.2

Supplemental Business Update Q4 and Full - Year 2025 Results This supplemental document provides selected unaudited financial and operational information for the three months ended December 31, 2025. As a foreign private issuer, Alvotech does not prepare or publish quarterly IFRS financial statements. Accordingly, the quarterly information presented herein is supplemental, unaudited, and provided for informational purposes only to assist investors in understanding recent operating trends. All financial information is unaudited unless otherwise stated. 18 March 2026 Earnings Release

Disclaimer 2 constitute an offer to sell, a solicitation of an offer to buy, or a recommendation to purchase any security of Alvotech (the “Company”) to any person in the United States or in any jurisdiction to whom or in which such offer or solicitation is unlawful. Any trademarks, servicemarks, trade names and copyrights of the Company and other property of their respective owners. This Presentation is strictly confidential to the recipient, it is being distributed to a limited range of invited persons solely for their own information, may not be distributed to the press or published, in whole or in part, in any form. Failure to comply with this restriction may constitute a violation of applicable securities laws. This supplemental document does not contain or its product candidates, the timing of regulatory Forward - Looking Statements Certain statements in this communication may be considered “forward - looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995, as amended. Forward - looking statements include, for example, Alvotech’s expectations regarding competitive advantages, business prospects and opportunities including pipeline product development, future plans and intentions, regulatory submissions, review and interactions, the potential approval and commercial launch of approval, market launches and financial projections. Such forward - looking statements are subject to risks, uncertainties, and other factors which could cause actual results to differ materially from those expressed or implied by such forward - looking statements. These forward - looking statements are based upon companies contained in this Presentation are the estimates and assumptions that, while considered reasonable by Alvotech and its management, are inherently uncertain and are inherently subject to risks, variability, and contingencies, many of which are beyond or any other person, and may not be reproduced results to differ materially from current expectations include, but are not limited to factors set forth in the sections entitled “Risk Factors” and “Cautionary Note Regarding Forward - Looking Statements” in documents that Alvotech may from time - to - time file or furnish with the SEC. There may be additional risks that Alvotech does not presently know or that Alvotech currently believes are immaterial that could also cause actual results to differ from those contained in the forward - looking statements. These forward - looking statements are provided for illustrative purposes only and are not intended to serve as, and must not be relied on by an investor as, a guarantee, assurance, prediction or definitive statement of a fact or probability. Alvotech does not undertake any duty to update these forward - looking statements or to inform the recipient of any matters of which any of them becomes aware of which may affect any matter referred to in this communication. Alvotech disclaims any and all liability for any loss or damage (whether foreseeable or not) suffered or incurred by any or omitted from this communication and such liability is expressly disclaimed . Non - IFRS Financial Measures This Presentation may include projections of certain financial measures not presented in Alvotech’s control. Factors that may cause actual accordance with International Financial Reporting Standards (“IFRS”) including, but not limited to, Adjusted EBITDA and certain ratios IFRS financial measures are not measures of financial performance in accordance with IFRS and may exclude items that are significant in understanding and assessing the Company’s financial results. Therefore, these measures should not be considered in isolation or as an alternative to net income, cash flows from operations or other measures of profitability, liquidity or performance under IFRS. You should be aware that the Company’s presentation of these measures may not be comparable to similarly - titled measures used by other companies. The Company believes these non - IFRS measures of financial results provide useful information to management and investors regarding certain financial and business trends relating to the Company’s financial condition and results of operations. The Company believes that the use of these non - IFRS financial measures provide an additional tool for investors to use in evaluating ongoing operating results and trends person or entity as a result of anything contained and in comparing the Company’s financial measures with other similar companies, many of which present similar non - IFRS financial measures to investors. These non - IFRS financial measures are subject to inherent limitations as they reflect the exercise of judgments by management about which expense and income are excluded or included in determining these non - IFRS financial measures. Due to the high variability and difficulty in making accurate and other metrics derived therefrom. These non - forecasts and projections of some of the information excluded from these projected measures, together with some of the excluded information not being ascertainable or accessible, the Company is unable to quantify certain amounts that would be required to be included in the most directly comparable IFRS financial measures without unreasonable effort. Consequently, no disclosure of estimated comparable IFRS measures is included and no reconciliation of the forward - looking non - IFRS financial measures is included. For the same reasons, the Company is unable to address the probable significance of the unavailable information, which could be material to future results.

3 The biosimilars opportunity remains large and durable. We believe Alvotech is well positioned to capture that opportunity. Lisa Graver CEO Designate Róbert Wessman Executive Chairman I’m excited to help maximize the full potential of the robust pipeline Alvotech has built and is continuing to build. During 2025 we achieved several important milestones. A particular highlight was the U.S. launch of our Stelara® biosimilar by our commercial partner, marking our second biosimilar launch in that market. We also achieved approvals and first launches for biosimilars to Prolia®/Xgeva®, Simponi® and Eyela® across Europe and Japan, targeting some of the largest biologic franchises in the world. 2025 was an important year for Alvotech. We continued to strengthen our position as a leading developer of biosimilar medicines, expanding our commercial footprint, advancing our industry leading pipeline of 30 biosimilar programs, and building our global commercial partnership network. With three important products approved during the year, we now have five on - market biosimilars, supported by our global partners which provide Alvotech with commercial reach into 90 countries worldwide. At the same time, we addressed the regulatory observations following the FDA inspection of our Reykjavik manufacturing facility and we implemented a comprehensive improvement program. Based on the progress made to date, we expect to resubmit the affected applications to the FDA during the second quarter of 2026. Our focus has been on strengthening the operational platform so that we can continue to scale the business globally. During the year we further strengthened our financial position, raising close to $300 million from the capital markets to support continued investment in our development programs and manufacturing platform. We broadened our investor base through the listing of shares on Nasdaq Stockholm, providing better access to Nordic and European investors. At the beginning of 2026, I was pleased to announce the appointment of Lisa Graver as Chief Executive Officer. Lisa and I have worked together for over 20 years, and she is ideally positioned to lead the company through this next stage. Following Lisa's appointment, the key management positions are all based onsite in Iceland. With the platform and people now firmly in place, the company is entering a new phase focused on operational execution and commercial scale. As Executive Chairman of the Board, I will continue to be actively engaged in the business, and I am looking forward working closely with Lisa and the leadership team as we continue building Alvotech into a leading biosimilars company. As part of our efforts to further strengthen our technical and regulatory capabilities, we continued to expand our process development organization. The integration of Xbrane's R&D team in Stockholm has enhanced our ability to advance multiple programs in parallel. Looking ahead, our priorities remain clear. We will continue advancing our biosimilar portfolio toward approval and commercialization in all markets, including the U.S. We will maintain a strong focus on operational excellence, efficiency and regulatory compliance. We will also continue expanding our pipeline in the most cost - effective way and strengthening our global partnerships. From the Executive Chairman and the CEO Designate

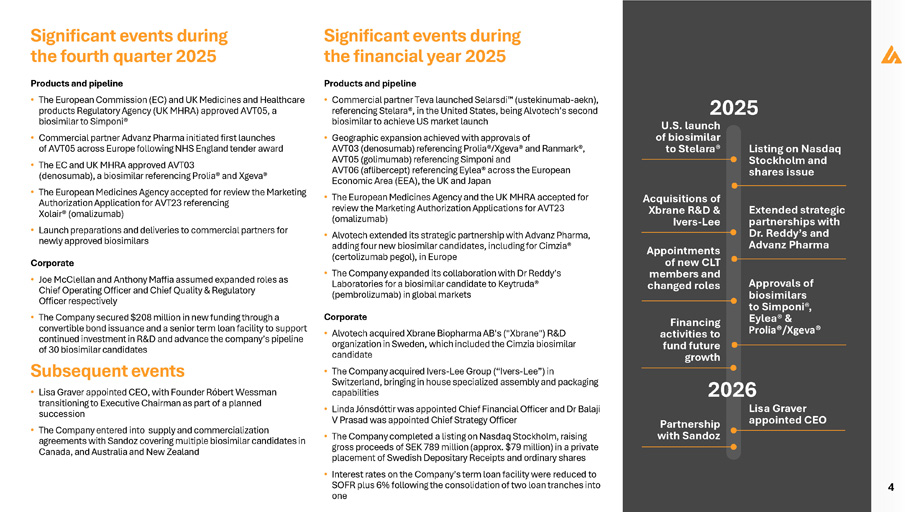

4 Significant events during the fourth quarter 2025 Products and pipeline • The European Commission (EC) and UK Medicines and Healthcare products Regulatory Agency (UK MHRA) approved AVT05, a biosimilar to Simponi® • Commercial partner Advanz Pharma initiated first launches of AVT05 across Europe following NHS England tender award • The EC and UK MHRA approved AVT03 (denosumab), a biosimilar referencing Prolia® and Xgeva® • The European Medicines Agency accepted for review the Marketing Authorization Application for AVT23 referencing Xolair® (omalizumab) • Launch preparations and deliveries to commercial partners for newly approved biosimilars Corporate • Joe McClellan and Anthony Maffia assumed expanded roles as Chief Operating Officer and Chief Quality & Regulatory Officer respectively • The Company secured $208 million in new funding through a convertible bond issuance and a senior term loan facility to support continued investment in R&D and advance the company’s pipeline of 30 biosimilar candidates Subsequent events • Lisa Graver appointed CEO, with Founder Róbert Wessman transitioning to Executive Chairman as part of a planned succession • The Company entered into supply and commercialization agreements with Sandoz covering multiple biosimilar candidates in Canada, and Australia and New Zealand Significant events during the financial year 2025 Products and pipeline • Commercial partner Teva launched Selarsdi (ustekinumab - aekn), referencing Stelara®, in the United States, being Alvotech’s second biosimilar to achieve US market launch • Geographic expansion achieved with approvals of AVT03 (denosumab) referencing Prolia®/Xgeva® and Ranmark®, AVT05 (golimumab) referencing Simponi and AVT06 (aflibercept) referencing Eylea® across the European Economic Area (EEA), the UK and Japan • The European Medicines Agency and the UK MHRA accepted for review the Marketing Authorization Applications for AVT23 (omalizumab) • Alvotech extended its strategic partnership with Advanz Pharma, adding four new biosimilar candidates, including for Cimzia® (certolizumab pegol), in Europe • The Company expanded its collaboration with Dr Reddy’s Laboratories for a biosimilar candidate to Keytruda® (pembrolizumab) in global markets Corporate • Alvotech acquired Xbrane Biopharma AB's ("Xbrane") R&D organization in Sweden, which included the Cimzia biosimilar candidate • The Company acquired Ivers - Lee Group (“Ivers - Lee”) in Switzerland, bringing in house specialized assembly and packaging capabilities • Linda Jónsdóttir was appointed Chief Financial Officer and Dr Balaji V Prasad was appointed Chief Strategy Officer • The Company completed a listing on Nasdaq Stockholm, raising gross proceeds of SEK 789 million (approx. $79 million) in a private placement of Swedish Depositary Receipts and ordinary shares • Interest rates on the Company’s term loan facility were reduced to SOFR plus 6% following the consolidation of two loan tranches into one 2025 Lisa Graver appointed CEO Financing activities to fund future growth U.S. launch of biosimilar to Stelara® Appointments of new CLT members and changed roles Listing on Nasdaq Stockholm and shares issue Acquisitions of Xbrane R&D & Ivers - Lee Extended strategic partnerships with Dr. Reddy’s and Advanz Pharma Approvals of biosimilars to Simponi®, Eylea® & Prolia®/Xgeva® 2026 Partnership with Sandoz

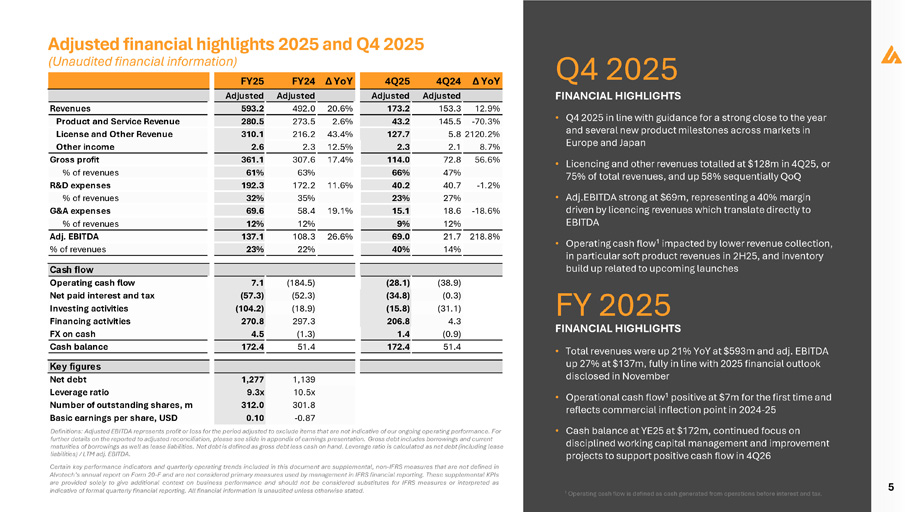

5 Adjusted financial highlights 2025 and Q4 2025 Q4 2025 FINANCIAL HIGHLIGHTS FY 2025 FINANCIAL HIGHLIGHTS • Q4 2025 in line with guidance for a strong close to the year and several new product milestones across markets in Europe and Japan • Licencing and other revenues totalled at $128m in 4Q25, or 75% of total revenues, and up 58% sequentially QoQ • Adj . EBITDA strong at $ 69 m, representing a 40 % margin driven by licencing revenues which translate directly to EBITDA • Operating cash flow 1 impacted by lower revenue collection, in particular soft product revenues in 2H25, and inventory build up related to upcoming launches • Total revenues were up 21% YoY at $593m and adj. EBITDA up 27% at $137m, fully in line with 2025 financial outlook disclosed in November • Operational cash flow 1 positive at $7m for the first time and reflects commercial inflection point in 2024 - 25 • Cash balance at YE25 at $172m, continued focus on disciplined working capital management and improvement projects to support positive cash flow in 4Q26 Definitions: Adjusted EBITDA represents profit or loss for the period adjusted to exclude items that are not indicative of our ongoing operating performance. For further details on the reported to adjusted reconciliation, please see slide in appendix of earnings presentation. Gross debt includes borrowings and current maturities of borrowings as well as lease liabilities. Net debt is defined as gross debt less cash on hand. Leverage ratio is calculated as net debt (including lease liabilities) / LTM adj. EBITDA. Certain key performance indicators and quarterly operating trends included in this document are supplemental, non - IFRS measures that are not defined in Alvotech’s annual report on Form 20 - F and are not considered primary measures used by management in IFRS financial reporting . These supplemental KPIs are provided solely to give additional context on business performance and should not be considered substitutes for IFRS measures or interpreted as indicative of formal quarterly financial reporting . All financial information is unaudited unless otherwise stated . 1 Operating cash flow is defined as cash generated from operations before interest and tax. (184.5) 7.1 (52.3) (57.3) (18.9) (104.2) 297.3 270.8 (1.3) 4.5 51.4 172.4 (38.9) (28.1) (0.3) (34.8) (31.1) (15.8) 4.3 206.8 (0.9) 1.4 51.4 172.4 1,139 1,277 10.5x 9.3x 301.8 312.0 - 0.87 0.10 4Q24 Δ YoY 12.9% Adjusted Adjusted Adjusted Adjusted 593.2 492.0 20.6% 173.2 153.3 280.5 273.5 2.6% 43.2 145.5 - 70.3% 310.1 2.6 216.2 43.4% 2.3 12.5% 361.1 307.6 17.4% 61% 63% 192.3 172.2 11.6% 32% 35% 69.6 58.4 19.1% 12% 12% 137.1 108.3 26.6% Revenues Product and Service Revenue License and Other Revenue Other income Gross profit % of revenues R&D expenses % of revenues G&A expenses % of revenues Adj. EBITDA % of revenues 23% 22% 127.7 5.8 2120.2% 2.3 2.1 8.7% 114.0 72.8 56.6% 66% 47% 40.2 40.7 - 1.2% 23% 27% 15.1 18.6 - 18.6% 9% 12% 69.0 21.7 218.8% 40% 14% Cash flow Operating cash flow Net paid interest and tax Investing activities Financing activities FX on cash Cash balance Key figures Net debt Leverage ratio Number of outstanding shares, m Basic earnings per share, USD (Unaudited financial information) FY25 FY24 Δ YoY 4Q25

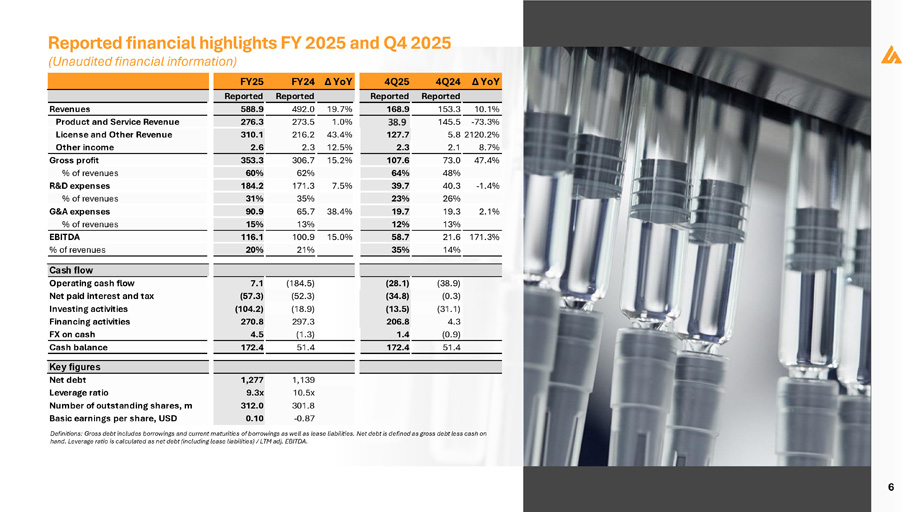

6 Definitions: Gross debt includes borrowings and current maturities of borrowings as well as lease liabilities. Net debt is defined as gross debt less cash on hand. Leverage ratio is calculated as net debt (including lease liabilities) / LTM adj. EBITDA. Revenues Product and Service Revenue License and Other Revenue Other income Gross profit % of revenues R&D expenses % of revenues G&A expenses % of revenues EBITDA % of revenues FY25 FY24 Δ YoY Reported Reported 19.7% 492.0 588.9 1.0% 273.5 276.3 216.2 43.4% 2.3 12.5% 310.1 2.6 15.2% 306.7 353.3 62% 60% 7.5% 171.3 184.2 35% 31% 38.4% 65.7 90.9 13% 15% 15.0% 100.9 116.1 21% 20% Δ YoY 4Q24 4Q25 Reported Reported 10.1% 153.3 168.9 - 73.3% 145.5 38.9 5.8 2120.2% 127.7 8.7% 2.1 2.3 47.4% 73.0 107.6 48% 64% - 1.4% 40.3 39.7 26% 23% 2.1% 19.3 19.7 13% 12% 171.3% 21.6 58.7 14% 35% (184.5) 7.1 (52.3) (57.3) (18.9) (104.2) 297.3 270.8 (1.3) 4.5 51.4 172.4 (38.9) (28.1) (0.3) (34.8) (31.1) (13.5) 4.3 206.8 (0.9) 1.4 51.4 172.4 Cash flow Operating cash flow Net paid interest and tax Investing activities Financing activities FX on cash Cash balance Key figures 1,139 10.5x 301.8 1,277 9.3x 312.0 Net debt Leverage ratio Number of outstanding shares, m - 0.87 0.10 Basic earnings per share, USD Reported financial highlights FY 2025 and Q4 2025 (Unaudited financial information)

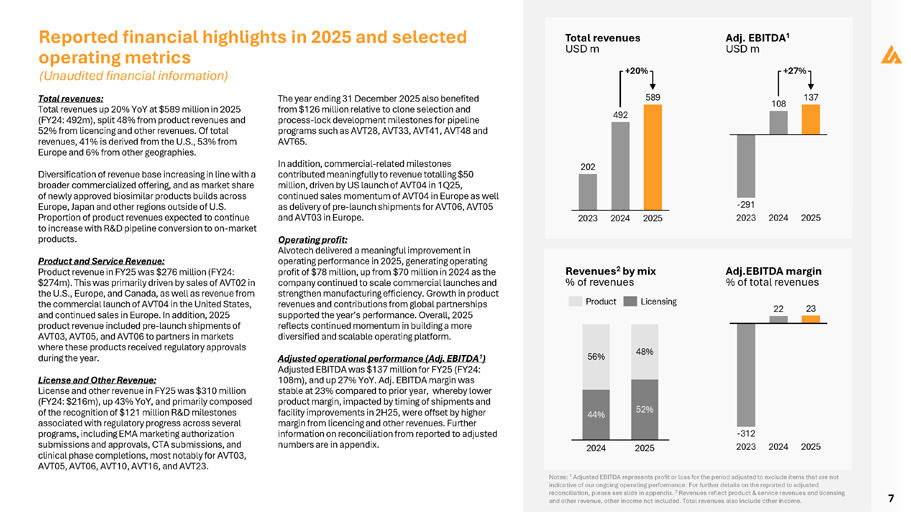

7 Total revenues: Total revenues up 20% YoY at $589 million in 2025 (FY24: 492m), split 48% from product revenues and 52% from licencing and other revenues. Of total revenues, 41% is derived from the U.S., 53% from Europe and 6% from other geographies. Diversification of revenue base increasing in line with a broader commercialized offering, and as market share of newly approved biosimilar products builds across Europe, Japan and other regions outside of U.S. Proportion of product revenues expected to continue to increase with R&D pipeline conversion to on - market products. Product and Service Revenue: Product revenue in FY25 was $276 million (FY24: $274m). This was primarily driven by sales of AVT02 in the U.S., Europe, and Canada, as well as revenue from the commercial launch of AVT04 in the United States, and continued sales in Europe. In addition, 2025 product revenue included pre - launch shipments of AVT03, AVT05, and AVT06 to partners in markets where these products received regulatory approvals during the year. License and Other Revenue: License and other revenue in FY25 was $310 million (FY24: $216m), up 43% YoY, and primarily composed of the recognition of $121 million R&D milestones associated with regulatory progress across several programs, including EMA marketing authorization submissions and approvals, CTA submissions, and clinical phase completions, most notably for AVT03, AVT05, AVT06, AVT10, AVT16, and AVT23. The year ending 31 December 2025 also benefited from $126 million relative to clone selection and process - lock development milestones for pipeline programs such as AVT28, AVT33, AVT41, AVT48 and AVT65. In addition, commercial - related milestones contributed meaningfully to revenue totalling $50 million, driven by US launch of AVT04 in 1Q25, continued sales momentum of AVT04 in Europe as well as delivery of pre - launch shipments for AVT06, AVT05 and AVT03 in Europe. Operating profit: Alvotech delivered a meaningful improvement in operating performance in 2025, generating operating profit of $78 million, up from $70 million in 2024 as the company continued to scale commercial launches and strengthen manufacturing efficiency. Growth in product revenues and contributions from global partnerships supported the year’s performance . Overall, 2025 reflects continued momentum in building a more diversified and scalable operating platform . Adjusted operational performance (Adj. EBITDA 1 ) Adjusted EBITDA was $137 million for FY25 (FY24: 108m), and up 27% YoY. Adj. EBITDA margin was stable at 23% compared to prior year, whereby lower product margin, impacted by timing of shipments and facility improvements in 2H25, were offset by higher margin from licencing and other revenues. Further information on reconciliation from reported to adjusted numbers are in appendix. Reported financial highlights in 2025 and selected operating metrics 202 492 589 2023 2024 2025 Total revenues USD m +20% 108 137 - 291 2023 2024 2025 Adj. EBITDA 1 USD m +27% - 312 2023 2024 2025 44% 52% 56% 48% 2024 2025 Product Licensing Revenues 2 by mix % of revenues Adj.EBITDA margin % of total revenues 22 23 Notes: 1 Adjusted EBITDA represents profit or loss for the period adjusted to exclude items that are not indicative of our ongoing operating performance. For further details on the reported to adjusted reconciliation, please see slide in appendix. 2 Revenues reflect product & service revenues and licensing and other revenue, other income not included. Total revenues also include other income. (Unaudited financial information)

8 Cost of product and service revenue (COGS): Cost of product revenue was $236 million in FY25 (FY24: $185m). This increase was primarily driven by increased overall volume, product mix and non - recurring manufacturing costs which increased overall cost levels without a corresponding increase in revenue. Research and development (R&D) expenses: R&D expenses were $184 million for FY25 (FY24: $171m). The increase was primarily driven by an increase of $47 million in direct program expenses mainly due to AVT16 and AVT29 programs that are advancing through clinical phase and overall higher other R&D expenses for $29 million due to the advancement of other programs and FDA readiness costs during 2H25. This was partially offset by a decrease of $63 million related to programs which reached commercialization (i.e., AVT04, AVT03, AVT05, and AVT06). General and administrative (G&A) expenses: G&A expenses were $91 million for FY25 (FY24: $66m). The increase was mainly driven by $22 million in higher legal, facility and external service costs, as well as $4 million increase in transaction costs mainly related to the Swedish offering. CAPEX and M&A activities: In 2025, Alvotech strengthened its development capabilities and supply chain through two targeted acquisitions. In June, the Company acquired Xbrane Biopharma’s R&D operations, including the XB003 biosimilar candidate referencing Cimzia, for approximately $29 million. In July, Alvotech expanded its European manufacturing and clinical supply footprint with the acquisition of Ivers - Lee, a Switzerland - and Germany - based provider of pharmaceutical packaging and clinical supply services, for a purchase price of $19 million, resulting in an $8 million gain, primarily driven by the uplift on acquired real estate. These acquisitions support Alvotech’s long - term biosimilar pipeline and enhance its integrated global supply network. Exchange rate differences: Exchange rate differences resulted in a loss of $17 million for FY25 (FY24: gain of $8 m). The change was primarily driven by the movements in the exchange rate of foreign currencies, predominantly Icelandic krona and euros. Income tax: Income tax expense was $108 million for FY25 (FY24: income tax expense of $14 million). The change is mainly driven by a $130 million deferred tax charge due to the derecognition of deferred tax assets related to Icelandic tax losses. This was partly offset by a $37 million FX - related deferred tax benefit and a modest increase in deferred tax expense from operating results. Profit / (loss) for the Period: The Company reported a net profit for the period of $28 million in 2025, compared to a net loss of $232 million in 2024, reflecting stronger overall performance driven by higher revenues and a more favorable finance result. Profit was partially offset by higher income tax expense due to the derecognition of deferred tax assets related to Icelandic tax losses.

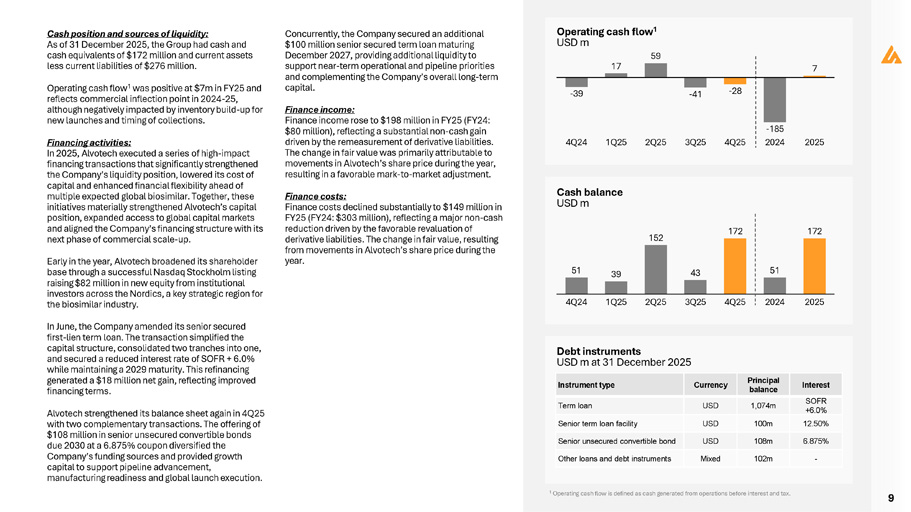

9 Cash position and sources of liquidity: As of 31 December 2025, the Group had cash and cash equivalents of $172 million and current assets less current liabilities of $276 million. Operating cash flow 1 was positive at $7m in FY25 and reflects commercial inflection point in 2024 - 25, although negatively impacted by inventory build - up for new launches and timing of collections. Financing activities: In 2025, Alvotech executed a series of high - impact financing transactions that significantly strengthened the Company’s liquidity position, lowered its cost of capital and enhanced financial flexibility ahead of multiple expected global biosimilar. Together, these initiatives materially strengthened Alvotech’s capital position, expanded access to global capital markets and aligned the Company’s financing structure with its next phase of commercial scale - up. Early in the year, Alvotech broadened its shareholder base through a successful Nasdaq Stockholm listing raising $82 million in new equity from institutional investors across the Nordics, a key strategic region for the biosimilar industry. In June, the Company amended its senior secured first - lien term loan. The transaction simplified the capital structure, consolidated two tranches into one, and secured a reduced interest rate of SOFR + 6.0% while maintaining a 2029 maturity. This refinancing generated a $18 million net gain, reflecting improved financing terms. Alvotech strengthened its balance sheet again in 4Q25 with two complementary transactions. The offering of $108 million in senior unsecured convertible bonds due 2030 at a 6.875% coupon diversified the Company’s funding sources and provided growth capital to support pipeline advancement, manufacturing readiness and global launch execution. Concurrently, the Company secured an additional $100 million senior secured term loan maturing December 2027, providing additional liquidity to support near - term operational and pipeline priorities and complementing the Company’s overall long - term capital. Finance income: Finance income rose to $198 million in FY25 (FY24: $80 million), reflecting a substantial non - cash gain driven by the remeasurement of derivative liabilities. The change in fair value was primarily attributable to movements in Alvotech’s share price during the year, resulting in a favorable mark - to - market adjustment. Finance costs: Finance costs declined substantially to $149 million in FY25 (FY24: $303 million), reflecting a major non - cash reduction driven by the favorable revaluation of derivative liabilities. The change in fair value, resulting from movements in Alvotech’s share price during the year. Cash balance USD m Debt instruments USD m at 31 December 2025 - 39 Operating cash flow 1 USD m 59 17 - 41 - 28 7 - 185 4Q24 1Q25 2Q25 3Q25 4Q25 2024 2025 51 39 152 43 172 51 172 4Q24 1Q25 2Q25 3Q25 4Q25 2024 2025 Interest Principal balance Currency Instrument type SOFR +6.0% 1,074m USD Term loan 12.50% 100m USD Senior term loan facility 6.875% 108m USD Senior unsecured convertible bond - 102m Mixed Other loans and debt instruments 1 Operating cash flow is defined as cash generated from operations before interest and tax.

10 Outlook 2026 Continued focus on robust cash flow and margin expansion by delivering solid sales growth and driving operational efficiencies across the company. Anticipate total revenues in the range of $650 - 700 million in 2026, reflecting continued double - digit sales growth Adj.EBITDA expected to increase to $180 - 220 million, supported by higher volumes of commercialized products and launches of newly approved products in Europe and Japan The lower end of the revenue range assumes the possibility of further delay of pending FDA approvals. Alvotech assumes to receive U.S. approval by late 2026 for the 4 Biologics License Applications pending with the FDA, with minimum impact on the topline Focus on disciplined working capital management and improvement projects to support positive cash flow in 4Q26 650 - 700m Revenues, USD 180 - 220m Adj. EBITDA, USD

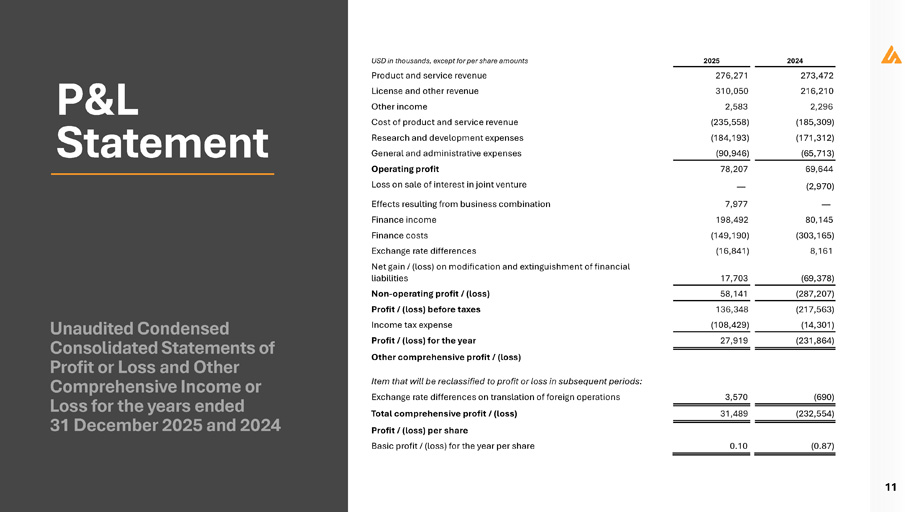

Unaudited Condensed Consolidated Statements of Profit or Loss and Other Comprehensive Income or Loss for the years ended 31 December 2025 and 2024 11 P&L Statement 2024 2025 USD in thousands, except for per share amounts 273,472 276,271 Product and service revenue 216,210 310,050 License and other revenue 2,296 2,583 Other income (185,309) (235,558) Cost of product and service revenue (171,312) (184,193) Research and development expenses (65,713) (90,946) General and administrative expenses 69,644 78,207 Operating profit (2,970) — Loss on sale of interest in joint venture — 7,977 Effects resulting from business combination 80,145 198,492 Finance income (303,165) (149,190) Finance costs 8,161 (16,841) Exchange rate differences (69,378) 17,703 Net gain / (loss) on modification and extinguishment of financial liabilities (287,207) 58,141 Non - operating profit / (loss) (217,563) 136,348 Profit / (loss) before taxes (14,301) (108,429) Income tax expense (231,864) 27,919 Profit / (loss) for the year Other comprehensive profit / (loss) Item that will be reclassified to profit or loss in subsequent periods: (690) 3,570 Exchange rate differences on translation of foreign operations (232,554) 31,489 Total comprehensive profit / (loss) Profit / (loss) per share (0.87) 0.10 Basic profit / (loss) for the year per share

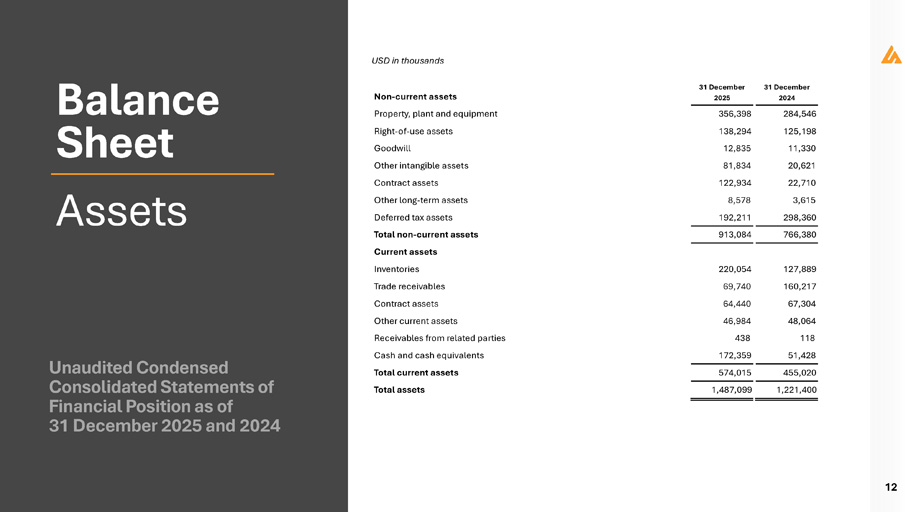

Unaudited Condensed Consolidated Statements of Financial Position as of 31 December 2025 and 2024 12 Balance Sheet Assets USD in thousands Non - current assets 31 December 2025 31 December 2024 284,546 356,398 Property, plant and equipment 125,198 138,294 Right - of - use assets 11,330 12,835 Goodwill 20,621 81,834 Other intangible assets 22,710 122,934 Contract assets 3,615 8,578 Other long - term assets 298,360 192,211 Deferred tax assets 766,380 913,084 Total non - current assets 127,889 220,054 Current assets Inventories 160,217 69,740 Trade receivables 67,304 64,440 Contract assets 48,064 46,984 Other current assets 118 438 Receivables from related parties 51,428 172,359 Cash and cash equivalents 455,020 574,015 Total current assets 1,221,400 1,487,099 Total assets

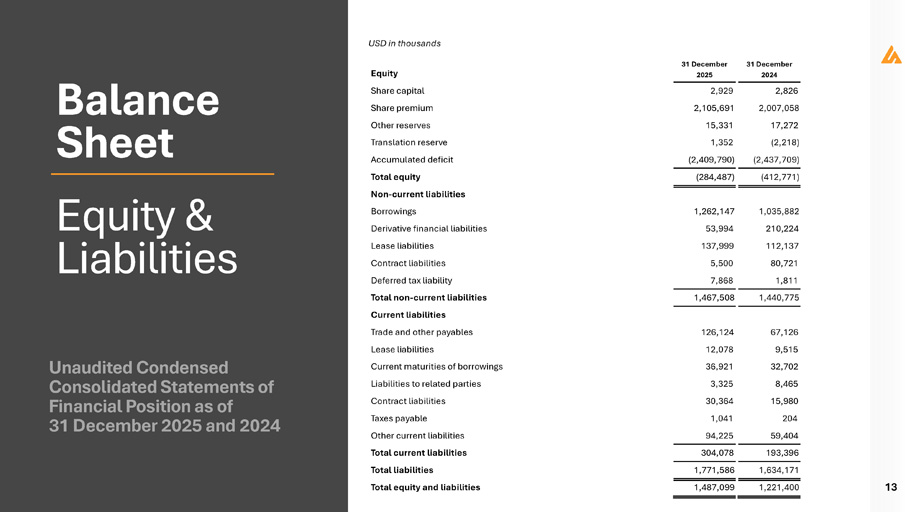

Unaudited Condensed Consolidated Statements of Financial Position as of 31 December 2025 and 2024 2,826 2,929 Share capital 2,007,058 2,105,691 Share premium 17,272 15,331 Other reserves (2,218) 1,352 Translation reserve (2,437,709) (2,409,790) Accumulated deficit (412,771) (284,487) Total equity 1,035,882 1,262,147 Non - current liabilities Borrowings 210,224 53,994 Derivative financial liabilities 112,137 137,999 Lease liabilities 80,721 5,500 Contract liabilities 1,811 7,868 Deferred tax liability 1,440,775 1,467,508 Total non - current liabilities 67,126 126,124 Current liabilities Trade and other payables 9,515 12,078 Lease liabilities 32,702 36,921 Current maturities of borrowings 8,465 3,325 Liabilities to related parties 15,980 30,364 Contract liabilities 204 1,041 Taxes payable 59,404 94,225 Other current liabilities 193,396 304,078 Total current liabilities 1,634,171 1,771,586 Total liabilities 13 1,221,400 1,487,099 Total equity and liabilities Balance Sheet Equity & Liabilities USD in thousands Equity 31 December 2025 31 December 2024

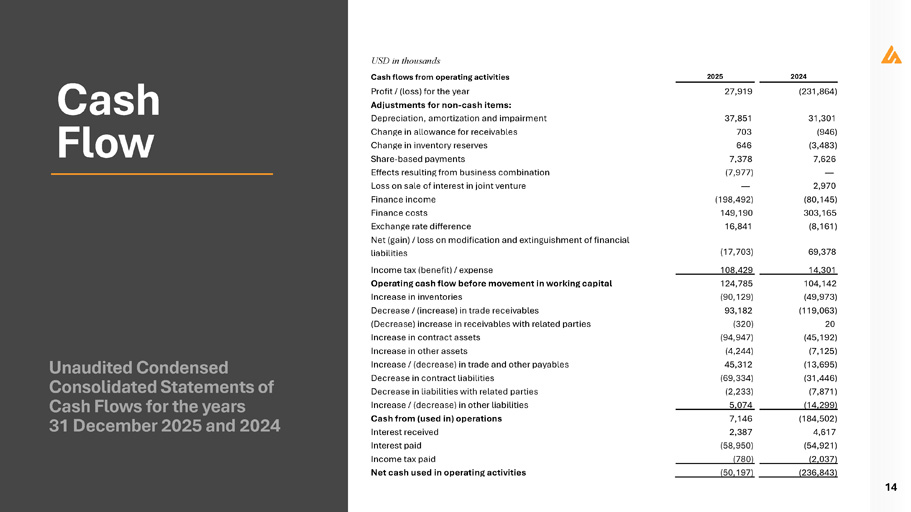

Unaudited Condensed Consolidated Statements of Cash Flows for the years 31 December 2025 and 2024 14 Cash Flow USD in thousands 2024 2025 Cash flows from operating activities (231,864) 27,919 Profit / (loss) for the year Adjustments for non - cash items: 31,301 37,851 Depreciation, amortization and impairment (946) 703 Change in allowance for receivables (3,483) 646 Change in inventory reserves 7,626 7,378 Share - based payments — (7,977) Effects resulting from business combination 2,970 — Loss on sale of interest in joint venture (80,145) (198,492) Finance income 303,165 149,190 Finance costs (8,161) 16,841 Exchange rate difference 69,378 (17,703) Net (gain) / loss on modification and extinguishment of financial liabilities 14,301 108,429 Income tax (benefit) / expense 104,142 124,785 Operating cash flow before movement in working capital (49,973) (90,129) Increase in inventories (119,063) 93,182 Decrease / (increase) in trade receivables 20 (320) (Decrease) increase in receivables with related parties (45,192) (94,947) Increase in contract assets (7,125) (4,244) Increase in other assets (13,695) 45,312 Increase / (decrease) in trade and other payables (31,446) (69,334) Decrease in contract liabilities (7,871) (2,233) Decrease in liabilities with related parties (14,299) 5,074 Increase / (decrease) in other liabilities (184,502) 7,146 Cash from (used in) operations 4,617 2,387 Interest received (54,921) (58,950) Interest paid (2,037) (780) Income tax paid (236,843) (50,197) Net cash used in operating activities

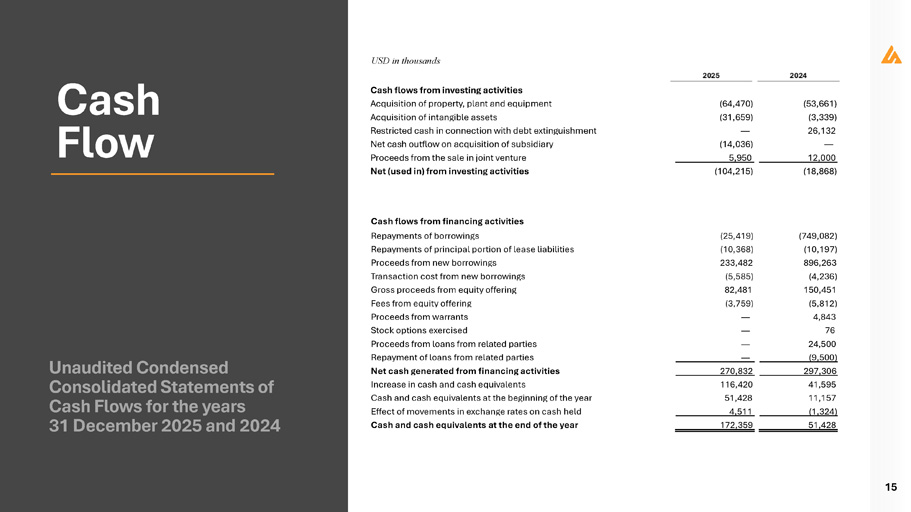

Unaudited Condensed Consolidated Statements of Cash Flows for the years 31 December 2025 and 2024 15 Cash Flow USD in thousands Cash flows from investing activities (53,661) (64,470) Acquisition of property, plant and equipment (3,339) (31,659) Acquisition of intangible assets 26,132 — Restricted cash in connection with debt extinguishment — (14,036) Net cash outflow on acquisition of subsidiary 12,000 5,950 Proceeds from the sale in joint venture (18,868) (104,215) Net (used in) from investing activities Cash flows from financing activities (749,082) (25,419) Repayments of borrowings (10,197) (10,368) Repayments of principal portion of lease liabilities 896,263 233,482 Proceeds from new borrowings (4,236) (5,585) Transaction cost from new borrowings 150,451 82,481 Gross proceeds from equity offering (5,812) (3,759) Fees from equity offering 4,843 — Proceeds from warrants 76 — Stock options exercised 24,500 — Proceeds from loans from related parties (9,500) — Repayment of loans from related parties 297,306 270,832 Net cash generated from financing activities 41,595 116,420 Increase in cash and cash equivalents 11,157 51,428 Cash and cash equivalents at the beginning of the year (1,324) 4,511 Effect of movements in exchange rates on cash held 51,428 172,359 Cash and cash equivalents at the end of the year

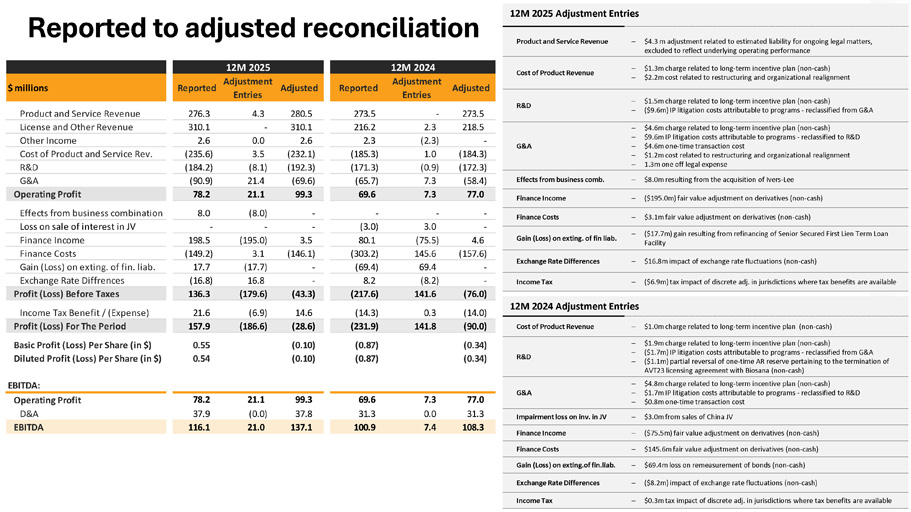

Reported to adjusted reconciliation 12M 2025 Adjustment Entries Product and Service Revenue $4.3 m adjustment related to estimated liability for ongoing legal matters, excluded to reflect underlying operating performance $1.3m charge related to long - term incentive plan (non - cash) $2.2m cost related to restructuring and organizational realignment $1.5m charge related to long - term incentive plan (non - cash) ($9.6m) IP litigation costs attributable to programs - reclassified from G&A $4.6m charge related to long - term incentive plan (non - cash) $9.6m IP litigation costs attributable to programs - reclassified to R&D $4.6m one - time transaction cost $1.2m cost related to restructuring and organizational realignment 1.3m one off legal expense $8.0m resulting from the acquisition of Ivers - Lee Finance Income ($195.0m) fair value adjustment on derivatives (non - cash) Finance Costs $3.1m fair value adjustment on derivatives (non - cash) Gain (Loss) on exting. of fin liab. ($17.7m) gain resulting from refinancing of Senior Secured First Lien Term Loan Facility Exchange Rate Differences $16.8m impact of exchange rate fluctuations (non - cash) ($6.9m) tax impact of discrete adj. in jurisdictions where tax benefits are available Income Tax 12M 2024 Adjustment Entries Cost of Product Revenue $1.0m charge related to long - term incentive plan (non - cash) R&D $1.9m charge related to long - term incentive plan (non - cash) ($1.7m) IP litigation costs attributable to programs - reclassified from G&A ($1.1m) partial reversal of one - time AR reserve pertaining to the termination of AVT23 licensing agreement with Biosana (non - cash) G&A $4.8m charge related to long - term incentive plan (non - cash) $1.7m IP litigation costs attributable to programs - reclassified to R&D $0.8m one - time transaction cost Impairment loss on inv. in JV $3.0m from sales of China JV Finance Income ($75.5m) fair value adjustment on derivatives (non - cash) Finance Costs $145.6m fair value adjustment on derivatives (non - cash) Gain (Loss) on exting.of fin.liab. $69.4m loss on remeasurement of bonds (non - cash) Exchange Rate Differences ($8.2m) impact of exchange rate fluctuations (non - cash) Income Tax $0.3m tax impact of discrete adj. in jurisdictions where tax benefits are available Cost of Product Revenue R&D Adjusted 273.5 12M 2024 Adjustment Entries - Reported 273.5 Adjusted 280.5 12M 2025 Adjustment Entries 4.3 Reported 276.3 $ millions Product and Service Revenue 218.5 2.3 216.2 310.1 - 310.1 License and Other Revenue G&A - (2.3) 2.3 2.6 0.0 2.6 Other Income (184.3) 1.0 (185.3) (232.1) 3.5 (235.6) Cost of Product and Service Rev. (172.3) (0.9) (171.3) (192.3) (8.1) (184.2) R&D Effects from business comb. (58.4) 7.3 (65.7) (69.6) 21.4 (90.9) G&A Operating Profit 78.2 21.1 99.3 69.6 7.3 77.0 Effects from business combination 8.0 (8.0) - - - - Loss on sale of interest in JV - - - (3.0) 3.0 - Finance Income 198.5 (195.0) 3.5 80.1 (75.5) 4.6 Finance Costs (149.2) 3.1 (146.1) (303.2) 145.6 (157.6) Gain (Loss) on exting. of fin. liab. 17.7 (17.7) - (69.4) 69.4 - Exchange Rate Diffrences (16.8) 16.8 - 8.2 (8.2) - Profit (Loss) Before Taxes 136.3 (179.6) (43.3) (217.6) 141.6 (76.0) Income Tax Benefit / (Expense) 21.6 (6.9) 14.6 (14.3) 0.3 (14.0) Profit (Loss) For The Period 157.9 (186.6) (28.6) (231.9) 141.8 (90.0) Basic Profit (Loss) Per Share (in $) Diluted Profit (Loss) Per Share (in $) 0.55 0.54 (0.10) (0.10) (0.87) (0.87) (0.34) (0.34) EBITDA: Operating Profit D&A 78.2 37.9 21.1 (0.0) 99.3 37.8 69.6 31.3 7.3 0.0 77.0 31.3 EBITDA 116.1 21.0 137.1 100.9 7.4 108.3

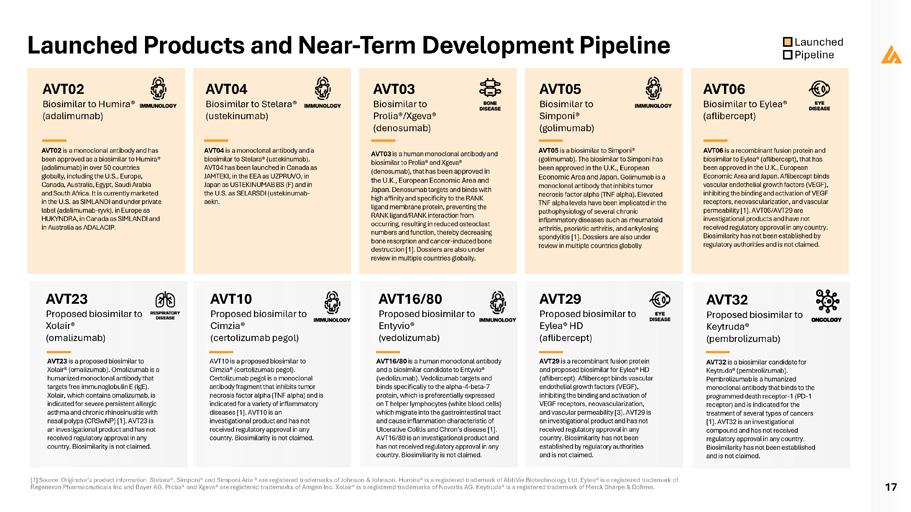

17 AVT02 Biosimilar to Humira® (adalimumab) AVT02 is a monoclonal antibody and has been approved as a biosimilar to Humira® (adalimumab) in over 50 countries globally, including the U.S., Europe, Canada, Australia, Egypt, Saudi Arabia and South Africa. It is currently marketed in the U.S. as SIMLANDI and under private label (adalimumab - ryvk), in Europe as HUKYNDRA, in Canada as SIMLANDI and in Australia as ADALACIP. AVT03 Biosimilar to Prolia®/Xgeva® (denosumab) AVT03 is a human monoclonal antibody and biosimilar to Prolia® and Xgeva® (denosumab), that has been approved in the U.K., European Economic Area and Japan . Denosumab targets and binds with high affinity and specificity to the RANK ligand membrane protein, preventing the RANK ligand/RANK interaction from occurring, resulting in reduced osteoclast numbers and function, thereby decreasing bone resorption and cancer - induced bone destruction [1]. Dossiers are also under review in multiple countries globally. AVT04 Biosimilar to Stelara® (ustekinumab) AVT04 is a monoclonal antibody and a biosimilar to Stelara® (ustekinumab). AVT04 has been launched in Canada as JAMTEKI, in the EEA as UZPRUVO, in Japan as USTEKINUMAB BS (F) and in the U.S. as SELARSDI (ustekinumab - aekn. AVT05 Biosimilar to Simponi® (golimumab) AVT05 is a biosimilar to Simponi® (golimumab). The biosimilar to Simponi has been approved in the U.K., European Economic Area and Japan. Golimumab is a monoclonal antibody that inhibits tumor necrosis factor alpha (TNF alpha). Elevated TNF alpha levels have been implicated in the pathophysiology of several chronic inflammatory diseases such as rheumatoid arthritis, psoriatic arthritis, and ankylosing spondylitis [1]. Dossiers are also under review in multiple countries globally AVT10 Proposed biosimilar to Cimzia® (certolizumab pegol) AVT10 is a proposed biosimilar to Cimzia® (certolizumab pegol). Certolizumab pegol is a monoclonal antibody fragment that inhibits tumor necrosis factor alpha (TNF alpha) and is indicated for a variety of inflammatory diseases [1]. AVT10 is an investigational product and has not received regulatory approval in any country. Biosimilarity is not claimed. AVT16/80 Proposed biosimilar to Entyvio® (vedolizumab) AVT16/80 is a human monoclonal antibody and a biosimilar candidate to Entyvio® (vedolizumab). Vedolizumab targets and binds specifically to the alpha - 4 - beta - 7 protein, which is preferentially expressed on T helper lymphocytes (white blood cells) which migrate into the gastrointestinal tract and cause inflammation characteristic of Ulcerative Colitis and Chron’s disease [ 1 ] . AVT 16 / 80 is an investigational product and has not received regulatory approval in any country . Biosimiliarity is not claimed . AVT06 Biosimilar to Eylea® (aflibercept) AVT06 is a recombinant fusion protein and biosimilar to Eylea® (aflibercept), that has been approved in the U.K., European Economic Area and Japan. Aflibercept binds vascular endothelial growth factors (VEGF), inhibiting the binding and activation of VEGF receptors, neovascularization, and vascular permeability [1]. AVT06/AVT29 are investigational products and have not received regulatory approval in any country. Biosimilarity has not been established by regulatory authorities and is not claimed. AVT23 Proposed biosimilar to Xolair® (omalizumab) AVT23 is a proposed biosimilar to Xolair® (omalizumab). Omalizumab is a humanized monoclonal antibody that targets free immunoglobulin E (IgE). Xolair, which contains omalizumab, is indicated for severe persistent allergic asthma and chronic rhinosinusitis with nasal polyps (CRSwNP) [1]. AVT23 is an investigational product and has not received regulatory approval in any country. Biosimilarity is not claimed. [1] Source: Originator’s product information. Stelara®, Simponi® and Simponi Aria ® are registered trademarks of Johnson & Johnson. Humira® is a registered trademark of AbbVie Biotechnology Ltd. Eylea® is a registered trademark of Regeneron Pharmaceuticals Inc and Bayer AG. Prolia® and Xgeva® are registered trademarks of Amgen Inc. Xolair® is a registered trademarks of Novartis AG. Keytruda® is a registered trademark of Merck Sharpe & Dohme. Launched Products and Near - Term Development Pipeline AVT29 Proposed biosimilar to Eylea® HD (aflibercept) AVT29 is a recombinant fusion protein and proposed biosimilar for Eylea® HD (aflibercept). Aflibercept binds vascular endothelial growth factors (VEGF), inhibiting the binding and activation of VEGF receptors, neovascularization, and vascular permeability [3]. AVT29 is an investigational product and has not received regulatory approval in any country. Biosimilarity has not been established by regulatory authorities and is not claimed. AVT32 Proposed biosimilar to Keytruda® (pembrolizumab) AVT32 is a biosimilar candidate for Keytruda® (pembrolizumab). Pembrolizumab is a humanized monoclonal antibody that binds to the programmed death receptor - 1 (PD - 1 receptor) and is indicated for the treatment of several types of cancers [1]. AVT32 is an investigational compound and has not received regulatory approval in any country. Biosimilarity has not been established and is not claimed. Launched Pipeline

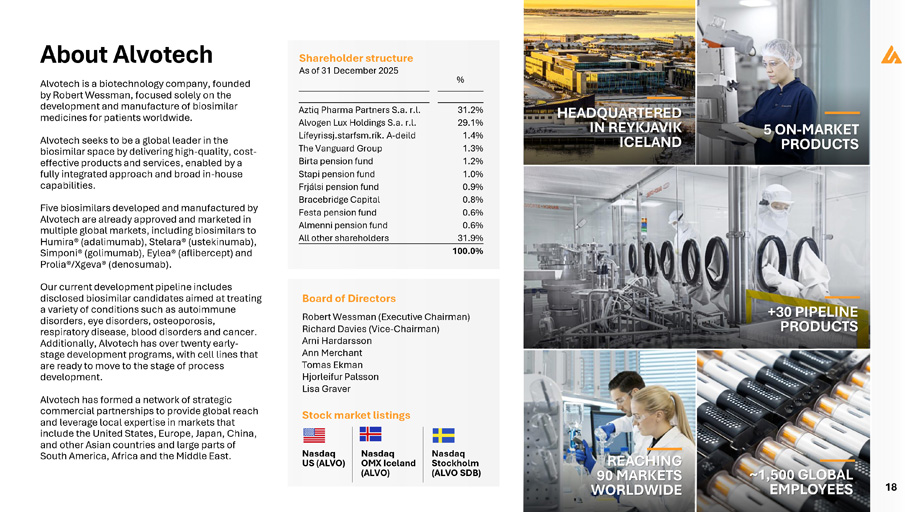

Q4 2025 Earnings Release 18 About Alvotech Alvotech is a biotechnology company, founded by Robert Wessman, focused solely on the development and manufacture of biosimilar medicines for patients worldwide. Alvotech seeks to be a global leader in the biosimilar space by delivering high - quality, cost - effective products and services, enabled by a fully integrated approach and broad in - house capabilities. Five biosimilars developed and manufactured by Alvotech are already approved and marketed in multiple global markets, including biosimilars to Humira® (adalimumab), Stelara® (ustekinumab), Simponi® (golimumab), Eylea® (aflibercept) and Prolia®/Xgeva® (denosumab). Our current development pipeline includes disclosed biosimilar candidates aimed at treating a variety of conditions such as autoimmune disorders, eye disorders, osteoporosis, respiratory disease, blood disorders and cancer. Additionally, Alvotech has over twenty early - stage development programs, with cell lines that are ready to move to the stage of process development. Alvotech has formed a network of strategic commercial partnerships to provide global reach and leverage local expertise in markets that include the United States, Europe, Japan, China, and other Asian countries and large parts of South America, Africa and the Middle East. HEADQUARTERED IN REYKJAVIK ICELAND +30 PIPELINE PRODUCTS 5 ON - MARKET PRODUCTS REACHING 90 MARKETS WORLDWIDE ~1,500 GLOBAL EMPLOYEES % 31.2% Aztiq Pharma Partners S.a. r.l. 29.1% Alvogen Lux Holdings S.a. r.l. 1.4% Lífeyrissj.starfsm.rík. A - deild 1.3% The Vanguard Group 1.2% Birta pension fund 1.0% Stapi pension fund 0.9% Frjálsi pension fund 0.8% Bracebridge Capital 0.6% Festa pension fund 0.6% Almenni pension fund 31.9% All other shareholders 100.0% Shareholder structure As of 31 December 2025 Board of Directors Robert Wessman (Executive Chairman) Richard Davies (Vice - Chairman) Arni Hardarsson Ann Merchant Tomas Ekman Hjorleifur Palsson Lisa Graver Stock market listings Nasdaq US (ALVO) Nasdaq OMX Iceland (ALVO) Nasdaq Stockholm (ALVO SDB)

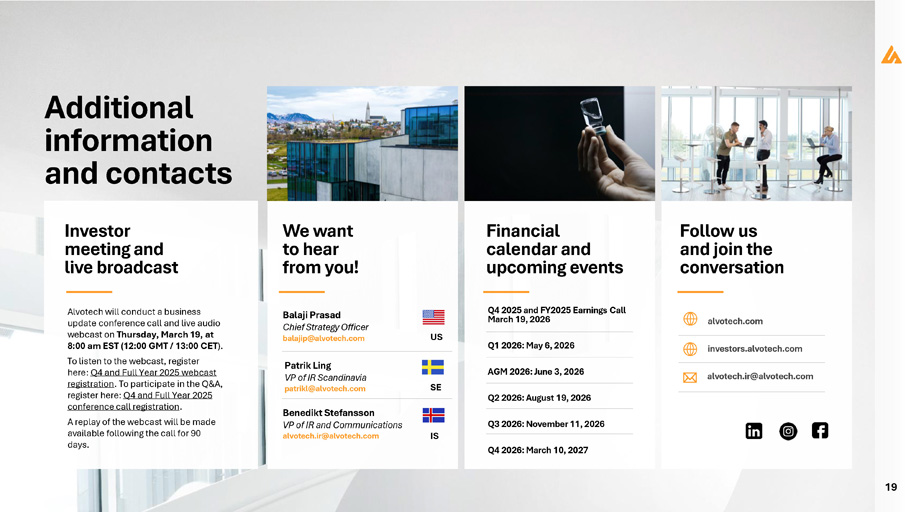

Additional information and contacts We want to hear from you! Follow us and join the conversation alvotech.com investors.alvotech.com alvotech.ir@alvotech.com Balaji Prasad Chief Strategy Officer balajip@alvotech.com Patrik Ling VP of IR Scandinavia patrikl@alvotech.com Benedikt Stefansson VP of IR and Communications alvotech.ir@alvotech.com US SE IS Financial calendar and upcoming events Q4 2025 and FY2025 Earnings Call March 19, 2026 Q1 2026: May 6, 2026 AGM 2026: June 3, 2026 Q2 2026: August 19, 2026 Q3 2026: November 11, 2026 Q4 2026: March 10, 2027 19 Investor meeting and live broadcast Alvotech will conduct a business update conference call and live audio webcast on Thursday, March 19, at 8:00 am EST (12:00 GMT / 13:00 CET ). To listen to the webcast, register here: Q4 and Full Year 2025 webcast registration . To participate in the Q&A, register here: Q4 and Full Year 2025 conference call registration . A replay of the webcast will be made available following the call for 90 days.