Africa and the Middle East.

DeFi Technologies Announces Closing of US$100 Million Registered Direct Offering

DeFi Technologies announced the closing of a US$100 million registered direct offering led by cornerstone investor Galaxy Digital. Investors purchased 45,662,101 common shares and warrants to buy up to 34,246,577 additional shares at a combined price of US$2.19 per share and three-quarters of a warrant. Each whole warrant is exercisable immediately at US$2.63 and has a three-year term with an acceleration feature. The Company plans to use net proceeds to expand Valour’s ETP lineup, pursue digital-asset trading, lending and staking transactions, fund potential acquisitions, and advance recently announced growth initiatives.

7

Normal Course Issuer Bid (NCIB)

During the year ended December 31, 2025, the Company repurchased 1,235,900 shares for $2,769,629 representing an average purchase price of $2.24. All shares repurchased were cancelled. The Company’s current NCIB program allows for the purchase of up to 31,673,791 shares and runs until August 26, 2026 (or earlier if completed).

DeFi Technologies Announces Strategic Investment and Partnership with Canada’s Stablecorp, Backer of QCAD Canadian-Dollar Stablecoin

DeFi Technologies invested in and partnered with Stablecorp Inc. (“Stablecorp”) to help scale their QCAD product alongside Coinbase Ventures, Circle Ventures, Side Door Ventures, and other industry leaders. With RPAA oversight of payment service providers taking effect on September 8, 2025, and growing attention from the Bank of Canada and FCAC as retail CBDC work remains paused, compliant CAD stablecoins are positioned for payments, cross-border trade, payroll, and treasury use. Execution includes launching QCAD-integrated products through Valour and naming Stillman Digital as a preferred liquidity provider for on/off-ramps and mint/redeem flows, subject to certain conditions.

DeFi Technologies Invests in Continental Stablecoin Inc., Backers of cNGN, to Accelerate Regulated Stablecoin Adoption Across Africa

DeFi Technologies announced it invested in Continental Stablecoin Inc. (“Continental Stablecoin”), alongside Coinbase Ventures, Adaverse, and other industry leaders, to advance regulated local currency stablecoins across Africa with an initial focus on Nigeria’s cNGN. cNGN, issued by Wrapped CBDC Limited, had ~602.9 million tokens in circulation as of September 15, 2025, with more than 75,000 on-chain transactions and ~20.1 billion cNGN in cumulative volume. The investment was intended to align with DeFi Technologies’ strategy to support compliant, bank- and fintech-ready digital-asset infrastructure, complement the Company’s broader platform spanning liquidity provision for the cNGN stablecoin via Stillman Digital, and create cNGN related Valour ETPs in Europe.

Nasdaq Listing

On May 12, 2025, the Company announced that its common shares started trading on the Nasdaq Capital Market under the symbol “DEFT”. Upon commencement of trading on Nasdaq, the Company’s common shares ceased to be quoted on the OTC Markets. DeFi Technologies continues to trade on the CBOE Canada exchange (CBOE: “DEFI”) and the Börse Frankfurt exchange (GR: R9B)

SUBSQUENT EVENTS

Possible Filing Delay

On March 23, 2026, the Company announced it may experience a delay in filings its annual financial statements, management’s discussion and analysis, and related CEO and CFO certifications for the year ended December 31, 2025 (the “Annual Filings”) relating solely to the possible timing of receipt of a SOC 2 Type 2 report from a material third-party counterparty that is relevant to the Company’s audit procedures. The Company also announced that, in connection with the potential delay and default in the completion of the Annual Filings, the Company has made an application to the Ontario Securities Commission (the “OSC”) as principal regulator, to approve a temporary management cease trade order (the “MCTO”) under National Policy 12-203 – Management Cease Trade Orders (“NP 12-203”).

8

Outlook

DeFi continues to cement its leadership in regulated digital asset ETPs, with 102 listed ETPs. The Company remains focused on expanding investor access to secure, transparent, and compliant digital asset exposure.

DeFi Technologies also reiterated its focus on accelerating growth through product innovation and geographic expansion. In 2025, DeFi Technologies, through Valour, advanced distribution across regulated venues, including the London Stock Exchange and SIX Swiss Exchange, and established a strategic beachhead in Brazil through B3.

DeFi Technologies aims to be the global leading provider of asset management services and investment products worldwide with a scalable, vertically integrated platform of investment vehicles and capital markets infrastructure aimed at disrupting traditional, over-regulated, and inefficient markets for investments, primary, and secondary markets. The legacy system is captured by obsolete infrastructure, bloated with inefficient and expensive middlemen who impose misguided regulation, affecting investors and entrepreneurs alike.

The Company is building in both centralized and decentralized finance, positioning ourselves for the convergence of these paradigms over time which will provide a better path for payments, storage of value, and frictionless capital markets.

The Company plans to announce a series of internally incubated innovations across these fields, lowering costs, increasing value added and scalability, enabling unparalleled customer value.

The Company is advancing second-generation products designed to be more institutionally compatible and suited to larger pools of capital. This next phase includes but is not limited to UCITS type fund structures (the EU’s Undertaking for the Collective Investment in Transferable Securities), actively managed certificates and exchange traded notes, fund of funds structures, and additional institutionally focused vehicles, which are intended to broaden distribution, expand addressable liquidity, and increase the durability of AUM.

The Company’s global expansion positions the Company for long-term growth, leveraging strategic partnerships, market-first advantages, and increasing investor demand to strengthen its market leadership.

The Company also constantly evaluates adjacent businesses that can add non-AUM driven revenues that perform well in both crypto bull and bear market cycles. The Company’s acquisition of Stillman Digital in October 2024 is an example of such a business. In terms of new initiatives, the Company expects to become more active in the stablecoin market going forward as demonstrated by its venture investments in Stablecorp and Continental Stablecoin.

9

Digital Assets, Digital assets loaned and Digital assets Staked

As at December 31, 2025, the Company’s digital assets consisted of the below digital currencies, with a fair value of $515,586,931 (December 31, 2024 - $ 555,838,900). Digital currencies are recorded at their fair value on the date they are acquired and are revalued to their current market value at each reporting date. Fair value is determined by taking the mid-point price at 17:30 CET from Kraken, Bitfinex, Binance, Coinbase, Bitstamp, Bybit OKX, Vinter, Compass and Gate.IO and other exchanges consistent with the final terms for each ETP. Fair value for Mobilecoin, Shyft, Blocto, Maps, Oxygen, Boba Network, Saffron.finance, Clover, Sovryn, Wilder World, Pyth and Volmex is determined by taking the last closing price for the day (UTC time) from www.coinmarketcap.com.

| December 31, 2025 | December 31, 2024 | |||||||

| $ | $ | |||||||

| Current digital assets | ||||||||

| Digital assets | 356,450,053 | 276,853,787 | ||||||

| Digital assets loaned | 87,326,227 | 38,618,758 | ||||||

| Digital assets staked | 38,986,741 | 240,031,645 | ||||||

| Total current digital assets | 482,763,021 | 555,504,190 | ||||||

| Non-current digital assets | ||||||||

| Digital assets | 62,367 | 334,710 | ||||||

| Digital assets loaned | 32,761,543 | - | ||||||

| Total non-current digital assets | 32,823,910 | 334,710 | ||||||

| Total digital assets | 515,586,931 | 555,838,900 | ||||||

In addition to the above noted digital assets, the Company has the following equity investments at fair value through profit and loss (“FVTPL”). See Note 7 of the audited consolidated financial statements for the year ended December 31, 2025 for further details.

| December 31, 2025 | ||||||||||||||||||||||||

| Current | Long Term | Total | ||||||||||||||||||||||

| Quantity | Amount | Quantity | Amount | Quantity | Amount | |||||||||||||||||||

| Fund A - Solana (SOL) | 192,949.9577 | $ | 19,860,832 | 220,396.5353 | $ | 22,685,979 | 413,346.4930 | $ | 42,546,811 | |||||||||||||||

| Fund A - Avalanche (AVAX) | 503,720.0812 | $ | 5,253,822 | 232,861.4009 | $ | 2,428,755 | 736,581.4821 | $ | 7,682,577 | |||||||||||||||

| $ | 25,114,654 | $ | 25,114,734 | $ | 50,229,388 | |||||||||||||||||||

| Fund B - Solana (SOL) | 470,185.9000 | $ | 50,297,302 | 294,049.0000 | $ | 31,455,370 | 764,234.9000 | $ | 81,752,672 | |||||||||||||||

| $ | 50,297,302 | $ | 31,455,370 | $ | 81,752,672 | |||||||||||||||||||

| Total | $ | 75,411,956 | $ | 56,570,104 | $ | 131,982,060 | ||||||||||||||||||

| December 31, 2024 | ||||||||||||||||||||||||

| Current | Long Term | Total | ||||||||||||||||||||||

| Quantity | Amount | Quantity | Amount | Quantity | Amount | |||||||||||||||||||

| Fund A - Solana (SOL) | 216,379.2216 | $ | 30,886,684 | 244,331.9458 | $ | 34,876,748 | 460,711.1675 | $ | 65,763,432 | |||||||||||||||

| Fund A - Avalanche (AVAX) | 223,905.1900 | $ | 6,020,811 | 707,540.4100 | $ | 19,025,762 | 931,445.6000 | $ | 25,046,572 | |||||||||||||||

| $ | 36,907,495 | $ | 53,902,510 | $ | 90,810,004 | |||||||||||||||||||

| Fund B - Solana (SOL) | 626,365.7000 | $ | 89,409,506 | 540,869.9000 | $ | 77,205,553 | 1,167,235.6000 | $ | 166,615,059 | |||||||||||||||

| Total | $ | 126,317,001 | $ | 131,108,063 | $ | 257,425,063 | ||||||||||||||||||

10

The Company’s holdings of digital assets consist of the following:

| December 31, 2025 | December 31, 2024 | |||||||||||||||

| Quantity | $ | Quantity | $ | |||||||||||||

| Binance Coin (BNB) | 1,763.4867 | 1,520,530 | 2,558.9747 | 1,818,875 | ||||||||||||

| Bitcoin (BTC) | 2,596.9563 | 223,491,846 | 2,705.7708 | 228,997,191 | ||||||||||||

| Ethereum (ETH) | 21,329.9035 | 63,656,646 | 20,676.9254 | 70,398,197 | ||||||||||||

| Cardano (ADA) | 69,150,950.0310 | 23,565,970 | 69,671,396.7593 | 60,542,418 | ||||||||||||

| Polkadot (DOT) | 3,340,140.2001 | 6,035,593 | 2,766,149.1833 | 18,869,900 | ||||||||||||

| Solana (SOL) | 169,185.2128 | 21,097,592 | 43,414.4191 | 8,654,328 | ||||||||||||

| Uniswap (UNI) | 399,616.8814 | 2,332,473 | 421,450.3048 | 5,712,570 | ||||||||||||

| USDC | - | 4,461,378 | 251,357 | |||||||||||||

| USDT | - | 18,098,752 | 5,271,542 | |||||||||||||

| Litecoin (LTC) | 11,073.8030 | 851,800 | 541.8400 | 56,378 | ||||||||||||

| Dogecoin (DOGE) | 56,534,119.7635 | 6,828,612 | 17,545,096.4535 | 5,708,209 | ||||||||||||

| Cosmos (ATOM) | 12,005.8560 | 23,143 | 735.9223 | 4,605 | ||||||||||||

| Avalanche (AVAX) | 461,501.5177 | 5,740,226 | 125,979.5440 | 4,612,185 | ||||||||||||

| Polygon (POL) | 304,295.6891 | 31,088 | 183,654.4400 | 82,957 | ||||||||||||

| Ripple (XRP) | 21,146,529.3119 | 39,186,475 | 17,223,963.4000 | 36,437,139 | ||||||||||||

| Enjin (ENJ) | 576,307.9792 | 15,849 | 127,360.9806 | 27,938 | ||||||||||||

| Tron (TRX) | 663,171.3819 | 187,723 | 341,529.3057 | 89,013 | ||||||||||||

| Terra Luna (LUNA) | 141,177.2041 | 13,436 | 205,057.0760 | - | ||||||||||||

| Shiba Inu (SHIB) | 20,643,542,012.0300 | 143,214 | 142,074,547.6000 | 2,995 | ||||||||||||

| Pyth Network (PYTH) | 4,935,058.3767 | 280,805 | 3,444,248.6000 | 876,946 | ||||||||||||

| AAVE (AAVE) | 4,429.5388 | 652,127 | 2,333.3875 | 735,390 | ||||||||||||

| Algorand (ALGO) | 1,380,335.0800 | 153,904 | 90,930.8700 | 30,180 | ||||||||||||

| Aptos Mainnet (APT) | 517,026.2356 | 875,222 | 287,849.7000 | 2,565,403 | ||||||||||||

| Arweave (AR) | 64,940.4200 | 223,096 | 14,202.0100 | 234,942 | ||||||||||||

| Aerodome (AERO0X91) | 2,113,572.4104 | 917,924 | - | - | ||||||||||||

| Arbitrum (ARB) | 1,489,777.0200 | 280,923 | 24.0000 | 17 | ||||||||||||

| Bitcoin Cash (BCH) | 860.1464 | 511,921 | 25.4800 | 11,075 | ||||||||||||

| Core (CORE) | 12,500,445.6036 | 1,377,549 | 3,995,185.7910 | 4,300,418 | ||||||||||||

| Curve DAO Token (CRV) | 3,939,395.2500 | 1,442,868 | 10,295.1200 | 9,307 | ||||||||||||

| EOS (EOS) | 1,513.8200 | 1,181 | 13,419.9100 | 10,374 | ||||||||||||

| Europa Coin (EURC) | 605,795.2800 | 708,780 | - | - | ||||||||||||

| Fetch.ai (FET) | 4,619,586.9000 | 946,091 | 561,613.1000 | 732,400 | ||||||||||||

| Filecoin (FIL) | 83,678.3922 | 109,612 | 8,471.8100 | 41,952 | ||||||||||||

| Sonic (FTM) | - | - | 1,342,653.2600 | 937,490 | ||||||||||||

| The Graph (GRT) | 542,238.9100 | 18,229 | 1,620.3700 | 323 | ||||||||||||

| Hedera (HBAR) | 76,729,676.9089 | 8,317,073 | 49,611,593.1918 | 13,883,790 | ||||||||||||

| Internet Computer (ICP) | 1,778,949.0942 | 4,866,716 | 1,436,614.1074 | 14,543,861 | ||||||||||||

| Immutable (IMX) | 274,878.9400 | 61,176 | 10,992.0200 | 14,345 | ||||||||||||

| Injective (INJ) | 335,577.3200 | 1,463,990 | 56,329.4200 | 1,136,125 | ||||||||||||

| Jupiter (JUP) | 3,089,314.6000 | 583,880 | 499,299.1000 | 423,006 | ||||||||||||

| Kusama (KSM) | 470.3390 | 3,198 | 470.3400 | 15,540 | ||||||||||||

| Lido DAO (LDO) | 513,196.1600 | 300,384 | 36,961.1000 | 68,633 | ||||||||||||

| Chainlink (LINK) | 347,418.3828 | 4,295,173 | 239,057.7313 | 4,932,495 | ||||||||||||

| NEAR Protocol (NEAR) | 1,701,315.2684 | 2,553,372 | 1,300,877.8800 | 163 | ||||||||||||

| Optimism (OP) | 173,791.6300 | 46,248 | 15,436.4300 | 6,609,639 | ||||||||||||

| MANTRA (OM) | 453,091.4000 | 31,807 | - | 27,245 | ||||||||||||

| Pendle (PDL) | 182,478.7000 | 343,772 | 31,265.4000 | 159,454 | ||||||||||||

| Quant (QNT) | 1,014.7880 | 71,156 | 1,086.7000 | 114,864 | ||||||||||||

| Ripple USD (RLUSD) | 50,126.0000 | 50,126 | - | - | ||||||||||||

| RENDERSOL (RNDR) | 1,703,278.0201 | 2,193,856 | 162,158.1000 | 1,127,499 | ||||||||||||

| THORChain (RUNE) | 269,953.8000 | 151,768 | 91,192.7000 | 423,581 | ||||||||||||

| Sei Network (SEI1) | 16,419,686.8978 | 1,848,857 | 2,078,991.0000 | 851,347 | ||||||||||||

| SKY Governance Token (SKY) | 645,038.0000 | 37,735 | - | - | ||||||||||||

| Stacks (STX) | 47,106.4000 | 11,744 | 203,450.0000 | 97,432 | ||||||||||||

| Sui (SUI) | 14,683,690.6345 | 16,459,983 | 10,785,375.0000 | 45,866,964 | ||||||||||||

| SushiSwap (SUSHI) | 135.0000 | 37 | 39,426.6800 | 53,068 | ||||||||||||

| Bittensor (TAO) | 22,107.9024 | 4,906,095 | 9,851.6400 | 4,443,335 | ||||||||||||

| The TON Coin (TON) | 454,318.1948 | 739,494 | 405,657.4300 | 2,266,408 | ||||||||||||

| Wormhole (W) | 4,760,219.0000 | 157,563 | 722,403.0000 | 213,761 | ||||||||||||

| Tether Gold (XAUT6) | 34.4628 | 149,372 | - | - | ||||||||||||

| dogwifhat (WIF) | 56,581.9600 | 15,277 | - | - | ||||||||||||

| Worldcoin (WLD2) | 2,002,365.2100 | 969,345 | 49,314.1000 | 106,139 | ||||||||||||

| Stellar (XLM) | 3,704,385.3200 | 753,012 | 140,437.4500 | 47,636 | ||||||||||||

| Tezos (XTZ) | 14,912.2100 | 7,259 | 17,822.5100 | 22,902 | ||||||||||||

| StarkNet (STRK1) | 2,990,189.0056 | 231,441 | - | - | ||||||||||||

| Sonic Labs (SONICLABS) | 3,959,492.2712 | 300,086 | - | - | ||||||||||||

| Akash Network (AKT) | 375,586.0011 | 135,737 | - | - | ||||||||||||

| Kaspa (KAS) | 24,576,822.7965 | 1,064,176 | - | - | ||||||||||||

| Official Trump (TRUMP) | 2,309.3700 | 10,891 | - | - | ||||||||||||

| Mantle (MNT) | 259,308.9369 | 251,037 | - | - | ||||||||||||

| Story (IP) | 5,951.7992 | 10,187 | - | - | ||||||||||||

| Crypto.com (CRO) | 1,453,014.1410 | 132,805 | - | - | ||||||||||||

| Hyperliquid (HYPE) | 32,103.2182 | 830,677 | - | - | ||||||||||||

| OKB (OKB) | 276.2829 | 30,051 | - | - | ||||||||||||

| IOTA (IOTA) | 1,233,469.0000 | 102,131 | - | - | ||||||||||||

| Ondo (ONDO) | 1,711,993.3233 | 634,291 | - | - | ||||||||||||

| Theta Token (THETA) | 100,410.4000 | 26,749 | - | - | ||||||||||||

| Celestia (TIA) | 111,295.8400 | 52,209 | - | - | ||||||||||||

| Flare (FLR) | 3,689,429.0635 | 39,108 | - | - | ||||||||||||

| Pi Network (PI) | 126,934.2148 | 25,895 | - | - | ||||||||||||

| Ethna (ENA) | 1,686,126.1900 | 340,092 | - | - | ||||||||||||

| Four (FORM) | 31,111.1000 | 10,777 | - | - | ||||||||||||

| Virtuals Protocol (VIRTUAL) | 1,776,320.7111 | 1,179,832 | - | - | ||||||||||||

| VeChain (VET) | 4,978,553.8000 | 52,773 | - | - | ||||||||||||

| Penut the Squirrel (PNUT) | 445,601.2200 | 30,657 | - | - | ||||||||||||

| Pepe (PEPE) | 40,164,090,458.7000 | 24,082 | - | - | ||||||||||||

| Zcash (ZEC) | - | 32,569 | - | - | ||||||||||||

| Other Coins | 1,903,696,977.2146 | 42,722 | 145,501.2142 | 26,475 | ||||||||||||

| Current | 482,763,021 | 555,499,721 | ||||||||||||||

| Clover (CLV) | - | - | 500,000.0000 | 31,910 | ||||||||||||

| Solana (SOL) | 196,500.0000 | 24,471,703 | - | - | ||||||||||||

| SUI (SUI) | 8,327,991.5556 | 8,289,840 | - | - | ||||||||||||

| Wilder World (WILD) | - | - | 148,810.0000 | 99,465 | ||||||||||||

| Other Coins | 271,406,137.0826 | 62,367 | 130,458,836.6519 | 207,804 | ||||||||||||

| Long-Term | 32,823,910 | 339,179 | ||||||||||||||

| Total Digital Assets | 515,586,931 | 555,838,900 | ||||||||||||||

11

The continuity of digital assets for the years ended December 31, 2025 and 2024:

| December 31, 2025 | December 31, 2024 | |||||||

| Opening balance | $ | 555,838,900 | $ | 370,469,700 | ||||

| Digital assets acquired | 273,427,760 | 401,118,676 | ||||||

| Digital assets disposed | (87,878,518 | ) | (514,217,138 | ) | ||||

| Digital assets earned from staking, lending and fees | 13,072,141 | 26,075,437 | ||||||

| Realized gain (loss) on digital assets | 48,283,105 | 306,744,937 | ||||||

| Net change in unrealized gains and losses on digital assets | (282,272,597 | ) | (34,372,022 | ) | ||||

| Settlement of Genesis loan | (6,100,598 | ) | - | |||||

| Digital assets transferred in from (out to) equity investments at FVTPL | 2,749,352 | - | ||||||

| Foreign exchange gain (loss) / Fees / Other | (1,532,614 | ) | 19,310 | |||||

| $ | 515,586,931 | $ | 555,838,900 | |||||

Digital assets held by counterparty for the period ended December 31, 2025 and December 31, 2024 are as follows:

| December 31, 2025 | December 31, 2024 | |||||||

| Counterparty A | $ | 41,304,262 | $ | 6,918,688 | ||||

| Counterparty C | 3,460,154 | 719,776 | ||||||

| Counterparty E | 1,492,892 | 7,007,055 | ||||||

| Counterparty F | 25,061,967 | 6,809,705 | ||||||

| Counterparty H | 171,980,818 | 58,438,204 | ||||||

| Counterparty K | 218,232,056 | 125,188,614 | ||||||

| Counterparty M | 4,954,135 | 3,787,814 | ||||||

| Other | 1,451,800 | 1,942,823 | ||||||

| Self custody | 47,648,847 | 345,026,221 | ||||||

| Total | $ | 515,586,931 | $ | 555,838,900 | ||||

Digital Assets held by lenders

The Company and Genesis Global Capital LLC (“Genesis”) entered into that certain master loan agreement (the “MLA”). Pursuant to the MLA and the loan term sheet dated September 9, 2022 (the “Term Sheet”), Genesis loaned $6,000,000 to Valour as an open term loan (the “Loan”) pursuant to the terms and conditions of the MLA and Term Sheet. As collateral for the Loan, Valour initially posted 362 BTC with Genesis, which was later increased to 475 BTC.

On January 19, 2023, Genesis and its group of companies filed for bankruptcy protection in the U.S. pursuant to a ‘Chapter 11’ bankruptcy filing under the U.S. Bankruptcy Code and listed the Company as a creditor.

On June 26, 2024, the Court entered an order (the “Order”) granting motion for relief from stay and allowing Genesis to exercise set off rights permitting the parties to set off any Company obligations ($6,000,000 loan plus interest) with corresponding Genesis obligations (475 BTC). According to the exhibit attached to the Order, the Company owed Genesis $5,990,953.70 in principal and $109,644 in interest against collateral of 475 BTC valued at $10,018,691, resulting in a claim by the Company against Genesis in the amount of $3,909,047 or 185.3 BTC. It was then agreed that the parties could set off leaving the Company with $3. 9 million which amounted to 185.3 BTC.

By the end of 2025, the Company had already received 115.62 BTC. Since DeFi and Valour previously received a further 1.7 BTC in October 2025, the outstanding balance is 67.98 BTC. Accordingly, the Company expects to receive up to 67.98 BTC in the future.

The digital assets and loan payable were previously recorded gross on the balance sheet at $6,100,598 and $6,100,598, respectively, with the digital assets being written down to the value of the loan payable. After the approval of the motion on June 26, 2024, the Company obtained the legally enforceable right to set off the digital assets being held as collateral against the loan payable. As a result, the Company has netted the asset and liability on the statement of financial position, reducing both the Company’s digital assets and loan payable by $6,100,598, which represents the principal amount of the loan plus interest.

12

Following the court approved set-off, the remaining exposure for the Genesis loan is 68 BTC. Considering Genesis’ low credit quality due to its bankruptcy, the Company has applied a loss rate approach of 75% to calculate it’s expected credit loss on digital assets held by Genesis based on management’s best estimate. The expected credit loss of $4,478,675 on these 68 BTC has been recorded under realized and net change in unrealized (loss) gain on digital assets in the consolidated statement of income.

As of December 31, 2025, digital assets held by lenders as collateral consisted of the following:

| Number of coins on loan | Fair Value | |||||||

| Bitcoin (BTC) | 67.9793 | $ | 1,492,892 | |||||

| Total | 67.9793 | $ | 1,492,892 | |||||

As of December 31, 2024, digital assets held by lenders as collateral consisted of the following:

| Number of coins on loan | Fair Value | |||||||

| Bitcoin (BTC) | 365.4480 | 7,007,055 | ||||||

| Total | 365.4480 | 7,007,055 | ||||||

As at December 31, 2024, the 365.4480 Bitcoin held by Genesis as collateral against a loan has been written down to $7,007,055, the fair value of the loan and interest held with Genesis.

In the normal course of business, the Company enters into open-ended lending arrangements with certain financial institutions, whereby the Company loans certain fiat and digital assets in exchange for interest income. The Company can demand the repayment of the loans and accrued interest at any time. The digital assets on loan are included in digital assets balances above.

Digital Assets loaned

As of December 31, 2025, the Company loaned select digital assets to borrowers at annual rates ranging from approximately 1.98% to 12.00% and accrued interest on a monthly basis. The digital assets on loan are measured at fair value through profit and loss.

As of December 31, 2024, the Company has loaned select digital assets to borrowers at annual rates ranging from approximately 3.25% to 5.5% and accrued interest on a monthly basis. The digital assets on loan are measured at fair value through profit and loss.

As of December 31, 2025, digital assets on loan consisted of the following:

| Number of coins on loan | Fair Value | Fair Value Share | ||||||||||

| Bitcoin (BTC) | 420.0000 | 36,894,425 | 31 | % | ||||||||

| Ethereum (ETH) | 8,000.0000 | 23,879,570 | 20 | % | ||||||||

| Solana (SOL) | 326,500.0000 | 40,661,634 | 34 | % | ||||||||

| SUI (SUI) | 18,737,981.0000 | 18,652,141 | 16 | % | ||||||||

| Total | 19,072,901.0000 | 120,087,770 | 100 | % | ||||||||

As of December 31, 2024, digital assets on loan consisted of the following:

| Number of coins on loan | Fair Value | |||||||

| Current | ||||||||

| Bitcoin (BTC) | 120.0000 | 11,379,938 | ||||||

| Ethereum (ETH) | 8,000.0000 | 27,238,820 | ||||||

| Total current digital assets on loan | 8,120.0000 | 38,618,758 | ||||||

| Total | 8,120.0000 | 38,618,758 | ||||||

13

The digital assets loaned are classified as follows:

| Number of coins on loan | Fair Value | |||||||

| Current | ||||||||

| Bitcoin (BTC) | 420.0000 | 36,894,425 | ||||||

| Ethereum (ETH) | 8,000.0000 | 23,879,570 | ||||||

| Solana (SOL) | 130,000.0000 | 16,189,931 | ||||||

| SUI (SUI) | 10,409,989.4444 | 10,362,301 | ||||||

| Total current digital assets on loan | 10,548,409.4444 | 87,326,227 | ||||||

| Long-Term | ||||||||

| Solana (SOL) | 196,500.0000 | 24,471,703 | ||||||

| SUI (SUI) | 8,327,991.5556 | 8,289,840 | ||||||

| Total long-term digital assets on loan | 8,524,491.5556 | 32,761,543 | ||||||

| Total | 19,072,901.0000 | 120,087,770 | ||||||

As of December 31, 2025, the digital assets on loan by significant borrowing counterparty is as follow:

| Interest rates | Number of coins on loan | Fair Value | Geography | Fair Value Share | ||||||||||||

| Counterparty A | 12% | 326,500.0000 | 40,661,634 | Grand Cayman | 34 | % | ||||||||||

| Counterparty F | 1.94% - 4.75% | 18,739,981.0000 | 24,622,033 | UAE | 21 | % | ||||||||||

| Counterparty H | 3.75% - 4.5% | 6,420.0000 | 54,804,103 | Switzerland | 46 | % | ||||||||||

| Total | 19,072,901.0000 | 120,087,770 | 100 | % | ||||||||||||

| Current | ||||||||||||||||

| Counterparty A | 130,000.0000 | 16,189,931 | Grand Cayman | 13 | % | |||||||||||

| Counterparty F | 10,411,989.4444 | 16,332,193 | UAE | 14 | % | |||||||||||

| Counterparty H | 6,420.0000 | 54,804,103 | Switzerland | 46 | % | |||||||||||

| Total current digital assets on loan | 10,548,409.4444 | 87,326,227 | 73 | % | ||||||||||||

| Long-term | ||||||||||||||||

| Counterparty A | 196,500.0000 | 24,471,703 | Grand Cayman | 20 | % | |||||||||||

| Counterparty F | 8,327,991.5556 | 8,289,840 | UAE | 7 | % | |||||||||||

| Total long-term digital assets on loan | 8,524,491.5556 | 32,761,543 | 27 | % | ||||||||||||

| Total loaned digital assets | 19,072,901.0000 | 120,087,770 | 100 | % | ||||||||||||

As of December 31, 2024, the digital assets on loan by significant borrowing counterparty is as follow:

| Interest rates | Number of coins on loan | Fair Value | Geography | Fair Value Share | ||||||||||||

| Current | ||||||||||||||||

| Counterparty F | 4.75% | 2,000.0000 | 6,809,705 | UAE | 18 | % | ||||||||||

| Counterparty H | 3.25% to 5.50% | 6,120.0000 | 31,809,053 | Switzerland | 82 | % | ||||||||||

| Total current digital assets on loan | 8,120.0000 | 38,618,758 | 100 | % | ||||||||||||

| Total | 8,120.0000 | 38,618,758 | 100 | % | ||||||||||||

The Company’s digital assets on loan are exposed to credit risk. The Company limits its credit risk by placing its digital assets on loan with high credit quality financial institutions that have sufficient capital to meet their obligations as they come due and on which the Company has performed internal due diligence procedures. The Company’s due diligence procedures may include, but are not limited to, review of the financial position of the borrower, review of the internal control practices and procedures of the borrower, review of market information, and monitoring the Company’s risk exposure thresholds. Digital asset loan receivables are assessed for expected credit losses under IFRS 9 using a loss-rate approach. Counterparty A is subject to a 1% Stage 1 expected credit loss, driven by the recall penalty. The $248,000 ECL on these coins has been expensed to bad debt expense. Counterparty H is not subject to any expected credit loss due to its recallability without penalty. The Company does not hold any collateral or other credit enhancements related to these loans.

14

The fair value of the SUI digital assets on loan include a discount for lack of marketability since the SUI coins are locked and not freely transferrable as at December 31, 2025. These coins unlock intermittently through April 2028. The DLOM was determined using the Finerty model. The model works by treating this loss of marketability as the equivalent of a European put option, which provides protection against price declines during the period the assets cannot be sold. By estimating the value of such a hypothetical put option, based on factors like the underlying stock price, volatility, risk-free rate, and expected holding period. No separate ECL was recorded for the SUI digital assets as management feels that any relevant default risk is captured in the fair value assumptions of the digital assets. The SUI digital assets are considered a level 3 in the financial instrument hierarchy.

| Borrower | Asset | Quantity | Current | Non-current | Gross Total | ECL | Net Total | |||||||||||||||||||

| Counterparty A | SOL | 326,500.00 | 16,189,931 | 24,719,701 | 40,909,632 | (248,000 | ) | 40,661,632 | ||||||||||||||||||

| Counterparty H | BTC | 420.00 | 36,894,425 | - | 36,894,425 | - | 36,894,425 | |||||||||||||||||||

| Counterparty H | ETH | 6,000.00 | 17,909,678 | - | 17,909,678 | - | 17,909,678 | |||||||||||||||||||

| Counterparty F | ETH | 2,000.00 | 5,969,893 | - | 5,969,893 | - | 5,969,893 | |||||||||||||||||||

| Counterparty F | SUI | 18,737,981.00 | 10,362,301 | 8,289,841 | 18,652,142 | - | 18,652,142 | |||||||||||||||||||

| 87,326,228 | 33,009,542 | 120,335,770 | (248,000 | ) | 120,087,770 | |||||||||||||||||||||

As of December 31, 2025, the Company has staked select digital assets to borrowers at annual rates ranging from approximately 1.24% to 14.93% and accrue rewards as they are earned. The digital assets staked are measured at fair value through profit and loss. As of December 31, 2024, the Company has staked select digital assets to borrowers at annual rates ranging from approximately 2.95% to 9.70% and accrue rewards as they are earned. The digital assets staked are measured at fair value through profit and loss. As of December 31, 2024, the Bitcoin staked digital assets were locked up until January 2025.

As of December 31, 2025, digital assets staked consisted of the following:

| Number of coins staked | Fair Value | Fair Value Share | ||||||||||

| Ethereum (ETH) | 128.0536 | 376,190 | 1 | % | ||||||||

| Bitcoin (BTC) | 300.0000 | 26,747,151 | 69 | % | ||||||||

| Cardano (ADA) | 43,639.3760 | 15,470 | 0 | % | ||||||||

| Core (CORE) | 12,017,441.5404 | 1,325,524 | 3 | % | ||||||||

| Polkadot (DOT) | 2,595,690.3230 | 4,762,573 | 12 | % | ||||||||

| Solana (SOL) | 0.5094 | 64 | 0 | % | ||||||||

| Hyperliquid (HYPE) | 25,600.4618 | 662,417 | 2 | % | ||||||||

| Hedera (HBAR) | 22,663,998.5645 | 2,463,577 | 6 | % | ||||||||

| Internet Computer (ICP) | 970,082.8229 | 2,633,775 | 7 | % | ||||||||

| Total | 38,316,881.6517 | 38,986,741 | 100 | % | ||||||||

15

As of December 31, 2024, digital assets staked consisted of the following:

| Number of coins staked | Fair Value | Fair Value Share | ||||||||||

| Bitcoin | 1,803.0000 | 170,996,662 | 71 | % | ||||||||

| Cardano | 57,965,439.1383 | 50,371,939 | 21 | % | ||||||||

| Ethereum | 32.0000 | 108,955 | 0 | % | ||||||||

| Core | 3,415,479.8499 | 3,676,423 | 2 | % | ||||||||

| Polkadot | 1,941,230.3100 | 13,244,432 | 6 | % | ||||||||

| Solana | 10,526.4620 | 1,633,634 | 1 | % | ||||||||

| Total | 63,334,510.7602 | $ | 240,031,645 | 100 | % | |||||||

As of December 31, 2025, the digital assets staked by significant borrowing counterparty is as follow:

| Interest rates | Number of coins staked | Fair Value | Geography | Fair Value Share | ||||||||||||

| Counterparty H | 2.76% - 7.67% | 23,634,179.8442 | 5,097,352 | Switzerland | 13 | % | ||||||||||

| Counterparty M | 2.87% | 32.0023 | 95,663 | United States | 0 | % | ||||||||||

| Self custody | 2.3% - 14.28% | 14,682,669.8053 | 33,793,726 | Switzerland | 87 | % | ||||||||||

| Total | 38,316,881.6517 | 38,986,741 | 100 | % | ||||||||||||

As of December 31, 2024, the digital assets staked by significant borrowing counterparty is as follow:

| Interest rates | Number of coins staked | Fair Value | Geography | Fair Value Share | ||||||||||||

| Counterparty B | 2.95% | 57,965,439.1383 | 50,371,939 | Switzerland | 21 | % | ||||||||||

| Counterparty M | 4.00% | 32.0000 | 108,955 | United States | 0 | % | ||||||||||

| Self custody | 3.00% to 8.02% | 5,369,071.6219 | 189,550,751 | Switzerland | 79 | % | ||||||||||

| Total | 63,334,542.7602 | 240,031,645 | 100 | % | ||||||||||||

The Company’s digital assets staked are exposed to market risk, liquidity risk, lockup duration risk, loss or theft of assets and return duration risk. These risks include:

| a) | Ethereum and Polkdot staking exposes the Company to an unbounding period liquidity restriction (approximately 28 days), during which time the tokens remain locked and do not earn rewards once unbounding has commenced. |

| b) | Polkadot, CORE and Hype staking may expose the Company to validator misconduct risk |

| c) | Bitcoin staking involves timelock risk, such that the coins are locked until expiry of the timelock and require a redemption transaction after expiry. |

| d) | BTC staking is described by the protocol as self-custodied with no wrapping, bridging or smart contract exposure. |

The Company places allocation limits by counterparty and only deals with high credit quality financial institutions that are believed to have sufficient capital to meet their obligations as they come due and on which the Company has performed internal due diligence procedures. The Company’s due diligence procedures may include, but are not limited to, review of the financial position of the counterparty, review of the internal control practices and procedures of the counterparty, review of market information, and monitoring the Company’s risk exposure thresholds. As of December 31, 2025 and 2024, the Company does not expect a material loss on any of its digital assets staked. While the Company intends to only transact with counterparties that it believes to meets the Company staking policy criteria, there can be no assurance that a counterparty will not default and that the Company will not sustain a material loss on a transaction as a result.

16

EQUITY INVESTMENTS IN DIGITAL ASSETS FUNDS AT FAIR VALUE THROUGH PROFIT AND LOSS

Equity investments were as follows at December 31, 2025 and December 31,2024:

| December 31, 2025 | ||||||||||||||||||||||||

| Current | Long Term | Total | ||||||||||||||||||||||

| Quantity | Amount | Quantity | Amount | Quantity | Amount | |||||||||||||||||||

| Fund A - Solana (SOL) | 192,949.9577 | $ | 19,860,832 | 220,396.5353 | $ | 22,685,979 | 413,346.4930 | $ | 42,546,811 | |||||||||||||||

| Fund A - Avalanche (AVAX) | 503,720.0812 | $ | 5,253,822 | 232,861.4009 | $ | 2,428,755 | 736,581.4821 | $ | 7,682,577 | |||||||||||||||

| $ | 25,114,654 | $ | 25,114,734 | $ | 50,229,388 | |||||||||||||||||||

Fund B - Solana (SOL) | 470,185.9000 | $ | 50,297,302 | 294,049.0000 | $ | 31,455,370 | 764,234.9000 | $ | 81,752,672 | |||||||||||||||

| $ | 50,297,302 | $ | 31,455,370 | $ | 81,752,672 | |||||||||||||||||||

| Total | $ | 75,411,956 | $ | 56,570,104 | $ | 131,982,060 | ||||||||||||||||||

| December 31, 2024 | ||||||||||||||||||||||||

| Current | Long Term | Total | ||||||||||||||||||||||

| Quantity | Amount | Quantity | Amount | Quantity | Amount | |||||||||||||||||||

| Fund A - Solana (SOL) | 216,379.2216 | $ | 30,886,684 | 244,331.9458 | $ | 34,876,748 | 460,711.1675 | $ | 65,763,432 | |||||||||||||||

| Fund A - Avalanche (AVAX) | 223,905.1900 | $ | 6,020,811 | 707,540.4100 | $ | 19,025,762 | 931,445.6000 | $ | 25,046,572 | |||||||||||||||

| $ | 36,907,495 | $ | 53,902,510 | $ | 90,810,004 | |||||||||||||||||||

Fund B - Solana (SOL) | 626,365.7000 | $ | 89,409,506 | 540,869.9000 | $ | 77,205,553 | 1,167,235.6000 | $ | 166,615,059 | |||||||||||||||

| Total | $ | 126,317,001 | $ | 131,108,063 | $ | 257,425,063 | ||||||||||||||||||

Fund A

During the year ended December 31, 2024, the Company through a subsidiary, invested $61,741,683 in three tranches of a private investment fund (“Fund A”) designed to acquire Solana and Avalanche tokens from a bankrupt company. The Company’s investment represents the acquisition by Fund A of 491,249 Solana at $105 per Solana and 931,446 Avalanche at $11 per Avalanche.

The Solana acquired by Fund A is locked and staked, earning staking rewards during the lock period. Staking rewards will accrue while Solana is locked and will become distributable on the same unlocking schedule as the Solana. The Solana will be released by Fund A in monthly increments from January 2025 through January 2028.

The Avalanche acquired by Fund A is locked and staked, earning staking rewards during the lock period. Staking rewards will accrue while Avalanche is locked and will become distributable on the same unlocking schedule as the Avalanche.

The Avalanche will be released by Fund A in weekly increments starting July 10, 2025 and continuing through July 1, 2027.

The investments in the investment fund were initially recognized based on the latest available net asset value as determined by the investment fund’s administrator less an applicable DLOM. The values of the investments were remeasured based on quarterly valuation reports provided by the investment fund administrator less an applicable DLOM.

17

Fund B

During the year ended December 31, 2024, the Company invested through a subsidiary, $112,072,453 in two tranches of limited partnership units of a private investment fund (“Fund B” and together with Fund A the “Equity Investments in Digital Assets”) designed to acquire Solana tokens from a bankrupt company.

The Company’s investment represents the acquisition by Fund B of 1,123,360 Solana at $100 per Solana. The Solana acquired by Fund B is locked and staked, earning staking rewards during the lock period and thereafter until such Solana is sold by the fund manager or an in-kind distribution to the limited partners of the fund. Staking rewards will accrue while Solana is locked and will become distributable on the same unlocking schedule as the Solana. Approximately 25% of the Solana were unlocked in March 2025, while the remaining 75% of the Solana will be unlocked linearly monthly until January 2028. The Company received a distribution of $71,685,819 in July 2025 from Fund B.

The investments in Fund B were initially recognized based on the latest available net asset value as determined by Fund B’s administrator less an applicable DLOM. The values of the investments were remeasured based on quarterly valuation reports provided by Fund B’s administrator less an applicable DLOM.

The investments in Fund B were initially recognized based on the latest available net asset value as determined by Fund B’s administrator less an applicable DLOM. The values of the investments were remeasured based on quarterly valuation reports provided by Fund B’s administrator less an applicable DLOM.

The continuity of equity investments for the years ended December 31, 2025 and 2024 is as follows:

| December 31, 2025 | December 31, 2024 | |||||||

| Opening Balance | $ | 257,425,063 | $ | - | ||||

| Acquisitions | - | 173,814,136 | ||||||

| Disposals | (71,685,819 | ) | - | |||||

| Staking income | 19,784,212 | 13,060,639 | ||||||

| Net change in realized and unrealized gain/loss | (68,261,189 | ) | 77,360,769 | |||||

| Management fees | (2,530,856 | ) | (1,396,016 | ) | ||||

| Transfers out to Digital Assets | (2,749,352 | ) | (5,414,464 | ) | ||||

| Closing Balance | $ | 131,982,060 | $ | 257,425,063 | ||||

18

Third Party Exchanges, Custodians and Funds

As of December 31, 2025, the Company used the following third-party exchanges and custodians and in the ordinary course of business:

| Exchange | Location | |

| Binance | Cayman Islands | |

| B2C2 Overseas LTD | Cayman Islands | |

| Bitcoin Suisse AG | Switzerland | |

| OKX | Seychelles | |

| Kraken | United States | |

| Wintermute | United Kingdom | |

| Coinbase | United States | |

| Laser Digital | Switzerland | |

| Custodian | ||

| Anchorage Digital | United States | |

| Bitgo Trust | United States | |

| Copper | Switzerland |

Each of the Custodians and Exchanges have not appointed a sub-custodian to hold crypto assets owned by the Company. The Custodian and Exchanges hold and safeguard the digital assets deposited by the Company and its subsidiaries. The Custodians and Exchanges also offer lending and staking services. The Custodians and Exchanges are not Canadian financial institutions. None of the Custodians and Exchanges are related parties of the Company.

Each Custodian maintains general commercial insurance on its own behalf, but the Corporation and other clients of such Custodians are not named insured under such policies. The Company is not aware of any security breaches or similar incidents at the Custodians. The Company believes that any event of insolvency or bankruptcy of a Custodian would be treated in accordance with the insolvency or bankruptcy laws of the applicable jurisdiction of such Custodian.

19

As of December 31, 2025, the breakdown of digital assets deposited with each of the Custodians, or Exchanges as a percentage of total digital assets custodied by the Company and its subsidiaries is as follows:

|

Custodian |

Location | % of digital assets custodied by market value | Regulatory Body | |||

| Binance | Cayman Islands | 42.6% | Cayman Islands Monetary Authority (CIMA) | |||

| B2C2 Overseas LTD | Cayman Islands | 8.0% | Cayman Islands Monetary Authority (CIMA) | |||

| Kraken | United States | 0.7% | Office of Comptroller of Currency | |||

| Laser Digital | Switzerland | 4.7% | Financial Services Standards Association (VQF). Zug. Switzerland | |||

| Copper | Switzerland | 33.5% | Financial Services Standards Association (VQF). Zug. Switzerland | |||

| Bitgo Trust | United States | 1% | South Dakota Division of Banking and Money Services Business (MSB) with Financial Crimes Enforcement Network (FinCEN) | |||

| Others | 2.9% | Anchorage, Wintermute, Bitcoin Suisse, Coinbase (Deribit), Genesis | ||||

| Self Custody | 6.5% | |||||

| Total | 100% |

Valour conducts diligence and reviews counterparty risk in accordance with the following principles:

| ● | Valour shall strive to spread counterparty risk between several counterparties, where relevant and practical. |

| ● | In relevant situations and as far as possible, counterparty (and settlement) risk shall be mitigated by conducting transactions in well-established settlement systems based on the principles of delivery versus payment or payment versus payment. |

| ● | The below methodology is to be applied when proposing and selecting counterparties and when granting limits on counterparty risk score. |

| ● | The counterparties are reviewed in regular intervals and re-evaluated. |

| ● | In case of significant events such as negative news or credit events, Valour can decide to close the business relationship with a counterparty irrespective of the review cycle. |

| ● | Valour manages a counterparty scorecard and captures, assesses and monitors the below information. |

20

| 1. | Contact information |

The name, the website and contact person at the exchange/counterparty, as well as the responsible onboarding owner on Valour side.

| 2. | Current status |

The current status of the relationship, the connection type, as well as the services, products and currency pairs used on the respective exchange/counterparty have to be documented and kept up to date

| 3. | Country of registration and regulation |

The country in which the exchange/counterparty is registered must be documented. In addition, all countries in which the exchange/counterparty holds a regulatory license have to be assessed and documented by stating the license number (if applicable).

| 4. | Country risk |

The country of registration as well as the country/-ies of regulation are evaluated by using the country risk matrix. The country risk matrix considers the FATF (and equivalent) country evaluation, the Transparency.org Corruption Perception Index (CPI) as well as the VQF SRO country risk recommendations.

| 5. | Adverse media search |

An adverse media search is being conducted. For example, information about an exchange having been hacked in the past or any news about a negative reputation, regulatory breaches etc. are documented.

| 6. | Public exchange scores |

Publicly available information and risk scores from data sources such as Coinmarketcap and Coingecko are being collected and documented.

| 7. | Information security certification |

The exchange/counterparty information security certification status is assessed. Information about the possession of certifications such as AICPA SOC 1, SOC 2 Type I and SOC 2 Type II as well as ISO 27001 are documented.

| 8. | Insurance coverage |

Information about insurance protection and regulatory status in terms of investor protection are assessed and documented.

| 9. | Proof of reserves |

It is being checked if the exchange/counterparty has made the public wallet addresses of its cold and hot storage publicly available or if any other cryptographic means of verification of the reserves held in custody are either publicly available or have been audited.

| 10. | Risk evaluation |

The risk score is evaluated on a scale of 1 to 5, with 1 being the lowest risk and 5 being the highest risk. Based on the information collected in the scorecard, with a focus on regulatory licences, a risk score is calculated and documented for each exchange or counterparty. By carefully evaluating the risk score, we can ensure that we are making responsible business decisions and protecting our customers and stakeholders.

21

| 11. | Business justification and restrictions |

In cases where an exchange or counterparty presents increased risks, a business justification must be provided. We must carefully consider the potential exposure and take appropriate measures to limit it through restrictions, thresholds, or other means. Any decision to establish a business relationship with an exchange or counterparty with increased risks must be approved by the board.

| 12. | Recurring review schedule |

The review date and review frequency of all exchanges/counterparties are documented and tracked in the scorecard. A review once a year is set as the default standard, however, an ad-hoc review has to be considered in case of any event that may result in any of the assessment criteria being changed.

| 13. | Account closure |

If the exchange or counterparty has been identified with an increased risk, such as a risk score of 4 or 5, Valour will determine if it is necessary to end the business relationship. This decision is based on the potential exposure and the potential impact on the business and stakeholders.

If it is determined that the business relationship should be terminated, a plan for closing the relationship in a controlled and orderly manner is developed. This may include transferring outstanding transactions, closing accounts, and ensuring that all necessary documents and records are properly transferred or retained. The decision to close the business relationship is communicated to the exchange or counterparty and a timeline for the closure is provided. Once the business relationship has been successfully terminated, the counterparty scorecard is updated in order to reflect the closure.

By following this process, we can ensure that we are taking a responsible and proactive approach to closing business relationships with risky counterparties. This can help protect our customers and stakeholders and maintain the integrity of our business operations.

Self-Custody of Digital Assets

At December 31, 2025, the Company had self-custody of digital assets totaling $35,581,901 (December 31, 2024 - $339,451,566).

The Company maintains controls around the hot and cold wallets with only certain senior management having access to the accounts, passwords and seed phases. All copies of passwords and seed phases are secured and partitioned with certain senior management. Duplicate partial copies of the passwords and seed phases are accessible by a minimum of two members of senior management in different secure locations.

Staking and Lending Policy

It is Valour’s policy to hedge 100% of the market risk, subject to allowing a US$2 million maximum unhedged exposure as a trading buffer. Valour purchases and sells the digital assets which its ETPs track. Valour may lend or stake such digital assets on its balance sheet to generate revenue in accordance with the policies in the product prospectus. Lending or staking transactions are only conducted with institutional-grade counterparties and only up to a certain percentage for risk management purposes in accordance with Valour’s lending and staking policy (the “Lending and Staking Policy”), which is reviewed and approved by Valour’s board of directors. The Lending and Staking activities undertaken by Fund A and Fund B in respect of the Company’s Equity Investments in Digital Assets are not subject to the Lending and Staking Policy and the Company has no control over how Fund A and Fund B lend and stake digital assets.

When deciding whether to lend or stake a particular asset, the Lending and Staking Policy provides that the decision will initially be made based on the risk profile of the potential counterparties, then the highest yield available, then prioritizing staking over lending.

22

The Lending and Staking Policy provides the following limits for lending and staking of digital assets:

|

Digital Asset |

Lending and staking limits | |

| Bitcoin, Ethereum, Solana, Avalanche |

Up to 75% of unrestricted tokens may be lent on open terms to eligible counterparties, 50% of tokens may be lent on terms up to six months.

100% of tokens may be staked

| |

| All other Digital Assets |

Up to 75% of unrestricted tokens may be lent on open terms to eligible counterparties, 50% of tokens may be lent on terms up to six months. If total AUM is greater than US$5 million, up to 95% may be staked, else 75% may be staked |

The Company’s typical lending arrangements have terms as follows:

(a) which party has legal title

The lender authorizes the counterparty e.g., Anchorage to draw down lent assets. Typically, the counterparty / borrower is then permitted to use Client’s Designated Assets for any lawful purpose.

(b) the status of the assets in the event of insolvency of the borrower

The lender shall have full recourse to Counterparty for any obligations hereunder in equity and at law. Upon any event of default, the lender shall be entitled to seek all remedies available at law or in equity for the full amount or any unpaid principal of any advance, accrued but unpaid fees or other amounts or property payable hereunder against Lender in addition to enforcing its security interest.

(c) contractual limitation on use and transfer of lent items by borrower

Typically, the Counterparty is then permitted to use client’s designated assets for any lawful purpose.

(d) borrower’s ability to initiate transactions with the borrowed assets, including but not limited to: sell, lend, pledge, and/or hypothecate

Typically, the Counterparty is then permitted to use Client’s Designated Assets for any lawful purpose, including selling, lending, pledging and/or hypothecating. Certain lending agreements require Counterparties to grant a security interest to the Company on any assets that are further lent out.

(e) borrowers’ rights regarding “co-mingling”

There is no specific language in the lending agreement but given the Counterparties can use for any lawful purpose, the Company’s believes that comingling can occur.

23

(f) callability terms and conditions (including “notice period”, if any).

Termination. Client may terminate any Advance of its Designated Assets upon three (3) business days’ prior notice (the date of such termination, the “Termination Date”), from time to time at its sole discretion through an Electronic Notice.

Investments, At Fair Value, Through Profit and Loss, As At December 31, 2025

At December 31, 2025, the Company’s twelve private investments had a total fair value of $29,372,628.

| Note | Note | Security description | Cost | Estimated Fair Value | % of FV | |||||||||||

| Amina Bank AG | 3,906,250 non-voting shares | $ | 24,749,403 | $ | 24,285,752 | 82.7 | % | |||||||||

| Earnity Inc. | 85,142 preferred shares | 95,538 | - | 0.0 | % | |||||||||||

| Luxor Technology Corporation | 201,633 preferred shares | 460,016 | 524,963 | 1.8 | % | |||||||||||

| SDK:meta, LLC | 1,000,000 units | 2,495,232 | - | 0.0 | % | |||||||||||

| Skolem Technologies Ltd. | 16,354 preferred shares | 129,495 | - | 0.0 | % | |||||||||||

| VolMEX Labs Corporation | Rights to certain preferred shares and warrants | 30,000 | - | 0.0 | % | |||||||||||

| Global Benchmarks AB | (i) | 53,300 common shares | 199,875 | 199,875 | 0.7 | % | ||||||||||

| ZKP Corporation | (i) | 370,370 common shares | 1,000,000 | 1,000,000 | 3.4 | % | ||||||||||

| CH Technical Solutions SA | 25 common shares | 3,952,977 | 362,038 | 1.2 | % | |||||||||||

| Canada Stablecorp Inc. | 303,030 common shares | 500,000 | 500,000 | 1.7 | % | |||||||||||

| Continental Stable Coin | Rights to certain preferred shares | 500,000 | 500,000 | 1.7 | % | |||||||||||

| Bonsol Labs Inc. | Rights to certain preferred shares | 2,000,000 | 2,000,000 | 6.8 | % | |||||||||||

| Total private investments | $ | 36,112,536 | $ | 29,372,628 | 100.0 | % | ||||||||||

| (i) | Investments in related party entities - see Note 26 |

At December 31, 2024, the Company’s nine private investments had a total fair value of $37,348,081.

| Private Issuer | Note | Security description | Cost | Estimated Fair Value | % of FV | |||||||||||

| 3iQ Corp. | 61,712 common shares | $ | 63,270 | $ | 300,459 | 0.8 | % | |||||||||

| Amina Bank AG | 3,906,250 non-voting shares | 25,286,777 | 35,457,982 | 95.0 | % | |||||||||||

| Earnity Inc. | 85,142 preferred shares | 95,980 | - | 0.0 | % | |||||||||||

| Luxor Technology Corporation | 201,633 preferred shares | 462,145 | 500,058 | 1.3 | % | |||||||||||

| Neuronomics AG | 724 common shares | 89,582 | 89,582 | 0.2 | % | |||||||||||

| SDK:meta, LLC | 1,000,000 units | 2,506,780 | - | 0.0 | % | |||||||||||

| Skolem Technologies Ltd. | 16,354 preferred shares | 130,095 | - | 0.0 | % | |||||||||||

| VolMEX Labs Corporation | Rights to certain preferred shares and warrants | 21,989 | - | 0.0 | % | |||||||||||

| ZKP Corporation | (i) | 370,370 common shares | 1,000,000 | 1,000,000 | 2.7 | % | ||||||||||

| Total private investments | $ | 29,656,618 | $ | 37,348,081 | 100.0 | % | ||||||||||

| (i) | Investments in related party entities |

24

Financial Results

The following is a discussion of the results of operations of the Company for the three and twelve months ended December 31, 2025, and 2024. They should be read in conjunction with the Company’s annual consolidated financial statements for the three and twelve months ended December 31, 2025 and 2024 and related notes. All amounts are in U.S. dollars.

| Three months ended December 31, | Year ended December 31, | |||||||||||||||

| 2025 | 2024 | 2025 | 2024 | |||||||||||||

| $ | $ | $ | $ | |||||||||||||

| Revenues | ||||||||||||||||

| Staking and lending income | 2,222,610 | 385,696 | 13,072,141 | 13,014,797 | ||||||||||||

| Management fees | 2,149,585 | 2,073,007 | 9,696,992 | 6,443,983 | ||||||||||||

| Trading commissions | 3,348,146 | 2,106,286 | 9,579,010 | 2,106,286 | ||||||||||||

| Research revenue | 65,000 | 619,593 | 533,000 | 1,433,378 | ||||||||||||

| Advisory revenue | 95,151 | - | 287,558 | - | ||||||||||||

| Revenues excluding realized and net change in unrealized gains (losses) | 7,880,492 | 5,184,582 | 33,168,701 | 22,998,444 | ||||||||||||

| Realized and net change in unrealized (loss) gain on digital assets | (263,320,471 | ) | 119,563,065 | (233,989,493 | ) | 252,040,373 | ||||||||||

| Realized and net change in unrealized (loss) gain on equity investments at FVTPL | (81,535,311 | ) | 94,442,981 | (51,007,843 | ) | 108,915,688 | ||||||||||

| Realized and net change in unrealized gain (loss) on ETP payables | 356,967,448 | (238,526,194 | ) | 350,965,104 | (352,528,754 | ) | ||||||||||

| Revenues from realized and net change in unrealized gains (losses) | 12,111,666 | (24,520,148 | ) | 65,967,768 | 8,427,307 | |||||||||||

| Total revenues | 19,992,158 | (19,335,566 | ) | 99,136,469 | 31,425,751 | |||||||||||

| Operating expenses | ||||||||||||||||

| Operating, general and administration | 11,150,492 | 7,515,824 | 34,219,133 | 36,735,665 | ||||||||||||

| Share based payments | 2,451,859 | 6,742,900 | 13,210,103 | 19,249,685 | ||||||||||||

| Depreciation - equipment | - | 492 | 1,666 | 5,990 | ||||||||||||

| Amortization - right-of-use assets | 156,148 | - | 207,328 | - | ||||||||||||

| Amortization - intangibles | 167,593 | 390,723 | 1,331,581 | 1,543,995 | ||||||||||||

| Fees and commissions | 1,175,290 | 2,022,714 | 6,200,681 | 4,107,102 | ||||||||||||

| Foreign exchange (gain) loss | (2,191,260 | ) | (4,069,658 | ) | (2,558,519 | ) | (321,322 | ) | ||||||||

| Total operating expenses | 12,910,122 | 12,602,995 | 52,611,973 | 61,321,115 | ||||||||||||

| Operating income (loss) | 7,082,036 | (31,938,561 | ) | 46,524,496 | (29,895,364 | ) | ||||||||||

| Realized (loss) gain on investments | (118,289 | ) | (353,251 | ) | (419,093 | ) | 112,984 | |||||||||

| Unrealized (loss) gain on investments | (16,503,925 | ) | 8,168,662 | (16,501,202 | ) | 7,908,831 | ||||||||||

| Interest income | 478,203 | 1,400 | 542,622 | 4,537 | ||||||||||||

| Interest recovery (expense) | 1,148,796 | (287,629 | ) | 773,244 | (2,824,092 | ) | ||||||||||

| Financing expense | (1,924 | ) | - | (4,677,123 | ) | - | ||||||||||

| Gain on deconsolidation | 583,966 | - | 583,966 | - | ||||||||||||

| Loss on investment in associate | (75,506 | ) | - | (75,506 | ) | - | ||||||||||

| Change in fair value of warrant liability | 39,595,879 | - | 39,595,879 | - | ||||||||||||

| Bad debt expense | (726,240 | ) | (216,635 | ) | (726,240 | ) | (216,635 | ) | ||||||||